Attached files

| file | filename |

|---|---|

| EX-32.1 - Ironwood Gold Corp. | v204057_ex32-1.htm |

| EX-32.2 - Ironwood Gold Corp. | v204057_ex32-2.htm |

| EX-31.1 - Ironwood Gold Corp. | v204057_ex31-1.htm |

| EX-31.2 - Ironwood Gold Corp. | v204057_ex31-2.htm |

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

FORM

10-K

|

x

|

ANNUAL REPORT PURSUANT TO

SECTION 13 OR 15 (d) OF THE SECURITIES ACT OF

1934

|

For the

fiscal year ended August 31, 2010

|

¨

|

TRANSACTION REPORT PURSUANT TO

SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

1934

|

For the

transition period from _____________________ to

_____________________

Commission

File Number: 000-53267

|

IRONWOOD

GOLD CORP.

|

|

(Exact

name of registrant as specified in

charter)

|

|

Nevada

|

74-3207792

|

|

State

or other jurisdiction of incorporation or organization

|

(I.R.S.

Employee I.D. No.)

|

|

7047

E. Greenway Parkway, #250

|

|

|

Scottsdale,

Arizona

|

85254

|

|

(Address

of principal executive offices)

|

(Zip

Code)

|

888-356-4942

(Registrant’s

telephone number, including area code)

Securities registered pursuant to

Section 12(b) of the Act:

|

Title

of each class

|

Name

of each exchange on which registered

|

|

None

|

None

|

Securities registered pursuant to

Section 12(g) of the Act:

None

(Title of

Class)

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined by

Rule 405 of the Securities Act. ¨ Yes x No

Indicate

by check mark if the registrant is not required to file reports pursuant to

Section 13 or Section 15 (d) of the Act. ¨

Yes x No

Indicate

by check mark whether the registrant (1) has filed all reports required to be

filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the

past 12 months (or for such shorter period that the registrant was required to

file such reports), and (2) has been subject to such filing requirements for the

past 90 days. x Yes ¨ No

Indicate

by check mark whether the registrant has submitted electronically and posted on

its corporate Website, if any, every Interactive Data File required to be

submitted and posted pursuant to Rule 405 of Regulation S-T (§229.405 of this

chapter) during the proceeding 12 months (or for such shorter period that the

registrant was required to submit and post such

files). ¨ Yes ¨ No

Indicate

by check mark if disclosure of delinquent filers pursuant to Item 405 of

Regulation S-K (§229.405 of this chapter) is not contained herein, and will not

be contained, to the best of registrant’s knowledge, in definitive proxy

information statements incorporated by reference in Part III of this Form 10-K

or any amendments to this Form 10-K. ¨

Indicate

by check mark whether the registrant is a large accelerated filer, an

accelerated filer, a non-accelerated filer, or a small reporting

company. See definition of “large accelerated filer,” “accelerated

filer” and “small reporting company” Rule 12b-2 of the Exchange

Act.

|

Large

accelerated filer

|

¨

|

Accelerated

filer

|

¨

|

|

Non-accelerated

filer

|

¨ (Do not check if

a small reporting company)

|

Small

reporting company

|

x

|

Indicate

by check mark whether the registrant is a shell company (as defined in Rule

12b-2 of the Exchange Act). Yes ¨ No x

State the

aggregate market value of the voting and non-voting common equity held by

non-affiliates computed by reference to the price at which the common equity was

last sold, or the average bid and asked price of such common equity, as of the

last business day of the registrant’s most recent completed second fiscal

quarter.

The

aggregate market value of the voting and non-voting common equity held by

non-affiliates of the registrant as of February 26, 2010 was approximately

$30,980,115 based upon the closing price of $0.45 per share reported for such

date on the Over-the-Counter Bulletin Board maintained by the

NASD. Shares of common stock held by each officer and director and by

each person who is known to own 10% of more of the outstanding Common Stock have

been excluded in that such persons may be deemed to be affiliates of the

Company. This determination of affiliate status is not necessarily a

conclusive determination for other purposes.

Indicate

the number of shares outstanding of each of the registrant’s classes of common

stock, as of the latest practicable date:

As of

November 23, 2010, there were 83,199,200 shares of the registrant’s $0.001 par

value common stock issued and outstanding.

DOCUMENTS

INCORPORATED BY REFERENCE

List

hereunder the following documents if incorporated by reference and the Part of

the Form 10-K (e.g., Part I, Part II, etc.) into which the document is

incorporated: (1) Any annual report to security holders; (2) Any proxy or

information statement; (3) Any prospectus filed pursuant to Rule 424 (b) or (c)

under the Securities Act of 1933. The listed documents should

be clearly described for identification purposes (e.g., annual report to

security holders for fiscal year ended December 24, 1980).

TABLE

OF CONTENTS

|

|

Page

|

|||

|

PART

1

|

||||

|

ITEM

1.

|

Business.

|

1

|

||

|

ITEM

1A.

|

Risk

Factors.

|

7

|

||

|

ITEM

1B.

|

Unresolved

Staff Comments.

|

13

|

||

|

ITEM

2.

|

Properties.

|

14

|

||

|

ITEM

3.

|

Legal

Proceedings.

|

18

|

||

|

ITEM

4.

|

[Removed

and Reserved].

|

18

|

||

|

PART

II

|

||||

|

ITEM

5.

|

Market

for Registrant’s Common Equity, Related Stockholder Matters and Issuer

Purchase of Equity Securities.

|

18

|

||

|

ITEM

6.

|

Selected

Financial Data.

|

19

|

||

|

ITEM

7.

|

Management’s

Discussion and Analysis of Financial Conditions and Results of

Operations.

|

20

|

||

|

ITEM

7A.

|

Quantitative

and Qualitative Disclosure about Market Risk.

|

23

|

||

|

ITEM

8.

|

Financial

Statement and Supplementary Data.

|

23

|

||

|

ITEM

9.

|

Changes

in and Disagreements with Accountants on Accounting and Financial

Disclosure.

|

23

|

||

|

ITEM

9A(T).

|

Controls

and Procedures.

|

23

|

||

|

ITEM

9B.

|

Other

Information.

|

24

|

||

|

PART

III

|

||||

|

ITEM

10.

|

Directors,

Executive Officers and Corporate Governance.

|

26

|

||

|

ITEM

11.

|

Executive

Compensation.

|

29

|

||

|

ITEM

12.

|

Security

Ownership of Certain Beneficial Owners and Management and Related

Stockholder Matters.

|

32

|

||

|

ITEM

13.

|

Certain

Relationships and Related Transactions, and Director

Independence.

|

33

|

||

|

ITEM

14.

|

Principal

Accounting Fees and Services.

|

34

|

||

|

PART

IV

|

||||

|

ITEM

15.

|

Exhibits,

Financial Statement Schedules.

|

35

|

||

|

SIGNATURES

|

37

|

i

PART

1

CAUTIONARY

STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

Some

discussions in this Annual Report on Form 10-K contain forward-looking

statements that have been made pursuant to the provisions of the Private

Securities Litigation Reform Act of 1995. These statements involve

risks and uncertainties and relate to future events or future financial

performance. A number of important factors could cause our actual

results to differ materially from those expressed in any forward-looking

statements made by us in this Form 10-K. Forward-looking statements

are often identified by words such as “believe,” “expect,” “estimate,”

“anticipate,” “intend,” “project,” “plans,” “seek” and similar expressions or

words which, by their nature, refer to future events. In some cases,

you can also identify forward-looking statements by terminology such as “may,”

“will,” “should,” “plans,” “predicts,” “potential” or “continue” or the negative

of these terms or other comparable terminology.

These

forward-looking statements are only predictions and involve known and unknown

risks, uncertainties and other factors, including the risks in the section

entitled “Risk Factors” below that may cause our or our industry’s actual

results, levels of activity, performance or achievements to be materially

different from any future results, levels of activity, performance or

achievements expressed or implied by these forward-looking statements. In

addition, you are directed to factors discussed in the “Management’s Discussion

and Analysis of Financial Condition and Results of Operations” section and as

well as those discussed elsewhere in this Form 10-K.

Although

we believe that the expectations reflected in the forward-looking statements are

reasonable, we cannot guarantee future results, levels of activity or

achievements. Except as required by applicable law, including the securities

laws of the United States, we do not intend to update any of the forward-looking

statements to conform these statements to actual results. However, readers

should carefully review the risk factors set forth in other reports or documents

the Company files from time to time with the Securities and Exchange Commission

(the “SEC”), particularly the Company’s Quarterly Reports on Form 10-Q and any

Current Reports on Form 8-K.

As

used in this Form 10-K, “we,” “us,” and “our” refer to Ironwood Gold Corp.,

which is also sometimes referred to as the “Company” or

“Ironwood.” In addition, references to “dollars” and “$” are to

United States dollars.

ITEM

1. BUSINESS.

History

Ironwood

Gold Corp., formerly known as Suraj Ventures, Inc., was incorporated on January

18, 2007 under the laws of the State of Nevada under the name Suraj Ventures,

Inc. for the purpose of acquiring, exploring and developing mineral

properties. On October 27, 2009, we changed our name to Ironwood Gold

Corp.

We are a

mineral exploration stage company building a strong portfolio of exploration

properties containing known deposits of gold. We have targeted

several prospective locations in Nevada, where approximately 80% of all gold in

America is produced today, with three significant properties being located in

proximity to a number of major producing companies. Having assembled

an expert team and developed a business relationship with Teck Resources, Ltd.,

we have already received four independent N.I. 43-101 reports.

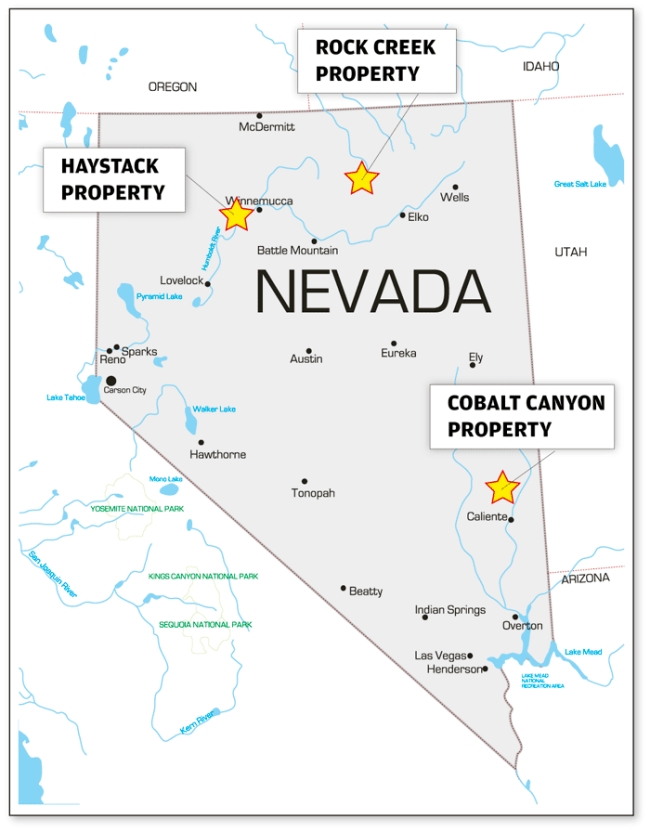

The Rock

Creek Project is a joint venture with Teck Resources, Ltd. Rock Creek

is 1,640 acres in size and is located in the prolific Carlin Trend of Nevada

which has produced 50 millions ounces of gold to date. A N.I. 43-101

compliant report of the property was completed in 2008 and recommended extensive

exploration to test known targets for gold mineralization.

Our

wholly-owned property is the 696-acre Cobalt Canyon Project, comprising 54

unpatented mining claims and 3 patented claims located in Lincoln County,

Nevada, in the historic Chief Mining District. Gold, silver, and lead

production was first recorded in the Chief District in 1868. A N.I.

43-101 compliant report of the property was completed in 2008, and this,

combined with historic drill data by Homestake, Barrick, and others, encourages

further development and exploration of the property as a potential gold deposit

with economically recoverable gold ore.

Our

Haystack Gold Mine Project (“Haystack”) is located in Pershing County, Nevada,

approximately 70 km west of Winnemucca and encompasses 60 federal mining claims

of the Solo group covering 1,110 acres. Gold-bearing quartz veins

hosted in granodiorite were discovered in 1914 in the Haystack district and a

stamp mill was erected two miles to the northeast during 1915. The

recently completed N.I. 43-101 compliant report found the potential for

significant gold deposits in the property’s contact zone with granitoid rock and

encouraged further development and exploration of the property. The

Haystack area represents an opportunity to pursue a Pogo/Fort Knox–type

intrusion related gold target.

1

Our

mining properties are discussed in further detail below.

Industry

By

industry standards, there are generally four types of mining

companies. We are considered an “exploration stage”

company. Typically, an exploration stage mining company is focused on

exploration to identify new, commercially viable gold

deposits. “Junior mining companies” typically have proven and

probable reserves of less than one million ounces of gold, generally produce

less than 100,000 ounces of gold annually, and/or are in the process of trying

to raise enough capital to fund the remainder of the steps required to move from

a staked claim to production. “Mid-tier” and large mining “senior”

companies may have several projects in production plus several million ounces of

gold in reserve.

The gold

mining and exploration industry has experienced several factors recently that

are favorable to our Company, as described below.

The spot

market price of an ounce of gold has increased from a low of $253 in February

2001 to a high of $1,421 in November 2010. This current price level

has made it economically more feasible to produce gold, as well as making gold a

more attractive investment for many. Accordingly, the gross margin

per ounce of gold produced per the historical spot market price range above

provides significant profit potential if we are successful in identifying and

extracting gold at our properties.

Further,

gold reserves have generally been declining for a number of years for the

following reasons:

|

|

·

|

the

extended period of low gold prices from 1996 to 2001 made it economically

unfeasible to explore for new deposits for most mining companies,

and

|

|

|

·

|

the

demand for and production of gold products have exceeded the amount of new

reserves added over the last several consecutive

years.

|

Reversing

the decline in lower gold reserves is a long term process. Due to the

extended time frame it takes to explore, develop, and bring new production

on-line, the large mining companies are facing an extended period of lower gold

reserves. Accordingly, junior companies that are able to increase

their gold reserves more quickly should directly benefit with an increased

valuation.

Additional

factors causing higher gold prices over the past several years have come from a

weakened U.S. dollar. Reasons for the lower dollar compared to other

currencies include, but are not limited to, the historically low U.S. interest

rates, the weak U.S. economy, the increasing U.S. budget and trade deficits, and

the general worldwide political instability caused by the war on

terrorism.

Recent

Events

Some of

our more significant recent events include the following:

On

October 26, 2009, our two former directors gifted back to treasury for

cancellation a total of 1,800,000 (90,000,000 post split) restricted common

shares. The cancellation of these shares resulted in the issued and

outstanding share capital being reduced to 970,000 (48,500,000 post split)

common shares. On October 27, 2009, we effected a 50-for-1 forward

stock split.

In an

effort to grow our Company, on October 28, 2009, we entered into an acquisition

agreement (the “Acquisition Agreement”) with Kingsmere Mining Ltd. (“KML”) and

Ironwood Mining Corp. (“IMC”), whereby we acquired an undivided 100% right,

title, and interest in and to certain mineral claims known as the Cobalt Canyon

Gold Project, in the Chief District, located in Lincoln County, Nevada (the

“Cobalt Canyon Property”), in exchange for an aggregate of 17,075,000 shares of

our common stock and an aggregate cash sum of $575,000. Previously, Gold

Canyon Partners LLP (“GC”) and KML entered into an option agreement (the “Option

Agreement”), dated January 31, 2009, wherein KML acquired an exclusive

option to acquire the Cobalt Canyon Property from GC. KML assigned all of

KML’s interest in the Property to IMC in an agreement (the “Cobalt Assignment

Agreement”) dated April 15, 2009.

On

November 30, 2009, we entered into a purchase agreement with KML (“Purchase

Agreement”), whereby we acquired certain rights in 32 unpatented placer mining

claims located at the Cobalt Canyon Gold Project in Lincoln County,

Nevada. As a result of the purchase agreement, the Cobalt Canyon Gold

Project encompasses a total of 696 acres in the Chief or Caliente mining

district of southeastern Nevada. We agreed to issue 500,000 shares of our

common stock and a cash sum of $65,000 in consideration for the assignment of

the rights. We have a work program planned for the Cobalt properties,

based on the recommended exploration program identified in the N.I. 43-101

compliant technical report on the properties, which will be executed over the

next twelve months and has determined that there is no impairment in value of

the properties at this point. On August 16, 2010, exploratory

drilling at the Cobalt Canyon Property in Nevada commenced. The drill

program consists of six initial drill holes at a number of previously

identified, and in some instances historically productive, locations known as

the Gold Chief, Soa, Contact, Old Democrat, Advance and Gold Stake Mines all

located within the property boundaries. On August 26, 2010, KML

agreed to the cancellation of all 500,000 shares of common stock issued to KML

pursuant to the Purchase Agreement. Except for the cancellation of the

500,000 shares noted above, the Purchase Agreement is still in full force and

effect.

2

On

December 1, 2009, we entered into an assignment agreement (the “Haystack

Assignment Agreement”) with KML, whereby we have the option to acquire an

undivided 100% right, title, and interest in and to certain mineral claims known

as the Haystack Property, located in Pershing County, Nevada (the “Haystack

Property”). We agreed to issue an aggregate of 10,000,000 shares of our

common stock and an aggregate of $300,000 in cash in consideration for the

assignment of all right, title, and interest in the Haystack Property as

follows: 8,500,000 shares and $255,000 to KML and 1,500,000 shares and $45,000

to Teck CO, LLC (“Teck”). Previously, KML and Teck entered into an option

agreement (the “Haystack Option Agreement”), dated October 26, 2009, wherein KML

acquired an exclusive option to acquire the Haystack Property from Teck.

We will obtain all right, title, and interest to the Haystack Property from KML

and Teck pursuant to the terms of the Haystack Assignment Agreement, subject to

certain of the terms and conditions of the Haystack Option Agreement, including

the right of Teck to certain royalties payments and the right of Teck to earn-in

to the Haystack Property by making certain expenditures related to the

exploration and development of the Haystack Property. On June 07,

2010, we announced the receipt of a N.I. 43-101 compliant report undertaken by

Crosby Consulting & Exploration Services regarding the Haystack

Property. The report provides key details regarding the mineral

assets and provides detailed exploratory recommendations. On August

26, 2010, KML agreed to the cancellation of all 8,500,000 shares of common stock

issued to KML pursuant to the Haystack Assignment Agreement. Except for

the cancellation of the 8,500,000 shares noted above, the Haystack Assignment

Agreement is still in full force and effect.

On

December 7, 2009, we entered into an assignment agreement (the “Rock Creek

Assignment Agreement”) with KML, whereby we have the option to acquire an

undivided 100% right, title, and interest in and to certain mineral claims known

as the Rock Creek property, located in Elko County, Nevada (the “Rock Creek

Property”). We agreed to issue an aggregate of 7,000,000 shares of

our common stock and an aggregate of $300,000 in cash in consideration for the

assignment of all right, title, and interest in and to the Rock Creek Property

as follows: 5,950,000 shares and $255,000 to KML and 1,050,000 shares and

$45,000 to Teck. Previously, KML and Teck entered into an option

agreement (the “Rock Creek Option Agreement”), dated October 26, 2009, wherein

KML acquired an exclusive option to acquire the Rock Creek Property from

Teck. We will obtain all right, title, and interest to the Rock Creek

Property from KML and Teck pursuant to the terms of the Rock Creek Assignment

Agreement, subject to certain of the terms and conditions of the Rock Creek

Option Agreement, including the right of Teck to certain royalties payments and

the right of Teck to earn-in to the Rock Creek Property by making certain

expenditures related to the exploration and development of the Rock Creek

Property. We have a work program planned for the Rock Creek property,

based on the recommended exploration program identified in the N.I. 43-101

compliant technical report on the properties, which will be executed over the

next twelve months and has determined that there is no impairment in value of

the property at this point. On August 26, 2010, KML

agreed to the cancellation of all 5,950,000 shares of common stock issued to KML

pursuant to the Rock Creek Assignment Agreement. Except for the

cancellation of the 5,950,000 shares noted above, the Rock Creek Assignment

Agreement is still in full force and effect.

On

January 13, 2010, we completed a private placement and issued 4,674,200 shares

of common stock of the Company at a price of $0.25 per share for gross proceeds

of $1,168,550. We issued 2,316,000 shares of Company common stock for net

cash proceeds of $579,000, which was gross proceeds of $594,000 less share issue

costs of $15,000. In addition, we issued 2,060,000 shares of Company

common stock in exchange for the cancellation of $515,000 owed to

KML.

Beginning

September 27, 2010 through October 21, 2010, we conducted a financing whereby we

entered into a standard form of Securities Purchase Agreement with certain

accredited investors pursuant to which such investors agreed to purchase in the

aggregate up to 5,300,000 Units (as defined below) of the Company at a price of

$0.05 per Unit for aggregate gross proceeds of $265,000. Each “Unit”

consists of one share of the Company’s common stock and one warrant to

purchase one share of common stock at a price of $0.07, exercisable over two

years.

Sources

of Available Land for Mining and Exploration

There are

at least five sources of land available for exploration, development and mining:

public lands, private fee lands, unpatented mining claims, patented mining

claims, and tribal lands. The primary sources for acquisition of

these lands are the United States government, through the Bureau of Land

Management and the United States Forest Service, state governments, tribal

governments, and individuals or entities that currently hold title to or lease

government and private lands.

There are

numerous levels of government regulation associated with the activities of

exploration and mining companies. Permits include “Notice of Intent”

to explore, “Plan of Operations” to explore, “Plan of Operations” to mine,

“Reclamation Permit,” “Air Quality Permit,” “Water Quality Permit,” “Industrial

Artificial Pond Permit,” and several other health and safety

permits. These permits are and will be subject to amendment or

renewal during our operations. Although there is no guarantee that

the regulatory agencies will timely approve, if at all, the necessary permits

for our current operations or other anticipated operations, we have no reason to

believe that necessary permits will not be issued in due course. The

total cost and effects on our operations of the permitting and bonding process

cannot be estimated at this time. The cost will vary for each project

when initiated and could be material.

3

The

Federal government owns public lands that are administered by the Bureau of Land

Management or the United States Forest Service. Ownership of the

subsurface mineral estate can be acquired by staking a twenty (20) acre mining

claim granted under the General Mining Law of 1872, as amended (the “General

Mining Law”). The Federal government still owns the surface estate

even though the subsurface can be controlled with a right to extract through

claim staking. Private fee lands are lands that are controlled by

fee-simple title by private individuals or corporations. These lands

can be controlled for mining and exploration activities by either leasing or

purchasing the surface and subsurface rights from the private

owner. Unpatented mining claims located on public land owned by

another entity can be controlled by leasing or purchasing the claims outright

from the owners. Patented mining claims are claims that were staked

under the General Mining Law, and through application and approval the owners

were granted full private ownership of the surface and subsurface estate by the

Federal government. These lands can be acquired for exploration and

mining through lease or purchase from the owners. Tribal lands are

those lands that are under control by sovereign Native American

tribes. Areas that show promise for exploration and mining can be

leased or joint ventured with the tribe controlling the land.

Competitive

Business Conditions

We

compete with many companies in the mining business, including larger, more

established mining companies with substantial capabilities, personnel and

financial resources. Of the four types of mining companies, we

believe junior mining companies represent the largest group of gold companies

that are publicly listed. All four types of mining companies may have

projects located in any of the gold producing continents of the world and many

have projects located in Nevada. Further, there is a limited supply

of desirable mineral lands available for claim-staking, lease or acquisition in

the United States and other areas where we may conduct exploration

activities. Because we compete with individuals and companies that

have greater financial resources and larger technical staffs, we may be at a

competitive disadvantage in acquiring desirable mineral

properties. From time to time, specific properties or areas that

would otherwise be attractive to us for exploration or acquisition are

unavailable due to their previous acquisition by other companies or our lack of

financial resources.

Competition

in the mining industry is not limited to the acquisition of mineral properties

but also extends to the technical expertise to find, advance, and operate such

properties; the labor to operate the properties; and the capital needed to fund

the acquisition and operation of such properties. Competition may

result in our company being unable not only to acquire desired properties, but

to recruit or retain qualified employees, to obtain equipment and personnel to

assist in our exploration activities or to acquire the capital necessary to fund

our operation and advance our properties. Our inability to compete

with other companies for these resources would have a material adverse effect on

our results of operation and business.

As noted

above, we compete with other mining and exploration companies, many of which

possess greater financial resources and technical facilities than we do, in

connection with the acquisition of suitable exploration properties and in

connection with the engagement of qualified personnel. The gold and

silver exploration and mining industry is fragmented, and we are a very small

participant in this sector. Many of our competitors explore for a

variety of minerals and control many different properties around the

world. Many of them have been in business longer than we have and

have established more strategic partnerships and relationships and have greater

financial accessibility than we have. Accordingly, given the

significant competition for gold and silver exploration properties, we may be

unable to continue to acquire interests in attractive gold and silver mineral

exploration properties on terms we consider acceptable.

While we

compete with other exploration companies in acquiring suitable properties, we

believe that there would be readily available purchasers of gold and/or silver

and other precious metals if they were to be produced from any of the properties

we currently have interests in. The price of precious metals can be

affected by a number of factors beyond our control, including:

|

|

·

|

fluctuations

in the market prices for gold and

silver;

|

|

|

·

|

fluctuating

supplies of gold and silver;

|

|

|

·

|

fluctuating

demand for gold and silver; and

|

|

|

·

|

mining

activities of others.

|

If we

find gold and/or silver mineralization that is determined to be of economic

grade and in sufficient quantity to justify production, we may then seek

significant additional capital through equity or debt financing to develop, mine

and sell our production. Our production would probably be sold to a

refiner that would in turn purify our material and then sell it on the open

market or through its agents or dealers. In the event we should find

economic concentrations of gold or silver mineralization and were able to

commence production, we do not believe that we would have any difficulty selling

the gold or silver we would produce.

We do not

engage in hedging transactions and we have no hedged mineral

resources.

4

Compliance

with Government Regulations

Various

levels of governmental controls and regulations address, among other things, the

environmental impact of mineral exploration and mineral processing operations

and establish requirements for decommissioning of mineral exploration properties

after operations have ceased. With respect to the regulation of

mineral exploration and processing, legislation and regulations in various

jurisdictions establish performance standards, air and water quality emission

standards and other design or operational requirements for various aspects of

the operations, including health and safety standards. Legislation

and regulations also establish requirements for decommissioning, reclamation and

rehabilitation of mineral exploration properties following the cessation of

operations and may require that some former mineral properties be managed for

long periods of time.

Our

exploration activities are subject to various levels of federal and state laws

and regulations relating to protection of the environment, including

requirements for closure and reclamation of mineral exploration

properties. Some of the laws and regulations include the Clean Air

Act, the Clean Water Act, the Comprehensive Environmental Response, Compensation

and Liability Act, the Emergency Planning and Community Right-to-Know Act, the

Endangered Species Act, the Federal Land Policy and Management Act, the National

Environmental Policy Act, the Resource Conservation and Recovery Act, and all

the related state laws in Nevada, some of which are discussed in more detail

below.

The state

of Nevada adopted the Mined Land Reclamation Act (the “Nevada Act”) in 1989 that

established design, operation, monitoring and closure requirements for all

mining operations in the state. The Nevada Act has increased the cost

of designing, operating, monitoring and closing new mining facilities and could

affect the cost of operating, monitoring and closing existing mining

facilities. New facilities are also required to provide a reclamation

plan and financial assurance to ensure that the reclamation plan is implemented

upon completion of operations. The Nevada Act also requires

reclamation plans and permits for exploration projects that will result in more

than five acres of surface disturbance.

We plan

to secure all necessary state and federal permits for our exploration activities

and we intend to file for the required permits to conduct our exploration

programs as necessary. These permits are usually obtained from either

the Bureau of Land Management or the United States Forest

Service. Obtaining such permits usually requires the posting of small

bonds for subsequent remediation of trenching, drilling and

bulk-sampling.

We do not

anticipate discharging water into active streams, creeks, rivers, lakes or any

other bodies of water without an appropriate permit. We also do not

anticipate disturbing any endangered species or archaeological sites or causing

damage to the properties in which we have an interest. Re-contouring

and re-vegetation of disturbed surface areas will be completed pursuant to the

applicable permits. The cost of remediation work varies according to

the degree of physical disturbance. It is difficult to estimate the

cost of compliance with environmental laws since the full nature and extent of

our proposed activities cannot be determined at present.

Environmental

Regulation

As noted

above, mining activities at and on our properties are subject to various

environmental laws, both federal and state, including but not limited to the

federal National Environmental Policy Act, CERCLA (as defined below), the

Resource Recovery and Conservation Act, the Clean Water Act, the Clean Air Act

and the Endangered Species Act, and certain state laws governing the discharge

of pollutants and the use and discharge of water. Various permits

from federal and state agencies are required under many of these

laws. Local laws and ordinances may also apply to such activities as

construction of facilities, land use, waste disposal, road use and noise

levels.

These

laws and regulations are continually changing and, as a general matter, are

becoming more restrictive. Our policy is to conduct our business in a

manner that safeguards public health and mitigates the environmental effects of

our business activities. To comply with these laws and regulations,

we have made, and in the future may be required to make, capital and operating

expenditures.

The Comprehensive Environmental

Response, Compensation, and Liability Act of 1980, as amended (“CERCLA”),

imposes strict, joint, and several liability on parties associated with releases

or threats of releases of hazardous substances. Liable parties

include, among others, the current owners and operators of facilities at which

hazardous substances were disposed or released into the environment and past

owners and operators of properties who owned such properties at the time of such

disposal or release. This liability could include response costs for

removing or remediating the release and damages to natural

resources. The properties in which we have certain interests, because

of past mining activities, could give rise to potential liability under

CERCLA.

Under the

Resource Conservation and

Recovery Act (“RCRA”) and related state laws, mining companies may

incur costs for generating, transporting, treating, storing, or disposing of

hazardous or solid wastes associated with certain mining-related

activities. RCRA costs may also include corrective action or clean up

costs. The majority of the waste which is produced by such operations

is “extraction” waste that Environmental Protection Agency (“EPA”) has

determined not to regulate under RCRA’s “hazardous waste”

program. Instead, the EPA is creating a solid waste regulatory

program specific to mining operations under the RCRA. Of particular

concern to the mining industry is a proposal by the EPA entitled “Recommendation

for a Regulatory Program for Mining Waste and Materials Under Subtitle D of the

Resource Conservation and Recovery Act” (“Strawman II”) which, if implemented,

would create a system of comprehensive Federal regulation of the entire mine

site. Many of these requirements would be duplicates of existing

state regulations. Strawman II as currently proposed would regulate

not only mine and mill wastes but also numerous production facilities and

processes which could limit internal flexibility in operating a

mine. To implement Strawman II the EPA must seek additional statutory

authority, which is expected to be requested in connection with Congress’

reauthorization of RCRA.

5

Mining

operations may produce air emissions, including fugitive dust and other air

pollutants, from stationary equipment, such as crushers and storage facilities,

and from mobile sources such as trucks and heavy construction

equipment. All of these sources are subject to review, monitoring,

permitting, and/or control requirements under the federal Clean Air Act and related

state air quality laws. Air quality permitting rules may impose

limitations on our production levels or create additional capital expenditures

in order to comply with the permitting conditions.

Under the

federal Clean Water

Act, point-source discharges are regulated by the National Pollution

Discharge Elimination System program. Stormwater discharges also are

regulated and permitted under that statute. Section 404 of the

Clean Water Act

regulates the discharge of dredge and fill material into waters of the

United States, including wetlands. All of those programs may impose

permitting and other requirements on our operations.

The National Environmental Policy Act

(“NEPA”) requires an assessment of the environmental impacts of

major federal actions. The federal action requirement must be

satisfied if the project involves federal land or if the federal government

provides financing or permitting approvals. NEPA does not establish

any substantive standards, but requires the analysis of any potential

impacts. The scope of the assessment process depends on the size of

the project. An Environmental Assessment (“EA”) may be adequate

for smaller projects. An Environmental Impact Statement, which is

much more detailed and broader in scope than an EA, is required for larger

projects. NEPA compliance requirements for any of our proposed

projects could result in additional costs or delays.

The Endangered Species Act

(“ESA”) is administered by the U.S. Fish and Wildlife Service of the

U.S. Department of Interior. The purpose of the ESA is to conserve

and recover listed endangered and threatened species and their

habitat. Under the ESA, endangered means that a species is in danger

of extinction throughout all or a significant portion of its

range. The term threatened under such statute means that a species is

likely to become endangered within the foreseeable future. Under the

ESA, it is unlawful to take a listed species, which can include harassing or

harming members of such species or significantly modifying their

habitat. Future identification of endangered species or habitat in

our project areas may delay or adversely affect our operations.

U.S.

federal and state reclamation requirements often mandate concurrent reclamation

and require permitting in addition to the posting of reclamation bonds, letters

of credit or other financial assurance sufficient to guarantee the cost of

reclamation. If reclamation obligations are not met, the designated

agency could draw on these bonds or letters of credit to fund expenditures for

reclamation requirements. Reclamation requirements generally include

stabilizing, contouring and re-vegetating disturbed lands, controlling drainage

from portals and waste rock dumps, removing roads and structures, neutralizing

or removing process solutions, monitoring groundwater at the mining site, and

maintaining visual aesthetics.

Capital

Equipment and Expenditures

During

the year ended August 31, 2010, our efforts were primarily focused on exploring

potential mining opportunities; therefore, no material capital equipment was

acquired by us.

Employees

We

currently use the services of subcontractors for manual labor exploration work

on our claims. At present, we have no employees as such although each

of our officers and directors devotes a portion of his time to the affairs of

the Company. None of our officers and directors has an employment

agreement with us. We presently do not have pension, health, annuity,

insurance, profit sharing or similar benefit plans; however, we may adopt such

plans in the future. There are presently no personal benefits

available to any employee.

Investment

Policies

We do not

have an investment policy at this time. Any excess funds the Company

has on hand will be deposited in interest bearing notes such as term deposits or

short term money instruments. There are no restrictions on what the directors

are able to invest or additional funds held by our

Company. Presently we do not have any excess funds to

invest.

Corporate

Information

Our

principal executive office is located at: 7047 E. Greenway Parkway, #250,

Scottsdale, Arizona, 85254. Our telephone number at that address is

888-356-4942. Our website address is

www.ironwoodgold.com. The information on our website is not a part of

this Annual Report on Form 10-K.

6

ITEM

1A. RISK

FACTORS.

You

should carefully consider the risks described below together with all of the

other information included in our public filings before making an investment

decision with regard to our securities. The statements contained in

or incorporated into this document that are not historic facts are

forward-looking statements that are subject to risks and uncertainties that

could cause actual results to differ materially from those set forth in or

implied by forward-looking statements. If any of the

following events described in these risk factors actually occurs,

our business, financial condition or results of operations could be

harmed. In that case, the trading price of our common stock could

decline, and you may lose all or part of your investment.

Risks

Related to our Business

Because

of the unique difficulties and uncertainties inherent in mineral exploration

ventures, we face a high risk of business failure.

Potential

investors should be aware of the difficulties normally encountered by new

mineral exploration companies and the high rate of failure of such

enterprises. The likelihood of success must be considered in light of

the problems, expenses, difficulties, complications, and delays encountered in

connection with the exploration of the mineral properties that we plan to

undertake. These potential problems include, but are not limited to,

unanticipated problems relating to exploration, environmental permitting

difficulties and delays, and additional costs and expenses that may exceed

current estimates. The expenditures to be made by us in the

exploration of the mineral claim may not result in the discovery of mineable

mineral deposits. Problems such as unusual or unexpected formations

and other conditions are involved in mineral exploration and often result in

unsuccessful exploration efforts. If the results of our exploration

do not reveal viable commercial mineralization, we may decide to abandon our

claims. If this happens, our business will likely fail.

Because

of the speculative nature of exploration of mineral properties, we may never

discover a commercially exploitable quantity of minerals, our business may fail

and investors may lose their entire investment.

We have

been conducting and plan to conduct mineral exploration on our mineral

properties. The search for valuable minerals as a business is

extremely risky. We can provide investors with no assurance that

additional exploration on our properties will establish that commercially

exploitable reserves of minerals exist on our property. Additional

potential problems that may prevent us from discovering any reserves of minerals

on our property include, but are not limited to, unanticipated problems relating

to exploration, environmental permitting difficulties and delays, and additional

costs and expenses that may exceed current estimates. If we are

unable to establish the presence of commercially exploitable reserves of

minerals on our properties our ability to fund future exploration activities

will be impeded, we will not be able to operate profitably and investors may

lose all of their investment in our company.

The nature of

mineral exploration and production activities involves a high degree

of risk and the

possibility of uninsured losses that could materially and

adversely affect our

operations.

Exploration

for minerals is highly speculative and involves greater risk than many other

businesses. Many exploration programs do not result in the discovery

of mineralization and any mineralization discovered may not be of sufficient

quantity or quality to be profitably mined. Few properties that are

explored are ultimately advanced to the stage of producing mines. Our

current exploration efforts are, and any future development or mining operations

we may elect to conduct will be, subject to all of the operating hazards and

risks normally incident to exploring for and developing mineral properties, such

as, but not limited to:

|

|

·

|

economically insufficient

mineralized material;

|

|

|

·

|

fluctuations in production costs

that may make mining

uneconomical;

|

|

|

·

|

labor

disputes;

|

|

|

·

|

unanticipated variations in grade

and other geologic problems;

|

|

|

·

|

environmental

hazards;

|

|

|

·

|

water

conditions;

|

|

|

·

|

difficult surface or underground

conditions;

|

|

|

·

|

industrial

accidents;

|

7

|

|

·

|

metallurgical and other

processing problems;

|

|

|

·

|

mechanical and equipment

performance problems;

|

|

|

·

|

failure of pit walls or

dams;

|

|

|

·

|

unusual or unexpected rock

formations;

|

|

|

·

|

personal injury, fire, flooding,

cave-ins, and

landslides; and

|

|

|

·

|

decrease in reserves due to a

lower gold price.

|

Any of

these risks can materially and adversely affect, among other things, the

development of properties, production quantities and rates, costs and

expenditures, and production commencement dates. We currently have no

insurance to guard against any of these risks. If we determine that

capitalized costs associated with any of our mineral interests are not likely to

be recovered, we would incur a write-down of our investment in these

interests. All of these factors may result in losses in relation to

amounts spent which are not recoverable.

The

potential profitability of mineral ventures depends in part upon factors beyond

the control of our company and even if we discover and exploit mineral deposits,

we may never become commercially viable and we may be forced to cease

operations.

The

commercial feasibility of mineral properties is dependent upon many factors

beyond our control, including the existence and size of mineral deposits in the

properties we explore, the proximity and capacity of processing equipment,

market fluctuations of prices, taxes, royalties, land tenure, allowable

production, and environmental regulation. These factors cannot be

accurately predicted and any one or a combination of these factors may result in

our company not receiving an adequate return on invested

capital. These factors may have material and negative effects on our

financial performance and our ability to continue operations.

Mineralized material is based on

interpretation and assumptions and may yield less mineral production under

actual conditions than is currently estimated.

Unless

otherwise indicated, mineralized material presented in our filings with

securities regulatory authorities, including the SEC, press releases, and other

public statements that may be made from time to time are based upon estimates

made by our consultants. When making determinations about whether to

advance any of our projects to development, we must rely upon such estimated

calculations as to the mineralized material on our properties. Until

mineralized material is actually mined and processed, it must be considered an

estimate only. These estimates are imprecise and depend on geological

interpretation and statistical inferences drawn from drilling and sampling

analysis, which may prove to be unreliable. We cannot assure you that

these mineralized material estimates will be accurate or that this mineralized

material can be mined or processed profitably. Any material changes

in estimates of mineralized material will affect the economic viability of

placing a property into production and such property’s return on

capital. There can be no assurance that minerals recovered in small

scale tests will be recovered at production scale. The mineralized

material estimates have been determined and valued based on assumed future

prices, cut-off grades, and operating costs that may prove

inaccurate. Extended declines in market prices for gold and silver

may render portions of our mineralized material uneconomic and adversely affect

the commercial viability of one or more of our properties and could have a

material adverse effect on our results of operations or financial

condition.

The

construction of mines are subject to all of the risks inherent in

construction.

These

risks include potential delays, cost overruns, shortages of material or labor,

construction defects, and injuries to persons and property. While we

anticipate taking all measures which we deem reasonable and prudent in

connection with the construction, there is no assurance that the risks

described above will not cause delays or cost overruns in connection with such

construction. Any delay would postpone our anticipated receipt of

revenue and adversely affect our operations. Cost overruns would

likely require that we obtain additional capital in order to commence

production. Any of these occurrences may adversely affect our ability

to generate revenues and the price of our stock.

An adequate supply of water may not

be available to undertake mining and production at our

property.

The

amount of water that we are entitled to use from wells must be determined by the

appropriate regulatory authorities. A determination of these rights

is dependent in part on our ability to demonstrate a beneficial use for the

amount of water that we intend to use. Unless we are successful in

developing a property to a point where it can commence commercial production of

gold or other precious metals, we may not be able to demonstrate such beneficial

use. Accordingly, there is no assurance that we will have access to

the amount of water needed to operate a mine at our properties.

8

Exploration

and exploitation activities are subject to comprehensive regulation which may

cause substantial delays or require capital outlays in excess of those

anticipated causing an adverse effect on our company.

Exploration

and exploitation activities are subject to federal, state, and local laws,

regulations, and policies, including laws regulating the removal of natural

resources from the ground and the discharge of materials into the

environment. Exploration and exploitation activities are also subject

to federal, state, and local laws and regulations which seek to maintain health

and safety standards by regulating the design and use of drilling methods and

equipment.

Various

permits from government bodies are required for drilling operations to be

conducted, and no assurance can be given that such permits will be

received. Environmental and other legal standards imposed by federal,

state, or local authorities may be changed and any such changes may prevent us

from conducting planned activities or increase our costs of doing so, which

would have material adverse effects on our business. Moreover,

compliance with such laws may cause substantial delays or require capital

outlays in excess of those anticipated, thus causing an adverse effect on

us. Additionally, we may be subject to liability for pollution or

other environmental damages which we may not be able to or elect not to insure

against due to prohibitive premium costs and other reasons. Any laws,

regulations, or policies of any government body or regulatory agency may be

changed, applied, or interpreted in a manner which will alter and negatively

affect our ability to carry on our business.

As

we face intense competition in the mineral exploration industry, we will have to

compete with our competitors for financing and for qualified managerial and

technical employees.

Our

mineral properties are in Nevada and our competition there includes large,

established mining companies with substantial capabilities and with greater

financial and technical resources than we have. As a result of this

competition, we may have to compete for financing and be unable to acquire

financing on terms we consider acceptable. We may also have to

compete with the other mining companies in the recruitment and retention of

qualified managerial and technical employees. If we are unable to

successfully compete for financing or qualified employees, our exploration

programs may be slowed down or suspended, which may cause us to cease operations

as a company.

Title to mineral

properties can be uncertain and we are at risk of loss of

ownership of one or more of

our properties.

Our

ability to explore and operate our properties depends on the validity of title

to that property. Unpatented mining claims provide only possessory

title and their validity is often subject to contest by third parties or the

federal government, which makes the validity of unpatented mining claims

uncertain and generally more risky. These uncertainties relate to

such things as the sufficiency of mineral discovery, proper posting and marking

of boundaries, assessment work, and possible conflicts with other claims not

determinable from descriptions of record. We have not obtained a

title opinion on any of our properties, with the attendant risk that title to

some claims, particularly title to undeveloped property, may be

defective. There may be valid challenges to the title to our property

which, if successful, could impair development and/or operations. We

remain at risk that the mining claims may be forfeited either to the United

States or to rival private claimants due to failure to comply with statutory

requirements as to location and maintenance of the claims or challenges to

whether a discovery of a valuable mineral exists on every claim.

Government

regulation may adversely affect our business and planned

operations.

Mineral

exploration and development activities are subject to various laws governing

prospecting, development, taxes, labor standards and occupational health, mine

safety, toxic substances, land use, water use, land claims of local people, and

other matters. We cannot assure you that new rules and regulations

will not be enacted or that existing rules and regulations will not be applied

in a manner which could limit or curtail our exploration or development of our

properties.

Legislation

has been proposed that could significantly affect the mining industry in the

United States of America.

Members

of the U.S. Congress have repeatedly introduced bills which would supplant or

alter the provisions of the Mining Law of 1872. If enacted, such

legislation could change the cost of holding unpatented mining claims and could

significantly impact our ability to develop mineralized material on unpatented

mining claims.

A

significant portion of the present Cobalt Canyon, Rock Creek and Haystack

projects’ land position is located on unpatented mining claims located on U.S.

federal public lands. The rights to use such claims are granted under

the Mining Law of 1872. Unpatented mining claims are unique property

interests in the United States, and are generally considered to be subject to

greater title risk than other real property interests because the validity of

unpatented mining claims is often uncertain. This uncertainty arises,

in part, out of the complex federal and state laws and regulations under the

1872 Mining Law and the interaction of the 1872 Mining Law and other federal and

state laws, such as those enacted for the protection of the

environment.

In recent

years, the U.S. Congress has considered a number of proposed amendments to the

1872 Mining Law. If adopted, such legislation could, among other

things:

9

|

|

·

|

impose a royalty on the

production of metals or minerals from unpatented mining

claims;

|

|

|

·

|

reduce or prohibit the ability of

a mining company to expand its operations;

and

|

|

|

·

|

require a material change in the

method of exploiting the reserves located on unpatented mining

claims.

|

All of

the foregoing could adversely affect the economic and financial viability of

future mining operations at the Cobalt Canyon Project. Although it is

impossible to predict at this point what any legislated royalties might be,

enactment could adversely affect the potential for development of such federal

unpatented mining claims.

Amendments

to current laws, regulations, and permits governing operations and activities of

mining and exploration companies, or more stringent implementation thereof,

could have a material adverse impact on our business and cause increases in

exploration expenses, capital expenditures, or production costs or reduction in

levels of production at producing properties or require abandonment or delays in

development of new mining properties.

Our

operating costs could be adversely affected by inflationary pressures especially

to labor, equipment, and fuel costs.

The

global economy is currently experiencing a period of high commodity prices and

as a result the mining industry is attempting to increase production at new and

existing projects, while also seeking to discover, explore and develop new

projects. This has caused significant upward price pressures in the

costs of mineral exploration companies, especially in the areas of skilled labor

and drilling equipment, both of which are in tight supply and whose costs are

increasing. Continued upward price pressures in our exploration costs

may have an adverse impact to our business.

We

may not have sufficient funding for exploration which may impair our

profitability and growth.

The

capital required for exploration of mineral properties is

substantial. From time to time, we will need to raise additional

cash, or enter into joint venture arrangements, in order to fund the exploration

activities required to determine whether mineral deposits on our projects are

commercially viable. New financing or acceptable joint venture

partners may or may not be available on a basis that is acceptable to

us. Inability to obtain new financing or joint venture partners on

acceptable terms may prohibit us from continued exploration of such mineral

properties. Without successful sale or future development of our

mineral properties through joint venture, we will not be able to realize any

profit from our interests in such properties, which could have a material

adverse effect on our financial position and results of operations.

We

have no reported mineral reserves and if we are unsuccessful in identifying

mineral reserves in the future, we may not be able to realize any profit from

our property interests.

We are an

exploration stage company and have no reported mineral reserves. Any

mineral reserves will only come from extensive additional exploration,

engineering, and evaluation of existing or future mineral

properties. The lack of reserves on our mineral properties could

prohibit us from sale or joint venture of our mineral properties. If

we are unable to sell or joint venture for development our mineral properties,

we will not be able to realize any profit from our interests in such mineral

properties, which could materially adversely affect our financial position or

results of operations. Additionally, if we or partners to whom we may

joint venture our mineral properties are unable to develop reserves on our

mineral properties we may be unable to realize any profit from our interests in

such properties, which could have a material adverse effect on our financial

position or results of operations.

Severe

weather or violent storms could materially affect our operations due to damage

or delays caused by such weather.

Our

exploration activities are subject to normal seasonal weather conditions that

often hamper and may temporarily prevent exploration

activities. There is a risk that unexpectedly harsh weather or

violent storms could affect areas where we conduct exploration

activities. Delays or damage caused by severe weather could

materially affect our operations or our financial position.

Our

business is extremely dependent on gold, commodity prices, and currency exchange

rates over which we have no control.

Our

operations will be significantly affected by changes in the market price of gold

and other commodities since the evaluation of whether a mineral deposit is

commercially viable is heavily dependent upon the market price of gold and other

commodities. The price of commodities also affects the value of

exploration projects we own or may wish to acquire. These prices of

commodities fluctuate on a daily basis and are affected by numerous factors

beyond our control. The supply and demand for gold and other

commodities, the level of interest rates, the rate of inflation, investment

decisions by large holders of these commodities, including governmental

reserves, and stability of exchange rates can all cause significant fluctuations

in prices. Such external economic factors are in turn influenced by

changes in international investment patterns and monetary systems and political

developments. The prices of commodities have fluctuated widely and

future serious price declines could have a material adverse effect on our

financial position or results of operations.

10

Fluctuating

gold prices could negatively impact our business plan.

The

potential for profitability of our gold mining operations and the value of our

mining properties are directly related to the market price of

gold. The price of gold may also have a significant influence on the

market price of our shares. If we obtain positive drill results and

progress one of our properties to a point where a commercial production decision

can be made, our decision to put a mine into production and to commit the funds

necessary for that purpose must be made long before any revenue from production

would be received. A decrease in the price of gold at any time during

future exploration and development may prevent our property from being

economically mined or result in the write-off of assets whose value is impaired

as a result of lower gold prices. The price of gold is affected by

numerous factors beyond our control, including inflation, fluctuation of the

United States dollar and foreign currencies, global and regional demand, the

purchase or sale of gold by central banks, and the political and economic

conditions of major gold producing countries throughout the

world. The volatility of mineral prices represents a substantial risk

which no amount of planning or technical expertise can fully

eliminate. In the event gold prices decline and remain low for

prolonged periods of time, we might be unable to develop our properties or

produce any revenue.

The

volatility in gold prices is illustrated by the following table, which sets

forth, for the periods indicated (calendar year), the high and low prices in

U.S. dollars per ounce of gold, based on the daily London P.M. fix.

Gold

Price per Ounce ($)

|

Year

|

High

|

Low

|

||||||

|

1999

|

$ | 326 | $ | 253 | ||||

|

2000

|

312 | 263 | ||||||

|

2001

|

293 | 256 | ||||||

|

2002

|

349 | 278 | ||||||

|

2003

|

416 | 320 | ||||||

|

2004

|

454 | 375 | ||||||

|

2005

|

537 | 411 | ||||||

|

2006

|

725 | 525 | ||||||

|

2007

|

691 | 608 | ||||||

|

2008

|

1,011 | 713 | ||||||

|

2009

|

1,213 | 810 | ||||||

|

2010

|

1,421 | 1,058 | ||||||

Estimates

of mineralized materials are subject to geologic uncertainty and inherent sample

variability.

Although

the estimated resources at our existing properties will be delineated with

appropriately spaced drilling, there is inherent variability between duplicate

samples taken adjacent to each other and between sampling points that cannot be

reasonably eliminated. There also may be unknown geologic details

that have not been identified or correctly appreciated at the proposed level of

delineation. This results in uncertainties that cannot be reasonably

eliminated from the estimation process. Some of the resulting

variances can have a positive effect and others can have a negative effect on

mining and processing operations. Acceptance of these uncertainties

is part of any mining operation.

Our

business is dependent on key executives and the loss of any of our key

executives could adversely affect our business, future operations and financial

condition.

We are

dependent on the services of key executives, including our Chief Executive

Officer, Behzad Shayanfar, and our President, Robert F. Reukl. The

above named officers have many years of experience and an extensive background

in the mining industry in general. We may not be able to replace that

experience and knowledge with other individuals. We do not have

“Key-Man” life insurance policies on any of our key executives. The

loss of these persons or our inability to attract and retain additional highly

skilled employees may adversely affect our business, future operations, and

financial condition.

Risks

Associated with our Company

We

have incurred losses in prior periods and may incur losses in the

future.

We cannot

be assured that we can achieve or sustain profitability on a quarterly or annual

basis in the future. Our operations are subject to the risks and

competition inherent in the establishment of a business

enterprise. There can be no assurance that future operations will be

profitable. We may not achieve our business objectives and the

failure to achieve such goals would have an adverse impact on us.

11

Our future is dependent

upon our ability to obtain financing. If we do not obtain such

financing, we may have to cease our exploration activities and investors could

lose their entire investment.

There is

no assurance that we will operate profitably or generate positive cash flow in

the future. We will require additional financing in order to proceed

beyond the first few months of our exploration program. We will also

require additional financing for the fees we must pay to maintain our status in

relation to the rights to our properties and to pay the fees and expenses

necessary to become and operate as a public company. We will

also need more funds if the costs of the exploration of our existing

projects are greater than we have anticipated. We will also require

additional financing to sustain our business operations if we are not successful

in earning revenues. We may not be able to obtain financing on

commercially reasonable terms or terms that are acceptable to us when it is

required. Our future is dependent upon our ability to obtain

financing. If we do not obtain such financing, our business could

fail and investors could lose their entire investment.

Because

we may never earn revenues from our operations, our business may fail and then

investors may lose all of their investment in our company.

We have

no history of revenues from operations. We have yet to generate

positive earnings and there can be no assurance that we will ever operate

profitably. Our company has a limited operating history and is in the

exploration stage. The success of our company is significantly

dependent on the uncertain events of the discovery and exploitation of mineral

reserves on our properties or selling the rights to exploit those mineral

reserves. If our business plan is not successful and we are not able

to operate profitably, then our stock may become worthless and investors may

lose all of their investment in our company.

Prior to

completion of the exploration and pre-feasibility and feasibility stages, we

anticipate that we will incur increased operating expenses without realizing any

revenues. We therefore expect to incur significant losses into the

foreseeable future. We recognize that if we are unable to generate

significant revenues from the exploration of our mineral claims in the future,

we will not be able to earn profits or continue operations. There is

no history upon which to base any assumption as to the likelihood that we will

prove successful, and we can provide no assurance that we will generate any

revenues or ever achieve profitability. If we are

unsuccessful in addressing these risks, our business will fail and

investors may lose all of their investment in our company.

We

are subject to new corporate governance and internal control reporting

requirements, and our costs related to compliance with, or our failure to comply

with existing and future requirements, could adversely affect our

business.

We may

face new corporate governance requirements under the Sarbanes-Oxley Act of 2002,

as well as new rules and regulations subsequently adopted by the SEC and the

Public Company Accounting Oversight Board. These laws, rules, and

regulations continue to evolve and may become increasingly stringent in the

future. In particular, under rules proposed by the SEC on August 6,

2006, we are required to include management’s report on internal controls as

part of our annual report pursuant to Section 404 of the Sarbanes-Oxley

Act. We strive to continuously evaluate and improve our control

structure to help ensure that we comply with Section 404 of the Sarbanes-Oxley

Act. The financial cost of compliance with these laws, rules, and

regulations is expected to remain substantial. We cannot assure you

that we will be able to fully comply with these laws, rules, and regulations

that address corporate governance, internal control reporting, and similar

matters. Failure to comply with these laws, rules and regulations

could materially adversely affect our reputation, financial condition, and the

value of our securities.

Risks

Related to an Investment in Our Securities

Our

stock is categorized as a penny stock. Trading of our stock may be

restricted by the SEC’s penny stock regulations which may limit a shareholder’s

ability to buy and sell our stock.

Our stock

is categorized as a penny stock. The SEC has adopted Rule 15g-9 which

generally defines “penny stock” to be any equity security that has a market