Attached files

Table of Contents

As filed with the U.S. Securities and Exchange Commission on September 20, 2010

Registration No. 333-169356

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 1 to

Form S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Kraton Performance Polymers, Inc.

(Exact name of Registrant as specified in its charter)

| Delaware | 2821 | 20-0411521 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

15710 John F. Kennedy Blvd.

Suite 300

Houston, TX 77032

Telephone: (218) 504-4700

(Address including zip code, telephone number, including area code, of Registrant’s Principal Executive Offices)

Stephen W. Duffy, Esq.

General Counsel

Kraton Performance Polymers, Inc.

15710 John F. Kennedy Blvd.

Suite 300

Houston, Texas 77032

Telephone: (281) 504-4700

Telecopy: (281) 504-4743

(Name, address including zip code, telephone number, including area code, of agent for service)

Copies To:

| William F. Gorin, Esq. Duane McLaughlin, Esq. Cleary Gottlieb Steen & Hamilton LLP One Liberty Plaza New York, New York 10006 Telephone: (212) 225-2000 Telecopy: (212) 225-3999 |

Peter Labonski, Esq. Keith Halverstam, Esq. Latham & Watkins LLP 885 Third Avenue New York, New York 10022 Telephone: (212) 906-1200 Telecopy: (212) 751-4864 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date hereof.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act, check the following box. ¨

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act (Check one):

| Large accelerated filer ¨ |

Accelerated filer ¨ | |

| Non-accelerated filer x |

Smaller reporting company ¨ | |

| (Do not check if a smaller reporting company) | ||

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

CALCULATION OF REGISTRATION FEE

| Title of each class of securities to be registered (1) |

Amount to be registered (1) |

Proposed maximum offering price per share (2) |

Proposed maximum aggregate offering price (1)(2) |

Amount of registration fees (3) | ||||

| Common stock, $0.01 par value per share |

9,200,000 | $27.49 | $252,908,000 | $18,032.34 | ||||

| (1) | Includes 1,200,000 shares that the underwriters have an option to purchase from the selling stockholders to cover over-allotments, if any. |

| (2) | Estimated solely for the purpose of calculating the registration fee, based on the average of the high and low prices of the registrant’s common stock on September 10, 2010, pursuant to Rule 457(c) promulgated under the Securities Act of 1933, as amended. |

| (3) | Previously paid. |

Table of Contents

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED SEPTEMBER 20, 2010

Prospectus

8,000,000 Shares

Kraton Performance Polymers, Inc.

Common Stock

The selling stockholders identified in this prospectus are offering all of the shares offered hereby and will receive all of the proceeds from this offering. We will not receive any proceeds from this offering. See “Principal and Selling Stockholders.”

Our common stock is listed on the New York Stock Exchange under the symbol “KRA.” On September 17, 2010 the closing price of our common stock as reported on the New York Stock Exchange was $29.72.

The selling stockholders have granted the underwriters the right to purchase up to 1,200,000 shares of common stock at the offering price less the underwriting discount if the underwriters sell more than 8,000,000 shares of common stock in this offering. The underwriters can exercise this right at any time and from time to time, in whole or in part, within 30 days after this offering.

Investing in our common stock involves a high degree of risk. See “Risk Factors” beginning on page 17.

| Price to Public |

Underwriting Discounts and Commissions |

Proceeds, Before Expenses, to the Selling Stockholders | |||||||

| Per Share |

$ | $ | $ | ||||||

| Total |

$ | $ | $ | ||||||

Delivery of the shares of common stock will be made on or about , 2010.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Credit Suisse | BofA Merrill Lynch | Morgan Stanley | Oppenheimer & Co. |

| KeyBanc Capital Markets |

UBS Investment Bank | |

The date of this prospectus is , 2010.

Table of Contents

We are responsible for the information contained and incorporated by reference in this prospectus. We have not authorized anyone to give you any other information, and we take no responsibility for any other information that others may give you. This document may only be used where it is legal to sell these securities. The information in this document may only be accurate on the date of this document.

Information contained in our web site does not constitute part of this prospectus.

The Kraton name, our logo and other trademarks mentioned in this prospectus are the property of their respective owners.

We obtained the industry and market data used throughout this prospectus from our own internal estimates and research as well as from industry and general publications and from research, surveys and studies conducted by third parties.

| Page | ||

| 1 | ||

| 17 | ||

| 32 | ||

| 34 | ||

| 35 | ||

| 36 | ||

| 37 | ||

| 38 | ||

| Management’s Discussion and Analysis of Financial Condition and Results of Operations |

40 | |

| 64 | ||

| 69 | ||

| 89 | ||

| 98 | ||

| 122 | ||

| 125 | ||

| 128 | ||

| 131 | ||

| 135 | ||

| Certain United States Federal Income Tax Considerations for Non-U.S. Holders |

137 | |

| 140 | ||

| 148 | ||

| 148 | ||

| 148 | ||

| 149 | ||

| F-1 |

Table of Contents

The following summary includes basic information about our company and this offering. It may not contain all of the information that is important to you. For a more comprehensive understanding of our company and this offering, you should read this entire prospectus.

In this prospectus, unless we indicate otherwise or the context requires:

| • | “Kraton Performance Polymers,” “our company,” “we,” “our,” “ours,” and “us” refer to Kraton Performance Polymers, Inc. and its consolidated subsidiaries; |

| • | “Kraton” refers to Kraton Polymers LLC; and |

| • | the “SBC industry” refers to the elastomeric styrenic block copolymers industry and does not include the high styrene or rigid SBC business. |

Our Company

General

We believe we are the world’s leading producer of styrenic block copolymers (SBCs) as measured by 2009 sales revenue. We market our products under the widely recognized Kraton® brand. SBCs are highly-engineered synthetic elastomers that we invented and commercialized almost 50 years ago, which enhance the performance of numerous end use products, imparting greater flexibility, resilience, strength, durability and processability. We focus on the end use markets we believe offer the highest growth potential and greatest opportunity to differentiate our products from competing products. Within these end use markets, we believe that we provide our customers with a broad portfolio of highly-engineered and value-enhancing polymers that are critical to the performance of our customers’ products. We seek to maximize the value of our product portfolio by introducing innovations that command premium pricing and by consistently upgrading from lower margin products. As the industry leader, we believe we maintain significant competitive advantages, including an almost 50-year proven track record of innovation; world-class technical expertise; customer, geographical and end use market diversity; and industry-leading customer service capabilities. These advantages are supported by a global infrastructure and a long history of successful capital investments and operational excellence.

Our SBC products are found in many everyday applications, including disposable baby diapers, the rubberized grips of toothbrushes, razor blades, power tools and in asphalt formulations used to pave roads. We believe that there are many untapped uses for our products, and we will continue to develop new applications for SBCs. We also develop, manufacture and market niche, non-SBC products that we believe have high growth potential, such as isoprene rubber latex, or IRL. IRL is a highly-engineered, reliable synthetic substitute for natural rubber latex. We believe the versatility of IRL offers significant opportunities for new, high-margin applications. Our IRL products, which are used in applications such as surgical gloves and condoms, have not been found to contain the proteins present in natural latex and are, therefore, not known to cause allergies. We believe we produce the highest purity IRL globally and that we are the only significant third-party supplier of the product. Our IRL business has grown at a compound annual growth rate of 28.8%, based on revenues, from 2007 to the end of 2009.

We currently offer approximately 800 products to more than 700 customers in over 60 countries worldwide, and we manufacture our polymers at five manufacturing facilities on four continents, including our flagship plant in Belpre, Ohio, the most diversified SBC plant in the world. Our facility in Japan is operated by an unconsolidated manufacturing joint venture. Our products are typically developed using our proprietary, and in many cases patent-protected, technology and require significant engineering, testing and certification. In 2009, we were awarded 94 patents for new products or applications and at December 31, 2009, we had approximately 1,000 granted patents and approximately 381 pending patent applications. We are widely regarded as the

1

Table of Contents

industry’s leading innovator and cost-efficient manufacturer in our end use markets. We work closely with our customers to design products that meet application-specific performance and quality requirements. We expect these innovations to drive our organic growth, sustain our leadership position, expand our market share, improve our margins and produce a high return on invested capital. For example, in 2008, we developed a family of environmentally-friendly products which provide an alternative to materials like polyvinyl chloride, or PVC, for medical packaging applications and wire and cable applications in electronics and automobiles.

Over the past several years, we have implemented a range of strategic initiatives designed to enhance our profitability and end use market position. These include fixed asset investments to expand our capacity in high value products, to enhance productivity at our existing facilities and to significantly reduce our fixed cost structure through headcount reductions, system upgrades and production line closures at our facility in Pernis, the Netherlands. During this period, we have shifted our portfolio to higher-margin products, substantially exited low-margin businesses such as footwear and implemented smart pricing strategies that have improved our overall margins and return on invested capital. We believe these initiatives provide us with a strong platform to drive growth, create significant operating leverage and position us to benefit from volume recovery in our end use markets.

We believe that starting in late 2008 the global economic downturn, and associated reduction in customer and end user inventory levels, caused an unprecedented slowdown across the industry. We experienced a decline in sales volume across all of our end use markets, including the traditionally more stable consumer and medical applications markets. We believe that a significant factor in this decline was inventory de-stocking. Our first and second quarter 2009 sales volumes were 39% and 24%, respectively, less than our sales volumes in the comparable 2008 quarters. The trend began to reverse itself in June 2009, as demand patterns began to shift towards recovery such that our third quarter 2009 sales volume was 10% less than the sales volume in the third quarter of 2008 and our fourth quarter 2009 sales volume was 16% above the sales volume in the fourth quarter of 2008. More recently, we have seen demand returning to more normal levels, with first-half 2010 sales volume up 34% compared to the first-half of 2009.

We generated total operating revenue of $968.0 million and $604.8 million for the twelve and six months ended December 31, 2009 and June 30, 2010, respectively, on volume of 260.3 kilotons and 159.1 kilotons, respectively. For the same periods, we generated net loss of $0.29 million and net income of $58.4 million, and Adjusted EBITDA of $91.4 million and $105.6 million, respectively. We define Adjusted EBITDA and reconcile it to net income in footnote 3 under “—Summary of Consolidated Financial Information and Other Data.” We report under one operating segment.

2

Table of Contents

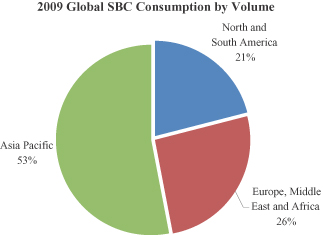

Our Industry Focus

The global demand for SBCs in 2009 exceeded 1,400 kilotons, resulting in sales of approximately $3.3 billion. According to management estimates, SBC demand for non-footwear applications grew at a compound annual growth rate of approximately 6.5% between 2001 and 2009. In 2008 and the first-half of 2009, the SBC market demand was negatively impacted by the global economic downturn. According to management estimates, prior to the economic downturn, SBC demand for non-footwear applications grew at a compound annual growth rate of approximately 9.0% between 2001 and 2007, or approximately 2.7 times global real GDP.

Source: Management Estimates

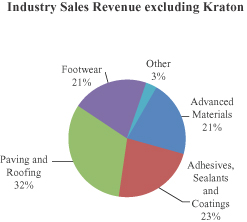

SBCs are primarily sold into four end uses: (1) Advanced Materials (compounding, personal care and polymer systems); (2) Adhesives, Sealants and Coatings; (3) Paving and Roofing; and (4) Footwear. Due to the higher selling prices in the Advanced Materials, Adhesives, Sealants and Coatings and Paving and Roofing end uses relative to the Footwear end use, the market share by end use on a revenue basis is meaningfully different than on a volume basis.

2009 Global SBC Consumption by End Use Market (1)

|

|

| (1) | Does not include Kraton Emerging Businesses volume or revenue. |

Source: Management Estimates

3

Table of Contents

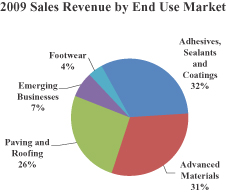

Kraton focuses on the high-value end use markets.

2009 Global SBC Consumption by End Use Market—Kraton vs. Industry (1)

|

|

| (1) | Does not include Kraton Emerging Businesses revenue. |

Source: Management Estimates

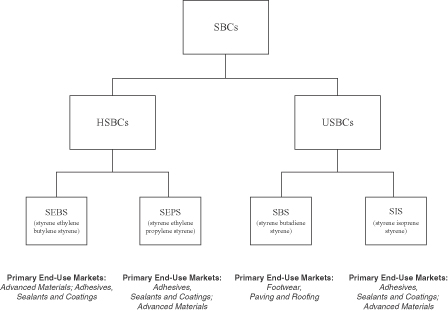

There are two major types of SBCs: hydrogenated styrenic block copolymers, or HSBCs, and unhydrogenated styrenic block copolymers, or USBCs.

HSBCs. HSBC products are significantly more complex to produce than USBC products and, consequently, generate higher margins and generally command selling prices between two and three times those for USBCs. We believe our 45% global end use market share of 2009 HSBC sales revenue leads the industry and is more than twice the size of our closest competitor. The HSBC class of products, which is typically more durable than USBC products, is primarily used in higher value-added Advanced Materials and Adhesives, Sealants and Coatings applications. We estimate that HSBCs accounted for approximately 21% of worldwide SBC industry sales revenue in 2009.

HSBCs are primarily used in our Advanced Materials and Adhesives, Sealants and Coatings end use markets, to impart improved performance characteristics such as:

| • | stretch properties in disposable diapers and adult incontinence products; |

| • | soft feel in numerous consumer products such as the handles for razor blades, power tools and automobile interiors; |

| • | impact resistance for demanding engineering plastic applications; |

| • | flexibility for wire and cable plastic outer layers; and |

| • | improved flow characteristics for many industrial and consumer sealants and lubricating fluids. |

USBCs. We believe that our 25% global market share of 2009 USBC sales revenue, excluding Footwear, leads the industry, and is approximately 1.3 times that of our closest competitor in terms of 2009 sales revenue. In 2009, we estimate that USBCs represented approximately 79% of worldwide SBC industry sales revenues and were used primarily in Footwear, Paving and Roofing and Adhesives, Sealants and Coatings end use.

USBCs are used in our Advanced Materials, Adhesives Sealants and Coatings and Paving and Roofing end use markets in a range of products to impart desirable characteristics, such as:

| • | resistance to temperature and weather extremes in roads and roofing; |

4

Table of Contents

| • | resistance to cracking, reduced sound transmission and better drainage in porous road surfaces; |

| • | impact resistance for consumer plastics; and |

| • | increased processing flexibility in materials used in disposable diapers and adhesive applications, such as packaging tapes and labels. |

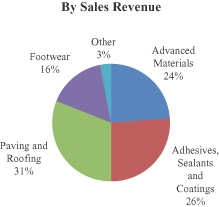

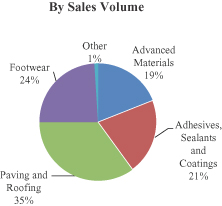

Our End Use Markets

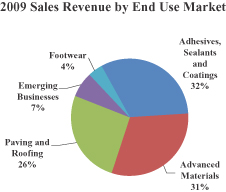

We believe we hold the number one global market position, based on 2009 sales revenue, in each of our targeted end use markets. We have aligned our commercial activities to serve four core end use markets that we believe have the highest growth and profitability potential: (1) Advanced Materials; (2) Adhesives, Sealants and Coatings; (3) Paving and Roofing; and (4) Emerging Businesses category.

The following table describes our core end use markets together with other end use markets and their approximate relative sizes:

| End Use Markets |

Revenue Mix (1) |

Our

End Use Market Position (2) |

Our

End Use Market Share (2) |

Our Relative End Use Market Share (3) |

Industry Compound Annual Growth Rate (4) |

Selected Applications/Products | |||||||||

| Advanced Materials |

31 | % | #1 | 36 | % | 2.0X | 7.4 | % | Soft touch for consumer products (tooth brushes and razor blades) and power tools Impact resistant engineering plastics Automotive components Elastic films for disposable diapers and adult incontinence branded products Skin care products and lotions Disposable food packaging Medical packaging films and tubing, often as alternatives to PVC | ||||||

| Adhesives, Sealants and Coatings |

32 | % | #1 | 34 | % | 1.9X | 5.9 | % | Tapes and labels Non-woven and industrial adhesives Industrial and consumer weather sealants | ||||||

| Paving and Roofing |

26 | % | #1 | 24 | % | 1.6X | 6.5 | % | Asphalt modification for performance roadways Asphalt modification for roofing felts and shingles | ||||||

| Emerging Businesses (5) |

7 | % | N/A | N/A | N/A | 26.8 | % | Surgical gloves Condoms | |||||||

| Other Markets (6) |

4 | % | N/A | N/A | N/A | N/A | Lubricants and fuel additives High styrenics packaging Footwear | ||||||||

5

Table of Contents

| (1) | Based on 2009 sales of $920.4 million (excludes by-product sales which are reported as other revenues). |

| (2) | Management estimates, based on 2009 sales. |

| (3) | Management estimates, versus next largest competitor based on 2009 sales. |

| (4) | Management estimates of volume growth, 2001 to 2009, except for Emerging Businesses, which is 2005 to 2009. |

| (5) | The Emerging Businesses end use market includes our IR and IRL business. We believe that we are the only major third-party supplier of IR and IRL, and therefore end use market position, end use market share and relative end use market share metrics are not meaningful. |

| (6) | Our Other Markets end use market is not directly comparable to our four core end use markets because it includes a mix of products ranging from lubricants and fuel additives to high styrenics packaging to footwear products. Therefore, we cannot estimate end use market position, end use market share, relative end use market share or industry compound annual growth rate. |

Our Competitive Strengths

We believe the following competitive strengths help us to sustain our market leadership position and contribute to our ability to generate superior margins and strong cash flow. We expect these strengths to support our growth in the future:

The Market Leader in SBCs

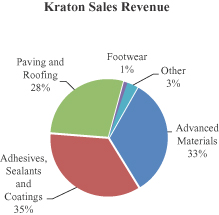

We believe we hold the number one global market position, based on 2009 sales revenue, in each of our four core end use markets, with sales of approximately $920.4 million and sales volumes of approximately 260.3 kilotons, excluding by-products, for the year ended December 31, 2009. We generated approximately 96% of our 2009 product sales revenues in our four core end use markets. Our Belpre, Ohio facility is the most diversified SBC plant in the world, and we believe our Wesseling, Germany, facility is world scale and cost efficient. As the pioneer of SBCs almost 50 years ago, we believe our Kraton® brand is widely recognized for our industry leadership, and we are particularly well regarded for our process technology expertise and long track record of market-driven innovation.

Growth Through Innovation and Technological Know-how

SBC production and product development requires complex and specific expertise, which we believe many of our competitors are unable to replicate. As the industry pioneer, Kraton maintains a constant focus on enhancing the value-added attributes of our products and on developing new applications for SBCs. At December 31, 2009, we had approximately 1,000 granted patents and approximately 381 pending patent applications. Our “Vision 20/20” program targets generating 20% of sales revenues from new products or applications introduced in the prior five years. In 2009, we generated 12.4% of our sales from innovation driven revenue. We believe that our new product innovation will allow us to drive increases in our volume, expand unit contribution margins (the excess of the sale price of a unit of product over the variable cost to produce that unit) and increase our customers’ reliance on Kraton’s products and technical expertise. For example, for the twelve months ended December 31, 2009, our Emerging Businesses end use market, which includes IR and IRL, represented 7.0% of sales revenues. Furthermore, our IRL business has grown at a compound annual growth rate of 28.8%, based on sales revenue, from 2007 to 2009 and is earning a unit contribution margin in excess of the company as a whole.

Diverse Global Manufacturing Capabilities and End Use Market Exposures

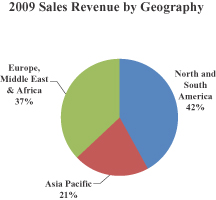

We manufacture our polymers at five manufacturing facilities on four continents (North America, Europe, South America and Asia) producing what we believe to be the highest quality grades available of USBCs; HSBCs and high purity IRL. We believe we are the only SBC producer with this breadth of technical capabilities and global footprint, selling approximately 800 products to more than 700 customers in over 60 countries

6

Table of Contents

worldwide. Since 2003, we have successfully completed plant expansions totaling 60 kilotons of capacity at a total cost of less than $50 million, giving us a total capacity of approximately 420 kilotons. Our manufacturing and product footprint allow revenue diversity, both geographically and by end use market. We believe our scale and footprint make us an attractive customer for our monomer suppliers, which in turn, allows us to offer a high degree of supply security to customers.

|

|

Source: Management Estimates

Long-Standing, Strong Customer Relationships Supported by Leading Service-Offering

We sell our products to over 700 customers, many of which we have had relationships with for 15 years or more. Our customers are broad-based, with no single customer accounting for more than 5% of our sales revenue in 2009. Our top 10 customers represented 26% of sales revenue in 2009. Our customers’ manufacturing processes are typically calibrated to the performance specifications of our products. Given the technical expertise and investment required to develop these formulations and the lead times required to replace them, we believe our customers face high switching costs. We believe our customers view our products as being high value-added, even though our products generally represent a small proportion of the overall cost of the finished product. Leveraging our global infrastructure, we believe we offer our customers a best-in-class service level that aligns us to their respective business models, through “on demand” order delivery and product development specifically designed for each customer’s needs.

Experienced Management Team with a Track Record of Growth and Productivity Improvements

Our senior management team has an average industry experience of approximately 25 years, most of which has been with some of the world’s leading companies, including General Electric, Koch Industries and Chevron Phillips Chemical. Since early 2008, when the current executive team was put in place, we have instituted a number of strategic initiatives designed to enhance productivity, reduce costs and capital intensity, expand margins and drive innovation-led growth.

Our Business Strategy

Building on these competitive strengths, we are focused on achieving profitable top-line growth and improving margins through the introduction of highly-engineered, high value-added products to drive strong and sustainable cash flow.

7

Table of Contents

Drive Growth and Margin Expansion Through Innovation

We have an almost 50-year track record of innovation dating back to our development of the first SBCs. Our research and development effort is focused on end use markets and new product developments that we believe offer high growth as well as opportunities to develop highly-differentiated products for our customers, thus yielding higher margin potential. We work very closely with our longstanding customer base to produce products that address their specific technical requirements. For example, to address an industry trend to provide an alternative to PVC in applications such as medical packaging and wire and cable, we have developed and commercialized a series of custom-designed polymers and compounds. In addition to this innovation-led growth, we believe that there are a number of end use market dynamics that will also drive growth in our business such as the general demand by customers for higher value-added product performance characteristics.

Pursue “Smart Pricing”

In late 2007, we undertook a comprehensive review of our entire product portfolio, including both product-specific and customer-specific profitability analyses. As a result, we took a variety of actions including reducing or eliminating our exposure to lower margin business and increasing our prices to reflect the significant value-added benefits of our products to our customers’ products. For example, since the end of 2007, we have increased our unit contribution margins by approximately 50%. We will continue to pursue pricing strategies that reflect the contribution to the end product of our high value and complex product offerings for which limited substitutes exist.

Invest in Key Growth Initiatives

We expect 2010 capital expenditures will be approximately $50.0 million to $55.0 million. Included in our 2010 capital expenditure estimate is approximately $9.0 million for the second phase of the Belpre systems and control upgrades, approximately $11.0 million to replace IR production from our Pernis facility, approximately $6.0 million for the IRL expansion and approximately $5.0 million for building upgrades at our Belpre facility. Through the six months ended June 30, 2010, capital expenditures were $19.4 million.

Continue to Pursue Operational Efficiencies

We have a history of implementing continuous process and cost improvement plans that have resulted in a significant reduction in our cost position and an improvement in the way we run our business. Since the beginning of 2007, we have implemented cost saving initiatives that have reduced costs by over $55 million, on an annual basis. In addition, as of December 31, 2009 we shut down IR production in our Pernis facility, which we expect will result in annual cost savings of approximately $12.0 million beginning in January 2010. Through these actions, we have created substantial operating leverage in our business model. We believe this demonstrates our management team’s ability to successfully manage the business in a downturn and position us for significant growth and margin expansion in a global economic recovery. For a discussion of the costs associated with the Pernis exit, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Recent Developments.”

Recent Developments

Project Assessment Underway for Additional HSBC Capacity in Asia. As a result of growth in Kraton’s differentiated grades of HSBCs globally, we see the need for additional manufacturing capacity. We are continuing to expand and strengthen our presence in Asia, and thus we believe Kraton’s regional, and global, business would benefit from such increased capacity. By committing the necessary resources, technology and capital, this would represent the next logical step to grow our position in the Asia Pacific region, in support of application and technology developments for Kraton’s leading, proprietary, SBC formulations. The anticipated 30 kiloton HSBC

8

Table of Contents

manufacturing facility would employ Kraton’s latest state-of-the-art technology for producing HSBCs and, we believe will set a new global standard for manufacturing cost and product quality, further demonstrating our commitment to our business, the region, and our customers. Our site-selection team is expected to make its recommendation to management by December 2010 by which time we will be in a better position to render a final project decision. While it is too early to estimate the expected cost of the new facility, we anticipate that construction could commence in the first half of 2012 with start-up occurring as early as the second half of 2013.

Shanghai Office. We have relocated our Shanghai office to a facility that is double the size of the previous location, in order to better accommodate our ongoing increase in staff and in-house capabilities. Our Shanghai staff has nearly doubled since 2006. The new facility also includes a multi-functional customer service center and a dedicated training facility.

New Innovation. In August 2010, we announced that our roof coating formulation containing Kraton G1643 exceeds requirements of the ASTM International D6083 standard specification that is recognized in the elastomeric roof coating market. ASTM International D6083 is an industry standard that establishes minimum performance levels in the following areas: viscosity, weight and volume solids; mechanical properties; adhesion; low temperature flexibility after accelerated weathering; tear resistance; permeation and water swelling; and fungi resistance. This gives innovators an opportunity to more effectively compare a polymer against other polymers for use in roof coating formulations. This SBC-based polymer has a proven track record of improving the performance of roof coatings because it adds superior water resistance, improved adhesion, and increased elongation to formulations. It can be used to help lower volatile organic compounds (VOCs) in a solvented formulation, which have significant vapor pressures that can affect the environment and human health. In addition, our tested formulation can be used under the EPA’s regulation for thermoplastic rubber coatings and mastic. A roof coating formulation containing Kraton G1643 can reduce the total cost of installation and provide fast cure coatings that will work better in cold, humid or wet conditions. Elastomeric roof coatings made with Kraton polymers will stand up better to ponding water, and provide excellent adhesion to all types of roofing substrates. Roof coatings made with Kraton G1643 are an excellent choice for low slope roofs, or high traffic areas, and will provide excellent reflectance to reduce energy costs and extend the life of a roof.

In July 2010, we announced the addition of Kraton D1183 BT, a new SIS grade, to our line of polymers for use in applications where softness, ease-in-processing and high temperature resistance are essential. Kraton D1183 BT is suitable for use in many adhesive applications including thermal printing labels, high temperature resistant labels, elastic labels and diaper tabs. It is an excellent choice for adhesives in hygiene applications and its shear strength is particularly good at 37 degrees Celsius. Moreover, it offers economically attractive adhesive formulations, and gives formulators the ability to dilute it further to obtain the equivalent performance levels of competing products, which can result in cost-savings. It can also achieve significantly higher cohesive strength and higher temperature resistance without the use of expensive endblock resins. Therefore, Kraton D1183 BT is not only economically attractive, but also substantially stronger and offers a wider formulating space. Prior to the commercialization of Kraton D1183 BT, innovators used low-coupled SIS block copolymers to impart softness to end-products. Although they offered improved adhesion on open and porous substrates and good label die-cutting performance, they often lacked cohesion, which hampered their use in applications where higher shear and temperature resistance were required. In comparison, Kraton D1183 BT is a 40% diblock SIS, which shows superior performance to low-coupled SIS block copolymers and is therefore the polymer of choice for these applications.

In May 2010, we announced the addition of Kraton DX405 to our product line of polymers for Adhesives, Sealants, and Coatings. This technology will allow our customers to more efficiently and expediently manufacture products that are stronger and softer. DX405 has a low styrene content, which promotes ease of processing, low viscosity, and the attainment of lower application temperatures. This adds efficiency and

9

Table of Contents

simplification to the manufacturing process, which shortens batch times, increases extrusion rates and improves productivity. DX405 has a wide formulation window and its versatility makes it suitable for solvent-based compositions, hot melt adhesives, and sealant applications. It can be formulated with other polymers, resins, fillers, pigments, oils, thickeners, waxes and stabilizers to obtain a desired balance of properties.

Polyisoprene Rubber Manufacturing at Belpre, Ohio. We plan to invest approximately $27.0 million in our Belpre, Ohio facility to enable production of IR. We will convert existing USBC capacity to allow us to swing production from USBC products to the production of IR. Plant modifications and upgrades commenced in the third quarter of 2010 with the new IR production capabilities expected to be completed by mid-2011.

Isoprene Rubber Latex Capacity Expansion at Paulinia, Brazil. We plan to invest approximately $10.0 million to debottleneck and expand IRL capacity at our Paulinia, Brazil, facility. We commenced spending on this initiative in the third quarter of 2010 with the project expected to be completed by mid-2011. When combined with the capacity that is contractually available to us at a third party site in Japan, this debottlenecking project will represent an estimated 33% increase in our total IRL capacity.

European Office Consolidation. We are consolidating our transactional functions as well as much of our European management to a new European central office in Amsterdam, the Netherlands. We believe that with this initiative we will achieve greater operating efficiency as well as service improvements by consolidating core competencies and further exploiting the advantages of our new global ERP system rolled out in 2009. We anticipate minimal impact on existing customer relationships and no interruption in customer service during the gradual implementation of this transition plan. We expect to incur approximately $5.0 million to $6.0 million of restructuring costs, largely in the second half of 2010 as a result of this consolidation. We expect operating cost reductions of more than $2.0 million on an annual basis starting in 2012 as a result of this consolidation.

Corporate and Other Information

We conduct our business through a Delaware limited liability company, Kraton Polymers LLC (“Kraton”), and its consolidated subsidiaries. Prior to our initial public offering, Kraton’s parent company was Polymer Holdings LLC, a Delaware limited liability company. On December 16, 2009, Polymer Holdings LLC, or Polymer Holdings, was converted from a Delaware limited liability company to a Delaware corporation and renamed Kraton Performance Polymers, Inc., which remains Kraton’s parent company. Trading in our common stock on the New York Stock Exchange commenced on December 17, 2009 under the symbol “KRA.” On December 22, 2009, we completed our initial public offering.

Our principal executive offices are located at 15710 John F. Kennedy Boulevard, Suite 300, Houston, Texas 77032, and our telephone number is (281) 504-4700. Our corporate web site address is www.kraton.com. We do not incorporate the information contained on, or accessible through, our corporate web site into this prospectus, and you should not consider it part of this prospectus.

Principal Stockholders

Prior to this offering, certain affiliates of TPG Capital, L.P., which we refer to collectively as “TPG,” owned approximately 36.90% of our common stock and certain affiliates of J.P. Morgan Partners, LLC, which we refer to collectively as “JPMP,” owned approximately 24.60% of our common stock. After the sale of our common stock by TPG and JPMP in this offering, TPG will own 21.52% of our common stock (approximately 19.21% pursuant to a full exercise of the underwriters’ over-allotment option) and JPMP will own 14.34% of our common stock (approximately 12.81% pursuant to a full exercise of the underwriters’ over-allotment option), and together TPG and JPMP will own approximately 35.86% of our common stock (approximately 32.02% pursuant to a full exercise of the underwriters’ over-allotment option).

10

Table of Contents

TPG Capital, L.P.

TPG is a leading private investment firm with approximately $47 billion of assets under management as of June 30, 2010. The firm was founded in 1992 and is led by David Bonderman and James G. Coulter. Through its global buyout platform, TPG Capital, the firm generally makes significant investments in companies through acquisitions and restructurings across a broad range of industries throughout North America, Europe, Asia and Australia. Notable investments include Alltel Corp., Avaya, Inc., Burger King Holdings, Inc., Continental Airlines, Inc., Energy Future Holdings Corp. (formerly, TXU Corp.), Graphic Packaging International Corp., Grohe AG, Harrah’s Entertainment, Inc., J Crew Group, Inc., Neiman Marcus Group, Inc., ON Semiconductor Corp., Seagate Technology, Shenzhen Development Bank Co., Ltd. and Texas Genco, LLC.

J.P. Morgan Partners

J.P. Morgan Partners, LLC is a private equity division of JPMorgan Chase & Co. (NYSE: JPM), one of the largest financial institutions in the United States. JPMP has invested over $15 billion worldwide in industrial, consumer, media, energy, financial services, healthcare and technology companies since its inception in 1984. In August 2006, the buyout and growth equity investment professionals of JPMP separated from JPMorgan Chase & Co. and formed CCMP Capital Advisors, LLC, or CCMP Capital, a global private equity firm specializing in buyout and growth equity investments. CCMP Capital has offices in New York, Texas and London. CCMP Capital advises JPMP on its portfolio of private equity investments, including the investment in our company; other notable investments include AMC Entertainment, Inc., Aramark Holdings Corporation, Grupo Corporative Ono, S.A., Jetro JMDH Holdings, Inc., Noble Environmental Power, LLC, QCE Holdings, LLC (Quiznos Sub), Warner Chilcott Holdings Co. and PQ Corporation.

11

Table of Contents

The Offering

| Common stock offered by the selling stockholders |

8,000,000 shares. |

| Use of proceeds |

The selling stockholders will receive all of the proceeds from this offering and we will not receive any proceeds from the sale of shares in this offering. |

| Principal and selling stockholders |

TPG and JPMP are our principal stockholders and the only selling stockholders in this offering. Upon completion of this offering, TPG will own 21.52% of our common stock and JPMP will own 14.34% of our common stock. Together, TPG and JPMP will own approximately 35.86% of our common stock. See “Principal and Selling Stockholders.” |

| Underwriters’ option to purchase additional shares |

The selling stockholders may sell up to 1,200,000 additional shares if the underwriters exercise their over-allotment option. |

| Dividend policy |

We have not previously declared or paid any dividends or distributions on our common stock. We currently expect to retain future earnings, if any, for use in the operation and expansion of our business and do not anticipate paying any cash dividends in the foreseeable future. We are currently prohibited from paying cash dividends on our common stock by the covenants in the senior secured credit facility and may be further restricted by the terms of future debt or preferred securities. See “Dividend Policy.” |

| Risk factors |

Investing in our common stock involves a high degree of risk. See “Risk Factors” for a discussion of factors you should carefully consider before deciding to invest in our common stock. |

| New York Stock Exchange symbol |

“KRA” |

Except as otherwise noted, all information in this prospectus:

| • | excludes 3,604,484 shares of common stock reserved for future issuance under the Polymer Holdings LLC 2009 Equity Incentive Plan; and |

| • | assumes the underwriters do not exercise their over-allotment option. |

12

Table of Contents

Summary of Consolidated Financial Information and Other Data

The table below sets forth our summary consolidated historical financial data for the periods indicated. The summary consolidated historical financial data presented below for the years ended December 31, 2009, 2008 and 2007 and as of December 31, 2009 and 2008 have been derived from our audited consolidated financial statements, which are included elsewhere in this prospectus. The summary consolidated historical financial data for the six months ended June 30, 2010 and 2009 and as of June 30, 2010 have been derived from our unaudited condensed consolidated financial statements, which are included elsewhere in this prospectus. The unaudited condensed consolidated financial statements include, in the opinion of management, all adjustments, consisting only of normal recurring adjustments, that management considers necessary for the fair presentation of the condensed consolidated financial information set forth in those statements. Results of operations for the interim periods are not necessarily indicative of the results that might be expected for any other interim period or for an entire year.

The summary consolidated financial information and other data presented below should be read in conjunction with the information contained in “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” the audited consolidated financial statements and the notes thereto and the unaudited condensed consolidated financial statements and the notes thereto, which are included elsewhere in this prospectus.

| Year ended December 31, | Six months ended June 30, | |||||||||||||||||

| 2009 | 2008 | 2007 | 2010 | 2009 | ||||||||||||||

| (In thousands, except per share data) | (unaudited) | |||||||||||||||||

| Consolidated Statements of Operations Data: |

||||||||||||||||||

| Operating Revenues |

||||||||||||||||||

| Sales |

$ | 920,362 | $ | 1,171,253 | $ | 1,066,044 | $ | 604,818 | $ | 411,607 | ||||||||

| Other (1) |

47,642 | 54,780 | 23,543 | — | 17,172 | |||||||||||||

| Total operating revenues |

968,004 | 1,226,033 | 1,089,587 | 604,818 | 428,779 | |||||||||||||

| Cost of Goods Sold |

792,472 | 971,283 | 938,556 | 446,578 | 384,085 | |||||||||||||

| Gross Profit |

175,532 | 254,750 | 151,031 | 158,240 | 44,694 | |||||||||||||

| Operating Expenses |

||||||||||||||||||

| Research and development expenses |

21,212 | 27,049 | 24,865 | 11,556 | 10,040 | |||||||||||||

| Selling, general and administrative |

79,504 | 101,431 | 69,020 | 43,834 | 36,303 | |||||||||||||

| Depreciation and amortization of identifiable intangibles |

66,751 | 53,162 | 51,917 | 23,015 | 25,106 | |||||||||||||

| Total operating expenses |

167,467 | 181,642 | 145,802 | 78,405 | 71,449 | |||||||||||||

| Gain on Extinguishment of Debt |

23,831 | — | — | — | 23,831 | |||||||||||||

| Earnings of Unconsolidated Joint Venture (2) |

403 | 437 | 626 | 236 | 176 | |||||||||||||

| Interest Expense, Net |

33,956 | 36,695 | 43,484 | 12,336 | 16,738 | |||||||||||||

| Income (Loss) Before Income Taxes |

(1,657 | ) | 36,850 | (37,629 | ) | 67,735 | (19,486 | ) | ||||||||||

| Income Tax Expense (Benefit) |

(1,367 | ) | 8,431 | 6,120 | 9,345 | 1,160 | ||||||||||||

| Net Income (Loss) |

$ | (290 | ) | $ | 28,419 | $ | (43,749 | ) | $ | 58,390 | $ | (20,646 | ) | |||||

| Earnings (Loss) per common share (3) |

||||||||||||||||||

| Basic |

$ | (0.01 | ) | $ | 1.46 | $ | (2.26 | ) | $ | 1.90 | $ | (1.06 | ) | |||||

| Diluted |

$ | (0.01 | ) | $ | 1.46 | $ | (2.26 | ) | $ | 1.88 | $ | (1.06 | ) | |||||

| Weighted average common shares outstanding (3) |

||||||||||||||||||

| Basic |

19,844 | 19,406 | 19,375 | 30,751 | 19,409 | |||||||||||||

| Diluted |

19,844 | 19,483 | 19,375 | 31,023 | 19,409 | |||||||||||||

13

Table of Contents

| (1) | Other revenues include the sale of by-products generated in the production of polyisoprene rubber, or IR, and styrene-isoprene-styrene, or SIS. |

| (2) | Represents our 50% joint venture interest in Kraton JSR Elastomers K.K., which is accounted for using the equity method of accounting. |

| (3) | See Note 12 to our audited consolidated financial statements and Note 7 to our unaudited condensed consolidated financial statements, which are included elsewhere in this prospectus. |

| December 31, | June 30, 2010 | ||||||||

| 2009 | 2008 | ||||||||

| (In thousands) | (unaudited) | ||||||||

| Balance Sheet Data |

|||||||||

| Cash and cash equivalents |

$ | 69,291 | $ | 101,396 | $ | 39,405 | |||

| Total assets |

974,499 | 1,031,874 | 997,179 | ||||||

| Total debt |

$ | 384,979 | $ | 575,316 | $ | 383,827 | |||

| Fiscal Year | Six months ended June 30, | ||||||||||||||

| 2009 | 2008 | 2007 | 2010 | 2009 | |||||||||||

| (In thousands) | (unaudited) | ||||||||||||||

| Other Data |

|||||||||||||||

| EBITDA (1)(2) |

$ | 99,050 | $ | 126,707 | $ | 57,772 | $ | 103,086 | $ | 22,358 | |||||

| Adjusted EBITDA (3) |

91,359 | 152,048 | 68,310 | 105,647 | 3,189 | ||||||||||

| (1) | EBITDA represents net income before interest, taxes, depreciation and amortization. We present EBITDA because it is used by management to evaluate operating performance. We consider EBITDA an important supplemental measure of our performance and believe it is frequently used by investors and other interested parties in the evaluation of companies in our industry. |

| We also use EBITDA for the following purposes: a portion of our executive compensation plan is based on our EBITDA performance (with certain adjustments) and the senior secured credit facilities and the senior subordinated notes use EBITDA (with additional adjustments) to measure our compliance with covenants such as leverage and interest coverage ratios. |

| EBITDA has limitations as an analytical tool, and you should not consider it in isolation, or as a substitute for analysis of our results as reported under generally accepted accounting principles in the United States (“GAAP”). Some of these limitations are: |

| • | EBITDA does not reflect our cash expenditures, or future requirements for capital expenditures or contractual commitments; |

| • | EBITDA does not reflect changes in, or cash requirements for, our working capital needs; |

| • | EBITDA does not reflect the significant interest expense, or the cash requirements necessary to service interest or principal payments, on our debt; |

| • | although depreciation and amortization are non-cash charges, the assets being depreciated and amortized will often have to be replaced in the future, and EBITDA does not reflect any cash requirements for such replacements; and |

| • | other companies in our industry may calculate EBITDA differently than we do, limiting its usefulness as a comparative measure. |

| Because of these and other limitations, EBITDA should not be considered as a measure of discretionary cash available to us to invest in the growth of our business. We compensate for these limitations by relying primarily on our GAAP results and using EBITDA and Adjusted EBITDA only supplementally. See the condensed consolidated statements of cash flows included in the condensed consolidated financial statements included elsewhere in this prospectus. |

14

Table of Contents

| (2) | We reconcile Net Income/(Net Loss) to EBITDA as follows: |

| Fiscal Year | Six months ended June 30, | |||||||||||||||||

| 2009 | 2008 | 2007 | 2010 | 2009 | ||||||||||||||

| (In thousands) | ||||||||||||||||||

| Net Income/(Net Loss) |

$ | (290 | ) | $ | 28,419 | $ | (43,749 | ) | $ | 58,390 | $ | (20,646 | ) | |||||

| Add (deduct) |

||||||||||||||||||

| Interest expense, net |

33,956 | 36,695 | 43,484 | 12,336 | 16,738 | |||||||||||||

| Income tax expense (benefit) |

(1,367 | ) | 8,431 | 6,120 | 9,345 | 1,160 | ||||||||||||

| Depreciation and amortization expenses |

66,751 | 53,162 | 51,917 | 23,015 | 25,106 | |||||||||||||

| EBITDA (a) |

$ | 99,050 | $ | 126,707 | $ | 57,772 | 103,086 | 22,358 | ||||||||||

| (a) | EBITDA in fiscal year 2009 was negatively impacted by approximately $17.6 million due to the sale of inventory produced when raw material costs were higher than the then current replacement cost. Conversely, EBITDA in fiscal year 2008 was positively impacted by approximately $37.1 million due to the sale of inventory produced when raw material costs were lower than the then current replacement cost. |

| EBITDA in the six months ended June 30, 2010 was positively impacted by approximately $21.9 million due to the sale of inventory produced when raw material costs were lower than the then current replacement cost. Conversely, EBITDA in the six months ended June 30, 2009 was negatively impacted by approximately $43.6 million due to the sale of inventory produced when raw material costs were higher than the then current replacement cost. |

| (3) | We present Adjusted EBITDA as a further supplemental measure of our performance and because we believe these additional adjustments provide additional and helpful information to investors and other interested parties evaluating our performance. We prepare Adjusted EBITDA by adjusting EBITDA to eliminate the impact of a number of items we do not consider indicative of our ongoing operating performance. We explain how each adjustment is derived and why we believe it is helpful and appropriate in the subsequent footnotes. You are encouraged to evaluate each adjustment and the reasons we consider it appropriate for supplemental analysis. As an analytical tool, Adjusted EBITDA is subject to all the limitations applicable to EBITDA. In addition, in evaluating Adjusted EBITDA, you should be aware that in the future we may incur expenses similar to the adjustments in this presentation. Our presentation of Adjusted EBITDA should not be construed as an inference that our future results will be unaffected by unusual or non-recurring items. |

We further reconcile EBITDA to Adjusted EBITDA as follows:

| Fiscal Year | Six months ended June 30, | ||||||||||||||||

| 2009 | 2008 | 2007 | 2010 | 2009 | |||||||||||||

| (In thousands) | (unaudited) | ||||||||||||||||

| EBITDA (a) |

$ | 99,050 | $ | 126,707 | $ | 57,772 | $ | 103,086 | $ | 22,358 | |||||||

| Add (deduct): |

|||||||||||||||||

| Sponsor fees and expenses |

2,000 | 2,000 | 2,000 | — | 1,000 | ||||||||||||

| Restructuring and related charges (b) |

9,677 | 13,671 | 5,633 | 790 | 1,107 | ||||||||||||

| Other non-cash expenses (c) |

4,463 | 9,670 | 2,905 | 1,771 | 2,555 | ||||||||||||

| Gain on extinguishment of debt (d) |

(23,831 | ) | — | — | — | (23,831 | ) | ||||||||||

| Adjusted EBITDA (a) |

$ | 91,359 | $ | 152,048 | $ | 68,310 | $ | 105,647 | $ | 3,189 | |||||||

| (a) | EBITDA and Adjusted EBITDA in fiscal year 2009 were negatively impacted by approximately $17.6 million due to the sale of inventory produced when raw material costs were higher than the then current replacement cost. Conversely EBITDA and Adjusted EBITDA in fiscal year 2008 were positively impacted by approximately $37.1 million due to the sale of inventory produced when raw material costs were lower than the then current replacement cost. |

15

Table of Contents

| EBITDA and Adjusted EBITDA in the six months ended June 30, 2010 were positively impacted by approximately $21.9 million due to the sale of inventory produced when raw material costs were lower than the then current replacement cost. Conversely EBITDA and Adjusted EBITDA in the six months ended June 30, 2009 were negatively impacted by approximately $43.6 million due to the sale of inventory produced when raw material costs were higher than the then current replacement cost. |

| (b) | 2009 costs consist principally of the costs to exit our Pernis facility and the one-time cost to terminate the sponsor management fee arrangement; 2008 costs consist primarily of severance and retention costs associated with the restructuring of our Westhollow Technical Center and our research and technical services organizations, senior management changes in the first quarter and workforce reductions in the fourth quarter; and 2007 costs are primarily costs in connection with the shutdown of our SIS plant in Pernis. Costs for six months ended June 30, 2010 consist primarily of legal and consulting fees associated with the restructuring of our European organization. All periods, including six months ended June 30, 2009, reflect costs associated with evaluating merger and acquisition transactions and potential debt refinancing. |

| (c) | For 2009, 2008 and 2007, consists primarily of non-cash compensation, asset impairment charges and losses on the sale of fixed assets. For 2008 and 2009, also reflects the non-cash adjustment to lower inventory from first in first out cost to market value. For six months ended June 30, 2010 and 2009, consists primarily of non-cash compensation. For six months ended June 30, 2009, also reflects the non-cash inventory impairment to lower inventory from first-in first-out cost to market value and losses on the sale of fixed assets. |

| (d) | For 2009 and six months ended June 30, 2009, reflects the non-recurring cash gain related to the repurchases of bonds. |

| Restructuring and related charges discussed above were recorded in the Consolidated Statements of Operations, as follows. |

| Fiscal Year | Six months ended June 30, | ||||||||||||||

| 2009 | 2008 | 2007 | 2010 | 2009 | |||||||||||

| (In thousands) | |||||||||||||||

| Cost of goods sold |

$ | 6,747 | $ | 355 | $ | 2,438 | $ | — | $ | 200 | |||||

| Research and development |

$ | — | $ | 2,430 | $ | 345 | $ | — | $ | — | |||||

| Selling, general and administrative |

$ | 2,930 | $ | 10,886 | $ | 2,850 | $ | 790 | $ | 907 | |||||

| Total restructuring and related charges |

$ | 9,677 | $ | 13,671 | $ | 5,633 | $ | 790 | $ | 1,107 | |||||

16

Table of Contents

Buying shares of our common stock involves risk. You should consider carefully the risks and uncertainties described below, together with all of the other information in this prospectus, including the financial statements and the related notes included elsewhere in this prospectus, before deciding to purchase shares of our common stock.

Risk Factors Relating to our Business

Conditions in the global economy and capital markets may adversely affect the company’s results of operations, financial condition and cash flows.

Our products are sold in markets that are sensitive to changes in general economic conditions, such as automotive and construction products. Downturns in general economic conditions can cause fluctuations in demand for our products, product prices, volumes and margins. A decline in the demand for our products or a shift to lower-margin products due to deteriorating economic conditions could adversely affect sales of our products and our profitability and could also result in impairments of certain of our assets.

Our business and operating results were affected by the global recession, dislocations in the housing and commercial real estate markets, fluctuating commodity prices, volatile exchange rates and other challenges currently affecting the global economy and our customers. Although the effects of the global recession on our business appear to have eased, there can be no assurance that this trend will continue. If the global recession continues for significant future periods or significantly worsens, our results of operations, financial condition and cash flows could be materially adversely affected.

LyondellBasell Industries provides significant operating and other services under agreements that are important to our business. The failure of LyondellBasell to perform its obligations, or the termination of these agreements, could adversely affect our operations.

We have operating and service agreements with LyondellBasell Industries, or LyondellBasell, that are important to our business. We are a party to:

| • | operating agreements pursuant to which LyondellBasell (in Berre, France, and Wesseling, Germany) operate and maintain our European manufacturing facilities and employs and provides almost all of the staff for those facilities; |

| • | site services, utilities, materials and facilities agreements pursuant to which LyondellBasell provides utilities and site services to our European manufacturing facilities; and |

| • | lease agreements pursuant to which we lease our European manufacturing sites from LyondellBasell. |

In January 2009, the U.S. operations of LyondellBasell along with one of its European holding companies, Basell Germany Holdings GmbH, filed for voluntary reorganization under Chapter 11 of the U.S. Bankruptcy Code. Its Chapter 11 reorganization plan was confirmed by the bankruptcy court in April 2010, and LyondellBasell has emerged from bankruptcy. LyondellBasell is one of our major suppliers of raw materials and also operates our facilities at Berre, France, and Wesseling, Germany. LyondellBasell’s emergence from bankruptcy and any resulting restructuring of LyondellBasell’s operations could adversely affect LyondellBasell’s ability to provide services to us. To date, our operations have not been negatively impacted and we do not anticipate any such negative impact. However, we cannot predict the effect, if any, that LyondellBasell’s bankruptcy or emergence from bankruptcy will ultimately have upon our business in general, or our relationship with LyondellBasell in particular.

Under the terms of the above agreements, either party is permitted to terminate the applicable agreement in a variety of situations. Should LyondellBasell fail to provide these services or should any operating agreement be terminated, we would be forced to obtain these services from third parties or provide them ourselves. Similarly, if in connection with or independent from the termination of an operating agreement, LyondellBasell terminates a facility lease, we would be forced to relocate our manufacturing facility. From time to time, as part of our

17

Table of Contents

ongoing business operations, we discuss potential changes in the terms of our various agreements with LyondellBasell, based upon changes in market conditions or other factors. Any agreed changes to any of these contractual arrangements are not binding until the execution of formal documentation. The failure of LyondellBasell to perform its obligations under, or the termination of, any of these agreements could adversely affect our operations and, depending on market conditions at the time of any such termination, we may not be able to enter into substitute arrangements in a timely manner, or on terms as favorable to us.

Under certain of these agreements, we are required to indemnify LyondellBasell in certain circumstances, including in certain circumstances for loss and damages resulting from LyondellBasell’s negligence in performing their obligations.

The failure of our raw materials suppliers to perform their obligations under long-term supply agreements, or our inability to replace or renew these agreements when they expire, could increase our cost for these materials, interrupt production or otherwise adversely affect our results of operations.

Our manufacturing processes use three primary raw materials: styrene, butadiene and isoprene. We use styrene in the production of most of our polymer products. We use butadiene in the production of SBS (styrene-butadiene-styrene) grades of USBCs and SEBS (styrene-ethylene-butylene-styrene) grades of HSBCs. We use isoprene in the production of SIS (styrene-isoprene-styrene) grades of USBCs, SEPS (styrene-ethylene-propylene-styrene) grades of HSBCs and polyisoprene rubber, or IR. We have entered into long-term supply agreements with Shell Chemicals L.P., or Shell Chemicals, LyondellBasell and others to supply our raw material needs in the United States and Europe. As these contracts expire, we may be unable to renew these contracts or obtain new long-term supply agreements on terms favorable to us, which may significantly impact our operations.

Isoprene is primarily produced and consumed by manufacturers, captively for the production of IR, which is primarily used in the manufacture of rubber tires. As a result, there is limited non-captive isoprene available for purchase in the markets in which we operate. Future isoprene requirements for our IR products will be met by our overall isoprene sourcing strategies. We may not be able to obtain isoprene required for our operations on terms favorable to us or at all.

In addition, most of our long-term contracts contain provisions that allow our suppliers to limit the amount of raw materials shipped to us below the contracted amount in certain circumstances. During 2009, butadiene producers had limited supply at times due to raw material shortages and operational problems, and we have satisfied our butadiene needs by supplementing with spot market purchases. If we are required to obtain alternate sources for raw materials because a supplier is unwilling or unable to perform under raw material supply agreements or if a supplier terminates its agreements with us, we may not be able to obtain these raw materials from alternative suppliers in a timely manner or be able to enter into long-term supply agreements on terms as favorable to us. A lack of availability of raw materials could have an adverse effect on our results of operations.

If the availability of isoprene is limited, we may be unable to produce some of our products in quantities demanded by our customers, which could have an adverse effect on our sales of products requiring isoprene.

Isoprene is not widely available, and the few isoprene producers tend to use their production for captive manufacturing purposes or sell only limited quantities into the world chemicals market. The major producers of isoprene are Goodyear, Shell Chemicals L.P., Nippon Zeon, Braskem, several Chinese producers and various Russian manufacturers. Currently, we source our isoprene requirements for the United States and Europe from a portfolio of suppliers. In Japan, we obtain the majority of our isoprene requirements from JSR Corporation, or JSR, on a commercial supply basis and from alternative suppliers as needed. In Brazil, isoprene is obtained from a local third party supplier. These suppliers may not be able to meet our isoprene requirements, and we may not be able to obtain substitute supplies of isoprene from alternative suppliers in a timely manner or on favorable terms.

18

Table of Contents

Because there is limited non-captive isoprene availability, the market for isoprene is thin and prices are particularly volatile. Prices for isoprene are determined by the supply and prices of natural and synthetic rubber, crude oil and natural gas prices and existing supply and demand in the market. Market prices for isoprene increased significantly during the second half of 2008 as energy prices peaked in the third quarter. Following the collapse of energy prices in late 2008, isoprene pricing declined in the first quarter of 2009, increased during the second quarter of 2009, stabilized, then increased again in the fourth quarter of 2009. Isoprene pricing continued to increase through the first quarter of 2010 then leveled off in the second quarter of 2010.

In the past, a significant factor contributing to higher prices was the extreme tightness in the market caused by operational problems of some key producers and reduced availability of crude C5 inputs for the extraction units. Although improved producer operation mitigated this risk in 2008, weak ethylene demand and light (ethane versus naphtha) ethylene inputs have limited isoprene production for some of the suppliers. In addition to this limit due to ethylene inputs, operational problems could return in the future. A lack of availability of isoprene could have an adverse effect on our results of operations if we are unable to produce products containing isoprene.

If the availability of butadiene is limited, we may be unable to produce some of our products in quantities demanded by our customers, which could have an adverse effect on plant utilization and our sales of products requiring butadiene.

The North American market is structurally short of butadiene and has relied on imports of crude C4 and/or butadiene to balance demand. Historically, the European market has been better balanced and provided exports to North America. Currently, our butadiene requirements in the United States are satisfied by several suppliers, and LyondellBasell is our major butadiene supplier in Europe. In January 2009, the U.S. operations of LyondellBasell along with one of its European holding companies, Basell Germany Holdings GmbH, filed for voluntary reorganization under Chapter 11 of the U.S. Bankruptcy Code. Its Chapter 11 reorganization plan was confirmed by the bankruptcy court in April 2010, and LyondellBasell has emerged from bankruptcy. To date, LyondellBasell’s emergence from bankruptcy has not negatively impacted our supply of butadiene in Europe. The quantity of butadiene available in any one region is dependent on the cracking inputs of olefins plants, ethylene demand, inter-regional demand for butadiene and demand for other oil derivatives. Suppliers may not be able to meet our butadiene requirements, and we may not be able to obtain substitute supplies of butadiene from alternative suppliers in a timely manner or on favorable terms.

Increases in the costs of our raw materials could have an adverse effect on our financial condition and results of operations if those costs cannot be passed onto our customers.

Our results of operations are directly affected by the cost of our raw materials. Our three principal raw materials (styrene, butadiene, and isoprene) together represented approximately 43% and 54% of our total cost of goods sold in fiscal year 2009 and for the six months ended June 30, 2010, respectively. Because of the significant portion of our cost of goods sold represented by these three monomers, our gross profit and margins could be adversely affected by changes in the cost of these raw materials if we are unable to pass the increases on to our customers.

Our end use markets are highly competitive, and we may lose market share to other producers of styrenic block copolymers or to producers of other products that can be substituted for our products.

Our industry is highly competitive and we face significant competition from large international producers, as well as from smaller regional competitors. Our competitors may improve their competitive position in our core end use markets by successfully introducing new products, improving their manufacturing processes or expanding their capacity or manufacturing facilities. If we are unable to keep pace with our competitors’ product and manufacturing process innovations, our financial condition and results of operations could be materially adversely affected.

19

Table of Contents

Our most significant competitors are Asahi Chemical, Chi Mei, Dexco Polymers, Dynasol Elastomers, Korea Kumho P.C., Kuraray Company, Lee Chang Yung, LG Chemical, Polimeri Europa, Sinopec, Taiwan Synthetic Rubber Corporation and Zeon Corporation. Kuraray Company, Dynasol Elastomers, Korea Kumho P.C. and Sinopec have all expanded HSBC capacity over the last three years. Several competitors, including Dynasol, Lee Chang Yung and Sinopec, have expanded USBC capacity over the last three years.

In addition, competition between styrenic block copolymers and other products within the end use markets in which we compete is intense. Increased competition from existing or newly developed non-SBC products may reduce demand for our products in the future and our customers may decide on alternate sources to meet their requirements.

| • | In the Advanced Materials end use market, our products compete against a wide variety of chemical and non-chemical alternatives, including thermoplastic vulcanizates, ethylene propylene diene monomer rubber, known as EPDM, thermoplastic polyolefin elastomers and thermoplastic polyurethanes, known as TPUs. The choice between these materials is influenced by performance characteristics, ease of use, desired aesthetics and total end-product cost. In addition, competing materials include spandex, natural rubber, polyvinyl chloride polymers and compounds, polyolefins, polyethylene terephthalate, known as PET, nylon and polycarbonate, based on performance, ease of use, desired aesthetics and total end-product cost. |

| • | In the Adhesives, Sealants and Coatings end use market, SBC products primarily compete with acrylics, silicones, solvent-based rubber systems and thermoplastic polyolefin elastomers. The choice between these materials is influenced by bond strength, specific adhesion, consistent performance to specification, processing speed, hot-melt application, resistance to water and total end-product cost. |

| • | In the Paving and Roofing end use market, our products primarily compete with atactic polypropylene, styrene butadiene rubber and unmodified asphalts. The choice between these materials is influenced by total end-product performance, cost and ease of use. |

If we are unable to successfully compete with other producers of styrenic block copolymers or if other products can be successfully substituted for our products, our sales may decline.

If we are not able to continue the technological innovation and successful commercial introduction of new products, our customers may turn to other producers to meet their requirements.

Our industry and the end use markets into which we sell our products experience periodic technological change and ongoing product improvements.

In addition, our customers may introduce new generations of their own products or require new technological and increased performance specifications that would require us to develop customized products. Innovation or other changes in our customers’ product performance requirements may also adversely affect the demand for our products. Our future growth will depend on our ability to gauge the direction of the commercial and technological progress in all key end use markets, and upon our ability to successfully develop, manufacture and market products in such changing end use markets. We need to continue to identify, develop and market innovative products on a timely basis to replace existing products in order to maintain our profit margins and our competitive position. We may not be successful in developing new products and technology that successfully compete with such materials and our customers may not accept any of our new products. If we fail to keep pace with evolving technological innovations or fail to modify our products in response to our customers’ needs, then our business, financial condition and results of operations could be adversely affected as a result of reduced sales of our products.

Our business relies on intellectual property and other proprietary information, and our failure to protect our rights could harm our competitive advantages with respect to the manufacturing of some of our products.

Our success depends to a significant degree upon our ability to protect and preserve our intellectual property and other proprietary information of our business. However, we may be unable to prevent third parties from using our intellectual property and other proprietary information without our authorization or independently

20

Table of Contents

developing intellectual property and other proprietary information that is similar to ours, particularly in those countries where the laws do not protect our proprietary rights to the same degree as in the United States. The use of our intellectual property and other proprietary information by others could reduce or eliminate any competitive advantage we have developed, cause us to lose sales or otherwise harm our business. If it becomes necessary for us to litigate to protect these rights, any proceedings could be burdensome and costly, and we may not prevail. In addition, we acquired a significant number of patents from Shell Chemicals L.P., or Shell Chemicals. Pursuant to the agreements with Shell Chemicals relating to their contribution of these patents to us and our ownership of these patents, Shell Chemicals retained for itself fully-transferable and exclusive licenses to their use outside of the elastomers business, as well as fully-transferable non-exclusive licenses within the field of elastomers for certain limited uses in non-competing activities. Shell Chemicals is permitted to sublicense these rights. Shell Chemicals also retains the right to enforce these patents outside the elastomers field and recover any damages resulting from these actions.