Attached files

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2010

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

333-126751

(Commission File Number)

LAZARD GROUP LLC

(Exact name of registrant as specified in its charter)

| Delaware | 51-0278097 | |

| (State or Other Jurisdiction of Incorporation | (I.R.S. Employer Identification No.) | |

| or Organization) |

30 Rockefeller Plaza

New York, NY 10020

(Address of principal executive offices)

Registrant’s telephone number: (212) 632-6000

| Securities Registered Pursuant to Section 12(b) of the Act: None | ||

| Securities Registered Pursuant to Section 12(g) of the Act: None | ||

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

| Large accelerated filer ¨ | Accelerated filer ¨ | |

| Non-accelerated filer x | Smaller reporting company ¨ |

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

As of June 30, 2010, none of the Registrant’s common membership interests were held by non-affiliates. As of June 30, 2010, LAZ-MD Holdings LLC held 13,874,679 common memberships interests of the Registrant, representing 11.0% of the Registrant’s then outstanding common membership interests. As of January 31, 2011, LAZ-MD Holdings LLC held 7,633,593 common membership interests, or 6.0% of the Registrant’s then outstanding common membership interests. If LAZ-MD Holdings LLC is not deemed an “affiliate” of the Registrant, then as of June 30, 2010 there would have been 13,874,679 outstanding common membership interests of the Registrant held by non-affiliates, with a market value of $370,592,676 (assuming each common membership interest has a value equivalent to one share of Lazard Ltd Class A common stock and based on a closing price per share of $26.71 of Lazard Ltd Class A common stock on June 30, 2010).

As of January 31, 2011, in addition to profit participation interests, there were 127,331,529 common membership interests and two managing member interests outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

None

Table of Contents

ANNUAL REPORT ON FORM 10-K

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2010

INDEX

i

Table of Contents

When we use the terms “Lazard Group”, “Lazard”, “we”, “us”, “our”, and “the Company”, we mean Lazard Group LLC, a Delaware limited liability company that is the current holding company for the subsidiaries that conduct our businesses. Lazard Ltd is a Bermuda exempt company whose shares of Class A common stock (the “Class A common stock”) are publicly traded on the New York Stock Exchange under the Symbol “LAZ”. Lazard Ltd’s subsidiaries include Lazard Group and their respective subsidiaries. Lazard Ltd has no material operating assets other than indirect ownership as of December 31, 2010 of approximately 94.0% of the common membership interests in Lazard Group. Lazard Ltd controls Lazard Group through two of its indirect wholly-owned subsidiaries who are co-managing members of Lazard Group.

Lazard Group has two primary holders of its common membership interests: Lazard Ltd and LAZ-MD Holdings LLC (“LAZ-MD Holdings”), a holding company that is owned by Lazard Group’s current and former managing directors. The Lazard Group common membership interests held by LAZ-MD Holdings are effectively exchangeable over time on a one-for-one basis with Lazard Ltd for shares of Lazard Ltd’s Class A common stock. In addition, Lazard Group has granted profit participation interests in Lazard Group to certain of its managing directors in connection with the recapitalization of Lazard Group at the time of Lazard Ltd’s equity public offering. The profit participation interests are discretionary profits interests that are intended to enable Lazard Group to compensate its managing directors in a manner consistent with historical practices.

| Item 1. | Business |

We are one of the world’s preeminent financial advisory and asset management firms and have long specialized in crafting solutions to the complex financial and strategic challenges of our clients. We serve a diverse set of clients around the world, including corporations, partnerships, institutions, governments and high-net worth individuals. The first Lazard partnership was established in 1848. Over time we have extended our activities beyond our roots in New York, Paris and London. We currently operate from 41 cities in key business and financial centers across 26 countries throughout Europe, North America, Asia, Australia, the Middle East and Central and South America.

The Separation and Recapitalization

On May 10, 2005, Lazard Ltd completed the equity public offering (the “equity public offering”) of its Class A common stock, the public offering of equity security units of Lazard Ltd, the private placements under an investment agreement with IXIS Corporate & Investment Bank (“IXIS” or, following its merger with and into its parent, “Natixis”) and the private offering of the 7.125% senior notes due 2015 of Lazard Group, primarily to recapitalize Lazard Group. We refer to these financing transactions and the recapitalization, collectively, as the “recapitalization.” As part of the recapitalization, Lazard Group used the net proceeds from the financing transactions primarily to redeem the outstanding Lazard Group membership interests of certain of its historical partners.

On May 10, 2005, Lazard Group also transferred its capital markets business, which consisted of equity, fixed income and convertibles sales and trading, broking, research and underwriting services, and fund management activities outside of France as well as other specified non-operating assets and liabilities, to LFCM Holdings LLC, a Delaware limited liability company (“LFCM Holdings”). We refer to these businesses, assets and liabilities as the “separated businesses” and these transfers collectively as the “separation.”

Principal Business Lines

We focus primarily on two business segments - Financial Advisory and Asset Management. We believe that the mix of our activities across business segments, geographic regions, industries and investment strategies helps to diversify and stabilize our revenue stream.

1

Table of Contents

Financial Advisory

We offer corporate, partnership, institutional, government, sovereign and individual clients across the globe a wide array of financial advisory services regarding mergers and acquisitions (“M&A”) and other strategic matters, restructurings, capital structure, capital raising and various other corporate finance matters. We focus on solving our clients’ most complex problems, providing advice to senior management, boards of directors and business owners of prominent companies and institutions in transactions that typically are of significant strategic and financial importance to them.

We continue to build our Financial Advisory business by fostering long-term, senior level relationships with existing and new clients as their independent advisor on strategic transactions. We seek to build and sustain long-term relationships with our clients rather than focusing simply on individual transactions, a practice that we believe enhances our access to senior management of major corporations and institutions around the world. We emphasize providing clients with senior level focus during all phases of transaction execution.

While we strive to earn repeat business from our clients, we operate in a highly competitive environment in which there are no long-term contracted sources of revenue. Each revenue-generating engagement is separately negotiated and awarded. To develop new client relationships, and to develop new engagements from historical client relationships, we maintain an active dialogue with a large number of clients and potential clients, as well as with their financial and legal advisors, on an ongoing basis. We have gained a significant number of new clients each year through our business development initiatives, through recruiting additional senior investment banking professionals who bring with them client relationships and through referrals from directors, attorneys and other third parties with whom we have relationships. At the same time, we lose clients each year as a result of the sale or merger of a client, a change in a client’s senior management, competition from other investment banks and other causes.

For the years ended December 31, 2010, 2009 and 2008, the Financial Advisory segment net revenue totaled $1.120 billion, $987 million and $1.023 billion, respectively, accounting for approximately 59%, 65% and 66%, respectively, of our consolidated net revenue for such years. We earned $1 million or more from 255 clients, 257 clients and 220 clients for the years ended December 31, 2010, 2009 and 2008, respectively. For the years ended December 31, 2010, 2009 and 2008, the ten largest fee paying clients constituted approximately 16%, 17% and 20% of our Financial Advisory segment net revenue, respectively, with no client individually having constituted more than 10% of segment net revenue during any of these years. For the years ended December 31, 2010, 2009 and 2008, the Financial Advisory segment reported operating income (loss) of $169 million, $(12) million and $226 million, respectively. Operating income in 2010 and 2009 included charges of approximately $20 million and $49 million, respectively, representing the portion of special items (as described in Management’s Discussion and Analysis of Financial Condition and Results of Operations and Note 22 of Notes to Consolidated Financial Statements) that are applicable to the Financial Advisory segment. Excluding the impact of such special items, our Financial Advisory segment had operating income of $189 million, $37 million and $226 million in the years ended December 31, 2010, 2009 and 2008, respectively. At December 31, 2010, 2009 and 2008, the Financial Advisory segment had total assets of $799 million, $707 million and $739 million, respectively.

We believe that we have been pioneers in offering financial advisory services on an international basis, with the establishment of our New York, Paris and London offices dating back to the nineteenth century. We maintain a major local presence in the U.S., the United Kingdom (the “U.K.”) and France, including a network of regional branch offices in the U.S. and France, as well a presence in Argentina, Australia, Belgium, Brazil, Chile, Colombia, Dubai, Germany, Hong Kong, India, Italy, Japan, the Netherlands, Panama, Peru, Singapore, South Korea, Spain, Sweden, Switzerland, Uruguay and mainland China.

Over the past several years, our Financial Advisory segment has made several business acquisitions and entered into certain other business relationships. On August 13, 2007, we acquired all of the outstanding ownership interests of Goldsmith, Agio, Helms & Lynner, LLC (“GAHL”), a Minneapolis-based investment bank specializing

2

Table of Contents

in financial advisory services to mid-sized private companies. On July 31, 2007, Lazard Ltd acquired all of the outstanding shares of Carnegie, Wylie & Company (Holdings) PTY LTD (“CWC”), an Australia-based financial advisory firm, and concurrently sold such investment to Lazard Group. Furthermore, on June 19, 2007, we entered into a joint cooperation agreement with Raiffeisen Investment AG (“Raiffeisen”) for merger and acquisition advisory services in Russia and the Central and Eastern European (the “CEE”) region. This cooperation agreement is currently in the process of being renewed. The cooperation between us and Raiffeisen, one of the CEE region’s top M&A advisors, provides domestic, international and cross-border expertise within Russia and the CEE region. In addition, on January 31, 2008, we acquired a 50% interest in Merchant Bankers Asociados (“MBA”), an Argentina-based financial advisory services firm with offices across Central and South America and the parent company of MBA Banco de Inversiones. In February 2009, we entered into a strategic alliance with a financial advisory firm in Mexico to provide global M&A advisory services for clients, both inside and outside of Mexico, who are seeking to acquire or sell assets in Mexico or have interests in other financial transactions with companies in Mexico, and to provide restructuring advisory services to clients in Mexico.

In addition to seeking business centered in the locations referred to above, we historically have focused in particular on advising clients with respect to cross-border transactions. We believe that we are particularly well known for our legacy of offering broad teams of professionals who are indigenous to their respective regions and who have long-term client relationships, capabilities and know-how in their respective regions, who will coordinate with our professionals with global sector expertise. We also believe that this positioning affords us insight around the globe into key industry, economic, government and regulatory issues and developments, which we can bring to bear on behalf of our clients.

Services Offered

We advise clients on a wide range of strategic and financial issues. When we advise clients on the potential acquisition of another company, business or certain assets, our services include evaluating potential acquisition targets, providing valuation analyses, evaluating and proposing financial and strategic alternatives and rendering, if appropriate, fairness opinions. We also may advise as to the timing, structure, financing and pricing of a proposed acquisition and assist in negotiating and closing the acquisition. In addition, we may assist in executing an acquisition by acting as a dealer-manager in transactions structured as a tender or exchange offer.

When we advise clients that are contemplating the sale of certain businesses, assets or their entire company, our services include advising on the appropriate sales process for the situation, valuation issues, assisting in preparing an offering circular or other appropriate sales materials and rendering, if appropriate, fairness opinions. We also identify and contact selected qualified acquirors and assist in negotiating and closing the proposed sale. As appropriate, we also advise our clients regarding financial and strategic alternatives to a sale including recapitalizations, spin-offs, carve-outs, split-offs and tracking stocks. Our advice includes recommendations with respect to the structure, timing and pricing of these alternatives.

For companies in financial distress, our services may include reviewing and analyzing the business, operations, properties, financial condition and prospects of the company, evaluating debt capacity, assisting in the determination of an appropriate capital structure and evaluating and recommending financial and strategic alternatives, including providing advice on dividend policy. If appropriate, we may provide financial advice and assistance in developing and seeking approval of a restructuring or reorganization plan, which may include a plan of reorganization under Chapter 11 of the U.S. Bankruptcy Code or other similar court administered processes in non-U.S. jurisdictions. In such cases, we may assist in all aspects of the implementation of such a plan, including advising and assisting in structuring and effecting the financial aspects of a sale or recapitalization, structuring new securities, exchange offers, other considerations or other inducements to be offered or issued, as well as assisting and participating in negotiations with affected entities or groups.

When we assist clients in raising private or public market financing, our services include originating and executing private placements of equity, debt and related securities, assisting clients in connection with securing, refinancing or restructuring bank loans, originating public underwritings of equity, debt and convertible securities and

3

Table of Contents

originating and executing private placements of partnership and similar interests in alternative investment funds such as leveraged buyout, mezzanine or real estate focused funds. In addition, we may advise on capital structure and assist in long-range capital planning and rating agency relationships.

Since the beginning of the financial crisis that began in mid-2007, we have been at the forefront of providing independent advice to governments and governmental agencies challenged by the current troubled environment. Lazard’s Sovereign Advisory Group is also highly active, advising a number of countries with respect to sovereign debt.

In connection with the separation, we entered into a business alliance agreement dated as of May 10, 2005 by and among Lazard Group, LAZ-MD Holdings and LFCM Holdings (the “business alliance agreement”), pursuant to which a subsidiary of LFCM Holdings generally underwrites and distributes U.S. securities offerings originated by our Financial Advisory business in a manner intended to be similar to our practice prior to the separation, with revenue from such offerings generally continuing to be divided evenly between Lazard Group and LFCM Holdings.

Staffing

We staff our assignments with a team of quality professionals who have appropriate product and industry expertise. We pride ourselves on, and we believe we differentiate ourselves from our competitors by, being able to offer a high level of attention from senior personnel to our clients and organizing ourselves in such a way that managing directors who are responsible for securing and maintaining client relationships also actively participate in providing related transaction execution services. Our managing directors have significant experience, and many of them are able to use this experience to advise on both M&A and restructuring transactions, depending on our clients’ needs. Many of our managing directors and senior advisors come from diverse backgrounds, such as senior executive positions at corporations and in government, law and strategic consulting, which we believe enhances our ability to offer sophisticated advice and customized solutions to our clients. As of December 31, 2010, our Financial Advisory segment had 129 managing directors, 673 other professionals (which includes directors, vice presidents, associates and analysts) and 222 support staff personnel.

Industries Served

We seek to offer our services across most major industry groups, including, in many cases, sub-industry specialties. Our Mergers and Acquisitions managing directors and professionals are organized to provide advice in the following major industry practice areas:

| • | consumer, |

| • | financial institutions, |

| • | financial sponsors, |

| • | healthcare and life sciences, |

| • | industrial, |

| • | power and energy/infrastructure, |

| • | real estate, and |

| • | technology, media and telecommunications. |

These groups are managed locally in each relevant geographic region and are coordinated globally, which allows us to bring local industry-specific knowledge to bear on behalf of our clients on a global basis. We believe that this enhances the quality of the advice that we can offer, which improves our ability to market our capabilities to clients.

4

Table of Contents

In addition to our Mergers and Acquisitions and Restructuring practices, we also maintain specialties in the following distinct practice areas within our Financial Advisory segment:

| • | government advisory, |

| • | capital structure and debt advisory, |

| • | fund raising for alternative investment funds, |

| • | private investment in public equities, or “PIPES”, and |

| • | corporate finance and other advisory services, including convertible exchange transactions, Registered Direct offerings and private placements. |

We endeavor to coordinate the activities of the professionals in these areas with our Mergers and Acquisitions industry specialists in order to offer clients customized teams of cross-functional expertise spanning both industry and practice area expertise.

Strategy

Our focus in our Financial Advisory business is on:

| • | making a significant investment in our intellectual capital with the addition of senior professionals who we believe have strong client relationships and industry expertise, |

| • | increasing our contacts with existing clients to further enhance our long-term relationships and our efforts in developing new client relationships, |

| • | expanding the breadth and depth of our industry expertise and selectively adding new practice areas, such as our capital structure advisory effort to help corporations and governments in addressing the significant deleveraging that is occurring in the developed markets, |

| • | coordinating our industry specialty activities on a global basis and increasing the integration of our industry experts in mergers and acquisitions with our Restructuring and Capital Markets professionals, and |

| • | broadening our geographic presence by adding new offices, including, since the beginning of 2007, offices in Australia (Melbourne and Perth), Switzerland (Zurich) and United Arab Emirates (Dubai City), as well as new regional offices in the U.S. (Boston, Minneapolis, Charlotte and Washington DC), acquiring a 50% interest in a financial advisory firm with offices in Central and South America (Argentina, Chile, Colombia, Panama, Peru and Uruguay) and entering into a joint cooperation agreement in Eastern Europe and Russia, as well as a strategic alliance with a financial advisory firm in Mexico. |

In addition to the investments made as part of this strategy, we believe that the following external market factors may enable our Financial Advisory business to benefit by:

| • | increasing demand for independent, unbiased financial advice, and |

| • | a potential increase in cross-border M&A and large capitalization M&A, two of our areas of historical specialization. |

Going forward, our strategic emphasis in our Financial Advisory business is to leverage the investments we have made in recent years to grow our business and drive our productivity. We continue to seek to opportunistically attract outstanding individuals to our business. We routinely reassess our strategic position and may in the future seek opportunities to further enhance our competitive position. In this regard, since 2007, as described above, we broadened our geographic footprint through acquisitions, investments and alliances.

5

Table of Contents

Relationship with Natixis

Lazard Group and Natixis have in place a cooperation arrangement to place and underwrite securities in the French capital markets under a common brand, currently “Lazard-Natixis,” and cooperate in their respective origination, syndication, placement and other activities, whose term continues through July 8, 2012. This arrangement primarily covers French listed companies included in the Société des Bourses Francaises (“SBF”) 120 Index and initial public offerings with an expected resulting market capitalization of at least €500 million.

Asset Management

Our Asset Management business provides investment management and advisory services to institutional clients, financial intermediaries, private clients and investment vehicles around the world. Our goal in our Asset Management business is to produce superior risk-adjusted investment returns and provide investment solutions customized for our clients. Many of our equity investment strategies share an investment philosophy that centers on fundamental security selection with a focus on the trade-off between a company’s valuation and its financial productivity.

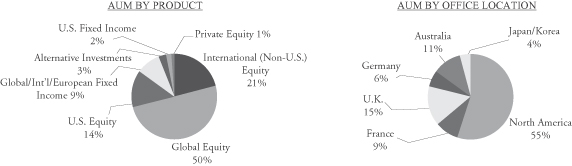

As of December 31, 2010, total assets under management (“AUM”) were $155.3 billion, of which approximately 85% was invested in equities, 11% in fixed income, 3% in alternative investments, and 1% in private equity funds. As of the same date, approximately 30% of our AUM was invested in international (i.e., non-U.S. and regional non-U.S.) investment strategies, 50% was invested in global investment strategies and 20% was invested in U.S. investment strategies, and our top ten clients accounted for 22% of our total AUM. Approximately 90% of our AUM as of that date was managed on behalf of institutional clients, including corporations, labor unions, public pension funds, insurance companies and banks, and through sub-advisory relationships, mutual fund sponsors, broker-dealers and registered advisors, and approximately 10% of our AUM as of December 31, 2010 was managed on behalf of individual client relationships, which are principally with family offices and high-net worth individuals.

The charts below illustrate the mix of our AUM as of December 31, 2010, measured by broad product strategy and by office location.

For the years ended December 31, 2010, 2009 and 2008, our Asset Management segment net revenue totaled $850 million, $602 million and $615 million, respectively, accounting for approximately 45%, 39% and 39%, respectively, of our consolidated net revenue for such years. For the years ended December 31, 2010, 2009 and 2008, Asset Management reported operating income (loss) of $265 million, $97 million and $(63) million, respectively. Operating income (loss) in 2010, 2009 and 2008 included charges of $3 million, $8 million and approximately $197 million, respectively, representing the portion of the special items (as described in Management’s Discussion and Analysis of Financial Condition and Results of Operations and Note 22 of Notes to Consolidated Financial Statements) that are applicable to the Asset Management segment. Excluding the impact of such special items, our Asset Management segment had operating income of $268 million, $105 million and $134 million in the years ended December 31, 2010, 2009 and 2008, respectively. At December 31, 2010, 2009 and 2008, our Asset Management segment had total assets of $687 million, $703 million and $420 million, respectively.

6

Table of Contents

LAM and LFG

Our largest Asset Management subsidiaries are Lazard Asset Management LLC and its subsidiaries (“LAM”), with offices in New York, San Francisco, Boston, Chicago, Toronto, Montreal, London, Milan, Frankfurt, Hamburg, Tokyo, Hong Kong, Sydney, Seoul and Bahrain (aggregating approximately $140.6 billion in total AUM as of December 31, 2010), and Lazard Frères Gestion SAS (“LFG”), with offices in Paris and Brussels (aggregating approximately $13.5 billion in total AUM as of December 31, 2010). These operations, with 630 employees as of December 31, 2010, provide our business with both a global presence and a local identity.

Primary distinguishing features of these operations include:

| • | a global footprint with global research, global mandates and global clients, |

| • | a broad-based team of approximately 250 investment professionals at December 31, 2010: LAM had approximately 215 investment professionals, including approximately 95 focused, in-house, investment analysts across all products and platforms, many of whom have substantial industry or sector specific expertise, and LFG had approximately 35 investment professionals, including research analysts, |

| • | a security selection-based investment philosophy applied across products, and |

| • | world-wide brand recognition and multi-channel distribution capabilities. |

Our Investment Philosophy, Process and Research. Our investment philosophy is generally based upon a fundamental security selection approach to investing. Across many of our products, we apply three key principles to investment portfolios:

| • | select securities, not markets, |

| • | evaluate the trade-off between returns and valuations, and |

| • | manage risk. |

In searching for equity investment opportunities, many of our investment professionals follow an investment process that incorporates several interconnected components that may include:

| • | analytical framework analysis and screening, |

| • | accounting validation, |

| • | fundamental analysis, |

| • | security selection and portfolio construction, and |

| • | risk management. |

At LAM, we conduct investment research on a global basis to develop market, industry and company specific insights and evaluate investment opportunities. The LAM global equity analysts, located in our worldwide offices, are organized around six global industry sectors:

| • | consumer goods, |

| • | financial services, |

| • | health care, |

| • | industrials, |

| • | power, and |

| • | technology, media and telecommunications. |

7

Table of Contents

Investment Strategies. Our Asset Management business provides equity, fixed income, cash management and alternative investment strategies to our clients, paying close attention to our clients’ varying and expanding investment needs. We offer the following product platform of investment strategies:

| Global |

Regional |

Domestic | ||||

| Equities |

Global Large Capitalization Small Capitalization Emerging Markets Thematic Convertibles* Listed Infrastructure Quantitative

EAFE (Non-U.S.) Large Capitalization Small Capitalization Multi-Capitalization Quantitative

Global Ex Global Ex-U.K. Global Ex-Japan Global Ex-Australia |

Pan-European Large Capitalization Small Capitalization Quantitative

Eurozone Large Capitalization** Small Capitalization**

Continental European Small Cap Multi Cap Eurozone (i.e., Euro Bloc) Euro-Trend (Thematic) |

U.S. Large Capitalization** Mid Capitalization Small/Mid Capitalization Multi-Capitalization

Other U.K. (Large Capitalization) U.K. (Small Capitalization) U.K. Quantitative Australia France (Large Capitalization)* France (Small Capitalization)* Japan** Korea | |||

| Fixed Income and Cash Management | Global Core Fixed Income High Yield Short Duration Emerging Markets |

Pan-European Core Fixed Income High Yield Cash Management* Duration Overlay

Eurozone Fixed Income** Cash Management* Corporate Bonds** |

U.S. Core Fixed Income High Yield Short Duration Municipals Cash Management*

Non-U.S. U.K. Fixed Income | |||

| Alternative |

Global Fund of Hedge Funds Fund of Closed-End Funds Convertible Arbitrage/Relative Value Emerging Income |

Regional European Explorer Japan (Long/Short) |

||||

All of the above strategies are offered by LAM, except for those denoted by *, which are offered exclusively by LFG. Investment strategies offered by both LAM and LFG are denoted by **.

In addition to the primary investment strategies listed above, we also provide locally customized investment solutions to our clients. In many cases, we also offer both diversified and more concentrated versions of our products. These products are generally offered on a separate account basis, as well as through pooled vehicles.

Distribution. We distribute our products through a broad array of marketing channels on a global basis. LAM’s marketing, sales and client service efforts are organized through a global market delivery and service network, with distribution professionals located in cities including New York, San Francisco, London, Milan, Frankfurt, Hamburg, Tokyo, Sydney, Hong Kong, Bahrain and Seoul. We have developed a well-established presence in the institutional asset management arena, managing money for corporations, labor unions, sovereign wealth funds and public pension funds around the world. In addition, we manage assets for insurance companies, savings and trust banks, endowments, foundations and charities.

8

Table of Contents

We also have become a leading firm in third-party distribution, managing mutual funds and separately managed accounts for many of the world’s largest broker-dealers, insurance companies, registered advisors and other financial intermediaries. In the area of wealth management, we cater to family offices and private clients.

LFG markets and distributes its products through 22 sales professionals based in France, who directly target both individual and institutional investors.

In June 2009, the Company formed a new wealth management subsidiary, Lazard Wealth Management LLC (“Lazard Wealth Management”). Lazard Wealth Management provides customized investment management and financial planning services to high net worth investors in the U.S. Lazard Wealth Management works with investors to construct, implement and monitor an asset allocation strategy designed to meet the individual client’s investment objectives, integrating tax planning, estate planning, philanthropic interests and legacy planning with investment and risk management services. Lazard Wealth Management is registered as an investment adviser with the United States Securities and Exchange Commission (the “SEC”). As of December 31, 2010, Lazard Wealth Management had 20 employees.

Strategy

Our strategic plan in our Asset Management business is to focus on delivering superior investment performance and client service and broadening our product offerings and distribution in selected areas in order to continue to drive improved business results. Over the past several years, in an effort to improve LAM’s operations and expand our business, we have:

| • | focused on enhancing our investment performance, |

| • | improved our investment management platform by adding a number of senior investment professionals (including portfolio managers and analysts), |

| • | continued to strengthen our marketing and consultant relations capabilities, |

| • | expanded our product platform, including the addition of a new emerging markets debt team, and |

| • | continued to expand LAM’s geographic reach, including through opening offices in Hong Kong and Bahrain. |

We believe that our Asset Management business has long maintained an outstanding team of portfolio managers and global research analysts. We intend to maintain and supplement our intellectual capital to achieve our goals. We routinely reassess our strategic position and may in the future seek acquisitions or other transactions, including the opportunistic hiring of new employees, in order to further enhance our competitive position. We also believe that our specific investment strategies, global reach, unique brand identity and access to multiple distribution channels may allow us to expand into new investment products, strategies and geographic locations. In addition, we plan to expand our participation in alternative investment activities through investments in new and successor funds, and are considering expanding the services we offer to high-net worth individuals, through organic growth, acquisitions or otherwise.

Alternative Investments

Lazard has a long history of making investments with its own capital, often alongside capital of qualified institutional and individual investors. These activities typically are organized in funds that make substantial or controlling investments in private or public companies, generally through privately negotiated transactions and with a view to divestment within two to seven years. While potentially risky and frequently illiquid, such investments, when successful, can yield investors substantial returns on capital and generate attractive management and performance fees for the sponsor of such funds.

As a part of the separation in 2005, we transferred to LFCM Holdings all of our alternative investment activities at that time, except for Fonds Partenaires Gestion SA (“FPG”), our private equity business in France,

9

Table of Contents

which, until September 30, 2009, was a subsidiary of our Paris-based banking affiliate, Lazard Frères Banque SA (“LFB”). We also transferred to LFCM Holdings certain principal investments by Lazard Group in the funds managed by the separated businesses. Effective September 30, 2009, the Company sold FPG.

LFCM Holdings operates the alternative investment business (including private equity activities) transferred to it in the separation. Consistent with our intent to support the development of the alternative investment business, including investing capital in funds managed or formed by Lazard Alternative Investments Holdings LLC (“LAI”), a subsidiary of LFCM Holdings, and in order to benefit from what we believe to be the potential of this business, we are entitled to receive from LFCM Holdings all or a portion of the payments from the incentive distributions attributable to these funds (net of compensation payable to investment professionals who manage these funds) pursuant to the business alliance agreement. In addition, pursuant to the business alliance agreement, we retained an option to acquire the North American and European fund management activities of LAI and have the right to participate in the oversight of LFCM Holdings’ funds and consent to certain actions. On December 15, 2009, Lazard Group exercised its option to acquire the European fund management activities of LAI. The remaining option to purchase the North American fund management activities is currently exercisable at any time prior to May 10, 2014 (see Note 20 of Notes to Consolidated Financial Statements). We will continue to abide by our obligations with respect to transferred funds. From time to time, we have considered exercising the option with respect to the remaining activities in North America.

Since 2005, consistent with our obligations to LFCM Holdings, we have engaged in a number of alternative investments and private equity activities. In February 2009 the business alliance agreement was amended to remove certain restrictions on the Company engaging in private equity businesses in North America and to reduce the price of our option to acquire the fund management activities of LAI in North America. We continue to explore and discuss opportunities to expand the scope of our alternative investment and private equity activities in Europe, the U.S. and elsewhere. These opportunities could include internal growth of new funds and direct investments by us, partnerships or strategic relationships, investments with third parties or acquisitions of existing funds or management companies. In that regard, on July 15, 2009, the Company established a private equity business with The Edgewater Funds (“Edgewater”), a Chicago-based private equity firm, through the acquisition of Edgewater’s management vehicles. The acquisition was structured as a purchase by Lazard of interests in a holding company that owns interests in the general partner and management company entities of the current Edgewater private equity funds (the “Edgewater Acquisition”) (see Note 9 of Notes to Consolidated Financial Statements). As of December 31, 2010, Edgewater, with 18 employees, had approximately $1.0 billion of AUM and unfunded fee-earning commitments. Also, consistent with our obligations to LFCM Holdings, we may explore discrete capital markets opportunities. See Notes 14 and 20 of Notes to Consolidated Financial Statements for additional information regarding alternative investments, including certain matters with respect to Corporate Partners II Limited (“CP II MgmtCo.”).

CWC operates our private equity business in Australia, which, as of December 31, 2010, had 8 employees and approximately $200 million of private equity AUM.

Employees

We believe that our people are our most important asset, and it is their reputation, talent, integrity and dedication that underpin our success. As of December 31, 2010, we employed 2,332 people, which included 129 managing directors and 673 other professionals in our Financial Advisory segment and 64 managing directors and 315 other professionals in our Asset Management segment. We strive to maintain a work environment that fosters professionalism, excellence, diversity and cooperation among our employees worldwide. We generally utilize an evaluation process at the end of each year to measure performance, determine compensation and provide guidance on opportunities for improved performance. Generally, our employees are not subject to any collective bargaining agreements, except that our employees in certain of our European offices, including France and Italy, are covered by national, industry-wide collective bargaining agreements. We believe that we have good relations with our employees.

10

Table of Contents

Competition

The financial services industry, and all of the businesses in which we compete, are intensely competitive, and we expect them to remain so. Our competitors are other investment banking and financial advisory firms, broker-dealers, commercial and “universal” banks, insurance companies, investment management firms, hedge fund management firms, alternative investment firms and other financial institutions. We compete with some of our competitors globally and with others on a regional, product or niche basis. We compete on the basis of a number of factors, including quality of people, transaction execution skills, investment track record, quality of client service, individual and institutional client relationships, absence of conflicts, range of products and services, innovation, brand recognition and business reputation.

While our competitors vary by country in our Mergers and Acquisitions practice, we believe our primary competitors in securing M&A advisory engagements are Bank of America, Barclays, Citigroup, Credit Suisse, Deutsche Bank AG, Goldman Sachs & Co., JPMorgan Chase, Mediobanca, Morgan Stanley, Rothschild and UBS. In our Restructuring practice, our primary competitors are The Blackstone Group, Evercore Partners, Greenhill & Co., Houlihan Lokey, Moelis & Company and Rothschild.

We believe that our primary global competitors in our Asset Management business include, in the case of LAM, Alliance Bernstein, Brandes Investment Partners, Capital Management & Research, Fidelity, Invesco, Lord Abbett, Aberdeen and Schroders and, in the case of LFG, private banks with offices in France as well as large institutional banks and fund managers. We face competition in private equity both in the pursuit of outside investors for our private equity funds and the acquisition of investments in attractive portfolio companies. We compete with hundreds of other funds, many of which are subsidiaries of or otherwise affiliated with large financial service providers.

Competition is also intense in each of our businesses for the attraction and retention of qualified employees, and we compete on the level and nature of compensation and equity-based incentives for key employees. Our ability to continue to compete effectively in our businesses will depend upon our ability to attract new employees and retain and motivate our existing employees.

In recent years there has been substantial consolidation and convergence among companies in the financial services industry. In particular, a number of large commercial banks, insurance companies and other broad-based financial services firms have established or acquired broker-dealers or have merged with other financial institutions. This trend was amplified in connection with the unprecedented disruption and volatility in the financial markets during the past several years, and, as a result, a number of financial services companies have merged, been acquired or have fundamentally changed their respective business models, including, in certain cases, becoming commercial banks. Many of these firms have the ability to offer a wider range of products than we offer, including loans, deposit taking, insurance and brokerage services. Many of these firms also offer more extensive asset management and investment banking services, which may enhance their competitive position. They also have the ability to support investment banking and securities products with commercial banking, insurance and other financial services revenue in an effort to gain market share, which could result in pricing pressure in our businesses. This trend toward consolidation and convergence has significantly increased the capital base and geographic reach of our competitors, and, in certain instances, has afforded them access to government funds.

Regulation

Our businesses, as well as the financial services industry generally, are subject to extensive regulation throughout the world. As a matter of public policy, regulatory bodies are charged with safeguarding the integrity of the securities and other financial markets and with protecting the interests of customers participating in those markets, not with protecting the interests of our stockholders or creditors. Many of our affiliates that participate in securities markets are subject to comprehensive regulations that include some form of capital structure regulations and customer protection rules. In the U.S., certain of our subsidiaries are subject to such regulations promulgated by the SEC or Financial

11

Table of Contents

Industry Regulatory Authority (“FINRA”) (formerly the NASD) or the Municipal Securities Rulemakers Board (the “MSRB”). Standards, requirements and rules implemented throughout the European Union are broadly comparable in scope and purpose to the regulatory capital and customer protection requirements imposed under the SEC and FINRA rules. European Union directives also permit local regulation in each jurisdiction, including those in which we operate, to be more restrictive than the requirements of such European Union-wide directives. These sometimes burdensome local requirements can result in certain competitive disadvantages to us.

In the U.S., the SEC is the federal agency responsible for the administration of the federal securities laws. FINRA is a voluntary, self-regulatory body composed of members, such as our broker-dealer subsidiaries, that have agreed to abide by FINRA’s rules and regulations. The MSRB is also a voluntary, self-regulatory body, composed of members, including “municipal advisors”, that have agreed to abide by the MSRB’s rules and regulations. The SEC, FINRA, MSRB and non-U.S. regulatory organizations may examine the activities of, and may expel, fine and otherwise discipline us and our employees. The laws, rules and regulations comprising this framework of regulation and the interpretation and enforcement of existing laws, rules and regulations are constantly changing, particularly in light of the extraordinary disruption and volatility in the global financial markets experienced in recent years. The effect of any such changes cannot be predicted and may impact the manner of operation and profitability of our company.

Our principal U.S. broker-dealer subsidiary, Lazard Frères & Co. LLC (“LFNY”), through which we conduct most of our U.S. Financial Advisory business, is currently registered as a broker-dealer with the SEC and FINRA, and as a broker-dealer in all 50 U.S. states, the District of Columbia and Puerto Rico. As such, LFNY is subject to regulations governing effectively every aspect of the securities business, including minimum capital requirements, record-keeping and reporting procedures, relationships with customers, experience and training requirements for certain employees, and business procedures with firms that are not members of certain regulatory bodies. LFNY is also currently registered with the SEC and the MSRB as a “municipal advisor”, a new registration category that includes placement agents that solicit investments from public pension funds on behalf of investments funds. The MSRB has adopted, and is in the process of adopting, additional rules to govern municipal advisors, including “pay-to-play” rules and rules regarding professional standards, and LFNY is subject to those rules. Lazard Asset Management Securities LLC, a subsidiary of LAM, is registered as a broker-dealer with the SEC and FINRA and in all 50 U.S. states, the District of Columbia and Puerto Rico. Lazard Middle Market LLC, a subsidiary of GAHL, is registered as a broker-dealer with the SEC and FINRA, and as a broker-dealer in various U.S. states and territories.

Certain U.K. subsidiaries of Lazard Group, including Lazard & Co., Limited, Lazard Fund Managers Limited and Lazard Asset Management Limited, which we refer to in this Annual Report on Form 10-K (this “Form 10-K”) as the “U.K. subsidiaries,” are regulated by the Financial Services Authority. We also have other subsidiaries that are registered as broker-dealers (or have similar non-US registration in various jurisdictions).

Compagnie Financière Lazard Frères SAS (“CFLF”), our French subsidiary through which non-corporate finance advisory activities are carried out in France, is subject to regulation by the Autorité de Contrôle Prudentiel for its banking activities conducted through its subsidiary, LFB. In addition, the investment services activities of the Paris group, exercised through LFB and other subsidiaries of CFLF, primarily LFG (asset management), are subject to regulation and supervision by the Autorité des Marchés Financiers. Our business is also subject to regulation by non-U.S. governmental and regulatory bodies and self-regulatory authorities in other countries where we operate.

Our U.S. broker-dealer subsidiaries, including LFNY, are subject to the SEC’s uniform net capital rule, Rule 15c3-1 under the Securities Exchange Act of 1934, as amended (the “Exchange Act”), and the net capital rules of FINRA, which may limit our ability to make withdrawals of capital from our broker-dealer subsidiaries. The uniform net capital rule sets the minimum level of net capital a broker-dealer must maintain and also requires that a portion of its assets be relatively liquid. FINRA may prohibit a member firm from expanding its business or paying cash dividends if it would result in net capital falling below FINRA’s requirements. In addition, our broker-dealer subsidiaries are subject to certain notification requirements related to withdrawals of

12

Table of Contents

excess net capital. Our broker-dealer subsidiaries are also subject to regulations, including the USA PATRIOT Act of 2001, which impose obligations regarding the prevention and detection of money-laundering activities, including the establishment of customer due diligence and other compliance policies and procedures. Failure to comply with these requirements may result in monetary, regulatory and, in certain cases, criminal penalties.

Certain of our Asset Management subsidiaries are registered as investment advisors with the SEC. As registered investment advisors, each is subject to the requirements of the Investment Advisers Act and the SEC’s regulations thereunder. Such requirements relate to, among other things, the relationship between an advisor and its advisory clients, as well as general anti-fraud prohibitions. LAM serves as an advisor to several mutual funds which are registered under the Investment Company Act. The Investment Company Act regulates, among other things, the relationship between a mutual fund and its investment advisor (and other service providers) and prohibits or severely restricts principal transactions between an advisor and its advisory clients, imposes record- keeping and reporting requirements, disclosure requirements, limitations on trades where a single broker acts as the agent for both the buyer and seller (known as “agency cross”), and limitations on affiliated transactions and joint transactions. Lazard Asset Management Securities LLC, a subsidiary of LAM, serves as the underwriter or distributor for mutual funds and hedge funds managed by LAM, and as an introducing broker to Lazard Capital Markets LLC for unmanaged accounts of LAM’s private clients.

In addition, the Japanese Ministry of Finance and the Financial Supervisory Agency, the Korean Financial Supervisory Commission, as well as Australian and German banking authorities, among others, regulate various of our operating entities and also have capital standards and other requirements comparable to the rules of the SEC.

Regulators are empowered to conduct administrative proceedings that can result in censure, fine, the issuance of cease-and-desist orders or the suspension or expulsion or other disciplining of a broker-dealer or its directors, officers or employees.

Lazard Ltd is currently subject to supervision by the SEC as a Supervised Investment Bank Holding Company (“SIBHC”). As a SIBHC, Lazard Ltd is subject to group-wide supervision, which requires it to compute allowable capital and risk allowances on a consolidated basis. However, the Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Dodd-Frank Act”), provides for the elimination of the SEC’s SIBHC program on July 21, 2011. Following this elimination, we will be required to be regulated on a comprehensive basis by another regulatory body, either in the U.S. or Europe, pursuant to relevant rules in Europe. The Dodd-Frank Act allows certain securities holding companies seeking consolidated supervision to elect to be regulated by the Board of Governors of the Federal Reserve. The Dodd-Frank Act could have other effects on us, which we are currently in the process of examining, including the impact of the elimination of the SIBHC program and the effects of various new regulations mandated by the Dodd-Frank Act.

Over the last several years, global financial markets experienced extraordinary disruption and volatility. As a result, the U.S. and other governments have taken actions, and may continue to take further actions, in response to this disruption and volatility, including expanding current or enacting new standards, requirements and rules that may be applicable to us and our subsidiaries. The effect of any such expanded or new standards, requirements and rules is uncertain and could have adverse consequences to our business and results of operations.

Executive Officers of the Registrant

Set forth below are the name, age, present title, principal occupation and certain biographical information for each of our executive officers as of February 22, 2011, all of whom have been appointed by, and serve at the pleasure of, our board of directors.

13

Table of Contents

Kenneth M. Jacobs, 52

Mr. Jacobs has served as Chairman and Chief Executive Officer of Lazard Ltd and Lazard Group LLC since November 2009. Mr. Jacobs served as a Managing Director of Lazard since 1991 and had been a deputy chairman of Lazard from January 2002 until November 2009. He had also served as Chief Executive Officer of Lazard North America beginning in 2002. Mr. Jacobs initially joined Lazard in 1988. Mr. Jacobs is a member of the Board of Trustees of the University of Chicago and the Brookings Institution.

Michael J. Castellano, 64

Mr. Castellano has served as Chief Financial Officer of Lazard Ltd since May 2005. Mr. Castellano has served as a Managing Director and Chief Financial Officer of Lazard Group since August 2001. Prior to joining Lazard, Mr. Castellano held various senior management positions at Merrill Lynch & Co. from August 1991 to August 2001, including Senior Vice President—Chief Control Officer for Merrill Lynch’s capital markets businesses, Chairman of Merrill Lynch International Bank and Senior Vice President—Corporate Controller. Prior to joining Merrill Lynch & Co., Mr. Castellano was a partner with Deloitte & Touche where he served a number of investment banking clients over the course of his 24 years with the firm.

Ashish Bhutani, 50

Mr. Bhutani is a Vice Chairman and Managing Director of Lazard and has been the Chief Executive Officer of LAM since March 2004. Mr. Bhutani has served as a director of Lazard Ltd and Lazard Group since March 2010. Mr. Bhutani previously served as Head of New Products and Strategic Planning for LAM from June 2003 to March 2004. Prior to joining Lazard, he was Co-Chief Executive Officer, North America, of Dresdner Kleinwort Wasserstein from 2001 to the end of 2002, and was a member of its Global Corporate and Markets Board, and a member of the Global Executive Committee. Mr. Bhutani worked at Wasserstein Perella Group (the predecessor to Dresdner Kleinwort Wasserstein) from 1989 to 2001, serving as Deputy Chairman of Wasserstein Perella Group and Chief Executive Officer of Wasserstein Perella Securities from 1994 to 2001. Mr. Bhutani began his career at Salomon Brothers in 1985, where he was a Vice President in Fixed Income. Mr. Bhutani is a member of the Board of Directors of four registered investment companies, which are part of the Lazard fund complex.

Scott D. Hoffman, 48

Mr. Hoffman has served as General Counsel of Lazard Ltd since May 2005. Mr. Hoffman has served as a Managing Director of Lazard Group since January 1999 and General Counsel of Lazard Group since January 2001. Mr. Hoffman previously served as Vice President and Assistant General Counsel from February 1994 to December 1997 and as a Director from January 1998 to December 1998. Prior to joining Lazard, Mr. Hoffman was an attorney at Cravath, Swaine & Moore LLP. Mr. Hoffman is a member of the Board of Trustees of the New York University School of Law.

Alexander F. Stern, 44

Mr. Stern has served as Chief Operating Officer of Lazard Ltd and Lazard Group LLC since November 2008. He has served as a Managing Director since January 2002 and as the Firm’s Global Head of Strategy since February 2006. Mr. Stern previously served as a Vice President in Lazard’s Financial Advisory business from January 1998 to December 2000 and as a Director from January 2001 to December 2001. Mr. Stern joined Lazard in 1994 and previously held various positions with Patricof & Co. Ventures and IBM.

Where You Can Find Additional Information

Lazard Group files current, annual and quarterly reports and other information required by the Exchange Act, with the SEC. You may read and copy any document the company files at the SEC’s public reference room

14

Table of Contents

located at 100 F Street, N.E., Washington, D.C. 20549, U.S.A. Please call the SEC at 1-800-SEC-0330 for further information on the public reference room. The Company’s SEC filings are also available to the public from the SEC’s internet site at http://www.sec.gov. Copies of these reports and other information can also be inspected at the offices of the New York Stock Exchange, Inc., 20 Broad Street, New York, New York 10005, U.S.A.

Our public internet site is http://www.lazard.com. and the investor relations SEC filings section of our public internet site is located at http://www.lazard.com/InvestorRelations/SEC-Filings.aspx. We will make available free of charge, on or through the investor relations section of our internet site, our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and any amendments to those reports filed or furnished pursuant to the Exchange Act as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC. Also posted on our website, and available in print upon request of any shareholder to the Investor Relations Department, are charters for Lazard Ltd’s Audit Committee, Compensation Committee and Nominating & Governance Committee. Copies of these charters and Lazard Ltd’s Corporate Governance Guidelines and Code of Business Conduct and Ethics governing our directors, officers and employees are also posted on our website in the “Corporate Governance” section.

| ITEM 1A. | RISK FACTORS |

You should carefully consider the following risks and all of the other information set forth in this Form 10-K, including our consolidated financial statements and related notes. The following risks comprise material risks of which we are aware. If any of the events or developments described below actually occurred, our business, financial condition or results of operations would likely suffer.

Risks Relating to the Financial Services Industry and Financial Markets

In 2007 through 2009, the U.S. and global capital markets and the economy generally experienced significant deterioration and volatility, which has had negative repercussions on the global economy, and any return to such deterioration and volatility could present challenges for our business.

Commencing in 2007 and continuing through 2009, certain adverse financial developments have impacted the U.S. and global capital markets. These developments included a general slowing of economic growth both in the U.S. and globally, substantial volatility in equity securities markets, and volatility and tightening of liquidity in credit markets. In addition, concerns over increasing unemployment levels, declining business and consumer confidence, volatile energy costs, geopolitical issues and a declining real estate market in the U.S. and elsewhere have contributed to increased volatility and diminished expectations for the economy and the markets going forward. Although the level of volatility in the equity securities markets and credit markets has declined, many of these concerns remain present. For example, investor concerns about the financial health of certain European countries caused market disruptions in 2010. If the 2007-2009 levels of market disruption and volatility return, or if current conditions materially worsen, our business may be adversely affected, which may have a material impact on our business and results of operations.

The full extent of the effects of governmental economic and regulatory involvement in the wake of disruption and volatility in global financial markets is uncertain.

As a result of market volatility and disruption in recent years, the U.S. and other governments have taken unprecedented steps to try to stabilize the financial system, including investing in financial institutions and taking certain regulatory actions. The full extent of the effects of these actions and legislative and regulatory initiatives (including the Dodd-Frank Act) effected in connection with, and as a result of, such extraordinary disruption and volatility is uncertain, both as to the financial capital markets and participants in general, and as to us in particular.

15

Table of Contents

The level of soundness of our clients and other financial institutions could adversely affect us.

We have exposure to many different industries, products and counterparties, and we routinely execute transactions with counterparties in the financial services industry, including brokers and dealers, commercial banks, investment banks, mutual and hedge funds, and other institutional clients. Many of these transactions expose us to credit risk in the event of default of our counterparty or client. In addition, our credit risk may be exacerbated when the collateral held by us cannot be fully realized or is liquidated at prices not sufficient to recover the full amount of the loan or derivative exposure due us.

Other Business Risks

Our ability to retain our managing directors and other key professional employees is critical to the success of our business, including maintaining compensation levels at an appropriate level of costs, and failure to do so may materially adversely affect our results of operations and financial position.

Our people are our most important resource. We must retain the services of our managing directors and other key professional employees, and strategically recruit and hire new talented employees, to obtain and successfully execute the advisory and asset management engagements that generate substantially all our revenue.

Lazard Group has experienced several significant events in recent years. In general, our industry continues to experience change and exerts competitive pressures for retaining top talent, which makes it more difficult for us to retain professionals. If any of our managing directors and other key professional employees were to join an existing competitor, form a competing company or otherwise leave us, some of our clients could choose to use the services of that competitor or some other competitor instead of our services. The employment arrangements, non-competition agreements and retention agreements we have or will enter into with our managing directors and other key professional employees may not prevent our managing directors and other key professional employees from resigning from practice or competing against us. In addition, these arrangements and agreements have a limited duration and will expire after a certain period of time. We continue to be subject to intense competition in the financial services industry regarding the recruitment and retention of key professionals, and have experienced departures from and added to our professional ranks as a result. Changes to our employee compensation arrangements, such as changes to the composition between cash and deferred compensation, may result in increased compensation and benefits expense in a particular year. Our compensation levels, results of operations and financial position may be significantly affected by many factors, including general economic and market conditions, our operating and financial performance, staffing levels and competitive pay conditions.

Difficult market conditions can adversely affect our business in many ways, including by reducing the volume of the transactions involving our Financial Advisory business and reducing the value or performance of the assets we manage in our Asset Management business, which, in each case, could materially reduce our revenue or income and adversely affect our financial position.

As a financial services firm, our businesses are materially affected by conditions in the global financial markets and economic conditions throughout the world. The financial environment in the U.S. and globally has been volatile during recent years. Unfavorable economic and market conditions can adversely affect our financial performance in both the Financial Advisory and Asset Management businesses.

For example, revenue generated by our Financial Advisory business is directly related to the volume and value of the transactions in which we are involved. During periods of unfavorable market or economic conditions, the volume and value of M&A transactions may decrease, thereby reducing the demand for our Financial Advisory services and increasing price competition among financial services companies seeking such engagements. Our results of operations would be adversely affected by any such reduction in the volume or value of M&A transactions. In addition, our profitability would be adversely affected due to our fixed costs and the possibility that we would be unable to scale back other costs within a timeframe sufficient to offset any decreases in revenue relating to changes in market and economic conditions. The future market and economic climate may deteriorate because of many factors, including possible increases in interest rates or inflation, terrorism or political uncertainty.

16

Table of Contents

Within our Financial Advisory business, we have typically seen that, during periods of economic strength and growth, our Mergers and Acquisitions practice historically has been more active and our Restructuring practice has been less active. Conversely, during periods of economic weakness and slowdown, we typically have seen that our Restructuring practice has been more active and our Mergers and Acquisitions practice has been less active. As a result, our revenue from our Restructuring practice has tended to correlate negatively to our revenue from our Mergers and Acquisitions practice over the course of business cycles. These trends are cyclical in nature and subject to periodic reversal. However, these trends do not cancel out the impact of economic conditions in our Financial Advisory business, which may be adversely affected by a downturn in economic conditions leading to decreased Mergers and Acquisitions practice activity, notwithstanding improvements in our Restructuring practice. Moreover, revenue improvements in our Mergers and Acquisitions practice in strong economic conditions could be offset in whole or in part by any related revenue declines in our Restructuring practice. While we generally have experienced a counter-cyclical relationship between our Mergers and Acquisitions practice and our Restructuring practice, this relationship may not continue in the future.

Our Asset Management business also would be expected to generate lower revenue in a market or general economic downturn. Under our Asset Management business’ arrangements, investment advisory fees we receive typically are based on the market value of AUM. Accordingly, a decline in the prices of securities, such as that which occurred on a global basis in 2008, or in specific geographic markets or sectors that constitute a significant portion of our AUM (i.e., our emerging markets strategies), would be expected to cause our revenue and income to decline by:

| • | causing the value of our AUM to decrease, which would result in lower investment advisory fees, |

| • | causing some of our clients to withdraw funds from our Asset Management business due to the uncertainty or volatility in the market, which would also result in lower investment advisory fees, |

| • | causing some of our clients or prospective clients to hesitate in allocating assets to our Asset Management business due to the uncertainty or volatility in the market, which would also result in lower investment advisory fees, |

| • | causing negative absolute performance returns for some accounts which have performance-based incentive fees, which would result in a reduction of revenue from such fees, or |

| • | causing some of our clients to withdraw funds from our Asset Management business in favor of investments they perceive as offering greater opportunity or lower risk, which also would result in lower investment advisory fees. |

If our Asset Management revenue declines without a commensurate reduction in our expenses, our net income would be reduced. In addition, in the event of a market downturn, our alternative investment and private equity practice also may be impacted by reduced exit opportunities in which to realize the value of its investments.

A majority of our revenue is derived from Financial Advisory fees, which are not long-term contracted sources of revenue and are subject to intense competition, and declines in our Financial Advisory engagements could have a material adverse effect on our financial condition and results of operations.

We historically have earned a substantial portion of our revenue from advisory fees paid to us by our Financial Advisory clients, which fees usually are payable upon the successful completion of a particular transaction or restructuring. For example, for the year ended December 31, 2010, Financial Advisory services accounted for approximately 59% of our consolidated net revenue. We expect that we will continue to rely on Financial Advisory fees for a substantial portion of our revenue for the foreseeable future, and a decline in our advisory engagements or the market for advisory services would adversely affect our business, financial condition and results of operations.

17

Table of Contents

In addition, we operate in a highly competitive environment where typically there are no long-term contracted sources of revenue. Each revenue-generating engagement typically is separately awarded and negotiated. Furthermore, many businesses do not routinely engage in transactions requiring our services and, as a consequence, our fee paying engagements with many clients are not likely to be predictable. We also lose clients each year as a result of the sale or merger of a client, a change in a client’s senior management, competition from other financial advisors and financial institutions, and other causes. As a result, our engagements with clients are constantly changing and our Financial Advisory fees could decline quickly due to the factors discussed above.

There will not be a consistent pattern in our financial results from period to period, which may make it difficult for us to achieve steady earnings growth on a quarterly basis.

We experience significant fluctuations in quarterly revenue and profits. These fluctuations generally can be attributed to the fact that we earn a significant portion of our Financial Advisory revenue upon the successful completion of a merger or acquisition transaction or a restructuring, the timing of which is uncertain and is not subject to our control. In addition, our Asset Management revenue is particularly sensitive to fluctuations in our AUM. Asset Management fees are often based on AUM as of the end of a quarter or month. As a result, a reduction in assets at the end of a quarter or month (as a result of market depreciation, withdrawals or otherwise) will result in a decrease in management fees. Similarly, timing of flows, contributions and withdrawals are often out of our control and may be inconsistent from quarter to quarter. As a result of quarterly fluctuations, it may be difficult for us to achieve steady earnings growth on a quarterly basis.

In many cases, we are paid for advisory engagements only upon the successful consummation of the underlying merger or acquisition transaction or restructuring. As a result, our Financial Advisory business is highly dependent on market conditions and the decisions and actions of our clients, interested third parties and governmental authorities. For example, a client could delay or terminate an acquisition transaction because of a failure to agree upon final terms with the counterparty, failure to obtain necessary regulatory consents or board of directors or stockholder approval, failure to secure necessary financing, adverse market conditions or because the target’s business is experiencing unexpected operating or financial problems. Anticipated bidders for assets of a client during a restructuring transaction may not materialize or our client may not be able to restructure its operations or indebtedness, for example, due to a failure to reach agreement with its principal creditors. In addition, a bankruptcy court may deny our right to collect a “success” or “completion” fee. In these circumstances, other than in engagements where we receive monthly retainers, we often do not receive any advisory fees other than the reimbursement of certain expenses despite the fact that we devote resources to these transactions. Accordingly, the failure of one or more transactions to close either as anticipated or at all could materially adversely affect our business, financial condition or results of operations. For more information, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

If the number of debt defaults, bankruptcies or other factors affecting demand for our Restructuring services declines, or we lose business to certain new entrants to the restructuring advisory practice who are no longer precluded from offering such services due to changes to the U.S. Bankruptcy Code, our Restructuring practice’s revenue could suffer.

We provide various restructuring and restructuring-related advice to companies in financial distress or to their creditors or other stakeholders. Historically, the fees from restructuring related services have been a significant part of our Financial Advisory revenue. A number of factors could affect demand for these advisory services, including improving general economic conditions, the availability and cost of debt and equity financing and changes to laws, rules and regulations, including deregulation or privatization of particular industries and those that protect creditors.

Section 327 of the U.S. Bankruptcy Code requires that “disinterested persons” be employed in a restructuring. The definition of “disinterested persons” has been modified. As previously in effect, certain of our competitors were disqualified from being employed in restructurings as a result of their status as an underwriter

18

Table of Contents

of securities. This basis for disqualification, however, no longer applies. Historically, we were not often disqualified from obtaining a role in a restructuring because we have not been a significant underwriter of securities. The change of the “disinterested persons” definition allows for more financial services firms to compete for restructuring engagements and make recruiting and retaining of professionals more difficult. If our competitors succeed in being retained in new restructuring engagements or in hiring our restructuring professionals, our Restructuring practice, and thereby our results of operations, could be materially adversely affected.

We could lose clients and suffer a decline in our Asset Management revenue and earnings if the investments we choose in our Asset Management business perform poorly or if we lose key employees, regardless of overall trends in the prices of securities.