Attached files

| file | filename |

|---|---|

| EX-5.1 - QKL Stores Inc. | v211115_ex5-1.htm |

| EX-23.3 - QKL Stores Inc. | v211115_ex23-3.htm |

| EX-23.2 - QKL Stores Inc. | v211115_ex23-2.htm |

As

filed with the Securities and Exchange Commission on February 17,

2011

Registration

No. 333-167087

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

FORM

S-1/A

(Amendment

No. 3)

REGISTRATION

STATEMENT UNDER THE SECURITIES ACT OF 1933

QKL

STORES INC.

(Exact

name of registrant as specified in its charter)

|

Delaware

|

445110

|

75-2180652

|

||

|

(State

or other jurisdiction of

|

(Primary

Standard Industrial

|

(I.R.S.

Employer Identification Number)

|

||

|

incorporation

or organization)

|

Classification

Code Number)

|

1

Nanreyuan Street

Dongfeng

Road

Sartu

District

163300

Daqing, P.R. China

+86-459-460-7626

(Address,

including zip code, and telephone number including area code, of registrant’s

principal executive offices)

National

Corporate Research, Ltd.

615

South DuPont Highway, County of Kent

Dover,

DE 19901

800-483-1140

(Name,

address, including zip code, and telephone number,

including

area code, of agent for service)

Copies

to:

Mitchell

S. Nussbaum, Esq.

Loeb

& Loeb LLP

345

Park Avenue

New

York, New York 10154

Tel.

No.: 212-407-4159 Fax No.: 212-407-4990

Approximate date of commencement of

proposed sale to the public: From time to time after this Registration

Statement becomes effective.

If any of

the securities being registered on this Form are to be offered on a delayed or

continuous basis pursuant to Rule 415 under the Securities Act of 1933, check

the following box. x

If this

Form is filed to register additional securities for an offering pursuant to Rule

462(b) under the Securities Act, check the following box and list the Securities

Act registration statement number of the earlier effective registration

statement for the same offering. ¨

If this

Form is a post-effective amendment filed pursuant to Rule 462(c) under the

Securities Act, check the following box and list the Securities Act registration

statement number of the earlier effective registration statement for the same

offering. ¨

If this

Form is a post-effective amendment filed pursuant to Rule 462(d) under the

Securities Act, check the following box and list the Securities Act registration

statement number of the earlier effective registration statement for the same

offering. ¨

Indicate

by check mark whether the registrant is a large accelerated filer, an

accelerated filer, a non-accelerated filer or a smaller reporting company. See

definitions of “large accelerated filer”, “accelerated filer” and “smaller

reporting company” in Rule 12b-2 of the Exchange Act.

Large

Accelerated Filer ¨

Accelerated Filer ¨

Non-Accelerated Filer ¨ Smaller

Reporting Company x

CALCULATION

OF REGISTRATION FEE

|

Title of each class of securities to be

registered

|

Amount to be

registered(1)

|

Proposed

maximum

offering price

per share (2)

|

Proposed

maximum

aggregate

offering price (2)

|

Amount of

registration

fee (3)

|

||||||||||||

|

Common

stock, par value $.001 per share (3)

|

798,875 | $ | 3.24 | $ | 2,588,355 | $ | 301 | |||||||||

|

Common

stock, par value $.001 per share, underlying Series A Preferred Stock

(4)

|

1,129,430 | $ | 3.24 | $ | 3,659,353 | $ | 425 | |||||||||

|

Common

stock, par value $.001 per share, underlying Series A Warrants

(5)

|

3,201,025 | $ | 3.24 | $ | 10,371,321 | $ | 1,204 | |||||||||

|

Common

stock, par value $.001 per share, underlying Series B Warrants

(6)

|

796,372 | $ | 3.24 | $ | 2,580,245 | $ | 300 | |||||||||

|

Total

|

5,925,702 | $ | 19,199,274 | $ | 2,230 | (7) | ||||||||||

|

(1)

|

Pursuant to Rule 416 promulgated

under the Securities Act of 1933, as amended, there are also registered

hereunder such indeterminate number of additional shares as may be issued

to the selling stockholders to prevent dilution resulting from stock

splits, stock dividends or similar

transactions.

|

|

|

|

|

(2)

|

Estimated solely for purposes

of calculating the registration fee. The registration fee is calculated

pursuant to Rule 457(c). Our common stock is quoted under the symbol

“QKLS” on the NASDAQ Capital Market (“NASDAQ”). On February 10, 2011,

the highest price reported was $3.28 per share and the lowest reported

price was $3.20 per share. The average of the highest and lowest reported

prices as of such date was $3.24 per share. Accordingly, the registration

fee is $2,230 based on $3.24 per

share.

|

|

(3)

|

Consists of 798,875 shares of

our common stock (for a more detailed description, see “Selling

Stockholders”).

|

|

|

|

|

(4)

|

Consists of 1,129,430 shares of

common stock issuable to the selling stockholders upon conversion of the

Series A Preferred Stock (for a more detailed description, see “Selling

Stockholders”).

|

|

|

|

|

(5)

|

Consists of 3,201,025 shares

of common stock issuable to the selling stockholders upon exercise of the

Series A Warrants (for a more detailed description, see “Selling

Stockholders”).

|

|

|

|

|

(6)

|

Consists of 796,372 shares of

common stock issuable to the selling stockholders upon exercise of Series

B Warrants (for a more detailed description, see “Selling

Stockholders”).

|

|

(7)

|

$6,020 was previously

paid.

|

Pursuant

to Rule 429 under the Securities Act of 1933, the prospectus included in this

registration statement is a combined prospectus relating to registration

statement no. 333-150800 previously filed by the registrant on Form S-1 and

declared effective August 11, 2009, under which sales ceased on April 1, 2010.

This registration statement, which is a new registration statement, also

constitutes post-effective amendment no. 3 to registration statement no.

333-150800, and such post-effective amendment shall hereafter become effective

concurrently with the effectiveness of this registration statement and in

accordance with Section 8(c) of the Securities Act of 1933. This

registration statement excludes an aggregate of 958,882 shares of common

stock that were included on registration statement no. 333-150800, including

shares of common stock underlying the Series A Preferred Stock, Series A

Warrants and Series B Warrants that have been sold under registration statement

no. 333-150800, pursuant to Rule 144 of the Securities Act of 1933, as amended

(the “Act”), or otherwise disposed of pursuant to an available exemption from

the Act.

The

registrant amends this registration statement on such date or dates as may be

necessary to delay its effective date until the registrant shall file a further

amendment which specifically states that this registration statement shall

hereafter become effective in accordance with Section 8(a) of the Securities Act

of 1933, or until the registration statement shall become effective on such date

as the Commission, acting pursuant to Section 8(a), may

determine.

PROSPECTUS

QKL

STORES INC.

5,925,702 Shares

of Common Stock

Offered

by Selling Stockholders

This

prospectus relates to the sale by the selling stockholders identified in this

prospectus of up to 5,925,702 shares of our common stock

comprising:

|

§

|

798,875 shares of common

stock held by selling

stockholders;

|

|

|

|

|

§

|

1,129,430 shares of common

stock that the selling stockholders may acquire on conversion of Series A

Preferred Stock;

|

|

|

|

|

§

|

3,201,025 shares of common

stock issuable to certain selling stockholders upon exercise of Series A

Warrants; and

|

|

|

|

|

§

|

796,372 shares of common stock

issuable to certain selling stockholders upon exercise of Series B

Warrants.

|

Of

the 798,875 shares of currently outstanding common stock being

registered, 392,616 were acquired by the selling stockholders prior to

completion of the private placement and the reverse merger described in this

prospectus, 6,000 were issued upon the exercise of Series A Warrants and Series

B Warrants that were issued to one of our consultants for services rendered in

connection with the private placement, 57,656 were issued upon exercise of

Series A Warrants and Series B Warrants issued to the placement agent for

services rendered in connection with the private placement, and 342,603 were

issued upon conversion of Series A Preferred Stock acquired in the private

placement. The Series A Preferred Stock was purchased by the selling

stockholders in a private placement completed on March 28, 2008. We

are required by the terms of a registration rights agreement and a separate

agreement to register the shares listed above. The Series A Preferred

Stock is convertible into common stock at the rate (subject to adjustment) of

one share of common stock for each share of Series A Preferred Stock. The

Series A Warrants are exercisable for one share of common stock at an exercise

price of $3.40 per share (subject to adjustment) and expire on March 27,

2013. The Series B Warrants are exercisable for one share of common stock

at an exercise price of $4.25 per share (subject to adjustment) and expire on

March 27, 2013.

Our

common stock is listed on the Nasdaq Capital Market (“NASDAQ”) under the symbol

“QKLS.” On February 15, 2011, the last reported sale price of our

common stock quoted on NASDAQ was $3.26 per share.

The

selling stockholders may sell all or any portion of their shares of common stock

in one or more transactions on NASDAQ or in private negotiated

transactions. Each selling stockholder will determine the prices at which

it sells its shares. Although we will incur expenses in connection with

the registration of the common stock (estimated to be approximately $55,230), we

will not receive any of the proceeds from the sale of the shares of common stock

by the selling stockholders. To the extent the warrants are exercised for cash,

if at all, we will receive the exercise price for those warrants. Under

the terms of the warrants, cashless exercise is permitted after September 28,

2009 but only if the resale of the warrant shares by the holder is not covered

by an effective registration statement. We cannot assure you that the

warrants will be exercised for cash or at all.

Investing

in our common stock involves a high degree of risk. See “Risk Factors” beginning

on page 6 for a discussion of certain risk factors that you should consider. You should read the entire

prospectus before making an investment decision.

Neither

the Securities and Exchange Commission nor any state securities commission has

approved or disapproved of these securities or passed upon the accuracy or

adequacy of this prospectus. Any representation to the contrary is a criminal

offense.

The

date of this prospectus is ,

2011

TABLE

OF CONTENTS

|

PROSPECTUS

SUMMARY

|

1

|

| THE OFFERING | 5 |

|

RISK

FACTORS

|

6

|

|

ABOUT

THIS PROSPECTUS

|

21

|

|

CAUTIONARY

NOTE REGARDING FORWARD-LOOKING STATEMENTS AND OTHER INFORMATION CONTAINED

IN THIS PROSPECTUS

|

22

|

|

OTHER

REFERENCES

|

23

|

|

EXPLANATORY

NOTE

|

23

|

|

SELLING

STOCKHOLDERS

|

24

|

|

PLAN

OF DISTRIBUTION

|

30

|

|

USE

OF PROCEEDS

|

31

|

|

MANAGEMENT’S

DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF

OPERATIONS

|

32

|

|

BUSINESS

|

44

|

|

PROPERTIES

|

56

|

|

LEGAL

PROCEEDINGS

|

60

|

|

OUR

HISTORY AND CORPORATE STRUCTURE

|

61

|

| MARKET PRICE OF COMMON EQUITY AND RELATED STOCKHOLDER MATTERS | 69 |

|

SECURITY

OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT

|

71

|

|

DIRECTORS

AND EXECUTIVE OFFICERS

|

72

|

|

EXECUTIVE

COMPENSATION

|

75

|

|

CERTAIN

RELATIONSHIPS AND RELATED PARTY TRANSACTIONS

|

78

|

|

DESCRIPTION

OF SECURITIES TO BE REGISTERED

|

81

|

|

LEGAL

MATTERS

|

82

|

|

EXPERTS

|

82

|

|

INTERESTS

OF NAMED EXPERTS AND COUNSEL

|

83

|

|

SERVICE

OF PROCESS AND ENFORCEMENT OF JUDGMENTS

|

83

|

|

CHANGES

IN AND DISAGREEMENTS WITH ACCOUNTANTS

|

83

|

|

WHERE

YOU CAN FIND MORE INFORMATION

|

84

|

|

DISCLOSURE

OF COMMISSION POSITION ON INDEMNIFICATION FOR SECURITIES ACT

LIABILITIES

|

84

|

| INDEX TO FINANCIAL STATEMENTS | 85 |

i

PROSPECTUS

SUMMARY

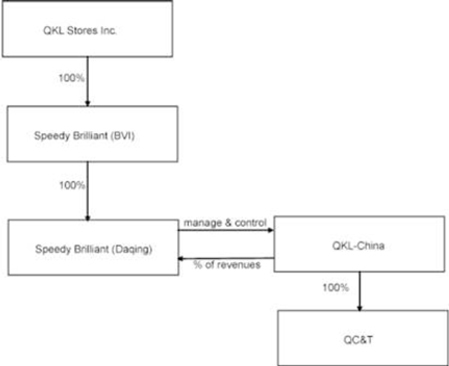

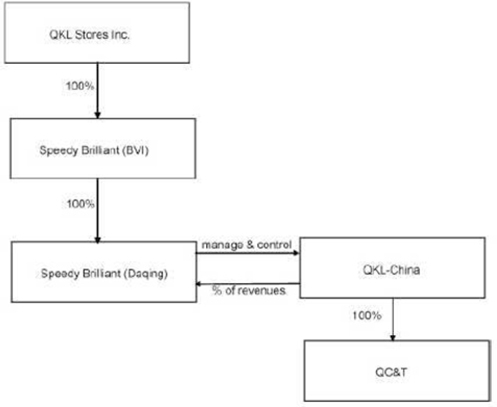

References

to “QKL-China” are to Daqing Qing Ke Long Chain Commerce & Trade Co., Ltd.,

a People’s Republic of China retail company that we control through a series of

contractual arrangements described in the section entitled “Our History and

Corporate Structure.” Unless otherwise specified or required by context,

references to “we,” “our,” “us” and the “Company” refer collectively to (i) QKL

Stores Inc. (formerly known as Forme Capital, Inc.), (ii) the subsidiaries of

QKL Stores Inc., which are Speedy Brilliant Group Limited, a British Virgin

Islands company (“Speedy Brilliant (BVI)”), which is wholly owned by QKL Stores

Inc., and Speedy Brilliant Commercial Consultancy Co., Ltd. (“Speedy Brilliant

(Daqing)”), which is wholly owned by Speedy Brilliant (BVI), (iii) QKL-China,

and (iv) Daqing Qinglongxin Commerce & Trade Co., Ltd. (“QC&T”), a

wholly owned subsidiary of QKL-China. For convenience, certain amounts in

Chinese Renminbi (“RMB”) have been converted to United States dollars at an

exchange rate of $1 = RMB 6.8282, the exchange rate on December 31, 2009.

References to “IGA” are to the Independent Grocers Alliance, an international

trade group and network of supermarkets that offers its members access to

industry information, bargaining advantages with suppliers, and other benefits

of affiliation with a large trade group. IGA reports that its member companies

operate in 40 countries worldwide and have total revenues of $21 billion per

year. Its website is www.IGA.com. References in this prospectus to the “PRC” or

“China” are to the People’s Republic of China.

In

keeping with standard practice and the practice of the National Bureau of

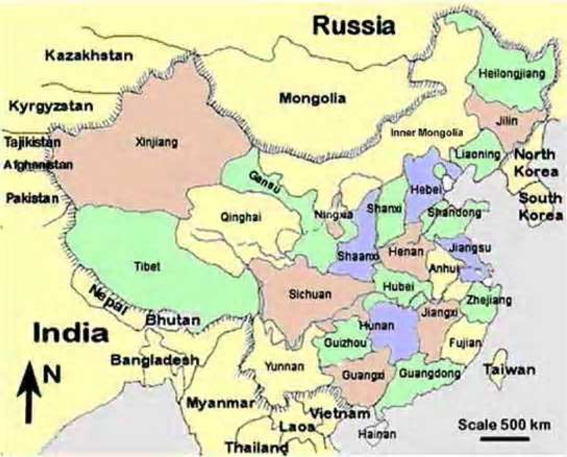

Statistics of China, references to “northeastern China” are to the three

northeastern provinces of Heilongjiang, Jilin and Liaoning. A map showing these

provinces is included in the section of this report entitled “Other

References.”

References

to QKL-China’s “registered capital” are to the equity of QKL-China, which under

PRC law is measured not in terms of shares owned but in terms of the amount of

capital that has been or will be contributed to a company by a particular

shareholder or all shareholders. The portion of a limited liability company’s

total capital contributed by a particular shareholder represents that

shareholder’s ownership of the company and the total amount of capital

contributed by all shareholders is the company’s total equity. Capital

contributions are made to a company by deposits into a dedicated account in the

company’s name, which the company may access in order to meet its financial

needs. When a company’s accountant certifies to PRC authorities that a capital

contribution has been made and the company has received the necessary government

permission to increase its contributed capital, the capital contribution is

registered with regulatory authorities and becomes a part of the company’s

“registered capital.”

Summary

We are

a regional supermarket chain that currently operates 45 supermarkets and 3

department stores in northeastern China and Inner Mongolia. Our supermarkets

sell a broad selection of merchandise including groceries, fresh food and

non-food items. We currently have 2 distribution centers servicing our

supermarkets, one for fresh food and another for grocery and non-food

merchandise.

We are

the first supermarket chain in northeastern China and Inner Mongolia that is a

licensee of the Independent Grocers Alliance, or IGA, a United States-based

global grocery network with aggregate retail sales of more than $21.0 billion

per year. As a licensee of IGA, we are able to engage in group bargaining with

suppliers and have access to more than 2,000 private IGA brands, including many

that are exclusive IGA brands.

Our total

revenues for the year ended December 31, 2009 was approximately $247.6 million,

an increase of $87.5 million, or 54.7%, compared to total revenues of $160.1

million for the year ended December 31, 2008. Our net income excluding changes

in fair value of warrants for the year ended December 31, 2009 was approximately

$10.8 million, an increase of $1.8 million, or 20.0%, from approximately $9.0

million for the year ended December 31, 2008.

1

Our

Industry

We

operate in the supermarket industry in China, which is a part of the country’s

retail trade sector. We believe the retail market has benefited from compelling

industry fundamentals such as rapid economic growth, urbanization and increasing

disposable income.

China’s

economy has been experiencing consistent growth with nominal GDP growing from

approximately $1.9 trillion in 2004 to approximately $4.9 trillion in 2009. As a

result of China’s rapid economic growth, the urban population has increased

dramatically as people in rural and less developed areas migrate to cities in

search of better jobs and higher living standards. During the period between

2004 and 2009, the total urban population in China increased by approximately

79.0 million, or approximately 14.6%. This growth has been accompanied by rising

income levels of urban households where annual per capita disposable income

increased from $1,379 in 2004 to $2514 in 2009 a compound growth rate of 12.8%.

A growing middle class combined with an increasing affluence and purchasing

power has driven the rapid development of the retail sector and in turn driven a

large increase in consumer spending. Consumer spending has grown from $789

billion in 2004 to approximately $1.8 trillion in 2009, a compound growth rate

of approximately 18.4%.

Northeast

China has a population of 133 million, or approximately 9% of China’s

population. In December 2007, a major economic-development plan for northeastern

China, the “Plan for Revitalizing Northeast China,” was announced by an office

of the PRC’s State Counsel. We believe that the plan indicates a commitment by

the PRC government to make economic development of northeastern China a high

priority. We also believe that this development is likely to contribute to our

growth.

Company

History

On March

28, 2008, QKL Stores Inc. (formerly known as Forme Capital, Inc.) acquired

control of QKL-China through a “reverse merger” transaction. Upon completion of

the reverse merger transaction, QKL Stores Inc. ceased to be a shell company (as

that term is defined in Rule 12b-2 under the Securities Exchange Act of 1934

(the “Exchange Act”)).

2

Shares

Issued To The Selling Stockholders

Placement

Agent Warrants

On March

9, 2007, QKL entered into an engagement agreement with Kuhns Brothers, Inc.

(“Kuhns Agreement”) for the provision of investment banking and other services

as in contemplation of a reverse merger of the company or a company affiliated

with the company with a publicly traded shell company and simultaneous $15.5

million financing transaction. On January 22, 2008, QKL terminated the

engagement agreement and the parties executed a settlement agreement. Under the

terms of the settlement agreement, Kuhns Brothers, Inc. was paid a cash fee

equal to 8.5% of the gross proceeds invested in the financing by investors

introduced to the Company by Kuhns Brothers, Inc. and was issued Series A

Warrants to purchase 191,250 shares of our common stock and Series B Warrants to

purchase 153,000 shares of our common stock. We believe that the designees to

whom Kuhns Brothers, Inc. transferred the securities it received pursuant to the

settlement agreement were employees or otherwise affiliated with Kuhns Brothers,

Inc. and received their shares as consideration for their services to Kuhns

Brothers, Inc.

Mass

Harmony Consulting Agreement

Yang

Miao, Ying Zhang and Fang Chen are principals of Mass Harmony Asset Management

(“Mass Harmony”). On March 13, 2007, QKL-China entered into a Financial

Consulting Agreement (the “Mass Harmony Agreement”) with Mass Harmony under

which Mass Harmony agreed to perform certain financial services for QKL-China.

QKL-China paid Mass Harmony an aggregate of RMB 500,000 (approximately $70,000)

and Mass Harmony also received 299,999 shares of common stock, Series A Warrants

to purchase 91,176 shares of common stock, and Series B Warrants to purchase

72,941 shares of common stock. 6,000 shares of common stock, 30,392 shares of

common stock underlying Series A Warrants and 24,314 shares of common stock

underlying Series B Warrants that have not previously been disposed of are being

registered in this prospectus. On March 30, 2010, Ying Zhang assigned her Series

A Warrant to purchase 30,392 shares of common stock and her Series B Warrant to

purchase 24,314 shares of common stock to Roth Capital Partners, a registered

broker-dealer. The remaining shares transferred to Yang Miao, Ying Zhang and

Fang Chen by Mass Harmony have been disposed of pursuant to our registration

statement on Form S-1 (file no. 333-150800) or pursuant to Rule 144 promulgated

under the Securities Act of 1933, as amended. Yang Miao and Fang Chen are

selling stockholders. Roth Capital Partners is not a selling

stockholder.

Other

Issuances in 2007

Robert

Scherne, a selling stockholder, served as a director and Chief Financial Officer

of Forme Capital from September 19, 2007 until March 28, 2008. In December 2007,

Mr. Scherne received 21,000 shares of common stock as compensation for his

services, of which he currently holds 17,000 shares of common stock that are

being registered on this prospectus.

In

December 2007, we issued 37,211 shares of our common stock to Menlo Venture

Partners, LLC, as repayment of a working capital advance in the amount of

$25,000.

Reverse

Merger and Private Placement Transaction

On March

28, 2008, we acquired control of QKL-China through a “reverse merger”

transaction. Through the reverse merger we ceased to be a shell company as that

term is defined in Rule 12b-2 under the Securities Exchange Act of 1934, as

amended (the “Exchange Act”) and then became in the business of operating

supermarkets in northeastern China.

At the

same time as the closing of the reverse merger transaction, we closed a private

placement of securities, in which we sold to certain accredited investors listed

under “Investors In Private Placement” in the Selling Stockholders table

included in the section of this prospectus entitled “Investors in Private

Placement,” for gross proceeds to us of $15.5 million, 9,117,647 units at a

purchase price of $1.70 per unit, each unit consisting of one share of Series A

Preferred Stock (each of which is convertible into one share of our common

stock), a 0.625 interest in a Series A Warrant and a 0.625 interest in a Series

B Warrant. The Series A Warrants have an exercise price of $3.40 per share

(subject to adjustment), the Series B Warrants have an exercise price of $4.25

per share (subject to adjustment). We received $13,523,530 as net proceeds from

this financing. The closing of the private placement was conditioned on the

closing of the reverse merger transaction.

On March

28, 2008, as part of a $15.5 million private placement, we entered into a

registration rights agreement (as amended on May 8, 2008) with certain

investors, pursuant to which we agreed to register for resale up to an aggregate

of 20,514,705 shares of common stock, including shares of common stock

underlying Series A Preferred Stock, Series A Warrants and Series B Warrants.

The registration rights agreement provided that if the initial registration

statement required to be filed thereunder was not declared effective by

September 24, 2008, we would be required to pay certain liquidated damages to

the investors. On March 9, 2009, the investors party to the registration rights

agreement waived their right to such liquidated damages and on August 11, 2009,

the initial registration statement covering 2,070,836 shares of the total shares

registrable pursuant to the registration rights agreement was declared

effective. We were not able to register the balance of the shares required to be

registered pursuant to the registration rights agreement due to limits imposed

by the Securities Exchange Commission’s interpretation of Rule 415 of Regulation

C promulgated under the Securities Act of 1933, as amended (the “ Securities Act

”).

There are

additional deadlines we are required to meet if the private placement investors

request that we file one or more registration statements covering the remaining

shares that we are obligated to register pursuant to the registration rights

agreement. In the event that we are required to file an additional registration

statements to cover securities that we have previously been unable to register,

we will be required to file any such additional registration statement within 30

days of receipt of demand notice from certain of our stockholders. We will

further be required to have any such additional registration statement declared

effective within 150 days of its initial filing date, or 180 days from its

initial filing date in the event that the registration statement is given a full

review by the Securities and Exchange Commission. If we fail to meet one or more

of those deadlines, we would, in the absence of an additional waiver, be

required to pay the investors up to a maximum of $1,550,000 in liquidated

damages. Payment of a significant amount of liquidated damages would harm our

profitability and we may not have sufficient cash to pay them.

Other

Issuances

Castle

Bison, Inc., a selling stockholder, is a California corporation owned and

controlled by Raul Silvestre. Mr. Silvestre was counsel to the Company from

September 17, 2007 to March 28, 2008. On September 17, 2007, Castle Bison

acquired its shares of our common stock from Synergy Business Consulting

pursuant to a stock purchase agreement (“2007 Private Placement”) by and among

the Company, Synergy Business Consulting and Lomond International, Inc., as

agent for several buyers. Prior to March 28, 2008, Castle Bison owned

approximately 9.19% of our outstanding common stock, or 137,790 shares.

Therefore, Castle Bison could be deemed to have been our affiliate at that

time.

Windermere

Insurance Company, a selling stockholder, is a British Virgin Islands business

development company. John Scardino has sole voting and dispositive power over

the shares held by Windermere. Windermere acquired its shares of our common

stock in the 2007 Private Placement. Prior to March 28, 2008, Windermere owned

approximately 7.75% of our outstanding common stock, or 116,234 shares.

Therefore, Windermere could be deemed to have been our affiliate at that

time.

Each

of Benjamin Hill, Fink Family Trust, Brandon Hill, Mark Bell M.D. Inc Retirement

Trust, Larry Chimerine, Irv Edwards M.D. Inc. Employee Retirement Trust, and

Marie Tillman acquired its shares of our common stock in the 2007 Private

Placement.

In

December 2007, we issued 37,211 shares of our common stock to Menlo Venture

Partners, LLC, as repayment of a working capital advance in the amount of

$25,000.

In

December 2007, Robert Scherne, our former chief financial officer and director,

acquired his shares of our common stock as compensation for his

services.

Pursuant

to a Warrant Purchase Agreement by and between Warberg Opportunistic Trading

Fund, LP (“Warberg”) and Straus-GEPT Partners, L.P. dated June 14, 2010, Warberg

acquired 147,059 Series B Warrants to purchase 147,059 shares of common

stock.

For

additional information regarding the Private Placement Transaction, please see

the section of this prospectus entitled “Our History and Corporate

Structure”.

3

The

following table compares:

A. the

number of shares of common stock issued and outstanding prior to our March 2008

private placement transaction, which were held by persons other than the selling

shareholders, affiliates of the company, and affiliates of the selling

shareholders;

B. the

number of shares registered for resale by the selling shareholders or affiliates

of the selling shareholders in our registration statement No. 333-150800

previously filed with the SEC and declared effective on August 11, 2009 (the

“2009 Registration Statement”);

C. the

number of shares registered for resale in the 2009 Registration Statement by the

selling shareholders or affiliates of the selling shareholders that continue to

be held by the selling shareholders or affiliates of the selling

shareholders;

D. the

number of shares registered for resale in the 2009 Registration Statement that

have been sold in resale transactions by the selling shareholders or affiliates

of the selling shareholders; and

E. the

number of shares registered for resale on behalf of the selling shareholders or

affiliates of selling Shareholders pursuant to this Registration

Statement.

|

A

|

B

|

C

|

D

|

E

|

||||||||||||

|

99,044

|

2,070,836

|

1,111,954

|

958,882

|

5,925,702

|

||||||||||||

Public

Offering

In

November 2009, we raised an aggregate of $39.7 million in a public offering of

6,900,000 shares of our common stock at a price of $5.75 per share.

Name

Change

On June

18, 2008, we changed our name from Forme Capital, Inc. to QKL Stores Inc. On the

same date, our name change was reflected on the Over-the-Counter Bulletin Board

(“OTCBB”) and our common stock began trading under the stock symbol QKLS.OB. On

October 21, 2009, our common stock was listed on NASDAQ under the symbol

“QKLS.”

Executive

Office

Our

executive offices are located at 1 Nanreyuan Street, Dongfeng Road, Sartu

District, Daqing, 163300 P.R.C. and our telephone number is (011)

86-459-4607987. Our corporate website is www.qklstoresinc.com.

Information contained on, or accessed through our website is not intended to

constitute and shall not be deemed to constitute part of this

report.

4

The

Offering

Offering

by Selling Stockholders

This

prospectus relates to the sale by the selling stockholders identified in this

prospectus of up to 5,925,702 shares of our common stock

comprising:

|

§

|

798,875 shares of common stock

held by selling

stockholders;

|

|

§

|

1,129,430 shares of common stock

that the selling stockholders may acquire on conversion of Series A

Preferred Stock; and

|

|

§

|

3,201,025 shares of common

stock issuable to certain selling stockholders upon exercise of Series A

Warrants

|

|

§

|

796,372 shares of common stock

issuable to certain selling stockholders upon exercise of Series B

Warrants.

|

The

shares being registered may be offered for sale by the selling stockholders from

time to time. No shares are being offered for sale by the Company.

|

Common

stock outstanding prior to Offering

|

29,769,590

as of February 16, 2011

|

|

|

Common

stock offered by the Company

|

0

|

|

|

Total

shares of common stock offered by selling stockholders

|

5,925,702

|

|

|

Common

stock to be outstanding after the offering (assuming conversion of all of

the Series A Preferred Stock being offered, exercise of all of the Series

A and exercise of all the Series B Warrants being offered Warrants being

offered )

|

48,490,903

|

|

|

Total

dollar value of common stock being registered

|

Our

common stock is listed on the Nasdaq Capital Market (“NASDAQ”) under the

symbol “QKLS.” On February 15, 2011, the last reported sale price of our

common stock quoted on NASDAQ was $3.26 per share. Using this value the

dollar value of the 5,925,702 shares of common stock (including the shares

underlying the Series A Preferred Stock, Series A Warrants and Series B

Warrants) being registered was $19,317,789.

|

|

|

Use

of Proceeds

|

We

will not receive any of the proceeds from the sales of the shares by the

selling stockholders. To the extent the warrants are exercised for cash we

will receive the exercise price for those warrants. Under the terms of the

warrants, cashless exercise is permitted after September 28, 2009 but only

if the underlying shares have not been registered. We intend to use any

cash proceeds received from the exercise of the warrants for working

capital and other general corporate purposes. We cannot assure you that

any of those warrants will ever be exercised for cash or at

all.

|

|

|

Our

NASDAQ

Trading

Symbol

|

QKLS

|

|

|

Risk

Factors

|

See

“Risk Factors” beginning on page 6 and other information included in this

prospectus for a discussion of factors you should consider before deciding

to invest in shares of our common

stock.

|

5

RISK

FACTORS

An

investment in our common stock involves a high degree of risk. You should

carefully consider the risks described below and the other information contained

in this report before deciding to invest in our common stock.

If

we do not receive prompt delivery of the goods we order, in good condition, and

at the prices we expect, our ability to generate profits could be

harmed.

As a

retail company, our ability to keep our shelves stocked with a wide variety of

merchandise is essential to our success and is dependent on the prompt delivery

of the goods we order, in good condition, and at the prices we expect.

Disruptions to our supply chain could cause us to reduce the variety or overall

amount of goods we sell; to seek alternative sources for affected supplies; or

to increase our prices, decrease our profit margins, or both. Any of these

consequences could lead to our customers buying less, shopping elsewhere or

criticizing our reputation. If this occurred, our income, profitability,

reputation and competitive position would all suffer.

Our

supply chain and costs could be disrupted by a wide variety of events. The most

significant of these are described below:

|

|

§

|

Problems with

transportation infrastructure in and around northeastern China and Inner

Mongolia

|

Delivery

of our supplies depends on the smooth passage of commercial cargo through the

railways, highways and waterways in and around northeastern China and Inner

Mongolia. Transportation infrastructure in and around northeastern China and

Inner Mongolia may suffer more breakdowns and offer fewer alternative routes

than systems in many western countries.

|

|

§

|

Bad harvests

and severe weather could harm the agricultural production on which we

depend, prevent customers from reaching our stores and disrupt our power

supply

|

Severe

storms could also reduce supplies of fresh foods by destroying crops and

livestock and, in extreme cases, could reduce supplies of processed foods by

reducing overall availability of the agricultural raw materials from which they

are made, and cause shortages of, and price increases for, the affected

supplies.

Poor

yields of crops and livestock, whether due to bad weather, disease, errors in

agricultural planning or other causes, could reduce the market supplies of fresh

foods as well as processed foods that depend on agricultural products as raw

materials. Such reductions could raise the cost of our supplies and cause the

supply shortages.

|

|

§

|

Quality

control problems and operational difficulties among a small number of

suppliers

|

We rely

on suppliers to provide sufficient amounts of merchandise that meet our quality

standards and government health and consumer-protection standards. A significant

portion of our supplies (approximately 14.7% in 2008 and 9.1% in 2007) come from

our top 10 suppliers, which are primarily large wholesalers and meat processors.

We usually secure a primary vendor and a secondary vendor for each category of

merchandise by entering into standard contracts with them, which typically have

a term of one year and provide for payment at market prices. In case there are

merchandise shortages, we utilize the secondary vendor. If one or more of these

suppliers experiences quality control failures or is unable to secure its own

supply of merchandise, whether self-produced or purchased from others, the

merchandise that it delivers to us could fail to meet our or the government’s

quality standards or arrive in insufficient amounts to meet our needs. If such

risks do materialize, there is no guarantee we would succeed in securing

replacement supplies meeting our and the government’s standards from other

suppliers quickly and at reasonable prices, or at all, and we could suffer the

consequences of supply chain disruption described above.

Under our

supply contracts, our suppliers are responsible for damage that occurs during

shipping and, under the PRC’s consumer protection laws, our suppliers must

reimburse us for the cost of spoiled goods returned to us by customers for a

refund. Nevertheless, significant spoilage could reduce the amount of fresh food

we are able to offer, which could reduce our income.

6

|

|

§

|

Economic

conditions

|

Economic

conditions, in northeastern China in particular, affect the price and

availability of our supplies. Inflation in prices of agricultural products and

in general is a significant concern in China. If inflation develops and becomes

a significant problem, many retailers in China, including us, will have to

choose between increasing the prices we charge our customers and reducing the

profit margins on our sales. In either case, our competitive position and

operating results could be harmed, and the value of any investment in our common

stock could be reduced.

In

addition, the geographic concentration of our operations exposes us to the risks

of the local economy. We operate in northeastern China and Inner Mongolia, and

our near-term plans call for expansion only within the three provinces of

northeastern China and the eastern region of Inner Mongolia. Our headquarters,

warehouses and distribution facilities and all of our stores are located within

a relatively limited geographic area. As a result, our business is more

susceptible to regional conditions, including conditions affecting

infrastructure, agriculture, inflation and employment, than our more

geographically diversified competitors.

The

supermarket industry in the PRC is becoming increasingly competitive and, unless

we are able to compete effectively with domestic and foreign retailers, and

restaurants and fast food chains, our profits could suffer.

The

supermarket industry in the PRC is highly and increasingly competitive. Giant

international retailers such as Wal-Mart and Carrefour have entered the market,

national retailers such as Bailian and Lianhua have expanded, and local and

regional competition has grown. Some of these companies have substantially

greater financial, marketing, personnel and other resources than we

do.

Our

competitors could adapt more quickly than we do to evolving consumer preferences

or market trends, have more success than we do in their marketing efforts,

control supply costs and operating expenses more effectively than we do, or do a

better job than we do in formulating and executing expansion plans. Increased

competition may also lead to price wars, counterfeit products or negative brand

advertising, all of which may adversely affect our market share and profit

margins. Expansion of large retailers into new locations may limit the locations

into which we may profitably expand. To the extent that our competitors are able

to take advantage of any of these factors, our competitive position and

operating results may suffer.

We also

face heightened competition from restaurants and fast food chains, which are

capturing an increasing portion of household food expenditures in the

PRC.

Because

we face intense competition, we must anticipate and quickly respond to changing

consumer demands more effectively than our competitors. In order to succeed in

implementing our business plan, we must achieve and maintain favorable

recognition of our private label brands, effectively market our products to

consumers, competitively price our products, and maintain and enhance a

perception of value for consumers. We must also source and distribute our

merchandise efficiently. Failure to accomplish these objectives could impair our

ability to compete successfully and adversely affect our growth and

profitability.

Our

limited operating history makes it difficult to evaluate our future prospects

and results of operations; our business could fail, and you could lose some or

all of your investment.

We have a

limited operating history and the PRC supermarket industry is young and

continually growing. Accordingly, you should consider our future prospects in

light of the risks and uncertainties experienced by early-stage companies in

evolving markets. Some of these risks and uncertainties relate to our ability

to:

|

§

|

Offer new products to attract and

retain a larger customer

base;

|

|

|

|

|

§

|

Respond to competitive and

changing market conditions;

|

|

|

|

|

§

|

Maintain effective control of our

costs and expenses;

|

7

|

§

|

Attract additional customers and

increase spending per

customer;

|

|

§

|

Increase awareness of our brand

and continue to develop customer

loyalty;

|

|

§

|

Attract, retain and motivate

qualified personnel;

|

|

§

|

Raise sufficient capital to

sustain and execute our expansion

plan;

|

|

§

|

Respond to changes in our

regulatory environment;

|

|

§

|

Manage risks associated with

intellectual property rights;

and

|

|

§

|

Foresee and understand long-term

trends.

|

Because

we are a relatively new company, we may not be experienced enough to address all

the risks in our business or in our expansion plan. If we are unsuccessful in

addressing any of these risks and uncertainties, our business may

fail.

Our

internal control over financial reporting and our disclosure controls and

procedures have been ineffective, and failure to improve them could lead to

future errors in our financial statements that could require a restatement or

untimely filings, which could cause investors to lose confidence in our reported

financial information, and a decline in our stock price.

In

connection with the preparation and audit of our 2009 financial statements and

notes, we were informed by our auditor, BDO China Li Xin Da Hua CPA Co. Ltd.

(“BDO”) of certain deficiencies in our internal controls that BDO considered to

be material weaknesses. These deficiencies related to our financial closing

procedures and errors in classification of warrants. After discussions between

management, our audit committee and BDO, we concluded that the Company had

improperly classified warrants pursuant to FASB ASC Topic 815 “Derivatives and

Hedging”) (“ASC 815”). As a result of the reclassification, the Company

recognized a $35.5 million loss for the year ended December 31,

2009.

In

addition, as a result of the reclassification, on March 31, 2009 our audit

committee met with BDO and made a determination that the Company’s financial

statements in each of its quarterly reports filed in 2009 could not be relied on

that it will restate the Company’s financial statement for each of the quarterly

reports it filed in 2009. The Company filed a current Report on Form 8-K

disclosing these determinations under Item 4.02 of Form 8-K concurrent with the

filing of its Annual Report on Form 10-K for the fiscal year ended December 31,

2009 (“Annual Report”) and filed amended 10-Qs on May 17, 2010.

As

required by Rule 13a-15 promulgated under the Exchange Act, in connection with

the filing of our Annual Report, our management, including our chief executive

officer and chief financial officer, evaluated the effectiveness of the design

and operation of our disclosure controls and procedures (as defined in Rule

13a-15(e) and 15d-15(e) promulgated under the Exchange Act) as of December 31,

2009 and determined that our disclosure controls and procedures were not

effective as of such date. This conclusion was based on the fact that on

December 30, 2009, we entered into an agreement to acquire a building for use as

our new headquarters. Pursuant to Item 1.01 of Form 8-K under the Exchange Act,

we should have filed a current report on Form 8-K disclosing the agreement by

January 6, 2010, but we did not file such current report until January 25,

2010.

As a

result of the material weakness in our internal controls and the ineffectiveness

of our disclosure controls and procedures described above, current and potential

stockholders could lose confidence in our financial reporting, which would harm

our business and the trading price of our stock.

Economic

conditions that affect consumer spending could limit our sales and increase our

costs.

Our

results of operations are sensitive to changes in overall economic conditions

that affect consumer spending, including discretionary spending. Inflation and

adverse changes to employment levels, business conditions, interest rates,

energy and fuel costs and tax rates can, in addition to causing the supply chain

cost challenges described above, reduce consumer spending and change consumer

purchasing habits.

8

As of

the date of this prospectus, we have not been significantly negatively impacted

by the economic downturn in the PRC. The recession in the PRC to date has mainly

impacted the export sector based in southeastern China. Northeastern China and

Inner Mongolia, where our stores are located, have not been affected to the same

extent. Should the economic downturn worsen and spread to northeastern China and

Inner Mongolia, where we are based, a general reduction in the level of consumer

spending in the region would likely result, which would reduce our sales

revenues and profits.

Much

of our income comes from sales of perishable merchandise, which can lose its

value quickly; such losses could harm our operating results.

We could

suffer spoilage if supply chain disruptions occur, if our refrigerators and

freezers malfunction or if we suffer lapses of quality control inspection and

supervision. If our inspections fail to discover spoilage in a shipment of fresh

food or if we fail to routinely inspect perishable merchandise on our shelves,

we could inadvertently offer spoiled food for sale, which could harm our

reputation, competitive position and operating results. Moreover, if we fail to

accurately predict future customer demand for perishable food, we would be

forced to discard unsold perishable food once it spoils, which would also

negatively affect our operating results.

Consumer

concerns regarding the safety and quality of food products or health concerns

could adversely affect sales of our high-margin products, which would negatively

impact our profits.

Our sales

results could be harmed if consumers lose confidence in the safety and quality

of our fresh food products. Consumers in the PRC are becoming increasingly

conscious of food safety and nutrition. Consumer concerns about, for example,

the safety of meat, fish, or dairy products, or about the safety of food

additives used in processed food products, could discourage them from buying

these relatively high-margin products and cause our profit margins to fall and

our results of operations to suffer.

We

rely on the performance of our individual stores, individual store managers,

three regional managers and our operating director for our sales, and should any

or all of them perform poorly for any reason, our sales results, reputation and

competitive position would suffer.

We sell

all of our products through our individual stores. Each supermarket is managed

by a store manager who reports directly to one of our three regional managers.

Each regional manager manages around 10 stores and reports to our operating

director, who reports to our COO, Mr. Alan Stewart. Regional managers spend

their time in stores to work together with each individual store manager. Each

region holds teleconferences every week. Although all purchasing decisions as to

vendors and costs are made by company management and not store managers, the

store manager makes the decision as to order quantities and is responsible for

the daily operation of the store. If factors either in or out of a store

manager’s control reduce a store’s business — for example, disruption of

customer traffic by nearby construction or customer dissatisfaction with store

employees — the individual store’s income could fall, which would negatively

impact our sales. Also, if our managers and operating director fail to

adequately manage store employees and day-to-day operations in a manner that

pleases our customers, our reputation and competitive position will

suffer.

We

may fail to identify or anticipate trends in consumer preferences, which could

result in decreased demand for our merchandise, and lower revenues and

profits.

Our

continued success in the retail market depends on our ability to anticipate the

changing tastes, dietary habits and lifestyle preferences of customers. If we

are not able to anticipate and identify new consumer trends and stock our

shelves accordingly, our sales may decline and our operating results may be

adversely affected. For example, we believe meat and dairy products have strong

growth potential in northeastern China and Inner Mongolia. Accordingly, we have

increased our focus on sales of these products, which tend to have higher profit

margins than our other products. If the market for these products in the PRC

does not grow as we expect, our income may not grow as we expect and our

operating results may suffer.

9

Our

profit margins could narrow and as a result the value of any investment in our

common stock could be reduced.

Profit

margins in the grocery retail industry are narrow. In order to increase or

maintain our profit margins, we are developing strategies to reduce costs by

attempting to increase efficiencies and increase sales of higher-margin items

such as private label merchandise, prepared-in-store foods, and meat and dairy

products, but we can offer no assurance that such strategies, or our execution

of such strategies, will be successful. We also implement promotional price

reductions as part of our competitive strategy that may further affect our

profit margin. Thus, there is no guarantee that our current profit margin will

not decline, which would negatively impact our profitability.

We

rely heavily on information technology systems, which could fail, causing damage

to our operations.

We have a

large and complex information technology system that we rely on to keep track of

inventory and sales, determine our ordering of supplies, and communicate among

stores, our distribution center and our corporate headquarters. Like any

electronic data management system, ours is subject to malfunction. In such a

case, our operations could be significantly disrupted as we work to fix the

problem, upgrade our system or adopt a new system.

In

addition, despite our efforts to secure our computer network, the security of

our network could be compromised, confidential information could be

misappropriated and other system disruptions could occur. This could lead to

loss of sales and diversion of corporate resources from operations and

planning.

If

we have difficulties finding and leasing new retail space for new stores or

retaining existing retail space, our operations could be disrupted and we will

be unable to grow as planned, which would negatively affect our stock

price.

We

currently lease the majority of our store locations. Typically our supermarket

leases have initial 10- to 20-year lease terms and may include renewal options

for up to an additional 10 or 20 years. Our revenues and profitability would be

negatively impacted if we are unable to renew these leases at reasonable

rates.

Under our

expansion plan, in 2009 we opened seven new stores that have, in the aggregate,

approximately 32,000 square meters of space and, in 2008, we opened 10 new

stores that have, in the aggregate, approximately 42,000 square meters of space.

Our success in executing our expansion plan depends on our ability to open or

acquire new stores in existing and new retail areas and to operate these stores

successfully. We may also choose to continue to expand through acquisitions. We

must find suitable locations for those stores and reach reasonable terms with

building owners and other interested parties, which could be difficult as we

face intense competition from other retailers for such sites. If we cannot find

suitable locations at a reasonable cost, our ability to grow will be

compromised, which would negatively affect our stock price.

Our

insurance coverage may be inadequate and, if any of the products we sell causes

personal injury or illness, we could be exposed to significant losses resulting

from negative publicity and harm to our reputation. This exposure could harm our

business.

The sale

of food products for human consumption involves an inherent risk of injury to

consumers. Such injuries may result from tampering by unauthorized third

parties, contamination, including by bacteria, insecticides, fertilizers and

other substances, spoilage and mislabeling. Although we and our suppliers are

subject to governmental inspections and regulations, consumption of our products

could still cause a health-related illness in the future and we could be subject

to claims or lawsuits relating to such events. Under certain circumstances, we

could be required to recall products. Unlike most supermarket companies in the

United States, but in line with industry practice in the PRC, we do not maintain

product liability insurance, and we cannot predict the extent of liability we

could face if such events were to occur.

10

Although

the standard contracts we sign with our suppliers include a provision that

shifts liability to our suppliers if a consumer is injured by a supplier’s

product, the negative publicity surrounding any assertions that merchandise we

carry caused personal injury or illness could adversely affect our reputation

and competitive position. In addition, our property and equipment insurance does

not cover the full value of our property and equipment, which leaves us with

exposure in the event of loss or damage to our properties. Except for property,

accident and automobile insurance, we do not have other insurance such as

business liability or disruption insurance coverage for our operations in the

PRC.

We do not

maintain a reserve fund for potential warranty or defective products claims. If

we experience an increase in warranty claims or if our repair and replacement

costs associated with warranty claims increase significantly, our results of

operations and financial condition would suffer.

Our

company name and private label merchandise may be subject to counterfeiting or

imitation, which could damage our reputation and brand image, and lead to higher

administrative costs.

We regard

brand positioning as an important element of our competitive strategy, and

intend to position our private label brands to be associated with low prices,

high quality, convenience and a positive shopping experience. There have been

frequent occurrences of counterfeiting and imitation of products in the PRC in

the past. Imitation of our company name or logo could occur in the future and

there is no guarantee that we will be able to detect it and deal with it

effectively. Any occurrence of counterfeiting or imitation could damage our

corporate and brand image.

If

we do not effectively manage our growth, our expansion efforts could fail, which

would negatively affect our stock price.

There is

no guarantee that our expansion plan will be successfully implemented. In order

to fully implement these plans, we will have to hire a large number of

additional employees, secure new retail locations, and integrate new stores and

distribution routes into our existing business. There is no guarantee that we

will meet all or any of these needs and therefore no guarantee that we will

succeed in our efforts to expand.

Moreover,

our future expansion will depend both on the profitability of our business and

our ability to raise capital from outside sources. We intend to finance our

expansion plan, which includes the opening of three additional stores during the

remainder of 2009, from funds generated from operations, bank loans, and

proceeds from this offering.

If our

business and markets grow and develop, it will be necessary for us to finance

and manage expansion in an orderly fashion. We may not have the requisite

experience to manage and operate a larger network of stores and distribution

centers. In addition, we may face challenges in integrating acquired businesses

with our own. These events would increase demands on our existing management,

workforce and facilities. Failure to satisfy these increased demands could

interrupt or adversely affect our operations and cause production backlogs,

longer product development time frames and administrative

inefficiencies.

If our

expansion plans are not fulfilled, our stock price will decline.

We

may not be able to hire and retain qualified personnel to support our growth and

if we are unable to retain or hire such personnel in the future, our ability to

implement our business objectives could be limited. Difficulties with hiring,

employee training and other labor issues could disrupt our

operations.

Our

operations depend on the work of nearly 3,900 employees. We may not be able to

retain those employees, successfully hire and train new employees or integrate

new employees into the programs and policies of the Company. Any such

difficulties would reduce our operating efficiency and increase our costs of

operations, and could harm our overall financial condition.

If one or

more of our senior executives or other key personnel are unable or unwilling to

continue in their present positions, we may not be able to replace them within a

reasonable time, and our business may be disrupted and our financial condition

and results of operations may be materially and adversely affected. Competition

for senior management and personnel is intense, the pool of qualified candidates

is very limited, and we may not be able to retain the services of our senior

executives or senior personnel, or attract and retain high-quality senior

executives or senior personnel in the future. This failure could limit our

future growth and reduce the value of our common stock.

11

We

may have difficulty establishing adequate management, legal and financial

controls in the PRC, which may result in a material misstatement of our annual

or interim consolidated financial statements.

Companies

in the PRC have not historically adopted a western style of management and

financial reporting concepts and practices, or a modern western style of

banking, computer and other control systems. We may have difficulty in hiring

and retaining a sufficient number of employees qualified in these areas to work

for our operating company in the PRC. As a result of these factors, we may

experience difficulty in establishing management, legal and financial controls,

collecting financial data, preparing financial statements, books of account and

corporate records, and instituting business practices relating to our PRC

operations that meet western standards. Any such difficulty could result in a

material misstatement of our annual or interim consolidated financial

statements.

We

could be required to pay liquidated damages to our investors under the

registration rights agreement entered into with our investors and such payment

could harm our financial condition.

On March

28, 2008, as part of a $15.5 million private placement, we entered into a

registration rights agreement (as amended on May 8, 2008) with certain

investors, pursuant to which we agreed to register for resale up to an aggregate

of 41,495,261 shares of common stock, including shares of common stock

underlying Series A Preferred Stock, Series A Warrants and Series B Warrants.

The registration rights agreement provided that if the initial registration

statement required to be filed thereunder was not declared effective by

September 24, 2008, we would be required to pay certain liquidated damages to

the investors. On March 9, 2009, the investors party to the registration rights

agreement waived their right to such liquidated damages and on August 11, 2009,

the initial registration statement covering 2,070,836 shares of the total shares

registrable pursuant to the registration rights agreement was declared

effective. We were not able to register all of the 41,495,261 shares in the

initial registration statement due to limits imposed by the Securities Exchange

Commission’s interpretation of Rule 415 of Regulation C promulgated under the

Securities Act of 1933, as amended (the “ Securities Act ”

).

There are

additional deadlines we are required to meet if the private placement investors

request that we file one or more registration statements covering the remaining

shares that we are obligated to register pursuant to the registration rights

agreement. In the event that we are required to file an additional registration

statement to cover securities that we have previously been unable to register,

we will be required to file any such additional registration statement within 30

days of receipt of demand notice from certain of our stockholders. We will

further be required to have any such additional registration statement declared

effective within 150 days of its initial filing date, or 180 days from its

initial filing date in the event that the registration statement is given a full

review by the Securities and Exchange Commission. If we fail to meet one or more

of those deadlines, we would, in the absence of an additional waiver, be

required to pay the investors up to a maximum of $1,550,000 in liquidated

damages. Payment of a significant amount of liquidated damages would harm our

profitability and we may not have sufficient cash to pay them.

If

our lease agreements for certain stores are nullified due to title deficiencies

of our landlords, our business may be adversely affected.

The PRC

real property laws and regulations require landlord to be the legal owner of the

relevant leased properties, otherwise the lease agreement may be nullified. We

have not received or confirmed documentation evidencing our landlord’s legal

ownership for 14 of our stores. If any of these landlords do not legally own the

leased properties, the actual legal owners could force the affected stores to

relocate and operation of the stores concerned may be temporarily terminated

until such stores are relocated.

In

addition, the PRC real property laws and regulations require landlords to obtain

prior consent from the legal owner of the relevant leased properties before the

execution of any sublease agreements; otherwise the sublease agreement may be

nullified if the legal owner refuses to rectify his consent. We have not

independently confirmed whether consents authorizing our subleases for our

supermarkets and distribution centers have been obtained. If the legal owners of

the stores claim that the subleases were invalid, operation of the supermarkets

or distribution centers concerned may be terminated until the supermarkets or

distribution centers are relocated.

12

Some

of our stores may not be in full compliance with legal requirement on their

sector approvals and business licenses and may therefore be subject to

punishment imposed by the relevant PRC authorities.

The PRC

laws and regulations require that store operators obtain a Public Site Hygiene

License and, if applicable, a Food Hygiene License if there are edible products

being processed or distributed in the store. Store operators are also required

to indicate “store operation” on the Public Site Hygiene License and to specify

each category of edible product (i.e., vegetables, fresh seafood, etc.)

distributed. Failure to do so may expose the store to administrative punishments

imposed by the relevant government authorities. Punishments include

administrative penalty up to RMB20,000 (approximately US$3,000), confiscation of

income generated from the excluded business items and, in extreme cases,

revocation of the business license of the violating store.

Several

of our stores have either not obtained the Public Site Hygiene License or are

distributing edible products without specifying the product category on their

Food Hygiene License. Such stores may be subject to sanction as discussed above,

which may be imposed at the sole discretion of PRC authorities.

In

addition, several of our stores are distributing products salt, alcohol,

audio-video products and tobacco which are not permitted on their business

license. While such stores have not been sanctioned for such discrepancy, we

cannot guaranty that the relevant PRC authority will not impose administrative

penalties on such stores in the future, which penalties could be up to

RMB100,000 (approximately US$15,000) per store.

We

are not current in our payment of social insurance and housing accumulation fund

for our employees and such shortfall may expose us to relevant administrative

penalties.

The PRC

laws and regulations require all the employers in China to fully contribute

their own portion of the social insurance premium and housing accumulation fund

for their employees within a certain period of time. Failure to do so may expose

the employers to make rectification for the accrued premium and fund by the

relevant labour authority. Also, an administrative fine may be imposed on the

employers as well as the key management members. Speedy Brilliant (Daqing),

QKL-China and QT&C have failed to fully contribute the social insurance

premium and housing accumulation fund. Therefore, they may be subject to the

administrative punishment as mentioned above.

Risks

Related to Our Corporate Structure

We

control QKL-China through a series of contractual arrangements, which may not be

as effective in providing control over the entity as direct ownership and may be

difficult to enforce.

We

operate our business in the PRC through our variable interest entity, QKL-China.

QKL-China holds the licenses, approvals and assets necessary to operate our

business in the PRC. We have no equity ownership interest in QKL-China and rely

on contractual arrangements with QKL-China and its shareholders that allow us to

substantially control and operate QKL-China. These contractual arrangements may

not be as effective as direct ownership in providing control over QKL-China

because QKL-China or its shareholders could breach the

arrangements.

Our

contractual arrangements with QKL-China are governed by PRC law and provide for

the resolution of disputes through arbitration in the PRC. Accordingly, these

contracts would be interpreted in accordance with PRC law and any disputes would

be resolved in accordance with PRC legal procedures. If QKL-China or its

shareholders fail to perform their respective obligations under these

contractual arrangements, we may have to

|

§

|

incur substantial costs to

enforce such arrangements,

and

|

|

|

|

|

§

|

rely on legal remedies under PRC

law, including seeking specific performance or injunctive relief, and

claiming damages.

|

The legal

environment in the PRC is not as developed as in the United States and

uncertainties in the Chinese legal system could limit our ability to enforce

these contractual arrangements. In the event that we are unable to enforce these

contractual arrangements, our business, financial condition and results of

operations could be materially and adversely affected.

13

If

the PRC government determines that the contractual arrangements through which we

control QKL-China do not comply with applicable regulations, our business could

be adversely affected.

Although

we believe our contractual relationships through which we control QKL-China

comply with current licensing, registration and regulatory requirements of the

PRC, we cannot assure you that the PRC government would agree, or that new and

burdensome regulations will not be adopted in the future. If the PRC government

determines that our structure or operating arrangements do not comply with

applicable law, it could revoke our business and operating licenses, require us

to discontinue or restrict our operations, restrict our right to collect

revenues, require us to restructure our operations, impose additional conditions

or requirements with which we may not be able to comply, impose restrictions on

our business operations or on our customers, or take other regulatory or

enforcement actions against us that could be harmful to our

business.

The

controlling shareholders of QKL-China have potential conflicts of interest with

us, which may adversely affect our business.

The

controlling shareholders of QKL-China are also beneficial holders of our common

shares. They are also directors of both QKL-China and us. These shareholders

hold a larger interest in QKL-China when compared to their beneficial ownership

in our shares. Conflicts of interest between their dual roles as shareholders

and directors of both QKL-China and us may arise. We cannot assure you that when

conflicts of interest arise, any or all of these individuals will act in the

best interests of the Company or that conflicts of interest will be resolved in

our favor. In addition, these individuals may breach or cause QKL-China to

breach or refuse to renew the existing contractual arrangements that allow us to

receive economic benefits from QKL-China. Currently, we do not have existing

arrangements to address potential conflicts of interest between these

individuals and our company. We rely on these individuals to abide by the laws

of the State of Delaware, which provide that directors owe a fiduciary duty to

the Company, and which require them to act in good faith and in the best