Attached files

| file | filename |

|---|---|

| 8-K - ROCK-TENN COMPANY 8-K - Rock-Tenn CO | a6623079.htm |

Exhibit 99.1

Credit Suisse 2011 Global Paper & Packaging Conference February 23, 2011 Filed by Rock-Tenn Company Pursuant to Rule 425 under the Securities Act of 1933 and Deemed Filed under Rule 14a-12 of theSecurities Exchange Act of 1934 Subject Company: Rock-Tenn Company

2 Cautionary Statement Regarding Forward-Looking Information This document contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements are typically identified by words or phrases such as “may,” “will,” “anticipate,” “estimate,” “expect,” “project,” “intend,” “plan,” “believe,” “target,” “forecast,” and other words and terms of similar meaning. Forward-looking statements involve estimates, expectations, projections, goals, forecasts, assumptions, risks and uncertainties. RockTenn cautions readers that any forward-looking statement is not a guarantee of future performance and that actual results could differ materially from those contained in the forward-looking statement. Such forward-looking statements include, but are not limited to, statements regarding the anticipated closing date of the transaction, the successful closing of the transaction and the integration of Smurfit-Stone as well as opportunities for operational improvement including but not limited to cost reduction and capital investment, the strategic opportunity and perceived value to RockTenn and shareholders of the transaction, the opportunity to recognize benefits from Smurfit-Stone’s NOLs, the transaction’s impact on, among other things, RockTenn’s business mix, margins, transitional costs and integration to achieve the synergies and the timing of such costs and synergies and earnings. With respect to these statements, RockTenn and Smurfit-Stone have made assumptions regarding, among other things, whether and when the proposed transaction will be approved; whether and when the proposed transaction will close; the availability of financing on satisfactory terms; the amount of debt RockTenn will assume; the results and impacts of the acquisition; preliminary purchase price allocations which may include material adjustments to the preliminary fair values of the acquired assets and liabilities; economic, competitive and market conditions generally; volumes and price levels of purchases by customers; competitive conditions in RockTenn and Smurfit-Stone’s businesses and possible adverse actions of our respective customers, competitors and suppliers. Further, Rock-Tenn and Smurfit-Stone’s businesses are subject to a number of general risks that would affect any such forward-looking statements including, among others, decreases in demand for their products; increases in energy, raw materials, shipping and capital equipment costs; reduced supply of raw materials; fluctuations in selling prices and volumes; intense competition; the potential loss of certain customers; and adverse changes in general market and industry conditions. Such risks and other factors that may impact management’s assumptions are more particularly described in RockTenn and Smurfit-Stone’s filings with the Securities and Exchange Commission, including under the caption “Business – Forward-Looking Information” and “Risk Factors” in RockTenn’s Annual Report on Form 10-K for the most recently ended fiscal year and “Business – Risk Factors” and “Forward-Looking Information” in Smurfit-Stone’s Annual Report on Form 10-K for the most recently ended fiscal year. The information contained herein speaks as of the date hereof and neither RockTenn nor Smurfit-Stone have or undertake any obligation to update or revise its forward-looking statements, whether as a result of new information, future events or otherwise.

3 Additional Information Additional Information and Where to Find It In connection with the proposed acquisition by RockTenn of all of the outstanding common stock of Smurfit-Stone, RockTenn and Smurfit-Stone will be filing documents with the Securities and Exchange Commission (the “SEC”), including the filing by RockTenn of a registration statement on Form S-4 that will include a joint proxy statement of RockTenn and Smurfit-Stone that also constitutes a prospectus of RockTenn. RockTenn and Smurfit-Stone stockholders are urged to read the registration statement on Form S-4 and the related joint proxy statement/prospectus when they become available, as well as other documents filed with the SEC, because they will contain important information. The final joint proxy statement/prospectus will be mailed to stockholders of RockTenn and stockholders of Smurfit-Stone. Investors and security holders may obtain free copies of these documents (when they are available) and other documents filed with the SEC at the SEC’s web site at www.sec.gov, or by contacting RockTenn Investor Relations at (678) 291-7901 or Smurfit-Stone Investor Relations at (314) 656-5553 or Smurfit-Stone Media Relations at (314) 656-5827. Participants in the Merger Solicitation RockTenn, Smurfit-Stone and their respective directors, executive officers and other members of management and employees may be deemed to be participants in the solicitation of proxies in respect of the transaction. Information concerning RockTenn’s executive officers and directors is set forth in its definitive proxy statement filed with the SEC on December 17, 2010. Information concerning Smurfit-Stone’s executive officers and directors is set forth in its annual report on Form 10-K for the year ended December 31, 2010, which was filed with the SEC on February 15, 2011. Additional information regarding the interests of participants of RockTenn and Smurfit-Stone in the solicitation of proxies in respect of the transaction will be included in the above-referenced registration statement on Form S-4 and joint proxy statement/prospectus when it becomes available. You can obtain free copies of these documents from RockTenn and Smurfit-Stone using the contact information above.

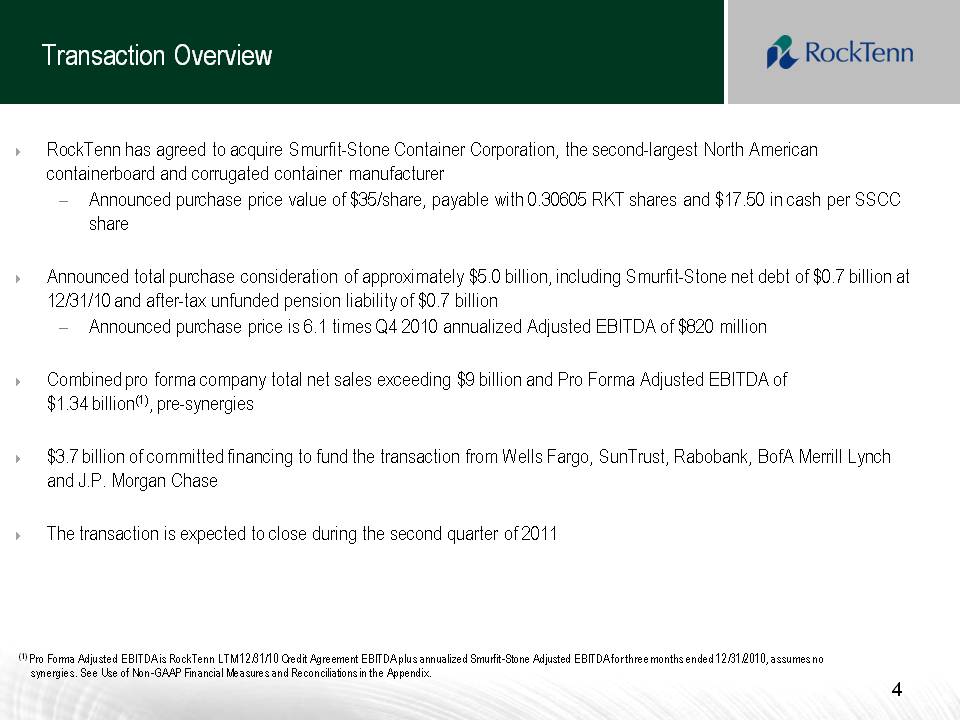

Transaction Overview 4 RockTenn has agreed to acquire Smurfit-Stone Container Corporation, the second-largest North American containerboard and corrugated container manufacturerAnnounced purchase price value of $35/share, payable with 0.30605 RKT shares and $17.50 in cash per SSCC share Announced total purchase consideration of approximately $5.0 billion, including Smurfit-Stone net debt of $0.7 billion at 12/31/10 and after-tax unfunded pension liability of $0.7 billion Announced purchase price is 6.1 times Q4 2010 annualized Adjusted EBITDA of $820 millionCombined pro forma company total net sales exceeding $9 billion and Pro Forma Adjusted EBITDA of $1.34 billion(1), pre-synergies$3.7 billion of committed financing to fund the transaction from Wells Fargo, SunTrust, Rabobank, BofA Merrill Lynch and J.P. Morgan ChaseThe transaction is expected to close during the second quarter of 2011 (1) Pro Forma Adjusted EBITDA is RockTenn LTM 12/31/10 Credit Agreement EBITDA plus annualized Smurfit-Stone Adjusted EBITDA for three months ended 12/31/2010, assumes no synergies. See Use of Non-GAAP Financial Measures and Reconciliations in the Appendix.

5 Acquisition Consistent with RockTenn’s Core Business Principles Providing superior paperboard, packaging and marketing solutions for consumer products companies at very low costs RockTenn’s expanded network of mills and converting plants are cost-competitive with numerous opportunities to further optimize the combined system RockTenn will be the most respected company in our business by: Investing for competitive advantage RockTenn’s and Smurfit-Stone’s assets are well-capitalized, with significant opportunities identified for further profit-improving investments Maximizing the efficiency of our manufacturing processes Acquisition significantly increases RockTenn’s opportunities for g y g p by optimizing economies of scale q g y pp optimizing scale Systematically improving processes and reducing costs throughout the Company Acquisition combines RockTenn’s Six Sigma continuous improvement method with Smurfit-Stone’s Lean Manufacturing method to further optimize manufacturing and administrative processes Seeking acquisitions that can dramatically improve the business RockTenn views Smurfit-Stone’s virgin containerboard mill system as a key strategic asset giving the acquisition a compelling strategic rationale

6 Compelling Strategic Acquisition Containerboard has become a very good business US virgin containerboard is a highly strategic global asset Smurfit-Stone’s assets are much lower cost than before their transformation Ample opportunities to improve cost position through continued transformation of box plant system and investments in mills Estimated annual transaction synergies run rate of $150 million within 24 months after transaction close RockTenn’s customer-focused value approach to the market, disciplined execution and record of continuous operational and administrative excellence provide broad runway for 6 operational gains

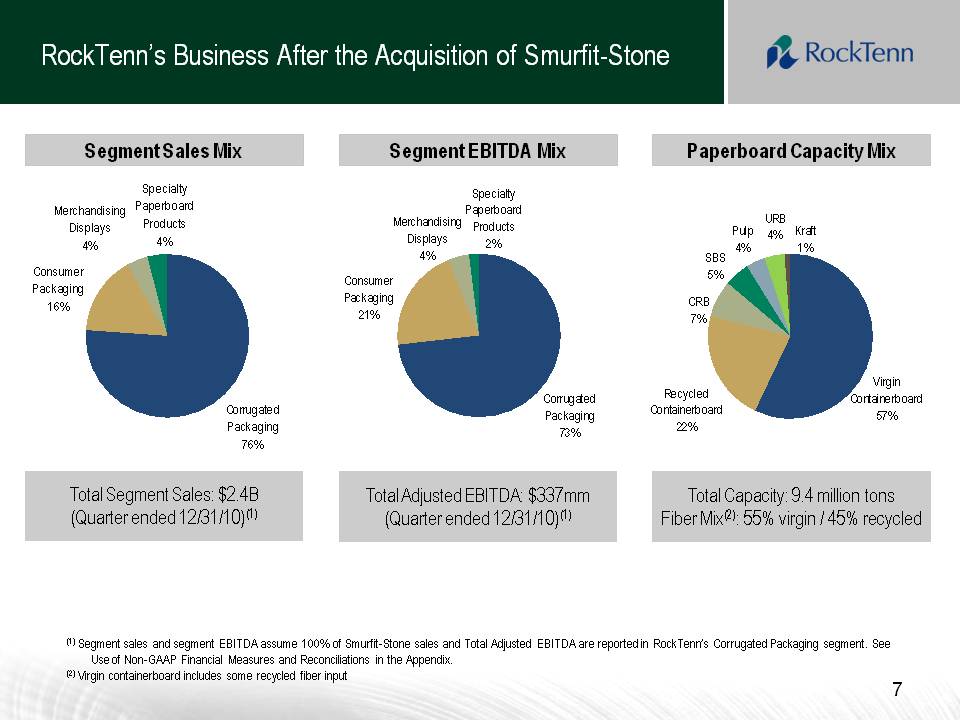

7 RockTenn’s Business After the Acquisition of Smurfit-Stone Segment Sales Mix Segment EBITDA Mix Paperboard Capacity Mix Specialty P b d Specialty Paperboard M h di i Consumer Packaging Merchandising Displays 4% Paperboard Products 2% Products 4% Merchandising Displays 4% Consumer Packaging 16% Pulp 4% URB 4% Kraft 1% SBS 5% CRB Corrugated P k i 21% Corrugated Virgin Containerboard 57% 7% Recycled Containerboard Total Adjusted EBITDA: $337mm (Q t d d 31/10)(1) Total Capacity: 9.4 million tons Fib Mi (2) 55% i i / 45% l d Total Segment Sales: $2.4B (Q t d d 31/10)(1) Packaging 73% Packaging 76% 22% Quarter ended 12/Fiber Mix(2): virgin recycled Quarter ended 12/7 (1) Segment sales and segment EBITDA assume 100% of Smurfit-Stone sales and Total Adjusted EBITDA are reported in RockTenn’s Corrugated Packaging segment. See Use of Non-GAAP Financial Measures and Reconciliations in the Appendix. (2) Virgin containerboard includes some recycled fiber input Management’s

8 Extensive operational and industry experience Demonstrated willingness to reduce debt – Opening leverage of 2.8x; Company plans to de-lever to 2.0x by December 2012 Proven track record of successfully integrating acquisitions Proven ability to meet or exceed stated financial objectives Committed to achieving and maintaining investment grade credit profile

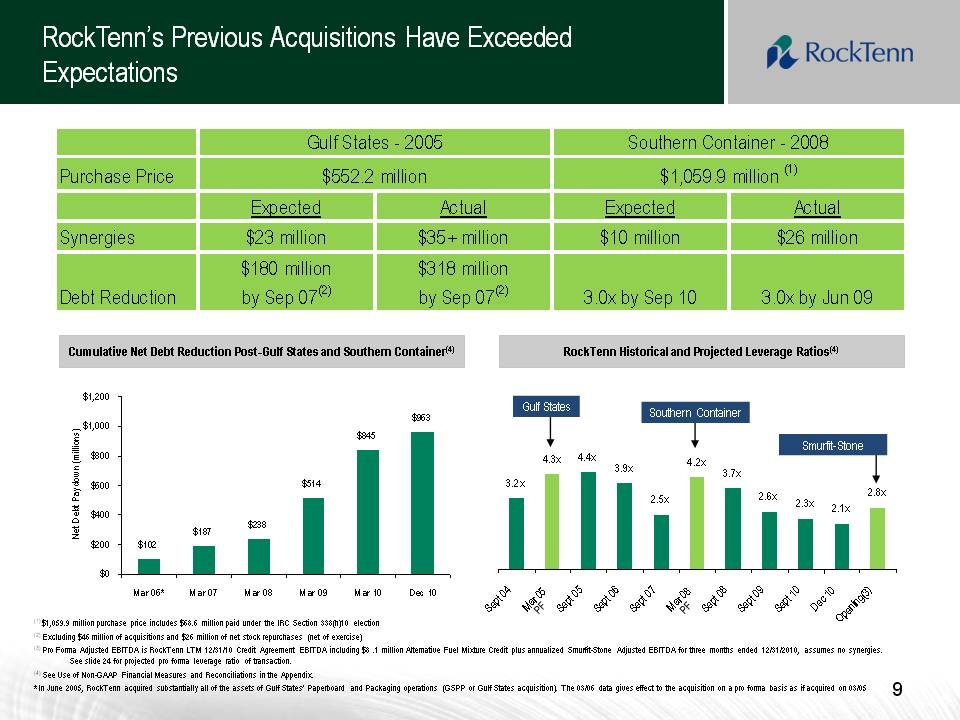

9 RockTenn’s Previous Acquisitions Have Exceeded Expectations Gulf States - 2005 Southern Container - 2008 Purchase Price $552.2 million $1,059.9 million (1) Expected Actual Expected Actual Synergies $23 million $35+ million $10 million $26 million Debt Reduction $180 million by Sep 07(2) $318 million by Sep 07(2) 3.0x by Sep 10 3.0x by Jun 09 RockTenn Historical and Projected Leverage Ratios(4) Cumulative Net Debt Reduction Post-Gulf States and Southern Container(4) Gulf States Southern Container $1,200 y y y y 3.2x 4.3x 4.4x 3.9x 2.5x 4.2x 3.7x 2.6x 2.3x 2.1x 2.8x Smurfit-Stone $514 $845 $963 $400 $600 $800 $1,000 ebt Paydown (millions) Sept 04 Mar 05 Sept 05 Sept 06 Sept 07 Mar 08 Sept 08 Sept 09 Sept 10 Dec 10 Opening(3) $102 $187 $238 $0 $200 Mar 06* Mar 07 Mar 08 Mar 09 Mar 10 Dec 10 Net De 9 (1) $1,059.9 million purchase price includes $68.6 million paid under the IRC Section 338(h)10 election (2) Excluding $46 million of acquisitions and $26 million of net stock repurchases (net of exercise) (3) Pro Forma Adjusted EBITDA is RockTenn LTM 12/31/10 Credit Agreement EBITDA including $8 .1 million Alternative Fuel Mixture Credit plus annualized Smurfit-Stone Adjusted EBITDA for three months ended 12/31/2010, assumes no synergies. See slide 24 for projected pro forma leverage ratio of transaction. (4) See Use of Non-GAAP Financial Measures and Reconciliations in the Appendix. * In June 2005, RockTenn acquired substantially all of the assets of Gulf States’ Paperboard and Packaging operations (GSPP or Gulf States acquisition). The 03/06 data gives effect to the acquisition on a pro forma basis as if acquired on 03/05

10 Combined RockTenn and Smurfit-Stone #2 producer of containerboard in North America – – #2 producer of coated recycled board in North America – Management team with strong record of shareholder value creation and excellent g g record of integrating acquisitions – The mix of fiber inputs is 55% virgin fiber and 45% recycled fiber – Expands geographic footprint to the Midwest and West Coast – Conservative capital structure with significant liquidity at close – Opportunity to improve results through cost reduction and capital investment We believe the acquisition of Smurfit-Stone represents a significant opportunity to continue our track record of creating shareholder value

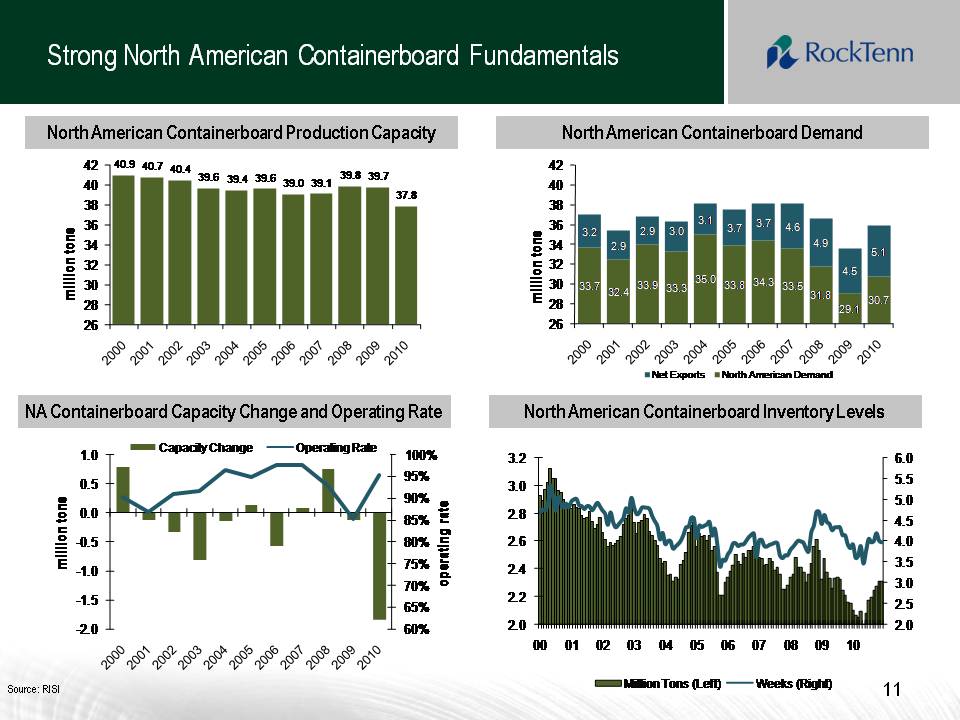

11 Strong North American Containerboard Fundamentals North American Containerboard Demand North American Containerboard Production Capacity 40.9 40.7 40.4 39.6 39.4 39.6 39.0 39.1 39.8 39.7 37.8 38 40 42 38 40 42 28 30 32 34 36 million tons 33.7 32.4 33.9 33.3 35.0 33.8 34.3 33.5 31.8 29 1 30.7 3.2 2.9 2.9 3.0 3.1 3.7 3.7 4.6 4.9 4.5 5.1 28 30 32 34 36 million tons North American Containerboard Inventory Levels NA Containerboard Capacity Change and Operating Rate 26 29.1 26 Net Exports North American Demand 90% 95% 100% 0 0 0.5 1.0 ate ons Capacity Change Operating Rate 5.0 5.5 6.0 2 8 3.0 3.2 65% 70% 75% 80% 85% -1.5 -1.0 -0.5 0.0 operating ra million to 2.5 3.0 3.5 4.0 4.5 2.2 2.4 2.6 2.8 11 Source: RISI 60% -2.0 2.0 2.0 00 01 02 03 04 05 06 07 08 09 10 Million Tons (Left) Weeks (Right) 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010

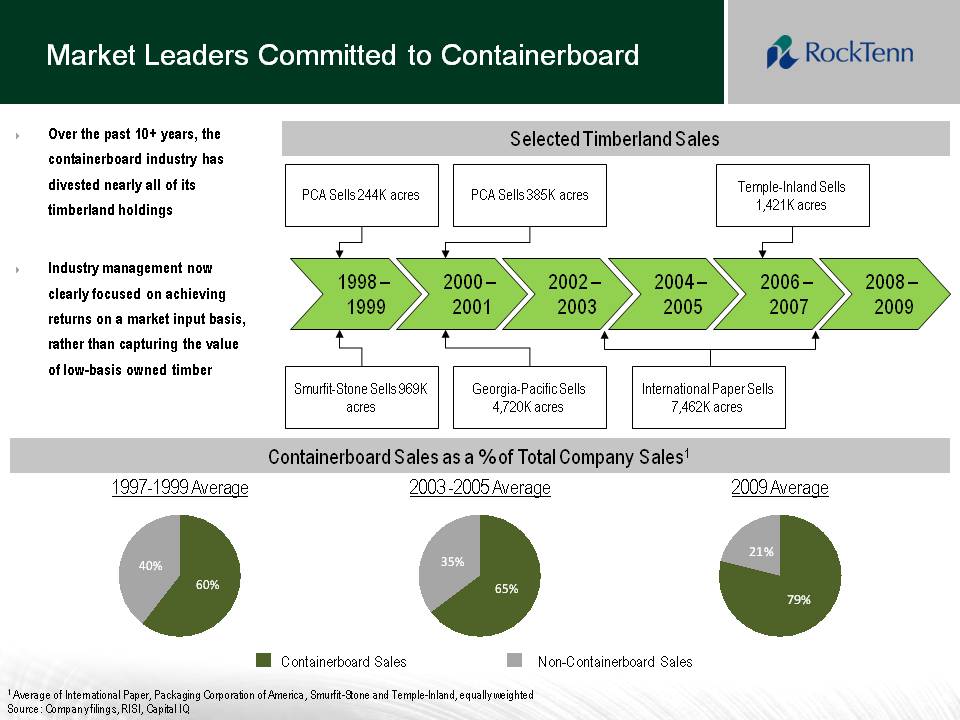

12 Market Leaders Committed to Containerboard PCA Sells 385K acres PCA Sells 244K acres Temple-Inland Sells 1 421K Selected Timberland Sales Over the past 10+ years, the containerboard industry has divested nearly all of its ti b l d h ldi 2000 – 2001 2002 – 2003 2004 – 2005 2006 – 2007 2008 – 2009 1998 – 1999 1,421K acres timberland holdings Industry management now clearly focused on achieving Smurfit-Stone Sells 969K acres International Paper Sells 7,462K acres Georgia-Pacific Sells 4,720K acres returns on a market input basis, rather than capturing the value of low-basis owned timber Containerboard Sales as a % of Total Company Sales1 1997-1999 Average 2003 -2005 Average 2009 Average 79% 21% 60% 40% 65% 35% 1 Average of International Paper, Packaging Corporation of America, Smurfit-Stone and Temple-Inland, equally weighted Source: Company filings, RISI, Capital IQ Containerboard Sales Non-Containerboard Sales

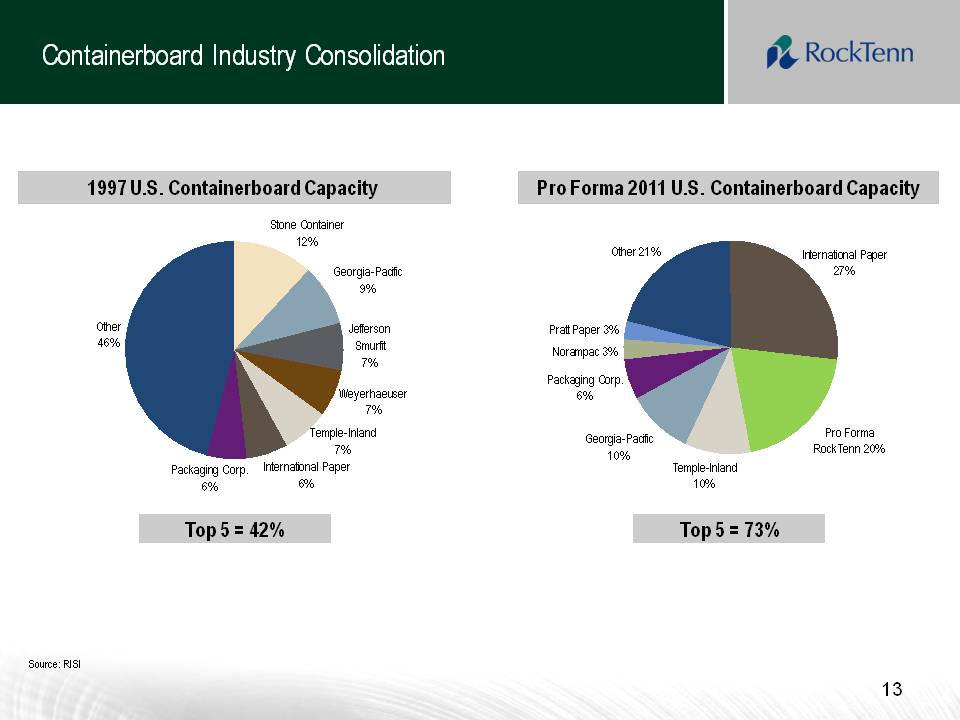

13 Containerboard Industry Consolidation 1997 U.S. Containerboard Capacity Pro Forma 2011 U.S. Containerboard Capacity Other 21% International Paper 27% Georgia-Pacific 9% Stone Container 12% Packaging Corp. 6% Norampac 3% Pratt Paper 3% Other 46% Weyerhaeuser 7% Jefferson Smurfit 7% Temple-Inland 10% Georgia-Pacific 10% Pro Forma RockTenn 20% International Paper 6% Packaging Corp. 6% Temple-Inland 7% Top 5 = 42% Top 5 = 73% 13 Source: RISI

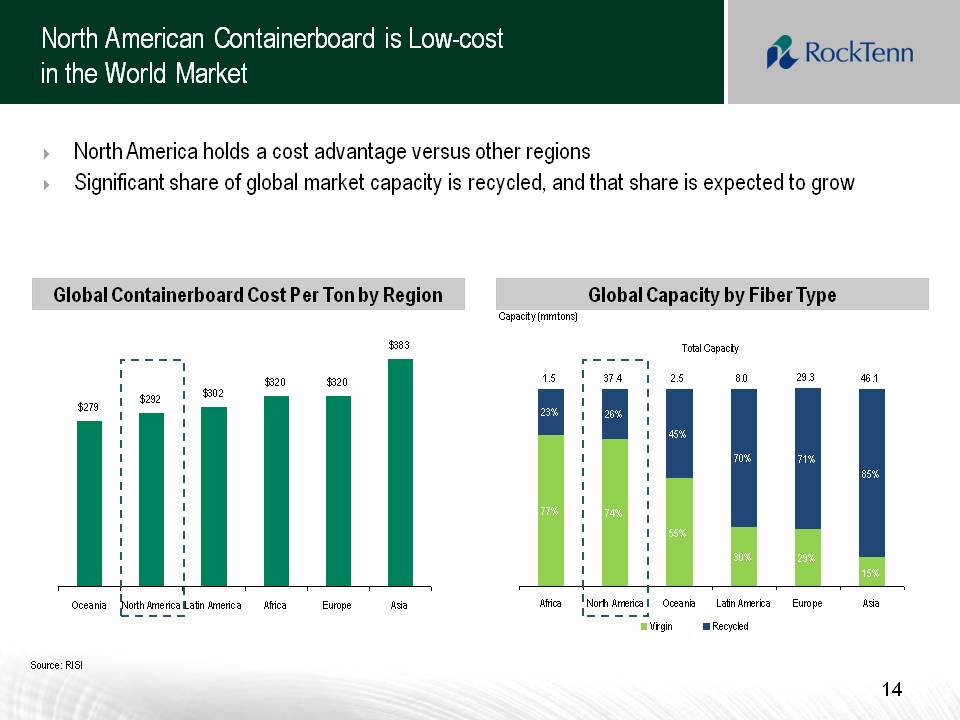

North American Containerboard is Low-cost in the World Market North America holds a cost advantage versus other regions Significant share of global market capacity is recycled, and that share is expected to grow Global Capacity by Fiber Type Global Containerboard Cost Per Ton by Region 23% 26% 1.5 37.4 2.5 8.0 29.3 46.1 Total Capacity $279 $292 $302 $320 $320 $383 Capacity (mm tons) 77% 74% 45% 70% 71% 85% % 55% 30% 29% 15% Africa North America Oceania Latin America Europe Asia Oceania North America Latin America Africa Europe Asia Virgin Recycled 14 Source: RISI

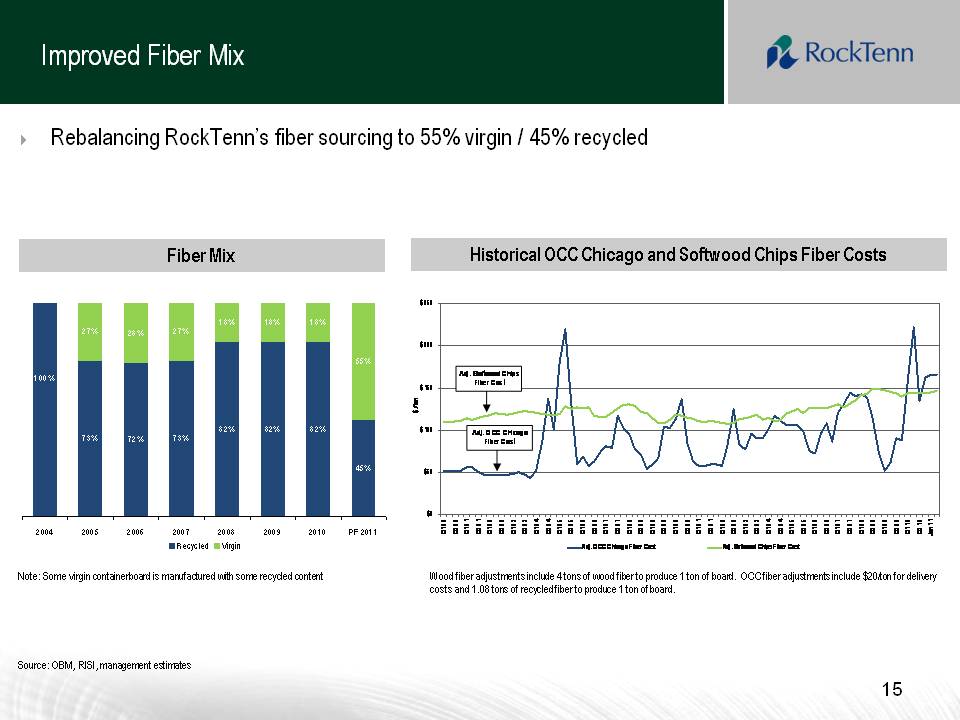

Improved Fiber Mix Rebalancing RockTenn’s fiber sourcing to 55% virgin / 45% recycled Fiber Mix $250 Historical OCC Chicago and Softwood Chips Fiber Costs 27% 28% 27% 18% 18% 18% 55% 100% $150 $200 $ / ton Adj. Softwood Chips Fiber Cost 73% 72% 73% 82% 82% 82% 45% $0 $50 $100 Adj. OCC Chicago Fiber Cost Note: Some virgin containerboard is manufactured with some recycled content Wood fiber adjustments include 4 tons of wood fiber to produce 1 ton of board. OCC fiber adjustments include $20/ton for delivery costs and 1.08 tons of recycled fiber to produce 1 ton of board. 2004 2005 2006 2007 2008 2009 2010 PF 2011 Recycled Virgin Q1 90 Q3 90 Q1 91 Q3 91 Q1 92 Q3 92 Q1 93 Q3 93 Q1 94 Q3 94 Q1 95 Q3 95 Q1 96 Q3 96 Q1 97 Q3 97 Q1 98 Q3 98 Q1 99 Q3 99 Q1 00 Q3 00 Q1 01 Q3 01 Q1 02 Q3 02 Q1 03 Q3 03 Q1 04 Q3 04 Q1 05 Q3 05 Q1 06 Q3 06 Q1 07 Q3 07 Q1 08 Q3 08 Q1 09 Q3 09 Q1 10 Q3 10 Jan 11 Adj. OCC Chicago Fiber Cost Adj. Softwood Chips Fiber Cost 15 Source: OBM, RISI, management estimates

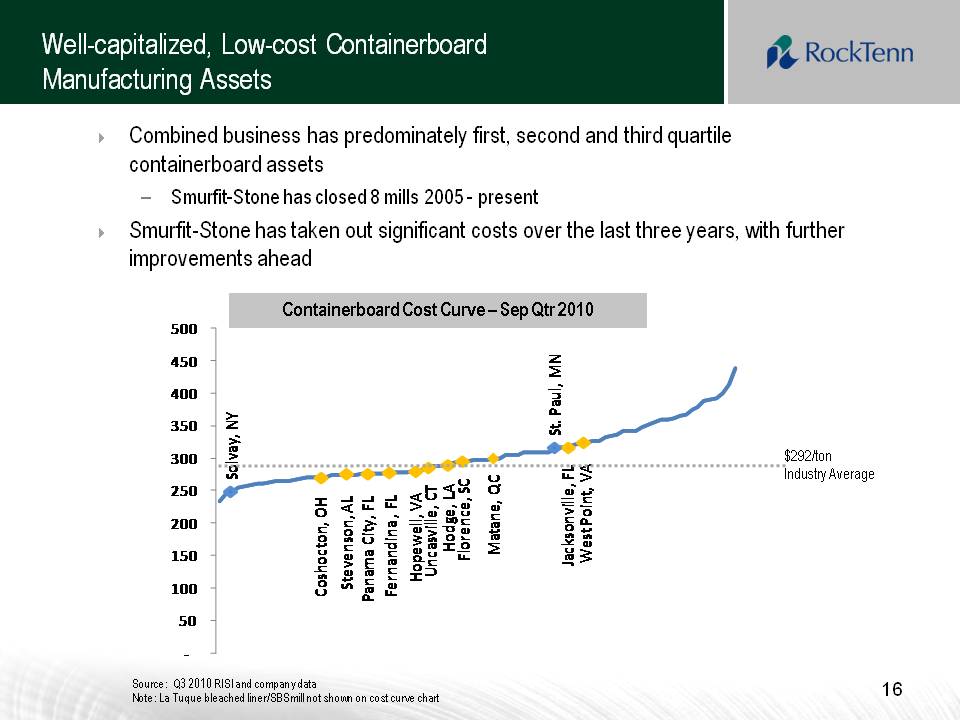

Well-capitalized, Low-cost Containerboard Manufacturing Assets Combined business has predominately first, second and third quartile containerboard assets – Smurfit-Stone has closed 8 mills 2005 - present Smurfit-Stone has taken out significant costs over the last three years, with further improvements ahead Containerboard Cost Curve Sep Qtr 2010 400 450 500 St. Paul, MN – 250 300 350 Hopewell, VA Florence, SC Fernandina, FL Stevenson, AL Coshocton, OH Panama City, FL Solvay, NY Uncasvile, CT Hodge, LA $ 292/ton Industry Average 0 100 150 200 Jacksonville, FL West Point, VA Matane, QC ‐ 50 16 Source: Q3 2010 RISI and company data Note: La Tuque bleached liner/SBS mill not shown on cost curve chart

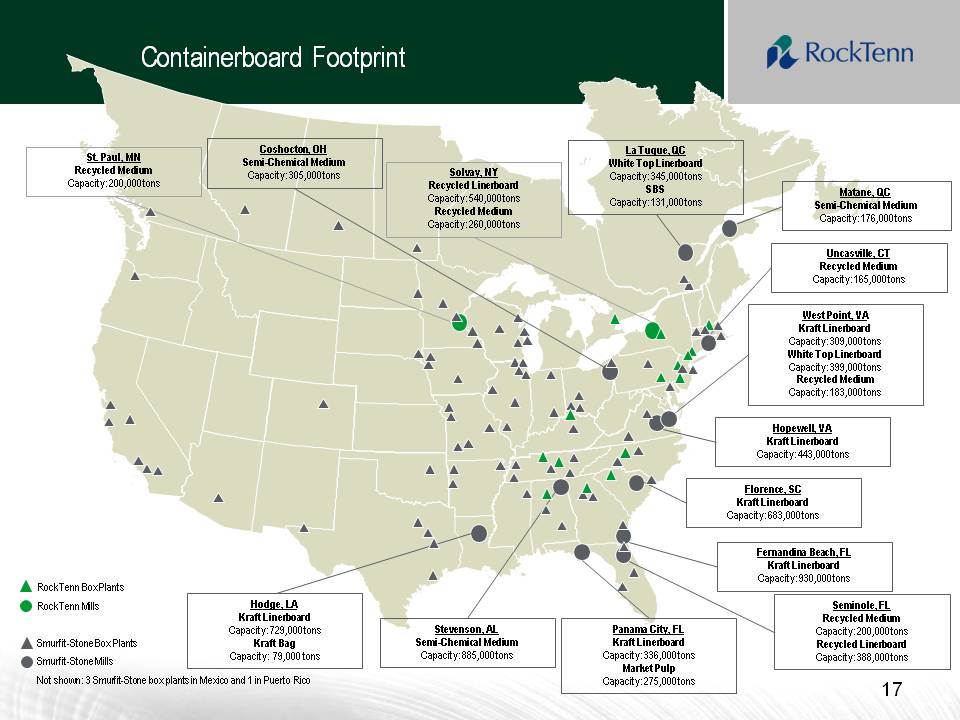

Containerboard Footprint Coshocton, OH Semi-Chemical Medium Capacity: 305,000 tons Solvay, NY Recycled Linerboard Capacity: 540,000 tons St. Paul, MN Recycled Medium Capacity: 200,000 tons Matane, QC Semi Chemical Medium La Tuque, QC White Top Linerboard Capacity: 345,000 tons SBS Capacity: 131,000 tons Uncasville, CT Recycled Medium Capacity: 165,000 tons Recycled Medium Capacity: 260,000 tons Semi-Capacity: 176,000 tons West Point, VA Kraft Linerboard Capacity: 309,000 tons White Top Linerboard Capacity: 399,000 tons Recycled Medium Capacity: 183,000 tons Florence, SC Kraft Linerboard Capacity: 683 000 Hopewell, VA Kraft Linerboard Capacity: 443,000 tons RockTenn Box Plants RockTenn Mills Hodge, LA Kraft Linerboard Seminole, FL Recycled Medium Fernandina Beach, FL Kraft Linerboard Capacity: 930,000 tons 683,000 tons 17 Smurfit-Stone Box Plants Smurfit-Stone Mills Not shown: 3 Smurfit-Stone box plants in Mexico and 1 in Puerto Rico Capacity: 729,000 tons Kraft Bag Capacity: 79,000 tons Capacity: 200,000 tons Recycled Linerboard Capacity: 388,000 tons Stevenson, AL Semi-Chemical Medium Capacity: 885,000 tons Panama City, FL Kraft Linerboard Capacity: 336,000 tons Market Pulp Capacity: 275,000 tons

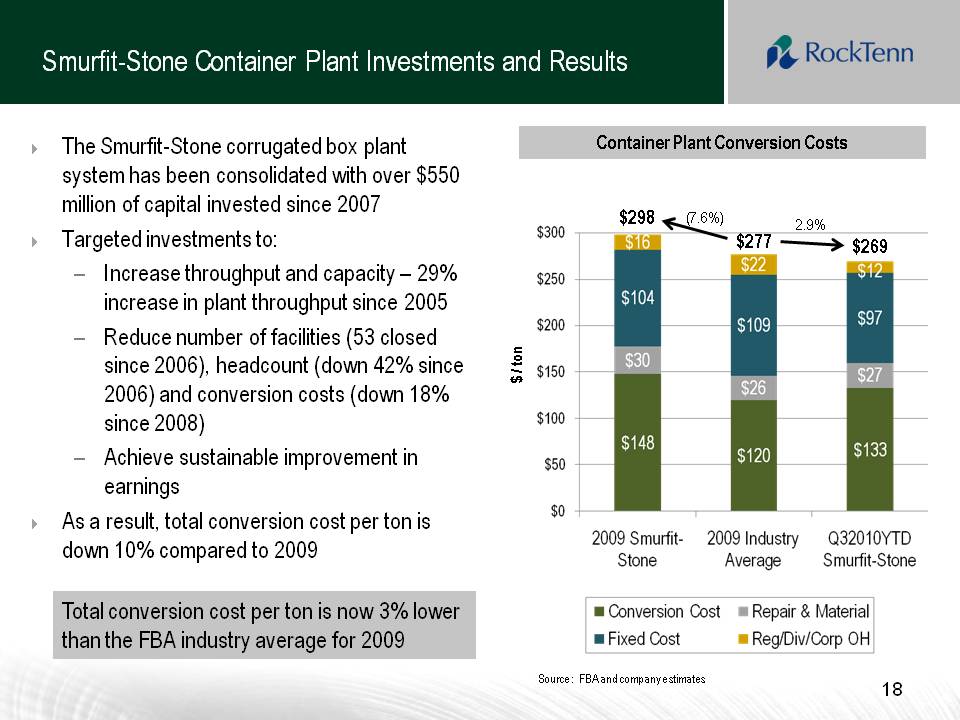

Smurfit-Stone Container Plant Investments and Results �� The Smurfit-Stone corrugated box plant system has been consolidated with over $550 million of capital invested since 2007 Container Plant Conversion Costs Targeted investments to: – Increase throughput and capacity – 29% $277 $298 $269 (7.6%) 2.9% increase in plant throughput since 2005 – Reduce number of facilities (53 closed since 2006), headcount (down 42% since 2006) and conversion costs (down 18% $ / ton since 2008) – Achieve sustainable improvement in earnings A As a result, total conversion cost per ton is down 10% compared to 2009 Total conversion cost per ton is now 3% lower 18 Source: FBA and company estimates than the FBA industry average for 2009 $16 $104 $30 $148 $120 $26 $109 $22 $ 277 $12 $97 $27 $133 $300 $ 250 $200 $150 $100 $50 $0 Conversion Cost Fixed Cost Repair & Material Reg/Div/Corp OH 2009 Smurfit-Stone 2009 Industry Average Q32010YTD Smurfit-Stone

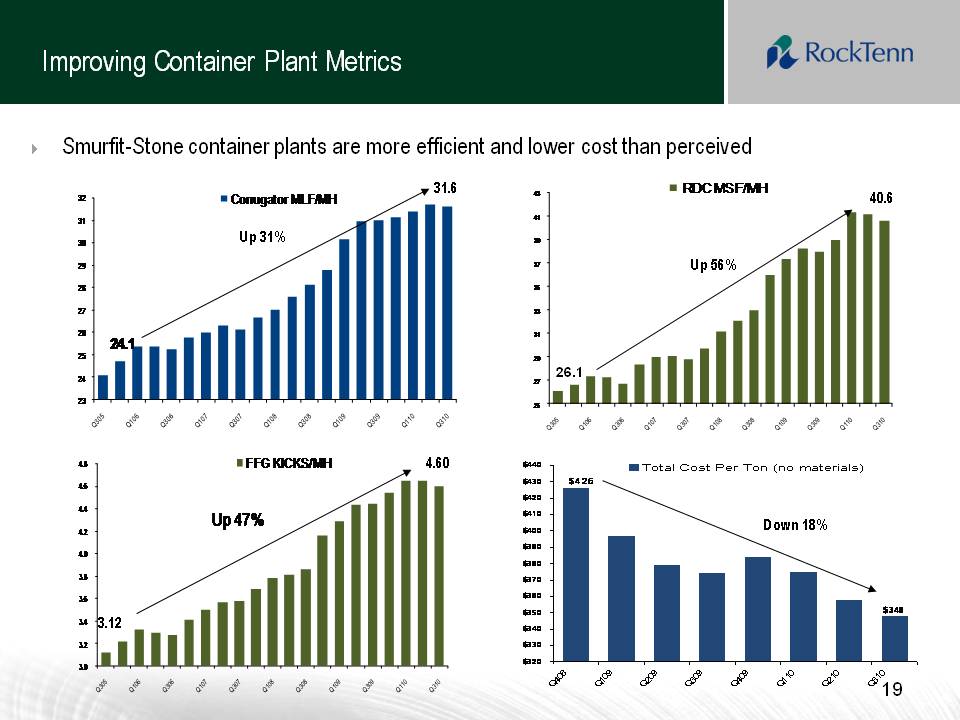

19 Improving Container Plant Metrics 32 Corrugator MLF/MH 43 RDC MSF/MH 31.6 40.6 Smurfit-Stone container plants are more efficient and lower cost than perceived 28 29 30 31 g 35 37 39 41 Up 56% Up 31% 23 24 25 26 27 24.1 25 27 29 31 33 26.1 $426 $410 $420 $430 $440 Total Cost Per Ton (no materials) 4.4 4.6 4.8 FFG KICKS/MH U 4.60 $348 $350 $360 $370 $380 $390 $400 3.6 3.8 4.0 4.2 Up 47% Down 18% $320 $330 $340 Q408 Q109 Q209 Q309 Q409 Q110 Q210 Q31019 Q305 Q106 Q306 Q107 Q307 Q108 Q308 Q109 Q309 Q110 Q310

20 Smurfit-Stone’s corrugated assets will be combined with RockTenn’s corrugated assets under the leadership of Jim Porter with a five-pronged integration strategy:Opportunities to invest capital in the mill system and optimize the footprint to reduce cost and maximize production efficiencyComplete the box plant consolidation and optimization strategy initiated by SSCC managementApply the RockTenn business model to the box plant system, driving product innovation, customer satisfaction and low-cost manufacturing while maximizing sales revenueConsolidate the divisional entity into one RockTenn headquarters located in Norcross, GABuild a single cultural model which inspires a high-performing corrugated business and creates the most respected company in the industryAdministrative integration to be led by Steve Voorhees, who led the successful Gulf States and Southern Container integrations Integration Strategy

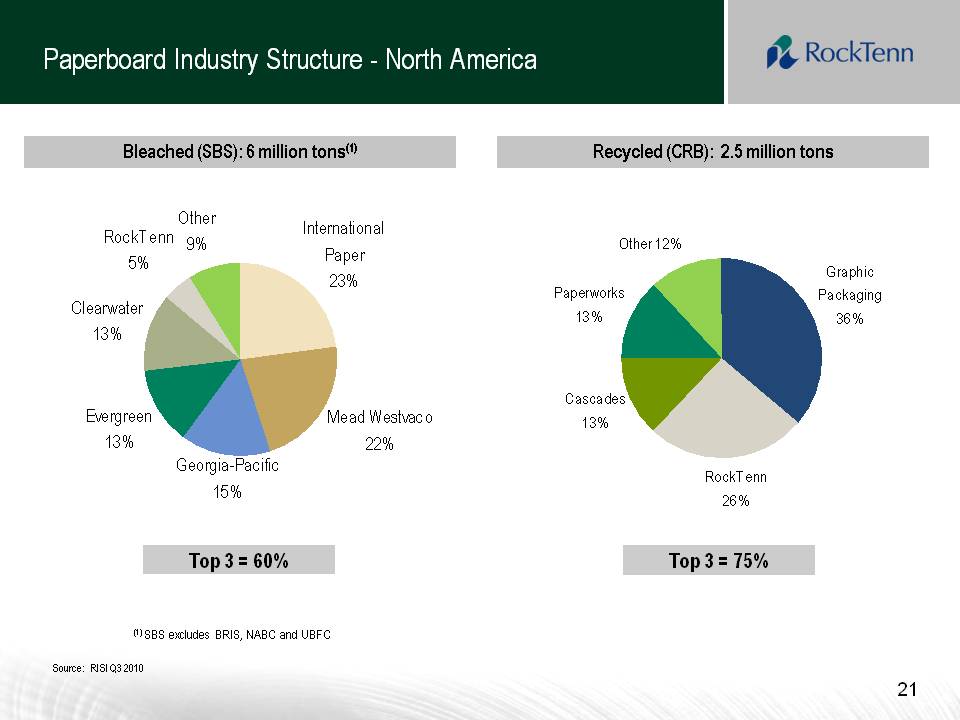

Paperboard Industry Structure - North America Bleached (SBS): 6 million tons(1) Recycled (CRB): 2.5 million tons Other 9% Clearwater RockTenn 5% International Paper 23% Graphic Packaging Paperworks Other 12% 13% M d W t E 36% Cascades 13% Mead Westvaco 22% Georgia-Pacific 15% Evergreen 13% RockTenn 26% 13% Top 3 = 60% Top 3 = 75% 21 Source: RISI Q3 2010 (1) SBS excludes BRIS, NABC and UBFC

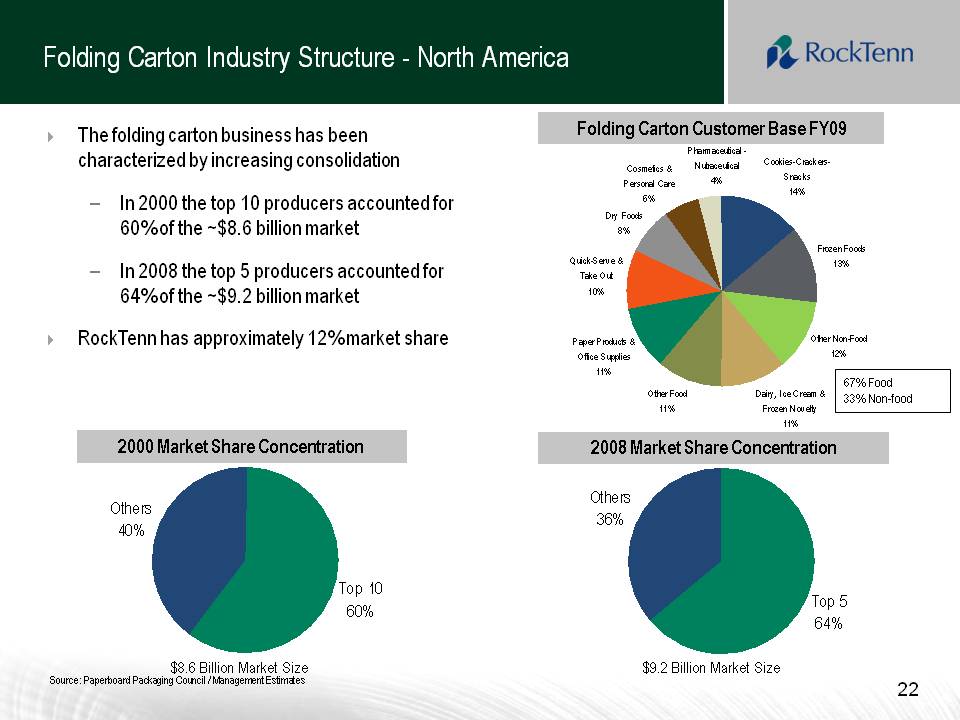

Folding Carton Industry Structure - North America Folding Carton Customer Base FY09 �� The folding carton business has been characterized by increasing consolidation – In 2000 the top 10 producers accounted for Cookies-Crackers- Snacks 14% Cosmetics & Personal Care 6% Pharmaceutical - Nutraceutical 4% 60% of the ~$8.6 billion market – In 2008 the top 5 producers accounted for 64% of the ~$9.2 billion market Dry Foods 8% Quick-Serve & Take Out 10% Frozen Foods 13% 67% Food 33% Non-food �� RockTenn has approximately 12% market share Paper Products & Office Supplies 11% Other Food 11% Dairy, Ice Cream & Frozen Novelty Other Non-Food 12% Others 2000 Market Share Concentration 2008 Market Share Concentration 11% Others 36% 40% Top 10 60% Top 5 % 22 Source: Paperboard Packaging Council / Management Estimates $8.6 Billion Market Size $9.2 Billion Market Size 64%

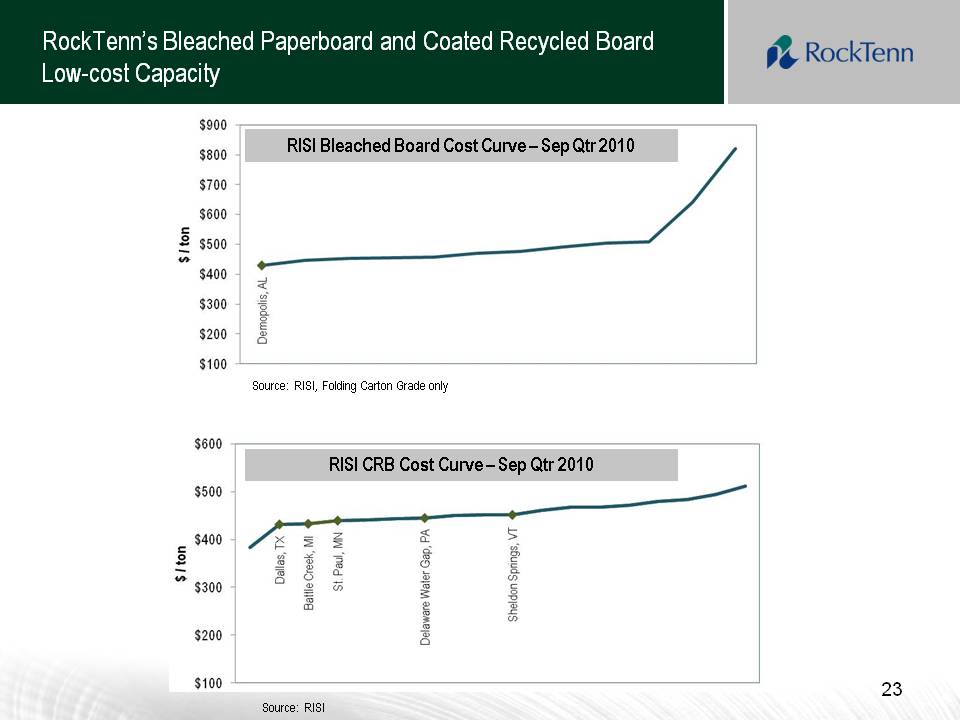

23 RockTenn’s Bleached Paperboard and Coated Recycled Board Low-cost Capacity RISI Bleached Board Cost Curve – Sep Qtr 2010 Source: RISI, Folding Carton Grade only RISI CRB Cost Curve – Sep Qtr 2010 23 Source: RISI $900 $800 $700 $600 $500 $400 $300 $200 $100 $600 $500 $400 $300 $200 $100 $/ton Demopolis, AL Dallas, TX Battle Creek, MI St. Paul, MN Delaware Water Gap, PA Sheldon Springs

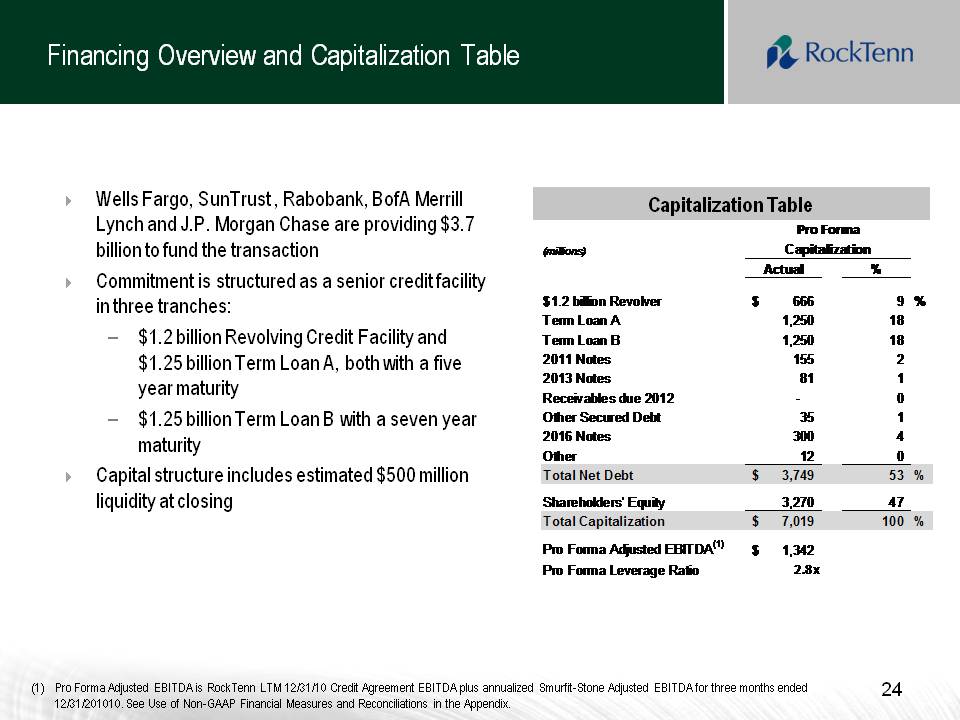

Financing Overview and Capitalization Table Wells Fargo, SunTrust , Rabobank, BofA Merrill Capitalization Table Lynch and J.P. Morgan Chase are providing $3.7 billion to fund the transaction Commitment is structured as a senior credit facility in three tranches: (millions) Actual % $1.2 billion Revolver 666 $ 9 % Capitalization Pro Forma – $1.2 billion Revolving Credit Facility and $1.25 billion Term Loan A, both with a five year maturity $1 25 billi T L B ith Term Loan A 1,250 18 Term Loan B 1,250 18 2011 Notes 155 2 2013 Notes 81 1 Receivables due 2012 - 0 – 1.25 billion Term Loan with a seven year maturity Capital structure includes estimated $500 million liquidity at closing Other Secured Debt 35 1 2016 Notes 300 4 Other 12 0 Total Net Debt 3,749 $ 53 % Shareholders' Equity 3,270 47 Total Capitalization 7,019 $ 100 % Pro Forma Adjusted EBITDA(1) 1,342 $ Pro Forma Leverage Ratio 2.8x 24 (1) Pro Forma Adjusted EBITDA is RockTenn LTM 12/31/10 Credit Agreement EBITDA plus annualized Smurfit-Stone Adjusted EBITDA for three months ended 12/31/201010. See Use of Non-GAAP Financial Measures and Reconciliations in the Appendix.

Conclusion Combined RockTenn and Smurfit-Stone#2 producer of containerboard in North America #2 producer of coated recycled board in North AmericaManagement team with strong record of shareholder value creation and excellent record of integrating acquisitionsThe mix of fiber inputs is 55% virgin fiber and 45% recycled fiberExpands geographic footprint to the Midwest and West CoastConservative capital structure with significant liquidity at closeOpportunity to improve results through cost reduction and capital investment 25 We believe the acquisition of Smurfit-Stone represents a significant opportunity to continue our track record of creating shareholder value

Acquisition Consistent with RockTenn’s Core Business Principles Providing superior paperboard, packaging and marketing solutions for consumer products companies at very low costs RockTenn’s expanded network of mills and converting plants are cost-competitive with numerous opportunities to further optimize the combined system RockTenn will be the most respected company in our business by: Investing for competitive advantage RockTenn’s and Smurfit-Stone’s assets are well-capitalized, with significant opportunities identified for further profit-improving investments Maximizing the efficiency of our manufacturing processes Acquisition significantly increases RockTenn’s opportunities for by optimizing economies of scale optimizing scale Systematically improving processes and reducing costs throughout the Company Acquisition combines RockTenn’s Six Sigma continuous improvement method with Smurfit-Stone’s Lean Manufacturing method to further optimize manufacturing and administrative processes Seeking acquisitions that can dramatically improve the business RockTenn views Smurfit-Stone’s virgin containerboard mill system as a key strategic asset giving the acquisition a compelling strategic rationale 26

27 Appendix

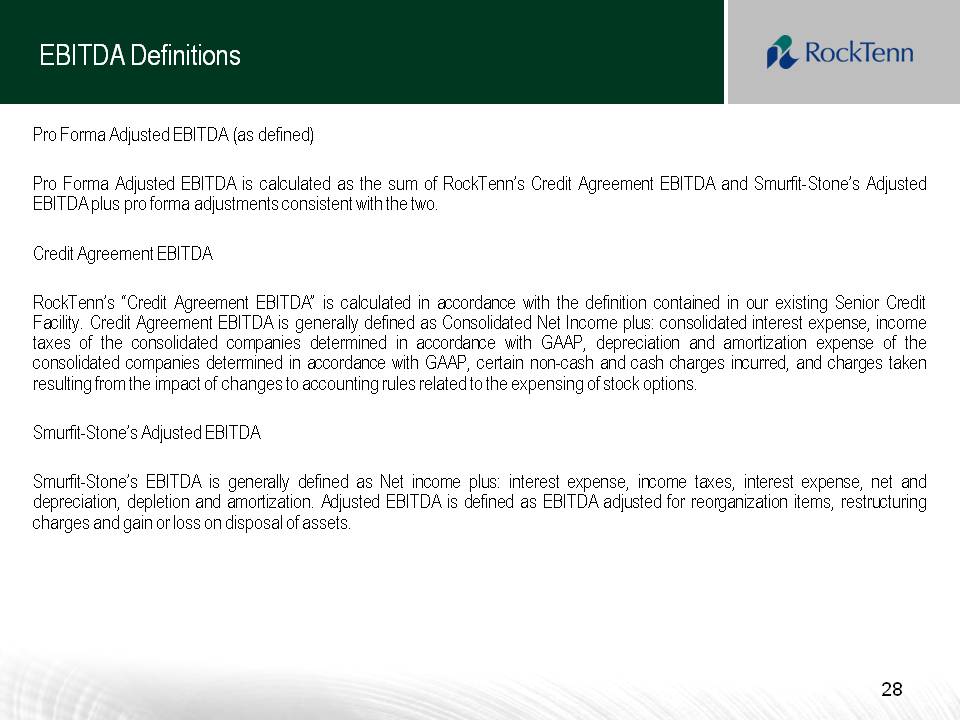

28 EBITDA Definitions Pro Forma Adjusted EBITDA (as defined) Pro Forma Adjusted EBITDA is calculated as the sum of RockTenn’s Credit Agreement EBITDA and Smurfit-Stone’s Adjusted EBITDA plus pro forma adjustments consistent with the two.Credit Agreement EBITDA RockTenn’s “Credit Agreement EBITDA” is calculated in accordance with the definition contained in our existing Senior Credit Facility. Credit Agreement EBITDA is generally defined as Consolidated Net Income plus: consolidated interest expense, income taxes of the consolidated companies determined in accordance with GAAP, depreciation and amortization expense of the consolidated companies determined in accordance with GAAP, certain non-cash and cash charges incurred, and charges taken resulting from the impact of changes to accounting rules related to the expensing of stock options. Smurfit-Stone’s Adjusted EBITDASmurfit-Stone’s EBITDA is generally defined as Net income plus: interest expense, income taxes, interest expense, net and depreciation, depletion and amortization. Adjusted EBITDA is defined as EBITDA adjusted for reorganization items, restructuring charges and gain or loss on disposal of assets.

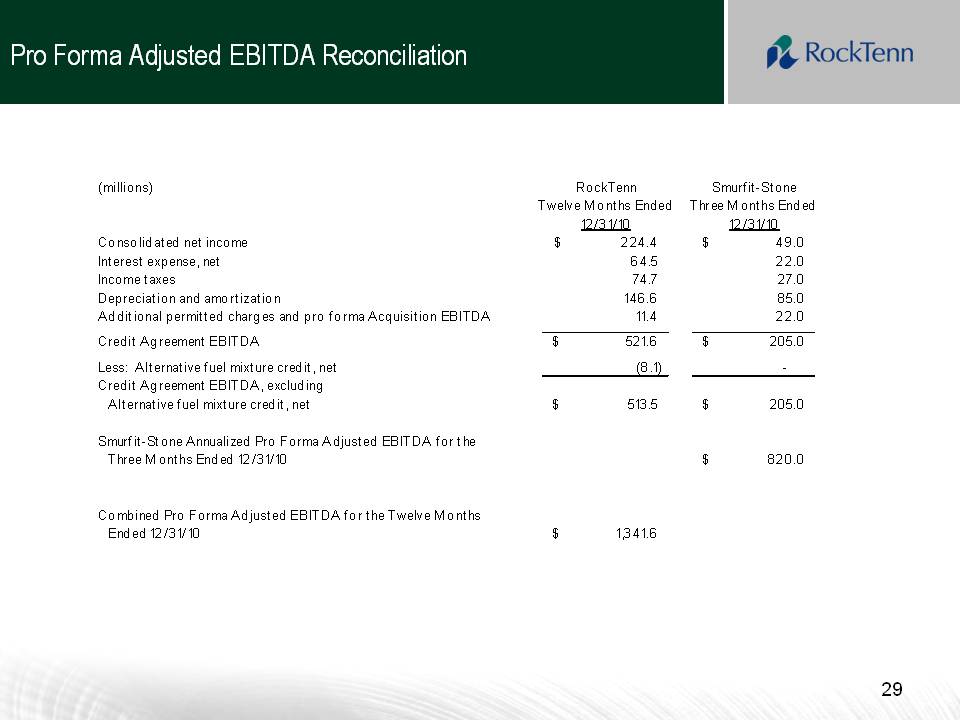

29 Pro Forma Adjusted EBITDA Reconciliation (millions) RockTenn Smurfit-Stone TwelveMonths Twelve Months Ended Three Months Ended 12/31/10 12/31/10 Consolidated net income 224.4 $ 49.0 $ Interest expense, net 64.5 22.0 Income taxes 74.7 27.0 Depreciation and amortization 146.6 85.0 Additional permitted charges and pro forma Acquisition EBITDA 11.4 22.0 Credit Agreement EBITDA 521.6 $ 205.0 $ Less: Alternative fuel mixture credit, net (8.1) - Credit Agreement EBITDA, excluding Alternative fuel mixture credit, net 513.5 $ 205.0 $ Smurfit-Stone Annualized Pro Forma Adjusted EBITDA for the Three M onths Ended 12/31/10 820.0 $ Combined Pro Forma Adjusted EBITDA for the Twelve Months Ended 12/31/10 1,341.6 $ 29

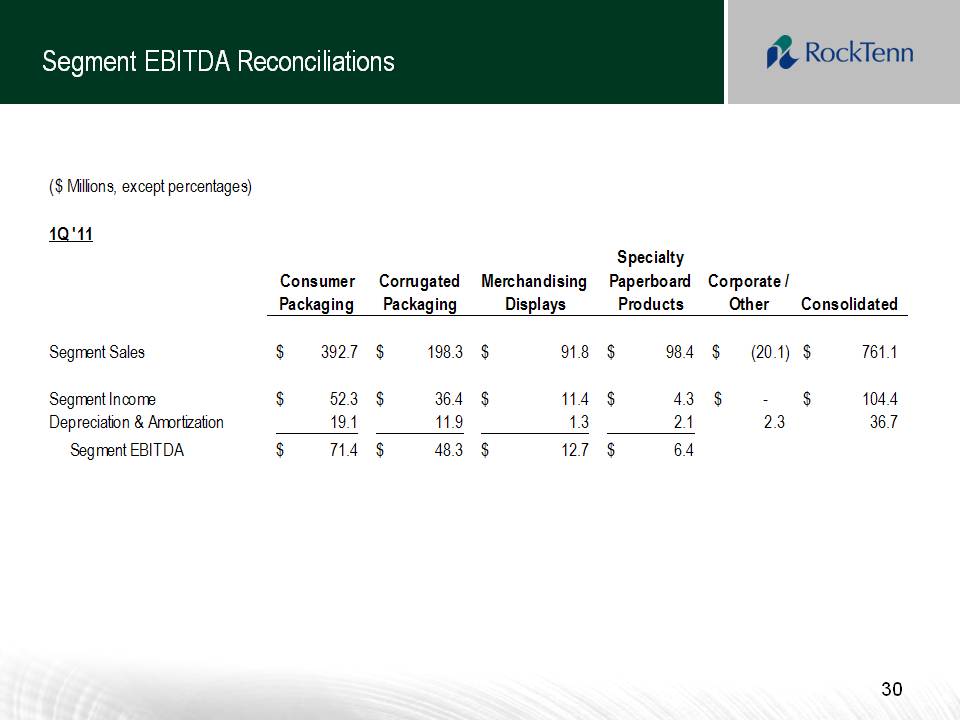

Segment EBITDA Reconciliations ($ Millions, except percentages) 1Q '11 Consumer Packaging Corrugated Packaging Merchandising Displays Specialty Paperboard Products Corporate / Other Consolidated Segment Sales 392.7 $ 198.3 $ 91.8 $ 98.4 $ (20.1) $ 761.1 $ Segment Income 52.3 $ 36.4 $ 11.4 $ 4.3 $ - $ 104.4 $ Depreciation & Amortization 19.1 11.9 1.3 2.1 2.3 36.7 Segment EBITDA 71.4 $ 48.3 $ 12.7 $ 6.4 $ 30

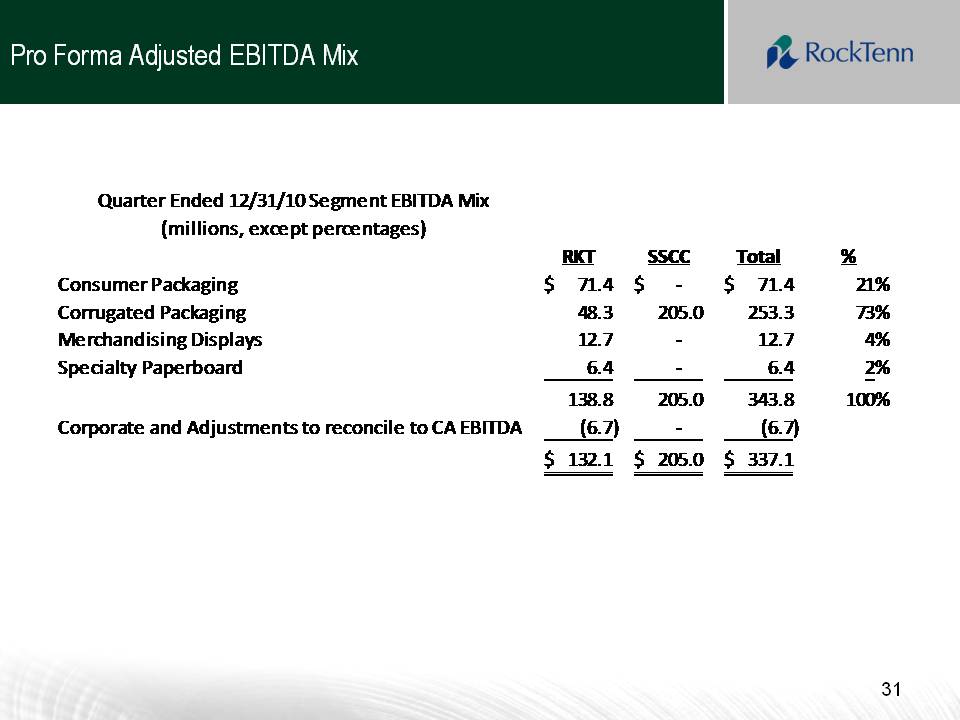

Pro Forma Adjusted EBITDA Mix Quarter Ended 12/31/10 Segment EBITDA Mix (millions, except percentages) RKT SSCC Total % Consumer Packaging 71.4 $ ‐ $ 71.4 $ 21% C tdP k i 48 3 205 0 253 3 73% Corrugated Packaging 48.3 205.0 253.3 Merchandising Displays 12.7 ‐ 12.7 4% Specialty Paperboard 6.4 ‐ 6.4 2% 138.8 205.0 343.8 100% Corporate and Adjustments to reconcile to CA EBITDA (6.7) ‐ (6.7) 132.1 $ 205.0 $ 337.1 $ 31

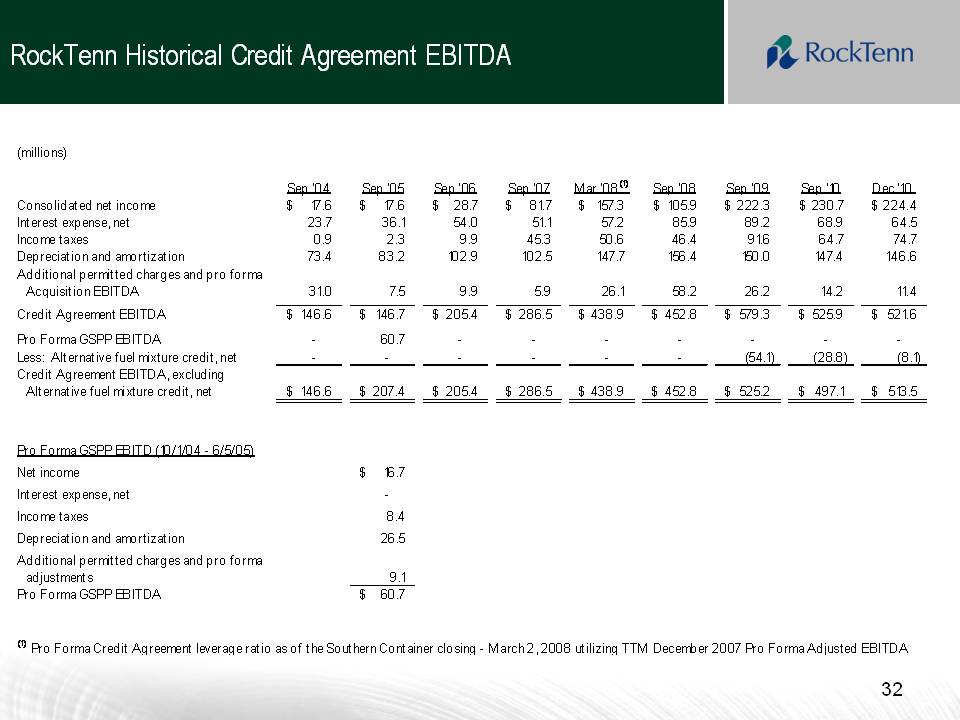

RockTenn Historical Credit Agreement EBITDA (millions) Sep '04 Sep '05 Sep '06 Sep '07 Mar '08(1) Sep '08 Sep '09 Sep '10 Dec '10 Consolidated 17 6 $ 17 6 $ 28 7 $ 817 $ 157 3 $ 105 9 $ 222 3 $ 230 7 $ 224 4 $ net income 17.6 17.6 28.7 81.7 157.3 105.9 222.3 230.7 224.4 Interest expense, net 23.7 36.1 54.0 51.1 57.2 85.9 89.2 68.9 64.5 Income taxes 0.9 2.3 9.9 45.3 50.6 46.4 91.6 64.7 74.7 Depreciation and amortization 73.4 83.2 102.9 102.5 147.7 156.4 150.0 147.4 146.6 Additional permitted charges and pro forma Acquisition EBITDA 31.0 7.5 9.9 5.9 26.1 58.2 26.2 14.2 11.4 C $ $ $ $ $ $ $ $ $ Credit Agreement EBITDA 146.6 146.7 205.4 286.5 438.9 452.8 579.3 525.9 521.6 Pro Forma GSPP EBITDA - 60.7 - - - - - - - Less: Alternative fuel mixture credit, net - - - - - - (54.1) (28.8) (8.1) Credit Agreement EBITDA, excluding Alternative fuel mixture credit, net 146.6 $ 207.4 $ 205.4 $ 286.5 $ 438.9 $ 452.8 $ 525.2 $ 497.1 $ 513.5 $ Pro Forma GSPP EBITD (10/1/04 - 6/5/05) Net income 16.7 $ Interest expense, net - 8 4 Income taxes 8.4 Depreciation and amortization 26.5 Additional permitted charges and pro forma adjustments 9.1 Pro Forma GSPP EBITDA 60.7 $ 32 (1) Pro Forma Credit Agreement leverage ratio as of the Southern Container closing - M arch 2, 2008 utilizing TTM December 2007 Pro Forma Adjusted EBITDA

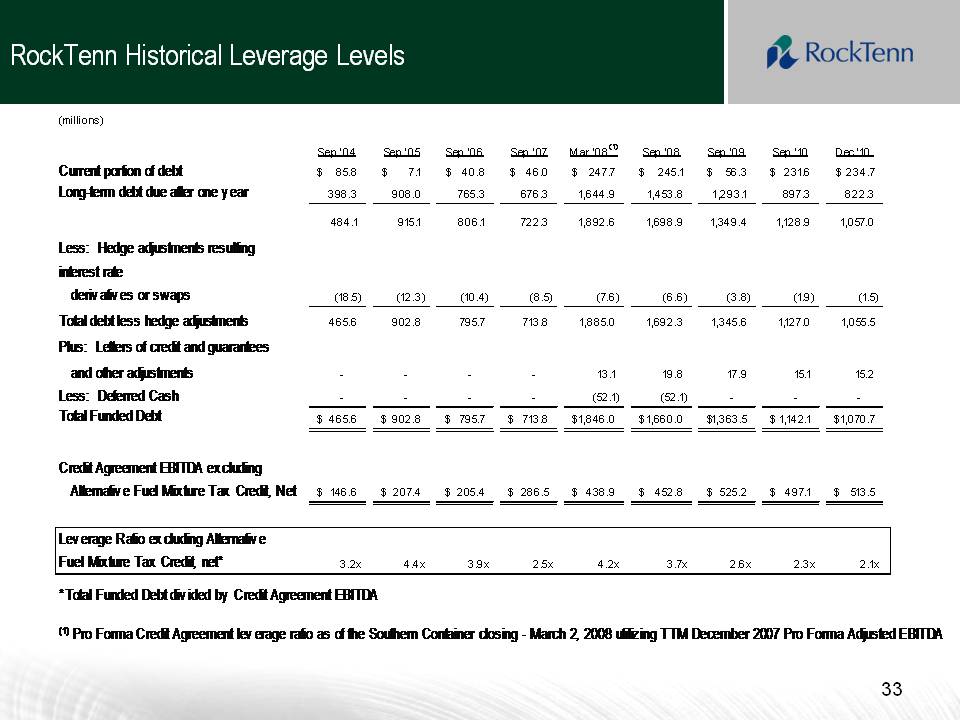

RockTenn Historical Leverage Levels (millions) Sep '04 Sep '05 Sep '06 Sep '07 Mar '08(1) Sep '08 Sep '09 Sep '10 Dec '10 Current portion of debt 85.8 $ 7.1 $ 40.8 $ 46.0 $ 247.7 $ 245.1 $ 56.3 $ 231.6 $ 234.7 $ Long-term debt due after one y ear 398.3 908.0 765.3 676.3 1,644.9 1,453.8 1,293.1 897.3 822.3 484.1 915.1 806.1 722.3 1,892.6 1,698.9 1,349.4 1,128.9 1,057.0 Less: Hedge adjustments resulting interest rate derivatives or swaps (18.5) (12.3) (10.4) (8.5) (7.6) (6.6) (3.8) (1.9) (1.5) Total debt less hedge adjustments 465.6 902.8 795.7 713.8 1,885.0 1,692.3 1,345.6 1,127.0 1,055.5 Plus: Letters of credit and guarantees and other adjustments - - - - 13.1 19.8 17.9 15.1 15.2 Less: Deferred Cash - - - - (52.1) (52.1) - - - Total Funded Funded Debt 465.6 $ 902.8 $ 795.7 $ 713.8 $ 1,846.0 $ 1,660.0 $ 1,363.5 $ 1,142.1 $ 1,070.7 $ Credit Agreement EBITDA excluding Alternative Fuel Mixture Tax Credit, Net 146.6 $ 207.4 $ 205.4 $ 286.5 $ 438.9 $ 452.8 $ 525.2 $ 497.1 $ 513.5 $ Leverage Ratio excluding Alternative Fuel Mixture Tax Credit, net* 3.2x 4.4x 3.9x 2.5x 4.2x 3.7x 2.6x 2.3x 2.1x *Total Funded Debt divided by Credit Agreement EBITDA 33 (1) Pro Forma Credit Agreement leverage ratio as of the Southern Container closing - March 2, 2008 utilizing TTM December 2007 Pro Forma Adjusted EBITDA

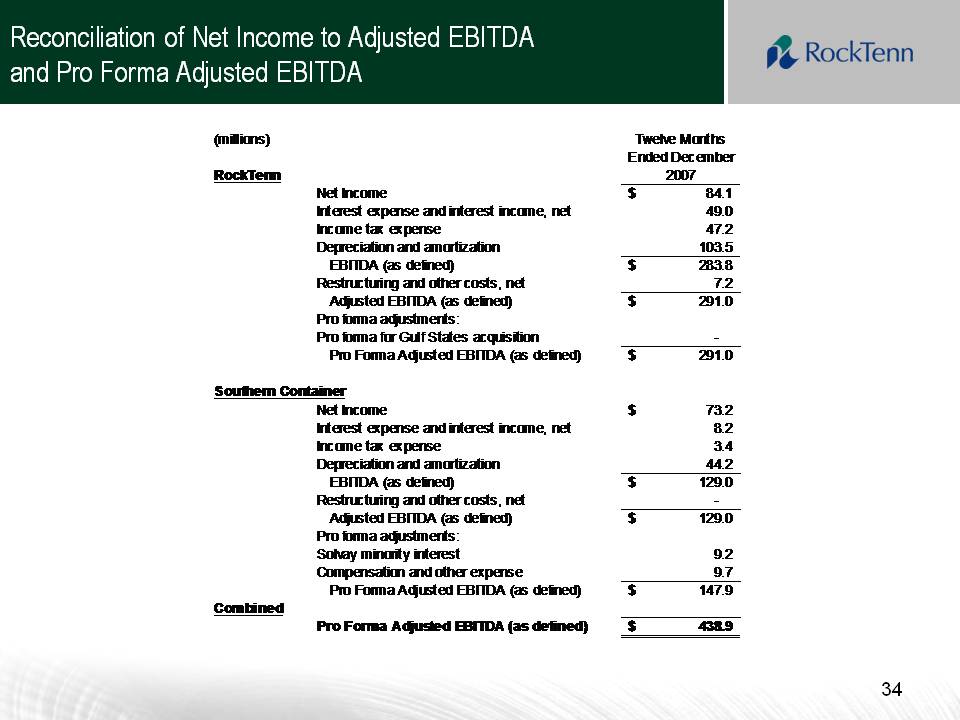

Reconciliation of Net Income to Adjusted EBITDA and Pro Forma Adjusted EBITDA (millions) Twelve Months Ended December RockTenn 2007 Net Income 84.1 $ Interest expense and interest income, net 49.0 Income tax expense 47.2 Depreciation and amortization 103.5 EBITDA (as defined) 283.8 $ Restructuring and other costs, net 7.2 Adjusted EBITDA ( as defined) 291.0 $ j ) Pro forma adjustments: Pro forma for Gulf States acquisition - Pro Forma Adjusted EBITDA (as defined) 291.0 $ Southern Container Net 73 2 $ Income 73.2 Interest expense and interest income, net 8.2 Income tax expense 3.4 Depreciation and amortization 44.2 EBITDA (as defined) 129.0 $ Restructuring and other costs, net - Adj t d d fi d) 129 0 $ Adjusted EBITDA ( as defined) 129.0 Pro forma adjustments: Solvay minority interest 9.2 Compensation and other expense 9.7 Pro Forma Adjusted EBITDA (as defined) 147.9 $ Combined 34 Pro Forma Adjusted EBITDA (as defined) 438.9 $

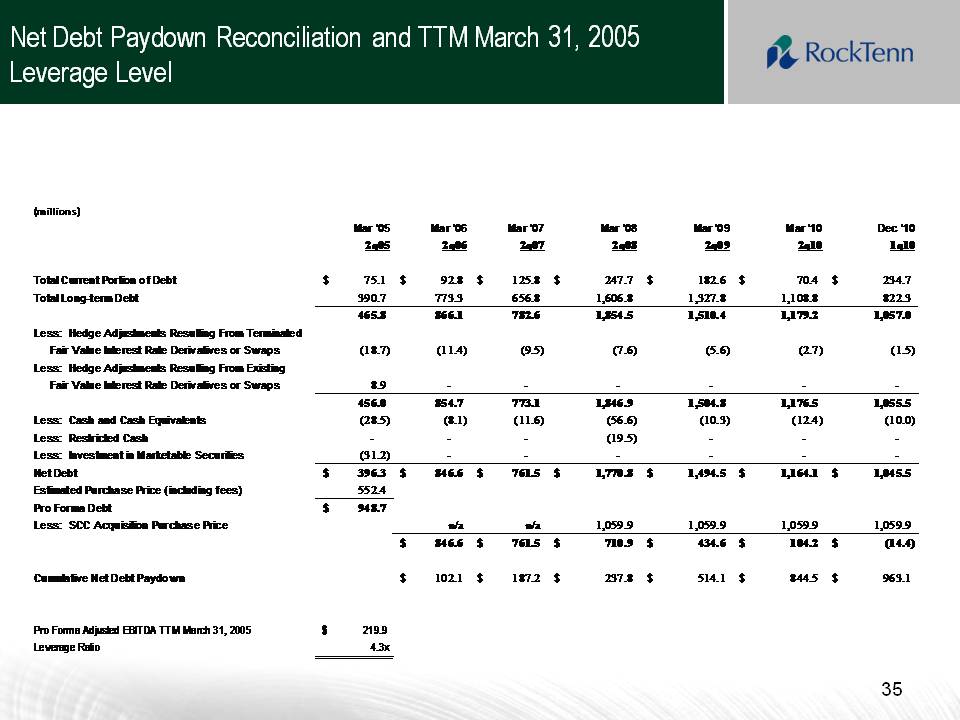

Net Debt Paydown Reconciliation and TTM March 31, 2005 Leverage Level (millions) Mar '05 Mar '06 Mar '07 Mar '08 Mar '09 Mar '10 Dec '10 2q05 2q06 2q07 2q08 2q09 2q10 1q10 Total Current Portion of Debt 75.1 $ 92.8 $ 125.8 $ 247.7 $ 182.6 $ 70.4 $ 234.7 $ Total Long-term Debt 390.7 773.3 656.8 1,606.8 1,327.8 1,108.8 822.3 465.8 866.1 782.6 1,854.5 1,510.4 1,179.2 1,057.0 Less: Hedge Adjustments Resulting From Terminated Fair Value Interest Rate Derivatives or Swaps (18.7) (11.4) (9.5) (7.6) (5.6) (2.7) (1.5) Less: Hedge Adjustments Resulting From Existing Fair Value Interest Rate Derivatives or Swaps 8.9 - - - - - - 456.0 854.7 773.1 1,846.9 1,504.8 1,176.5 1,055.5 Less: Cash and Cash Equivalents (28.5) (8.1) (11.6) (56.6) (10.3) (12.4) (10.0) Less: Restricted Cash - - - (19.5) - - - Less: Investment in Marketable Securities (31.2) - - - - - - Net Debt 396.3 $ 846.6 $ 761.5 $ 1,770.8 $ 1,494.5 $ 1,164.1 $ 1,045.5 $ Estimated Purchase Price (including fees) 552.4 Pro Forma Debt 948.7 $ Less: SCC Acquisition Purchase Price n/a n/a 1,059.9 1,059.9 1,059.9 1,059.9 846.6 $ 761.5 $ 710.9 $ 434.6 $ 104.2 $ (14.4) $ Cumulative Net Debt Paydow n 102.1 $ 187.2 $ 237.8 $ 514.1 $ 844.5 $ 963.1 $ 35 Pro Forma Adjusted EBITDA TTM March 31, 2005 219.9 $ Leverage Ratio 4.3x

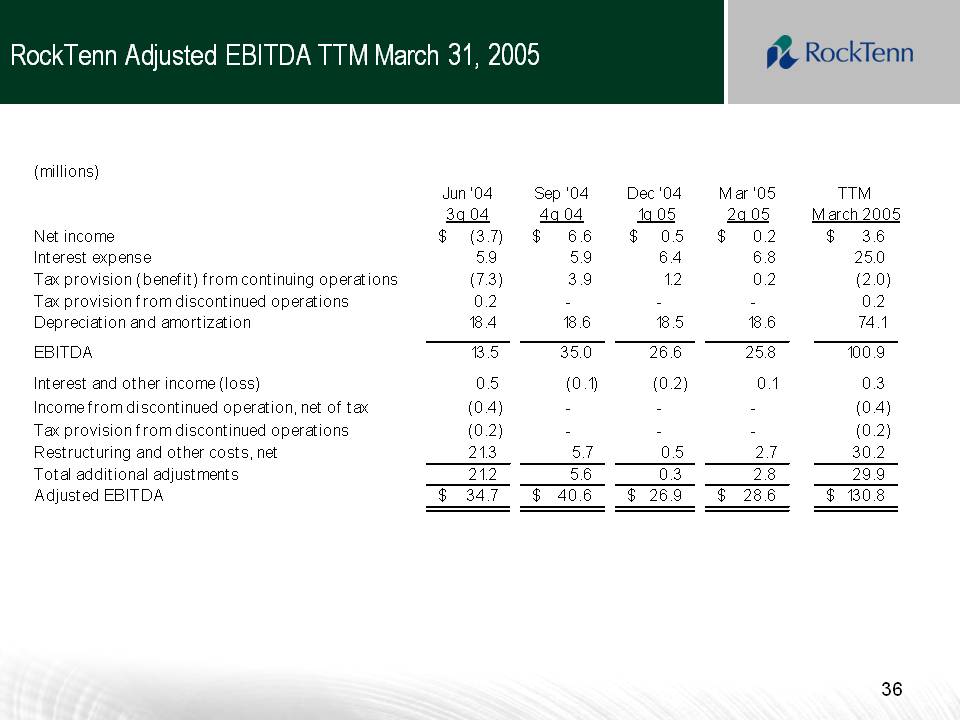

RockTenn Adjusted EBITDA TTM March 31, 2005 (millions) Jun '04 Sep '04 Dec '04 Mar '05 TTM 3q 04 4q 04 1q 05 2q 05 March 2005 Net income (3.7) $ 6.6 $ 0.5 $ 0.2 $ 3.6 $ Interest expense 5.9 5.9 6.4 6.8 25.0 Tax provision (benefit) from continuing operations (7.3) 3.9 1.2 0.2 (2.0) Tax provision from discontinued operations 0.2 - - - 0.2 p p Depreciation and amortization 18.4 18.6 18.5 18.6 74.1 EBITDA 13.5 35.0 26.6 25.8 100.9 Interest and other income (loss) 0.5 (0.1) (0.2) 0.1 0.3 Income fromdiscontinued (0.4) - - - (0.4) from discontinued operation, net of tax Tax provision from discontinued operations (0.2) - - - (0.2) Restructuring and other costs, net 21.3 5.7 0.5 2.7 30.2 Total additional adjustments 21.2 5.6 0.3 2.8 29.9 Adjusted EBITDA 34.7 $ 40.6 $ 26.9 $ 28.6 $ 130.8 $ 36

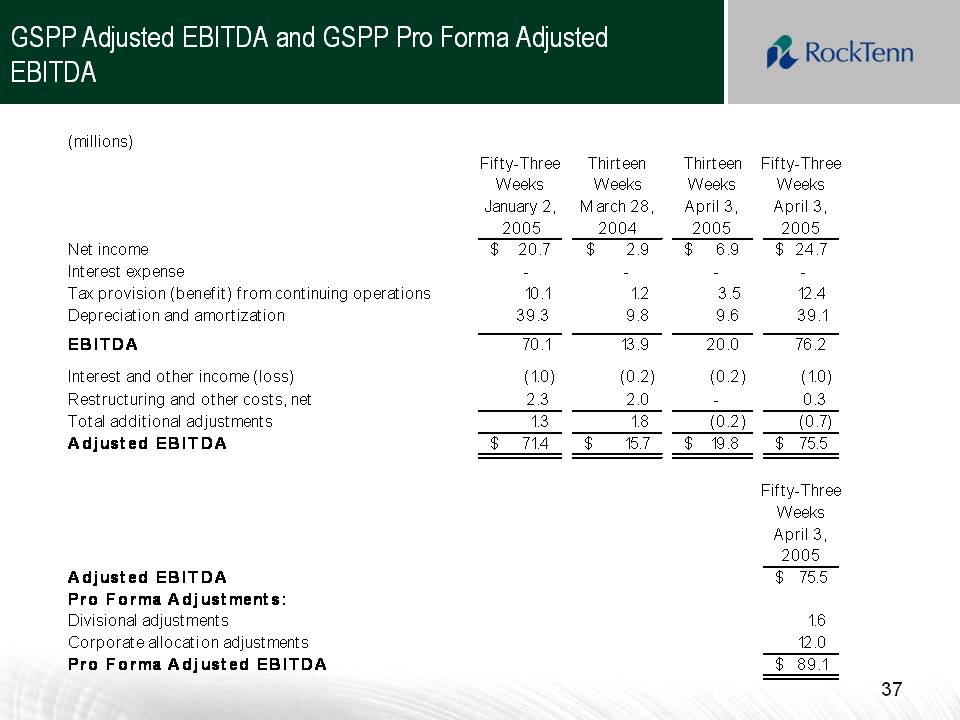

GSPP Adjusted EBITDA and GSPP Pro Forma Adjusted EBITDA (millions) Fifty-Three Thirteen Thirteen Fifty-Three Weeks January 2 Weeks March 28 Weeks April 3 Weeks April 3 2, 2005 28, 2004 3, 2005 3, 2005 Net income 20.7 $ 2.9 $ 6.9 $ 24.7 $ Interest expense - - - - Tax provision (benefit) from continuing operations 10.1 1.2 3.5 12.4 Depreciation and amortization 39.3 9.8 9.6 39.1 EBITDA 70.1 13.9 20.0 76.2 Interest and other income (loss) (1.0) (0.2) (0.2) (1.0) Restructuring and other costs, net 2.3 2.0 - 0.3 Total additional adjustments 1.3 1.8 (0.2) (0.7) Adjusted EBITDA 71.4 $ 15.7 $ 19.8 $ 75.5 $ Fifty-Three Weeks April 3, 2005 Adjusted EBITDA 75.5 $ Pro Forma Adjustments: 16 37 Divisional adjustments 1.6 Corporate allocation adjustments 12.0 Pro Forma Adjusted EBITDA 89.1 $

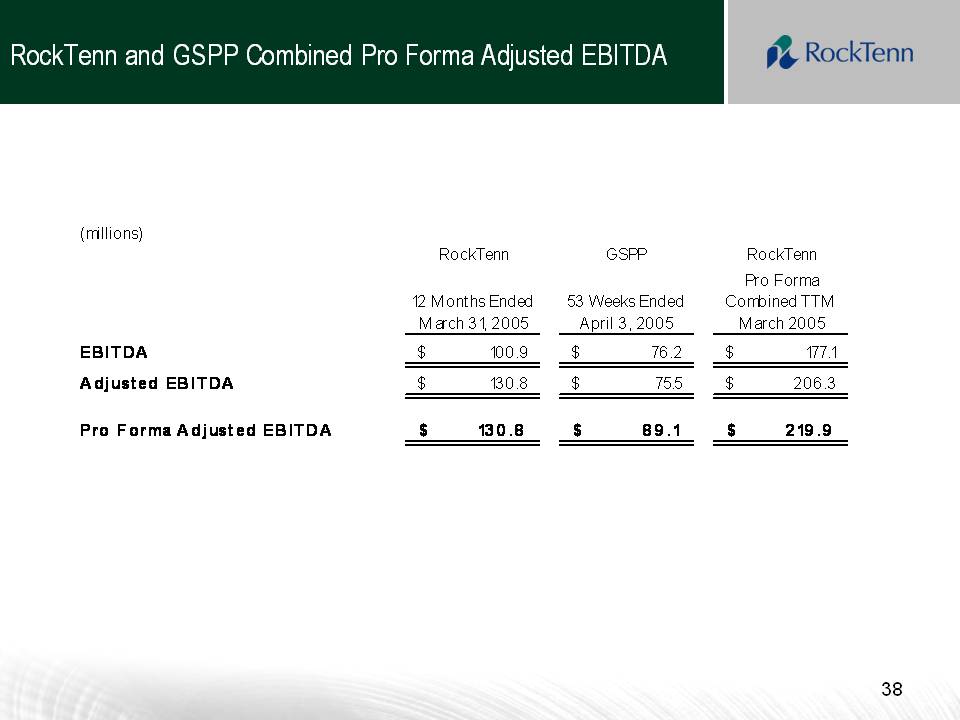

RockTenn and GSPP Combined Pro Forma Adjusted EBITDA (millions) RockTenn GSPP RockTenn 12 M onths Ended 53 Weeks Ended Pro Forma Combined TTM March 31, 2005 April 3, 2005 March 2005 EBITDA 100.9 $ 76.2 $ 177.1 $ Adjust ed EBITDA 130.8 $ 75.5 $ 206.3 $ Pro Forma Adjust ed EBITDA 13 0 .8 $ 8 9 .1 $ 2 19 .9 $ 38