Attached files

| file | filename |

|---|---|

| EX-32 - EXHIBIT 32 - CERTIFICATION - TECHE HOLDING CO | ex-32.htm |

| EX-23 - EXHIBIT 23 - CONSENT OF AUDITORS - TECHE HOLDING CO | ex-23.htm |

| EX-31.2 - EXHIBIT 31.2 - CERTIFICATION OF CFO - TECHE HOLDING CO | ex-31_2.htm |

| EX-31.1 - EXHIBIT 31.1 - CERTIFICATION OF CEO - TECHE HOLDING CO | ex-31_1.htm |

| 10-K - FORM 10-K 09-30-10 TECHE HOLDING COMPANY - TECHE HOLDING CO | f10k_093010-0123.htm |

|

Teche Holding Company

|

New Iberia

|

Baton Rouge

|

|

1120 Jefferson Terrace Boulevard

|

142 W. St. Peter Street

|

Wal-Mart Neighborhood Market

|

|

New Iberia, LA 70560

|

New Iberia, LA 70560

|

9830 Old Hammond Highway

|

|

PHONE (337) 560-7151

|

(337) 364-5528

|

Baton Rouge, LA 70816

|

|

FAX (337) 365-7130

|

(225) 926-7378

|

|

|

Lafayette

|

||

|

New Iberia

|

Broadmoor

|

Breaux Bridge

|

|

1120 Jefferson Terrace Boulevard

|

5121 Johnston Street

|

601 East Bridge Street

|

|

New Iberia, LA 70560

|

Lafayette, LA 70503

|

Breaux Bridge, LA 70517

|

|

(337) 365-0366

|

(337) 981-1887

|

(337) 332-2149

|

|

Call Center (800) 897-0315

|

||

|

Lafayette

|

Houma

|

|

|

Franklin

|

Downtown

|

706 Barrow Street

|

|

211 Willow Street

|

1001 Johnston Street

|

Houma, LA 70360

|

|

Franklin, LA 70538

|

Lafayette, LA 70501

|

(985) 868-8766

|

|

(337) 828-3212

|

(337) 232-6463

|

|

|

Houma

|

||

|

Franklin Drive-Thru

|

Lafayette

|

912 Grand Caillou Road

|

|

1823 Main Street

|

2200 W. Pinhook Road

|

Houma, LA 70363

|

|

Franklin, LA 70538

|

Lafayette, LA 70508

|

(985) 857-9990

|

|

(337) 828-4177

|

(337) 232-3419

|

|

|

Thibodaux

|

||

|

Morgan City

|

Baton Rouge

|

921 Canal Boulevard

|

|

1001 7th Street

|

3524 S. Sherwood Forest Boulevard

|

Thibodaux, LA 70301

|

|

Morgan City, LA 70380

|

Baton Rouge, LA 70816

|

(985) 446-6707

|

|

(985) 384-0653

|

(225) 293-0954

|

|

|

Opelousas

|

||

|

Bayou Vista

|

Baton Rouge

|

428 E. Landry Street

|

|

206 Arlington Street

|

Wal-Mart Supercenter

|

Opelousas, LA 70570

|

|

Bayou Vista, LA 70380

|

2171 O’Neal Lane

|

(337) 942-5748

|

|

(985) 395-5244

|

Baton Rouge, LA 70816

|

|

|

(225) 751-0264

|

Eunice

|

|

|

New Iberia

|

840 E. Laurel Avenue

|

|

|

529 N. Lewis Street

|

Eunice, LA 70535

|

|

|

New Iberia, LA 70563

|

(337) 457-9585

|

|

|

(337) 367-2516

|

||

|

www.teche.com

|

|

Table of Contents

|

|

|

President’s Message

|

2

|

|

Selected Financial Data

|

6

|

|

Business of the Bank - Business of the Company

|

7

|

|

Summary of Quarterly Operating Results

|

7

|

|

Market and Dividend Information

|

8

|

|

Management’s Discussion and Analysis of Financial

|

|

|

Condition and Results of Operations

|

9

|

|

Management’s Report

|

17

|

|

Report of Independent Registered Public Accounting Firm

|

18

|

|

Consolidated Balance Sheets

|

19

|

|

Consolidated Statements of Income

|

20

|

|

Consolidated Statements of Stockholders’ Equity

|

21

|

|

Consolidated Statements of Cash Flows

|

22

|

|

Notes to Consolidated Financial Statements

|

24

|

|

Directors and Officers

|

58

|

1

Message from Patrick Little, Chairman and CEO

|

|

|

|

Teche achieved superior results for our fiscal year 2010. We exceeded our record earnings of 2009, paid the highest dividend in our history to our shareholders, strengthened our capital position and maintained asset quality. Our team has consistently demonstrated profitability and returned profits to our shareholders with cash dividends since we have been a public company. |

| |

|

Results of Fiscal Year 2010

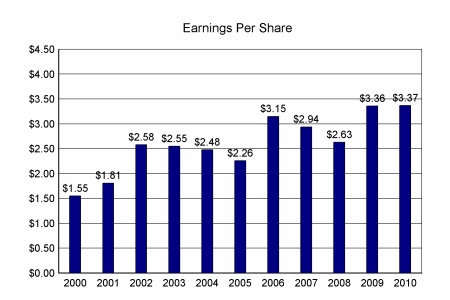

Teche Holding Company, parent of Teche Federal Bank set an earnings per share record in fiscal year 2010 of $3.36. Teche also paid a record cash dividend of $1.42 per share. We are proud of our results. These results were achieved, in spite of, a deep water oil drilling moratorium, national economic slowdown and anticipated regulatory changes.

Teche did not take TARP and our consistent earnings has put us in a strong capital position. Tangible equity increased to 9.48% of total assets compared to 8.90% in fiscal year 2009. Risk based capital was also a strong 13.52% compared to 12.72% in fiscal year 2009 and tangible book value increased to a record $34.43.

|

|

|

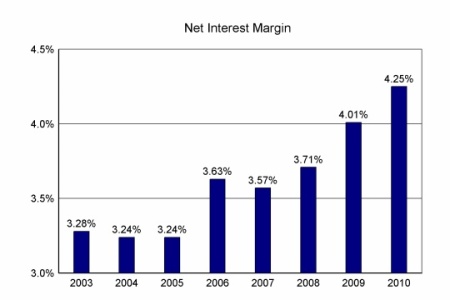

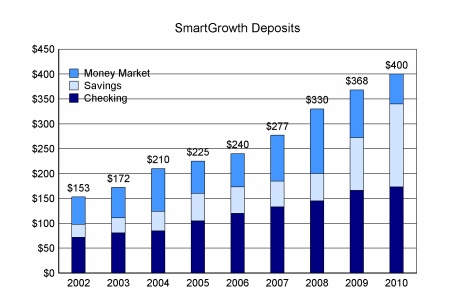

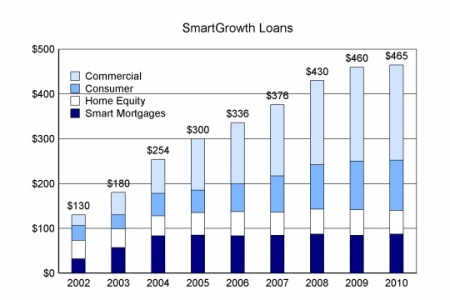

Our SmartGrowth strategy of growing high quality, higher yielding and shorter term loans and lower cost core deposits again contributed to an increase in our net interest margin. Our net interest margin increased to 4.25% compared to 4.01% in 2009. SmartGrowth loans now comprise 78% of our loan portfolio whereas in 2001 SmartGrowth loans were only 27% of total loans and SmartGrowth deposits are 69% of total deposits compared to 29% in 2001. Over the course of 10 years we have significantly changed our loan and deposit mix with excellent results for our shareholders.

|

|

|

Deposit Growth

This year as in the previous 10 years we have grown the “right kind of deposits.” SmartGrowth deposits increased $32.5 million or 8.8% from $367.7 million at fiscal year end in 2009 to $400.2 million at fiscal year end in 2010. Checking account balances alone increased $7.4 million or 4.5% in the last twelve months. Teche has continued its Totally Free Checking program and our customers have continued to respond. Savings accounts also increased significantly to $166.7 million at 2010 year end from $106.5 at 2009 year end, an increase of 57%.

|

|

2

|

Loan Growth

Teche this year as in the previous 10 years grew the “right kinds of loans.” SmartGrowth loans increased to $464.9 million in fiscal year 2010. SmartGrowth loans consist of consumer, commercial, home equity and SmartMortgages. Consumer loans grew 3.3%, commercial loan balances increased 1.3% and SmartMortgages grew by 3.8% reversing the decline that the bank saw in this segment during 2009. SmartMortgages are mortgages which don’t fit the customary home mortgage profile and have slightly higher rates of interest. They are NOT ‘subprime mortgages’ and the borrowers have passed the high standards of credit that Teche requires. Home equity loans declined by 8.5% as home owners retained the equity in their homes as part of the national trend of conservative spending and increased savings.

|

|

Teche has $131 million in traditional fixed or adjustable rate mortgages and these have decreased slightly over the last twelve months as Teche sold a portion of its originated loans.

Asset Quality

Teche did not take TARP funds. Teche has continued the Company’s strong commitment to asset quality with sound underwriting standards, excellent servicing and diligent collection efforts. Non-performing assets to total assets were 2.06% at fiscal year end. This is a quality metric that favorably compares to 68 other southern banks with an average of 3.65% in non-performing assets to total assets in the last twelve months. Teche’s net charge-offs to average loans were 0.24% at fiscal year end compared to 0.29% in 2009. The average of net charge-offs to average loans at 66 other southern banks was 1.65%.

While asset quality at the company has remained strong overall, Teche feels that a prudent policy of provisioning is the correct path in this current economy and has increased the allowance for loan losses to $9.2 million from $6.8 million in the last twelve months.

Technology and Efficiency

Teche recognizes that smartly deployed technology is critical to superior customer service and cost containment in a highly competitive banking future. As part of our strategic plan, we initiated several improvements this year. We implemented a state-of-the-art content management and document imaging system which allows for more streamlined processing and improved efficiency in all aspects of our operations. In a concentrated effort to deliver the products and services that our business customers need to succeed, we introduced several exciting business services such as remote deposit capture and enhanced cash management tools. In 2011 these efforts continue as we embark on a significant upgrade to our core banking platforms and electronic delivery channels. Our investment in new technology increases the Bank’s capacity for future growth with high levels of efficiency.

Regulatory Changes

In 2010 a regulatory reform bill was passed by Congress and signed into law on July 21, 2010. It is anticipated that this legislation will have wide ranging effects on the financial industry. The media has focused on the effects of the bill on large financial firms, however, some aspects of this new law will affect community banks like Teche Federal Bank. For example, the Consumer Financial Protection Bureau created by the bill may alter the relationship between individuals and all financial providers including community banks like Teche.

The new law is complex and it will take a considerable amount of time to enact all of its parts. One aspect of the law, the Durbin amendment, gives the Federal Reserve control over the pricing of interchange fees between merchants and banks and its effective date is July 21, 2011. Another part of the bill that will be also effective on July 21, 2011 will be the absorption of the authority and duties of The Office of Thrift Supervision, Teche’s current regulator, by the Office of the Comptroller of the Currency. We will closely monitor the implementation of all aspects of this law as it evolves and respond in the best interests of our customers and shareholders.

3

Louisiana Economy

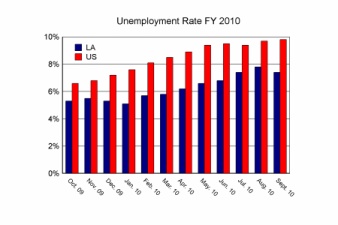

Louisiana, in recent years, has had lower unemployment rates than the rest of the country. Louisiana’s unemployment rate in September 2010 was 7.8% while the U.S. rate was 9.6%. The MSAs of Teche’s locations have comparatively low unemployment rates as well. Houma is the lowest with 5.5%, Lafayette’s rate was 6.2% and Baton Rouge’s rate was 7.8% in September of 2010. The deep water oil exploration moratorium is now lifted, however, the long term effects are still to be determined. Teche up to this point has had minimal direct exposure. In addition, onshore oil and gas exploration has remained active in Louisiana and unaffected by offshore restrictions. Teche believes that continued demand for oil and gas will accrue benefits in our markets.

Louisiana is the number one state for oil exploration and numerous oil platforms are operating off of Louisiana’s coast in both deep and shallow water. The energy industry is important to our economy. Up until the BP Horizon event, 55,000 wells had been drilled in the Gulf of Mexico without a single major spill as defined by the Minerals Management Service according to Dr. Loren Scott’s “Louisiana Economic Outlook, 2011-2012.” The Industry record overall is a good one for safety and this industry will continue to supply the energy needs of our country.

|

The petrochemical industry is also a large supplier of economic vitality and jobs especially in the Baton Rouge to New Orleans region. Baton Rouge has a heavy concentration of the industry with 78 manufacturing plants employing ~12,000 people in a nine parish (county) area.

New projects by ExxonMobil, SNF Polymer and Westlake Chemicals combine for a future investment of $912 million in the region. Improvements in the Huey P. Long and Twin Span Bridges for a $2.0 billion investment and the completion of the Audubon Bridge north of Baton Rouge for $406 million will enhance the transportation network that is vital to the petrochemical industry.

Louisiana has also strategically diversified its economy. The generous state incentive of 30% for movie production is now permanent and Louisiana is the third largest producer of movies after California and New York. The Louisiana Office of Entertainment reported that in-state spending was $803 million in 2009 and they are predicting $1.3 billion in 2010. The Baton Rouge area is also seeing major expansions of Woman’s Hospital, one of the largest specialty hospitals in the country, with a $300 million investment in a new facility which is under construction. In addition two hospitals - Our Lady of the Lake and Lane Memorial have expansions and improvements underway for a $70 million investment in the area.

|

|

Houma and Lafayette both are affected to some degree by the oil drilling moratorium. Houma however sees expansion and development in its shipbuilding and fabrication industries with Edison Chouest completing its new shipyard this year which will employ 1000 people. Lafayette is experiencing expansion with a $70 million building project for Lafayette General Hospital and growth in employment at Stuller Settings and Bruce Foods. However Lafayette’s growth in the next two years will be related to the return of offshore oil drilling activities.

4

|

Shareholder Return

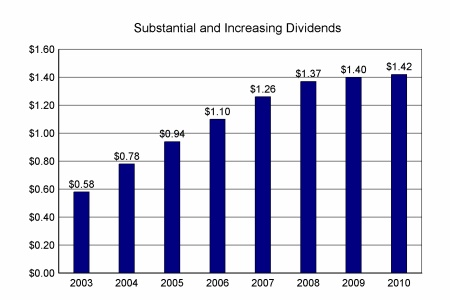

Teche has been consistently profitable since becoming a public company. Warren Buffet said, “A good CEO has the mind of an investor and a good investor has the mind of a CEO.” Our directors and employees have the minds of investors because many are investors in the Company’s stock. Insider ownership including employees is 36%. Our goals are aligned with our investors in a very real way. We paid a record dividend for fiscal year 2010 of $1.42 and we have paid dividends for sixty-one consecutive quarters. Our dividend yield was 4.58% and our payout ratio was 41.77% for fiscal year 2010. These metrics favorably compare to 1.76% average dividend yield for 72 other southern banks and 26.88% average payout ratio for 55 other southern banks. In addition our board has approved a plan to repurchase up to 3% of the Company’s stock. If you purchased 100 shares of Teche’s stock at the end of fiscal year 2000 and sold those shares at the end of fiscal year 2010 you would have a gain of 208% pre-tax income. This year our annualized return on average equity was 9.43% and our annualized return on average tangible equity was 9.94%. We believe that shareholders who learn our story and monitor our consistent results will understand that we have their interests foremost in our minds.

|

|

Consistency and Resiliency

Throughout my remarks I have alluded to Teche’s 10 year strong track record of results. I believe the resiliency and growth of our Company is attributable to our focus on our successful SmartGrowth strategy, our talented leadership team and the support and training that we provide to our employees. Year after year our employees service our customers and ask them for more of their business. Our growth is mainly due to increasing market share in our current markets and we have more room to expand in those areas. We are always looking for new ways to continue to increase the value of our Company.

We are proud of our progress this year and we believe that we can continually improve and grow our institution in the future. We appreciate your investment and your support.

|

Sincerely,

Patrick Little

Chairman and President/CEO

|

|

|

5

SELECTED FINANCIAL DATA (Dollars in thousands, except per share data)

At or for the Year Ended September 30,

|

2010

|

2009

|

2008

|

2007

|

2006

|

||||||||||||||||

|

Assets

|

$ | 761,524 | $ | 765,071 | $ | 769,488 | $ | 719,367 | $ | 685,750 | ||||||||||

|

Loans Receivable, Net

|

586,635 | 588,527 | 584,139 | 561,623 | 520,185 | |||||||||||||||

|

Securities-Available for Sale

|

14,996 | 20,936 | 26,652 | 51,647 | 63,517 | |||||||||||||||

|

Securities-Held to Maturity

|

59,566 | 75,384 | 54,291 | 31,855 | 38,743 | |||||||||||||||

|

Cash and Cash Equivalents

|

40,655 | 23,675 | 50,112 | 21,811 | 17,528 | |||||||||||||||

|

Deposits

|

579,355 | 585,469 | 589,228 | 555,569 | 537,549 | |||||||||||||||

|

FHLB Advances

|

100,017 | 100,628 | 104,877 | 89,756 | 77,386 | |||||||||||||||

|

Stockholders’ Equity

|

75,513 | 71,485 | 68,044 | 67,006 | 63,929 | |||||||||||||||

|

SUMMARY OF OPERATIONS

|

||||||||||||||||||||

|

Interest Income

|

$ | 41,336 | $ | 44,237 | $ | 45,633 | $ | 43,041 | $ | 39,197 | ||||||||||

|

Interest Expense

|

11,704 | 15,297 | 19,733 | 19,857 | 16,720 | |||||||||||||||

|

Net Interest Income

|

29,632 | 28,940 | 25,900 | 23,184 | 22,477 | |||||||||||||||

|

Provision for Loan Losses

|

3,896 | 3,026 | 825 | 605 | 210 | |||||||||||||||

|

Net Interest Income after

|

||||||||||||||||||||

|

Provision for Loan Losses

|

25,736 | 25,914 | 25,075 | 22,579 | 22,267 | |||||||||||||||

|

Non-Interest Income

|

15,923 | 15,951 | 16,001 | 14,572 | 13,031 | |||||||||||||||

|

Non-Interest Expense

|

31,229 | 31,372 | 30,740 | 27,464 | 24,364 | |||||||||||||||

|

Income Before Gains (Losses) on

|

||||||||||||||||||||

|

Securities and Income Taxes

|

10,430 | 10,493 | 10,336 | 9,687 | 10,934 | |||||||||||||||

|

Gains (Losses) on Sales of Securities

|

37 | (99 | ) | (2,580 | ) | 164 | 34 | |||||||||||||

|

Income Tax Expense

|

3,366 | 3,258 | 2,047 | 3,170 | 3,651 | |||||||||||||||

|

Net Income

|

$ | 7,101 | $ | 7,136 | $ | 5,709 | $ | 6,681 | $ | 7,317 | ||||||||||

|

SELECTED FINANCIAL RATIOS

|

||||||||||||||||||||

|

Ratio of Equity to Assets

|

9.92 | % | 9.34 | % | 8.84 | % | 9.31 | % | 9.32 | % | ||||||||||

|

Book Value/Common Share

|

$ | 36.19 | $ | 34.09 | $ | 32.12 | $ | 30.42 | $ | 28.68 | ||||||||||

|

Dividends declared per Share

|

$ | 1.42 | $ | 1.41 | $ | 1.37 | $ | 1.26 | $ | 1.10 | ||||||||||

|

Basic Income per Common Share

|

$ | 3.40 | $ | 3.38 | $ | 2.65 | $ | 3.01 | $ | 3.22 | ||||||||||

|

Diluted Income per Common Share

|

$ | 3.37 | $ | 3.36 | $ | 2.63 | $ | 2.94 | $ | 3.15 | ||||||||||

|

Return on Average Assets

|

0.93 | % | 0.91 | % | 0.76 | % | 0.95 | % | 1.07 | % | ||||||||||

|

Return on Average Equity

|

9.43 | % | 9.98 | % | 8.29 | % | 10.24 | % | 11.79 | % | ||||||||||

|

Net Interest Margin

|

4.25 | % | 4.01 | % | 3.71 | % | 3.57 | % | 3.53 | % | ||||||||||

|

Non-Interest Expense/Average Assets

|

4.10 | % | 4.02 | % | 4.07 | % | 3.89 | % | 3.54 | % | ||||||||||

|

Non-Interest Income/Average Assets

|

2.11 | % | 2.08 | % | 2.11 | % | 2.06 | % | 1.89 | % | ||||||||||

|

Non-Performing Loans/Loans (1)

|

2.47 | % | 1.21 | % | 1.09 | % | 0.68 | % | 0.74 | % | ||||||||||

|

Allowance for Loan Losses/Loans (1)

|

1.55 | % | 1.14 | % | 0.94 | % | 0.90 | % | 0.93 | % | ||||||||||

|

Dividend Payout

|

42.14 | % | 41.32 | % | 51.90 | % | 41.66 | % | 33.65 | % | ||||||||||

(1) Total loans before allowance for loan losses

6

Business of the Bank

Teche Federal Bank (the "Bank") attracts savings deposits from the general public and uses such deposits to originate primarily residential mortgage loans, commercial mortgage loans and consumer loans. Additionally, the Bank invests in mortgage-backed and investment securities. (See “Management Strategy” on page 9)

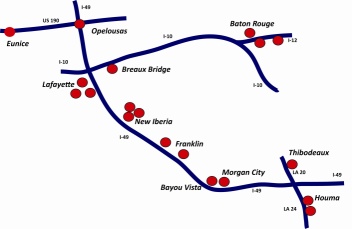

It is the Bank's intention to remain an independent community savings bank serving the local banking needs of its primary market area, which presently includes twenty offices in the Louisiana Parishes of St. Mary, Iberia, Lafayette, St. Landry, St. Martin, Terrebonne, Lafourche, East Baton Rouge and Ascension. The FDIC insures deposits at the Bank up to the maximum legal amount.

Business of the Company

Teche Holding Company (the "Company") is a Louisiana corporation organized in December 1994 at the direction of the Board of Directors of the Bank to acquire all of the capital stock that the Bank issued upon its conversion from the mutual to stock form of organization.

Summary of Quarterly Operating Results

|

2010

|

2009

|

|||||||||||||||||||||||||||||||

|

First

|

Second

|

Third

|

Fourth

|

First

|

Second

|

Third

|

Fourth

|

|||||||||||||||||||||||||

|

(Amounts in thousands, except per share data)

|

||||||||||||||||||||||||||||||||

|

Interest Income

|

$ | 10,500 | $ | 10,374 | $ | 10,299 | $ | 10,163 | $ | 11,214 | $ | 11,013 | $ | 11,130 | $ | 10,880 | ||||||||||||||||

|

Interest Expense

|

3,067 | 2,940 | 2,969 | 2,728 | 4,378 | 3,950 | 3,583 | 3,386 | ||||||||||||||||||||||||

|

Net Interest Income

|

7,433 | 7,434 | 7,330 | 7,435 | 6,836 | 7,063 | 7,547 | 7,494 | ||||||||||||||||||||||||

|

Provision for Loan Losses

|

1,196 | 900 | 900 | 900 | 155 | 1,035 | 550 | 1,286 | ||||||||||||||||||||||||

|

Income before

|

2,574 | 2,502 | 2,713 | 2,678 | 2,602 | 2,482 | 2,395 | 2,915 | ||||||||||||||||||||||||

|

Income Taxes

|

||||||||||||||||||||||||||||||||

|

Net Income

|

1,733 | 1,700 | 1,821 | 1,847 | 1,764 | 1,656 | 1,733 | 1,983 | ||||||||||||||||||||||||

|

Basic Income

|

0.83 | 0.81 | 0.87 | 0.89 | 0.83 | 0.78 | 0.82 | 0.95 | ||||||||||||||||||||||||

|

per Common Share

|

||||||||||||||||||||||||||||||||

|

Diluted Income

|

0.82 | 0.80 | 0.87 | 0.88 | 0.83 | 0.78 | 0.81 | 0.94 | ||||||||||||||||||||||||

|

per Common Share

|

||||||||||||||||||||||||||||||||

7

Market and Dividend Information

Teche Holding Company's common stock trades on the NYSE Amex under the symbol "TSH.” The following sets forth the high and low closing prices and cash dividends declared for the common stock for the last two fiscal years.

|

Quarter ended

|

Closing Price

|

Period End Close

|

Cash Dividend Declared

|

Date Declared

|

|||||||||||||

|

High

|

Low

|

||||||||||||||||

|

December 31, 2008

|

$ | 31.81 | $ | 22.90 | $ | 25.01 | $ | 0.35 |

November 20, 2008

|

||||||||

|

March 31, 2009

|

$ | 30.95 | $ | 22.40 | $ | 30.50 | $ | 0.35 |

February 19, 2009

|

||||||||

|

June 30, 2009

|

$ | 35.50 | $ | 28.85 | $ | 33.10 | $ | 0.35 |

May 29, 2009

|

||||||||

|

September 30, 2009

|

$ | 35.75 | $ | 31.90 | $ | 33.10 | $ | 0.355 |

August 27, 2009

|

||||||||

|

December 30, 2009

|

$ | 33.40 | $ | 30.75 | $ | 31.71 | $ | 0.355 |

November 19, 2009

|

||||||||

|

March 31, 2010

|

$ | 33.40 | $ | 30.80 | $ | 32.90 | $ | 0.355 |

February 17, 2010

|

||||||||

|

June 30, 2010

|

$ | 33.00 | $ | 28.10 | $ | 28.10 | $ | 0.355 |

May 26, 2010

|

||||||||

|

September 30, 2010

|

$ | 31.56 | $ | 26.60 | $ | 31.00 | $ | 0.355 |

August 23, 2010

|

||||||||

According to the records of the Company's transfer agent, there were 429 registered stockholders of record at November 30, 2010. This number does not include any persons or entities that hold their stock in nominee or "street" name through various brokerage firms.

The Company's ability to pay dividends is substantially dependent upon the dividends it receives from the Bank. Under current regulations, the Bank is not permitted to pay dividends if its regulatory capital would thereby be reduced below (1) the amount then required for the liquidation account established in connection with the Bank's conversion from mutual to stock form, or (2) the regulatory capital requirements imposed by the Office of Thrift Supervision ("OTS"). Capital distributions are also subject to certain limitations based on the Bank's net income. See Notes 18 and 19 of Notes to Consolidated Financial Statements. The Bank's total capital at September 30, 2010 exceeded the amounts of its liquidation account and regulatory capital requirements.

8

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

General

The Private Securities Litigation Reform act of 1995 contains safe harbor provisions regarding forward-looking statements. When used in this discussion, the words “believe”, “anticipates”, “contemplates”, “expects”, and similar expressions are intended to identify forward-looking statements. Such statements are subject to certain risks and uncertainties that could cause actual results to differ materially from those projected. Those risks and uncertainties include changes in interest rates, risk associated with the effect of opening new branches, the ability to control costs and expenses, and general economic conditions. The Company undertakes no obligation to publicly release the results of any revisions to those forward-looking statements that may be made to reflect events or circumstances after the date hereof or to reflect the occurrences of unanticipated events.

The Company's consolidated results of operations are primarily dependent on the Bank's net interest income, or the difference between the interest income earned on its loan, mortgage-backed securities and investment securities portfolios, and the interest expense paid on its savings deposits and other borrowings. Net interest income is affected not only by the difference between the yields earned on interest-earning assets and the costs incurred on interest-bearing liabilities, but also by the relative amounts of such interest-earning assets and interest-bearing liabilities.

Other components of net income include: provisions for losses on loans and other assets, non-interest income (primarily, service charges on deposit accounts and other fees), and non-interest expenses (primarily, compensation and employee benefits, office occupancy expense, marketing expense and expenses associated with foreclosed real estate) and income taxes.

Earnings of the Company also are significantly affected by economic and competitive conditions, particularly changes in interest rates, government policies and regulations of regulatory authorities.

References to the "Bank" herein, unless the context requires otherwise, refer to the Company on a consolidated basis.

Overview

The Company’s net income remained relatively stable at $7.1 million for fiscal 2010 and 2009. Net income for fiscal 2009 compared to 2008 was higher due to an increase in net interest income of $3.0 million offset somewhat by an increase in provision for loan losses of $2.2 million. The Company’s assets in fiscal 2010 decreased $3.5 million to $761.5 million primarily due to decreases in both the loan and security portfolios.

Management Strategy

Management's strategy has been to maximize earnings and profitability through steady growth while maintaining asset quality. The Bank's lending strategy has historically focused on the origination of traditional one- to four-family mortgage loans with the primary emphasis on single-family residences in the Bank's primary market area. Additionally, management emphasizes a “SmartGrowth” strategy that focuses on the origination of consumer loans (primarily home equity and mobile home loans), SmartMortgage loans, commercial loans and commercial real estate loans for retention in the Company’s loan portfolio. SmartMortgage loans originated by the Bank are residential real estate loans that do not meet all of the Bank’s standard loan underwriting criteria for residential real estate loans. Consumer loans, commercial loans and commercial real estate loans generally have shorter terms to maturity and higher yields than residential real estate loans. While SmartMortgage loans, consumer loans, commercial loans, and commercial real estate loans have greater credit risk than conforming residential real estate loans, the Company believes its SmartGrowth strategy will have a favorable impact on the Company’s net interest margin, as well as assist in interest rate risk management. SmartGrowth also emphasizes growth in core deposits (primarily transaction accounts), which include demand deposits, NOW accounts, money market deposit accounts and savings accounts.

Asset and Liability Management

Interest Rate Sensitivity Analysis. Net interest income, the primary component of the Bank's net income, is derived from the difference between the interest income on interest-earning assets and the interest expense of interest-bearing liabilities. The Bank has sought to manage its exposure to changes in interest rates by monitoring the effective maturities or re-pricing characteristics of its interest-earning assets and interest-bearing liabilities. The matching of the Bank's assets and liabilities may be analyzed by examining the extent to which its assets and liabilities are interest rate sensitive and by monitoring the expected effects of interest rate changes on its net interest income and net portfolio value.

The ability to maximize net interest income is largely dependent upon achieving a positive interest rate spread that can be sustained during fluctuations in prevailing interest rates. The Bank is exposed to interest rate risk as a result of the difference in the maturity of interest-bearing liabilities and interest-earning assets and the volatility of interest rates. Because most deposit accounts

9

react more quickly to market interest rate movements than do traditional mortgage loans due to their shorter terms to maturity, increases in interest rates may have an adverse effect on the Bank's earnings. Conversely, this same mismatch will generally benefit the Bank's earnings during periods of declining or stable interest rates.

The Bank attempts to manage its interest rate exposure by shortening the maturities of its interest-earning assets by emphasizing adjustable rate mortgages ("ARMs"), periodically selling loans from the portfolio of long term fixed rate mortgages, originating shorter term loans such as residential construction, consumer, home equity and commercial loans and the investment of excess liquidity in purchased loans, adjustable rate mortgage-backed securities and other securities with relatively short terms to maturity. Furthermore, the Bank works to manage the interest rates it pays on deposits while maintaining a stable deposit base and providing quality services to its customers. In recent years, the Bank has used borrowings while continuing to rely primarily upon deposits as its source of funds. At September 30, 2010, the weighted average term to re-pricing of the Bank’s ARM loan and ARM mortgage-backed securities portfolio was approximately 17 months. In contrast, at September 30, 2010, $70.8 million of the Bank's certificate accounts and $400.2 million of the Bank's regular deposit accounts (e.g. demand, NOW, money market, savings), out of $579.4 million of total deposits, were scheduled to mature or re-price within one year or sooner.

Management believes that it has adequate capital to accept a certain degree of interest rate risk. Should interest rates rise management believes the Bank's capital position will enable it to withstand the negative impact on earnings.

Rate/Volume Analysis. The table below sets forth certain information regarding changes in interest income and interest expense of the Bank for the periods indicated. For each category of interest-earning assets and interest-bearing liabilities, information is provided on changes attributable to (i) changes in volume (changes in average volume multiplied by old rate); (ii) changes in rates (changes in rate multiplied by old average volume); and (iii) the net change. The changes attributable to the combined impact of volume and rate have been allocated proportionately to the changes due to volume and the changes due to rate.

| September 30, | September 30, | |||||||||||||||||||||||

| 2010 vs. 2009 | 2009 vs. 2008 | |||||||||||||||||||||||

| Increase (Decrease) Due to | Increase (Decrease) Due to | |||||||||||||||||||||||

| Volume | Rate | Net | Volume | Rate | Net | |||||||||||||||||||

| (Dollars in thousands) | ||||||||||||||||||||||||

| Interest-Earning Assets: | ||||||||||||||||||||||||

|

Securities (1)

|

$ | (522 | ) | $ | (664 | ) | $ | (1,186 | ) | $ | 90 | $ | (115 | ) | $ | (25 | ) | |||||||

|

Loans Receivable, Net

|

(505 | ) | (1,279 | ) | (1,784 | ) | 1,200 | (2,290 | ) | (1,090 | ) | |||||||||||||

|

Other Interest-Earning Assets (2)

|

(39 | ) | 108 | 69 | 304 |

(585)

|

(281 | ) | ||||||||||||||||

|

Total Interest-Earning Assets

|

(1,066 | ) | (1,835 | ) | (2,901 | ) | 1,594 | (2,990 | ) | (1,396 | ) | |||||||||||||

|

Interest-Bearing Liabilities

|

||||||||||||||||||||||||

|

Deposits

|

(293 | ) | (3,070 | ) | (3,363 | ) | 130 | (4,891 | ) | (4,761 | ) | |||||||||||||

|

FHLB Advances

|

(126 | ) | (104 | ) | (230 | ) | 447 | (122 | ) | 325 | ||||||||||||||

|

Total Interest-Bearing Liabilities

|

(419 | ) | (3,174 | ) | (3,593 | ) | 577 | (5,013 | ) | (4,436 | ) | |||||||||||||

| Net Change in Net Interest Income | $ | (647 | ) | $ | 1,339 | $ | 692 | $ | 1,017 | $ | 2,023 | $ | 3,040 | |||||||||||

(1) Includes investment securities and FHLB stock.

(2) Includes certificates of deposit and other interest-bearing accounts.

10

Average Balance Sheet. The following table sets forth certain information relating to the Company's average balance sheet and reflects the average yield on assets and average cost of liabilities for the periods indicated. Such yields and costs are derived by dividing income or expenses by the average balance of assets or liabilities, respectively, for the periods presented. Average balances are derived from daily average balances.

|

Year Ended September 30,

|

||||||||||||||||||||||||||||||||||||

|

2010

|

2009

|

2008

|

||||||||||||||||||||||||||||||||||

|

Average

|

Average

|

Average

|

Average

|

Average

|

Average

|

|||||||||||||||||||||||||||||||

|

Balance

|

Interest

|

Yield/Cost

|

Balance

|

Interest

|

Yield/Cost

|

Balance

|

Interest

|

Yield/Cost

|

||||||||||||||||||||||||||||

|

(Dollars in Thousands)

|

||||||||||||||||||||||||||||||||||||

|

Assets

|

||||||||||||||||||||||||||||||||||||

|

Interest-Earning Assets

|

||||||||||||||||||||||||||||||||||||

|

Securities (1)

|

$ | 74,519 | $ | 2,662 | 3.57 | % | $ | 86,215 | $ | 3,848 | 4.46 | % | $ | 84,249 | $ | 3,872 | 4.60 | % | ||||||||||||||||||

|

Loans Receivable (2) (3)

|

599,134 | 38,406 | 6.41 | % | 606,751 | 40,190 | 6.62 | % | 589,614 | 41,280 | 7.00 | % | ||||||||||||||||||||||||

|

Other Interest-Earning Assets (4)

|

23,662 | 268 | 1.13 | % | 29,443 | 199 | 0.67 | % | 18,043 | 481 | 2.67 | % | ||||||||||||||||||||||||

|

Total Interest-Earning Assets

|

697,315 | $ | 41,336 | 5.93 | % | 722,409 | $ | 44,237 | 6.12 | % | 691,906 | $ | 45,633 | 6.60 | % | |||||||||||||||||||||

|

Non-Interest Earning Assets

|

65,040 | 58,778 | 57,919 | |||||||||||||||||||||||||||||||||

|

Total Assets

|

$ | 762,355 | $ | 781,187 | $ | 749,825 | ||||||||||||||||||||||||||||||

|

Liabilities and Stockholders’ Equity

|

||||||||||||||||||||||||||||||||||||

|

Interest-Bearing Liabilities

|

||||||||||||||||||||||||||||||||||||

|

NOW Accounts

|

$ | 104,176 | $ | 427 | 0.41 | % | $ | 100,817 | $ | 538 | 0.53 | % | $ | 83,515 | $ | 456 | 0.55 | % | ||||||||||||||||||

|

Statement & Regular Savings Accounts

|

143,408 | 1,301 | 0.91 | % | 76,214 | 664 | 0.87 | % | 52,851 | 409 | 0.77 | % | ||||||||||||||||||||||||

|

Money Funds Accounts

|

71,958 | 282 | 0.39 | % | 115,721 | 1,440 | 1.24 | % | 125,905 | 3,190 | 2.53 | % | ||||||||||||||||||||||||

|

Certificates of Deposit

|

192,591 | 5,151 | 2.67 | % | 240,270 | 7,882 | 3.28 | % | 264,185 | 11,230 | 4.25 | % | ||||||||||||||||||||||||

|

Total Deposits

|

512,133 | 7,161 | 1.40 | % | 533,022 | 10,524 | 1.97 | % | 526,456 | 15,285 | 2.90 | % | ||||||||||||||||||||||||

|

FHLB Advances

|

102,254 | 4,543 | 4.44 | % | 105,060 | 4,773 | 4.54 | % | 95,225 | 4,448 | 4.67 | % | ||||||||||||||||||||||||

|

Total Interest-Bearing Liabilities

|

614,387 | $ | 11,704 | 1.90 | % | 638,082 | $ | 15,297 | 2.40 | % | 621,681 | $ | 19,733 | 3.17 | % | |||||||||||||||||||||

|

Non-Interest-Bearing Liabilities

|

72,689 | 71,626 | 59,311 | |||||||||||||||||||||||||||||||||

|

Total Liabilities

|

687,076 | 709,708 | 680,992 | |||||||||||||||||||||||||||||||||

|

Stockholders’ Equity

|

75,279 | 71,479 | 68,833 | |||||||||||||||||||||||||||||||||

|

Total Liabilities and Stockholders’ Equity

|

$ | 762,355 | $ | 781,187 | $ | 749,825 | ||||||||||||||||||||||||||||||

|

Net Interest Income/Interest Rate Spread (5)

|

$ | 29,632 | 4.02 | % | $ | 28,940 | 3.72 | % | $ | 25,900 | 3.42 | % | ||||||||||||||||||||||||

|

Net Interest Margin (6)

|

4.25 | % | 4.01 | % | 3.74 | % | ||||||||||||||||||||||||||||||

|

Interest-Earning Assets/

|

||||||||||||||||||||||||||||||||||||

|

Interest-Bearing Liabilities

|

113.50 | % | 113.22 | % | 112.15 | % | ||||||||||||||||||||||||||||||

(1) Includes securities and Federal Home Loan Bank (“FHLB”) stock.

(2) Amount is net of deferred loan fees, loan discounts and premiums and loans-in-process and includes non-accruing loans.

(3) Interest income includes loan fees of approximately $555,000 in 2010, $585,000 in 2009 and $565,000 in 2008.

(4) Amount includes certificates of deposit and other interest-bearing deposits.

(5) Interest rate spread represents the difference between the yield on average interest-earning assets and the cost of average interest-bearing liabilities.

(6) Net interest margin represents net interest income divided by average interest-earning assets

11

Changes in Financial Condition from September 30, 2009 to September 30, 2010

General. Total assets decreased $3.6 million, or 0.5% to $761.5 million at September 30, 2010 from $765.1 million at September 30, 2009, due to reductions in securities and loan portfolios offset somewhat by increases in cash and interest bearing deposits.

Cash and Cash Equivalents. Cash increased $17.0 million from $23.7 million at September 30, 2009 to $40.7 million at September 30, 2010. The increase resulted primarily from loan repayments along with principal payments on securities.

Securities Available-for-Sale and Held to Maturity. Securities available-for-sale decreased $5.9 million from $20.9 million at September 30, 2009 to $15.0 million at September 30, 2010 due primarily to repayments on existing mortgage backed securities. Securities held-to-maturity decreased $15.8 million from $75.4 million to $59.6 million due primarily to repayments on existing mortgage backed securities along with maturities of government sponsored agency securities, offset somewhat by purchases of time deposits at other banks. (See Note 3 of the Consolidated Financial Statements.)

Loans Receivable, Net. The Bank’s net loans receivable decreased $1.9 million or 0.3% to $586.6 million from $588.5 million at September 30, 2009 due primarily to decreases in home equity loans and loans on savings accounts offset by growth in one-to-four family mortgage loans, mobile home loans, and travel trailer loans. (See Note 4 of the Consolidated Financial Statements for a comparative breakdown of the Bank’s loan portfolio.)

Premises and Equipment, Net. Premises and equipment decreased $0.5 million or 1.7% due to depreciation offset by equipment purchases.

Deposits. The Bank’s deposits decreased $6.1 million or 1.0% to $579.4 million at September 30, 2010, from $585.5 million at September 30, 2009. SmartGrowth deposits which consist of non-interest bearing checking, interest-bearing checking, savings accounts, and money market accounts increased $32.4 million during the fiscal year. Time deposits decreased $38.5 million from $217.7 million to $179.2 million. (See Note 7 of the Consolidated Financial Statements for a comparative breakdown of the Bank’s deposit portfolio.)

Advances from FHLB. Advances from the Federal Home Loan Bank of Dallas decreased $0.6 million, or 0.6% to $100.0 million from $100.6 million at September 30, 2009. The decrease was due to repayments on existing advances along with advance maturities offset by advance purchases.

Stockholders’ Equity. Stockholders’ equity increased $4.0 million, or 5.6% from $71.5 million at September 30, 2009, to $75.5 million at September 30, 2010. The increase was due primarily to net income less dividends and the purchase of treasury stock.

Comparison of Operating Results for Years Ended September 30, 2010, 2009 and 2008

Analysis of Net Income

General. The Company had net income of $7.1million, $7.1 million and $5.7 million for the years ended 2010, 2009 and 2008. Fiscal 2010 net income remained relatively the same as fiscal 2009. The $1.4 million increase during fiscal 2009 was primarily due to $3.0 million increase in net interest income, offset by an increase in the provision for loan losses of $2.2 million.

Operating Revenue. Operating revenue for the fiscal year ended September 30, 2010, consisting of net interest income (before provision for loan losses and gain (loss) on securities and sale of loans) plus non-interest income, amounted to $45.7 million, $45.3 million and $42.4 million for the years ended 2010, 2009 and 2008, respectively. The $0.4 million increase during fiscal 2010 was primarily due to a reduction in total interest expense of $3.6 million offset by a decrease of $2.9 million in interest income. The $3.5 million increase during fiscal 2009 was primarily due to a reduction in total interest expense of $4.4 million offset somewhat by a decrease in interest income on loans of $1.1 million.

Interest Income. Interest income amounted to $41.3 million, $44.2 million and $45.6 million for the years ended 2010, 2009 and 2008, respectively. The $2.9 million decrease during fiscal 2010 was primarily due to a decrease in interest rates along with a decrease in average balances on earning assets. The $1.4 million decrease during fiscal 2009 was primarily due to a decrease in interest rates offset by an increase in the average balance on earning assets.

The average balance of loans decreased during fiscal 2010 by $7.6 million, or 1.3% while increasing in fiscal 2009 by $17.1 million, or 2.9%.

Interest Expense. Interest expense totaled $11.7 million, $15.3 million and $19.7 million for the years ended September 30, 2010, 2009 and 2008. The $3.6 million decrease from fiscal 2009 to fiscal 2010 was primarily due to lower interest rates on deposits. The $4.4 million decrease from fiscal 2008 to fiscal 2009 was primarily due to lower interest rates offset by a modest increase in both deposit and FHLB advance average balances.

12

Net Interest Income. Net interest income increased $0.7 million to $29.6 million during the year ended September 30, 2010 primarily due to lower rates on interest bearing liabilities offset somewhat by lower rates on interest bearing assets. Net interest income increased $3.1 million to $28.9 million during the year ended September 30, 2009 primarily due to a decrease in interest expense on deposits and FHLB advances, offset by a decrease in interest income on loans.

Provision for Loan Losses. The Bank provided $3.9 million, $3.0 million and $825,000 to the allowance for loan losses for the years ended September 30, 2010, 2009 and 2008 respectively. The provision increased in fiscal 2010 and 2009 due to an increase in historical charge-off rates and qualitative adjustments necessary to address negative economic and credit quality trends. The provision increased in fiscal 2008 primarily due to growth in the loan portfolio as well as changes to the qualitative and quantitative factors considered during the analysis of the allowance for loan losses.

Management periodically estimates the likely level of losses to determine whether the allowance for loan losses is adequate to absorb probable losses inherent in the existing portfolio. Based on these estimates, an amount is charged or credited to the provision for loan losses and credited or charged to the allowance for loan losses in order to adjust the allowance to a level determined to adequately absorb probable inherent losses.

While the Bank maintains its allowance for losses at a level that it considers to be adequate to provide for existing losses, there can be no assurance that further additions will not be made to the loss allowances and that such losses will not exceed the estimated amounts. (See Note 1 to the Consolidated Financial Statements.)

Non-Interest Income. Non-interest income during the years ended September 30, 2010, 2009 and 2008 amounted to $16.0 million, $15.9 million and $13.4 million respectively. Non-interest income in fiscal 2010 increased slightly from fiscal 2009 due to reductions in impairment charges on certain securities offset somewhat by decreases in gains on the sale of loans. Non-interest income in fiscal 2008 and 2009 included charges for certain investment securities in the investment portfolio in the amount of $3.0 million and $1.0 million respectively. Non-interest income in fiscal 2009 included a gain of $559,000 on the sale of $26 million of conforming loans. (See Loans Receivable, Net) Excluding these charges, non-interest income remained relatively stable between fiscal 2008 and 2009.

Non-Interest Expense. Non-interest expense totaled $31.2 million, $31.4 million and $30.7 million during the years ended September 30, 2010, 2009 and 2008, respectively. Non-interest expenses remained relatively stable in fiscal 2010 compared to fiscal 2009. The $0.7 million increase during fiscal 2009 was primarily due to an increase in deposit insurance premiums.

The Bank is subject to the Louisiana Shares Tax, which amounted to an expense of $513,000, $567,000 and $666,000 in the fiscal years ended September 30, 2010, 2009 and 2008, respectively.

Gain (loss) on Sale of Securities. In the years ended September 30, 2010, 2009 and 2008, gain (losses) on the sale of securities amounted to $37,000, ($99,000) and ($2,580,000), respectively. The $37,000 gain recorded in 2010 resulted from the sale of some equity securities. The loss recorded in 2009 resulted from the Company’s recording an impairment loss on an equity security for $175,000, offset by a gain on sale of equity securities of $76,000. The loss recorded in 2008 resulted from the Company’s withdrawal of a $16.1 million investment in a mortgage mutual fund that had continued to decline in value during the year as a result of the turmoil that existed in the mortgage markets in general. (See Note 3 of the Consolidated Financial Statements.)

Income Tax Expense. For the years ended September 30, 2010, 2009 and 2008, the Company incurred income tax expense of $3.4 million, $3.3 million and $2.0 million, respectively. There was a slight increase in the effective tax rate in 2010 due to a decrease in the benefits of tax credits as compared to 2009. There was an increase in the effective tax rate in 2009 due to higher pre-tax income and the benefit of tax credits were lower than in 2008. (See Note 10 of the Consolidated Financial Statements for further explanation.)

Liquidity and Capital Resources

The Bank's average liquidity ratio is based on deposits and was approximately 16.0% percent during September 2010. The liquidity ratio is calculated by dividing cash and cash equivalents plus securities less securities pledged by total assets. The Bank manages its average liquidity ratio to meet its funding needs, including: deposit outflows; disbursement of payments collected from borrowers for taxes and insurance; repayment of Federal Home Loan Bank advances and other borrowings; and loan principal disbursements. The Bank also monitors its liquidity position in accordance with its asset/liability management objectives.

In addition to funds provided from operations, the Bank's primary sources of funds are: savings deposits, principal repayments on loans and mortgage-backed securities, and matured or called investment securities. The Bank also borrows funds from the Federal Home Loan Bank of Dallas (the “FHLB”).

Scheduled loan repayments and maturing investment securities are a relatively predictable source of funds. However, savings deposit flows and prepayments on loans and mortgage-backed securities are significantly influenced by changes in market interest rates, economic conditions and competition. The Bank strives to manage the pricing of its deposits to maintain a balanced stream of cash flows commensurate with its loan commitments and other predictable funding needs.

13

The Bank usually maintains a portion of its cash on hand in interest-bearing demand deposits with the FHLB and other correspondent banks to meet immediate loan commitment and savings withdrawal funding requirements. When applicable, cash in excess of immediate funding needs is invested into longer-term investment and mortgage-backed securities, some of which may also qualify as liquid investments under current OTS regulations.

Funds available under existing credit facilities from the FHLB totaled $167.1 million. The Bank has total FHLB borrowings of $100.0 million, or 13.1% of the Bank’s assets. Approximately $21.6 million is due in the year ending September 30, 2011.

Management believes the Bank has sufficient resources available to meet its foreseeable funding requirements. At September 30, 2010, the Bank had outstanding loan commitments of $48.8 million, and certificates of deposit scheduled to mature within one year of $70.8 million, much of which management expects, based on past experience, will remain with the Bank upon maturity.

Regulations of the OTS require the Bank to meet or exceed three separate standards of capital adequacy. These regulations require financial institutions to have minimum tangible capital equal to 1.5% of total adjusted assets; minimum core capital equal to 4.0% of total adjusted assets; and risk-based capital equal to 8.0% of total risk-weighted assets. At September 30, 2010, the Bank exceeded all regulatory capital requirements. (See Note 18 to the Consolidated Financial Statements.)

Net Portfolio Value Analysis - Interest Rate Risk

The Bank is subject to interest rate risk to the degree that its interest-bearing liabilities, primarily deposits with short- and medium-term maturities, mature or re-price at different rates than our interest-earning assets. Although having liabilities that mature or re-price less frequently on average than assets will be beneficial in times of rising interest rates, such an asset/liability structure will result in lower net income during periods of declining interest rates, unless offset by other factors.

The Bank believes it is critical to manage the relationship between interest rates and the effect on its net portfolio value (“NPV”). This approach calculates the difference between the present value of expected cash flows from assets and the present value of expected cash flows from liabilities, as well as cash flows from off-balance sheet contracts. The Bank manages assets and liabilities within the context of the marketplace, regulatory limitations and within its limits on the amount of change in NPV which is acceptable given certain interest rate changes.

The OTS requires all regulated thrift institutions to calculate the estimated change in the institution’s NPV assuming instantaneous parallel shifts in the Treasury yield curve of 100 to 300 basis points either up or down in 100 basis point increments. The NPV is defined as the present value of expected cash flows from existing assets less the present value of expected cash flows from existing liabilities plus the present value of net expected cash inflows from existing off-balance sheet contracts.

The OTS provides an interest rate sensitivity report of NPV to all institutions that file with the OTS a Consolidated Maturity & Rate Schedule (“CMR”) as a part of the institution’s quarterly Thrift Financial Report. The OTS simulation model uses a discounted cash flow analysis and an option-based pricing approach to measuring the interest rate sensitivity of NPV. The OTS model estimates the economic value of each type of asset, liability, and off-balance sheet contract under the assumption that the Treasury yield curve shifts instantaneous and parallel up and down 100 to 300 basis points in 100 basis point increments. The OTS allows thrifts with under $1 billion in total assets to use the results of their interest rate sensitivity model, which is based on information provided by the institution, to estimate the sensitivity of NPV.

The OTS model utilizes an option-based pricing approach to estimate the sensitivity of mortgage loans. The most significant embedded option in these types of assets is the prepayment option of the borrowers. The OTS model uses various price indications and prepayment assumptions to estimate sensitivity of mortgage loans.

In the OTS model, the value of deposit accounts appears on the asset and liability side of the NPV analysis. In estimating the value of certificates of deposit accounts (“CD”), the liability portion of the CD is represented by the implied value when comparing the difference between the CD face rate and available wholesale CD rates. On the asset side of the NPV calculation, the value of the “customer relationship” due to the rollover of retail CD deposits represents an intangible asset in the NPV calculation.

Other deposit accounts such as NOW accounts, money market demand accounts, passbook accounts, and non-interest-bearing accounts also are included on the asset and liability side of the NPV calculation in the OTS model. These accounts are valued at 100% of the respective account balances on the liability side. On the asset side of the analysis, the value of the “customer relationship” of the various types of deposit accounts is reflected as a deposit intangible.

The NPV sensitivity of borrowed funds is estimated by the OTS model based on a discounted cash flow approach.

The OTS uses, as a critical point, a change of plus or minus 200 basis points in order to set its “normal” institutional results and peer comparisons. A resulting change in NPV of more than 2% of the estimated market value of its assets will require the institution to deduct from its capital 50% of that excess change. The rules provide that the OTS will calculate the IRR component quarterly for each institution. The

14

greater the change, positive or negative, in NPV, the more interest rate risk is assumed to exist with the institution. The following table lists the Bank’s latest percentage change in NPV assuming an immediate change of plus or minus 100, 200, and 300 basis points from the level of interest rates at September 30, 2010.

| Net Portfolio Value | NPV as % of PV of Assets | |||||||||||||||||||||

|

Change

In Rates

|

$ Amount | $ Change (2) | % of Change (3) |

NPV

Ratio

|

Change (5) | |||||||||||||||||

| +300 | bp | $ | 101,723 | $ | 5,969 | +6% | 12.87 | % | +101 | bp | ||||||||||||

| +200 | bp | 103,190 | 7,437 | +8% | 12.92 | % | +106 | bp | ||||||||||||||

| +100 | bp | 101,744 | 5,990 | +6% | 12.64 | % | +78 | bp | ||||||||||||||

| +50 | bp | 99,148 | 3,395 | +4% | 12.29 | % | +43 | bp | ||||||||||||||

| 0 | bp | 95,754 | 11.86 | % | ||||||||||||||||||

| -50 | bp | 92,525 | -3,229 | -3% | 11.45 | % | -41 | bp | ||||||||||||||

| -100 | bp | 90,124 | -5,630 | -6% | 11.13 | % | -73 | bp | ||||||||||||||

|

(1)

|

The -200bp and -300bp scenarios are not shown due to low interest rate environment.

|

|

(2)

|

Represents the excess (deficiency) of the estimated NPV assuming the indicated change in interest rates minus the estimated NPV assuming no change in interest rates.

|

|

(3)

|

Calculated as the amount of change in the estimated NPV divided by the estimated NPV assuming no change in interest rates.

|

|

(4)

|

Calculated as the estimated NPV divided by average total assets.

|

|

(5)

|

Calculated as the excess (deficiency) of the NPV ratio assuming the indicated change in interest rates over the estimated NPV ratio assuming no change in interest rates.

|

|

September 30,

2010

|

September 30,

2009

|

||||

|

*** RISK MEASURES: +200 BP RATE SHOCK ***

|

|||||

|

Pre-Shock NPV Ratio: NPV as % of PV of Assets

|

11.86

|

%

|

12.02

|

%

|

|

|

Exposure Measure: Post-Shock NPV Ratio

|

12.92

|

%

|

12.35

|

%

|

|

|

Sensitivity Measure: Increase in NPV Ratio

|

106

|

bp

|

33

|

bp

|

|

|

*** CALCULATION OF CAPITAL COMPONENT ***

|

|||||

|

Change in NPV as % of PV of Assets

|

0.50

|

%

|

0.11

|

%

|

As the table shows, increases in interest rates would result in net increases in the Bank’s NPV. The Bank’s NPV increases by 7.8% if interest rates increase by 200 basis points. Certain shortcomings are inherent in the methodology used in the above table. Modeling changes in NPV requires the making of certain assumptions that may tend to oversimplify the manner in which actual yields and costs respond to changes in market interest rates. First, the models assume that the composition of the Bank’s interest sensitive assets and liabilities existing at the beginning of a period remains constant over the period being measured. Second, the models assume that a particular change in interest rates is reflected uniformly across the yield curve regardless of the duration to maturity or re-pricing of specific assets and liabilities. Accordingly, although the NPV measurements do provide an indication of the Bank’s interest rate risk exposure at a particular point in time, such measurements are not intended to provide a precise forecast of the effect of changes in market interest rates on the Bank’s net interest income.

In times of increasing interest rates, the value of fixed-rate assets could decrease in value and the lag in re-pricing of interest rate sensitive assets could be expected to have a negative effect on the Bank.

Contractual Obligations

The Company has various contractual obligations related to borrowings, deposits and operating lease payments. These obligations are outlined in Notes 6, 7 and 8 in the Consolidated Financial Statements of the Company.

Critical Accounting Policies

Certain critical accounting policies affect the more significant judgments and estimates used in the preparation of the consolidated financial statements. The Company’s most critical accounting policies are as follows:

Allowance for Loan Losses - The allowance for loan losses is a valuation allowance available for losses incurred on loans. Any losses are charged to the allowance for loan losses when the loss actually occurs or when a determination is made that a loss is probable to occur. Recoveries are credited to the allowance at the time of recovery.

15

Management estimates the likely level of losses to determine whether the allowance for loan losses is adequate to absorb losses inherent in the existing portfolio. Based on the estimates, an amount is charged to or recovered from the provision for loan losses and credited or debited to the allowance for loan losses in order to adjust the allowance to a level determined to be adequate to absorb such losses.

Management’s judgment as to the level of losses on existing loans involves the consideration of current and anticipated economic conditions and their potential effects on specific borrowers; an evaluation of the existing relationships among loans, known and inherent risks in the loan portfolio, and the present level of the allowance; results of examination of the loan portfolio by regulatory agencies; and management’s internal review of the loan portfolio. In determining the collectability of certain loans, management also considers the fair value of any underlying collateral.

It should be understood that estimates of loan losses involve an exercise of judgment. During the fiscal year ending September 30, 2009, the company made changes to the allowance model. These changes included using a three year rolling average charge-off history instead of five years, switching to actual charge-off history instead of a blend with peer rates and increased the qualitative factors due to an overall negative economic environment and credit quality trends in the banks portfolio. While it is possible that in particular periods the Company may sustain losses, which are substantial relative to the allowance for loan losses, it is the judgment of management that the allowance for loan losses reflected in the consolidated balance sheets is adequate to absorb probable losses inherent in the existing loan portfolio.

Goodwill – Goodwill does not require amortization but is subject to at least an annual assessment for impairment unless interim events or circumstances make it more likely than not that an impairment loss has occurred. Impairment is defined at that amount by which the implied fair value of the goodwill is less than the goodwill’s carrying value. Impairment losses would be charged to operating expense. Goodwill is not deductible for income tax purposes. The Company’s market value based upon the last trade on the last working day of the fiscal quarter was $31.00 or $3.46 below tangible book value. The turmoil in the financial markets and stock markets in general continues to have a negative impact on the Company’s stock price which does not reflect the fundamental performance of the Company. For the quarter ended September 30, 2010, the Company recorded record earnings of $1.8 million. Management reviews various bank peer data to aid in management’s analysis of goodwill for possible impairment. Management’s judgment is that goodwill is not impaired and no adjustment is necessary.

Impact of Off-Balance Sheet Instruments

The Company has certain off-balance-sheet instruments in the form of contractual commitments to extend credit to customers. These legally binding commitments have set expiration dates and are at predetermined interest rates. The underwriting criteria for these commitments are the same as for loans in our loan portfolio. Collateral is also obtained, if necessary, based on the credit evaluation of each borrower. Although many of the commitments will expire unused, management believes that we have the necessary resources to fund these commitments. (See Note 16 in the accompanying Consolidated Financial Statements.)

16

MANAGEMENT’S REPORT ON INTERNAL CONTROL

OVER FINANCIAL REPORTING

Management is responsible for establishing and maintaining adequate internal control over financial reporting, as such term is defined in Exchange Act Rule 13a- 15(f). The Company’s internal control over financial reporting includes those policies and procedures that (i) pertain to the maintenance of records that, in reasonable detail, accurately and fairly reflect the transactions and dispositions of the assets of the Company; (ii) provide reasonable assurance that transactions are recorded as necessary to permit preparation of financial statements in accordance with generally accepted accounting principles, and that receipts and expenditures of the Company are being made only in accordance with authorization of management and directors of the Company; and (iii) provide reasonable assurance regarding prevention or timely detection of unauthorized acquisition, use, or disposition of the Company’s assets that could have a material effect on the financial statements.

Internal control over financial reporting is designed to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements prepared for external purposes in accordance with generally accepted accounting principles. Because of inherent limitations, internal control over financial reporting may not prevent or detect misstatements. Also, projections of any evaluation of effectiveness to future periods are subject to the risk that controls may become inadequate because of changes in conditions, or that the degree of compliance with the policies and procedures may deteriorate.

Under supervision and with the participation of management, including our principal executive officer and principal financial officer, we conducted an evaluation of the effectiveness of our internal control over financial reporting based on the framework in Internal Control- Integrated Framework issued by the Committee of Sponsoring Organizations of the Treadway Commission. Based on our evaluation under the framework in Internal Control- Integrated Framework, management concluded that our internal control over financial reporting was effective as of September 30, 2010.

This annual report does not include an attestation report of the Company’s registered public accounting firm regarding internal control over financial reporting. Management’s report was not subject to attestation by the Company’s registered public accounting firm pursuant to rules of the Securities and Exchange Commission that permit the Company to provide only management’s report in this annual report.

|

|

|

|

Patrick Little

President and Chief Executive Officer

|

J. L. Chauvin

Senior Vice President and Chief Financial Officer

|

17

Report of Independent Registered Public Accounting Firm

To the Board of Directors and Stockholders

Teche Holding Company

Franklin, Louisiana

We have audited the accompanying consolidated balance sheets of Teche Holding Company and subsidiary (hereinafter referred to as the “Company”) as of September 30, 2010 and 2009, and the related consolidated statements of income, stockholders’ equity and cash flows for each of the years in the three-year period ended September 30, 2010. These consolidated financial statements are the responsibility of the Company’s management. Our responsibility is to express an opinion on these consolidated financial statements based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. We were not engaged to perform an audit of the Company’s internal control over financial reporting. Our audit included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Company’s internal control over financial reporting. Accordingly, we express no such opinion. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the consolidated financial statements referred to above present fairly, in all material respects, the financial position of Teche Holding Company and subsidiary as of September 30, 2010 and 2009, and the results of their operations and their cash flows for each of the years in the three-year period ended September 30, 2010, in conformity with accounting principles generally accepted in the United States of America.

Atlanta, Georgia

December 17, 2010

18

TECHE HOLDING COMPANY AND SUBSIDIARY

CONSOLIDATED BALANCE SHEETS

September 30, 2010 and 2009

|

2010

|

2009

|

|||||||

|

ASSETS

|

(Amounts in thousands,

|

|||||||

|

Except share and per share data)

|

||||||||

|

Cash and due from banks

|

$ | 15,420 | $ | 13,958 | ||||

|

Interest-bearing deposits

|

25,235 | 9,717 | ||||||

|

Securities available-for-sale - at estimated fair value

|

||||||||

|

(amortized cost of $ 14,307 in 2010 and $20,277 in 2009)

|

14,996 | 20,936 | ||||||

|

Securities held-to-maturity—at amortized cost (estimated fair

|

||||||||

|

value of $61,711 in 2010 and $76,887 in 2009)

|

59,566 | 75,384 | ||||||

|

Loans receivable—net of allowance for loan losses of

|

||||||||

|

$9,256 in 2010 and $6,806 in 2009

|

586,635 | 588,527 | ||||||

|

Accrued interest receivable

|

2,480 | 2,622 | ||||||

|

Investment in Federal Home Loan Bank stock, at cost

|

5,402 | 5,063 | ||||||

|

Real estate owned, net

|

1,181 | 1,953 | ||||||

|

Prepaid expenses and other assets

|

6,898 | 3,321 | ||||||

|

Goodwill

|

3,647 | 3,647 | ||||||

|

Life insurance contracts

|

13,310 | 12,724 | ||||||

|

Premises and equipment, net

|

26,754 | 27,219 | ||||||

|

TOTAL ASSETS

|

$ | 761,524 | $ | 765,071 | ||||

|

LIABILITIES AND STOCKHOLDERS’ EQUITY

|

||||||||

|

Deposits

|

579,355 | $ | 585,469 | |||||

|

Advances from Federal Home Loan Bank

|

100,017 | 100,628 | ||||||

|

Advance payments by borrowers for taxes and insurance

|

2,463 | 2,433 | ||||||

|

Accrued interest payable

|

429 | 743 | ||||||

|

Accounts payable and other liabilities

|

3,747 | 4,313 | ||||||

|

TOTAL LIABILITIES

|

686,011 | 693,586 | ||||||

|

COMMITMENTS AND CONTINGENCIES

|

||||||||

|

STOCKHOLDERS’ EQUITY:

|

||||||||

|

Preferred stock, 5,000,000 shares authorized, none issued

|

— | — | ||||||

|

Common stock, $.01 par value, 10,000,000 shares authorized;

|

||||||||

|

4,672,567 and 4,666,950 shares issued

|

47 | 47 | ||||||

|

Additional paid-in capital

|

52,685 | 52,285 | ||||||

|

Retained earnings

|

73,942 | 69,786 | ||||||

|

Unearned compensation

|

(326 | ) | (586 | ) | ||||

|

Treasury stock 2,591,081 and 2,570,296 shares - at cost

|

(50,862 | ) | (50,234 | ) | ||||

|

Accumulated other comprehensive loss on held-to-maturity

|

||||||||

|

securities

|

(428 | ) | (247 | ) | ||||

|

Accumulated other comprehensive income on available for sale

|

||||||||

|

Securities

|

455 | 434 | ||||||

|

TOTAL STOCKHOLDERS’ EQUITY

|

75,513 | 71,485 | ||||||

|

TOTAL LIABILITIES AND STOCKHOLDERS’ EQUITY

|

$ | 761,524 | $ | 765,071 | ||||

See notes to consolidated financial statements

19

TECHE HOLDING COMPANY AND SUBSIDIARY

CONSOLIDATED STATEMENTS OF INCOME

Years Ended September 30, 2010, 2009 and 2008

|

2010

|

2009

|

2008

|

||||||||||

|

(Amounts in thousands, except per share amounts)

|

||||||||||||

|

INTEREST INCOME:

|

||||||||||||

|

Interest and fees on loans

|

$ | 38,406 | $ | 40,190 | $ | 41,280 | ||||||

|

Interest and dividends on securities

|

2,662 | 3,848 | 3,873 | |||||||||

|

Other interest income

|

268 | 199 | 480 | |||||||||

|

TOTAL INTEREST INCOME

|

41,336 | 44,237 | 45,633 | |||||||||

|

INTEREST EXPENSE:

|

||||||||||||

|

Deposits

|

7,161 | 10,524 | 15,285 | |||||||||

|

Advances from Federal Home Loan Bank

|

4,543 | 4,773 | 4,448 | |||||||||

|

TOTAL INTEREST EXPENSE

|

11,704 | 15,297 | 19,733 | |||||||||

|

NET INTEREST INCOME

|

29,632 | 28,940 | 25,900 | |||||||||

|

PROVISION FOR LOAN LOSSES

|

3,896 | 3,026 | 825 | |||||||||

|

NET INTEREST INCOME AFTER

|

||||||||||||

|

PROVISION FOR LOAN LOSSES

|

25,736 | 25,914 | 25,075 | |||||||||

|

NON-INTEREST INCOME:

|

||||||||||||

|

Total other-than temporary impairment losses

|

(451 | ) | (1,311 | ) | (408 | ) | ||||||

|

Portion of impairment losses recognized in other

|

||||||||||||

|

comprehensive loss

|

274 | 375 | -- | |||||||||

|

Net impairment losses recognized in earnings

|

(177 | ) | (936 | ) | (408 | ) | ||||||

|

Service charges and other

|

15,227 | 15,415 | 15,482 | |||||||||

|

Gain on sale of premises and equipment

|

— | 10 | 1 | |||||||||

|

Gain (Loss) on sale and impairments of equity securities

|

37 | (99 | ) | (2,580 | ) | |||||||

|

Gain (Loss) on sale of loans

|

13 | 559 | (172 | ) | ||||||||

|

Other income

|

860 | 903 | 1,098 | |||||||||

|

TOTAL NON-INTEREST INCOME

|

15,960 | 15,852 | 13,421 | |||||||||

|

NON-INTEREST EXPENSE:

|

||||||||||||

|

Compensation and employee benefits

|

16,414 | 16,418 | 16,746 | |||||||||

|

Occupancy, equipment and data processing expense

|

6,329 | 6,244 | 6,084 | |||||||||

|

Marketing and professional fees

|

2,558 | 2,743 | 2,986 | |||||||||

|

Deposit insurance premiums

|

1,081 | 1,082 | 74 | |||||||||

|

Louisiana shares tax

|

513 | 567 | 666 | |||||||||

|

Other operating expenses

|

4,334 | 4,318 | 4,184 | |||||||||

|

TOTAL NON-INTEREST EXPENSE

|

31,229 | 31,372 | 30,740 | |||||||||

|

INCOME BEFORE INCOME TAXES

|

10,467 | 10,394 | 7,756 | |||||||||

|

INCOME TAXES

|

3,366 | 3,258 | 2,047 | |||||||||

|

NET INCOME

|

$ | 7,101 | $ | 7,136 | $ | 5,709 | ||||||

|

BASIC INCOME PER COMMON SHARE

|

$ | 3.40 | $ | 3.38 | $ | 2.65 | ||||||

|

DILUTED INCOME PER COMMON SHARE

|

$ | 3.37 | $ | 3.36 | $ | 2.63 | ||||||

|

DIVIDENDS PER SHARE

|

$ | 1.42 | $ | 1.41 | $ | 1.37 | ||||||