Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - MOSAIC CO | d8k.htm |

The Mosaic

Company Goldman Sachs Fifteenth Annual Agricultural Biotech Forum

February 9, 2011

Larry Stranghoener

Executive Vice President and Chief Financial Officer

Exhibit 99.1 |

| Good morning everyone. I’m delighted to have the opportunity

to speak with you today about Mosaic, our strong market

position

in

both

potash

and

phosphate

and

the

outstanding

long-term

outlook

for

the

crop

nutrient

industry.

We’d like to thank Bob Koort

and Lindsey Drucker

Mann

for coverage of the sector and sponsoring this conference.

This is a great time to be in the ag

business. The world needs crop nutrients to meet food demand and Mosaic is

positioned to capitalize on this long-term opportunity.

|

This presentation

contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Such

statements include, but are not limited to, statements about future strategic plans and other

statements about future financial and operating results, including statements about the

proposed split-off by Cargill, Incorporated of its equity interest in The Mosaic Company and related

transactions

(the

“Split-Off”),

the

terms

and

effects

of

the

proposed

Split-Off,

the

nature

and

impact

of

the

proposed

Split-Off

and

benefits

of

the proposed Split-Off. Such statements are based upon the current beliefs and expectations

of The Mosaic Company’s management and are subject to significant risks and

uncertainties. These risks and uncertainties include but are not limited to risks and uncertainties arising

from the predictability and volatility of, and customer expectations about, agriculture, fertilizer,

raw material, energy and transportation markets that are subject to competitive and other

pressures and economic and credit market conditions; the level of inventories in the

distribution channels for crop nutrients; changes in foreign currency and exchange rates;

international trade risks; changes in government policy; changes in environmental and other

governmental regulation, including greenhouse gas regulation and implementation of the U.S.

Environmental

Protection

Agency’s

numeric

water

quality

standards

for

the

discharge

of

nutrients

into

Florida

lakes

and

streams;

further

developments in the lawsuit involving the federal wetlands permit for the extension of the

Company’s South Fort Meade, Florida, mine into Hardee

County,

including

orders,

rulings,

injunctions

or

other

actions

by

the

court

or

actions

by

the

plaintiffs,

the

Army

Corps

of

Engineers

or

others

in

relation

to

the

lawsuit,

or

any

actions

the

Company

may

identify

and

implement

in

an

effort

to

mitigate

the

effects

of

the

lawsuit;

other

difficulties

or

delays

in

receiving,

or

increased

costs

of,

or

revocation

of,

necessary

governmental

permits

or

approvals;

the

effectiveness of the Company’s processes for managing its strategic priorities; adverse weather

conditions affecting operations in Central Florida

or

the

Gulf

Coast

of

the

United

States,

including

potential

hurricanes

or

excess

rainfall;

actual

costs

of

various

items

differing

from

management’s current estimates, including, among others, asset retirement, environmental

remediation, reclamation or other environmental obligations, or Canadian resource taxes and

royalties; accidents and other disruptions involving Mosaic’s operations, including brine

inflows at its Esterhazy, Saskatchewan, potash mine and other potential mine fires, floods, explosions, seismic events or

releases of hazardous or volatile chemicals; the possibility that the expected timeline for the

proposed Split-Off may be delayed or the proposed Split-Off may not occur, or that

there may be difficulties with realizing the benefits of the proposed Split-Off; and other risks and

uncertainties reported from time to time in The Mosaic Company’s reports filed with the

Securities and Exchange Commission. Actual results may differ from those set forth in the

forward-looking statements. Safe Harbor Statement

2 |

| Before I proceed, I would like to remind you that our presentation

contains forward-looking statements. The statements include, but

are not limited to, statements about future financial and operating results. They are based upon

management’s beliefs and expectations as of today’s date, February 9, 2011

and are subject to significant risks and uncertainties. Actual results

may differ materially from those projected in the forward-looking statements. Additional

information concerning factors that could cause actual results to differ materially

from those in the forward-looking statements is included in our reports

filed with the Securities and Exchange Commission. |

In connection with

the proposed Split-Off, a registration statement on Form S-4 that has been filed with the

Securities and Exchange Commission includes a preliminary proxy statement/prospectus for the

stockholders of The Mosaic Company.

The Mosaic Company will mail the final proxy statement/prospectus to its

stockholders.

INVESTORS AND SECURITY HOLDERS ARE ADVISED TO READ THE PROXY STATEMENT

WHEN IT BECOMES AVAILABLE. IT WILL CONTAIN IMPORTANT INFORMATION.

Investors and security

holders may obtain a free copy of the proxy statement (when available) and other documents filed by

The Mosaic Company at the Securities and Exchange Commission’s web site at

http://www.sec.gov. Certain Information Regarding Participants:

The Mosaic Company and its directors, executive officers and other members of its management and

employees may be deemed to be participants in the solicitation of proxies from its

stockholders in connection with the proposed Split-Off.

Information concerning the interests of The Mosaic Company’s participants in the

solicitation is set forth in The Mosaic Company’s proxy statements and Annual Reports on Form

10-K, previously filed with the Securities and Exchange Commission, and in the proxy

statement relating to the Split- Off when it becomes available.

Important Information

3 |

| Slide three summarizes important information about the proxy

statement/prospectus that we have filed with the SEC in preliminary form and

that you should read when available in final form. |

Introduction

•

Strategic overview

–

Mosaic is the leading P&K company in the world

–

Orderly distribution of shares held by Cargill

•

Business overview

–

Potash growth through expansions

–

Largest

integrated

phosphate

producer

–

low

cost

and geographic advantage

•

Market outlook

–

Crop nutrient markets extremely tight due to a

variety of supply and demand factors

–

Healthy farmer economics support continued

investment in crop nutrients

4 |

| This morning I will first review Mosaic’s strategy. We are

very upbeat about the long-term fundamentals of our business and continue

to position ourselves for the growth of this sector. I’ll also provide a

brief overview of the recently announced plan to work with Cargill for an orderly distribution of its

Mosaic shares.

Next, I will review each of our two business lines.

Finally, I will discuss our market outlook and today’s favorable

conditions. |

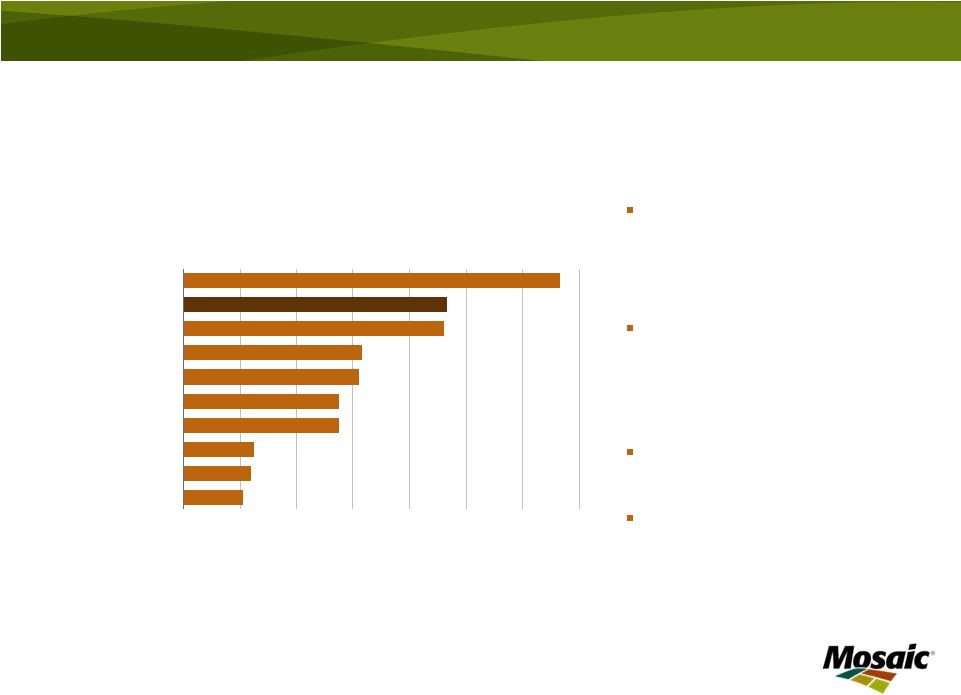

Leader in Potash and

Phosphate 5

Source: IFA, company reports and Mosaic estimate

WORLD’S LARGEST P&K COMPANIES

0

1

2

3

4

5

6

7

8

9

Mosaic

PotashCorp

Belaruskali

Israel Chemicals

OCP

K+S

Silvinit

Uralkali

GCT

Yuntianhua

MILLION TONNES PRODUCTION, 3 YEAR AVERAGE

K2O

P2O5 |

| As the leading producer of potash and phosphate, there is no company

better positioned to capture the growth in crop nutrient markets.

Farmers need to plant record areas and harvest ever increasing yields to meet the

world’s accelerating appetite for grains and oilseeds. That

implies strong growth in global crop nutrient markets. Strong

agricultural markets have contributed to high demand for our products. This comes at a time when producer

inventories are low and there are growing supply concerns.

|

Strategic

Overview As a global leader in crop nutrients, Mosaic

is positioned to benefit from attractive long-

term agricultural fundamentals:

Potash –

grow volume

–

Brownfield expansion program

Phosphates –

grow value

–

Leverage scale and geographic location

–

Extend phosphate reserves

Global

distribution assets aligned with

production

6 |

| At

Mosaic,

our

focus

is

on

shareholder

value

creation,

driven

by

the

attractive

fundamentals

of

our

business.

Our

mission

is

to

help

the

world

grow

the

food

it

needs.

We

run

our

business

with

a

long-term

view

–

and

this

view

is

compelling!

We

are

executing

well

on

our

strategy.

In

Potash,

we

are

growing

volume

by

pursuing

brownfield

expansion

opportunities. In Phosphates, we are focusing on growing the value of our

business and maintaining our position as one of the lowest cost phosphate

producers in the world. Our expansive global distribution network, aligned with our

North American production assets, provides us access to the largest global markets

on a counter seasonal basis. Over time, the combination of two strong product

lines has produced great returns for our shareholders. Our balanced

portfolio of both potash and phosphate gives more stability to our sales volumes

and cash flow than single nutrient focused companies.

|

Transaction

Benefits Enhances long-term strategic and financial flexibility by facilitating exit

of majority shareholder

Increases Mosaic’s public float –

improving attractiveness of stock

Greater stock liquidity, removes Cargill overhang, satisfies public float criteria for

potential future inclusion in S&P 500 index

Number

of

outstanding

shares

unchanged;

no

dilution

to

earnings

per

share

Robust balance sheet remains intact and operations unchanged

7

Mosaic well positioned to capture

positive industry fundamentals |

| As most of you know, Mosaic and Cargill recently agreed to a transaction

that will result in the distribution of Cargill’s 64% stake in Mosaic to

Cargill’s shareholders and debt holders. This transaction will enhance

Mosaic’s long-term strategic and financial flexibility by facilitating the exit of our majority

shareholder.

This transaction came about because of Cargill’s desire to maintain its

private company status while meeting the diversification and distribution

needs of charitable trusts formed through the estate planning of one of Cargill’s largest

shareholders.

The release of these shares will increase Mosaic’s liquidity and public

float. We will also satisfy the 50% public float requirement for

potential inclusion in the S&P 500 index. Note

that

there

will

be

no

change

to

the

number

of

shares

or

the

economic

rights

associated

with

those

shares.

The

transaction has been designed to ensure an orderly distribution and to minimize

disruption to the market. There is significant

investor

interest

in

our

sector

and

we

believe

ample

demand

exists

to

expand

our

shareholder

base.

Finally, this

transaction

will

not

have

any

impact

on

operations

and

our

balance

sheet

will

remain

intact. |

Cargill’s

286

million

Mosaic

shares

will

be

recapitalized

into

three

new

classes

to

comply

with

IRS

rules

regarding tax free split-offs. Cargill will then distribute all shares to debt holders and

participating Cargill shareholders in a split off transaction.

Recapitalization and Split-Off

8

Amount of shares to be exchanged with Cargill shareholders and debt holders represent estimates

|

| Now, let me give you a very brief overview of the transaction.

The distribution will take place in three steps. Slide seven

illustrates the first two steps. Slide eight summarizes the third

step. First, Mosaic will recapitalize its shares into three classes. Of

Cargill’s 286 million shares, an estimated 179 million will be

converted into Class A and Class B restricted shares. These shares will have the same economic rights as common

shares but will be subject to transferability restrictions. To comply with

tax rules regarding tax free split offs, the Class B shares will be high

vote shares solely with respect to the election of directors. The Class B shares can be converted

to Class A shares at the discretion of Mosaic’s Board of Directors post

closing. Next, Cargill will exchange its Mosaic shares with its debt holders,

the charitable trusts and other Cargill shareholders in a split off

transaction. |

Orderly

Distribution 9

Formation Offerings

Post –

Formation Offerings

Up to approximately 107 million shares

from debt/equity exchange, 49.5 million

shares from Charitable Trusts.

Offerings to take place within 15 months

after closing

Beginning 2 ½

years from closing, 1/3

shares remaining after formation offerings

held by Charitable Trusts and other Cargill

shareholders become eligible to be

distributed annually

Closing

6-9 months

<15 months

2.5 years

3.5 years

4.5 years

Initial

Formation

Offering

Second

Formation

Offering

Additional

offerings until

157 million

shares sold

Released

share offering

Released

share offering

Released

share offering

Amount of shares to be exchanged with Cargill shareholders and debt holders represent estimates

|

| In the third step, we have planned for an orderly distribution of all 286

million shares to occur over the next several years. These shares will

be distributed to the public markets in a series of registered secondary offerings.

The first offering, which we expect to be the largest, will occur at the closing of

the recapitalization and split off. We anticipate closing will take

place in the second calendar quarter of this year. Remaining shares may be made available

in

a

series

of

offerings

designed

to

minimize

disruptions

to

the

market.

A

total

of

up

to

157

million

shares

will

be

distributed within the first 15 months from closing.

In summary, this transaction will give us a freer hand to control our own

destiny. We will all benefit from the long-term strategic

and

financial

flexibility

that,

as

a

fully

independent

company,

will

enable

us

to

capitalize

on

the

dynamic

crop

nutrient environment in which we operate.

Now, I would like to move to a review of our phosphate and potash businesses before

I finish with an overview of the market. |

MURIATE OF POTASH CAPACITY

MILLION TONNES KCL

0

2

4

6

8

10

12

14

PotashCorp

Mosaic

Belaruskali

Silvinit

ICL

Uralkali

K+S

Qinghai

APC

Agrium

A Leading Global Potash Producer

10

World capacity

approximates 74 million

tonnes

(all potash

products)

Mosaic FY10 MOP

production share

–

12% Global

–

38% North America

World scale & efficient

operations

Brownfield expansions

underway

Peaking capacity for PotashCorp, Mosaic and K+S

Source: Fertecon, Mosaic |

| First, let’s talk about potash.

Mosaic

is

one

of

the

world’s

top

producers

of

potash

with

an

estimated

12%

of

global

market

share.

Potash

is

produced in only 14 countries in the world, and agricultural giants such as China,

India and Brazil depend on imports. |

Potash –

Grow Volume

Projected additional annual capacity of 5.1

million tonnes

Multiple projects spanning a decade

Reversion of 1.3 million tonnes

currently

produced for a third party under a tolling

agreement expected soon

11 |

| The

world

will

need

substantially

more

potash

this

decade.

In

the

long

term,

we

forecast

demand

growth

of

3.5

–

4%

per year.

We

believe

the

best

way

to

meet

long-term

demand

growth

is

through

brownfield

expansions

at

existing

mine

sites.

Our

ongoing

expansions

in

Canada

are

expected

to

increase

annual

capacity

by

over

five

million

tonnes

by

2020,

ensuring

that

we

will

maintain

our

position

as

one

of

the

premier

potash

companies

in

the

world.

In

addition,

we

have

allocated

up

to

1.3

million

tonnes

of

annual

peaking

capacity

for

Potash

Corp

under

a

tolling

agreement. As many of you know, the expiration date for this agreement is the

subject of a dispute currently pending before

the

Saskatchewan

courts.

We

believe

that

our

obligation

to

provide

tonnes

to

PCS

ends

this

coming

summer,

at

which time these tonnes

revert to us. |

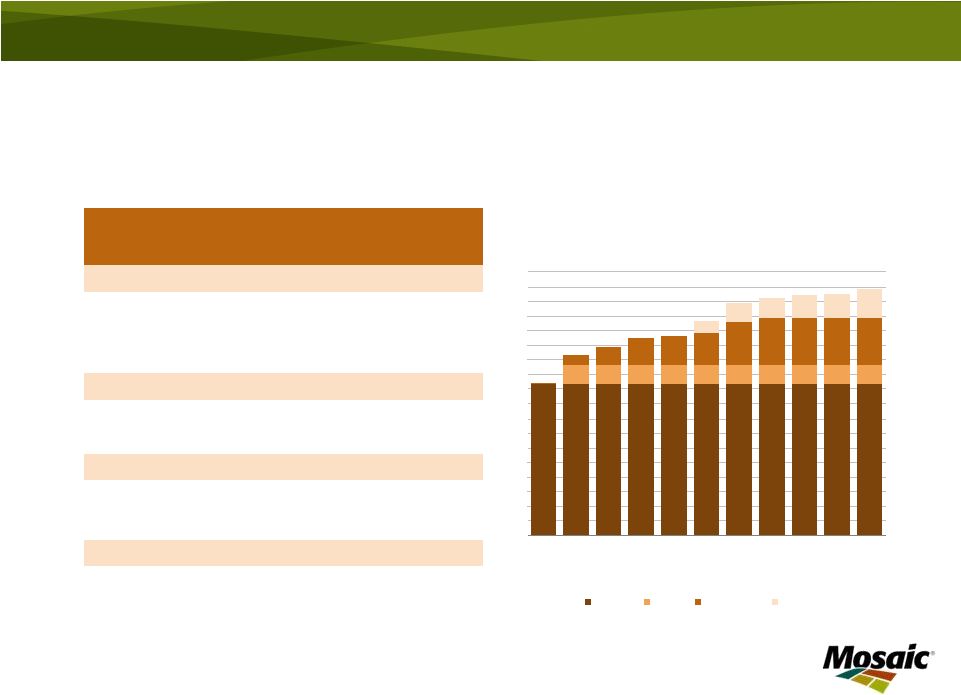

Potash Capacity

Expansions 12

PROJECTED CAPACITY

MILLION TONNES

0

2

4

6

8

10

12

14

16

18

2011

2013

2015

2017

2019

2021

FISCAL YEAR

Existing

Tolling

In progress

Future

INVESTMENT

($ IN BILLIONS)

PEAKING

CAPACITY

(MILLION TONNES)

ESTIMATED

CONSTRUCTION

COMPLETION

(FISCAL YEAR)

IN PROCESS

Belle Plaine

0.5

0.6

2012

Colonsay

0.7

0.7

2014

Esterhazy

2.0

1.8

2011-17

FUTURE

Belle Plaine

1.4

2016-19

Colonsay

0.6

2016

5.1

Tolling agreement

1.3

Capacity at May 31, 2010

10.4

16.8 |

| Our potash expansion program consists of nearly a dozen separate,

multi-year projects at our three Canadian mines. We have made good

progress on a number of these projects and we can adjust the pace of these projects in response

to supply/demand dynamics.

We expect this additional capacity to begin coming on-line over the next few

years. Within a decade, we expect our capacity to reach almost 17

million tonnes of finished product.

Our biggest project is the construction of the K3 shaft at Esterhazy. We are

currently drilling freeze holes and anticipate shaft sinking to begin

in calendar 2012. As our expansions come on line, we expect our

increased sales and production volumes to lead to lower per tonne

costs.

Our

industry

leadership,

together

with

our

investments

to

expand

capacity,

places

us

in

a

strong

competitive

position

to

leverage the growth of this market. |

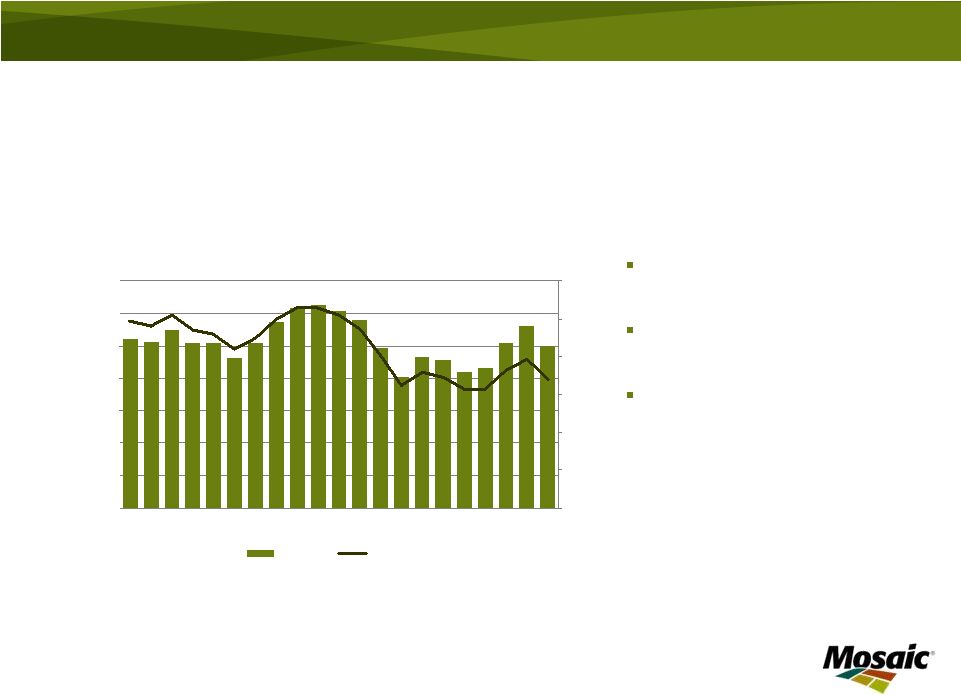

Rebounding Potash

Demand Positive potash market

fundamentals:

Producers running hard to

keep up

Lean inventories

Healthy farmer economics

Expect 2011 global

shipments of 53 to 56 million

tonnes

13

Source: Fertecon

and Mosaic

WORLD MOP DEMAND

MILLION TONNES

0

10

20

30

40

50

60

00

01

02

03

04

05

06

07

08

09

10F

11F

CALENDAR YEAR |

| Turning

to

demand,

the

potash

market

is

very

tight

and

we

expect

2011

global

shipments

to

rival

the

record

of

2007.

Producers are running hard to keep up with strong demand and inventories remain

low. The strong North American fall season was a catalyst for potash demand

and we see this trend continuing through this spring.

Export

prices

are

increasing

and

narrowing

the

gap

with

domestic

prices

as

demonstrated

by

the

recent

agreement between Canpotex

and our Chinese customers.

Lean

inventories,

solid

crop

prices

and

healthy

farmer

economics

all

point

to

a

great

future

for

potash.

As

we

bring

on

new

capacity

to

meet

increased

potash

demand

over

the

coming

years,

we

expect

the

higher

sales

volume from our Potash business to favorably contribute to our profitability and

company valuation. |

FINISHED PHOSPHATE CAPACITY

MILLION TONNES

0

2

4

6

8

10

Mosaic

YTH

OCP

Kailin

IFFCO

PhosAgro

Wengfu

GCT

Eurochem

Vale

Crop Nutrients

Feed

World’s Largest Phosphate Producer

World capacity

approximates 80 million

tonnes

(DAP/MAP/TSP)

Mosaic FY10 phosphate

production share

–

13% Global

–

56% North America

World scale & efficient

operations

Source: company reports, Mosaic

14 |

| Now, let’s move to phosphate.

Mosaic produces more phosphate crop nutrient and animal feed products than any other

company in the world by a wide margin. We rank among the lowest cost

producers in the industry today due to: •The tight vertical integration

of our phosphate rock mining and processing operations; •The large scale

of our mines and chemical plants; •The

important

location

advantages

we

have

from

being

situated

on

the

Gulf

of

Mexico

and

the

Mississippi

River;

•And, our international distribution business. |

Phosphates

– Grow

Value

Leverage scale and location

–

Low cost producer

–

Cost advantaged sulfur, competitive ammonia

–

Procurement leverage

Operational excellence

–

Maintenance practices

–

Capital deployment

–

Energy use and co-generation capacity

–

Improve coordination of sales and operations

planning

Grow MicroEssentials

®

sales

Extend phosphate reserves

15 |

| In order to strengthen our competitive advantage, we are focusing on four

strategic priorities for our Phosphates business:

First, we are working on several initiatives to leverage our scale and

geographic location. We have a strong competitive position due to

low rock and conversion costs as well as preferential geographic access to sulfur and

ammonia.

Next, we are focused on operational efficiency. We are implementing

improved processes for maintenance, capital deployment, energy use and

co-generation capacity. Our global sales and operations teams are working closely

together to optimize production planning in order to reduce operating costs.

Another highlight of our Phosphates segment is MicroEssentials

®

, a premium product that incorporates sulfur and other

micronutrients. We have over ten years of research trials demonstrating value

to famers through higher yields. We are on pace to sell over one

million tonnes this fiscal year and are converting existing capacity to

produce up to two million tonnes

annually.

Finally, we continue work to secure the mineral resource base for our U.S.

operations and to obtain advantaged access to rock reserves elsewhere in the

world. One recent example is our joint venture rock mine in Peru. As many of you

know, a permit needed to continue operations at our South Fort Meade mine is the

subject of a lawsuit. We are pursuing a number of strategies to

mitigate the impacts of this lawsuit. The process for the South Fort Meade permit

was robust and we believe it is not a matter of if we receive the permit, but

rather a matter of when. |

Record Phosphate

Demand Positive phosphate market

fundamentals:

Strong demand

Lean inventories

Healthy farmer economics

Expect 2011 global

shipments of 59 to 61 million

tonnes

16

Source: Fertecon

and Mosaic

WORLD PROCESSED PHOSPHATE DEMAND

MILLION TONNES

0

10

20

30

40

50

60

70

00

01

02

03

04

05

06

07

08

09

10F

11F

CALENDAR YEAR |

| Phosphate fundamentals are constructive and we expect the phosphate

market to remain snug for several years. In 2011, we expect record

demand coupled with supply uncertainties to keep this market tight during the remainder of this

fertilizer year.

Large shipments to both domestic and offshore destinations have tightened the global

phosphate market. Producer stocks remain at low levels and grain

prices have been supportive. Since

last

summer,

prices

have

rebounded

and

stayed

at

levels

around

$600

per

tonne

FOB

Tampa.

Now,

dealers

are

positioning product for the North American spring season.

We

forecast

processed

phosphate

demand

will

grow

to

a

record

59

to

61

million

tonnes

in

2011.

In addition to strong demand, several supply uncertainties are exacerbating the

situation. Questions about the Ma’aden startup in Saudi Arabia,

shut down of Agrifos and Fertiberia

phosphate operations, raw material uncertainty, changes in

China’s export duties and permit litigation at our own South Fort Meade mine

have all contributed to the tight market conditions.

|

Solid Financial

Position TOTAL CASH AND CASH EQUIVALENTS LESS DEBT*

$ IN BILLIONS

(3)

(2)

(1)

-

1

2

3

31-May-06

31-May-07

31-May-08

31-May-09

31-May-10

30-Nov-10

PERIOD END

17

*

See appendix for reconciliation of Cash and Cash Equivalents less Debt |

| As we have noted, our overall strategy is to capitalize on attractive

long-term agricultural fundamentals by investing in and reengineering our

Potash and Phosphate businesses. Through the ups and downs of the

markets we serve, we have created long-term value through sound capital allocation

decisions. Our strong cash flow has allowed us to build one of the strongest

balance sheets in the industry despite the economic downturn. We have

demonstrated our willingness and ability to make investments, to divest non-strategic

assets and to return cash to shareholders, as appropriate.

Our cash allocation priorities include investing in our business, maintaining a

large liquidity buffer, funding strategic opportunities, maintaining our

credit rating and distributing cash to shareholders. In addition, when

Cargill is no longer a majority shareholder, we will have additional flexibility as we evaluate M&A

opportunities and shareholder distributions. |

Accelerated Grain

and Oilseed Use 18

Disappointing global

harvests

Strong agricultural

commodity prices

Need to re-stock crop

nutrients in the

distribution pipeline and in

many farm fields

Source: USDA, lighter bars indicate recession years

WORLD GRAIN AND OILSEED PRODUCTION

AND USE

BILLION TONNES

1.8

2.0

2.2

2.4

2.6

2.8

00/01

02/03

04/05

06/07

08/09

10/11F

CROP YEAR

Use

Production |

| Let me finish with a few thoughts on the market outlook which look great

from any angle we can see. As you can see, grain and oilseed use has grown

slowly, but consistently. History has proven that economic

slowdowns

don’t

have

a

large

negative

impact

on

food

consumption

–

people

need

to

eat

regardless

of

the

economic

climate. The most recent global economic downturn was no exception.

On the production side, we have seen significant increases over the past three

years. This growth has come from increased harvested land and above

trend yields. However, we need to continue this above trend growth just to stay

even with projected use. |

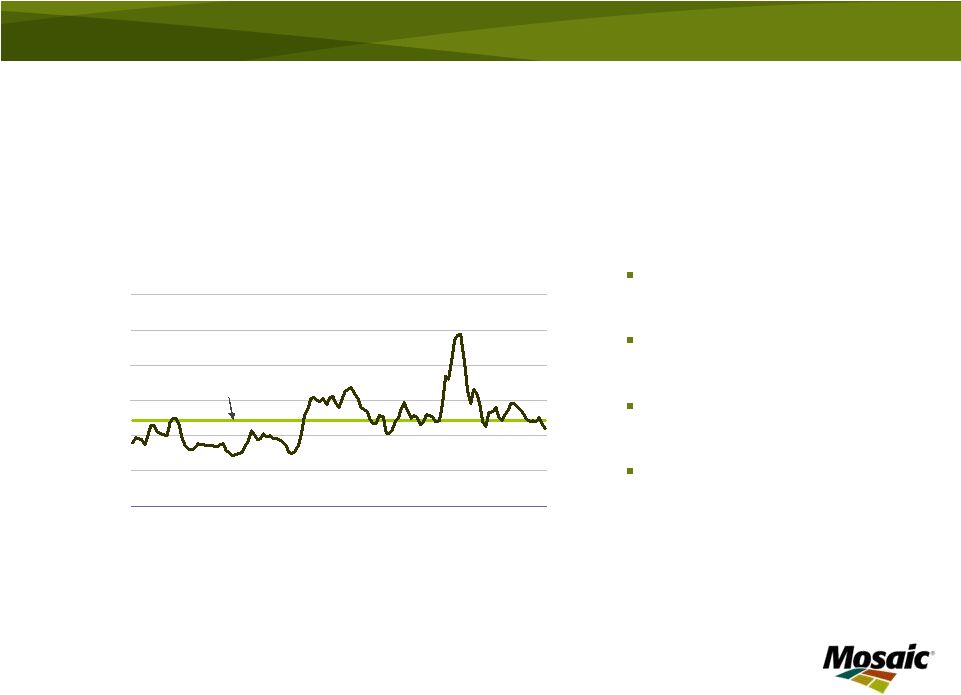

Stocks Remain at Low

Levels 19

Days of use remains at

low levels

Stocks still not at secure

levels

2011 new crop prices

signaling farmers to

expand planted area and

intensify cropping

practices

WORLD GRAIN AND OILSEED STOCKS

MILLION TONNES

0

100

200

300

400

500

600

700

90/91

94/95

98/99

02/03

06/07

10/11F

CROP YEAR

0

20

40

60

80

100

120

Stocks

Days of Use

DAYS OF USE

Source: USDA |

| Dramatic improvement in production has not translated into improving

stocks. World grain and oilseed stocks continue to remain at low

levels. We believe global grain and oilseed stocks still are not at levels secure enough to withstand

weather or other shocks over a period of time.

Over this past year, we have seen droughts in Russia and the Southern Cone, and

floods in Australia that have affected grain and oilseed production.

Corn

looks

especially

tight

at

only

56

days

of

use

estimated

for

the

end

of

this

crop

year.

That

is

the

second

lowest

ratio since the early 1970s. This ratio is even lower if you exclude India

and China which hold large strategic reserves. |

Farmer

Economics 20

CROP NUTRIENT AFFORDABILITY IN THE U.S

CROP NUTRIENT PRICE INDEX/CROP PRICE INDEX

0.0

0.5

1.0

1.5

2.0

2.5

3.0

2000

2002

2004

2006

2008

2010

CALENDAR YEAR

Average

Farmer profitability remains

at healthy levels:

Grain prices high relative

to historical prices

Input costs well below

their highs

Similar conditions for

cotton, rice and palm oil

China, Brazil and India

farm economics at, or

near, record levels

Crop Nutrient Price Index: NPK weighting based on US nutrient use from 2005/06 thru

2007/08, indexed to average prices in 2000 = 100

Crop Price Index: Crop price weighting based on Corn/Wheat/Soybean US acreage in

2007, indexed to average prices in 2000 = 100

Source: Mosaic |

| Another factor we keep an eye on is grain pricing. Farm

profitability remains at healthy levels. Grain prices are at relatively

high levels compared to historical prices. At the same time, farmer input costs have fallen

from their high levels of 2008 and 2009. This has allowed farmers to remain

profitable. The graph on this slide shows that the cost of crop nutrients,

relative to grain prices, is well within historic norms. Similar

conditions exist for other crops such as cotton, rice and palm oil. In

China,

Brazil

and

India,

farm

economics

are

at

record

or

near

record

levels

due

to

high

domestic

crop

prices

and,

in

the case of India, subsidized input costs. |

Key Points

Cargill distribution will give us additional

flexibility to pursue M&A and shareholder

distributions in the future

Potash brownfield

expansions on track to

add five million tonnes

additional capacity

Largest integrated phosphate producer –

low cost, geographic advantage and

expanding reserves

Confluence of supply and demand factors

keeping crop nutrient markets extremely

tight

Healthy farmer economics support

continued investment in crop nutrients

21 |

| Let me recap with a few key points.

First, Cargill’s exit as majority shareholder will give us additional

flexibility to pursue strategic opportunities and shareholder

distributions. We will ensure this exit is accomplished in an orderly manner.

Second, expected potash demand growth requires that we continue to expand our

production capacity. Third, we are the largest integrated phosphate producer

in the world. We have very low production costs, we have advantaged

access to raw materials through our location on the US Gulf coast, and, we are expanding our sources of

rock.

Fourth,

a

confluence

of

supply

and

demand

factors

will

keep

crop

nutrient

markets

extremely

tight

until

new

supply

comes on-line.

Finally,

crop

prices

are

providing

farmers

with

the

incentive

to

apply

optimal

amounts

of

crop

nutrient

in

order

to

maximize yield.

Mosaic is well positioned in both potash and phosphate to take advantage of these

favorable market conditions. |

Thank you

|

| Thank you for your time today. Now, I will be glad to answer any

questions you may have. |

Appendix

23

As of Period End

Cash and Cash

Equivalents

Short-Term Debt

Current

Maturities

Long-Term Debt

Total Debt

Net (Debt) Cash

31-May-06

173.3

152.8

69.3

2,388.1

2,610.2

(2,436.9)

31-May-07

420.6

138.6

403.8

1,818.1

2,360.5

(1,939.9)

31-May-08

1,960.7

133.1

43.3

1,375.0

1,551.4

409.3

31-May-09

2,703.2

92.7

43.3

1,256.5

1,392.5

1,310.7

31-May-10

2,523.0

83.1

15.2

1,245.6

1,343.9

1,179.1

30-Nov-10

3,659.4

54.5

466.3

788.4

1,309.2

2,350.2

Reconciliation of Cash and Cash Equivalents less Debt

Source: Cash and cash equivalents from 10Q/10K as filed. Total debt includes Short term debt,

current maturities of long-term debt, long-term debt less current maturities and

long-term debt due to Cargill Inc. and Affiliates. We believe this non-GAAP

measure provides additional information regarding the liquidity and financial position of the

Company. |