Attached files

| file | filename |

|---|---|

| EXCEL - IDEA: XBRL DOCUMENT - DECKERS OUTDOOR CORP | Financial_Report.xls |

| EX-31.1 - EX-31.1 - DECKERS OUTDOOR CORP | a2202162zex-31_1.htm |

| EX-32.1 - EX-32.1 - DECKERS OUTDOOR CORP | a2202162zex-32_1.htm |

| EX-23.1 - EX-23.1 - DECKERS OUTDOOR CORP | a2202162zex-23_1.htm |

| EX-31.2 - EX-31.2 - DECKERS OUTDOOR CORP | a2202162zex-31_2.htm |

| EX-21.1 - EX-21.1 - DECKERS OUTDOOR CORP | a2202162zex-21_1.htm |

| EX-10.24 - EX-10.24 - DECKERS OUTDOOR CORP | a2202162zex-10_24.htm |

| EX-10.22 - EX-10.22 - DECKERS OUTDOOR CORP | a2202162zex-10_22.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| (Mark one) | ||

ý |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the fiscal year ended December 31, 2010 |

||

or |

||

o |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

|

For the transition period from to |

||

Commission File No. 0-22446

DECKERS OUTDOOR CORPORATION

(Exact name of registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) |

95-3015862 (I.R.S. Employer Identification No.) |

|

495-A South Fairview Avenue, Goleta, California (Address of principal executive offices) |

93117 (Zip Code) |

|

Registrant's telephone number, including area code: (805) 967-7611 |

||

Securities registered pursuant to Section 12(b) of the Act: None |

||

Title of each class

|

Name of each exchange on which registered | |

|---|---|---|

| Common Stock, Par value $0.01 per share | NASDAQ Global Select Market |

Securities registered pursuant to Section 12(g) of the Act:

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15 (d) of the Exchange Act. Yes o Noý

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ý | Accelerated filer o | Non-accelerated filer o (Do not check if a smaller reporting company) |

Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No ý

The aggregate market value of the common stock held by non-affiliates of the registrant was $1,763,604,129 based on the June 30, 2010 closing price of $47.62 on the NASDAQ Global Select Market on such date.

The number of shares of the registrant's Common Stock outstanding at February 15, 2011 was 38,581,395.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant's definitive proxy statement relating to the registrant's 2011 annual meeting of stockholders, which will be filed pursuant to Regulation 14A within 120 days after the end of the registrant's fiscal year ended December 31, 2010, are incorporated by reference in Part III of this Annual Report on Form 10-K.

DECKERS OUTDOOR CORPORATION

For the Fiscal Year Ended December 31, 2010

Table of Contents to Annual Report on Form 10-K

2

SPECIAL NOTE ON FORWARD-LOOKING STATEMENTS

This report and the information incorporated by reference in this report contain "forward-looking statements" within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. We sometimes use words such as "anticipate," "believe," "continue," "estimate," "expect," "intend," "may," "project," "will" and similar expressions, as they relate to us, our management and our industry, to identify forward-looking statements. Forward-looking statements relate to our expectations, beliefs, plans, strategies, prospects, future performance, anticipated trends and other future events. Specifically, this report and the information incorporated by reference in this report contain forward-looking statements relating to, among other things:

- •

- our global business, growth, operating and financing strategies;

- •

- our product and geographic mix;

- •

- the success of new products, new brands, and other growth initiatives;

- •

- the impact of seasonality on our operations;

- •

- expectations regarding our net sales and earnings growth and other financial metrics;

- •

- our development of worldwide distribution channels;

- •

- trends affecting our financial condition or results of operations;

- •

- overall global economic trends; and

- •

- reliability of overseas factory production and storage and availability of raw materials.

We have based our forward-looking statements largely on our current expectations and projections about future events and financial trends affecting our business. Actual results may differ materially. Some of the risks, uncertainties and assumptions that may cause actual results to differ from these forward-looking statements are described in Part I, Item 1A, "Risk Factors." In light of these risks, uncertainties and assumptions, the forward-looking events and circumstances discussed in this report and the information incorporated by reference in this report might not happen. You should read this report in its entirety, together with the documents that we file as exhibits to this report and the documents that we incorporate by reference in this report with the understanding that our future results may be materially different from what we expect. We qualify all of our forward-looking statements by these cautionary statements and we assume no obligation to update such forward-looking statements publicly for any reason.

References in this Annual Report on Form 10-K to "Deckers", "we", "our", "us", or the "Company" refer to Deckers Outdoor Corporation. Ahnu®, Deckers®, Simple®, Teva®, TSUBO®, and UGG® are some of our trademarks. Other trademarks or trade names appearing elsewhere in this report are the property of their respective owners.

Unless otherwise specifically indicated, all amounts in Item 1. and Item 1A. herein are expressed in thousands, except for share quantity, per share data, selling prices, and employees.

General

Deckers Outdoor Corporation was incorporated in 1975 under the laws of the State of California and, in 1993, reincorporated under the laws of the State of Delaware. We strive to be a premier lifestyle marketer that builds niche brands into global market leaders by designing and marketing innovative, functional and fashion-oriented footwear developed for both high performance outdoor activities and everyday casual lifestyle use. We believe that our footwear is distinctive and appeals broadly to men, women and children. We sell our products, including accessories such as handbags and outerwear, through

3

quality domestic and international retailers, international distributors, and directly to end-user consumers, both domestically and internationally, through our websites, call centers, retail concept stores and retail outlet stores. Our primary objective is to build our footwear lines into global lifestyle brands with market leadership positions. We seek to differentiate our brands and products by offering diverse lines that emphasize authenticity, functionality, quality and comfort and products tailored to a variety of activities, seasons and demographic groups. Virtually all of our products are manufactured by independent contractors outside of the United States (US). Our continued growth will depend upon the broadening of our products offered under each brand, expanding domestic and international distribution, successfully opening new retail stores, increasing sales to end-user consumers, and developing or acquiring new brands.

In July 2008, we entered into a joint venture agreement with an affiliate of Stella International Holdings Limited ("Stella International") for the opening of retail stores and wholesale distribution for the UGG brand in China. The joint venture is owned 51% by Deckers and 49% by Stella International. Stella International is also one of our major manufacturers in China. In May 2008, we acquired 100% of the ownership interest of TSUBO, LLC, a high-end casual footwear brand. In March 2009, we acquired 100% of the ownership interest of Ahnu, Inc., an outdoor performance and lifestyle footwear brand. In September 2009, we began to reacquire our international distribution rights, beginning in Japan. In January 2010, we acquired certain assets and liabilities, including reacquisition of our distribution rights, from our Teva distributor that sold to retailers in Belgium, the Netherlands, and Luxemburg (Benelux) as well as France. In September 2010, we purchased a portion of a privately held footwear company as an equity method investment.

On May 28, 2010, we announced that our Board of Directors authorized a three-for-one stock split to be effected in the form of a stock dividend. Each stockholder of record received two additional shares of common stock for each share held on June 17, 2010, that was paid on July 2, 2010. All share and related information presented in this Annual Report on Form 10-K reflect the increased number of shares and decreased stock prices resulting from this stock split for all periods presented.

Products

We market our products primarily under two proprietary brands:

UGG®. UGG Australia is our luxury comfort brand and the category creator for luxury sheepskin footwear. The UGG brand has enjoyed several years of strong growth and positive consumer reception, driven by consistent introductions of new styles in the fall and spring seasons and strategic geographic expansion of our distribution. We carefully manage the distribution of our UGG products within high-end specialty and department store retailers in order to best reach our target consumers, preserve the UGG brand's retail channel positioning and maintain the UGG brand's position as a mid- to upper-price luxury brand.

In recent years, sales of UGG products have benefited from significant national media attention and celebrity endorsement through our marketing programs and product placement activities, raising the profile of our UGG brand as a luxury comfort brand. We have further supported the UGG brand's market positioning by expanding the selection of styles available in order to build consumer interest in our UGG brand collection. We also remain committed to limiting distribution of UGG products to high-end retail channels.

Teva®. Teva is our outdoor performance and lifestyle brand and pioneer of the sport sandal market. We have expanded the Teva product line over time to include open and closed-toe outdoor lifestyle footwear, as well as additional outdoor performance footwear, including multi-sport shoes, light hiking shoes, amphibious footwear, and rugged outdoor travel shoes.

In recent years, we have focused on regaining our leadership position in the performance sandal market, while broadening our performance platform to include other outdoor activities such as multi-sport and light hiking to lessen our overall reliance on sandal sales, while bringing youthfulness back to the brand through contemporary designs, colors and materials. In 2008, we introduced a modest assortment of

4

fall and winter footwear. We followed that up in fall 2009 with a more complete collection of seasonally appropriate performance and lifestyle products for men, women and children. The fall 2009 line included high performance light hikers with eVent waterproof membranes and Vibram rubber outsoles, rugged multi-sport shoes and a range of women's lifestyle boots in both leather and suede with warm, faux fur linings. In 2010, we continued to build on our water-related performance heritage and continued to inject youthfulness into the Teva brand. We introduced a more expansive collection of performance and lifestyle open-toe product, while also significantly increasing our offering in closed-toe light hiking, multi-sport and rugged casual footwear.

In addition to our primary brands, our other brands include Simple®, a line of sustainable and stylish footwear, TSUBO®, a line of high-end casual footwear that incorporates style, function and maximum comfort, and Ahnu®, a line of outdoor performance and lifestyle footwear.

Sales and Distribution

At the wholesale level, we distribute our products in the US through a dedicated network of independent sales representatives, as well as through employee sales representatives who serve as territory representatives or key account executives for several of our largest customers. Our sales representatives are organized geographically and by brand and visit retail stores to communicate the features, styling and technology of our products. In addition to our wholesale business, we also sell products directly to consumers through our websites and retail stores. Our brands are generally advertised and promoted through a variety of consumer media campaigns. We benefit from editorial coverage in both consumer and trade publications. Each brand's dedicated marketing team works closely with targeted accounts to maximize advertising and promotional effectiveness.

Our sales force is generally separated by brand, as each brand generally has certain specialty consumers; however, there is overlap between the sales teams and customers. We have aligned our brands' sales forces to position them for the future of the brands. Each brand's respective sales manager recruits and manages their network of sales representatives and coordinates sales to national accounts. We believe this approach for the US market maximizes the selling efforts to our national retail accounts on a cost-effective basis.

We distribute products sold in the US through our distribution centers in Ventura and Camarillo, California. Our distribution centers feature a warehouse management system that enables us to efficiently pick and pack products for direct shipment to customers. For certain customers requiring special handling, each shipment is pre-labeled and packed to the retailer's specifications, enabling the retailer to easily unpack our product and immediately display it on the sales floor. All incoming and outgoing shipments must meet our quality inspection process.

Internationally, we distribute our products through independent distributors and retailers in a vast number of countries, including countries throughout Europe, Asia Pacific, Canada, and Latin America, among others. In addition, as we do in the US, we sell products directly to international consumers through our websites and our retail stores, including retail stores with our joint venture partner in China. We utilize a third-party logistics company in the United Kingdom (UK) for the distribution of inventory to our UK retail stores. In Japan, we work with a trading company for importation and use a third-party logistics company for distribution to our wholesale customers and to our retail store. We operate a distribution center in the Netherlands for the distribution of Teva products in Belgium, the Netherlands, and Luxembourg (Benelux) and France. Our principal customers include specialty retailers, selected department stores, outdoor retailers, sporting goods retailers, shoe stores, and online retailers. In 2010, we continued to assume the distribution rights from certain international distributors and sell directly to retailers in those regions, and we plan to continue distributor conversions in the future.

Our five largest customers accounted for approximately 28.9% of our net sales for 2010, compared to 30.0% for 2009. One customer, Nordstrom, accounted for greater than 10% of our consolidated net sales in 2010 and 2009, with the majority of those being related to our UGG segment.

5

UGG. We sell our UGG footwear and accessories primarily through high-end department stores such as Nordstrom, Neiman Marcus and Bloomingdale's, as well as independent specialty retailers such as Journey's, David Z. and internet customers such as Zappos.com. We believe these retailers support the luxury positioning of our brand and are the destination shopping choice for the consumer who seeks out the fashion and functional elements of our UGG products.

Teva. We sell our Teva footwear primarily through specialty outdoor and sporting goods retailers such as REI, L.L. Bean, Dick's Sporting Goods and The Sports Authority as well as on-line retailers such as Zappos.com. We believe these retail channels are the first choice for athletes, outdoor enthusiasts and adventurers seeking technical and performance-oriented outdoor footwear. Furthermore, we believe that retailers who appreciate and can fully market the technical attributes of our performance products to the consumer best sell our Teva footwear.

Other brands. Our other brands are sold throughout the world primarily at better department stores, outdoor specialty accounts, independent specialty retailers, and with online retailers that support our brand ideals of comfort, style and quality. We also sell our Simple brand through health and wellness retailers that target consumers seeking fashionable, youthful, functional, and sustainable footwear. Key accounts of our other brands include Nordstrom, Dillard's, Hanigs, REI and Zappos.com.

eCommerce. Our eCommerce business enables us to interact and reinforce our relationships with the consumer. We operate our eCommerce business primarily through uggaustralia.com, Teva.com, Tsubo.com, Ahnu.com, and SimpleShoes.com websites. Our websites support the brands' marketing goals and also drive offline sales by providing information to consumers about the brands' products and where to find retailers that carry our brands. We have expanded our international capabilities by developing sites to service international markets. These sites are translated into the local language, provide product through local distribution centers and price the products in the consumers' local currency. In 2010, we significantly upgraded our eCommerce platform to support our international and domestic sites and opened and operated an international call center to accommodate these international website sales. Our eCommerce business has offices in Flagstaff, Arizona and Richmond, England. Order fulfillment is performed by our distribution centers in California and the UK in order to reduce the cost of order fulfillment, minimize out of stock positions and further leverage our distribution centers' operations. Products sold through our eCommerce business are sold at prices which approximate retail prices, enabling us to capture the full retail margin on each direct to consumer transaction.

Retail Stores. Our retail store business allows us to directly reach our customers and meet the growing demand for our products. In addition, our UGG Australia concept stores allow us to showcase the entire lines for spring and fall; whereas, most retailers do not carry our full line. In 2010, we opened six stores in the US and three internationally. As of December 31, 2010, we had a total of 18 UGG Australia concept stores and nine retail outlet stores worldwide. Products sold through our concept stores are sold at prices which approximate department store prices, enabling us to capture the full retail margin on each direct to consumer transaction. The outlet stores sell some of our discontinued styles from the previous season, plus products made specifically for the outlet stores. During 2011, we plan to open additional retail stores in the US and significantly expand our retail store business internationally.

Product Design and Development

The design and product development staff for each of our brands creates new innovative footwear products that combine our standards of high quality, comfort and functionality. The design function for all of our brands is performed by a combination of our internal design and development staff plus outside freelance designers. By utilizing outside designers, we believe we are able to review a variety of different design perspectives on a cost-efficient basis and anticipate color and style trends more quickly. Refer to Note 1 to our accompanying consolidated financial statements for a discussion of our research and development costs for the last three years.

6

In order to ensure quality, consistency and efficiency in our design and product development process, we continually evaluate the availability and cost of raw materials, the capabilities and capacity of our independent contract manufacturers and the target retail price of new models and lines. The design and development staff works closely with brand management to develop new styles of footwear and accessories for our various product lines. We develop detailed drawings and prototypes of our new products to aid in conceptualization and to ensure our contemplated new products meet the standards for innovation and performance that our consumers demand. Throughout the development process, we have multiple design and development reviews, and members of the design staff coordinate with our domestic and overseas product development, manufacturing and sourcing personnel. This ensures that we are addressing the needs of our consumers and are working toward a common goal of developing and producing a high quality product to be delivered on a timely basis.

Manufacturing

We do not manufacture our products; we outsource the production of our brand footwear primarily to independent manufacturers in China. During 2009, we began to diversify our manufacturing locations by outsourcing a limited amount of production to manufacturers in Vietnam, and in 2010 increased this production volume. We also outsource the production of a portion of our UGG footwear to an independent manufacturer in New Zealand. We require our independent contract manufacturers and designated suppliers to adopt our Factory Charter, which specifies that they comply with all local laws and regulations governing human rights, working conditions and environmental compliance before we are willing to conduct business with them. We also require our manufacturing partners to comply with our Ethical Supply Chain guidelines and Restricted Substances policy as a condition of doing business with our company. We require our licensees to demand the same from their contract factories and suppliers. We have no long-term contracts with our manufacturers. As we grow, we expect to continue to rely exclusively on independent manufacturers for our sourcing needs.

The production of footwear by our independent manufacturers is performed in accordance with our detailed specifications and is subject to our quality control standards. We maintain on-site supervisory offices in Pan Yu City, China and Macau that serve as local links to our independent manufacturers, enabling us to carefully monitor the production process from receipt of the design brief to production of interim and final samples and shipment of finished product. We believe this local presence provides greater predictability of material availability, product flow and adherence to final design specifications than we could otherwise achieve through an agency arrangement. To ensure the production of high quality products, the majority of the materials and components used in production of our products by these independent manufacturers are purchased from independent suppliers designated by us. Excluding sheepskin, we believe that substantially all the various raw materials and components used in the manufacture of our footwear, including rubber, leather and nylon webbing are generally available from multiple sources at competitive prices. We generally outsource our manufacturing requirements on the basis of individual purchase orders rather than maintaining long-term purchase commitments with our independent manufacturers.

At our direction, our manufacturers currently purchase the majority of the sheepskin used in our products from two tanneries in China, which source their skins from Australia, Europe and the US. We maintain constant communication with the tanneries to monitor the supply of sufficient high quality sheepskin available for our projected UGG brand production. To ensure adequate supplies for our manufacturers, we forecast our usage of top grade sheepskin in advance at a forward price. We believe current supplies are sufficient to meet our needs in the near future, but we continue to search for alternate suppliers in order to accommodate any unexpected future growth.

We have instituted pre-production, in-line, and post-production inspections to meet or exceed the high quality demanded by us and consumers of our products. Our quality assurance program includes our own employee on-site inspectors at our independent manufacturers who oversee the production process

7

and perform quality assurance inspections. We also inspect our products upon arrival at our distribution centers.

Patents and Trademarks

We utilize trademarks on nearly all of our products and believe that having distinctive marks that are readily identifiable is an important factor in creating a market for our goods, in identifying the Company, and in distinguishing our goods from the goods of others. We currently hold trademark registrations for UGG, Teva, Simple, TSUBO, Ahnu and other marks in the US and in many other countries, including the countries of the European Union, Canada, China, Japan and Korea. We now hold more than 260 utility and design patents and registrations in the US and abroad and have filed for more than 100 new patents which are currently pending. These patents expire at various times, and patents issued for applications filed this year will generally have a remaining duration from now to 2025 for design patents and from now to 2031 for utility patents. We regard our proprietary rights as valuable assets and vigorously protect such rights against infringement by third parties.

Seasonality

Our business is seasonal, with the highest percentage of UGG brand net sales occurring in the third and fourth quarters and the highest percentage of Teva brand net sales occurring in the first and second quarters of each year. Thus, our net sales in the last half of the year have exceeded that for the first half of the year, and we expect this trend to continue. Our other brands do not have a significant seasonal impact on our business. Nonetheless, actual results could differ materially depending upon consumer preferences, availability of product, competition and our customers continuing to carry and promote our various product lines, among other risks and uncertainties. See Part I, Item 1A, "Risk Factors." For further discussion on our working capital and inventory management, see Item 7 of Part II, "Management's Discussion and Analysis of Financial Condition and Results of Operations — Liquidity and Capital Resources."

Backlog

Historically, we have encouraged our customers to place, and we have received, a significant portion of orders as preseason orders, generally four to eight months prior to shipment date. We provide customers with price incentives, and in certain cases extended payment terms, to participate in such preseason programs to enable us to better plan our production schedule, inventory and shipping needs. Unfilled customer orders as of any date, which we refer to as backlog, represent orders scheduled to be shipped at a future date, which can be cancelled prior to shipment. The backlog as of a particular date is affected by a number of factors, including seasonality, manufacturing schedule and the timing of product shipments as well as variations in the quarter-to-quarter and year-to-year preseason incentive programs. The mix of future and immediate delivery orders can vary significantly from quarter-to-quarter and year-to-year. As a result, comparisons of the backlog from period-to-period may be misleading.

At December 31, 2010, our backlog of orders from our wholesale customers and distributors was approximately $336,000 compared to approximately $245,000 at December 31, 2009. While all orders in the backlog are subject to cancellation by customers, we expect that the majority of such orders will be filled in 2011. We believe that backlog at year-end is an imprecise indicator of total revenue that may be achieved for the full year for several reasons. Backlog only relates to wholesale orders for the next season and current season fill-in orders and excludes potential sales in our eCommerce business and retail stores during the year. Backlog also is effected by the timing of customers' orders and product availability.

Competition

The casual, outdoor, athletic, fashion and formal footwear markets are highly competitive. Our competitors include athletic and footwear companies, branded apparel companies, and retailers with their own private labels. Although the footwear industry is fragmented to a certain degree, many of our competitors are larger and have substantially greater resources than us, including athletic shoe companies,

8

several of which compete directly with some of our products. In addition, access to offshore manufacturing has made it easier for new companies to enter the markets in which we compete, further increasing competition in the footwear and accessory industries. Due to the popularity of our UGG products, we face increasing competition from a significant number of competitors selling imitation products.

Our footwear lines compete primarily on the basis of brand recognition and authenticity, product quality and design, functionality, performance, fashion appeal and price. Our ability to successfully compete depends on our ability to:

- •

- shape and stimulate consumer tastes and preferences by offering innovative, attractive and exciting products;

- •

- anticipate and respond to changing consumer demands in a timely manner;

- •

- maintain brand authenticity;

- •

- develop high quality products that appeal to consumers;

- •

- suitably price our products;

- •

- provide strong and effective marketing support; and

- •

- ensure product availability.

We believe we are well positioned to compete in the footwear industry. We continually look to acquire or develop more footwear brands to complement our existing portfolio and grow our existing consumer base.

Employees

At December 31, 2010, we employed approximately 1,500 employees in the US, Europe and Asia, none of whom were represented by a union. This figure includes approximately 800 employees in our retail stores worldwide, which includes part-time and seasonal employees. The large increase in employees during the year was primarily related to increased selling, general and administration headcount commensurate with our growth. We intend to increase our employee count further in 2011 primarily related to retail stores and our other expansion initiatives. We believe our relationships with our employees are good.

Financial Information about Segments and Geographic Areas

Our five reportable business segments include the strategic business units responsible for the worldwide operations of our brands' (UGG, Teva and other brands) wholesale divisions, as well as our eCommerce and retail store businesses. The majority of our sales and long-lived assets are in the US. Refer to Note 9 to our accompanying consolidated financial statements for further discussion of our business segment data. Refer to Item 1A of this Part I for a discussion of the risks attendant to our foreign operations.

Compliance with federal, state and local environmental regulations has not had, nor is it expected to have, any material effect on our capital expenditures, earnings or competitive position based on information and circumstances known to us at this time.

Available Information

Our internet address is www.deckers.com. We post links to our website to the following filings as soon as reasonably practicable after they are electronically filed with or furnished to the Securities and Exchange Commission (SEC): annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, Proxy Statements, and any amendment to those reports filed or furnished pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934, as amended. All such filings are available through our website free of charge. Our filings may also be read and copied at the SEC's Public Reference Room at 100 F Street, NE, Washington, DC 20549. Information on the operation of the Public Reference Room may be obtained by calling the SEC at 1-800-SEC-0330. The SEC also maintains an internet site at www.sec.gov that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC.

9

Our short and long-term success is subject to many factors beyond our control. Stockholders and potential stockholders should carefully consider the following risk factors related to our company as well as general investor risks, in addition to the other information contained in this report and the information incorporated by reference in this report. If any of the following risks occur, our business, financial condition or results of operations could be adversely affected. In that case, the value of our common stock could decline and stockholders and potential stockholders may lose all or part of their investment. Please also see Item 7 of Part II — "Management's Discussion and Analysis of Financial Condition and Results of Operations — Forward-Looking Statements."

The recent financial crisis and current economic uncertainty may adversely affect our financial condition and results of operations.

The recent economic recession and continuing economic uncertainty, have affected, and will likely continue to affect consumer spending generally and the buying habits and preferences of our customers in particular. A significant portion of the products we sell, especially those sold under the UGG Australia brand, are considered to be luxury retail products. The purchase of these products by customers is largely discretionary, and is therefore highly dependent upon the level of consumer spending, particularly among affluent customers. Sales of these products may be adversely affected by a continuation or worsening of recent economic conditions, increases in consumer debt levels, uncertainties regarding future economic prospects, or a decline in consumer confidence. During an actual or perceived economic downturn, fewer customers may shop for our products and those who do shop may limit the amounts of their purchases. As a result, we could be required to reduce the price we can charge for our products or increase our marketing and promotional expenses in response to lower than anticipated levels of demand for our products. In either case, these changes, or other similar changes in our marketing strategy, would reduce our revenues and profit margins and could have a material adverse affect on our financial condition and results of operations.

We sell the majority of our products through high-end specialty and department store retailers. These retailer customers may be impacted by continuing economic uncertainty, reduced customer demand for luxury products, and a significant decrease in available credit. If reduced consumer spending, lower demand for luxury products, or credit pressures result in financial difficulties or insolvency for these customers, it would adversely impact our estimated allowances and reserves as well as our overall financial results. Also, economic factors such as increased transportation costs, inflation, higher costs of labor, insurance and healthcare, and changes in other laws and regulations may increase our cost of sales and our operating expenses, and otherwise adversely affect our financial condition, results of operations, and cash flows. Our business, financial condition, results of operations, access to credit, and trading price of common stock could be materially and adversely affected if the economy fails to stabilize, or if current economic conditions do not improve or worsen.

Our financial success is influenced by the success of our customers.

Much of our financial success is directly related to the success of our retailers and distributors to market and sell our brands through to the consumer. If a retailer fails to meet annual sales goals, it may be difficult to locate an acceptable substitute retailer. If a distributor fails to meet annual sales goals, it may be difficult and costly to either locate an acceptable substitute distributor or convert to a wholesale direct model. If a change becomes necessary, we may experience increased costs, loss of customers, increased credit risk, and increased inventory risk, as well as substantial disruption to operations and a potential loss of sales.

We currently do not have long-term contracts with any of our customers. Sales to our customers are generally on an order-by-order basis and are subject to rights of cancellation and rescheduling by our wholesale customers. We use the timing of delivery dates in our wholesale customer orders to forecast our

10

sales and earnings for future periods. If any of our major customers, including independent distributors, experience a significant downturn in business or fail to remain committed to our products or brands, then these customers could postpone, reduce, or discontinue purchases from us. As a result, we could experience a decline in sales or gross margins, write downs of excess inventory, increased discounts or extended credit terms to our customers, which could have a material adverse effect on our business, results of operations, financial condition, cash flows, and our common stock price.

Our five largest customers accounted for approximately 28.9% of worldwide net sales in 2010 and 30.0% of worldwide net sales in 2009. Any loss of a key customer, the financial collapse or bankruptcy of a key customer, or a significant reduction in purchases from a key customer could have a material adverse effect on our business, results of operations and financial condition.

Our new and existing retail stores may not realize returns on our investments.

Our retail segment has grown substantially in both net sales and total assets during the past year, and we intend to rapidly expand this segment in the future. We have entered into significant long-term leases for certain of our retail locations. Global store openings involve substantial investments, including constructing leasehold improvements, furniture and fixtures, equipment, information systems, inventory and personnel. In addition, since certain of our retail store costs are fixed, if we have insufficient sales, we may be unable to reduce expenses in order to avoid losses or negative cash flows. Due to the high fixed cost structure associated with the retail segment, negative cash flows or the closure of a store could result in write-downs of inventory and leasehold improvements, severance costs, significant lease termination costs, impairment losses on long-lived assets, or loss of our working capital, which could adversely impact our financial position, results of operations, or cash flows.

If we do not accurately forecast consumer demand, we may have excess inventory to liquidate or have difficulty filling our customers' orders.

Because the footwear industry has relatively long lead times for design and production, we must plan our production tooling and projected volumes many months before consumer tastes become apparent. The footwear industry is subject to rapid changes in consumer preferences, as well as the effects of weather, general market conditions, competition, and other factors affecting demand. A large number of models, colors and sizes in our product lines can increase these risks. As a result, we may fail to accurately forecast styles, colors and features that will be in demand. If we overestimate demand for any products or styles, we may be forced to provide additional marketing assistance, incur higher markdowns, or sell excess inventories at reduced prices resulting in lower, or negative, gross margins.

Our success depends on our ability to anticipate fashion trends.

Our success depends largely on the continued strength of our brands, on our ability to anticipate, understand and react to the rapidly changing fashion tastes of footwear and accessory consumers and to provide appealing merchandise in a timely and cost effective manner. Our products must appeal to a broad range of consumers whose preferences cannot be predicted with certainty and are subject to rapid change. We are also dependent on customer receptivity to our products and marketing strategy. There can be no assurance that consumers will continue to prefer our brands or that we will (1) respond quickly enough to changes in consumer preferences, (2) market our products successfully, or (3) successfully introduce acceptable new models and styles of footwear or accessories to our target consumer. Achieving market acceptance for new products also will likely require us to exert substantial product development and marketing efforts and expend significant funds to attract consumers. A failure to introduce new products that gain market acceptance or maintain market share with our current products would erode our competitive position, which would reduce our profits and could adversely affect the image of our brands, resulting in long-term harm to our business.

11

Our UGG brand has experienced strong growth over the past several years, with double-digit increases in net wholesale sales of UGG products. We cannot anticipate how long we will continue sustaining this growth rate in the future. UGG products include fashion items that could go out of style at any time. UGG products represent a majority of our business, and if UGG product sales were to decline or fail to increase in the future, our overall financial performance and common stock price would be adversely affected.

Many of our products are seasonal, and our sales are sensitive to weather conditions.

Sales of our products are highly seasonal and are sensitive to weather conditions. For example, extended periods of unseasonably warm weather during the fall and winter months may reduce demand for our UGG products. Even though we are creating more year-round styles for our brands, the effect of favorable or unfavorable weather on sales can be significant enough to affect our quarterly results, with a resulting effect on our common stock price.

We may not succeed in implementing our growth strategies.

As part of our growth strategy, we seek to enhance the positioning of our brands, extend our brands into complementary product categories and markets, partner with or acquire compatible companies, expand geographically, increase our retail presence, and improve our operational performance. We continue to expand the nature and scope of our operations considerably, including significantly increasing the number of employees worldwide. We anticipate that substantial further expansion will be required to realize our growth potential and new market opportunities.

We are growing globally through our retail, eCommerce, wholesale, consignment, and distributor channels. In addition, as part of our international growth strategy, we intend to continue reacquiring distribution rights from select distributors and transition from third-party distribution to direct distribution through wholly-owned subsidiaries. Implementing our growth strategies, or failure to effectively execute them, could affect near term revenues from the postponement of sales recognition to future periods, our rate of growth or profitability, which in turn could have a negative effect on the value of our common stock. In addition, our growth initiatives could:

- •

- increase our working capital needs beyond our capacity;

- •

- increase costs if we fail to successfully integrate a newly acquired business or achieve expected cost savings;

- •

- result in impairment charges related to newly acquired businesses;

- •

- create remote-site management issues, which would adversely affect our internal control environment;

- •

- have significant domestic or international legal or compliance implications;

- •

- make it difficult to attract, retain, and manage adequate human resources in remote locations;

- •

- cause additional inventory manufacturing, distribution, and management costs;

- •

- cause us to experience difficulty in filling customer orders;

- •

- result in distribution termination transaction costs; or

- •

- create other production, distribution, and operating difficulties.

Failure to adequately protect our trademarks, patents and other intellectual property rights or deter counterfeiting could diminish the value of our brands and reduce sales.

We believe that our trademarks and other intellectual property rights are of value and are integral to our success and our competitive position. Some countries' laws do not protect intellectual property rights

12

to the same extent as do US laws. From time to time, we discover counterfeit products in the marketplace that infringe upon our intellectual property rights. If we are unsuccessful in challenging a third party's products on the basis of patent, trademark and trade dress rights, particularly in some foreign countries, this could adversely affect our continued sales, financial condition and results of operation. If our brands are associated with infringers' or competitors' inferior products, this could also adversely affect the integrity of our brands. Furthermore, our efforts to enforce our intellectual property rights are typically met with defenses and counterclaims attacking the validity and enforceability of our intellectual property rights.

Similarly, from time to time we may need to defend against claims that the word "ugg" is a generic term and that "UGG Australia" should not be registered as a trademark. Such a claim was successful in Australia, but such claims have been rejected by courts in the United States and in the Netherlands. Any decision or settlement in any of these matters that prevents trademark protection of the "UGG Australia" brand in our major markets, or that allows a third party to continue to use our brand trademarks in connection with the sale of products similar to our products, or to continue to manufacture or distribute counterfeit products could result in intensified commercial competition and could have a material adverse effect on our results of operations and financial condition. Unplanned increases in legal fees and other costs associated with the defense of our intellectual property or rebranding could result in higher operating expenses and lower earnings.

Our goodwill and other intangible assets may incur impairment losses.

We conducted our annual impairment tests of goodwill and other intangible assets for 2010, 2009, and 2008. In addition, we conducted interim impairment evaluations when impairment indicators arose. In 2010, we did not recognize any impairment charges on our goodwill and other intangible assets. We recognized the following impairment charges in 2009 and 2008 in our income from operations:

| |

Years Ended December 31, | ||||||

|---|---|---|---|---|---|---|---|

| |

2009 | 2008 | |||||

Teva trademarks |

$ | — | $ | 20,400 | |||

Teva goodwill |

— | 11,929 | |||||

Other brands trademarks |

1,000 | — | |||||

Other brands goodwill |

— | 3,496 | |||||

Total impairment loss on intangible assets |

$ | 1,000 | $ | 35,825 | |||

If any brand's product sales or operating margins decline to a point that the fair value falls below its carrying value, we may be required to further write down the related intangible assets. These or other related declines could cause us to incur additional impairment losses, which could materially affect our consolidated financial statements and results of operations. The value of our trademarks is highly dependent on forecasted revenues and earnings before interest and taxes for our brands, as well as derived discount and royalty rates. In addition, the valuation of intangible assets is subject to a high degree of judgment and complexity. We may also decide to discontinue a brand which would result in the write down of all related intangible assets. The balances of goodwill and nonamortizable intangibles by brand are as follows:

| |

As of December 31, 2010 | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

UGG | Teva | Other Brands | Total | |||||||||

Trademarks |

$ | 152 | $ | 15,300 | $ | — | $ | 15,452 | |||||

Goodwill |

6,101 | — | 406 | 6,507 | |||||||||

Total nonamortizable intangibles |

$ | 6,253 | $ | 15,300 | $ | 406 | $ | 21,959 | |||||

13

If raw materials do not meet our specifications, or experience price increases or shortages, we could realize interruptions in manufacturing, increased costs, higher product return rates, a loss of sales, or a reduction in our gross margins.

We depend on a limited number of key sources for certain raw materials like sheepskin, the principal raw material of our UGG Classic products. The top grade sheepskin used in UGG products is in high demand and limited supply. The supply of sheepskin can be adversely impacted by weather conditions, disease, and harvesting decisions that are completely outside our control. The potential inability to obtain top grade raw materials could impair our ability to meet our production requirements and could lead to inventory shortages, which can result in lost sales, delays in shipments to customers, strain on our relationships with customers and diminished brand loyalty. There have also been significant increases in the prices of top grade sheepskin as the demand from competitors for this material has increased. Any price increases in key raw materials will likely raise our costs and decrease our profitability unless we are able to commensurately increase our selling prices.

Our independent manufacturers use various raw materials in the production of our footwear and accessories that must meet our design specifications and, in some cases, additional technical requirements for performance footwear. If these raw materials and the end product do not conform to our specifications, we could experience a higher rate of customer returns and deterioration in the image of our brands, which could have a material adverse effect on our business, results of operations, and financial condition.

Because we depend on independent manufacturers, we face challenges in maintaining a continuous supply of finished goods that meet our quality standards.

Most of our production is performed by a limited number of independent manufacturers in China. We depend on these manufacturers' ability to finance the production of goods ordered and to maintain manufacturing capacity, and store completed goods pending shipment in a safe and sound location. We do not possess direct control over either the independent manufacturers or their materials suppliers, so we may be unable to obtain timely and continuous delivery of acceptable products. In addition, while we do have long standing relationships with most of our factories, we currently do not have long-term contracts with these independent manufacturers, and any of them may unilaterally terminate their relationship with us at any time or seek to increase the prices they charge us. As a result, we are not assured of an uninterrupted supply of acceptable quality and competitively priced products from our independent manufacturers. If there is an interruption, we may not be able to substitute suitable alternative manufacturers to provide products or services of a comparable quality at an acceptable price or on a timely basis. If a change in our independent manufacturers becomes necessary, we would likely experience increased costs as well as substantial disruption of our business, which could result in a loss of sales and earnings.

Interruptions in the supply chain can also result from natural disasters and other adverse events that would impair our manufacturers' operations. We keep proprietary materials involved in the production process, such as shoe molds, knives, and raw materials, under the custody of our independent manufacturers. If these independent manufacturers were to experience loss or damage to our proprietary materials involved in the production process, we cannot be assured that such independent manufacturers would have adequate insurance to cover such loss or damage and, in any event, the replacement of such materials would likely result in significant delays in the production of our products and could result in a loss of sales and earnings.

14

Our independent manufacturers are located outside the US, where we are subject to the risks of international commerce.

Substantially all of our independent manufacturers are in China and Vietnam, with the vast majority of production performed by a limited number of manufacturers in China. Foreign manufacturing is subject to numerous risks, including the following:

- •

- tariffs, import and export controls and other non-tariff barriers such as quotas and local content rules on

raw materials and finished products, including the potential threat of anti-dumping duties and quotas such as those which have been imposed by the European Union on the import of certain

types of footwear from China and Vietnam;

- •

- increasing transportation costs;

- •

- poor infrastructure and shortages of equipment, which can disrupt transportation and utilities;

- •

- restrictions on the transfer of funds;

- •

- changing economic conditions;

- •

- violations or changes in governmental policies and regulations including labor, safety, and environmental regulations in

China, Vietnam, the US and elsewhere;

- •

- refusal to adopt or comply with our Factory Charter, Ethical Supply Chain guidelines, and Restricted Substances Policy;

- •

- customary business traditions in China and Vietnam such as local holidays, which are traditionally accompanied by high

levels of turnover in the factories;

- •

- labor unrest, which can lead to work stoppages and interruptions in transportation or supply;

- •

- delays during shipping, at the port of entry, or at the port of departure;

- •

- political instability, which can interrupt commerce;

- •

- use of unauthorized or prohibited materials or reclassification of materials;

- •

- expropriation and nationalization; and

- •

- adverse changes in consumer perception of goods, trade or political relations with China and Vietnam.

These factors could severely interfere with the manufacture or shipment of our products, which could make it difficult to obtain adequate supplies of quality products when we need them, thus materially affecting our sales and results of operations. While we periodically visit and audit the operations of our independent manufacturers, we do not control their business practices. If we discovered non-compliant manufacturers or suppliers that cannot or will not become compliant, we would cease dealing with them, and we could suffer an interruption in our product supply chain. In addition, the manufacturers' or designated suppliers' actions could damage our reputation and the value of our brands, resulting in negative publicity and discouraging customers and consumers from buying our products.

We conduct business outside the US, which exposes us to foreign currency, global liquidity, and other risks.

As we increase our international operations, our sales and expenditures in foreign currencies will become more material and subject to currency fluctuations and global credit markets. A significant portion of our international operating expenses are paid in local currencies. Also, our foreign distributors sell in local currencies, which impacts the price to foreign customers. Effective January 1, 2011, our business changed such that certain of our subsidiaries' functional currency designations changed from US dollars to the local currencies. We currently utilize forward contracts or other derivative instruments to mitigate exposure to fluctuations in the foreign currency exchange rate, for the amounts we expect to purchase and sell in foreign currencies. As we expand international operations and increase purchases and sales in

15

foreign currencies, we will evaluate and may utilize additional derivative instruments, as needed, to hedge our foreign currency exposures. Our hedging strategies depend on our forecasts of sales, expenses and cash flows, which are inherently subject to inaccuracies. Therefore, our hedging strategies may be ineffective. Future changes in foreign currency exchange rates and global credit markets may cause changes in the US dollar value of our purchases or sales and materially affect our sales, profit margins or results of operations, when converted to US dollars. In addition, the failure of financial institutions that underwrite our derivative contracts may negate our efforts to hedge our foreign currency exposures and result in material foreign currency or contract losses. Foreign currency hedging activities, transactions, or translations could materially impact our financial statements.

While our purchases from overseas factories are currently denominated in US dollars, certain operating and manufacturing costs of the factories are denominated in other currencies. As a result, fluctuations in these currencies versus the US dollar could impact our purchase prices from the factories in the event that they adjust their selling prices accordingly.

The currency exchange rate between US dollars and the Chinese Renminbi (RMB) could adversely affect our financial condition.

To the extent we need to convert US dollars into RMB for our operational needs, our financial position and the price of our common stock may be adversely affected should the RMB appreciate against the US dollar. Conversely, if we decide to convert our RMB into US dollars for operational needs, the dollar equivalent of earnings from our subsidiaries in China would be reduced should the US dollar appreciate against the RMB.

In 2005, the People's Republic of China revalued its currency and abandoned its peg to the US dollar. Under this policy, which was halted in 2008 due to the worldwide financial crisis, the RMB was permitted to fluctuate within a narrow and managed band against a basket of certain foreign currencies. In June 2010, the Chinese government announced its intention to again allow the RMB to fluctuate within the 2005 parameters. It is possible that the Chinese government could adopt an even more flexible currency policy, which could result in further and more significant appreciation of the RMB against the US dollar. We currently source substantially all production from China. While our purchases from the Chinese factories are currently denominated in US dollars, certain operating and manufacturing costs of the factories are denominated in the RMB. As a result, any further revaluations in the RMB versus the US dollar could impact our purchase prices from the factories in the event that they adjust their selling prices accordingly. Any increase in our footwear purchase costs will reduce our gross margin unless we are able to raise our selling prices to our customers in order to compensate for the increased costs.

Key business processes and supporting information systems could be interrupted and adversely affect our business.

Our future success and growth depend on the continued operation of our key business processes, including information systems, global communications, the internet, and key personnel. Hackers and computer viruses have disrupted operations at many major companies. We may be vulnerable to similar acts of sabotage. Key processes could also be interrupted by a failure due to weather, natural disaster, power loss, telecommunications failure, failure of our computer systems, sabotage, terrorism, or similar event such that:

- •

- critical business systems become inoperable or require significant costs to restore;

- •

- key personnel are unable to perform their duties, communicate, or access information systems;

- •

- significant quantities of merchandise are damaged or destroyed;

- •

- we are required to make unanticipated investment in state-of-the-art technologies and security measures;

16

- •

- key wholesale customers cannot place or receive orders;

- •

- eCommerce customer orders may not be received or fulfilled;

- •

- we are exposed to unanticipated liabilities; or

- •

- carriers cannot ship or unload shipments.

These interruptions to key business processes could have a material adverse effect on our business and operations and result in lost sales and reduced earnings.

We rely on our information management, internet cloud providers and other enterprise resource planning systems to operate our business, prepare forecasts and track our operating results. Our information management and enterprise planning systems will require modification and refinement as we grow and our business needs change. We may experience difficulties in transitioning to new or upgraded information technology systems, including loss of data, unreliable data, and decreases in productivity as our personnel become familiar with the new systems. If we experience a significant system failure or if we are unable to competitively modify our information management systems to respond to changes in our business needs, then our ability to properly run our business and report financial results could be adversely affected.

The loss of the services and expertise of any key employee could also harm our business. Our future success depends on our ability to identify, attract and retain qualified personnel on a timely basis.

We could be adversely affected by the loss of our warehouses.

The warehousing of our inventory is located at a limited number of self-managed domestic and primarily third party managed international facilities, the loss of any of which could adversely impact our sales, business performance and operating results. In addition, we could face a significant disruption in our domestic distribution center operations if our automated pick module does not perform as anticipated or ceases to function for an extended period.

The costs of production and transportation of our products can increase as petroleum and other energy prices rise, or demand for ocean containers or other means of transportation exceed existing supply.

The manufacture and transportation of our products requires the use of petroleum-based materials and energy costs. Any future increases in the costs of, or interruption of access to, these materials and energy sources could increase the cost of our goods which would reduce our gross margins unless we can successfully raise our selling prices to compensate for the increased costs. In addition, we rely on ocean carriers and other freight companies to transport our goods. In the event demand for transportation exceeds existing capacity, additional costs will be incurred which will increase our cost of goods sold and could decrease our profitability.

Our sales in international markets are subject to a variety of laws and political and economic risks that may adversely impact our sales and results of operations in certain regions, which could increase our costs and adversely impact our operating results.

Our ability to capitalize on growth in new international markets and to maintain the current level of operations in our existing international markets is subject to risks associated with international operations and joint ventures with international partners that could adversely affect our sales and results of operations. These include:

- •

- changes in currency exchange rates, which impact the price to international consumers;

- •

- ability to move currency out of international markets;

- •

- the burdens of complying with a variety of foreign laws and regulations;

- •

- legal costs and penalties related to defending allegations of non-compliance;

17

- •

- unexpected changes in regulatory requirements;

- •

- inability to fulfill import tariff quota requirements;

- •

- changes in tax laws;

- •

- complications due to lack of familiarity with local customs;

- •

- difficulties associated with promoting products in unfamiliar cultures;

- •

- political instability;

- •

- changes in diplomatic and trade relationships; and

- •

- general economic fluctuations in specific countries or markets.

International trade and import regulations may impose unexpected duty costs or other non-tariff barriers to markets while the increasing number of free trade agreements has the potential to stimulate increased competition; security procedures may cause significant delays.

Products manufactured overseas and imported into the US and other countries are subject to import duties. While we have implemented internal measures to comply with applicable customs regulations and to properly calculate the import duties applicable to imported products, customs authorities may disagree with our claimed tariff treatment for certain products, resulting in unexpected costs that may not have been factored into the sales price of the products and our forecasted gross margins.

We cannot predict whether future domestic laws, regulations or trade remedy actions or international agreements may impose additional duties or other restrictions on the importation of products from one or more of our sourcing venues. Such changes could increase the cost of our products, require us to withdraw from certain restricted markets or change our business methods, and could generally make it difficult to obtain products of our customary quality at a competitive price. Meanwhile, the continued negotiation of bilateral and multilateral free trade agreements by the US and our other market countries with countries other than our principal sourcing venues may stimulate competition from manufacturers in these other sourcing venues, which now export, or may seek to export, footwear and accessories to our target markets at preferred rates of duty, which may have an effect on our sales and operations.

In 2006, the European Commission imposed definitive duties on leather upper footwear originating from China and certain other countries imported into European Member states. These duties were effective for a two-year period with a final 16.5% rate for China-sourced footwear and 10% on Vietnam-sourced footwear. In December 2009, the European Commission decided to extend the duties for a 15 month period, and accordingly, the duties are extended through March 31, 2011. Any increase in duties or the requirement for quotas will increase the cost of our products and may limit the amount of China and Vietnam sourced products that we are able to sell to the European market. The extension of anti-dumping duties or quotas on products manufactured in China and Vietnam may impact our sales and gross margins in the European market.

Additionally, the increased threat of terrorist activity and law enforcement responses to this threat have required greater levels of inspection of imported goods and have caused delays in bringing imported goods to market. Any tightening of security procedures, for example, in the aftermath of a terrorist incident, could worsen these delays and increase our costs.

The investment of our substantial cash and cash equivalents and short-term investments are subject to risks, which may cause losses and affect the liquidity of these investments.

At December 31, 2010 we had cash and cash equivalents of $445,226. A portion of these are held as cash in operating accounts that are with third party financial institutions. These balances routinely exceed the Federal Deposit Insurance Corporation (FDIC) insurance limits. While we regularly monitor the cash balances in our operating accounts and adjust the balances as appropriate, these cash balances could lose

18

value or become inaccessible if the underlying financial institutions fail or are subject to other adverse conditions in the financial markets. To date, we have experienced no loss or lack of access to cash in our operating accounts.

The remainder of our cash and cash equivalents and short-term investments are invested in funds managed by third party investment management institutions. These investments include US treasuries and government agencies, money market funds, and municipal bonds, among other investments. Certain of these investments are subject to general credit, liquidity, market, and interest rate risks. While we do not hold any investments whose value is directly correlated to mortgage debt, investment risk has been and may further be exacerbated by US mortgage defaults and credit and liquidity issues, which have affected various sectors of the financial markets. To date, we have experienced no material loss or lack of access to our cash and cash equivalents and short-term investments. However, we can provide no assurance that access to our cash and cash equivalents and short-term investments, or their earning potential, will not be impacted by adverse conditions in the financial markets. These market risks associated with our investment portfolio may have an adverse effect on our results of operations, liquidity and financial condition.

The tax laws applicable to our business are very complicated and we may be subject to additional income tax liabilities as a result of audits by various taxing authorities or changes in tax laws applicable to our business.

We conduct our operations through subsidiaries in several countries including the US, the UK, Japan, China, Hong Kong, the Netherlands and Bermuda. As a result, we are subject to tax laws and regulations in each of those jurisdictions, and to tax treaties between the US and other nations. These tax laws are highly complex, and significant judgment and specialized expertise is required in evaluating and estimating our worldwide provision for income taxes.

We are subject to audits in each of the various jurisdictions where we conduct business, and any of these jurisdictions may assess additional income taxes against us as a result of their audits. Although we believe our tax estimates are reasonable, and we undertake to prepare our tax filings in accordance with all applicable tax laws, the final determination with respect to any tax audits, and any related litigation, could be materially different from our estimates or from our historical income tax provisions and accruals. The results of an audit or litigation could have a material effect on our operating results or cash flows in the periods for which that determination is made and may require a restatement of prior financial reports at a material cost. In addition, future period earnings may be adversely impacted by litigation costs, settlements, penalties, or interest assessments.

We are also subject to constant changes in tax laws, regulations and treaties in and between the nations in which we operate. Our income tax expense is based upon our interpretation of the tax laws in effect in various countries at the time that the expense was incurred. A change in these tax laws, treaties or regulations, including those in and involving the US, or in the interpretation thereof, could result in a materially higher tax expense or a higher effective tax rate on our worldwide earnings. For example, on February 1, 2010, the US Department of the Treasury released a general explanation of the Obama administration's tax proposals for its fiscal year 2011 budget, which describes a number of proposed amendments to the international provisions of the US Internal Revenue Code that may be applicable to our business. It is possible that these proposals could result in changes to the existing US tax laws that affect us. We are unable to predict whether any of these or other proposals will ultimately be enacted. Any such changes could increase our income tax liability and adversely affect our net income and long term effective tax rates.

We face intense competition, including competition from companies with significantly greater resources than ours, and if we are unable to compete effectively with these companies, our market share may decline and our business could be harmed.

The footwear industry is highly competitive, and many new competitors have entered into the marketplace, as well as increased competition from established companies. A number of our competitors

19

have significantly greater financial, technological, engineering, manufacturing, marketing and distribution resources than we do, as well as greater brand awareness in the footwear and accessory markets. Our competitors include athletic and footwear companies, branded apparel companies and retailers with their own private labels. Their greater capabilities in these areas may enable them to better withstand periodic downturns in the footwear industry, compete more effectively on the basis of price and production, and more quickly develop new products. In addition, access to offshore manufacturing has made it easier for new companies to enter the markets in which we compete, further increasing competition in the footwear and accessory industries.

Additionally, efforts by our competitors to dispose of their excess inventories may significantly reduce prices that we can expect to receive for the sale of our competing products and may cause our customers to shift their purchases away from our products. If we fail to compete successfully in the future, our sales and earnings will decline, as will the value of our business, financial condition and common stock price.

Our common stock price has been volatile, which could result in substantial losses for stockholders.

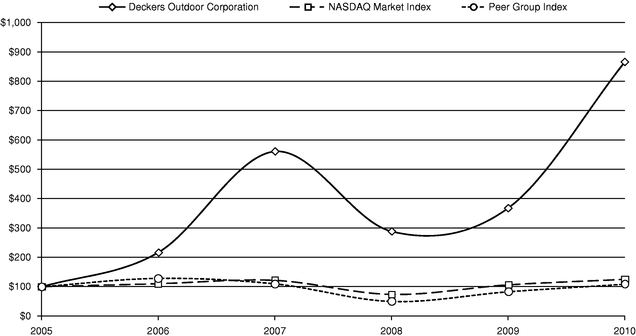

Our common stock is traded on the NASDAQ Global Select Market. While our average daily trading volume for the 52-week period ended February 15, 2011 was approximately 1,420,000 shares, we have experienced more limited volume in the past and may do so in the future. The trading price of our common stock has been and may continue to be volatile. The closing prices of our common stock, as reported by the NASDAQ Global Select Market, have ranged from $33.71 to $87.02 for the 52-week period ended February 15, 2011. The trading price of our common stock could be affected by a number of factors, including, but not limited to the following:

- •

- changes in expectations of our future performance, whether realized or perceived;

- •

- changes in estimates by securities analysts or failure to meet such estimates;

- •

- published research and opinions by securities analysts and other market forecasters;

- •

- changes in our credit ratings;

- •

- the financial results and liquidity of our customers;

- •

- shift of revenue recognition as a result of changes in our distribution model, delivery of merchandise, or entering into

agreements with related parties;

- •

- claims brought against us by a regulatory agency or our stockholders;

- •

- quarterly fluctuations in our sales, expenses, and financial results;

- •

- general equity market conditions and investor sentiment;

- •

- economic conditions and consumer confidence;

- •

- broad market fluctuations in volume and price;

- •

- increasing short sales of our stock;

- •

- announcements to repurchase our stock;

- •

- the declaration of stock or cash dividends; and

- •

- a variety of risk factors, including the ones described elsewhere in this Annual Report on Form 10-K and in our other periodic reports.

In addition, the stock market in general has experienced extreme price and volume fluctuations that have often been unrelated or disproportionate to the operating performance of individual companies. Accordingly, the price of our common stock is volatile and any investment in our stock is subject to risk of loss. These broad market and industry factors and other general macroeconomic conditions unrelated to our financial performance may also affect our common stock price.

20

Item 1B. Unresolved Staff Comments.

None.