Attached files

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2010

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to .

Commission File Number: 0-19582

OLD DOMINION FREIGHT LINE, INC.

(Exact name of registrant as specified in its charter)

| VIRGINIA | 56-0751714 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

500 Old Dominion Way

Thomasville, NC 27360

(Address of principal executive offices)

(Zip Code)

(336) 889-5000

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Name of each exchange on which registered | |

| Common Stock ($0.10 par value) | The NASDAQ Stock Market LLC | |

| (NASDAQ Global Select Market) |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | x | Accelerated filer | ¨ | |||

| Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

The aggregate market value of voting stock held by non-affiliates of the registrant as of June 30, 2010 was $930,329,743, based on the closing sales price as reported on the NASDAQ Global Select Market.

As of February 25, 2011, the registrant had 55,926,945 outstanding shares of Common Stock ($0.10 par value).

DOCUMENTS INCORPORATED BY REFERENCE

Certain portions of the Company’s Proxy Statement for the 2011 Annual Meeting of Shareholders are incorporated by reference into Part III of this report.

Table of Contents

Table of Contents

Forward-looking statements appear in this Annual Report, including but not limited to Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and in other written and oral statements made by or on behalf of us. These forward-looking statements include, but are not limited to, statements relating to our goals, strategies, expectations, competitive environment, regulation, availability of resources, future events and future financial performance. Such forward-looking statements are made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. These forward-looking statements typically can be identified by such words as “anticipate,” “estimate,” “forecast,” “project,” “intend,” “expect,” “believe,” “should,” “could,” “may,” or other similar words or expressions. We caution readers that such forward-looking statements involve risks and uncertainties that could cause actual events or results to differ materially from those expressed or implied herein, including, but not limited to, the risk factors detailed in this Annual Report.

Our forward-looking statements are based on our beliefs and assumptions using information available at the time the statements are made. We caution the reader not to place undue reliance on our forward-looking statements (i) as these statements are neither a prediction nor a guarantee of future events or circumstances and (ii) the assumption, beliefs, expectations and projections about future events may differ materially from actual results. The Company undertakes no obligation to publicly update any forward-looking statement to reflect developments occurring after the statement is made.

PART I

Unless the context requires otherwise, references in this report to “Old Dominion,” the “Company,” “we,” “us” and “our” refer to Old Dominion Freight Line, Inc.

Overview

Old Dominion is a leading, less-than-truckload (“LTL”), non-union motor carrier providing regional, inter-regional and national LTL service and value-added logistics services. We are the seventh largest LTL motor carrier in the United States, as measured by 2009 revenue, according to Transport Topics. In addition to our core LTL services, we offer our customers a broad range of logistics services including ground and air expedited transportation, supply chain consulting, transportation management, truckload brokerage, container delivery and warehousing services. Through marketing and carrier relationships, we also offer door-to-door international freight services to and from all of North America, Central America, South America and the Far East. Our services are complemented by our technological capabilities, which we believe provide the tools to improve the efficiency of our operations while empowering our customers to manage their shipping needs.

We have grown our revenue and customer base through both organic growth and strategic acquisitions and now provide our domestic LTL services throughout the entire continental United States. Our infrastructure allows us to provide next-day and second-day service within each of our six regions, as well as inter-regional and national service between these regions. To support our ongoing expansion, we have added 59 new service centers in the past five years for a total of 213 at December 31, 2010.

We believe our growth can be attributed to our focus on meeting our customers’ complete supply chain needs from a single point of contact with a high level of customer service supported by ongoing investment in our employees, service center network and technology. Our integrated structure allows us to offer our customers consistent service from origin to destination. We believe our operating structure and proprietary information systems enable us to provide higher customer service levels and better manage our operating costs.

We were organized in 1934 and incorporated in Virginia in 1950. Our principal executive offices are located at 500 Old Dominion Way, Thomasville, North Carolina 27360. Please refer to the Balance Sheets and Statements of Operations included in Item 8, “Financial Statements and Supplementary Data” of this report for information regarding our total assets, revenue from operations and net income.

3

Table of Contents

Our Industry

Trucking companies provide transportation services to virtually every industry operating in the United States and generally offer higher levels of reliability and faster transit times than other surface transportation options. The trucking industry is comprised principally of two types of motor carriers: LTL and truckload. LTL carriers typically pick up multiple shipments from multiple customers on a single truck and then route that freight for delivery through service centers where the freight may be transferred to other trucks with similar destinations. In contrast, truckload carriers generally dedicate an entire trailer to one customer from origin to destination.

According to the American Trucking Associations, total domestic freight revenue in 2009 was $664.7 billion, of which the trucking industry accounted for 81.9%. The LTL sector had revenue in 2009 of $38.6 billion, which represented 5.8% of total domestic freight revenue. In contrast to truckload carriers, LTL motor carriers require expansive networks of local pickup and delivery (“P&D”) service centers, as well as larger breakbulk, or hub, facilities. Significant capital is required of LTL motor carriers to create and maintain a network of service centers and a fleet of tractors and trailers. The high fixed costs and capital spending requirements for LTL motor carriers makes it difficult for new start-up or small operators to effectively compete with established companies. In addition, successful LTL motor carriers generally employ, and continuously update, a high level of technology to provide information to customers and to reduce operating costs.

The LTL industry is highly competitive on the basis of service and price and has consolidated significantly since the industry was deregulated in 1980. Based on 2009 revenue, the top 25 LTL motor carriers accounted for approximately 65% of the total LTL market. Consolidation has accelerated in recent years due to an increase in customer demand for single transportation providers offering both national and regional LTL service and complex supply chain services. Smaller regional carriers with lesser financial resources are generally unable to meet this demand. We believe consolidation will continue, particularly due to the negative impact on industry fundamentals from the recent recessionary economic environment, which appears to have substantially weakened the financial condition of many of our competitors.

Competition

We compete with regional, inter-regional and national LTL carriers and, to a lesser extent, with truckload carriers, small package carriers, airfreight carriers and railroads. Competition is based primarily on service, price and business relationships. We believe that we are able to compete effectively in our markets by providing high-quality and timely service at competitive prices.

At all levels of our organization, we seek to continuously improve customer service by maximizing on-time performance while reducing transit times and minimizing cargo claims. We believe our transit times are generally faster than those of our principal national competitors, in part because of our more efficient service center network, use of team drivers and proprietary technology. In addition, we provide greater geographic coverage than most of our regional competitors. Our diversified mix and scope of regional, inter-regional and national service enables us to provide our customers with a single source to meet their LTL shipping needs, and we believe this provides us with a distinct advantage over our regional, multi-regional and national competition.

We also believe our non-union workforce gives us a significant advantage over our unionized LTL competitors. By utilizing flexible scheduling and training our employees to perform multiple tasks, we believe we achieve greater productivity and higher levels of customer service. We believe our focus on employee communication, continued education, development and motivation strengthens the relationships among our employees.

We compete with several larger transportation service providers, each of which may have more equipment, a broader coverage network and a wider range of services than we have. Our larger competitors may also have greater financial resources and, in general, the ability to reduce prices to gain business, especially during times of reduced growth rates in the economy.

4

Table of Contents

Service Center Operations

At December 31, 2010, we conducted operations through 213 service center locations, of which we owned 132 and leased 81. We operate ten major breakbulk facilities in Rialto, California; Atlanta, Georgia; Chicago, Illinois; Indianapolis, Indiana; Greensboro, North Carolina; Harrisburg, Pennsylvania; Memphis and Morristown, Tennessee; Dallas, Texas; and Salt Lake City, Utah, while using other service centers for limited breakbulk activity in order to serve our next-day markets. Our service centers are strategically located in six regions of the country to provide the highest quality service and minimize freight rehandling costs.

Each of our service centers is responsible for the pickup and delivery of freight within its service area. Each service center loads outbound freight by destination the day it is picked up. All inbound freight received by the service center in the evening or during the night is scheduled for local delivery the next business day, unless a customer requests a different delivery schedule. Our management reviews the productivity and service performance of each service center on a daily basis to ensure quality service and efficient operations.

While we have established primary responsibility for customer service at the local service center level, our customers may access information and initiate transactions through our centralized customer service department located at our corporate office or through several other gateways, such as our website, electronic data interchange (“EDI”), automated voice response systems and automated fax systems. Our systems offer direct access to information such as freight tracking, shipping documents, rate quotes, rate databases and account activity. These centralized systems and our customer service department provide our customers with a single point of contact to access information across all areas of our operations and for each of our service products.

Linehaul Transportation

Linehaul dispatchers are centralized at our corporate office and control the movement of freight among service centers through integrated freight movement systems. We also utilize load-planning software to optimize efficiencies in our linehaul operations. Our senior management regularly monitors freight movements, transit times, load factors and other productivity measurements to ensure that we maintain our highest levels of service and efficiency.

We utilize scheduled routes, and additional linehaul dispatches as necessary, to meet our published service standards. In addition, we lower our cost structure by maintaining flexible workforce rules and by primarily using twin 28-foot trailers in our linehaul operations. The use of twin 28-foot trailers permits us to transport freight directly from its point of origin to destination with minimal unloading and reloading, which also reduces cargo loss and damage expenses. We also utilize long-combination vehicles, such as triple 28-foot trailers and combinations of 48-foot and 28-foot trailers, in states where permitted. Twin trailers and long-combination vehicles permit more freight to be hauled behind a tractor than could otherwise be hauled by one large trailer.

Tractors, Trailers and Maintenance

At December 31, 2010, we owned 5,718 tractors. We generally use new tractors in linehaul operations for approximately three to five years and then transfer those tractors to P&D operations for the remainder of their useful lives. In many of our service centers, tractors perform P&D functions during the day and linehaul functions at night to maximize tractor utilization.

At December 31, 2010, we owned 20,986 trailers. We primarily purchase new trailers for our operations; however, we occasionally purchase pre-owned equipment that meets our specifications.

5

Table of Contents

At various times, we have also acquired tractors and trailers through our acquisition of business assets from other carriers. The purchase of pre-owned equipment can provide an excellent value but also can increase our fleet’s average age. The table below reflects, as of December 31, 2010, the average age of our tractors, trucks and trailers:

| Type of equipment (categorized by primary use) |

Number of units |

Average age (in years) |

||||||

| Linehaul tractors |

3,428 | 3.5 | ||||||

| P&D tractors |

2,290 | 8.8 | ||||||

| P&D trucks |

112 | 4.5 | ||||||

| Linehaul trailers |

15,178 | 8.4 | ||||||

| P&D trailers |

5,808 | 12.9 | ||||||

We develop certain specifications for tractors and trailers and then negotiate the production and purchase of this equipment with several manufacturers. These purchases are planned well in advance of anticipated delivery dates in order to accommodate manufacturers’ production schedules. We believe that there is sufficient capacity among suppliers to ensure an uninterrupted supply of equipment to support our operations.

The table below sets forth our capital expenditures for tractors and trailers for the years ended December 31, 2010, 2009 and 2008. Our capital expenditures for tractors and trailers for the past three years were limited to replacing a portion of the equipment scheduled to be retired through the normal replacement cycle. We retained much of the equipment scheduled for replacement, however, to provide sufficient capacity for us to take advantage of any increase in demand for our services caused by improvements in the economy and potential business failures or consolidation in the LTL industry. Due to our anticipated growth and our planned efforts to reduce the average age of our fleet in 2011, our equipment purchases in 2011 are expected to be significantly higher than in recent years.

| Year ended December 31, | ||||||||||||

| (In thousands) |

2010 | 2009 | 2008 | |||||||||

| Tractors |

$ | 35,777 | $ | 33,072 | $ | 27,516 | ||||||

| Trailers |

5,020 | 32,639 | 20,599 | |||||||||

| Total |

$ | 40,797 | $ | 65,711 | $ | 48,115 | ||||||

At December 31, 2010, we had major maintenance operations at our service centers in Rialto, California; Denver, Colorado; Atlanta, Georgia; Indianapolis, Indiana; Kansas City and Parsons, Kansas; Greensboro, North Carolina; Columbus, Ohio; Harrisburg, Pennsylvania; Morristown and Memphis, Tennessee; Dallas, Texas; and Salt Lake City, Utah. In addition, 19 other service center locations are equipped to perform routine and preventive maintenance and repairs on our equipment.

We adhere to established maintenance policies and procedures to help ensure our fleet is properly maintained. Linehaul tractors are routed to appropriate maintenance facilities at designated mileage or time intervals, depending upon how the equipment has been utilized. P&D tractors and trailers are scheduled for maintenance every 90 days.

Marketing and Customers

At December 31, 2010, we had a sales staff of 487 employees. We compensate our sales force, in part, based upon on-time service performance, revenue generated and Company and service center profitability, which we believe helps motivate our sales employees to achieve our service, growth and profitability objectives.

We utilize a computerized freight-costing model to determine the price level at which a particular shipment of freight will be profitable. We can modify elements of this freight-costing model to simulate the actual conditions under which the freight will be moved. We also compete for business by participating in bid solicitations. Customers generally solicit bids for relatively large numbers of shipments for a period of one to two years, and typically choose to enter into contractual arrangements with a limited number of motor carriers based upon price and service.

6

Table of Contents

Revenue is generated by customers dispersed primarily throughout the United States and North America. In 2010, our largest customer accounted for approximately 2.8% of our revenue and our largest 5, 10 and 20 customers accounted for approximately 9.1%, 13.9% and 20.8% of our revenue, respectively. For each of the previous three years, at least 90% of our revenue was derived from transporting LTL shipments for our customers and less than 5% of our revenue was generated from international services. We believe the diversity of our customer base helps protect our business from adverse developments in a single geographic region and the reduction or loss of business from a single customer.

Seasonality

Our operations are subject to seasonal trends common in the trucking industry. Our operating margins in the first quarter are normally lower due to reduced demand during the winter months. Harsh weather can also adversely affect our performance by reducing demand and reducing our ability to transport freight, which could result in decreased revenue and increased operating expenses.

Technology

We continually upgrade our technological capabilities, and we provide access to our systems through multiple gateways that offer our customers maximum flexibility and immediate access to information. We employ vehicle safety systems, freight handling systems and logistics technology to reduce costs and transit times. We continue to focus on the development and enhancement of the technology used in our operations in order to improve the efficiency and effectiveness of our services.

Insurance

We carry a significant amount of insurance with third-party insurance carriers, but we are exposed to the risk of loss on claims up to the limit for which we are self-insured. We are currently self-insured for bodily injury and property damage (“BIPD”) claims up to $2.75 million per occurrence. Cargo loss and damage claims are self-insured up to $100,000 per occurrence. We are exposed to workers’ compensation claims up to $1.0 million per occurrence, through either self-insurance or insurance deductibles. We are self-insured for group health claims up to $375,000 per occurrence plus an aggregate $200,000 over this retention level. Our long-term disability claims are self-insured to a maximum of $3,000 per month for each of our non-salaried employees. Effective April 2, 2010, salaried employees were offered an elective long-term disability plan and, as a result, the Company has no liability for new claims occurring subsequent to this date for its salaried employees.

We believe that our policy of self-insuring a portion of our risks, together with our safety and loss prevention programs, is an effective means of managing insurance costs. We also believe that our current insurance coverage is adequate to cover our liability risks.

Diesel Fuel Availability and Cost

Our industry depends heavily upon the availability of diesel fuel. Although we maintained fuel storage and pumping facilities at 45, or 21%, of our service center locations at December 31, 2010, we may experience shortages at certain locations and may be forced to incur additional expense to ensure adequate supply on a timely basis to prevent a disruption to our service schedules. We implemented a fuel surcharge program in August 1999. The program has remained in effect since that time and is one of many components that we use to determine the overall price for our transportation services. Our fuel surcharges are generally indexed to fuel prices published by the U.S. Department of Energy (the “DOE”) that reset each week. Our management believes that our operations and financial condition are susceptible to the same diesel fuel price increases or shortages as those of our competitors. Diesel fuel costs, including fuel taxes, totaled 13.1% and 11.4% of revenue in 2010 and 2009, respectively.

7

Table of Contents

Employees

As of December 31, 2010, we employed 11,179 individuals on a full-time basis, none of which were represented under a collective bargaining agreement. Our full-time employees work in the following roles:

| Category |

Number of employees |

|||

| Drivers |

5,930 | |||

| Platform |

1,701 | |||

| Fleet technicians |

375 | |||

| Sales |

487 | |||

| Salaried, clerical and other |

2,686 | |||

As of December 31, 2010, we employed 3,002 linehaul drivers and 2,928 P&D drivers on a full-time basis. Each of our drivers is required to pass a drug test and have a current U.S. Department of Transportation (“DOT”) physical and a valid commercial driver’s license prior to employment. Once employed, drivers are required to obtain and maintain hazardous materials endorsements to their commercial driver’s licenses. Drivers, as well as all employees, are required to take pre-employment drug and alcohol tests and are randomly selected for periodic additional testing.

To help fulfill driver needs, we offer qualified employees the opportunity to become drivers through the “Old Dominion Driver Training Program.” Since its inception in 1988, 2,738 individuals have graduated from this program. Of the program graduates, we have experienced an annual turnover rate of approximately 7.4%, which is below our company-wide average turnover rate of approximately 12.3% for drivers. We believe our driver training and qualification programs have been important factors in improving our safety record and retaining our qualified drivers. Drivers with safe driving records are rewarded with bonuses of up to $3,000 payable each year. Driver safety bonuses paid during 2010 and 2009 were $2.1 million and $2.0 million, respectively.

Governmental Regulation

We are subject to regulation by the Federal Motor Carrier Safety Administration (the “FMCSA”), the Pipeline and Hazardous Materials Safety Agency and the Surface Transportation Board, which are agencies within the DOT, as well as the regulations of various state agencies. These regulatory authorities have broad powers, generally governing matters such as authority to engage in motor carrier operations, motor carrier registration, driver hours of service, safety and fitness of transportation equipment and drivers, certain mergers, consolidations and acquisitions, and periodic financial reporting. In addition, we are subject to compliance with cargo-security and transportation regulations issued by the Transportation Security Administration within the U.S. Department of Homeland Security.

The trucking industry is subject to regulatory and legislative changes from a variety of other governmental authorities, which address matters such as: (i) increasingly stringent environmental and occupational safety and health regulations; (ii) limits on vehicle weight and size; (iii) ergonomics; and (iv) hours of service. These changes may affect our business or the economics of our industry by requiring changes in operating practices, or by influencing the demand for and increasing the costs of providing our services.

The cost of compliance with current applicable laws and regulations has not materially impacted our results of operations or financial condition. However, future changes to laws or regulations, including proposed changes to hours of service, may adversely affect our operations and could result in unforeseen costs to our business.

Environmental Regulation

We are subject to various federal, state and local environmental laws and regulations that focus on, among other things: the emission and discharge of hazardous materials into the environment or their presence on or in our properties and vehicles; fuel storage tanks; transportation of certain materials; and the discharge or retention of storm water. Under specific environmental laws, we could also be held responsible for any costs relating to contamination at our past or present facilities and at third-party waste

8

Table of Contents

disposal sites, as well as costs associated with clean-up of accidents involving our vehicles. We do not believe that the cost of future compliance with current environmental laws or regulations will have a material adverse effect on our operations, financial condition, competitive position or capital expenditures for the remainder of fiscal year 2011 or fiscal year 2012. However, future changes to laws or regulations may adversely affect our operations and could result in unforeseen costs to our business.

Available Information

Through our website, http://www.odfl.com, we make available, free of charge, our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and any amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Act of 1934, as soon as practicable after we electronically file the material with or furnish it to the U.S. Securities and Exchange Commission (the “SEC”). The public may read or copy any document we file with the SEC at the SEC’s website, http://www.sec.gov (File No. 0-19582), or at the SEC’s Public Reference Room at 100 F Street, NE, Washington, D.C. 20549. The SEC can be reached at 1-800-SEC-0330 for further information on the operation of the Public Reference Room. Information contained on our website is neither part of nor incorporated by reference into this Form 10-K or any other report we file with or furnish to the SEC.

| ITEM 1A. | RISK FACTORS |

Various factors exist that could cause our actual results to differ materially from those projected in any forward-looking statement. In addition to the factors discussed elsewhere in this report, we believe the following are some of the important risks and uncertainties that could materially affect our business, financial condition or results of operations:

We operate in a highly competitive industry, and our business will suffer if we are unable to adequately address potential downward pricing pressures and other factors that may adversely affect our operations and profitability.

Numerous competitive factors could impair our ability to maintain our current profitability. These factors include, but are not limited to, the following:

| • | we compete with many other transportation service providers of varying sizes, some of which may have more equipment, a broader coverage network, a wider range of services, greater capital resources or other competitive advantages; |

| • | some of our competitors periodically reduce their prices to gain business, especially during times of reduced growth rates in the economy, which may limit our ability to maintain or increase prices or maintain revenue; |

| • | we may be unable to continue to collect fuel surcharges or our fuel surcharge program may become ineffective in mitigating the impact of fluctuating costs for fuel and other petroleum-based products; |

| • | many customers reduce the number of carriers they use by selecting “core carriers” as approved transportation service providers and we may not be selected; |

| • | many customers periodically accept bids from multiple carriers for their shipping needs, and this process may depress prices or result in the loss of some business to competitors; |

| • | some customers may choose to operate their own private trucking fleet or may choose to increase the volume of freight they transport if they have an existing private trucking fleet; |

| • | the trend towards consolidation in the ground transportation industry may create other large carriers with greater financial resources and other competitive advantages relating to their size; |

| • | advances in technology require increased investments to remain competitive, and our customers may not be willing to accept higher prices to cover the cost of these investments; and |

| • | competition from non-asset-based logistics and freight brokerage companies may adversely affect our customer relationships and ability to maintain sufficient pricing. |

If we are unable to effectively compete with other LTL carriers, whether on the basis of pricing, service or otherwise, we may be unable to retain existing customers or attract new customers, either of which could have a material adverse effect on our business, financial condition and results of operations.

9

Table of Contents

If our employees were to unionize, our operating costs would increase and our ability to compete would be impaired.

None of our employees are currently represented under a collective bargaining agreement. However, from time to time there have been efforts to organize our employees at various service centers. Further, Congress or one or more states could approve legislation significantly affecting our business and our relationship with our employees, such as the proposed federal legislation referred to as the Employee Free Choice Act, which would substantially liberalize the procedures for union organization. In addition, we can offer no assurance that the Department of Labor will not adopt new regulations or interpret existing regulations in a manner that would favor the agenda of unions, or that our employees will not unionize in the future, particularly if regulatory changes occur that facilitate unionization.

The unionization of our employees could have a material adverse effect on our business, financial condition and results of operations because:

| • | some shippers have indicated that they intend to limit their use of unionized trucking companies because of the threat of strikes and other work stoppages; |

| • | restrictive work rules could hamper our efforts to improve and sustain operating efficiency; |

| • | restrictive work rules could impair our service reputation and limit our ability to provide next-day services; |

| • | a strike or work stoppage would negatively impact our profitability and could damage customer and employee relationships; and |

| • | an election and bargaining process could divert management’s time and attention from our overall objectives and impose significant expenses. |

If we are unable to successfully execute our growth strategy, our business and future results of operations may suffer.

Our growth strategy includes increasing the volume of freight moving through our existing service center network, selectively expanding our geographic footprint and broadening the scope of our service offerings. In connection with our growth strategy, at various times, we have made selective acquisitions, purchased additional equipment, expanded and upgraded service centers and increased our sales and marketing efforts, and we expect to continue to do so. Our growth strategy exposes us to a number of risks, including the following:

| • | geographic expansion requires start-up costs that could expose us to temporary losses; |

| • | growth and geographic expansion are dependent on the availability of real estate, and shortages of suitable real estate may limit our geographic expansion and might cause congestion in our service center network, which could result in increased operating expenses; |

| • | growth may strain our management, capital resources, information systems and customer service; |

| • | hiring new employees may increase training costs and may result in temporary inefficiencies until those employees become proficient in their jobs; and |

| • | expanding our service offerings may require us to enter into new markets and encounter new competitive challenges. |

We cannot assure that we will overcome the risks associated with our growth strategy. If we fail to overcome those risks, we may not realize additional revenue or profits from our efforts, we may incur additional expenses and, therefore, our financial position and results of operations could be materially and adversely affected.

We may be unable to successfully consummate and integrate acquisitions as part of our growth strategy.

Growth through acquisitions has been a key component of our LTL growth strategy throughout our history. In the future, we may seek to acquire other LTL carriers as well as other complementary businesses. Exploration of potential acquisitions requires significant attention from our senior management team. In addition, we expect to compete for acquisition opportunities with other companies, some of which may have greater financial and other resources than we do. We cannot assure that we will

10

Table of Contents

have sufficient cash with which to consummate an acquisition or otherwise be able to obtain financing for any acquisition. If we are unable to access sufficient funding for potential acquisitions, we may not be able to complete transactions that we otherwise find advantageous.

Any subsequent acquisition will entail numerous risks, including:

| • | we may not achieve anticipated levels of revenue, efficiency, cash flows and profitability; |

| • | we may experience difficulties managing businesses that are outside our historical core competency and markets; |

| • | we may underestimate the resources required to support acquisitions, which could disrupt our ongoing business and distract our management; |

| • | we may incur unanticipated costs to our infrastructure to support new business lines or separate legal entities; |

| • | we may be required to temporarily match existing customer pricing in the acquiree’s markets, which may be lower than the rates that we would typically charge for our services; |

| • | liabilities we assume could be greater than our original estimates or not disclosed to us at the time of acquisition; |

| • | we may incur additional indebtedness or we may issue additional shares of stock to finance future acquisitions, which could be dilutive to our shareholders; |

| • | potential loss of key employees and customers of the acquired company; and |

| • | an inability to recognize projected cost savings and economies of scale and scope. |

In addition, we may have difficulty in integrating any acquired business and its operations, services and personnel into our existing operations, and such integration may require a significant amount of time and effort by our management team. To the extent we do not successfully avoid or overcome the risks or problems resulting from any acquisitions we undertake, there could be a material adverse effect on our business, financial condition and results of operations.

Our customers’ and suppliers’ business may be impacted by a downturn in the economy and/or a disruption of financial markets.

Adverse economic conditions can negatively affect our customers’ business levels, the amount of transportation services they need, their ability to pay for our services and overall freight levels, all of which might impair our asset utilization. Customers encountering adverse economic conditions may be unable to obtain additional financing, or financing under acceptable terms, due to disruptions in the capital and credit markets. These customers represent a greater potential for bad debt losses, which may require us to increase our reserve for bad debt. Economic conditions resulting in bankruptcies of one or more of our large customers could have a significant impact on our financial position, results of operations or liquidity in a particular year or quarter. Further, when adverse economic times arise customers may bid out freight or select competitors that offer lower rates from among existing choices in an attempt to lower their costs and we might be forced to lower our rates or lose freight.

Our suppliers’ business levels also may be negatively affected by adverse economic conditions or financial constraints, which could lead to disruptions in the supply and availability of equipment, parts and services critical to our operations. A significant interruption in our normal supply chain could disrupt our operations, increase our costs and negatively impact our ability to serve our customers.

We also are subject to cost increases outside our control that could materially reduce our profitability if we are unable to increase our rates sufficiently. Such cost increases include, but are not limited to, increases in fuel prices, driver wages, interest rates, taxes, tolls, license and registration fees, insurance, revenue equipment and healthcare for our employees.

Increases in driver compensation or other difficulties attracting and retaining qualified drivers could adversely affect our profitability and ability to maintain or grow our fleet.

From time to time we have experienced difficulty in attracting and retaining sufficient numbers of qualified drivers and such shortages may recur in the future. Because of the intense competition for drivers, we may face difficulty maintaining or increasing our number of drivers. The compensation we offer our drivers is subject to market conditions that may require increases in driver compensation, which will be more likely to the extent that economic conditions improve. If we are unable to continue to attract and

11

Table of Contents

retain a sufficient number of drivers, we could be required to adjust our compensation packages, or operate with fewer trucks and face difficulty meeting shipper demands, all of which could adversely affect our profitability and ability to maintain our size or grow.

Insurance and claims expenses could significantly reduce our profitability.

We are exposed to claims related to cargo loss and damage, property damage, personal injury, workers’ compensation, long-term disability, group health and dental. We have insurance coverage with third-party insurance carriers, but self-insure for a significant portion of the risk associated with these claims. Our operating results would be adversely affected if any of the following were to occur: (i) the number or severity of claims for which we are self-insured increases; (ii) we are required to accrue or pay additional amounts because the claims prove to be more severe than our original assessment; or (iii) claims exceed our excess coverage amounts. If claims exceed our retention levels or insurance market conditions change, insurers could raise premiums for excess coverage to cover their expenses and anticipated future losses. In addition, insurance companies require us to obtain letters of credit to collateralize our self-insured retention. If these requirements increase, our borrowing capacity could be adversely affected.

We have significant ongoing cash requirements that could limit our growth and affect our profitability if we are unable to obtain sufficient capital.

Our business is highly capital intensive. We generally finance our capital expenditures and planned growth with existing cash, cash flow from operations, issuance of senior notes and through available borrowings under our existing senior unsecured credit agreement. We may require additional capital to finance long-term real estate purchase opportunities and acquisitions, which we may fund through additional debt or through equity offerings. If we are unable in the future to generate sufficient cash from our operations or raise capital by accessing the debt and equity markets, we may be forced to limit our growth and operate our equipment for longer periods of time, which could have a material adverse effect on our operating results.

Our business also has significant ongoing operating cash requirements. If our cash requirements are high or our cash flow from operations is low during particular periods, we may need to seek additional financing, which may be costly or difficult to obtain.

Limited supply and increased prices for new equipment may adversely affect our earnings and cash flow.

Investment in new equipment is a significant part of our annual capital expenditures and we require an available supply of tractors and trailers from equipment manufacturers to operate and grow our business. We may face difficulty in purchasing new equipment due to decreased supply. We have experienced higher prices for new tractors over the past few years. The price of our equipment may also be adversely affected in the future by regulations on newly manufactured tractors and diesel engines. For example, the U.S. Environmental Protection Agency (the “EPA”) has issued regulations that require progressive reductions in exhaust emissions from diesel engines through 2010. Beginning in October 2002, new diesel engines were required to meet these new emission limits. Some of the regulations required reductions in the sulfur content of diesel fuel beginning in June 2006 and the introduction of emissions after-treatment devices on newly-manufactured engines and vehicles beginning with model-year 2007. The final phase of the regulations requires reduced nitrogen and non-methane hydrocarbon emissions beginning with model-year 2010. These regulations have resulted in higher prices for tractors and diesel engines and increased fuel, diesel exhaust fluid and maintenance costs, and there can be no assurance that continued increases in pricing or costs will not have an adverse effect on our business and operations.

A decrease in the demand and value of used equipment may impact our results of operations.

As we purchase new tractors as part of our normal replacement cycle each year, we rely on the used equipment market to dispose of our older equipment. Oversupply in the transportation industry as well as adverse domestic and foreign economic conditions can negatively impact the demand for used tractors and, therefore, reduce the value we can obtain on our used equipment. If we are unable to sell our replacement vehicles at or above salvage value, the resulting losses could have a significant impact on our results of operations.

12

Table of Contents

We may be adversely impacted by fluctuations in the availability and price of diesel fuel.

Diesel fuel is a critical component of our operations and a significant operating expense for our business. Diesel fuel prices and fuel availability can be impacted by factors beyond our control, such as natural or man-made disasters, political events, price and supply decisions by oil producing countries and cartels, terrorist activities, armed conflict and world supply and demand imbalances. We maintain fuel storage and pumping facilities at many of our service center locations; however, we may experience shortages in the availability of diesel fuel at certain locations and may be forced to incur additional expense to ensure adequate supply on a timely basis to prevent a disruption to our service schedules. An interruption in the supply of diesel fuel could have a material adverse effect on our operating results.

We do not hedge against the risk of diesel fuel price increases. An increase in diesel fuel prices or diesel fuel taxes, or any change in federal or state regulations that results in such an increase, could have a material adverse effect on our operating results. We have fuel surcharge programs in place with a majority of our customers, which have helped us offset the majority of the negative impact of the increased cost of diesel fuel and other petroleum-based products. However, we also incur fuel costs that cannot be recovered even with respect to customers with which we maintain fuel surcharge programs, such as those associated with empty miles, deadhead miles or the time when our engines are idling. Because our fuel surcharge recovery lags behind changes in fuel prices, our fuel surcharge recovery may not capture the increased costs we pay for fuel, especially when prices are rising, leading to fluctuations in our levels of reimbursement. Further, during periods of low freight volumes, shippers can use their negotiating leverage to impose less compensatory fuel surcharge policies. We regularly monitor the components of our pricing, including fuel surcharges, and address individual account profitability issues with our customers when necessary; however, there can be no assurance that fuel surcharges can be maintained indefinitely or will be sufficiently effective in offsetting increases in diesel fuel prices.

We are subject to various environmental laws and regulations, and costs of compliance with, liabilities under, or violations of, existing or future environmental laws or regulations could adversely affect our business.

We are subject to various federal, state and local environmental laws and regulations that govern, among other things, the emission and discharge of hazardous materials into the environment, the presence of hazardous materials at our properties or in our vehicles, fuel storage tanks, the transportation of certain materials and the discharge or retention of storm water. Under certain environmental laws, we could also be held responsible for any costs relating to contamination at our past or present facilities and at third-party waste disposal sites, as well as costs associated with the clean-up of accidents involving our vehicles. Environmental laws have become and are expected to continue to be increasingly more stringent over time, and there can be no assurance that our costs of complying with current or future environmental laws or liabilities arising under such laws will not have a material adverse effect on our business, operations or financial condition.

In addition to the EPA regulations on exhaust emissions with which we must comply, there is an increased regulatory focus on climate change and greenhouse gas emissions in the United States. As a result, we may become subject to additional legislation that could adversely impact our business. At this time, we cannot predict the requirements of any future regulations. However, any limitations on the emission of greenhouse gases or other environmental legislation could increase our future capital expenditures and have an adverse impact on our financial condition, results of operations and liquidity.

We operate in a highly regulated industry, and increased costs of compliance with, or liability for violation of, existing or future regulations could have a material adverse effect on our business.

We are regulated by the DOT and by various state agencies. These regulatory authorities have broad powers, generally governing matters such as authority to engage in motor carrier operations, as well as motor carrier registration, driver hours of service, safety and fitness of transportation equipment and drivers, transportation of hazardous materials, certain mergers and acquisitions and periodic financial reporting. In addition, the trucking industry is subject to regulatory and legislative changes from a variety of other governmental authorities, which address matters such as: (i) increasingly stringent environmental, occupational safety and health regulations; (ii) limits on vehicle weight and size; (iii) ergonomics; (iv) port security; and (v) hours of service. In addition, we are subject to compliance with cargo-security and transportation regulations issued by the Transportation Security Administration within the U.S. Department

13

Table of Contents

of Homeland Security. Regulatory requirements, and changes in regulatory requirements, may affect our business or the economics of the industry by requiring changes in operating practices or by influencing the demand for and increasing the costs of providing transportation services.

In October 2009, the U.S. Court of Appeals for the District of Columbia Circuit ordered the FMCSA to review and re-issue rules governing hours of service for commercial truck drivers by July 26, 2011. In response to this ruling, on December 23, 2010, the FMCSA issued a regulatory proposal subject to a public comment period that ends March 4, 2011. This proposal addresses the length of driver work days, the length and frequency of driver rest breaks, driver “restart” periods following specified off-duty hours and other matters relating to hours of service. The final rules that will be adopted by the FMCSA are uncertain at this time and could have a significant impact on our operations and the cost of providing our services. We are also subject to future rulemaking by the FMCSA and other regulatory agencies, which could be more stringent, require changes to our operations, increase our operating costs and otherwise adversely impact our results of operations.

The implementation of FMCSA’s Compliance, Safety, Accountability initiative (“CSA”) could adversely impact our ability to hire qualified drivers, meet our growth projections and maintain our customer relationships, each of which could adversely impact our results of operations.

In December 2010, the FMCSA began implementation of CSA, a new compliance and enforcement initiative designed to monitor and improve commercial motor vehicle safety. CSA measures both the safety record of the motor carrier and the driver. These measurements are scored and used by the FMCSA to identify potential safety risks and to direct enforcement action. CSA scores for transportation companies are currently available on the FMCSA’s website and replace SafeStat, the FMCSA’s former safety measurement system.

Our CSA scores are dependent upon our safety and compliance experience, which could change at any time. In addition, the safety standards prescribed in CSA could change and our ability to maintain an acceptable score could be adversely impacted. If we receive an unacceptable CSA score, our relationships with our customers could be damaged, which could result in a loss of business.

The implementation of CSA could also shrink the industry’s pool of drivers as those with unfavorable scores could leave the industry. As a result, the costs to attract, train and retain qualified drivers could increase. In addition, a shortage of qualified drivers could increase driver turnover, decrease asset utilization, limit growth and adversely impact our results of operations.

Our results of operations may be affected by seasonal factors and harsh weather conditions.

Our operations are subject to seasonal trends common in the trucking industry. Our operating margins in the first quarter are normally lower due to reduced demand during the winter months. Harsh weather can also adversely affect our performance by reducing demand and reducing our ability to transport freight, which could result in decreased revenue and increased operating expenses.

If we are unable to retain our key employees, our financial condition, results of operations and liquidity could be adversely affected.

Our success will continue to depend upon the experience and leadership of our key employees and executive officers. In that regard, the loss of the services of any of our key personnel could have a material adverse effect on our financial condition, results of operations and liquidity.

Our principal shareholders control a large portion of our outstanding common stock.

Earl E. Congdon, John R. Congdon and members of their respective families beneficially own approximately 28% of the outstanding shares of our common stock. As long as the Congdon family controls a large portion of our voting stock, they may be able to significantly influence the election of the entire Board of Directors and the outcome of all matters involving a shareholder vote. The Congdon family’s interests may differ from the interests of other shareholders and the status of their ownership could change at their discretion. In addition, our Chief Executive Officer, David S. Congdon, has pledged approximately 648,000 shares of our common stock held in a revocable trust for his benefit to secure an approximately $3.5 million margin loan. If there were a default, the bank would have the right to sell shares to satisfy this obligation. Such an event could cause our stock price to decline.

14

Table of Contents

Our financial results may be adversely impacted by potential future changes in accounting practices.

Future changes in accounting standards or practices, and related legal and regulatory interpretations of those changes, may adversely impact public companies in general, the transportation industry or our operations specifically. New accounting standards or requirements, such as a conversion from U.S. generally accepted accounting principles to International Financial Reporting Standards, could change the way we record revenues, expenses, assets and/or liabilities or could be costly to implement. These types of regulations could have a negative impact on our financial position, liquidity, results of operations and/or access to capital.

Our information technology systems are subject to certain risks that we cannot control.

Our information systems, including our accounting systems, are dependent upon third-party software, global communications providers, telephone systems and other aspects of technology and Internet infrastructure that are susceptible to failure. Although we have implemented redundant systems and network security measures, our information technology remains susceptible to outages, computer viruses, break-ins and similar disruptions that may inhibit our ability to provide services to our customers and the ability of our customers to access our systems. This may result in the loss of customers or a reduction in demand for our services.

If we raise additional capital in the future, your ownership in us could be diluted.

Any issuance of equity we may undertake in the future to raise additional capital could cause the price of our common stock to decline, or require us to issue shares at a price that is lower than that paid by holders of our common stock in the past, which would result in those newly issued shares being dilutive. If we obtain funds through a credit facility or through the issuance of debt or preferred securities, these obligations and securities would likely have rights senior to your rights as a common shareholder, which could impair the value of our common stock.

The market value of our common stock may fluctuate and could be substantially affected by various factors.

The price of our common stock on the NASDAQ Global Select Market, or Nasdaq, constantly changes. We expect that the market price of our common stock will continue to fluctuate. Our share price may fluctuate as a result of a variety of factors, many of which are beyond our control. These factors include, among others:

| • | Actual or anticipated variations in earnings, financial or operating performance or liquidity; |

| • | Changes in analysts’ recommendations or projections; |

| • | Failure to meet analysts’ projections; |

| • | General economic and capital market conditions; |

| • | Announcements of developments related to our business; |

| • | Operating and stock performance of other companies deemed to be peers; |

| • | Actions by government regulators; and |

| • | News reports of trends, concerns and other issues related to us or our industry, including changes in regulations. |

Our common stock price may fluctuate significantly in the future, and these fluctuations may be unrelated to our performance. General market price declines or market volatility in the future could adversely affect the price of our common stock, and the current market price of our common stock may not be indicative of future market prices.

15

Table of Contents

Our articles of incorporation, our bylaws and Virginia law contain provisions that could discourage, delay or prevent a change in our control or our management.

Provisions of our articles of incorporation, bylaws and the laws of Virginia, the state in which we are incorporated, may discourage, delay or prevent a change in control of us or a change in management that shareholders may consider favorable. These provisions:

| • | limit who may call a special meeting of shareholders; |

| • | require shareholder action by written consent to be unanimous; |

| • | establish advance notice requirements for nominations for election to our Board of Directors or for proposing matters that can be acted upon at shareholder meetings; |

| • | may make it difficult to merge with or otherwise absorb a Virginia corporation acquired in a tender offer for the three years after the acquisition; and |

| • | may make an unsolicited attempt to gain control of us more difficult by restricting the right of specified shareholders to vote newly acquired large blocks of stock. |

These provisions could discourage proxy contests and make it more difficult for you and other shareholders to take certain corporate actions. These provisions could also limit the price that investors might be willing to pay in the future for shares of our common stock.

ITEM 1B. UNRESOLVED STAFF COMMENTS

None.

16

Table of Contents

We own our general office located in Thomasville, North Carolina, consisting of a two-story office building of approximately 160,000 square feet on 30.1 acres of land. At December 31, 2010, we operated 213 service centers, of which 132 were owned and 81 were leased. Our service centers that are owned include most of our larger facilities and account for 79% of the total door capacity in our network. With the exception of our Chicago, Illinois facility, which has a lease that expires in 2021, we own our major breakbulk facilities. Each of our breakbulk facilities is listed below with the number of doors as of December 31, 2010.

| Service Center |

Doors | |||

| Harrisburg, Pennsylvania |

305 | |||

| Morristown, Tennessee |

247 | |||

| Dallas, Texas |

234 | |||

| Atlanta, Georgia |

227 | |||

| Indianapolis, Indiana |

223 | |||

| Greensboro, North Carolina |

219 | |||

| Memphis, Tennessee |

169 | |||

| Rialto, California |

152 | |||

| Chicago, Illinois |

134 | |||

| Salt Lake City, Utah |

129 | |||

Our 213 facilities are strategically dispersed over the states in which we operate. At December 31, 2010, the terms of our leased properties ranged from month-to-month to a lease that expires in 2023. We believe that as current leases expire, we will be able to renew them or find comparable facilities without incurring any material negative impact on service to our customers or our operating results.

We also own 22 non-operating properties, all of which are held for lease or are planned for future use. Five of these properties are leased with lease terms that range from month-to-month to a lease that expires in 2012.

We believe that all of our properties are in good repair and are capable of providing the level of service required by current business levels and customer demands. In addition, we believe we have sufficient capacity in our service center network to accommodate a substantial increase in demand for our services.

We are involved in various legal proceedings and claims that have arisen in the ordinary course of our business that have not been fully adjudicated. Many of these are covered in whole or in part by insurance. Our management does not believe that these actions, when finally concluded and determined, will have a material adverse effect upon our financial position, liquidity or results of operations.

ITEM 4. (REMOVED AND RESERVED)

PART II

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Common Stock and Dividend Information

Our common stock is traded on the NASDAQ Global Select Market, which we refer to as the Nasdaq, under the symbol ODFL. At February 18, 2011, there were approximately 11,330 holders of our common stock, including 158 shareholders of record. We did not pay any dividends on our common stock during fiscal year 2010 or 2009, and we have no current plans to declare or pay any dividends on our common stock during fiscal year 2011. For information concerning restrictions on our ability to make dividend payments, see Liquidity and Capital Resources in Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and Note 2 in Item 8, “Financial Statements and Supplementary Data” of this report.

17

Table of Contents

On July 30, 2010, our Board of Directors approved a three-for-two common stock split for shareholders of record as of the close of business on August 9, 2010. On August 23, 2010, those shareholders received one additional share of common stock for every two shares owned. In lieu of fractional shares, shareholders received a cash payment based on the average of the high and low sales prices of the common stock on the record date.

The following table sets forth the high and low sales price of our common stock for the periods indicated, as reported by the Nasdaq and as adjusted to give effect to the three-for-two stock split effected in August 2010:

| 2010 | ||||||||||||||||

| First Quarter |

Second Quarter |

Third Quarter |

Fourth Quarter |

|||||||||||||

| High |

$ | 23.07 | $ | 25.89 | $ | 27.29 | $ | 32.24 | ||||||||

| Low |

$ | 17.56 | $ | 21.02 | $ | 22.45 | $ | 24.36 | ||||||||

| 2009 | ||||||||||||||||

| First Quarter |

Second Quarter |

Third Quarter |

Fourth Quarter |

|||||||||||||

| High |

$ | 19.67 | $ | 22.54 | $ | 25.83 | $ | 23.30 | ||||||||

| Low |

$ | 12.46 | $ | 15.07 | $ | 19.75 | $ | 16.07 | ||||||||

18

Table of Contents

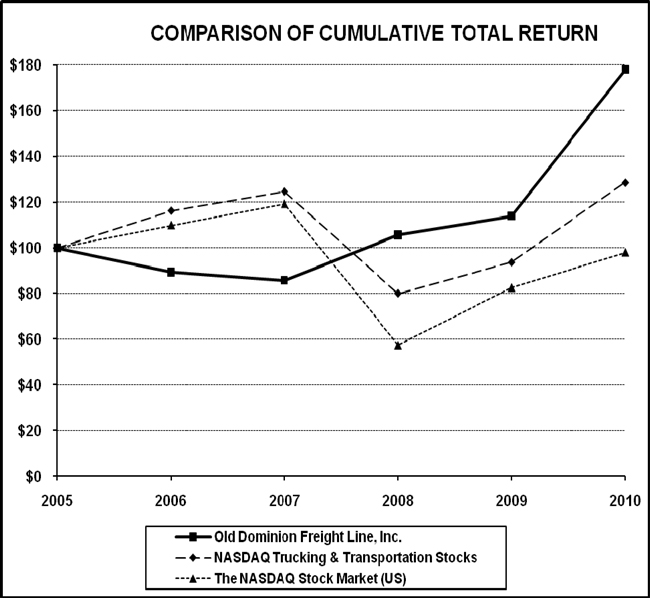

Performance Graph

The following graph compares the total shareholder cumulative returns, assuming the reinvestment of all dividends, of $100 invested on December 31, 2005, in (i) our common stock, (ii) the NASDAQ Trucking & Transportation Stocks and (iii) The NASDAQ Stock Market (US) for the five-year period ended December 31, 2010:

Cumulative Total Return

| 12/31/05 | 12/31/06 | 12/31/07 | 12/31/08 | 12/31/09 | 12/31/10 | |||||||||||||||||||

| Old Dominion Freight Line, Inc. |

$ | 100 | $ | 89 | $ | 86 | $ | 106 | $ | 114 | $ | 178 | ||||||||||||

| NASDAQ Trucking & Transportation Stocks |

$ | 100 | $ | 116 | $ | 125 | $ | 80 | $ | 94 | $ | 129 | ||||||||||||

| The NASDAQ Stock Market (US) |

$ | 100 | $ | 110 | $ | 119 | $ | 57 | $ | 83 | $ | 98 | ||||||||||||

19

Table of Contents

ITEM 6. SELECTED FINANCIAL DATA

| Year Ended December 31, | ||||||||||||||||||||

| (In thousands, except per share amounts and operating statistics) |

2010 | 2009 | 2008 | 2007 | 2006 | |||||||||||||||

| Operating Data: |

||||||||||||||||||||

| Revenue from operations |

$ | 1,480,998 | $ | 1,245,005 | $ | 1,537,724 | $ | 1,401,542 | $ | 1,279,431 | ||||||||||

| Depreciation and amortization expense (1) |

80,362 | 94,784 | 87,083 | 79,863 | 67,634 | |||||||||||||||

| Total operating expenses |

1,343,259 | 1,174,614 | 1,408,654 | 1,271,605 | 1,148,946 | |||||||||||||||

| Operating income |

137,739 | 70,391 | 129,070 | 129,937 | 130,485 | |||||||||||||||

| Interest expense, net (2) |

12,465 | 12,998 | 13,012 | 12,960 | 10,206 | |||||||||||||||

| Provision for income taxes |

48,775 | 22,294 | 43,989 | 43,963 | 46,774 | |||||||||||||||

| Net income |

75,651 | 34,871 | 68,677 | 71,832 | 72,569 | |||||||||||||||

| Per Share Data: |

||||||||||||||||||||

| Diluted earnings per share (3) |

1.35 | 0.62 | 1.23 | 1.28 | 1.30 | |||||||||||||||

| Balance Sheet Data: |

||||||||||||||||||||

| Cash, cash equivalents and short-term investments |

5,450 | 4,171 | 28,965 | 30,703 | 87,724 | |||||||||||||||

| Current assets |

222,582 | 174,175 | 209,230 | 216,277 | 256,367 | |||||||||||||||

| Total assets |

1,239,881 | 1,159,278 | 1,074,905 | 981,048 | 892,193 | |||||||||||||||

| Current liabilities |

170,046 | 148,125 | 142,190 | 127,723 | 121,546 | |||||||||||||||

| Long-term debt (including current maturities) |

271,217 | 305,532 | 251,989 | 263,754 | 274,582 | |||||||||||||||

| Shareholders’ equity |

668,649 | 593,000 | 558,129 | 489,452 | 417,620 | |||||||||||||||

| Operating Statistics: |

||||||||||||||||||||

| Operating ratio |

90.7 | % | 94.3 | % | 91.6 | % | 90.7 | % | 89.8 | % | ||||||||||

| Revenue per hundredweight |

$ | 13.09 | $ | 12.70 | $ | 13.88 | $ | 13.30 | $ | 13.16 | ||||||||||

| Revenue per intercity mile |

$ | 4.38 | $ | 4.16 | $ | 4.60 | $ | 4.31 | $ | 4.32 | ||||||||||

| Intercity miles (in thousands) |

338,504 | 299,330 | 334,219 | 325,268 | 296,464 | |||||||||||||||

| Total tons (in thousands) |

5,656 | 4,902 | 5,545 | 5,271 | 4,859 | |||||||||||||||

| Total shipments (in thousands) |

6,327 | 5,750 | 6,691 | 6,765 | 6,428 | |||||||||||||||

| Average length of haul (miles) (4) |

948 | 928 | 901 | 926 | 922 | |||||||||||||||

| (1) | Our 2010 results also reflect reductions in our depreciation and amortization expenses of approximately $12.7 million, due to changes in the estimated useful lives and salvage values of certain equipment, which are described further under “Critical Accounting Policies” below. |

| (2) | For the purpose of this table, interest expense is presented net of interest income. |

| (3) | Per share data has been restated retroactively for the three-for-two stock split effected in August 2010. |

| (4) | We refined our average length of haul in 2008 by excluding miles driven by our agent carriers. As a result, our average length of haul is restated for years prior to 2008 presented in this report. |

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Overview

We are a leading, less-than-truckload (“LTL”), non-union motor carrier providing regional, inter-regional and national LTL service and value-added logistics services from a single integrated organization. In addition to our core LTL services, we offer our customers a broad range of logistics services including ground and air expedited transportation, supply chain consulting, transportation management, truckload brokerage, container delivery and warehousing services. Through marketing and carrier relationships, we also offer door-to-door international freight services to and from all of North America, Central America, South America and the Far East. More than 90% of our revenue has historically been derived from transporting LTL shipments for our customers, whose demand for our services is generally tied to industrial production and the overall health of the U.S. domestic economy.

20

Table of Contents

In analyzing the components of our revenue, we monitor changes and trends in the following key metrics:

| • | Revenue Per Hundredweight – This measurement reflects our pricing policies, which are influenced by competitive market conditions and our growth objectives. Generally, freight is rated by a class system, which is established by the National Motor Freight Traffic Association, Inc. Light, bulky freight typically has a higher class and is priced at higher revenue per hundredweight than dense, heavy freight. Changes in the class, packaging of the freight and length of haul of the shipment can also affect this average. Fuel surcharges, accessorial charges, revenue adjustments and revenue for undelivered freight are included in this measurement. Revenue for undelivered freight is deferred for financial statement purposes in accordance with our revenue recognition policy; however, we believe including this deferred revenue in our revenue per hundredweight measurements results in a better indicator of changes in our yields by matching total billed revenue with the corresponding weight of those shipments. |

| • | Weight Per Shipment – Fluctuations in weight per shipment can indicate changes in the class, or mix, of freight we receive from our customers, as well as changes in the number of units included in a shipment. Generally, increases in weight per shipment indicate higher demand for our customers’ products and overall increased economic activity. |

| • | Average Length of Haul – We consider lengths of haul less than 500 miles to be regional traffic, lengths of haul between 500 miles and 1,000 miles to be inter-regional traffic, and lengths of haul in excess of 1,000 miles to be national traffic. By analyzing this metric, we can determine the success and growth potential of our service products in these markets. |

| • | Revenue Per Shipment – This measurement is primarily determined by the three metrics listed above and is used, in conjunction with the number of shipments we receive, to calculate total revenue, excluding adjustments for undelivered freight. |

Our primary revenue focus is to increase shipment and tonnage growth within our existing infrastructure, generally referred to as increasing density, thereby maximizing asset utilization and labor productivity. We measure density over many different functional areas of our operations including revenue per service center, linehaul load factor, P&D stops per hour, P&D shipments per hour, platform pounds handled per hour and platform shipments per hour. In addition to our focus on density, it is critical for us to obtain an appropriate yield on the shipments we handle. We manage our yields by focusing on individual account profitability. We believe yield management and improvements in density are key components in our ability to produce profitable growth.

Our primary cost elements are direct wages and benefits associated with the movement of freight; operating supplies and expenses, which includes fuel and repair parts; and depreciation of our equipment fleet and service center facilities. We gauge our overall success in managing these costs by monitoring our operating ratio, a measure of profitability calculated by dividing total operating expenses by revenue, which also allows industry-wide comparisons with our competition.

We continually upgrade our technological capabilities to improve our customer service and lower our operating costs. Our technology provides our customers with visibility of their shipments throughout our network, increases the productivity of our workforce and provides key metrics from which we can monitor our processes.

21

Table of Contents

Results of Operations

The following table sets forth, for the years indicated, expenses and other items as a percentage of revenue from operations:

| 2010 | 2009 | 2008 | ||||||||||

| Revenue from operations |

100.0 | % | 100.0 | % | 100.0 | % | ||||||

| Operating expenses: |

||||||||||||

| Salaries, wages and benefits |

54.6 | 57.7 | 52.3 | |||||||||

| Operating supplies and expenses |

16.5 | 14.6 | 19.9 | |||||||||

| General supplies and expenses |

2.8 | 2.8 | 2.8 | |||||||||

| Operating taxes and licenses |

3.8 | 4.0 | 3.4 | |||||||||

| Insurance and claims |

1.7 | 1.8 | 2.3 | |||||||||

| Communication and utilities |

1.0 | 1.2 | 1.0 | |||||||||

| Depreciation and amortization |

5.4 | 7.6 | 5.7 | |||||||||

| Purchased transportation |

3.4 | 2.7 | 2.8 | |||||||||

| Building and office equipment rents |

1.0 | 1.2 | 1.0 | |||||||||

| Miscellaneous expenses, net |

0.5 | 0.7 | 0.4 | |||||||||

| Total operating expenses |

90.7 | 94.3 | 91.6 | |||||||||

| Operating income |

9.3 | 5.7 | 8.4 | |||||||||

| Interest expense, net (1) |

0.8 | 1.1 | 0.8 | |||||||||

| Other expense, net |

0.1 | 0 | 0.2 | |||||||||

| Income before income taxes |

8.4 | 4.6 | 7.4 | |||||||||

| Provision for income taxes |

3.3 | 1.8 | 2.9 | |||||||||

| Net income |

5.1 | % | 2.8 | % | 4.5 | % | ||||||

| (1) | For the purpose of this table, interest expense is presented net of interest income. |

2010 Compared to 2009

Key financial and operating metrics for 2010 and 2009 are presented below:

| 2010 | 2009 | Change | % Change | |||||||||||||

| Work days |

253 | 253 | 0 | 0 | ||||||||||||

| Revenue (in thousands) |

$ | 1,480,998 | $ | 1,245,005 | $ | 235,993 | 19.0 | |||||||||

| Operating ratio |

90.7 | % | 94.3 | % | (3.6 | )% | (3.8 | ) | ||||||||

| Net income (in thousands) |

$ | 75,651 | $ | 34,871 | $ | 40,780 | 116.9 | |||||||||

| Diluted earnings per share |

$ | 1.35 | $ | 0.62 | $ | 0.73 | 117.7 | |||||||||

| Total tons (in thousands) |

5,656 | 4,902 | 754 | 15.4 | ||||||||||||

| Total shipments (in thousands) |

6,327 | 5,750 | 577 | 10.0 | ||||||||||||

| Weight per shipment (lbs.) |

1,788 | 1,705 | 83 | 4.9 | ||||||||||||

| Revenue per hundredweight |

$ | 13.09 | $ | 12.70 | $ | 0.39 | 3.1 | |||||||||

| Revenue per shipment |

$ | 234.09 | $ | 216.49 | $ | 17.60 | 8.1 | |||||||||

| Average length of haul (miles) |

948 | 928 | 20 | 2.2 | ||||||||||||

During 2010 we achieved significant increases in our shipments and tonnage, which accelerated during the second half of the year. We believe these increases were the result of our ability to gain market share during the year as well as general growth in U.S. industrial production and manufacturing. As industry capacity tightened in 2010, many of our competitors implemented significant rate increases. This

22

Table of Contents

reversed an industry trend of several years in which many of our competitors had discounted prices. While we implemented a modest general rate increase in November 2010, our pricing philosophy remained consistent with our strategy throughout the recession, which was to provide “best-in-class” on-time and claims-free service at a fair and equitable price. We believe more shippers are shifting their focus to evaluating the overall value of the service they receive as industry pricing increases. We believe this trend, along with other market dynamics, will provide additional opportunities for us to increase tonnage and market share growth in 2011.