Attached files

| file | filename |

|---|---|

| EX-31.2 - United States Commodity Index Funds Trust | v196137_ex31-2.htm |

| EX-32.2 - United States Commodity Index Funds Trust | v196137_ex32-2.htm |

| EX-32.1 - United States Commodity Index Funds Trust | v196137_ex32-1.htm |

| EX-31.1 - United States Commodity Index Funds Trust | v196137_ex31-1.htm |

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

FORM

10-Q

|

x

|

Quarterly report pursuant to

Section 13 or 15(d) of the Securities Exchange Act of 1934 for the

quarterly period ended June 30,

2010.

|

OR

|

¨

|

Transition report pursuant to

Section 13 or 15(d) of the Securities Exchange Act of 1934 for the

transition period from

to

.

|

Commission

File Number: 001-34833

United

States Commodity Index Funds Trust

(Exact

name of registrant as specified in its charter)

|

Delaware

|

27-1537655

|

|

|

(State or other jurisdiction of

incorporation or organization)

|

(I.R.S. Employer

Identification No.)

|

1320

Harbor Bay Parkway, Suite 145

Alameda,

California 94502

(Address

of principal executive offices) (Zip code)

(510)

522-9600

(Registrant’s

telephone number, including area code)

N/A

(Former

name, former address and former fiscal year, if changed since last

report)

Indicate

by check mark whether the registrant (1) has filed all reports required to

be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934

during the preceding 12 months (or for such shorter period that the registrant

was required to file such reports), and (2) has been subject to such filing

requirements for the past 90 days.

x

Yes ¨ No

Indicate

by check mark whether the registrant has submitted electronically and posted on

its corporate Web site, if any, every Interactive Data File required to be

submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this

chapter) during the preceding 12 months (or for such shorter period that the

registrant was required to submit and post such files).

¨

Yes ¨ No

Indicate

by check mark whether the registrant is a large accelerated filer, an

accelerated filer, a non-accelerated filer, or a smaller reporting

company. See the definitions of “large accelerated filer,”

“accelerated filer” and “smaller reporting company” in Rule 12b-2 of the

Exchange Act.

|

Large accelerated filer ¨

|

Accelerated filer ¨

|

|

Non-accelerated filer x

|

Smaller reporting company ¨

|

|

(Do not check if a smaller reporting company)

|

Indicate

by check mark whether the registrant is a shell company (as defined in Rule

12b-2 of the Exchange Act).

¨

Yes x No

UNITED

STATES COMMODITY INDEX FUNDS TRUST

Table

of Contents

|

|

Page

|

|

|

Part

I. FINANCIAL INFORMATION

|

||

|

Item

1. Condensed Financial Statements.

|

1

|

|

|

Item

2. Management’s Discussion and Analysis of Financial Condition and Results

of Operations.

|

10

|

|

|

Item

3. Quantitative and Qualitative Disclosures About Market

Risk.

|

27

|

|

|

Item

4. Controls and Procedures.

|

28

|

|

|

Part

II. OTHER INFORMATION

|

||

|

Item

1. Legal Proceedings.

|

29

|

|

|

Item

1A. Risk Factors.

|

29

|

|

|

Item

2. Unregistered Sales of Equity Securities and Use of

Proceeds.

|

29

|

|

|

Item

3. Defaults Upon Senior Securities.

|

29

|

|

|

Item

4. Reserved.

|

29

|

|

|

Item

5. Other Information.

|

29

|

|

|

Item

6. Exhibits.

|

29

|

Part

I. FINANCIAL INFORMATION

Item 1. Condensed Financial

Statements.

United

States Commodity Index Funds Trust

Condensed

Statement of Financial Condition

At

June 30, 2010 (Unaudited)

|

United States

Commodity

Index Fund

|

Total

|

|||||||

|

Assets

|

||||||||

|

Cash

|

$ | 1,000 | $ | 1,000 | ||||

|

Capital

|

||||||||

|

Capital

|

$ | 1,000 | $ | 1,000 | ||||

See

accompanying notes to condensed statement of financial condition.

1

United

States Commodity Index Funds Trust

Notes

to Condensed Statement of Financial Condition

For

the period ended June 30, 2010 (Unaudited)

NOTE

1 - ORGANIZATION AND BUSINESS

The

United States Commodity Index Funds Trust (the “Trust”) was organized as a

Delaware statutory trust on December 21, 2009. The Trust is a series

trust formed pursuant to the Delaware Statutory Trust Act and includes the

United States Commodity Index Fund (“USCI”), which is a commodity pool that will

issue units (“units”) that may be purchased and sold on the NYSE Arca, Inc. (the

“NYSE Arca”). Additional series of the Trust that will be separate commodity

pools may be created in the future, but USCI is currently the Trust’s only

series. The Trust and USCI operate pursuant to the Amended and

Restated Declaration of Trust and Trust Agreement dated as of April 1, 2010 (the

“Trust Agreement”). United States Commodity Funds LLC (the “Sponsor”) is the

sponsor of the Trust and USCI and is also responsible for the management of the

Trust and USCI.

The

Sponsor shall have the power and authority to establish and designate one or

more series (“Funds”) and to issue units thereof, from time to time as it deems

necessary or desirable. The Sponsor shall have exclusive power to fix

and determine the relative rights and preferences as between the units of any

series as to right of redemption, special and relative rights as to dividends

and other distributions and on liquidation, conversion rights, and conditions

under which the series shall have separate voting rights or no voting rights.

The term for which the Trust is to exist shall commence on the date of the

filing of the Certificate of Trust, and the Trust and any Fund shall exist in

perpetuity, unless earlier terminated in accordance with the provisions of the

Trust Agreement. Separate and distinct records shall be maintained

for each Fund and the assets associated with a Fund shall be held in such

separate and distinct records (directly or indirectly, including a nominee or

otherwise) and accounted for in such separate and distinct records separately

from the assets of any other Fund. Each Fund shall be separate from

all other Funds created as series of the Trust in respect of the assets and

liabilities allocated to that Fund and shall represent a separate investment

portfolio of the Trust.

The sole

Trustee of the Trust is Wilmington Trust Company (the “Trustee”), a Delaware

banking corporation. The Trustee is unaffiliated with the

Sponsor. The Trustee’s duties and liabilities with respect to the

offering of units and the management of the Trust are limited to its express

obligations under the Trust Agreement.

The

Sponsor is a member of the National Futures Association (the

“NFA”) and became a commodity pool operator (“CPO”) registered with

the Commodity Futures Trading Commission (the “CFTC”) effective December 1,

2005. The Trust and USCI have a fiscal year ending on December

31.

The

Sponsor is the general partner of the United States Oil Fund, LP (“USOF”), the

United States Natural Gas Fund, LP (“USNG”), the United States 12 Month Oil

Fund, LP (“US12OF”), the United States Gasoline Fund, LP (“UGA”) and the United

States Heating Oil Fund, LP (“USHO”), which listed their limited partnership

units on the American Stock Exchange (the “AMEX”) under the ticker

symbols “USO” on April 10, 2006, “UNG” on April 18, 2007,

“USL” on December 6, 2007, “UGA” on February 26, 2008 and “UHN” on April 9,

2008, respectively. As a result of the acquisition of the AMEX by NYSE Euronext,

each of USOF’s, USNG’s, US12OF’s, UGA’s and USHO’s units commenced trading on

the NYSE Arca on November 25, 2008. The Sponsor is also the general partner of

the United States Short Oil Fund, LP (“USSO”), the United States 12 Month

Natural Gas Fund, LP (“US12NG”) and the United States Brent Oil Fund, LP

(“USBO”), which listed their limited partnership units on the NYSE Arca under

the ticker symbols “DNO” on September 24, 2009, “UNL” on November 18, 2009 and

“BNO” on June 2, 2010, respectively.

The

accompanying unaudited condensed statement of financial condition has been

prepared in accordance with Rule 10-01 of Regulation S-X promulgated by the U.S.

Securities and Exchange Commission (the “SEC”) and, therefore, does not

include all information and footnote disclosure required under accounting

principles generally accepted in the United States of America (“GAAP”).

The financial information included herein is unaudited; however, such financial

information reflects all adjustments which are, in the opinion of management,

necessary for the fair presentation of the condensed statement of financial

condition for the interim period.

2

USCI will

issue units to certain authorized purchasers (“Authorized Purchasers”) by

offering baskets consisting of 100,000 units (“Creation Baskets”) through

ALPS Distributors, Inc., as the marketing agent (the “Marketing Agent”).

The purchase price for a Creation Basket will be based upon the net asset value

of a unit calculated shortly after the close of the core trading session on

the NYSE Arca on the day the order to create the basket is properly

received.

In

addition, Authorized Purchasers will pay USCI a $1,000 fee for each order placed

to create one or more Creation Baskets or to redeem one or more baskets

consisting of 100,000 units (“Redemption Baskets”). Units may be purchased

or sold on a nationally recognized securities exchange in smaller increments

than a Creation Basket or Redemption Basket. Units purchased or sold on a

nationally recognized securities exchange will not be purchased or sold at the

net asset value of USCI but rather at market prices quoted on such

exchange.

NOTE

2 - SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Revenue

Recognition

Commodity

futures contracts, forward contracts, physical commodities, and related options

will be recorded on the trade date. All such transactions will be recorded on

the identified cost basis and marked to market daily. Unrealized gains or losses

on open contracts will be reflected in the condensed statement of financial

condition and represent the difference between the original contract amount and

the market value (as determined by exchange settlement prices for futures

contracts and related options and cash dealer prices at a predetermined time for

forward contracts, physical commodities, and their related options) as of the

last business day of the year or as of the last date of the condensed

financial statements. Changes in the unrealized gains or losses between periods

will be reflected in the condensed statement of operations. USCI will earn

interest on its assets denominated in U.S. dollars on deposit with the futures

commission merchant at the 90-day Treasury bill rate. In addition, USCI

will earn income on funds held at the custodian at prevailing market rates

earned on such investments.

Brokerage

Commissions

Brokerage

commissions on all open commodity futures contracts will be accrued on a

full-turn basis.

Income

Taxes

USCI will

not be subject to federal income taxes; each investor will report his/her

allocable share of income, gain, loss deductions or credits on his/her own

income tax return.

In

accordance with GAAP, USCI will be required to determine whether a tax position

is more likely than not to be sustained upon examination by the applicable

taxing authority, including resolution of any tax related appeals or litigation

processes, based on the technical merits of the position. USCI will file an

income tax return in the U.S. federal jurisdiction, and may file income tax

returns in various U.S. states. USCI will not be subject to income tax return

examinations by major taxing authorities for years before 2009 (year of

inception). The tax benefit recognized will be measured as the

largest amount of benefit that has a greater than fifty percent likelihood of

being realized upon ultimate settlement. De-recognition of a tax

benefit previously recognized will result in USCI recording a tax liability that

reduces net assets. However, USCI’s conclusions regarding this policy

may be subject to review and adjustment at a later date based on factors

including, but not limited to, on-going analyses of and changes to tax laws,

regulations and interpretations thereof. USCI will recognize interest accrued

related to unrecognized tax benefits and penalties related to unrecognized tax

benefits in income tax fees payable, if assessed. No interest expense

or penalties have been recognized as of and for the six months ended June 30,

2010.

Creations

and Redemptions

Authorized

Purchasers may purchase Creation Baskets or redeem Redemption Baskets only in

blocks of 100,000 units at a price equal to the net asset value of the units

calculated shortly after the close of the core trading session on the NYSE Arca

on the day the order is placed.

3

USCI will

receive or pay the proceeds from units sold or redeemed within three business

days after the trade date of the purchase or redemption. The amounts due from

Authorized Purchasers will be reflected in USCI’s condensed statement of

financial condition as receivable for units sold, and amounts payable to

Authorized Purchasers upon redemption will be reflected as payable for units

redeemed.

Trust

Capital and Allocation of Income and Losses

Profit or

loss shall be allocated among the unitholders of USCI in proportion to the

number of units each investor holds as of the close of each month. The Sponsor

may revise, alter or otherwise modify this method of allocation as described in

the Trust Agreement.

Calculation

of Net Asset Value

USCI’s

net asset value will be calculated on each NYSE Arca trading day by taking the

current market value of its total assets, subtracting any liabilities and

dividing the amount by the total number of units issued and

outstanding. USCI will use the closing prices on the relevant

Futures Exchanges (as defined in Note 3) of the Benchmark Component Futures

Contracts (determined at the earlier of the close of such exchange or 2:30 p.m.

New York time) for the contracts traded on the Futures Exchanges, but will

calculate or determine the value of all other USCI investments using market

quotations, if available, or other information customarily used to determine the

fair value of such investments.

Net

Income (Loss) per Unit

Net

income (loss) per unit is the difference between the net asset value per

unit at the beginning of each period and at the end of each period. The

weighted average number of units outstanding will be computed for purposes

of disclosing net income (loss) per weighted average unit. The weighted average

units will be equal to the number of units outstanding at the end of the period,

adjusted proportionately for units redeemed based on the amount of time the

units were outstanding during such period.

Offering

Costs

Offering

costs incurred in connection with the registration of additional units after the

initial registration of units will be borne by USCI. These costs will include

registration fees paid to regulatory agencies and all legal, accounting,

printing and other expenses associated with such offerings. These costs will be

accounted for as a deferred charge and thereafter amortized to expense over

twelve months on a straight-line basis or a shorter period if

warranted.

Cash

Equivalents

Cash

equivalents will include money market funds and overnight deposits or time

deposits with original maturity dates of three months or less.

Use

of Estimates

The

preparation of condensed financial statements in conformity with GAAP requires

USCI’s management to make estimates and assumptions that affect the reported

amount of assets and liabilities and disclosure of contingent assets and

liabilities at the date of the condensed financial statements, and the reported

amounts of the revenue and expenses during the reporting period. Actual results

could differ from those estimates and assumptions.

NOTE

3 - TRUST SERIES

In

connection with the execution of the Trust Agreement on April 1, 2010, USCI was

designated as the first series of the Trust. The Sponsor made the

initial contribution to USCI of $1,000.

USCI’s

trading advisor is SummerHaven Investment Management, LLC (“SummerHaven”), a

Delaware limited liability company that is registered as a commodity trading

advisor and CPO with the CFTC and is a member of the NFA. SummerHaven provides

advisory services to the Sponsor with respect to the SummerHaven Dynamic

Commodity Index Total Return (the “Index”) and the investment decisions of

USCI.

4

The

Trustee will accept service of legal process on the Trust in the State of

Delaware and will make certain filings under the Delaware Statutory Trust Act.

The Trustee does not owe any other duties to the Trust, the Sponsor or the

unitholders.

The

investment objective of USCI will be for the daily changes in percentage terms

of its units’ net asset value to reflect the daily changes in percentage terms

of the Index, less USCI’s expenses. USCI will accomplish its

objective through investments in futures contracts for commodities that are

traded on the New York Mercantile Exchange (the “NYMEX”), ICE Futures (“ICE

Futures”), Chicago Board of Trade (“CBOT”), Chicago Mercantile Exchange (“CME”),

London Metal Exchange (“LME”), Commodity Exchange, Inc. (“COMEX”) or on other

foreign exchanges (such exchanges, collectively, the “Futures Exchanges”) (such

futures contracts, collectively, “Futures Contracts”) and, to a lesser extent,

in order to comply with regulatory requirements or in view of market conditions,

other commodity-based contracts and instruments such as cash-settled options on

Futures Contracts, forward contracts relating to commodities, cleared swap

contracts and other over-the-counter transactions that are based on the price of

commodities and Futures Contracts (collectively, “Other Commodity-Related

Investments”). As of June 30, 2010, USCI did not hold any Futures

Contracts or Other Commodity-Related Investments since it had not yet commenced

operations.

As of

June 30, 2010, USCI had not registered any units.

NOTE 4

- FEES PAID BY THE FUND AND RELATED PARTY TRANSACTIONS

Sponsor

Management Fee

Under the

Trust Agreement, the Sponsor will be responsible for investing the assets of

USCI in accordance with the objectives and policies of USCI. In addition, the

Sponsor has arranged for one or more third parties to provide trading advisory,

administrative, custody, accounting, transfer agency and other necessary

services to USCI. For these services, USCI is contractually obligated to pay the

Sponsor a fee, which will be paid monthly, that will be equal to 0.95% per annum

of average daily net assets.

Trustee

Fee

The

Trustee is the Delaware trustee of the Trust. In connection with the

Trustee’s services, USCI will be responsible for paying the Trustee’s annual

fees in the amount of $6,000.

Ongoing

Registration Fees and Other Offering Expenses

USCI will

pay all costs and expenses associated with the ongoing registration of its units

subsequent to the initial offering. These costs will include

registration or other fees paid to regulatory agencies in connection with the

offer and sale of units, and all legal, accounting, printing and other expenses

associated with such offer and sale. For the six months ended

June 30, 2010, USCI did not incur any registration fees or other offering

expenses.

Investor

Tax Reporting Cost

The fees

and expenses associated with USCI’s audit expenses and tax accounting and

reporting requirements, with the exception of certain initial implementation

service fees and base service fees which will be borne by the Sponsor, will be

paid by USCI. These costs are estimated to be $200,000 for the

calendar year 2010.

Other

Expenses and Fees and Expense Waivers

In

addition to the fees described above, USCI will pay all brokerage fees and

other expenses in connection with the operation of USCI, excluding costs and

expenses paid by the Sponsor as outlined in Note 5. The Sponsor, though under no

obligation to do so, agreed to pay certain expenses, to the extent that such

expenses exceed 0.15% (15 basis points) of USCI’s NAV, on an annualized basis,

through December 31, 2010, after which such payments are no longer expected to

be necessary. The Sponsor has no obligation to continue such payment

into subsequent periods.

5

NOTE

5 - CONTRACTS AND AGREEMENTS

The

Sponsor and the Trust, on its own behalf and on behalf of USCI, are party to a

marketing agent agreement, dated as of July 22, 2010, as amended from time to

time, with the Marketing Agent, whereby the Marketing Agent will provide

certain marketing services for USCI as outlined in the agreement. The fee of the

Marketing Agent, which will be borne by the Sponsor, will be equal to 0.06% on

USCI’s assets up to $3 billion and 0.04% on USCI’s assets in excess of $3

billion.

The above

fee will not include the following expenses, which also will be borne by the

Sponsor: the cost of placing advertisements in various periodicals; web

construction and development; or the printing and production of various

marketing materials.

The

Sponsor and the Trust, on its own behalf and on behalf of USCI, are also party

to a custodian agreement, dated July 22, 2010, as amended from time to time,

with Brown Brothers Harriman & Co. (“BBH&Co.”), whereby BBH&Co. will

hold investments on behalf of USCI. The Sponsor will pay the

fees of the custodian, which will be determined by the parties from time to

time. In addition, the Sponsor and the Trust, on its own behalf and

on behalf of USCI, are party to an administrative agency agreement, dated July

22, 2010, as amended from time to time, with BBH&Co., whereby BBH&Co.

will act as the administrative agent, transfer agent and registrar for USCI. The

Sponsor will also pay the fees of BBH&Co. for its services under such

agreement and such fees will be determined by the parties from time to

time.

The

Sponsor will pay BBH&Co. for its services, in the foregoing capacities, a

minimum amount of $75,000 annually for its custody, fund accounting and fund

administration services rendered to USCI and each of the affiliated funds

managed by the Sponsor, as well as a $20,000 annual fee for its transfer agency

services. In addition, the Sponsor will pay BBH&Co. an asset-based charge of

(a) 0.06% for the first $500 million of USCI’s, USOF’s, USNG’s, US12OF’s, UGA’s,

USHO’s, USSO’s, US12NG’s and USBO’s combined net assets, (b) 0.0465% for USCI’s,

USOF’s, USNG’s, US12OF’s, UGA’s, USHO’s, USSO’s, US12NG’s and USBO’s combined

net assets greater than $500 million but less than $1 billion, and (c) 0.035%

once USCI’s, USOF’s, USNG’s, US12OF’s, UGA’s, USHO’s, USSO’s, US12NG’s and

USBO’s combined net assets exceed $1 billion. The annual minimum amount will not

apply if the asset-based charge for all accounts in the aggregate exceeds

$75,000. The Sponsor also will pay transaction fees ranging from $7.00 to $15.00

per transaction.

USCI has

entered into a brokerage agreement, dated March 1, 2010, as amended from time to

time, with Newedge USA, LLC (“Newedge”). The agreement requires

Newedge to provide services to USCI in connection with the purchase and sale of

Futures Contracts and Other Commodity-Related Investments that may be purchased

and sold by or through Newedge for USCI’s account. In accordance with the

agreement, Newedge will charge USCI commissions of approximately $7 per

round-turn trade, including applicable exchange and NFA fees for Futures

Contracts and options on Futures Contracts.

The

Sponsor is party to an advisory agreement, dated December 11, 2009, as amended

from time to time, with SummerHaven, whereby SummerHaven will provide advisory

services to the Sponsor with respect to the Index and investment decisions for

USCI. SummerHaven’s advisory services will include, but will not be

limited to, general consultation regarding the calculation and maintenance of

the Index, anticipated changes to the Index and the nature of the Index’s

current or anticipated component securities. For these services, the Sponsor

will pay SummerHaven a fee based on a percentage of the average daily assets of

USCI that will be equal to the percentage fees paid to the Sponsor by USCI minus

the greater of 0.1% or 0.1% plus the percentage fees paid by the Sponsor to the

Marketing Agent that exceed 0.02%, multiplied by 0.06%.

The

Sponsor is also party to a licensing agreement, dated December 11, 2009, as

amended from time to time, with SummerHaven whereby SummerHaven sub-licensed to

USCI the use of certain names and marks, including the Index, which SummerHaven

licensed from SummerHaven Index Management, LLC, the owner of the

Index. Under the licensing agreement, the Sponsor will pay

SummerHaven an annual fee of $30,000 for the calendar year 2010 and $15,000

annually in subsequent years, plus an annual fee of 0.06% of the average daily

assets of USCI.

6

NOTE

6 - FINANCIAL INSTRUMENTS, OFF-BALANCE SHEET RISKS AND

CONTINGENCIES

USCI intends

to engage in the trading of futures contracts and options on futures contracts

and may engage in cleared swaps (collectively, “derivatives”). USCI

will be exposed to both market risk, which is the risk arising from changes in

the market value of the contracts, and credit risk, which is the risk of failure

by another party to perform according to the terms of a contract.

USCI may

enter into Futures Contracts and options on Futures Contracts to gain exposure

to changes in the value of an underlying commodity. A futures contract obligates

the seller to deliver (and the purchaser to accept) the future delivery of a

specified quantity and type of a commodity at a specified time and place. Some

futures contracts may call for physical delivery of the asset, while others are

settled in cash. The contractual obligations of a buyer or seller may

generally be satisfied by taking or making physical delivery of the underlying

commodity or by making an offsetting sale or purchase of an identical Futures

Contract on the same or linked exchange before the designated date of

delivery.

The

purchase and sale of futures contracts and options on futures contracts require

margin deposits with a futures commission merchant. Additional deposits may be

necessary for any loss on contract value. The Commodity Exchange Act requires a

futures commission merchant to segregate all customer transactions and assets

from the futures commission merchant’s proprietary activities.

Futures

contracts involve, to varying degrees, elements of market risk (specifically

commodity price risk) and exposure to loss in excess of the amount of variation

margin. The face or contract amounts reflect the extent of the total exposure

USCI has in the particular classes of instruments. Additional risks associated

with the use of futures contracts are an imperfect correlation between movements

in the price of the futures contracts and the market value of the underlying

securities and the possibility of an illiquid market for a futures

contract.

Initially,

all of the Futures Contracts traded by USCI are expected to be

exchange-traded. The risks associated with exchange-traded contracts

are generally perceived to be less than those associated with over-the-counter

transactions since, in over-the-counter transactions, USCI must rely solely on

the credit of its respective individual counterparties. However, in

the future, if USCI were to enter into non-exchange traded contracts, it would

be subject to the credit risk associated with counterparty non-performance. The

credit risk from counterparty non-performance associated with such instruments

will be the net unrealized gain, if any. USCI will also incur credit

risk since the sole counterparty to all domestic and foreign futures

contracts is the clearinghouse for the exchange on which the relevant

contracts are traded. In addition, USCI bears the risk of financial

failure by the clearing broker.

USCI’s

cash and other property, such as U.S. Treasuries, deposited with a futures

commission merchant are considered commingled with all other customer funds,

subject to the futures commission merchant’s segregation requirements. In the

event of a futures commission merchant’s insolvency, recovery may be limited to

a pro rata share of segregated funds available. It is possible that the

recovered amount could be less than the total of cash and other property

deposited. The insolvency of a futures commission merchant could result in the

complete loss of USCI’s assets posted with that futures commission merchant;

however, the vast majority of USCI’s assets are expected to be held in U.S.

Treasuries, cash and/or cash equivalents with USCI’s custodian and would not be

impacted by the insolvency of a futures commission merchant. Also, the failure

or insolvency of USCI’s custodian could result in a substantial loss of USCI’s

assets.

The

Sponsor intends to invest a portion of USCI’s cash in money market funds that

seek to maintain a stable net asset value. USCI will be exposed to any risk of

loss associated with an investment in these money market funds.

For

derivatives, risks arise from changes in the market value of the contracts.

Theoretically, USCI will be exposed to a market risk equal to the value of

Futures Contracts purchased and unlimited liability on such contracts sold

short. As both a buyer and a seller of options, USCI pays or receives a premium

at the outset and then bears the risk of unfavorable changes in the price of the

contract underlying the option.

7

USCI’s

policy will be to continuously monitor its exposure to market and counterparty

risk through the use of a variety of financial, position and credit exposure

reporting controls and procedures. In addition, USCI has a policy of requiring

review of the credit standing of each broker or counterparty with which it

conducts business.

The

financial instruments that will be held by USCI will be reported

in its condensed statement of financial condition at market or fair

value, or at carrying amounts that approximate fair value, because of their

highly liquid nature and short-term maturity.

NOTE 7

– FAIR VALUE OF FINANCIAL INSTRUMENTS

USCI will

value its investments in accordance with Accounting Standards Codification 820 –

Fair Value Measurements and Disclosures (“ASC 820”). ASC 820 defines

fair value, establishes a framework for measuring fair value in generally

accepted accounting principles, and expands disclosures about fair value

measurement. The changes to past practice resulting from the application of ASC

820 relate to the definition of fair value, the methods used to measure fair

value, and the expanded disclosures about fair value measurement. ASC 820

establishes a fair value hierarchy that distinguishes between (1) market

participant assumptions developed based on market data obtained from sources

independent of USCI (observable inputs) and (2) USCI’s own assumptions about

market participant assumptions developed based on the best information available

under the circumstances (unobservable inputs). The three levels defined by the

ASC 820 hierarchy are as follows:

Level I –

Quoted prices (unadjusted) in active markets for identical assets or

liabilities that the reporting entity has the ability to access at the

measurement date.

Level II

– Inputs other than quoted prices included within Level I that are observable

for the asset or liability, either directly or indirectly. Level II assets

include the following: quoted prices for similar assets or liabilities

in active markets, quoted prices for identical or similar assets or liabilities

in markets that are not active, inputs other than quoted prices that are

observable for the asset or liability, and inputs that are derived principally

from or corroborated by observable market data by correlation or other means

(market-corroborated inputs).

Level III

– Unobservable pricing input at the measurement date for the asset or liability.

Unobservable inputs shall be used to measure fair value to the extent that

observable inputs are not available.

In some

instances, the inputs used to measure fair value might fall in different levels

of the fair value hierarchy. The level in the fair value hierarchy within which

the fair value measurement in its entirety falls shall be determined based on

the lowest input level that is significant to the fair value measurement in its

entirety.

NOTE

8 – RECENT ACCOUNTING PRONOUNCEMENTS

In

January 2010, the Financial Accounting Standards Board issued Accounting

Standards Update (“ASU”) No. 2010-06 “Improving

Disclosures about Fair Value Measurements.” ASU No. 2010-06 clarifies existing

disclosure and requires additional

disclosures regarding fair value measurements. Effective for fiscal years

beginning after

December 15, 2010, and for interim periods within those fiscal years, entities

will need to disclose information about purchases, sales,

issuances and settlements of Level 3 securities on a gross basis, rather than as

a net number as currently required. The

implementation of ASU No. 2010-06 will have no impact on USCI’s financial

statement disclosures.

NOTE

9 – SUBSEQUENT EVENTS

USCI has

performed an evaluation of subsequent events through the date the financial

statements were issued. This evaluation did not result in any subsequent events

that necessitated disclosures and/or adjustments except as set forth

below.

The

Sponsor contributed $1,000 to USCI upon its formation representing an initial

contribution of capital to USCI. In connection with the commencement

of USCI’s initial offering of units, the Sponsor received 20 Sponsor’s Units of

USCI in exchange for the previously received capital contribution, representing

a beneficial ownership interest in USCI.

8

On July

30, 2010, USCI received a notice of effectiveness from the SEC for its

registration of 50,000,000 units on Form S-1 with the SEC. On August

10, 2010, USCI listed its units on the NYSE Arca under the ticker symbol

“USCI”. USCI established its initial net asset value by setting the

price at $50.00 per unit and issued 100,000 units in exchange for $5,000,000 on

August 9, 2010. In order to satisfy NYSE Arca listing standards that

at least 100,000 units be outstanding at the beginning of the trading day on the

NYSE Arca, the Sponsor purchased the initial Creation Basket from the initial

Authorized Purchaser at the initial offering price. The $1,000 fee that would

otherwise be charged to the Authorized Purchaser in connection with an order to

create or redeem was waived in connection with the initial Creation

Basket. The Sponsor agreed not to resell the units comprising such

basket except that it may require the initial Authorized Purchaser to repurchase

all of these units at a per unit price equal to USCI’s per unit NAV within 5

days following written notice from the Sponsor, subject to the conditions that

(i) on the date of repurchase, the initial Authorized Purchaser must immediately

redeem these units in accordance with the terms of the Authorized Purchaser

Agreement and (ii) immediately following such redemption at least 100,000 units

of USCI remain outstanding. The Sponsor held such initial Creation Basket until

September 3, 2010, at which time the initial Authorized Purchaser repurchased

the units comprising such basket in accordance with the specified conditions

noted above.

USCI

commenced investment operations on August 9, 2010 by purchasing Futures

Contracts traded on the Futures Exchanges.

9

Item 2. Management’s

Discussion and Analysis of Financial Condition and Results of

Operations.

The

following discussion should be read in conjunction with the condensed statement

of financial condition and the notes thereto of the United States Commodity

Index Funds Trust (the “Trust”) included elsewhere in this quarterly report on

Form 10-Q.

Forward-Looking

Information

This

quarterly report on Form 10-Q, including this “Management’s Discussion and

Analysis of Financial Condition and Results of Operations,” contains

forward-looking statements regarding the plans and objectives of management for

future operations. This information may involve known and unknown risks,

uncertainties and other factors that may cause the Trust’s actual results,

performance or achievements to be materially different from future results,

performance or achievements expressed or implied by any forward-looking

statements. Forward-looking statements, which involve assumptions and describe

the Trust’s future plans, strategies and expectations, are generally

identifiable by use of the words “may,” “will,” “should,” “expect,”

“anticipate,” “estimate,” “believe,” “intend” or “project,” the negative of

these words, other variations on these words or comparable terminology. These

forward-looking statements are based on assumptions that may be incorrect, and

the Trust cannot assure investors that the projections included in these

forward-looking statements will come to pass. The Trust’s actual

results could differ materially from those expressed or implied by the

forward-looking statements as a result of various factors.

The Trust

has based the forward-looking statements included in this quarterly report on

Form 10-Q on information available to it on the date of this quarterly report on

Form 10-Q, and the Trust assumes no obligation to update any such

forward-looking statements. Although the Trust undertakes no obligation to

revise or update any forward-looking statements, whether as a result of new

information, future events or otherwise, investors are advised to consult any

additional disclosures that the Trust may make directly to them or through

reports that the Trust in the future files with the U.S. Securities and

Exchange Commission (the “SEC”), including annual reports on Form 10-K,

quarterly reports on Form 10-Q and current reports on Form 8-K.

Introduction

United

States Commodity Index Fund (“USCI”) is a commodity pool that will issue units

representing fractional undivided beneficial interests in USCI (“units”) that

may be purchased and sold on the NYSE Arca, Inc. (the “NYSE

Arca”). USCI is a series of the Trust, a Delaware statutory trust

formed on December 21, 2009. Additional series of the Trust that will be

separate commodity pools may be created in the future, but USCI is currently the

Trust’s only series. The Trust and USCI operate pursuant to the Trust’s Amended

and Restated Declaration of Trust and Trust Agreement (the “Trust Agreement”),

dated April 1, 2010. Wilmington Trust Company (the “Trustee”), a

Delaware banking corporation, is the Delaware trustee of the

Trust. USCI and the Trust are managed and controlled by United States

Commodity Funds LLC (the “Sponsor”).

USCI will

invest in futures contracts for commodities that are traded on the New York

Mercantile Exchange (the “NYMEX”), ICE Futures (“ICE Futures”), Chicago Board of

Trade (“CBOT”), Chicago Mercantile Exchange (“CME”), London Metal Exchange

(“LME”), Commodity Exchange, Inc. (“COMEX”) or on other foreign exchanges (such

exchanges, collectively, the “Futures Exchanges”) (such futures contracts,

collectively, “Futures Contracts”) and, to a lesser extent, in order to comply

with regulatory requirements or in view of market conditions, other

commodity-based contracts and instruments such as cash-settled options on

Futures Contracts, forward contracts relating to commodities, cleared swap

contracts and other over-the-counter transactions that are based on the price of

commodities and Futures Contracts (collectively, “Other Commodity-Related

Investments”). Market conditions that the Sponsor currently anticipates could

cause USCI to invest in Other Commodity Related Investments would be those

allowing USCI to obtain greater liquidity or to execute transactions with more

favorable pricing. Futures Contracts and Other Commodity-Related Investments

collectively are referred to as “Commodity Interests” in this quarterly report

on Form 10-Q.

10

The

investment objective of USCI will be for the daily changes in percentage terms

of its units’ net asset value (“NAV”) to reflect the daily changes in percentage

terms of the SummerHaven Dynamic Commodity Index Total Return (the “Index”),

less USCI’s expenses. The Index is comprised of 14 Futures Contracts

that will be selected on a monthly basis from a list of 27 possible Futures

Contracts. The Futures Contracts that at any given time make up the Index are

referred to herein as “Benchmark Component Futures Contracts.” USCI

anticipates that to meet its investment objective it will invest first, in the

current Benchmark Component Futures Contracts and other Futures Contracts

intended to replicate the return on the current Benchmark Component Futures

Contracts and, thereafter, to comply with regulatory requirements or in view of

market conditions, in Other Commodity-Related Investments intended to replicate

the return on the Benchmark Component Futures Contracts, including cleared swap

contracts and other over-the-counter transactions, and in other Futures

Contracts.

USCI will

seek to achieve its investment objective by investing in Futures Contracts and

Other Commodity-Related Investments such that daily changes in its NAV will

closely track the daily changes in the price of the Index. USCI’s

positions in Commodity Interests will be rebalanced on a monthly basis in order

to track the changing nature of the Index. If Futures Contracts

relating to a particular commodity remain in the Index from one month to the

next, such Futures Contracts will be rebalanced to the 7.14% target

weight. Specifically, on a specified day near the end of each month

(the “Selection Date”), it will be determined if a current Benchmark Component

Futures Contract will be replaced by a new Futures Contract in either the same

or different underlying commodity as a Benchmark Component Futures Contract for

the following month, in which case USCI’s investments would have to be changed

accordingly. In order that USCI’s trading does not unduly cause

extraordinary market movements, and to make it more difficult for third parties

to profit by trading based on market movements that could be expected from

changes in the Benchmark Component Futures Contracts, USCI’s investments

typically will not be rebalanced entirely on a single day, but rather will

typically be rebalanced over a period of four days. After fulfilling the margin

and collateral requirements with respect to its Commodity Interests, the Sponsor

will invest the remainder of USCI’s proceeds from the sale of units in

short-term obligations of the United States government (“Treasuries”) or cash

equivalents, and/or merely hold such assets in cash (generally in

interest-bearing accounts).

The

regulation of commodity interests in the United States is a rapidly changing

area of law and is subject to ongoing modification by governmental and judicial

action. As stated under the heading, “Risk Factors” in USCI’s

Registration Statement on Form S-1, regulation of commodity interests and energy

markets is extensive and constantly changing; future regulatory developments in

commodity interests and energy markets are impossible to predict but may

significantly and adversely affect USCI.

On July

21, 2010, a broad financial regulatory reform bill, “The Dodd-Frank Wall Street

Reform and Consumer Protection Act,” was signed into law that includes

provisions altering the regulation of commodity interests. Provisions

in the new law include the requirement that position limits on energy-based

commodity futures contracts be established; new registration, recordkeeping,

capital and margin requirements for “swap dealers” and “major swap participants”

as determined by the new law and applicable regulations; and the forced use of

clearinghouse mechanisms for most over-the-counter transactions. Additionally,

the new law requires the aggregation, for purposes of position limits, of all

positions in energy futures held by a single entity and its affiliates, whether

such positions exist on U.S. futures exchanges, non-U.S. futures exchanges, or

in over-the-counter contracts. The U.S. Commodity Futures Trading Commission

(the “CFTC”), along with the SEC and other federal regulators, has been tasked

with developing the rules and regulations enacting the provisions noted

above. The new law and the rules to be promulgated may negatively

impact USCI’s ability to meet its investment objective either through limits or

requirements imposed on it or upon its counterparties. In particular,

new position limits imposed on USCI or its counterparties may impact USCI’s

ability to invest in a manner that most efficiently meets its investment

objective, and new requirements, including capital and mandatory clearing, may

increase the cost of USCI’s investments and doing business, which could

adversely affect USCI’s investors.

The

Sponsor is a limited liability company formed in Delaware on May 10, 2005, that

is registered as a commodity pool operator (“CPO”) with the CFTC and is a member

of the National Futures Association (the “NFA”). USCI’s trading advisor is

SummerHaven Investment Management, LLC (“SummerHaven”), a Delaware limited

liability company that is registered as a commodity trading advisor and CPO with

the CFTC and is a member of the NFA. The Sponsor manages USCI’s

investments directly, using the trading advisory services of SummerHaven for

guidance with respect to the Index and the Sponsor’s selection of investments on

behalf of USCI. The Sponsor is also authorized to select futures

commission merchants to execute USCI’s transactions in Futures Contracts and

Other Commodity-Related Investments.

11

Price

Movements

Commodity

futures prices exhibited moderate daily swings along with an uneven upward trend

during the six months ended June 30, 2010. The price of the Index

started the period at $1,532.841. The period ended with the Index at

$1,355.159, down approximately 11.591% over the period. The return of

approximately -11.591% on the Index listed above is a hypothetical return only

and could not actually be achieved by an investor holding Futures

Contracts. An investment in Futures Contracts would need to be rolled

forward during the time period described in order to achieve such a

result. Furthermore, the change in the nominal price of the differing

commodity Futures Contracts, measured from the start of the period to the end of

the period, does not represent the actual benchmark results that USCI seeks to

track, which are more fully described below, in the section titled “Tracking the

Index”.

Valuation

of Futures Contracts and the Computation of the NAV

The NAV

of USCI’s units will be calculated once each NYSE Arca trading

day. The NAV for a particular trading day will be released after 4:00

p.m. New York time. Trading during the core trading session on the

NYSE Arca typically closes at 4:00 p.m. New York time. USCI’s administrator will

use the closing prices on the relevant Futures Exchanges of the Benchmark

Component Futures Contracts (determined at the earlier of the close of such

exchange or 2:30 p.m. New York time) for the contracts held on the Futures

Exchanges, but will calculate or determine the value of all other USCI

investments using market quotations, if available, or other information

customarily used to determine the fair value of such investments.

Results

of Operations and the Commodity Markets

Results of

Operations. During the six months ended June

30, 2010, USCI had not yet commenced investment activities nor issued

units. In addition, USCI did not purchase or own any Futures

Contracts or Other Commodity-Related Investments during the six months ended

June 30, 2010, nor were there any receipts or disbursements of cash from USCI

during this reporting period. Also, USCI did not receive any revenue

or capital gains (losses), or incur any expenses during this reporting

period.

Expenses

incurred during the six months ended June 30, 2010 in connection with organizing

USCI and the initial offering costs of the units were borne by the Sponsor, and

are not subject to reimbursement by USCI.

Portfolio Expenses. USCI’s

expenses will consist of investment management fees, brokerage

fees and commissions, certain offering costs and expenses relating to tax

accounting and reporting requirements. The management fee that USCI

will pay to the Sponsor will be calculated as a percentage of the total net

assets of USCI. USCI will pay the Sponsor a management fee of 0.95%

of its average net assets. The fee will be accrued daily and paid

monthly.

In

addition to the management fee, USCI will pay all brokerage fees and other

expenses, including certain tax reporting costs, ongoing registration or other

fees paid to the SEC, the Financial Industry Regulatory Authority (“FINRA”)

and any other regulatory agency in connection with offers and sales of

its units subsequent to the initial offering and all legal, accounting, printing

and other expenses associated therewith.

USCI will

incur commissions to brokers for the purchase and sale of Futures Contracts,

Other Commodity-Related Investments or Treasuries.

The fees

and expenses associated with USCI’s audit expenses and tax accounting and

reporting requirements, with the exception of certain initial implementation

service fees and base service fees which will be borne by the Sponsor, will be

paid by USCI. These costs are estimated to be $200,000 for the

calendar year 2010. The Sponsor, though under no obligation to do so,

agreed to pay certain expenses, to the extent that such expenses exceed 0.15%

(15 basis points) of USCI’s NAV, on an annualized basis, through December 31,

2010, after which date such payments are no longer expected to be

necessary. The Sponsor has no obligation to continue such payment

into subsequent periods.

12

Dividend and Interest

Income. USCI will seek to invest its assets such that it

holds Futures Contracts and Other Commodity-Related Investments in an

amount equal to the total net assets of its portfolio. Typically, such

investments will not require USCI to pay the full amount of the contract value

at the time of purchase, but rather require USCI to post an amount as a margin

deposit against the eventual settlement of the contract. As a result, USCI will

retain an amount that is approximately equal to its total net assets, which USCI

will invest in Treasuries, cash and/or cash equivalents. This will include

both the amount on deposit with the futures commission merchant as margin, as

well as unrestricted cash and cash equivalents held with USCI’s custodian bank.

The Treasuries, cash and/or cash equivalents will earn income that accrues on a

daily basis.

Tracking

the Index

USCI’s

management will seek to manage USCI’s portfolio such that changes in its average

daily NAV, on a percentage basis, closely track the changes in the price of the

Index, also on a percentage basis. Specifically, USCI’s management will seek to

manage the portfolio such that over any rolling period of 30 valuation days, the

average daily change in USCI’s NAV is within a range of 90% to 110% (0.9 to 1.1)

of the average daily change in the price of the Index. As an example,

if the average daily movement of the price of the Index for a particular

30-valuation day time period was 0.5% per day, USCI management would attempt to

manage the portfolio such that the average daily movement of the NAV during that

same time period fell between 0.45% and 0.55% (i.e., between 0.9 and 1.1 of

the Index’s results). USCI’s portfolio management goals do not include trying to

make the nominal price of USCI’s NAV equal to the nominal price of the Index,

the nominal price of any particular commodity Futures Contract or the spot price

for any particular commodity. Management believes that it is not

practical to manage the portfolio to achieve such an investment goal when

investing in listed Futures Contracts.

An

alternative tracking measurement of the return performance of USCI versus the

return of the Index can be calculated by comparing the actual return of USCI,

measured by changes in its NAV, versus the expected changes in its NAV

under the assumption that USCI’s returns had been exactly the same as the daily

changes in the price of the Index.

There are

currently three factors that have impacted or are most likely to impact USCI’s

ability to accurately track the Index.

First,

USCI may buy or sell its holdings in the then current Benchmark Component

Futures Contracts at a price other than the closing settlement price of that

contract on the day during which USCI executes the trade. In that case, USCI may

pay a price that is higher, or lower, than that of the Benchmark Component

Futures Contracts, which could cause the changes in the daily NAV of USCI

to either be too high or too low relative to the changes in the price of the

Index. Management will attempt to minimize the effect of these

transactions by seeking to execute its purchase or sale of the Benchmark

Component Futures Contracts at, or as close as possible to, the end of the day

settlement price. However, it may not always be possible for USCI to obtain the

closing settlement price and there is no assurance that failure to obtain the

closing settlement price in the future will not adversely impact USCI’s attempt

to track the Index over time.

Second,

USCI will earn dividend and interest income on its cash, cash equivalents and

Treasury holdings. USCI is not required to distribute any portion of its income

to its unitholders. Interest payments, and any other income, will be retained

within the portfolio and added to USCI’s NAV. At the same time, USCI will incur

expenses for its management fee, brokerage commissions and other expenses

(including ongoing registration). The calculation of the Index includes an

interest portion, calculated daily using the 90 Day U.S. Treasury Bill's total

return, but does not include an expense component. When USCI's income

exceeds the level of USCI’s expenses by more than the yield on the 90 Day U.S.

Treasury Bill, USCI will realize a net yield that will tend to cause daily

changes in the NAV of USCI to track slightly higher than daily changes in the

price of the Index. If this net yield is lower than the yield on the 90 Day U.S.

Treasury Bill, that will tend to cause daily changes in the NAV of USCI to track

slightly lower than daily changes in the price of the

Index.

Third,

USCI may hold Other Commodity-Related Investments in its portfolio that may

fail to closely track the Index’s total return movements. In that

case, the error in tracking the Index could result in daily changes in the NAV

of USCI that are either too high, or too low, relative to the daily changes in

the price of the Index.

13

The

Index

The Index

was developed based upon academic research by Yale University professors Gary B.

Gorton and K. Geert Rouwenhorst, and Hitotsubashi University professor Fumio

Hayashi. The Index is designed to reflect the performance of a fully margined or

collateralized portfolio of 14 commodity futures contracts with equal weights,

selected each month from a universe of 27 eligible commodity futures contracts.

The Index is rules-based and rebalanced monthly based on observable price

signals. In this context, the term “rules-based” is meant to indicate that the

composition of the Index in any given month will be determined by quantitative

formulas relating to the prices of the futures contracts that relate to the

commodities that are eligible to be included in the Index. Such formulas are not

subject to adjustment based on other factors. The overall return on the Index is

generated by two components: (i) uncollateralized returns from the commodity

futures contracts comprising the Index and (ii) a daily fixed income return

reflecting the interest earned on a hypothetical 3-month U.S. Treasury Bill

collateral portfolio, calculated using the weekly auction rate for the 3-Month

U.S. Treasury Bills published by the U.S. Department of the

Treasury. SummerHaven Index Management, LLC (“SummerHaven Indexing”)

is the owner of the Index.

The Index

is composed of physical non-financial commodity futures contracts with active

and liquid markets traded upon futures exchanges in major industrialized

countries. The futures contracts are denominated in U.S. dollars and weighted

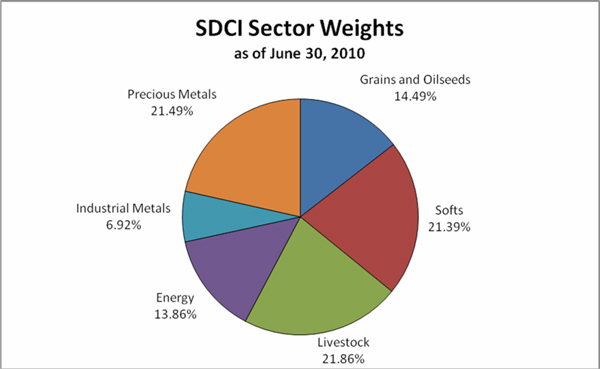

equally by notional amount. The Index currently reflects commodities in six

commodity sectors: energy (e.g., crude oil, natural gas,

heating oil, etc.), precious metals (e.g., gold, silver platinum),

industrial metals (e.g., zinc, nickel, aluminum,

copper, etc.), grains (e.g., wheat, corn, soybeans,

etc.), softs (e.g.,

sugar, cotton, coffee, cocoa), and livestock (e.g., live cattle, lean hogs,

feeder cattle).

Table 1

below lists the eligible commodities, the relevant futures exchange on which the

futures contract is listed and quotation details. Table 2 lists the eligible

futures contracts, their sector designation and maximum allowable

tenor.

TABLE

1

|

Commodity

|

Designated Contract

|

Exchange

|

Units

|

Quote

|

||||

|

Crude

Oil (Brent)

|

Crude

Oil

|

ICE-UK

|

1,000

barrels

|

USD/barrel

|

||||

|

Crude

Oil (WTI)

|

Light,

Sweet Crude Oil

|

NYMEX

|

1,000

barrels

|

USD/barrel

|

||||

|

Gas

Oil

|

Gas

Oil

|

ICE-UK

|

100

metric tons

|

USD/metric

ton

|

||||

|

Heating

Oil

|

Heating

Oil

|

NYMEX

|

42,000

gallons

|

U.S.

cents/gallon

|

||||

|

Natural

Gas

|

Henry

Hub Natural Gas

|

NYMEX

|

10,000

mmbtu

|

USD/mmbtu

|

||||

|

Unleaded

Gasoline

|

Reformulated

Blendstock for Oxygen Blending “RBOB”

|

NYMEX

|

42,000

gallons

|

U.S.

cents/gallon

|

||||

|

Feeder

Cattle

|

Feeder

Cattle

|

CME

|

50,000

lbs.

|

U.S.

cents/pound

|

||||

|

Lean

Hogs

|

Lean

Hogs

|

CME

|

40,000

lbs.

|

U.S.

cents/pound

|

||||

|

Live

Cattle

|

Live

Cattle

|

CME

|

40,000

lbs.

|

U.S.

cents/pound

|

||||

|

Bean

Oil

|

Bean

Oil

|

CBOT

|

60,000

lbs.

|

U.S.

cents/pound

|

||||

|

Corn

|

Corn

|

CBOT

|

5,000

bushels

|

U.S.

cents/bushel

|

||||

|

Soybeans

|

Soybeans

|

CBOT

|

5,000

bushels

|

U.S.

cents/bushel

|

||||

|

Soybean

Meal

|

Soybean

Meal

|

CBOT

|

100

tons

|

USD/ton

|

||||

|

Wheat

|

Wheat

|

CBOT

|

5,000

bushels

|

U.S.

cents/bushel

|

||||

|

Aluminum

|

High

Grade Primary Aluminum

|

LME

|

25

metric tons

|

USD/metric

ton

|

||||

|

Copper

|

Copper

|

COMEX

|

25,000

lbs

|

U.S.

cents/pound

|

||||

|

Lead

|

Lead

|

LME

|

25

metric tons

|

USD/metric

ton

|

||||

|

Nickel

|

Primary

Nickel

|

LME

|

6

metric tons

|

USD/metric

ton

|

||||

|

Tin

|

Tin

|

LME

|

5

metric tons

|

USD/metric

ton

|

||||

|

Zinc

|

Special

High Grade Zinc

|

LME

|

25

metric tons

|

USD/metric

ton

|

||||

|

Gold

|

Gold

|

COMEX

|

100

troy oz.

|

USD/troy

oz.

|

||||

|

Platinum

|

Platinum

|

NYMEX

|

50

troy oz.

|

USD/troy

oz.

|

||||

|

Silver

|

Silver

|

COMEX

|

5,000

troy oz.

|

U.S.

cents/troy oz.

|

||||

|

Cocoa

|

Cocoa

|

ICE-US

|

10

metric tons

|

USD/metric

ton

|

||||

|

Coffee

|

Coffee

“C”

|

ICE-US

|

37,500

lbs

|

U.S.

cents/pound

|

||||

|

Cotton

|

Cotton

|

ICE-US

|

50,000

lbs

|

U.S.

cents/pound

|

||||

|

Sugar

|

World

Sugar No. 11

|

ICE-US

|

112,000

lbs.

|

U.S.

cents/pound

|

14

TABLE

2

|

Commodity Symbol

|

Commodity

Name

|

Sector

|

Allowed Contracts

|

Max.

tenor

|

||||

|

CO

|

Brent

Crude

|

Energy

|

All

12 Calendar Months

|

12

|

||||

|

CL

|

Crude

Oil

|

Energy

|

All

12 Calendar Months

|

12

|

||||

|

QS

|

Gas

Oil

|

Energy

|

All

12 Calendar Months

|

12

|

||||

|

HO

|

Heating

Oil

|

Energy

|

All

12 Calendar Months

|

12

|

||||

|

NG

|

Natural

Gas

|

Energy

|

All

12 Calendar Months

|

12

|

||||

|

XB

|

RBOB

|

Energy

|

All

12 Calendar Months

|

12

|

||||

|

FC

|

Feeder

Cattle

|

Livestock

|

Jan,

Mar, Apr, May, Aug, Sep, Oct, Nov

|

5

|

||||

|

LH

|

Lean

Hogs

|

Livestock

|

Feb,

Apr, Jun, Jul, Aug, Oct, Dec

|

5

|

||||

|

LC

|

Live

Cattle

|

Livestock

|

Feb,

Apr, Jun, Aug, Oct, Dec

|

5

|

||||

|

BO

|

Bean

Oil

|

Grains

|

Jan,

Mar, May, Jul, Aug, Sep, Oct, Dec

|

7

|

||||

|

C

|

Corn

|

Grains

|

Mar,

May, Jul, Sep, Dec

|

12

|

||||

|

S

|

Soybeans

|

Grains

|

Jan,

Mar, May, Jul, Aug, Sep, Nov

|

12

|

||||

|

SM

|

Soymeal

|

Grains

|

Jan,

Mar, May, Jul, Aug, Sep, Oct, Dec

|

7

|

||||

|

W

|

Wheat

|

Grains

|

Mar,

May, Jul, Sep, Dec

|

7

|

||||

|

LA

|

Aluminum

|

Industrial

Metals

|

All

12 Calendar months

|

12

|

||||

|

HG

|

Copper

|

Industrial

Metals

|

All

12 Calendar Months

|

12

|

||||

|

LL

|

Lead

|

Industrial

Metals

|

All

12 Calendar Months

|

7

|

||||

|

LN

|

Nickel

|

Industrial

Metals

|

All

12 Calendar Months

|

7

|

||||

|

LT

|

Tin

|

Industrial

Metals

|

All

12 Calendar Months

|

7

|

||||

|

LX

|

Zinc

|

Industrial

Metals

|

All

12 Calendar Months

|

7

|

||||

|

GC

|

Gold

|

Precious

Metals

|

Feb,

Apr, Jun, Aug, Oct, Dec

|

12

|

||||

|

PL

|

Platinum

|

Precious

Metals

|

Jan,

Apr, Jul, Oct

|

5

|

||||

|

SI

|

Silver

|

Precious

Metals

|

Mar,

May, Jul, Sep, Dec

|

5

|

||||

|

CC

|

Cocoa

|

Softs

|

Mar,

May, Jul, Sep, Dec

|

7

|

||||

|

KC

|

Coffee

|

Softs

|

Mar,

May, Jul, Sep, Dec

|

7

|

||||

|

CT

|

Cotton

|

Softs

|

Mar,

May, Jul, Dec

|

7

|

||||

|

SB

|

Sugar

|

Softs

|

Mar,

May, Jul, Oct

|

7

|

15

Prior to

the end of each month, SummerHaven Indexing determines the composition of the

Index and provides such information to Bloomberg, L.P.

(“Bloomberg”). Values of the Index are computed by Bloomberg and

disseminated approximately every fifteen (15) seconds from 8:00 a.m. to 5:00

p.m., New York City time, which also publishes a daily Commodity Index value at

approximately 5:30 p.m., New York City time, under the index ticker symbol

“SDCITR:IND”. Only settlement and last-sale prices are used in the Index’s

calculation, bids and offers are not recognized — including limit-bid

and limit-offer price quotes. Where no last-sale price exists, typically in the

more deferred contract months, the previous days’ settlement price is used. This

means that the underlying Index may lag its theoretical value. This tendency to

lag is evident at the end of the day when the Index value is based on the

settlement prices of the component commodities, and explains why the underlying

Index often closes at or near the high or low for the day.

Composition

of the Index

The

composition of the Index on any given day, as determined and published by

SummerHaven Indexing, is determinative of the benchmark for

USCI. Neither the Summerhaven Dynamic Commodity Index (“SDCI”) index

methodology nor any set of procedures, however, are capable of anticipating all

possible circumstances and events that may occur with respect to the Index and

the methodology for its composition, weighting and calculation. Accordingly, a

number of subjective judgments must be made in connection with the operation of

the Index that cannot be adequately reflected in this description of the Index.

All questions of interpretation with respect to the application of the

provisions of the SDCI index methodology, including any determinations that need

to be made in the event of a market emergency or other extraordinary

circumstances, will be resolved by SummerHaven Indexing.

Contract

Expirations

Because

the Index is comprised of actively traded contracts with scheduled expirations,

it can be calculated only by reference to the prices of contracts for specified

expiration, delivery or settlement periods, referred to as contract expirations.

The contract expirations included in the Index for each commodity during a given

year are designated by SummerHaven Indexing, provided that each contract must be

an active contract. An active contract for this purpose is a liquid,

actively-traded contract expiration, as defined or identified by the relevant

trading facility or, if no such definition or identification is provided by the

relevant trading facility, as defined by standard custom and practice in the

industry.

If a

trading facility ceases trading in all contract expirations relating to a

particular contract, SummerHaven Indexing may designate a replacement contract

on the commodity. The replacement contract must satisfy the eligibility criteria

for inclusion in the Index. To the extent practicable, the replacement will be

effected during the next monthly review of the composition of the Index. If that

timing is not practicable, SummerHaven Indexing will determine the date of the

replacement based on a number of factors, including the differences between the

existing contract and the replacement contract with respect to contractual

specifications and contract expirations.

16

If a

contract is eliminated and there is no replacement contract, the underlying

commodity will necessarily drop out of the Index. The designation of a

replacement contract, or the elimination of a commodity from the Index because

of the absence of a replacement contract, could affect the value of the Index,

either positively or negatively, depending on the price of the contract that is

eliminated and the prices of the remaining contracts. It is impossible, however,

to predict the effect of these changes, if they occur, on the value of the

Index.

Commodity

Selection

14 of the

27 eligible commodities are selected for inclusion in the Index for the next

month, subject to the constraint that each of the six commodity sectors is

represented by at least one commodity. The methodology used to select the 14

commodities is based solely on quantitative data using observable futures prices

and is not subject to human bias.

Monthly

commodity selection is a two-step process based upon examination of the relevant

futures prices for each commodity:

|

|

1)

|

The

annualized percentage price difference between the closest-to-expiration

futures contract and the next closest-to-expiration futures contract is

calculated for each of the 27 eligible commodities on the Selection Date.

The seven commodities with the highest percentage price difference are

selected. A hypothetical example is included below, with the seven

selected commodities shaded below (the selected commodities are ranked

1 – 7):

|

|

Eligible

Commodity

|

Percentage

Price

Difference

|

Ranking

|

||||||

|

Crude

Oil (Brent)

|

-4.75

|

%

|

13

|

|||||

|

Crude

Oil (WTI)

|

-5.01

|

%

|

14

|

|||||

|

Gas

Oil

|

20.78

|

%

|

1

|

|||||

|

Heating

Oil

|

-7.87

|

%

|

21

|

|||||

|

Natural

Gas

|

-19.92

|

%

|

25

|

|||||

|

Unleaded

Gasoline (RBOB)

|

1.27

|

%

|

5

|

|||||

|

Feeder

Cattle

|

-27.42

|

%

|

27

|

|||||

|

Lean

Hogs

|

-20.68

|

%

|

26

|

|||||

|

Live

Cattle

|

14.31

|

%

|

3

|

|||||

|

Bean

Oil

|

-6.70

|

%

|

20

|

|||||

|

Corn

|

-17.58

|

%