Attached files

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-Q

| x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE QUARTERLY PERIOD ENDED DECEMBER 31, 2010

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE TRANSITION PERIOD FROM TO

Commission File Number: 1-33428

Pharmasset, Inc.

(Exact name of registrant as specified in its charter)

| DELAWARE | 98-0406340 | |

| (State or other jurisdiction of incorporation or organization) | (IRS Employer Identification No.) | |

| 303-A College Road East Princeton, New Jersey |

08540 | |

| (Address of registrant’s principal executive offices) | (Zip Code) | |

(609) 613-4100

(Telephone number, including area code)

N/A

(Former Name, Former Address and Former Fiscal Year, if Changed Since Last Report)

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes ¨ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). ¨ Yes ¨ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer or a smaller reporting company. See definition of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | x | |||

| Non-accelerated filer | ¨ | Smaller reporting company | ¨ | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ¨ Yes No x

The number of shares of the registrant’s common stock, $0.001 par value, outstanding as of January 31, 2011 was 37,022,855.

Table of Contents

FORM 10-Q

FOR THE QUARTER ENDED DECEMBER 31, 2010

INDEX

The “Company,” “Pharmasset,” “we,” and “us” as used in this Form 10-Q refer to Pharmasset, Inc., a Delaware corporation. Pharmasset, our logo and Racivir are our trademarks. Other trademarks mentioned in this Form 10-Q are the property of their respective owners.

Table of Contents

FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q contains forward-looking statements. The forward-looking statements are principally contained in the sections entitled “Business” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” These statements involve known and unknown risks, uncertainties, and other factors that may cause our actual results, performance, or achievements to be materially different from any future results, performance, or achievements expressed or implied by the forward-looking statements. For this purpose, any statement that is not a statement of historical fact should be considered a forward-looking statement. We may, in some cases, use words such as “project,” “believe,” “anticipate,” “plan,” “expect,” “estimate,” “intend,” “potential,” or other words that convey uncertainty of future events or outcomes to identify these forward-looking statements. These forward-looking statements include statements about the following:

| • | our product development efforts, primarily with respect to the preclinical studies, clinical trial results and regulatory approval of RG7128, PSI-7977, PSI-938, and PSI-661 for the treatment of hepatitis C virus (“HCV”); |

| • | the initiation, termination, completion, or success of preclinical studies and clinical trials for our product candidates; |

| • | clinical trial initiation and completion dates, anticipated regulatory filing dates, and regulatory approval for our product candidates; |

| • | the commercialization of our product candidates; |

| • | our collaboration agreement with F. Hoffmann-LaRoche Ltd. and Hoffmann-La Roche Inc. (collectively, “Roche”), including potential milestone or royalty payments thereunder, and our clinical collaboration agreement with Bristol Myers Squibb Company (“BMS”); |

| • | our intentions regarding the establishment of collaborations or the licensing of product candidates or intellectual property; |

| • | the scope and enforceability of our intellectual property rights, including claims that we or our collaborators may infringe third party intellectual property rights or be otherwise required to pay license fees under such third party rights; |

| • | our intentions to expand our capabilities and hire additional employees; |

| • | anticipated operating losses, future revenues, research and development expenses, and the need for additional financing; and |

| • | our financial performance. |

Forward-looking statements reflect our current views with respect to future events and are subject to risks and uncertainties. We discuss many of the risks and uncertainties associated with our business in greater detail in our Annual Report on Form 10-K for the fiscal year ended September 30, 2010 under the heading “Risk Factors.” Given these risks and uncertainties, you should not place undue reliance on these forward-looking statements. All forward-looking statements represent our estimates and assumptions only as of the date of this Quarterly Report on Form 10-Q.

You should read this Quarterly Report on Form 10-Q and the documents that we reference in it completely and with the understanding that our actual future results may be materially different from what we expect. You should assume that the information appearing in this Quarterly Report on Form 10-Q is accurate as of the date on the front cover of this Quarterly Report on Form 10-Q only. Our business, financial condition, results of operations, and prospects may change. We may not update these forward-looking statements, even though our situation may change in the future, unless we have obligations under the federal securities laws to update and disclose material developments related to previously disclosed information. The forward-looking statements contained in this Quarterly Report on Form 10-Q are subject to the safe-harbor protection provided by the Private Securities Litigation Reform Act of 1995 and Section 21E of the Securities Exchange Act of 1934, as amended (“Exchange Act”).

Table of Contents

| ITEM 1. | FINANCIAL STATEMENTS |

CONDENSED BALANCE SHEETS

(in thousands, except par value, share and per share amounts)

| As of December 31, 2010 |

As of September 30, 2010 |

|||||||

| (unaudited) | ||||||||

| ASSETS |

||||||||

| CURRENT ASSETS: |

||||||||

| Cash and cash equivalents |

$ | 102,651 | $ | 127,081 | ||||

| Amounts due from collaboration partner |

6 | 6 | ||||||

| Prepaid expenses and other current assets |

702 | 718 | ||||||

| Total current assets |

103,359 | 127,805 | ||||||

| EQUIPMENT AND LEASEHOLD IMPROVEMENTS: |

||||||||

| Equipment |

4,098 | 4,060 | ||||||

| Leasehold improvements |

1,837 | 1,837 | ||||||

| 5,935 | 5,897 | |||||||

| Less accumulated depreciation and amortization |

(4,327 | ) | (4,184 | ) | ||||

| Total equipment and leasehold improvements, net |

1,608 | 1,713 | ||||||

| Restricted cash |

100 | 100 | ||||||

| Other assets |

141 | 143 | ||||||

| Total |

$ | 105,208 | $ | 129,761 | ||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY |

||||||||

| CURRENT LIABILITIES: |

||||||||

| Current portion of long-term debt |

$ | 7,796 | $ | 8,705 | ||||

| Accounts payable |

3,687 | 5,037 | ||||||

| Accrued expenses |

4,554 | 5,863 | ||||||

| Deferred rent |

25 | 25 | ||||||

| Deferred revenue |

985 | 985 | ||||||

| Total current liabilities |

17,047 | 20,615 | ||||||

| Deferred rent |

86 | 93 | ||||||

| Deferred revenue |

1,724 | 1,971 | ||||||

| Long-term debt, net of discount of $97 and $150 as of December 31, 2010 and September 30, 2010, respectively |

1,515 | 2,934 | ||||||

| Total liabilities |

20,372 | 25,613 | ||||||

| Commitments and contingencies |

||||||||

| STOCKHOLDERS’ EQUITY: |

||||||||

| Common stock, $0.001 par value, 100,000,000 shares authorized, 34,220,379 and 34,043,898 shares issued and outstanding at December 31, 2010 and September 30, 2010, respectively |

34 | 34 | ||||||

| Warrants to purchase 63,623 shares of common stock for $12.05 per share at December 31, 2010, and 127,248 shares of common stock for $12.05 per share at September 30, 2010 |

640 | 1,230 | ||||||

| Additional paid-in capital |

341,132 | 336,351 | ||||||

| Accumulated deficit |

(256,970 | ) | (233,467 | ) | ||||

| Total stockholders’ equity |

84,836 | 104,148 | ||||||

| Total |

$ | 105,208 | $ | 129,761 | ||||

See notes to financial statements.

4

Table of Contents

CONDENSED STATEMENTS OF OPERATIONS

(UNAUDITED)

(in thousands, except share and per share amounts)

| Three Months Ended December 31, |

||||||||

| 2010 | 2009 | |||||||

| Revenues |

$ | 247 | $ | 269 | ||||

| COSTS AND EXPENSES: |

||||||||

| Research and development |

18,768 | 9,197 | ||||||

| General and administrative |

5,076 | 4,239 | ||||||

| Total costs and expenses |

23,844 | 13,436 | ||||||

| Operating loss |

(23,597 | ) | (13,167 | ) | ||||

| Investment income |

3 | 4 | ||||||

| Other income |

489 | — | ||||||

| Interest expense |

(398 | ) | (706 | ) | ||||

| Loss before income taxes |

(23,503 | ) | (13,869 | ) | ||||

| Provision for income taxes |

— | — | ||||||

| Net loss |

$ | (23,503 | ) | $ | (13,869 | ) | ||

| Net loss per share: basic and diluted |

$ | (0.69 | ) | $ | (0.49 | ) | ||

| Weighed average shares outstanding: basic and diluted |

34,106,890 | 28,287,609 | ||||||

See notes to financial statements.

5

Table of Contents

CONDENSED STATEMENTS OF CASH FLOWS

(UNAUDITED)

(in thousands)

| December 31, | ||||||||

| 2010 | 2009 | |||||||

| CASH FLOWS FROM OPERATING ACTIVITIES: |

||||||||

| Net loss |

$ | (23,503 | ) | $ | (13,869 | ) | ||

| Adjustments to reconcile net loss to net cash used in operating activities: |

||||||||

| Depreciation and amortization |

143 | 250 | ||||||

| Non-cash stock compensation |

2,181 | 1,791 | ||||||

| Non-cash interest expense |

64 | 118 | ||||||

| Changes in operating assets and liabilities: |

||||||||

| Amounts due from collaboration partner, prepaid expenses and other assets |

6 | 1,398 | ||||||

| Accounts payable |

(1,351 | ) | (88 | ) | ||||

| Accrued expenses |

(1,309 | ) | (3,862 | ) | ||||

| Deferred rent |

(6 | ) | (31 | ) | ||||

| Deferred revenue |

(247 | ) | (246 | ) | ||||

| Net cash used in operating activities |

(24,022 | ) | (14,539 | ) | ||||

| CASH FLOWS FROM INVESTING ACTIVITIES: |

||||||||

| Purchase of equipment and leasehold improvements |

(37 | ) | (25 | ) | ||||

| Net cash used in investing activities |

(37 | ) | (25 | ) | ||||

| CASH FLOWS FROM FINANCING ACTIVITIES: |

||||||||

| Proceeds from exercise of stock options |

2,010 | 270 | ||||||

| Principal payments on long-term debt |

(2,381 | ) | (1,841 | ) | ||||

| Net cash used in financing activities |

(371 | ) | (1,571 | ) | ||||

| Net decrease in cash and cash equivalents |

(24,430 | ) | (16,135 | ) | ||||

| Cash and cash equivalents - Beginning of period |

127,081 | 58,408 | ||||||

| Cash and cash equivalents - End of period |

$ | 102,651 | $ | 42,273 | ||||

| SUPPLEMENTAL DISCLOSURES: |

||||||||

| Cash paid during the period for: |

||||||||

| Interest |

$ | 333 | $ | 588 | ||||

| Noncash transactions: |

||||||||

| Value of warrants exercised by converting warrants into shares of common stock (“net issuance method”) |

$ | 590 | $ | — | ||||

See notes to financial statements.

6

Table of Contents

Notes to Financial Statements (Unaudited)

1. DESCRIPTION OF BUSINESS AND BASIS OF PRESENTATION

Description of Business - Pharmasset, Inc. is a clinical-stage pharmaceutical company committed to discovering, developing, and commercializing novel drugs to treat viral infections. The Company’s primary focus is on the development of nucleoside/tide analogs as oral therapeutics for the treatment of chronic hepatitis C virus (“HCV”) infection. Nucleoside/tide analogs are a class of compounds which act as alternative substrates for the viral polymerase, thus inhibiting viral replication. The Company currently has three clinical-stage product candidates, two of which it is developing itself and one of which it is developing with a strategic partner. The Company is also advancing a series of preclinical candidates in preparation for clinical development. Pharmasset, Inc.’s three clinical stage product candidates are:

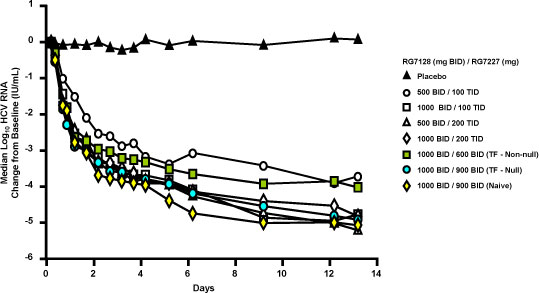

| • | RG7128, an HCV cytosine nucleoside polymerase inhibitor the Company is developing through a strategic collaboration with F. Hoffmann-La Roche Ltd and Hoffmann-La Roche Inc. (collectively, “Roche”). In October 2010, Roche presented data from a 12-week interim analysis from the Phase 2b “PROPEL” study of RG7128 in combination with Pegasys® (pegylated interferon) plus Copegus® (ribavirin), the standard of care for treating HCV (“SOC”) in patients with HCV genotypes 1 or 4. In addition, RG7128 is in a 24-week Phase 2b “JUMP-C” study in combination with SOC in patients with HCV genotypes 1 or 4. Roche is planning to conduct the next study of RG7128 in combination with ritonavir-boosted danoprevir. This “INFORM-SVR” study is part of a series of studies designed to investigate the combination of two oral, direct acting antivirals (“DAAs”) in the absence of pegylated interferon. Roche is also planning to conduct a Phase 2b study in patients with HCV genotypes 2 or 3. All of these studies are being, or are expected to be, conducted by Roche; |

| • | PSI-7977, an HCV uracil nucleotide analog polymerase inhibitor that is in a 12-week Phase 2b dose-finding study (“PROTON”) in combination with SOC in patients with HCV genotypes 1, 2 or 3. In addition, PSI-7977 recently began dosing in an exploratory Phase 2 study (“ELECTRON”) in combination with ribavirin, administered without and with varying durations of pegylated interferon, in patients with HCV genotypes 2 or 3; and |

| • | PSI-938, an HCV guanine nucleotide analog polymerase inhibitor that is in Part 2 of a Phase 1 study with PSI-7977 in patients with HCV genotype 1. |

The Company is subject to risks common to companies in the pharmaceutical industry including, but not limited to, risks relating to product development, protection of proprietary intellectual property, compliance with government regulations, collaboration partners, dependence on key personnel, the need to obtain additional financing, uncertainty of market acceptance of products, and product liability. (See Part II, Item 1A. - Risk Factors for additional information.)

Basis of Presentation - The Company was incorporated as Pharmasset, Inc. under the laws of Delaware on June 8, 2004. Management has evaluated subsequent events for disclosure or recognition in the accompanying financial statements up to the filing of this report.

The accompanying unaudited condensed financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America for interim financial information and with the instructions to Form 10-Q and Rule 10-01 of Regulation S-X. Accordingly, they do not contain all of the information and footnotes required for complete financial statements. In the opinion of management, the accompanying unaudited condensed financial statements reflect all adjustments, which include normal recurring adjustments, necessary to present fairly the Company’s interim financial information. The accompanying unaudited condensed financial statements and notes to the condensed financial statements should be read in conjunction with the audited financial

7

Table of Contents

statements for the fiscal year ended September 30, 2010 included in the Company’s Annual Report on Form 10-K filed with the Securities and Exchange Commission (“SEC”) on November 23, 2010.

2. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Use of Estimates - The preparation of the Company’s financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities, the disclosure of contingent assets and liabilities at the date of the financial statements, and the reported amounts of revenue and expenses during the reporting period. Actual results could differ from those estimates.

Cash and Cash Equivalents - Cash and cash equivalents represent cash and highly liquid investments purchased within three months of the maturity date and consist primarily of mutual and/or money market funds.

Investments - The Company invests available cash primarily in mutual and money market funds, bank certificates of deposit and investment-grade commercial paper, corporate notes, and government securities. All investments are classified as available-for-sale and are carried at fair market value with unrealized gains and losses recorded in accumulated other comprehensive (loss) income. For purposes of determining realized gains and losses, the cost of securities sold is based on specific identification.

Deferred Offering Costs - Costs incurred in connection with an equity offering are deferred and, upon completion of the equity offering, are applied against the proceeds from the offering.

Deferred Financing Costs - Costs incurred in connection with debt offerings are deferred (and included in prepaid expenses and other current assets and other long-term assets on the balance sheet) and amortized as interest expense over the term of the related debt using the effective interest method. The amortization expense is included in interest expense in the statements of operations.

Equipment and Leasehold Improvements - Equipment and leasehold improvements are recorded at cost and are depreciated using the straight-line method over the following estimated useful lives of the assets: computer equipment—three years; laboratory and office equipment—seven years; and leasehold improvements—the lesser of the estimated life of the asset or the lease term. Expenditures for maintenance and repairs are expensed as incurred. Capital expenditures which improve and extend the life of the related assets are capitalized.

Intangible Assets - Intangible assets are recorded at cost and are amortized on a straight-line basis over the estimated useful life. The estimated useful life is determined based upon a review of several factors including the nature of the asset, its expected use, length of the agreement and the period over which benefits are expected to be received from the use of the asset.

Impairment of Long-Lived Assets - The Company continually evaluates whether events or circumstances have occurred that indicate the estimated remaining useful lives of long-lived assets may require revision or that the carrying value of these assets may be impaired. To determine whether assets have been impaired, the estimated undiscounted future cash flows for the estimated remaining useful life of the respective assets are compared to the carrying value. To the extent that the undiscounted future cash flows are less than the carrying value, a new fair value of the asset is required to be determined. If such fair value is less than the current carrying value, the asset is written down to its estimated fair value.

Fair Value of Financial Instruments - The Company categorizes its financial assets based on the priority of the inputs to the valuation technique into a three-level fair value hierarchy as set forth below. Except for its debt with its lender (See Note 6), the Company does not have any financial liabilities that are required to be measured at fair value on a recurring basis. If the inputs used to measure the financial instruments fall within different levels of the hierarchy, the categorization is based on the lowest level input that is significant to the fair value measurement of the instrument.

Financial assets recorded on the balance sheets are categorized as follows:

8

Table of Contents

| • | Level 1 – Financial assets whose values are based on unadjusted quoted prices for identical assets or liabilities in an active market which the company has the ability to access at the measurement date (examples include active exchange-traded equity securities and most U.S. Government and agency securities). |

| • | Level 2 – Financial assets whose values are based on quoted market prices in markets where trading occurs infrequently or whose values are based on quoted prices of instruments with similar attributes in active markets. |

| • | Level 3 – Financial assets whose values are based on prices or valuation techniques that require inputs that are both unobservable and significant to the overall fair value measurement. These inputs reflect management’s own assumptions about the assumptions a market participant would use in pricing the asset. |

As of December 31, 2010 and September 30, 2010, the Company did not have any Level 2 or 3 financial assets and the Company’s Level 1 financial assets were as follows:

| Level 1 | ||||||||

| December 31, 2010 |

September 30, 2010 |

|||||||

| (in thousands) | ||||||||

| Money Market Funds |

$ | 102,651 | $ | 127,081 | ||||

| Certificate of Deposit |

100 | 100 | ||||||

| Total |

$ | 102,751 | $ | 127,181 | ||||

The Certificate of Deposit included above as of December 31, 2010 and September 30, 2010 is for a letter of credit in place to support a performance bond required to ensure payment of import duties on supplies used in the Company’s development programs, and is classified as Restricted Cash on the balance sheet as of December 31, 2010 and September 30, 2010.

Concentrations of Credit Risk, Suppliers, and Revenues - The Company’s financial instruments that potentially subject it to concentrations of credit risk are cash and cash equivalents and investments. The Company invests cash that is not currently being used in operations in accordance with its investment policy. The policy allows for the purchase of low-risk, investment grade debt securities issued by the United States government and very highly-rated banks and corporations, subject to certain concentration limits. The policy allows for maturities that are not longer than two years for individual securities and an average of one year for the portfolio as a whole.

The Company relies on certain materials used in its development process, some of which are procured from a single source. The failure of a supplier, including a subcontractor, to deliver on schedule could delay or interrupt the development process and thereby adversely affect the Company’s operating results.

During the three months ended December 31, 2010 and 2009, the Company derived all of its revenues from one customer (See Note 4).

Revenue Recognition - The Company recognizes revenues when all of the following four criteria are present: persuasive evidence of an arrangement exists; delivery has occurred or services have been rendered; the fee is fixed or determinable; and collectability is reasonably assured.

The Company’s revenues are primarily related to its collaboration agreement with Roche. This agreement provides for various types of payments to the Company, including non-refundable upfront license fees, research and/or development payments, and milestone payments.

9

Table of Contents

Where the Company has continuing performance obligations under the terms of a collaborative arrangement, non-refundable upfront license payments received upon contract signing are recorded as deferred revenue and recognized as revenue as the related activities are performed. The period over which these activities are to be performed is based upon management’s estimate of the development period. Changes in management’s estimate could change the period over which revenue is recognized. Research and/or development payments are recognized as revenues as the related research and/or development activities are performed and when the Company has no continuing performance obligations related to the research and development payment received.

Where the Company has no continuing involvement under a collaborative arrangement, the Company records nonrefundable license fee revenues when the Company has the contractual right to receive the payment, in accordance with the terms of the collaboration agreement, and records milestones upon appropriate notification to the Company of achievement of the milestones by the collaborative partner.

Effective October, 1, 2010, the Company adopted the new accounting standards for determining whether the milestone method of revenue recognition is appropriate. The Company recognizes revenue from milestone payments when earned, provided that (i) the milestone event is substantive and its achievability was not reasonably assured at the inception of the agreement and (ii) the Company does not have ongoing performance obligations related to the achievement of the milestone earned. Milestone payments are considered substantive if all of the following conditions are met: the milestone payment (a) is commensurate with either the vendor’s performance to achieve the milestone or the enhancement of the value of the delivered item or items as a result of a specific outcome resulting from the vendor’s performance to achieve the milestone, (b) relates solely to past performance, and (c) is reasonable relative to all of the deliverables and payment terms (including other potential milestone consideration) within the arrangement. Any amounts received under the agreement in advance of performance, if deemed substantive, are recorded as deferred revenue and recognized as revenue as the Company completes its performance obligations.

Effective October 1, 2010, the Company also adopted the new accounting standards for revenue recognition for multiple deliverable revenue arrangements. Each deliverable within a multiple-deliverable revenue arrangement is accounted for as a separate unit of accounting under the guidance of the new authoritative guidance if both of the following criteria are met: (1) the delivered item or items have value to the customer on a standalone basis and (2) for an arrangement that includes a general right of return relative to the delivered item(s), delivery or performance of the undelivered item(s) is considered probable and substantially in our control.

This new authoritative guidance amends previously issued guidance to eliminate the residual method of allocation for multiple-deliverable revenue arrangements, and requires that arrangement consideration be allocated at the inception of an arrangement to all deliverables using the relative selling price method. The new authoritative guidance also establishes a selling price hierarchy for determining the selling price of a deliverable, which includes (1) vendor-specific objective evidence, if available, (2) third-party evidence, if vendor-specific objective evidence is not available, and (3) estimated selling price if neither vendor-specific nor third-party evidence is available. Additionally, it expands the disclosure requirements related to a vendor’s multiple-deliverable revenue arrangements.

Deferred revenue associated with a non-refundable payment received under a collaborative agreement that is terminated prior to its completion results in an immediate recognition of the deferred revenue.

Research and Development Expenses - Research and development expenses consist primarily of salaries and related personnel expenses, fees paid to external service providers, costs of preclinical studies and clinical trials, drug and laboratory supplies, costs for facilities and equipment, and the costs of intangibles that are purchased from others for use in research and development activities, such as in-licensed product candidates, that have no alternative future uses. Research and development expenses are included in operating expenses when incurred. Reimbursements received from the Company’s collaborator(s) for third-party research and development expenses incurred by the Company on their behalf are recorded as a contra-expense. Amounts due from collaborators for reimbursement of research and development expenses are recorded on the balance sheets as “Amounts due from collaboration partner.”

Nonrefundable advance payments for goods or services that will be used or rendered for future research and development activities are deferred and capitalized. Such amounts are then recognized as an expense as the related goods are delivered or the services are performed, or when the goods or services are no longer expected to be provided.

10

Table of Contents

Stock-Based Compensation - The Company recognizes stock compensation expense for awards of equity instruments to employees and directors based on the grant-date fair value of those awards (with limited exceptions). The grant-date fair value of the award is recognized as compensation expense on a straight-line basis over the requisite service period. Equity instruments granted to consultants are periodically valued and recorded as stock compensation expense as the equity instrument vests.

Stock-based compensation expense is included in both research and development expenses and in general and administrative expenses in the statements of operations. Since the Company’s stock was not publicly traded prior to April 27, 2007, the expected volatility was calculated for each equity award granted based on the “peer method.” The Company identified companies that trade publicly within the pharmaceutical industry that have similar SIC codes, employee count and revenues. Prior to October 1, 2006, the Company had chosen the weekly high price volatility for these companies for a period of five years. Subsequent to October 1, 2006, the Company has used the weekly high price for these companies for a period of six years to coincide with the expected term.

Income Taxes - The Company accounts for income taxes under the asset and liability method. The Company provides deferred tax assets and liabilities for the expected future tax consequences of temporary differences between the Company’s financial statement carrying amounts and the tax bases of assets and liabilities using enacted tax rates expected to be in effect in the years in which the differences are expected to reverse. A valuation allowance is provided to reduce the deferred tax assets to the amount that is expected to be realized.

The Company uses a comprehensive model for how it recognizes, measures, presents, and discloses in its financial statements uncertain tax positions that the Company has taken or expects to take on a tax return (including a decision whether to file or not to file a return in a particular jurisdiction). Under this comprehensive model, the financial statements reflect expected future tax consequences of such positions presuming the taxing authorities’ full knowledge of the position and all relevant facts.

As a result of adopting this new comprehensive model, there were no changes to the Company’s deferred tax assets as of October 1, 2007. The total amount of unrecognized tax benefits at October 1, 2007 was $0.1 million, all of which would favorably impact the Company’s effective tax rate if recognized. Since the unrecognized tax benefit has not been utilized on the Company’s tax returns, there is no liability recorded on the balance sheets. The Company does not have any interest or penalties accrued related to tax positions at adoption. In the event the Company determines that accrual of interest or penalties are necessary in the future, the amount will be presented as a component of income taxes.

Net Income (Loss) Per Common Share - Basic net income (loss) per common share is calculated by dividing net income (loss) by the weighted average number of common shares outstanding during the period. Diluted net income (loss) per common share is calculated by dividing net income (loss) by the weighted average number of common shares and other dilutive securities outstanding during the period. Dilutive potential common shares resulting from the assumed exercise of outstanding stock options and warrants are determined based on the treasury stock method.

11

Table of Contents

| Three Months Ended December 31, |

||||||||

| 2010 | 2009 | |||||||

| (In thousands, except per share amounts) |

||||||||

| Numerator: |

||||||||

| Net loss |

$ | (23,503 | ) | $ | (13,869 | ) | ||

| Denominator: |

||||||||

| Weighted average common shares outstanding used in calculation of basic net loss per share |

34,107 | 28,288 | ||||||

| Effect of dilutive securities: |

||||||||

| Common stock options |

— | — | ||||||

| Common stock warrants |

— | — | ||||||

| Weighted average common shares outstanding used in calculation of diluted net loss per share |

34,107 | 28,288 | ||||||

| Net loss per share: basic and diluted |

$ | (0.69 | ) | $ | (0.49 | ) | ||

The following table summarizes the securities outstanding at the end of each period with the potential to become common stock that have been excluded from the computation of diluted net income (loss) per share, as their effect would have been anti-dilutive.

| Three Months Ended December 31, |

||||||||

| 2010 | 2009 | |||||||

| (In thousands) | ||||||||

| Options to purchase common stock |

3,167 | 3,058 | ||||||

| Common stock warrants |

64 | 127 | ||||||

| Total |

3,231 | 3,185 | ||||||

Segment Reporting - Operating segments are identified as components of an enterprise about which separate financial information is available for evaluation by the chief operating decision-maker, or decision-making group, in making decisions regarding resource allocation and assessing performance. The Company has determined that it operates in one segment, which focuses on developing nucleoside/tide analog drugs for the treatment of viral infections.

Recently Adopted Accounting Pronouncements - In October 2009, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update (“ASU”) No. 2009-13, Multiple-Deliverable Revenue Arrangements. This ASU provides new accounting standards for determining whether multiple deliverables exist, how the arrangement should be separated, and how the consideration should be allocated. This guidance requires an entity to allocate revenue in an arrangement using estimated selling prices of deliverables if a vendor does not have vendor-specific objective evidence or third-party evidence of selling price. The update eliminates the use of the residual method and requires an entity to allocate revenue using the relative selling price method and also significantly expands the disclosure requirements for multiple-deliverable revenue arrangements. The Company adopted these new accounting standards on October 1, 2010 on a prospective basis. Adoption of these new accounting standards did not have any impact on the Company’s financial position or results of operations.

In April 2010, the FASB issued ASU No. 2010-17, Revenue Recognition — Milestone Method. This ASU provides guidance on the criteria that should be met for determining whether the milestone method of revenue

12

Table of Contents

recognition is appropriate. Under the milestone method of revenue recognition, consideration that is contingent upon achievement of a milestone in its entirety can be recognized as revenue in the period in which the milestone is achieved only if the milestone meets all criteria to be considered substantive. This standard provides the criteria to be met for a milestone to be considered substantive which includes that: a) performance consideration earned by achieving the milestone be commensurate with either performance to achieve the milestone or the enhancement of the value of the item delivered as a result of a specific outcome resulting from performance to achieve the milestone; b) relate to past performance; and c) be reasonable relative to all deliverables and payment terms in the arrangement. The Company adopted these new accounting standards on October 1, 2010 on a prospective basis. Adoption of these new accounting standards did not have any impact on the Company’s financial position or results of operations.

3. ACCRUED EXPENSES

Accrued expenses consisted of the following:

| As of December 31, 2010 |

As of September 30, 2010 |

|||||||

| (In thousands) | ||||||||

| Accrued clinical trial expenses |

$ | 2,682 | $ | 1,771 | ||||

| Accrued compensation |

514 | 1,801 | ||||||

| Accrued legal fees |

824 | 1,770 | ||||||

| Other accrued expenses |

534 | 521 | ||||||

| $ | 4,554 | $ | 5,863 | |||||

4. CONTRACT REVENUE AGREEMENTS

The following is a reconciliation between cash payments received and receivable under contract revenue agreements and contract revenues reported:

| Three Months Ended December 31, |

||||||||

| 2010 | 2009 | |||||||

| (In thousands) | ||||||||

| Cash received/receivable |

$ | — | $ | 23 | ||||

| Deferred |

— | — | ||||||

| Amortization |

247 | 246 | ||||||

| Revenues |

$ | 247 | $ | 269 | ||||

The Company recorded revenues from the collaboration agreement with Roche, comprising 100% of total revenues during the three months ended December 31, 2010 and 2009. Revenues during each period primarily reflect amortization of up-front and subsequent collaborative and license payments received from Roche previously recorded as deferred revenue.

Roche - In October 2004, the Company entered into a collaboration and license agreement with Roche to develop PSI-6130 and PSI-6130 prodrugs (including RG7128) for treating chronic HCV infection, and to discover chemically related nucleoside polymerase inhibitors pursuant to a research collaboration. The research collaboration ended in December 2006. The Company granted Roche worldwide rights, excluding Latin America and Korea, to PSI-6130 and its prodrugs (including RG7128). Roche paid the Company an up-front payment of $8.0 million in 2004 and agreed to pay future research and development costs. The up-front payment has been recorded as deferred revenue and is being amortized over the estimated development period. The portion of the above payments recorded as deferred revenue on the Company’s balance sheets as of December 31, 2010 and September 30, 2010 was approximately $2.7 million and $3.0 million, respectively. Roche is also required to make certain future payments to

13

Table of Contents

the Company for RG7128 upon the achievement of predefined development and marketing milestones in Roche’s territories. In addition, the Company will receive royalties paid as a percentage of total annual net product sales, if any, in Roche’s territories, and the Company will be entitled to receive one time performance payments should net sales from the product exceed specified thresholds.

The Company retained certain co-promotion rights in the United States. The Company will be required to pay Roche royalties on net product sales, if any, in the territories the Company has retained. Prior to the transfer of the IND for RG7128 to Roche, which occurred during December 2008, Roche funded and the Company was responsible for preclinical work, the IND submission, and the initial clinical trial, while Roche managed other preclinical studies and clinical development. Roche reimbursed the Company approximately $14 thousand during the three months ended December 31, 2009 under this agreement. Roche will continue to fund all of the expenses of, and be responsible for, other preclinical studies and future clinical development of RG7128 in the territories licensed to Roche. Roche and the Company will continue to jointly oversee all development and marketing activities of RG7128 in the territories licensed to Roche.

The agreement will terminate once there are no longer any royalty or payment obligations. Additionally, Roche may terminate the agreement in whole or in part by providing six months’ written notice to the Company. Otherwise, either party may terminate the agreement in whole or in part in connection with a material breach of the agreement by the other party that is not timely cured. In the event of termination, Roche must assign or transfer to the Company all regulatory filings, trademarks, patents, and preclinical and clinical data related to this collaboration.

5. IN-LICENSE AGREEMENTS

In 1998 and 2004, the Company entered into various license agreements with the University of Georgia Research Foundation (“UGARF”), Emory University and the University of Alabama at Birmingham Research Foundation, Inc. (collectively, the “Universities”) to pursue the research, development, and commercialization of certain human antiviral, anticancer, and antibacterial applications and uses of certain specified technologies. Under each of these agreements, the Universities have granted an exclusive right and license under the related patents to the Company. The Company and the Universities will share in any proceeds received by the Company related to internal development or sublicensing of the specified technologies, including milestone payments, fees, and royalties.

In April 2002, the license agreement between UGARF, Emory University, and the Company dated June 16, 1998 was selectively modified to terminate certain technologies and related rights and obligations.

6. DEBT

On September 30, 2007, the Company entered into a Loan Agreement that allowed the Company to borrow up to $30.0 million in $10.0 million increments (“Loan Agreement”). The Company borrowed the first and second $10.0 million increments by signing two Secured Promissory Notes (“Notes A and B”) on October 5, 2007 and March 28, 2008, respectively. Notes A and B bear interest at 12%. On December 12, 2008, the Company amended the Loan Agreement and borrowed $3.3 million by signing a Secured Promissory Note (“Note C”). Note C bears interest at 12.5%. Notes A, B and C are to be repaid over a 45-month period with the first 15 monthly payments representing interest only followed by 30 equal monthly payments of principal and interest. The principal monthly repayments on each of the following notes begin and end as follows:

| Note |

Begin |

End | ||

| Note A |

March 1, 2009 | August 1, 2011 | ||

| Note B |

August 1, 2009 | January 1, 2012 | ||

| Note C |

May 1, 2010 | October 1, 2012 | ||

Prepayment of the loans made pursuant to the Loan Agreement is subject to penalty and substantially all of the Company’s tangible and intangible assets (except for intellectual property) are pledged as collateral for the Loan Agreement. Future total principal repayments of the three Notes amount to $6.3 million in fiscal 2011, $3.0 million in fiscal 2012, and $0.1 million in fiscal 2013. There are no additional borrowings available under the Loan Agreement.

14

Table of Contents

Under the Loan Agreement, the Company agreed that in the event its market capitalization is below $90.0 million for 15 consecutive days in which the principal market for its common stock is open for trading to the public, the Company will be required to repay 50% of the then outstanding principal balance of the loans. The Company further agreed that in the event its market capitalization is below $40.0 million for 15 consecutive days in which the principal market for its common stock is open for trading to the public, the Company will be required to repay all of the then outstanding principal balance of the loans.

In conjunction with entering into the Loan Agreement, the Company granted warrants to the lender to purchase shares of the Company’s common stock (See Note 8). Since these warrants were granted in conjunction with entering into the Loan Agreement and with the intention of executing promissory notes, the relative fair value of the warrant was recorded as equity and deferred interest as the warrants became exercisable and the deferred financing costs and debt discount are being amortized over the term of the promissory notes using the effective interest method.

7. STOCK COMPENSATION

The Company’s 1998 Stock Plan (“1998 Plan”), as amended, was originally adopted by its board of directors during 1998 and subsequently amended in 2000, 2004 and 2006. A maximum of 3,517,015 shares of the Company’s common stock are authorized for issuance under the 1998 Plan. Upon the closing of the IPO, which occurred on May 2, 2007, the Company adopted the 2007 Equity Incentive Plan (“2007 Plan”). Upon the adoption of the 2007 Plan, no additional awards will be issued under the 1998 Plan and the shares remaining for future grant under the 1998 Plan were transferred to the 2007 Plan. The purpose of the 2007 Plan is to provide an incentive to officers, directors, employees, independent contractors, and to other persons who provide significant services to the Company. On September 23, 2009, the Company’s stockholders approved amendments to the 2007 Plan to remove a provision that allowed for repricing stock options without stockholder approval, added certain minimum vesting periods for nonperformance based grants, and increased the number of shares authorized under the 2007 Plan by 1,000,000 shares (the “Revised 2007 Plan”). As of December 31, 2010, under the Revised 2007 Plan 209,826 shares of the Company’s common stock were reserved for future grants of stock options, stock appreciation rights, restricted stock, deferred stock, restricted stock units, performance shares, phantom stock, and similar types of stock awards as well as cash awards. The Company’s Board of Directors has approved an increase of 2,000,000 shares to the shares of the Company’s common stock reserved for future grants under the Revised 2007 Plan. This increase will be presented to the Company’s stockholders for their approval at the Company’s 2011 annual stockholders meeting to be held on March 23, 2011. Options granted under the Revised 2007 Plan may be either “incentive stock options,” as defined under Section 422 of the Internal Revenue Code or nonstatutory stock options. Options granted under the Revised 2007 Plan shall be at per share exercise prices equal to the fair value of the shares on the dates of grant. The Revised 2007 Plan will terminate in fiscal 2017 unless it is extended or terminated earlier pursuant to its terms.

Stock Options - The assumptions used and weighted-average information for employee and director grants for the three months ended December 31, 2010 and 2009 are as follows:

| Three Months Ended December 31, |

||||||||

| 2010 | 2009 | |||||||

| Risk free interest rate |

1.67 | % | 2.91 | % | ||||

| Expected dividend yield |

0.0 | % | 0.0 | % | ||||

| Expected lives (years) |

6.01 | 6.00 | ||||||

| Expected volatility |

62.21 | % | 64.25 | % | ||||

| Weighted-average fair value of options granted |

$ | 18.71 | $ | 13.11 | ||||

Generally, stock options granted under these plans have a contractual life of ten years and vest pro rata over three or four year terms. A summary of the Company’s stock option activity during the three months ended December 31, 2010 is as follows:

15

Table of Contents

| Number of Shares |

Weighted Average Exercise Price |

|||||||

| Outstanding - September 30, 2010 |

2,796,289 | $ | 12.66 | |||||

| Granted (unaudited) |

540,287 | $ | 32.46 | |||||

| Exercised (unaudited) |

(130,633 | ) | $ | 15.39 | ||||

| Forfeited (unaudited) |

(38,751 | ) | $ | 20.46 | ||||

| Outstanding - December 31, 2010 (unaudited) |

3,167,192 | $ | 15.83 | |||||

| Exercisable - September 30, 2010 |

1,788,794 | $ | 9.23 | |||||

| Exercisable - December 31, 2010 (unaudited) |

1,923,047 | $ | 10.25 | |||||

The range of exercise prices of stock options outstanding at December 31, 2010 was $3.00 to $40.84. The weighted average remaining contractual life of stock options outstanding at December 31, 2010 was 7.14 years. The total intrinsic value of options exercised during the three months ended December 31, 2010 was $3,598,184. The Company recognized compensation expense of $2,136,869 and $1,725,273 during the three months ended December 31, 2010 and 2009 respectively, related to stock options issued to non-employees and employees. As of December 31, 2010 and September 30, 2010, $14,743,030 and $8,048,915 respectively, of deferred stock-based compensation expense related to non-employee and employee stock options remained unamortized. The unamortized amount of $14,743,030 as of December 31, 2010 has a weighted-average period of approximately 1.60 years to be recognized.

| Outstanding as of December 31, 2010 | Exercisable as of December 31, 2010 | |||||||||||||||||||

| Number of |

Exercise Price | Weighted Average Remaining Contractual Life (in Years) |

Weighted Average Exercise Price |

Number of Options |

Weighted Average Exercise Price |

|||||||||||||||

| 926,136 | 3.00 - 4.49 | 4.66 | $ | 3.41 | 919,302 | $ | 3.41 | |||||||||||||

| 6,500 | 4.50 - 5.99 | 6.25 | $ | 5.58 | 5,479 | $ | 5.58 | |||||||||||||

| 6,668 | 6.00 - 7.49 | 1.79 | $ | 6.75 | 6,668 | $ | 6.75 | |||||||||||||

| 86,666 | 7.50 - 10.49 | 6.36 | $ | 8.88 | 84,166 | $ | 8.89 | |||||||||||||

| 563,229 | 10.50 - 15.00 | 6.82 | $ | 13.65 | 402,179 | $ | 13.64 | |||||||||||||

| 1,036,793 | 15.01 - 29.99 | 8.26 | $ | 20.13 | 475,252 | $ | 19.56 | |||||||||||||

| 541,200 | 30.00 - 45.00 | 9.78 | $ | 32.47 | 30,001 | $ | 32.33 | |||||||||||||

As of December 31, 2010, after considering estimated forfeitures, there were 3,048,010 options outstanding that were either vested or expected to vest in the future, of which 1,923,047 options were currently exercisable, with weighted average exercise prices of $15.50 and $10.25 per share, aggregate intrinsic values of $85,518,016 and $64,061,816 and weighted average remaining contractual terms of 7.08 and 6.09 years, respectively.

Restricted Stock - Restricted stock has been issued to the Company’s non-employee directors and to a consultant. Restricted stock issued to non-employee directors prior to fiscal 2010 vested no later than one year from the date of issuance, as long as the director remained in continuous service to the Company as of the vest date. Restricted stock issued to non-employee directors subsequent to fiscal 2009 vests 50% on the first anniversary of the date of grant, 25% on the second anniversary, and 25% on the third anniversary, provided that the director is and has remained in continuous service to the Company as a director as of such anniversary. Restricted stock issued to a consultant vests equally on a quarterly basis over four years.

With regard to restricted stock granted to non-employee directors, the fair value of the restricted stock issued was determined using the closing price of the Company’s common stock as reported on the Global Market of The NASDAQ Stock Market LLC (“NASDAQ”) on the date of grant and is recognized as stock-based compensation expense as the shares vest over the vesting period. With regard to the restricted stock granted to the consultant, stock-based compensation expense equal to the fair value of the restricted shares that vest is recorded on a quarterly

16

Table of Contents

basis over the vesting period of four years. The fair value of each of the restricted shares that vest is equal to the fair value of a share of the Company’s common stock as of each vesting date.

A summary of the Company’s restricted stock activity during the three months ended December 31, 2010 is as follows:

| Number of Shares |

||||

| Outstanding - September 30, 2010 |

66,666 | |||

| Granted |

— | |||

| Forfeited |

— | |||

| Outstanding - December 31, 2010 |

66,666 | |||

As of December 31, 2010, holders were vested in 54,666 of the 66,666 restricted shares outstanding, leaving a total of 12,000 restricted shares unvested as of quarter end. The weighted average fair value of the shares granted in fiscal 2010 was $29.01 per share.

The Company recognized compensation expense of $44 thousand and $66 thousand during the three months ended December 31, 2010 and 2009, respectively, related to restricted stock issued to its non-employee directors and to the consultant. Unrecognized compensation expense for the restricted shares granted to the non-employee directors was $211 thousand at December 31, 2010. This amount will be recognized over the remaining vesting period of the restricted shares.

8. STOCKHOLDERS’ EQUITY AND WARRANTS

Common Stock - As of December 31, 2010, the Company had 100,000,000 shares of common stock authorized with a par value of $0.001 per share and the Company had reserved 3,167,192 shares of common stock for issuance upon the exercise of outstanding common stock options. Also, 209,826 shares of the Company’s common stock were reserved for future grants of stock options (or other similar equity instruments) under the Company’s Revised 2007 Plan as of December 31, 2010. The Company’s Board of Directors has approved an increase of 2,000,000 shares to the shares of the Company’s common stock reserved for future grants under the Revised 2007 Plan. This increase will be presented to the Company’s stockholders for their approval at the Company’s 2011 annual stockholders meeting to be held on March 23, 2011. In addition, 63,623 shares of the Company’s common stock were reserved for future exercise of outstanding warrants as of December 31, 2010.

Warrants - In conjunction with entering into a Loan Agreement and with executing three secured promissory notes (See Note 6), the Company granted warrants to the lender to purchase 127,248 shares of the Company’s common stock at an exercise price of $12.05 per share. During the three months ended December 31, 2010, the lender elected to exercise 63,625 warrants using the net issuance method, which resulted in the issuance of 45,848 shares of common stock by the Company. The remaining warrants expire seven years from the date of grant (or upon a change of control as defined in the Loan Agreement) as follows: 22,130 expire on September 30, 2014, 30,428 expire on March 28, 2015, and 11,065 expire on December 12, 2015.

9. INCOME TAXES

There was no income tax expense during the three months ended December 31, 2010 and 2009. The Company’s effective tax rate for the three months ended December 31, 2010 and 2009 was 0% due to uncertainties related to the realizability of the deferred tax assets as a result of the Company’s history of operating losses. The net deferred tax asset as of December 31, 2010 remains fully offset by a valuation allowance since it is more likely than not that such tax benefits will not be realized.

17

Table of Contents

As of September 30, 2010, the Company had United States federal net operating loss (“NOL”) carryforwards of approximately $219.5 million available to offset future taxable income, if any. Of the federal NOLs, $14.1 million was generated from windfall tax benefit stock option deductions. The tax benefit of this portion of the NOL will be accounted for directly to equity as additional paid in capital as the stock option related losses are utilized. As of September 30, 2010, the Company also had research and development tax credits of $0.1 million available to offset future tax liabilities. The loss carryovers and the research and development tax credits expire over a period of 2020 to 2030.

As of September 30, 2010, the Company’s unrecognized tax benefits of $0.1 million have not significantly changed since October 1, 2007. The Company does not expect any significant changes to the unrecognized tax benefits within 12 months of the reporting date.

The Internal Revenue Service (“IRS”) could challenge tax positions taken by the Company for the periods for which there are open tax years. The Company is open to challenge for the periods of 2004-2009 from federal and state jurisdictions.

Under Section 382 of the Internal Revenue Code (the “Code”), utilization of the NOL and research and development tax credit carryforwards may be subject to a limitation if a change in ownership of the Company, as defined in the Code, occurred previously or could occur in the future. The Company completed a Section 382 analysis regarding limitation of its NOL and research and development tax credit carryforwards that covered the period three years prior to its IPO on May 2, 2007 through a public offering of its common stock on February 5, 2009, and concluded that a change in control occurred at the Company during the quarter ended September 30, 2008. This change in control limits the future use of the Company’s NOL and research and development tax credit carryforwards from fiscal 2008 and prior years. However, based upon the Company’s financial projections, it does not believe that this limitation will result in the expiration of any of these NOL and research and development tax credit carryforwards before they are able to be utilized. The Company is in the process of assessing whether another change in control occurred since the quarter ended September 30, 2008 and expects to disclose the results of this assessment when it is complete. Such a change and any future changes in ownership could impact the use of the Company’s NOL and research and development tax credit carryforwards generated in the affected years. Any limitation may result in expiration of a portion of the NOL or research and development tax credit carryforwards before utilization, which would reduce the Company’s gross deferred tax assets.

On October 29, 2010, the Company was awarded two grants ($244,479 each) totaling $489 thousand under the IRS Qualifying Therapeutic Discovery Project (QTDP) program, which was created by Congress as part of the Patient Protection and Affordable Care Act of 2010. The grants were received on November 12, 2010. One of the grants was awarded for the development of PSI-7977 and the other grant was awarded for the development of PSI-938 or PSI-661. All three of these product candidates are being developed for the treatment of HCV and all of the $489 thousand was recorded as Other income in the Statement of Operations during the three months ended December 31, 2010.

10. COMMITMENTS AND CONTINGENCIES

The Company has entered into an operating lease for office and laboratory space located in Princeton, New Jersey through May 22, 2015. The Company has also entered into an operating lease for office space located in Durham, North Carolina through December 31, 2015.

As of December 31, 2010, minimum future payments under non-cancellable operating leases are as follows:

18

Table of Contents

| December 31, 2010 | ||||

| (In thousands) | ||||

| Fiscal 2011 |

660 | |||

| Fiscal 2012 |

918 | |||

| Fiscal 2013 |

920 | |||

| Fiscal 2014 |

922 | |||

| Fiscal 2015 |

626 | |||

| Thereafter |

22 | |||

| Total minimum payments required |

$ | 4,068 | ||

Under a license agreement with Emory University for Racivir, the Company agreed to pay Emory University up to an aggregate of $1.0 million in future marketing milestone payments. None of these potential future payments are included in the Company’s financial statements, as the payments are contingent on the achievement of milestones, which it has not yet achieved.

On July 28, 2009, Emory University and University of Georgia Research Foundation, Inc. (“Claimants”) filed a Demand for Arbitration and Relief (the “Demand”) with the American Arbitration Association (“AAA”) in Atlanta, Georgia (the “Emory Arbitration”), claiming certain payments and seeking specific performance under the Company’s January 8, 2004 license agreement with Claimants (the “Emory License”).

The Demand alleged that payments Pharmasset had received under the Roche collaboration agreement were subject to the Emory License and that Pharmasset had not paid fees to Claimants based on such payments. In addition, the Demand alleged that Pharmasset had not complied with certain terms and conditions of the Emory License and that other Pharmasset product candidates were, or will be, covered by the Emory License. The Demand requested, among other things, specific performance of the Emory License, including the payment of license fees related to past payments received by Pharmasset. The Company’s response to the Demand was filed on August 14, 2009.

On December 6, 2010 a final arbitration award (the “Award”) was issued by a panel of AAA arbitrators. According to the Award, none of the payments the Company received under the Roche collaboration agreement were subject to the Emory License and, therefore, no license fees were owed to Emory based upon such payments. Furthermore, according to the Award, none of the other Company product candidates that were subject to the Demand are covered by the Emory License.

11. SUBSEQUENT EVENT

On January 26, 2011, the Company completed an underwritten public offering of 2,795,000 shares of the Company’s common stock, which includes the underwriter’s exercise in full of its over-allotment option of 495,000 shares and excludes 1,000,000 shares that were sold by selling stockholders, for a price to the public of $46.33 per share. The underwriter purchased the shares from the Company at a price of $44.25, pursuant to the underwriting agreement. The Company’s net proceeds from the sale of the shares, after deducting the underwriter’s discount and estimated offering expenses, was $123.4 million.

19

Table of Contents

| ITEM 2. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

The following discussion and analysis should be read together with our condensed financial statements and the related notes to those condensed financial statements included elsewhere in this Quarterly Report on Form 10-Q.

Overview

We are a clinical-stage pharmaceutical company committed to discovering, developing, and commercializing novel drugs to treat viral infections. Our primary focus is on the development of nucleoside/tide analogs as oral therapeutics for the treatment of chronic hepatitis C virus (“HCV”) infection. Nucleoside/tide analogs are a class of compounds which act as alternative substrates for the viral polymerase, thus inhibiting viral replication. We currently have three clinical-stage product candidates, two of which we are developing ourselves and one of which we are developing with a strategic partner. We are also advancing a series of preclinical candidates in preparation for clinical development. Our three clinical stage product candidates are:

| • | RG7128, an HCV cytosine nucleoside polymerase inhibitor we are developing through a strategic collaboration with F. Hoffmann-La Roche Ltd and Hoffmann-La Roche Inc. (collectively, “Roche”). In October 2010, Roche presented data from a 12-week interim analysis from the Phase 2b “PROPEL” study of RG7128 in combination with Pegasys® (pegylated interferon) plus Copegus® (ribavirin), the standard of care for treating HCV (“SOC”) in patients with HCV genotypes 1or 4. In addition, RG7128 is in a 24-week Phase 2b “JUMP-C” study in combination with SOC in patients with HCV genotypes 1 or 4. Roche is planning to conduct the next study of RG7128 in combination with ritonavir-boosted danoprevir. This “INFORM-SVR” study is part of a series of studies designed to investigate the combination of two oral, direct acting antivirals (“DAAs”) in the absence of pegylated interferon. Roche is also planning to conduct a Phase 2b study in patients with HCV genotypes 2 or 3. All of these studies are being, or are expected to be, conducted by Roche; |

| • | PSI-7977, an HCV uracil nucleotide analog polymerase inhibitor that is in a 12-week Phase 2b dose-finding study (“PROTON”) in combination with SOC in patients with HCV genotypes 1, 2 or 3. In addition, PSI-7977 recently began dosing in an exploratory Phase 2 study (“ELECTRON”) in combination with ribavirin, administered without and with varying durations of pegylated interferon, in patients with HCV genotypes 2 or 3. We expect to initiate a 24-week Phase 2b study of PSI-7977 in combination with SOC during the second calendar quarter of 2011; and |

| • | PSI-938, an HCV guanine nucleotide analog polymerase inhibitor that is enrolling patients in Part 2 of a Phase 1 study with PSI-7977 in patients with HCV genotype 1. We plan to initiate a Phase 2 study of PSI-938 in combination with PSI-7977 during mid (calendar year) 2011 |

In addition, we are developing PSI-661, an HCV guanine nucleotide analog polymerase inhibitor we nominated as a development candidate in October 2009. PSI-661 is in preclinical studies required for submission of an Investigational New Drug (“IND”) application with the U.S. Food and Drug Administration (“FDA”) or equivalent foreign regulatory application. PSI-938 or PSI-661 could potentially be used in combination with our current nucleoside/tide analogs, RG7128 or PSI-7977, as well as other classes of DAAs. Given the similarities of PSI-938 and PSI-661, our plan is to select one of these product candidates for later-stage clinical development based upon a review of the early human clinical trial results of both PSI-938 and PSI-661.

We are continuing to research nucleoside/tide analogs (both pyrimidines and purines) with the intention of identifying additional product candidates that can potentially be used in combination with our nucleoside/tides, RG7128 and PSI-7977, in combination with other classes of DAAs, or with SOC for the treatment of HCV. We have identified proprietary nucleotide prodrugs that are referred to as phosphate prodrugs because they have the ability to

20

Table of Contents

deliver the biologically available monophosphate forms of the compounds into infected liver cells, thus bypassing a rate-limiting step in the metabolic pathway to the active triphosphate form of the drug. The goal of these efforts is to identify compounds with improved potency, safety, convenience, oral bioavailability, and increased intrahepatic nucleotide triphosphate levels. Certain of these compounds have demonstrated exceptional in vitro anti-HCV activity, with up to 100 times greater potency than PSI-6130 (of which RG7128 is a prodrug). Early studies in animals indicate that several of these compounds can achieve concentrations of the active triphosphate form in the liver up to 1000 times higher than PSI-6130 at equivalent doses.

We are developing PSI-7977, PSI-938, and PSI-661 ourselves. We have a strategic collaboration with Roche for the development of PSI-6130 and its prodrugs, including RG7128. Under the collaboration, Roche pays all development costs associated with RG7128 and provides us with potential income from milestone payments that can be used to fund the advancement of our proprietary product candidates.

21

Table of Contents

Our Product Candidates

Our research and development programs are primarily focused on discovering and developing drugs that treat HCV. Our product candidates are nucleoside/tide analogs that we believe have potential competitive advantages with respect to safety, efficacy, drug resistance, and/or convenience of dosing as compared to currently approved drugs and other known investigational agents. The following table summarizes the four product candidates on which we are focusing:

| Product Candidate |

Status |

Next Expected Milestone(s) |

Commercialization Partner | |||

| RG7128 | • Completing the Phase 2b “PROPEL” study and 24-week Phase 2b “JUMP C” study in patients with HCV genotypes 1 or 4. • Planning for an INFORM-SVR study and a Phase 2b study in patients with HCV genotypes 2 or 3. All of the above studies are being, or are expected to be, conducted by Roche. |

• Initiate INFORM-SVR study during the first calendar quarter of 2011. • Initiate a Phase 2b study in patients with HCV genotypes 2 or 3 during the first half of calendar year 2011. • Initiate a Phase 3 program during 2011. • All of the above studies are expected to be conducted by Roche. |

Roche | |||

| PSI-7977 | • In a 12-week Phase 2b dose-finding “PROTON” study in combination with SOC in patients with HCV genotypes 1, 2, or 3. • In a Phase 2 exploratory study “ELECTRON” in combination with ribavirin, administered without and with varying durations of pegylated interferon, in patients with HCV genotypes 2 or 3. |

• Report SVR121 results from the ongoing genotype 2/3 arm of the Phase 2b “PROTON” study during the second calendar quarter of 2011. • Report 12 week interim analysis from the genotype 1 arms of the Phase 2b study “PROTON” during the second calendar quarter of 2011. • Report interim data from the Phase 2 exploratory study “ELECTRON” in combination with ribavirin in the second half of calendar year 2011. • Initiate a 24-week Phase 2b study in combination with SOC during the second calendar quarter of 2011. • Initiate proof of concept study of PSI-7977 in combination with BMS-790052 during the first half of 20112. |

— | |||

| PSI-938 | • In Part 2 of a 14 day Phase 1 study with PSI-7977 in patients with HCV genotype 1. |

• Report preliminary results from Part 2 of the Phase 1 study during the quarter ending March 31, 2011. • Initiate a Phase 2 combination study with PSI-7977 in mid (calendar year) 2011. |

— | |||

| PSI-661 | • In IND-enabling preclinical studies. |

• Submit IND application during the first calendar quarter of 2011. • Initiate a Phase 1 study during the second calendar quarter of 2011. |

— | |||

| 1 | SVR12 – Sustained virologic response 12, or SVR12, is defined as a level of HCV RNA in a patient that is below the limit of detection (<15 IU/ml) 12 weeks after the discontinuation of therapy. |

| 2 | During January 2011, we entered into a clinical collaboration agreement with Bristol-Myers-Squibb Company (“BMS”) to evaluate the utility of PSI-7977 in combination with BMS-790052, BMS’s NS5a replication complex inhibitor, for the treatment of HCV. BMS is responsible for all costs of the study, except for the cost of PSI-7977, which will be supplied by Pharmasset. Neither party has licensed any commercial rights to the other party. |

22

Table of Contents

Product Candidates for the Treatment of HCV

HCV Background

HCV is a leading cause of chronic liver disease and liver transplants. The World Health Organization estimates nearly 180 million people worldwide, or approximately three percent of the world’s population, are infected with HCV. About 130 million of these individuals are chronic HCV carriers who are at an increased risk of developing liver cirrhosis or liver cancer, approximately 15 million of whom are in the United States, Europe, and Japan. The Centers for Disease Control and Prevention (“CDC”) has reported that 4.1 million people in the United States have been infected with HCV, of whom 3.2 million are chronically infected. Of those chronically infected, the majority are undiagnosed and unaware of their HCV infection. Separately, approximately ten percent of diagnosed HCV patients in the United States are treated each year.

At least six major genotypes of HCV have been identified, each with multiple subtypes. Genotypes are designated with numbers (genotypes 1-6) and subtypes with letters. HCV genotypes 1, 2, 3, and 4 have a worldwide distribution, but their prevalence varies from one geographic area to another. Genotype 1 and its subtypes (1a and 1b) are the most common genotype globally, accounting for approximately 70% of infections. In the United States, approximately 67% and 33% of all of the genotype 1 HCV infections are subtypes 1a and 1b, respectively. Patients with genotype 2 or 3 represent approximately 25% of the worldwide chronically infected HCV population and the remaining five percent is comprised of genotypes 4 through 6. Worldwide sales of HCV drugs in 2005 were approximately $2.2 billion and are forecasted to reach more than $8.0 billion in 2015. Historically, sales of HCV drugs increase as new therapies are introduced that improve the sustained virologic response (“SVR”), defined as the inability to detect HCV RNA in a patient’s blood six months after discontinuation of therapy, with a standard polymerase chain reaction (“PCR”) test, which measures the amount of HCV in the blood.

Limitations of Current HCV Infection Therapy

The current standard of care for treating HCV is a combination of pegylated interferon plus ribavirin. Pegylated interferon is a modified version of alpha interferon, a protein that occurs naturally in the human body and boosts the immune system’s ability to fight viral infections. Roche, our collaboration partner in the development of RG7128, is the market leader in sales of pegylated interferon and branded ribavirin under the brand names Pegasys® and Copegus®, respectively.

Patients currently being treated for HCV are given pegylated interferon as a weekly injection, administered together with twice daily ribavirin tablets. The current SOC, however, has limitations that result in less than optimal SVR rates. Substantial side effects can render treatment intolerable for many patients. For example, SOC-treated patients can have difficulties with fatigue, bone marrow suppression, anemia, and neuropsychiatric effects. In addition, genotype 1 patients typically receive 48 weeks of SOC, but less than 50% of these patients achieve an SVR, which many physicians and patients consider a low rate of success. Between 60% and 80% of the genotype 2 and 3 patients treated with SOC for 24 weeks achieve an SVR. The occurrence of side effects combined with the inconvenient treatment regimen can result in many patients not completing therapy. Furthermore, a majority of individuals with HCV are unable to be treated with interferon due to contraindications, such as advanced liver disease or psychiatric conditions. The less than optimal antiviral efficacy, potential for dose-limiting side effects (some of which can be serious), contraindications, and inconvenient dosing regimen illustrate the unmet medical need of the currently available SOC. Current therapies may also not directly target the virus, suggesting additional patient benefit from agents which directly interfere with HCV replication.

Nucleoside/tide Analogs and Other Direct Acting Antivirals for HCV

HCV has several viral specific enzymes that are essential for its replication, thus providing multiple opportunities for therapeutic intervention. Many drug developers have focused on three of the HCV enzymes: a protease (“NS3”), the polymerase (“NS5b”) and more recently, another protein, “NS5a”. The goal of HCV drug development is to discover and develop molecules that have a high affinity for binding to these enzymes thereby inhibiting enzymatic activity and, in turn, inhibiting viral replication. These compound classes are often referred to as protease inhibitors and polymerase inhibitors. There are two types of polymerase inhibitors, each with a different

23

Table of Contents

mechanism of action. Nucleoside/tide analog polymerase inhibitors work by acting as alternative substrates that block the synthesis of HCV RNA, which is essential for the virus to replicate. The other type of polymerase inhibitor, non-nucleoside polymerase inhibitors, binds directly to the polymerase enzyme, causing a change in its shape. This conformational change inhibits its enzymatic activity.

Our research efforts focus on blocking HCV replication by discovering and developing nucleoside/tide analog polymerase inhibitors. A nucleoside is a basic building block of the nucleic acids, DNA and RNA, the genetic material of all living cells and viruses. Nucleosides consist of a molecule of sugar linked to a nitrogen-containing organic ring compound. In the most important naturally occurring nucleosides, the sugar is either ribose (used to construct RNA) or deoxyribose (used to construct DNA), and the nitrogen-containing organic ring compound, referred to as the base, is either a pyrimidine (cytosine, thymine, or uracil) or a purine (adenine or guanine). A nucleoside combined with a phosphate group becomes a nucleotide.