Attached files

| file | filename |

|---|---|

| 8-K - CURRENT REPORT - INTERNATIONAL PAPER CO /NEW/ | d8k.htm |

| EX-99.1 - PRESS RELEASE OF INTERNATIONAL PAPER COMPANY - INTERNATIONAL PAPER CO /NEW/ | dex991.htm |

Third Quarter

2010 Review

October 27, 2010

Third Quarter

2010 Review

October 27, 2010

John V. Faraci

Chairman &

Chief Executive Officer

Tim S. Nicholls

Senior Vice President &

Chief Financial Officer

Exhibit 99.2 |

2

Forward-Looking Statements

Forward-Looking Statements

These slides and statements made during this presentation contain forward-looking

statements. These statements reflect management's current views and are subject to

risks and uncertainties that could cause actual results to differ materially from those

expressed or implied in these statements. Factors which could cause actual results to

differ relate to: (i) increases in interest rates; (ii) industry conditions, including but

not limited to changes in the cost or availability of raw materials, energy and

transportation costs, competition we face, cyclicality and changes in consumer preferences,

demand and pricing for our products; (iii) global economic conditions and political

changes, including but not limited to the impairment of financial institutions, changes in

currency exchange rates, credit ratings issued by recognized credit rating organizations,

the amount of our future pension funding obligation and changes in pension and health care

costs; (iv) unanticipated expenditures related to the cost of compliance with environmental

and other governmental regulations and to actual or potential litigation; and (v) whether

we experience a material disruption at one of our manufacturing facilities and risks

inherent in conducting business through a joint venture. We undertake no obligation to

publicly update any forward-looking statements, whether as a result of new information,

future events or otherwise. These and other factors that could cause or contribute to

actual results differing materially from such forward looking statements are discussed in

greater detail in the company's Securities and Exchange Commission filings.

|

3

Statements Relating to Non-GAAP

Financial Measures

Statements Relating to Non-GAAP

Financial Measures

During the course of this presentation, certain

non-U.S. GAAP financial information will be

presented.

A reconciliation of those numbers to U.S.

GAAP financial measures is available on the

company’s

website

at

internationalpaper.com

under Investors. |

4

Third Quarter 2010

Headlines

Third Quarter 2010

Headlines

Outstanding Earnings

All global segments

More than double 2Q

Strong Free Cash Flow

More than double 2Q

Cost-of-Capital Returns

$1.2 B Pension Contribution

& $200 MM Debt Reduction |

5

Third Quarter 2010

Significant Earnings Improvement

Third Quarter 2010

Significant Earnings Improvement

Excellent Earnings in All Three

U.S. Mill Businesses

Continued Strong Earnings in

EMEA Paper and Packaging

Strong Contribution from Ilim

Joint Venture

Restructuring Benefits

Incremental Price Increase

Realization

Continued Strong Operations

Earnings from continuing operations before

special items |

6

3Q10 Financial Snapshot

Strong EBITDA & Free Cash Flow

3Q10 Financial Snapshot

Strong EBITDA & Free Cash Flow

3Q09

2Q10

3Q10

Sales ($B)

$5.9

$6.1

$6.7

EBITDA

1

($MM)

$780

$782

$1,061

EBITDA Margin

13%

13%

16%

Free Cash Flow

2

($MM)

$605

$356

$753

Debt ($B)

$9.6

$8.9

$8.7

Cash Balance ($B)

$1.7

$1.9

$1.4

1.

Earnings from continuing operations before special items

2.

Cash provided by continuing operations less capital expenditures, excluding cash received from

alternative fuel credits of $463 MM in 3Q09, $132 MM in 2Q10, cash received under European

accounts receivable securitization of $0.2B in 3Q09, and cash paid for voluntary pension

contributions of $1.2 B in 3Q10. |

7

Transformation Enabling Improved Returns

Recovering from Global Recession

Transformation Enabling Improved Returns

Recovering from Global Recession

Cost of Capital |

8

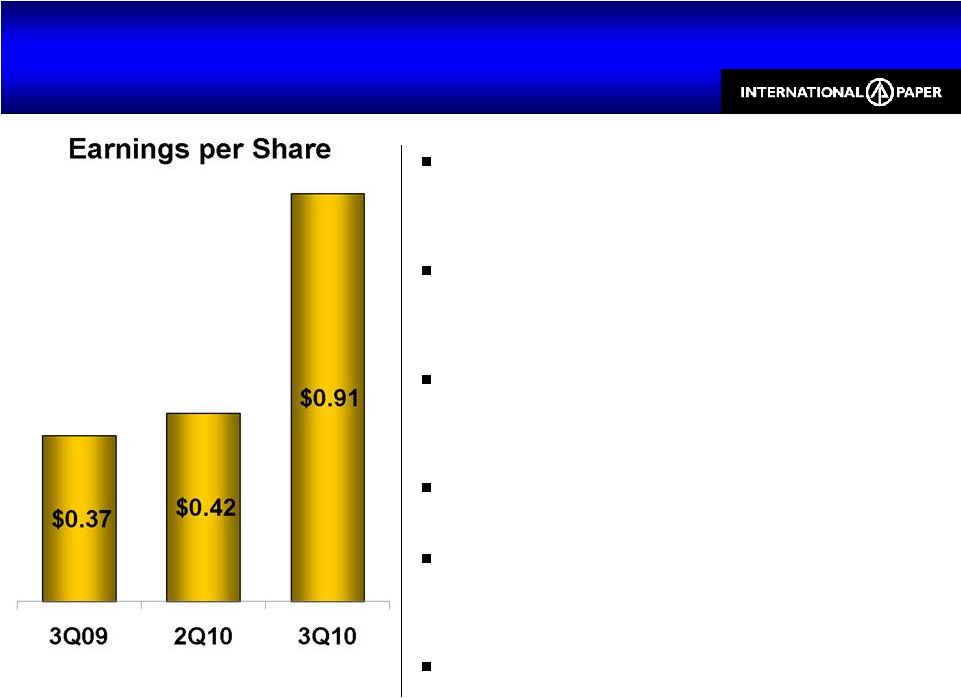

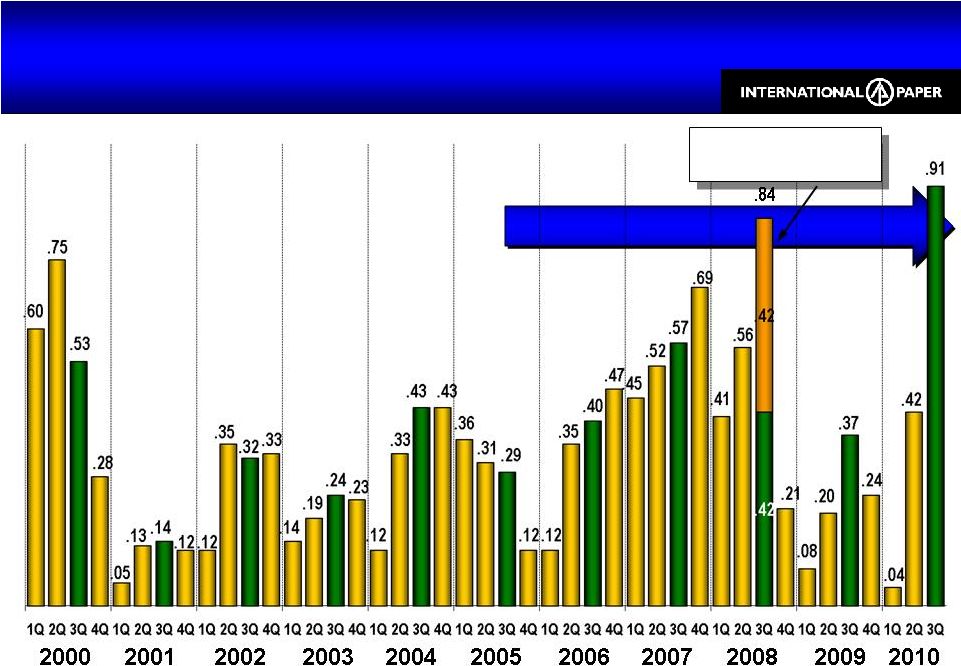

Operating EPS

Record Quarterly Earnings

Operating EPS

Record Quarterly Earnings

2003

2004

2005

2006

2007

2010

2002

2000

2001

2008

Impact of Mineral

Rights Gain

2009

Earnings from continuing operations before special items as reported at the

time Transformation |

9

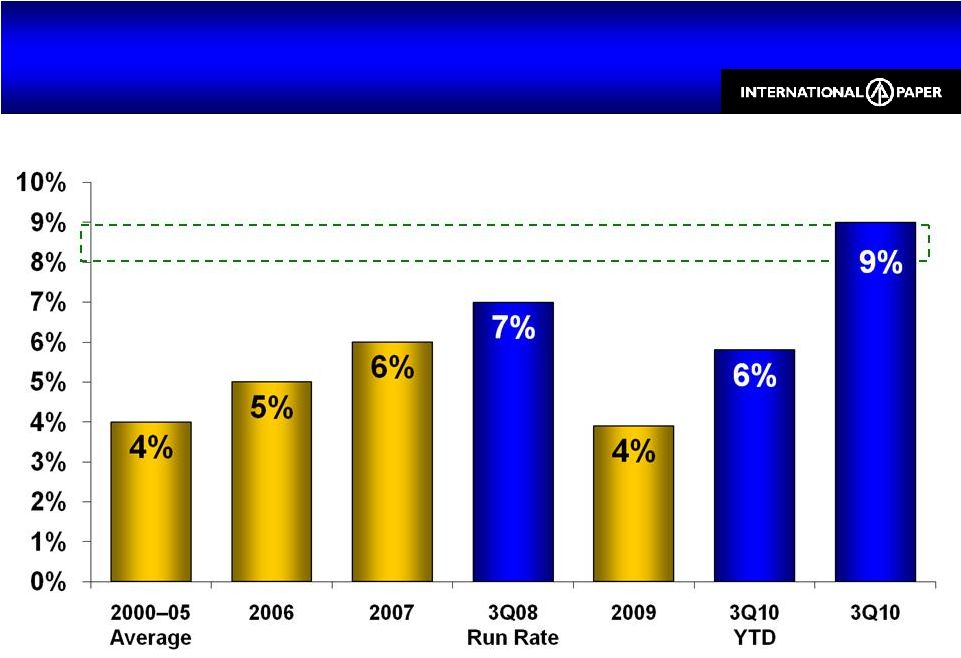

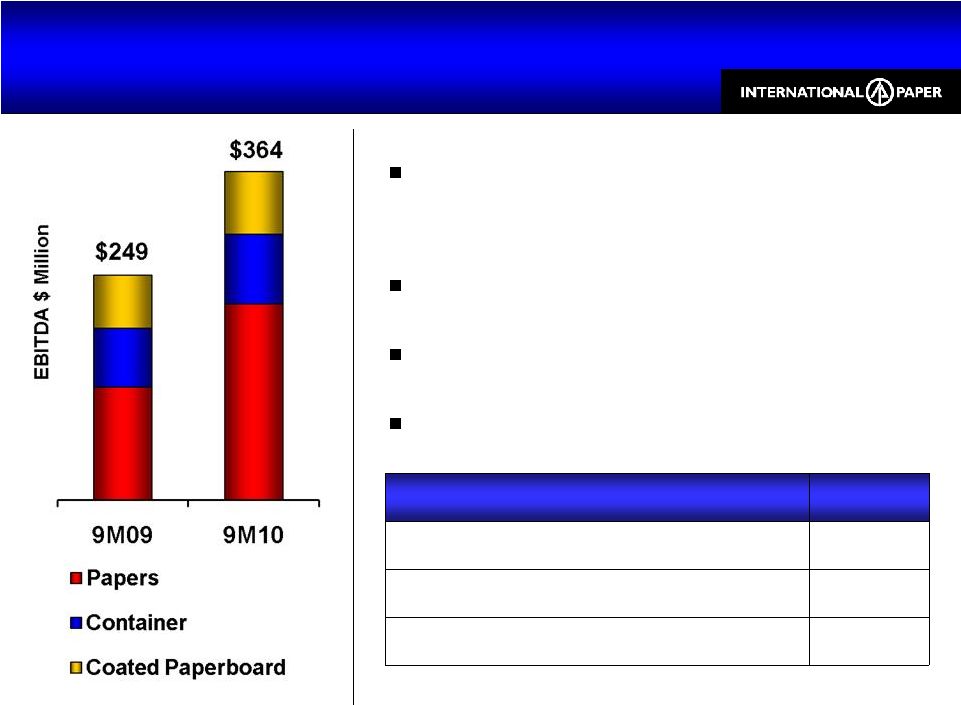

EBITDA Momentum Accelerating

EBITDA Momentum Accelerating

EBITDA

and

EBITDA

Margins

before

special

items,

excluding

Forest

Products |

10

Earnings before special items

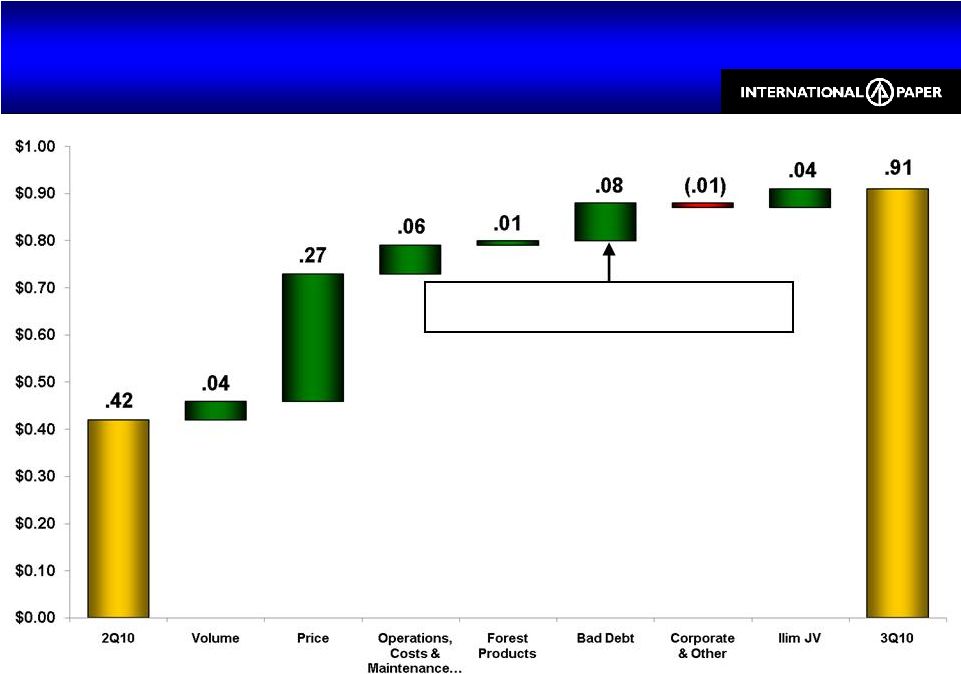

3Q10 vs. 2Q10 EPS

Price Realization, Improved Volumes, Strong Operations

3Q10 vs. 2Q10 EPS

Price Realization, Improved Volumes, Strong Operations

Reflects the delta between a $33 MM charge

in 2Q and $16 MM recovered in 3Q |

11

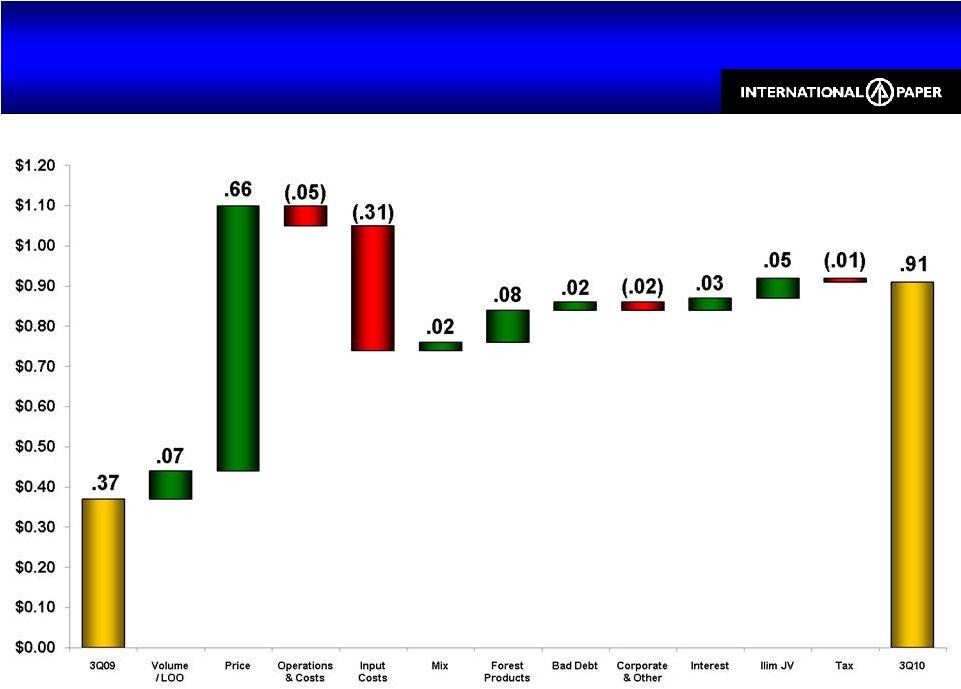

Earnings from continuing operations before special items

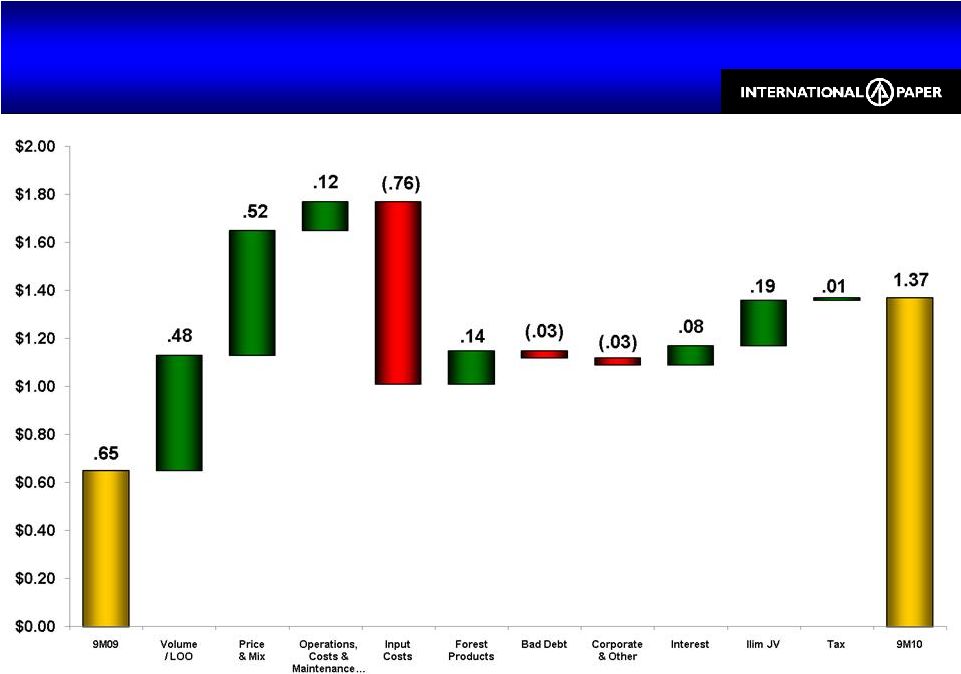

9M10 vs. 9M09 EPS

Higher

Prices, Improved Volumes, Elevated Fiber Costs

9M10 vs. 9M09 EPS

Higher

Prices, Improved Volumes, Elevated Fiber Costs |

12

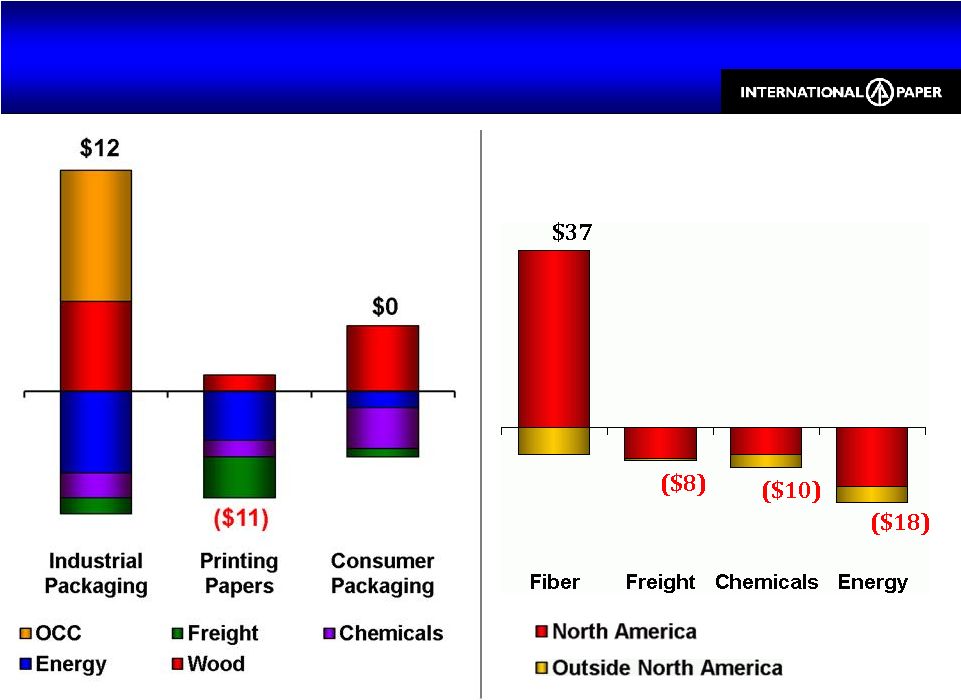

Stable Global Input Costs vs. 2Q10

$1 MM Favorable, or $0.00/Share

Stable Global Input Costs vs. 2Q10

$1 MM Favorable, or $0.00/Share

By Business

By Input Type |

13

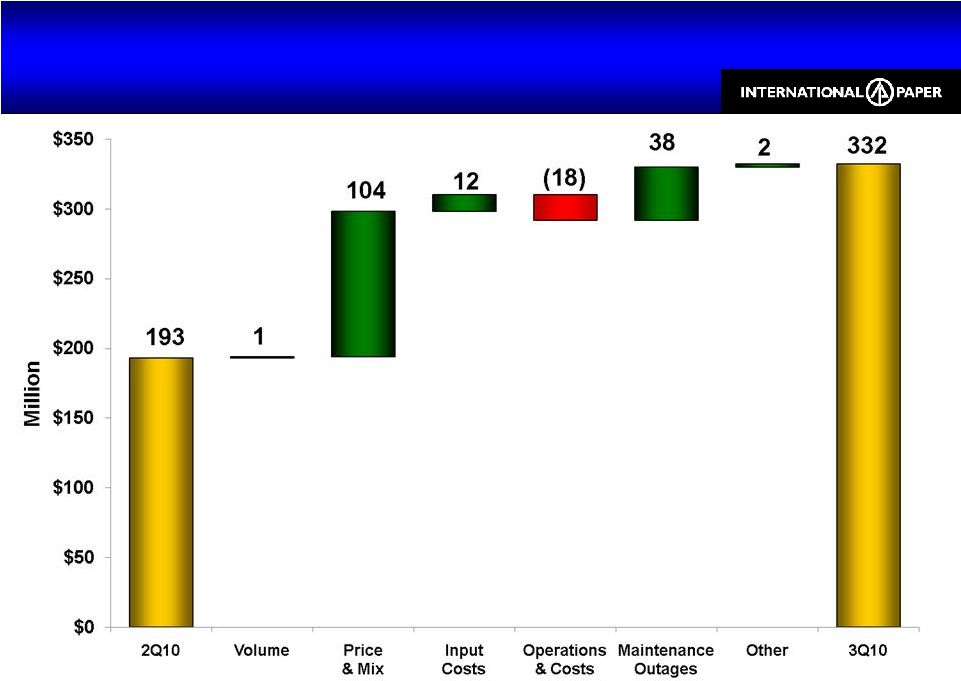

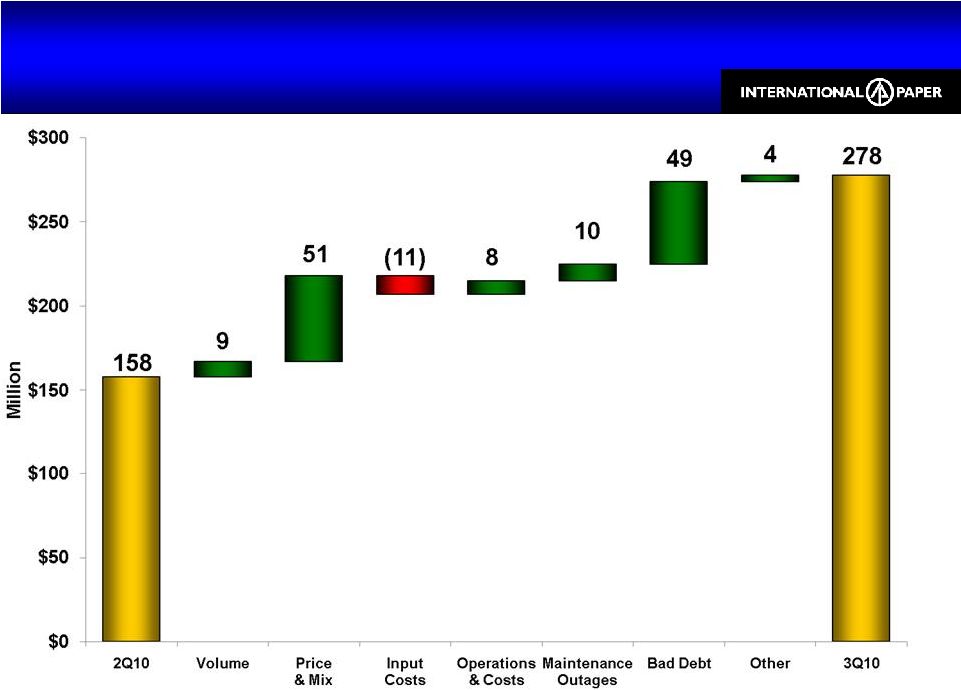

Industrial Packaging Earnings

3Q10 vs. 2Q10

Industrial Packaging Earnings

3Q10 vs. 2Q10

Earnings before special items |

14

3Q10 vs. 2Q10

3Q10 vs. 3Q09

Business

Volume

Price /

Ton

Volume

Price /

Ton

N.A. Container

(1%)

$38

4%

$72

European Container*

(4%)

€36

6%

€47

Industrial Packaging

Volume Recovery, Price Increase Realization

Industrial Packaging

Volume Recovery, Price Increase Realization

N.A. Price Improvement per Ton

vs. December 2009 Price

Sept 2010

Price / Ton

Corrugated Boxes

$95

* European Container volumes reflect box shipments only, including the shipments by

the non-consolidated joint venture in Turkey

|

15

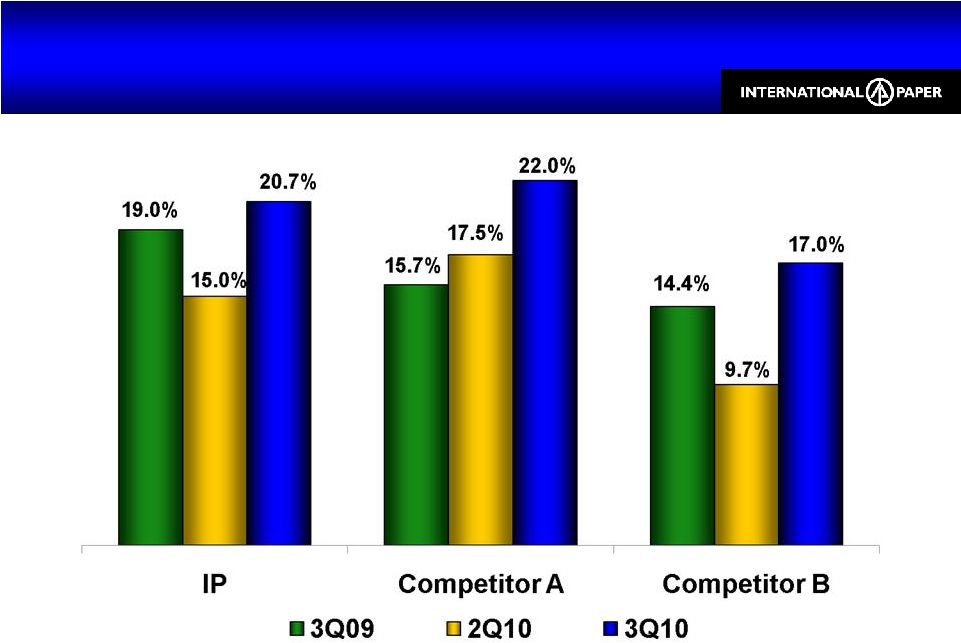

N.A. Industrial Packaging Relative EBITDA Margins

N.A. Industrial Packaging Relative EBITDA Margins

IP EBITDA margins based on North American Industrial Packaging operating profit

before special items Competitor EBITDA margin estimates obtained from public

filings and IP analysis |

16

Printing Papers Earnings

3Q10 vs. 2Q10

Printing Papers Earnings

3Q10 vs. 2Q10

Earnings before special items |

17

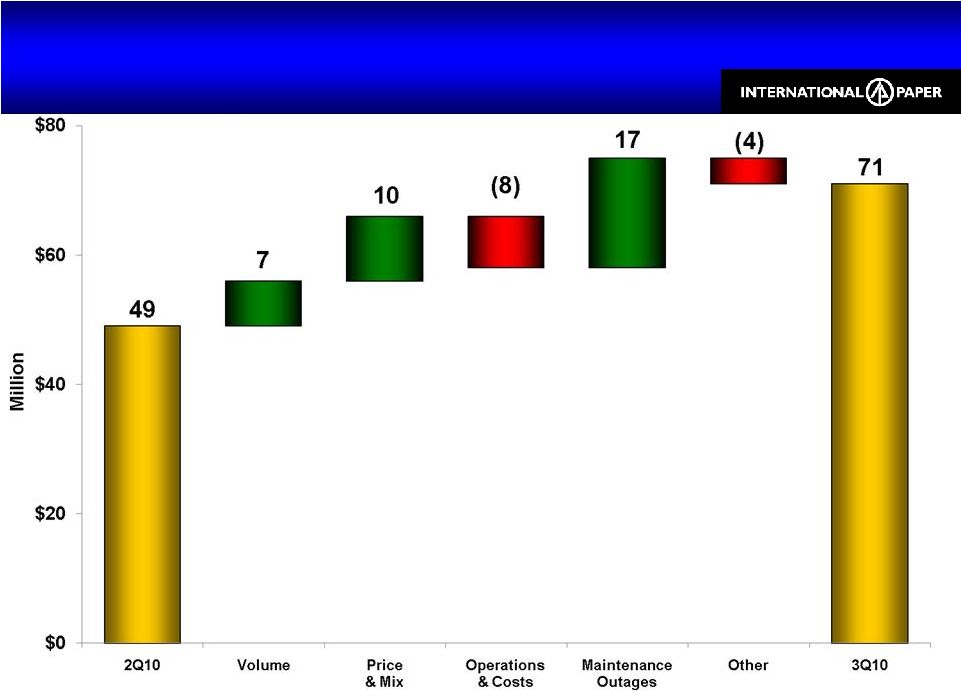

Consumer Packaging Earnings

3Q10 vs. 2Q10

Consumer Packaging Earnings

3Q10 vs. 2Q10

Earnings before special items |

18

$ Million

3Q09

2Q10

3Q10

Sales

$1,665

$1,630

$1,755

Earnings

$21

$26

$22

xpedx

3Q10 vs. 2Q10

xpedx

3Q10 vs. 2Q10

Revenues up 8% from 2Q10

Daily sales rate best since 4Q08

Daily Sales Change

vs. 2Q10

Printing

8.6%

Packaging

7.0%

Facility Supplies

4.4% |

19

Forest Products

Substantial

Completion of Land Sales

Forest Products

Substantial

Completion of Land Sales

Rock Creek Transaction Closed

Sales Price

$199MM

Retained Profit Interest in Partnership

20%

Cash Received at Closing

$160MM

To Be Received within 3 Years

$39MM

(plus Interest)

IP

has

minimal

land

remaining

for

sale

and

will

no

longer

report

land

sales

separately

after

4Q10

$ Million

3Q09

2Q10

3Q10

Earnings

$2

$40

$49 |

20

$ Million

3Q09

2Q10

3Q10

Sales (100%)

$305

$435

$465

Earnings (IP Share)

$0

$5

$22

Ilim’s

results are reported on a one-quarter lag

IP’s shares of Ilim’s

reported earnings for 3Q09 & 3Q10 include an after-tax foreign exchange

gain of $10 MM and an after-tax foreign exchange loss of $6 MM,

respectively. The foreign exchange impact in 2Q10 was minimal. Ilim

Joint Venture

3Q10 vs. 2Q10

Ilim

Joint Venture

3Q10 vs. 2Q10

3Q10 vs. 2Q10

3Q10 vs. 3Q09

Business

Volume

Price /

Ton

Volume

Price /

Ton

Pulp

(7%)

$131

3%

$327

Containerboard

(6%)

$61

1%

$141 |

21

IP Europe, Middle East & Africa

9M10: 10% of IP Sales & 15% of IP EBITDA

IP Europe, Middle East & Africa

9M10: 10% of IP Sales & 15% of IP EBITDA

On Pace for Record

Annual Earnings

Continued Demand Recovery

Price Increases Realized

Solid Operations

Return on Investment

9M10

European Papers, excl. Russia

19%

Russian Papers

15%

EMEA Container

11% |

22

Cellulosic Biofuel

Tax Credit

Analyzing the Potential Benefit to

IP Cellulosic Biofuel

Tax Credit

Analyzing the Potential Benefit to

IP CBTC is $1.01/gallon credit

against taxable income (excess may be carried forward until

2015)

OCT 5

th

–

IRS rules companies may qualify

for AFMTC and CBTC within 2009

Companies can pick & choose in order to

maximize benefit

To claim higher CBTC credit, companies

would have to repay cash received for

AFMTC & file amended tax returns

IP cannot quantify the value of CBTC

because it depends on future taxable

earnings, but it could be significant

IP produced

3.5 billion

gallons of

black liquor

in 2009 |

23

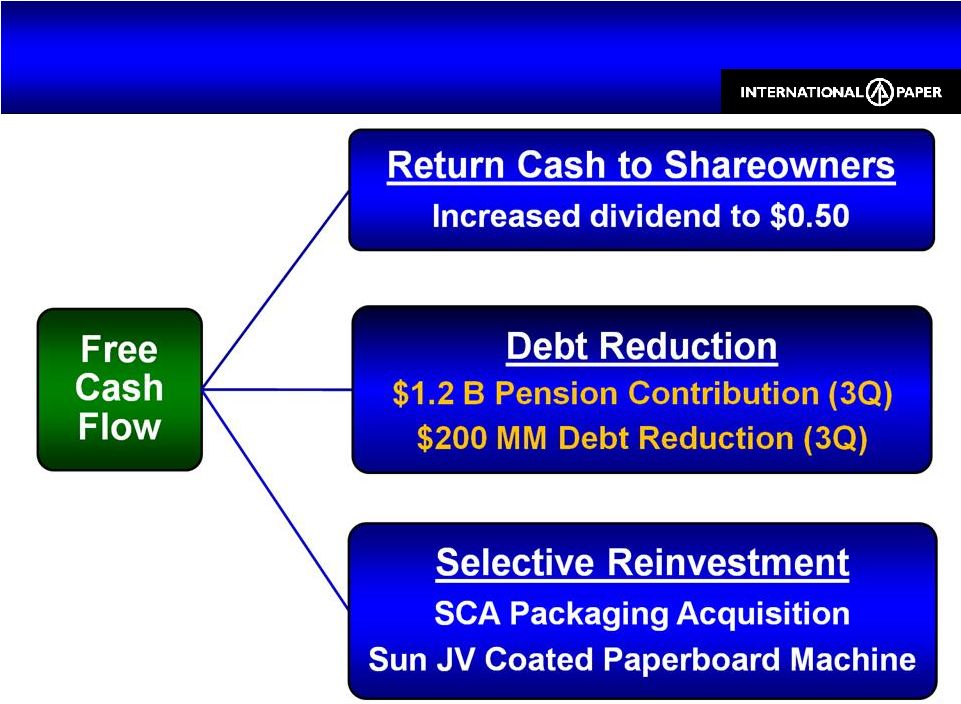

Balanced Capital Allocation

to Increase Shareowner Value

Balanced Capital Allocation

to Increase Shareowner Value |

24

Fourth Quarter Outlook

Changes from 3Q10

Fourth Quarter Outlook

Changes from 3Q10

North America

Europe

Brazil

Asia

Volume

Paper

Seasonal

Decrease

Stable

Stable

Packaging

Seasonal

Decrease

Seasonal

Increase

Stable

Pricing

Paper

Paper Stable;

Pulp Decrease

Stable

Stable

Packaging

Stable

Improving

Stable

Maintenance Outages

~$37MM

Increase

Stable

~$6MM

Decrease

Input & Freight Costs

Higher OCC

& Chemicals

Stable

Stable

Stable

xpedx

Seasonal

Decrease

Ilim

Stable

Forest

Products

$50MM

Decrease |

25

3Q Summary & 4Q Outlook

Strong, but Seasonally Lower, 4Q EPS & FCF

3Q Summary & 4Q Outlook

Strong, but Seasonally Lower, 4Q EPS & FCF

3Q10 Summary

Volume ended strong as

quarter progressed

Incremental price increase

realizations

Strong operations

Flat input costs

4Q10 Outlook

Seasonal demand declines

Stable prices

Higher maintenance outages

Increasing OCC & chemicals

costs

No more Forest Products

earnings

Strong 3Q Earnings

& Free Cash Flow

Strong, but Seasonally

Lower, 4Q EPS & FCF |

26

Appendix

Investor Relations Contacts

Thomas A. Cleves

901-419-7566

Emily Nix

901-419-4987

Media Contact

Tom Ryan

901-419-4333 |

27

$ Million

2008

2009

2010

Estimate

Capital Spending

$1,002

$534

$800

Depreciation &

Amortization

$1,347

$1,472

$1,450

Net Interest Expense

$492

$669

$600 -

$625

Corporate Items

$103

$181

$200 -

$225

Effective Tax Rate

31.5%

30%

30-32%

Before special items and excluding Ilim

Key Financial Statistics

Key Financial Statistics |

28

Free Cash Flow

Free Cash Flow

$ Million

3Q09

2Q10

3Q10

Cash from Operations

$713

$509

$937

Cash Received from Alternative Fuel

Mixture Tax Credits (AFMTC)

$463

$132

$0

Cash Provided by Operations,

as Adjusted

$1,381

$641

$937

Less Capital Investment

($108)

($153)

($184)

Free Cash Flow

$1,273

$488

$753

Free Cash Flow Excluding AFMTC

$605

$356

$753

1

Excludes $205 MM cash received under European accounts receivable securitization in

3Q09 2

Excludes $1.2 B cash paid for voluntary pension contributions.

1

2 |

29

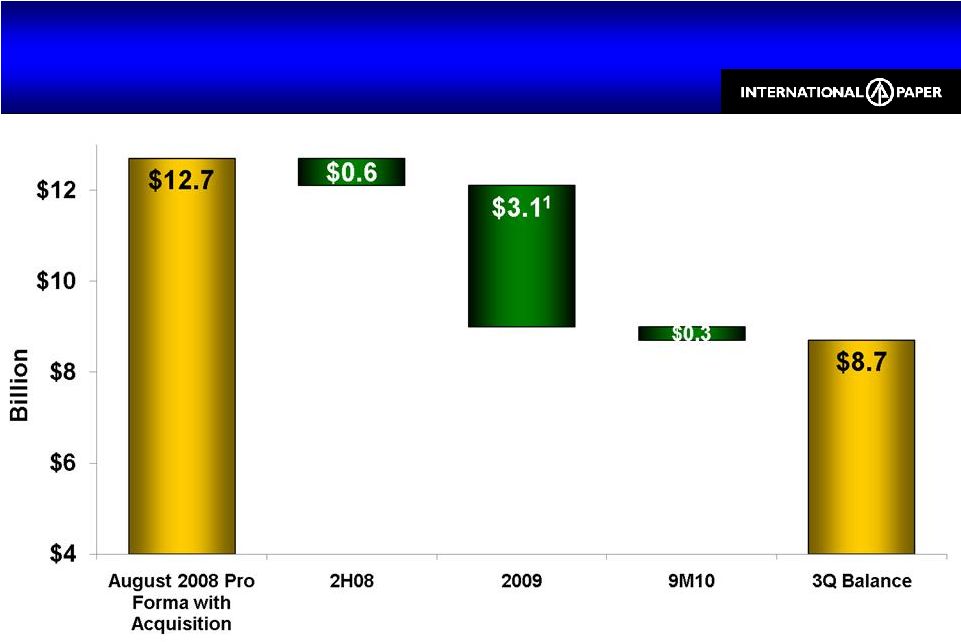

Balance Sheet Debt Reduction Progress

$4 Billion Reduction since Acquisition

Balance Sheet Debt Reduction Progress

$4 Billion Reduction since Acquisition

1

Excludes the debt repayment of $1 B from the proceeds of our May bond issuance: $1

B 9.375% notes due 2019 1

Excludes the debt repayment of $1 B from the proceeds of our August bond issuance:

$1 B 7.5% notes due 2021 1

Excludes the debt repayment of $750 MM from the proceeds of our November bond

issuance: $750 MM 7.3% notes due 2039 |

30

Monetization & Other: Intend to rollover or refinance timber monetization debt,

Sun JV debt and other foreign subsidiary debt Debt Maturity Profile

Maturities as of Quarter-End

Debt Maturity Profile

Maturities as of Quarter-End |

31

$ Million

1Q10

2Q10

3Q10

4Q10E

2010E

Industrial Packaging

$70

$41

$3

$26

$140

Printing Papers Total

$27

$60

$52

$44

$183

North America

$27

$45

$30

$28

$130

Europe

0

10

14

14

$38

Brazil

0

5

8

2

$15

Consumer Packaging

$6

$19

$0

$16

$41

Total Impact

$103

$120

$55

$86

$364

Dollar impact of planned maintenance outages are estimates and subject to

change Maintenance Outages Expenses

Maintenance Outages Expenses |

32

Average

IP

price

realization

(includes

the

impact

of

mix

across

all

grades)

3Q10 vs. 2Q10

3Q10 vs. 3Q09

Business

Volume

Price / Ton

Volume

Price / Ton

N.A. Paper

3%

$21

(9%)

$72

N.A. Pulp

30%

$19

(7%)

$244

European Paper

0%

€34

2%

€53

Printing Papers

Printing Papers |

33

Average IP price realization (includes the impact of mix across all grades)

3Q10 vs. 2Q10

3Q10 vs. 3Q09

Volume

Price/Ton

Volume

Price/Ton

U.S. Coated Paperboard

3%

$37

12%

$53

Revenue

Price

Revenue

Price

Converting Businesses

5%

NA

(1%)

NA

Consumer Packaging

Consumer Packaging |

34

3Q10 EBITDA

3Q10 EBITDA

Operating

Profit

$ Million

D & A

$ Million

Tons

Thousand

EBITDA

per Ton

EBITDA

Margin

Industrial Packaging

North America

$319

$138

2,607

$175

21.9%

Europe

$14

$7

251

$84

8.9%

Printing Papers

North America

$125

$49

707

$246

24.4%

Western Europe

$6

$5

62

$177

15.3%

Eastern Europe & Russia

$44

$14

249

$233

27.2%

Brazil

$46

$33

262

$302

28.7%

U.S. Market Pulp

$49

$14

279

$226

29.9%

Consumer Packaging

U.S. Coated Paperboard

$56

$38

364

$258

22.4%

1

Excludes Recycling & Bag businesses; includes Saturating Kraft business

2

Includes Bleached Kraft business

3

Excludes Market Pulp

1

2

3

3 |

35

Operating Profits by Industry Segment

Operating Profits by Industry Segment

$ Million

3Q09

2Q10

3Q10

Industrial Packaging

$214

$193

$332

Printing Papers

$138

$158

$278

Consumer Packaging

$68

$49

$71

Distribution

$21

$26

$22

Forest Products

$2

$40

$49

Operating Profit

$443

$466

$752

Net Interest Expense

($169)

($157)

($152)

Noncontrolling Interest / Equity Earnings Adjustment

$5

$7

$5

Corporate Items

($46)

($54)

($58)

Special Items

$356

($144)

$0

Earnings from continuing operations before income

taxes, equity earnings & noncontrolling interest

$589

$118

$547

Equity Earnings, net of taxes -

Ilim

$0

$5

$22 |

36

Geographic Business Segment Operating Results

Before Special Items

Geographic Business Segment Operating Results

Before Special Items

$ Million

Sales

Operating Profit

3Q09

2Q10

3Q10

3Q09

2Q10

3Q10

Industrial Packaging

North American

$1,890

$2,120

$2,210

$201

$172

$320

European

$240

$235

$235

$13

$18

$14

Asian

$100

$85

$165

$0

$2

($2)

Printing Papers

North American

$725

$675

$715

$92

$46

$125

European

$300

$320

$325

$28

$55

$58

Brazilian

$275

$275

$275

$36

$39

$46

U.S. Market Pulp

$155

$160

$210

($18)

$18

$49

Asian

$15

$15

$25

$0

$0

$0

Consumer Packaging

North American

$565

$580

$615

$44

$17

$51

European

$80

$80

$85

$17

$19

$17

Asian

$145

$185

$170

$7

$13

$3

Distribution

$1,665

$1,630

$1,755

$21

$26

$22

Excludes Forest Products |

37

1

2

Pre-Tax

$MM

Tax

$MM

Non-

controlling

Interest

$MM

Equity

Earnings

Net

Income

$MM

Estimated

Tax Rate

Average

Shares

MM

Diluted

EPS

Before Special Items

1Q10

$40

($13)

($9)

($2)

$16

32%

429

$0.04

2Q10

$262

($81)

($7)

$7

$181

31%

433

$0.42

3Q10

$547

($170)

($2)

$22

$397

31%

434

$0.91

Special Items

1Q10

($215)

$37

$0

$0

($178)

17%

429

($0.42)

2Q10

($144)

$56

$0

$0

($88)

39%

433

($0.21)

3Q10

$0

$0

$0

$0

$0

0%

434

$0

Earnings

1Q10

($175)

$24

($9)

($2)

($162)

14%

429

($0.38)

2Q10

$118

($25)

($7)

$7

$93

21%

433

$0.21

3Q10

$547

($170)

($2)

$22

$397

31%

434

$0.91

2010 Earnings from Continuing Operations

2010 Earnings from Continuing Operations

1

2

Assuming dilution

A

reconciliation to GAAP EPS is available at www.internationalpaper.com under the Investors tab at

Webcasts and Presentations |

38

Earnings from continuing operations before special items

3Q10 vs. 3Q09 EPS

3Q10 vs. 3Q09 EPS |

39

Industrial Packaging Earnings

3Q10 vs. 3Q09

Industrial Packaging Earnings

3Q10 vs. 3Q09

Earnings before special items |

40

Printing Papers Earnings

3Q10 vs. 3Q09

Printing Papers Earnings

3Q10 vs. 3Q09

Earnings before special items |

41

$ Million

3Q09

2Q10

3Q10

Sales

$275

$275

$275

Earnings

$36

$39

$46

EBITDA Margin

25%

27%

29%

IP Brazil results are reported in the Printing Papers segment

IP Brazil

IP Brazil

3Q10 vs. 2Q10

3Q10 vs. 3Q09

Business

Volume

Price /

Ton

Volume

Price /

Ton

Uncoated Freesheet

(7%)

$58

(7%)

$80

Domestic

17%

$5

(6%)

($10)

Export

(21%)

$102

(8%)

$153 |

42

Consumer Packaging Earnings

3Q10 vs. 3Q09

Consumer Packaging Earnings

3Q10 vs. 3Q09

Earnings before special items |

43

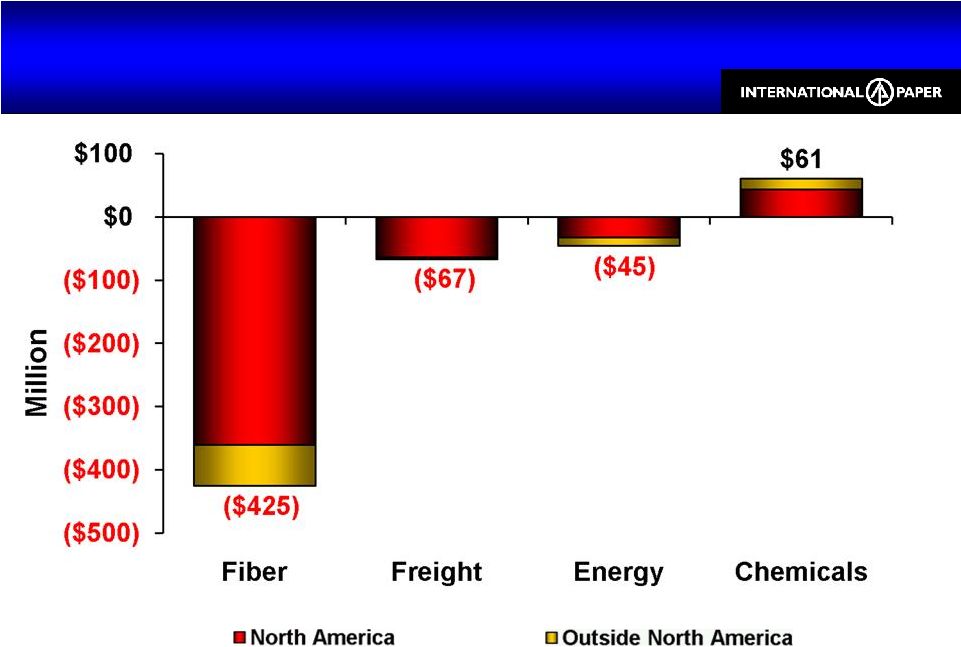

Total Cash Cost Components

3Q10 YTD

Total Cash Cost Components

3Q10 YTD

North American Mills Only |

44

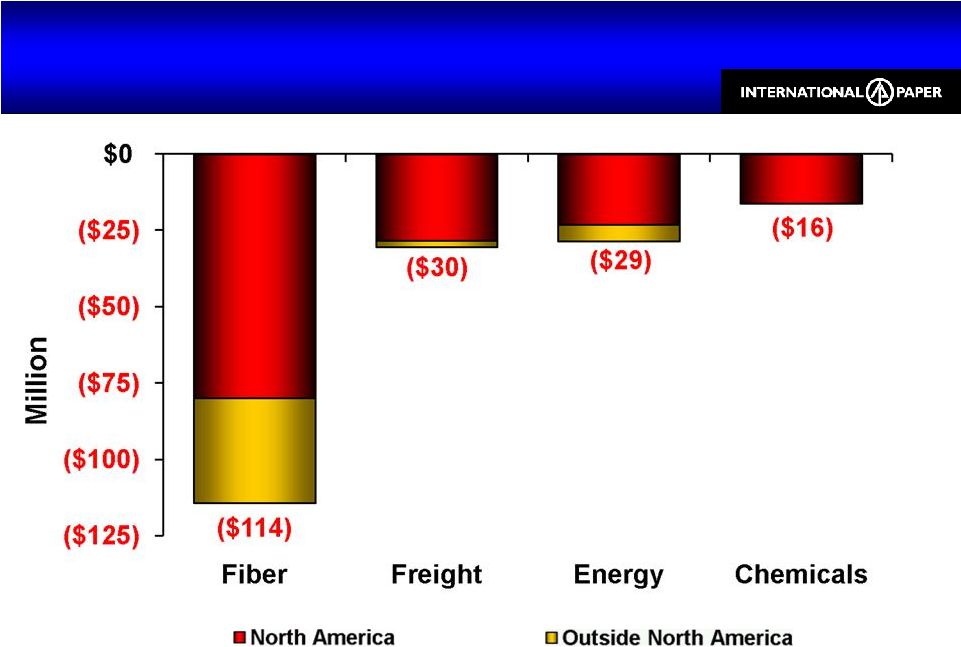

Global Input & Freight Costs vs. 9M09

$476 MM Unfavorable, or

$0.76/Share Global Input &

Freight Costs vs. 9M09 $476 MM Unfavorable, or $0.76/Share Input costs for continuing

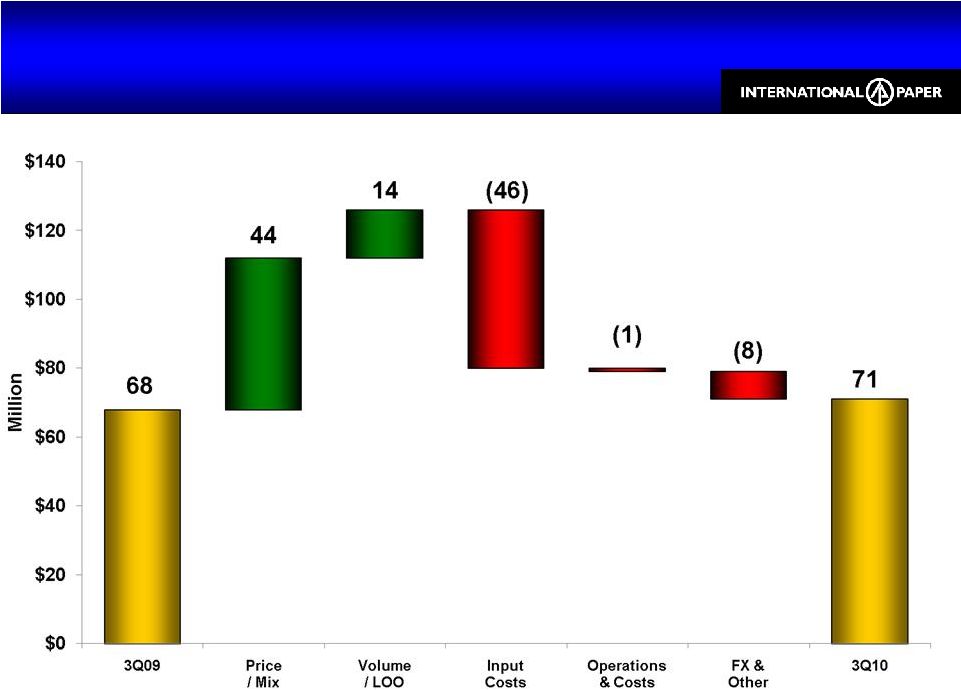

businesses |

45

Global Input & Freight Costs vs. 3Q09

$189 MM Unfavorable, or

$0.31/Share Global Input &

Freight Costs vs. 3Q09 $189 MM Unfavorable, or $0.31/Share Input costs for continuing

businesses |

46

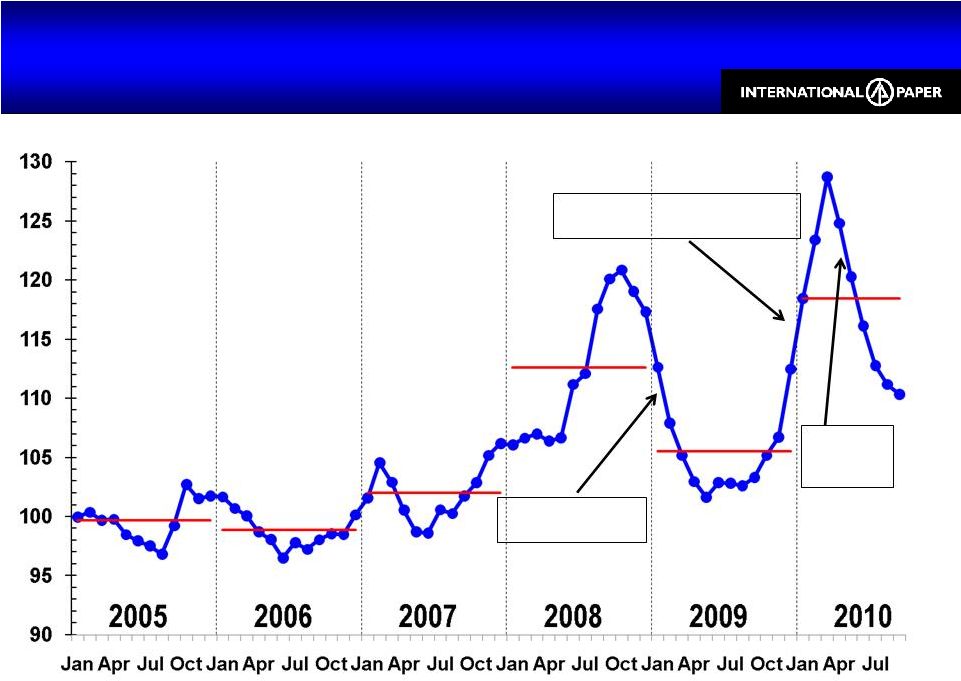

U.S. Mill Wood Delivered Cost Trends

7% Decrease vs. 2Q10 Average Cost

U.S. Mill Wood Delivered Cost Trends

7% Decrease vs. 2Q10 Average Cost

Declining Wood

Demand

Poor Harvesting Conditions &

Higher Wood Demand

Normal

Harvesting

Conditions |

47

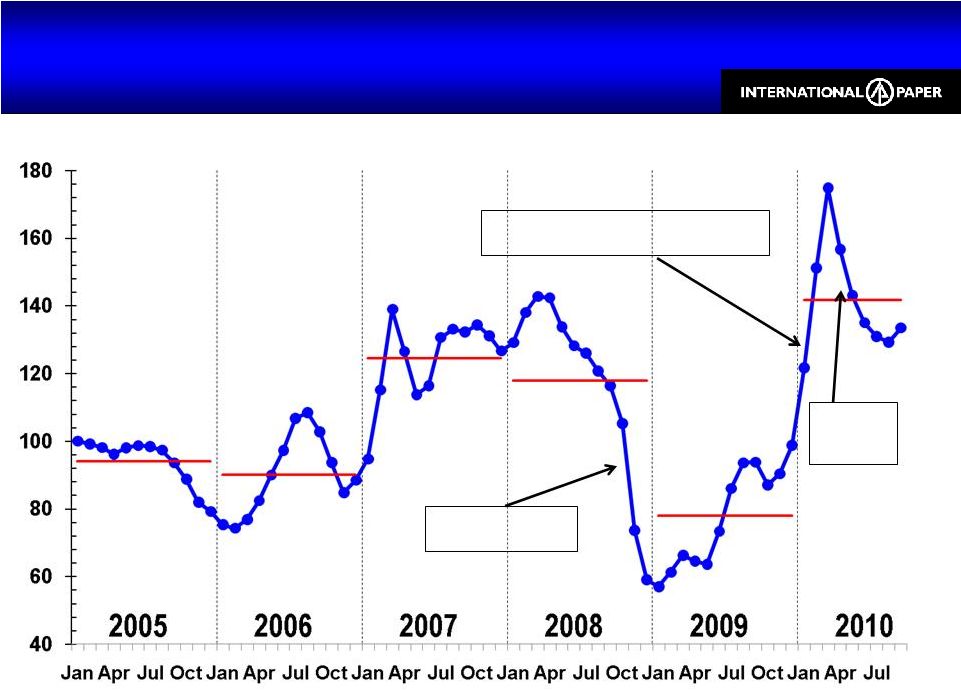

U.S. OCC Delivered Cost Trends

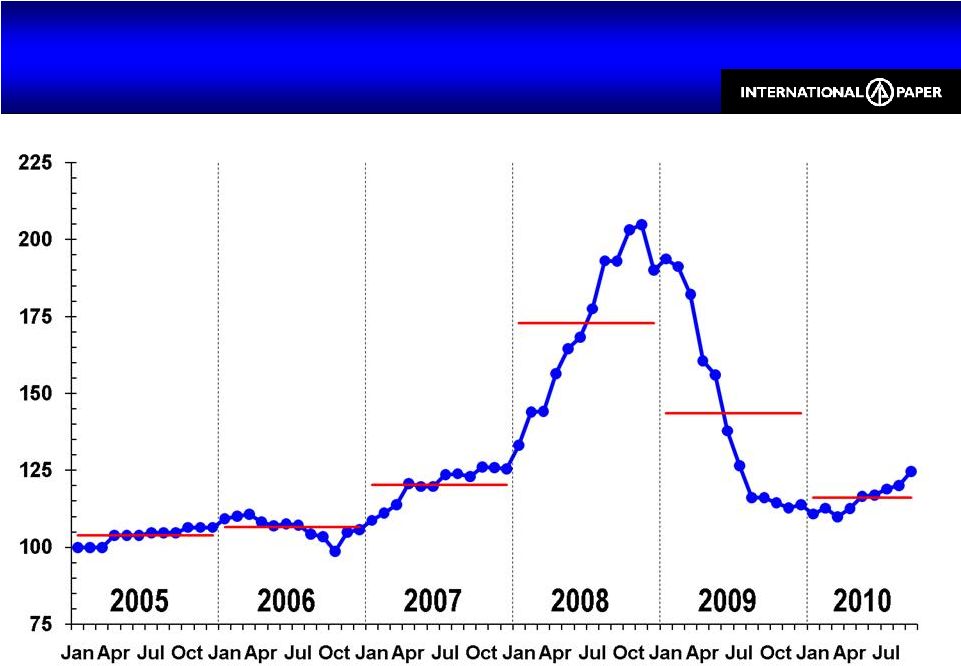

9% Decrease vs. 2Q10 Average Cost

U.S. OCC Delivered Cost Trends

9% Decrease vs. 2Q10 Average Cost

2005-2007 represents WY PKG delivered costs; 2008-2010 represents delivered

costs to the integrated system Reduced

OCC Demand

Reduced

China

Demand

Increasing Demand in China & in

U.S. as Wood Substitute |

48

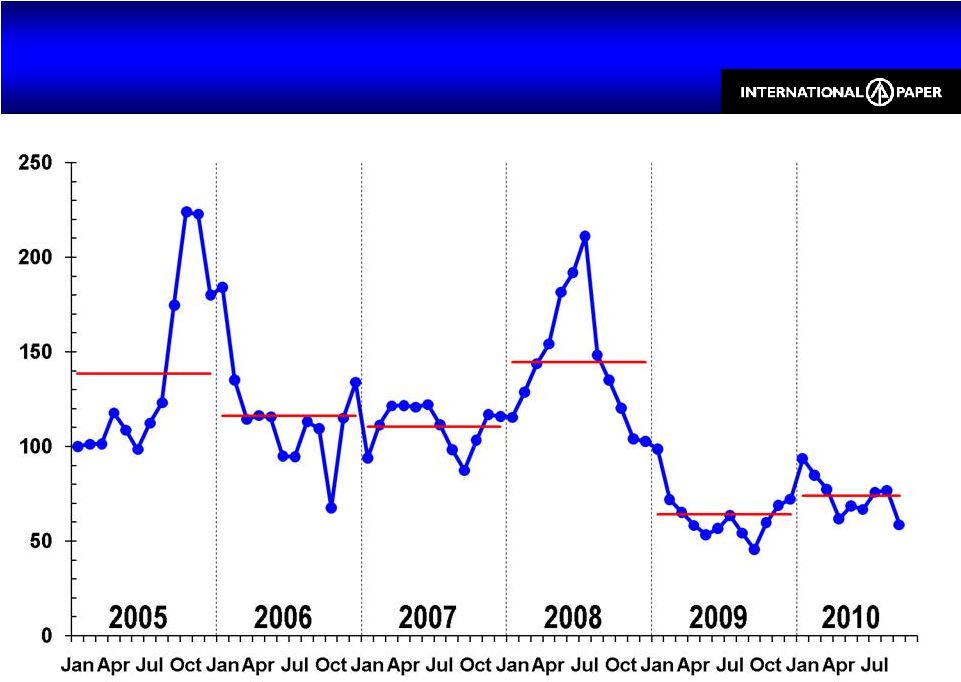

NYMEX Natural Gas closing prices

Natural Gas Costs

7% Increase vs. 2Q10 Average Cost

Natural Gas Costs

7% Increase vs. 2Q10 Average Cost |

49

U.S. Fuel Oil

3% Decrease vs. 2Q10 Average Cost

U.S. Fuel Oil

3% Decrease vs. 2Q10 Average Cost

WTI Crude prices |

50

U.S. Chemical Composite Index

5% Increase vs. 2Q10 Average Cost

U.S. Chemical Composite Index

5% Increase vs. 2Q10 Average Cost

Delivered

cost

to

U.S.

facilities;

includes

Caustic

Soda,

Sodium

Chlorate,

Starch

and

Sulfuric

Acid

2005 -

2008 excludes WY PKG |

51

2010 Global Consumption

Annual Purchase Estimates for Key Inputs

2010 Global Consumption

Annual Purchase Estimates for Key Inputs

Does not include Asian or Ilim consumption

Estimates are based on normal operations and may be impacted by downtime

Commodity

U. S.

Non –

U. S.

Energy

Natural Gas (MM BTUs)

42,000,000

13,000,000

Fuel Oil (Barrels)

1,500,000

500,000

Coal (Tons)

860,000

260,000

Fiber

Wood (Tons)

44,200,000

8,800,000

Old Corrugated Containers (Tons)

3,000,000

310,000

Chemicals

Caustic Soda (Tons)

250,000

70,000

Starch (Tons)

394,000

96,000

Sodium Chlorate (Tons)

180,000

40,000

LD Polyethylene (Tons)

39,000

-

Latex (Tons)

22,000

4,000 |