Attached files

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-Q

| x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the quarterly period ended September 30, 2010 |

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the transition period from to |

Commission File Number 333-08322

KANSAS CITY SOUTHERN DE MÉXICO, S.A. DE C.V.

(Exact name of Company as specified in its charter)

Kansas City Southern of Mexico

(Translation of Registrant’s name into English)

| Mexico |

|

98-0519243 | ||

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) | |||

|

Montes Urales 625 Lomas de Chapultepec 11000 Mexico, D.F. Mexico (Address of Principal Executive Offices) |

(5255) 9178-5686

(Company’s telephone number, including area code)

No Changes

(Former name, former address and former fiscal year, if changed since last report.)

Indicate by check mark whether the Company (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Company was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨ Not applicable ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer ¨ Accelerated filer ¨ Non-accelerated filer x Smaller reporting company ¨

(Do not check if a smaller reporting company)

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of September 30, 2010: 4,785,510,235

Kansas City Southern de México, S.A. de C.V. meets the conditions set forth in General Instruction H(1)(a) and (b) of Form 10-Q and is therefore filing this Form with the reduced disclosure format.

Table of Contents

Kansas City Southern de México, S.A. de C.V. and Subsidiaries

Form 10-Q

September 30, 2010

Index

2

Table of Contents

Kansas City Southern de México, S.A. de C.V. and Subsidiaries

Form 10-Q

September 30, 2010

PART I—FINANCIAL INFORMATION

| Item 1. | Financial Statements |

The Consolidated Financial Statements included herein have been prepared by Kansas City Southern de México, S.A. de C.V. (“KCSM” or the “Company”), without audit, pursuant to the rules and regulations of the Securities and Exchange Commission (“SEC”). For the purposes of this report, unless the context otherwise requires, all references herein to “KCSM” and the “Company” shall mean Kansas City Southern de México, S.A. de C.V. and its subsidiaries. Certain information and footnote disclosures normally included in financial statements prepared in accordance with U.S. generally accepted accounting principles (“U.S. GAAP”) have been condensed or omitted pursuant to such rules and regulations. The Company believes that the disclosures are adequate to enable a reasonable understanding of the information presented. The Consolidated Financial Statements and Management’s Discussion and Analysis of Financial Condition and Results of Operations included in this Form 10-Q should be read in conjunction with the consolidated financial statements and the related notes, as well as Management’s Discussion and Analysis of Financial Condition and Results of Operations, included in the Company’s Annual Report on Form 10-K for the year ended December 31, 2009. Results for the three and nine months ended September 30, 2010 are not necessarily indicative of the results expected for the full year ending December 31, 2010.

3

Table of Contents

Kansas City Southern de México, S.A. de C.V. and Subsidiaries

Consolidated Statements of Operations

| Three Months Ended September 30, |

Nine Months Ended September 30, |

|||||||||||||||

| 2010 | 2009 | 2010 | 2009 | |||||||||||||

| (In millions) (Unaudited) |

||||||||||||||||

| Revenues |

$ | 184.8 | $ | 158.3 | $ | 582.4 | $ | 438.5 | ||||||||

| Operating expenses: |

||||||||||||||||

| Compensation and benefits |

18.3 | 19.8 | 66.0 | 53.9 | ||||||||||||

| Purchased services |

32.0 | 22.3 | 95.7 | 80.4 | ||||||||||||

| Fuel |

26.9 | 22.6 | 85.7 | 61.0 | ||||||||||||

| Equipment costs |

18.7 | 22.4 | 57.1 | 64.5 | ||||||||||||

| Depreciation and amortization |

24.4 | 25.5 | 72.7 | 81.3 | ||||||||||||

| Casualties and insurance |

2.0 | 1.4 | 6.0 | 5.6 | ||||||||||||

| Materials and other |

10.7 | 8.6 | 32.8 | 27.9 | ||||||||||||

| Total operating expenses |

133.0 | 122.6 | 416.0 | 374.6 | ||||||||||||

| Operating income |

51.8 | 35.7 | 166.4 | 63.9 | ||||||||||||

| Equity in net earnings of unconsolidated affiliates |

1.1 | 1.6 | 5.5 | 1.2 | ||||||||||||

| Interest expense |

(22.4 | ) | (28.1 | ) | (75.6 | ) | (81.2 | ) | ||||||||

| Debt retirement costs |

(1.9 | ) | — | (33.5 | ) | (0.6 | ) | |||||||||

| Foreign exchange gain (loss) |

2.1 | (1.5 | ) | 3.4 | (0.6 | ) | ||||||||||

| Other income, net |

0.4 | 0.8 | 1.9 | 2.0 | ||||||||||||

| Income (loss) before income taxes |

31.1 | 8.5 | 68.1 | (15.3 | ) | |||||||||||

| Income tax (benefit) expense |

12.1 | 2.6 | 22.9 | (4.7 | ) | |||||||||||

| Net income (loss) |

$ | 19.0 | $ | 5.9 | $ | 45.2 | $ | (10.6 | ) | |||||||

See accompanying notes to consolidated financial statements.

4

Table of Contents

Kansas City Southern de México, S.A. de C.V. and Subsidiaries

Consolidated Balance Sheets

| September 30, 2010 |

December 31, 2009 |

|||||||

| (In millions, except share amounts) |

||||||||

| (Unaudited) | ||||||||

| ASSETS | ||||||||

| Current assets: |

||||||||

| Cash and cash equivalents |

$ | 11.6 | $ | 92.6 | ||||

| Accounts receivable, net |

93.6 | 61.6 | ||||||

| Related company receivable |

16.6 | 16.8 | ||||||

| Materials and supplies |

34.6 | 37.4 | ||||||

| Deferred income tax asset |

153.4 | 117.3 | ||||||

| Other current assets |

82.0 | 48.9 | ||||||

| Total current assets |

391.8 | 374.6 | ||||||

| Investments |

10.9 | 46.8 | ||||||

| Property and equipment (including concession assets), net |

2,259.2 | 2,239.7 | ||||||

| Related company receivable |

— | 31.1 | ||||||

| Other assets |

32.5 | 25.3 | ||||||

| Total assets |

$ | 2,694.4 | $ | 2,717.5 | ||||

| LIABILITIES AND STOCKHOLDERS' EQUITY | ||||||||

| Current liabilities: |

||||||||

| Debt due within one year |

$ | 16.0 | $ | 11.0 | ||||

| Accounts payable and accrued liabilities |

145.1 | 112.7 | ||||||

| Related company payable |

4.9 | 27.1 | ||||||

| Total current liabilities |

166.0 | 150.8 | ||||||

| Long-term debt |

863.9 | 1,103.5 | ||||||

| Related company debt |

21.6 | 21.6 | ||||||

| Deferred income tax liability |

78.4 | 16.8 | ||||||

| Other noncurrent liabilities and deferred credits |

93.6 | 94.5 | ||||||

| Total liabilities |

1,223.5 | 1,387.2 | ||||||

| Commitments and contingencies |

— | — | ||||||

| Stockholders’ equity: |

||||||||

| Common stock, 4,785,510,235 shares authorized, issued without par value |

602.3 | 507.3 | ||||||

| Additional paid-in capital |

243.6 | 243.6 | ||||||

| Retained earnings |

628.0 | 582.8 | ||||||

| Accumulated other comprehensive loss |

(3.0 | ) | (3.4 | ) | ||||

| Total stockholders’ equity |

1,470.9 | 1,330.3 | ||||||

| Total liabilities and stockholders’ equity |

$ | 2,694.4 | $ | 2,717.5 | ||||

See accompanying notes to consolidated financial statements.

5

Table of Contents

Kansas City Southern de México, S.A. de C.V. and Subsidiaries

Consolidated Statements of Cash Flows

| Nine

Months Ended September 30, |

||||||||

| 2010 | 2009 | |||||||

| (In millions) | ||||||||

| (Unaudited) | ||||||||

| Operating activities: |

||||||||

| Net income (loss) |

$ | 45.2 | $ | (10.6 | ) | |||

| Adjustments to reconcile net income (loss) to net cash provided by operating activities: |

||||||||

| Depreciation and amortization |

72.7 | 81.3 | ||||||

| Deferred income taxes (benefit) |

22.9 | (4.7 | ) | |||||

| Equity in undistributed earnings of unconsolidated affiliates |

(5.5 | ) | (1.2 | ) | ||||

| Deferred compensation |

5.9 | (1.8 | ) | |||||

| Distributions from unconsolidated affiliates |

1.5 | — | ||||||

| Debt retirement cost |

33.5 | 0.6 | ||||||

| Gain on sale of Mexrail, Inc. |

(0.7 | ) | — | |||||

| Changes in working capital items: |

||||||||

| Accounts receivable |

(31.6 | ) | (6.4 | ) | ||||

| Related companies |

(22.3 | ) | 5.1 | |||||

| Materials and supplies |

2.8 | (11.1 | ) | |||||

| Other current assets |

(3.2 | ) | 7.7 | |||||

| Accounts payable and accrued liabilities |

24.9 | 12.8 | ||||||

| Other, net |

(19.0 | ) | 12.6 | |||||

| Net cash provided by operating activities |

127.1 | 84.3 | ||||||

| Investing activities: |

||||||||

| Capital expenditures |

(79.4 | ) | (107.8 | ) | ||||

| Proceeds from disposal of property |

2.2 | 6.0 | ||||||

| Proceeds and repayments from loan to related company |

31.4 | — | ||||||

| Acquisition of an intermodal facility, net of cash acquired |

(25.0 | ) | — | |||||

| Proceeds from sale of Mexrail, Inc. |

41.0 | — | ||||||

| Other, net |

0.1 | (1.3 | ) | |||||

| Net cash used for investing activities |

(29.7 | ) | (103.1 | ) | ||||

| Financing activities: |

||||||||

| Proceeds from issuance of long-term debt |

300.7 | 189.0 | ||||||

| Proceeds from issuance of related company debt |

— | 21.6 | ||||||

| Repayment of long-term debt |

(539.7 | ) | (39.0 | ) | ||||

| Debt costs |

(34.4 | ) | (4.2 | ) | ||||

| Pro-rata contribution (distribution) on common stock |

95.0 | (101.0 | ) | |||||

| Net cash provided by (used for) financing activities |

(178.4 | ) | 66.4 | |||||

| Cash and cash equivalents: |

||||||||

| Net increase (decrease) during each period |

(81.0 | ) | 47.6 | |||||

| At beginning of the year |

92.6 | 38.9 | ||||||

| At end of the period |

$ | 11.6 | $ | 86.5 | ||||

See accompanying notes to consolidated financial statements.

6

Table of Contents

Kansas City Southern de México, S.A. de C.V. and Subsidiaries

Notes to Consolidated Financial Statements

(Amounts in millions of U.S. dollars)

1. Accounting Policies, Interim Financial Statements and Basis of Presentation

In the opinion of the management of KCSM, the accompanying unaudited consolidated financial statements contain all adjustments necessary for a fair presentation of the results for interim periods. All adjustments made were of a normal recurring nature. Certain information and footnote disclosures normally included in financial statements prepared in accordance with U.S. GAAP have been condensed or omitted. These consolidated financial statements should be read in conjunction with the consolidated financial statements and accompanying notes included in the Company’s Annual Report on Form 10-K for the year ended December 31, 2009. The results of operations for the three and nine months ended September 30, 2010, are not necessarily indicative of the results expected for the full year ending December 31, 2010. Certain prior year amounts have been reclassified to conform to the current year presentation.

During the first quarter of 2010, the Company elected to change its accounting policy for rail grinding costs from a capitalization method to a direct expense method. Previously, the Company capitalized rail grinding costs as an improvement to the rail. The Company believes it is preferable to expense these costs as incurred to eliminate the subjectivity in determining the period of benefit associated with rail grinding over which to depreciate the associated capitalized costs. The Company has reflected this change as a change in accounting principle from an accepted accounting principle to a preferable accounting principle in accordance with Accounting Standards Codification 250 “Accounting for Changes and Error Corrections.” Comparative financial statements for all periods have been adjusted to apply the change in accounting principle retrospectively.

The following line items in the consolidated statements of operations were affected by the change in accounting principle (in millions):

| Three Months Ended September 30, 2009 | ||||||||||||

| As reported | As adjusted | Change | ||||||||||

| Purchased services |

$ | 21.6 | $ | 22.3 | $ | 0.7 | ||||||

| Equity in net earnings of unconsolidated affiliates |

1.5 | 1.6 | 0.1 | |||||||||

| Income before income taxes |

9.1 | 8.5 | (0.6 | ) | ||||||||

| Income tax expense |

2.8 | 2.6 | (0.2 | ) | ||||||||

| Net income |

$ | 6.3 | $ | 5.9 | $ | (0.4 | ) | |||||

| Nine Months Ended September 30, 2009 | ||||||||||||

| As reported | As adjusted | Change | ||||||||||

| Compensation and benefits |

$ | 54.0 | $ | 53.9 | $ | (0.1 | ) | |||||

| Purchased services |

79.3 | 80.4 | 1.1 | |||||||||

| Loss before income taxes |

(14.3 | ) | (15.3 | ) | (1.0 | ) | ||||||

| Income tax benefit |

(4.4 | ) | (4.7 | ) | (0.3 | ) | ||||||

| Net loss |

$ | (9.9 | ) | $ | (10.6 | ) | $ | (0.7 | ) | |||

| The following line items in the consolidated balance sheet were affected by the change in accounting principle (in millions): | ||||||||||||

| December 31, 2009 | ||||||||||||

| As reported | As adjusted | Change | ||||||||||

| Investments |

$ | 46.9 | $ | 46.8 | $ | (0.1 | ) | |||||

| Property and equipment (including concession assets), net |

2,246.0 | 2,239.7 | (6.3 | ) | ||||||||

| Deferred income taxes |

18.2 | 16.8 | (1.4 | ) | ||||||||

| Other noncurrent liabilities and deferred credits |

95.0 | 94.5 | (0.5 | ) | ||||||||

| Retained earnings |

587.3 | 582.8 | (4.5 | ) | ||||||||

| Total stockholders' equity |

$ | 1,334.8 | $ | 1,330.3 | $ | (4.5 | ) | |||||

7

Table of Contents

Kansas City Southern de México, S.A. de C.V. and Subsidiaries

Notes to Consolidated Financial Statements—(Continued)

(Amounts in millions of U.S. dollars)

As of January 1, 2008, the cumulative effect of the change in accounting principle on investments, property and equipment (including concession assets), deferred income tax liability, other noncurrent liabilities and deferred credits and retained earnings was ($0.1) million, ($3.9) million, ($1.0) million, ($0.4) million and ($2.6) million, respectively.

The following line items in the consolidated statement of cash flow were affected by the change in accounting principle (in millions):

| Nine Months Ended September 30, 2009 | ||||||||||||

| As reported | As adjusted | Change | ||||||||||

| Net cash provided by operating activities |

$ | 85.4 | $ | 84.3 | $ | (1.1 | ) | |||||

| Net cash used for investing activities |

$ | (104.2 | ) | $ | (103.1 | ) | $ | 1.1 | ||||

2. Hurricane Alex

Hurricane Alex made landfall on June 30, 2010, causing widespread damage and flooding in central and northeastern Mexico. The hurricane resulted in extensive damage to the Company’s track and bridge infrastructures, and also caused multiple track-related incidents and significantly disrupted the Company’s rail service.

Kansas City Southern (“KCS”), KCSM’s controlling stockholder, and KCSM maintain a comprehensive insurance program intended to cover such events. The property and casualty insurance program covers loss or damage to Company property and third party property over which the Company has custody and control and covers losses associated with business interruption. This program has combined coverage for both property damage and business interruption and has a self-insured retention amount of $10.0 million for flood related losses. In addition, KCS and KSCM also maintain a general liability insurance program with a self-insured retention of $1.0 million in Mexico covering claims from third parties. The policy limits are in excess of the hurricane losses incurred.

Hurricane Alex affected revenues as customers were required to use alternate carriers or modes of transportation until rail service was restored. Based on data contained in the initial insurance claim filing, which will be updated and adjusted, the Company currently estimates that resulting lost revenues in the third quarter of 2010 were $25.0 million, less related avoided costs. Additionally, the Company incurred losses of $31.0 million related to property damage and incremental expenses. Through its insurance programs, the Company expects to recover its losses, net of related self-insured retentions of $11.0 million. Accordingly, the Company recognized a receivable for probable insurance recoveries which offsets the impact of incurred losses related to property damage and incremental expenses. The recognition of remaining probable insurance recoveries represents a contingent gain, which will be recognized when all contingencies have been resolved, which generally occurs at the time of final settlement or when nonrefundable cash payments are received.

The initial claim filing includes estimates of costs the Company expects to incur in the fourth quarter of 2010 related to ongoing property repair which are expected to be fully offset by probable insurance recoveries. As of the date of this filing, no payments have been received from the insurance programs.

3. Post-Employment Benefits

Mexican law requires that KCSM provide certain post-employment benefits to its union and non-union employees. These plans provide statutorily calculated benefits which are payable upon retirement, death, disability, voluntary or involuntary termination of employees based on length of service.

During September 2010, KCSM completed negotiations with the labor union. Among other matters resolved in these negotiations, KCSM is not required to provide an incremental benefit to its union employees upon retirement. Previous to the agreement reached with the labor union, KCSM had recorded a liability for an incremental retirement benefit which was based on various factors including retirement eligibility based on a combination of age and years of credited service and the employee’s salary at the time of retirement. KCSM has no legal obligation to fund any benefit previously calculated under these factors.

8

Table of Contents

Kansas City Southern de México, S.A. de C.V. and Subsidiaries

Notes to Consolidated Financial Statements—(Continued)

(Amounts in millions of U.S. dollars)

The completion of the negotiations resulted in a new measurement date for KCSM’s post-employment benefit obligations as of September 30, 2010. These post-employment benefit obligations are funded as obligations become due. The following table reconciles the change in the benefit obligations as of and for the nine months ended September 30, 2010 (in millions):

| For the Nine Months Ended September 30, 2010 |

||||

| Benefit obligation at beginning of period |

$ | 15.9 | ||

| Service cost |

1.0 | |||

| Interest cost |

1.1 | |||

| Actuarial gain |

(6.2 | ) | ||

| Foreign currency gain |

(0.7 | ) | ||

| Benefits paid |

(0.8 | ) | ||

| Benefit obligation at end of period |

$ | 10.3 | ||

The assumptions used to determine benefit obligations and costs are selected based on current and expected market conditions. Discount rates are selected based on low risk government bonds with cash flows approximating the timing of expected benefit payments. The Mexico bond market is utilized for the KCSM post-employment obligation.

Weighted average assumptions used to determine benefit cost were as follows:

| September 30, 2010 |

December 31, 2009 |

|||||||

| Discount Rate |

7.5 | % | 8.5 | % | ||||

| Rate of compensation increase |

4.5 | % | 4.5 | % | ||||

4. Property and Equipment (including Concession Assets)

Property and Equipment. Property and equipment, including concession assets, and related accumulated depreciation and amortization are summarized below (in millions):

| September 30, 2010 |

December 31, 2009 |

|||||||

| Land |

$ | 79.5 | $ | 65.0 | ||||

| Concession land rights |

141.2 | 137.6 | ||||||

| Road property |

1,953.2 | 1,900.4 | ||||||

| Equipment |

405.2 | 373.7 | ||||||

| Technology and other |

19.7 | 17.7 | ||||||

| Construction in progress |

65.8 | 95.4 | ||||||

| Total property |

2,664.6 | 2,589.8 | ||||||

| Accumulated depreciation |

405.4 | 350.1 | ||||||

| Net property and equipment (including concession assets) |

$ | 2,259.2 | $ | 2,239.7 | ||||

Concession assets, net of accumulated amortization of $290.5 million and $259.4 million, totaled $1,775.9 million and $1,768.0 million at September 30, 2010 and December 31, 2009, respectively.

5. Foreign Currency Balances

At September 30, 2010, KCSM had financial assets and financial liabilities denominated in Mexican pesos of Ps.1,435.6 million and Ps.328.3 million, respectively. At December 31, 2009, KCSM had financial assets and financial liabilities denominated in Mexican pesos of Ps.1,355.2 million and Ps.459.2 million, respectively. At September 30, 2010 and at December 31, 2009, the exchange rate was Ps.12.50 and Ps.13.06 per U.S. dollar, respectively.

9

Table of Contents

Kansas City Southern de México, S.A. de C.V. and Subsidiaries

Notes to Consolidated Financial Statements—(Continued)

(Amounts in millions of U.S. dollars)

6. Fair Value Measurements

The Company’s short term financial instruments include cash and cash equivalents, accounts receivable, and accounts payable. The carrying value of the short term financial instruments approximates their fair value.

The fair value of the Company’s debt is estimated using quoted market prices when available. When quoted market prices are not available, fair value is estimated based on current market interest rates for debt with similar maturities. The fair value of the Company’s debt was $969.0 million and $1,170.0 million at September 30, 2010 and December 31, 2009, respectively. The carrying value was $901.5 million and $1,136.1 million at September 30, 2010 and December 31, 2009, respectively.

Assets and liabilities recognized at fair value are required to be classified into a three-level hierarchy. In general, fair values determined by Level 1 inputs utilize quoted prices (unadjusted) in active markets for identical assets or liabilities that the Company has the ability to access. Level 2 inputs include quoted prices for similar assets and liabilities in active markets, and inputs other than quoted prices that are observable for the asset or liability. Level 3 inputs are unobservable inputs for the asset or liability, and include situations where there is little, if any, market activity for the asset or liability. In certain cases, the inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, the level in the fair value hierarchy within which the fair value measurement in its entirety falls has been determined based on the lowest level input that is significant to the fair value measurement in its entirety. The Company’s assessment of the significance of a particular input to the fair value in its entirety requires judgment and considers factors specific to the asset or liability.

At September 30, 2010, the fair value of the Company’s fuel swap agreements was a $0.3 million derivative asset. Fair value is determined using a level 2 valuation.

7. Derivative Instruments

The Company does not engage in the trading of derivative financial instruments except where the Company’s objective is to manage the variability of forecasted fuel price risk. In general, the Company enters into derivative transactions in limited situations based on management’s assessment of current market conditions and perceived risks.

Fuel Derivative Transactions. In the first quarter of 2010, the Company entered into fuel swap agreements, which have not been designated as hedging instruments. Gains and losses relating to these derivatives are recorded in fuel expense in the consolidated statements of operations. As of September 30, 2010, the Company has outstanding fuel swap agreements for 3.3 million gallons of diesel fuel purchases, from October 1, 2010 through December 31, 2010, at an average swap price of $2.17 per gallon. At September 30, 2010, the fair value of the fuel swaps agreements was a $0.3 million derivative asset, which was included in other current assets on the consolidated balance sheet. For the three and nine months ended September 30, 2010, the Company recognized a gain of $0.6 million and $0.2 million, respectively, in fuel expense related to fuel swaps agreements. The Company did not have any fuel derivative transactions for the three and nine months ended September 30, 2009.

8. Related Company Receivable

KCSM, as lender, and The Kansas City Southern Railway Company (“KCSR”), as borrower, entered into a Revolving Credit Agreement effective as of April 1, 2008 (the “Revolving Agreement”), pursuant to the terms of which KCSM may make one or more loans from time to time during the term of the Revolving Agreement. The Revolving Agreement is secured by certain assets of KCSR and terminates on December 31, 2013. As of September 30, 2010 and December 31, 2009, the amount outstanding was zero and $30.0 million, respectively, under the terms of the Revolving Agreement.

9. Capital Contribution

On June 3, 2010, KCSM shareholders approved a pro-rata increase of $95.0 million in the variable portion of the common stock of the Company (the “Capital Contribution”). KCSM used the proceeds from the Capital Contribution to redeem $70.0 million of the 12 1/2% Senior Notes and a portion of the 9 3/8% Senior Notes, plus accrued and unpaid interest and expenses. The shares representing the Company’s common stock have no par value and, therefore, the capital increase of the common stock in its variable portion, represented by Class II shares, did not result in the issuance of new shares.

10

Table of Contents

Kansas City Southern de México, S.A. de C.V. and Subsidiaries

Notes to Consolidated Financial Statements—(Continued)

(Amounts in millions of U.S. dollars)

10. Acquisition

On March 3, 2010, the Company acquired an intermodal facility in Mexico. The aggregate purchase price for the intermodal facility was $25.1 million, which was funded by existing cash. As a result of the final valuation completed in the second quarter 2010, the Company recorded goodwill of $2.6 million and identifiable intangible assets of $2.0 million. The acquisition is not material to the Company’s consolidated financial statements.

11. Long-Term Debt

On January 7, 2010, pursuant to an offer to purchase, KCSM commenced a cash tender offer for a portion of its 9 3/8% senior unsecured notes due May 1, 2012 (the “9 3/8% Senior Notes”). On January 22, 2010, the Company purchased $290.0 million of the tendered 9 3/8% Senior Notes in accordance with the terms and conditions of the tender offer set forth in the offer to purchase using the proceeds received from the issuance of $300.0 million of 8.0% senior unsecured notes due February 1, 2018 (the “8.0% Senior Notes”). Additionally, on February 1, 2010, the Company purchased $6.3 million of the 9 3/8% Senior Notes. KCSM recorded debt retirement costs of $14.9 million in the first quarter of 2010.

On January 22, 2010, KCSM issued $300.0 million principal amount of 8.0% Senior Notes, which bear interest semiannually at a fixed annual rate of 8.0%. The 8.0% Senior Notes were issued at a discount to par value, resulting in a $4.3 million discount and a yield to maturity of 8 1/4%. KCSM used the net proceeds from the issuance of the 8.0% Senior Notes and cash on hand to purchase $290.0 million in principal amount of the 9 3/8% Senior Notes tendered under an offer to purchase and pay all fees and expenses incurred in connection with the 8.0% Senior Notes offering and the 9 3/8% Senior Notes tender offer. The 8.0% Senior Notes are redeemable at KCSM’s option, in whole or in part, on and after February 1, 2014, at the following redemption prices (expressed as percentages of principal amount) plus any accrued and unpaid interest: 2014 —104.000%, 2015 —102.000% and 2016 —100.000%. In addition, KCSM may redeem up to 35% of the 8.0% Senior Notes any time prior to February 1, 2013 from the proceeds of the sale of capital stock in KCSM or its ultimate parent Kansas City Southern (“KCS”) and the notes are redeemable, in whole but not in part, at KCSM’s option at their principal amount in the event of certain changes in the Mexican withholding tax rate.

The 8.0% Senior Notes are denominated in dollars and are unsecured, unsubordinated obligations, rank pari passu in right of payment with KCSM’s existing and future unsecured, unsubordinated obligations, and are senior in right of payment to KCSM’s future subordinated indebtedness. In addition, the 8.0% Senior Notes include certain covenants which are customary for these types of debt instruments and borrowers with similar credit ratings. The 8.0% Senior Notes contain certain covenants that, among other things, prohibit or restrict KCSM from taking certain actions, including the ability to incur debt, pay dividends or make other distributions in respect of our stock, issue guarantees, enter into certain transactions with affiliates, make restricted payments, sell certain assets, create liens, engage in sale-leaseback transactions and engage in mergers, divestitures and consolidations. However, these limitations are subject to a number of important qualifications and exceptions.

On June 4, 2010, KCSM redeemed $100.0 million aggregate principal amount of its 9 3/8% Senior Notes. The redemption price was 102.344% of the principal amount of the 9 3/8% Senior Notes, plus accrued and unpaid interest. KCSM recorded debt retirement costs associated with this transaction of $3.1 million in the second quarter 2010. On June 4, 2010 KCSM also redeemed $70.0 million aggregate principal amount of its 12 1/2% senior notes due 2016 (the “12 1/2% Senior Notes”). The redemption price was 112.5% of the principal amount of the 12 1/2% Senior Notes, plus accrued and unpaid interest. KCSM recorded debt retirement costs associated with this transaction of $13.6 million in the second quarter 2010.

On August 30, 2010, KCSM entered into a secured credit agreement (the “2010 Credit Agreement”) with various lenders and other institutions as named in the 2010 Credit Agreement which provides KCSM with a three-year $100.0 million revolving credit facility consisting of (i) a revolving facility in an amount up to $100.0 million (the “Revolving Facility”) and, (ii) a letter of credit and a swing line facility (the “Swing Line Facility”) in an amount up to $10.0 million each, which constitutes usage under the Revolving Facility. At KCSM’s option, the outstanding principal balance of loans under the Revolving Facility will bear interest at either (i) the greater of (a) The Bank of Nova Scotia’s base rate, (b) federal funds rate plus 50 basis points or (c) one-month London Interbank Offered Rate (“LIBOR”) plus 100 basis points (the “Base Rate”) plus a spread depending on KCSM’s leverage ratio or (ii) LIBOR plus a spread depending on KCSM’s leverage ratio. The outstanding principal balance of loans under the Swing Line Facility will bear interest at the Base Rate plus a spread depending on KCSM’s leverage ratio.

11

Table of Contents

Kansas City Southern de México, S.A. de C.V. and Subsidiaries

Notes to Consolidated Financial Statements—(Continued)

(Amounts in millions of U.S. dollars)

The 2010 Credit Agreement is secured by the accounts receivable and certain locomotives of KCSM and certain KCSM subsidiaries and the pledge of equity interests of certain KCSM subsidiaries. In addition, KCSM and certain KCSM subsidiaries agreed to subordinate payment of intercompany debt and certain KCSM subsidiaries guaranteed repayment of the amounts due under the 2010 Credit Agreement. The 2010 Credit Agreement contains representations, warranties, and affirmative and negative covenants that are customary for credit agreements of this type, including financial covenants related to a leverage ratio and an interest coverage ratio as defined in the 2010 Credit Agreement.

As of September 30, 2010, KCSM had $5.0 million outstanding under the Revolving Facility. The Company intends to repay the outstanding balance under the Revolving Facility within the next twelve months and has classified this amount as a debt due within one year.

On September 30, 2010, KCSM used available cash to redeem the remaining outstanding 9 3/8% Senior Notes of $63.7 million, plus accrued and unpaid interest, at a price of 102.344% and recognized debt retirement costs of $1.9 million related to the call premium and the write-off of unamortized debt issuance costs.

12. Comprehensive Income

Other comprehensive income refers to revenues, expenses, gains and losses that under U.S. GAAP are included in comprehensive income, a component of stockholders’ equity within the consolidated balance sheets, rather than net income. Under existing accounting standards, other comprehensive income for KCSM reflects the cumulative translation adjustment on Ferrocarril y Terminal del Valle de México, S.A. de C.V. (“FTVM”).

KCSM’s total comprehensive income is as follows (in millions):

| Three Months Ended September 30, |

Nine Months Ended September 30, |

|||||||||||||||

| 2010 | 2009 | 2010 | 2009 | |||||||||||||

| (Unaudited) | ||||||||||||||||

| Net income (loss) |

$ | 19.0 | $ | 5.9 | $ | 45.2 | $ | (10.6 | ) | |||||||

| Other comprehensive income (loss): |

||||||||||||||||

| Cumulative translation adjustment — FTVM |

0.1 | (0.2 | ) | 0.4 | (0.7 | ) | ||||||||||

| Total comprehensive income (loss) |

$ | 19.1 | $ | 5.7 | $ | 45.6 | $ | (11.3 | ) | |||||||

13. Commitments and Contingencies

Concession duty. Under KCSM’s railroad concession from the Mexican government (the “Concession”), the Mexican government has the right to receive a payment from the Company equivalent to 0.5% of the gross revenue during the first 15 years of the Concession period and 1.25% during the remaining years of the Concession period. For the three and nine months ended September 30, 2010 and 2009, the concession duty expense amounted to $1.0 million and $3.1 million compared to $0.8 million and $2.3 million, respectively, which was recorded within operating expenses.

Litigation. The Company is a party to various legal proceedings and administrative actions, all of which, except as set forth below, are of an ordinary, routine nature and incidental to its operations. Included in these proceedings are various tort claims brought by current and former employees for job-related injuries and by third parties for injuries related to railroad operations. KCSM aggressively defends these matters and has established liability reserves, which management believes are adequate to cover expected costs. Although it is not possible to predict the outcome of any legal proceeding, in the opinion of management, other than those proceedings described in detail below, such proceedings and actions should not, individually, or in the aggregate, have a material adverse effect on the Company’s financial condition and liquidity. However, a material adverse outcome in one or more of these proceedings could have a material adverse impact on the operating results of a particular quarter or fiscal year.

Environmental Liabilities. The Company’s operations are subject to Mexican federal and state laws and regulations relating to the protection of the environment through the establishment of standards for water discharge, water supply, emissions, noise pollution, hazardous substances and transportation and handling of hazardous and solid waste. The Mexican government may bring administrative and criminal proceedings and impose economic sanctions against companies that violate environmental laws, and temporarily or even permanently close non-complying facilities.

12

Table of Contents

Kansas City Southern de México, S.A. de C.V. and Subsidiaries

Notes to Consolidated Financial Statements—(Continued)

(Amounts in millions of U.S. dollars)

The risk of incurring environmental liability is inherent in the railroad industry. As part of serving the petroleum and chemicals industry, the Company transports hazardous materials and has a professional team available to respond and handle environmental issues that might occur in the transport of such materials.

Settlement Agreement. On February 9, 2010, (i) KCSM and (ii) Ferrocarril Mexicano, S.A. de C.V. (“Ferromex”), Ferrosur, S.A. de C.V. (“Ferrosur”), Minera México, S.A. de C.V., Infraestructura y Transportes Ferroviarios, S.A. de C.V., Infraestructura y Transportes México, S.A. de C.V., Líneas Ferroviarias de México, S.A. de C.V., Grupo Ferroviario Mexicano, S.A. de C.V., and Grupo México, S.A.B. de C.V. (jointly, the “Ferromex Parties”) entered into a Settlement Agreement (the “Settlement Agreement”).

Pursuant to the Settlement Agreement, the parties agreed to completely, definitively and irrevocably terminate (i) certain disputes, procedures and controversies among KCSM and the Ferromex Parties, in connection with the merger between Ferromex and Ferrosur, including KCSM’s involvement in such procedures as an interested party; and (ii) the lawsuit filed against KCSM and the Mexican Government in connection with several disputes, procedures and controversies before judicial authorities with respect to the acquisition of the shares of Ferrocarril del Noreste, S.A. de C.V. (now KCSM) by Grupo Transportación Ferroviaria Mexicana, S.A. de C.V., in 1997 (the “Settlement Procedures”). The parties waived their rights to any future actions derived from or related to the Settlement Procedures. Further, the parties did not settle or agree to settle any disputes, controversies or procedures other than the Settlement Procedures.

Under the Settlement Agreement, Ferrosur agreed to grant KCSM certain trackage and switching rights within Veracruz, México, and switching rights in the Puebla-Tlaxcala zone. In a related agreement, the parties further agreed to amend the Ferrocarril y Terminal del Valle de México, S.A. de C.V. by-laws to, among other changes, grant certain veto and voting rights to KCSM at the shareholders’ and the board of directors’ levels.

The Settlement Agreement shall remain in effect until the term of the concession title of KCSM expires, unless the parties mutually agree to renew the Settlement Agreement beyond the expiration of KCSM’s concession title. The Settlement Agreement may be terminated earlier upon delivery by KCSM of a notice to the Ferromex Parties indicating any breach by the Ferromex Parties of any of their respective obligations under the Settlement Agreement. Notwithstanding, the settlement and termination of the Settlement Procedures shall not be subject to rescission or termination.

The Settlement Agreement may be terminated, at KCSM’s option, before its stipulated term if Ferromex is sold or if it transfers, directly or indirectly, its concession under its concession title. A change in control of KCSM or its affiliates, however, shall not be a cause for termination. Likewise, the Settlement Agreement will terminate three years after Ferromex and Ferrosur cease to be under the common control of one person or group of persons acting jointly or in agreement to adopt coordinated resolutions (“Common Control”). Notwithstanding, if for any reason Ferromex and Ferrosur are under Common Control within five years after the Settlement Agreement is terminated due to Ferromex and Ferrosur ceasing to be under Common Control, the Settlement Agreement would automatically be reinstated.

In November 2005, Ferromex acquired control of and merged with Ferrosur creating Mexico’s largest railway, though such merger has been previously rejected by the Comisión Federal de Competencia (Mexican Antitrust Commission) (“COFECO”). The Settlement Agreement provides that if COFECO does not authorize the merger of Ferromex and Ferrosur, the Settlement Agreement will be terminated twelve months after the relevant resolution of the Governmental Authority is issued or when the unwinding is effective, whichever is later. On May 12, 2010, the Administrative and Fiscal Federal Court annulled the decision of COFECO and approved the merger between Ferromex and Ferrosur. COFECO has the right to challenge the court decision once it is notified.

Trackage Rights Settlement Agreement with Ferromex. KCSM’s operations are subject to certain trackage rights, switching rights, and interline services with Ferromex. KCSM and Ferromex entered into a Trackage Rights, Switching and Interline Settlement Agreement, dated February 9, 2010 (the “Trackage Rights Agreement”). Pursuant to the Trackage Rights Agreement, the parties terminated, in a definitive and irrevocable manner, all actions and procedures regarding: (a) rates applicable to trackage rights, switching and interlinear services from January 1, 2009 onward, but not regarding the applicable rates before January 1, 2009 or the amounts owed by the parties to one another prior to the execution of the Trackage Rights Agreement; (b) the scope of certain trackage rights in Monterrey, Nuevo León, Guadalajara, Jalisco and Altamira, Tamaulipas, the Long Trackage Rights and Aguascalientes; and (c) court costs, as well as any other directly-related issue or dispute that arises from, are related in any manner directly or indirectly to the terms and conditions and/or scope of such mandatory trackage and/or switching rights or that arises by reason of the definition of trackage rights (the “Settlement Controversies”). The parties waived their rights to any future actions derived from or related to the

13

Table of Contents

Kansas City Southern de México, S.A. de C.V. and Subsidiaries

Notes to Consolidated Financial Statements—(Continued)

(Amounts in millions of U.S. dollars)

Settlement Controversies. Further, KCSM and Ferromex set the rates applicable for January 1, 2009 for each party for the use of the other party’s trackage. The retroactive application of these rates to January 1, 2009 did not have a material impact on the results of operations.

Excluded from the scope and purpose of the Trackage Rights Agreement are all procedures, disputes, lawsuits, remedies, appeals and disagreements that were not expressly identified in the Trackage Rights Agreement, including without limitation, the disputes, claims and lawsuits that relate to the determination of rates for mandatory trackage and/or switching rights and for interconnection and/or terminal services, accrued prior to January 1, 2009, as well as the disputes among the parties regarding amounts payable to one another for trackage rights, interline services and switching services, that are currently being disputed by both parties at the Federal Court of Fiscal and Administrative Justice. Furthermore, the parties did not settle or agree to settle any other trackage and switching rights not specifically mentioned in the Trackage Rights Agreement.

The Trackage Rights Agreement shall remain in effect until the term of the concession title of Ferromex or the concession title of KCSM expire, unless the parties mutually agree to renew the Trackage Rights Agreement beyond the expiration of either party’s concession title. The Trackage Rights Agreement may be terminated, at KCSM’s option, before its stipulated term if Ferromex is sold or if it transfers, directly or indirectly, its concession under its concession title. A change in control of KCSM or its affiliates, however, shall not be a cause for termination.

Certain Disputes with Ferromex. KCSM’s operations are subject to certain trackage rights, haulage rights, and interline services (the “Services”) with Ferromex. Other than the rates to be charged pursuant to the Trackage Rights Agreement, dated February 9, 2010, between KCSM and Ferromex, the rates payable for these Services have not been agreed upon by KCSM and Ferromex for the periods beginning in 1998 through December 31, 2008. If KCSM cannot reach an agreement with Ferromex for rates applicable for Services prior to January 1, 2009 which are not subject to the Trackage Rights Agreement, the Mexican Secretaría de Comunicaciones y Transportes (“Ministry of Communications and Transportation” or “SCT”) is entitled to set the rates in accordance with Mexican law and regulations. KCSM and Ferromex both initiated administrative proceedings seeking a determination by the SCT of the rates that KCSM and Ferromex should pay each other in connection with the Services. The SCT issued rulings in 2002 and 2008 setting the rates for the Services and both KCSM and Ferromex challenged these rulings.

In addition, KCSM is currently involved in judicial, civil and administrative proceedings and negotiations with Ferromex regarding the rates payable to each other for the Services for the periods prior to January 1, 2009. Although KCSM and Ferromex have challenged these matters based on different grounds and these cases continue to evolve, management believes the amounts recorded related to these matters are adequate and does not believe there will be a future material impact to the results of operations arising out of these disputes.

SCT Sanction Proceedings. In April 2006, the SCT initiated proceedings against KCSM, claiming that KCSM had failed to make certain minimum capital investments projected for 2004 and 2005 under its five-year business plan filed with the SCT prior to its April 2005 acquisition by Kansas City Southern (“ KCS”) (collectively, the “Capital Investment Proceedings”). KCSM believes it made capital expenditures exceeding the required amounts. KCSM responded to the SCT by providing evidence in support of its investments and explaining why it believes sanctions are not appropriate. In May 2007, KCSM was served with an SCT resolution regarding the Capital Investment Proceeding for 2004, in which the SCT resolved to impose no sanction. In June 2007, KCSM was served with an SCT resolution regarding the Capital Investment Proceeding for 2005, in which the SCT determined that KCSM had indeed failed to make the minimum capital investments required for such year, and imposed a minimum fine. KCSM has filed an action in the Mexican Administrative and Fiscal Federal Court challenging this ruling. KCSM will have the right to challenge any adverse ruling.

In May 2008, the SCT initiated a proceeding against KCSM, at the request of a Mexican subsidiary of a large U.S. Auto Manufacturer (the “Auto Manufacturer”), alleging that KCSM impermissibly bundled international rail services and engaged in discriminatory pricing practices with respect to rail services provided by KCSM to the Auto Manufacturer. In March 2009, the SCT issued a decision determining that KCSM had engaged in the activities alleged, but imposed no sanction since this was the first time KCSM had engaged in such activities. On May 6, 2009, KCSM challenged the SCT’s decision and the appeal is currently pending in the Administrative and Fiscal Federal Court.

On July 23, 2008, the SCT delivered notice to KCSM of new proceedings against KCSM, claiming, among other things, that KCSM refused to grant Ferromex access to certain trackage over which Ferromex alleges it has trackage rights on six different occasions and, thus denied Ferromex the ability to provide service to the Auto Manufacturer at this location. On August 13, 2008,

14

Table of Contents

Kansas City Southern de México, S.A. de C.V. and Subsidiaries

Notes to Consolidated Financial Statements—(Continued)

(Amounts in millions of U.S. dollars)

KCSM filed a response to the SCT. On July 15, 2010, the SCT resolved to consolidate these six sanction proceedings into a single proceeding, determining that the actions that motivated the underlying claims constitute a single occasion. On August 19, 2010 Ferromex filed an appeal which KCSM considers to be without merit. Management believes that even if KCSM were to be found liable, a single sanction would be imposed and could be challenged in the Administrative and Fiscal Federal Court. A single sanction makes it more likely that any unfavorable resolution will not have a material impact on KCSM’s results of operations.

KCSM believes it has defenses to the imposition of sanctions for the foregoing proceedings and intends to vigorously contest these allegations. KCSM does not believe that these SCT proceedings will have a material adverse effect on KCSM’s results of operations or financial condition. However, if KCSM is ultimately sanctioned by the SCT for “generic” sanctions on five occasions over the term of the Concession, KCSM could be subject to possible future SCT action seeking revocation of the Concession.

Agreement with the Auto Manufacturer. KCSM has been involved in several disputes related to providing services to the Auto Manufacturer. In October 2010, KCSM and the Auto Manufacturer reached an agreement to settle all disputes related to services provided prior to May 28, 2010 by KCSM to the Auto Manufacturer, other than matters pending before the SCT involving KCSM and the Auto Manufacturer which are not subject to this agreement. This agreement did not have a significant impact on KCSM’s results of operations.

Credit Risk. The Company continually monitors risks related to economic changes and certain customer receivable concentrations. Significant changes in customer concentration or payment terms, deterioration of customer credit-worthiness or further weakening in economic trends could have a significant impact on the collectability of KCSM’s receivables and operating results. If the financial condition of KCSM’s customers were to deteriorate, resulting in an impairment of their ability to make payments, additional allowances may be required. The Company has recorded reserves for uncollectability based on its best estimate at September 30, 2010.

Income Tax. Tax returns filed in Mexico from 2003 through the current year remain open to examination by the taxing authority in Mexico. The 2003 through 2005 Mexico tax returns are currently under examination. The Company received an audit assessment for the year ended December 31, 2003, from Servicio de Administracion Tributaria (“SAT”), the Mexican equivalent of the IRS. The Company filed its response to this assessment on March 8, 2010. On October 15, 2010, the SAT issued a resolution which settled the most significant matters included in the 2003 audit assessment, with no resulting impact to the Company’s financial results.

The Company believes that an adequate provision has been made for any adjustment (tax and interest) that will be due for all open years. However, an unexpected adverse resolution could have a material effect on the results of operations in a particular quarter or fiscal year.

14. Subsequent Events

On October 1, 2010, KCSM entered into an amended loan agreement (the “Amendment Agreement”) with a wholly-owned subsidiary of KCS. Pursuant to the terms of the Amendment Agreement the principal amount of the loan was increased from $21.6 million to $39.0 million and the annual interest rate was decreased from 7.5% to 4.25%.

On October 1, 2010, KCSM prepaid The Kansas City Southern Railway (“KCSR”) $17.5 million for shared services which will be provided by KCSR during 2011.

15

Table of Contents

Report of Independent Registered Public Accounting Firm

The Board of Directors and Stockholders

Kansas City Southern de México, S.A. de C.V.:

We have reviewed the accompanying consolidated balance sheet of Kansas City Southern de México, S.A. de C.V. and subsidiaries (the Company) as of September 30, 2010, and the related consolidated statements of operations for the three-month and nine-month periods ended September 30, 2010 and 2009, and the related consolidated statements of cash flows for nine-month periods ended September 30, 2010 and 2009. These consolidated financial statements are the responsibility of the Company’s management.

We conducted our reviews in accordance with the standards of the Public Company Accounting Oversight Board (United States). A review of interim financial information consists principally of applying analytical procedures and making inquiries of persons responsible for financial and accounting matters. It is substantially less in scope than an audit conducted in accordance with the standards of the Public Company Accounting Oversight Board (United States), the objective of which is the expression of an opinion regarding the consolidated financial statements taken as a whole. Accordingly, we do not express such an opinion.

Based on our review, we are not aware of any material modifications that should be made to the consolidated financial statements referred to above for them to be in conformity with U.S. generally accepted accounting principles.

We have previously audited, in accordance with the standards of the Public Company Accounting Oversight Board (United States), the consolidated balance sheet of the Company as of December 31, 2009, and the related consolidated statements of income, changes in stockholders’ equity and comprehensive income, and cash flows for the year then ended (not presented herein); and in our report dated February 11, 2010, except for Note 13-Change in accounting policy, which is as of September 13, 2010, we expressed an unqualified opinion on those consolidated financial statements. In our opinion, the information set forth in the accompanying consolidated balance sheet as of December 31, 2009 is fairly stated, in all material respects, in relation to the consolidated balance sheet from which it has been derived.

KPMG LLP

Kansas City, Missouri

October 26, 2010

16

Table of Contents

| Item 2. | Management’s Discussion and Analysis of Financial Condition and Results of Operations. |

The discussion below, as well as other portions of this Form 10-Q, contain forward-looking statements that are not based upon historical information. Readers can identify these forward-looking statements by the use of such verbs as “expects,” “anticipates,” “believes” or similar verbs or conjugations of such verbs. Such forward-looking statements are based upon information currently available to management and management’s perception thereof as of the date of this Form 10-Q. However, such statements are dependent on and, therefore, can be influenced by, a number of external variables over which management has little or no control, including: domestic and international economic conditions; interest rates; the business environment in industries that produce and consume rail freight; competition and consolidation within the transportation industry; fluctuation in prices or availability of key materials, in particular diesel fuel; labor difficulties, including strikes and work stoppages; credit risk of customers and counterparties and their failure to meet their financial obligation; the outcome of claims and litigation; legislative and regulatory developments; political and economic conditions in Mexico and the level of trade between the United States and Mexico; changes in securities and capital markets; disruptions to the Company’s technology infrastructure, including its computer systems; natural events such as severe weather, hurricanes and floods; acts of terrorism or risk of terrorist activities; and war or risk of war. For more discussion about each risk factor, see Part I, Item 1A – Risk Factors of the Company’s Annual Report on Form 10-K for the year ended December 31, 2009, which is on file with the U.S. Securities and Exchange Commission (File No. 333-08322) and which “Risk Factors” section is hereby incorporated by reference and any updates contained herein. Readers are strongly encouraged to consider these factors when evaluating forward-looking statements. Forward-looking statements should not be read as a guarantee of future performance or results and will not necessarily be accurate indications of the timing when, or by which, such performance or results will be achieved. As a result, actual outcomes or results could materially differ from those indicated in forward-looking statements. Forward-looking statements contained in this Form 10-Q will not be updated.

The following discussion, which is intended to clarify and focus on Kansas City Southern de México, S. A. de C.V.’s (“KCSM” or the “Company”) results of operations, certain changes in its financial position, liquidity, capital structure and business developments for the periods covered by the consolidated financial statements included under Item 1 of this Form 10-Q, is abbreviated pursuant to General Instruction H(2)(a) of Form 10-Q. This discussion should be read in conjunction with those consolidated financial statements and the related notes, and is qualified by reference to them.

Critical Accounting Policies and Estimates

The Company’s discussion and analysis of its financial position and results of operations is based upon its consolidated financial statements. The preparation of these consolidated financial statements requires estimation and judgment that affect the reported amounts of revenue, expenses, assets, and liabilities. The Company bases its estimates on historical experience and on various other factors that are believed to be reasonable under the circumstances, the results of which form the basis for making judgments about the accounting for assets and liabilities that are not readily apparent from other sources. If the estimates differ materially from actual results, the impact on the consolidated financial statements may be material. The Company’s significant accounting policies are disclosed in the 2009 Annual Report on Form 10-K.

In the first quarter of 2010, the Company elected to change its accounting policy for rail grinding costs from a capitalization method to a direct expense method. Refer to Note 1, Accounting Policies, Interim Financial Statements and Basis of Presentation, for further details of this change in accounting policy. Comparative financial information for all prior periods have been adjusted to reflect the retroactive application of this change in accounting principle.

Third Quarter Analysis

The Company reported quarterly earnings of $19.0 million for the three months ended September 30, 2010, compared to quarterly earnings of $5.9 million for the same period in 2009. This earnings increase reflects a 17% increase in revenues during the three months ended September 30, 2010 as compared to the same period in 2009, driven primarily by positive pricing impacts in certain commodity groups, the overall increase in carload/unit volumes resulting from the relative improvement in the economy and increased fuel surcharge.

Operating expenses increased 8% compared to the same period in 2009, primarily due to the overall increase in carload/unit volumes, higher fuel prices and purchased services, partially offset by a decrease in equipment costs. In addition, the Company was able to leverage its cost control program initiated in 2009 as operating expenses as a percentage of revenues declined to 72.0% for the three months ended September 30, 2010 as compared to 77.4% for the same period in 2009.

Hurricane Alex made landfall on June 30, 2010, causing widespread damage and flooding in central and northeastern Mexico. The hurricane resulted in extensive damage to KCSM’s track and bridge infrastructures, and also caused multiple track-related incidents and significantly disrupted the Company’s rail service. Kansas City Southern (“KCS”), KCSM’s controlling stockholder, and KCSM maintain a comprehensive insurance program intended to cover such events. The property and casualty insurance program

17

Table of Contents

covers loss or damage to Company property and third party property over which the Company has custody and control and covers losses associated with business interruption. This program has combined coverage for both property damage and business interruption and has a self-insured retention amount of $10.0 million for flood related losses. In addition, KCS and KCSM also maintain a general liability insurance program with a self-insured retention of $1.0 million in Mexico covering claims from third parties. KCSM has filed an initial claim under the property and casualty program for $71.5 million. This claim includes estimates of both incurred and expected losses in the U.S. and Mexico. The claim filing will be updated and adjusted as additional information becomes available. KCSM expects to file its initial claim under the general liability program in the fourth quarter of 2010. The policy limits are in excess of the hurricane losses incurred. The Company expects to recover the amount of the adjusted claim, less related self-insured retentions of $11.0 million. As of the date of this filing, no payments have been received from the insurance programs. The Company expects to receive its first insurance payment during the fourth quarter of 2010, and to reach final settlement during 2011.

Hurricane Alex affected revenues for certain commodity groups as customers were required to use alternate carriers or modes of transportation until rail service was restored. Based on data contained in the initial insurance claim, which will be updated and adjusted, the Company currently estimates the related effect on its third quarter of 2010 financial results includes $25.0 million of lost revenue, less related avoided costs.

For the third quarter of 2010, the Company has recognized probable insurance recoveries which offset the $31.0 million of incurred losses related to property damage and incremental expenses. The Company expects to incur additional costs in the fourth quarter 2010 related to ongoing property repair, which are also expected to be offset by probable insurance recoveries. Remaining insurance recoveries will be recognized upon final settlement of the claim or when nonrefundable cash payments are received.

The Company estimates that if the effects of Hurricane Alex were excluded from its third quarter of 2010 financial results, operating expenses as a percentage of revenues would have been approximately 400 basis points lower.

Results of Operations

The following summarizes the consolidated statement of operations (in millions).

| Three Months Ended September 30, |

Change | |||||||||||

| 2010 | 2009 | Dollars | ||||||||||

| Revenues |

$ | 184.8 | $ | 158.3 | $ | 26.5 | ||||||

| Operating expenses |

133.0 | 122.6 | 10.4 | |||||||||

| Operating income |

51.8 | 35.7 | 16.1 | |||||||||

| Equity in net earnings of unconsolidated affiliates |

1.1 | 1.6 | (0.5 | ) | ||||||||

| Interest expense |

(22.4 | ) | (28.1 | ) | 5.7 | |||||||

| Debt retirement costs |

(1.9 | ) | — | (1.9 | ) | |||||||

| Foreign exchange gain (loss) |

2.1 | (1.5 | ) | 3.6 | ||||||||

| Other income, net |

0.4 | 0.8 | (0.4 | ) | ||||||||

| Income before income taxes |

31.1 | 8.5 | 22.6 | |||||||||

| Income tax expense |

12.1 | 2.6 | 9.5 | |||||||||

| Net income |

$ | 19.0 | $ | 5.9 | $ | 13.1 | ||||||

| Nine

Months Ended September 30, |

Change | |||||||||||

| 2010 | 2009 | Dollars | ||||||||||

| Revenues |

$ | 582.4 | $ | 438.5 | $ | 143.9 | ||||||

| Operating expenses |

416.0 | 374.6 | 41.4 | |||||||||

| Operating income |

166.4 | 63.9 | 102.5 | |||||||||

| Equity in net earnings of unconsolidated affiliates |

5.5 | 1.2 | 4.3 | |||||||||

| Interest expense |

(75.6 | ) | (81.2 | ) | 5.6 | |||||||

| Debt retirement costs |

(33.5 | ) | (0.6 | ) | (32.9 | ) | ||||||

| Foreign exchange gain (loss) |

3.4 | (0.6 | ) | 4.0 | ||||||||

| Other income, net |

1.9 | 2.0 | (0.1 | ) | ||||||||

| Income (loss) before income taxes |

68.1 | (15.3 | ) | 83.4 | ||||||||

| Income tax expense (benefit) |

22.9 | (4.7 | ) | 27.6 | ||||||||

| Net income (loss) |

$ | 45.2 | $ | (10.6 | ) | $ | 55.8 | |||||

18

Table of Contents

Revenues

The following table summarizes revenues (in millions), carload/unit statistics (in thousands) and revenue per carload/unit:

| Revenues | Carloads and Units | Revenue per Carload/Unit | ||||||||||||||||||||||||||||||||||

| Three Months Ended September 30, |

Three Months Ended September 30, |

Three Months Ended September 30, |

||||||||||||||||||||||||||||||||||

| 2010 | 2009 | % Change | 2010 | 2009 | % Change | 2010 | 2009 | % Change | ||||||||||||||||||||||||||||

| Chemical and petroleum |

$ | 39.6 | $ | 36.8 | 8 | % | 22.9 | 23.6 | (3 | )% | $ | 1,729.3 | $ | 1,559.3 | 11 | % | ||||||||||||||||||||

| Industrial and consumer products |

42.1 | 35.7 | 18 | % | 34.9 | 31.5 | 11 | % | 1,206.3 | 1,133.3 | 6 | % | ||||||||||||||||||||||||

| Agriculture and minerals |

46.9 | 44.7 | 5 | % | 27.9 | 28.8 | (3 | )% | 1,681.0 | 1,552.1 | 8 | % | ||||||||||||||||||||||||

| Total general commodities |

128.6 | 117.2 | 10 | % | 85.7 | 83.9 | 2 | % | 1,500.6 | 1,396.9 | 7 | % | ||||||||||||||||||||||||

| Coal |

3.7 | 3.2 | 16 | % | 4.4 | 4.0 | 10 | % | 840.9 | 800.0 | 5 | % | ||||||||||||||||||||||||

| Intermodal |

27.8 | 21.4 | 30 | % | 79.9 | 62.1 | 29 | % | 347.9 | 344.6 | 1 | % | ||||||||||||||||||||||||

| Automotive |

21.3 | 13.6 | 57 | % | 14.9 | 12.9 | 16 | % | 1,429.5 | 1,054.3 | 36 | % | ||||||||||||||||||||||||

| Subtotal |

181.4 | 155.4 | 17 | % | 184.9 | 162.9 | 14 | % | $ | 981.1 | $ | 954.0 | 3 | % | ||||||||||||||||||||||

| Other revenue |

3.4 | 2.9 | 17 | % | ||||||||||||||||||||||||||||||||

| Total revenues (i) |

$ | 184.8 | $ | 158.3 | 17 | % | ||||||||||||||||||||||||||||||

| (i) Included in revenues: |

||||||||||||||||||||||||||||||||||||

| Fuel surcharge |

$ | 19.5 | $ | 13.4 | ||||||||||||||||||||||||||||||||

| Revenues | Carloads and Units | Revenue per Carload/Unit | ||||||||||||||||||||||||||||||||||

| Nine Months Ended September 30, |

Nine Months Ended September 30, |

Nine Months Ended September 30, |

||||||||||||||||||||||||||||||||||

| 2010 | 2009 | % Change | 2010 | 2009 | % Change | 2010 | 2009 | % Change | ||||||||||||||||||||||||||||

| Chemical and petroleum |

$ | 125.6 | $ | 101.5 | 24 | % | 73.7 | 65.6 | 12 | % | $ | 1,704.2 | $ | 1,547.3 | 10 | % | ||||||||||||||||||||

| Industrial and consumer products |

136.1 | 111.0 | 23 | % | 108.4 | 99.4 | 9 | % | 1,255.5 | 1,116.7 | 12 | % | ||||||||||||||||||||||||

| Agriculture and minerals |

150.9 | 120.5 | 25 | % | 91.7 | 85.8 | 7 | % | 1,645.6 | 1,404.4 | 17 | % | ||||||||||||||||||||||||

| Total general commodities |

412.6 | 333.0 | 24 | % | 273.8 | 250.8 | 9 | % | 1,506.9 | 1,327.8 | 13 | % | ||||||||||||||||||||||||

| Coal |

10.5 | 10.5 | 0 | % | 13.5 | 13.0 | 4 | % | 777.8 | 807.7 | (4 | )% | ||||||||||||||||||||||||

| Intermodal |

82.1 | 53.4 | 54 | % | 230.9 | 155.8 | 48 | % | 355.6 | 342.7 | 4 | % | ||||||||||||||||||||||||

| Automotive |

65.2 | 31.1 | 110 | % | 47.5 | 30.1 | 58 | % | 1,372.6 | 1,033.2 | 33 | % | ||||||||||||||||||||||||

| Subtotal |

570.4 | 428.0 | 33 | % | 565.7 | 449.7 | 26 | % | $ | 1,008.3 | $ | 951.7 | 6 | % | ||||||||||||||||||||||

| Other revenue |

12.0 | 10.5 | 14 | % | ||||||||||||||||||||||||||||||||

| Total revenues (i) |

$ | 582.4 | $ | 438.5 | 33 | % | ||||||||||||||||||||||||||||||

| (i) Included in revenues: |

||||||||||||||||||||||||||||||||||||

| Fuel surcharge |

$ | 58.6 | $ | 33.8 | ||||||||||||||||||||||||||||||||

Freight revenues include both revenue for transportation services and fuel surcharges. For the three and nine months ended September 30, 2010, revenues increased $26.5 million and $143.9 million compared to the same periods in 2009, primarily due to positive pricing impacts, the overall increase in carload/unit volumes resulting from the relative improvement in the economy and increased fuel surcharge. For the three months ended September 30, 2010, revenues for certain commodity groups were affected by Hurricane Alex as customers were required to use alternate carriers or modes of transportation until the services were restored. Revenue per carload/unit increased by 3% and 6% for the three and nine months ended September 30, 2010, compared to the same periods in 2009, reflecting favorable commodity mix in addition to the factors discussed above. The effect of fluctuations in the value of the U.S. dollar against the value of the Mexican peso for revenues denominated in Mexican pesos was not significant for either period.

19

Table of Contents

KCSM’s fuel surcharge is a mechanism to adjust revenue based upon changing fuel prices. Fuel surcharges are calculated differently depending on the type of commodity transported. For most commodities, fuel surcharge is calculated using a fuel price from a prior time period that can be as much as 60 days earlier. In a period of volatile fuel prices or changing customer business mix, changes in fuel expense and fuel surcharge may differ.

The following discussion provides an analysis of revenues by commodity group:

| Revenues by Commodity Group for the three months ended September 30, 2010 | ||

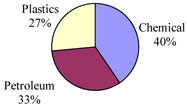

| Chemical and petroleum. Revenues increased $2.8 million and $24.1 million for the three and nine months ended September 30, 2010, compared to the same periods in 2009, primarily due to increases in price and volume. Volume increased for the nine months ended September 30, 2010 as a result of an increase in plastic product shipments primarily due to higher demand. Additionally, petroleum revenues increased due to a Mexican government initiated oil export program, which resulted in record high levels of oil production and storage. Chemical and petroleum volumes were significantly affected by Hurricane Alex in the third quarter of 2010. |

| |

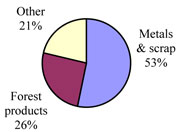

| Industrial and consumer products. Revenues increased $6.4 million and $25.1 million for the three and nine months ended September 30, 2010, compared to the same periods in 2009, primarily due to increases in volume, fuel surcharge, and pricing. Metals and scrap business growth was primarily due to growing demand for slab and steel coil. Industrial and consumer product volumes were significantly affected by Hurricane Alex in the third quarter of 2010. |

| |

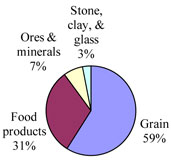

| Agriculture and minerals. Revenues increased $2.2 million and $30.4 million for the three and nine months ended September 30, 2010, compared to the same periods in 2009, due to increases in price and volume. Volume increased for the nine months ended September 30, 2010 as a result of increased grain shipments as a portion of the traffic lost to vessel in 2009 was converted back to rail in 2010. Food products showed continued strength primarily due to increased distiller dried grain shipments from the U.S. Food products and grain volumes were significantly affected by Hurricane Alex in the third quarter of 2010. |

| |

Coal. Revenue increased $0.5 million and was flat for the three and nine months ended September 30, 2010, compared to the same periods in 2009, as increases in volume, fuel surcharge and fluctuations in the value of the U.S. dollar against the value of the Mexican Peso were offset by decreases in pricing and shorter average length of haul.

Intermodal. Revenues increased $6.4 million and $28.7 million for the three and nine months ended September 30, 2010, compared to the same periods in 2009, primarily due to an increase in volume. Growth was driven by increased automotive parts traffic, conversion of cross border truck traffic to rail, trans-Pacific container volume, the emergence of cross border international cargo and improvement in the economy. Intermodal volumes were significantly affected by Hurricane Alex in the third quarter of 2010.

Automotive. Revenues increased $7.7 million and $34.1 million for the three and nine months ended September 30, 2010, compared to the same periods in 2009, primarily due to increases in volume and price. The volume increase was driven by strong year over year growth in North American automobile sales, a shift in production from the U.S. to Mexico and new cross border vehicle routings. Automotive volumes were significantly affected by Hurricane Alex in the third quarter of 2010.

20

Table of Contents

Operating expenses

Operating expenses, as shown below (in millions), increased $10.4 million and $41.4 million for the three and nine months ended September 30, 2010, when compared to the same periods in 2009, primarily due to increased carload/unit volumes and the effect of fluctuations in the value of the U.S. dollar against the value of the Mexican peso for operating expenses denominated in Mexican pesos.

| Three Months Ended September 30, |

Change | |||||||||||||||

| 2010 | 2009 | Dollars | Percent | |||||||||||||

| Compensation and benefits |

$ | 18.3 | $ | 19.8 | $ | (1.5 | ) | (8 | )% | |||||||

| Purchased services |

32.0 | 22.3 | 9.7 | 43 | % | |||||||||||

| Fuel |

26.9 | 22.6 | 4.3 | 19 | % | |||||||||||

| Equipment costs |

18.7 | 22.4 | (3.7 | ) | (17 | )% | ||||||||||

| Depreciation and amortization |

24.4 | 25.5 | (1.1 | ) | (4 | )% | ||||||||||

| Casualties and insurance |

2.0 | 1.4 | 0.6 | 43 | % | |||||||||||

| Materials and other |

10.7 | 8.6 | 2.1 | 24 | % | |||||||||||

| Total operating expenses |

$ | 133.0 | $ | 122.6 | $ | 10.4 | 8 | % | ||||||||

| Nine Months Ended September 30, |

Change | |||||||||||||||

| 2010 | 2009 | Dollars | Percent | |||||||||||||

| Compensation and benefits |

$ | 66.0 | $ | 53.9 | $ | 12.1 | 22 | % | ||||||||

| Purchased services |

95.7 | 80.4 | 15.3 | 19 | % | |||||||||||

| Fuel |

85.7 | 61.0 | 24.7 | 40 | % | |||||||||||

| Equipment costs |

57.1 | 64.5 | (7.4 | ) | (11 | )% | ||||||||||

| Depreciation and amortization |

72.7 | 81.3 | (8.6 | ) | (11 | )% | ||||||||||

| Casualties and insurance |

6.0 | 5.6 | 0.4 | 7 | % | |||||||||||

| Materials and other |

32.8 | 27.9 | 4.9 | 18 | % | |||||||||||

| Total operating expenses |

$ | 416.0 | $ | 374.6 | $ | 41.4 | 11 | % | ||||||||

Compensation and benefits. Compensation and benefits decreased $1.5 million for the three months ended September 30, 2010, compared to the same period in 2009, primarily due to a decrease of $6.2 million in post-employment benefit obligations as a result of the completion of negotiations with the labor union in the third quarter of 2010. This decrease was partially offset by an increase in statutory profit sharing and annual incentive compensation expense and annual wage and salary rate increases. For the nine months ended September 30, 2010, compensation and benefits increased $12.1 million compared to the same period in 2009, primarily due to an increase in statutory profit sharing, annual incentive compensation expense and annual wage and salary rate increases. In addition, compensation and benefits increased due to fluctuations in the value of the U.S. dollar against the value of the Mexican peso. These increases were partially offset by the decrease in post-employment benefit obligations as a result of the completion of negotiations with the labor union in the third quarter of 2010.

Purchased services. Purchased services expense increased $9.7 million and $15.3 million for the three and nine months ended September 30, 2010, compared to the same periods in 2009. The Company recognized a deferred credit of $6.1 million related to the partial cancellation of a maintenance contract in third quarter of 2009. In addition, purchased services increased due to increases in corporate expenses, volume-sensitive costs including security, track and terminal services, and joint facilities. These increases were partially offset by lower locomotive maintenance as a result of a newer locomotive fleet and having fewer locomotives covered by maintenance agreements.