Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K Q3 2010 - KITE REALTY GROUP TRUST | form8kq3_2010.htm |

| EX-99.1 - EXHIBIT 99.1 PRESS RELEASE - KITE REALTY GROUP TRUST | exhibit99_1.htm |

EXHIBIT 99.2

KITE REALTY GROUP TRUST

SEPTEMBER 30, 2010

INVESTOR RELATIONS CONTACTS:

Dan Sink, Chief Financial Officer

Adam Chavers, Vice President, Acquisitions & Investor Relations

|

30 S. MERIDIAN STREET • INDIANAPOLIS, INDIANA 46204 • 317.577.5600

|

|

SUPPLEMENTAL INFORMATION – SEPTEMBER 30, 2010

|

PAGE NO.

|

TABLE OF CONTENTS

|

|

|

3

|

Corporate Profile

|

|

|

4

|

Contact Information

|

|

|

5

|

Important Notes

|

|

|

6

|

Corporate Structure Chart

|

|

|

7

|

Condensed Consolidated Balance Sheets

|

|

|

8

|

Condensed Consolidated Statements of Operations for the Three and Nine Months Ended September 30

|

|

|

9

|

Funds from Operations and Other Financial Information for the Three and Nine Months Ended September 30

|

|

|

10

|

Market Capitalization

|

|

|

10

|

Ratio of Debt to Total Undepreciated Assets as of September 30, 2010

|

|

|

11

|

Same Property Net Operating Income for the Three and Nine Months Ended September 30

|

|

|

12

|

Net Operating Income by Quarter

|

|

|

13

|

Summary of Outstanding Debt as of September 30, 2010

|

|

|

14

|

Schedule of Outstanding Debt as of September 30, 2010

|

|

|

17

|

Joint Venture Summary – Unconsolidated Properties

|

|

|

18

|

Condensed Combined Balance Sheets of Unconsolidated Properties

|

|

|

19

|

Condensed Combined Statements of Operations of Unconsolidated Properties for the Three and Nine Months Ended September 30

|

|

|

20

|

Top 10 Retail Tenants by Gross Leasable Area

|

|

|

21

|

Top 25 Tenants by Annualized Base Rent

|

|

|

22

|

Lease Expirations – Operating Portfolio

|

|

|

23

|

Lease Expirations – Retail Anchor Tenants

|

|

|

24

|

Lease Expirations – Retail Shops

|

|

|

25

|

Lease Expirations – Commercial Tenants

|

|

|

26

|

Summary Retail Portfolio Statistics Including Joint Venture Properties

|

|

|

27

|

Summary Commercial Portfolio Statistics

|

|

|

28

|

Current Development Pipeline

|

|

|

29

|

Current Redevelopment Projects

|

|

|

30

|

Shadow Pipeline

|

|

|

31

|

Geographic Diversification – Operating Portfolio

|

|

|

32

|

Operating Retail Properties

|

|

|

36

|

Operating Commercial Properties

|

|

|

37

|

Retail Operating Portfolio – Tenant Breakdown

|

Kite Realty Group Trust Supplemental Financial and Operating Statistics – 9/30/10

p.2

CORPORATE PROFILE

General Description

Kite Realty Group Trust is a full-service, vertically integrated real estate company engaged primarily in the development, construction, acquisition, ownership and operation of high-quality neighborhood and community shopping centers in selected markets in the United States. We are organized as a real estate investment trust ("REIT") for federal income tax purposes. As of September 30, 2010, we owned interests in 60 properties totaling approximately 8.9 million square feet and an additional 0.6 million square feet in two properties currently under development.

Our strategy is to maximize the cash flow of our operating properties, successfully complete the construction and lease-up of our development portfolio and identify additional growth opportunities in the form of new developments and acquisitions. New investments are focused in the shopping center sector, although we may selectively pursue commercial development or acquisition opportunities in markets where we currently operate and where we believe we can leverage existing infrastructure and relationships to generate attractive risk-adjusted returns.

Company Highlights as of September 30, 2010

|

·

|

Operating Retail Properties

|

51

|

|||

|

·

|

Operating Commercial Properties

|

4

|

|||

|

·

|

Total Properties Under Redevelopment

|

5

|

|||

|

·

|

Total Properties Under Development

|

2

|

|||

|

·

|

States

|

9

|

|||

|

·

|

Total GLA/NRA of 55 Operating Properties

|

8,385,675

|

|||

|

·

|

Owned GLA/NRA of 55 Operating Properties

|

5,498,230

|

|||

|

·

|

Owned GLA of Properties Under Development (2)/Redevelopment (5)

|

791,506

|

|||

|

·

|

Percentage of Owned GLA/NRA Leased – Total Portfolio

|

92.5%

|

|||

|

·

|

Percentage of Owned GLA Leased – Retail Operating

|

92.2%

|

|||

|

·

|

Percentage of Owned NRA Leased – Commercial Operating

|

95.5%

|

|||

|

·

|

Total Full-Time Employees

|

76

|

|||

Stock Listing: New York Stock Exchange symbol: KRG

Kite Realty Group Trust Supplemental Financial and Operating Statistics – 9/30/10

p.3

CONTACT INFORMATION

Corporate Office

30 South Meridian Street, Suite 1100

Indianapolis, IN 46204

(888) 577-5600

(317) 577-5600

www.kiterealty.com

|

Investor Relations Contacts:

|

Analyst Coverage:

|

Analyst Coverage:

|

||

|

Dan Sink, Chief Financial Officer

|

BMO Capital Markets

|

Raymond James

|

||

|

Adam Chavers, Vice President

Acquisitions & Investor Relations

|

Mr. Paul E. Adornato, CFA

|

Mr. Paul Puryear/Mr. R. J. Milligan

|

||

|

(212) 885-4170

|

(727) 567-2253/(727) 567-2660

|

|||

|

Kite Realty Group Trust

|

paul.adornato@bmo.com

|

paul.puryear@raymondjames.com

|

||

|

30 South Meridian Street, Suite 1100

|

Richard.milligan@raymondjames.com

|

|||

|

Indianapolis, IN 46204

|

Citigroup Global Markets

|

|||

|

(317) 577-5609/(317) 713-5684

|

Mr. Michael Bilerman/Mr. Quentin Velleley

|

RBC Capital Markets

|

||

|

dsink@kiterealty.com

|

(212) 816-1383/(212) 816-6981

|

Mr. Rich Moore/Mr. Wes Golladay

|

||

|

achavers@kiterealty.com

|

michael.bilerman@citigroup.com

|

(440) 715-2646/(440) 715-2650

|

||

|

Quentin.velleley@citi.com

|

rich.moore@rbccm.com

|

|||

|

Transfer Agent:

|

wes.golladay@rbccm.com

|

|||

|

Janney Montgomery Scott

|

||||

|

BNY Mellon Shareholder Services

|

Mr. Andrew T. Dizio, CFA

|

Stifel, Nicolaus & Company, Inc.

|

||

|

Mr. James Balsan

|

(215) 665-6439

|

Mr. Nathan Isbee

|

||

|

480 Washington Blvd., 29th Floor

|

adizio@jmsonline.com

|

(443) 224-1346

|

||

|

Jersey City, NJ 07310

|

nisbee@stifel.com

|

|||

|

(800) 820-8521

|

KeyBanc Capital Markets

|

|||

|

Mr. Jordan Sadler/Mr. Todd Thomas

|

Wells Fargo Securities, LLC

|

|||

|

(917) 368-2280/(917) 368-2286

|

Mr. Jeffrey J. Donnelly, CFA

|

|||

|

Stock Specialist:

|

tthomas@keybanccm.com

|

(617) 603-4262

|

||

|

jsadler@keybanccm.com

|

jeff.donnelly@wachovia.com

|

|||

|

Barclays Capital

|

||||

|

45 Broadway

|

Morgan Keegan

|

|||

|

20th Floor

|

Steve Swett

|

|||

|

New York, NY 10006

|

(212) 508-7585

|

|||

|

(646) 333-7000

|

stephen.swett@morgankeegan.com

|

|||

Kite Realty Group Trust Supplemental Financial and Operating Statistics – 9/30/10

p.4

IMPORTANT NOTES

Interim Information

This Quarterly Financial Supplement contains historical information of Kite Realty Group Trust (“the Company” or “KRG”) and is intended to supplement the Company’s Quarterly Report on Form 10-Q for the three and nine months ended September 30, 2010 to be filed on or about November 9, 2010, which should be read in conjunction with this supplement. The supplemental information is unaudited, although it reflects all adjustments which, in the opinion of management, are necessary for a fair presentation of operating results for the interim periods.

Forward-Looking Statements

This supplemental information package contains certain forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Such statements are based on assumptions and expectations that may not be realized and are inherently subject to risks, uncertainties and other factors, many of which cannot be predicted with accuracy and some of which might not even be anticipated. Future events and actual results, performance, transactions or achievements, financial or otherwise, may differ materially from the results, performance, transactions or achievements expressed or implied by the forward-looking statements. Risks, uncertainties and other factors that might cause such differences, some of which could be material, include, but are not limited to:

|

·

|

national and local economic, business, real estate and other market conditions, particularly in light of the current recession;

|

|

·

|

financing risks, including the availability of and costs associated with sources of liquidity;

|

|

·

|

the Company’s ability to refinance, or extend the maturity dates of, its indebtedness;

|

|

·

|

the level and volatility of interest rates;

|

|

·

|

the financial stability of tenants, including their ability to pay rent and the risk of tenant bankruptcies;

|

|

·

|

the competitive environment in which the Company operates;

|

|

·

|

acquisition, disposition, development and joint venture risks;

|

|

·

|

property ownership and management risks;

|

|

·

|

the Company’s ability to maintain its status as a real estate investment trust (“REIT”) for federal income tax purposes;

|

|

·

|

potential environmental and other liabilities;

|

|

·

|

impairment in the value of real estate property the Company owns;

|

|

·

|

risks related to the geographical concentration of our properties in Indiana, Florida and Texas;

|

|

·

|

other factors affecting the real estate industry generally; and

|

|

·

|

other risks identified in reports the Company files with the Securities and Exchange Commission (“the SEC”) or in other documents that it publicly disseminates, including, in particular, the section titled “Risk Factors” in our Annual Report on Form 10-K for the fiscal year ended December 31, 2009 and in our quarterly reports on Form 10-Q.

|

The Company undertakes no obligation to publicly update or revise these forward-looking statements, whether as a result of new information, future events or otherwise.

Funds from Operations

Funds from Operations (FFO) is a widely used performance measure for real estate companies and is provided here as a supplemental measure of operating performance. We calculate FFO in accordance with the best practices described in the April 2002 National Policy Bulletin of the National Association of Real Estate Investment Trusts (NAREIT), which we refer to as the White Paper. The White Paper defines FFO as net income (determined in accordance with generally accepted accounting principles (GAAP)), excluding gains (or losses) from sales of depreciated property, plus depreciation and amortization, and after adjustments for unconsolidated partnerships and joint ventures.

Considering the nature of our business as a real estate owner and operator, we believe that FFO is helpful to investors in measuring our operational performance because it excludes various items included in net income that do not relate to or are not indicative of our operating performance, such as gains or losses from sales of depreciated property and depreciation and amortization, which can make periodic and peer analyses of operating performance more difficult. FFO should not be considered as an alternative to net income (determined in accordance with GAAP) as an indicator of our financial performance, is not an alternative to cash flow from operating activities (determined in accordance with GAAP) as a measure of our liquidity, and is not indicative of funds available to satisfy our cash needs, including our ability to make distributions. Our computation of FFO may not be comparable to FFO reported by other REITs that do not define the term in accordance with the current NAREIT definition or that interpret the current NAREIT definition differently than we do.

Net Operating Income

Net operating income (NOI) is provided here as a supplemental measure of operating performance. NOI is defined as property revenues less property operating expenses, excluding depreciation and amortization, interest expense, impairment, and other items. We believe this presentation of NOI is helpful to investors as a measure of our operational performance because it is widely used in the real estate industry to measure the performance of real estate assets without regard to various items, included in net income, that do not relate to or are not indicative of operating performance, such as depreciation and amortization, which can vary depending upon accounting methods and book value of assets. We also believe NOI helps our investors to meaningfully compare the results of our operating performance from period to period by removing the impact of our capital structure (primarily interest expense on our outstanding indebtedness) and depreciation of the basis in our assets from our operating results. NOI should not, however, be considered as an alternative to net income (determined in accordance with GAAP) as an indicator of our financial performance.

Kite Realty Group Trust Supplemental Financial and Operating Statistics – 9/30/10

p.5

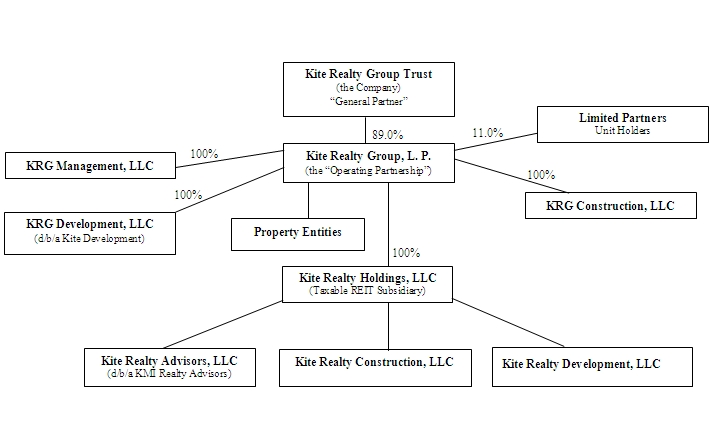

CORPORATE STRUCTURE CHART – SEPTEMBER 30, 2010

Kite Realty Group Trust Supplemental Financial and Operating Statistics – 9/30/10

p.6

CONDENSED CONSOLIDATED BALANCE SHEETS (UNAUDITED)

|

September 30,

2010

|

December 31,

2009

|

|||||||

|

Assets:

|

||||||||

|

Investment properties, at cost:

|

||||||||

|

Land

|

$ | 229,078,232 | $ | 226,506,781 | ||||

|

Land held for development

|

27,358,808 | 27,546,315 | ||||||

|

Buildings and improvements

|

764,638,869 | 736,027,845 | ||||||

|

Furniture, equipment and other

|

5,144,470 | 5,060,233 | ||||||

|

Construction in progress

|

167,414,630 | 176,689,227 | ||||||

| 1,193,635,009 | 1,171,830,401 | |||||||

|

Less: accumulated depreciation

|

(145,266,371 | ) | (127,031,144 | ) | ||||

| 1,048,368,638 | 1,044,799,257 | |||||||

|

Cash and cash equivalents

|

12,724,095 | 19,958,376 | ||||||

|

Tenant receivables, including accrued straight-line rent of $8,982,455 and $8,570,069, respectively, net of allowance for uncollectible accounts

|

17,822,311 | 18,537,031 | ||||||

|

Other receivables

|

6,543,165 | 9,326,475 | ||||||

|

Investments in unconsolidated entities, at equity

|

10,854,037 | 10,799,782 | ||||||

|

Escrow deposits

|

10,801,443 | 11,377,408 | ||||||

|

Deferred costs, net

|

21,830,481 | 21,509,070 | ||||||

|

Prepaid and other assets

|

4,274,989 | 4,378,045 | ||||||

|

Total Assets

|

$ | 1,133,219,159 | $ | 1,140,685,444 | ||||

|

Liabilities and Equity:

|

||||||||

|

Mortgage and other indebtedness

|

$ | 669,003,276 | $ | 658,294,513 | ||||

|

Accounts payable and accrued expenses

|

38,573,656 | 32,799,351 | ||||||

|

Deferred revenue and other liabilities

|

15,850,978 | 19,835,438 | ||||||

|

Total Liabilities

|

723,427,910 | 710,929,302 | ||||||

|

Commitments and contingencies

|

||||||||

|

Redeemable noncontrolling interests in the Operating Partnership

|

44,489,803 | 47,307,115 | ||||||

|

Equity:

|

||||||||

|

Kite Realty Group Trust Shareholders’ Equity:

|

||||||||

|

Preferred Shares, $.01 par value, 40,000,000 shares authorized, no shares issued and outstanding

|

— | — | ||||||

|

Common Shares, $.01 par value, 200,000,000 shares authorized 63,332,646 shares and 63,062,083 shares issued and outstanding at September 30, 2010 and

December 31, 2009, respectively

|

633,326 | 630,621 | ||||||

|

Additional paid in capital

|

451,045,438 | 449,863,390 | ||||||

|

Accumulated other comprehensive loss

|

(4,866,031 | ) | (5,802,406 | ) | ||||

|

Accumulated deficit

|

(88,484,324 | ) | (69,613,763 | ) | ||||

|

Total Kite Realty Group Trust Shareholders’ Equity

|

358,328,409 | 375,077,842 | ||||||

|

Noncontrolling Interests

|

6,973,037 | 7,371,185 | ||||||

|

Total Equity

|

365,301,446 | 382,449,027 | ||||||

|

Total Liabilities and Equity

|

$ | 1,133,219,159 | $ | 1,140,685,444 | ||||

Kite Realty Group Trust Supplemental Financial and Operating Statistics – 9/30/10

p.7

CONSOLIDATED STATEMENTS OF OPERATIONS – THREE AND NINE MONTHS (UNAUDITED)

|

Three Months Ended

September 30,

|

Nine Months Ended

September 30,

|

|||||||||||||||

|

2010

|

2009

|

2010

|

2009

|

|||||||||||||

|

Revenue:

|

||||||||||||||||

|

Minimum rent

|

$ | 18,292,136 | $ | 17,777,146 | $ | 53,768,732 | $ | 53,611,820 | ||||||||

|

Tenant reimbursements

|

4,246,120 | 4,220,185 | 13,347,228 | 13,412,648 | ||||||||||||

|

Other property related revenue

|

1,346,672 | 1,027,057 | 3,295,520 | 4,387,131 | ||||||||||||

|

Construction and service fee revenue

|

1,270,928 | 2,684,209 | 5,101,126 | 14,595,667 | ||||||||||||

|

Total revenue

|

25,155,856 | 25,708,597 | 75,512,606 | 86,007,266 | ||||||||||||

|

Expenses:

|

||||||||||||||||

|

Property operating

|

4,496,055 | 4,210,950 | 12,804,258 | 13,367,022 | ||||||||||||

|

Real estate taxes

|

3,158,006 | 2,677,703 | 9,697,406 | 8,958,326 | ||||||||||||

|

Cost of construction and services

|

1,147,383 | 2,381,885 | 4,543,084 | 12,958,935 | ||||||||||||

|

General, administrative, and other

|

1,260,314 | 1,387,407 | 3,891,076 | 4,276,451 | ||||||||||||

|

Depreciation and amortization

|

10,731,138 | 7,725,827 | 31,441,383 | 23,865,302 | ||||||||||||

|

Total expenses

|

20,792,896 | 18,383,772 | 62,377,207 | 63,426,036 | ||||||||||||

|

Operating income

|

4,362,960 | 7,324,825 | 13,135,399 | 22,581,230 | ||||||||||||

|

Interest expense

|

(6,978,767 | ) | (6,815,787 | ) | (21,313,368 | ) | (20,583,919 | ) | ||||||||

|

Income tax (expense) benefit of taxable REIT subsidiary

|

(80,954 | ) | 80,714 | (234,054 | ) | 29,529 | ||||||||||

|

(Loss) income from unconsolidated entities

|

(1,847 | ) | 73,524 | (100,442 | ) | 226,041 | ||||||||||

|

Non-cash gain from consolidation of subsidiary

|

— | 1,634,876 | — | 1,634,876 | ||||||||||||

|

Other income

|

53,633 | 42,229 | 186,193 | 126,735 | ||||||||||||

|

(Loss) income from continuing operations

|

(2,644,975 | ) | 2,340,381 | (8,326,272 | ) | 4,014,492 | ||||||||||

|

Discontinued operations:

|

||||||||||||||||

|

Operating loss from discontinued operations

|

— | (231,261 | ) | — | (714,007 | ) | ||||||||||

|

Non-cash loss on impairment of real estate asset

|

— | (5,384,747 | ) | — | (5,384,747 | ) | ||||||||||

|

Loss from discontinued operations

|

— | (5,616,008 | ) | — | (6,098,754 | ) | ||||||||||

|

Consolidated net loss

|

(2,644,975 | ) | (3,275,627 | ) | (8,326,272 | ) | (2,084,262 | ) | ||||||||

|

Net loss (income) attributable to noncontrolling interests

|

255,021 | (107,743 | ) | 841,083 | (340,781 | ) | ||||||||||

|

Net loss attributable to Kite Realty Group Trust

|

$ | (2,389,954 | ) | $ | (3,383,370 | ) | $ | (7,485,189 | ) | $ | (2,425,043 | ) | ||||

|

(Loss) income per common share – basic and diluted

|

||||||||||||||||

|

(Loss) income from continuing operations attributable to Kite Realty Group Trust common shareholders

|

$ | (0.04 | ) | $ | 0.03 | $ | (0.12 | ) | $ | 0.06 | ||||||

|

Loss from discontinued operations attributable to Kite Realty Group Trust common shareholders

|

— | (0.08 | ) | — | (0.11 | ) | ||||||||||

|

Net loss attributable to Kite Realty Group Trust common shareholders

|

$ | (0.04 | ) | $ | (0.05 | ) | $ | (0.12 | ) | $ | (0.05 | ) | ||||

|

Weighted average common shares outstanding - basic

|

63,288,181 | 62,980,447 | 63,206,901 | 48,489,799 | ||||||||||||

|

Weighted average common shares outstanding - diluted

|

63,288,181 | 62,980,447 | 63,206,901 | 48,489,799 | ||||||||||||

|

Dividends declared per common share

|

$ | 0.0600 | $ | 0.0600 | $ | 0.1800 | $ | 0.2725 | ||||||||

|

(Loss) income attributable to Kite Realty Group Trust common shareholders:

|

||||||||||||||||

|

(Loss) income from continuing operations

|

$ | (2,389,954 | ) | $ | 1,445,303 | $ | (7,485,189 | ) | $ | 2,807,688 | ||||||

|

Discontinued operations

|

— | (4,828,673 | ) | — | (5,232,731 | ) | ||||||||||

|

Net loss attributable to Kite Realty Group Trust

|

$ | (2,389,954 | ) | $ | (3,383,370 | ) | $ | (7,485,189 | ) | $ | (2,425,043 | ) | ||||

Kite Realty Group Trust Supplemental Financial and Operating Statistics – 9/30/10

p.8

FUNDS FROM OPERATIONS AND OTHER FINANCIAL INFORMATION –THREE AND NINE MONTHS

|

Three Months Ended

September 30,

|

Nine Months Ended

September 30,

|

|||||||||||||||

|

2010

|

2009

|

2010

|

2009

|

|||||||||||||

|

Consolidated net loss1

|

$ | (2,644,975 | ) | $ | (3,275,627 | ) | $ | (8,326,272 | ) | $ | (2,084,262 | ) | ||||

|

Less non-cash gain from consolidation of subsidiary, net of noncontrolling interests

|

— | (980,926 | ) | — | (980,926 | ) | ||||||||||

|

Less net income attributable to noncontrolling interests in properties

|

(42,182 | ) | (695,655 | ) | (96,708 | ) | (742,130 | ) | ||||||||

|

Add depreciation and amortization of consolidated entities, net of noncontrolling interests

|

10,359,890 | 7,724,160 | 30,687,142 | 23,693,084 | ||||||||||||

|

Add depreciation and amortization of unconsolidated entities

|

124,077 | 52,797 | 165,436 | 157,623 | ||||||||||||

|

Funds From Operations of the Operating Partnership2

|

7,796,810 | 2,824,749 | 22,429,598 | 20,043,389 | ||||||||||||

|

Less redeemable noncontrolling interests in Funds From Operations

|

(850,813 | ) | (319,197 | ) | (2,489,685 | ) | (3,173,320 | ) | ||||||||

|

Funds From Operations allocable to the Company2

|

$ | 6,945,997 | $ | 2,505,552 | $ | 19,939,913 | $ | 16,870,069 | ||||||||

|

Basic FFO per share of the Operating Partnership

|

$ | 0.11 | $ | 0.04 | $ | 0.32 | $ | 0.35 | ||||||||

|

Diluted FFO per share of the Operating Partnership

|

$ | 0.11 | $ | 0.04 | $ | 0.31 | $ | 0.35 | ||||||||

|

Basic FFO per share of the Operating Partnership (excluding non-cash loss on impairment of real estate asset)3

|

$ | 0.11 | $ | 0.12 | $ | 0.32 | $ | 0.45 | ||||||||

|

Diluted FFO per share of the Operating Partnership (excluding non-cash loss on impairment of real estate asset)3

|

$ | 0.11 | $ | 0.12 | $ | 0.31 | $ | 0.45 | ||||||||

|

Basic weighted average Common Shares outstanding

|

63,288,181 | 62,980,447 | 63,206,901 | 48,489,799 | ||||||||||||

|

Diluted weighted average Common Shares outstanding

|

63,522,229 | 63,090,887 | 63,439,031 | 48,575,947 | ||||||||||||

|

Basic weighted average Common Shares and Units outstanding

|

71,190,157 | 71,028,373 | 71,154,942 | 56,540,744 | ||||||||||||

|

Diluted weighted average Common Shares and Units outstanding

|

71,424,206 | 71,138,814 | 71,387,071 | 56,626,892 | ||||||||||||

|

Other Financial Information:

|

||||||||||||||||

|

Capital expenditures4

|

||||||||||||||||

|

Tenant improvements - Retail

|

$ | 349,511 | $ | 326,248 | $ | 935,789 | $ | 479,228 | ||||||||

|

Tenant improvements – Commercial

|

— | — | — | — | ||||||||||||

|

Leasing commissions - Retail

|

152,434 | 189,951 | 533,263 | 326,762 | ||||||||||||

|

Leasing commissions – Commercial

|

— | — | 30,662 | 1,816 | ||||||||||||

|

Capital improvements5

|

335,527 | 354,962 | 622,154 | 559,213 | ||||||||||||

|

Scheduled debt principal payments

|

1,205,192 | 1,090,481 | 3,605,217 | 2,872,676 | ||||||||||||

|

Straight line rent

|

175,984 | 477,209 | 415,806 | 1,331,491 | ||||||||||||

|

Market rent amortization income from acquired leases

|

710,601 | 770,643 | 2,196,266 | 2,333,755 | ||||||||||||

|

Market debt adjustment

|

107,714 | 107,714 | 323,143 | 323,143 | ||||||||||||

|

Non-cash compensation expense

|

143,688 | 491,663 | ||||||||||||||

|

Capitalized interest

|

2,433,281 | 2,388,944 | 6,587,523 | 6,591,078 | ||||||||||||

|

Mark to market lease amount in Deferred revenue and Other liabilities on consolidated balance sheet

|

10,493,945 | 13,337,265 | ||||||||||||||

|

Additional Construction in progress not in development pipelines

|

34,676,000 | |||||||||||||||

|

Acreage of undeveloped, vacant land in the operating portfolio6

|

41.2 | |||||||||||||||

|

____________________

|

|

|

1

|

Includes non-cash loss on impairment of real estate asset of $5,384,747 for the three and nine months ended September 30, 2009.

|

|

2

|

“Funds From Operations of the Operating Partnership” measures 100% of the operating performance of the Operating Partnership’s real estate properties and construction and service subsidiaries in which the Company owns an interest. “Funds From Operations allocable to the Company” reflects a reduction for the redeemable noncontrolling weighted average diluted interest in the Operating Partnership.

|

|

3

|

The Company believes the supplemental presentation of Funds from Operations of the Operating Partnership excluding the non-cash loss on the impairment of a real estate asset provides useful information to investors regarding its financial condition and results of operations because the measure provides investors with useful comparative information about the recurring operating performance of its core real estate portfolio presented on the same basis as prior periods. The Company also believes the presentation of this measure provides an investor with the ability to meaningfully assess the operating performance of its portfolio (e.g., an assessment of the amount of revenue and operating expenses a property is experiencing) in a clear and concise manner. Further, the Company believes that this measure allows investors to make a meaningful comparison of its operations compared with its peer real estate investment trusts.

|

|

4

|

Excludes tenant improvements and leasing commissions relating to development and redevelopment projects and first-generation space.

|

|

5

|

A portion of these capital improvements are reimbursed by tenants and are revenue producing.

|

| 6 | Excludes land in construction in progress and land held for development. |

Kite Realty Group Trust Supplemental Financial and Operating Statistics – 9/30/10

p.9

MARKET CAPITALIZATION AS OF SEPTEMBER 30, 2010

|

As of September 30, 2010

|

|||||||||||

|

Total

|

Percent of

|

||||||||||

|

Percent of

|

Market

|

Total Market

|

|||||||||

|

Total Equity

|

Capitalization

|

Capitalization

|

|||||||||

|

Equity Capitalization:

|

|||||||||||

|

Total Common Shares Outstanding

|

89.0

|

%

|

63,332,646

|

||||||||

|

Operating Partnership ("OP") Units Outstanding

|

11.0

|

%

|

7,863,498

|

||||||||

|

Combined Common Shares and OP Units

|

100.0

|

%

|

71,196,144

|

||||||||

|

Market Price of Common Shares at September 30, 2010

|

$

|

4.44

|

|||||||||

|

Total Equity Capitalization

|

$

|

316,110,881

|

33

|

%

|

|||||||

|

Debt Capitalization:

|

|||||||||||

|

Company Outstanding Debt

|

$

|

669,003,276

|

|||||||||

|

Less: Partner Share of Consolidated Joint Venture Debt

|

(45,666,460

|

)

|

|||||||||

|

Company Share of Outstanding Debt

|

623,336,816

|

||||||||||

|

Pro-rata Share of Unconsolidated Joint Venture Debt

|

17,030,951

|

||||||||||

|

Less: Cash and Cash Equivalents

|

(12,724,095

|

)

|

|||||||||

|

Total Net Debt Capitalization

|

$

|

627,643,672

|

67

|

%

|

|||||||

|

Total Market Capitalization as of September 30, 2010

|

$

|

943,754,553

|

100

|

%

|

|||||||

|

RATIO OF DEBT TO TOTAL UNDEPRECIATED ASSETS AS OF SEPTEMBER 30, 2010

|

|||||||||||

|

Consolidated Undepreciated Real Estate Assets

|

$

|

1,201,576,577

|

|||||||||

|

Company Share of Unconsolidated Real Estate Assets

|

28,990,591

|

||||||||||

|

Escrow Deposits

|

10,801,443

|

||||||||||

|

$

|

1,241,368,611

|

||||||||||

|

Total Consolidated Debt

|

$

|

669,003,276

|

|||||||||

|

Company Share of Joint Venture Debt

|

17,030,951

|

||||||||||

|

Less: Cash

|

(12,724,095

|

)

|

|||||||||

|

|

$

|

673,310,132

|

|||||||||

|

Ratio of Debt to Total Undepreciated Real Estate Assets

|

54.2

|

%

|

|||||||||

|

RATIO OF COMPANY SHARE OF DEBT TO EBITDA AS OF SEPTEMBER 30, 2010

|

|||||||||||

|

Company share of:

|

|||||||||||

|

- consolidated debt

|

$

|

623,336,816

|

|||||||||

|

- unconsolidated debt

|

17,030,951

|

||||||||||

|

Less: Cash

|

(12,724,095

|

)

|

|||||||||

|

627,643,672

|

|||||||||||

|

Q3 2010 EBITDA, annualized:

|

|||||||||||

|

- consolidated

|

$

|

60,264,996

|

|||||||||

|

- unconsolidated

|

632,290

|

60,897,286

|

|||||||||

|

10.3

|

x

|

||||||||||

Kite Realty Group Trust Supplemental Financial and Operating Statistics – 9/30/10

p.10

SAME PROPERTY NET OPERATING INCOME (NOI)

|

Three Months Ended September 30,

|

Nine Months Ended September 30,

|

|||||||||||||||

|

2010

|

2009

|

%

Change

|

2010

|

2009

|

%

Change

|

|||||||||||

|

Number of properties at period end1

|

55

|

55

|

55

|

55

|

||||||||||||

|

Leased percentage at period end

|

92.5%

|

91.2%

|

92.5%

|

91.2%

|

||||||||||||

|

Minimum rent

|

$

|

16,876,763

|

$

|

16,893,000

|

$

|

49,952,127

|

$

|

50,891,551

|

||||||||

|

Tenant recoveries

|

3,924,777

|

4,149,871

|

12,451,953

|

13,089,777

|

||||||||||||

|

Other income

|

50,420

|

31,783

|

183,232

|

149,717

|

||||||||||||

|

20,851,960

|

21,074,654

|

62,587,312

|

64,131,045

|

|||||||||||||

|

Property operating expenses

|

3,805,076

|

3,876,583

|

11,832,234

|

12,266,736

|

||||||||||||

|

Real estate taxes

|

2,845,088

|

2,917,777

|

8,578,259

|

8,981,488

|

||||||||||||

|

6,650,164

|

6,794,360

|

20,410,493

|

21,248,224

|

|||||||||||||

|

Net operating income – same properties (55 properties)2

|

$

|

14,201,796

|

$

|

14,280,294

|

-0.5

|

%

|

$

|

42,176,819

|

$

|

42,882,821

|

-1.6

|

%

|

||||

|

Reconciliation to Most Directly Comparable GAAP Measure:

|

||||||||||||||||

|

Net operating income – same properties

|

$

|

14,201,796

|

$

|

14,280,294

|

$

|

42,176,819

|

$

|

42,882,821

|

||||||||

|

Other income (expense), net

|

(16,591,750

|

)

|

(17,663,664

|

)

|

(49,662,008

|

)

|

(45,307,864

|

)

|

||||||||

|

Net loss

|

$

|

(2,389,954

|

)

|

$

|

(3,383,370

|

)

|

$

|

(7,485,189

|

)

|

$

|

(2,425,043

|

)

|

||||

|

____________________

|

|

|

1

|

Same Property analysis excludes Courthouse Shadows, Four Corner Square, Shops at Rivers Edge, Coral Springs and Bolton Plaza properties as the Company pursues redevelopment of these properties.

|

|

2

|

Same Property net operating income is considered a non-GAAP measure because it excludes net gains from outlot sales, write offs of straight-line rent and lease intangibles, bad debt expense and related recoveries, lease termination fees and significant prior year expense recoveries and adjustments, if any.

|

The Company believes that Net Operating Income is helpful to investors as a measure of its operating performance because it excludes various items included in net income that do not relate to or are not indicative of its operating performance, such as depreciation and amortization, interest expense, and impairment, if any. The Company believes that Same Property NOI is helpful to investors as a measure of its operating performance because it includes only the NOI of properties that have been owned for the full period presented, which eliminates disparities in net income due to the redevelopment, acquisition or disposition of properties during the particular period presented, and thus provides a more consistent metric for the comparison of the Company's properties. NOI and Same Property NOI should not, however, be considered as alternatives to net income (calculated in accordance with GAAP) as indicators of the Company's financial performance.

Kite Realty Group Trust Supplemental Financial and Operating Statistics – 9/30/10

p.11

NET OPERATING INCOME BY QUARTER (NOI)

|

Three Months Ended

|

|||||||||||||||||||

|

September 30,

2010

|

June 30,

2010

|

March 31,

2010

|

December 31,

2009

|

September 30,

2009

|

|||||||||||||||

|

Revenue:

|

|||||||||||||||||||

|

Minimum rent

|

$

|

18,292,136

|

$

|

17,741,385

|

$

|

17,735,211

|

$

|

18,000,595

|

$

|

17,777,146

|

|||||||||

|

Tenant reimbursements

|

4,246,120

|

4,259,847

|

4,841,261

|

4,750,543

|

4,220,185

|

||||||||||||||

|

Other property related revenue1

|

934,004

|

466,819

|

678,157

|

1,233,143

|

671,534

|

||||||||||||||

|

Parking revenue, net2

|

19,999

|

(23,196

|

)

|

(38,254

|

)

|

56,305

|

201,823

|

||||||||||||

|

23,492,259

|

22,444,855

|

23,216,375

|

24,040,586

|

22,870,688

|

|||||||||||||||

|

Expenses:

|

|||||||||||||||||||

|

Property operating – Recoverable3

|

3,189,813

|

2,928,684

|

3,512,414

|

3,618,959

|

3,296,572

|

||||||||||||||

|

Property operating – Non-Recoverable3

|

1,124,230

|

615,317

|

896,183

|

966,653

|

706,716

|

||||||||||||||

|

Real estate taxes

|

2,975,198

|

2,975,372

|

3,109,088

|

2,994,526

|

2,755,011

|

||||||||||||||

|

7,289,241

|

6,519,373

|

7,517,685

|

7,580,138

|

6,758,299

|

|||||||||||||||

|

Net Operating Income – Properties

|

16,203,018

|

15,925,482

|

15,698,690

|

16,460,448

|

16,112,389

|

||||||||||||||

|

Other Income (Expense):

|

|||||||||||||||||||

|

Construction and service fee revenue

|

1,270,928

|

1,950,848

|

1,879,350

|

4,855,122

|

2,684,209

|

||||||||||||||

|

Cost of construction and services

|

(1,147,383

|

)

|

(1,637,383

|

)

|

(1,758,318

|

)

|

(4,233,332

|

)

|

(2,381,885

|

)

|

|||||||||

|

General, administrative, and other

|

(1,260,314

|

)

|

(1,254,792

|

)

|

(1,375,970

|

)

|

(1,435,172

|

)

|

(1,387,407

|

)

|

|||||||||

|

(1,136,769

|

)

|

(941,327

|

)

|

(1,254,938

|

)

|

(813,382

|

)

|

(1,085,083

|

)

|

||||||||||

|

Earnings Before Interest, Taxes, Depreciation and Amortization

|

15,066,249

|

14,984,155

|

14,443,752

|

15,647,066

|

15,027,306

|

||||||||||||||

|

Depreciation and amortization

|

(10,703,289

|

)

|

(12,137,541

|

)

|

(8,517,927

|

)

|

(8,246,013

|

)

|

(7,702,481

|

)

|

|||||||||

|

Interest expense

|

(6,978,767

|

)

|

(7,237,738

|

)

|

(7,096,863

|

)

|

(6,567,135

|

)

|

(6,815,787

|

)

|

|||||||||

|

Income tax (expense) benefit of taxable REIT subsidiary

|

(80,954

|

)

|

(127,264

|

)

|

(25,836

|

)

|

(7,236

|

)

|

80,714

|

||||||||||

|

(Loss) income from unconsolidated entities

|

(1,847

|

)

|

(98,595

|

)

|

—

|

—

|

73,524

|

||||||||||||

|

Non-cash gain from consolidation of subsidiary4

|

—

|

—

|

—

|

—

|

1,634,876

|

||||||||||||||

|

Other income

|

53,633

|

66,810

|

65,750

|

98,191

|

42,229

|

||||||||||||||

|

(Loss) income from continuing operations

|

(2,644,975

|

)

|

(4,550,173

|

)

|

(1,131,124

|

)

|

924,873

|

2,340,381

|

|||||||||||

|

Discontinued operations5:

|

|||||||||||||||||||

|

Operating loss from discontinued operations

|

—

|

—

|

—

|

(18,614

|

)

|

(231,261

|

)

|

||||||||||||

|

Non-cash loss on impairment of real estate asset

|

—

|

—

|

—

|

—

|

(5,384,747

|

)

|

|||||||||||||

|

Loss from discontinued operations

|

—

|

—

|

—

|

(18,614

|

)

|

(5,616,008

|

)

|

||||||||||||

|

Net (loss) income

|

(2,644,975

|

)

|

(4,550,173

|

)

|

(1,131,124

|

)

|

906,259

|

(3,275,627

|

)

|

||||||||||

|

Net loss (income) attributable to noncontrolling interest

|

255,021

|

529,618

|

56,444

|

(262,982

|

)

|

(107,743

|

)

|

||||||||||||

|

Net (loss) income attributable to Kite Realty Group Trust

|

$

|

(2,389,954

|

)

|

$

|

(4,020,555

|

)

|

$

|

(1,074,680

|

)

|

$

|

643,277

|

$

|

(3,383,370

|

)

|

|||||

|

NOI/Revenue

|

69.0%

|

71.0%

|

67.6%

|

68.5%

|

70.4%

|

||||||||||||||

|

Recovery Ratios:6

|

|||||||||||||||||||

|

- Retail Only

|

77.2%

|

||||||||||||||||||

|

- Total Portfolio

|

68.9%

|

72.2%

|

73.1%

|

71.8%

|

69.7%

|

||||||||||||||

|

____________________

|

|

|

1

|

Other property related revenue for the three months ended September 30, 2010 includes net gains on land and outlot sales of $0.8 million and excludes $0.4 million of gross parking revenues which are included in “Parking revenue, net”.

|

|

2

|

Parking revenue, net, represents the net operating results of the Eddy Street Parking Garage and KR Washington Parking.

|

|

3

|

Recoverable expenses include total management fee expense, a portion of which is recoverable. Non-recoverable expenses primarily include bad debt and legal expense.

|

|

4

|

In September 2009, the Company consolidated the financial statements of The Centre operating property at the fair value of the underlying assets and liabilities. It recorded a non-cash gain of $1.6 million, its share of which was approximately $1.0 million.

|

|

5

|

In December 2009, the Company transferred its Galleria Plaza operating property to the ground lessor. The Company had recognized a non-cash impairment charge of $5.4 million to write off the net book value of the property in September 2009. Since the Company ceased operating this property during the fourth quarter of 2009, it was appropriate to reclassify the non-cash impairment loss and the operating results related to this property to discontinued operations for each of the periods presented above.

|

|

6

|

“Recovery Ratio” is computed by dividing tenant reimbursements by the sum of recoverable property operating expense and real estate tax expense.

|

Kite Realty Group Trust Supplemental Financial and Operating Statistics – 9/30/10

p.12

SUMMARY OF OUTSTANDING DEBT AS OF SEPTEMBER 30, 20102

|

TOTAL OUTSTANDING DEBT

|

||||||||||||||||

|

Outstanding Amount

|

Ratio

|

Weighted Average

Interest Rate

|

Weighted Average

Maturity (in years)

|

|||||||||||||

|

Fixed Rate Debt

|

||||||||||||||||

|

Consolidated

|

$ | 296,592,410 | 43 | % | 6.08 | % | 4.7 | |||||||||

|

Floating Rate Debt (Hedged)

|

219,447,225 | 32 | % | 5.70 | % | 1.2 | ||||||||||

|

Total Fixed Rate Debt

|

516,039,635 | 75 | % | 5.92 | % | 3.2 | ||||||||||

|

Variable Rate Debt:1

|

||||||||||||||||

|

Construction Loans

|

73,330,157 | 11 | % | 3.64 | % | 2.0 | ||||||||||

|

Other Variable

|

298,426,083 | 44 | % | 2.57 | % | 1.6 | ||||||||||

|

Floating Rate Debt (Hedged)

|

(219,447,225 | ) | -32 | % | -2.49 | % | -1.2 | |||||||||

|

Unconsolidated

|

17,030,951 | 2 | % | 3.41 | % | 1.1 | ||||||||||

|

Total Variable Rate Debt

|

169,339,966 | 25 | % | 3.22 | % | 2.3 | ||||||||||

|

Net Premiums on Fixed Rate Debt

|

654,626 | N/A | N/A | N/A | ||||||||||||

|

Total

|

$ | 686,034,227 | 100 | % | 5.25 | % | 3.0 | |||||||||

|

SCHEDULE OF MATURITIES BY YEAR

|

||||||||||||||

|

Mortgage Debt

|

Construction

Loans

|

Total Consolidated Outstanding Debt

|

KRG Share of Unconsolidated Mortgage

Debt

|

Total Consolidated and Unconsolidated Debt

|

||||||||||

|

Annual

Maturity

|

Term

Maturities

|

Corporate

Debt

|

||||||||||||

|

2010

|

$

|

810,471

|

$

|

—

|

$

|

—

|

$

|

—

|

$

|

810,471

|

$

|

—

|

$

|

810,471

|

|

2011

|

3,145,646

|

67,258,776

|

55,000,000

|

28,876,339

|

154,280,761

|

13,549,200

|

167,829,961

|

|||||||

|

20122

|

4,008,420

|

65,243,372

|

104,800,000

|

—

|

174,051,792

|

—

|

174,051,792

|

|||||||

|

2013

|

4,075,785

|

42,839,017

|

—

|

44,453,818

|

91,368,620

|

—

|

91,368,620

|

|||||||

|

2014

|

3,812,854

|

31,417,367

|

—

|

—

|

35,230,221

|

3,481,751

|

38,711,972

|

|||||||

|

2015

|

3,539,592

|

38,301,943

|

—

|

—

|

41,841,535

|

—

|

41,841,535

|

|||||||

|

2016 and Beyond

|

5,380,607

|

165,384,643

|

—

|

—

|

170,765,250

|

—

|

170,765,250

|

|||||||

|

Net Premiums on Fixed Rate Debt

|

—

|

—

|

—

|

—

|

654,626

|

—

|

654,626

|

|||||||

|

Total

|

$

|

24,773,375

|

$

|

410,445,118

|

$

|

159,800,000

|

$

|

73,330,157

|

$

|

669,003,276

|

$

|

17,030,951

|

$

|

686,034,227

|

|

____________________

|

||||||||

|

1

|

Variable rate debt, net of interest rate swap transactions:

|

|||||||

|

- Construction

|

$

|

73,330,157

|

11

|

%

|

||||

|

- Other Variable

|

78,978,858

|

12

|

%

|

(includes debt on land held for development)

|

||||

|

- Unconsolidated

|

17,030,951

|

2

|

%

|

(includes debt on land held for development)

|

||||

| - Total |

$

|

169,339,966

|

25

|

%

|

||||

|

2

|

In October 2010, the Company exercised an option to extend the maturity date of the Unsecured Credit Facility from February 2011 to February 2012.

|

|||||||

Kite Realty Group Trust Supplemental Financial and Operating Statistics – 9/30/10

p.13

SCHEDULE OF OUTSTANDING DEBT AS OF SEPTEMBER 30, 2010 (CONTINUED)

|

CONSOLIDATED DEBT

|

|||||||||||||||

|

Fixed Rate Debt

|

Interest

Rate

|

Maturity Date

|

Balance as of

September 30, 2010

|

Monthly Debt Service

As of September 30, 2010

|

|||||||||||

|

50th & 12th

|

5.67

|

%

|

11/11/14

|

$

|

4,312,883

|

$

|

27,190

|

||||||||

|

The Centre at Panola

|

6.78

|

%

|

1/1/22

|

3,514,293

|

36,583

|

||||||||||

|

Cool Creek Commons

|

5.88

|

%

|

4/11/16

|

17,700,036

|

106,534

|

||||||||||

|

The Corner

|

7.65

|

%

|

7/1/11

|

1,509,101

|

17,111

|

||||||||||

|

Fox Lake Crossing

|

5.16

|

%

|

7/1/12

|

11,111,556

|

68,604

|

||||||||||

|

Geist Pavilion

|

5.78

|

%

|

1/1/17

|

11,125,000

|

55,372

|

||||||||||

|

Indian River Square

|

5.42

|

%

|

6/11/15

|

13,085,521

|

74,849

|

||||||||||

|

International Speedway Square

|

7.17

|

%

|

3/11/11

|

18,353,591

|

139,142

|

||||||||||

|

Kedron Village

|

5.70

|

%

|

1/11/17

|

29,700,000

|

145,778

|

||||||||||

|

Pine Ridge Crossing

|

6.34

|

%

|

10/11/16

|

17,500,000

|

95,601

|

||||||||||

|

Plaza at Cedar Hill

|

7.38

|

%

|

2/1/12

|

25,285,158

|

193,484

|

||||||||||

|

Plaza Volente

|

5.42

|

%

|

6/11/15

|

28,217,498

|

161,405

|

||||||||||

|

Preston Commons

|

5.90

|

%

|

3/11/13

|

4,244,525

|

28,174

|

||||||||||

|

Riverchase Plaza

|

6.34

|

%

|

10/11/16

|

10,500,000

|

57,360

|

||||||||||

|

Sunland Towne Centre

|

6.01

|

%

|

7/1/16

|

25,000,000

|

129,382

|

||||||||||

|

30 South

|

6.09

|

%

|

1/11/14

|

21,401,793

|

142,257

|

||||||||||

|

Traders Point

|

5.86

|

%

|

10/11/16

|

45,895,436

|

231,593

|

||||||||||

|

Whitehall Pike

|

6.71

|

%

|

7/5/18

|

8,136,019

|

77,436

|

||||||||||

|

Subtotal

|

$

|

296,592,410

|

$

|

1,787,855

|

|||||||||||

|

Floating Rate Debt (Hedged)

|

Lender

|

Interest

Rate

|

Maturity Date

|

Balance as of

September 30, 2010

|

Monthly Debt Service as of September 30, 2010

|

||||||||||

|

Unsecured Credit Facility1

|

KeyBank (Admin. Agent)

|

6.42

|

%

|

2/20/11

|

$

|

50,000,000

|

$

|

267,583

|

|||||||

|

Unsecured Credit Facility1

|

KeyBank (Admin. Agent)

|

6.27

|

%

|

2/18/11

|

25,000,000

|

130,521

|

|||||||||

|

Unsecured Term Loan1

|

KeyBank (Admin. Agent)

|

5.92

|

%

|

7/15/11

|

55,000,000

|

271,104

|

|||||||||

|

Bayport Commons

|

Bank of America

|

5.23

|

%

|

12/27/11

|

14,923,016

|

65,039

|

|||||||||

|

Beacon Hill

|

Fifth Third Bank

|

2.98

|

%

|

12/27/11

|

5,161,984

|

12,819

|

|||||||||

|

Eastgate Pavilion

|

PNC Bank

|

4.84

|

%

|

4/30/12

|

14,937,770

|

60,249

|

|||||||||

|

Gateway Shopping Center

|

Charter One Bank

|

4.88

|

%

|

10/31/11

|

20,000,000

|

81,333

|

|||||||||

|

Glendale Town Center

|

M&I Bank

|

4.40

|

%

|

12/19/11

|

19,615,000

|

71,922

|

|||||||||

|

Ridge Plaza

|

TD Bank

|

6.56

|

%

|

1/3/17

|

14,809,455

|

80,958

|

|||||||||

|

Subtotal

|

$

|

219,447,225

|

$

|

1,041,528

|

|||||||||||

|

TOTAL CONSOLIDATED FIXED RATE DEBT

|

$

|

516,039,635

|

$

|

2,829,383

|

|||||||||||

|

TOTAL NET PREMIUMS

|

$

|

654,626

|

|||||||||||||

|

Variable Rate Debt:

Mortgages

|

Lender

|

Interest

Rate2

|

Maturity Date

|

Balance as of

September 30, 2010

|

|||||||||||

|

Bayport Commons3

|

Bank of America

|

LIBOR + 350

|

1/6/12

|

$

|

14,923,016

|

||||||||||

|

Beacon Hill4

|

Fifth Third Bank

|

LIBOR + 125

|

3/30/14

|

7,443,150

|

|||||||||||

|

Eastgate Pavilion

|

PNC Bank

|

LIBOR + 295

|

4/30/12

|

14,964,960

|

|||||||||||

|

Estero Town Commons5

|

Wachovia Bank/Wells Fargo

|

LIBOR + 325

|

1/15/13

|

10,500,000

|

|||||||||||

|

Fishers Station6

|

National City Bank/PNC

|

LIBOR + 350

|

6/6/11

|

3,733,116

|

|||||||||||

|

Gateway Shopping Center4

|

Charter One Bank

|

LIBOR + 190

|

10/31/11

|

20,802,866

|

|||||||||||

|

Glendale Town Center

|

M&I Bank

|

LIBOR + 275

|

12/19/11

|

19,615,000

|

|||||||||||

|

Indiana State Motor Pool

|

Old National Bank

|

LIBOR + 135

|

2/4/11

|

3,514,395

|

|||||||||||

|

Ridge Plaza

|

TD Bank

|

LIBOR + 325

|

1/3/17

|

14,818,054

|

|||||||||||

|

Shops at Rivers Edge

|

Huntington Bank

|

LIBOR + 400

|

2/1/13

|

14,311,526

|

|||||||||||

|

Tarpon Springs Plaza

|

Wachovia Bank/Wells Fargo

|

LIBOR + 325

|

1/15/13

|

14,000,000

|

|||||||||||

|

Subtotal

|

$

|

138,626,083

|

|||||||||||||

|

____________________

|

||||||||||||||||||

|

1

|

The Company entered into a fixed rate swap agreement, which is designated as a hedge against the Unsecured Credit Facility and Term Loan.

|

|||||||||||||||||

|

2

|

At September 30, 2010, one-month LIBOR was 0.26%.

|

|||||||||||||||||

|

3

|

The Company has a preferred return, then a 60% interest. The loan is guaranteed by Kite Realty Group, LP.

|

|||||||||||||||||

|

4

|

The Company has a preferred return, then a 50% interest. The loan is guaranteed by Kite Realty Group, LP.

|

|||||||||||||||||

|

5

|

The Company has a preferred return, then a 40% interest. The loan is guaranteed by Kite Realty Group, LP.

|

|||||||||||||||||

|

6

|

The Company has a 25% interest in this property. The loan is guaranteed by Kite Realty Group, LP.

|

|||||||||||||||||

Kite Realty Group Trust Supplemental Financial and Operating Statistics – 9/30/10

p.14

SCHEDULE OF OUTSTANDING DEBT AS OF SEPTEMBER 30, 20107 (CONTINUED)

|

Variable Rate Debt:

Construction Loans

|

Lender

|

Interest

Rate1

|

Maturity Date

|

Total

Commitment

|

Balance as of

September 30, 2010

|

|||||||

|

Bridgewater Marketplace2

|

Indiana Bank And Trust

|

LIBOR + 185

|

6/29/13

|

$

|

7,000,000

|

$

|

7,000,000

|

|||||

|

Cobblestone Plaza3

|

Wachovia Bank/Wells Fargo

|

LIBOR + 350

|

2/12/13

|

34,000,000

|

28,223,818

|

|||||||

|

Delray Marketplace3

|

Wachovia Bank/Wells Fargo

|

LIBOR + 300

|

6/30/11

|

4,725,000

|

4,725,000

|

|||||||

|

Eddy Street Commons

|

Bank of America

|

LIBOR + 230

|

12/30/11

|

29,460,000

|

24,151,339

|

|||||||

|

South Elgin Commons4

|

Charter One Bank

|

LIBOR + 325

|

9/30/13

|

9,440,000

|

9,230,000

|

|||||||

|

Subtotal

|

$

|

84,625,000

|

$

|

73,330,157

|

||||||||

|

Corporate Debt

|

Lender

|

Interest

Rate1

|

Maturity Date

|

Balance as of

September 30, 2010

|

||||||||

|

Unsecured Credit Facility5,6

|

KeyBank (Admin. Agent)

|

LIBOR + 135

|

2/20/12

|

7 |

$

|

104,800,000

|

||||||

|

Unsecured Term Loan5

|

KeyBank (Admin. Agent)

|

LIBOR + 265

|

7/15/11

|

55,000,000

|

||||||||

|

Subtotal

|

$

|

159,800,000

|

||||||||||

|

Floating Rate Debt (Hedged)

|

Lender

|

Interest

Rate1

|

Maturity Date

|

Balance as of

September 30, 2010

|

||||||||

|

Unsecured Credit Facility6

|

KeyBank (Admin. Agent)

|

LIBOR + 135

|

2/20/11

|

$

|

(50,000,000)

|

|||||||

|

Unsecured Credit Facility6

|

KeyBank (Admin. Agent)

|

LIBOR + 135

|

2/18/11

|

(25,000,000)

|

||||||||

|

Unsecured Term Loan6

|

KeyBank (Admin. Agent)

|

LIBOR + 265

|

7/15/11

|

(55,000,000)

|

||||||||

|

Bayport Commons

|

Bank of America

|

LIBOR + 350

|

12/27/11

|

(14,923,016)

|

||||||||

|

Beacon Hill

|

Fifth Third Bank

|

LIBOR + 125

|

12/27/11

|

(5,161,984)

|

||||||||

|

Eastgate Pavilion

|

PNC Bank

|

LIBOR + 295

|

4/30/12

|

(14,937,770)

|

||||||||

|

Gateway Shopping Center

|

Charter One Bank

|

LIBOR + 190

|

10/31/11

|

(20,000,000)

|

||||||||

|

Glendale Town Center

|

M&I Bank

|

LIBOR + 275

|

12/19/11

|

(19,615,000)

|

||||||||

|

Ridge Plaza

|

TD Bank

|

LIBOR + 325

|

1/3/17

|

(14,809,455)

|

||||||||

|

Subtotal

|

$

|

(219,447,225)

|

||||||||||

|

TOTAL CONSOLIDATED VARIABLE RATE DEBT

|

$

|

152,309,015

|

||||||||||

|

TOTAL DEBT PER CONSOLIDATED BALANCE SHEET

|

$

|

669,003,276

|

||||||||||

|

____________________

|

|

|

1

|

At September 30, 2010, the one-month LIBOR interest rate was 0.26%.

|

|

2

|

The loan has a LIBOR floor of 3.15%.

|

|

3

|

The Company has a preferred return, then a 50% interest. This loan is guaranteed by Kite Realty Group, LP.

|

|

4

|

The loan has a LIBOR floor of 2.00%.

|

|

5

|

The Company has 51 unencumbered properties and other assets of which 47 are wholly owned and used as collateral under the unsecured credit facility and four of which are owned in a joint venture. The major unencumbered properties include: Boulevard Crossing, Broadstone Station, Coral Springs Plaza, Courthouse Shadows, Four Corner Square, Hamilton Crossing, King's Lake Square, Market Street Village, Naperville Marketplace, PEN Products, Publix at Acworth, Redbank Commons, Shops at Eagle Creek, Traders Point II, Union Station Parking Garage, Wal-Mart Plaza and Waterford Lakes.

|

|

6

|

The Company entered into a fixed rate swap agreement which is designated as a hedge against the unsecured credit facility and term loan.

|

|

7

|

In October 2010, the Company exercised an option to extend the maturity date of the Unsecured Credit Facility from February 2011 to February 2012.

|

Kite Realty Group Trust Supplemental Financial and Operating Statistics – 9/30/10

p.15

SCHEDULE OF OUTSTANDING DEBT AS OF SEPTEMBER 30, 2010 (CONTINUED)

|

UNCONSOLIDATED DEBT

|

|||||||||||

|

Variable Rate Debt - Construction Loans

|

Lender

|

Interest

Rate1

|

Maturity Date

|

Total

Commitment

|

Balance as of

June 30, 2010

|

||||||

|

Parkside Town Commons2

|

Bank of America

|

LIBOR + 300

|

2/28/11

|

$

|

33,873,000

|

$

|

33,873,000

|

||||

|

Eddy Street Commons – Limited Service Hotel3

|

1st Source Bank |

LIBOR + 315

|

8/18/14

|

10,850,000

|

6,963,502

|

||||||

| 40,836,502 | |||||||||||

|

Parkside Town Commons Joint Venture Partners' Share – 60%

|

(20,323,800

|

)

|

|||||||||

|

Eddy Street Commons – Limited Service Hotel Joint Venture Partners' Share – 50%

|

(3,481,751

|

)

|

|||||||||

|

KRG SHARE OF UNCONSOLIDATED DEBT

|

$

|

17,030,951

|

|||||||||

|

TOTAL KRG CONSOLIDATED DEBT

|

$

|

669,003,276

|

|||||||||

|

TOTAL KRG DEBT

|

$

|

686,034,227

|

|||||||||

|

____________________

|

|

|

1

|

At September 30, 2010, the one-month LIBOR interest rate was 0.26%.

|

|

2

|

The Company owns a 40% interest in Parkside Town Commons. This will change to a 20% ownership at the time of the hard cost construction financing.

|

|

3

|

The Company owns a 50% interest in Eddy Street Commons – Limited Service Hotel. The loan has a LIBOR floor of 0.85%.

|

Kite Realty Group Trust Supplemental Financial and Operating Statistics – 9/30/10

p.16

JOINT VENTURE SUMMARY – UNCONSOLIDATED PROPERTIES

During 2010, the Company owned the following unconsolidated properties with joint venture partners:

|

Property

|

Percentage Owned

by the Company

|

|

|

Parkside Town Commons – Development Property1

|

40%

|

|

|

Eddy Street Commons Limited Service Hotel – Development Property

|

50%

|

|

____________________

|

|

|

1

|

The Company's 40% interest in Parkside Town Commons will change to 20% at the time of project specific construction financing.

|

Kite Realty Group Trust Supplemental Financial and Operating Statistics – 9/30/10

p.17

CONDENSED COMBINED BALANCE SHEETS OF UNCONSOLIDATED PROPERTIES

(Parkside Town Commons and Eddy Street Commons Limited Service Hotel)

(Unaudited)

|

September 30,

2010

|

December 31,

2009

|

|||||||

|

Assets:

|

||||||||

|

Investment properties, at cost:

|

||||||||

|

Buildings and improvements

|

$ | 8,746,727 | $ | — | ||||

|

Furniture, equipment and other

|

167,646 | — | ||||||

|

Construction in progress

|

60,517,347 | 62,204,124 | ||||||

| 69,431,720 | 62,204,124 | |||||||

|

Less: accumulated depreciation

|

(323,039 | ) | — | |||||

| 69,108,681 | 62,204,124 | |||||||

|

Cash and cash equivalents

|

197,775 | 540,264 | ||||||

|

Other receivables

|

119,435 | — | ||||||

|

Escrow deposits

|

600,000 | 600,000 | ||||||

|

Deferred costs, net

|

92,027 | — | ||||||

|

Prepaid and other assets

|

86,438 | 243,236 | ||||||

|

Total Assets

|

$ | 70,204,356 | $ | 63,587,624 | ||||

|

Liabilities and Shareholders’ Equity:

|

||||||||

|

Mortgage and other indebtedness

|

$ | 40,836,502 | $ | 35,836,186 | ||||

|

Accounts payable and accrued expenses

|

2,304,141 | 980,677 | ||||||

|

Total Liabilities

|

43,140,643 | 36,816,863 | ||||||

|

Accumulated equity

|

27,063,713 | 26,770,761 | ||||||

|

Total Liabilities and Accumulated Equity

|

$ | 70,204,356 | $ | 63,587,624 | ||||

|

Company’s share of unconsolidated assets

|

$ | 28,990,591 | $ | 25,729,647 | ||||

|

Company’s share of mortgage and other indebtedness

|

$ | 17,030,951 | $ | 14,530,793 | ||||

Kite Realty Group Trust Supplemental Financial and Operating Statistics – 9/30/10

p.18

CONDENSED COMBINED STATEMENTS OF OPERATIONS OF UNCONSOLIDATED PROPERTIES

(The Centre1, Parkside Town Commons and Eddy Street Commons Limited Service Hotel)

(Unaudited)

|

Three Months Ended

September 30,

|

Nine Months Ended

September 30,

|

||||||||||||

|

2010

|

2009

|

2010

|

2009

|

||||||||||

|

Revenue:

|

|||||||||||||

|

Minimum rent

|

$

|

—

|

$

|

230,328

|

$

|

—

|

$

|

691,739

|

|||||

|

Tenant reimbursements

|

—

|

86,272

|

—

|

256,426

|

|||||||||

|

Other property related revenue

|

926,006

|

(723

|

)

|

1,027,202

|

20,916

|

||||||||

|

Total revenue

|

926,006

|

315,877

|

1,027,202

|

969,081

|

|||||||||

|

Expenses:

|

|||||||||||||

|

Property operating2

|

537,568

|

69,914

|

741,122

|

195,656

|

|||||||||

|

Real estate taxes

|

44,000

|

46,043

|

44,000

|

142,198

|

|||||||||

|

Other income

|

28,293

|

—

|

28,293

|

—

|

|||||||||

|

Total expenses

|

609,861

|

115,957

|

813,415

|

337,854

|

|||||||||

|

Net operating income

|

316,145

|

199,920

|

213,787

|

631,227

|

|||||||||

|

Depreciation and amortization

|

(248,155

|

)

|

(34,635

|

)

|

(330,873

|

)

|

(102,626

|

)

|

|||||

|

Interest expense

|

(71,685

|

)

|

(54,999

|

)

|

(83,798

|

)

|

(179,177

|

)

|

|||||

|

Other income

|

—

|

32,090

|

—

|

32,090

|

|||||||||

|

(Loss) income from continuing operations

|

(3,695

|

)

|

142,376

|

(200,884

|

)

|

381,514

|

|||||||

|

Net (loss) income

|

$

|

(3,695

|

)

|

$

|

142,376

|

$

|

(200,884

|

)

|

$

|

381,514

|

|||

|

Company’s share of unconsolidated net operating income

|

$

|

158,073

|

$

|

119,952

|

$

|

106,893

|

$

|

378,736

|

|||||

|

Company’s share of unconsolidated interest expense

|

$

|

(35,843

|

)

|

$

|

(32,999

|