Attached files

| file | filename |

|---|---|

| EX-5.1 - EXHIBIT 5.1 - ATLANTIC POWER CORP | a2199864zex-5_1.htm |

| EX-23.6 - EXHIBIT 23.6 - ATLANTIC POWER CORP | a2199864zex-23_6.htm |

| EX-23.3 - EXHIBIT 23.3 - ATLANTIC POWER CORP | a2199864zex-23_3.htm |

| EX-23.4 - EXHIBIT 23.4 - ATLANTIC POWER CORP | a2199864zex-23_4.htm |

| EX-23.5 - EXHIBIT 23.5 - ATLANTIC POWER CORP | a2199864zex-23_5.htm |

| EX-23.2 - EXHIBIT 23.2 - ATLANTIC POWER CORP | a2199864zex-23_2.htm |

Use these links to rapidly review the document

TABLE OF CONTENTS

Atlantic Power Corporation Index to Consolidated Financial Statements

As filed with the Securities and Exchange Commission on August 13, 2010

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM S-1

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

ATLANTIC POWER CORPORATION

(Exact Name of Registrant as Specified in Its Charter)

| British Columbia, Canada (State or Other Jurisdiction of Incorporation or Organization) |

4900 (Primary Standard Industrial Classification Code Number) |

55-0886410 (I.R.S. Employer Identification Number) |

200 Clarendon St., Floor 25

Boston, Massachusetts 02116

(617) 977-2400

(Address, Including Zip Code, and Telephone Number, Including

Area Code, of Registrant's Principal Executive Offices)

Barry E. Welch

President and Chief Executive Officer

Atlantic Power Corporation

200 Clarendon St., Floor 25

Boston, Massachusetts 02116

(617) 977-2400

(Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent For Service)

| Copies to: | ||

| Laura Hodges Taylor, Esq. Yoel Kranz, Esq. Goodwin Procter LLP Exchange Place Boston, Massachusetts 02109 (617) 570-1000 |

Christopher J. Cummings, Esq. Shearman & Sterling LLP Commerce Court West, Suite 4405 Toronto, Ontario Canada M5L 1E8 (416) 360-8484 |

|

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box: o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definition of "larger accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer ý (Do not check if a smaller reporting company) |

Smaller reporting company o |

CALCULATION OF REGISTRATION FEE

|

||||

| Title of Securities to be Registered |

Proposed Maximum Aggregate Offering Price(1)(2) |

Amount of Registration Fee |

||

|---|---|---|---|---|

Common Shares, no par value |

$69,000,000.00 | $4,919.70 | ||

|

||||

- (1)

- Estimated

solely for the purpose of calculating the registration fee pursuant to Rule 457(o) under the Securities Act of 1933, as amended.

- (2)

- Includes the offering price of the common shares that may be purchased by the underwriters pursuant to their option to purchase additional common shares.

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until this registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and we are not soliciting offers to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to Completion

| |

|

|

|---|---|---|

| PRELIMINARY PROSPECTUS | August 13, 2010 |

Shares

Common Shares

We are offering common shares, no par value per share.

Our common shares are listed on the New York Stock Exchange under the symbol "AT" and on the Toronto Stock Exchange under the symbol "ATP." On August 12, 2010, the last reported sale price of our common shares on the New York Stock Exchange and the Toronto Stock Exchange was $12.69 and Cdn$13.25, respectively, per share.

Investing in our common shares involves a high degree of risk. Before buying any shares you should carefully read the discussion of material risks of investing in our common shares under the heading "Risk Factors" beginning on page 10 of this prospectus.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

|

||||

| |

Per Share |

Total |

||

|---|---|---|---|---|

Public offering price |

$ | $ | ||

Underwriting discounts and commissions |

$ | $ | ||

Proceeds, before expenses, to us |

$ | $ | ||

|

||||

The underwriters may also purchase up to an additional common shares from us at the public offering price, less the underwriting discounts and commissions payable by us to cover over-allotments, if any, within 30 days from the date of this prospectus.

The underwriters are offering the common shares as set forth under "Underwriting." Delivery of the common shares will be made on or about , 2010.

Sole Book-Running Manager

UBS Investment Bank

The date of this prospectus is , 2010

You should rely only on information contained in this document or to which we have referred you. We have not, and our underwriters have not, authorized anyone to provide any information or to make any representations other than those contained in this prospectus or in any free writing prospectuses we have prepared. If anyone provides you with different or inconsistent information, you should not rely on it. We take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. We are not, and the underwriters are not, making an offer to sell the securities in any jurisdiction where the offer or sale is not permitted. This document may only be used where it is legal to sell these securities. The information contained in this prospectus may only be accurate as of the date on the cover of this prospectus. Our business, financial condition and results of operations may have changed since that date.

As used in this prospectus, the terms "Atlantic Power," the "Company," "we," "our," and "us" refer to Atlantic Power Corporation, together with those entities owned or controlled by Atlantic Power Corporation, unless the context indicates otherwise. All references to "Cdn$" and "Canadian dollars" are to the lawful currency of Canada and references to "$," "US$" and "U.S. dollars" are to the lawful currency of the United States. All dollar amounts herein are in U.S. dollars, unless otherwise indicated. This prospectus includes our trademarks and other trade names identified herein. All other trademarks and trade names appearing in this prospectus are the property of their respective holders.

i

The following summary may not contain all the information that may be important to you or that you should consider before deciding to purchase any common shares and is qualified in its entirety by the more detailed information appearing elsewhere in this prospectus. You should read the entire prospectus, especially the risks set forth under the heading "Risk Factors" in this prospectus, as well as the financial and other information included herein, before making an investment decision.

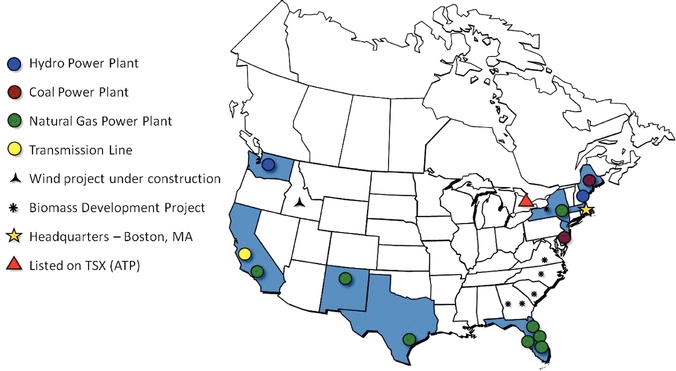

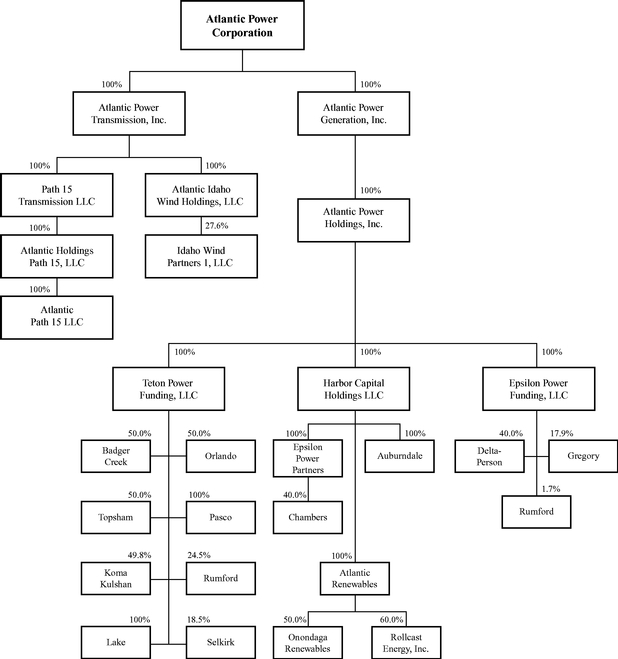

Atlantic Power Corporation is an independent power producer, with power projects located in major markets in the United States. Our current portfolio consists of interests in 12 operational power generation projects across eight states, one wind project under construction, a 500 kilovolt 84-mile electric transmission line located in California, and six development projects in five states. Our power generation projects have an aggregate gross electric generation capacity of approximately 1,823 megawatts (or "MW") in which our ownership interest is approximately 808 MW.

The following map shows the location of our projects, including joint venture interests, across the United States:

We sell the capacity and power from our power generation projects under power purchase agreements (or "PPAs") with a variety of utilities and other parties. Under the PPAs, which have expiration dates ranging from 2010 to 2037, we receive payments for electric energy sold to our customers (known as energy payments), in addition to payments for electric generation capacity (known as capacity payments). We also sell steam and/or other forms of thermal energy from a number of our projects under energy sales agreements to industrial purchasers ("steam sales agreements"). The transmission system rights (or "TSRs") we own in our power transmission project entitle us to payments indirectly from the utilities that make use of the transmission line.

Our power generation projects generally operate pursuant to long-term supply agreements, typically accompanied by fuel transportation arrangements. In most cases, the fuel supply and

1

transportation arrangements correspond to the term of the relevant PPAs and most of the PPAs and steam sales agreements provide for the pass-through or indexing of fuel costs to our customers.

We partner with recognized leaders in the independent power business to operate and maintain our projects, including Caithness Energy, LLC ("Caithness"), Cogentrix Energy, Inc. ("Cogentrix") and the Western Area Power Administration ("Western"). Under these operation, maintenance and management agreements, the operator is typically responsible for operations, maintenance and repair services.

Atlantic Power Corporation is organized under the laws of the Province of British Columbia. Our registered office is located at 355 Burrard Street, Suite 1900, Vancouver, British Columbia, Canada V6C 2G8 and our headquarters are located at 200 Clarendon Street, Floor 25, Boston, Massachusetts, USA 02116. Our telephone number is (617) 977-2400. Our website address is www.atlanticpower.com. Information contained on, or otherwise accessible through, our website is not incorporated into, and does not constitute a part of, this prospectus or any other report or documents we file with or furnish to the SEC.

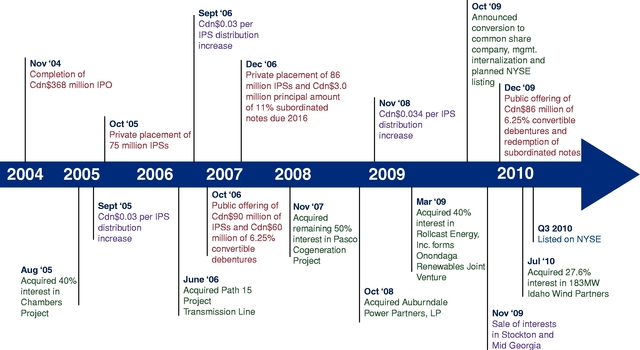

We completed our initial public offering on the Toronto Stock Exchange, or the TSX, in November 2004. At the time of the initial public offering, our publicly-traded security was an "income participating security," or "IPS," each of which was comprised of one common share and Cdn$5.767 principal value of 11% subordinated notes due 2016. On November 27, 2009, our shareholders approved a conversion from the IPS structure to a traditional common share structure. Each IPS has been exchanged for one new common share and each old common share that did not form a part of an IPS was exchanged for approximately 0.44 of a new common share. Our shares trade on the TSX under the symbol "ATP" and began trading on the New York Stock Exchange, or the NYSE, under the symbol "AT" on July 23, 2010.

We believe we distinguish ourselves from other independent power producers through the following competitive strengths:

- •

- Diversified Projects. Our power generation projects have an aggregate gross electric generation capacity of approximately 1,823 MW, and our net ownership interest in the electric generation capacity of these projects is approximately 808 MW. Our power generation projects are diversified by geographic location, electricity and steam customers, and project operators. These projects are generally located in the deregulated and more liquid electricity markets of New England, New York, Mid-Atlantic, California and Texas, or are located in regions of relatively high electricity demand growth such as Florida and New Mexico.

- •

- Strong Customer

Base. Our customers are generally large utilities, and other parties with investment-grade credit ratings. The largest customers of our

power generation projects are Progress Energy Florida, Inc. ("PEF"), Tampa Electric Company ("TECO"), and Atlantic City Electric ("ACE"), which purchase approximately 40%, 15% and 11%,

respectively, of the net electric generation capacity of our projects. No other electric customer purchases more than 7% of the net electric generation capacity of our power generation projects.

- •

- Leading Third-Party Managers. Our power generation projects rely on a number of different operators for their operation, which are generally recognized leaders in the independent power business. Affiliates of Caithness, Cogentrix and Babcock and Wilcox Power Generation

Our power transmission project, known as the Path 15 project, is an 84-mile, 500-kilovolt transmission line built in order to alleviate north-south transmission congestion in California. It is a traditional rate-base asset whose revenues are regulated by the Federal Energy Regulatory Commission ("FERC") and is operated by Western, a U.S. Federal power agency.

2

- •

- Stability of Project Cash Flow. Each of our power generation projects has been in operation for over ten years. Cash flows from each project are generally supported by energy sales contracts with investment-grade utilities and other sophisticated counterparties. We believe that each project's combination of PPA(s), fuel supply agreement(s) and/or commodity hedges help stabilize operating margins as fuel prices fluctuate.

Group, Inc. operate projects representing approximately 49%, 21% and 9%, respectively, of the net electric generation capacity of our power generation projects. No other operator is responsible for the operation of projects representing more than 8% of the net electric generation capacity of our power generation projects.

Our Objectives and Business Strategies

Our objectives include maintaining the stability and sustainability of dividends to shareholders and to maximize the value of our company. In order to achieve these objectives, we intend to focus on enhancing the operating and financial performance of the projects and on pursuing additional acquisitions primarily in the electric power industry in the U.S. and Canada.

Organic Growth

We intend to enhance the operation and financial performance of our projects through:

- •

- optimization of commercial arrangements such as PPAs, fuel supply and transportation contracts, steam sales agreements,

and operations and maintenance agreements;

- •

- achievement of improved operating efficiencies;

- •

- upgrade or enhancement of existing equipment or plant configurations; and

- •

- expansion of existing projects.

Successfully extending PPAs and fuel agreements may facilitate refinancings that provide capital to fund growth opportunities.

Extending PPAs Following Their Expiration

PPAs in our portfolio have expiration dates ranging from 2010 to 2037. In each case, we plan for expirations by evaluating various options in the market for maximizing project cash flows. New arrangements may involve responses to utility solicitations for capacity and energy, direct negotiations with the original purchasing utility for PPA extensions, arrangements with creditworthy energy trading firms for tolling agreements, full service PPAs or the use of derivatives to lock in value. We do not assume that pricing under existing PPAs will necessarily be sustained after PPA expirations, since most original PPAs included capacity payments related to return of and return on original capital invested and counterparties or evolving regional electricity markets may or may not provide similar payments under new or extended PPAs.

Acquisition and Investment Strategy

We believe that new electricity generation projects will be required in the United States and Canada over the next several years as a result of growth in electricity demand, transmission constraints and the retirement of older generation projects due to obsolescence or environmental concerns. There is also a very active secondary market for existing projects. We intend to expand our operations by making accretive acquisitions with a focus on power generation, transmission, distribution and related facilities in the United States and Canada. We may also invest in other forms of energy-related projects, utility projects and infrastructure projects, as well as additional investments in development stage projects or companies where the prospects for creating long-term predictable cash flows are

3

attractive. Since the time of our initial public offering on the TSX in 2004, we have twice acquired the interest of another partner in one of our existing projects and will continue to look for such opportunities.

Our senior management has significant experience in the independent power industry and we believe the experience, reputation and industry relationships of our management team will provide us with enhanced access to future acquisition opportunities.

On July 2, 2010, we acquired a 27.6% equity interest in Idaho Wind Partners 1, LLC ("IWP" or "Idaho Wind") for approximately $40 million. IWP recently commenced construction of a 183 MW wind power project located near Twin Falls, Idaho, which is currently scheduled to be completed in late 2010 or early 2011. IWP has 20-year fixed-price PPAs with Idaho Power Company. Our investment in IWP was funded with cash on hand and a $20 million borrowing under our senior credit facility. Upon completion of construction, we expect Idaho Wind to provide after-tax cash flows to us of $4.5 million to $5.5 million for each full year of operations. Our investment in IWP will be accounted for under the equity method of accounting.

In April 2010, our majority-owned subsidiary, Rollcast Energy, Inc., signed an agreement with two banks to co-arrange project-level debt financing and entered into a construction agreement for a 53.5 MW biomass project, known as Piedmont Green Power, to be located in Barnesville, Georgia. Pursuant to the terms of our investment in Rollcast, we have the option, but not the obligation, to invest directly in biomass power plants under development by Rollcast. We are currently in advanced discussions that we expect will lead to our commitment to invest up to $75 million in the Piedmont Green Power project, representing substantially all of the equity interests in the project. Construction of the project is scheduled to begin in the third quarter of 2010. The Piedmont Green Power project has obtained a 20-year PPA with Georgia Power Company which includes an adjustment related to the cost of biomass fuel for the plant.

Concurrently with this offering, we are offering Cdn$ in aggregate principal amount of our % Series B convertible unsecured subordinated debentures due in a public offering in Canada. The debentures will be convertible into our common shares at the option of the holder at any time prior to the close of business on the earlier of and the business day immediately preceding the date specified by us for redemption of the debentures.

The completion of this offering of common shares is not subject to the completion of the concurrent offering of convertible debentures and the completion of the concurrent offering of convertible debentures is not subject to the completion of this offering. See "Description of Concurrent Offering of Convertible Debentures."

4

The following table outlines our portfolio of power generating and transmission assets in operation and under construction as of August 9, 2010, including our interest in each facility. Management believes the portfolio is well diversified in terms of electricity and steam buyers, fuel type, regulatory jurisdictions and regional power pools, thereby partially mitigating exposure to market, regulatory or environmental conditions specific to any single region.

|

|

||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Project Name |

Location (State) |

Type |

Total MW |

Economic Interest(1) |

Accounting Treatment(2) |

Net MW(3) |

Electricity Purchaser |

Power Contract Expiry |

Customer S&P Credit Rating |

|||||||||||||

|

|

||||||||||||||||||||||

Auburndale |

Florida | Natural Gas | 155 | 100.00 | % | C | 155 | Progress Energy Florida | 2013 | BBB+ | ||||||||||||

|

|

||||||||||||||||||||||

Lake |

Florida | Natural Gas | 121 | 100.00 | % | C | 121 | Progress Energy Florida | 2013 | BBB+ | ||||||||||||

|

|

||||||||||||||||||||||

Pasco |

Florida | Natural Gas | 121 | 100.00 | % | C | 121 | Tampa Electric Co. | 2018 | BBB | ||||||||||||

|

|

||||||||||||||||||||||

Chambers |

New Jersey | Coal | 262 | 40.00 | % | E | 89(4) | ACE | 2024 | BBB | ||||||||||||

|

|

||||||||||||||||||||||

|

16 | DuPont | 2024 | A | ||||||||||||||||||

|

|

||||||||||||||||||||||

Path 15 |

California | Transmission | N/A | 100.00 | % | C | N/A | California Utilities via CAISO(5) | N/A | (6) | BBB+ to A(7) | |||||||||||

|

|

||||||||||||||||||||||

Orlando |

Florida | Natural Gas | 129 | 50.00 | % | E | 46 | Progress Energy Florida | 2023 | BBB+ | ||||||||||||

|

|

||||||||||||||||||||||

|

19 | Reedy Creek Improvement District | 2013 | (8) | A(9) | |||||||||||||||||

|

|

||||||||||||||||||||||

Selkirk |

New York | Natural Gas | 345 | 17.70% | (10) | E | 14 | Merchant | N/A | N/R | ||||||||||||

|

|

||||||||||||||||||||||

|

47 | Consolidated Edison | 2014 | A- | ||||||||||||||||||

|

|

||||||||||||||||||||||

Gregory |

Texas | Natural Gas | 400 | 17.10 | % | E | 59 | Fortis Energy Marketing and Trading | 2013 | A- | ||||||||||||

|

|

||||||||||||||||||||||

|

9 | Sherwin Alumina | 2020 | NR | ||||||||||||||||||

|

|

||||||||||||||||||||||

Topsham(11) |

Maine | Hydro | 14 | 50.00 | % | E | 7 | Central Maine Power | 2011 | BBB+ | ||||||||||||

|

|

||||||||||||||||||||||

Badger Creek |

California | Natural Gas | 46 | 50.00 | % | E | 23 | Pacific Gas & Electric | 2011 | BBB- | ||||||||||||

|

|

||||||||||||||||||||||

Rumford |

Maine | Coal/Biomass | 85 | 26.40 | % | E | 22 | Rumford Paper Co. | 2010 | N/R | ||||||||||||

|

|

||||||||||||||||||||||

Koma Kulshan |

Washington | Hydro | 13 | 49.80 | % | E | 6 | Puget Sound Energy | 2037 | BBB | ||||||||||||

|

|

||||||||||||||||||||||

Delta-Person |

New Mexico | Natural Gas | 132 | 40.00 | % | E | 53 | PNM | 2020 | BB- | ||||||||||||

|

|

||||||||||||||||||||||

Idaho Wind(12) |

Idaho | Wind | 183 | 27.56 | % | E | 51 | Idaho Power Co. | 2030 | BBB | ||||||||||||

|

|

||||||||||||||||||||||

- (1)

- Except

as otherwise noted, economic interest represents the percentage ownership interest in the project held indirectly by Atlantic Power.

- (2)

- Accounting

Treatment: C—Consolidated; and E—Equity Method of Accounting (for additional details, see Note 2 of

the accompanying consolidated financial statements for the year ended December 31, 2009).

- (3)

- Represents

our interest in each project's electric generation capacity based on our economic interest.

- (4)

- Includes

separate power sales agreement in which the project and ACE share profits on spot sales of energy and capacity not purchased by ACE

under the base PPA.

- (5)

- California

utilities pay TACs to California Independent System Operator ("CAISO"), who then pays owners of TSRs, such as Path 15, in

accordance with its FERC approved annual revenue requirement.

- (6)

- Path 15

is a FERC regulated asset with a FERC-approved regulatory life of 30 years: through 2034.

- (7)

- Largest

payers of fees supporting Path 15's annual revenue requirement are PG&E (BBB+), SoCal Ed (BBB+) and SDG&E (A). CAISO imposes

minimum credit quality requirements for any participants of A or better unless collateral is posted per CAISO imposed schedule.

- (8)

- Upon the expiry of the Reedy Creek PPA, the associated capacity and energy will be sold to PEF.

5

- (9)

- Fitch

rating on Reedy Creek Improvement District bonds.

- (10)

- Represents

our residual interest in the project after all priority distributions are paid, which is estimated to occur in 2012.

- (11)

- We

own our interest in this project as a lessor.

- (12)

- Project currently under construction and is expected to be completed in late 2010 or early 2011.

6

Issuer |

Atlantic Power Corporation, a British Columbia corporation. | |

Common Shares to Be Offered by Us |

shares. |

|

Common Shares to Cover Over-Allotments |

We have granted the underwriters an option to purchase up to additional common shares to cover over-allotments. |

|

Common Shares to Be Outstanding after this Offering |

Shares (or shares if the underwriters exercise their over-allotment option in full). |

|

Risk Factors |

Prospective purchasers should carefully review and evaluate certain risk factors relating to an investment in the common shares, including, but not limited to trading market for common shares and discretion in the use of proceeds. See "Risk Factors." |

|

United States Federal Income Tax Considerations |

You should consult your tax advisor with respect to the U.S. federal income tax consequences of owning the common shares in light of your own particular situation and with respect to any tax consequences arising under the laws of any state, local, foreign or other taxing jurisdiction. See "Certain United States Federal Income Tax Considerations." |

|

Concurrent Public Offering of Convertible Debentures |

Concurrently with this offering, we are also conducting a separate public offering in Canada of Cdn$ in aggregate principal amount of our convertible unsecured subordinated debentures (plus up to an additional Cdn$ in aggregate principal amount of our convertible debentures that we may issue and sell upon the exercise of the underwriter's option to purchase additional convertible debentures). |

|

|

This offering is not conditioned upon the successful completion of the concurrent offering of convertible debentures and the concurrent offering of convertible debentures is not conditioned upon the successful completion of this offering. See "Description of Concurrent Offering of Convertible Debentures." |

7

Use of Proceeds |

We expect to receive net proceeds from this offering of approximately $ million after deducting the underwriting discount and our estimated expenses (or approximately $ million if the underwriters exercise their option to purchase additional shares in full). We intend to use the net proceeds from this offering, along with the net proceeds we receive from our concurrent offering of convertible debentures, for (i) repayment of approximately $20 million borrowed under our revolving credit facility in June 2010 to partially fund our previously-announced acquisition of a 27.6% equity interest in Idaho Wind Partners 1, LLC, and (ii) to fund a likely investment of up to $75 million in the Piedmont Green Power biomass project in Barnesville, Georgia for substantially all of the equity interest in the project, which is currently in advanced discussions that we expect to lead to a commitment. Any remaining net proceeds will be used to fund additional growth opportunities and for general corporate purposes. |

|

Listing |

Our outstanding common shares are listed on the TSX under the symbol "ATP" and on the New York Stock Exchange under the symbol "AT." |

The number of common shares to be outstanding after this offering is based upon 60,510,070 shares outstanding as of August 13, 2010. The number of common shares to be outstanding after this offering does not include:

- •

- 582,000 shares reserved for issuance in connection with our Long Term Incentive Plan;

- •

- 11,473,000 shares issuable upon conversion, redemption, purchase for cancellation or maturity of our outstanding

convertible debentures; and

- •

- any shares reserved for issuance upon the conversion, redemption, purchase for cancellation or maturity of the convertible debentures being offered by us in the concurrent public offering.

8

Summary Historical Financial Information

The following table presents summary consolidated financial information, which should be read in conjunction with our consolidated financial statements beginning on page F-1 and the related notes thereto, and "Management's Discussion and Analysis of Financial Condition and Results of Operations" beginning on page 33. The annual historical information for each of the years in the three-year period ended December 31, 2009 has been derived from our audited consolidated financial statements included elsewhere in this prospectus. The historical information for the six-month periods ended June 30, 2009 and 2010 have been derived from our unaudited consolidated financial statements included elsewhere in this prospectus.

| |

|

|

|

|

|

Six months ended June 30, |

||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

Year Ended December 31, | |||||||||||||||||||||

| (in thousands of U.S. dollars, except as otherwise stated) |

||||||||||||||||||||||

| 2009 | 2008 | 2007 | 2006(a) | 2005(a) | 2010(a) | 2009(a) | ||||||||||||||||

Project revenue |

$ | 179,517 | $ | 173,812 | $ | 113,257 | $ | 69,374 | $ | 57,711 | $ | 95,125 | $ | 90,304 | ||||||||

Project income |

48,415 | 41,006 | 70,118 | 57,247 | 48,256 | 19,405 | 25,995 | |||||||||||||||

Net (loss) income attributable to Atlantic Power Corporation |

(38,486 | ) | 48,101 | (30,596 | ) | (2,408 | ) | (509 | ) | (4,618 | ) | (6,486 | ) | |||||||||

Basic earnings per share, US$ |

$ |

(0.63 |

) |

$ |

0.78 |

$ |

(0.50 |

) |

$ |

(0.05 |

) |

$ |

(0.01 |

) |

$ |

(0.08 |

) |

$ |

(0.11 |

) |

||

Basic earnings per share, Cdn$ |

$ |

(0.72 |

) |

$ |

0.84 |

$ |

(0.53 |

) |

$ |

(0.06 |

) |

$ |

(0.02 |

) |

$ |

(0.08 |

) |

$ |

(0.13 |

) |

||

Diluted earnings per share, US$ |

$ |

(0.63 |

) |

$ |

0.73 |

$ |

(0.50 |

) |

$ |

(0.05 |

) |

$ |

(0.01 |

) |

$ |

(0.08 |

) |

$ |

(0.11 |

) |

||

Diluted earnings per share, Cdn$ |

$ |

(0.72 |

) |

$ |

0.86 |

$ |

(0.53 |

) |

$ |

(0.06 |

) |

$ |

(0.02 |

) |

$ |

(0.08 |

) |

$ |

(0.13 |

) |

||

Distribution declared per IPS |

$ |

0.51 |

$ |

0.60 |

$ |

0.59 |

$ |

0.57 |

$ |

0.53 |

$ |

— |

$ |

0.29 |

||||||||

Dividend declared per common share |

$ | 0.46 | $ | 0.40 | $ | 0.40 | $ | 0.37 | $ | 0.31 | $ | 0.52 | $ | 0.19 | ||||||||

Total assets |

$ |

869,576 |

$ |

907,995 |

$ |

880,751 |

$ |

965,121 |

$ |

636,138 |

$ |

862,525 |

$ |

873,923 |

||||||||

Total long-term liabilities |

$ |

402,212 |

$ |

654,499 |

$ |

715,923 |

$ |

613,423 |

$ |

475,533 |

$ |

407,413 |

$ |

675,159 |

||||||||

- (a)

- Unaudited

9

Investing in our common shares involves a high degree of risk. In addition to other information contained in this prospectus you should carefully consider the risks described below in evaluating our company and our business before making a decision to invest in our common shares. These risks are not the only ones faced by us. Additional risks not presently known or that we currently deem immaterial could also materially and adversely affect our financial condition, results of operations, business and prospects. The trading price of our common shares could decline due to any of these risks, and you may lose all or part of your investment. This prospectus also contains forward-looking statements that involve risks and uncertainties. Actual results could differ materially from those anticipated in these forward-looking statements as a result of certain factors, including the risks faced by us described below and elsewhere in this prospectus. Please refer to the section entitled "Cautionary Statements Regarding Forward-Looking Statements" in this prospectus.

Risks Related to Our Business and Our Projects

Our revenue may be reduced upon the expiration or termination of our power purchase agreements

Power generated by our projects, in most cases, is sold under PPAs that expire at various times. For example, PPAs at our Rumford, Badger Creek and Topsham projects expire between now and the end of 2011 and represent 52 MWs of our net generating capacity and the PPAs at our Auburndale, Lake and Gregory projects expire by the end of 2013 and represent 335 MWs of our net generating capacity. The table on page 5 contains details about all our projects' PPAs. In addition, these PPAs may be subject to termination in certain circumstances, including default by the project. When a PPA expires or is terminated, it is possible that the price received by the project for power under subsequent arrangements may be reduced significantly. It is possible that subsequent PPAs may not be available at prices that permit the operation of the project on a profitable basis. If this occurs, the affected project may temporarily or permanently cease operations.

Our projects depend on their electricity, thermal energy and transmission services customers

Each of our projects rely on one or more PPAs, steam sales agreements or other agreements with one or more utilities or other customers for a substantial portion of its revenue. The largest customers of our power generation projects, including projects recorded under equity method of accounting, are Progress Energy Florida, Inc. ("PEF"), Tampa Electric Company ("TECO"), and Atlantic City Electric ("ACE"), which purchase approximately 40%, 15% and 11%, respectively, of the net electric generation capacity of our projects. The amount of cash available to pay dividends to shareholders is highly dependent upon customers under such agreements fulfilling their contractual obligations. There is no assurance that these customers will perform their obligations or make required payments.

Certain of our projects are exposed to fluctuations in the price of electricity

Those of our projects with no PPA or PPAs based on spot market pricing will be exposed to fluctuations in the wholesale price of electricity. In addition, should any of the long-term PPAs expire or terminate, the relevant project will be required to either negotiate a new PPA or sell into the electricity wholesale market, in which case the prices for electricity will depend on market conditions at the time.

Our most significant exposure to market power prices is at the Selkirk and Chambers projects. At Selkirk, approximately 23% of the capacity of the facility is not contracted and is sold at market prices or not sold at all if market prices do not support profitable operation of that portion of the facility. At Chambers, our utility customer has the right to sell a portion of the plant's output into the spot power market if it is economical to do so and the Chambers project shares in the profits from these sales.

10

Our projects may not operate as planned

The revenue generated by our power generation projects is dependent, in whole or in part, on the amount of electric energy and steam generated by them. The ability of our projects to generate the required amount of power to be sold to customers under the PPAs is a primary determinant of the amount of cash that will be distributed from the projects to us, and that will in turn be available for dividends paid to our shareholders. There is a risk of equipment failure due to wear and tear, latent defect, design error or operator error, among other things, which could adversely affect revenues and cash flow. To the extent that our projects' equipment requires more frequent and/or longer than forecast down times for maintenance and repair, or suffers disruptions of power generation for other reasons, the amount of cash available for dividends may be adversely affected.

In general, our power generation projects transmit electric power to the transmission grid for purchase under the PPAs through a single step up transformer. As a result, the transformer represents a single point of vulnerability and may exhibit no abnormal behavior in advance of a catastrophic failure that could cause a temporary shutdown of the facility until a spare transformer can be found or a replacement manufactured.

If the reason for a shutdown is outside of the control of the operator, a power generation project may be able to make a force majeure claim for temporary relief of its obligations under the project contracts such as the PPA, fuel supply, steam sales agreement, a project-level debt agreement or otherwise mitigate impacts through business interruption insurance policies. If successful, such a claim may prevent a default or reduce monetary losses under such contracts. However, a force majeure claim may be challenged by the contract counterparty and, to the extent the challenge is successful, the outage may still have a materially adverse effect on the project.

Our projects depend on suppliers under fuel supply agreements and increases in fuel costs may adversely affect the profitability of the projects

Revenues earned by our projects may be affected by the availability, or lack of availability, of a stable supply of fuel at reasonable or predictable prices. To the extent possible, the projects attempt to match fuel cost setting mechanisms in supply agreements to energy payments formulas in the PPA. To the extent that fuel costs are not matched well to PPA energy payments, increases in fuel costs may adversely affect the profitability of the projects.

The amount of energy generated at the projects is highly dependent on suppliers under certain fuel supply agreements fulfilling their contractual obligations. The loss of significant fuel supply agreements or an inability or failure by any supplier to meet its contractual commitments may adversely affect our results.

Upon the expiration or termination of existing fuel supply agreements, we or our project operators will have to renegotiate these agreements or may need to source fuel from other suppliers. Our project operators may not be able to renegotiate these agreements or enter into new agreements on similar terms. Furthermore, there can be no assurance as to availability of the supply or pricing of fuel under new arrangements and it can be very difficult to accurately predict the future prices of fuel. For example, a portion of the required natural gas at our Auburndale project and all of the natural gas required at our Lake project is purchased at market prices, but the projects' PPAs that expire in 2013 do not effectively pass through changes in natural gas prices. We have executed a hedging program to substantially mitigate this risk through 2013.

The amount of energy generated at the projects is dependent upon the availability of natural gas, coal, oil or biomass. The long-term availability of such resources may not remain unchanged.

11

Our projects depend on a favorable regulatory regime

The profitability of our projects is in part dependent upon the continuation of a favorable regulatory climate with respect to the continuing operations and the future growth and development of the independent power industry. Should the regulatory regime in an applicable jurisdiction be modified in a manner which adversely affects the projects, including increases in taxes and permit fees, dividends to shareholders may be adversely affected. The failure to obtain all necessary licenses or permits, including renewals thereof or modifications thereto, may also adversely affect cash available to pay dividends.

Our operations are subject to the provisions of various energy laws and regulations

Generally, in the United States, our projects are subject to regulation by the Federal Energy Regulatory Commission, or "FERC," regarding the terms and conditions of wholesale service and rates, as well as by state agencies regarding PPAs entered into by qualifying facility projects and the siting of the generation facilities. The majority of our generation is sold by qualifying facility projects under PPAs that required approval by state authorities.

In August 2005, the Energy Policy Act of 2005 was enacted, which removed certain regulatory constraints on investment in utility power producers. The Energy Policy Act of 2005 also limited the requirement that electric utilities buy electricity from qualifying facilities to certain markets that lack competitive characteristics, potentially making it more difficult for our current and future projects to negotiate favorable PPAs with these utilities. Finally, the Energy Policy Act of 2005 amended and expanded the reach of the FERC's merger approval authority.

If any project that is a qualifying facility were to lose its status as a qualifying facility, then such project may no longer be entitled to exemption from provisions of the Public Utility Holding Company Act of 2005 or from provisions of the Federal Power Act and state law and regulations. Such project may be able to obtain exempt wholesale generator status to maintain its exemption from the provisions of the Public Utility Holding Company Act of 2005, however our projects may not be able to obtain such exemptions. Loss of qualifying facility status could trigger defaults under covenants to maintain qualifying facility status in the PPAs, steam sales agreements and project-level debt agreements and if not cured within allowed cure periods, could result in termination of agreements, penalties or acceleration of indebtedness under such agreements, plus interest.

Our projects would also have to file with the FERC for market-based rates or file for acceptance for filing of the rates set forth in the applicable PPA, and our projects' rates would then be subject to initial and potentially subsequent reviews by the FERC under the Federal Power Act, which could result in reductions to the rates.

Our projects require licenses, permits and approvals which can be in addition to any required environmental permits. No assurance can be provided that we will be able to obtain, comply with and renew, as required, all necessary licenses, permits and approvals for these facilities. If we cannot comply with and renew as required all applicable licenses, permits and approvals, our business, results of operations and financial condition could be adversely affected.

The Energy Policy Act of 2005 provides incentives for various forms of electric generation technologies, which may subsidize our competitors. In addition, pursuant to the Energy Policy Act of 2005, the FERC selected an electric reliability organization which imposes mandatory reliability rules and standards. Among other things, the FERC's rules implementing these provisions allow such reliability organizations to impose sanctions on generators that violate their new reliability rules.

The introductions of new laws, or other future regulatory developments, may have a material adverse impact on our business, operations or financial condition.

12

Future FERC rate determinations could negatively impact Path 15's cash flows

The stability of Path 15's cash flows will continue to be subject to the risk of the FERC's adjusting the expected formulation of revenues upon its rate review every three years, and a rate review is set to commence in 2011. The cost-of-service methodology currently applied by the FERC is well established and transparent; however, certain inputs in the FERC's determination of rates are subject to its discretion, including in response to protests from interveners in such rate cases, which include return on equity and the recovery of certain extraordinary expenses. Unfavorable decisions on these matters could adversely affect the cash flow, financial position and results of operations of us and Path 15, and could adversely affect our cash available for dividends.

Noncompliance with federal reliability standards may subject us and our projects to penalties

Our operations are subject to the regulations of the North American Electric Reliability Corporation ("NERC"), a self-regulatory organization that is a non-governmental entity which has statutory responsibility to regulate bulk power system users, generation and transmission owners and operators. NERC groups the users, owners, and operators of the bulk power system into 17 categories, known as functional entities—e.g., Generator Owner, Generator Operator, Purchasing-Selling Entity, etc.—according to the tasks they perform. The NERC Compliance Registry lists the entities responsible for complying with the mandatory reliability standards and the FERC, NERC, or a regional reliability organization may assess penalties against any responsible entity found to be in noncompliance. Violations may be discovered through self-certification, compliance audits, spot checking, self-reporting, compliance investigations by NERC (or a regional reliability organization) and the FERC, periodic data submittals, exception reporting, and complaints. NERC and the FERC have assigned a Violation Risk Factor of High, Medium, or Lower to each requirement of the mandatory reliability standards corresponding to the risk to the bulk power system associated with a violation of that requirement. The penalty that might be imposed for violating the requirements of the standards is a function of the Violation Risk Factor. Penalties for the most severe violations can reach as high as $1 million per violation, per day, and our projects could be exposed to these penalties if violations occur.

Our projects are subject to significant environmental and other regulations

Our projects are subject to numerous and significant federal, state and local laws, including statutes, regulations, by-laws, guidelines, policies, directives and other requirements governing or relating to, among other things: air emissions; discharges into water; ash disposal; the storage, handling, use, transportation and distribution of dangerous goods and hazardous, residual and other regulated materials, such as chemicals; the prevention of releases of hazardous materials into the environment; the prevention, presence and remediation of hazardous materials in soil and groundwater, both on and off site; land use and zoning matters; and workers' health and safety matters. As such, the operation of our projects carries an inherent risk of environmental, health and safety liabilities (including potential civil actions, compliance or remediation orders, fines and other penalties), and may result in the projects being involved from time to time in administrative and judicial proceedings relating to such matters.

The Clean Air Act and related regulations and programs of the Environmental Protection Agency extensively regulate the air emissions of sulfur dioxide, nitrogen oxides, mercury and other compounds emitted by power plants. Environmental laws and regulations have generally become more stringent over time, and this trend may continue. In particular, the U.S. Environmental Protection Agency has promulgated regulations under the federal Clean Air Interstate Rule ("CAIR") requiring additional reductions in nitrogen oxides, or "NOX," and sulphur dioxide, or "SO2," emissions, beginning in 2009 and 2010 respectively, and has also promulgated regulations requiring reductions in mercury emissions from coal-fired electric generating units, beginning in 2010 with more substantial reductions in 2018.

13

Moreover, certain of the states in which we operate have promulgated air pollution control regulations which are more stringent than existing and proposed federal regulations.

While CAIR was set aside by a court decision in 2008, that decision allowed the CAIR requirements to remain in place pending further rulemaking by the Environmental Protection Agency. On July 6, 2010, the Environmental Protection Agency proposed to replace CAIR by requiring 31 states and the District of Columbia to curb emissions of sulfur dioxide and nitrogen oxides from power plants through more aggressive state-by-state emissions budgets for nitrogen oxides and sulfur dioxide. Compliance with the proposed rule, which would take effect in 2012, may have a material adverse impact on our business, operations or financial condition.

The Environmental Protection Agency intends to propose new mercury emissions standards for power plants by March 2011 and to have new standards in place by November 2011. Meeting these new standards at our coal-fired facilities may have a material adverse impact on our business, operations or financial condition.

The Resource Conservation and Recovery Act ("RCRA") has historically exempted fossil fuel combustion wastes from hazardous waste regulation. However, in June 2010 the Environmental Protection Agency proposed two alternative sets of regulations governing coal ash. One set of proposed regulations would designate coal ash as "special waste" and bring ash impoundments at coal-fired power plants under federal regulations governing hazardous solid waste under Subtitle C of RCRA. Another set of proposed regulations would regulate coal ash as a non-hazardous solid waste. If the Environmental Protection Agency determines to regulate coal ash as a hazardous waste, our coal-fired facilities may be subject to increased compliance obligations and costs that may have a material adverse impact on our business, operations or financial condition.

Significant expenditures may be required for either capital expenditures or the purchase of allowances under any or all of these programs to keep the projects compliant with environmental laws and regulations. The projects' PPAs do not allow for the pass through of emissions allowance or emission reduction capital expenditure costs, with the exception of Pasco. If it is not economical to make those expenditures it may be necessary to retire or mothball facilities, or restrict or modify our operations to comply with more stringent standards.

Our projects have obtained environmental permits and other approvals that are required for their operations. Compliance with applicable environmental laws, regulations, permits and approvals and material future changes to them could materially impact our businesses. Although we believe the operations of the projects are currently in material compliance with applicable environmental laws, licenses, permits and other authorizations required for the operation of the projects and although there are environmental monitoring and reporting systems in place with respect to all the projects, there is no guarantee that more stringent laws will not be imposed, that there will not be more stringent enforcement of applicable laws or that such systems may not fail, which may result in material expenditures. Failure by the projects to comply with any environmental, health or safety requirements, or increases in the cost of such compliance, including as a result of unanticipated liabilities or expenditures for investigation, assessment, remediation or prevention, could result in additional expense, capital expenditures, restrictions and delays in the projects' activities, the extent of which cannot be predicted.

Our projects are subject to regulation of CO2 and other greenhouse gases (GHGs)

Ongoing public concerns about emissions of CO2 and other GHGs from power plants have resulted in the enactment of, and proposals for, laws and regulations at the federal, state and regional levels, some of which do or could apply to some of our project operations. For example, the multi-state CO2 cap-and-trade program known as the Regional Greenhouse Gas Initiative (RGGI) applies to our fossil fuel facilities in the Northeast region. The RGGI program went into effect on January 1, 2009.

14

CO2 allocations are now a tradeable commodity, currently averaging in the $2.05 to $3.20/ton range. The State of Florida has conducted stakeholder meetings as part of the process of developing GHG emissions regulations, the most recent of which was in January 2009. Discussions indicate favoring a program similar to that of RGGI.

California, New Mexico, Washington and other states are part of the Western Climate Initiative, which is developing a regional cap-and-trade program to reduce GHG emissions in the region to 15% below 2005 levels by 2020.

In 2006, the State of California passed legislation initiating two programs to control/reduce the creation of GHGs. The two laws, more commonly known as AB 32 and SB 1368, are currently in the regulatory rulemaking phase which will involve public comment and negotiations over specific provisions. Development towards the implementation of these programs continues.

Under AB 32 (the California Global Warming Act of 2006) the California Air Resources Board ("CARB") is required to adopt a GHG emissions cap on all major sources (not limited to the electric sector). In order to do so, it must adopt regulations for the mandatory reporting and verification of GHG emissions and to reduce state-wide emissions of GHGs to 1990 levels by 2020. This will most likely require that electric generating facilities reduce their emissions of GHGs or pay for the right to emit by the implementation date of January 1, 2012. The program has yet to be finalized and the decision as to whether allocations will be distributed or auctioned will be determined in the rulemaking process that is currently underway. Discussion to date favors an auction-based allocation program.

SB 1368 added the requirement that the California Energy Commission, in consultation with the California Public Utilities Commission (the "CPUC") and the CARB establish GHG emission performance standards and implement regulations for power purchase agreements that exceed five years entered into prospectively by publicly-owned electric utilities. The legislation directs the California Energy Commission to establish the performance standard as one not exceeding the rate of GHG emitted per megawatt-hour associated with combined-cycle, gas turbine baseload generation, such as our Badger Creek project. Provisions are under consideration in the rulemaking to allow facilities that have higher CO2 emissions to be able to negotiate PPA's for up to a five-year period or sell power to entities not subject to SB 1368.

In addition to the regional initiatives, legislation for the regulation of GHGs has been introduced at the federal level and if passed, may eventually override the regional efforts with a national cap and trade program. Federal bills to create both a cap-and-trade allowance system and a renewable/efficiency portfolio standard have been introduced in both the house and senate. Separately, the U.S. Environmental Protection Agency has taken several recent actions to regulate GHG emissions.

The Environmental Protection Agency's recent actions include its finding of "endangerment" to public health and welfare from GHGs, its issuance in September 2009 of the Final Mandatory Reporting of Greenhouse Gases Rule which requires large sources, including power plants, to monitor and report GHG emissions to the Environmental Protection Agency annually starting in 2011, and its publication in May 2010 of its final Prevention of Significant Deterioration and Title V Greenhouse Gas Tailoring Rule, to take effect in 2011, which requires large industrial facilities, including power plants, to obtain permits to emit, and to use best available control technology to curb emissions of, GHGs.

In addition, the United States is actively participating in various international initiatives to reduce GHG emissions globally that may result in further regulatory developments in the United States.

The implementation of existing CO2 and other GHG regulations, the introduction of new regulation, or other future regulatory developments may subject the Company to increased compliance obligations and costs that could have a material adverse impact on our business, operations or financial condition.

15

Increasing competition could adversely affect our performance and the performance of our projects

The power generation industry is characterized by intense competition, and our projects encounter competition from utilities, industrial companies and other independent power producers, in particular with respect to un-contracted output. In recent years, there has been increasing competition among generators for power sales agreements, and this has contributed to a reduction in electricity prices in certain markets where supply has surpassed demand plus appropriate reserve margins. In addition, many states have implemented or are considering regulatory initiatives designed to increase competition in the U.S. power industry. Increasing competition among participants in the power generation industry may adversely affect our performance and the performance of our projects.

We have limited control over management decisions at certain projects

In many cases, our projects are not wholly-owned by us or we have contracted for their operations and maintenance, and in some cases we have limited control over the operation of the projects. Although we generally prefer to acquire projects where we have control, we may make acquisitions in non-control situations to the extent that we consider it advantageous to do so and consistent with regulatory requirements and restrictions, including the Investment Company Act of 1940. Third-party operators (such as Caithness and GE) operate many of the projects. As such, we must rely on the technical and management expertise of these third-party operators, although typically we are represented on a management or operating committee if we do not own 100% of a project. To the extent that such third party operators do not fulfill their obligations to manage the operations of the projects or are not effective in doing so, the amount of cash available to pay dividends may be adversely affected.

We may face significant competition for acquisitions and may not successfully integrate acquisitions

Our business plan includes growth through identifying suitable acquisition opportunities, pursuing such opportunities, consummating acquisitions and effectively integrating them with our business. We may be unable to identify attractive acquisition candidates in the power industry in the future, and we may not be able to make acquisitions on an accretive basis or that acquisitions will be successfully integrated into our existing operations.

Although electricity demand is expected to grow, creating the need for more generation, and the U.S. power industry is continuing to undergo consolidation and may offer attractive acquisition opportunities, we are likely to confront significant competition for those opportunities and, to the extent that any opportunities are identified, we may be unable to effect acquisitions or investments.

Any acquisition or investment may involve potential risks, including an increase in indebtedness, the inability to successfully integrate operations, the potential disruption of our ongoing business, the diversion of management's attention from other business concerns and the possibility that we pay more than the acquired company or interest is worth. There may also be liabilities that we fail to discover, or are unable to discover, in our due diligence prior to the consummation of an acquisition, and we may not be indemnified for some or all these liabilities. In addition, our funding requirements associated with acquisitions and integration costs may reduce the funds available to us to make dividend payments.

Insurance may not be sufficient to cover all losses

Our business involves significant operating hazards related to the generation of electricity. While we believe that the projects' insurance coverage addresses all material insurable risks, provides coverage that is similar to what would be maintained by a prudent owner/operator of similar facilities, and are subject to deductibles, limits and exclusions which are customary or reasonable given the cost of procuring insurance, current operating conditions and insurance market conditions, there can be no

16

assurance that such insurance will continue to be offered on an economically feasible basis, nor that all events that could give rise to a loss or liability are insurable, nor that the amounts of insurance will at all times be sufficient to cover each and every loss or claim that may occur involving our assets or operations of our projects. Any losses in excess of those covered by insurance, which may include a significant judgment against any project or project operator, the loss of a significant permit or other approval or the imposition of a significant fine or penalty, could have a material adverse effect on our business, financial condition and future prospects and could adversely affect dividends to our shareholders.

Financing arrangements could negatively impact our business

Our current or future borrowings could increase the level of financial risk to us and, to the extent that the interest rates are not fixed and rise, or that borrowings are refinanced at higher rates, then cash available for dividends could be adversely affected. Covenants in those borrowings may also adversely affect cash available for dividends. In addition, most of the projects currently have term loan or other financing arrangements in place with various lenders. These financing arrangements are typically secured by all of the project assets and contracts as well as the equity interests in the project operator (including those owned by us). The terms of these financing arrangements generally impose many covenants and obligations on the part of the project operator and other borrowers and guarantors. For example, some agreements contain requirements to maintain specified debt service coverage ratios before cash may be distributed from the relevant project to us. In many cases, a default by any party under other project agreements (such as a PPA or a fuel supply agreement) will also constitute a default under the project's term loan or other financing arrangement. Failure to comply with the terms of these term loans or other financing arrangements, or events of default thereunder, may prevent cash distributions by the project to us and may entitle the lenders to demand repayment and/or enforce their security interests.

Our failure to refinance or repay any indebtedness when due could constitute a default under such indebtedness. Under such circumstances, it is expected that dividends to our shareholders would not be permitted until such indebtedness was refinanced or repaid and we may be required to sell assets or take other actions, including the initiation of bankruptcy proceedings or the commencement of an out-of-court debt restructuring.

Our equity interests in our projects may be subject to transfer restrictions

The partnership or other agreements governing some of the projects may limit a partner's ability to sell its interest. Specifically, these agreements may prohibit any sale, pledge, transfer, assignment or other conveyance of the interest in a project without the consent of the other partners. In some cases, other partners may have rights of first offer or rights of first refusal in the event of a proposed sale or transfer of our interest. These restrictions may limit or prevent us from managing our interests in the projects in the manner we see fit, and may have an adverse effect on our ability to sell our interests in these projects at the prices we desire.

The projects are exposed to risks inherent in the use of derivative instruments

We and the projects may use derivative instruments, including futures, forwards, options and swaps, to manage commodity and financial market risks. In the future, the project operators could recognize financial losses on these arrangements as a result of volatility in the market values of the underlying commodities or if a counterparty fails to perform under a contract. If actively quoted market prices and pricing information from external sources are not available, the valuation of these contracts would involve judgment or use of estimates. As a result, changes in the underlying assumptions or use of alternative valuation methods could affect the reported fair value of these contracts.

17

Most of these contracts are recorded at fair value with changes in fair value recorded currently in earnings, resulting in significant volatility in our income (as calculated in accordance with GAAP) that does not significantly affect current period cash flows or the underlying risk management purpose of the derivative instruments. As a result, we may be unable to accurately predict the impact that our risk management decisions may have on our quarterly and annual income (as calculated in accordance with GAAP).

If the values of these financial contracts change in a manner that we do not anticipate, or if a counterparty fails to perform under a contract, it could harm our financial condition, results of operations and cash flows. We have executed natural gas swaps to reduce our risks to changes in the market price of natural gas, which is the fuel consumed at many of our projects. Due to declining natural gas prices, we have incurred losses on these natural gas swaps. We execute these swaps only for the purpose of managing risks and not for speculative trading.

Risks Related to Our Structure

We are dependent on our projects for virtually all cash available for dividends

We are dependent on the operations and assets of the projects through our indirect ownership of interests in the projects. The actual amount of cash available for dividends to our shareholders depends upon numerous factors, including profitability, changes in revenues, fluctuations in working capital, availability under existing credit facilities, capital expenditure levels, applicable laws, compliance with contracts and contractual restrictive covenants contained in any debt documentation.

Distribution of available cash may restrict our potential growth

A payout of a significant portion of substantially all of our operating cash flow will make additional capital and operating expenditures dependent on increased cash flow or additional financing in the future. Lack of these funds could limit our future growth and cash flow. In addition, we may be precluded from pursuing otherwise attractive acquisitions or investments because they may not be accretive to us on a short-term basis.

Future dividends are not guaranteed

Our board of directors may, in their discretion, amend or repeal our existing dividend policy. Future dividends, if any, will depend on, among other things, the results of operations, working capital requirements, financial condition, restrictive covenants, business opportunities, provisions of applicable law and other factors that our board of directors may deem relevant. Our board of directors may decrease the level of or entirely discontinue payment of dividends.

Exchange rate fluctuations may impact our amount of cash available for dividends

Our payments to shareholders and convertible debenture holders are denominated in Canadian dollars. Conversely, all of our projects' revenues and expenses are denominated in U.S. dollars. As a result, we are exposed to currency exchange rate risks. Despite our hedges against this risk through 2013, any arrangements to mitigate this exchange rate risk may not be sufficient to fully protect against this risk. If hedging transactions do not fully protect against this risk, changes in the currency exchange rate between U.S. and Canadian dollars could adversely affect our cash available for distribution.

18

Our indebtedness could negatively impact our business and our projects

The degree to which we are leveraged on a consolidated basis could increase and have important consequences to our shareholders, including:

- •

- our ability in the future to obtain additional financing for working capital, capital expenditures, acquisitions or other

purposes may be limited;

- •

- we may be unable to refinance indebtedness on terms acceptable to us or at all; and

- •

- we may be limited in our ability to react to competitive pressures.

As of June 30, 2010, our consolidated long-term debt and our share of the debt of our unconsolidated affiliates represented approximately 55% of our total capitalization, comprised of debt and balance sheet equity.

Changes in our creditworthiness may affect the value of our common shares

Changes to our perceived creditworthiness may affect the market price or value and the liquidity of our common shares. The interest rate we pay on our credit facility may increase if certain credit ratios deteriorate.

Future issuances of our common shares could result in dilution

Our articles of incorporation authorize the issuance of an unlimited number of common shares for such consideration and on such terms and conditions as are established by our board of directors without the approval of any of our shareholders. We may issue additional common shares in connection with a future financing or acquisition. The issuance of additional common shares may dilute an investor's investment in us and reduce cash available for distribution per common share.

Investment eligibility

There can be no assurance that our common shares will continue to be qualified investments under relevant Canadian tax laws for trusts governed by registered retirement savings plans, registered retirement income funds, deferred profit sharing plans, registered education savings plans, registered disability savings plans and tax-free savings accounts.

We are subject to Canadian tax

As a Canadian corporation, we are generally subject to Canadian federal, provincial and other taxes, and dividends paid by us are generally subject to Canadian withholding tax if paid to a shareholder that is not a resident of Canada. We completed our initial public offering on the TSX in November 2004. At the time of the initial public offering, our public security was an IPS. Each IPS was comprised of one common share and Cdn$5.767 principal value of 11% subordinated notes due 2016. In the fourth quarter of 2009, we converted to a traditional common share company through a shareholder approved plan of arrangement in which each IPS was exchanged for one of our new common shares. Our new common shares were listed and posted for trading on the TSX commencing on December 2, 2009 and trade under the symbol "ATP," and the former IPSs, which traded under the symbol "ATP.UN," were delisted at that time. In connection with our conversion from an IPS structure to a traditional common share structure and the related reorganization of our organizational structure, we received a note from our primary U.S. holding company (the "Intercompany Note"). We are required to include in computing our taxable income interest on the Intercompany Note. We expect that our existing tax attributes initially will be available to offset this income inclusion such that it will not result in an immediate material increase to our liability for Canadian taxes. However, once we fully utilize our existing tax attributes (or if, for any reason, these attributes were not available to us), our

19

Canadian tax liability would materially increase. Although we intend to explore potential opportunities in the future to preserve the tax efficiency of our structure, no assurances can be given that our Canadian tax liability will not materially increase at that time.

Other Canadian federal income tax risks

There can be no assurance that Canadian federal income tax laws and Canada Revenue Agency ("CRA") administrative policies respecting the Canadian federal income tax consequences generally applicable to us, to our subsidiaries, or to a holder of common shares will not be changed in a manner which adversely affects holders of our common shares.

Our prior and current structure may be subject to additional U.S. federal income tax liability

Under our prior IPS structure, we treated the subordinated notes as debt for U.S. federal income tax purposes. Accordingly, we deducted the interest payments on the subordinated notes and reduced our net taxable income treated as "effectively connected income" for U.S. federal income tax purposes. Under our current structure, our subsidiaries that are incorporated in the United States are subject to U.S. federal income tax on their income at regular corporate rates (currently as high as 35%, plus state and local taxes), and our U.S. holding company will claim interest deductions with respect to the Intercompany Note in computing its income for U.S. federal income tax purposes. To the extent this interest expense is disallowed or is otherwise not deductible, the U.S. federal income tax liability of our U.S. holding company will increase, which could materially affect the after-tax cash available to distribute to us. While we received advice from our U.S. tax counsel, based on certain representations by us and our U.S. holding company and determinations made by our independent advisors, as applicable, that the subordinated notes and the Intercompany Note should be treated as debt for U.S. federal income tax purposes, it is possible that the Internal Revenue Service ("IRS") could successfully challenge those positions and assert that subordinated notes or the Intercompany Note should be treated as equity rather than debt for U.S. federal income tax purposes. In this case, the otherwise deductible interest on the subordinated notes or the Intercompany Note would be treated as non-deductible distributions and, in the case of the Intercompany Note, would be subject to U.S. withholding tax to the extent our U.S. holding company had current or accumulated earnings and profits. The determination of whether the subordinated notes and the U.S. holding company's indebtedness to us is debt or equity for U.S. federal income tax purposes is based on an analysis of the facts and circumstances. There is no clear statutory definition of debt for U.S. federal income tax purposes, and its characterization is governed by principles developed in case law, which analyzes numerous factors that are intended to identify the nature of the purported creditor's interest in the borrower. Furthermore, not all courts have applied this analysis in the same manner, and some courts have placed more emphasis on certain factors than other courts have. To the extent it were ultimately determined that our interest expenses on either the subordinated notes or the Intercompany Note were disallowed, our U.S. federal income tax liability for the applicable open tax years would materially increase, which could materially affect the after-tax cash available to us to distribute. Alternatively, the IRS could argue that the interest on the subordinated notes or the Intercompany Note exceeded or exceeds an arm's length rate, in which case only the portion of the interest expense that does not exceed an arm's length rate may be deductible and, in the case of the Intercompany Note, the remainder would be subject to U.S. withholding tax to the extent our U.S. holding company had current or accumulated earnings and profits. We have received advice from independent advisors that the interest rate on the subordinated notes and the Intercompany Note was and is, as applicable, commercially reasonable in the circumstances, but the advice is not binding on the IRS.