Attached files

| file | filename |

|---|---|

| EX-2.1 - TEEN EDUCATION GROUP, INC. | v208786_ex2-1.htm |

| EX-10.1 - TEEN EDUCATION GROUP, INC. | v208786_ex10-1.htm |

| EX-99.3 - TEEN EDUCATION GROUP, INC. | v208786_ex99-3.htm |

| EX-10.9 - TEEN EDUCATION GROUP, INC. | v208786_ex10-9.htm |

| EX-10.3 - TEEN EDUCATION GROUP, INC. | v208786_ex10-3.htm |

| EX-10.4 - TEEN EDUCATION GROUP, INC. | v208786_ex10-4.htm |

| EX-16.1 - TEEN EDUCATION GROUP, INC. | v208786_ex16-1.htm |

| EX-10.5 - TEEN EDUCATION GROUP, INC. | v208786_ex10-5.htm |

| EX-10.6 - TEEN EDUCATION GROUP, INC. | v208786_ex10-6.htm |

| EX-10.8 - TEEN EDUCATION GROUP, INC. | v208786_ex10-8.htm |

| EX-10.2 - TEEN EDUCATION GROUP, INC. | v208786_ex10-2.htm |

| EX-99.4 - TEEN EDUCATION GROUP, INC. | v208786_ex99-4.htm |

| EX-99.2 - TEEN EDUCATION GROUP, INC. | v208786_ex99-2.htm |

| EX-99.1 - TEEN EDUCATION GROUP, INC. | v208786_ex99-1.htm |

| EX-10.7 - TEEN EDUCATION GROUP, INC. | v208786_ex10-7.htm |

| EX-14.1 - TEEN EDUCATION GROUP, INC. | v208786_ex14-1.htm |

| EX-10.10 - TEEN EDUCATION GROUP, INC. | v208786_ex10-10.htm |

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

WASHINGTON,

D.C. 20549

FORM

8-K/A

Amendment

No. 1

CURRENT

REPORT

Pursuant

to Section 13 or 15(d) of the

Securities

Exchange Act of 1934

Date of

report (Date of earliest event reported): November 12 , 2010

|

TEEN

EDUCATION GROUP, INC.

|

|

(Exact

name of registrant as specified in its

charter)

|

|

Delaware

|

333-147045

|

26-032648

|

||

|

(State

or other jurisdiction

of

incorporation)

|

(Commission

File Number)

|

(I.R.S.

Employer

Identification

No.)

|

|

NO.

288 Maodian Road

Liantang

Industrial Park, Qingpu District

Shanghai,

PRC

|

|

(Address

of principal executive

offices)

|

|

+86

21-39252120

|

|

(Registrant’s

telephone number,

including

area code)

|

|

6767

W. Tropicana Ave., Suite 207

|

|

Las

Vegas, NV 89103

|

|

(Former

name or former address,

if

changed since last

report)

|

Check the

appropriate box below if the Form 8-K filing is intended to simultaneously

satisfy the filing obligation of the registrant under any of the following

provisions (see General Instruction A.2. below):

¨

Written communications pursuant to Rule 425

under the Securities Act (17 CFR 230.425)

¨

Soliciting material pursuant to Rule 14a-12

under the Exchange Act (17 CFR 240.14a-12)

¨

Pre-commencement communications pursuant to

Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b))

¨

Pre-commencement communications pursuant to

Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c))

CAUTIONARY NOTE REGARDING

FORWARD-LOOKING STATEMENTS

This

Current Report on Form 8-K contains forward looking statements that involve

risks and uncertainties, principally in the sections entitled “Description of

Business,” “Risk Factors,” and “Management’s Discussion and Analysis of

Financial Condition and Results of Operations,” and those discussed in other

documents we file with the U.S. Securities and Exchange Commission that are

incorporated into this Current Report on Form 8-K by reference. All statements

other than statements of historical fact contained in this Current Report on

Form 8-K, including statements regarding future events, our future financial

performance, business strategy, and plans and objectives of management for

future operations, are forward-looking statements. We have attempted to identify

forward-looking statements by terminology including “anticipates,” “believes,”

“can,” “continue,” “could,” “estimates,” “expects,” “intends,” “may,” “plans,”

“potential,” “predicts,” “should,” or “will” or the negative of these terms or

other comparable terminology. We have based these forward-looking statements

largely on our current expectations and projections about future events and

financial trends that we believe may affect our financial condition, results of

operations, business strategy, short term and long term business operations, and

financial needs. Although we do not make forward-looking statements unless we

believe we have a reasonable basis for doing so, we cannot guarantee their

accuracy. These statements are only predictions and involve known and unknown

risks, uncertainties and other factors, including the risks outlined under “Risk

Factors” or elsewhere in this Current Report on Form 8-K, which may cause our or

our industry’s actual results, levels of activity, performance or achievements

expressed or implied by these forward-looking statements. Moreover, we operate

in a very competitive and rapidly changing environment. New risks emerge from

time to time and it is not possible for us to predict all risk factors, nor can

we address the impact of all factors on our business or the extent to which any

factor, or combination of factors, may cause our actual results to differ

materially from those contained in any forward-looking statements.

You

should not place undue reliance on any forward-looking statement, each of which

applies only as of the date of this Current Report on Form 8-K. Before you

invest in our common stock, you should be aware that the occurrence of the

events described in the section entitled “Risk Factors” and elsewhere in this

Current Report on Form 8-K could negatively affect our business, operating

results, financial condition and stock price. Except as required by law, we

undertake no obligation to update or revise publicly any of the forward-looking

statements after the date of this Current Report on Form 8-K to conform our

statements to actual results or changed expectations.

EXPLANATORY

NOTE

This

Amendment No. 1 on Form 8-K/A (the “8-K/A”) amends and restates in its entirety

the Current Report on Form 8-K for Teen Education Group, Inc. (the “Company”)

dated and filed with the Securities and Exchange Commission on November 12, 2010

(the “Original 8-K”) to amend certain disclosures and to include updated

financial information of Hongkong Charter International Group, Limited, which

the Company recently acquired through a reverse merger transaction, for the

quarter ended September 30, 2010 and the parent-only financial statements as a

supplement to the unaudited condensed consolidated financial statements.

Item

1.01 Entry into a Material Definitive Agreement.

As more

fully described in Item 2.01 below, Teen Education Group, Inc. (“we,” “us,”

“our,” “Teen Education” or the “Company”), a Delaware corporation, acquired an

automotive parts distribution company in accordance with a share exchange

agreement, dated November 12, 2010 (the “Exchange Agreement”), by and among the

Company, Robert L. Wilson, the majority shareholder of the Company (the

“Majority Shareholder”), Hongkong Charter International Group Limited, a

Hongkong company (“Hongkong Limited”), and the sole shareholder of Hongkong

Limited (the “Hongkong Limited Shareholder”). Hongkong Limited was incorporated

in Hongkong on August 21, 2009 and owns 100% of the issued and outstanding

capital stock of Shanghai Vomart Auto Parts Co., Ltd. (“Vomart”), which was

incorporated as a People’s Republic of China (“PRC” or “China”) limited

liability company on January 4, 2008, and became a wholly foreign owned

enterprise under the laws of the PRC on May 12, 2010. A copy of the Exchange

Agreement is included as Exhibit 2.1 to this Current Report on Form 8-K/A and is

hereby incorporated by reference. All references to the Exchange Agreement and

other exhibits to this Current Report on Form 8-K are qualified, in their

entirety, by the text of such exhibits.

The

closing of the transaction (the “Closing”) took place on November 12, 2010 (the

“Closing Date”). On the Closing Date, pursuant to the terms of the Exchange

Agreement, the Company acquired all of the outstanding shares of Hongkong

Limited from the Hongkong Limited Shareholder (the “Hongkong Limited Shares”).

In exchange, we issued to the Hongkong Limited Shareholder, their designees or

assigns, 2,250,000 shares of the Company’s

common stock (the “Exchange Shares”). The Exchange Shares represent

90% of the issued and outstanding shares of the Company’s common stock on a

fully diluted basis as of and immediately after the Closing (the “Share

Exchange”). In addition, Hongkong Limited agreed to pay $350,000 in cash to the Majority

Shareholder.

Pursuant

to the terms of the Exchange Agreement, the Majority Shareholder canceled a

total of 2,000,000 shares of the Company’s common stock, which represents 100%

of his security interests in the Company.

Pursuant

to the Exchange Agreement, Hongkong Limited became a wholly owned subsidiary of

the Company. The sole director of the Company approved the Exchange Agreement

and the transactions contemplated under the Exchange Agreement. The directors of

Hongkong Limited approved the Exchange Agreement and the transactions

contemplated under the Exchange Agreement.

As a

further condition of the Share Exchange, on the Closing Date, Robert L. Wilson

resigned as the sole director of the Company, effective on such date that is ten

(10) calendar days after the Company mails an Information Statement to the

Company’s shareholders prepared pursuant to Rule 14f-1 under the Securities

Exchange Act of 1934, as amended (the “Exchange Act”), relating to the Exchange

Agreement, and further, appointed Qun Hu to the Company’s board of directors

(the “Board”). Mr. Wilson also resigned on the Closing Date as the sole officer

of the Company, effective as of the Closing Date, and the following persons were

appointed as officers of our Company: Mr. Zhoufeng Shen was appointed as the

Company’s President and Chief Executive Officer and Ms. Xiaomei Wang was

appointed as the Company’s Chief Financial Officer.

Item 2.01

Completion of Acquisition or Disposition of Assets.

On the

Closing Date, the Company completed an acquisition of Hongkong Limited pursuant

to the Exchange Agreement. The acquisition was accounted for as a

recapitalization effected by a share exchange, wherein, Hongkong Limited is

considered the acquirer for accounting and financial reporting purposes. The

assets and liabilities of the acquired entity have been brought forward at their

book value and no goodwill has been recognized.

2

FORM

10 DISCLOSURE

As

disclosed throughout this Current Report on Form 8-K, on the Closing Date, the

Company acquired Hongkong Limited in a reverse acquisition transaction. Item

2.01(f) of Form 8-K states that if the registrant was a shell company

immediately before the reverse acquisition transaction disclosed under Item

2.01, then the registrant must disclose the information that would be required

if the registrant were filing a general form for registration of securities on

Form 10.

Since

Teen Education Group, Inc. was a shell company immediately before the reverse

acquisition transaction disclosed under Item 2.01, we are providing below the

information that would be included in a Form 10 if we were to file a Form 10.

Please note that the information provided below relates to the combined

enterprises after the acquisition of Teen Education Group, Inc., except that

information relating to periods prior to the date of the reverse acquisition

only relate to Hongkong Limited and its consolidated subsidiaries unless

otherwise specifically indicated.

Our

Corporate History and Background

We were

organized under the laws of the State of Delaware on April 16, 2007. From

inception until the Closing Date, we were primarily engaged in the business

of providing a financial literacy and money

management educational program for teenagers on a fee for service

offered basis.

Acquisition

of Hongkong Limited

On the

Closing Date, we acquired Hongkong Limited, which is in the business of

automotive parts distribution in the PRC. On the Closing Date,

pursuant to the terms of the Exchange Agreement, we acquired all of the Hongkong

Limited Shares from the Hongkong Limited Shareholder, and the Hongkong Limited

Shareholder transferred and contributed all of the Hongkong Limited Shares to

us. In exchange, we issued the Exchange Shares to the Hongkong Limited

Shareholder, their designees or assigns.

Pursuant

to the terms of the Exchange Agreement, the Majority Shareholder canceled

2,000,000 shares of common stock of our Company, which constituted 100% of his

security interests in the Company. Following the Share Exchange, there are

2,500,000 shares of common stock issued and outstanding, 2,250,000 of which are

restricted and issued to the Hongkong Limited Shareholder, their designees or

assigns.

We have

relocated our principal executive offices to NO. 288 Maodian Road, Liantang

Industrial Park, Qingpu District, Shanghai, PRC, and our new telephone number is

+86 21-39252120.

DESCRIPTION

OF BUSINESS

Business

Overview

We are

one of the largest distributors of automotive replacement parts and accessories

in the PRC based on the number of stores we own and the geographic areas where

we have presence. We began our operations in 2008 and currently own

thirty-seven (37) stores in nine (9) provinces and municipalities, namely

Jiangsu, Zhejiang, Hebei, Anhui, Fujian, Shanxi, Shanghai, Beijing, and

Tianjin. In comparison, other large auto parts distributors in China

own fewer stores and/or their stores are located in fewer provinces or

municipalities. For example, Shandong Youpei Auto Parts owns

twenty-four stores of which eighteen are located in Shangdong

Province. Jiangsu Youpei Auto Parts owns seventeen

stores of which sixteen are located in Jiangsu Province. Putong Auto

Service owns fifteen stores in thirteen different provinces and

municipalities. We distribute a broad selection of international

brand name (such as Philips, Mahle, Denso, Bosch and Osr) and private label

(such as Olande, Vanik, Mikef and Shengf) automotive replacement parts, such as,

accessories and maintenance items for cars, minivans, vans, sport utility

vehicles, light trucks, and heavy-duty trucks. Our typical products include

batteries, brake pads, filters, storage batteries, and transmission

fluid.

Historical

Sales & Income Summary

|

(Amounts expressed in USD)

|

Three month Period Ended

September 30,

|

Fiscal Year Ended

June 30,

|

||||||||||||||||||||||

|

|

2010

|

2009

|

%

Growth

|

2010

|

2009

|

%

Growth

|

||||||||||||||||||

|

Revenue

|

$ | 2,762,293 | $ | 1,029,888 | 168.2 | % | $ | 4,782,754 | $ | 1,282,918 | 272.8 | % | ||||||||||||

|

Gross

Profit

|

529,680 | 275,879 | 92.0 | % | 1,245,800 | 365,589 | 240.8 | % | ||||||||||||||||

|

Net

Income

|

$ | 24,228 | $ | 15,650 | 54.8 | % | $ | 38,514 | $ | 79,890 | (51.8 | )% | ||||||||||||

3

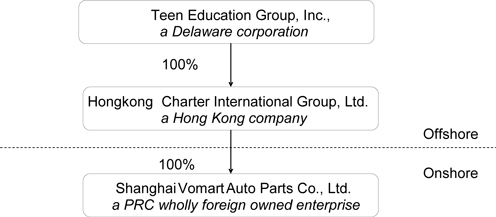

Corporate

Organization

After the

Share Exchange, we have approximately 80 shareholders of our

common stock. Our organizational structure was developed to allow

foreign capital infusion under the laws of the PRC and maintain an efficient tax

structure, as well as maintain internal organizational efficiencies. Our

organizational structure after the consummation of the Share Exchange is

illustrated in the table below:

Business

Strategy

Our

indirect wholly-owned subsidiary, Vomart, was incorporated in the PRC on January

4, 2008, and become a wholly-owned foreign enterprise under the laws of the PRC

on May 12, 2010.

We are

committed to providing customers with superior service, value, and quality

automotive parts and products at conveniently located, well-designed, and

unified stores. We intend to be one of China’s leading and largest national

chain auto parts distributor within the next five (5) years by, among other

things, providing a highly efficient distribution network integrating upstream

suppliers and downstream end users, growing organically through aggressively

marketing our existing stores (each of which we wholly own), opening new stores,

and strategic acquisitions of regional vendors that meet our quality

standards. By 2015, we plan to expand our distribution network to

cover two thirds (2/3) of China, covering 27 different provinces and

municipalities. The total number of automotive vehicles in China continues to

grow at a rapid pace, which directly relates to the need for an increase of

aftermarket auto parts.

In order

to boost the Company’s market share, we intend to:

|

|

·

|

Achieve a national scale and

penetrate the auto parts market by growing the number of wholly owned

stores to over 250 stores and the number of franchise stores to 300

franchise stores within five years. As a terminal market distributor, our

market strategy is to cover the market as fast as possible. Depending on

the gross domestic product (“GDP”) and the market capacity of different

areas, we plan to open 1-2 wholly-owned stores in the prefecture-level

cities and 2-5 wholly-owned stores in the capital cities. At the same

time, we will grow our market share by opening franchise stores in the

county level cities and less developed

areas;

|

|

|

·

|

Build an efficient first-class

distribution and logistics system that is effectively managed by

constantly improving our Enterprise Resource Planning (as defined herein)

software;

|

|

|

·

|

Provide a broad selection of

brand name replacement parts and a complete line of private-label

products; and

|

|

|

·

|

Build a national and well-known

brand name in the China automotive replacement market through intensive

marketing campaigns.

|

Therefore,

our strategies are to capitalize on our competitive advantages, expand our

current market penetration, and benefit from the anticipated rapid growth in

China’s automotive replacement market.

4

Industry

and Market Analysis

Fast

Growing China Automotive Market

China has

experienced rapid economic growth in the last 20 years and is currently the

world’s second largest economy after the United States. In 2009, China achieved

a GDP of USD $5.2 trillion. According to the China State Statistics Bureau, by

2013, China’s automotive market is expected to comprise over ten percent (10%)

of global automotive sales.

Today,

all of the world’s major automakers are present in China, including but not

limited to, Ford, General Motors, Volkswagen, Toyota, Honda, and Chrysler.

China’s automotive industry has shown double-digit growth in terms of percentage

growth in recent years and such robust growth is expected to continue. There are

several key drivers that fuel China’s future growth, such as government policy,

higher disposable income of urban residents, infrastructure improvement, and

rapid proliferation of car models.

China

Automotive Replacement Market

The China

automotive replacement market is experiencing significant growth alongside the

rapid growth of China’s automotive market. Some of the key growth drivers

include:

|

|

·

|

Increase

in Vehicle Population – According to the Xinhua News

Agency, the vehicle population grew to over 76.19

million vehicles as of the end of 2009, and is forecasted to rise to 200

million vehicles by 2020 at an average annual growth rate of approximately

20%;

|

|

|

·

|

Increase

in the Number of Cars that are Between Four and Seven Years

Old – As a result of

the large sales in the last decade, the vehicles in China are relatively

new, but more and more vehicles are owned in the PRC between four and

seven years. We expect to see more repairs and maintenance needed as

vehicles grow older, leading to the generation of more replacement sales;

and

|

|

|

·

|

Breadth

of Automotive Parts Needed – For a replacement market

distributor/retailer to serve the largest possible market, it has to have

the scale and the capacity to carry an extensive line of products. We see

American, Japanese, Korean and other foreign original equipment

manufacturers (OEMs) bring a great variety of vehicle technologies and car

models into China. This complicates and challenges the young and immature

China automotive replacement market. We are able to serve the largest

possible market, and have the scale and capacity to carry an extensive

line of products.

|

Growth

Strategy

We

believe that we are positioned to be a leading national distributor of

automotive replacement parts in China. We plan to first build store networks by

opening wholly-owned stores in capital cities throughout China, such as

Shanghai, Beijing, Hangzhou, Nanjing, Shijiazhuang, Hefei, and Fuzhou that will

provide middle-to-high end brand name products as well as a wide selection of

private label products.

We

believe that automotive parts chain stores like us which have multiple locations

have competitive advantages in customer service, product offerings, marketing,

and distribution, as compared to independent retailers. This allows

us to address and effectively respond to the following trends:

|

|

·

|

The need for the ability to

provide a broad selection of brands and replacement/maintenance

items;

|

|

|

·

|

The phase out of the prevailing

brand dealership as the primary distribution channel for automotive

replacement parts; and

|

|

|

·

|

The need for an automotive

replacement parts chain operation to consolidate and regulate the market

disorganization and fragmentation of the China automotive

aftermarket.

|

Aggressively

Open New Stores in New Markets

We intend

to aggressively open new stores and acquire/consolidate with, regional

distributors to achieve penetration in more geographic locations. As a result,

we plan to open approximately 40 stores by the end of 2010 and 250

stores by 2014.

Our

selection process begins by targeting provincial capitals/large markets for

expansion of our store networks. Such current target markets

include Shanghai City and Jinan City in Shandong Province, Guangzhou City

in Guangdong Province, Chengdu City in Sichuan Province and Zhengzhou City in

Henan Province. While we have faced, and expect to continue to face,

aggressive competition in the more densely populated markets, we believe that we

have competed effectively in certain developed coastal areas in China, such as

Shanghai City, Zhejiang, and Jiangsu Provinces, and that we are well

positioned to continue to compete effectively in such markets. Once we have a

well-established presence in our selected capital cities (Hangzhou, Fuzhou,

Shijiazhuang, and Hefei), we will start to penetrate into second tier cities

such as Qingdao, Weifang, and Yantai in Shandong Province, and

Shenzhen, Dongguan, and Foshan in Guangdong Province.

5

To date,

we have been successful in locating suitable sites for the construction of new

stores. We typically open new stores by constructing the store at a site we

lease. Then, according to our Company’s inventory control (IC) system,

we stock the new store with furniture and inventory and hire and train

employees to complete the opening of our new stores.

We choose

store sites that are strategically located in clusters within geographic areas

that complement our distribution system in order to achieve economies of scale

in management, advertising, and distribution costs. Other key factors we

consider in the site selection process include:

|

|

·

|

projected future

profitability;

|

|

|

·

|

cost of real

estate;

|

|

|

·

|

population density and growth

patterns;

|

|

|

·

|

administrative level of the

city;

|

|

|

·

|

transportation

infrastructure;

|

|

|

·

|

local GDP and “R ratio” (vehicle

price/per capita GDP);

|

|

|

·

|

demographics such as age and per

capita income;

|

|

|

·

|

vehicle counts and vehicle

profiles;

|

|

|

·

|

the number and type of existing

automotive repair

facilities;

|

|

|

·

|

the number and type of customers

(such as automotive repair facilities) to be served;

and

|

|

|

·

|

the number of other retail auto

parts competitors within a pre-determined radius and the operational

strength of such

competitors.

|

Same

Store Sales Growth

We will

constantly improve our service and product mix to achieve higher sales and

profitability in our existing stores. We believe that superior customer service

generates customer satisfaction, which ultimately generates increased sales. To

increase our profitability, we will constantly seek to add more profitable

private label products to our existing product lines.

Selectively

Develop Franchise Stores

We

believe that national chains operate more efficiently than smaller independent

operators. When our brand image is well accepted by the market, we will

selectively develop franchise stores in smaller cities to rapidly penetrate the

market and strengthen our position as a leading automotive replacement parts

distributor.

Store

Network

Current

Store Locations

Our

business plan divides the China market into the six geographic regions listed

below. Each geographic region is led by a regional (subsidiary) manager, who

reports directly to our headquarters. Our regional managers currently oversee

seven to ten stores. The following table describes the six sales

regions:

6

|

Regions

|

Provinces

and Municipalities Covered

|

|

|

East

China

|

Fujian,

Shanghai, Zhejiang, Jiangsu, Anhui, Shandong

|

|

|

North

China

|

Hebei,

Henan, Shanxi, Beijing, Tianjin, Shanxi

|

|

|

North-East

China

|

Inner

Mongolia, Jilin, Liaoning, Heilongjiang

|

|

|

North-West

China

|

Ningxia,

Xinjiang

|

|

|

South-West

China

|

Sichuan,

Yunnan, Guizhou, Chongqing, Chengdu

|

|

|

South

China

|

|

Guangdong,

Hubei, Hunan,

Jiangxi

|

On

average, our stores carry approximately 19,000 individual stock units and cover

approximately 1039 square feet. As of September 30, 2010, we operate an

aggregate of approximately 38,441 square feet in our 37 stores. Our stores are

served primarily by the nearest regional distribution center, but they also have

access to the larger selection of inventory available at the applicable master

distribution store. Our East China master distribution center covers

approximately 53,820 square feet. Two of our regional distribution centers,

Nanjing and Hangzhou, cover approximately 2,150 square feet and 3,230 square

feet, respectively.

The

following table lists the geographic location of our 37 stores:

|

Regions

|

Provinces

|

No. of Stores

|

Store locations

|

|||

|

East

China

|

Shanghai

|

6

|

Qingpu,

Putuo, Fengxian, Longhua, Pudong, Xuhuihuaji

|

|||

|

Zhejiang

|

9

|

Jintong,

Yiwu, Jinhua, Jiaxing, Ningbo (2), Taizhou, Wenzhou,

Shaoxing

|

||||

|

Anhui

|

2

|

Hefei

and Wuhu

|

||||

|

Jiangsu

|

9

|

Nanjing

Ningnan, Nanjing Xinyi, Nantong, Wuxi, Suzhou, Yangzhou, Kunshan, Xuzhou

and Changzhou

|

||||

|

Fujian

|

1

|

Fuzhou

|

||||

|

North

China

|

Hebei

|

5

|

Shijiazhuang,

Jiyuan, Shijiazhuang Donglian, Tangshan, Baoding Handan

|

|||

|

Beijing

|

1

|

Beijing

|

||||

|

Tianjin

|

2

|

Tianjin,

Tanggu

|

||||

|

|

Shanxi

|

|

2

|

|

Taiyuan,

Datong

|

We use a

uniform and consistent corporate visual image in terms of store layout and

merchandise presentation. Merchandise is arranged to satisfy our “14 Rules for

Merchandise Presentation” to provide easy customer access, maximum selling

space, and to prominently display high-turnover products and accessories to

customers. The “14 Rules for Merchandise Presentation” require (i) the products

should be displayed in the right place where the customers can easily see them;

(ii) we put as many products as we can on the storage racks; (iii) the products

should be displayed in vertical centralized; (iv) we put heavy products downside

and light products upside; (v) we make sure there

are complete range of products displayed; (vi) the storage racks should be fully

displayed (vii) the display should be designed dynamic and full of originality;

(viii) key products should be given a prominent position on the display; (ix)

make sure the products on the racks are easy to reach for the customer; (x) the

display should be unified and integrated; (xi) the products should be displayed

in a tidy and neat condition; (xii) first in first out (FIFO) rotation of

display units; (xiii) the minimum reserve principle; and (xiv) the products

stack base should be regular.

Store

Automation

To manage

store operations and enhance customer service, we use computers and Ufida

Enterprise Resource Planning systems in all of our stores. Our system is linked

with the computers located in each of our distribution centers and our

headquarters. This system reduces a customer’s checkout time, facilitates

customer management, and enhances services and customer loyalty. It also

collects detailed sales information, which assists in store and financial

management, internal communications, strategic planning, inventory control, and

distribution efficiency.

7

Target

Customers

We target

two groups of customers: (i) second tier wholesalers and (ii) professional

installers, such as repair shops, automobile cosmetics shops and 4S shops

(automobile dealers) in China. Commercial sales are the foundation of our

business because, in the past in China, private vehicle owners usually rely on

professionals for repair and maintenance. The Do-It-Yourself (DIY) market, which

is comprised of consumers who typically repair and maintain their vehicles

themselves, is currently very limited. Therefore, we are focused on commercial

sales at this time.

Second

Tier Wholesalers

We define

second tier wholesalers as automotive replacement parts wholesalers in the

provinces, provincial capitals, and second tier cities. Provincial wholesalers

sell in the large provinces, provincial capital wholesalers sell in the capital

cities of the provinces, and second tier city wholesalers sell in large cities

that are not as well known as first tier cities (such as Beijing and Shanghai

and Shenzhen). The second tier wholesalers’ distribution network typically

covers most of the small retailers and repair shops in the provinces, provincial

cities, and second tier cities, as applicable. Their purchasing volume is large,

but their returns

are low. As of

September 30, 2010, we had 225 wholesaler customers.

Professional

Installers

The

demand of professional installer customers is typically smaller, but generally

steady. Such professional installer customers purchase a variety of products and

represent a majority of our customer list. There are some

professional installers responsible for a significant amount of our sales, but

the loss of such professional installers won’t have a material adverse effect on

our financial condition and results of operation because the gross profits from

sales to professional installers only constitutes approximately 1% of our

current gross profits. We seek to develop long-term strategic

relationships with these customers. The category of professional installer can

be divided into three groups:

|

|

·

|

Repair

shops : Repair shops provide regular

vehicle maintenance and repair services. Repair shops are sales terminals

with small purchasing quantity, but high margin contribution. We consider

repair shops as our priority customers. While domestic and foreign chain

shops are emerging in China, we believe that this business type will

become the dominant channel for vehicle owners to get services/parts upon

expiration of their OEM warranty. According to Auto China, as of 2003,

there were over 300,000 automotive service providers in China, of which

approximately 220,000 were professional installer repair shops that are

accredited to perform classified services. The remaining 80,000 did not

have proper accreditation. We attract these repair shop customers with our

full line of products, on time delivery, inventory management, and

professional solutions;

|

|

|

·

|

Cosmetics

shops : Cosmetics

shops provide simple regular vehicle maintenance services on the exterior

of vehicles. Cosmetics shops are also sales terminals with small

purchasing quantities, but high margin contribution;

and

|

|

|

·

|

4S

and OEM authorized shops : These professional installers

are automobile dealers that provide related after-sale maintenance and

repair services. 4S shops are considered sales terminals with uncertain

purchasing quantity, but high margin contribution. Many vehicle

owners prefer these shops for major repairs and genuine

parts.

|

There are

also small, independently owned repair garages that sometimes use substitute and

counterfeit parts. These types of shops are not our priority customers. We

believe in the long run, most of these repair shops will eventually be

eliminated from the market.

Major

Suppliers

We select

brand name global and local automotive parts manufacturers as our suppliers. We

will purchase collectively and directly from manufacturers so as to eliminate

the middle layers of distributors/wholesalers and gain large order discounts,

enabling us to offer more competitive prices.

There

were approximately 2,000 auto parts manufacturers in China at the end of 2005.

Among those are about 500 joint ventures/wholly-owned foreign enterprises,

including such enterprises as Bosch, Delphi, Visteon, Denso, Siemens, and

Halla. These manufacturers seek reliable and competent distributors

to market their brand name products and protect their intellectual property from

the attacks of counterfeiters. These are our priority suppliers because they can

help us reinforce our brand name and enhance our product image.

8

The

approximately 1,500 local parts producers are relatively small and still in

their early growth stage with respect to the replacement market, though a

significant number of them are able to produce good quality

parts. Some of these smaller producers have supplied the foreign

replacement market for years. We plan on leveraging our distribution/retail

network and buyer’s bargaining power to source private label products from these

manufacturers to increase our profit margins.

As of

September 30, 2010, we had 52 suppliers. Our largest supplier, YBM Group Co.,

Ltd., accounted for 27.97% of our total purchase dollars and our top five

suppliers combined accounted for approximately 73.56%of our total

purchases. We have no long-term contractual purchase commitments with

any of our suppliers and our supplier contracts usually have a term of one year.

We believe that alternative supply sources exist, at similar cost, for most

types of products sold. The following table sets forth the names of our major

suppliers.

|

Brand

|

Products

|

Supplier

Name

|

||

|

YBM

|

Filter

|

Shanghai

YBM Filter Co. Ltd

|

||

|

Olande

|

Filter

|

Shanghai

YBM Filter Co. Ltd

|

||

|

YBM

|

Belt

|

Jiangsu

YBM Rubber Co. Ltd

|

||

|

Senlite

|

Belt

|

Jiangsu

YBM Rubber Co. Ltd

|

||

|

MAHLE

|

Filter

|

Mahle

Trade (Shanghai) Co. Ltd

|

||

|

PHILIPS

|

Light

bulb

|

Philips

(China) Co. Ltd

|

||

|

Narva

|

Light

bulb

|

Philips

(China) Co. Ltd

|

||

|

DENSO

|

Sparkplug

|

Beijing

Zhongqi United Auto Parts Chain Co. Ltd

|

||

|

DENSO

|

Windshield

wiper

|

Beijing

Zhongqi United Auto Parts Chain Co. Ltd

|

||

|

ELF

|

Oil

and Transmission Fluid

|

Elf

Lubricant (Guangzhou) Co. Ltd

|

||

|

BOSCH

|

Windshield

wiper

|

Bosch

Trade (Shanghai) Co. Ltd

|

||

|

BOSCH

|

Sparkplug

|

Bosch

Trade (Shanghai) Co. Ltd

|

||

|

BOSCH

|

Filter

|

Bosch

Trade (Shanghai) Co. Ltd

|

||

|

BOSCH

|

Brake

pads

|

Bosch

Trade (Shanghai) Co. Ltd

|

||

|

OP

|

Belt

|

OP

(China) Co. Ltd

|

||

|

7CF

|

Maintenance

items

|

Shenzhen

Rainbow Fine Chemicals Co. Ltd

|

||

|

Osram

|

|

Light

bulb

|

|

Osram

(China) Lighting Co.

Ltd

|

Competitive

Strengths

Under the

current circumstances, we believe the following strengths allow us to compete

effectively in the automotive aftermarket in China:

Fast

decision-making and execution

Unlike

some other chain retailers in the industry, which developed their network

through acquiring the majority shares of independently-owned stores and thus

have uncoordinated interests, we have only one direct parent and one indirect

parent at the top of our capital structure and all of our stores are wholly

owned, enabling us to make and execute decisions quickly. Moreover, our flat and

lean organizational structure allows us to have efficient

execution.

Extensive

industry experiences and resources

Key

members of our senior management team have, on average, six (6) years of

experience in the China automotive aftermarket industry. We have developed deep

relationships and connections with local industry players and accumulated

extensive local knowledge that will serve as critical building blocks for our

success. As a result, we have a clear understanding of the local customers’

preferences and needs, and are able to cater our products to those local

characteristics. Our supporting management and workforce are well trained and

motivated.

Broad

selection of brands represented

In less

than one year, we entered into dealership contracts with eight brands: Philips,

Bosch, Denso, Mahle, Osram, 7CF, Lihua, and Elf. We have confidence that with

the strengths we possess in our brand name, store location, marketing

assistance, product mix, inventory/logistics, and management, we will be able to

attract more brands to our store. We believe that under existing market

conditions, with dozens of car makes and models, our ability to carry a great

variety of name brand products is a key component to acquiring customers and a

crucial element to chain store success.

9

Products

and Services

Products

We offer

a broad selection of national brand name and private label automotive

aftermarket products for domestic and imported vehicles. Our products include

automotive replacement parts, maintenance items, and accessories. We mainly

serve the professional installers and second tier wholesalers.

Our

merchandise generally consists of nationally recognized and well-advertised

brand names with big market influence products, such as Philips, Bosch,

Denso, Mahle, Osram, 7CF, and Elf. In addition to our brand name products, our

stores carry a variety of high-quality private label products. Because most of

our private label products are produced by carefully selected manufacturers and

meet or exceed original equipment manufacturer specifications, we believe that

our private label products are generally of equal quality with comparable brand

name products carried in our stores, but at equal or lower prices. These factors

play key roles in influencing our customers’ purchasing behaviors. Currently,

our private label products include, but are not limited to, brake pads, filters,

transmission belts, and refrigerants.

Our

products are grouped into two categories:

|

|

·

|

Dealer

products - Products

sold under dealership agreement in defined regions;

and

|

|

|

·

|

OEM

products - Private

label proprietary name

products.

|

The items

below are examples of the typical products we keep in our stores:

|

—

Batteries

|

—

Filters

|

|

|

— Brake

pads

|

— Windshield

wipers

|

|

|

— Spark

plugs

|

—

Refrigerants

|

|

|

—

Horns

|

—

Bulbs

|

|

|

— Oil &

transmission fluids

|

|

— Maintenance

items

|

The

following table sets forth our top 10 best selling products in

2010:

|

Model

|

Product

|

Units sold

|

||||

|

1

|

f8dcor

|

Bosch

Sparkplug

|

226341

|

|||

|

2

|

12499

|

Philips

Light bulb

|

174442

|

|||

|

3

|

w7dc

|

Bosch

Sparkplug

|

161099

|

|||

|

4

|

12498

|

Philips

Light bulb

|

112537

|

|||

|

5

|

ac247

|

7CF

Cleaning agent

|

93660

|

|||

|

6

|

12754

|

Philips

Light bulb

|

76049

|

|||

|

7

|

510038

|

YBM

Filter

|

17930

|

|||

|

8

|

512005

|

YBM

Filter

|

15163

|

|||

|

9

|

oc488

|

MahleFilter

|

12762

|

|||

|

10

|

514002

|

YBM

Filter

|

10044

|

The

following table sets forth the percentage sales by product types in

2010:

|

Products

|

Percent

of sales

|

|||

|

Brake

systems

|

4

|

%

|

||

|

Filters

|

10

|

%

|

||

|

Transmission

belts

|

2

|

%

|

||

|

Oil

& transmission fluids

|

26

|

%

|

||

|

Spark

plugs

|

12

|

%

|

||

|

Lighting

|

30

|

%

|

||

|

Windshield

wipers

|

4

|

%

|

||

|

Storage

battery cells

|

5

|

%

|

||

|

Maintenance

items

|

7

|

%

|

||

|

Total

|

100

|

%

|

||

10

Product

pricing is generally established to compete with the pricing policies of

competitors in the same market area. We seek to optimize profitability while

maintaining competitiveness. Most products that we sell are priced based on a

combination of internal gross margin targets of 18% and the prices of our

competitors. Additional savings are available to our customers through volume

discounts and special promotional pricing. Consistent with our low price

guarantee, each of our stores will match any verifiable price on any in-stock

product of the same or comparable quality offered by our

competitors.

Services

We are

constantly working to understand our customers’ needs and wants in order to

better serve them and build long-lasting, loyal relationships .

Warranty

We only

distribute products to wholesalers/repair shops which provide services related

thereto. Our parts suppliers are responsible for all warranties related to the

parts. Repair shops are responsible for their after sales

services.

Customer

Service

We seek

to attract new professional installer customers and to retain existing customers

by offering superior customer service, the key elements of which

include:

|

|

·

|

Superior in-store point of sale

service from highly-motivated, professional, and technically proficient

store personnel;

|

|

|

·

|

Extensive selection and

availability of products;

|

|

|

·

|

Attractive stores in convenient

locations; and

|

|

|

·

|

Competitive pricing that is

supported by a “good, better, best” product assortment designed to meet

all of our customers’ quality and value

preferences.

|

We

believe that the satisfaction of professional installer customers is

substantially dependent upon our ability to provide, in a timely fashion, the

specific automotive products requested. We continuously refine the inventory

levels and product mix carried in our stores based, in large part, on the sales

movement tracked by (i) our IC system, (ii) market vehicle registration data and

(iii) management’s assessment of the changes and trends in the

marketplace.

Distribution

and Logistics

We employ

a policy of centralized procurement and de-centralized sales. By implementing

this policy, we seek to assure product availability while lowering our inventory

carrying costs and controlling our inventory. We use the Ufida ERP system

(version U8.72) to manage our inventory and warehousing. By centralizing the

procurement function, we gain strong bargaining power from our suppliers.

Further, centralized procurement equips us with better credit terms and better

services.

We

currently operate three distribution centers (Hangzhou, Nanjing, Shijiazhuang)

covering an aggregate of approximately 59,200 square feet. Our distribution

centers are equipped with forklifts and hydraulic power trailers, which expedite

the loading and unloading of our inventory. The distribution centers utilize

technology to electronically receive orders from computers located in each of

our stores. Each of our stores is connected through secured data transmission

technology to our distribution centers and corporate headquarters.

We have a

three-tier warehousing and distribution system to optimize inventory and

logistics management. Under this system, we have (i) master distribution

centers, (ii) regional distribution centers, and (iii) store

inventories.

The first

tier, the master distribution center, is able to supply dealer products,

distribution products, and OEM products. It accepts orders directly from stores

and delivers the merchandise. The master distribution centers have two important

functions: (i) retail sales to professional installers by stocking a complete

line of parts for different vehicle models/makes to assure product availability

and (ii) wholesales of dealer products by assuring prompt action to competition

and market demand.

11

The

second tier is the regional distribution center, such as our Nanjing regional

distribution center and Hangzhou regional distribution center, which is further

categorized into two subcategories: (i) the circulation distribution center and

(ii) the supply distribution center. The circulation distribution center manages

all dealer products while the supply distribution center is setup for

transitional inventory.

The third

tier is the store inventories, which assure the store’s daily operation and is

only responsible for the store’s everyday sales. The store inventories are

determined based on sales numbers. Currently, the number of inventory is

determined by the average inventory level to sales ratio. The average

inventory level is determined by the (i) sum of the (A) storage during the early

part of a month and (B) storage at the end of the month, divided by

2.

Most of

our merchandise flows from our distribution centers to our stores by third-party

transportation companies. Currently, the distribution centers typically carry an

inventory of 40%-50% of our average monthly sales. We believe that with our

growing scale, we will be able to have more orders shipped directly from

suppliers to our distribution centers to reduce the warehousing and

transportation costs. Each of our stores and distribution centers have at least

one van or truck for merchandise delivery to satisfy customer

needs.

Sales and

Marketing

Our sales

team’s salary is performance based. We have formulated specific performance

evaluation standards for each sales position.

Sales

to the Professional Installer

We have

139 full-time sales managers and sales representatives strategically located

across our primary market areas of Shanghai, Nanjing,

Hangzhou, Shijiazhuang, Beijing, and Tianjin. Each sales representative is

dedicated solely to selling to, keeping communication with, and supporting the

professional installers. Marketing materials, such as brochures, flyers,

catalogs, and complementary items are distributed on a continuous basis to

professional installer customers. We attract customers mainly through

competitive pricing, our full line of products, timely delivery, and good

customer service. We also seek to develop mutually beneficial strategic

relationships with repair shops, cosmetic shops, and 4S shops. One of our

strategic alliances is with Automobile Repair Chain, which has 40 shops and has

entered into joint collaborations with us on selected products.

Sales

to Second Tier Wholesalers

Currently,

approximately 235 second tier wholesalers purchase automotive replacement

products from us. Our subsidiaries’ managers are

responsible for developing and managing wholesale customers in their region.

These customers are typically parts wholesalers and maintenance item wholesalers

in provincial capitals, as well as parts wholesalers in smaller cities. We

develop relationships with wholesaler customers by providing them volume

discounts, promotional assistance, marketing and sales support.

Marketing

of Vomart Brand

We will

launch marketing campaigns to promote the Vomart brand name to suppliers,

customers, and the general public. In the first phase of our marketing strategy,

we will support our marketing through print advertising, in-store promotional

displays, promotional gifts, and other direct communications with the

marketplace. The print advertising will consist of color circulars, flyers,

brochures, and newspaper advertisements. In the second phase, we will advertise

in selected industry journals, Internet websites, and trade shows to reinforce

our image and name recognition. We will then analyze and measure the results of

each marketing campaign and identify different customer segments and

corresponding needs to enhance our future marketing success rate in attracting

new customers.

Competition

The sale

of automotive parts, accessories, and maintenance items is highly competitive in

the China market. We operate mainly in the commercial sale (professional

installers) markets of the automotive replacement industry. Our primary

competitors are (i) regional retail chains of automotive parts stores, (ii)

wholesale stores and stores that purchase large quantities of goods, but

resell merchandise to merchants rather than to the end user customers

(“jobbers”) and (iii) independent retailers. We believe that chains of

automotive parts stores like us that have multiple locations in one or more

markets have competitive advantages in the assortment of products, customer

service, inventory selection, marketing, purchasing, and distribution as

compared to independent retailers and “jobbers” that are not part of a chain. We

are able to compete primarily through product selection and availability,

quality and price, store location and store layout, name recognition, and

customer service.

12

For chain

operators, we identified the following domestic competitors: Youpei Auto Parts,

Putong Auto Service, Longfeng Auto Parts, and Andesen Auto Parts. We also

identified several foreign competitors such as Lanba Auto Supermarket. We

believe that compared with our foreign peers, we have a deeper understanding of

the local market and flexibility/efficiency in our decision making.

Properties

As of

September 30, 2010 and June 30, 2010, the detail of property, plant and

equipment was as follows:

|

As

of September

30,

2010

|

As

of June

30,

2010

|

|||||||

|

Office

equipment

|

$

|

107,456

|

$

|

129,981

|

||||

|

Furniture

and fixture

|

79,710

|

44,414

|

||||||

|

Automobiles

|

280,068

|

217,148

|

||||||

|

Sub-total

|

467,234

|

391,543

|

||||||

|

Less:

accumulated depreciation

|

(96,620

|

)

|

(81,263

|

)

|

||||

|

Property,

plant and equipment, net

|

$

|

370,614

|

$

|

310,280

|

||||

Intellectual

Property

We regard

our trademarks, trade secrets, patents, and similar intellectual property as

critical factors to our success. We rely on patent, trademark, and trade secret

law, as well as confidentiality and license agreements with certain of our

employees, customers, and others to protect our proprietary rights.

We

currently use the trademark “VOMART” which is owned by YBM Group China Co., Ltd.

(“YBM”), an affiliated company. We are exclusively licensed to use

the “VOMART” trademark without consideration pursuant to the Letter of

Undertaking issued by YBM, dated July 30, 2010. On September 1, 2010,

YBM filed an application with the Trademark Office of the State Administration

for Industry & Commerce of the PRC (“Trademark Office”) to transfer the

trademark “VOMART” to us. Such transfer application has been accepted and is

currently under review by the Trademark Office. For details about our

relationship with YBM, please refer to the Related Party Transactions

section.

We have

also submitted the application for trademark “WOT” and which is under review by

the Trademark Office.

Set forth

below is a detailed description of the trademarks we currently use:

|

Trademark

|

Registration

/Application No.

|

Class

|

Effective Date

|

Expiration Date

|

Owner/Applicant

|

|||||

|

6454234

|

12

|

March

14, 2010

|

March

13, 2020

|

YBM

Group

China

Co., Ltd.

|

|||||

|

8248870

|

9

|

Registration

Application Accepted on

May

20, 2010

|

Hongkong

Charter

International

Group

Limited

|

||||||

Currently

we do not own any patent or copyright since we concentrate on distribution of

automotive replacement parts and accessories rather than manufacture of

those. The use of the patents or copyrights involved in our

distribution business shall be in accordance with particular agreements with the

owners of intellectual property rights in question, and relative laws and

regulations.

Employees

As of

September 30, 2010, we employed approximately 290 full-time employees who work

at the store level, in distribution centers, and in support functions at our

corporate office.

13

We

believe that capable management and well-trained employees are the most

important success factors for our business. Each of our stores typically employs

between five and six persons, including a store manager. A majority of our

employees have prior automotive industry experience. In addition to on-the-job

training, we provide formal training programs by providing rotations, weekly

training sessions on products and technology, standardized training manuals, and

specialized programs.

Store

managers and sales representatives are incentivized through performance-based

bonuses. In addition, our growth has provided opportunities for the promotion of

qualified employees. We believe that these opportunities are important to

attract, motivate, and retain high quality people. We have never experienced any

material labor disruption. We believe we are efficient in retaining talented

employees and team building.

Government

Regulations

Below is

a list of PRC governmental agencies which may have a jurisdiction over our

business:

|

Agency

|

Functions

|

|

|

Stated

Administration of Industry and Commerce (“SAIC”)

|

Maintaining

market order and protecting the legitimate rights and interests of

businesses and consumers by carrying out regulations in the fields of

enterprise registration, competition, consumer protection, trademark

protection and combating economic illegalities.

|

|

|

Ministry

of Science and Technology (“MST”)

|

Lay

out science and technology development plans and policies; draft relevant

regulations and rules and guarantee implementation of regulations and

rules

|

|

|

State

Administration of Taxation (“SAT”)

|

Draft

tax regulations and implementation rules and propose tax

policies.

|

|

|

State

Administration of Foreign Exchange (“SAFE”)

|

Make

regulations and policies governing foreign exchange market activities and

manage state foreign exchange

reserves.

|

The PRC

government imposes extensive regulations over the automotive

industries. The following provides a brief description of the PRC

laws or government regulations that materially influence our business and their

expected impact on our business:

PRC

Product Quality Law

On

February 22, 1993, the Standing Committee of the National People's Congress

passed Product Quality Law of the People's Republic of China, which was amended

on July 8, 2000. This Law is enacted with a view to strengthen the

supervision and control over product quality, to define the liability for

product quality, to protect the legitimate rights and interests of users and

consumers. Manufacturers and distributors of products are subject to this

Law.

We sell

automotive replacement parts and accessories as a distributor instead of

manufacturing products by ourselves. We offer a broad selection of national

brand name and private label automotive aftermarket products for domestic and

imported vehicles. No matter which kind of products we sell, as a seller, we are

responsible for the quality of the products we distribute by all prudent manners

and are responsible for repair, replacement or return and compensation for the

damages done to end-users or consumers in accordance with PRC Product Quality

Law.

It is

harmful, as well as prohibited for us, to sell any products that are

unqualified, counterfeit or expired. If unqualified products were

sold to customers, the seller might face damage claims from

customer. If relevant authority found that we did not comply with PRC

Product Quality Law, we would be ordered to stop selling unqualified products

and pay a fine. The gain as a result of our sale of unqualified products may be

confiscated. Our business license may be revoked. If this kind of violation were

very serious, it would be deemed a crime.

PRC

Standardization Law

On

December 29, 1988, the Standing Committee of the National People's Congress

passed Standardization Law of the People's Republic of China This Law

stipulates the formulation and implementation of standards on industrial

products with the purpose of promoting technical progress, proving product

quality and increasing social and economic interest. Manufacturers of different

automotive replacement parts and accessories are subject to PRC Standardization

Law.

14

When we

purchase brand name as well as private label automotive replacement parts for

distribution, we must ensure those products are in compliance with the relevant

production standards under this law. If relevant authority found that the

products we distribute do not conform to the applicable standards, we may be

ordered to discontinue our sale of such products. The gains as a result of our

sale of such products may be confiscated. We may also be fined by the relevant

authorities.

PRC

Trademark Law

On August

23, 1982, the Standing Committee of the National People's Congress passed

Trademark Law of the People's Republic of China, which was amended on February

22, 1993 and on October 27, 2001. This Law is enacted for the

purposes of improving the administration of trademarks, protecting the exclusive

right to use a trademark, and encouraging producers to guarantee the quality of

their goods and maintain the reputation of their trademarks, with a view to

protecting consumers' interests.

As an

auto parts distributor, our business involves the registration, assignment and

protection of the trademark. The trademark "VOMART" we are authorized to

exclusively and freely use is owned by YBM Group China Co., Ltd. and is in the

process of being transferred to us. We have also submitted the application for

trademark "WOT" which is under review by the Trademark Office.

We are in

compliance with this Trademark Law. If we commit any acts prohibited

by the law, we may be ordered to make rectification within a certain time frame,

subject to a fine and the registered trademark in question may be revoked by the

Trademark Office of the PRC.

Regulation

on the Administration of Commercial Franchises

On

January 31, 2007, the State Council of PRC passed Regulation on the

Administration of Commercial Franchises. This regulation is

formulated for the purpose of regulating commercial franchises, promoting the

healthy and orderly development of the commercial franchise industry and

maintaining the market order.

Since we

operate business by establishing franchise chains, we are required by this

Regulation to file our commercial franchises contract with governmental

authority, ensure the product and service quality, disclose information to

licensees and so on.

We are in

compliance with this Regulation. If we violate the provisions of this

regulation, we may be subject to a fine. If any of our earnings are

deemed illegal, they may be confiscated by the relevant

authorities.

PRC

Law on Import and Export Commodity Inspection

On

February 21, 1989 the Standing Committee of the National People's Congress

passed the Law of the People's Republic of China on Import and Export Commodity

Inspection, which was amended on April 28, 2002. This Law is enacted

with a view to strengthen the inspection and ensure the quality of import and

export goods, and to protect the legitimate rights and interests of the parties

involved in foreign trade. This law has a material influence on us since we are

engaged in the business of imports and exports of auto parts, motorcycle

accessories, machinery parts, instrument, meter, hardware and electrical

products. We are in compliance with this law. Any failure to comply

with the law will subject us to a fine. The goods in question may be

confiscated and we may be subject to criminal investigations if the violation

constitutes a crime.

Research

and Development

We did

not incur any research and development expenses as of September 30, 2010, June

30, 2010 and 2009, and do not anticipate incurring such expenses in the

future.

RISK

FACTORS

You

should carefully consider the risks described below together with all of the

other information included in this Current Report before making an investment

decision with regard to our securities. The statements contained in

or incorporated herein that are forward-looking statements are subject to risks

and uncertainties that could cause actual results to differ materially from

those set forth in or implied by forward-looking statements. If any of the

following risks actually occurs, our business, financial condition or results of

operations could be harmed. In that case, you may lose all or part of your

investment.

15

RISKS RELATING TO OUR

BUSINESS

WE

FACE RISKS RELATED TO GENERAL DOMESTIC AND GLOBAL ECONOMIC CONDITIONS AND TO THE

RECENT CREDIT CRISIS.

We

currently generate sufficient operating cash flows, which combined with access

to the credit markets, provide us with significant discretionary funding

capacity.

However,

the current uncertainty arising out of domestic and global economic conditions,

including the recent disruption in credit markets, poses a risk to the economies

in which we operate that has affected demand for our products and services, and

may affect our ability to manage normal relationships with our customers,

suppliers, and creditors. If the current situation deteriorates significantly,

our business could be materially negatively affected, including such areas as

reduced demand for our products and services from a slow-down in the general

economy, or supplier or customer disruptions resulting from tighter credit

markets. In addition, terrorist activities may cause unpredictable or

unfavorable economic conditions and could have a material adverse effect on the

Company’s operating results and financial condition.

WE

PLAN TO RAPIDLY GROW OUR BUSINESS AND MAY NOT BE ABLE TO MANAGE OUR GROWTH IF WE

EXPAND TOO QUICKLY, WHICH COULD HURT OUR RELATIONSHIPS WITH OUR CURRENT AND

FUTURE CUSTOMERS AND ULTIMATELY OUR BUSINESS, RESULTS OF OPERATIONS AND

FINANCIAL CONDITION.

We plan

to open approximately 40 new stores in 2010 and 250 new stores by 2014 in order

to, among other things, achieve market penetration in more geographic

locations. Our period of rapid growth will place a significant strain

on our senior management team, especially at our headquarters, and our financial

and other resources. Our rapid growth may require us to incur

additional expenses before experiencing an increase in revenue, which increase

pressure on our management to ramp up sales as quickly as possible. Any

expansion may expose us to increased competition, greater overhead, marketing

and support costs and other risks associated with the expansion of a business.

Our ability to manage rapid growth effectively will require us to continue to

improve our operations, improve our financial and management information systems

(e.g., account receivables, cash management, asset allocation, etc.) and to

train, motivate and manage our employees. Our current personnel,

systems, procedures and controls will likely not adequately support future

operations. In that event, we will need to expand our finance, administrative,

and operations staff. Difficulties in effectively managing issues

presented by such a rapid expansion may result in a reduction in the quality of

our services and our customer support may deteriorate. This could prompt our

current customers to discontinue their relationships with us and hurt our

business results.

AS

WE OPEN NEW STORES AND GROW IN SCALE, WE WILL NEED TO STOCK MORE INVENTORY TO

PROVIDE PRODUCT AVAILABILITY WHILE AT THE SAME TIME ACHIEVING COST REDUCTION AND

EFFICIENCY TO BE COMPETITIVE. IF WE ARE UNABLE TO OVERCOME THE

CHALLENGES, OUR BUSINESS WILL SUFFER.

The

number of new stores that we plan to open will require us to significantly

increase our inventory. We will have to adjust our systems in order to meet the

challenges presented by the expansion impact on procurement, inventory and

logistics. We may not be able to do so to be profitable within our

timeline or at all. We may not be able to acquire the additional

inventory needed to implement our business plan. If we are unable to

acquire auto parts or there is a significant delay in providing the parts, our

customers may look to our competitors to provide such parts, which will decrease

our market share and damage our reputation for our prompt service.

OUR

GROWTH STRATEGY DEPENDS ON OUR ABILITY TO OPEN NEW STORES AND OPERATE THEM

PROFITABLY.

A key

element of our growth strategy is to open additional stores in locations that we

believe will provide attractive returns. Our ability to open new stores on a

timely and cost-effective basis is dependent on a number of factors, many of

which are beyond our control, including our ability to: find quality locations;

reach acceptable agreements regarding the lease or purchase of locations; comply

with applicable zoning, land use and environmental regulations; raise or have

available an adequate amount of money for construction and opening costs; timely

hire, train and retain the skilled management and other employees necessary to

meet staffing needs; and -efficiently manage the amount of time and money used

to build and open each new store. If we succeed in opening new stores on a

timely and cost-effective basis, we may nonetheless be unable to attract enough

customers to new stores because potential customers may be unfamiliar with our

stores or atmosphere. We cannot provide any assurance that our new stores will

meet or exceed the performance of our existing stores or meet or exceed our

performance targets. New stores may even operate at a loss, which could have a

significant adverse effect on our overall operating results. Opening a new store

in an existing market could reduce the revenue at our existing stores in that

market. In addition, historically, new stores experience a drop in revenues

after their first year of operation. Typically, this drop has been temporary and

has been followed by increases in comparable store revenue in line with the rest

of our comparable store base, but there can be no assurance that this will be

the case in the future or that a new store will succeed in the long

term.

16

WE

RELY ON INFORMATION TECHNOLOGY IN CRITICAL AREAS OF OUR AUTO PARTS BUSINESS

OPERATIONS, AND A DISRUPTION RELATING TO SUCH TECHNOLOGY COULD HARM OUR

BUSINESS.

We use

information technology systems for the management of our inventories, processing

costs and customer sales. If the providers of these systems terminate their

relationships with us, or if we decide to switch providers or to implement our

own systems, we may suffer disruptions, which could have a material adverse

effect on our results of operations and financial condition. In addition, we may

underestimate the costs and expenses of switching providers or developing and

implementing our own systems.

OUR

PLANS TO EXPAND OUR PRODUCT LINES AND TO IMPROVE AND UPGRADE OUR INTERNAL

CONTROL AND MANAGEMENT SYSTEM WILL REQUIRE CAPITAL EXPENDITURES IN

2011.

Our plans

to expand our product lines and to improve and upgrade our internal control and