Attached files

| file | filename |

|---|---|

| 8-K/A - BTHC XV, INC. - BTHC XV, Inc. | bthcxv8ka120610.htm |

Long Fortune Valley Tourism International Limited

Form 10-Q Disclosure Information

for the Quarterly Period Ended September 30, 2010

Table of Contents

|

Page

|

|

|

PART I – FINANCIAL INFORMATION

|

1

|

|

Item 1. Financial Statements (Unaudited)

|

1

|

|

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

|

19

|

|

Item 3. Quantitative and Qualitative Disclosure About Market Risk

|

31

|

|

Item 4. Controls and Procedures

|

31

|

|

PART II - OTHER INFORMATION

|

32

|

|

Item 1. Legal Proceedings.

|

32

|

|

Item 1A Risk Factors.

|

33

|

i

PART I – FINANCIAL INFORMATION

Long Fortune Valley Tourism International Limited

Condensed Consolidated Balance Sheets

| (US$ amounts expressed in thousands) | September 30, 2010 | December 31, 2009 | ||||||

|

(Unaudited)

|

(Audited)

|

|||||||

| ASSETS | ||||||||

|

|

||||||||

|

Cash and cash equivalents

|

$ | 564 | $ | 1,076 | ||||

|

Receivables, net of allowance for doubtful accounts

|

2,099 | 508 | ||||||

|

Amounts due from related parties

|

13,986 | 4,778 | ||||||

|

Short term prepaid rent

|

24 | 24 | ||||||

|

Total current assets

|

16,673 | 6,386 | ||||||

|

Property, plant and equipment, net of accumulated depreciation

|

11,774 | 9,925 | ||||||

|

Land occupancy rights

|

327 | 71 | ||||||

|

Long term prepaid rent

|

174 | 179 | ||||||

|

Long term investment

|

301 |

-

|

||||||

|

Total assets

|

$ | 29,249 | $ | 16,561 | ||||

|

LIABILITIES AND SHAREHOLDERS’ EQUITY

|

||||||||

|

Current liabilities:

|

||||||||

|

Accounts payable

|

$ | 94 | $ | 737 | ||||

|

Accrued expenses and other liabilities

|

43 | 76 | ||||||

|

Short-term loans

|

10,297 | 2,490 | ||||||

|

Total current liabilities

|

10,434 | 3,303 | ||||||

|

Shareholders’ equity:

|

||||||||

|

Share capital - $1 par value, authorized 50,000 shares; issued 1,000 shares

|

1 | 1 | ||||||

|

Additional paid in capital

|

967 | 967 | ||||||

|

Accumulated other comprehensive income

|

762 | 472 | ||||||

|

Retained earnings

|

17,085 | 11,818 | ||||||

|

Total shareholders’ equity

|

18,815 | 13,258 | ||||||

|

Total liabilities and shareholders’ equity

|

$ | 29,249 | $ | 16,561 | ||||

See accompanying notes to condensed consolidated financial statements.

1

Long Fortune Valley Tourism International Limited

Condensed Consolidated Statements of Operations

|

|

Three months ended |

Nine months ended

|

|||||||||||||||

| September 30, |

September 30,

|

||||||||||||||||

|

(US$ amounts expressed in thousands)

|

(unaudited) |

(unaudited)

|

|||||||||||||||

|

2010

|

2009

|

2010

|

2009

|

||||||||||||||

|

|

|

|

|

|

|||||||||||||

|

Revenues

|

$ | 3,444 | $ | 3,068 | $ | 8,159 | $ | 7,777 | |||||||||

|

Costs and expenses

|

(620 | ) | (673 | ) | (2,237 | ) | (2,109 | ) | |||||||||

|

Operating income

|

2,824 | 2,395 | 5,922 | 5,668 | |||||||||||||

|

Other income (Expense)

|

(104 | ) | 12 | (203 | ) | 19 | |||||||||||

|

Income before income taxes

|

2,720 | 2,407 | 5,719 | 5,687 | |||||||||||||

|

Income tax expense

|

(166 | ) | (153 | ) | (452 | ) | (498 | ) | |||||||||

|

Net income

|

$ | 2,554 | $ | 2,254 | $ | 5,267 | $ | 5,189 | |||||||||

|

|

|

||||||||||||||||

|

Other comprehensive income - Foreign Translation Adjustment

|

212 | 4 | 290 | 17 | |||||||||||||

|

Comprehensive income

|

$ | 2,766 | $ | 2,258 | $ | 5,557 | $ | 5,206 | |||||||||

See accompanying notes to condensed consolidated financial statements.

2

Long Fortune Valley Tourism International Limited

Condensed Consolidated Statements of Stockholders’ Equity

|

(US$ amounts expressed in thousands)

|

Share

Capital

|

Additional

paid in

capital

|

Retained

Earnings

|

Accumulated

Other

Comprehensive

Income

|

Total

Equity

|

|||||||||||||||

|

Balances at Dec 31, 2009

|

$ | 1 | $ | 967 | $ | 11,818 | $ | 472 | $ | 13,258 | ||||||||||

|

Net income

|

|

|

5,267 |

|

5,267 | |||||||||||||||

|

Translation adjustments

|

|

|

290 | 290 | ||||||||||||||||

|

Balances at September 30, 2010

|

$ | 1 | $ | 967 | $ | 17,085 | $ | 762 | $ | 18,815 | ||||||||||

See accompanying notes to condensed consolidated financial statements.

3

Long Fortune Valley Tourism International Limited

Condensed Consolidated Statements of Cash Flows

|

Nine months ended September 30,

|

||||||||

|

(US$ amounts expressed in thousands)

|

(Unaudited)

|

|||||||

|

2010

|

2009

|

|||||||

|

Cash flows from operating activities:

|

||||||||

|

Net income

|

$ | 5,267 | $ | 5,189 | ||||

|

Depreciation expense

|

563 | 440 | ||||||

|

Amortization expense

|

5 | 3 | ||||||

|

(Increase)/decrease in other receivable

|

(1,591 | ) | (107 | ) | ||||

|

Increase/(decrease) in accounts payable

|

(644 | ) | (167 | ) | ||||

|

Increase/(decrease) in accrued expenses and other liabilities

|

(33 | ) | 15 | |||||

|

Net cash provided by operating activities

|

3,567 | 5,373 | ||||||

|

|

|

|||||||

|

Cash flows from investing activities:

|

|

|||||||

|

Cash paid for purchase of fixed assets and intangible assets

|

(2,645 | ) | (1,943 | ) | ||||

|

Long term investment

|

(301 | ) |

|

|||||

|

Amounts due from related parties

|

(9,208 | ) | (2,062 | ) | ||||

|

Net cash used in investing activities

|

(12,154 | ) | (4,005 | ) | ||||

|

|

|

|||||||

|

Cash flows from financing activities:

|

|

|||||||

|

Proceeds from loans

|

7,807 | 586 | ||||||

|

Cash paid for reduction of capital

|

- | (1,271 | ) | |||||

|

Net cash provided by (used in) financing activities

|

7,807 | (685 | ) | |||||

|

|

|

|||||||

|

Effect of foreign exchange rate changes

|

268 | 15 | ||||||

|

|

|

|||||||

|

Net increase (decrease) in cash and cash equivalents

|

(512 | ) | 698 | |||||

|

Cash and cash equivalents at beginning of period

|

1,076 | 57 | ||||||

|

Cash and cash equivalents at end of period

|

$ | 564 | $ | 755 | ||||

|

|

|

|||||||

|

Supplemental information:

|

|

|||||||

|

Income taxes paid

|

$ | 452 | $ | 498 | ||||

|

Interest paid

|

$ | 268 | $ | 15 | ||||

See accompanying notes to condensed consolidated financial statements.

4

Long Fortune Valley Tourism International Limited

Notes to Condensed Consolidated Financial Statements

(Unless the context requires otherwise, US$ amounts expressed in thousands)

1. Organization and nature of operations

Organization

Long Fortune Valley Tourism International Limited (the “Company”) was incorporated on December 9, 2009 as an exempted company limited by shares in the Cayman Islands. The Company is an investment holding company. Its registered office is located at the offices of Harneys Services (Cayman) Limited, 4th Floor, Genesis Building, 13 Genesis Close, P.O. Box 10240, Grand Cayman, Cayman Islands, KY1-1002. The Company’s principal subsidiary, Shandong Longkong Travel Management Co., Ltd. (formerly known as Shandong Longkong Travel Development Co., Ltd.) (“Longkong”), operates its business in Linyi City, Yishui County, Shandong Province, PRC.

Pursuant to a group reorganization (the “Reorganization”) to rationalize the structure of the Company and its subsidiaries (hereinafter, collectively referred to as the “Group”) in preparation for the proposed listing of the Company’s shares, the Company acquired all the equity interests of the subsidiaries from its ultimate shareholders, thereby becoming the holding company of the subsidiaries comprising the Group after the Reorganization. The Group resulting from the Reorganization is regarded as a continuing entity as the Group is ultimately controlled by the same parties both before and after the Reorganization. Accordingly, the condensed consolidated balance sheets at September 30, 2009 have been prepared using the principles of merger accounting. The condensed consolidated statements of operations, condensed statements of stockholder’s equity and condensed statements of cash flows for the nine months ended September 30, 2009 have been prepared on a combined basis as if the current structure had been in existence throughout the nine months ended September 30, 2009.

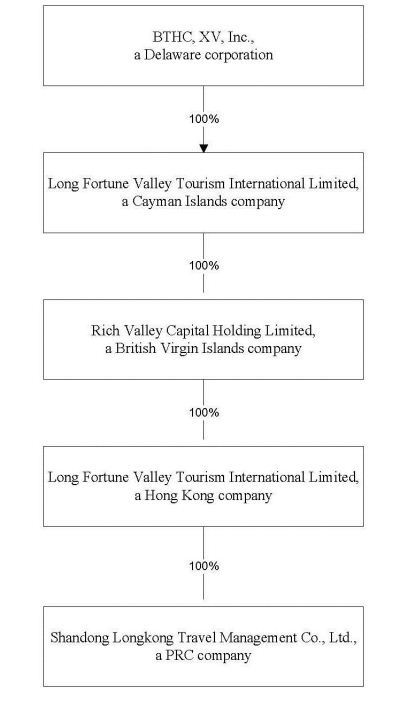

As of September 30, 2010, the Company holds 100% of the equity interests in Rich Valley Capital Holdings Limited, a company incorporated in the British Virgin Islands, which holds 100% of the equity interests in Long Fortune Valley Tourism International Limited, a company incorporated in Hong Kong, which holds 100% of the equity interests in Longkong. The following is an organizational chart of the Group as of September 30, 2010:

5

Long Fortune Valley Tourism International Limited

Notes to Condensed Consolidated Financial Statements

(Unless the context requires otherwise, US$ amounts expressed in thousands)

Nature of operations

The business scope of Longkong is tourism management. The key business project is a cave named the “Underground Grand Canyon” that is located in Linyi City, Yishui County, Shandong Province, PRC. In April 2004, Longkong signed a contract with the local government regarding the development and management of the “Underground Grand Canyon” from April 2, 2004 to October 15, 2062.

6

Long Fortune Valley Tourism International Limited

Notes to Condensed Consolidated Financial Statements

(Unless the context requires otherwise, US$ amounts expressed in thousands)

2. Significant accounting policies

Basis of presentation

The consolidated financial statements of the Group have been prepared in accordance with the accounting principles generally accepted in the United States of America (“US GAAP”).

Basis of consolidation

The consolidated financial statements include the financial statements of the Company and its subsidiaries. All inter-company transactions and balances have been eliminated upon consolidation.

Use of Estimates

The preparation of financial statements in conformity with US GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and the disclosures of contingent assets and liabilities at the date of the financial statements, and the reported amounts of revenues and expenses during the reporting periods. Actual results could differ from those estimates.

Cash and cash equivalents

Cash and cash equivalents include interest bearing and non-interest bearing bank deposits, money market accounts, and short-term certificates of deposit with original maturities of three months or less.

Allowance for doubtful accounts

The Group provides an allowance for doubtful accounts equal to the amount of estimated uncollectible accounts. The Group’s estimates are based on historical collection experience and a review of the current status of accounts receivable and advances to suppliers. It is reasonably possible that the Group’s estimate of the allowance for doubtful accounts will change. Accounts receivable and advances to suppliers are presented net of the allowance for doubtful accounts.

Property, plant and equipment, net

Property, plant and equipment are recorded at cost and are stated net of accumulated depreciation. Depreciation expense is calculated using the straight-line method over the estimated useful lives of the assets, taking into account the estimated residual value. The estimated useful lives are as follows:

|

Building

|

20 years

|

|

|

Machinery and equipment

|

10 years

|

|

|

Motor vehicle

|

5 years

|

|

|

Office equipment

|

5 years

|

Maintenance and repairs are charged directly to expense as incurred, whereas betterments and renewals are generally capitalized in their respective property accounts. When an item is retired or otherwise disposed of, the cost and applicable accumulated depreciation are removed and the resulting gain or loss is recognized and reflected in current operations. For all periods presented in the statement of operations and comprehensive income, certain labor charges normally capitalized were charged to operating expenses as the Group was unable to adequately separate these costs.

Construction in progress

Construction in progress represents property and equipment under construction. No depreciation is recorded in respect of construction in progress. Construction in progress is transferred to property and equipment, and depreciation of the asset commences, when the asset has been substantially completed and is ready for its intended use.

Land use right, net

Land use right is recorded at cost less accumulated amortization. Amortization is provided over the term of the land use right agreement on a straight-line basis over the term of the agreement, which is 30 years.

7

Long Fortune Valley Tourism International Limited

Notes to Condensed Consolidated Financial Statements

(Unless the context requires otherwise, US$ amounts expressed in thousands)

Impairment of long-lived assets

The carrying values of the Group’s long-lived assets are reviewed for impairment whenever events or changes in circumstances indicate that they may not be recoverable. When such an event occurs, the Group projects the undiscounted cash flows to be generated from the use of the asset and its eventual disposition over the remaining life of the asset. If projections indicate that the carrying value of the long-lived asset will not be recovered, the carrying value is reduced by the estimated excess of the carrying value over the projected discounted cash flows.

Revenue Recognition

The Group recognizes revenue when it is realized and earned. The Group considers revenue realized and earned when (1) it has persuasive evidence of an arrangement, (2) service has occurred, (3) the sales price is fixed or determinable, and (4) collectability is reasonably assured.

Operating leases

Leases in which substantially all the rewards and risks of ownership of the asset remain with the lessor are accounted for as operating leases. Payments made under operating leases are charged to the statements of operations on a straight-line basis over the shorter of the lease term or estimated useful life.

Foreign currency transactions and translation

The Company uses the U.S. dollar as its functional currency and Renminbi (“RMB”), the national currency of China, as the functional currency of Longkong.

Longkong translates assets and liabilities into U.S. dollars using the rate of exchange prevailing at the balance sheet date, and the consolidated statements of operations are translated at average rates during the reporting periods. Adjustments resulting from the translation of financial statements from RMB into U.S. dollars are recorded in shareholders’ equity as part of accumulated other comprehensive income/(loss). Gains or losses resulting from transactions in currencies other than RMB are reflected in income for the reporting periods.

Fair value

When determining the fair value measurements for assets and liabilities required or permitted to be recorded at fair value, the Group considers the principal or most advantageous market in which it would transact business and considers assumptions that market participants would use when pricing the asset or liability, such as inherent risk, transfer restrictions, and risk of nonperformance. The Group uses the following three levels of inputs in determining the fair value of the Group’s assets and liabilities, focusing on the most observable inputs when available:

Level 1 applies to assets or liabilities for which there are quoted prices in active markets for identical assets or liabilities.

Level 2 applies to assets or liabilities for which there are inputs other than quoted prices included within Level 1 that are observable for the asset or liability such as quoted prices for similar assets or liabilities in active markets; quoted prices for identical assets or liabilities in markets with insufficient volume or infrequent transactions (less active markets); or model-derived valuations in which significant inputs are observable or can be derived principally from, or corroborated by, observable market data.

Level 3 applies to assets or liabilities for which there are unobservable inputs to the valuation methodology that are significant to the measurement of the fair value of the assets or liabilities.

The Group did not have any financial assets and liabilities or nonfinancial assets and liabilities that are measured at fair value on a recurring basis as of September 30, 2010.

Fair value of financial instruments

The Group’s financial instruments consist primarily of cash and cash equivalents and short-term borrowings. The fair value of these financial instruments approximate their carrying amounts reported in the balance sheets due to the short-term maturity of these instruments.

8

Long Fortune Valley Tourism International Limited

Notes to Condensed Consolidated Financial Statements

(Unless the context requires otherwise, US$ amounts expressed in thousands)

Income taxes

Deferred income taxes are recognized for temporary differences between the tax basis of assets and liabilities and their reported amounts in the financial statements, net of operating loss carry forwards and credits, by applying enacted statutory tax rates applicable to future years. Deferred tax assets are reduced by a valuation allowance when, in the opinion of management, it is more likely than not that some portion or all of the deferred tax assets will not be realized. Current income taxes are provided for in accordance with the laws of the relevant taxing authorities.

In July 2006, the Financial Accounting Standards Board (“FASB”) issued Financial Interpretation (FIN) 48, Accounting for Uncertainty in Income Taxes—an Interpretation of FASB 109 (“FIN 48”). The Group adopted the provisions of FIN 48, which did not have a material impact on its operating results, financial position or cash flows.

Advertising costs

The Group expenses advertising costs as incurred. Total advertising expenses were US$393 and US$289 during the nine months ended September 30, 2009 and 2010, respectively, and have been included as part of Costs and expenses.

Comprehensive income

Comprehensive income includes net income and foreign currency translation adjustments. Comprehensive income is reported as a component of the consolidated statements of shareholders’ equity.

Recent Accounting Pronouncements adopted

In June 2009, the FASB issued the Accounting Standards Codification (“Codification”). Effective July 1, 2009, the Codification is the single source of authoritative accounting principles recognized by the FASB to be applied by nongovernmental entities in the preparation of financial statements in conformity with US GAAP. The Codification is intended to reorganize, rather than change, existing US GAAP. Accordingly, all references to currently existing US GAAP have been removed and have been replaced with plain English explanations of the Group’s accounting policies. The adoption of the Codification did not have a material impact on the Group’s financial position or results of operations.

In May 2009, the FASB revised the authoritative guidance for subsequent events, which establishes general standards of accounting for and disclosure of events that occur after the balance sheet date but before financial statements are issued or are available to be issued. This guidance was effective for financial statements issued for interim and annual reporting periods ending after June 15, 2009. We adopted this guidance for the period ended June 30, 2009, and have provided the disclosures required for the period ended September 30, 2010.

Recent Accounting Pronouncements not yet adopted

In October 2009, the FASB issued Update No. 2009-13, which amends the Revenue Recognition topic of the Codification. This update provides amendments to the criteria in Subtopic 605-25 of the Codification for separating consideration in multiple-deliverable arrangements. As a result of those amendments, multiple-deliverable arrangements will be separated in more circumstances than under existing US GAAP. The amendments establish a selling price hierarchy for determining the selling price of a deliverable and will replace the term fair value in the revenue allocation guidance with selling price to clarify that the allocation of revenue is based on entity-specific assumptions rather than assumptions of a marketplace participant. The amendments will also eliminate the residual method of allocation and require that arrangement consideration be allocated at the inception of the arrangement to all deliverables using the relative selling price method and will require that a vendor determine its best estimate of selling price in a manner that is consistent with that used to determine the price to sell the deliverable on a standalone basis. These amendments will be effective prospectively for revenue arrangements entered into or materially modified in fiscal years beginning on or after June 15, 2010, with early adoption permitted. We are currently evaluating the impact that the adoption of this update might have on our results of operations and financial condition.

9

Long Fortune Valley Tourism International Limited

Notes to Condensed Consolidated Financial Statements

(Unless the context requires otherwise, US$ amounts expressed in thousands)

3. Property, plant and equipment, net

Property, plant and equipment consisted of the following:

|

September 30,

|

December 31,

|

|||||||

|

2010

|

2009

|

|||||||

|

(Unaudited)

|

||||||||

|

Building

|

$ | 10,352 | $ | 10,141 | ||||

|

Machinery and equipment

|

568 | 527 | ||||||

|

Motor vehicle

|

884 | 832 | ||||||

|

Office equipment

|

144 | 128 | ||||||

| 11,948 | 11,628 | |||||||

|

Less: Accumulated depreciation

|

(2,899 | ) | (2,336 | ) | ||||

|

Property, plant and equipment, net

|

9,049 | 9,292 | ||||||

|

Construction in progress

|

2,725 | 633 | ||||||

| $ | 11,774 | $ | 9,925 |

4. Land occupancy rights

|

September 30,

|

December 31,

|

|||||||

|

2010

|

2009

|

|||||||

|

(Unaudited)

|

(Audited)

|

|||||||

|

Land occupancy rights

|

$ | 339 | $ | 78 | ||||

|

Less: Accumulated amortization

|

(12 | ) | (7 | ) | ||||

|

Land occupancy rights, net

|

$ | 327 | $ | 71 |

5. Long term investment

During the nine months ended September 30, 2010, Longkong acquired a less than 1% interest in Yishui Rural Credit Cooperative (“Yishui Credit”), which is a financial institution located in Yishui County, Shandong Province. Because the Group owns a less than 1% interest and has no representation on Yishui Credit’s board of directors, the Group’s management concluded that the Group could not exercise significant influence over the operating and financial policies of Yishui Credit. Accordingly, the cost method is used to account for the investment.

10

Long Fortune Valley Tourism International Limited

Notes to Condensed Consolidated Financial Statements

(Unless the context requires otherwise, US$ amounts expressed in thousands)

6. Short-term loans

The following table reflects the balance of short-term loans at September 30, 2010 and December 31, 2009:

|

|

Maturity date

|

Interest rate

|

As of September 30, 2010

(unaudited)

|

As of December 31, 2009

(audited)

|

||||||||||

|

Industrial and Commercial Bank of China Yishui Branch

|

04/28/2010

|

7.97 | % | $ | -- | $ | 293 | |||||||

|

Bank of China Yishui Branch

|

10/27/2010

|

5.38 | % | 2,239 | 2,197 | |||||||||

|

Industrial and Commercial Bank of China Yishui Branch

|

10/15/2010

|

5.83 | % | 746 | -- | |||||||||

|

Yishui Rural Credit Cooperative

|

01/08/2011

|

10.62 | % | 448 | -- | |||||||||

|

Yishui Rural Credit Cooperative

|

04/20/2011

|

10.62 | % | 895 | -- | |||||||||

|

Yishui Rural Credit Cooperative

|

04/26/2011

|

11.15 | % | 448 | -- | |||||||||

|

Yishui Rural Credit Cooperative

|

04/26/2011

|

5.31 | % | 298 | -- | |||||||||

|

Yishui Rural Credit Cooperative

|

05/20/2011

|

10.62 | % | 1,492 | -- | |||||||||

|

Bank of Linshang

|

05/28/2011

|

7.97 | % | 746 | -- | |||||||||

|

China Construction Bank Yishui Branch

|

07/24/2011

|

5.84 | % | 895 | -- | |||||||||

|

China Construction Bank Yishui Branch

|

08/01/2011

|

5.84 | % | 597 | -- | |||||||||

|

Industrial and Commercial Bank of China Yishui Branch

|

9/15/2011

|

6.37 | % | 1,045 | -- | |||||||||

|

Industrial and Commercial Bank of China Yishui Branch

|

09/28/2011

|

5.84 | % | 448 | -- | |||||||||

| $ | 10,297 | $ | 2,490 | |||||||||||

The weighted average interest rate for short-term loans as of September 30, 2010 and December 31, 2009 was 7.48% and 5.68%, respectively.

As of September 30, 2010, the short-term loans are secured by guarantees provided by related parties, as well as the pledge by Longkong of its operation fee charging rights and its interest in real property. Refer to Note 8 - Related-party transactions.

11

Long Fortune Valley Tourism International Limited

Notes to Condensed Consolidated Financial Statements

(Unless the context requires otherwise, US$ amounts expressed in thousands)

7. Income tax

Cayman Islands and British Virgin Islands

Under the current laws of the Cayman Islands and the British Virgin Islands, the members of the Group that are incorporated in the Cayman Islands and the British Virgin Islands are not subject to income taxes.

PRC

The local competent tax authorities collect enterprise tax from Longkong through verification collection. According to PRC law, if an enterprise satisfies certain conditions it may be eligible to pay its enterprise tax through verification collection. Conditions include: (i) the enterprise is not required to establish accounting books under relevant laws and administrative regulations; (ii) the enterprise is required to establish accounting books under relevant laws and administrative regulations but fails to do so; (iii) the enterprise illegally destroys the accounting books or refuses to provide tax paying references; (iv) the enterprise has established accounting books but it is difficult to audit such books because the accounts are in disorder or the cost references, income vouchers and expenditure vouchers are incomplete; (v) the enterprise fails to file a tax return for a tax obligation within the prescribed time limit and refuses to file a tax return even after the taxing authority orders it to do so within a time limit; or (vi) the enterprise reports an obviously low tax basis without any justifiable reason. Upon the satisfaction of these conditions, the taxing authorities, on the basis of the circumstance of a taxpayer subject to verification collection, verify the enterprise’s taxable income rate or income tax liability. The taxing authorities may verify the enterprise income tax to be collected through the following approaches: (i) by referring to the tax burden on local taxpayers in the same or similar industry and with approximate business scale and income level; (ii) by referring to the amount of taxable income or the amount of costs and expenses; (iii) on the basis of calculation and inference or measurement of consumed raw materials, fuel, energy, etc.; or (iv) through other reasonable approaches. Longkong has obtained receipts from the local competent tax authorities indicating that it has paid all taxes in full for the nine months ended September 30, 2010 and 2009.

8. Related-party transactions

(1) Outstanding balances with related parties are as follows:

|

|

Amounts due from related parties

|

|||||||

|

September 30,

2010

|

December 31, 2009

|

|||||||

|

(Unaudited)

|

(Audited)

|

|||||||

|

US$

|

US$

|

|||||||

|

Yishui Underground Fluorescent Lake Travel Development Co., Ltd.

|

Controlled by Zhang Shanjiu’s immediate family – Note 8(a)

|

5,467 | 4,778 | |||||

|

Mr. Zhang Shanjiu

|

Director – Note 8(b)

|

2 | - | |||||

|

Mr. Yu Xinbo

|

Director – Note 8(b)

|

5 | - | |||||

|

Mr. Chen Rongguang

|

Director – Note 8(b)

|

1 | - | |||||

|

Junan Tianma Island Travel Development Co., Ltd.

|

Controlled by Zhang Shanjiu – Note 8(c)

|

619 | - | |||||

|

Yishui Yinhe Travel Development Co., Ltd.

|

Zhang Shanjiu, as an investor, has significant influence over the entity – Note 8(d)

|

7,892 | - | |||||

| 4,778 | ||||||||

| 13,986 | ||||||||

12

Long Fortune Valley Tourism International Limited

Notes to Condensed Consolidated Financial Statements

(Unless the context requires otherwise, US$ amounts expressed in thousands)

As of September 30, 2009, amounts due from related parties were unsecured and carried interest rates between 5.38% and 9.6% per annum.

Notes:

|

a.

|

The details of loans to Yishui Underground Fluorescent Lake Travel Development Co., Ltd. (“Fluorescent Lake”) at September 30,2010 are:

|

|

Date of loan

|

Due date

|

Interest

|

Amount

|

|||

|

11/30/09

|

11/29/10

|

free of interest

|

1,792

|

|||

|

11/27/09

|

10/27/10

|

free of interest

|

2,238

|

|||

|

12/16/09

|

12/15/10

|

free of interest

|

839

|

|||

|

01/08/10

|

01/07/11

|

free of interest

|

1

|

|||

|

01/09/10

|

01/08/11

|

free of interest

|

2

|

|||

|

02/03/10

|

02/02/11

|

free of interest

|

23

|

|||

|

03/02/10

|

03/01/11

|

free of interest

|

75

|

|||

|

03/31/10

|

03/30/11

|

free of interest

|

10

|

|||

|

04/01/10

|

03/31/11

|

free of interest

|

12

|

|||

|

04/02/10

|

04/01/11

|

free of interest

|

15

|

|||

|

04/03/10

|

04/02/11

|

free of interest

|

25

|

|||

|

04/11/10

|

04/10/11

|

free of interest

|

7

|

|||

|

04/12/10

|

04/11/11

|

free of interest

|

22

|

|||

|

04/13/10

|

04/12/11

|

free of interest

|

7

|

|||

|

04/23/10

|

04/22/11

|

free of interest

|

60

|

|||

|

04/26/10

|

04/25/11

|

free of interest

|

149

|

|||

|

07/06/10

|

07/06/11

|

free of interest

|

7

|

|||

|

07/19/10

|

07/19/11

|

free of interest

|

18

|

|||

|

08/25/10

|

08/25/11

|

free of interest

|

45

|

|||

|

09/01/10

|

09/01/11

|

free of interest

|

75

|

|||

|

09/17/10

|

09/17/11

|

free of interest

|

6

|

|||

|

09/20/10

|

09/20/11

|

free of interest

|

30

|

|||

|

09/21/10

|

09/21/11

|

free of interest

|

9

|

|||

|

5,467

|

Longkong generally executes written agreements with Fluorescent Lake, unless the dollar amount of the loan is less than $150,000. These loan agreements provide that the loans are interest free and are due within 12 months of the date of the loan. Periodic payments of principal are not required with respect to these loans.

13

Long Fortune Valley Tourism International Limited

Notes to Condensed Consolidated Financial Statements

(Unless the context requires otherwise, US$ amounts expressed in thousands)

|

b.

|

The parties did not execute written agreements with respect to these loans, which are interest-free, and there was no formal due date for repayment. These loans were repaid in November 2010.

|

|

c.

|

The parties did not execute a written agreement with respect to this loan, which is interest-free, and there is no formal due date for repayment.

|

|

d.

|

The details of loans to Yishui Yinhe Travel Development Co., Ltd. (“Yinhe Travel”) at September 30,2010 are:

|

|

Date of loan

|

Due date

|

Interest

|

Amount

|

||||||||||||

|

01/05/10

|

12/31/10

|

free of interest

|

463 | ||||||||||||

|

01/09/10

|

12/31/10

|

free of interest

|

149 | ||||||||||||

|

01/11/10

|

12/31/10

|

free of interest

|

388 | ||||||||||||

|

04/22/10

|

04/21/11

|

free of interest

|

448 | ||||||||||||

|

04/23/10

|

04/21/11

|

free of interest

|

433 | ||||||||||||

|

05/07/10

|

05/06/11

|

free of interest

|

149 | ||||||||||||

|

05/14/10

|

05/13/11

|

free of interest

|

1,418 | ||||||||||||

|

05/02/10

|

05/21/11

|

free of interest

|

777 | ||||||||||||

|

05/29/10

|

05/28/11

|

free of interest

|

1,493 | ||||||||||||

|

06/05/10

|

06/04/11

|

free of interest

|

149 | ||||||||||||

|

06/07/10

|

06/06/11

|

free of interest

|

198 | ||||||||||||

|

06/09/10

|

06/09/11

|

free of interest

|

56 | ||||||||||||

|

07/08/10

|

07/08/11

|

free of interest

|

75 | ||||||||||||

|

07/12/10

|

07/12/11

|

free of interest

|

224 | ||||||||||||

|

07/12/10

|

07/12/11

|

free of interest

|

75 | ||||||||||||

|

07/30/10

|

07/30/11

|

free of interest

|

313 | ||||||||||||

|

08/11/10

|

08/11/11

|

free of interest

|

119 | ||||||||||||

|

08/11/10

|

08/11/11

|

free of interest

|

149 | ||||||||||||

|

08/12/10

|

08/12/11

|

free of interest

|

70 | ||||||||||||

|

08/13/10

|

08/13/11

|

free of interest

|

746 | ||||||||||||

| 7892 | |||||||||||||||

Longkong generally executes written agreements with Yinhe Travel, which provide that the loans are interest free and are due within 12 months of the date of the loan. Periodic payments of principal are not required with respect to these loans.

(2) Guarantees

The following table lists details of related-party guarantees pursuant to which a related party has executed a Guarantee Contract with Longkong and the creditor to guarantee loans of Longkong:

14

Long Fortune Valley Tourism International Limited

Notes to Condensed Consolidated Financial Statements

(Unless the context requires otherwise, US$ amounts expressed in thousands)

|

Creditor

|

Guarantor

|

Relationship

|

Date of commencement of Guarantee

|

Date of termination of Guarantee

|

Due Date of Loan

|

Loan amount

|

||||

|

Industrial and Commercial Bank of China Yishui branch

|

Zhang Shanjiu and Chen Rongxia (spouse of Zhang Shanjiu)

|

Director

|

05/11/2010

|

10/16/2010

|

10/15/2010

|

746

|

||||

|

Bank of China Yishui branch

|

Yishui Yinhe Travel Development Co., Ltd.

|

Zhang Shanjiu, as an investor, has significant influence over the entity

|

11/17/2009

|

11/17/2012

|

10/27/2010

|

2,239

|

||||

|

Bank of China Yishui branch

|

Junan Tianma Island Travel Development Co., Ltd.

|

Controlled by Zhang Shanjiu

|

11/17/2009

|

11/17/2012

|

10/27/2010

|

2,239

|

||||

|

Bank of China Yishui branch

|

Zhang Shanjiu

|

Director

|

11/17/2009

|

11/17/2012

|

10/27/2010

|

2,239

|

||||

|

Yishui Rural Credit Cooperative

|

Chen Rongguang

|

Director

|

01/31/2009

|

01/30/2011

|

01/08/2011

|

179

|

||||

|

Yishui Rural Credit Cooperative

|

Zhang Shanjiu

|

Director

|

01/09/2010

|

01/08/2011

|

01/08/2011

|

269

|

||||

|

Yishui Rural Credit Cooperative

|

Zhang Shanjiu

|

Director

|

01/09/2010

|

01/08/2011

|

01/08/2011

|

179

|

||||

|

Yishui Rural Credit Cooperative

|

Zhang Shanjiu

|

Director

|

04/21/2010

|

04/20/2011

|

04/20/2011

|

895

|

||||

|

Yishui Rural Credit Cooperative

|

Junan Tianma Island Travel Development Co., Ltd.

|

Controlled by Zhang Shanjiu

|

05/21/2010

|

04/26/2011

|

04/26/2011

|

746

|

||||

|

Yishui Rural Credit Cooperative

|

Zhang Shanjiu

|

Director

|

05/21/2010

|

04/26/2011

|

04/26/2011

|

746

|

||||

|

Yishui Rural Credit Cooperative

|

Yishui Underground Fluorescent Lake Travel Development Co., Ltd.

|

Controlled by Zhang Shanjiu’s immediate family

|

05/21/2010

|

04/26/2011

|

04/26/2011

|

746

|

||||

|

Yishui Rural Credit Cooperative

|

Zhang Shanjiu

|

Director

|

05/24/2010

|

05/20/2011

|

05/20/2011

|

1,492

|

15

Long Fortune Valley Tourism International Limited

Notes to Condensed Consolidated Financial Statements

(Unless the context requires otherwise, US$ amounts expressed in thousands)

|

Industrial and Commercial Bank of China Yishui branch

|

Zhang Shanjiu

|

Director

|

9/21/2010

|

9/15/2011

|

9/15/2011

|

1,045

|

||||

|

Bank of China Yishui branch

|

Zhang Shanjiu

|

Director

|

09/29/2010

|

09/28/2011

|

09/28/2011

|

448

|

||||

|

Bank of China Yishui branch

|

Junan Tianma Island Travel Development Co., Ltd.

|

Controlled by Zhang Shanjiu

|

09/29/2010

|

09/28/2011

|

09/28/2011

|

448

|

||||

|

Bank of China Yishui branch

|

Yishui Underground Fluorescent Lake Travel Development Co., Ltd.

|

Controlled by Zhang Shanjiu’s immediate family

|

09/29/2010

|

09/28/2011

|

09/28/2011

|

448

|

||||

|

Bank of China Yishui branch

|

Yishui Yinhe Travel Development Co., Ltd.

|

Zhang Shanjiu, as an investor, has significant influence over the entity

|

09/29/2010

|

09/28/2011

|

09/28/2011

|

448

|

Pursuant to the Guarantee Contract, dated March 14, 2008, between Longkong and the Agricultural Development Bank of China, Junan Branch, Longkong has guaranteed a loan of Junan Tianma Island Travel Development Co., Ltd. (“Tianma Island”), a company controlled by Zhang Shanjiu, a director of the Company. The loan bears interest at a rate of 7.83% per annum and is due March 13, 2014. Periodic payments of $736,000, $1.2 million, $1.5 million and $1.8 million are due by Tianma Island on March 13, 2011, March 13, 2012, March 13, 2013 and March 13, 2014, respectively. The balance due of the loan at September 30, 2010 was $5.2 million.

9. Commitments

Operating Lease

The Group conducts significant operations from leased lands. The terms of substantially all of these leases are ten years or more. Future minimum lease payments at September 30, 2010, by year and in the aggregate, under all non-cancelable operating leases are as follows:

|

Years ending Dec 31:

|

|

Continuing

operations

|

|||

|

2010

|

$ | 5 | |||

|

2011

|

|

20 | |||

|

2012

|

|

20 | |||

|

2013

|

|

20 | |||

|

2014

|

|

20 | |||

|

Thereafter

|

|

603 | |||

|

$

|

688 | ||||

16

Long Fortune Valley Tourism International Limited

Notes to Condensed Consolidated Financial Statements

(Unless the context requires otherwise, US$ amounts expressed in thousands)

10. Subsequent events

The following table lists the details of additional loans obtained by the Group since September 30, 2010:

|

Creditor

|

Loan Amount

|

Date of loan

|

Due date

|

Interest

|

|||||||||

|

Industrial and Commercial Bank of China Yishui branch

|

746

|

10/22/2010

|

10/14/2011

|

6.672% | |||||||||

|

Bank of China Yishui branch

|

2,238

|

10/21/2010

|

10/20/2011

|

6.12% | |||||||||

|

Bank of China Yishui branch

|

299

|

10/27/2010

|

10/26/2011

|

6.12% | |||||||||

On October 6, 2010, the Company entered into a Share Exchange Agreement with its shareholders, BTHC XV, Inc. (“BTHC”) and BTHC’s principal shareholder. Pursuant to the terms of the Share Exchange Agreement, BTHC agreed to acquire all of the issued and outstanding shares of the Company from the Company’s shareholders in exchange for the issuance by BTHC to the Company’s shareholders of an aggregate of 17,185,177 newly-issued shares of BTHC’s common stock, which, upon completion of the transactions contemplated by the Share Exchange Agreement, constituted approximately 95% of the entity’s issued and outstanding shares of common stock. Upon consummation of the share exchange on October 18, 2010, the Company became a wholly-owned subsidiary of BTHC.

On October 22, 2010, BTHC and BTHC’s principal shareholder received a letter from counsel (“Greentree Letter”) to Greentree Financial Group, Inc. (“Greentree”), in which it was alleged that the Company breached the Exclusive Service Agreement, dated September 1, 2010, between the Company and Greentree (the “Service Agreement”) and that BTHC and BTHC’s principal shareholder facilitated the Company’s alleged breach of the Service Agreement. The Service Agreement purportedly provides that Greentree was engaged by the Company to provide certain financial advisory services, including, among others: (i) advising and assisting the Company with redesigning its capital structure, consistent with US GAAP and usual and customary business practices for companies similar to the Company; (ii) advising and assisting the Company in the conversion of its financial reporting systems to a format that is consistent with US GAAP; (iii) assisting the Company in evaluating prospective merger candidates, including due diligence; (iv) assisting in the preparation of English language closing documents in connection with a proposed reverse takeover transaction (“RTO”), including filings with the SEC; (v) assisting in the preparation and filing of registration statements with the SEC; (vi) assisting in the preparation of corporate governance documents and a NASDAQ listing application; and (vii) providing management training to the Company’s senior management with respect to usual and customary practices for U.S. companies with business plans similar to the Company’s business plan. In consideration of the financial advisory services to be performed by Greentree, the Service Agreement purportedly provides that the Company would pay to Greentree: (i) $25,000 in cash; (ii) 500,000 shares of common stock of the proposed public company (based on an assumed capital structure of 7,500,000 shares issued and outstanding following the closing of the RTO); and (iii) warrants to purchase 200,000 shares of the proposed public company’s common stock. The Service Agreement provides that the warrants: (i) are to be exercisable for a period of 18 months following the closing of the RTO; (ii) have an exercise price of $2.00 per share; (iii) would not be redeemable by the proposed public company; (iv) would contain registration rights; and (v) would contain anti-dilution and price protection provisions for 18 months following the closing of the RTO. With respect to any shares that may be issuable to Greentree, the Service Agreement purportedly provides that the shares would be anti-dilutive for a period of 18 months and that to the extent more than 10,000,000 shares are issued, additional shares would be issued to Greentree to bring Greentree’s ownership up to 5% ownership in the proposed public company. The Service Agreement contains a one year term, subject to extension upon mutual written agreement of the Company and Greentree, and may be terminated by the Company prior to the expiration of the term upon 45 days’ written notice. In addition, the Service Agreement purportedly provides that if the Company were to terminate the Service Agreement prior to the expiration of the term, Greentree would be entitled to the fee set forth above, except that the proposed public company would not be required to issue to Greentree 125,000 of the 500,000 shares of common stock.

17

Long Fortune Valley Tourism International Limited

Notes to Condensed Consolidated Financial Statements

(Unless the context requires otherwise, US$ amounts expressed in thousands)

In the Greentree Letter, Greentree has demanded: (i) 5% of BTHC’s issued and outstanding shares of common stock, subject to anti-dilution provisions; (ii) warrants to purchase 200,000 shares of BTHC’s common stock at an exercise price of $2.00 per share, exercisable for three years; and (iii) the reimbursement and payment of all past, current and future out-of-pocket expenses, including, but not limited to, legal fees.

The Company, BTHC and BTHC’s principal shareholder are in the process of evaluating the merits of the claims contained in the Greentree Letter. To the Company’s, BTHC’s and BTHC’s principal shareholder’s knowledge, no formal legal action has been taken by Greentree as of this date. If any such legal action is commenced by Greentree, there can be no assurance that the Company, BTHC and BTHC’s principal shareholder will be successful in such action.

18

Special Note Regarding Forward-Looking Statements

The following discussion and analysis, as well as other sections in this Form 10-Q Disclosure Information document, should be read in conjunction with the unaudited interim consolidated financial statements and related notes to the unaudited interim consolidated financial statements included elsewhere herein.

The information contained in this Form 10-Q Disclosure Information document includes some statements that are not purely historical and that are “forward-looking statements.” Such forward-looking statements include, but are not limited to, statements regarding our and our management’s expectations, hopes, beliefs, intentions or strategies regarding the future, including our financial condition and results of operations. In addition, any statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. The words “anticipates,” “believes,” “continues,” “could,” “estimates,” “expects,” “intends,” “may,” “might,” “plans,” “possible,” “potential,” “predicts,” “projects,” “seeks,” “aims,” “should,” “will,” “would” and similar expressions, or the negatives of such terms, may identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking.

The forward-looking statements contained in this Form 10-Q Disclosure Information document are based on current expectations and beliefs concerning future developments. There can be no assurance that future developments actually affecting us will be those anticipated. These forward-looking statements involve a number of risks, uncertainties (some of which are beyond our control) or other assumptions that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements, including our ability to increase our revenues and expand our business operations; our ability to successfully implement our acquisition strategy; availability and cost of external financing; our ability to manage our growth; competition for discretionary spending; weather conditions; the length of our operating season; importance of our land use rights to the operation of our business; unanticipated construction delays in completing capital improvements; accidents occurring at our tourist destinations; lack of business interruption or third-party liability insurance; factors that affect tourist destination attendance, such as local conditions, events, natural disasters, disturbances and terrorist activities; dependence on key management personnel; obligations under guarantees; our significant debt load; control by a limited number of principal stockholders; our ability to increase revenues through price increases; our ability to obtain, maintain and renew necessary safety inspections on the special equipment we operate; failure to maintain an effective system of internal control over financial reporting; our business’ susceptibility to the economic, political and legal policies, developments and conditions in China; uncertain legal environment in China; the degree to which the PRC government influences the conduct of our business; ambiguities in the implementation of the New M&A Rule; our ability to use equity compensation to attract and retain qualified personnel; rapid growth of the PRC economy and inflation as a result thereof; government control of currency conversion; fluctuations in exchange rates; outbreaks of widespread public health problems in the PRC, such as the Swine Flu, SARS or the Avian Flu; lack of deposit insurance for funds held in local banks; our ability to comply with the FCPA and Chinese anti-corruption laws; our ability to pay dividends to our stockholders; the implementation of the new PRC employment contact law; our classification as a “resident enterprise” under the Enterprise Income Tax Law; cultural, political and language differences between China and the United States; adverse changes in the securities markets; development of a public trading market for our securities; and other risks described in our Current Report on Form 8-K filed with the SEC on November 4, 2010 and this Form 10-Q Disclosure Information document.

19

Should one or more of these risks or uncertainties materialize, or should any of our assumptions prove incorrect, actual results may vary in material respects from those projected in these forward-looking statements. You should not place undue reliance on forward-looking statements. Such statements speak only as to the date on which they are made, and we undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

Use of Certain Defined Terms

As used in this Form 10-Q Disclosure Information document, unless the context requires or is otherwise indicated, terms “we,” “us,” “our,” the “Registrant,” the “Company,” “our company” and similar expressions include the following entities, after giving effect to the Share Exchange (as defined below):

|

·

|

BTHC XV, Inc., a Delaware corporation (“BTHC”), which is a publicly traded company;

|

|

·

|

Long Fortune Valley Tourism International Limited, a company organized under the laws of the Cayman Islands and a wholly-owned subsidiary of BTHC (“Long Fortune”);

|

|

·

|

Rich Valley Capital Holding Limited, a company organized under the laws of the British Virgin Islands and a wholly-owned subsidiary of Long Fortune (“Rich Valley”);

|

|

·

|

Long Fortune Valley Tourism International Limited, a company organized under the laws of Hong Kong and a wholly-owned subsidiary of Rich Valley (“LFHK”); and

|

|

·

|

Shandong Longkong Travel Management Co., Ltd., a company organized under the laws of China and a wholly-owned subsidiary of LFHK (“Longkong”).

|

“China” or “PRC” refers to the People’s Republic of China, excluding Hong Kong, Macau and Taiwan. “RMB” or “Renminbi” refers to the legal currency of China and “$” or “U.S. Dollars” refers to the legal currency of the United States. The Company maintains its books and accounting records in Renminbi. We make no representation that the RMB or U.S. Dollar amounts referred to in this

Form 10-Q Disclosure Information document could have been or could be converted into U.S. Dollars or RMB, as the case may be, at any particular rate or at all. “GAAP” unless otherwise indicated refers to United States generally accepted accounting principles. All U.S. Dollar amounts referenced herein are in thousands, unless the context requires otherwise.

Background

On October 6, 2010, BTHC entered into a Share Exchange Agreement with Long Fortune, the former shareholders of Long Fortune (the “Long Fortune Shareholders”), and the former principal shareholder of BTHC, pursuant to which the Long Fortune Shareholders agreed to transfer all of the issued and outstanding securities of Long Fortune to BTHC in exchange for 17,185,177 shares of BTHC common stock (the “Share Exchange”). The Share Exchange closed on October 18, 2010, at which time Long Fortune became a wholly-owned subsidiary of BTHC. The acquisition of Long Fortune has been accounted for as a reverse merger. For accounting purposes, Long Fortune is the acquirer in the reverse acquisition transaction and, consequently, its financial results have been reported on a historical basis.

All of our business operations are carried out by Longkong, which is a cave tourism development and management company whose tourist destination and operations are based solely in the PRC, principally in Shandong Province.

20

The corporate structure of BTHC, after taking into account the Share Exchange, is as follows:

Overview

Long Fortune is a tourism development and management company headquartered in Shandong Province, China. Long Fortune’s business specializes in the development and management of natural, cultural and historic scenic sites and ecotourism projects in China, with particular emphasis on the cave tourism sector of the tourism industry. Long Fortune currently operates the “Underground Grand Canyon” tourist destination. In terms of the number of tourists, revenue and net profits from a tourism business, we believe we are one of the leading companies in the cave tourism sector in China.

The Underground Grand Canyon

The Underground Grand Canyon, located in Linyi City, Yishui County, Shandong Province, at 6,100 meters (approximately 3.75 miles), is the longest cave system in northern China and contains several stalactite and stalagmite formations, as well as rivers and streams. To date, approximately 3,100 meters (approximately 2 miles) have been developed into four entertainment attractions, including: (i) the “Underground Water Drifting” attraction; (ii) the “Electric Slide Car” attraction; (iii) the “Battery Vehicle” attraction; and (iv) the “Strop Ropeway” attraction.

21

In 2004, Longkong entered into a development and management agreement with the Yaodianzi Town Government, Linyi City, Yishui County, Shandong Province to operate and manage the Underground Grand Canyon tourist destination from 2004 through 2062. Long Fortune has invested approximately $12 million to improve the infrastructure and facilities at the Underground Grand Canyon and has steadily increased the number of visitors from approximately 150,000 in 2004 to approximately 750,000 in 2009, which is a compounded annual growth rate of 38%.

Long Fortune’s visitors come to the Underground Grand Canyon both on their own, attracted either by advertisements or through word of mouth (“self-drivers”), and through touring with domestic PRC travel agencies. Visitors from travel agencies accounted for approximately 55% of the total number of visitors in 2009, while self-drivers accounted for the remaining 45% of Long Fortune’s visitors.

Results of Operations

Three Months Ended September 30, 2010 Compared to Three Months Ended September 30, 2009

The following table sets forth key components of Long Fortune’s results of operations for the periods indicated, both in dollars and as a percentage of revenues.

|

For the three months ended September 30,

|

||||||||||||||||

|

2010

|

2009

|

|||||||||||||||

|

(All amounts, other than

percentages, in thousands of U.S. dollars)

|

||||||||||||||||

|

(Unaudited)

|

(Unaudited)

|

|||||||||||||||

|

Revenues

|

$ | 3,444 | 100 | % | $ | 3,068 | 100 | % | ||||||||

|

Costs and expenses

|

(620 | ) | 18 | (673 | ) | 22 | ||||||||||

|

Operating income

|

2,824 | 82 | 2,395 | 78 | ||||||||||||

|

Other income (expenses)

|

(104 | ) | 3 | 12 | - | |||||||||||

|

Income before income taxes

|

2,720 | 79 | 2,407 | 78 | ||||||||||||

|

Income tax expense

|

(166 | ) | 5 | (153 | ) | 5 | ||||||||||

|

Net income

|

2,554 | 74 | 2,254 | 73 | ||||||||||||

Long Fortune’s functional currency is RMB; however, its financial information is expressed in U.S. Dollars. The results of operations reported in the table above are based on the exchange rate of RMB 6.746 to $1 for the three months ended September 30, 2010 and the exchange rate of RMB 6.8305 to $1 for the three months ended September 30, 2009.

22

Revenues. Long Fortune’s sales revenue is generated from admission tickets, water drifting attraction fees, rail car fees and other fees and services, including battery vehicle fees, strop ropeway fees and parking fees. An admission ticket is for general access to the “Underground Grand Canyon” tourist destination. Long Fortune’s visitors are charged additional fees for the entertainment attractions in and around the Underground Grand Canyon. Long Fortune’s sales revenue increased approximately $0.4 million, or approximately 10.9%, to approximately $3.4 million in the three months ended September 30, 2010 from approximately $3.0 million in the three months ended September 30, 2009.

Revenue from sales of admission tickets increased approximately $0.5 million, or approximately 24.0%, to approximately $2.3 million in the three months ended September 30, 2010 from approximately $1.8 million in the three months ended September 30, 2009. Revenue from fees for the entertainment attractions decreased approximately $0.1 million, or approximately 5.6%, to approximately $1.1 million in the three months ended September 30, 2010 from approximately $1.2 million in the three months ended September 30, 2009.

Costs and Expenses. Long Fortune’s costs and expenses are primarily comprised of advertising and promotion expenses, administrative expenses, salaries and fringe benefits, depreciation and amortization costs. Costs and expenses decreased approximately $0.05 million, or approximately 7.9%, to approximately $0.62 million in the three months ended September 30, 2010 from approximately $0.67 million in the three months ended September 30, 2009. This is primarily due to decreases in advertising and promotion expenses, administrative expenses and amortization costs, which were due to cost control measures, being slightly offset by an increase in salaries and fringe benefits.

Operating Income and Operating Margin. Long Fortune’s operating income increased approximately $0.4 million, or approximately 17.9%, to approximately $2.8 million in the three months ended September 30, 2010 from approximately $2.4 million in the three months ended September 30, 2009. Operating income as a percentage of revenues was 82% and 78% for the three months ended September 30, 2010 and 2009, respectively. The increase in operating income and operating margin are primarily due to an increase in revenues and to a lesser extent a decrease in costs and expenses.

Other Income (Expenses). Long Fortune incurred net other expenses of approximately $0.1 million in the three months ended September 30, 2010 compared to net other income of approximately $0.01 million in the three months ended September 30, 2009. The decrease was primarily due to an increase in interest expenses.

Income Tax Expense. Long Fortune’s income tax expense increased approximately $0.01 million, or approximately 8.5%, to approximately $0.16 million in the three months ended September 30, 2010 from approximately $0.15 million in the three months ended September 30, 2009.

Net Income. Long Fortune’s net income increased approximately $0.3 million, or approximately 13.3%, to approximately $2.5 million in the three months ended September 30, 2010 from approximately $2.2 million in the three months ended September 30, 2009.

23

Nine Months Ended September 30, 2010 Compared to Nine Months Ended September 30, 2009

The following table sets forth key components of Long Fortune’s results of operations for the periods indicated, both in dollars and as a percentage of revenues.

|

For the nine months ended September 30,

|

||||||||||||||||

|

2010

|

2009

|

|||||||||||||||

|

(All amounts, other than percentages,

in thousands of U.S. dollars)

|

||||||||||||||||

|

(Unaudited)

|

(Unaudited)

|

|||||||||||||||

|

Revenues

|

$ | 8,159 | 100 | % | $ | 7,777 | 100 | % | ||||||||

|

Costs and expenses

|

(2,237 | ) | 27 | (2,109 | ) | 27 | ||||||||||

|

Operating income

|

5,922 | 73 | 5,668 | 73 | ||||||||||||

|

Other income (expenses)

|

(203 | ) | 3 | 19 | - | |||||||||||

|

Income before income taxes

|

5,719 | 70 | 5,687 | 73 | ||||||||||||

|

Income tax expense

|

(452 | ) | 6 | (498 | ) | 6 | ||||||||||

|

Net income

|

5,267 | 64 | 5,189 | 67 | ||||||||||||

Long Fortune’s functional currency is RMB; however, its financial information is expressed in U.S. Dollars. The results of operations reported in the table above are based on the exchange rate of RMB 6.7647 to $1 for the nine months ended September 30, 2010 and the exchange rate of RMB 6.8363 to $1 for the nine months ended September 30, 2009.

Revenues. Long Fortune’s sales revenue is generated from admission tickets, water drifting attraction fees, rail car fees and other fees and services, including battery vehicle fees, strop ropeway fees and parking fees. An admission ticket is for general access to the “Underground Grand Canyon” tourist destination. Long Fortune’s visitors are charged additional fees for the entertainment attractions in and around the Underground Grand Canyon. Long Fortune’s sales revenue increased approximately $0.4 million, or approximately 4.9%, to approximately $8.2 million in the nine months ended September 30, 2010 from approximately $7.8 million in the nine months ended September 30, 2009.

Revenue from sales of admission tickets increased approximately $0.8 million, or approximately 16.6%, to approximately $5.4 million in the nine months ended September 30, 2010 from approximately $4.6 million in the nine months ended September 30, 2009. Revenue from fees for the entertainment attractions decreased approximately $0.4 million, or approximately 11.8%, to approximately $2.8 million in the nine months ended September 30, 2010 from approximately $3.2 million in the nine months ended September 30, 2009.

24

Costs and Expenses. Long Fortune’s costs and expenses are primarily comprised of advertising and promotion expenses, administrative expenses, salaries and fringe benefits, depreciation and amortization costs. Costs and expenses increased approximately $0.1 million, or approximately 6.1%, to approximately $2.1 million in the nine months ended September 30, 2010 from approximately $2.0 million in the nine months ended September 30, 2009. The increase is primarily due to increases in administrative expenses and salaries and fringe benefits.

Operating Income and Operating Margin. Long Fortune’s operating income increased approximately $0.2 million, or approximately 4.5%, to approximately $5.7 million in the nine months ended September 30, 2010 from approximately $5.9 million in the nine months ended September 30, 2009. Operating income as a percentage of revenues was 73% for each of the nine months ended September 30, 2010 and 2009. The increase in Long Fortune’s operating income was primarily due to an increase in revenues slightly offset by an increase in costs and expenses.

Other Income (Expenses). Long Fortune incurred net other expenses of approximately $0.2 million in the nine months ended September 30, 2010 compared to net other income of approximately $0.02 million in the nine months ended September 30, 2009. The decrease was primarily due to an increase in interest expenses.

Income Tax Expense. Long Fortune’s income tax expense decreased approximately $0.05 million, or approximately 9.2%, to approximately $0.45 million in the nine months ended September 30, 2010 from approximately $0.50 million in the nine months ended September 30, 2009.

Net Income. Long Fortune’s net income increased approximately $0.1 million, or approximately 1.5%, to approximately $5.3 million in the nine months ended September 30, 2010 from approximately $5.2 million in the nine months ended September 30, 2009.

Liquidity and Capital Resources

Cash Flow

As of September 30, 2010, Long Fortune had cash and cash equivalents of approximately $0.6 million. The following table sets forth key components of net cash flow for the periods indicated.

|

Nine Months Ended September 30,

|

||||||||

|

(Unaudited)

|

||||||||

|

(All amounts in thousands of U.S. dollars)

|

||||||||

|

2010

|

2009

|

|||||||

|

Net cash provided by operating activities

|

$ | 3,567 | $ | 5,373 | ||||

|

Net cash used in investing activities

|

(12,154 | ) | (4,005 | ) | ||||

|

Net cash provided by (used in) financing activities

|

7,807 | (685 | ) | |||||

|

Effect of foreign exchange rate changes

|

268 | 15 | ||||||

|

Cash and cash equivalents at the beginning of the period

|

1,076 | 57 | ||||||

|

Cash and cash equivalents at the end of the period

|

564 | 755 | ||||||

25

Cash Flows from Operating Activities.

Net cash provided by operating activities was approximately $3.6 million in the nine months ended September 30, 2010, a decrease of approximately $1.8 million from approximately $5.4 million in the nine months ended September 30, 2009. The decrease was primarily attributable to the increase in other receivable and the decrease in accounts payable in the nine months ended September 30, 2010.

Cash Flows from Investing Activities.

Net cash used in investing activities for the nine months ended September 30, 2010 was approximately $12.2 million, an approximately $8.2 million increase from approximately $4.0 million for the nine months ended September 30, 2009. The increase was primarily due to an approximately $7.2 million increase in loans to related parties in the nine months ended September 30, 2010.

Cash Flows from Financing Activities.

Net cash provided by financing activities was approximately $7.8 million in the nine months ended September 30, 2010. Net cash used in financing activities was approximately $0.7 million in the nine months ended September 30, 2009. The increase was primarily due to an approximately $7.2 million increase in proceeds from bank loans in the nine months ended September 30, 2010.

Capital Sources

At September 30, 2010, Long Fortune did not have any unused credit facilities available to its company. As of September 30, 2010, Long Fortune’s outstanding borrowings consisted of the following:

|

September30,

2010

|

||||

|

(Unaudited)

|

||||

|

(All amounts in thousands of U.S. dollars)

|

||||

|

Secured short-term borrowings

|

||||

|

Interest bearing:

|

||||

|

- 5.31% per annum

|

298 | |||

|

- 5.38% per annum

|

2,985 | |||

|

- 5.84% per annum

|

1,940 | |||

|

- 6.37% per annum

|

1,045 | |||

|

- 7.97% per annum

|

746 | |||

|

- 10.62% per annum

|

2,835 | |||

|

- 11.15% per annum

|

448 | |||

| 10,297 | ||||

26

Long Fortune believes that cash on hand, cash flow from operations and anticipated additional cash resources will meet its expected capital expenditures and working capital requirements for the next 12 months. In addition, we may, in the future, require additional cash resources due to changed business conditions, implementation of Long Fortune’s strategy to expand its business or acquisitions it may decide to pursue. If Long Fortune’s financial resources are insufficient to satisfy its capital requirements, we may seek to sell equity or debt securities or obtain additional credit facilities. The sale of equity securities could result in dilution to our stockholders. The incurrence of indebtedness would result in increased debt service obligations and could require us to agree to operating and financial covenants that would restrict Long Fortune’s operations. Financing may not be available in amounts or on terms acceptable to us, if at all. Any failure by us to raise additional funds on terms favorable to us, or at all, could limit our ability to expand Long Fortune’s business and could harm Long Fortune’s overall business prospects.

Capital Expenditures

Long Fortune’s capital expenditures were approximately $1.8 million for the nine months ended September 30, 2010. Capital expenditures were mainly used to acquire fixed assets to build and expand Long Fortune’s entertainment attractions. Capital expenditures for the fiscal year ended December 31, 2010 are expected to be approximately $3.2 million, which will also be used to build and expand Long Fortune’s entertainment attractions.

Quantitative and Qualitative Disclosures about Market Risk

Long Fortune does not use derivative financial instruments and it has no foreign exchange contracts. Long Fortune’s financial instruments consist of cash and cash equivalents, trade accounts receivable, accounts payable and long-term obligations. Long Fortune generally considers investments in highly liquid instruments purchased with a remaining maturity of 90 days or less at the date of purchase to be cash equivalents.

Interest Rates. Long Fortune generally does not invest in or hold debt securities. Accordingly, fluctuations in applicable interest rates would not have a material impact on our company. At September 30, 2010, Long Fortune had short-term loans payable of approximately $10.3 million. These notes have interest rates ranging from 5.31% to 11.15%. Due to the short-term nature of the notes, a hypothetical 10% increase or decrease in applicable interest rates is not expected to have a material impact on our earnings, loss or cash flows.

Foreign Exchange Rate. All of Long Fortune’s transactions are transacted in RMB. As a result, changes in the relative values of U.S. Dollars and RMB affect Long Fortune’s reported levels of revenues and profitability as the results are translated into U.S. Dollars for reporting purposes. However, because Long Fortune conducts its sales and purchases in RMB, fluctuations in exchange rates are not expected to significantly affect financial stability, or gross and net profit margins. We do not currently expect to incur significant foreign exchange gains or losses, or gains or losses associated with any foreign operations.

Income Taxes