Attached files

| file | filename |

|---|---|

| EX-24.1 - Titan Oil & Gas, Inc. | form10k83110ex32.htm |

| EX-31.1 - Titan Oil & Gas, Inc. | form10k83110ex31.htm |

U.S. SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934

For the fiscal year ended August 31, 2010

Commission file number: 333-153762

TITAN OIL & GAS, INC.

(Exact name of registrant as specified in its charter)

|

Nevada

|

26-2780766

|

|

|

(State of incorporation)

|

(I.R.S. Employer Identification No.)

|

7251 West Lake Mead Boulevard, Suite 300

Las Vegas, Nevada 89128

(Address of principal executive offices)

(702) 562-4315

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Exchange Act:

None

Securities registered pursuant to Section 12(g) of the Exchange Act:

Common Stock, $0.001 par value

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated filer ¨

|

Accelerated filer ¨

|

|

Non-accelerated filer ¨ (Do not check if a smaller reporting company)

|

Smaller Reporting Company x

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The issuer’s revenues for its most recent fiscal year were $Nil

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the average bid and asked price of such common equity as February 28, 2010 was approximately $488,000.

The number of shares of the issuer’s common stock issued and outstanding as of December 8, 2010 was 53,760,000 shares.

Documents Incorporated By Reference: None

i

TABLE OF CONTENTS

| Page | |||

|

Oil and Gas Glossary

|

iii | ||

|

PART I

|

|||

|

Item 1

|

Business

|

1 | |

|

Item 1A

|

Risk Factors

|

6 | |

|

Item 1B

|

Unresolved Staff Comments

|

17 | |

|

Item 2

|

Properties

|

17 | |

|

Item 3

|

Legal Proceedings

|

25 | |

|

Item 4

|

(Removed and Reserved)

|

25 | |

|

PART II

|

|||

|

Item 5

|

Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

|

26 | |

|

Item 6

|

Selected Financial Data

|

28 | |

|

Item 7

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations

|

28 | |

|

Item 7A

|

Quantitative and Qualitative Disclosures About Market Risk.

|

33 | |

|

Item 8

|

Financial Statements and Supplementary Data.

|

33 | |

|

Item 9

|

Changes in and Disagreements With Accountants on Accounting and Financial Disclosure

|

33 | |

|

Item 9A

|

Controls and Procedures

|

34 | |

|

Item 9B

|

Other Information

|

35 | |

|

PART III

|

|||

|

Item 10

|

Directors, Executive Officers and Corporate Governance

|

36 | |

|

Item 11

|

Executive Compensation

|

38 | |

|

Item 12

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters

|

39 | |

|

Item 13

|

Certain Relationships and Related Transactions, and Director Independence

|

40 | |

|

Item 14

|

Principal Accountant Fees and Services

|

40 | |

|

PART IV

|

|||

|

Item 15

|

Exhibits, Financial Statement Schedules

|

41 | |

|

SIGNATURES

|

|||

ii

Oil and Gas Glossary

Adsorption: The accumulation of gases, liquids, or solutes on the surface of a solid or liquid.

Basin: A depressed area where sediments have accumulated during geologic time and considered to be prospective for oil and gas deposits.

Banff Formation: It is a stratigraphical unit of Devonian age in the Western Canadian Sedimentary Basin.

Coal: A carbon-rich rock derived from plant material (peat).

Development: The phase in which a proven oil or gas field is brought into production by drilling production (development) wells.

Drilling: The using of a rig and crew for the drilling, suspension, production testing, capping, plugging and abandoning, deepening, plugging back, sidetracking, re-drilling or reconditioning of a well.

Drilling Logs: Recorded observations made of rock chips cut from the formation by the drill bit, and brought to the surface with the mud, as well as rate of penetration of the drill bit through rock formations. Used by geologists to obtain formation data.

Exploration: The phase of operations which covers the search for oil or gas by carrying out detailed geological and geophysical surveys followed up where appropriate by exploratory drilling. Compare to "Development" phase.

Fracturing: The application of hydraulic pressure to the reservoir formation to create fractures through which oil or gas may move to the wellbore.

Mannville Formation: It is a stratigraphical unit of Cretaceous age in the Western Canadian Sedimentary Basin.

Methane: The simplest of the various hydrocarbons and is the major hydrocarbon component of natural gas, and in fact is commonly known as natural gas. It is colorless, odorless, and burns efficiently without many byproducts.

Milk River Formation: A near- shore to terrestrial sedimentary unit deposited during the Late Cretaceous period in southern Alberta.

Mineral Lease: A legal instrument executed by a mineral owner granting exclusive right to another to explore, drill, and produce oil and gas from a piece of land.

Mississippian Period: The period beginning about 359 million years ago and ending about 318 million years ago.

PN&G: Petroleum and Natural Gas.

Permeability: A measure of the ability of a rock to transmit fluid through pore spaces.

Reserves: Generally the amount of oil or gas in a particular reservoir that is available for production.

Reservoir: The underground rock formation where oil and gas has accumulated. It consists of a porous rock to hold the oil or gas, and a cap rock that prevents its escape.

Stratigraphy: A branch of geology that studies rock layers and layering (stratification). It is primarily used in the study of sedimentary and layered volcanic rocks.

iii

Forward-Looking Statements

This Annual Report on Form 10-K contains forward-looking information. Forward-looking information includes statements relating to future actions, prospective products, future performance or results of current or anticipated products, sales and marketing efforts, costs and expenses, interest rates, outcome of contingencies, financial condition, results of operations, liquidity, business strategies, cost savings, objectives of management of Titan Oil & Gas, Inc. (the “Company”, “Titan”, or “we”) and other matters. Forward-looking information may be included in this Annual Report on Form 10-K or may be incorporated by reference from other documents filed with the Securities and Exchange Commission (the “SEC”) by the Company. One can find many of these statements by looking for words including, for example, “believes,” “expects,” “anticipates,” “estimates” or similar expressions in this Annual Report on Form 10-K or in documents incorporated by reference in this Annual Report on Form 10-K. The Company undertakes no obligation to publicly update or revise any forward-looking statements, whether as a result of new information or future events.

The Company has based the forward-looking statements relating to the Company’s operations on management’s current expectations, estimates and projections about the Company and the industry in which it operates. These statements are not guarantees of future performance and involve risks, uncertainties and assumptions that we cannot predict. In particular, we have based many of these forward-looking statements on assumptions about future events that may prove to be inaccurate. Accordingly, the Company’s actual results may differ materially from those contemplated by these forward-looking statements. Any differences could result from a variety of factors, including, but not limited to general economic and business conditions, competition, and other factors.

iv

PART I

Item 1. Description of Business.

Titan Oil & Gas, Inc. (formerly Xtrasafe, Inc.) (An Exploration Stage Company) was incorporated in the state of Florida on June 5, 2008 under the laws of the State of Florida to market and sell an electronic safe system, through wholesale distribution channels and directly to institutional buyers such as hospitals, colleges, universities, and assisted living facilities throughout the United States. Currently we are principally a company engaged in the acquisition and exploration of oil and gas properties.

On February 25, 2010 the Company’s principal shareholder entered into a Stock Purchase Agreement which provided for the sale of 72,000,000 shares of common stock of the Company to Depinder Grewal. Effective as of February 25, 2010 in connection with the share acquisition, Mr. Grewal was appointed President, Chief Executive Officer, Chief Financial Officer, Treasurer, Director, and Chairman of the Company.

On March 24, 2010, Mr. Grewal returned 36,000,000 common shares to the Company for cancellation. Mr. Grewal returned the shares for cancellation in order to reduce the number of shares issued and outstanding. Subsequent to the cancellation, the Company had 51,600,000 shares issued and outstanding, a number that Mr. Grewal, who was at the time also a director of the Company, considered more in line with the Company’s business plans at that time. Following the share cancellation, Mr. Grewal owned 36,000,000 common shares, or at the time 70%, of the remaining 51,600,000 issued and outstanding common shares of the Company.

Effective as of March 26, 2010 the Board of Directors of the Company elected Vivek Warrier as a director of the Company.

On April 12, 2010 the Company closed a private placement of 2,000,000 common shares at $0.025 per share for a total offering price of $50,000. The common shares were offered by the Company pursuant to an exemption from registration under Regulation S of the Securities Act of 1933, as amended. The private placement was fully subscribed to by two non-U.S. persons.

Also, on April 12, 2010 the Company executed a Sale and Conveyance Agreement (the “Agreement”) with 966749 Alberta Corp. (the “Vendor”) for the acquisition of a 2.51255% working interest in an oil well located in Alberta, Canada. Under the Agreement the Company paid the Vendor $6,043 including taxes and closing costs. The underlying property lease is with the Alberta provincial government.

In addition, on April 12, 2010 the Company acquired an interest in two Petroleum and Natural Gas (“PN&G”) Leases (the “Leases”) in the province of Saskatchewan. Including fees and closing costs the rights to the Leases were acquired for an aggregate $9,873 and the purchase price includes the first year’s aggregate annual lease payments of $372. The total area covered by the Registrant’s portion of the Leases is 132 hectares. The interests in the Leases were acquired through a public land sale process held on a regular basis by the Saskatchewan provincial government.

1

On April 19, 2010, Mr. Grewal, as the holder of 36,500,000 (at the time representing 67%) of the issued and outstanding shares of the Company’s common stock, provided the Company with written consent in lieu of a meeting of stockholders authorizing the Company to amend the Company’s Articles of Incorporation for the purpose of changing the name of the Company from “Xtrasafe, Inc.” to “Titan Oil & Gas, Inc.” and to change its domicile from Florida to Nevada. In order to undertake the name and domicile change, the Company incorporated a wholly-owned subsidiary in Nevada named Titan Oil & Gas, Inc. and merged Xtrasafe, Inc. with the new subsidiary. Subsequent to the merger, the Company continued as a Nevada company named Titan Oil & Gas, Inc.

In connection with the change of the Company’s name to Titan Oil & Gas, Inc. the Company’s business was changed to oil and gas exploration. The change in name, business, and domicile received its final approval by the regulatory authorities on June 30, 2010.

On July 6, 2010 the Company adopted a resolution to split the Company’s common stock. The Board of Directors approved a 1:8 forward stock split. The record and payment dates of the forward split were July 22 and July 23, 2010, respectively. All of the common shares issued and outstanding on July 22, 2010 were split. All references to share and per share amounts have been restated in this form 10-K to reflect the split.

Effective as of August 1, 2010 the Board of Directors of the Company elected Jack Adams as a director of the Company.

On August 3, 2010 the Company adopted its 2010 Stock Option Plan (“the 2010 Plan”). The 2010 Plan provides for the granting of up to 5,000,000 stock options to key employees, directors and consultants, of common shares of the Company. Currently, 550,000 options have been granted under the 2010 Plan at an exercise price of $0.26 per share.

On August 18, 2010 the Company closed a private placement of 160,000 common shares at $0.50 per share for a total offering price of $80,000. The common shares were offered by the Company pursuant to an exemption from registration under Regulation S of the Securities Act of 1933, as amended. The private placement was fully subscribed to one non-U.S. person.

On August 19, 2010 the Company acquired an interest in one Petroleum and Natural Gas (“PN&G) Lease (the “Lease”) in the province of Alberta, Canada. Including fees and closing costs the rights to the Lease were acquired for an aggregate $13,099 and the purchase price includes the first year’s aggregate annual lease payments of $842. The total area covered by the Lease is 256 hectares

Between September 2 and 30, 2010 the Company entered into six additional PN&G leases (the “Leases”) with the Alberta provincial government. The terms of the Leases are the same as those previously entered into between the Company and the Alberta government. The additional leases cover a total area of 1,536 hectares and have minimum annual lease payments of $5,052.

2

Effective as of September 13, 2010 the Board of Directors of Titan elected Mr. Jarnail Dhaddey President, Chief Executive Officer, Chief Financial Officer, Chief Accounting Officer, Secretary, Treasurer and Director of the Company. Also effective as of September 13, 2010 Mr. Depinder Grewal resigned as President, Chief Executive Officer, Chief Financial Officer, Chief Accounting Officer, Secretary, Treasurer and Director of the Company.

Business Operations

Titan Oil & Gas Inc. is principally a company engaged in the acquisition and exploration of oil and gas properties.

On April 12, 2010 the Company executed a Sale and Conveyance Agreement (the “Agreement”) with 966749 Alberta Corp. (the “Vendor”) for the acquisition of a 2.51255% working interest in an oil well located in Alberta, Canada. Under the Agreement the Company paid the Vendor $6,043 including taxes and closing costs. The underlying property lease is with the Alberta provincial government.

Also on April 12, 2010 the Company acquired an interest in two PN&G Leases (the “Leases”) in the province of Saskatchewan. Including fees and closing costs the rights to the Leases were acquired for an aggregate $9,873 and the purchase price includes the first year’s aggregate annual lease payments of $372. The total area covered by the Registrant’s portion of the Leases is 132 hectares. The interests in the Leases were acquired through a public land sale process held on a regular basis by the Saskatchewan provincial government. Upon being notified that it has submitted the highest bid for a specific land parcel the Company immediately pays the government the bid price and enters into a formal lease with the government. The Lease is for a 5 year term, requires minimum annual lease payments, and grants the Company the right to explore for potential petroleum and natural gas opportunities on the respective lease.

On August 19, 2010 the Company acquired an interest in one PN&G Lease (the “Lease”) in the province of Alberta, Canada. Including fees and closing costs the rights to the Lease were acquired for an aggregate $13,099 and the purchase price includes the first year’s aggregate annual lease payments of $842. The total area covered by the Lease is 256 hectares. The interest in the Lease was acquired through a public land sale process held on a regular basis by the Alberta provincial government. Upon being notified that it has submitted the highest bid for a specific land parcel the Company immediately pays the government the bid price and enters into a formal lease with the government. The Lease is for a 5 year term, requires minimum annual lease payments, and grants the Company the right to explore for potential petroleum and natural gas opportunities on the respective lease.

Between September 2 and 30, 2010 the Company entered into six additional PN&G leases (the “Leases”) with the Alberta provincial government. The terms of the Leases are the same as those previously entered into between the Company and the Alberta government. The additional leases cover a total area of 1,536 hectares and have minimum annual lease payments of $5,052.

3

All of the Company’s Leases are subject to royalties payable to the governments of Alberta or Saskatchewan. The royalty is calculated using a revenue-less-cost formula. The leases are renewable if certain conditions are met. For all of its leased properties, the Company has obtained the Petroleum and Natural Gas rights only.

Financing

On April 12, 2010 the Company closed a private placement of 2,000,000 common shares at $0.025 per share for a total offering price of $50,000. The common shares were offered by the Company pursuant to an exemption from registration under Regulation S of the Securities Act of 1933, as amended. The private placement was fully subscribed to by two non-U.S. persons.

On August 18, 2010 the Company closed a private placement of 160,000 common shares at $0.50 per share for a total offering price of $80,000. The common shares were offered by the Company pursuant to an exemption from registration under Regulation S of the Securities Act of 1933, as amended. The private placement was fully subscribed to one non-U.S. person.

Over the next twelve months, the Company intends to explore various options for obtaining funding. The Company does not intend to hire any employees or to make any purchases of equipment over the next twelve months, as it intends to rely upon outside consultants to provide all the necessary expertise for any work being conducted.

Current cash on hand is insufficient for all of the Company’s commitments for the next 12 months. We anticipate that the additional funding that we require will be in the form of equity financing from the sale of our common stock. However, we cannot provide investors with any assurance that we will be able to raise sufficient funding from the sale of our common stock to fund additional phases of the Exploration program, should we decide to proceed. We believe that debt financing will not be an alternative for funding any further phases in our Exploration program. The risky nature of this enterprise and lack of tangible assets places debt financing beyond the credit-worthiness required by most banks or typical investors of corporate debt until such time as an economically viable mine can be demonstrated. We do not have any arrangements in place for any future equity financing.

Notwithstanding, we cannot be certain that the required additional financing will be available or available on terms favorable to us. If additional funds are raised by the issuance of our equity securities, such as through the issuance and exercise of warrants, then existing stockholders will experience dilution of their ownership interest. If additional funds are raised by the issuance of debt or other equity instruments, we may be subject to certain limitations in our operations, and issuance of such securities may have rights senior to those of the then existing holders of common stock. If adequate funds are not available or not available on acceptable terms, we may be unable to fund expansion, develop or enhance services or respond to competitive pressures.

4

Competition

The oil and gas exploration industry is intensely competitive, highly fragmented and subject to rapid change. We may be unable to compete successfully with our existing competitors or with any new competitors. We compete with many exploration companies that have significantly greater personnel, financial, managerial, and technical resources than we do. This competition from other companies with greater resources and reputations may result in our failure to maintain or expand our business.

Government Regulation

Development, production and sale of natural gas and oil in Canada are subject to extensive laws and regulations, including environmental laws and regulations. The oil and gas properties currently leased by the Company are owned by either the Province of Alberta or Saskatchewan and are managed by the respective Departments of Energy. We may be required to make large expenditures to comply with environmental and other governmental regulations. Matters subject to regulation include:

|

• location and density of wells;

|

|

|

• the handling of drilling fluids and obtaining discharge permits for drilling operations;

|

|

|

• accounting for and payment of royalties on production from state, federal and Indian lands;

|

|

|

• bonds for ownership, development and production of natural gas and oil properties;

|

|

|

• transportation of natural gas and oil by pipelines;

|

|

|

• operation of wells and reports concerning operations; and

|

|

|

• taxation.

|

Under these laws and regulations, we could be liable for personal injuries, property damage, oil spills, discharge of hazardous materials, remediation and clean-up costs and other environmental damages. Failure to comply with these laws and regulations also may result in the suspension or termination of our operations and subject us to administrative, civil and criminal penalties. Moreover, these laws and regulations could change in ways that substantially increase our costs. Accordingly, any of these liabilities, penalties, suspensions, terminations or regulatory changes could materially adversely affect our financial condition and results of operations enough to possibly force us to cease our business operations.

Employees

We have commenced only limited operations. Therefore, we have no full time employees. Our sole officer and three directors provide planning and organizational services for us on a part-time basis.

Subsidiaries

We do not have any subsidiaries and we are not part of a group.

5

Item 1A. Risk Factors

Factors that May Affect Future Results

This investment has a high degree of risk. Before you invest you should carefully consider the risks and uncertainties described below and the other information included in this form 10-K. If any of the following risks actually occur, our business, operating results and financial condition could be harmed and the value of our stock could go down. This means you could lose all or a part of your investment.

RISKS RELATING TO OUR COMPANY

|

1.

|

We are an exploration stage company, with limited operating history in oil and gas exploration and we have focused primarily on establishing our operations, all of which raises substantial doubt as to our ability to successfully develop profitable business operations and makes an investment in our common shares very risky.

|

On April 19, 2010, our principal shareholder provided the Company with written consent in lieu of a meeting of stockholders authorizing the Company to amend the Company’s Articles of Incorporation for the purpose of changing the name of the Company from “Xtrasafe, Inc.” to “Titan Oil & Gas, Inc.” and to change its domicile from Florida to Nevada. In order to undertake the name and domicile change, the Company incorporated a wholly-owned subsidiary in Nevada named Titan Oil & Gas, Inc. and merged Xtrasafe, Inc. with the new subsidiary. Subsequent to the merger, the Company continued as a Nevada company named Titan Oil & Gas, Inc.

In connection with the change of the Company’s name to Titan Oil & Gas, Inc. the Company’s business was changed to oil and gas exploration. The change in name, business, and domicile received its final approval by the regulatory authorities on June 30, 2010. As a result we have only recently commenced oil and gas exploration operations.

Our prospects must be considered in light of the risks, expenses and difficulties frequently encountered in establishing a business in the oil and natural gas industries. We have yet to generate any revenues from operations and have been focused on organizational, start-up, property acquisition, and fund raising activities. Since we have not generated any revenues, we will have to raise additional capital to fund our operations for the next twelve months, which we may do through loans from existing shareholders, the sale of our equity securities or strategic arrangement with a third party in order to continue our business operations. There is nothing at this time on which to base an assumption that our business operations will prove to be successful or that we will ever be able to operate profitably. Our future operating results will depend on many factors, including:

6

|

• our ability to raise adequate working capital;

|

|

|

• success of our exploration and development;

|

|

|

• demand for natural gas and oil;

|

|

|

• the level of our competition;

|

|

|

• our ability to attract and maintain key management and employees; and

|

|

|

• our ability to efficiently explore, develop and produce sufficient quantities of marketable natural gas or oil in a highly competitive and speculative environment while maintaining quality and controlling costs.

|

To achieve profitable operations, we must, alone or with others, successfully execute on the factors stated above. If we are not successful in executing any of the above stated factors, our business will not be profitable and may never even generate any revenue, which make our common shares a less attractive investment and may harm the trading of our common shares, if a market ever develops.

|

2.

|

The field of oil and gas exploration is difficult to predict because of technological advancements and market factors, which factors our management may not correctly assess and it may make it difficult for investors to sell their our common shares.

|

Because the nature of our business is expected to change as a result of shifts in the market price of oil and natural gas, competition, and the development of new and improved technology, management forecasts are not necessarily indicative of future operations and should not be relied upon as an indication of future performance.

Our Management may incorrectly estimate projected occurrences and events within the timetable of our business plan, which would have an adverse effect on our results of operations and, consequently, make our common shares a less attractive investment and harm the future trading of our common shares trading on the OTC Bulletin Board. Investors may find it difficult to sell their shares on the OTC Bulletin Board should a market ever develop for our shares.

|

3.

|

Because we have no plan to generate revenue unless and until our exploration program is successful in finding productive wells, we will need to raise a substantial amount of additional capital in order to fund our operations for the next twelve months and in order to develop our properties and acquire and develop new properties. If the prospects for our properties are not favorable or the capital markets are tight, we would not be able to raise the necessary capital and we will not be able to pursue our business plan, which would likely cause our common shares to become worthless.

|

7

Cash on hand is insufficient to fund our anticipated operating needs of approximately $96,000 for the next twelve months. As we have no plan to generate revenue unless and until our exploration program is successful in finding productive wells, we will require substantial additional capital to fund our operations for the next twelve months and in order to explore our leased properties which have not had any production of oil or natural gas, as well as for the future acquisition and/or development of other properties. Because we currently do not have any cash flow from operations we need to raise additional capital, which may be in the form of loans from current shareholders and/or from public and private equity offerings. Our ability to access capital will depend on our success in participating in properties that are successful in exploring for and producing oil and gas at profitable prices. It will also be dependent upon the status of the capital markets at the time such capital is sought. Should sufficient capital not be available, the development of our business plan could be delayed and, accordingly, the implementation of our business strategy would be adversely affected. In such event it would not be likely that investors would obtain a profitable return on their investments or a return of their investments at all.

|

4.

|

Even if we discover unconventional tight gas on our properties, a great deal more effort has to be put into extracting gas from a tight formation than a conventional natural gas deposit, where once drilled, the gas can usually be extracted quite readily, and easily. Several techniques exist that allow natural gas to be extracted, including fracturing and acidizing, however, these techniques are very costly. Accordingly, we will require substantial additional capital to fund our operations and should we fail to do so, we will not be able to pursue our business plan, which would likely cause our common shares to become worthless.

|

Currently, we are focused primarily on exploring our properties to determine the potential for hosting natural gas in the form of unconventional tight gas. Unconventional tight gas is stuck in very tight formations underground, trapped in unusually impermeable, hard rock, or in a sandstone or limestone formations that are unusually impermeable and non-porous (tight sand). We have no revenues, and we do not have any plan to generate revenue unless and until our exploration program is successful in finding productive wells. However, even if we discover unconventional tight gas on our properties, a great deal more effort has to be put into extracting gas from a tight formation than a conventional natural gas deposit, where once drilled, the gas can usually be extracted quite readily, and easily. Several techniques exist that allow natural gas to be extracted, including fracturing and acidizing, however, these techniques are very costly. Accordingly, we will require substantial additional capital to fund our operations. Because we currently do not have any cash flow from operations, we will need to raise additional capital, which may be in the form of loans from current shareholders and/or from public and private equity offerings. Should sufficient capital not be available, the development of our business plan could be delayed and, accordingly, the implementation of our business strategy would be adversely affected. In such event it would not be likely that investors would obtain a profitable return on their investments or a return of their investments at all.

8

|

5.

|

We are heavily dependent on contracted third parties. The inability to identify and obtain the services of third party contractors would harm our ability to execute our business plan and continue our operations until we found a suitable replacement.

|

We are dependent on the continued contributions of third party contractors whose knowledge and technical expertise is critical for future of the Company. Our success is also heavily dependent on our ability to retain and attract experienced engineers, geoscientists and other technical and professional staff. We do not currently have any long-term consulting agreements in place with third parties under which we can ensure that we will have sufficient expertise to undertake our planned exploration program. If we were unable to obtain the services of third party contractors our ability to execute our business plan would be harmed and we may be forced to cease operations until such time as we could hire suitable contractors.

|

6.

|

Volatility of oil and gas prices and markets, over which we have no control, could make it difficult for us to achieve profitability and investors are likely to lose their investment in our common shares.

|

Our ability to achieve profitability is substantially dependent on prevailing prices for natural gas and oil. The amounts of, and price obtainable for, any oil and gas production that we achieve will be affected by market factors beyond our control. If these factors are not favorable over time to our financial interests, it is likely that owners of our common shares will lose their investments. Such factors include:

|

• worldwide or regional demand for energy, which is affected by economic conditions;

|

|

|

• the domestic and foreign supply of natural gas and oil;

|

|

|

• weather conditions;

|

|

|

• domestic and foreign governmental regulations;

|

|

|

• political conditions in natural gas and oil producing regions;

|

|

|

• the ability of members of the Organization of Petroleum Exporting Countries to agree upon and maintain oil prices and production levels; and

|

|

|

• the price and availability of other fuels.

|

9

|

7.

|

Drilling wells is speculative, often involving significant costs that are difficult to project and may be more than our estimates, unsuccessful drilling of wells or successful drilling of wells that are, nonetheless, unprofitable, any one of which is likely to reduce the profitability of our business and negatively affect our results of operations.

|

Exploration and the development of oil and natural gas properties involves a high degree of operational and financial risk, which precludes definitive statements as to the time required and costs involved in reaching certain objectives. The budgeted costs of drilling, completing and operating wells are often exceeded and can increase significantly when drilling costs rise due to a tightening in the supply of various types of oilfield equipment and related services. Drilling may be unsuccessful for many reasons, including title problems, weather, cost overruns, equipment shortages and mechanical difficulties. Moreover, the successful drilling of a natural gas or oil well does not ensure a profit on investment. Exploratory wells bear a much greater risk of loss than development wells. A variety of factors, both geological and market-related, can cause a well to become uneconomical or only marginally economic and the results of our operations will be negatively affected as well.

|

8.

|

The natural gas and oil business involves numerous uncertainties and operating risks that can prevent us from realizing profits and can cause substantial losses.

|

Our exploration, development, and exploitation activities may be unsuccessful for many reasons, including weather, cost overruns, equipment shortages and mechanical difficulties. Moreover, the successful drilling of a natural gas and oil well does not ensure a profit on investment. A variety of factors, both geological and market-related, can cause a well to become uneconomical or only marginally economical.

The natural gas and oil business involves a variety of operating risks, including:

|

• fires;

|

|

|

• explosions;

|

|

|

• blow-outs and surface cratering;

|

|

|

• uncontrollable flows of oil, natural gas, and formation water;

|

|

|

• natural disasters, such as hurricanes and other adverse weather conditions;

|

|

|

• pipe, cement, or pipeline failures;

|

|

|

• casing collapses;

|

|

|

• embedded oil field drilling and service tools;

|

|

|

• abnormally pressured formations; and

|

|

|

• environmental hazards, such as natural gas leaks, oil spills, pipeline ruptures and discharges of toxic gases.

|

If we experience any of these problems, it could affect well bores, gathering systems and processing facilities, which could adversely affect our ability to conduct operations. We could also incur substantial losses as a result of:

10

|

• injury or loss of life;

|

|

|

• severe damage to and destruction of property, natural resources and equipment;

|

|

|

• pollution and other environmental damage;

|

|

|

• clean-up responsibilities;

|

|

|

• regulatory investigation and penalties;

|

|

|

• suspension of our operations; and

|

|

|

• repairs to resume operations.

|

|

9.

|

If we commence drilling, we do not currently have any contracts with equipment providers, we may face the unavailability or high cost of drilling rigs, equipment, supplies, personnel and other services which could adversely affect our ability to execute on a timely basis our development, exploitation and exploration plans within our budget and, as a result, negatively impact our financial condition and results of operations.

|

If we commence drilling, shortages or an increase in cost of drilling rigs, equipment, supplies or personnel could delay or interrupt our operations, which could negatively impact our financial condition and results of operations. Drilling activity in the geographic areas in which we conduct drilling activities may increase, which would lead to increases in associated costs, including those related to drilling rigs, equipment, supplies and personnel and the services and products of other vendors to the industry. Increased drilling activity in these areas may also decrease the availability of rigs. We do not currently have any contracts with providers of drilling rigs and, consequently we may not be able to obtain drilling rigs when we need them. Therefore, our drilling and other costs may increase further and necessary equipment and services may not be available to us at economical prices.

|

10.

|

We are subject to complex laws and regulations, including environmental regulations, which can significantly increase our costs and possibly force our operations to cease.

|

If we commence drilling and experience any leakage of crude oil and/or gas from the subsurface portions of a well, our gathering system could cause degradation of fresh groundwater resources, as well as surface damage, potentially resulting in suspension of operation of a well, fines and penalties from governmental agencies, expenditures for remediation of the affected resource, and liabilities to third parties for property damages and personal injuries. In addition, any sale of residual crude oil collected as part of the drilling and recovery process could impose liability on us if the entity to which the oil was transferred fails to manage the material in accordance with applicable environmental health and safety laws.

Drilling operations generally involve a high degree of risk. Hazards such as unusual or unexpected geological formations, power outages, labor disruptions, blow-outs, sour gas leakage, fire, inability to obtain suitable or adequate machinery, equipment or labor, and other risks are involved. We may become subject to liability for pollution or hazards against which it cannot adequately insure or which it may elect not to insure. Incurring any such liability may have a material adverse effect on our financial position and operations.

11

Development, production and sale of natural gas and oil in Canada are subject to extensive laws and regulations, including environmental laws and regulations. We may be required to make large expenditures to comply with environmental and other governmental regulations. Matters subject to regulation include:

|

• location and density of wells;

|

|

|

• the handling of drilling fluids and obtaining discharge permits for drilling operations;

|

|

|

• accounting for and payment of royalties on production from state, federal and Indian lands;

|

|

|

• bonds for ownership, development and production of natural gas and oil properties;

|

|

|

• transportation of natural gas and oil by pipelines;

|

|

|

• operation of wells and reports concerning operations; and

|

|

|

• taxation.

|

Under these laws and regulations, we could be liable for personal injuries, property damage, oil spills, discharge of hazardous materials, remediation and clean-up costs and other environmental damages. Failure to comply with these laws and regulations also may result in the suspension or termination of our operations and subject us to administrative, civil and criminal penalties. Moreover, these laws and regulations could change in ways that substantially increase our costs. Accordingly, any of these liabilities, penalties, suspensions, terminations or regulatory changes could materially adversely affect our financial condition and results of operations enough to possibly force us to cease our business operations.

|

11.

|

The potential profitability of oil and gas ventures depends upon various factors beyond the control of our company, which may materially affect our financial performance.

|

The potential profitability of oil and gas properties is dependent upon many factors beyond our control. For instance, world prices and markets for oil and gas are unpredictable, highly volatile, potentially subject to governmental fixing, pegging, controls, or any combination of these and other factors, and respond to changes in domestic, international, political, social, and economic environments. Additionally, due to worldwide economic uncertainty, the availability and cost of funds for production and other expenses have become increasingly difficult, if not impossible, to project. These changes and events may materially affect our financial performance.

12

|

12.

|

Our auditors’ opinion in our August 31, 2010 financial statements includes an explanatory paragraph in respect of there being substantial doubt about our ability to continue as a going concern. We will need to raise additional capital in order to fund our operations for the next twelve months, and if we fail to raise such capital investors may lose some or all of their investment in our common shares.

|

We have incurred net losses of $75,552 from June 5, 2008 (inception) to August 31, 2010. Our financial statements do not include any adjustments relating to the recoverability and classification of recorded assets, or the amounts of and classification of liabilities that might be necessary in the event the Company cannot continue in existence. We anticipate generating losses for at least the next 12 months. Therefore, there is substantial doubt about our ability to continue operations in the future as a going concern. We will need to obtain additional funds in order to fund our operations for the next twelve months. Our plans to deal with this cash requirement include loans from existing shareholders, raising additional capital from the public or private sale of equity or entering into a strategic arrangement with a third party. If we cannot continue as a viable entity, our shareholders may lose some or all of their investment in our company.

|

13.

|

If we do not maintain the property lease payments on our properties, we will lose our interests in the properties as well as losing all monies incurred in connection with the properties.

|

We have seven PN&G leases in Alberta and two in Saskatchewan, Canada. Our leases require annual lease payments to the respective Alberta and Saskatchewan provincial governments. See Item 2 of this Form 10-K for a more detailed description of the property obligations. If we do not continue to make the annual lease payments, we will lose our ability to explore and develop the properties and we will not retain any kind of interest in the properties.

|

14.

|

We may not be able to compete with current and potential exploration companies, some of whom have greater resources and experience than we do in locating and commercializing oil and natural gas reserves and, as a result, we may fail in our ability to maintain or expand our business.

|

The natural gas and oil market is intensely competitive, highly fragmented and subject to rapid change. We may be unable to compete successfully with our existing competitors or with any new competitors. We compete with many exploration companies which have significantly greater personnel, financial, managerial, and technical resources than we do. This competition from other companies with greater resources and reputations may result in our failure to maintain or expand our business.

13

|

15.

|

We expect losses to continue in the next 12 months because we have no oil or gas reserves and, consequently, no revenue to offset losses.

|

Based upon the fact that we currently do not have any oil or gas reserves, we expect to incur operating losses in next 12 months. The operating losses will occur because there are expenses associated with the acquisition of, and exploration of natural gas and oil properties which do not have any income-producing reserves. Failure to generate revenues may cause us to go out of business. We will require additional funds to achieve our current business strategy and our inability to obtain additional financing will interfere with our ability to expand our current business operations.

|

16.

|

Since our directors work for other natural resource exploration companies, their other activities for those other companies may involve a conflict of interest with regard to their time, could slow down our operations or negatively affect our profitability.

|

Our sole officer and three directors are not required to work exclusively for us and do not devote all of their time to our operations. In fact, our directors work for other natural resource exploration companies. Therefore, it is possible that a conflict of interest with regard to their time may arise based on their employment by such other companies. Their other activities may prevent them from devoting full-time to our operations which could slow our operations and may reduce our financial results because of the slowdown in operations. It is expected that each of our directors will devote approximately 1 hour per week to our operations on an ongoing basis, and when required will devote whole days and even multiple days at a stretch when property visits are required or when extensive analysis of information is needed.

|

17.

|

Our principal shareholder owns a controlling interest in our voting stock and investors will not have any voice in our management, which could result in decisions adverse to our general shareholders.

|

Our principal shareholder beneficially owns approximately 67% of our outstanding common stock. As a result, this stockholder will have the ability to control substantially all matters submitted to our stockholders for approval including:

|

·

|

election of our board of directors;

|

|

·

|

removal of any of our directors;

|

|

·

|

amendment of our Articles of Incorporation or bylaws; and

|

|

·

|

adoption of measures that could delay or prevent a change in control or impede a merger, takeover or other business combination involving us.

|

14

As a result of his ownership, our principal shareholder is able to influence all matters requiring shareholder approval, including the election of directors and approval of significant corporate transactions. In addition, it is possible for our principal shareholder to sell or otherwise dispose of all or a part of his shareholdings could affect the market price of our common stock if the marketplace does not orderly adjust to the increase in shares in the market and the value of your investment in the Company may decrease. The controlling shareholder’s stock ownership may discourage a potential acquirer from making a tender offer or otherwise attempting to obtain control of us, which in turn could reduce our stock price or prevent our stockholders from realizing a premium over our stock price.

|

18.

|

We have no employees and our only officer works one day per week on our business and our directors work only one hour per week on our business. Consequently, we may not be able to monitor our operations and respond to matters when they arise in a prompt or timely fashion. Until we have additional capital or generate revenue, we will have to rely on consultants and service providers, which will increase our expenses and increase our losses.

|

We do not have any employees, our only officer works on our business one day per week and our directors each spends one hour a week on our business. With practically no personnel, we have a limited ability to monitor our operations, such as the progress of oil and gas exploration, and to respond to inquiries from third parties, such as regulatory authorities or potential business partners. Though we may rely on third party service providers, such as accountants and lawyers, to address some of our matters, until we raise additional capital or generate revenue, we will have to rely on consultants and third party service providers to monitor our operations, which will increase our expenses and have a negative effect on our results of operations.

RISKS RELATING TO OUR COMMON SHARES

|

19.

|

We may, in the future, issue additional common shares, which would reduce investors’ percent of ownership and may dilute our share value.

|

Our Articles of Incorporation authorize the issuance of 100,000,000 common shares, of which 53,760,000 shares are issued and outstanding. The future issuance of our common shares may result in substantial dilution in the percentage of our common shares held by our then existing shareholders. We may value any common shares issued in the future on an arbitrary basis. The issuance of common shares for future services or acquisitions or other corporate actions may have the effect of diluting the value of the shares held by our investors, and might have an adverse effect on any trading market for our common shares.

15

|

20.

|

Our common shares are subject to the "Penny Stock" Rules of the SEC and we have no established market for our securities, which makes transactions in our stock cumbersome and may reduce the value of an investment in our stock.

|

The Securities and Exchange Commission has adopted Rule 15g-9 which establishes the definition of a "penny stock," for the purposes relevant to us, as any equity security that has a market price of less than USD $5.00 per share or with an exercise price of less than USD $5.00 per share, subject to certain exceptions. For any transaction involving a penny stock, unless exempt, the rules require:

|

·

|

that a broker or dealer approve a person’s account for transactions in penny stocks; and

|

|

·

|

the broker or dealer receive from the investor a written agreement to the transaction, setting forth the identity and quantity of the penny stock to be purchased.

|

In order to approve a person's account for transactions in penny stocks, the broker or dealer must:

|

·

|

obtain financial information and investment experience objectives of the person; and

|

|

·

|

make a reasonable determination that the transactions in penny stocks are suitable for that person and the person has sufficient knowledge and experience in financial matters to be capable of evaluating the risks of transactions in penny stocks.

|

The broker or dealer must also deliver, prior to any transaction in a penny stock, a disclosure schedule prescribed by the Commission relating to the penny stock market, which, in highlight form:

|

·

|

sets forth the basis on which the broker or dealer made the suitability determination; and

|

|

·

|

that the broker or dealer received a signed, written agreement from the investor prior to the transaction.

|

Generally, brokers may be less willing to execute transactions in securities subject to the "penny stock" rules. This may make it more difficult for investors to dispose of our common shares and cause a decline in the market value of our stock.

Disclosure also has to be made about the risks of investing in penny stocks in both public offerings and in secondary trading and about the commissions payable to both the broker-dealer and the registered representative, current quotations for the securities and the rights and remedies available to an investor in cases of fraud in penny stock transactions. Finally, monthly statements have to be sent disclosing recent price information for the penny stock held in the account and information on the limited market in penny stocks.

16

|

21.

|

Because we do not intend to pay any cash dividends on our common shares, our stockholders will not be able to receive a return on their shares unless they sell them.

|

We intend to retain any future earnings to finance the development and expansion of our business. We do not anticipate paying any cash dividends on our common shares in the foreseeable future. Unless we pay dividends, our stockholders will not be able to receive a return on their shares unless they sell them.

|

22.

|

We may become a passive foreign investment company, or PFIC, which could result in adverse U.S. tax consequences to U.S. investors.

|

If we are a “passive foreign investment company” or “PFIC” as defined in Section 1297 of the Code, U.S. Holders will be subject to U.S. federal income taxation under one of two alternative tax regimes at the election of each such U.S. Holder. Section 1297 of the Code defines a PFIC as a corporation that is not formed in the United States and either (i) 75% or more of its gross income for the taxable year is “passive income”, which generally includes interest, dividends and certain rents and royalties or (ii) the average percentage, by fair market value (or, if we elect, adjusted tax basis), of its assets that produce or are held for the production of “passive income” is 50% or more. Whether we are a PFIC in any year and the tax consequences relating to PFIC status will depend on the composition of our income and assets, including cash. U.S. Holders should be aware, however, that if we become a PFIC, we may not be able or willing to satisfy record-keeping requirements that would enable U.S. Holders to make an election to treat us as a “qualified electing fund” for purposes of one of the two alternative tax regimes applicable to a PFIC, which would result in adverse tax consequences to our shareholders who are U.S. citizens.

Item 1B. Unresolved Staff Comments

There are no unresolved staff comments.

Item 2. Description of Properties.

Corporate Office

We currently maintain our corporate office on a one-year lease basis at 7251 West Lake Mead Boulevard, Suite 300, Las Vegas, Nevada, 89128. Management believes that our office space is suitable for our current needs.

17

Oil and Gas Property Lease Information

The Company’s oil and gas properties are comprised of seven Petroleum & Natural Gas (“PN&G”) leases with the government of the province of Alberta, Canada and two PN&G leases with the province of Saskatchewan, Canada. All of the interests in the leases were acquired through a public land sale process held on a regular basis by the provinces of Alberta and Saskatchewan respectively. Upon being notified that it has submitted the highest bid for a specific land parcel the Company immediately pays the respective government the bid price and enters into a formal lease with the government. The lease is for a 5 year term with a commencement date equal to the date of acquisition, requires minimum annual lease payments, and grants the Company the right to explore for potential petroleum and natural gas opportunities on the respective lease. The leases are renewable if certain conditions are met. All leases require the payment of the first year’s minimum annual lease payments at the time of acquisition. In general, minimum annual lease payments are CDN $3.50 (USD $3.29) per hectare. All of the Company’s leases are subject to royalties payable to the respective provincial governments of Alberta or Saskatchewan. The royalty is calculated using a revenue-less-cost formula.

Unconventional Tight Gas Sands Background

Canada has large deposits of natural gas in rock formations that are especially difficult and expensive to produce. The gas in these difficult-to-produce formations is often referred to as “unconventional”. Most commonly, the formations are low permeability, or “tight” sandstones and limestones, coal seams, organic shales, or interbedded combinations of these formations.

Unconventional gas is found in virtually all Canadian sedimentary basins with the gas resource estimated at over 60 trillion cubic metres. Over the last several decades, new technologies have allowed it to be commercially developed. Between 20% and 30% of Canada's current natural gas production is unconventional. In the United States, unconventional gas accounts for over 40% of gas production.

Tight sandstones and limestones are Canada's most important unconventional gas resource in terms of production. A recent study, funded in part by the Canadian government, indicates that between 85 and 113 million cubic metres per day of Canada's gas production is from tight gas formations. Historically, it has not been the practice in Canada to distinguish between conventional and unconventional gas production from sandstones and limestones. Over the last decade or so, the contribution of tight zones to production has been increasingly recognized and targeted for development.

Significant tight gas production occurs in shallow gas plays in Alberta, and the deep basin of Alberta. Over the years there has been significant success in accessing natural gas locked in these tight gas reservoirs primarily through the application of horizontal drilling technology. As conventional sandstones and limestones continue to decline in production, these tight formations will become increasingly important as industry currently shows a high level of interest in this play.

18

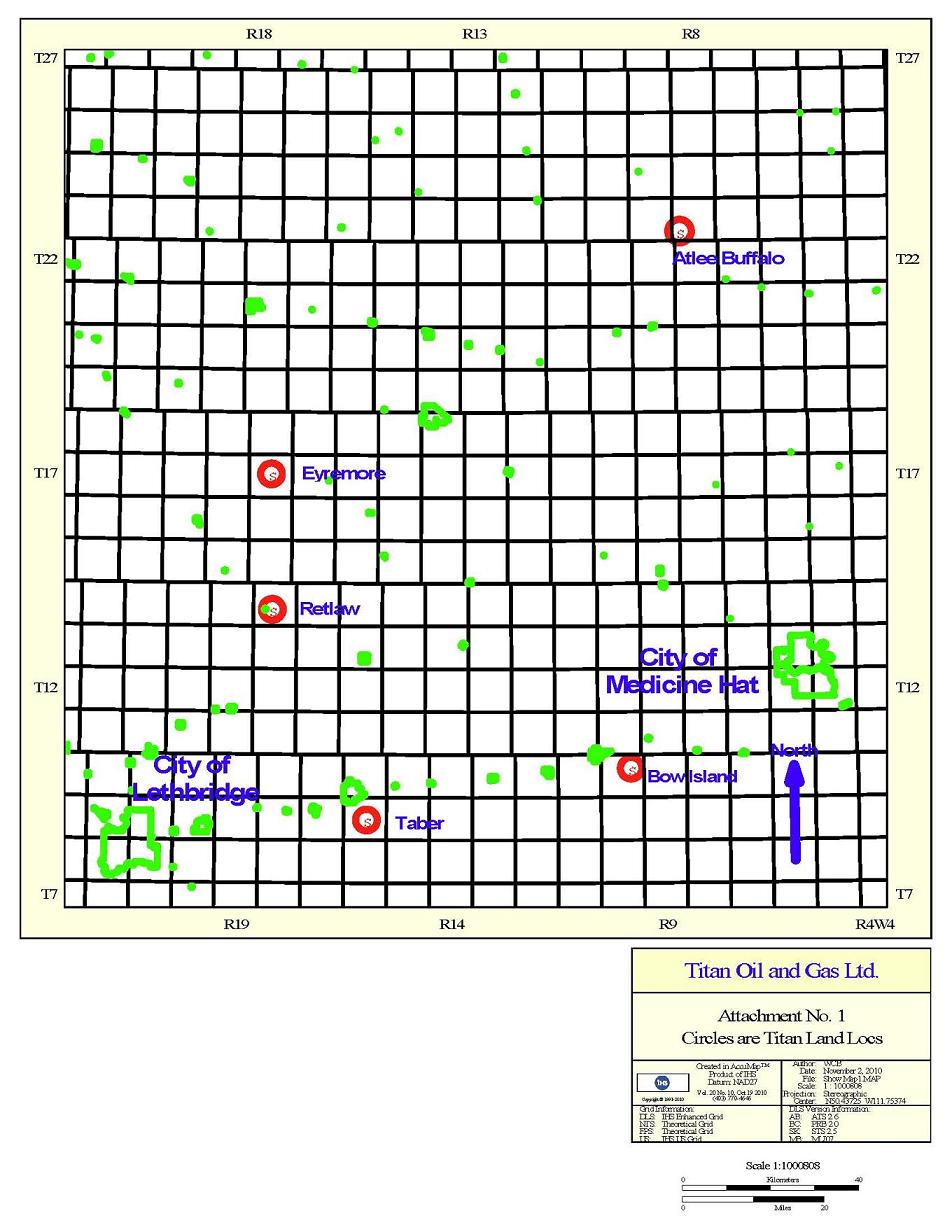

Southeast Alberta Properties

Map of the Southeast Alberta Properties. Red circles indicate the location of Titan’s interests.

19

Acquisition of Interests

On August 19, 2010 the Company acquired an interest in one PN&G Lease (the “Lease”) in the province of Alberta, Canada. Including fees and closing costs the rights to the Lease were acquired for an aggregate $13,099 and the purchase price includes the first year’s aggregate annual lease payments of $842. The total area covered by the Lease is 256 hectares

Between September 2 and 30, 2010 the Company entered into six additional PN&G leases (the “Leases”) with the Alberta provincial government. The terms of the Leases are the same as those previously entered into between the Company and the Alberta government. The additional leases cover a total area of 1,536 hectares and have minimum annual lease payments of $5,052.

Description and Location of the Southeast Alberta Properties

The Company has acquired the following leases:

|

Date

|

Location

|

Number of Leases

|

Land Area

(Hectares)

|

Annual Lease Payments

|

|

August 19, 2010

|

Retlaw

|

1

|

256

|

CDN $896 / USD $842

|

|

September 2, 2010

|

Bow Island

|

1

|

256

|

CDN $896 / USD $842

|

|

September 2, 2010

|

Eyremore

|

1

|

256

|

CDN $896 / USD $842

|

|

September 2, 2010

|

Eyremore

|

1

|

256

|

CDN $896 / USD $842

|

|

September 16, 2010

|

Atlee Buffalo

|

1

|

256

|

CDN $896 / USD $842

|

|

September 30, 2010

|

Taber

|

1

|

256

|

CDN $896 / USD $842

|

|

September 30,2010

|

Bow Island

|

1

|

256

|

CDN $896 / USD $842

|

|

7

|

1,792

|

CDN $6,272 / USD $5,894

|

Regional Geology

Alberta contains vast amounts of coal distributed throughout the southern Plains, Foothills, and Mountains. Originally deposited in relatively flat-lying peat swamps, organic matter (peat) was buried by sediments derived from uplift (mountain building), in the west and gradually changed into coal with increasing heat and pressure of burial. Over time, the coals were uplifted and partially eroded away, resulting in the present distribution of coal across the Plains. Coal-bearing strata dip gently westward toward the Mountains where coals are folded and abruptly turn toward the surface to be exposed in the Foothills.

Coal typically occurs within a coal zone as discrete seams and/or packages with several thin and thick seams interbedded with non-coaly rock layers or beds. A coal zone may be traceable over a large geographic area. Coal zones are found in strata ranging in age from Late Jurassic (approximately 145 million years old) to Tertiary (approximately 65 million years old).

20

The oldest and deepest coals of the Alberta Plains belong to the Lower Cretaceous Mannville Group coals. The Mannville coals are widely distributed across the Alberta Plains, are thick, continuous and contain some of the highest gas contents of any coals in the Alberta Plains. Typically six or more seams with cumulative coal thickness ranging from 2 to 14 meters occur over a stratigraphic interval of 40 to 100 meters. The thickest coals extend from southeast Grande Prairie in a widening wedge between Edmonton and Calgary to the Coronation area with coals occurring at depths ranging from about 800 meters to 2800 meters.

Upper Cretaceous through Tertiary-aged coal also occurs across the Plains with older coals being overlain by progressively younger rocks and coals. Three coal zones are recognized within the Upper Cretaceous Belly River Group: the McKay Coal Zone, near the base of the Belly River Group; the Taber Coal Zone, located in the middle; and the Lethbridge Coal Zone, at the top of the Belly River Group. Compared to the Mannville coals, the overall thin coals and restricted lateral continuity of the Belly River Group coal seams have resulted in limited exploration efforts in these coals.

The rank of coal in Alberta ranges from very low (lignite) to high (anthracite). Coal near the surface in the Plains is generally of sub-bituminous rank with lignite occurring in the north and northeast part of the Plains, and high volatile bituminous C in the northwest and southwest areas of the Plains. Coal rank increases with burial depth. In the Plains, coal rank increases towards the west as seams dip and become progressively deeper toward the mountains. With increasing depth also comes increasing overburden pressure, which may restrict permeability.

To date, Horseshoe Canyon coals with relatively low gas contents, but with favourable fracturing are being successfully exploited for unconventional production in the south-central plains. Mannville coals are showing potentially favourable amounts of fracturing and high gas contents in some locations are undergoing evaluation in the north central to central plains.

Exploration History and Geology of the Southeast Alberta Properties

Atlee- Buffalo

The Atlee-Buffalo land parcel A0350 4-08-023 6 is located in Section 6, Township 23, Range 8 West of the 4th Meridian and is approximately sixty miles north of Medicine Hat, Alberta, Canada. The land contains one abandoned well 6-6-23-8W4 which was drilled and the rig released on 1989-08-27 with total depth (TD) to the Banff formation of the Mississippian age. Shallow Milk River stringers run from 1090 to 1340 feet in depth. The Company owns all P&NG rights and there has been no production to date. The offset wells at 16-36-22-9W4 and 6-31-22-8W4 are producing from the Milk River formation at a current rate of 10 to15 and 25 to 30 mcf/d (thousand cubic feet per day) respectively. Regionally, production in the area has been from the Belly River, Colorado, Medicine Hat, and Second White Specks zones.

21

Bow Island

The two Bow Island land parcels A0027 4-10-010 23 and A0617 4-10-010-36 are located in Sections 23 and 25 both in Township 10, Range 10 West of the 4th Meridian and are approximately twenty miles southwest of Medicine Hat, Alberta, Canada. Section 23 contains one abandoned well while no wells have been drilled on section 25. The Company owns all P&NG rights and there has been no production from the lands to date. The abandoned well 7-23-10-10W4 was drilled and rig released on 1990-01-25 with TD in the Madison horizon.

The Bow Island formation, at 2486 to 2493 feet and from 2630 to 2650 feet, was identified as having potential production. The formation has been damaged and will require fracturing.

Regionally, production in the area has been from the Milk River, Medicine Hat and Second White Specks in the vicinity of the Company lands and as these are generally blanket sands should be considered for future development. New drilling in the region has been to the Sawtooth formation.

Eyremore

The two Eyremore land parcels A0041 4-18-017 20 and A0042 4-18-017-21 are located in Sections 20 and 21 in Township 18 Range 17 West of the 4th Meridian and are approximately forty-eight miles north of Lethbridge, Alberta, Canada. The two land parcels contain a total of eight producing gas wells which are producing from above the base of the Mannville formation. These eight wells are not Company gas wells as the lands acquired contain P&NG rights below the base of the Mannville. All new wells that have their productive formation identified are producing from zones that are above the base of the Mannville.

Retlaw

The Retlaw land parcel A0407 4-18-014 09 is located in Section 9 Township 14 Range 18 West of the 4th Meridian and is approximately thirty miles northeast of Lethbridge, Alberta, Canada. The Company acquired P&NG rights below the base of the Mannville. The section contains one abandoned and one producing gas well however neither well penetrates to the zones acquired.

Regionally, production has been from the Mannville, Belly River, Arcs, Nisku, and Glaucautic zones.

Taber

The Taber land parcel A0613 4-16-009 22 is located in Section 22 Township 9 Range 16 West of the 4th Meridian and is located approximately thirty miles east of Lethbridge, Alberta, Canada. The land has one abandoned well 5-22-9-16W4 which was drilled and rig released on 1942-11-22. The existing logs are too old to be useful. The Company owns all P&NG rights. Regionally, newly drilled wells are located in a major Mannville field to the west of the Company land and have had production from the Mannville and Sawtooth formations.

22

Current State of Exploration

The Company has not undertaken any drilling on its properties. There are abandoned wells on the Company’s properties drilled by former property owners. In addition, there are producing wells on the Company’s properties but all production from these wells is owned by other companies as the production is from zones whose rights have been leased by other enterprises. Drill log information from wells drilled on adjacent properties is publicly available. The Company has only recently begun its review of these data.

Geological Exploration Program

The Province of Alberta maintains a significant publicly-available database of drilling information from all wells drilled under leases issued by the provincial government. Companies who drill on government land in Alberta are required to submit their drill results to the province. Therefore, previous drilling undertaken on land adjacent to the Company’s holding, or drilling on the Company’s land by companies exploring for other resources (oil sands for example) are required to submit their drill log data to the Alberta government. As a result, there is a large database of drill results available to the public. The Company has only recently begun its initial review of the publicly available data to determine the potential of its properties for exploration. The Company intends to undertake a more comprehensive review of this drill log data from surrounding properties in order to gain a better understanding of the exploration potential of its properties. The Company does not currently have agreements in place with qualified geologists who can undertake this review. Currently, the Company is attempting to engage consultants to perform the reviews.

The review of the data will include preparing detailed geological maps using existing drill log data with the aim of identifying potential drill targets and to obtain a better understanding of potential strategies for acquiring new land holdings. The Company will not undertake any drilling in 2010, as the review of available information will take between twelve to eighteen months to complete commencing January 2010. Therefore, the Company is not expecting to undertake any drilling until at least 2011.

Saskatchewan Properties

Acquisition of Interests

On April 12, 2010 the Company acquired an interest in two PN&G Leases (the “Leases”) in the province of Saskatchewan. Including fees and closing costs the rights to the Leases were acquired for an aggregate $9,873 and the purchase price includes the first year’s aggregate annual lease payments of $372. The total area covered by the Registrant’s portion of the Leases is 132 hectares. The interests in the Leases were acquired through a public land sale process held on a regular basis by the Saskatchewan provincial government. Upon being notified that it has submitted the highest bid for a specific land parcel the Company immediately pays the government the bid price and enters into a formal lease with the government. The term of the Leases is for 5 years, requires minimum annual lease payments, and grants the Company the right to explore for potential petroleum and natural gas opportunities on the respective lease.

23

Description and Location of the Saskatchewan Properties

The Company has acquired the following leases:

|

Date

|

Location

|

Number of Leases

|

Land Area

(Hectares)

|

Annual Lease Payments

|

|

April 12, 2010

|

SW 6 12 30 1

|

1

|

67.17

|

CDN $202 / USD $189

|

|

April 12, 2010

|

NW 22 14 30 1

|

1

|

64.75

|

CDN $194 / USD $183

|

|

7

|

131.92

|

CDN $396 / USD $372

|

Both of the properties are located in the Estevan area of Southeastern Saskatchewan, Canada.

Exploration History and Geology of the Saskatchewan Properties

The geology of Saskatchewan can be divided into two main geological regions, the Precambrian Canadian Shield and the Phanerozoic Western Canadian Sedimentary Basin. Within the Precambrian shield exists the Athabasca sedimentary basin. Meteorite impacts have altered the natural geological formation processes. The prairies were most recently affected by glacial events in the Quaternary period. The Bakken Formation is present over a large portion of southeastern Saskatchewan and ranges in thickness from zero to 30 m but is locally over 70 m thick when associated with salt collapse structures. It is subdivided into three members characterized by a middle siltstone to sandstone unit sandwiched between black organic-rich shales. In southeastern Saskatchewan, the Late Devonian to Early Misssissippian Bakken Formation is conformably overlain by grey, fossiliferous limestones of the Souris Valley (Lodgepole) Formation of Mississippian (Kinderhookian) age. There have been no wells drilled on the Company’s Saskatchewan properties.

Current State of Exploration

The Company has not undertaken any exploration or drilling on its properties. There are no known resources or reserves of oil or natural gas on the Company’s properties.

Geological Exploration Program

The Province of Saskatchewan maintains a significant publicly-available database of drilling information from all wells drilled under leases issued by the provincial government. Companies who drill on government land in Saskatchewan are required to submit their drill results to the province. Therefore, previous drilling undertaken on land adjacent to the Company’s holding, or drilling on the Company’s land by companies exploring for other resources (oil sands for example) are required to submit their drill log data to the Saskatchewan government. As a result, there is a large database of drill results available to the public. The Company intends to focus on its Southeast Alberta properties in the short term and as a result does not intend to undertake any significant exploration work on its Saskatchewan properties until at least 2011.

24

Alberta Well Interest

Acquisition of Interest

On April 12, 2010 the Company executed a Sale and Conveyance Agreement (the “Agreement”) with 966749 Alberta Corp. (the “Vendor”) for the acquisition of a 2.51255% working interest in an oil well located in Alberta, Canada. Under the Agreement the Company paid the Vendor $6,043 including taxes and closing costs. The underlying property lease is with the Alberta provincial government.

Description and Location of the Alberta Well Interest

The underlying lease with the Alberta government is Crown Lease 0587090167 and is located at Township 49, Range 15 W5M: 7 with the well known as Apex et al Peco 100/06-07-049-15W5/00 (the “Well”). The Well is located approximately 30 miles from Edson, Alberta, Canada.

Exploration History of the Alberta Well Interest

The Well was initially drilled in 1998 and re-entered by Apex Energy (Canada) Inc. (”Apex”) in November 2003. To date there has been only minimal production from the well and currently the Well is not in production. Apex was the original operator but currently Harness Petroleum Inc. (“Harness”) the operator of the Well.

Current State of Exploration

To date there has been only minimal production from the well and currently the Well is not in production.

Geological Exploration Program

Harness is currently assessing the potential for future development of the Well.

Item 3. Legal Proceedings.