Attached files

| file | filename |

|---|---|

| 8-K - WILLIS GROUP HOLDINGS PLC 8-K - WILLIS TOWERS WATSON PLC | a6512854.htm |

Exhibit 99.1

1 WILLIS GROUP HOLDINGS FACT BOOK For the quarter ended September 30, 2010

2 Leading global insurance brokerBroad range of professional insurance, reinsurance, risk management, financial and human resource consulting and actuarial services Global distribution capabilities to meet risk management needs of large multinational and middle market clientsMore than 400 offices in 120 countries, with approximately 17,000 employees2009 total revenues $3.3 billionStrong sales culture and relentless focus on cost controlMarket capitalization $5.7 billion (as of November 12, 2010) Willis snapshot

3 Group financial summary – 3Q 2010 1 percent reported growth in commissions and fees (C&F) 4 percent organic growth in C&F - strong new business generation and steady retention2 percent in North America, 6 percent in International, and4 percent in Global (reinsurance and specialties) 14.5 percent reported and adjusted operating margin Organic revenue growth, rigorous expense management and favorable FX, partially offset by higher incentive compensation Shaping our Future (profitable growth initiatives) net benefits of approximately $12 millionReported and adjusted EPS from continuing operations of $0.37 (includes $0.02 of favorable FX) Organic growth in commissions and fees in each segment; rigorous expense management See important disclosures regarding Non-GAAP measures on page 26 ($ in millions, except for adjusted EPS)

4 Group financial summary – 3Q YTD 2010 3 percent reported growth in C&F4 percent organic growth in C&F1 percent in North America, 6 percent in International, and 6 percent in Global (reinsurance and specialties) 150 basis points increase in adjusted operating margin Organic revenue growth and cost discipline while investing in current and future growthShaping our Future (profitable growth initiatives) net benefits of approximately $37 millionAdjusted EPS from continuing operations of $2.18 (includes $0.11 of favorable FX)Continued solid performance; organic growth across all segments and ongoing cost discipline while funding current and future growth ($ in millions, except for adjusted EPS) See important disclosures regarding Non-GAAP measures on page 26

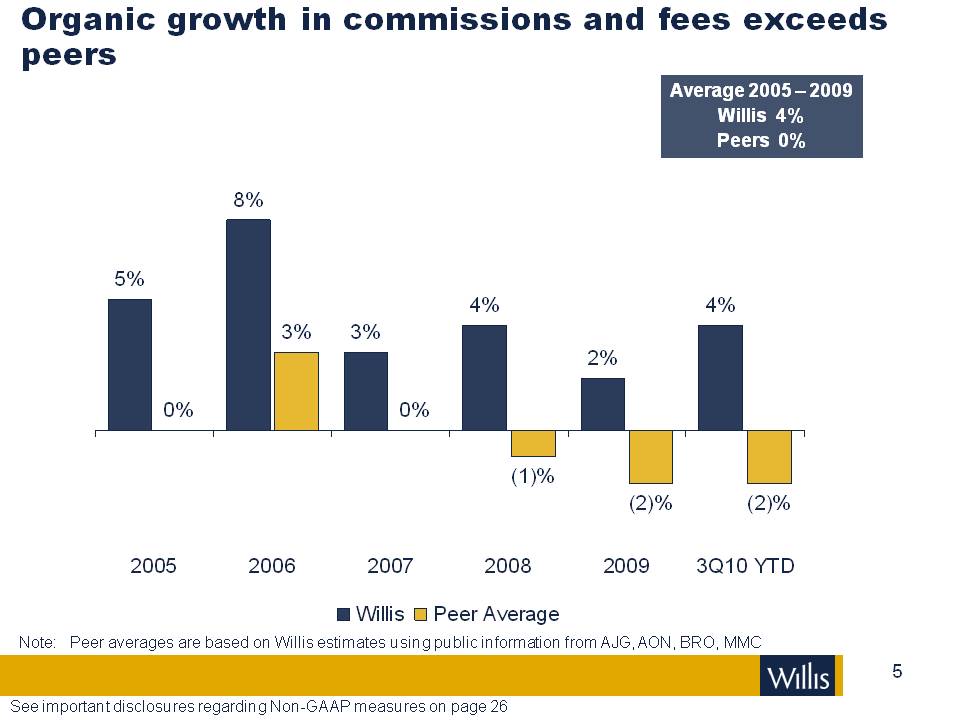

5 Organic growth in commissions and fees exceeds peers Average 2005 – 2009 Willis 4% Peers 0% Note: Peer averages are based on Willis estimates using public information from AJG, AON, BRO, MMC See important disclosures regarding Non-GAAP measures on page 26

6 Growth driven by strong new business production % Organic growth in commissions and fees See important disclosures regarding Non-GAAP measures on page 26 6% average net newunderlying business 2005 – 2009

7 Adjusted operating margin exceeds peers Average 2005 – 2009 Willis 22% Peers 20% See important disclosures regarding Non-GAAP measures on page 26 Note: Peer averages are based on Willis estimates using public information from AJG, AON, BRO, MMC

8 Segment highlights – 3Q 2010 NORTH AMERICA INTERNATIONAL Organic C&F growth of 2 percent, up from negative 3 percent in year ago quarter Double-digit new business generation, improved retention with continued soft market and economic headwinds Employee Benefits up 4 percent, strong results from specialty businesses; including Executive Risk, Healthcare and Financial Services Operating margin of 21.4 percent Organic C&F growth of 6 percent; double digit new business generation Double digit organic growth in Latin America, Asia and Eastern Europe UK positive for second sequential quarter Operating margin of 9.6 percent; organic growth negated by unfavorable FX GLOBAL Strong organic C&F growth of 4 percent, strong new business generation Reinsurance organic growth in mid-single digits; strong new business while market remains soft Global Specialties organic growth in mid-single digits, led by Financial and Executive Risk, Inspace, Aerospace and Construction, despite ongoing tough environment Operating margin of 19.7 percent 2009 COMMISSIONS AND FEES See important disclosures regarding Non-GAAP measures on page 26

9 Segment highlights – 3Q YTD 2010 NORTH AMERICA INTERNATIONAL Organic C&F growth of 1 percent, up from negative 5 percent in year ago quarter Double-digit new business generation, improved retention with continued soft market and economic headwinds Employee Benefits up 2 percent, strong results from specialty businesses; including Healthcare and Financial ServicesOperating margin of 22.6 percent Organic C&F growth of 6 percent; double digit new business generation Double digit organic growth in Latin America, Asia and Eastern Europe Positive growth in the UK, with continued economic headwinds Operating margin of 23.7 percent GLOBAL Strong organic C&F growth of 6 percent, strong new business generation Reinsurance organic growth in mid-single digits; strong new business while market remains soft Global Specialties organic growth in mid-single digits, led by Financial and Executive Risk, and Construction, despite ongoing tough environmentOperating margin of 34.6 percent 2009 COMMISSIONS AND FEES See important disclosures regarding Non-GAAP measures on page 26

10 Willis North America overview Segment overview 2009 commissions and fees 2009 = $1,368 million Body: Extensive retail platform with leading positions in major markets Distribution network for all core businesses Client centric approach Able to leverage industry and specialty practice group expertise across network Major practice groups include: Employee Benefits (approximately 20 percent of 2009 North America C&F) Construction (approximately 10 percent of 2009 North America C&F) Financial and Executive Risk CAPPPS (Captives/Programs)

11 Segment overview 2009 commissions and fees Willis International overview Body: Represents all of the Group’s retail operations excluding US & Canada Network of subsidiaries, affiliates and correspondents in more than 100 countries; leading positions in UK, France, Scandinavia, China and Russia Offices designed to grow business locally around the world, making use of the skills, industry knowledge and expertise available elsewhere in the Group International operations produce significant flows of revenue for retail network and Global Specialties International Employee Benefits generated approximately 10 percent of 2009 International C&F 2009 = $1,020 million

12 Segment overview 2009 commissions and fees 2009 = $822 million Willis Global overview Body: Reinsurance Willis Re One of only three global reinsurance brokers Significant market share in major markets, particularly marine and aviation Cutting edge analytical and advisory services, including Willis Research Network Complete range of transactional capabilities including, in conjunction with Willis Capital Markets & Advisory, risk transfer via the capital markets

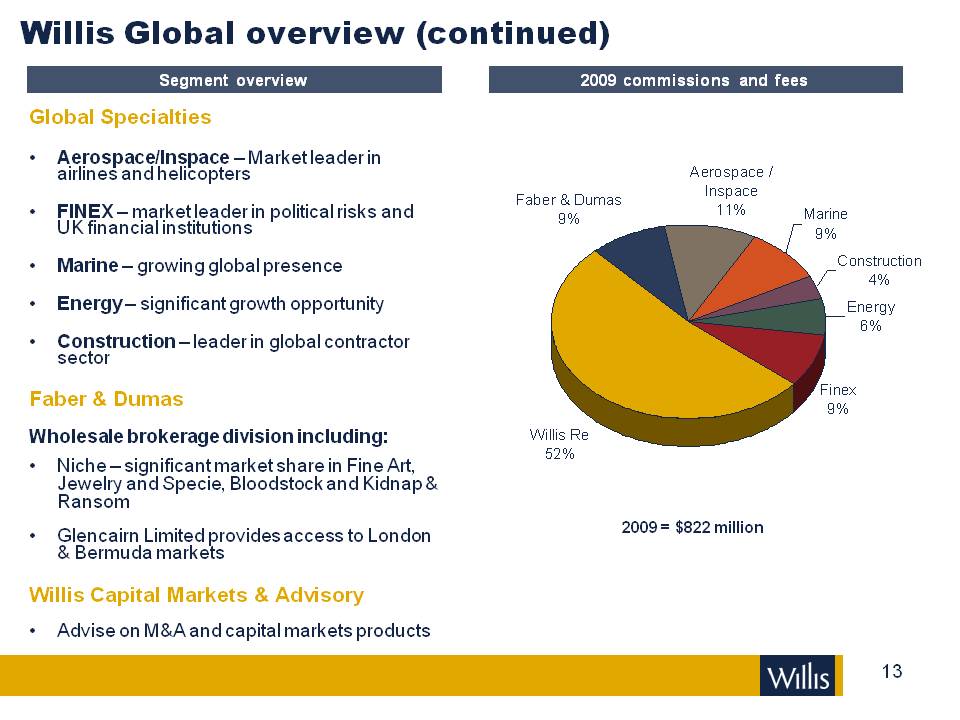

13 Segment overview 2009 commissions and fees Willis Global overview (continued) Body: Global Specialties Aerospace/Inspace – Market leader in airlines and helicopters FINEX – market leader in political risks and UK financial institutions Marine – growing global presence Energy – significant growth opportunity Construction – leader in global contractor sector Faber & Dumas Wholesale brokerage division including: Niche – significant market share in Fine Art, Jewelry and Specie, Bloodstock and Kidnap & Ransom Glencairn Limited provides access to London & Bermuda markets Willis Capital Markets & Advisory Advise on M&A and capital markets products 2009 = $822 million

14 Adjusted cash flow is defined as cash flow from operating and investing activities excluding acquisitions and disposals, and other items listed below: Additional pension contributions of $31 million, $107 million, $153 million, $211 million and $50 million, for LTM 3Q10, 2008, 2007, 2006, and 2005, respectively. Cash flow in LTM 3Q10, 2009, 2008 and 2007 excludes $30 million, $30 million, $41 million and $106 million, respectively, related to one-time spending on new US and UK head offices. 2006 cash flow excludes $202 million received from the sale of our London headquarters and $76 million invested in the Shaping our Future initiatives. 2005 cash flow also excludes $155 million impact of new Financial Services Authority regulations which came into force in the UK in 2005 and regulatory settlement payment of $51 million. LTM 3Q10 cash flow excludes $12 million impact of Venezuela currency devaluation. Adjusted cash flow (1) ($ millions) Strong cash flow See important disclosures regarding Non-GAAP measures on page 26 Cash and cash equivalents of $141 million at September 30, 2009Dividends $174 million paid in 2009 2010 debt repayments $112 million on term loan $83 million 2010 bond maturities Ordinary stock buyback program $1 billion current buyback approval; $925 million outstanding

15 Total debt approximately $2.3 billion RatingsMoody’s Baa3 (stable outlook) Standard & Poor’s BBB- (stable outlook)Significantly improved debt maturity profile ($ in millions) Debt and maturity profile 2010 mandatory debt repayments of $112 million on term loan (approx $84 million paid through 9M10) $83 million 2010 bond maturities (paid 3Q10) 5.125% L + 225 L+ 225 L+ 225 5.625% 12.875% 6.20% 7.00%L+ 225 Swap

16 2010 Focus

17 The Willis CauseContinue to drive industry leading revenue growthContinue to execute Shaping our FutureFunding for Growth - incremental savings to support current and future growth initiatives Main priorities See important disclosures regarding forward-looking statements on page 25

18 We thoroughly understand our clients’ needs and their industriesWe develop client solutions with the best markets, price and termsWe relentlessly deliver quality client serviceWe get claims paid quickly The Willis Cause WITH INTEGRITY See important disclosures regarding forward-looking statements on page 25

19 Delivering the Willis Cause CLIENT UNDERSTANDING SERVICE QUALITY CLAIMS PAID Segments Specialization Analytics Client profitability Sales operations Client advocacy Placement proposition Programs & facilities Placement organization WillPlace Willis Quality Index Willis Capital Markets Operational excellence TOM / EPIC SoF Retail SoF London Service centers Metrics Contract certainty Carrier relationships Claims advocacy Claim metrics… WITH INTEGRITY BEST SOLUTION See important disclosures regarding forward-looking statements on page 25

20 Further develop aggressive sales cultureFurther enhance Client AdvocacyContinue to make strategic hiresReinsuranceInternationalSpecialty lines (Energy, Marine, Aerospace)Build on already strong client retentionMonitor specific growth metrics for all regions, countries and linesImprove tracking of the sales pipelineDriving growth Despite industry leading growth, we believe there is an opportunity to further drive top line growth See important disclosures regarding forward-looking statements on page 25

21 Shaping our Future continues to deliver Cumulative SOF gross and net benefits($ millions) See important disclosures regarding forward-looking statements on page 24 2010 priorities:Greater emphasis on retention, cross-selling and pipeline initiativesFurther development of global marketing capabilitiesFurther develop retail platform initiativesTechnology infrastructure programs, process changes and use of support and service centers continue to drive efficiencies and increase service performance

22 Funding for Growth 2010 Generate incremental savings in 2010 to invest in new producers and growth initiatives Drive incremental growth and create a real sales culture through best practice in growth drivers Out-recruiting competitors with producer pipelines Developing new products or packages Developing new clients with existing products Systematic and scientific cross-sell campaigns Drive new business growth and higher retention levels Closely manage savings and only invest when savings achieved STRATEGY EXECUTION RESULTS See important disclosures regarding forward-looking statements on page 25

23 Wrap up – 3Q10 Willis 3Q10 performance4 percent organic growth in C&F; organic growth in each segmentStrong new business generation and steady retention14.5 percent reported and adjusted operating margin reflects organic revenue growth, rigorous expense management and favorable FX, partially offset by higher incentive compensation Reported and adjusted EPS from continuing operations of $0.37Willis 2010The Willis CauseSolid underlying business fundamentals in placeEconomic environment continues to present challenges Continue to drive industry leading revenue growthFocus on Funding for Growth – incremental savings to be invested in growth initiatives See important disclosures regarding forward-looking statements and important disclosures regarding Non-GAAP measures on page 25

24 Appendix

25 Important disclosures regarding forward-looking statements This presentation contains certain “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, and Section 21E of the Securities Exchange Act of 1934, which are intended to be covered by the safe harbors created by those laws. These forward-looking statements include information about possible or assumed future results of our operations. All statements, other than statements of historical facts, included in this document that address activities, events or developments that we expect or anticipate may occur in the future, including such things as our outlook, future capital expenditures, growth in commissions and fees, business strategies, competitive strengths, goals, the benefits of new initiatives, growth of our business and operations, plans, and references to future successes are forward-looking statements. Also, when we use the words such as ‘anticipate’, ‘believe’, ‘estimate’, ‘expect’, ‘intend’, ‘plan’, ‘probably’, or similar expressions, we are making forward-looking statements. There are important uncertainties, events and factors that could cause our actual results or performance to differ materially from those in the forward-looking statements contained in this document, including the following: the impact of any regional, national or global political, economic, business, competitive, market, environmental and regulatory conditions on our global business operations; the impact of current financial market conditions on our results of operations and financial condition, including as a result of any insolvencies or other difficulties experienced by our clients, insurance companies or financial institutions; our ability to continue to manage our significant indebtedness; our ability to compete effectively in our industry; our ability to implement or realize anticipated benefits of the Shaping Our Future, Right Sizing Willis, Funding for Growth initiatives or any other new initiatives; material changes in commercial property and casualty markets generally or the availability of insurance products or changes in premiums resulting from a catastrophic event, such as a hurricane, or otherwise; the volatility or declines in other insurance markets and the premiums on which our commissions are based, but which we do not control; our ability to retain key employees and clients and attract new business; the timing or ability to carry out share repurchases or take other steps to manage our capital and the limitations in our long-term debt agreements that may restrict our ability to take these actions; any fluctuations in exchange and interest rates that could affect expenses and revenue; rating agency actions that could inhibit ability to borrow funds or the pricing thereof; a significant decline in the value of investments that fund our pension plans or changes in our pension plan funding obligations; our ability to achieve the expected strategic benefits of transactions; changes in the tax or accounting treatment of our operations; any potential impact from the US healthcare reform legislation; the potential costs and difficulties in complying with a wide variety of foreign laws and regulations and any related changes, given the global scope of our operations; our involvements in and the results of any regulatory investigations, legal proceedings and other contingencies; underwriting, advisory and reputational risks we assume in connection with our non-core operations; our exposure to potential liabilities arising from errors and omissions and other potential claims against us; and the interruption or loss of our information processing systems or failure to maintain secure information systems. The foregoing list of factors is not exhaustive and new factors may emerge from time to time that could also affect actual performance and results. For additional information see also Part I, Item 1A “Risk Factors” included in Willis’ Form 10-K for the year ended December 31, 2009, and our subsequent filings with the Securities and Exchange Commission. Copies are available online at http://www.sec.gov or on request from the Company. Although we believe that the assumptions underlying our forward-looking statements are reasonable, any of these assumptions, and therefore also the forward-looking statements based on these assumptions, could themselves prove to be inaccurate. In light of the significant uncertainties inherent in the forward-looking statements included in this presentation, our inclusion of this information is not a representation or guarantee by us that our objectives and plans will be achieved. Our forward-looking statements speak only as of the date made and we will not update these forward-looking statements unless the securities laws require us to do so. In light of these risks, uncertainties and assumptions, the forward-looking events discussed in this presentation may not occur, and we caution you against unduly relying on these forward-looking statements.

26 This presentation contains references to "non-GAAP financial measures" as defined in Regulation G of SEC rules. We present these measures because we believe they are of interest to the investment community and they provide additional meaningful methods of evaluating certain aspects of the Company’s operating performance from period to period on a basis that may not be otherwise apparent on a generally accepted accounting principles (GAAP) basis. These financial measures should be viewed in addition to, not in lieu of, the Company’s condensed consolidated income statements and balance sheet as of the relevant date. Consistent with Regulation G, a description of such information is provided below and a reconciliation of certain of such items to GAAP information can be found in our periodic filings with the SEC. Our method of calculating these non-GAAP financial measures may differ from other companies and therefore comparability may be limited. Important disclosures regarding Non-GAAP measures Adjusted earnings per share from continuing operations (Adjusted EPS from continuing operations) is defined as adjusted net income from continuing operations per diluted share. Adjusted net income from continuing operations is defined as net income from continuing operations, excluding certain items as set out on pages 29 and 30. Adjusted operating income is defined as operating income, excluding certain items as set out on pages 27 and 28. Adjusted operating margin is defined as the percentage of adjusted operating income to total revenues. Adjusted cash flow is defined as cash flow from operating and investing activities excluding acquisitions and disposals and certain items as set out on page 14. Organic commissions & fees growth excludes: (i) the impact of foreign currency translation; (ii) the first twelve months of net commission and fee revenues generated from acquisitions; (iii) the net commission and fee revenues related to operations disposed of in each period presented; (iv) in North America, legacy contingent commissions assumed as part of the HRH acquisition and that had not been converted into higher standard commission; and (v) investment income and other income from reported revenues, as set out on pages 31 and 32. Reconciliations to GAAP measures are provided for selected non-GAAP measures.

27 Important disclosures regarding Non-GAAP measures (continued) See related footnotes on page 33 Operating Income to Adjusted Operating Income 20052006200720082009(In millions) FY FY FY FY FY Operating Income, GAAP Basis$451 $552 $620 $503 $694 Excluding:Venezuela currency devaluation (a)-----Net (gain)/loss on disposal of operations(78)4 (2)-(13)Salaries and benefits - severance costs (b)28 35 -24 -Salaries and benefits – other (c)---42 -Regulatory settlements and related costs (d)60 ----Legal settlement20 ----Shaping our Future expenditure (e)-59 ---Gain on disposal of London headquarters (f)-(99)---HRH integration costs (g)---5 18 Other operating expenses (h)---26 -Accelerated amortization of intangibles assets (i)----7 Redomicile costs (j)----6 Adjusted Operating Income$481 $551 $618 $600 $712 Operating Margin, GAAP basis19.9%22.7%24.0%17.8%21.3% Adjusted Operating Margin21.2%22.7%24.0%21.2%21.8%

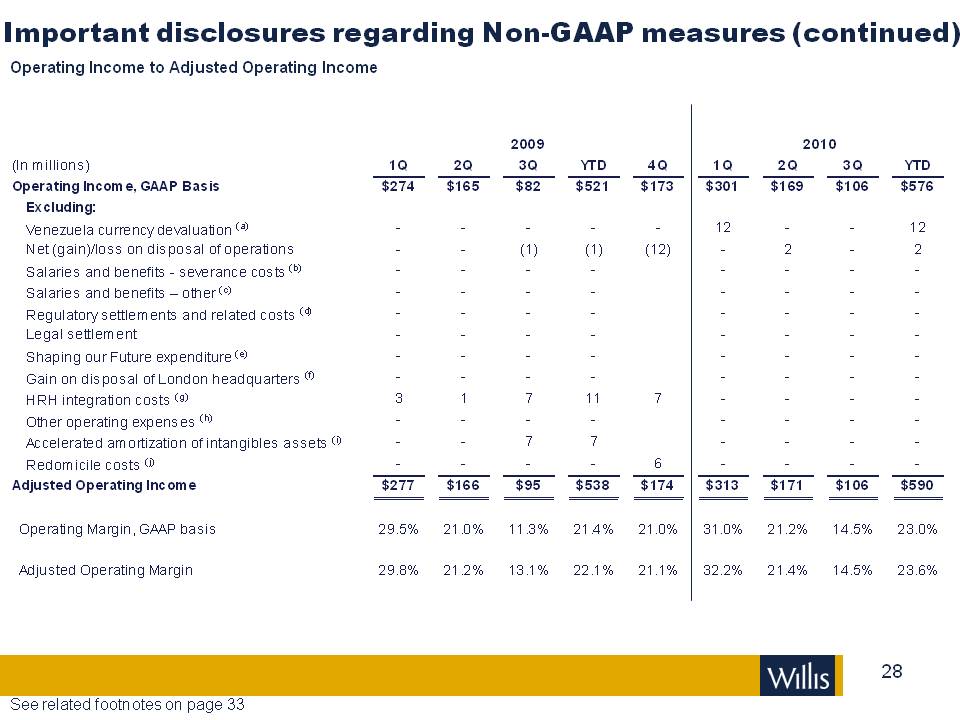

28 Important disclosures regarding Non-GAAP measures (continued) See related footnotes on page 33 Operating Income to Adjusted Operating Income 20092010(In millions) 1Q 2Q 3Q YTD 4Q 1Q 2Q 3Q YTD Operating Income, GAAP Basis$274 $165 $82 $521 $173 $301 $169 $106 $576 Excluding:Venezuela currency devaluation (a)-----12 --12 Net (gain)/loss on disposal of operations--(1)(1)(12)-2 -2 Salaries and benefits - severance costs (b)--------Salaries and benefits – other (c)--------Regulatory settlements and related costs (d)--------Legal settlement--------Shaping our Future expenditure (e)--------Gain on disposal of London headquarters (f)--------HRH integration costs (g)3 1 7 11 7 ----Other operating expenses (h)--------Accelerated amortization of intangibles assets (i)--7 7 ----Redomicile costs (j)----6 ----Adjusted Operating Income$277 $166 $95 $538 $174 $313 $171 $106 $590 Operating Margin, GAAP basis29.5%21.0%11.3%21.4%21.0%31.0%21.2%14.5%23.0% Adjusted Operating Margin29.8%21.2%13.1%22.1%21.1%32.2%21.4%14.5%23.6%

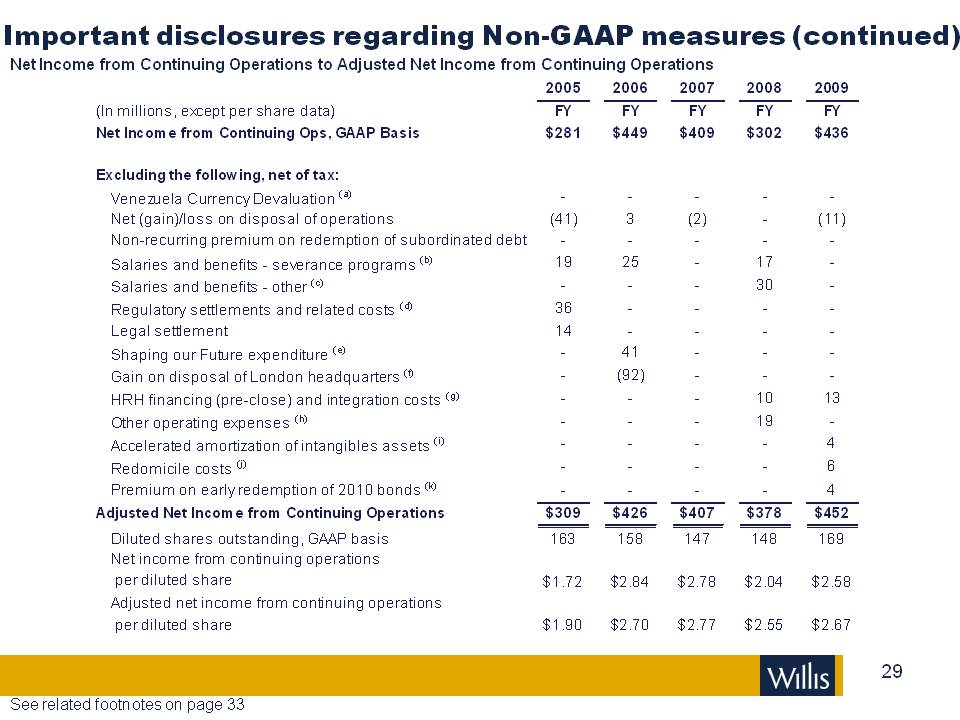

29 Important disclosures regarding Non-GAAP measures (continued) See related footnotes on page 33 Net Income from Continuing Operations to Adjusted Net Income from Continuing Operations 20052006200720082009(In millions, except per share data)FYFYFYFYFYNet Income from Continuing Ops, GAAP Basis$281 $449 $409 $302 $436 Excluding the following, net of tax:Venezuela Currency Devaluation (a)-----Net (gain)/loss on disposal of operations(41)3 (2)-(11)Non-recurring premium on redemption of subordinated debt-----Salaries and benefits - severance programs (b)19 25 -17 -Salaries and benefits - other (c)---30 -Regulatory settlements and related costs (d)36 ----Legal settlement14 ----Shaping our Future expenditure (e)-41 ---Gain on disposal of London headquarters (f)-(92)---HRH financing (pre-close) and integration costs (g)---10 13 Other operating expenses (h)---19 -Accelerated amortization of intangibles assets (i)----4 Redomicile costs (j)----6 Premium on early redemption of 2010 bonds (k)----4 Adjusted Net Income from Continuing Operations$309 $426 $407 $378 $452 Diluted shares outstanding, GAAP basis163158147148169Net income from continuing operations per diluted shareAdjusted net income from continuing operations per diluted share$2.55 $2.67

30 Important disclosures regarding Non-GAAP measures (continued) See related footnotes on page 33 Net Income from Continuing Operations to Adjusted Net Income from Continuing Operations 20092010(In millions, except per share data)1Q2Q3QYTD4Q1Q2Q3QYTDNet Income from Continuing Ops, GAAP Basis$192 $87 $78 $357 $79 $204 $89 $64 $357 Excluding the following, net of tax:Venezuela Currency Devaluation (a)-----12 --12 Net (gain)/loss on disposal of operations--(1)(1)(10)-3 -3 Non-recurring premium on redemption of subordinated debt---------Salaries and benefits - severance programs (b)---------Salaries and benefits - other (c)---------Regulatory settlements and related costs (d)---------Legal settlement---------Shaping our Future expenditure (e)---------Gain on disposal of London headquarters (f)---------HRH financing (pre-close) and integration costs (g)2 1 5 8 5 ----Other operating expenses (h)---------Accelerated amortization of intangibles assets (i)--4 4 -----Redomicile costs (j)----6 ----Premium on early redemption of 2010 bonds (k)--4 4 -----Adjusted Net Income from Continuing Operations$194 $88 $90 $372 $80 $216 $92 $64 $372 Diluted shares outstanding, GAAP basis167168169168169170171171171Net income from continuing operations per diluted shareAdjusted net income from continuing operations per diluted share$1.15 $0.52 $2.13 $2.09 $1.16 $0.52 $2.21 $1.20 $0.54 $0.37 $0.52 $0.37 $2.18

31 Commissions and Fees Analysis* Important disclosures regarding Non-GAAP measures (continued) 20092008ChangeForeign currency translationAcquisitions and disposalsOrganic commissions and fees growth($ millions)%%%%2009 Full yearGlobal$822 $784 5 (3)4 4 North America1,36890551 0 54 (3)International1,0201,055(3)(8)1 4 Commissions and Fees$3,210 $2,744 17 (4)19 2 20082007ChangeForeign currency translationAcquisitions and disposalsOrganic commissions and fees growth($ millions)%%%%2008 Full yearGlobal$784 $750 5 0 3 2 North America90575121 0 22 (1)International1,05596210 1 0 9 Commissions and Fees$2,744 $2,463 11 1 6 4

32 Commissions and Fees Analysis* Important disclosures regarding Non-GAAP measures (continued)* Included in North America reported commissions and fees were legacy HRH contingent commissions of $1 million in the third quarter of 2010 compared with $2 million in the third quarter of 2009 and $11 million in the first nine months of 2010 compared with $26 million in the first nine months of 2009. 2010 2009 ChangeForeign currency translation Acquisitions and disposalsContingent CommissionsOrganic commissions and fees growth($ millions)%%%%%Three months ended September 30, Global $181 $175 3 (2)1 0 4 North America3283202 0 0 0 2 International214219(2)(7)(1)0 6 Commissions and Fees$723 $714 1 (3)0 0 4 Nine months ended September 30, Global$698 $657 6 0 0 0 6 North America1,0151,023(1)0 0 (2)1 International7627216 (1)1 0 6 Commissions and Fees$2,475 $2,401 3 0 1 (2)4

33 Important disclosures regarding Non-GAAP measures (continued) Notes to the Operating Income to Adjusted Operating Income reconciliation and Net Income from Continuing Operations to Adjusted Net Income from Continuing Operations reconciliation With effect from January 1, 2010, the Venezuelan economy was designated as hyper-inflationary. The Venezuelan government also devalued the Bolivar Fuerte in January 2010. As a result of these actions, the Company recorded a one-time charge in other expenses to reflect the re-measurement of its net assets denominated in Venezuelan Bolivar Fuerte.Severance costs excluded from adjusted operating income and adjusted net income in 2008 relate to approximately 350 positions through the year ended December 31, 2008 that were eliminated as part of the 2008 expense review. Severance costs also arise in the normal course of business and these charges (pre-tax) amounted to $3 million and $2 million for the second quarter of 2010 and 2009, respectively, $11 million and $18 million for the first six months of 2010 and 2009, respectively, and $24 million and $2 million for the years ended December 31, 2009 and 2008, respectively.Other 2008 expense review salaries and benefits costs relate primarily to contract buyouts.Comprises $51 million to establish the reimbursement funds agreed with the New York and Minnesota Attorneys General and New York Department of Insurance in April 2005 and $9 million of related legal and administrative expensesIn addition to severance costs and a net loss on disposal of operations, the Company incurred significant additional expenditure in 2006 to launch its strategic initiatives, including professional fees, lease termination costs and vacant space provisions.The gain on disposal of London headquarters is shown net of leaseback costs.2009 HRH integration costs include $nil million severance costs ($2 million in 2008).Other operating expenses primarily relate to property and systems rationalization.The charge for the accelerated amortization for intangibles relates to the HRH brand name. Following the successful integration of HRH into our North American operations, we announced on October 1, 2009 that our North America retail operations would change their name from Willis HRH to Willis North America. Consequently, the intangible asset recognized on the acquisition of HRH relating to the HRH brand has been fully amortized.These are legal and professional fees incurred as part of the Company’s redomicile of its parent Company from Bermuda to Ireland.On September 29, 2009 we repurchased $160 million of our 5.125 percent Senior Notes due July 2010 at a premium of $27.50 per $1,000 face value, resulting in a total pre-tax premium on redemption, including fees, of pre-tax $5 million.

34 WILLIS GROUP HOLDINGS FACT BOOK For the quarter ended September 30, 2010