Attached files

| file | filename |

|---|---|

| 8-K - MEADOWBROOK INSURANCE GROUP 8-K 2-22-2011 - MEADOWBROOK INSURANCE GROUP INC | form8k.htm |

| EX-99.2 - EXHIBIT 99.2 - MEADOWBROOK INSURANCE GROUP INC | ex99_2.htm |

Exhibit 99.1

Investor Presentation

February 2011

Bob Cubbin, CEO

Karen Spaun, CFO

2

Forward-Looking Statements

Certain statements made by Meadowbrook Insurance Group, Inc. in this presentation may

constitute forward-looking statements including, but not limited to, those statements that include

the words "believes," "expects," "anticipates," "estimates," or similar expressions. Please refer

to the Company's most recent 10-K, 10-Q, and other Securities and Exchange Commission

filings for more information on risk factors. Actual results could differ materially. These forward-

looking statements involve risks and uncertainties including, but not limited to the following: the

frequency and severity of claims; uncertainties inherent in reserve estimates; catastrophic

events; a change in the demand for, pricing of, availability or collectability of reinsurance;

increased rate pressure on premiums; obtainment of certain rate increases in current market

conditions; investment rate of return; changes in and adherence to insurance regulation;

actions taken by regulators, rating agencies or lenders; obtainment of certain processing

efficiencies; changing rates of inflation; and general economic conditions. Meadowbrook is not

under any obligation to (and expressly disclaims any such obligation to) update or alter its

forward-looking statements whether as a result of new information, future events or otherwise.

constitute forward-looking statements including, but not limited to, those statements that include

the words "believes," "expects," "anticipates," "estimates," or similar expressions. Please refer

to the Company's most recent 10-K, 10-Q, and other Securities and Exchange Commission

filings for more information on risk factors. Actual results could differ materially. These forward-

looking statements involve risks and uncertainties including, but not limited to the following: the

frequency and severity of claims; uncertainties inherent in reserve estimates; catastrophic

events; a change in the demand for, pricing of, availability or collectability of reinsurance;

increased rate pressure on premiums; obtainment of certain rate increases in current market

conditions; investment rate of return; changes in and adherence to insurance regulation;

actions taken by regulators, rating agencies or lenders; obtainment of certain processing

efficiencies; changing rates of inflation; and general economic conditions. Meadowbrook is not

under any obligation to (and expressly disclaims any such obligation to) update or alter its

forward-looking statements whether as a result of new information, future events or otherwise.

3

The Meadowbrook Approach

Our objective is to generate predictable results across the market cycle,

with a target return on average equity of 10% - 17%

with a target return on average equity of 10% - 17%

To achieve these results we seek to leverage the unique characteristics of

our balanced business model to generate:

our balanced business model to generate:

Consistent, profitable underwriting results

Predictable investment income in a low-risk, high-quality, fixed income portfolio

Profitable growth both organically and through acquisitions

Strong cash flow from our insurance company subsidiaries and non-regulated fee-

based services to leverage invested assets to equity and manage debt service

based services to leverage invested assets to equity and manage debt service

Steady fee and commission income

We strive to deliver consistent results with a balanced business model

We are a specialty niche focused commercial insurance underwriter and

insurance administration services company

insurance administration services company

4

Meadowbrook Vitals

Current market cap (at 2/18/11): $559.5 million

Outstanding shares at 12/31/10: 53.2 million

Weighted average shares (At 12/31/10): 54.3 million

Book value (12/31/2010): $547.1 million

Book value per share: $10.28 (TTM Dec -10 ROAE 11.4%)

– Excluding unrealized gain / loss, net of deferred taxes: $9.61 (TTM Dec -10 ROAE 12.1%)

– Tangible book value per share (excluding goodwill and intangibles):$7.36 (TTM Dec -10 ROAE 15.7%)

Debt to equity: 21.7%; 6.9% excluding debentures

Debt to total capital: 17.8%; 5.7% excluding debentures

Current price / book: 1.02 (at $10.51/share market price - as of 2/18/11)

Dividend yield (at 2/18/11): 1.60%

Statutory premium leverage Actual Target

– GWP to Statutory surplus 2.2 to 1 2.75 to 1

– NWP to Statutory surplus 1.9 to 1 2.25 to 1

Insider ownership (at 12/31/10): 7.1%

5

What Makes Us Different:

We are Flexible and are Able to Adapt to Changing Market Conditions

Diverse Revenue

Sources

Sources

Positioned to Manage

Insurance Cycles

Insurance Cycles

Conservative

Investment

Philosophy

Investment

Philosophy

Ability to Attract and

Retain Talented

Professionals

Retain Talented

Professionals

Our model allows us to deliver more predictable results

Strong Capital and

Liquidity Position

Liquidity Position

Earned premium from insurance operations Fee revenue from risk management services Flexibility to utilize multiple distribution channels Product, program and geographic diversification Admitted market capabilities contribute to stability and higher renewal retention Non-admitted capabilities enable opportunistic response in volatile pricing environment High-quality fixed income approach to our $1.3 billion portfolio Investment approach reinforces our focus on underwriting profitability Team of talented insurance professionals with a wide range of expertise across all functions and lines of business Regional structure enables associates to deliver strong and responsive local service to clients Insurance subsidiaries rated A- (Excellent) by A.M. Best Insurance subsidiary surplus levels can support meaningful premium growth Generate cash flows from both regulated and non-regulated sources, which provides flexibility Manageable debt levels, with access to $35 million line of credit (no outstanding balance)

6

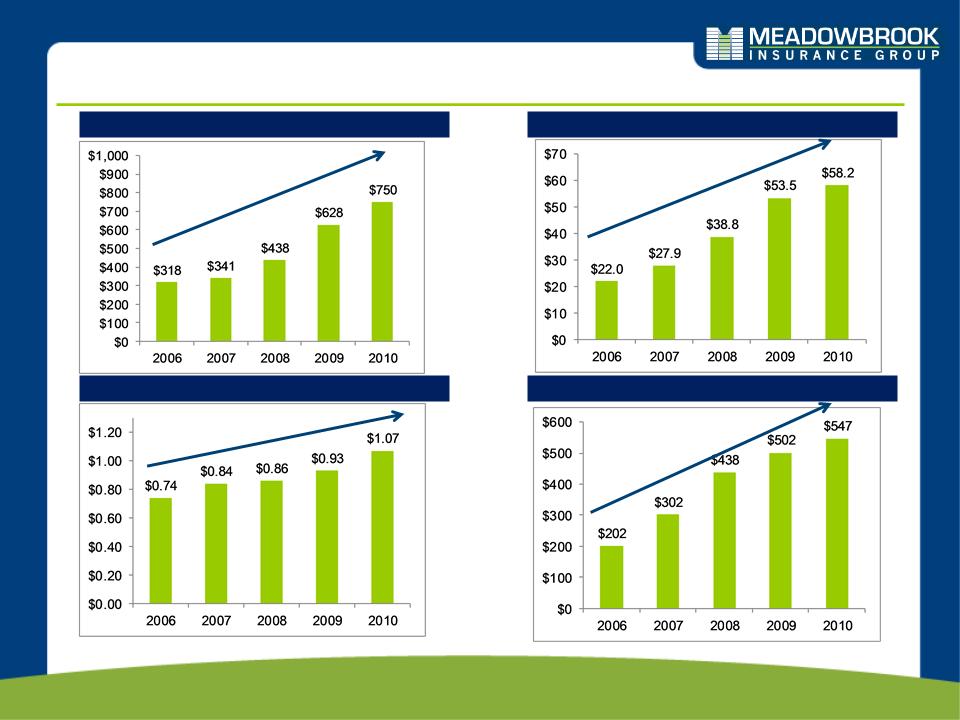

Our Approach Has Delivered Results Over Time

Total Revenue ($M)

Net Operating Income ($M)

Shareholders’ Equity ($M)

Net Operating Income per Share

CAGR (2006 to 2010) = 24%

CAGR (2006 to 2010) = 28%

CAGR (2006 to 2010) = 28%

CAGR (2006 to 2010) = 10%

7

Capability Building Through Successful Acquisitions

Retail Agency Only

1955: Founded as a retail insurance agency

Core Capability Build Out

1985: Star Insurance Company

1990: Savers Property & Casualty Insurance Company

1994: American Indemnity Insurance Company

1996: Association Self Insurance Services

1997: Williamsburg National Insurance Company

Crest Financial Services

1998: Ameritrust Insurance Corporation

Florida Preferred Administrators, Inc.

1999: TPA Insurance Agency

Continued Synergistic Expansion

2007: USSU

2008: Procentury

Strategic Staging of Acquisitions

• Opportunity to leverage our diverse revenue

platform, by expanding current distribution,

servicing capabilities, and complementary

product lines and classes

platform, by expanding current distribution,

servicing capabilities, and complementary

product lines and classes

• Ability to attract talented insurance

professionals that are a good fit with

Meadowbrook culture

professionals that are a good fit with

Meadowbrook culture

• Opportunity to create “win-win” situation by

mitigation our downside risk and providing seller

with opportunity to obtain fair value through deal

structure

mitigation our downside risk and providing seller

with opportunity to obtain fair value through deal

structure

Meadowbrook actively reviews acquisition prospects on a strategic basis and enters into transactions that will increase long-term shareholder value We consider a range of strategic factors when looking at acquisitions including:

8

Diverse Revenue Sources

Insurance Operations

Commission Revenue

Fee Revenue

Our most prominent source of revenue and income comes from our insurance operation;

commission revenue and fee-for-service revenue generate unregulated free cash flow

commission revenue and fee-for-service revenue generate unregulated free cash flow

Admitted and non-admitted products and

programs

programs

Risk sharing vehicles

Managed program revenue

Municipality and Association clients

Agency commission from non-affiliated carriers

TTM Dec -10 Earned Premium: $659.8 M

TTM Dec -10 Net Investment Income: $54.2M

TTM Dec -10 Fee Revenue: $23.0 M

TTM Dec -10 Commission Revenue: $11.2 M

9

Insurance Operations

Diversified Commercial Positions Built to Manage Across Cycles

Main Street Excess

and Surplus Lines

and Surplus Lines

Admitted Programs

Non-Admitted

Programs

Programs

Specialty Markets

Homogeneous specialized programs

Heterogeneous geographic centers

Product focused

Promotes specialty agents

Broad classes of “Main Street”

commercial risks

commercial risks

Promotes General Agent

distribution

distribution

Specialized programs ignored or

underserved by the standard market

underserved by the standard market

Promotes wholesalers with specialty

underwriting authority

underwriting authority

Solutions designed for very specific

products and market segments

products and market segments

TTM Dec-10 GWP:$532 M

TTM Dec-10 GWP: $147 M

TTM Dec-10 GWP: $47 M

TTM Dec-10 GWP: $76 M

Picture framers

Music equipment stores

Christian booksellers

Chemical distributors

Description

Examples

Restaurants, bars and taverns

Apartments, hotels and motels

Mercantile

Contractors liability

Pet-sitters

Oil and gas contractors

Assisted care facilities

Package delivery

Excess workers’ comp

Transportation

Agriculture

Marine

10

National Scope with Regional Perspective

Bermuda

Talented associates are located throughout the country to serve the needs of

regional clients

regional clients

Support from headquarters enables efficient resource deployment and cross-unit

coordination

coordination

Balance of effective local touch, with efficient national coordination

Meadowbrook locations

Top 10 production states (As of 12/31/2010)

1

2

4

6

3

1

2

7

5

10

8

9

11

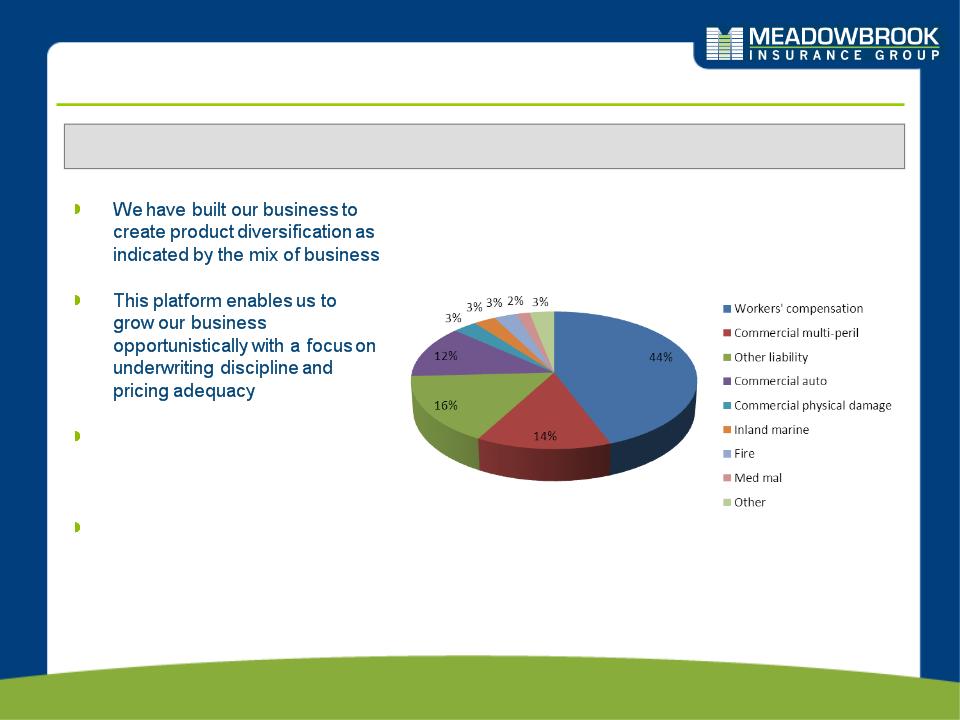

Diverse Mix of Business

Full Year 2010 Gross Written Premium Business Mix

Year Ended December 31, 2010

Our wide range of product

expertise positions us well to

support future growth

expertise positions us well to

support future growth

Our new business is primarily

rollover books of business with

a proven track record of

profitability

rollover books of business with

a proven track record of

profitability

Loss and Expense Ratios

12

Loss ratio

2006 - 2010 GAAP and Accident Year Combined Ratios

96.8%

Our GAAP combined ratio has improved over time and our accident year combined ratio

has remained profitable

has remained profitable

2006

2007

2008

2009#

2010

97.9%

95.4%

98.0%

93.3%

97.8%

93.2%

98.5%

95.0%

99.7%

Re-estimated AY Combined Ratio†

(as of 12/31/2010)

94.7%*

94.7%*

93.2%*

98.3%

†The re-estimated AY combined ratio reflects reserve adjustments made following the accident year, for example, the 94.7% re-estimated 2006 AY

combined ratio reflects new loss development information gathered over the 4 years from 12/31/2006 to 12/31/2010; the 94.7% re-estimated 2007 AY

combined ratio reflects new loss development gathered over the 3 years from 12/31/2007 to 12/31/2010; etc.

combined ratio reflects new loss development information gathered over the 4 years from 12/31/2006 to 12/31/2010; the 94.7% re-estimated 2007 AY

combined ratio reflects new loss development gathered over the 3 years from 12/31/2007 to 12/31/2010; etc.

* The 2006 - 2007 initial and re-estimated AY combined ratios excludes Century. The 2008 re-estimated AY combined ratio includes a pro-rata portion of

the Century AY 2008 development for the 5 post-merger months.

the Century AY 2008 development for the 5 post-merger months.

# 2009 AY and CY expense ratio reflects expense reclassification as disclosed in our May 3, 2010 8-k filing with the SEC.

99.7%

Expense Ratio Analysis

13

Twelve Month Ended GAAP Expense Ratio Comparison

Net earned premium $539.6M $659.8M

Policy acquisition $175.1M $227.0M

and other u/w expenses

and other u/w expenses

Expense ratio 32.5% 34.4%

*As a result of our internal cost allocation study,1.0% of internal claims administration is included in the 2010 expense

ratio instead of ULAE

ratio instead of ULAE

14

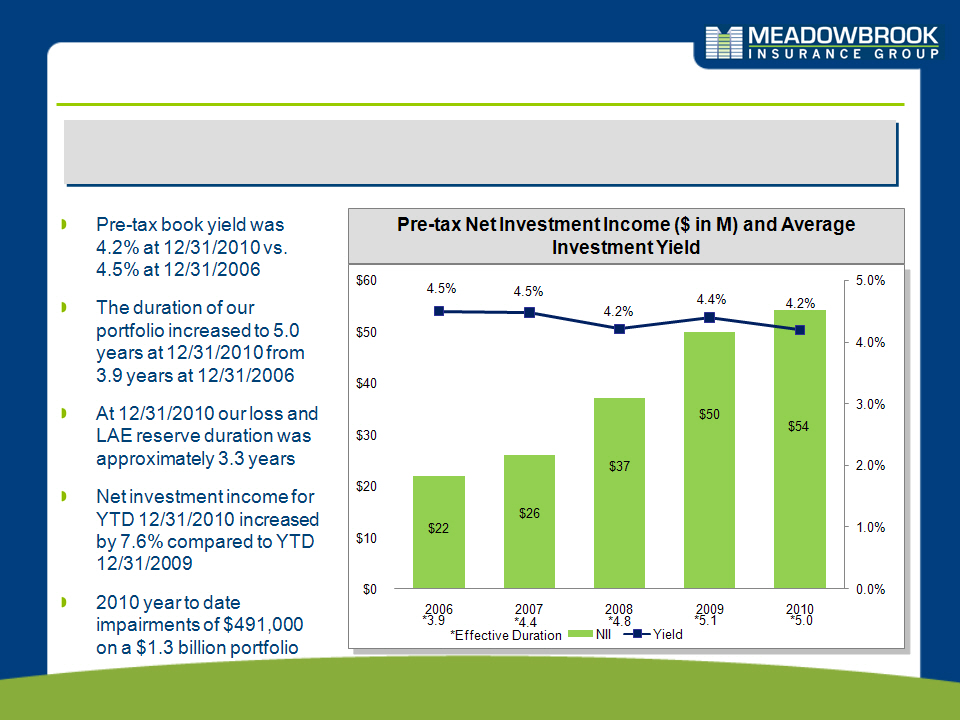

Focus on Generating Consistent Investment

Income

Income

Robust top line growth has led to a larger investment base and a meaningful

increase in full year NII

increase in full year NII

Pre-tax book yield was 4.2% at 12/31/2010 vs. 4.5% at 12/31/2006 The duration of our portfolio increased to 5.0 years at 12/31/2010 from 3.9 years at 12/31/2006 At 12/31/2010 our loss and LAE reserve duration was approximately 3.3 years Net investment income for YTD 12/31/2010 increased by 7.6% compared to YTD 12/31/2009 2010 year to date impairments of $491,000 on a $1.3 billion portfolio

15

We Maintain a High Quality, Low Risk Investment Portfolio

We maintain a conservative investment portfolio

Portfolio Allocation and Quality

Allocation based on market value

Low equity risk exposure

– 98% fixed income and cash

– 2% equity

High credit quality

– 98% of bonds are investment grade

– Average S&P rating of AA / Moody’s

of Aa2

of Aa2

The effective duration of our $1.3 billion

portfolio is 5.0 years

portfolio is 5.0 years

The duration on net reserves of $784

million is approximately 3.3 years

million is approximately 3.3 years

NOTE: Data above as of December 31, 2010

16

Fee-Based and Agency Operations Give Us

Flexibility with Unregulated Cash Flow

Flexibility with Unregulated Cash Flow

We serve the self-insurance market for municipalities and associations

– Sample clients include the Michigan Municipal League, the Minnesota County

Insurance Trust and the Alabama Forest Fund

Insurance Trust and the Alabama Forest Fund

We provides clients administrative and back office services

In many cases, programs have been built on long-standing

relationships

relationships

A source of non-regulated liquidity that has low capital requirements

Agency

Operations

Operations

Managed

Programs

Programs

Original foundation of the company in 1955

We operate five retail / wholesale agencies and generate commission

income from more than 50 unaffiliated carriers

income from more than 50 unaffiliated carriers

Our fee-based and commission businesses are relatively small but continue to

provide a valuable source of unregulated cash flow

provide a valuable source of unregulated cash flow

17

Capital Management

Our goal is to be efficient managers of capital; we initiated a dividend during

2008 and since this time we have returned $54.4M to shareholders through

dividends and share repurchases

2008 and since this time we have returned $54.4M to shareholders through

dividends and share repurchases

18

Capital Management

Since 2008 our share repurchase activity has been accretive, increasing

BVPS by $0.20

BVPS by $0.20

12/31/2010 BVPS: $10.28

19

Recent Financial Highlights:

Highlights ($ in M)

20

Full Year 2011 Guidance and Long Term Value Creation

Looking ahead to 2011, we expect a market similar to that which we have

experienced during 2010

experienced during 2010

Gross Written Premium

$802M

Combined Ratio

95.0%

Net income from operations

$58.2M

Net operating income per share

$1.07

2010 Results

Leverage multiple revenue

sources and diverse insurance

offering to maximize

opportunities across market

cycles

sources and diverse insurance

offering to maximize

opportunities across market

cycles

Increase underwriting leverage

through selective growth

opportunities, while sustaining

appropriate diversification

through selective growth

opportunities, while sustaining

appropriate diversification

Increase investment leverage

through cash from operations

through cash from operations

Leverage fixed costs over a

larger revenue base

larger revenue base

Increase fee-for service

income through new

opportunities and margin

expansion

income through new

opportunities and margin

expansion

Driving Long-term

Enterprise Value

Enterprise Value

2011 Guidance*

Gross Written Premium

Range of $830M - $850M

Combined Ratio

Range of 96.0% - 97.0%

Net income from operations

$53.0M - $58.5M

Net operating income per share

$1.00 to $1.10 per share

*Our guidance range does not

include any favorable or

unfavorable development on

prior year reserves

include any favorable or

unfavorable development on

prior year reserves