Attached files

| file | filename |

|---|---|

| EX-3.1 - AMENDED ARTICLES - Keyuan Petrochemicals, Inc. | fs1a1ex3i_keyuan.htm |

| EX-5.1 - OPINION LETTER - Keyuan Petrochemicals, Inc. | fs1a1ex5i_keyuan.htm |

| EX-23.2 - CONSENT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM - Keyuan Petrochemicals, Inc. | fs1a1ex23ii_keyuan.htm |

| As filed with the Securities and Exchange Commission on | Registration No. 333-170324 |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form S-1 /A1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

KEYUAN PETROCHEMICALS, INC.

(Exact name of Registrant as specified in its charter)

|

Nevada

|

1311

|

45-0538522

|

||

|

(State or Other Jurisdiction of Incorporation or Organization)

|

(Primary Standard Industrial Classification Code Number)

|

(I.R.S. Employer Identification Number)

|

|

Qingshi Industrial Park

Ningbo Economic & Technological Development Zone

Ningbo, Zhejiang Province

P.R. China 315803

(86) 574-8623-2955

|

(Address, including zip code, and telephone number,

including area code, of Registrant’s principal executive offices)

Copies to:

Louis E. Taubman, Esq.

Leser, Hunter, Taubman & Taubman

17 State Street, Suite 2000

New York, New York 10004

Approximate date of commencement of proposed sale to the public: From time to time after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. x

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer

|

o |

Accelerated filer

|

o | ||

|

Non-accelerated filer

|

o |

Smaller reporting company

|

x

|

||

|

(Do not check if a smaller reporting company)

|

|||||

CALCULATION OF REGISTRATION FEE

| Title of each class of securities to be registered |

Amount to be

Registered(1)

|

Proposed

maximum

offering price per

share(2)

|

Proposed

maximum

aggregate

offering price

|

Amount of

registration fee

|

||||||||||||

|

Shares of Common Stock Underlying Preferred Stock

|

5,400,010(3) | $ | 5.13 | $ | 27,702,051.30 | $ | 1975.16 | |||||||||

|

Shares of Common Stock Underlying Warrants

|

810,002(4) | $ | 5.13 | $ | 4,155,310.26 | $ | 296.27 | |||||||||

|

Shares of Common Stock Underlying Warrants

|

810,002(5) | $ | 5.13 | $ | 4,155,310.26 | $ | 296.27 | |||||||||

|

Shares of Common Stock Underlying Placement Agent Warrants

|

561,601(6) | $ | 5.13 | $ | 2,881,013.13 | $ | 205.42 | |||||||||

|

Total

|

7,581,615 | $ | 38,893,684.95 | $ | 2,773.12 | |||||||||||

|

(1)

|

Pursuant to Rule 416 under the Securities Act of 1933, this registration statement includes an indeterminate number of additional shares as may be issuable as a result of stock splits or stock dividends which occur during this continuous offering.

|

|

(2)

|

Estimated solely for purposes of calculating the registration fee in accordance with Rule 457(c) under the Securities Act of 1933, as amended based upon the average of the bid and asked price of the Registrant's common stock as quoted on the Nasdaq Stock Market of $5.19 on November 1, 2010.

|

|

(3)

|

Represents shares of the Company’s Series B Convertible Preferred Stock, par value $0.001 per share, convertible into the same number of shares of the company’s common stock, par value $0.001 per share the Company issued pursuant to the financings that the Company consummated on September 28, 2010.

|

|

(4)

|

Represents shares of common stock underlying Series C Warrants at an exercise price of $4.50 per share that the Company issued pursuant to the financings they consummated on September 28, 2010.

|

|

(5)

|

Represents shares of common stock underlying Series D Warrants at an exercise price of $5.25 per share that the Company issued pursuant to the financings they consummated on September 28, 2010.

|

|

(6)

|

Represents shares of common stock underlying Placement Agent Warrants that the Company issued to the placement agent in connection with the financings they consummated on September 28, 2010, including 432,001 shares of common stock underlying Placement Agent Warrants at an exercise price of $ 3 .75 per share; 64,800 shares of common stock underlying Placement Agent Warrants at an exercise price of $4.50 per share and 64,800 shares of common stock underlying Placement Agent Warrants at an exercise price of 5.25 per share.

|

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with section 8(a) of the Securities Act of 1933, as amended, or until the registration statement shall become effective on such date as the Commission, acting pursuant to said section 8(a), may determine.

THE INFORMATION IN THIS PROSPECTUS IS NOT COMPLETE AND MAY BE CHANGED. THE SELLING STOCKHOLDERS MAY NOT SELL THESE SECURITIES PUBLICLY UNTIL THE REGISTRATION STATEMENT FILED WITH THE SECURITIES AND EXCHANGE COMMISSION IS EFFECTIVE. THIS PROSPECTUS IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT SOLICITING AN OFFER TO BUY THESE SECURITIES IN ANY STATE WHERE THE OFFER OR SALE IS NOT PERMITTED.

SUBJECT TO COMPLETION, DATED

PROSPECTUS

KEYUAN PETROCHEMICALS, INC.

7,581,615Shares of Common Stock

This prospectus relates to the resale of up to 7,581,615 shares of our common stock, $0.001 par value, including 5,400, 010 shares of our Common Stock (the “Conversion Shares”) issuable upon the conversion of our Series B Preferred Stock, and 2,181,605 shares of our Common Stock issuable upon exercise of warrants (the “Warrant Shares”). The Warrant Shares are comprised of (i) 810,002 shares of Common Stock issuable upon exercise of Series C Warrants to purchase our Common Stock, (ii) 810,002 shares of Common Stock issuable upon exercise of Series D Warrants to purchase our Common Stock and (iii) 561,601 shares of Common Stock issuable upon exercise of Placement Agent Warrants to purchase our Common Stock issued to TriPoint Global Equities, LLC , as placement agent in connection with the Private Placement. The selling stockholders named herein may sell common stock from time to time in the principal market on which the stock is traded at the prevailing market price, at prices related to such prevailing market price, in negotiated transactions or a combination of such methods of sale. We will not receive any proceeds from the sales by the selling stockholders.

Our Common Stock is quoted on the Nasdaq Stock Market under the symbol “KEYP” and has very limited trading. The closing price for our Common Stock on the Nasdaq Stock Market on Decmeber 27 , 2010 was $ 4.45 per share.

The selling stockholders, and any broker-dealer executing sell orders on behalf of the selling stockholders, may be deemed to be “underwriters” within the meaning of the Securities Act of 1933, as amended. Commissions received by any broker-dealer may be deemed underwriting commissions under the Securities Act of 1933, as amended.

THIS INVESTMENT INVOLVES A HIGH DEGREE OF RISK. YOU SHOULD PURCHASE SHARES ONLY IF YOU CAN AFFORD A COMPLETE LOSS OF YOUR INVESTMENT. SEE “RISK FACTORS” BEGINNING ON PAGE 6 FOR A DISCUSSION OF RISKS APPLICABLE TO US AND AN INVESTMENT IN OUR COMMON STOCK.

NEITHER THE SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES COMMISSION HAS APPROVED OR DISAPPROVED THESE SECURITIES, OR DETERMINED IF THIS PROSPECTUS IS TRUTHFUL OR COMPLETE. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

The date of this prospectus is December 28 , 2010.

TABLE OF CONTENTS

|

1

|

||

|

20

|

||

| 20 | ||

| 20 | ||

|

20

|

||

|

22

|

||

|

24

|

||

|

26

|

||

| 26 | ||

| 110 | ||

| 110 | ||

| 110 | ||

|

Part II

|

||

| 111 | ||

| 111 | ||

| 111 | ||

| 113 | ||

|

115

|

We have not authorized any person to give you any supplemental information or to make any representations for us. You should not rely upon any information about us that is not contained in this prospectus or in one of our public reports filed with the Securities and Exchange Commission (“SEC”) and incorporated into this prospectus. Information contained in this prospectus or in our public reports may become stale. You should not assume that the information contained in this prospectus, any prospectus supplement or the documents incorporated by reference are accurate as of any date other than their respective dates, regardless of the time of delivery of this prospectus or of any sale of the shares. Our business, financial condition, results of operations and prospects may have changed since those dates. The selling stockholders are offering to sell, and seeking offers to buy, shares of our common stock only in jurisdictions where offers and sales are permitted.

In this prospectus the “company,” “we,” “us,” and “our” refer to KEYUAN PETROCHEMICALS, INC., a Nevada corporation and its subsidiaries, after giving effect to the Share Exchange that the Company completed on April 22, 2010.

Until [ ], all dealers that effect transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to the dealers’ obligation to deliver a prospectus when acting as underwriters.

ITEM 3. SUMMARY INFORMATION, RISK FACTORS AND RATIO OF EARNINGS TO FIXED CHANGES

This summary highlights selected information appearing elsewhere in this prospectus. While this summary highlights what we consider to be the most important information about us, you should carefully read this prospectus and the registration statement of which this prospectus is a part in their entirety before investing in our common stock, especially the risks of investing in our common stock, which we discuss later in “Risk Factors,” and our financial statements and related notes beginning on page 6 and 51, respectively. Unless the context requires otherwise, the words “we,” “us” and “our” refer to Keyuan Petrochemicals, Inc.. and our subsidiaries, and the word “Keyuan Petrochemicals” refers only to Keyuan Petrochemicals, Inc.. All market and industry data provided in this prospectus represents information that is generally available to the public and was not prepared for us for a fee. We did not fund nor were we otherwise affiliated with these sources and we are not attempting to incorporate the information on external web sites into this prospectus. We are only providing textual reference of the information of market and industry data and the web addresses provided in this prospectus are not intended to be hyperlinks and we do not assure that those external web sites will remain active and current.

Our Company

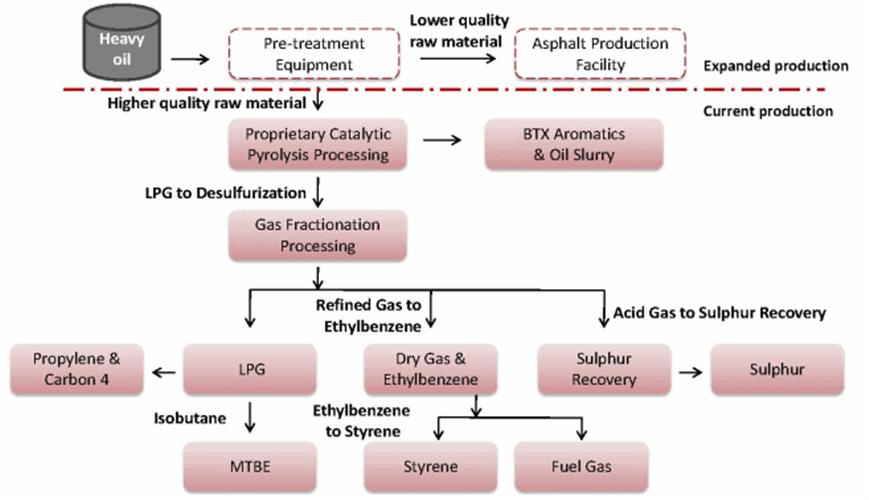

Prior to the consummation of the share exchange transaction described below, we were a shell company with nominal operations and nominal assets. Currently, we are a holding company operating through our wholly-owned subsidiary, Keyuan Plastics, located in Ningbo, China. We are a manufacturer and supplier of various petrochemical products in China. Through Keyuan Plastics, our operations include (i) an annual petrochemical manufacturing capacity of 550,000 metric tons (MT) of a variety of petrochemical products, (ii) facilities for the storage and loading of raw materials and finished goods, (iii) a manufacturing technology that can support our manufacturing process with low raw material costs and high utilization and yields, (iv) a strong management team consisting of petrochemical experts with proven track records from some of China’s largest state-owned enterprises in the petrochemical industry.

Due to China’s growing demand for refined petrochemical products, which is mainly attributable to China’s significant economic growth and under-developed domestic supply capacity, our customer request orders for the year 2010 has exceeded our current annual production capacity. In order to increase our production capacity to meet the increasing market demands, our management team plans to expand our manufacturing capacity to include a raw material pre-treatment facility, additional storage capacity and an asphalt production facility.

In order to expand our facility, we need to acquire use rights of additional land. In China, the government is responsible for overall land planning and they will often select a target company to maximize the benefits of land use for a particular area. We have been in regular communications with the Ningbo Municipal Government about the land use rights for approximately 1.2 million square feet of land adjacent to our current production facility. We submitted our application to the local government for a land bidding process slated on July 13, 2010 which is a necessary legal proceeding to acquire the land use rights in China. We were the only bidder in this process because the land is well integrated with our existing site. The bidding process was completed on August 13, 2010 and we entered into land use right transfer agreements with the local government on August 18, 2010.

In order to expand our facility, we need to acquire use rights of additional land. In China, the government is responsible for overall land planning and they will often select a target company to maximize the benefits of land use for a particular area. We have been in regular communications with the Ningbo Municipal Government about the land use rights for approximately 1.2 million square feet of land adjacent to our current production facility. We submitted our application to the local government for a land bidding process slated on July 13, 2010 which is a necessary legal proceeding to acquire the land use rights in China. We were the only bidder in this process because the land is well integrated with our existing site. The bidding process was completed on August 13, 2010 and we entered into land use right transfer agreements with the local government on August 18, 2010.

Share Exchange

On April 22, 2010, Silver Pearl entered into a Share Exchange Agreement, by and among Keyuan International Group Limited (“Keyuan International”), a company organized under the laws of the British Virgin Islands, Delight Reward Limited, the sole shareholder of Keyuan International and a company organized under the laws of the British Virgin Islands (the “Keyuan International Shareholder”), and Denise D. Smith, our former principal stockholder (“Smith”). Pursuant to the terms of the Exchange Agreement, the Keyuan International Shareholder transferred to us all of the issued and outstanding ordinary shares of Keyuan International (the “Keyuan International Shares”) in exchange for the issuance of 47,658 shares of our Series M preferred stock, par value $0.001 per share (the “Series M Preferred Stock”) (such transaction is sometimes referred to herein as the “Share Exchange”). The Series M shares vote with the common stock on an as converted basis and are convertible into 47,658,000 shares of common stock upon the Company’s shareholders approving an increase in authorized common stock to at least 100,000,000 shares. As a result of the Share Exchange, we are now the holding company of Keyuan Plastics Co., Ltd., the operating subsidiary of Keyuan International organized in the People’s Republic of China (“China” or the “PRC”) and engaged in manufacturing and supplying various petrochemical products in China.

Immediately prior to the Share Exchange, 3,264,000 shares of our common stock, par value $0.001 (the “Common Stock”) then outstanding were cancelled and retired.

April – May 2010 Private Financing

Following the Share Exchange, we entered into a securities purchase agreement with 122 accredited investors for the issuance and sale of 748,704 Units at a purchase price of $35 per unit, consisting of, in the aggregate, (a) 6,738,336 shares of Series A convertible preferred stock, par value $0.001 per share convertible into the same number of shares of Common Stock, (b) 748,704 shares of Common Stock, (c) three-year Series A Warrants to purchase up to 748,704 shares of Common Stock, at an exercise price of $4.50 per, and (d) three-year Series B Warrants to purchase up to 748,704 shares of Common Stock, at an exercise price of $5.25 per share, for aggregate gross proceeds of approximately $26,204,640 million.

In connection with the April-May 2010 private placement, we also entered into a registration rights agreement with the investors, in which we agreed to file a registration statement with the SEC to register for resale of the Common Stock, the Common Stock issuable upon conversion of the Series A Preferred Stock, the Series A Warrant Shares and the Series B Warrant Shares issued in the financing, within 30 calendar days of April 22, 2010 and to have such registration statement declared effective within 150 calendar days of April 22, 2010 or within 180 calendar days of April 22, 2010 in the event of a full review of the registration statement by the SEC. If we do not comply with the foregoing obligations under the Registration Rights Agreement, we will be required to pay cash liquidated damages to each investor, at the rate of 1% of the applicable subscription amount for each 30 day period in which we are not in compliance; provided, that such liquidated damages will be capped at 10% of the subscription amount of each investor and will not apply to any registrable securities that may be sold pursuant to Rule 144 under the Securities Act if all of the conditions in Rule 144(i)(2) are satisfied at the time of the proposed sale, or are subject to an SEC comment with respect to Rule 415 promulgated under the Securities Act. Accordingly, we filed a registration statement on Form S-1 in connection with the April-May 2010 private placement transaction, and the Amendment No. 4 to such Form S-1 which we filed on October 15, 2010 was declared effective on October 19, 2010. Therefore, we are not filing this prospectus to satisfy the provisions of the registration rights agreement we entered into in connection with the April-May 2010 private placement transaction.

A copy of the Exchange Agreement, the Purchase Agreement and the Registration Rights Agreement are incorporated herein by reference and are filed as Exhibit 2.1 , Exhibits 10.1 and 10.2, respectively. The description of the transactions contemplated by such agreements set forth herein do not purport to be complete and is qualified in its entirety by reference to the full text of the exhibits filed herewith and incorporated herein by reference.

Short Form Merger and Name Change

On May 12, 2010, we caused to be formed a corporation under the laws of the State of Nevada called Keyuan Petrochemicals, Inc. and on the same day, acquired one hundred (100) shares (95%) of this entity’s stock for cash. As such, this entity became our wholly-owned subsidiary (the “Merger Subsidiary”).

Effective as of May 17, 2010, the merger subsidiary was merged with and into us. As a result of the merger, our corporate name was changed to “Keyuan Petrochemicals, Inc.” Prior to the merger, the merger subsidiary had no liabilities and nominal assets and, as a result of the merger, the separate existence of the merger subsidiary ceased. We are the surviving corporation in the merger and, except for the name change provided for in the Agreement and Plan of Merger, there was no change in our directors, officers, capital structure or business.

A copy of the Agreement and Plan of Merger and a copy of the Articles of Merger are incorporated herein by reference and filed as Exhibits 2.2 and 3. 2 , respectively.

September 2010 Private Placement

On September 28, 2010, we closed the offering of $20,250,000 for a total of 540,001 units at a purchase price of $37.5 0 per unit, each consisting of, (a) ten (10) shares of Series B convertible preferred stock of the Company, (b) one and a half (1.5) three year Series C warrant to purchase one and a half (1.5) share of Common Stock, at an exercise price of $4.50 per share, and (c) one and a half (1.5) three year Series D warrant to purchase one and a half (1.5 ) share of Common Stock, at an exercise price of $5.25 per share (the “ September 2010 Private Placement”) in reliance upon the exemption from securities registration afforded by Regulation S as promulgated under the Securities Act of 1933.

In connection with the September 2010 Private Placement, we also entered into the following agreements:

|

a.

|

A Registration Rights Agreement with the investors, in which we agreed to file a registration statement with the Commission to register for resale the Common Stock issuable upon conversion of the Series B Preferred Stock, the Series C Warrant Shares and the Series B Warrant Shares, within 30 calendar days of October 19, 2010 and to have the registration statement declared effective within 150 calendar days of October 19, 2010 or within 180 calendar days of October 19, 2010 in the event of a full review of the registration statement by the Commission. If we do not comply with the foregoing obligations under the Registration Rights Agreement, we will be required to pay cash liquidated damages to each Investor, at the rate of 1% of the applicable subscription amount for each 30 day period in which we are not in compliance; provided, that such liquidated damages will be capped at 10% of the subscription amount of each investor and will not apply to any registrable securities that may be sold pursuant to Rule 144 under the Securities Act, or are subject to an SEC comment with respect to Rule 415 promulgated under the Securities Act.

|

In addition, pursuant to the Registration Rights Agreement, the Investors acknowledged and agreed that the registration rights granted under the Registration Rights Agreement are subject in all respects to the full realization of the registration rights granted to the purchasers in the private placement closed on September 28, 2010.

|

b.

|

A Securities Escrow Agreement with the investors and Delight Reward Limited, holder of all of our issued and outstanding Series M preferred stock, pursuant to which, Delight Reward agrees to deliver into an escrow account 3,400 shares of our Series M Preferred Stock convertible into 3,400,000 shares of Common Stock to be used as escrow shares after we amend our Articles of Incorporation to increase our authorized Common Stock to one hundred million (100,000,000) shares. With respect to the 2010 performance year, if we achieve less than 95% of the 2010 performance threshold, then the escrow shares for such year will be delivered to the Investors in the amount of 500,000 shares of Common Stock for each full percentage point by which such threshold was not achieved up to a maximum of 3,400,000 shares of Common Stock.

|

|

c.

|

A Lock-Up Agreement with each of Messers Chunfeng Tao, Jicun Wang, Peijun Chen and Xin Yue (collectively, the “Affiliates”), whereby the Affiliates are prohibited from selling our securities that they directly or indirectly own until the registration statement in connection with the September 2010 Private Placement is declared effective by the Commission (the “Lock-Up Period”). In addition, the Affiliates further agree that during the twenty four (24) months immediately following the Lock-Up Period, the Affiliates shall not offer, sell, contract to sell, assign, transfer (the “Transfer”) more than twenty percent (20%) of the Lock-Up Shares in the aggregate, provided, that the Affiliates may Transfer not more than 0.83333% of the Lock-Up Shares during each calendar month following the Lock-Up Period, other than engaging in a Transfer in a private sale of the Lock-Up Shares if the transferee agrees in writing to be bound by and subject to the terms of the Lock-Up Agreement.

|

|

d.

|

A Voting Agreement with Delight Reward and the investors, pursuant to which the Stockholder agreed to (i) give its written consent in any action to approve the issuance of the Underlying Shares which will result in issuance of securities greater than 20% of the then outstanding shares of Common Stock at a price less that the applicable market, and (ii) to appoint a person designated by the investors holding a majority of the Preferred Shares as a member of the board of directors of the Company and the subsidiary of the Company organized under the laws of the People’s Republic of China.

|

A copy of the Purchase Agreement and the Registration Rights Agreement are incorporated herein by reference and are filed as Exhibits 10.37 and 10.38, respectively. A copy of the Securities Escrow Agreement, the Lock-Up Agreement, the Voting Agreement the Form of Series C warrants, Form of Series D warrants and Series B Certificate of Designation, are filed incorporated herein by reference as Exhibits 10.39, 10.40, 10.41, 10.42, 10.43 and 4.3, respectively . The description of the transactions contemplated by such agreements set forth herein do not purport to be complete and is qualified in its entirety by reference to the full text of the exhibits filed herewith and incorporated herein by reference.

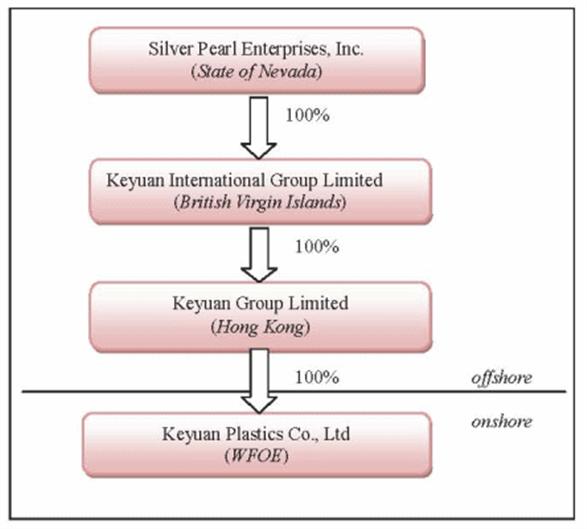

Our Organizational Structure

Below is a chart of our structure after the closing of the Share Exchange:

Principal Executive Office

Our principal executive offices are located at Ningbo Industrial Park, Ningbo Economic & Technological Development Zone, Ningbo, China 315803, Tel: (86) 574-8623-2955.

Risk Factors

The securities offered by this prospectus are speculative and involve a high degree of risks associated with our business. For more discussion of these and other risk factors affecting us and our business, see the “Risk Factors” section beginning on page 6 of this prospectus.

The Offering

|

Common Stock being offered by Selling Stockholders

|

Up to 7,581,615 shares(1)

|

|

Common Stock outstanding

|

3,707,510 shares as of the date of this Prospectus

|

|

Common Stock outstanding after the Offering

|

11,289,125 (2)

|

|

Use of Proceeds

|

We will not receive any proceeds from the sale of shares by the Selling Stockholders, although we may receive additional proceeds of up to $10,149,323 if all of the Series C Warrants and Series D Warrants are exercised for cash. We will not receive any additional proceeds to the extent that the Warrants are exercised by cashless exercise.

|

|

Nasdaq Stock Market Symbol

|

KEYP

|

|

Risk Factors

|

The securities offered by this prospectus are speculative and involve a high degree of risk and investors purchasing securities should not purchase the securities unless they can afford the loss of their entire investment. See “Risk Factors” beginning on page 6.

|

|

(1)

|

This prospectus relates to the resale by the Selling Stockholders of up to 7,581,615 shares of our Common Stock, including 5,400,010 shares of our Common Stock (the “Conversion Shares”) issuable upon the conversion of our Series B Preferred Stock, and 2,181,605 shares of our Common Stock issuable upon exercise of Warrants. The Warrant Shares are comprised of (i) 810,002 shares of Common Stock issuable upon exercise of Series C Warrants to purchase our Common Stock, (ii) 810,002 shares of Common Stock issuable upon exercise of Series D Warrants to purchase our Common Stock and (iii) 561,601 shares of Common Stock issuable upon exercise of placement agent Warrants to purchase our Common Stock issued to TriPoint Global Equities, LLC, as placement agent in connection with the Private Placement, and certain of its designees as set forth in this prospectus.

|

|

(2)

|

Assumes issuance of all Conversion Shares and Warrant Shares.

|

Summary Financial Information

The following summary financial data for the fiscal years ended December 31, 2009 and 2008, were derived from the consolidated financial statements of our recently acquired subsidiary, Keyuan International Group Ltd., and the interim financial data for the period ending June 30, 2010 for Keyuan International Group Ltd.. This information is only a summary and does not provide all of the information contained in our financial statements and related notes. You should read the “Management’s Discussion and Analysis or Plan of Operation” beginning on page 89 of this prospectus and our financial statements and related notes included elsewhere in this prospectus.

Statement of Operations Data:

|

For the Years Ended

December 31,

|

For the Quarter ended September 30,

|

For the Nine Months

Ended September 30,

|

||||||||||||||

|

2009

|

2008

|

2010

|

2010

|

|||||||||||||

|

Sales

|

$ | 68,653,603 | $ | -- | $ | 151,343,966 | 400,713,069 | |||||||||

|

Cost of sales

|

75,311,595 | - | 138,277,229 | 370,185,046 | ||||||||||||

|

Gross profit

|

(6,657,992 | - | 13,066,737 | 30,528,023 | ||||||||||||

|

Operating expenses

|

||||||||||||||||

|

Selling expenses

|

24,836 | - | 97,871 | 441,284 | ||||||||||||

|

General and administrative expenses

|

2,714,093 | 1,839,253 | 1,645,321 | 3,539,109 | ||||||||||||

|

Total operating expenses

|

2,738,929 | 1,839,253 | 1,734,192 | 3,980,393 | ||||||||||||

|

Gain (loss) from operations

|

(9,396,921 | ) | (1,839,253 | ) | 11,323,545 | 26,547,630 | ||||||||||

|

Other income (expenses):

|

||||||||||||||||

|

Interest expense, net

|

(2,031,983 | ) | (64,584 | ) | (3,850,777 | ) | (6,514,240 | ) | ||||||||

|

Non-operating expenses

|

(348,515 | ) | (39,885 | ) | 1,897,007 | 1,906,606 | ||||||||||

|

Total other expenses

|

(2,380,498 | ) | (104,469 | ) | (1,953,770 | ) | (4,607,634 | ) | ||||||||

|

Income (loss) before provision for income tax

|

(11,777,419 | ) | (1,943,722 | ) | 9,369,775 | 21,939,996 | ||||||||||

|

Provision(benefit) for income tax

|

(2,944,350 | ) | (441,794 | ) | 1,477,677 | 3,392,623 | ||||||||||

|

Income (net) loss

|

(8,833,069 | ) | (1,501,928 | ) | 7,892,098 | 18,547,373 | ||||||||||

|

Other comprehensive income

|

||||||||||||||||

|

Foreign currency translation adjustment

|

15,991 | 649,089 | 1,976,139 | 2,175,395 | ||||||||||||

|

Comprehensive income (loss)

|

$ | (8,817,078 | ) | $ | (852,839 | ) | $ | 9,868,237 | 20,722,768 | |||||||

|

Basic earnings (loss) per common share

|

$ | 0.00 | $ | 0.00 | $ | 2.26 | 9.56 | |||||||||

|

Diluted earnings (loss) per common share

|

$ | 0.00 | $ | 0.00 | $ | 0.14 | 0.35 | |||||||||

|

Weighted average number of common shares

|

||||||||||||||||

|

Outstanding

|

||||||||||||||||

|

Basic

|

- | - | 3,181,504 | 1,867,972 | ||||||||||||

|

Diluted

|

- | - | 57,948,173 | 53,609,751 | ||||||||||||

|

PRO FORMA EPS (UNAUDITED)

|

||||||||||||

|

Keyuan International

Group LTD.

|

Keyuan International

Group LTD.

|

Keyuan International

Group LTD.

|

||||||||||

| Six Months Ended |

Six Months Ended

|

Year Ended

|

||||||||||

| June 30, |

June 30,

|

December 31,

|

||||||||||

| 2010 |

2010

|

2009

|

||||||||||

| (unaudited) |

(unaudited)

|

(unaudited)

|

||||||||||

|

Net income/(loss)

|

$

|

4,924,004

|

$

|

10,655,276

|

$

|

(8,833,069

|

)

|

|||||

|

Other comprehensive income (loss)

|

||||||||||||

|

Foreign currency translation gain

|

196,958

|

199,256

|

15,991

|

|||||||||

|

Comprehensive income (loss)

|

$

|

5,120,962

|

$

|

10,854,532

|

$

|

(8,817,078

|

)

|

|||||

|

Net income (loss) per Share

|

||||||||||||

|

Basic

|

$

|

0.41

|

$

|

0.88

|

$

|

(0.73

|

)

|

|||||

|

Diluted

|

$

|

0.08

|

$

|

0.16

|

$

|

(0.73

|

)

|

|||||

|

Weighted average shares outstanding

|

||||||||||||

|

Basic

|

12,136,003

|

12,136,003

|

12,136,003

|

|||||||||

|

Diluted

|

65,194,013

|

65,194,013

|

12,136,003

|

|||||||||

-5-

Balance Sheet Data:

|

As of December 31, 2009

|

As of December 31, 2008

|

As of

September 30,

2010

|

||||||||||

|

Cash and cash equivalents

|

$

|

14,030,655

|

$

|

9,094,537

|

$

|

44,932,623

|

||||||

|

Restricted cash

|

6,012,690

|

-

|

68,422,905

|

|||||||||

|

Trade notes receivable

|

400,491

|

-

|

3,292,506

|

|||||||||

|

Inventory

|

32,595,045

|

333,187

|

77,135,949

|

|||||||||

|

Advanced payments

|

7,417,202

|

17,849,208

|

18,173,457

|

|||||||||

| Prepaid taxes | 15,263,949 | 0 | 29,617,022 | |||||||||

| Tax rebate receivable | 0 | 0 | 8,171,637 | |||||||||

|

Property and equipment, net

|

131,824,617

|

32,351,840

|

129,086,205

|

|||||||||

| Intangible assets net | 6,378,316 | 6,646,190 | 12,256,149 | |||||||||

|

Total assets

|

219,060,334

|

67,154,129

|

391,573,599

|

|||||||||

|

Accounts payable – trade and accrued expenses

|

2,888,860

|

45,000

|

57,040,944

|

|||||||||

|

Trade notes payable

|

13,719,134

|

-

|

52,844,100

|

|||||||||

|

Short term bank loans

|

82,885,500

|

-

|

123,104,239

|

|||||||||

|

Total liabilities

|

208,432,375

|

57,409,089

|

318,703,507

|

|||||||||

|

Shareholders’ equity

|

10,627,959

|

9,745,040

|

72,870,092

|

|||||||||

RISK FACTORS

An investment in our Common Stock is speculative and involves a high degree of risk and uncertainty. You should carefully consider the risks described below, together with the other information contained in this prospectus, including the consolidated financial statements and notes thereto, before deciding to invest in our Common Stock. If any of the following risks occur, our business, financial condition and results of operations and the value of our Common Stock could be materially and adversely affected.

THE FOLLOWING MATTERS MAY HAVE A MATERIAL ADVERSE EFFECT ON OUR BUSINESS, FINANCIAL CONDITION, LIQUIDITY, RESULTS OF OPERATIONS OR PROSPECTS, FINANCIAL OR OTHERWISE. REFERENCE TO THIS CAUTIONARY STATEMENT IN THE CONTEXT OF A FORWARD-LOOKING STATEMENT OR STATEMENTS SHALL BE DEEMED TO BE A STATEMENT THAT ANY ONE OR MORE OF THE FOLLOWING FACTORS MAY CAUSE ACTUAL RESULTS TO DIFFER MATERIALLY FROM THOSE IN SUCH FORWARD-LOOKING STATEMENT OR STATEMENTS.

Risks Related to Our Business

Our limited operating history makes evaluation of our business difficult.

We have a limited operating history and have encountered and expect to continue to encounter many of the difficulties and uncertainties often faced by early stage companies. Our limited operating history makes it difficult to evaluate our future prospects, including our ability to develop a wide customer and distribution network for our services, to expand our operations to include additional services and to control raw material costs, all of which are critical to our success. An investor must consider our business and our prospects in light of the risks, uncertainties and difficulties common to early stage companies. We may encounter unanticipated problems, expenses and delays in developing and marketing our services and securing additional blending and storage facilities. We may not be able to successfully address these risks. If we are unable to address these risks, our business may not grow, our stock price may suffer, and we may be unable to stay in business.

As of December 31, 2009, we had not yet generated any net income from our operations.

We have incurred net operating losses since our inception. Our net loss was approximately $8,800,000 and $1,500,000 for the years ended December 31, 2009 and 2008, respectively. As of December 31, 2009, we had an accumulated net loss of $10,664,819. Although we anticipate that we will cease to incur operating losses commencing this year, there is no assurance that we will be able to generate net income in the near future or in such amount that meets our anticipation.

Key employees are essential to growing our business.

Chunfeng Tao, Jingtao Ma, Shifa Wang, Weifeng Xue and Mingliang Liu are essential to our ability to continue to grow our business. They have established relationships with customers and suppliers within the industries in which we operate. If one or more of these key employees were to leave us, our relationships with our customers and suppliers may become strained, and our growth strategy might be hindered, which could limit our ability to increase revenue.

In addition, although we are located in an area with good supply of skilled labor, we still face competition from other companies located in the same area for attracting skilled personnel. If we fail to attract and retain qualified personnel to meet current and future needs, this could slow our ability to grow our business, which could result in a decrease in market share.

We need additional capital to expand our manufacturing facility and we may not be able to obtain it at acceptable terms, or at all, which could adversely affect our ability to increase our production capacity and expand our business.

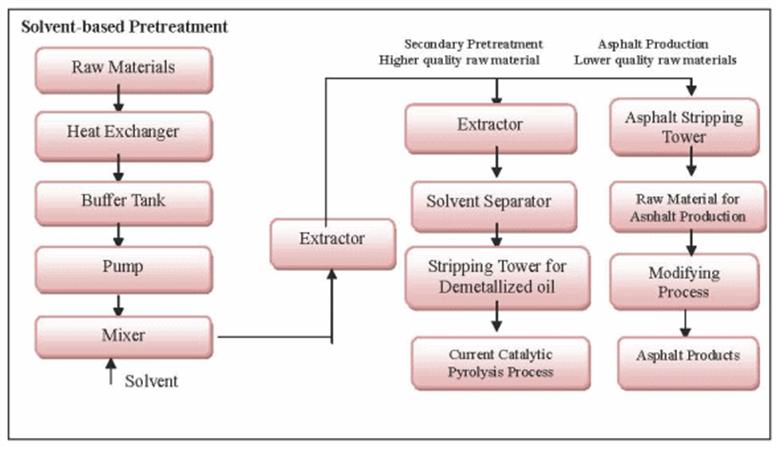

The estimated cost of our facility expansion and the addition of asphalt development is approximately $93.3 million including $5.8 million for purchasing land, $20 million for facility construction, $40 million for new equipment, $17.5 million for SBS project and $10 million for working capital for the whole business. We received gross proceeds of $46.5 million from the April-May 2010 Private Placement and the September 2010 Private Placement. We had originally planned to use $20 million of the net proceeds for the purchase of the land. However, due to the decrease of the actual cost of land purchase versus our original estimates, we were able to allocate a greater percentage of the net proceeds received toward raw material purchases in the second quarter. We currently plan to use cash from operations and other sources to fund the purchase of the land use rights. However, we still need additional cash resources to expand our manufacturing facility to include an SBS production facility , additional storage capacity, a raw material pre-treatment facility and an asphalt production facility. We plan to be funded through short-term borrowings, cash from operations and potential equity financing. However, our ability to obtain additional capital on acceptable terms is subject to a variety of uncertainties, including, but not limited to:

|

·

|

investors’ perception of, and demand for, securities of petrochemical manufacturing and supply companies;

|

|

·

|

conditions of the U.S. and other capital markets in which we may seek to raise funds;

|

|

·

|

our future results of operations, financial condition and cash flow;

|

|

·

|

PRC governmental regulation of foreign investment in petrochemical manufacturing companies in China;

|

|

·

|

economic, political and other conditions in China; and

|

|

·

|

PRC governmental policies relating to foreign currency borrowings.

|

Our operations may be adversely affected by the cyclical nature of the petroleum and petrochemical market and by the volatility of prices of petrochemical products.

All of our revenues are attributable to petrochemical products, which have historically been cyclical and sensitive to the availability and price of raw materials and general economic conditions. Markets for many of our products are sensitive to changes in industry capacity and output levels, cyclical changes in regional and global economic conditions, the price and availability of substitute products and changes in consumer demand, which from time to time have had a significant impact on product prices in the regional and global markets. Historically, the markets for these products have experienced alternating periods of tight supply, causing prices and margins to increase, followed by periods of capacity additions, finally resulting in oversupply and declining prices and margins. As tariffs and other import restrictions are reduced and the control of product pricing is relaxed in China, the markets for many of our products have become increasingly subject to the cyclicality of regional and global markets.

Our manufacturing processes could expose us to substantial production liability claims which will negatively impact our profitability.

We face an inherent business risk of exposure to product liability claims in the event that the use of our products is alleged to have resulted in adverse side effects. Side effects or marketing or manufacturing problems pertaining to any of our products could result in product liability claims or adverse publicity. These risks will exist for those products in clinical development and with respect to those products that have received regulatory approval for commercial sale. To date, we have not experienced any product liability claims. However, that does not mean that we will not have any such claims with respect to our products in the future which will negatively impact our profitability.

In the past several years we have derived a significant portion of our revenues from a small group of customers and we have purchased raw material from a small group of suppliers. If we are to remain dependent upon only a few customers and a few raw material suppliers, such dependency could negatively impact our business, operating results and financial condition.

For the years ended December 31, 2009, our five largest customers accounted for 70% of our total revenue, and the single largest customer accounted for 26% of our total sales. For the nine months ended September 30 , 2010, our five largest customers accounted for 42 % of our total sales. As our customer base may change from year-to-year, during such years that the customer base is highly concentrated, the loss of, or reduction of our sales to, any of such major customers could have a material adverse effect on our business, operating results and financial condition.

For the years ended December 31, 2009, our five largest suppliers accounted for approximately 70% of our raw material purchases. For the nine months ended June 30, 2010, our five largest suppliers accounted for 73.08 % of our total raw material purchase. As our supplier base may change from year-to-year, during such years that the supplier base is highly concentrated, the loss of, or reduction of our raw material supply from, any of such major suppliers could have a material adverse effect on our business, operating results and financial condition.

We may be exposed to risks relating to our disclosure controls and our internal controls and may need to incur significant costs to comply with applicable requirements.

During the fiscal years ended December 31, 2009 and 2008, and subsequent interim period ended June 30, 2010 and through the date of dismissal, we did not experience any reportable events, except that in its letter to us in 2009 pursuant to “Statement on Auditing Standards (SAS) 112: Communicating Internal Control Related Matters,” Hall, our former auditor, identified the following material weakness of our internal controls, which constitute a reportable event under Item 304(a)(1)(v) of Regulation S-K:

|

●

|

Reliance on financial reporting consultants for review of critical accounting areas and disclosures and material non-standard transactions;

|

|

●

|

Lack of sufficient accounting staff which results in a lack of segregation of duties necessary for a good system of internal control.

|

On April 22, 2010, Silver Pearl entered into a Share Exchange Agreement, by and among Keyuan International Group Limited (“Keyuan International”), a company organized under the laws of the British Virgin Islands, Delight Reward Limited, the sole shareholder of Keyuan International and a company organized under the laws of the British Virgin Islands (the “Keyuan International Shareholder”), and Denise D. Smith, our former principal stockholder (“Smith”). Pursuant to the terms of the Exchange Agreement, the Keyuan International Shareholder transferred to us all of the issued and outstanding ordinary shares of Keyuan International (the “Keyuan International Shares”) in exchange for the issuance of 47,658 shares of our Series M preferred stock, par value $0.001 per share (the “Series M Preferred Stock”) (such transaction is sometimes referred to herein as the “Share Exchange”). The Series M shares vote with the common stock on an as converted basis and are convertible into 47,658,000 shares of common stock upon the Company’s shareholders approving an increase in authorized common stock to at least 100,000,000 shares. As a result of the Share Exchange, we are now the holding company of Keyuan Plastics Co., Ltd., the operating subsidiary of Keyuan International organized in the People’s Republic of China (“China” or the “PRC”) and engaged in manufacturing and supplying various petrochemical products in China. The Share Exchange also caused a change-in-control of Silver Pearl as the Company’s shareholders have acquired the majority ownership of the combined entity. As a result, the accounting staff of our operating entity in China became the primary accounting staff of our company.

As of September 30 , 2010, considering the material weaknesses identified in our internal control, we performed an evaluation, under the supervision and with the participation of our management, including our Chief Executive Officer and Chief Financial Officer, of the effectiveness of the design and operation of our disclosure controls and procedures. This evaluation was designed to evaluate if our disclosure control and procedures provide reasonable assurance that material information required to be disclosed by us in the reports we file or submit under the Securities Exchange Act of 1934 is recorded, processed, summarized and reported within the time periods specified in the SEC’s rules and that the information is accumulated and communicated to our management as appropriate to allow timely decisions regarding required disclosure. Based on the evaluation, our management including our Chief Executive Officer and Chief Financial Officer, concluded that that the disclosure controls and procedures are effective as the date of September 30 , 2010 in giving us reasonable assurance that the information we are required to disclose in the reports we file or submit under the Exchange Act is recorded, processed, summarized and reported, within the time periods specified in the Commission's rules and forms and to ensure that such information is accumulated and communicated to our management, including our principal executive and principal financial officers, or persons performing similar functions, as appropriate to allow timely decisions regarding required disclosure. This conclusion was based on the following factors as the date of September 30 , 2010:

|

a)

|

We had a much expanded accounting team and employee base in our operating entity in China that allows for segregation of duties necessary for a good system of internal control. For example, our accounting staff had one Chief Financial Officer, one Vice President of Accounting, two accounting managers, and nine accountants responsible for four different accounting functions: financial accounting, cost accounting, capital/fund management and data analysis. The expansion of our team not only allowed the proper segregation of duties, but also allowed implementation of proper review processes necessary for ensuring the accuracy of financial data used in preparing financial statements.

|

|

b)

|

We had improved our accounting staff’s knowledge of U.S. accounting standards and requirements by hiring a CFO with significant U.S. accounting and finance experience and a bi-lingual accounting manager with significant financial reporting experience. As a result, we were able to prepare and review certain important accounting transactions and disclosures internally rather than relying on outside consultants.

|

|

c)

|

Finally, we have recently appointed an audit committee comprised of independent members of our board of directors, including an audit committee chairman, whom we believe to meet the SEC’s definition of a “financial expert” in the Sarbanes-Oxley Act Section 406 and 407. We concluded that increased oversight and experience provided by the audit committee assisted us in the establishment and oversight of our controls and procedures.

|

-8-

In addition, our CFO and our accounting staff are currently working on documenting our internal controls and we expect such documentation to be complete in 2010 and we plan testing of internal controls thereafter. If our market capitalization exceeds $75 million in 2011, we will be required to be in compliance with the Sarbanes-Oxley Act Section 404 in the fiscal year of 2011. However our CFO and accounting staff have already taken actions to start our Sarbanes-Oxley Action 404 compliance project. We expect this compliance project will enhance the Company’s internal controls significantly. We are also looking to fill additional financial staff positions. Specifically, we believe that additional accounting staff trained in U.S. GAAP would improve our controls and procedures, specifically with regard to the preparation of our financial statements. Finally, we have recently appointed an audit committee comprised of independent members of our board of directors, including an audit committee chairman, whom we believe to meet the SEC’s definition of a “financial expert” in the Sarbanes-Oxley Act Section 406 and 407. We believe that the increased oversight and experience provided by the audit committee will assist us in the establishment and oversight of our controls and procedures. Although we believe that these corrective steps will remediate the material weaknesses discussed above when all of the additional financial staff positions are filled, we cannot assure you that this will be sufficient. We may be required to expend additional resources to identify, assess and correct any additional weaknesses in our internal control. We cannot make assurances that we will not identify additional material weaknesses in our internal control over financial reporting in the future.

Insurance coverage for some of our operations may be insufficient to cover losses.

The insurance industry in China is still at an early stage of its development. Insurance companies in China offer limited business insurance products or offer them at a high price. We do not maintain insurance coverage for various risks, including environmental claims. A significant uninsured claim against us would have a material adverse effect on our financial position and results of operations.

Failure to comply with environmental laws and regulations may have a material adverse effect on our business and results of operations.

We are subject to various environmental laws and regulations that require us to obtain environmental permits for our operations. If we fail to obtain all required environmental permits for our operations, or comply with the provisions of our permit, we could be subject to fines, criminal charges or other sanctions by regulators, including the suspension or termination of our operations. We are required to comply with extensive and complex environmental laws and regulations at various levels in the PRC relating to, among other things:

|

•

|

the handling of petrochemical products;

|

|

•

|

the operation of petrochemical product storage facilities;

|

|

•

|

workplace safety;

|

|

•

|

environmental damage; and

|

|

•

|

hazardous waste disposal.

|

If we are involved in a spill or other accident involving hazardous substances, or if we are found to be in violation of environmental laws or regulations, we could be subject to liabilities that could have a material adverse effect on our business, financial condition and results of operations. If we should fail to comply with applicable environmental regulations, we could be subject to substantial fines or penalties and to civil and criminal liability. We cannot assure you that at all times we will be in compliance with environmental laws and regulations or our environmental permits or that we will not be required to expend significant funds to comply with, or discharge liabilities arising under, environmental laws, regulations and permits.

Our failure to protect our technologies could have a negative impact on our business.

Our manufacturing technologies and process, which have not been patented or registered as our property, are key components of our competitive advantage and our growth strategy. We rely on confidentiality and license agreements with certain of our employees, customers and others to protect the confidentiality of our technologies. If we are unable to adequately protect the confidentiality of these technologies, our business, results of operations, financial condition and prospects could be materially and adversely affected.

If we are unable to establish appropriate internal financial reporting controls and procedures, it could cause us to fail to meet our reporting obligations, result in the restatement of our financial statements, harm our operating results, subject us to regulatory scrutiny and sanction, cause investors to lose confidence in our reported financial information and have a negative effect on the market price for shares of our Common Stock.

Effective internal controls are necessary for us to provide reliable financial reports and to effectively prevent fraud. We maintain a system of internal control over financial reporting, which is defined as a process designed by, or under the supervision of, our principal executive officer and principal financial officer, or persons performing similar functions, and effected by our board of directors, management and other personnel, to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles.

As a public company, we will have significant additional requirements for enhanced financial reporting and internal controls. We are aware of that smaller reporting companies (market cap less than $75,000,000) are exempted from the requirements of the Sarbanes-Oxley Act Section 404 pursuant to the Dodd-Frank Wall Street Reform and Consumer Protection Act, which was adopted on July 21, 2010. However, with the current development pace of the Company, we anticipate that we may exceed the market cap of $75,000,000 soon. Therefore, we plan to continue our efforts to design and implement effective internal controls. The process of designing and implementing effective internal controls is a continuous effort that requires us to anticipate and react to changes in our business and the economic and regulatory environments and to expend significant resources to maintain a system of internal controls that is adequate to satisfy our reporting obligations as a public company.

We cannot assure you that we will not, in the future, identify areas requiring improvement in our internal control over financial reporting. We cannot assure you that the measures we will take to remediate any areas in need of improvement will be successful or that we will implement and maintain adequate controls over our financial processes and reporting in the future as we continue our growth. If we are unable to establish appropriate internal financial reporting controls and procedures before we exceed the market cap of $75,000,000, it could cause us to fail to meet our reporting obligations, result in the restatement of our financial statements, harm our operating results, subject us to regulatory scrutiny and sanction, cause investors to lose confidence in our reported financial information and have a negative effect on the market price for shares of our Common Stock.

We will incur increased costs as a result of being a public company.

As a public company, we will incur significant legal, accounting and other expenses that we did not incur as a private company. In addition, the Sarbanes-Oxley Act, as well as new rules subsequently implemented by the SEC, has required changes in corporate governance practices of public companies. We expect these new rules and regulations to increase our legal, accounting and financial compliance costs and to make certain corporate activities more time-consuming and costly. In addition, we will incur additional costs associated with our public company reporting requirements. We are currently evaluating and monitoring developments with respect to these new rules, and we cannot predict or estimate the amount of additional costs we may incur or the timing of such costs. Additionally, if we are unable to comply with the Sarbanes-Oxley Act’s internal controls requirements, we may not be able to obtain the independent auditor certifications that Sarbanes-Oxley Act requires publicly-traded companies to obtain.

Risks Relating to Regulation of Our Business

Uncertainties with respect to the governing regulations could have a material and adverse effect on us.

There are substantial uncertainties regarding the interpretation and application of the PRC laws and regulations, including, but not limited to, the laws and regulations governing our business and our ownership of equity interest in Keyuan Plastics, a wholly foreign owned enterprise under the PRC laws. These laws and regulations are relatively new and may be subject to change, and their official interpretation and enforcement may involve substantial uncertainty. The effectiveness of newly enacted laws, regulations or amendments may be delayed, resulting in detrimental reliance by foreign investors. New laws and regulations that affect existing and proposed future businesses may also be applied retroactively.

The PRC government has broad discretion in dealing with violations of laws and regulations, including levying fines, revoking business permits and other licenses and requiring actions necessary for compliance. In particular, licenses and permits issued or granted to the PRC subsidiary by relevant governmental bodies may be revoked at a later time by higher regulatory bodies. We cannot predict the effect of the interpretation of existing or new PRC laws or regulations on our businesses. We cannot assure you that our current ownership and operating structure would not be found in violation of any current or future PRC laws or regulations. As a result, we may be subject to sanctions, including fines, and could be required to restructure our operations or cease to provide certain services. In addition, any litigation in China may be protracted and result in substantial costs and diversion of resources and management attention. Any of these or similar actions could significantly disrupt our business operations or restrict us from conducting a substantial portion of our business operations, which could materially and adversely affect our business, financial condition and results of operations.

Keyuan Plastics will be subject to restrictions on dividend payments.

Though currently we have not received any dividends from Keyuan Plastics, in the future, we may rely on dividends and other distributions from Keyuan Plastics to provide us with cash flow and to meet our other obligations. Current regulations in the PRC would permit the PRC subsidiary to pay dividends to us only out of its accumulated distributable profits, if any, determined in accordance with Chinese accounting standards and regulations. In addition, Keyuan Plastics will be required to set aside at least 10% (up to an aggregate amount equal to half of its registered capital) of its accumulated profits each year. Such cash reserve may not be distributed as cash dividends. In addition, if the PRC subsidiary incurs debt on its own behalf in the future, the instruments governing the debt may restrict its ability to pay dividends or make other payments to us.

PRC regulations on loans and direct investments by overseas holding companies in PRC entities may delay or prevent us to make overseas loans or additional capital contributions to our PRC subsidiary.

Under the PRC laws, foreign investors may make loans to their PRC subsidiaries or foreign investors may make additional capital contributions to their PRC subsidiaries. Any loans to such PRC subsidiaries are subject to the PRC regulations and foreign exchange loan registrations, i.e. loans by foreign investors to their PRC subsidiaries to finance their activities cannot exceed statutory limits and must be registered with the State Administration of Foreign Exchange (the “SAFE”), or its local branch. Foreign investors may also decide to finance their PRC subsidiaries by means of additional capital contributions. These capital contributions must be examined and approved by the Ministry of Commerce of the People’s Republic of China (the “MOFCOM”), or its local branch in advance.

Under the PRC Enterprise Income Tax Law, we may be classified as a “resident enterprise” of China, and such classification would likely result in unfavorable tax consequences to us and our non-PRC stockholders.

On March 16, 2007, the National People’s Congress (the “NPC”), approved and promulgated the PRC Enterprise Income Tax Law (herein referred as the “New EIT Law”). The New EIT Law took effect on January 1, 2008. Under the New EIT Law, Foreign Investment Enterprises ( “FIEs”), and domestic companies are subject to a uniform tax rate of 25%. In addition, an enterprise established outside of China with “de facto management bodies” within China is considered a “resident enterprise” which means that we may be treated in a manner similar to a Chinese enterprise for enterprise income tax purposes. The New EIT Law provides a five-year transition period starting from its effective date for those enterprises which were established before the promulgation date of the New EIT Law and which were entitled to a preferential lower tax rate under the then-effective tax laws or regulations. However, since we were established after the promulgation date of the NEW EIT law, the five-year transition period will not be applicable to us if the PRC tax authorities determine that we are a “resident enterprise” for PRC enterprise income purposes.

On December 26, 2007, the State Council issued a Notice on Implementing Transitional Measures for Enterprise Income Tax, or the Notice, providing that the enterprises that have been approved to enjoy a low tax rate prior to the promulgation of the New EIT Law will be eligible for a five-year transition period since January 1, 2008, during which time the tax rate will be increased step by step to the 25% unified tax rate set out in the New EIT Law. From January 1, 2008, for the enterprises whose applicable tax rate was 15% before the promulgation of the New EIT Law , the tax rate will be increased to 18% for year 2008, 20% for year 2009, 22% for year 2010, 24% for year 2011 and 25% for year 2012. For the enterprises whose applicable tax rate was 24%, the tax rate will be changed to 25% from January 1, 2008.

Under the New EIT Law, an enterprise established outside of China with “de facto management bodies” within China is considered a “resident enterprise,” meaning that it can be treated in a manner similar to a Chinese enterprise for enterprise income tax purposes. The implementing rules of the New EIT Law define de facto management as “substantial and overall management and control over the production and operations, personnel, accounting, and properties” of the enterprise. Because the New EIT Law and its implementing rules are new, no official interpretation or application of this new “resident enterprise” classification is available. Therefore, it is unclear how tax authorities will determine tax residency based on the facts of each case.

If the PRC tax authorities determine that we are “resident enterprises” for PRC enterprise income tax purposes, a number of unfavorable PRC tax consequences could follow. First, we may be subject to the enterprise income tax at a rate of 25% on our worldwide taxable income as well as PRC enterprise income tax reporting obligations. In our case, this would mean that income such as interest on offering proceeds and non-China source income would be subject to PRC enterprise income tax at a rate of 25%. Second, although under the New EIT Law and its implementing rules, dividends paid to us from our PRC subsidiaries would qualify as “tax-exempt income,” we cannot guarantee that such dividends will not be subject to a 10% withholding tax, as the PRC foreign exchange control authorities, which enforce the withholding tax, have not yet issued guidance with respect to the processing of outbound remittances to entities that are treated as resident enterprises for PRC enterprise income tax purposes. Finally, it is possible that “resident enterprise” classification could result in a situation in which a 10% withholding tax is imposed on dividends we pay to our non-PRC stockholders and with respect to gains derived by our non-PRC stockholders from transferring our shares. We are actively monitoring the possibility of “resident enterprise” treatment for the applicable tax years and are evaluating appropriate organizational changes to avoid this treatment, to the extent possible.

If we were treated as a “resident enterprise” by PRC tax authorities, we would be subject to taxation in both the U.S. and China, and our PRC tax may not be credited against our U.S. tax.

If we receive any dividends from Keyuan Plastics in the future, the dividends may be subject to PRC withholding tax.

The New EIT Law and the Implementation Rules of the New EIT Law provides that an income tax rate of 10% may be applicable to dividends payable to non-PRC investors that are “non-resident enterprises”, which (i) do not have an establishment or place of business in the PRC, or (ii) have such establishment or place of business in the PRC but the relevant income is not effectively connected with the establishment or place of business, to the extent such dividends are derived from sources within the PRC. The income tax for non-resident enterprises shall be subject to withholding at the income source, with the payer acting as the obligatory withholder under the New EIT Law, and therefore such income taxes are generally called withholding tax in practice. It is currently unclear in what circumstances a source will be considered as located within the PRC. We are an offshore holding company. Thus, if we are considered as a “non-resident enterprise” under the New EIT Law and the dividends paid to us by our subsidiary in the PRC are considered income sourced within the PRC, such dividends may be subject to a 10% withholding tax. Currently, we have not received any dividends paid by our subsidiary in the PRC. Furthermore, since we intend to reinvest its earnings to further expand its businesses in mainland China, our subsidiary in the PRC does not intend to declare dividends to their immediate foreign holding companies in the foreseeable future.

In January 2009, the State Administration of Taxation, or SAT, promulgated the Provisional Measures for the Administration of Withholding of Enterprise Income Tax for Non-resident Enterprises (“Measures”), pursuant to which, the entities which have the direct obligation to make the following payment to a non-resident enterprise shall be the relevant tax withholders for such non-resident enterprise, and such payment includes: incomes from equity investment (including dividends and other return on investment), interests, rents, royalties, and incomes from assignment of property as well as other incomes subject to enterprise income tax received by non-resident enterprises in China. Further, the Measures provides that in case of equity transfer between two non-resident enterprises which occurs outside China, the non-resident enterprise which receives the equity transfer payment shall, by itself or engage an agent to, file tax declaration with the PRC tax authority located at place of the PRC company whose equity has been transferred, and the PRC company whose equity has been transferred shall assist the tax authorities to collect taxes from the relevant non-resident enterprise. However, it is unclear whether the Measures refer to the equity transfer by a non-resident enterprise which is a direct or an indirect shareholder of the said PRC company. Given these Measures, there is a possibility that Keyuan Plastics may have an obligation to withhold income tax in respect of the dividends paid to non-resident enterprise investors.

The new tax law provides only a framework of the enterprise tax provisions, leaving many details on the definitions of numerous terms as well as the interpretation and specific applications of various provisions unclear and unspecified. Any increase in the combined company’s tax rate in the future could have a material adverse effect on its financial conditions and results of operations.

We face uncertainty from China’s Circular on Strengthening the Administration of Enterprise Income Tax on Non-Resident Enterprises' Share Transfer (Circular 698 that was released in December 2009 with retroactive effect from January 1, 2008.)

The Chinese State Administration of Taxation released a circular (“Circular 698”) on December 10, 2009 that addresses the transfer of shares by nonresident companies. Circular 698, which is effective retroactively to January 1, 2008, may have a significant impact on many companies that use offshore holding companies to invest in China. Pursuant to Circular 698, where the withholding agent does not withhold in accordance with laws or can’t perform the withholding obligation, the non-resident enterprises shall file tax declaration with the PRC tax authority located at place of the resident enterprise whose equity has been transferred, within seven days since the date of equity transfer provided under the contracts.

Where a foreign investor indirectly transfers equity interests in a Chinese resident enterprise by selling the shares in an offshore holding company, and the latter is located in a country or jurisdiction where the effective tax burden is less than 12.5% or where the offshore income of his, her, or its residents is not taxable, the foreign investor is required to provide the tax authority in charge of that Chinese resident enterprise with the relevant information within 30 days of the transfers. Moreover, where a foreign investor indirectly transfers equity interests in a Chinese resident enterprise through an abuse of form of organization and there are no reasonable commercial purposes such that the corporate income tax liability is avoided, the PRC tax authority will have the power to re-assess the nature of the equity transfer in accordance with PRC’s “substance-over-form” principle and deny the existence of the offshore holding company that is used for tax planning purposes.

There is uncertainty as to the application of Circular 698. For example, while the term "indirectly transfer" is not defined, it is understood that the relevant PRC tax authorities have jurisdiction regarding requests for information over a wide range of foreign entities having no direct contact with China. Moreover, the relevant authority has not yet promulgated any formal provisions or formally declared or stated how to calculate the effective tax in the country or jurisdiction and to what extent and the process of the disclosure to the tax authority in charge of that Chinese resident enterprise. In addition, there are no formal declarations with regard to how to decide abuse of form of organization and reasonable commercial purpose, which can be utilized by us to balance if our company complies with the Circular 698. As a result, we may become at risk of being taxed under Circular 698 and we may be required to expend valuable resources to comply with Circular 698 or to establish that we should not be taxed under Circular 698, which could have a material adverse effect on our financial condition and results of operations.

Keyuan Plastics is obligated to withhold and pay PRC individual income tax on behalf of our employees who are subject to PRC individual income tax. If we fail to withhold or pay such individual income tax in accordance with applicable PRC regulations, we may be subject to certain sanctions and other penalties and may become subject to liability under PRC laws.

Under PRC laws, Keyuan Plastics is obligated to withhold and pay individual income tax on behalf of our employees who are subject to PRC individual income tax. If the PRC subsidiary fails to withhold and/or pay such individual income tax in accordance with PRC laws, it may be subject to certain sanctions and other penalties and may become subject to liability under PRC laws.

In addition, the SAT has issued several circulars concerning employee stock options. Under these circulars, our employees working in the PRC (which could include both PRC employees and expatriate employees subject to PRC individual income tax) who exercise stock options will be subject to PRC individual income tax. Our PRC subsidiary has obligations to file documents related to employee stock options with relevant tax authorities and withhold and pay individual income taxes for those employees who exercise their stock options. While tax authorities may advise us that our policy is compliant, they may change their policy, and we could be subject to sanctions.

Regulation of foreign currency’s conversion into RMB and investment by FIEs may adversely affect our PRC subsidiary’s direct investment in China