Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - BILL BARRETT CORP | d8k.htm |

Exhibit 99.1

|

Press Release |

For immediate release

Company contact: Jennifer Martin, Director of Investor Relations, 303-312-8155

Bill Barrett Corporation Announces

16% Increase in 2010 Proved Reserves and Provides 2011 Guidance

DENVER – February 3, 2011 – Bill Barrett Corporation (NYSE: BBG) announced today certain unaudited operating results for year-end 2010 and certain operating guidance for 2011. Highlights from 2010 include (unaudited):

| • | Proved reserve growth of 16% to 1.1 Tcfe, or 263% production replacement |

| • | Production growth of 8% to 96.5 Bcfe |

| • | Total estimated capital expenditures of $473 million |

| • | Finding and development costs of approximately $1.84 per Mcfe for 2010 or $1.76 per Mcfe three-year average (preliminary, see “Disclosure Statements” below) |

| • | Maintained strong balance sheet with zero drawn on $700 million line of credit |

Chairman, Chief Executive Officer and President Fred Barrett commented: “2010 challenged our team with low natural gas prices, increasing service costs and a difficult regulatory environment and, once again, our Bill Barrett team executed on all fronts. We received the Record of Decision for full field development at West Tavaputs and continued to drive efficiencies at our key Piceance asset achieving significant savings in drilling time and operating costs. We initiated a continuous development program at Blacktail Ridge, where rates of return on oil development are nearing 50%, and we continued with an active exploration program that provides a balanced, large scale exposure to unconventional oil and gas prospects. We successfully grew production and reserves while aligning our capital program with cash flow and generated low finding and development costs preliminarily estimated at $1.84 per thousand cubic feet equivalent (“Mcfe”). Our balance sheet and debt metrics are in excellent condition, and we entered 2011 with zero drawn on our credit facility. And, as a result of our excellent execution, our stock delivered a 32% return to our shareholders in 2010.

“Going forward, we expect similar macro headwinds in 2011, and again we are well positioned to manage these challenges. Our capital expenditure budget for 2011 is $525 to $565 million, allowing our team to initiate full field, year-round development at West Tavaputs. Full-scale development at West Tavaputs requires up front capital expenditures for facilities and infrastructure necessary for growth over the coming years. We recognize this as a large, lower cost, lower risk asset and are eager to grow reserves and production, while realizing further efficiency gains. Our capital budget range of $40 million is more sizable than in the past to accommodate possible increased exploration activities that may occur based upon results throughout the year. Our production guidance at 103 to 107 billion cubic feet equivalent (“Bcfe”) offers 7% to 11% growth, including nearly 40% growth in oil production. Currently, we have more than 50% of total production hedged at an average price of $7.58 per Mcfe and expect approximately 9% of 2011 production to be oil and approximately 10% of natural gas production to receive natural gas liquid (“NGL”) related pricing. We are approaching 2011 to maximize the long-term value of our ample portfolio of opportunities and to remain flexible to increase our pace through the drillbit, acquisitions or exploration success.”

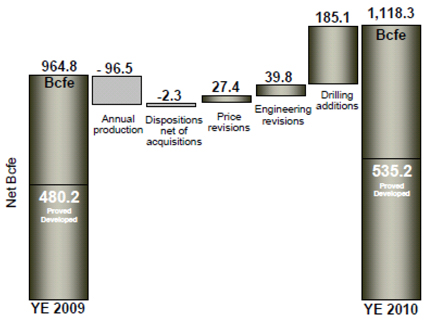

2010 YEAR-END ESTIMATED RESERVES, PRODUCTION AND CAPITAL EXPENDITURES

(The following information is unaudited and preliminary. Audited and final results will be provided in our Annual Report on Form 10-K for the year ended December 31, 2010 currently planned to be filed with the Securities and Exchange Commission (“SEC”) by the end of February 2011.)

The increase in 2010 reserves primarily reflects continued development at Gibson Gulch and growth from our Blacktail Ridge development project.

| Reserves |

Bcfe | |||

| 2009 year-end estimated proved reserves |

964.8 | |||

| 2010 estimated production |

(96.5 | ) | ||

| 2010 dispositions |

(3.7 | ) | ||

| 2010 reserve additions, including acquisitions and revisions |

253.7 | |||

| 2010 year-end estimated proved reserves |

1,118.3 | |||

| Production replacement ratio |

263 | % | ||

Year-end estimated proved reserves of 1,118.3 Bcfe were 93% natural gas and 7% oil. Further, estimated proved reserves were 48% developed and 52% undeveloped. The present value of proved reserves was estimated at $1.5 billion, before the effect of income taxes, based on a Colorado Interstate Gas (“CIG”) natural gas price of $3.95 per million British thermal units (“MMBtu”), a West Texas Intermediate (“WTI”) oil price of $75.96 per barrel and a 10% per annum discount rate. See “Disclosure Statements” below.

2

In addition to proved reserves, the Company estimates it has probable and possible reserves of 1.4 trillion cubic feet equivalent (“Tcfe”) at December 31, 2010 for total proved, probable and possible reserves of approximately 2.5 Tcfe. See “Reserve Disclosure” note below.

Pricing Sensitivities

The Company believes it is helpful to consider price sensitivities to the proved reserve calculation due to fluctuations and long-term trends in commodity prices. In the following table, “PV10” represents the present value of our proved reserves, pretax, using a 10% discount rate. For context, the five-year strip price as of December 31, 2010 averaged $4.76 per MMBtu CIG natural gas and $93.08 per barrel WTI oil:

| Commodity Price |

Natural Gas |

Oil |

Bcfe |

PV10 |

||||||||||||

| (Bcf) | (MMbbls) | (in millions) | ||||||||||||||

| 2010: $3.95 gas, $75.96 oil |

1,040 | 13.0 | 1,118 | $ | 1,496 | |||||||||||

| +$1.00/$10: $4.95 gas, $85.96 oil |

1,048 | 13.3 | 1,127 | $ | 2,261 | |||||||||||

| +$2.00/$20: $5.95 gas, $95.96 oil |

1,053 | 13.4 | 1,133 | $ | 3,028 | |||||||||||

| • | Commodity prices up $1.00 per MMBtu and $10.00 per barrel to $4.95 per MMBtu and $85.96 per barrel, respectively: Applying these modified commodity prices to 2010 reserves, proved reserves would have been up slightly to 1,127 Bcfe with a present value of $2.3 billion, before the effect of income taxes. |

| • | Commodity prices up $2.00 per MMBtu and $20.00 per barrel to $5.95 per MMBtu and $95.96 per barrel, respectively: Applying these modified commodity prices to 2010 reserves, proved reserves would have been 1,133 Bcfe with a present value of $3.0 billion, before the effect of income taxes. |

Production

Estimated production for 2010 was 96.5 Bcfe and was comprised of 93% natural gas and 7% oil. Of natural gas production, approximately 88% was sold as dry gas and approximately 12% was processed, resulting in a benefit from higher prices related to natural gas liquids than dry gas. Estimated fourth quarter 2010 production was 24.2 Bcfe, up 6% from 22.8 Bcfe in the fourth quarter of 2009. Fourth quarter 2010 production was down sequentially from 25.5 Bcfe in the third quarter, primarily due to refinery and infrastructure downtime that affected production from the Company’s Blacktail Ridge project as well as the delayed timing of certain well completions.

Capital Expenditures

Preliminary, unaudited capital expenditures for 2010 were $473.3 million, slightly less than the most recent guidance range of $475 to $485 million. The following is a summary of proved reserves at December 31, 2010 and unaudited production and capital expenditures for 2010 for each of our primary development areas:

3

| Year-ended December 31, 2010 | ||||||||||||

| Basin |

Reserves | Production | Capital Expenditures |

|||||||||

| (Bcfe) | (Bcfe) | (in millions) | ||||||||||

| Piceance |

634.3 | 48.1 | $ | 270 | ||||||||

| Uinta |

386.9 | 27.7 | 143 | |||||||||

| Powder River-CBM |

60.8 | 13.4 | 12 | |||||||||

| Wind River |

34.7 | 6.9 | 8 | |||||||||

| Other |

1.6 | 0.4 | 40 | |||||||||

| Totals |

1,118.3 | 96.5 | $ | 473 | ||||||||

Other

Under successful efforts accounting, the Company expects to record impairment, dry hole and abandonment expenses in the fourth quarter of 2010 estimated at approximately $36 million (pre-tax), of which approximately $19 million relates to exploratory dry holes and approximately $16 million relates to impairment of undeveloped leaseholds. The dry hole expenses are primarily the result of sub-economic performing wells in the Yellow Jacket prospect in the Paradox Basin as well as unsuccessful fracture stimulations in deep testing of the Mesaverde formation in the Big Horn Basin. The impairment expenses relate to several exploration properties. For the full year 2010, impairment, dry hole and abandonment expenses are estimated at $45 million (unaudited).

2010 YEAR-END DEBT AND LIQUIDITY

The Company had no amounts drawn on its revolving credit facility at December 31, 2010. The revolving credit facility has commitments totaling $700.0 million and a borrowing base of $800.0 million. Including an outstanding letter of credit for $26.0 million, the Company had $674.0 million of borrowing capacity at December 31, 2010. The Company expects to draw from its revolving credit facility during 2011 as capital expenditures are expected to exceed cash flows from operations. The Company also had $172.5 million of convertible senior notes and $250.0 million in 9.875% senior notes outstanding at December 31, 2010.

2011 OPERATING GUIDANCE

The Company plans to spend between $525 and $565 million for capital expenditures in 2011 for exploration and development programs, including facilities costs predominantly associated with growth at the West Tavaputs development project as the Company initiates full field, year-round development. The Company expects to drill approximately 215 gross development wells in 2011, which will include approximately 100 wells at West Tavaputs, 30-40 wells at Gibson Gulch, approximately 50 wells at Blacktail Ridge-Lake Canyon and approximately 30 wells in the Powder River CBM. Capital expenditures are expected to be allocated approximately 85% for development projects and concentrated in West Tavaputs where the Company plans to drive substantial growth in production and reserves as well as implement drilling and operating efficiencies similar to those in its Gibson Gulch program. Up to approximately 15% of capital will be allocated toward exploration and delineation activities, for which total expenditures will depend upon results from exploration activities. At year-end 2010, the Company had 50 wells drilled to be completed during 2011.

4

The Company is providing the following guidance for its 2011 activities. See “Forward-Looking Statements” below.

| 2011 Capital Expenditures, Production and Costs Guidance |

||||

| Capital expenditures before the effect of significant acquisitions or divestitures (in millions) |

$525 - $565 | |||

| Production (Bcfe) |

103 – 107 | |||

| Operating costs per unit (per Mcfe) |

||||

| Lease operating |

$ | 0.58 - $0.62 | ||

| Gathering, processing & transportation |

$ | 0.89 - $0.94 | ||

| General & administrative expenses excluding non-cash, stock-based compensation (in millions) |

$45.0 - $47.0 | |||

Gathering, processing and transportation expense is expected to increase over previous years primarily due to firm transportation charges on interstate pipelines (specifically, the expected start-up of the Ruby pipeline.).

COMMODITY HEDGES UPDATE

The Company has hedges in place for approximately 50% of forecast 2011 production. Natural gas hedges are predominantly tied to Rocky Mountain regional pricing. Generally, it is the Company’s strategy to hedge 50% to 70% of production through basis at regional sales points on a forward 12-month basis in order to reduce the risks associated with unpredictable future natural gas and oil prices and to provide certainty for a portion of its cash flow to support its capital expenditure program.

The following table summarizes hedge positions as of January 31, 2011:

| SWAPS & COLLARS |

||||||||||||||||||||||||

| Period |

Natural Gas /NGLs | Oil | EQUIVALENT | |||||||||||||||||||||

| Volume MMBtu/d |

Price $/MMBtu |

Volume Bbl/d |

Price $/Bbl |

Volume Mmcfe |

Price $/Mcfe |

|||||||||||||||||||

| 1Q11 |

152,075 | $ | 6.72 | 1,866 | $ | 90.20 | 13,450 | $ | 7.96 | |||||||||||||||

| 2Q11 |

162,511 | $ | 6.18 | 2,100 | $ | 90.83 | 14,591 | $ | 7.45 | |||||||||||||||

| 3Q11 |

161,267 | $ | 6.16 | 2,100 | $ | 90.83 | 14,647 | $ | 7.43 | |||||||||||||||

| 4Q11 |

129,461 | $ | 6.08 | 2,100 | $ | 90.83 | 11,987 | $ | 7.50 | |||||||||||||||

| 1Q12 |

55,000 | $ | 4.55 | 200 | $ | 95.43 | 4,659 | $ | 5.26 | |||||||||||||||

| 2Q12 |

55,000 | $ | 4.55 | 200 | $ | 95.43 | 4,659 | $ | 5.26 | |||||||||||||||

| 3Q12 |

55,000 | $ | 4.55 | 200 | $ | 95.43 | 4,710 | $ | 5.26 | |||||||||||||||

| 4Q12 |

41,739 | $ | 4.59 | 200 | $ | 95.43 | 3,601 | $ | 5.39 | |||||||||||||||

5

In addition, the Company has basis only hedges in place for 2011 and 2012, which hedge the price difference between CIG and NYMEX natural gas prices, none of which currently is in the money. For 2011, the Company has hedged 20,000 MMBtu/d at a basis differential price of ($1.72), and in 2012 the Company has hedged 20,000 MMBtu/d at a basis differential price of ($1.22).

UPCOMING EVENTS

Investor Presentation Update

The Company intends to post an updated investor presentation on Thursday, February 3, 2011 at 5:00 p.m. Mountain time. Updated investor presentations are posted on the homepage of the Company’s website at www.billbarrettcorp.com.

Credit Suisse Conference

Chairman and CEO Fred Barrett plans to present at the Credit Suisse Energy Summit 2011 on Friday, February 11, 2011 at 8:10 a.m. Mountain time. The event will be webcast and may be accessed live and for replay on the Company’s website. The Company will post an investor presentation to be used for this event on Tuesday, February 8, 2011 at 5:00 p.m. Mountain time.

2010 Fourth Quarter and Full Year Results Release

The Company intends to release its fourth quarter and full year 2010 results on Wednesday, February 23, 2011 before the market opens and host a webcast and conference call at noon eastern time the same day. Please join Bill Barrett Corporation executive management for the webcast and call for an update on operations and strategy for 2011. The webcast may be accessed at www.billbarrettcorp.com or the call-in number is 866-788-0544 (857-350-1682) with passcode 19887539. A replay of the call will also be available through February 28, 2011 at call-in number 888-286-8010 (617-801-6888) with passcode 15024076.

DISCLOSURE STATEMENTS

Finding and Development Cost

Finding and development cost is a non-GAAP metric commonly used in the exploration and production industry. Calculations presented by the Company are based on costs incurred, as adjusted by the Company, divided by reserve additions. Reconciliation of adjustments to costs incurred is provided in the Company’s earnings release and Form 8-K issued February 23, 2010. The 2010 year-end estimate provided in this release is based on the same calculation method and the unaudited, preliminary results submitted above. The final 2011 reconciliation will be provided in the press release planned for February 23, 2011.

PV10

The present value of the cash flows from proved reserves, before the effect of income taxes and discounted at 10% per annum, or PV10, is a commonly used metric in the exploration and production industry.

6

Reserve Disclosure

The SEC, under its recently revised guidelines, permits oil and gas companies to disclose probable and possible reserves in their filings with the SEC. The Company does not plan to include probable and possible reserve estimates in its filings with the SEC.

The Company has provided internally generated estimates for probable and possible reserves in this release. The estimates conform to SEC guidelines. They are not prepared or reviewed by third party engineers. Our probable and possible reserve estimates are determined using strip pricing which we use internally for planning and budgeting purposes. The Company’s estimate of probable and possible reserves is provided in this release because management believes it is useful, additional information that is widely used by the investment community in the valuation, comparison and analysis of companies. U.S. investors are urged to consider closely the disclosure in our Annual Report on Form 10-K for the year ended December 31, 2009, available on the Company’s website at www.billbarrettcorp.com or from the corporate offices at 1099 18th Street, Suite 2300, Denver, CO 80202. You can also obtain this form from the SEC by calling 1-800-SEC-0330 or at www.sec.gov.

Forward-Looking Statements

This press release contains forward-looking statements, including statements regarding projected results and future events. In particular, the Company is providing “2011 Guidance,” which contains projections for certain 2011 operational and financial results. These forward-looking statements are based on management’s judgment as of this date and include certain risks and uncertainties. Please refer to the Company’s Annual Report on Form 10-K for the year-ended December 31, 2009 filed with the SEC, and other filings including our Current Reports on Form 8-K and Quarterly Reports on Form 10-Q, for a list of certain risk factors. The Company also provides unaudited estimates of certain year-end results, which are subject to revision in our audited financial statements to be included in our Annual Report on Form 10-K to be filed in February 2011.

Actual results may differ materially from Company projections and can be affected by a variety of factors outside the control of the Company including, among other things, market conditions, oil and gas price volatility, exploration drilling and testing results, the ability to receive drilling and other permits, regulatory approvals, governmental laws and regulations and changes in enforcement of those laws and regulations, new laws and regulations, risks related to and costs of hedging activities including counterparty viability, surface access and costs, availability of third party gathering, transportation and processing, the availability and cost of services and materials, the ability to obtain industry partners to jointly explore certain prospects and the willingness and ability of those partners to meet capital obligations when requested, availability and costs of financing to fund the Company’s operations, uncertainties inherent in oil and gas production operations and estimating reserves, the speculative actual recovery of estimated potential volumes, unexpected future capital expenditures, competition, risks associated with operating in one major geographic area, the success of the Company’s risk management activities, title to properties, litigation, environmental liabilities, and other factors discussed in the Company’s reports filed with the SEC. Bill Barrett Corporation encourages readers to consider the risks and uncertainties associated with projections and other forward-looking statements. In addition, the Company assumes no obligation to publicly revise or update any forward-looking statements based on future events or circumstances.

7

ABOUT BILL BARRETT CORPORATION

Bill Barrett Corporation (NYSE: BBG), headquartered in Denver, Colorado, explores for and develops natural gas and oil in the Rocky Mountain region of the United States. Additional information about the Company may be found on its website www.billbarrettcorp.com.

8