Attached files

Table of Contents

Index to Financial Statements

As filed with the Securities and Exchange Commission on November 30, 2010

Registration No. 333-166092

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 6

TO

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

FLEETCOR TECHNOLOGIES, INC.

(Exact name of Registrant as specified in its charter)

| Delaware | 7389 | 72-1074903 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

655 Engineering Drive, Suite 300

Norcross, Georgia 30092-2830

(770) 449-0479

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

Sean Bowen

Senior Vice President and General Counsel

655 Engineering Drive, Suite 300

Norcross, Georgia 30092-2830

(770) 449-0479

(Name, address, including zip code, and telephone number, including area code, of agent for service)

with copies to:

| Jon R. Harris, Jr., Esq. Alan J. Prince, Esq. King & Spalding LLP 1180 Peachtree Street, N.E. Atlanta, Georgia 30309 (404) 572-4600 |

John W. White, Esq. Andrew J. Pitts, Esq. Cravath, Swaine & Moore LLP Worldwide Plaza 825 Eighth Avenue New York, New York 10019 (212) 474-1000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ¨ | Accelerated filer ¨ | |||

| Non-accelerated filer x |

(Do not check if a smaller reporting company) | Smaller reporting company ¨ |

CALCULATION OF REGISTRATION FEE

| Title of each class of securities to be registered |

Amount to be registered (1) |

Proposed maximum offering price per |

Proposed maximum aggregate offering price (1)(2) |

Amount of registration fee | ||||

| Common Stock, $0.001 par value per share |

14,576,250 shares | $26.00 | $378,982,500 | $27,022(3) | ||||

| (1) | Includes shares issuable upon exercise of the underwriters’ over-allotment options. See “Underwriting.” |

| (2) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(a) under the Securities Act. |

| (3) | Previously paid. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

Index to Financial Statements

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Preliminary Prospectus

Subject to Completion. Dated November 30, 2010

12,675,000 Shares

Common Stock

This is an initial public offering of the common stock of FleetCor Technologies, Inc.

FleetCor Technologies, Inc. is offering 430,961 of the shares to be sold in the offering. The selling stockholders identified in this prospectus are offering an additional 12,244,039 shares. FleetCor will not receive any proceeds from the sale of the shares being sold by the selling stockholders.

Prior to this offering, there has been no public market for the common stock. It is currently estimated that the initial public offering price per share will be between $23.00 and $26.00. FleetCor’s common stock has been approved for listing on the New York Stock Exchange, subject to official notice of issuance, under the symbol “FLT”.

See “Risk factors” beginning on page 11 to read about risks you should consider before buying shares of common stock.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

| Per Share | Total | |||||||

| Initial public offering price |

$ | $ | ||||||

| Underwriting discount |

$ | $ | ||||||

| Proceeds, before expenses, to us |

$ | $ | ||||||

| Proceeds, before expenses, to the selling stockholders |

$ | $ | ||||||

To the extent the underwriters sell more than 12,675,000 shares of common stock, the underwriters have the option to purchase up to an additional 1,901,250 shares from the selling stockholders at the initial public offering price less the underwriting discount.

Delivery of the shares of common stock will be made on or about , 2010.

| J.P. Morgan |

Goldman, Sachs & Co. | |||

| Barclays Capital |

Morgan Stanley | |||

| PNC Capital Markets LLC |

Raymond James |

Wells Fargo Securities | ||

Prospectus dated , 2010.

Table of Contents

Index to Financial Statements

| Page | ||||

| 1 | ||||

| 11 | ||||

| 29 | ||||

| 30 | ||||

| 31 | ||||

| 32 | ||||

| 34 | ||||

| Unaudited pro forma condensed consolidated financial information |

36 | |||

| 39 | ||||

| Management’s discussion and analysis of financial condition and results of operations |

41 | |||

| 75 | ||||

| 92 | ||||

| 101 | ||||

| 124 | ||||

| 130 | ||||

| 135 | ||||

| 140 | ||||

| 143 | ||||

| 145 | ||||

| 149 | ||||

| 156 | ||||

| 156 | ||||

| 156 | ||||

| F-1 | ||||

No dealer, salesperson or other person is authorized by us or the selling stockholders to give any information or to represent anything not contained in this prospectus. You must not rely on any unauthorized information or representations. This prospectus is an offer to sell only the shares offered hereby, but only under circumstances and in jurisdictions where it is lawful to do so. The information contained in this prospectus is current only as of the date on the front of this prospectus.

i

Table of Contents

Index to Financial Statements

This summary highlights significant aspects of our business and this offering that appear later in this prospectus, but it is not complete and does not contain all of the information that you should consider before making your investment decision. You should read carefully the entire prospectus, including the section entitled “Risk factors” and the information presented in the historical financial data and related notes, before making an investment decision. This summary contains forward-looking statements, which involve risks and uncertainties. Our actual results may differ significantly from the results discussed in the forward-looking statements as a result of certain factors, including those set forth in this prospectus under the headings “Risk factors” and “Special note regarding forward-looking statements.” In this prospectus, unless indicated otherwise or the context otherwise requires, “we,” “us,” “our” and “FleetCor” refer to FleetCor Technologies, Inc., the issuer of the common stock, and its subsidiaries.

Overview

FleetCor is a leading independent global provider of specialized payment products and services to commercial fleets, major oil companies and petroleum marketers. We serve more than 530,000 commercial accounts in 18 countries in North America, Europe, Africa and Asia, and we had approximately 2.5 million commercial cards in use during the month of December 2009. Through our proprietary payment networks, our cards are accepted at approximately 83,000 locations in North America and internationally. In 2009, we processed approximately $14 billion in purchases on our proprietary networks and third-party networks. We believe that our size and scale, geographic reach, advanced technology and our expansive suite of products, services, brands and proprietary networks contribute to our leading industry position.

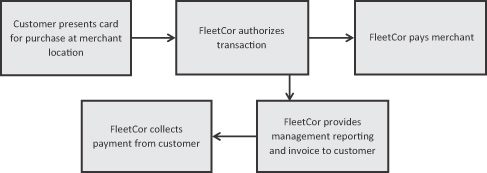

We provide our payment products and services in a variety of combinations to create customized payment solutions for our customers and partners. Our payment programs enable businesses to better manage and control employee spending and provide card-accepting merchants with a high volume customer base that can increase their sales and customer loyalty. In order to deliver our payment programs and services and process transactions, we own and operate six proprietary “closed-loop” networks through which we electronically connect to merchants and capture, analyze and report customized information. We also use third-party networks to deliver our payment programs and services in order to broaden our card acceptance and use. To support our payment products, we also provide a range of services, such as issuing and processing, as well as specialized information services that provide our customers with value-added functionality and data. Our customers can use this data to track important business productivity metrics, combat fraud and employee misuse, streamline expense administration and lower overall fleet operating costs.

We market our payment products directly to a broad range of commercial fleet customers, including vehicle fleets of all sizes and government fleets. Among these customers, we provide our products and services predominantly to small and medium commercial fleets. We believe these fleets represent an attractive segment of the global commercial fleet market given their relatively high use of less efficient payment products, such as cash and general purpose credit cards. We also manage commercial fleet card programs for major oil companies, such as British Petroleum (BP) (including its subsidiary Arco), Chevron and Citgo, and over 800 petroleum marketers. These companies collectively maintain hundreds of thousands of end-customer relationships with commercial fleets. We refer to these major oil companies and petroleum marketers with whom we have strategic relationships as our “partners.”

FleetCor benefits from an attractive business model, which is characterized by our recurring revenue, significant operating margins and low capital expenditure requirements. Our revenue is recurring in nature because we

1

Table of Contents

Index to Financial Statements

generate fees every time a card is used, customers rely on our payment programs to control their own recurring operating expenses and our partners and customers representing a substantial portion of our revenue enter into multi-year service contracts. Our highly-scalable business model creates significant operating efficiencies, which enable us to generate strong cash flow that may be used to repay indebtedness, make acquisitions and fund the future growth of our business. In addition, this business model enables us to continue to grow our business organically without significant additional capital expenditures.

We believe the fleet card industry is positioned for further consolidation because it is served by a fragmented group of suppliers, few with the size and scale to adequately invest to keep pace with industry advancements. For example, there is significant time and investment required to establish the “closed-loop” networks and technology solutions that address the diverse requirements of customers and partners across various geographic markets. We believe this dynamic will continue to shift market share to larger scale vendors with advanced technology platforms and drive further consolidation globally.

FleetCor’s predecessor company was organized in the United States in 1986. In 2000, our current chief executive officer joined us and we changed our name to FleetCor Technologies, Inc. Since 2000, we have grown significantly through a combination of organic initiatives, product and service innovation and over 40 acquisitions of businesses and commercial account portfolios. We have grown our revenue from $30.7 million in 2001 to $381.3 million on a “managed basis” (as defined in “Management’s discussion and analysis of financial condition and results of operations”) in 2009, representing a compound annual growth rate of 37.0%. In 2009, we generated 35.8% of our revenue from our international operations, compared to none in 2005. For the years ended December 31, 2005, 2006, 2007, 2008 and 2009, our consolidated revenue was $143.3 million, $186.2 million, $264.1 million, $341.1 million and $354.1 million, respectively. In the same periods, we generated operating income of $59.0 million, $71.8 million, $105.8 million, $152.5 million and $146.0 million, respectively. In addition, we have grown our net income from a net loss of $12.6 million in 2000 to net income of $89.1 million in 2009.

Industry background

| • | The electronic payments industry is a large and fast-growing sector that is benefiting from favorable trends around the world. Packaged Facts, a research firm, estimates that total global card purchase volumes reached $6.8 trillion in 2009, growing at a compound annual growth rate of 10.8% from 2005 to 2009. |

| • | Commercial cards provide specialized capabilities and are among the fastest growing segments of the electronic payments industry. Commercial card products are typically charge cards, which are paid in full every month and provide businesses with control over the types of authorized purchases, integration with accounting systems, detailed reporting, and the ability to incorporate and transmit additional data with a payment transaction. Packaged Facts estimates that total global commercial card purchase volumes reached $916.5 billion in 2009, growing at a compound annual growth rate of 8.2% from 2005 to 2009, and will reach $1.5 trillion in 2014, growing at a compound annual growth rate of 10.6% from 2009 to 2014. |

| • | Fleet cards typically provide differentiated services that help commercial fleet operators operate their businesses more effectively. Fleet cards are specialized commercial cards that fleet operators provide to their drivers to pay for fuel, maintenance, repairs and other approved purchases. Fleet cards typically provide differentiated services, which include significant cost controls (managed through business rules implemented at the point of sale) and access to “level 3” data regarding transactions, such as the amount of the expenditure, the identification of the driver and vehicle, the odometer reading, the identity of the fuel or vehicle maintenance provider and the items purchased. |

2

Table of Contents

Index to Financial Statements

| • | Fleets represent a large customer base around the world. Fleets are composed of one or more vehicles, including automobiles, vans, SUVs, trucks and buses, used by businesses and governments. We believe small and medium commercial fleets represent a significant market opportunity for growth. |

| • | Packaged Facts estimates that there were approximately 41.9 million fleet vehicles in the United States in 2008 and that total U.S. closed-loop fleet card purchase volumes reached $50.8 billion in 2009, growing at a compound annual growth rate of 6.0% from 2005 to 2009. Based on research by Packaged Facts, 35% of U.S. fleet vehicle fuel volume in 2009 was purchased utilizing closed-loop fleet cards. |

| • | Based on our analysis of data from several sources, we believe there were approximately 68 million fleet vehicles in 30 European and Eurasian countries in 2007. Datamonitor, a research firm, estimates that the total value of fuel sold on commercial fuel cards in 16 major European countries reached approximately €68 billion in 2006. Based on our analysis of data available for several of the largest European countries, including France, Germany, Italy, the Netherlands, Spain and the United Kingdom, we estimate that during 2005, approximately 59% of fleet vehicle fuel volume in Europe was purchased with some form of fleet card product. |

| • | Industry characteristics provide an attractive growth opportunity. The fleet card industry is served by a fragmented group of participants with varying distribution models, including oil companies, petroleum marketers, third-party independent fleet card issuers and network operators, transaction processors and software service providers. We believe there is a significant amount of aging technology, legacy systems, and “dated” business practices within the fleet card industry, which we believe will continue to shift market share to larger scale vendors with advanced technology platforms and create significant barriers to entry. Given the generally rising levels of fuel prices and the continued increase in the number and size of commercial fleets, we believe the use of fleet cards will continue to increase around the world. We believe increasing penetration could accelerate the growth of the fleet card sector relative to alternative payment methods, and we believe larger scale participants may be able to grow at a faster rate than the sector due to the fragmented nature of the industry. We believe there will be an increasingly limited number of vendors that can serve the fleet card market effectively and even fewer with the ability to provide products and network services on a global scale. |

Our competitive strengths

We believe our competitive strengths include the following:

| • | Global leadership. We are a leading independent global provider of specialized commercial payment products and services to fleets, major oil companies and petroleum marketers. We believe that our deep and diverse relationships, geographic reach, strong brands and scale contribute to our leading industry position. |

| • | Broad distribution capabilities. We target new customers across different markets by using multiple distribution channels and tailored sales and marketing efforts designed to address the unique characteristics of individual market segments. By targeting and effectively marketing our products to several different customer segments, we are able to address a variety of growth opportunities and diversify our revenue base. |

| • | Proprietary closed-loop networks. We operate six proprietary closed-loop networks which, as of December 31, 2009, served approximately 83,000 acceptance locations in North America and internationally. We believe that the significant time and investment required to establish a large-scale network with mass merchant acceptance makes our model extremely difficult to replicate and creates a significant barrier to entry in our industry. |

3

Table of Contents

Index to Financial Statements

| • | Advanced, reliable technology systems. We operate proprietary and industry-leading technology systems that use modern, scalable and standardized architecture. Our business models and best practices are codified in our technology systems, allowing us to take advantage of revenue-enhancing and cost-saving opportunities across our different businesses and geographies. |

| • | Superior products and services. We provide products and services tailored to the specific needs of our fleet customers, which we believe makes them more attractive than alternative payment methods such as cash, house accounts and general purpose credit cards, as well as many other fleet card products. We believe we are also able to achieve a competitive advantage over many other fleet card vendors by designing products targeting the unique needs of our customers and partners in different markets. |

| • | Strong execution capabilities. Our leadership team has a long and demonstrated track record of growing our business. We have achieved our growth through a strategy combining operational initiatives, strategic relationships and acquisitions. |

Our growth strategy

Our strategy is to grow our revenue and profits by further penetrating our target markets, expanding our product and service offerings, entering new geographic markets and acquiring companies that meet our strategic criteria. The key elements of our growth strategy are to:

| • | Penetrate our target markets further. We intend to expand our presence in target markets by adding more customers, cross-selling additional products and services to existing customers, entering into additional strategic relationships and making acquisitions. |

| • | Expand our products and services. We will seek to grow revenue by introducing new product features and functionality to our fleet card products, including additional maintenance, lodging and travel and entertainment capabilities. We aim to extend our network offerings in order to help major oil companies and petroleum marketers compete more effectively with other fleet cards and alternative payment methods. |

| • | Enter new geographic markets. We intend to continue expanding in areas of Europe and the United States where we currently do not have a significant presence. We are also evaluating other opportunities in markets we believe to be under-penetrated, such as Latin America and parts of Asia. |

| • | Pursue growth through strategic acquisitions. Since 2002, we have completed over 40 acquisitions of companies and commercial account portfolios. In certain international markets, where fleet card penetration is below levels observed in the United States, we will seek opportunities to increase our customer base through further strategic acquisitions. |

Our products and services

We sell a range of customized fleet and lodging payment programs directly and indirectly through partners, such as major oil companies and petroleum marketers. We provide our customers with various card products that typically function like a charge card to purchase fuel, lodging and related products and services at participating locations. We support these cards with specialized issuing, processing and information services that enable us to manage card accounts, facilitate the routing, authorization, clearing and settlement of transactions, and provide value-added functionality and data including customizable card-level controls and productivity analysis tools. Depending on our customer’s and partner’s needs, we provide these services in a variety of outsourced solutions

4

Table of Contents

Index to Financial Statements

ranging from a comprehensive “end-to-end” solution (encompassing issuing, processing and network services) to limited back office processing services. In order to deliver our payment programs and services, we own and operate six proprietary closed-loop networks in North America and internationally. Our networks have well-established brands in local markets and proprietary technology that enable us to capture, transact, analyze and report value-added information pertinent to managing and controlling employee spending.

Risk factors

Investing in our common stock involves substantial risk, and our ability to successfully operate our business is subject to numerous risks, including those that are generally associated with our industry. Any of the risks set forth in this prospectus under the heading “Risk factors” may limit our ability to successfully execute our business strategy. You should carefully consider all of the information set forth in this prospectus and, in particular, should evaluate the specific risks set forth in this prospectus under the heading “Risk factors” in deciding whether to invest in our common stock.

Our principal executive offices are located at 655 Engineering Drive, Suite 300, Norcross, Georgia 30092-2830, and our telephone number at that address is (770) 449-0479. Our website is located at www.fleetcor.com. The information on our website is not part of this prospectus.

Certain data included in this prospectus regarding our industry is derived from our internal assessments, which are based on a variety of sources, including publicly available data and information obtained from customers, other industry sources and management estimates. Independent consultant reports, industry publications and other published industry sources generally indicate that the information contained therein was obtained from sources believed to be reliable but do not guarantee the accuracy and completeness of such information. Our internal data and estimates are based upon information obtained from our investors, customers, suppliers, trade and business organizations, contacts in the markets in which we operate and management’s understanding of industry conditions. Although we believe that such information is reliable, we cannot give you any assurance that any projections or estimates will be achieved.

5

Table of Contents

Index to Financial Statements

The offering

| Shares of common stock offered by us |

430,961 shares |

| Shares of common stock offered by the selling stockholders |

12,244,039 shares |

| Shares of our common stock to be outstanding after this offering |

78,719,146 shares |

| Option to purchase additional shares of common stock |

The selling stockholders have granted the underwriters a 30-day option to purchase up to 1,901,250 additional shares of common stock at the initial public offering price. |

| Voting rights |

Each share of common stock will entitle its holder to one vote. |

| Use of proceeds |

We estimate that the net proceeds we will receive from this offering, after deducting underwriting discounts and other estimated offering expenses payable by us, will be approximately $6.3 million, assuming the shares are offered at $24.50 per share, which is the mid-point of the price range set forth on the cover page of this prospectus. |

| We intend to use approximately $3.1 million of the net proceeds we will receive from this offering to repay a portion of our outstanding term loans under the 2005 Credit Facility. We intend to use the remaining net proceeds for working capital and other general corporate purposes. |

| We will not receive any proceeds from the sale of shares of our common stock by the selling stockholders. |

| Dividend policy |

We currently expect to retain all future earnings, if any, for use in the operation and expansion of our business and debt repayment; therefore, we do not anticipate paying cash dividends on our common stock in the foreseeable future. See “Dividend policy” below. |

| Proposed New York Stock Exchange ticker symbol |

“FLT”. |

| Risk factors |

You should carefully read and consider the information set forth under the heading “Risk factors” beginning on page 11 of this prospectus and all other information set forth in this prospectus before investing in our common stock. |

The common stock to be outstanding after this offering is based on 77,700,311 shares outstanding as of September 30, 2010, and excludes the following:

| • | as of September 30, 2010, 7,348,344 shares issuable upon the exercise of outstanding stock options at a weighted-average exercise price of $8.11 per share (which amount excludes 587,874 shares in respect of options to be exercised by selling stockholders in connection with this offering); and |

6

Table of Contents

Index to Financial Statements

| • | 6,750,000 shares reserved for future issuance under our 2010 Equity Compensation Plan. |

Except as otherwise indicated, the information in this prospectus:

| • | assumes the automatic conversion of all outstanding shares of our preferred stock into 43,575,148 shares of our common stock immediately prior to the closing of this offering; |

| • | assumes the underwriters do not exercise their option to purchase up to 1,901,250 additional shares from the selling stockholders, which would also include the exercise of additional options by selling stockholders in connection with this offering; |

| • | reflects the two and one-half-for-one stock split of shares of our common stock effected on November 29, 2010; and |

| • | assumes that our shares of common stock will be sold at $24.50 per share, which is the mid-point of the price range set forth on the cover page of this prospectus. |

7

Table of Contents

Index to Financial Statements

Summary consolidated data for FleetCor Technologies, Inc.

The table below summarizes our consolidated financial information for the periods indicated and has been derived from our consolidated financial statements and presents certain other financial information. You should read the following information together with the more detailed information contained in “Selected consolidated financial data,” “Management’s discussion and analysis of financial condition and results of operations” and our consolidated financial statements and the accompanying notes, each appearing elsewhere in this prospectus. The consolidated statement of income data for the years ended December 31, 2006 and 2005 as well as the consolidated balance sheet data as of December 31, 2007, 2006 and 2005 are derived from our audited consolidated financial statements not included in this prospectus. The unaudited consolidated financial statements include, in the opinion of management, all adjustments, which include only normal recurring adjustments, that management considers necessary for the fair presentation of the financial information set forth in those statements. Our historical results are not necessarily indicative of the results to be expected in any future period.

| (in thousands, except per share data) | Nine months ended September 30, |

Year ended December 31, | ||||||||||||||||||||||||||

| 2010 | 2009 | 2009 | 2008 | 2007 | 2006 | 2005 | ||||||||||||||||||||||

| (unaudited) | ||||||||||||||||||||||||||||

| Statement of income data(1): |

||||||||||||||||||||||||||||

| Revenues, net |

$ | 327,294 | $ | 256,761 | $ | 354,073 | $ | 341,053 | $ | 264,086 | $ | 186,209 | $ | 143,334 | ||||||||||||||

| Expenses: |

||||||||||||||||||||||||||||

| Merchant commissions |

39,549 | 28,860 | 39,709 | 38,539 | 39,358 | 32,784 | 24,247 | |||||||||||||||||||||

| Processing |

52,608 | 43,099 | 57,997 | 51,406 | 34,060 | 26,388 | 18,360 | |||||||||||||||||||||

| Selling |

23,155 | 21,470 | 30,579 | 23,778 | 22,625 | 19,464 | 13,740 | |||||||||||||||||||||

| General and administrative |

40,025 | 38,251 | 51,375 | 47,635 | 41,986 | 23,175 | 20,562 | |||||||||||||||||||||

| Depreciation and amortization |

25,238 | 20,235 | 28,368 | 27,240 | 20,293 | 12,571 | 7,448 | |||||||||||||||||||||

| Operating income |

146,719 | 104,846 | 146,045 | 152,455 | 105,764 | 71,827 | 58,977 | |||||||||||||||||||||

| Other (income) expense, net |

(767 | ) | (369 | ) | (933 | ) | (2,488 | ) | (1,554 | ) | 39 | 1,997 | ||||||||||||||||

| Interest expense, net |

16,352 | 13,023 | 17,363 | 20,256 | 19,735 | 11,854 | 7,564 | |||||||||||||||||||||

| Total other expense |

15,585 | 12,654 | 16,430 | 17,768 | 18,181 | 11,893 | 9,561 | |||||||||||||||||||||

| Income before income taxes |

131,134 | 92,192 | 129,615 | 134,687 | 87,583 | 59,934 | 49,416 | |||||||||||||||||||||

| Provision for income taxes |

40,752 | 28,088 | 40,563 | 37,405 | 25,998 | 21,957 | 18,748 | |||||||||||||||||||||

| Net income |

$ | 90,382 | $ | 64,104 | $ | 89,052 | $ | 97,282 | $ | 61,585 | $ | 37,977 | $ | 30,668 | ||||||||||||||

| Pro forma earnings per share (unaudited)(2): |

||||||||||||||||||||||||||||

| Earnings per share, basic |

$ | .89 | $ | .78 | $ | 1.10 | $ | 1.36 | $ | .87 | $ | .58 | $ | .46 | ||||||||||||||

| Earnings per share, diluted |

.93 | .82 | 1.13 | 1.35 | .86 | .57 | .44 | |||||||||||||||||||||

| Weighted average shares outstanding, basic |

77,600 | 74,548 | 75,253 | 68,108 | 67,271 | 61,892 | 65,812 | |||||||||||||||||||||

| Weighted average shares outstanding, diluted |

82,045 | 77,978 | 78,854 | 71,913 | 71,720 | 66,660 | 69,852 | |||||||||||||||||||||

| Balance sheet data (at end of period) |

||||||||||||||||||||||||||||

| Cash and cash equivalents |

$ | 110,773 | $ | 69,019 | $ | 84,701 | $ | 70,355 | $ | 68,864 | $ | 18,191 | $ | — | ||||||||||||||

| Restricted cash (3) |

65,927 | 73,485 | 67,979 | 71,222 | 76,797 | 64,016 | — | |||||||||||||||||||||

| Total assets |

1,503,527 | 1,201,655 | 1,209,545 | 929,062 | 875,106 | 657,925 | 266,359 | |||||||||||||||||||||

| Total debt |

501,326 | 360,250 | 351,551 | 370,747 | 341,851 | 255,032 | 127,543 | |||||||||||||||||||||

| Total stockholders’ equity |

571,929 | 445,005 | 474,049 | 273,264 | 192,009 | 158,482 | 58,179 | |||||||||||||||||||||

| Other financial information (unaudited): |

||||||||||||||||||||||||||||

| EBITDA(4) |

$ | 172,724 | (5) | $ | 125,450 | $ | 175,346 | $ | 182,183 | $ | 127,611 | $ | 84,359 | $ | 64,428 | |||||||||||||

| Adjusted EBITDA(4) |

172,724 | (5) | 129,506 | 180,646 | 197,983 | 143,811 | 97,494 | 71,411 | ||||||||||||||||||||

| Adjusted net income(4) |

103,566 | 74,807 | 103,938 | 112,732 | 71,139 | 42,756 | 33,127 | |||||||||||||||||||||

8

Table of Contents

Index to Financial Statements

| (1) | In June 2009, the Financial Accounting Standards Board, or FASB, issued authoritative guidance limiting the circumstances in which a financial asset may be derecognized when the transferor has not transferred the entire financial asset or has continuing involvement with the transferred asset. This guidance was effective for us as of January 1, 2010. As a result of the adoption of such guidance, effective January 1, 2010, our statements of income will no longer include securitization activities in revenue. Rather, we will report interest income, provision for bad debts and interest expense associated with the debt securities issued from our securitization facility. |

| (2) | Pro forma to give effect to (1) the conversion of all outstanding shares of our convertible preferred stock into 43,575,148 shares of our common stock immediately prior to the closing of this offering as though the conversion had occurred at the beginning of the indicated fiscal period, (2) the forgiveness of all cumulative dividends on our convertible preferred stock, except for a portion of the dividends related to the Series D-3 convertible preferred stock where holders will receive cash dividends of approximately $7.3 million calculated as of September 30, 2010, (3) a two and one-half-for-one stock split of shares of our common stock effected on November 29, 2010 and (4) compensation expense of approximately $14.1 million related to 1,631,805 shares of restricted stock which will vest upon the closing of this offering (assuming the price to the public is at the midpoint of the estimated price range set forth on the cover page of this prospectus). |

| (3) | Restricted cash represents customer deposits repayable on demand. |

| (4) | EBITDA is calculated as net income before the provision for income taxes, interest expense, net and depreciation and amortization. Adjusted EBITDA is calculated as EBITDA adjusted for the incremental interest expense attributable to our securitization facility. Adjusted net income is calculated as net income, adjusted to eliminate (a) stock-based compensation expense related to share-based compensation awards, (b) amortization of deferred financing costs and intangible assets and (c) amortization of the premium recognized on the purchase of receivables. We prepare adjusted net income to eliminate the effect of items that we do not consider indicative of our core operating performance. EBITDA, adjusted EBITDA and adjusted net income are supplemental measures of operating performance that do not represent and should not be considered as an alternative to net income or cash flow from operations, as determined by U.S. generally accepted accounting principles, or U.S. GAAP, and our calculation thereof may not be comparable to that reported by other companies. EBITDA, Adjusted EBITDA and adjusted net income have limitations as analytical tools, and you should not consider them in isolation, or as a substitute for analysis of our results as reported under U.S. GAAP. Some of the limitations are: |

| • | EBITDA, adjusted EBITDA and adjusted net income do not reflect our cash expenditures or future requirements for capital expenditures or contractual commitments; |

| • | EBITDA, adjusted EBITDA and adjusted net income do not reflect changes in, or cash requirements for, our working capital needs; |

| • | adjusted net income does not reflect the non-cash component of employee compensation; |

| • | EBITDA and adjusted EBITDA do not reflect the significant interest expense, or the cash requirements necessary to service interest or principal payments, on our debt; and |

| • | although depreciation and amortization are non-cash charges, the assets being depreciated and amortized will often have to be replaced in the future, and EBITDA and adjusted EBITDA do not reflect any cash requirements for such replacements. |

We compensate for these limitations by relying primarily on our U.S. GAAP results and using EBITDA, adjusted EBITDA and adjusted net income only supplementally. We also compensate for these limitations by disclosing such limitations and reconciling EBITDA, adjusted EBITDA and adjusted net income to the most directly comparable U.S. GAAP measure, net income. Further, we also review U.S. GAAP measures and evaluate individual measures that are not included in EBITDA, adjusted EBITDA and adjusted net income. We believe that our presentation of these U.S. GAAP and non-GAAP financial measurements provides information that is useful to analysts and investors because they are important indicators of the strength of our operations and the performance of our core business. We believe it is useful to exclude stock-based compensation expense from adjusted net income because non-cash equity grants made at a certain price and point in time do not necessarily reflect how our business is performing at any particular time and stock-based compensation expense is not a key measure of our core operating performance. We also believe that amortization expenses can vary substantially from company to company and from period to period depending upon their financing and accounting methods, the fair value and average expected life of their acquired intangible assets, their capital structures and the method by which their assets were acquired; therefore, we have excluded amortization expense from our adjusted net income.

Management uses EBITDA, adjusted EBITDA and adjusted net income:

| • | as measurements of operating performance because they assist us in comparing our operating performance on a consistent basis; |

| • | for planning purposes, including the preparation of our internal annual operating budget; |

| • | to allocate resources to enhance the financial performance of our business; and |

| • | to evaluate the performance and effectiveness of our operational strategies. |

In addition, management uses EBITDA and adjusted EBITDA to calculate incentive compensation for our employees.

We believe these measurements are used by investors as supplemental measures to evaluate the overall operating performance of companies in our industry. By providing these non-GAAP financial measures, together with reconciliations, we believe we are enhancing investors’ understanding of our business and our results of operations, as well as assisting investors in evaluating how well we are executing strategic initiatives.

9

Table of Contents

Index to Financial Statements

The following table reconciles net income to EBITDA and adjusted EBITDA:

| Nine Months ended September 30, |

Year ended December 31, | |||||||||||||||||||||||||||

| (in thousands) | 2010 | 2009 | 2009 | 2008 | 2007 | 2006 | 2005 | |||||||||||||||||||||

| Net income |

$ | 90,382 | $ | 64,104 | $ | 89,052 | $ | 97,282 | $ | 61,585 | $ | 37,977 | $ | 30,668 | ||||||||||||||

| Provision for income taxes |

40,752 | 28,088 | 40,563 | 37,405 | 25,998 | 21,957 | 18,748 | |||||||||||||||||||||

| Interest expense, net |

16,352 | 13,023 | 17,363 | 20,256 | 19,735 | 11,854 | 7,564 | |||||||||||||||||||||

| Depreciation and amortization |

25,238 | 20,235 | 28,368 | 27,240 | 20,293 | 12,571 | 7,448 | |||||||||||||||||||||

| EBITDA |

172,724 | (5) | 125,450 | 175,346 | 182,183 | 127,611 | 84,359 | 64,428 | ||||||||||||||||||||

| Incremental interest expense(a) |

N/A | (5) | 4,056 | 5,300 | 15,800 | 16,200 | 13,135 | 6,983 | ||||||||||||||||||||

| Adjusted EBITDA(a) |

$ | 172,724 | (5) | $ | 129,506 | $ | 180,646 | $ | 197,983 | $ | 143,811 | $ | 97,494 | $ | 71,411 | |||||||||||||

| (a) | We utilize an off-balance sheet securitization facility in the ordinary course of our business to finance a portion of our accounts receivable. Accounts receivable that we sell under the securitization facility are reported in our consolidated financial statements in accordance with relevant authoritative literature. Trade accounts receivable sold under this program are excluded from accounts receivable in our consolidated financial statements. In June 2009, the Financial Accounting Standards Board, or FASB, issued authoritative guidance limiting the circumstances in which a financial asset may be derecognized when the transferor has not transferred the entire financial asset or has continuing involvement with the transferred asset. This guidance was effective for us as of January 1, 2010. As a result of the adoption of such guidance, effective January 1, 2010, our statements of income no longer include securitization activities in revenue. Rather, we report interest income, provision for bad debts and interest expense associated with the debt securities issued from our securitization facility. Although the provision for bad debts and interest expense related to our securitization facility are currently reported in revenue, we monitor these costs on a managed basis. Our revenue, processing expense, provision for bad debts and interest expense on a managed basis are set forth and reconciled under “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Accounts Receivable Securitization” . The incremental interest expense represents the additional amount of interest expense that would have been reported if the new authoritative guidance discussed herein was applied to all years presented. |

The following table reconciles net income to adjusted net income:

| Twelve Months ended September 30, |

Nine Months ended September 30, |

Year ended December 31, | ||||||||||||||||||||||||||||||

| (in thousands) | 2010 | 2010 | 2009 | 2009 | 2008 | 2007 | 2006 | 2005 | ||||||||||||||||||||||||

| Net income |

$115,330 | $ | 90,382 | $ | 64,104 | $ | 89,052 | $ | 97,282 | $ | 61,585 | $ | 37,977 | $ | 30,668 | |||||||||||||||||

| Stock-based compensation expense |

3,120 | 2,453 | 1,999 | 2,666 | 2,758 | 1,165 | 139 | 93 | ||||||||||||||||||||||||

| Amortization of intangible assets |

16,867 | 12,749 | 9,782 | 13,900 | 12,038 | 9,825 | 4,978 | 2,060 | ||||||||||||||||||||||||

| Amortization of premium on receivables |

3,262 | 2,447 | 2,442 | 3,257 | 5,471 | 1,702 | 1,443 | 581 | ||||||||||||||||||||||||

| Amortization of deferred financing costs |

2,153 | 1,480 | 1,169 | 1,842 | 1,123 | 895 | 982 | 1,229 | ||||||||||||||||||||||||

| Total pre-tax adjustments |

25,402 | 19,129 | 15,392 | 21,665 | 21,390 | 13,587 | 7,542 | 3,963 | ||||||||||||||||||||||||

| Income tax impact of pre-tax adjustments at the effective tax rate |

(7,856) | (5,945 | ) | (4,689 | ) | (6,779 | ) | (5,940 | ) | (4,033 | ) | (2,763 | ) | (1,504 | ) | |||||||||||||||||

| Adjusted net income |

$132,876 | $ | 103,566 | $ | 74,807 | $ | 103,938 | $ | 112,732 | $ | 71,139 | $ | 42,756 | $ | 33,127 | |||||||||||||||||

In addition, adjusted net income (loss) was $24,579, $11,734, $(12,492) and $(1,455) for the years ended December 31, 2004, 2003, 2002 and 2001, respectively. The following table reconciles net income to adjusted net income (loss) for these periods.

| Year ended December 31, | ||||||||||||||||

| (in thousands) | 2004 | 2003 | 2002 | 2001 | ||||||||||||

| Net income (loss) |

$ | 22,708 | $ | 10,806 | $ | (18,956 | ) | $ | (3,680 | ) | ||||||

| Stock based compensation expense |

244 | 523 | — | — | ||||||||||||

| Amortization of goodwill and intangible assets |

376 | 178 | — | 990 | ||||||||||||

| Goodwill impairment |

— | — | 4,305 | — | ||||||||||||

| Amortization of discount on related-party notes |

119 | — | 1,664 | 732 | ||||||||||||

| Amorization of deferred financing costs |

1,132 | 238 | 513 | 503 | ||||||||||||

| Total pre-tax adjustments |

1,871 | 939 | 6,482 | 2,225 | ||||||||||||

| Income tax impact of pre-tax adjustments at the effective tax rate |

— | (11 | ) | (18 | ) | — | ||||||||||

| Adjusted net income (loss) |

$ | 24,579 | $ | 11,734 | $ | (12,492 | ) | $ | (1,455 | ) | ||||||

| (5) | For periods ended subsequent to January 1, 2010 interest expense, net includes incremental interest expense attributable to our securitization facility. Had we continued to include the incremental interest expense attributable to the securitization facility of $3.7 million within revenue for the nine months ended September 30, 2010, EBITDA would have been $169.0 million. |

10

Table of Contents

Index to Financial Statements

This offering involves a high degree of risk. In addition to the other information contained in this prospectus, prospective investors should carefully consider the following risks before investing in our common stock. If any of the following risks actually occur, our business, operating results and financial condition could be materially adversely affected. As a result, the trading price of our common stock could decline, and you may lose all or part of your investment in our common stock. The risks discussed below also include forward-looking statements, and our actual results may differ substantially from those discussed in these forward-looking statements. See “Special note regarding forward-looking statements” in this prospectus.

Risks related to our business

A decline in retail fuel prices could adversely affect our revenue and operating results.

Our fleet customers use our products and services primarily in connection with the purchase of fuel. Accordingly, our revenue is affected by fuel prices, which are subject to significant volatility. A decline in retail fuel prices could cause a decrease in our revenue from fees paid to us by merchants based on a percentage of each transaction purchase amount. We believe that in 2009, approximately 19.1% of our consolidated revenue, as adjusted for the impact of the new accounting guidance related to our securitization facility as described under the heading “Management’s discussion and analysis of financial condition and results of operations—Accounts receivable securitization”, was directly influenced by the absolute price of fuel. In this prospectus, for the periods between January 1, 2005 and December 31, 2009, we refer to our consolidated revenue as adjusted for the impact of the new accounting guidance related to our securitization facility as our “consolidated revenue on a managed basis”. For the periods prior to January 1, 2005, we did not maintain a securitization facility. Changes in the absolute price of fuel may also impact unpaid account balances and the late fees and charges based on these amounts. A decline in retail fuel prices could adversely affect our revenue and operating results.

Fuel prices are dependent on several factors, all of which are beyond our control. These factors include, among others:

| • | supply and demand for oil and gas, and market expectations regarding supply and demand; |

| • | actions by members of OPEC and other major oil-producing nations; |

| • | political conditions in oil-producing and gas-producing nations, including insurgency, terrorism or war; |

| • | oil refinery capacity; |

| • | weather; |

| • | the prices of foreign exports; |

| • | the implementation of fuel efficiency standards and the adoption by our fleet customers of vehicles with greater fuel efficiency or alternative fuel sources; |

| • | general worldwide economic conditions; and |

| • | governmental regulations, taxes and tariffs. |

A portion of our revenue is derived from fuel-price spreads. As a result, a contraction in fuel-price spreads could adversely affect our operating results.

Approximately 18.6% of our consolidated revenue on a managed basis in 2009 was derived from transactions where our revenue is tied to fuel-price spreads. Fuel-price spreads equal the difference between the fuel price we charge to the fleet customer and the fuel price paid to the fuel merchant. In transactions where we derive revenue

11

Table of Contents

Index to Financial Statements

from fuel-price spreads, the fuel price paid to the fuel merchant is calculated as the merchant’s wholesale cost of fuel plus a commission. The merchant’s wholesale cost of fuel is dependent on several factors including, among others, the factors described above affecting fuel prices. The fuel price that we charge to our fleet customer is dependent on several factors including, among others, the fuel price paid to the fuel merchant, posted retail fuel prices and competitive fuel prices. We experience fuel-price spread contraction when the merchant’s wholesale cost of fuel increases at a faster rate than the fuel price we charge to our fleet customers, or the fuel price we charge to our fleet customers decreases at a faster rate than the merchant’s wholesale cost of fuel. Accordingly, when fuel-price spreads contract, we generate less revenue, which could adversely affect our operating results.

If we fail to adequately assess and monitor credit risks of our customers, we could experience an increase in credit loss.

We are subject to the credit risk of our customers, many of which are small to mid-sized businesses. We use various methods to screen potential customers and establish appropriate credit limits, but these methods cannot eliminate all potential credit risks and may not always prevent us from approving customer applications that are fraudulently completed. Changes in our industry and movement in fuel prices may result in periodic increases to customer credit limits and spending and, as a result, increased credit losses. We may also fail to detect changes to the credit risk of customers over time. Further, during a declining economic environment, we experience increased customer defaults. If we fail to adequately manage our credit risks, our bad debt expense could be significantly higher than historic levels and adversely affect our business, operating results and financial condition. Although the provision for bad debts and interest expense related to our securitization facility were included as a component of net revenue for the periods prior to January 1, 2010 in accordance with then-prevailing accounting guidance, we considered such amounts an expense for the periods prior to January 1, 2010. Accordingly, for internal reporting purposes, we included such amount as a component of operating expense, which we refer to as on a “managed basis.” As further described under the heading “Management’s discussion and analysis of financial condition and results of operations—Accounts receivable securitization”, on a managed basis, our provision for bad debts equaled $32.6 million for the year ended December 31, 2009. For the nine months ended September 30, 2010, our provision for bad debts equaled $15.1 million.

We derive a portion of our revenue from program fees and charges paid by the users of our cards. Any decrease in our receipt of such fees and charges, or limitations on our fees and charges, could adversely affect our business, results of operations and financial condition.

Our card programs include a variety of fees and charges associated with transactions, cards, reports, late payments and optional services. We derived approximately 54.0% of our consolidated revenue on a managed basis from these fees and charges during the year ended December 31, 2009 and approximately 55.0% of our consolidated revenue from these fees and charges during the nine months ended September 30, 2010. If the users of our cards decrease their transaction activity, the extent to which they pay invoices late or their use of optional services, our revenue could be materially adversely affected. In addition, several market factors can affect the amount of our fees and charges, including the market for similar charges for competitive card products and the availability of alternative payment methods such as cash or house accounts. Furthermore, regulators and Congress have scrutinized the electronic payments industry’s pricing, charges and other practices related to its customers. Any legislative or regulatory restrictions on our ability to price our products and services could materially and adversely affect our revenue. Any decrease in our revenue derived from these fees and charges could materially and adversely affect our business, operating results and financial condition.

12

Table of Contents

Index to Financial Statements

We operate in a competitive business environment, and if we are unable to compete effectively, our business, operating results and financial condition would be adversely affected.

The market for our products and services is highly competitive, and competition could intensify in the future. Our competitors vary in size and in the scope and breadth of the products and services they offer. Our primary competitors in the United States are small, regional and large independent fleet card providers, major oil companies and petroleum marketers that issue their own fleet cards and major financial services companies that provide card services to major oil companies and petroleum marketers. We also compete for customers with providers of alternative payment mechanisms, such as financial institutions that issue corporate and consumer credit cards and merchants offering house cash accounts or other forms of credit. Our primary competitors in Europe are independent fleet card providers, major oil companies and petroleum marketers that issue branded fleet cards, and providers of card outsourcing services to major oil companies and petroleum marketers.

The most significant competitive factors in our business are the breadth of product and service features, network acceptance size, customer service and account management and price. We may experience competitive disadvantages with respect to any of these factors from time to time as potential customers prioritize or value these competitive factors differently. As a result, a specific offering of our products and service features, networks and pricing may serve as a competitive advantage with respect to one customer and a disadvantage for another based on the customers’ preferences.

Some of our existing and potential competitors have longer operating histories, greater brand name recognition, larger customer bases, more extensive customer relationships or greater financial and technical resources. In addition, our larger competitors may also have greater resources than we do to devote to the promotion and sale of their products and services and to pursue acquisitions. For example, major oil companies and petroleum marketers and large financial institutions may choose to integrate fuel-card services as a complement to their existing card products and services. As a result, they may be able to adapt more quickly to new or emerging technologies and changing opportunities, standards or customer requirements. To the extent that our competitors are regarded as leaders in specific categories, they may have an advantage over us as we attempt to further penetrate these categories.

Future mergers or consolidations among competitors, or acquisitions of our competitors by large companies may present competitive challenges to our business. Resulting combined entities could be at a competitive advantage if their fuel-card products and services are effectively integrated and bundled into sales packages with their widely utilized non-fuel-card-related products and services. Further, larger competitors have reduced, and could continue to reduce, the fees for their services, which has increased and may continue to increase pricing pressure within our markets.

Overall, increased competition in our markets could result in intensified pricing pressure, reduced profit margins, increased sales and marketing expenses and a failure to increase, or a loss of, market share. We may not be able to maintain or improve our competitive position against our current or future competitors, which could adversely affect our business, operating results and financial condition.

Our business is dependent on several key strategic relationships, the loss of which could adversely affect our operating results.

We intend to seek to expand our strategic relationships with major oil companies. We refer to the major oil companies and petroleum marketers with whom we have strategic relationships as our “partners.” During 2009 and the nine months ended September 30, 2010, our top three strategic relationships with major oil companies accounted for approximately 18% and 22%, respectively, of our consolidated revenue. No single partner represented more than 10% of our consolidated revenue in 2009. In the nine months ended September 30, 2010, one partner accounted for approximately 11% of our consolidated revenue. Two of our partners each represented

13

Table of Contents

Index to Financial Statements

greater than 5% of our consolidated revenue during 2009. Our agreements with our major oil company partners typically have initial terms of five to ten years with current remaining terms ranging from less than one year up to seven years.

The success of our business is in part dependent on our ability to maintain these strategic relationships and enter into additional strategic relationships with major oil companies. In our relationships with these major oil companies, our services are marketed under our partners’ brands. If these partners fail to maintain their brands, or decrease the size of their branded networks, our ability to grow our business may be adversely affected. Our inability to maintain or further develop these relationships or add additional strategic relationships could materially and adversely affect our business and operating results.

To enter into a new strategic relationship or renew an existing strategic relationship with a major oil company, we often must participate in a competitive bidding process, which may focus on a limited number of factors, such as pricing. The use of these processes may affect our ability to effectively compete for these relationships. Our competitors may be willing to bid for these contracts on pricing or other terms that we consider uneconomical in order to win this business. The loss of our existing major oil company partners or the failure to contract with additional partners could materially and adversely affect our business, operating results and financial condition.

We depend, in part, on our merchant relationships to grow our business. To grow our customer base, we must retain and add relationships with merchants who are located in areas where our customers purchase fuel and lodging. If we are unable to maintain and expand these relationships, our business may be adversely affected.

A portion of our growth is derived from acquiring new merchant relationships to serve our customers, our new and enhanced product and service offerings and cross-selling our products and services through existing merchant relationships. We rely on the continuing growth of our merchant relationships and our distribution channels in order to expand our customer base. There can be no guarantee that this growth will continue. Similarly, our growth also will depend on our ability to retain and maintain existing merchant relationships that accept our proprietary closed-loop networks in areas where our customers purchase fuel and lodging. Our contractual agreements with fuel merchants typically have initial terms of one year and automatically renew on a year-to-year basis unless either party gives notice of termination. Our agreements with lodging providers typically have initial terms of one year and automatically renew on a month-to-month basis unless either party gives notice of termination. Furthermore, merchants with which we have relationships may experience bankruptcy, financial distress, or otherwise be forced to contract their operations. The loss of existing merchant relationships, the contraction of our existing merchants’ operations or the inability to acquire new merchant relationships could adversely affect our ability to serve our customers and our business and operating results.

A decline in general economic conditions, and in particular, a decline in demand for fuel and other vehicle products and services would adversely affect our business, operating results and financial condition.

Our operating results are materially affected by conditions in the economy generally, both in the United States and internationally. We generate revenue based in part on the volume of fuel purchase transactions we process. Our transaction volume is correlated with general economic conditions in the United States and Europe and in particular, the amount of business activity in these economies. Downturns in these economies are generally characterized by reduced commercial activity and, consequently, reduced purchasing of fuel and other vehicle products and services by businesses. The recession in 2007 and 2008 negatively affected the organic growth of our business in 2009, which resulted from lower transaction volume from existing customers. Unfavorable changes in economic conditions, including declining consumer confidence, inflation, recession or other changes, may lead our customers, which are largely comprised of commercial fleets, to demand less fuel, or lead our partners to reduce their use of our products and services. These declines could result from, among other things, reduced fleet traffic, corporate purchasing, travel and other commercial activities from which we derive revenue.

14

Table of Contents

Index to Financial Statements

Further, economic conditions also may impact the ability of our customers or partners to pay for fuel or other services they have purchased and, as a result, our reserve for credit losses and write-offs of accounts receivable could increase. In addition, demand for fuel and other vehicle products and services may be reduced by other factors that are beyond our control, such as the development and use of vehicles with greater fuel efficiency and alternative fuel sources.

We are unable to predict the likely duration and severity of the current disruption in financial markets and adverse economic conditions in the United States and Europe. As a result, a sustained deterioration in general economic conditions in the United States or Europe, or increases in interest rates in key countries in which we operate, could adversely affect our business and operating results.

We have expanded into new lines of business in the past and may do so in the future. If we are unable to successfully integrate these new businesses, our results of operations and financial condition may be adversely affected.

We have expanded our business to encompass new lines of business in the past. For example, within the past several years we have entered into the lodging card business in the United States and now offer a limited telematics service to European customers. We may continue to enter new lines of business and offer new products and services in the future. There is no guarantee that we will be successful in integrating these new lines of business into our operations. If we are unable to do so, our operating results and financial condition may be adversely affected.

If we fail to develop and implement new technology, products and services, adapt our products and services to changes in technology or the marketplace, or if our ongoing efforts to upgrade our technology, products and services are not successful, we could lose customers and partners.

The markets for our products and services are highly competitive, and characterized by technological change, frequent introduction of new products and services and evolving industry standards. We must respond to the technological advances offered by our competitors and the requirements of our customers and partners, in order to maintain and improve upon our competitive position. We may be unsuccessful in expanding our technological capabilities and developing, marketing or selling new products and services that meet these changing demands, which could jeopardize our competitive position. In addition, we engage in significant efforts to upgrade our products and services and the technology that supports these activities on a regular basis. If we are unsuccessful in completing the migration of material technology, otherwise upgrading our products and services and supporting technology or completing or gaining market acceptance of new technology, products and services, it would have a material adverse effect on our ability to retain existing customers and attract new ones in the impacted business line.

Our debt obligations, or our incurrence of additional debt obligations, could limit our flexibility in managing our business and could materially and adversely effect our financial performance.

As of September 30, 2010, we had approximately $323.5 million of long-term indebtedness outstanding. In addition, we are permitted under our credit agreement to incur additional indebtedness, subject to specified limitations. Our substantial indebtedness currently outstanding, or as may be outstanding if we incur additional indebtedness, could have important consequences, including the following:

| • | we may have difficulty satisfying our obligations under our debt facilities and, if we fail to satisfy these obligations, an event of default could result; |

15

Table of Contents

Index to Financial Statements

| • | we may be required to dedicate a substantial portion of our cash flow from operations to required payments on our indebtedness, thereby reducing the availability of cash flow for acquisitions, working capital, capital expenditures and other general corporate activities. See “Management’s discussion and analysis of financial condition and results of operations—Contractual obligations,” which sets forth our payment obligations with respect to our existing long-term debt; |

| • | covenants relating to our debt may limit our ability to enter into certain contracts or to obtain additional financing for acquisitions, working capital, capital expenditures and other general corporate activities; |

| • | covenants relating to our debt may limit our flexibility in planning for, or reacting to, changes in our business and the industry in which we operate, including by restricting our ability to make strategic acquisitions; |

| • | we may be more vulnerable than our competitors to the impact of economic downturns and adverse developments in the industry in which we operate; |

| • | we are exposed to the risk of increased interest rates because certain of our borrowings are subject to variable rates of interest; |

| • | although we have no current intention to pay any dividends, we may be unable to pay dividends or make other distributions with respect to your investment; and |

| • | we may be placed at a competitive disadvantage against any less leveraged competitors. |

The occurrence of one or more of these potential consequences could have a material adverse effect on our business, financial condition, operating results, and ability to satisfy our obligations under our indebtedness.

In addition, we and our subsidiaries may be able to incur substantial additional indebtedness in the future. Although our credit agreement contains restrictions on the incurrence of additional indebtedness, these restrictions are subject to a number of significant qualifications and exceptions, and under certain circumstances, the amount of additional indebtedness that could be incurred in compliance with these restrictions could be substantial. If new debt is added to our existing debt levels, the related risks that we will face would increase.

We meet a significant portion of our working capital needs through a securitization facility, which we must renew on an annual basis.

We meet a significant portion of our working capital needs through a securitization facility, pursuant to which we sell accounts receivable to a special-purpose entity that in turn sells undivided participation interests in the accounts receivable to certain purchasers, who finance their purchases through the issuance of short-term commercial paper. The securitization facility has a one year term. During the financial crisis that began in 2008, the market for commercial paper experienced significant volatility. Although we have been able to renew our securitization facility annually, there can be no assurance that we will continue to be able to renew this facility in the future on terms acceptable to us.

A significant rise in fuel prices could cause our accounts receivable to increase beyond the capacity of the securitization facility. There can be no assurance that the size of the facility can be expanded to meet these increased working capital needs. Further, we may not be able to fund such increases in accounts receivable with our available cash resources. Our inability to meet working capital needs could adversely affect our financial condition and business, including our relationships with merchants, customers and partners. Further, we are exposed to the risk of increased interest rates because our borrowings under the securitization facility are subject to variable rates of interest.

16

Table of Contents

Index to Financial Statements

We are subject to risks related to volatility in foreign currency exchange rates, and restrictions on our ability to utilize revenue generated in foreign currencies.

As a result of our foreign operations, we are subject to risks related to changes in currency rates for revenue generated in currencies other than the U.S. dollar. For the year ended December 31, 2009 and the nine months ended September 30, 2010, approximately 36.0% and 33.0% of our revenue, respectively, was denominated in currencies other than the U.S. dollar (primarily Czech koruna and British pound). Revenue and profit generated by international operations may increase or decrease compared to prior periods as a result of changes in foreign currency exchange rates. Resulting exchange gains and losses are included in our net income. Volatility in foreign currency exchange rates may materially adversely affect our operating results and financial condition.

Furthermore, we are subject to exchange control regulations that restrict or prohibit the conversion of more than a specified amount of our foreign currencies into U.S. dollars, and, as we expand, we may become subject to further exchange control regulations that limit our ability to freely utilize and transfer currency in and out of particular jurisdictions. These restrictions may make it more difficult to effectively utilize the cash generated by our operations and may adversely effect our financial condition.

We conduct a significant portion of our business in foreign countries and we expect to expand our operations into additional foreign countries where we may be adversely affected by operational and political risks that are greater than in the United States.

We have foreign operations in, or provide services in, Belarus, Belgium, Canada, the Czech Republic, Estonia, Ireland, Latvia, Lithuania, Luxembourg, the Netherlands, Pakistan, Poland, the Russian Federation, Slovakia, South Africa, Ukraine and the United Kingdom. We also expect to seek to expand our operations into various countries in Asia, Europe and Latin America as part of our growth strategy.

Some of the countries where we operate, and other countries where we will seek to operate, have undergone significant political, economic and social change in recent years, and the risk of unforeseen changes in these countries may be greater than in the United States. In particular, changes in laws or regulations, including with respect to taxation, information technology, data transmission and the Internet, or in the interpretation of existing laws or regulations, whether caused by a change in government or otherwise, could materially adversely affect our business, operating results and financial condition. In addition, conducting and expanding our international operations subjects us to other risks that we do not generally face in the United States. These include:

| • | difficulties in managing the staffing of our international operations, including hiring and retaining qualified employees; |

| • | increased expense related to localization of our products and services, including language translation and the creation of localized agreements; |

| • | potentially adverse tax consequences, including the complexities of foreign value added tax systems, restrictions on the repatriation of earnings and changes in tax rates; |

| • | increased expense to comply with foreign laws and legal standards, including laws that regulate pricing and promotion activities and the import and export of information technology, which can be difficult to monitor and are often subject to change; |

| • | increased expense to comply with U.S. laws that apply to foreign operations, including the Foreign Corrupt Practices Act and Office of Foreign Assets Control regulations; |

| • | longer accounts receivable payment cycles and difficulties in collecting accounts receivable; |

| • | increased financial accounting and reporting burdens and complexities; |

17

Table of Contents

Index to Financial Statements

| • | political, social and economic instability; |

| • | terrorist attacks and security concerns in general; and |

| • | reduced or varied protection for intellectual property rights and cultural norms in some geographies that are simply not respectful of intellectual property rights. |

The occurrence of one or more of these events could negatively affect our international operations and, consequently, our operating results. Further, operating in international markets requires significant management attention and financial resources. Due to the additional uncertainties and risks of doing business in foreign jurisdictions, international acquisitions tend to entail risks and require additional oversight and management attention that are typically not attendant to acquisitions made within the United States. We cannot be certain that the investment and additional resources required to establish, acquire or integrate operations in other countries will produce desired levels of revenue or profitability.

We are dependent on technology systems and electronic communications networks managed by third parties, which could result in our inability to prevent disruptions in our services.

Our ability to process and authorize transactions electronically depends on our ability to communicate with our fuel, lodging and vehicle maintenance providers electronically through point-of-sale devices and electronic networks that are owned and operated by third parties. In addition, in order to process transactions promptly, our computer equipment and network servers must be functional 24 hours a day, which requires access to telecommunications facilities managed by third-parties and the availability of electricity, which we do not control. A severe disruption of one or more of these networks, including as a result of utility or third-party system interruptions, could impair our ability to authorize transactions and process information, which could harm our reputation, result in a loss of customers or partners and adversely affect our business and operating results.