Attached files

Table of Contents

Index to Financial Statements

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2010

or

¨ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission file number 001-33556

SPECTRA ENERGY PARTNERS, LP

(Exact name of registrant as specified in its charter)

| Delaware | 41-2232463 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) | |

| 5400 Westheimer Court, Houston, Texas | 77056 | |

| (Address of principal executive offices) | (Zip Code) | |

713-627-5400

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class |

Name of Each Exchange on Which Registered | |

| Common Units Representing Limited Partner Interests | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer x | Accelerated filer ¨ | Non-accelerated filer ¨ | Smaller reporting company ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Securities Exchange Act). Yes ¨ No x

Estimated aggregate market value of the Common Units held by non-affiliates of the registrant at June 30, 2010: $720,000,000.

At January 31, 2011, there were 89,150,429 Common Units and 1,819,396 General Partner Units outstanding.

Table of Contents

Index to Financial Statements

SPECTRA ENERGY PARTNERS, LP

FORM 10-K FOR THE YEAR ENDED

DECEMBER 31, 2010

| Item |

Page | |||||

| PART I. | ||||||

| 1. | 4 | |||||

| 4 | ||||||

| 4 | ||||||

| 4 | ||||||

| 5 | ||||||

| 5 | ||||||

| 6 | ||||||

| 6 | ||||||

| 8 | ||||||

| 10 | ||||||

| 11 | ||||||

| 12 | ||||||

| 12 | ||||||

| 12 | ||||||

| 13 | ||||||

| 13 | ||||||

| 15 | ||||||

| 1A. |

16 | |||||

| 1B. |

34 | |||||

| 2. |

35 | |||||

| 3. |

35 | |||||

| 4. |

35 | |||||

| PART II. | ||||||

| 5. |

36 | |||||

| 6. |

38 | |||||

| 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

40 | ||||

| 7A. |

58 | |||||

| 8. |

59 | |||||

| 9. |

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

88 | ||||

| 9A. |

88 | |||||

| 9B. |

89 | |||||

| PART III. | ||||||

| 10. |

90 | |||||

| 11. |

95 | |||||

| 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Unitholder Matters |

113 | ||||

| 13. |

Certain Relationships and Related Transactions, and Director Independence |

114 | ||||

| 14. |

118 | |||||

| PART IV. | ||||||

| 15. |

119 | |||||

| 120 | ||||||

2

Table of Contents

Index to Financial Statements

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING INFORMATION

This document includes forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Forward-looking statements are based on management’s beliefs and assumptions. These forward-looking statements are identified by terms and phrases such as: anticipate, believe, intend, estimate, expect, continue, should, could, may, plan, project, predict, will, potential, forecast, and similar expressions. Forward-looking statements involve risks and uncertainties that may cause actual results to be materially different from the results predicted. Factors that could cause actual results to differ materially from those indicated in any forward-looking statement include, but are not limited to:

| • | state and federal legislative and regulatory initiatives that affect cost and investment recovery, have an effect on rate structure, and affect the speed at and degree to which competition enters the natural gas industries; |

| • | outcomes of litigation and regulatory investigations, proceedings or inquiries; |

| • | weather and other natural phenomena, including the economic, operational and other effects of hurricanes and storms; |

| • | the timing and extent of changes in interest rates; |

| • | general economic conditions, including the risk of a prolonged economic slowdown or decline, or the risk of delay in a recovery, which can affect the long-term demand for natural gas and related services; |

| • | potential effects arising from terrorist attacks and any consequential or other hostilities; |

| • | changes in environmental, safety and other laws and regulations; |

| • | the development of alternative energy resources; |

| • | results of financing efforts, including the ability to obtain financing on favorable terms, which can be affected by various factors, including credit ratings and general market and economic conditions; |

| • | increases in the cost of goods and services required to complete capital projects; |

| • | growth in opportunities, including the timing and success of efforts to develop domestic pipeline, storage, gathering and other infrastructure projects and the effects of competition; |

| • | the performance of natural gas transmission, storage and gathering facilities; |

| • | the extent of success in connecting natural gas supplies to transmission and gathering systems and in connecting to expanding gas markets; |

| • | the effects of accounting pronouncements issued periodically by accounting standard-setting bodies; |

| • | conditions of the capital markets during the periods covered by these forward-looking statements; and |

| • | the ability to successfully complete merger, acquisition or divestiture plans; regulatory or other limitations imposed as a result of a merger, acquisition or divestiture; and the success of the business following a merger, acquisition or divestiture. |

In light of these risks, uncertainties and assumptions, the events described in the forward-looking statements might not occur or might occur to a different extent or at a different time than Spectra Energy Partners, LP has described. Spectra Energy Partners, LP undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

3

Table of Contents

Index to Financial Statements

PART I

The terms “we,” “our,” “us,” and “Spectra Energy Partners” as used in this report refer collectively to Spectra Energy Partners, LP and its subsidiaries unless the context suggests otherwise. These terms are used for convenience only and are not intended as a precise description of any separate legal entity within Spectra Energy Partners.

Spectra Energy Partners, LP, through its subsidiaries and equity affiliates, is engaged in the transportation and gathering of natural gas through interstate pipeline systems with over 3,100 miles of pipelines that serve the southeastern quadrant of the United States and the storage of natural gas in underground facilities with aggregate working gas storage capacity of approximately 49 billion cubic feet (Bcf) that are located in southeast Texas, south central Louisiana and southwest Virginia. We are a Delaware master limited partnership (MLP) formed on March 19, 2007. Our common units are listed on the New York Stock Exchange (NYSE) under the symbol “SEP.” Our internet website is http://www.spectraenergypartners.com.

We transport, gather and store natural gas for a broad mix of customers, including local gas distribution companies (LDCs, companies that obtain a major portion of their revenues from retail distribution systems for the delivery of natural gas for ultimate consumption), municipal utilities, interstate and intrastate pipelines, direct industrial users, electric power generators, marketers and producers, and exploration and production companies. In addition to serving the directly connected southeastern quadrant of the United States, our pipeline, storage and gathering systems have access to customers in the mid-Atlantic, northeastern and midwestern regions of the United States through numerous interconnections with major pipelines. Our rates are regulated under the Federal Energy Regulatory Commission’s (FERC’s) rate-making policies with the exception of Market Hub Partners Holding’s (Market Hub’s) intrastate storage operations and our gathering facilities. The FERC is the U.S. agency that regulates the transportation of natural gas in interstate commerce.

Our operations and activities are managed by our general partner, Spectra Energy Partners (DE) GP, LP, which in turn is managed by its general partner, Spectra Energy Partners GP, LLC, (the General Partner). The General Partner is wholly owned by a subsidiary of Spectra Energy Corp (Spectra Energy). Spectra Energy is a separate, publicly traded entity which trades on the NYSE under the symbol “SE.” As of December 31, 2010, Spectra Energy and its subsidiaries collectively owned 69% of us and the remaining 31% was publicly owned.

On July 2, 2007, immediately prior to the closing of our initial public offering (IPO), Spectra Energy contributed to us 100% of the ownership of East Tennessee Natural Gas, LLC (East Tennessee), 50% of the ownership of Market Hub and a 24.5% interest in Gulfstream Natural Gas System, L.L.C. (Gulfstream). Spectra Energy indirectly owned 100% of us prior to the closing of the IPO. On July 2, 2007, we issued 11.5 million common units to the public, representing 17% of our outstanding equity.

In 2008, we completed the acquisition of the equity interests of Saltville Gas Storage Company L.L.C. (Saltville) and the P-25 pipeline from a wholly owned subsidiary of Spectra Energy at a purchase price of $107.0 million, which included the issuance of 4.2 million common units and 0.1 million general partner units, and a cash payment of $4.7 million to Spectra Energy.

4

Table of Contents

Index to Financial Statements

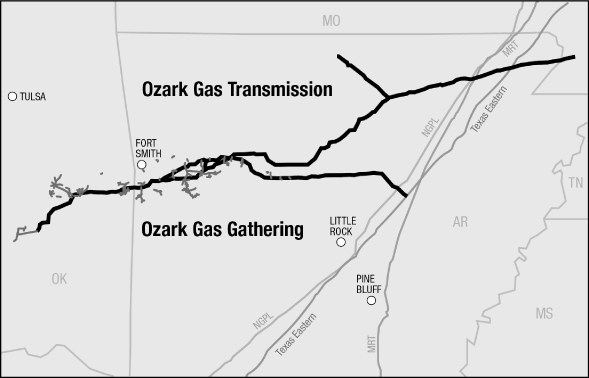

In 2009, we acquired all of the ownership interests of NOARK Pipeline System, Limited Partnership (NOARK) from Atlas Pipeline Partners, L.P. (Atlas) for approximately $294.5 million in cash. NOARK’s assets consist of 100% ownership interests of Ozark Gas Transmission, L.L.C. (Ozark Gas Transmission) and Ozark Gas Gathering, L.L.C. (Ozark Gas Gathering) (collectively referred to as “Ozark”). This transaction was partially refinanced in 2009 through a sale of 9.8 million common units.

In the fourth quarter of 2010, we acquired an additional 24.5% interest in Gulfstream from a wholly owned subsidiary of Spectra Energy for the aggregate consideration of $330.0 million, consisting of $66.0 million of newly issued units, the assumption of approximately $7.4 million in debt owed to a subsidiary of Spectra Energy and a cash payment of $256.6 million to Spectra Energy. Following the acquisition, we own a 49% interest in Gulfstream.

For financial information on our acquisitions, see Item 8. Financial Statements and Supplementary Data, Note 2 of Notes to Consolidated Financial Statements.

Gas Transportation and Storage

Our sole segment, Gas Transportation and Storage, includes East Tennessee, Saltville and Ozark. Gas Transportation and Storage provides interstate transportation, storage, fee-based gathering of natural gas, and storage and redelivery of liquefied natural gas (LNG, natural gas that has been converted to liquid form) for customers in the southeastern quadrant of the United States. These operations are mainly subject to the FERC’s and the Department of Transportation’s (DOT’s) rules and regulations.

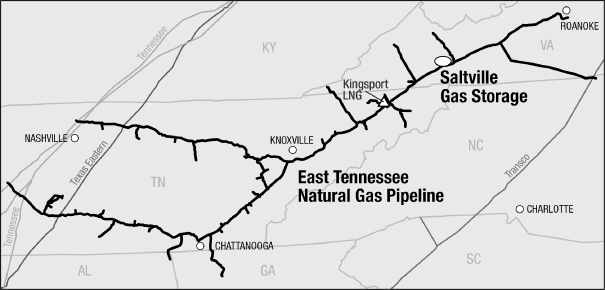

General

We own and operate 100% of the 1,510-mile East Tennessee interstate natural gas transportation system, which extends from central Tennessee eastward into southwest Virginia and northern North Carolina, and southward into northern Georgia. East Tennessee supports the energy demands of the southeast and mid-Atlantic regions of the United States through connections to 31 receipt points and 179 delivery points and has market

5

Table of Contents

Index to Financial Statements

delivery capability of approximately 1.5 billion cubic feet per day (Bcf/d) of natural gas. East Tennessee also owns and operates a LNG storage facility in Kingsport, Tennessee with a working gas storage capacity of 1.1 Bcf and regasification capability of 150 million cubic feet per day (MMcf/d).

During the first quarter of 2010, East Tennessee executed a precedent agreement with the Tennessee Valley Authority for the Northeastern Tennessee Project (NET), and received full FERC certification in October 2010. This project will provide 150,000 dekatherms per day (Dth/d) of gas service to a generation plant in Hawkins County, Tennessee. The $135 million project is expected to be in service in the third quarter of 2011.

We own and operate 100% of the Saltville natural gas storage facilities which consist of 5.5 Bcf of total storage capacity. The storage facilities interconnect with the East Tennessee system in southwest Virginia and offer high deliverability salt cavern and reservoir storage capabilities that are strategically located near markets in Tennessee, Virginia and North Carolina.

We own and operate 100% of the 565-mile Ozark Gas Transmission interstate natural gas transportation system, which extends from southeastern Oklahoma through Arkansas to southeastern Missouri. This system has connections to 53 receipt points and 28 delivery points and market delivery capability of approximately 0.5 Bcf/d of natural gas. We also own and operate 100% of the 365-mile Ozark Gas Gathering system that accesses the Fayetteville Shale and Arkoma natural gas production that feeds into Ozark Gas Transmission.

Customers and Contracts

Gas Transportation and Storage’s customers include LDCs, utilities, interstate and intrastate pipelines, industrial companies, natural gas marketers and producers, electric power generators, and exploration and production companies. Gas Transportation and Storage’s largest customer in 2010 was Atmos Energy Corporation, which accounted for 9% of its revenues.

6

Table of Contents

Index to Financial Statements

Gas Transportation and Storage has contracts with its customers to provide firm transportation and storage services as well as fee-based gathering services. Payments under firm transportation and storage services are mainly based on the volume of capacity reserved on the system regardless of the capacity actually used, and also include a variable charge based on the volume of natural gas actually transported. As a result, firm transportation revenues typically remain relatively constant over the term of the contracts. Gathering service contracts, which represent less than 5% of Gas Transportation and Storage 2010 operating revenues, include variable charges based on volume of natural gas actually gathered and the number of compression stages needed to deliver the gathered gas. Maximum and minimum rates for transportation and storage services are governed by the applicable FERC-approved natural gas tariff while fee-based gathering services are governed by the applicable state oil and gas commissions.

There has been a combination of contract renewals, extensions and new customers, along with notices of termination on certain contracts that expire at the end of the first quarter of 2011 on Ozark. We currently estimate that 2011 operating revenues and cash flow from operations could be reduced by approximately $10 million as compared to 2010 as a result of this net Ozark customer activity.

Gas Transportation and Storage also provides interruptible transportation and storage services under which gas is transported or stored for customers when operationally feasible and customers pay only for the actual volume of gas transported or stored. Under all contracts, Gas Transportation and Storage retains, at no cost, a fixed percentage of the natural gas it transports in order to supply the fuel needed for natural gas compression on the system.

As of December 31, 2010, East Tennessee and Saltville firm transportation and storage contracts had a weighted average remaining life of approximately eight years and Ozark, excluding gathering contracts, had a weighted average remaining life of approximately two years. In 2010, 96% of East Tennessee and Saltville and 76% of Ozark Gas Transmission’s revenues were derived from capacity reservation charges under firm contracts (including LNG storage services), with the remainder representing variable usage fees under firm and interruptible transportation contracts.

In 2005, East Tennessee entered into a five year rate settlement which expired on October 31, 2010. Following the expiration of the settlement agreement, the November 2005 approved tariff rates for East Tennessee remain in effect.

In 2008, Saltville placed into effect new rates approved by the FERC as a result of a settlement with customers associated with a rate proceeding. This settlement includes a rate moratorium until October 1, 2011. Following expiration of the moratorium, Saltville’s rates will remain the same, subject to further negotiation or a future rate proceeding. Also pursuant to the settlement, Saltville is required to file a rate case by October 1, 2013.

On November 18, 2010, the FERC announced that it is commencing an investigation (Ozark Rate Proceeding), pursuant to Section 5 of the Natural Gas Act (NGA), into the rates charged by Ozark Gas Transmission to determine whether it is over-recovering its costs. A Cost and Revenue Study was filed on February 1, 2011 by Ozark Gas Transmission as a result of the rate proceeding. Any resulting rate changes, if necessary, would be prospective and are not expected to be material.

Source of Supply

Gas supply attachments are a critical factor for Gas Transportation and Storage customers. Its customers benefit from gas supply from the Gulf Coast region through Tennessee Gas Pipeline Company, and to a lesser degree Texas Eastern Transmission, L.P. (Texas Eastern, a subsidiary of Spectra Energy), Southern Natural Gas Company, Columbia Gulf Transmission Company and Midwestern Gas Pipeline System. Its customers also receive natural gas supply from conventional and non-conventional sources such as Appalachian Shale and coal-bed methane, as well as from Fayetteville Shale and Arkoma supply basins. Natural gas withdrawn from East Tennessee’s LNG storage facility and other on-system storage fields, including Saltville’s natural gas storage facilities, provide customers with additional supply sources used to supplement supplies during periods of peak demand.

7

Table of Contents

Index to Financial Statements

Competition

The mountainous geography of the regions served by East Tennessee creates natural barriers to entry that make competition from new pipeline entrants difficult and expensive. As a result, East Tennessee is the sole source of interstate natural gas transportation for many of the firm capacity customers that transport natural gas on this system. At both ends of this system, East Tennessee is subject to competition from other pipelines.

Natural gas is in direct competition with electricity for residential and commercial heating demand in East Tennessee’s and Saltville’s market areas. While this competition does not directly affect firm sales, LDC customers’ growth is partially dependent upon the installation of natural gas furnaces in new home construction. Although substitution of electric heat for natural gas heat could have a long-term negative effect on certain electric plant customers’ demand requirements, East Tennessee and Saltville are benefiting from the addition of natural gas fired electric generation that is also supplied by our pipeline.

An increase in competition in the region served by East Tennessee and Saltville could arise from new ventures or expanded operations from existing competitors. Other competitive factors include the quantity, location and physical flow characteristics of interconnected pipelines, the ability to offer service from multiple storage or production locations, and the cost-of-service and rates offered by East Tennessee’s and Saltville’s competitors.

The Ozark assets compete with CenterPoint Energy Gas Transmission Company, Texas Gas Transmission, LLC’s Fayetteville Lateral, which went into service in 2009, and the Fayetteville Express Pipeline LLC, which went into service in the latter half of 2010.

General

8

Table of Contents

Index to Financial Statements

Following the acquisition of an additional 24.5% interest from a subsidiary of Spectra Energy in the fourth quarter 2010, we own a 49% interest in the 745-mile Gulfstream interstate natural gas transportation system which extends from Pascagoula, Mississippi and Mobile, Alabama across the Gulf of Mexico and into Florida. The Gulfstream pipeline currently includes approximately 295 miles of onshore pipeline in Florida, 15 miles of onshore pipeline in Alabama and Mississippi, and 435 miles of offshore pipeline in the Gulf of Mexico. Facilities also include gas treatment facilities and a compressor station in Coden, Alabama. Gulfstream supports the south and central Florida markets through its connection to eight receipt points and 23 delivery points and has market delivery capability of 1.29 Bcf/d of natural gas. Spectra Energy and affiliates of The Williams Companies, Inc. (Williams) own the remaining 1.0% and 50% interests in Gulfstream, respectively, and jointly operate the system.

Customers, Contracts and Supply

In 2010, Florida Power & Light Company and Florida Power Corporation d/b/a Progress Energy Florida, Inc. accounted for approximately 53% and 26%, respectively, of Gulfstream’s revenues.

Gulfstream provides firm and interruptible transportation services, interruptible park and loan services, and operational balancing agreements to resolve any differences between scheduled and actual receipts and deliveries. All of Gulfstream’s firm transportation contracts include negotiated rates through the life of the contract.

As of December 31, 2010, Gulfstream’s firm transportation and storage contracts had a weighted average remaining life of 18 years. In 2010, 95% of Gulfstream’s revenues were derived from capacity reservation charges under firm contracts, with the remainder derived from variable usage fees under firm and interruptible transportation contracts.

Gulfstream is connected to processing plants and supply pipelines in the Mobile Bay area. Gulfstream shippers have the ability to source supply through eight receipt points. The abundant supplies interconnected directly or indirectly to Gulfstream provide supply diversity to Gulfstream’s customers, potentially offsetting some of the risks associated with offshore Gulf of Mexico natural gas production.

Competition

Within the Florida market for natural gas, Gulfstream competes with other pipelines that transport and supply natural gas to end-users. Gulfstream’s competitors attempt to either attract new supply or attach new load to their pipelines, including those that are currently connected to markets served by Gulfstream. Gulfstream’s most direct competitor is Florida Gas Transmission Company, LLC, owned by subsidiaries of El Paso Corporation and Southern Union Company.

An increase in competition in the market could arise from new ventures or expanded operations from existing competitors. Other competitive factors include the quantity, location and physical flow characteristics of interconnected pipelines, access to natural gas storage, the cost-of-service and rates, and the terms of service offered.

9

Table of Contents

Index to Financial Statements

General

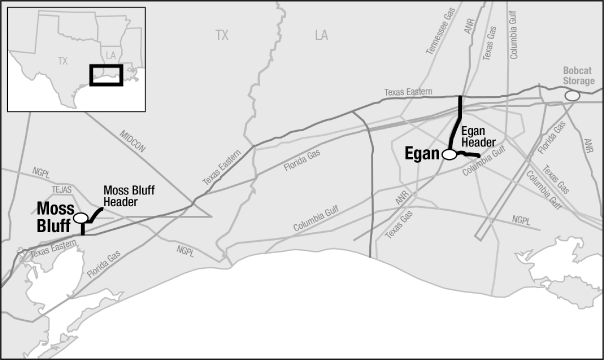

We own a 50% interest in Market Hub, which owns and operates two high-deliverability salt cavern natural gas storage facilities — the Egan facility and the Moss Bluff facility. These storage facilities are capable of being fully or partially filled and depleted, or “cycled,” multiple times per year. Market Hub’s storage facilities offer access to traditional Gulf of Mexico natural gas supplies, onshore Texas and Louisiana supplies, mid-continent production, non-conventional (shale and tight-sands) onshore production, and imports of LNG to the Gulf Coast. Spectra Energy owns the remaining 50% interest in Market Hub and operates the system.

The Egan storage facility, located in Acadia Parish, Louisiana, has four storage caverns with a working gas capacity of approximately 30 Bcf, and includes a 55-mile pipeline system that interconnects with eight interstate pipeline systems, including Texas Eastern. Egan offers access to Gulf Coast, midwest, southeast and northeast markets. Egan is undergoing a multi-year expansion program to add approximately 8 Bcf of storage capacity and 16 miles of pipeline extensions. The initial phase-in of storage expansion of 6 Bcf occurred in mid-2009, and the remaining portion of the project is scheduled to be completed in the second half of 2011.

The Moss Bluff storage facility, located in Liberty County, Texas, has three storage caverns with a working gas capacity of approximately 15 Bcf, and includes a 22-mile pipeline system that interconnects with two interstate pipeline systems, including Texas Eastern, and three intrastate pipeline systems. Moss Bluff offers access to Texas, northeast and midwest markets. The Cavern 4 multi-year project is expected to increase working capacity by 6.5 Bcf as well as upgrade top-side facilities and expand pipeline interconnects. The cavern is expected to be placed in service in 2011.

Customer, Contracts and Supply

Market Hub provides storage services to a broad mix of customers including marketers, electric power generators, gas producers, pipelines and LDCs. In 2010, there were no customers that accounted for more than 10% of Market Hub’s revenues.

10

Table of Contents

Index to Financial Statements

Market Hub provides firm storage, park and loan, and wheeling services. Under firm storage contracts, customers pay a reservation rate for the right to inject, withdraw and store a specified volume of natural gas. Under park and loan contracts, customers pay for the interruptible right to park (store) or loan (borrow) gas for a specific period of time. Customers who desire to wheel gas through a Market Hub facility pay for the interruptible right to receive natural gas at one interconnecting pipeline on the storage facility header system and have it simultaneously delivered to a different interconnecting pipeline on the storage facility header system.

As of December 31, 2010, Market Hub’s firm storage contracts had a weighted average remaining life of approximately three years, which is typical of the shorter contract life of market-based storage facilities as compared to transportation systems. Approximately 91% of Market Hub’s revenues in 2010 were derived from capacity reservation fees under firm storage contracts and 9% from interruptible storage contracts including park and loan services.

Egan has aggregate receipt capacity from major interconnecting pipelines of approximately 4.3 Bcf/d and an injection capability of 1.3 Bcf/d. Moss Bluff has aggregate receipt capacity from major interconnecting pipelines of approximately 2.3 Bcf/d and an injection capability of 0.6 Bcf/d. Egan has access to major interstate pipelines, while Moss Bluff has access to major interstate and intrastate pipelines. This level of supply connectivity gives customers access to a broad range of natural gas supply sources from existing onshore and offshore Gulf Coast and mid-Continent production areas as well as LNG supplies.

Competition

Market Hub competes with several regional storage facilities along the Gulf Coast as well as the storage services offered by interstate and intrastate pipelines that serve the same markets as Market Hub. The principal elements of competition among storage facilities are rates, terms of service, types of service, deliverability, supply and market access, and flexibility and reliability of service. An increase in competition in the market could arise from new ventures or expanded operations from existing competitors.

As noted previously, we provide a significant portion of our transportation and storage services through firm contracts and derive a smaller portion of our revenue through interruptible contracts, seeking to maximize the portion of physical capacity sold under firm contracts. To the extent physical capacity that is contracted for firm service is not being fully utilized, we can contract such capacity for interruptible service. Our gathering services, representing less than 5% of Gas Transportation and Storage operating revenues, are fee-based and dependent upon the volume of natural gas gathered. The table below summarizes certain information regarding our contracts and revenues as of and for the year ended December 31, 2010:

| Revenue Composition % | % of Physical Capacity Subscribed Under Firm Contracts |

Weighted Average Remaining Firm Contract Life (in years)(a) |

||||||||||||||||||||||

| Firm Contracts | Interruptible Contracts |

Volume- based Fees |

||||||||||||||||||||||

| Asset |

Capacity Reservation Fees |

Variable Fees |

||||||||||||||||||||||

| East Tennessee |

98 | % | 1 | % | 1 | % | — | % | 94 | % | 8 | |||||||||||||

| Ozark |

||||||||||||||||||||||||

| Transmission |

76 | 22 | 2 | — | 95 | 2 | ||||||||||||||||||

| Gathering |

— | — | — | 100 | n/a | n/a | ||||||||||||||||||

| Saltville |

85 | 8 | 7 | — | 99 | 7 | ||||||||||||||||||

| Gulfstream |

95 | 2 | 3 | — | 100 | 18 | ||||||||||||||||||

| Market Hub |

91 | — | 9 | — | 100 | 3 | ||||||||||||||||||

| (a) | The average life of each contract is calculated based on contract revenues. |

| n/a | Indicates not applicable. |

11

Table of Contents

Index to Financial Statements

We purchase a variety of manufactured equipment and materials for use in operations and expansion projects. The primary equipment and materials utilized in operations and project execution processes are steel pipe, compression engines, valves, fittings, polyethylene plastic pipe, gas meters and other consumables.

We utilize Spectra Energy’s supply chain management function which operates a North American supply chain management network. The supply chain management group uses the economies-of-scale of Spectra Energy to maximize the efficiency of supply networks where applicable.

There can be no assurance that the ability to obtain sufficient equipment and materials will not be adversely affected by unforeseen developments. In addition, the price of equipment and materials may vary, perhaps substantially, from year to year.

Our interstate gas transmission pipeline and storage operations are regulated by the FERC with the exception of Moss Bluff intrastate storage operations and the Ozark gathering facilities. The FERC regulates natural gas transportation in U.S. interstate commerce including the establishment of recourse rates for services. The FERC also regulates the construction of U.S. interstate pipelines and storage facilities, including the extension, enlargement and abandonment of facilities. Our Ozark gathering operations are subject to oversight by the Arkansas Public Service Commission and Oklahoma Corporation Commission. The Moss Bluff intrastate storage operations are subject to oversight by the Texas Railroad Commission (TRC).

The FERC may propose and implement new rules and regulations affecting interstate natural gas transmission and storage companies, which remain subject to the FERC’s jurisdiction. These initiatives may also affect certain transportation of gas by intrastate pipelines.

Our gas transmission and storage operations are subject to the jurisdiction of the Environmental Protection Agency (EPA) and various other federal, state and local environmental agencies. See “Environmental Matters” for a discussion of environmental regulation. Our interstate natural gas pipelines are also subject to the regulations of the DOT concerning pipeline safety.

Under current policy, the FERC permits pipelines and storage companies to include a tax allowance in the cost-of-service used as the basis for calculating their regulated rates. For pipelines and storage companies owned by partnerships or limited liability company interests, the tax allowance will reflect the actual or potential income tax liability on the FERC jurisdictional income attributable to all partnership or limited liability company interests if the ultimate owner of the interest has an actual or potential income tax liability on such income. This policy was upheld on May 29, 2007 by the Court of Appeals for the District of Columbia Circuit. Whether the owners of a pipeline or storage company have such actual or potential income tax liability will be reviewed by the FERC on a case-by-case basis. In a future rate case, the pipelines and storage companies in which we own an interest may be required to demonstrate the extent to which inclusion of an income tax allowance in the applicable cost-of-service is permitted under the current income tax allowance policy. Egan and Moss Bluff have authority to charge market-based rates and therefore this tax allowance issue does not affect the rates that they charge their customers.

We are subject to federal, state and local laws and regulations with regard to air and water quality, hazardous and solid waste disposal, and other environmental matters. These regulations often impose substantial testing and certification requirements.

12

Table of Contents

Index to Financial Statements

Environmental laws and regulations affecting us include, but are not limited to:

| • | The Clean Air Act (CAA) and the 1990 amendments to the CAA, as well as state laws and regulations affecting air emissions (including State Implementation Plans related to existing and new national ambient air quality standards), which may limit new sources of air emissions. Our natural gas transmission, storage and gathering assets are considered sources of air emissions and are thereby subject to the CAA. Owners and/or operators of air emission sources, like ourselves, are responsible for obtaining permits for existing and new sources of air emissions and for annual compliance and reporting. |

| • | The Federal Water Pollution Control Act (Clean Water Act), which requires permits for facilities that discharge wastewaters into the environment. The Oil Pollution Act (OPA), was enacted in 1990 and amends parts of the Clean Water Act and other statutes as they pertain to the prevention of and response to oil spills. OPA imposes certain spill prevention, control and countermeasure requirements. Although we are primarily a natural gas business, OPA affects our business because of the presence of liquid hydrocarbons (condensate) in our offshore pipeline. |

| • | The Solid Waste Disposal Act, as amended by the Resource Conservation and Recovery Act, which requires certain solid wastes, including hazardous wastes, to be managed pursuant to a comprehensive regulatory regime. As part of our business, we generate solid waste within the scope of these regulations and therefore must comply with such regulations. |

| • | The National Environmental Policy Act, which requires federal agencies to consider potential environmental effects in their decisions, including site approvals. Many of our capital projects require federal agency review, and therefore the environmental effects of proposed projects are a factor in determining whether we will be permitted to complete proposed projects. |

For more information on environmental matters, including possible liability and capital costs, see Part II. Item 8. Financial Statements and Supplementary Data, Note 15 of Notes to Consolidated Financial Statements.

Except to the extent discussed in Note 15, compliance with federal, state and local provisions regulating the discharge of materials into the environment, or otherwise protecting the environment, is incorporated into the routine cost structure of our partnership and is not expected to have a material adverse effect on our competitive position or consolidated results of operations, financial position or cash flows.

We do not have any employees. We are managed by the directors and officers of our general partner. Our general partner or its affiliates currently employ 110 people who spend a majority of their time operating the East Tennessee, Ozark and Saltville facilities, and 5 people who are primarily dedicated to us. Market Hub is operated by Spectra Energy pursuant to an operating and maintenance agreement and the employees who operate the Market Hub assets are therefore not included in the above numbers. Gulfstream is jointly operated by Spectra Energy (with respect to business functions) and Williams (with respect to technical functions) pursuant to an operating and maintenance agreement, and therefore, the employees who operate the Gulfstream assets are also not included in the above numbers.

Terms used to describe our business are defined below.

Available Cash. For any quarter ending prior to liquidation:

(a) the sum of:

(1) all cash and cash equivalents of the partnership and our subsidiaries on hand at the end of that quarter; and

13

Table of Contents

Index to Financial Statements

(2) if our general partner so determines all or a portion of any additional cash or cash equivalents of our partnership and our subsidiaries on hand on the date of determination of Available Cash for that quarter;

(b) less the amount of cash reserves established by our general partner to:

(1) provide for the proper conduct of the business of the partnership and our subsidiaries (including reserves for future capital expenditures and for future credit needs of the partnership and our subsidiaries) after that quarter;

(2) comply with applicable law or any debt instrument or other agreement or obligation to which we or any of our subsidiaries are a part or our assets are subject; and

(3) provide funds for minimum quarterly distributions and cumulative common unit arrearages for any one or more of the next four quarters;

provided, however, that our general partner may not establish cash reserves pursuant to clause (b)(3) immediately above unless our general partner has determined that the establishment of reserves will not prevent us from distributing the minimum quarterly distribution on all common units and any cumulative common unit arrearages thereon for that quarter; and provided, further, that disbursements made by us or any of our subsidiaries or cash reserves established, increased or reduced after the end of that quarter but on or before the date of determination of Available Cash for that quarter shall be deemed to have been made, established, increased or reduced, for purposes of determining Available Cash, within that quarter if our general partner so determines.

Operating Surplus. For any period prior to liquidation, on a cumulative basis and without duplication:

(a) the sum of:

(1) all cash receipts of our partnership and our subsidiaries for the period beginning on the closing date of our initial public offering and ending with the last day of the period, other than cash receipts from interim capital transactions; and

(2) an amount equal to the sum of (A) two times the amount needed for any one quarter for us to pay the minimum quarterly distribution on all units (including the general partner units) and (B) two times the amount in excess of the minimum quarterly distribution for any quarter to pay a distribution on all Common Units at the same per unit amount as was distributed on the Common Units in excess of the minimum quarterly distribution in the immediately preceding quarter, provided the amount in (B) will be deemed to be Operating Surplus only to the extent that the distribution paid in respect of such amounts is paid on Common Units, less

(b) the sum of:

(1) operating expenditures for the period beginning on the closing date of our initial public offering and ending with the last day of that period; and

(2) the amount of cash reserves (or our proportionate share of cash reserves in the case of subsidiaries that are not wholly owned) established by our general partner to provide funds for future operating expenditures; provided however, that disbursements made (including contributions to us or our subsidiaries or disbursements on behalf of us or our subsidiaries) or cash reserves established, increased or reduced after the end of that period but on or before the date of determination of Available Cash for that period shall be deemed to have been made, established, increased or reduced for purposes of determining operating surplus, within that period if our general partner so determines.

14

Table of Contents

Index to Financial Statements

We were formed on March 19, 2007 as a Delaware master limited partnership. Our principal executive offices are located at 5400 Westheimer Court, Houston, Texas 77056 and our telephone number is 713-627-5400. We electronically file various reports with the Securities and Exchange Commission (SEC), including annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to such reports. The public may read and copy any materials that we file with the SEC at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC also maintains an internet site that contains reports and information statements, and other information regarding issuers that file electronically with the SEC at http://www.sec.gov. Additionally, information about us, including our reports filed with the SEC, is available through our web site at http://www.spectraenergypartners.com. Such reports are accessible at no charge through our web site and are made available as soon as reasonably practicable after such material is filed with or furnished to the SEC. Our website and the information contained on that site, or connected to that site, is not incorporated by reference into this report.

15

Table of Contents

Index to Financial Statements

Discussed below are the more significant risk factors relating to us.

Risks Related to our Business

We may not have sufficient cash from operations to enable us to make cash distributions to common unitholders.

In order to make cash distributions at our minimum distribution rate of $0.30 per common unit per quarter, or $1.20 per unit per year, we will require Available Cash of approximately $27 million per quarter, or $108 million per year, depending on the actual number of common units outstanding. We may not have sufficient Available Cash from operating surplus each quarter to enable us to make cash distributions at the minimum distribution rate. The amount of cash we can distribute on our units principally depends upon the amount of cash we generate from operations, which will fluctuate based on, among other things:

| • | the rates charged for transportation, storage and gathering services, and the volumes of natural gas contracted by customers for transportation, storage and gathering services; |

| • | the overall demand for natural gas in the southeastern, mid-Continent and mid-Atlantic regions of the United States and the quantities of natural gas available for transport, especially from the Gulf of Mexico, Appalachian and mid-Continent areas; |

| • | regulatory action affecting the demand for natural gas, the supply of natural gas, the rates we can charge, contracts for services, existing contracts, operating costs and operating flexibility; |

| • | regulatory and economic limitations on the development of LNG import terminals in the Gulf Coast region; and |

| • | the level of operating and maintenance, and general and administrative costs. |

In addition, the actual amount of cash available for distribution will depend on other factors, some of which are beyond our control, including:

| • | the level of capital expenditures to complete construction projects; |

| • | the cost and form of payment of acquisitions; |

| • | debt service requirements and other liabilities; |

| • | fluctuations in working capital needs; |

| • | the ability to borrow funds and access capital markets; |

| • | restrictions on distributions contained in debt agreements; and |

| • | the amount of cash reserves established by our general partner. |

Our subsidiaries and equity affiliates conduct operations and own our operating assets, which may affect our ability to make distributions to our unitholders. In addition, we cannot control the amount of cash that will be received from Gulfstream and Market Hub, and we may be required to contribute significant cash to fund their operations.

We are a partnership holding company and our operating subsidiaries conduct all of our operations and own all of our operating assets. We have no significant assets other than the ownership interests in our subsidiaries and our equity investments, including Gulfstream and Market Hub. As a result, our ability to make distributions to our unitholders depends on the performance of these subsidiaries and equity investments and their ability to distribute funds to us. The ability of our subsidiaries and equity investments to make distributions to us may be

16

Table of Contents

Index to Financial Statements

restricted by, among other things, the provisions of existing and future indebtedness, applicable state partnership and limited liability company laws and other laws and regulations, including FERC policies.

Market Hub and Gulfstream are expected to generate approximately 60% of the cash available for distribution. Spectra Energy operates Market Hub and the operation of Gulfstream is shared between Spectra Energy and Williams. Accordingly, we do not control the amount of cash distributed to us nor do we control ongoing operational decisions, including the incurrence of capital expenditures that we may be required to fund.

Our lack of control over the operations of Gulfstream and Market Hub may mean that we do not receive the amount of cash we expect to be distributed to us. In addition, we may be required to provide additional capital, and these contributions may be material. Neither Gulfstream nor Market Hub is prohibited from incurring indebtedness by the terms of their respective limited liability company agreement and general partnership agreements. If Gulfstream or Market Hub were to incur significant additional indebtedness, it could inhibit their respective abilities to make distributions to us. This lack of control may significantly and adversely affect our ability to distribute cash.

Our natural gas pipeline systems and certain of our storage facilities and related assets are subject to regulation by the FERC, which could have an adverse effect on our ability to establish transportation, storage and gathering rates that would allow us to recover the full cost of operating our pipelines, including a reasonable return, and our ability to make distributions. For example, the rates charged for Ozark Gas Transmission could be decreased as a result of a recently announced FERC investigation.

Our natural gas pipeline systems and certain of our storage facilities and related assets are subject to regulation by the FERC. Its authority to regulate natural gas pipeline transportation services includes the rates charged for the services, terms and conditions of service, certification and construction of new facilities, the extension or abandonment of services and facilities, the maintenance of accounts and records, the acquisition and disposition of facilities, the initiation and discontinuation of services, and various other matters.

On November 18, 2010, the FERC commenced the Ozark Rate Proceeding alleging that Ozark Gas Transmission’s revenues might substantially exceed their actual cost of service and therefore may be unjust and unreasonable. A Cost and Revenue Study was filed on February 1, 2011 by Ozark Gas Transmission as a result of the rate proceeding. Interested parties, including Ozark Gas shippers, will be able to intervene and participate in the Ozark Rate Proceeding. This investigation could be resolved either through administrative litigation or settlement. In the absence of an earlier settlement, the FERC could issue an order, which is not expected until late 2011 or early 2012, finding the rates are not just and reasonable and establishing new lower rates prospectively for Ozark Gas Transmission.

Action by the FERC on currently pending regulatory matters as well as matters arising in the future could adversely affect our ability to establish or charge rates that would cover future increase in their costs, such as additional costs related to environmental matters including any climate change regulation, or even to continue to collect rates that cover current costs, including a reasonable return. We cannot assure unitholders that our pipeline systems will be able to recover all of their costs through existing or future rates.

In addition, we cannot give assurance regarding the likely future regulations under which we will operate our natural gas transportation, storage and gathering businesses or the effect such regulation could have on our business, financial condition, results of operations and our ability to make distributions.

Certain transportation services are subject to long-term, fixed-price “negotiated rate” contracts that are not subject to adjustment, even if our cost to perform services exceeds the revenues received from such contracts, and, as a result, our costs could exceed our revenues received under such contracts.

Under the FERC policy, a regulated service provider and a customer may mutually agree to sign a contract for service at a “negotiated rate” which may be above or below the FERC-regulated “recourse rate” for that

17

Table of Contents

Index to Financial Statements

service. For 2010, 99% of Gulfstream’s firm revenues were derived from such negotiated rate contracts and approximately 43% of Gas Transportation and Storage’s firm revenues were derived from capacity reservation charges under negotiated rate contracts. These negotiated rate contracts are not subject to adjustment for increased costs which could be produced by inflation or other factors relating to the specific facilities being used to perform the services. It is possible that Gulfstream’s, East Tennessee’s, Ozark’s and Saltville’s costs to perform services under these negotiated rate contracts will exceed the negotiated rates. If this occurs, it could decrease cash flows from Gulfstream, East Tennessee, Ozark and Saltville.

Market Hub’s right to charge “market-based rates” at its Egan storage facility is subject to the continued existence of certain conditions related to the competitive position of Market Hub and, if those conditions change, the right to charge market-based rates could be terminated.

Rates charged by Egan are regulated by the FERC pursuant to its market-based rate policy, which allows regulated storage companies to charge rates above those which would be permitted under traditional cost-of-service regulation. The right of Egan to charge market-based rates is based upon determinations by the FERC that it does not have market power in the relevant market areas it serves. This determination of a lack of market power is subject to review and revision by the FERC if circumstances change. In the event of an adverse determination concerning market power with respect to Egan, its rates could become subject to cost-of-service regulation which could have adverse consequences for the cash flows of Egan.

Increased competition from alternative natural gas transportation, storage and gathering options and alternative fuel sources could have a significant financial effect on us.

We compete primarily with other interstate and intrastate pipelines, storage and gathering facilities in the transportation, storage and gathering of natural gas. Some of our competitors have greater financial resources and access to greater supplies of natural gas than we do. Some of these competitors may expand or construct transportation, storage and gathering systems that would create additional competition for the services we provide to our customers. Moreover, Spectra Energy and its affiliates are not limited in their ability to compete with us. Further, natural gas also competes with other forms of energy available to our customers, including electricity, coal and fuel oils.

The principal elements of competition among natural gas transportation, storage and gathering assets are rates, terms of service, access to natural gas supplies, flexibility and reliability. The FERC’s policies promoting competition in natural gas markets are having the effect of increasing the natural gas transportation, storage and gathering options for our traditional customer base. As a result, we could experience some “turnback” of firm capacity as existing agreements expire. If East Tennessee, Ozark, Saltville, Gulfstream or Market Hub are unable to remarket this capacity or can remarket it only at substantially discounted rates compared to previous contracts, they may have to bear the costs associated with the turned back capacity. Increased competition could reduce the volumes of natural gas transported, stored or gathered by our systems or, in cases where we do not have long-term fixed rate contracts, could force us to lower our transportation, storage or gathering rates. Competition could intensify the negative effect of factors that significantly decrease demand for natural gas in the markets served by our pipeline systems, such as competing or alternative forms of energy, a recession or other adverse economic conditions, weather, higher fuel costs and taxes or other governmental or regulatory actions that directly or indirectly increase the cost or limit the use of natural gas. Our ability to renew or replace existing contracts at rates sufficient to maintain current revenues and cash flows could be adversely affected by the activities of our competitors. All of these competitive pressures could have a material adverse effect on our business, financial condition, results of operations and ability to make distributions.

18

Table of Contents

Index to Financial Statements

Any significant decrease in supplies of natural gas connected to our areas of operation could adversely affect business and operating results, and reduce cash available for distribution.

All of our businesses are dependent on the continued availability of natural gas production and reserves. Low prices for natural gas or regulatory limitations could adversely affect development of additional reserves and production that is accessible by our pipeline and storage assets. Production from existing wells and natural gas supply basins with access to our pipelines will naturally decline over time. Additionally, the amount of natural gas reserves underlying these wells may also be less than anticipated, and the rate at which production from these reserves declines may be greater than anticipated. Accordingly, to maintain or increase throughput on our pipelines and cash flows associated with the transportation of gas, our customers must continually obtain new supplies of natural gas.

If new supplies of natural gas are not obtained to replace the natural decline in volumes from existing supply basins, the overall volume of natural gas transported, stored and gathered on our systems would decline, which could have a material adverse effect on our business, financial condition, results of operations and ability to make distributions.

We may not be able to maintain or replace expiring natural gas transportation, storage and gathering contracts at favorable rates.

Our primary exposure to market risk occurs at the time existing transportation, storage and gathering contracts expire and are subject to renegotiation and renewal. A portion of the revenue generated by our systems in 2010 is attributable to firm capacity reservation fees that are set to expire on or prior to December 31, 2013. For Gas Transportation and Storage, Gulfstream and Market Hub, those portions were 25%, 1% and 50%, respectively. Upon expiration, we may not be able to extend contracts with existing customers or obtain replacement contracts at favorable rates or on a long-term basis. The extension or replacement of existing contracts depends on a number of factors beyond our control, including:

| • | the level of existing and new competition to deliver natural gas to our markets; |

| • | the growth in demand for natural gas in our markets; |

| • | whether the market will continue to support long-term contracts; |

| • | whether our business strategy continues to be successful; and |

| • | the effects of state regulation on customer contracting practices. |

There has been a combination of contract renewals, extensions and new customers, along with notices of termination on certain contracts that expire at the end of the first quarter of 2011 on Ozark. We currently estimate that 2011 operating revenues and cash flow from operations could be reduced by approximately $10 million as compared to 2010 as a result of this net Ozark customer activity.

Our key markets are projected to continue to exhibit higher than average annual growth in natural gas demand of approximately 2.5% through 2020 as compared with the U.S. lower 48 average growth rate of approximately 2% for the same period. This demand growth is primarily driven by the natural gas-fired electric generation sector.

Any failure to extend or replace a significant portion of our existing contracts may have a material adverse effect on our business, financial condition, results of operations and ability to make distributions.

We depend on certain key customers for a significant portion of our revenues. The loss of any of these key customers could result in a decline in our revenues and cash available to make distributions.

We rely on a limited number of customers for a significant portion of revenues. For the year ended December 31, 2010, the three largest customers for Gas Transportation and Storage were Atmos Energy Corporation, CNX Gas Corporation and Southwestern Energy Company; for Gulfstream were Florida Power &

19

Table of Contents

Index to Financial Statements

Light Company, Florida Power Corporation d/b/a Progress Energy Florida, Inc. and TECO Energy and its affiliates; and for Market Hub were AGL Resources Inc., Eletrecite de France Sa and JP Morgan Chase & Co. In 2010, these customers accounted for approximately 25%, 87% and 26% of the operating revenues for Gas Transportation and Storage, Gulfstream and Market Hub, respectively. While most of these customers are subject to long-term contracts, with the exception of Southwestern Energy Company, the loss of all or even a portion of the contracted volumes of these customers as a result of competition, creditworthiness, inability to negotiate extensions or replacements of contracts or otherwise, could have a material adverse effect on our financial condition, results of operations and ability to make distributions, unless we are able to contract for comparable volumes from other customers at favorable rates.

If third-party pipelines and other facilities interconnected to our pipelines become unavailable to transport natural gas, our revenues and cash available to make distributions could be adversely affected.

We depend upon third-party pipelines and other facilities that provide delivery options to and from our pipelines and storage facilities. Because we do not own these third-party pipelines or facilities, their continuing operation is not within our control. If these or any other pipeline connection were to become unavailable for current or future volumes of natural gas due to repairs, damage to the facility, lack of capacity or any other reason, our ability to operate efficiently and continue shipping natural gas to end-markets could be restricted, thereby reducing revenues. Any temporary or permanent interruption at any key pipeline interconnect could have a material adverse effect on our business, results of operations, financial condition and ability to make distributions.

If we do not complete expansion projects or make and integrate acquisitions, our future growth may be limited.

A principal focus of our strategy is to continue to grow the cash distributions on our units by expanding our business. Our ability to grow depends on our ability to complete expansion projects and make acquisitions that result in an increase in cash generated. We may be unable to complete successful, accretive expansion projects or acquisitions for any of the following reasons:

| • | an inability to identify attractive expansion projects or acquisition candidates or we are outbid by competitors; |

| • | an inability to obtain necessary rights-of-way or government approvals, including regulatory agencies; |

| • | an inability to successfully integrate the businesses we build or acquire; |

| • | we are unable to raise financing for such expansion projects or acquisitions on economically acceptable terms; |

| • | incorrect assumptions about volumes, reserves, revenues and costs, including synergies and potential growth; or |

| • | we are unable to secure adequate customer commitments to use the newly expanded or acquired facilities. |

Expansion projects or future acquisitions that appear to be accretive may nevertheless reduce our cash from operations on a per unit basis.

Even if we complete expansion projects or make acquisitions that we believe will be accretive, these expansion projects or acquisitions may nevertheless reduce our cash from operations on a per-unit basis. Any expansion project or acquisition involves potential risks, including, among other things:

| • | an inability to complete expansion projects on schedule or within the budgeted cost due to the unavailability of required construction personnel, equipment or materials, and the risk of cost overruns resulting from inflation or increased costs of materials, labor and equipment; |

20

Table of Contents

Index to Financial Statements

| • | a decrease in our liquidity as a result of us using a significant portion of our Available Cash or borrowing capacity to finance the project or acquisition; |

| • | an inability to complete expansion projects on schedule due to accidents, weather conditions or an inability to obtain necessary permits; |

| • | an inability to receive cash flows from a newly built or acquired asset until it is operational; |

| • | unforeseen difficulties operating in new product areas or new geographic areas; and |

| • | customer losses at the acquired business. |

As a result, our new facilities may not achieve expected investment returns, which could adversely affect our results of operations, financial position or cash flows. If any expansion projects or acquisitions that we ultimately complete are not accretive to cash available for distribution, our ability to make distributions may be reduced.

The amount of our cash available for distribution depends primarily on our cash flows and not solely on profitability, which may prevent us from making cash distributions during periods when we record net income.

Our amount of cash available for distribution depends primarily upon our cash flows, including cash flow from financial reserves and working capital or other borrowings, and not solely on profitability, which will be affected by non-cash items. As a result, we may make cash distributions during periods when we record a net loss for financial accounting purposes and may not make cash distributions during periods when we record net earnings for financial accounting purposes.

Significant prolonged changes in natural gas prices could affect supply and demand, reducing contracted volumes on our systems and adversely affecting revenues and cash available to make distributions over the long-term.

Higher natural gas prices over the long term could result in a decline in the demand for natural gas and, therefore, in the throughput on our systems. Also, lower natural gas prices over the long term could result in a decline in the production of natural gas resulting in reduced contracted volumes on our systems. In addition, prolonged reduced price volatility could reduce the revenues generated by our storage services. As a result, significant prolonged changes in natural gas prices could have a material adverse effect on our financial condition, results of operations and ability to make distributions.

Our operations are subject to environmental laws and regulations that may expose us to significant costs and liabilities.

Our natural gas transportation, storage and gathering activities are subject to stringent and complex federal, state and local environmental laws and regulations. We may incur substantial costs in order to conduct our operations in compliance with these laws and regulations. Moreover, new and stricter environmental laws regulations or enforcement policies could be implemented that significantly increase our compliance costs or the cost of any remediation of environmental contamination that may become necessary, and these costs could be material.

Failure to comply with environmental laws and regulations, or the permits issued under them, may result in the assessment of administrative, civil and criminal penalties, the imposition of remedial obligations and the issuance of injunctions limiting or preventing some or all of our operations. In addition, strict joint and several liability may be imposed under certain environmental laws, which could cause us to become liable for the conduct of others or for consequences of our own actions that were in compliance with all applicable laws at the time those actions were taken. Private parties may also have the right to pursue legal actions against us to enforce compliance, as well as to seek damages for noncompliance, with environmental laws and regulations or for personal injury or property damage that may result from environmental and other effects of operations. We may not be able to recover some or any of these costs through insurance or increased revenues, which may have a material adverse effect on our business, results of operations, financial condition and ability to make cash distributions.

21

Table of Contents

Index to Financial Statements

The enactment of future climate change legislation could result in increased operating costs and delays in obtaining necessary permits for our capital projects.

The current international climate framework, the United Nations-sponsored Kyoto Protocol, prescribes specific targets to reduce greenhouse gas (GHG) emissions for developed countries for the 2008-2012 period. The Kyoto Protocol expires in 2012 and has not been signed by the United States. United Nations-sponsored international negotiations were held in Cancun, Mexico in December 2010 with the intent of defining a future agreement for 2012 and beyond. While the talks resulted in a limited political agreement, to date, a binding successor accord to the Kyoto Protocol has not been realized.

In the United States, climate change action is evolving at state, regional and federal levels. We expect that some of our assets and operations could be affected either directly or indirectly by eventual mandatory GHG programs; however, the timing and specific policy objectives in many jurisdictions, including at the federal level, remain uncertain. In addition, a number of states in the U.S. have joined regional greenhouse gas initiative, and a number are developing their own programs that would mandate reductions in GHG emissions. However, as the key details of future GHG restrictions and compliance mechanisms remain undefined, the likely future effects on our business are highly uncertain.

The EPA finalized a Prevention of Significant Deterioration and Title V Greenhouse Gas Tailoring Rule in 2009 to address how GHG emissions would be regulated under the existing Clean Air Act. Regulation is scheduled to begin in 2011, and over time, certain existing facilities will be subject to this regulation. Some new construction and modification projects in the future may be subject to this regulation as well. At this time, it is not anticipated that the costs will be material; however, many implementation details are still unknown. There may be additional permitting requirements which may result in delays in completing capital projects. In addition, several legislation proposals that would impose GHG emissions constraints have been considered by the U.S. Congress. To date, no such legislation has been enacted into law.

Due to the speculative outlook regarding any U.S. federal and state policies, we cannot estimate the potential effect of proposed GHG policies on our future consolidated results of operations, financial position or cash flows. However, such legislation or regulation could materially increase our operating costs, require material capital expenditures or create additional permitting, which could delay proposed construction projects.

We may incur significant costs and liabilities as a result of pipeline integrity management program testing and any necessary pipeline repair or preventative or remedial measures.

The DOT has adopted regulations requiring pipeline operators to develop integrity management programs for transportation pipelines located where a leak or rupture could do the most harm in “high consequence areas.” The regulations require operators to:

| • | perform ongoing assessments of pipeline integrity; |

| • | identify and characterize applicable threats to pipeline segments that could affect a high consequence area; |

| • | improve data collection, integration and analysis; |

| • | repair and remediate the pipeline as necessary; and |

| • | implement preventive and mitigating actions. |

Our actual implementation costs may be affected by industry-wide demand for the associated contractors and service providers. Additionally, should we fail to comply with DOT regulations, we could be subject to penalties and fines.

22

Table of Contents

Index to Financial Statements

Our operations are subject to operational hazards and unforeseen interruptions.

Our operations are subject to many hazards inherent in the transportation, storage and gathering of natural gas, including:

| • | damage to pipelines, facilities and related equipment caused by hurricanes, tornadoes, floods, fires and other natural disasters, explosions and acts of terrorism; |

| • | inadvertent damage from third parties, including from construction, farm and utility equipment; |

| • | leaks of natural gas and other hydrocarbons or losses of natural gas as a result of the malfunction of equipment or facilities; |

| • | collapse of storage caverns; |

| • | operator error; |

| • | environmental pollution; |

| • | explosions and blowouts; |

| • | risks related to underwater pipelines in the Gulf of Mexico, which are susceptible to damage from shifting as a result of water currents (as seen in the Gulf of Mexico following Hurricanes Katrina, Rita, Gustav and Ike), as well as damage from vessels; |

| • | risks related to pipeline that traverses areas in Florida where karst conditions exist. Karst conditions refers to terrain, usually found where limestone or other carbonate rock is present, that may subside or result in a sinkhole collapse when the underlying water table changes; and |

| • | risks related to operating in a marine environment. |

These risks could result in substantial losses due to personal injury and/or loss of life, severe damage to and destruction of property and equipment, and pollution or other environmental damage which may result in curtailment or suspension of our related operations. A natural disaster or other hazard affecting the areas in which we operate could have a material adverse effect on our operations.

We are subject to pipeline safety laws and regulations, compliance with which can require significant capital expenditures, can increase our cost of operations and may affect or limit our business plans.

Our interstate pipeline operations are subject to pipeline safety regulation administered by the Pipeline and Hazardous Materials Safety Administration (the PHMSA) of the U.S. Department of Transportation. These laws and regulations require us to comply with a significant set of requirements for the design, construction, maintenance and operation of our interstate pipelines. These regulations, among other things, include requirements to monitor and maintain the integrity of our pipelines. The regulations determine the pressures at which our pipelines can operate. Pipeline failures or failure to comply with applicable regulations could result in reduction of allowable operating pressures as authorized by the PHMSA, which would reduce available capacity on our pipelines. Should any of these risks materialize, it could have a material adverse effect on our operations, earnings, financial condition and cash flows.

We do not insure against all potential losses and could be seriously harmed by unexpected liabilities.

We are not fully insured against all risks inherent to our business. We are not insured against all environmental accidents that might occur. If a significant accident or event occurs that is not fully insured, it could adversely affect our operations and financial condition. In addition, we may not be able to maintain or obtain insurance of the type and amount we desire at reasonable rates. Changes in the insurance markets subsequent to the September 11, 2001 terrorist attacks, and Hurricanes Katrina, Rita, Gustav and Ike have made it more difficult for us to obtain certain types of coverage, and we may elect to self insure a portion of our asset portfolio. In addition, we do not maintain offshore business interruption insurance. There can be no assurance that we will be able to obtain the levels or types of insurance we would otherwise have obtained prior to these

23

Table of Contents

Index to Financial Statements

market changes or that the insurance coverage we do obtain will not contain large deductibles or fail to cover certain hazards or cover all potential losses. The occurrence of any operating risks not fully covered by insurance could have a material adverse effect on our business, financial condition, results of operations and ability to make distributions.

Our debt levels may limit our flexibility in obtaining additional financing and in pursuing other business opportunities.

At December 31, 2010, we had $298.6 million in revolving debt outstanding under our $500 million credit facility. We continue to have the ability to incur additional debt, subject to limitations in our credit facility. Our level of debt could have important consequences, including the following:

| • | our ability to obtain additional financing, if necessary, for working capital, capital expenditures, acquisitions or other purposes may be impaired or such financing may not be available on favorable terms; |

| • | we will need a substantial portion of our cash flow to make principal and interest payments on our indebtedness, reducing the funds that would otherwise be available for operations, future business opportunities and distributions to unitholders; and |