Attached files

| file | filename |

|---|---|

| EX-23.1 - CONSENT OF ERNST & YOUNG LLP - PLAINSCAPITAL CORP | dex231.htm |

Table of Contents

As filed with the Securities and Exchange Commission on August 12, 2010

Registration No. 333-161548

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 4

to

Form S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

PLAINSCAPITAL CORPORATION

(Exact Name of Registrant as Specified in its Charter)

| Texas | 6022 | 75-2182440 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

2323 Victory Ave., Suite 1400

Dallas, Texas 75219

(214) 252-4100

(Address, including zip code, and telephone number,

including area code, of registrant’s principal executive offices)

PlainsCapital Corporation

Attention: Alan B. White, Chief Executive Officer

2323 Victory Ave., Suite 1400

Dallas, Texas 75219

(214) 252-4100

(Name, address, including zip code, and telephone number,

including area code, of agent for service)

Copies to:

| Greg R. Samuel, Esq. Haynes and Boone, LLP

2323 Victory Avenue, Suite 700 Dallas, TX 75219 (214) 651-5000 Fax: (214) 200-0577 |

Richard D. Truesdell, Jr., Esq. Davis Polk & Wardwell LLP

450 Lexington Avenue New York, New York 10017 (212) 450-4000 Fax: (212) 450-3800 |

Approximate date of proposed sale to public: As soon as practicable on or after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | x (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Commission, acting pursuant to said section 8(a), may determine.

Table of Contents

Explanatory Note

As contemplated by Rule 479 promulgated under the Securities Act of 1933, as amended, this Pre-Effective Amendment No. 4 to our Registration Statement on Form S-1 is filed to update the registration statement to comply with the applicable requirements of the Securities Act of 1933, as amended, and the rules and regulations promulgated thereunder. We have not determined when, or if, we will make a public offering of our securities or whether any such offering will be pursuant to the prospectus contained herein. Accordingly, all statements in this Amendment No. 4 concerning our intention to offer for sale and list our securities, and our intended use of the proceeds from any such offer and sale, are subject to our determination to proceed with such offering.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities, and we are not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to completion, dated August 12, 2010

Preliminary Prospectus

shares

Common stock

This is an initial public offering of Common Stock by PlainsCapital Corporation. PlainsCapital Corporation is selling shares of our Common Stock and the selling shareholders, including certain members of our senior management, are selling shares of our Common Stock. The estimated initial public offering price is between $ and $ per share.

We have applied to list our Common Stock on the New York Stock Exchange under the symbol “PCB.”

| Per share | Total | |||||

| Initial public offering price |

$ | $ | ||||

| Underwriting discounts and commissions |

$ | $ | ||||

| Proceeds to PlainsCapital Corporation, before expenses |

$ | $ | ||||

| Proceeds to selling shareholders, before expenses |

$ | $ | ||||

We have granted the underwriters an option for a period of 30 days to purchase from us up to additional shares of Common Stock. We will not receive any proceeds from the sale of shares by the selling shareholders.

Following this offering, we will have two outstanding classes of common stock, Common Stock and Original Common Stock. The rights of the holders of the shares of Common Stock and Original Common Stock are identical, except with respect to conversion. Each share of Original Common Stock is convertible at any time at our election into one share of Common Stock. The Original Common Stock also will automatically convert into shares of Common Stock in certain circumstances. See “Description of capital stock” beginning on page 128.

Investing in our Common Stock involves a high degree of risk. See “Risk factors” beginning on page 8.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed on the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The Common Stock is not a deposit or savings account. The Common Stock is not insured by the Federal Deposit Insurance Corporation or any other governmental agency or instrumentality.

J.P. Morgan

Sole book-running manager

Macquarie Capital

Keefe, Bruyette & Woods

Stephens Inc.

, 2010

Table of Contents

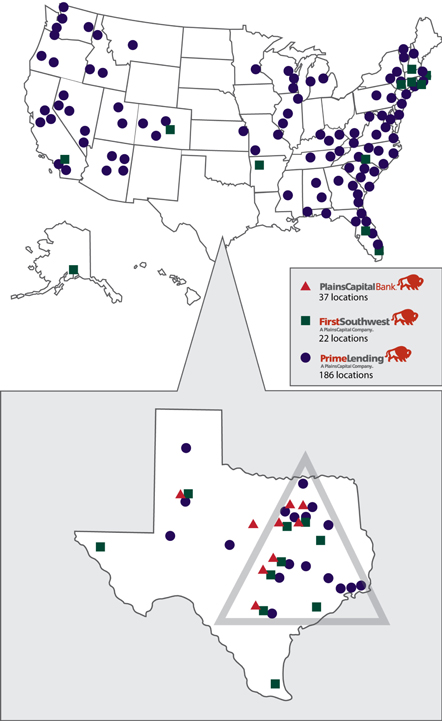

MARKETS OF PRINCIPAL SUBSIDIARIES

* PlainsCapital Bank Cayman Islands location not pictured.

Table of Contents

| 1 | ||

| 8 | ||

| 21 | ||

| 22 | ||

| 23 | ||

| 24 | ||

| 25 | ||

| Management’s discussion and analysis of financial condition and results of operations |

28 | |

| 71 | ||

| 94 | ||

| 101 | ||

| 123 | ||

| 125 | ||

| 128 | ||

| 132 | ||

| Certain material U.S. federal income and estate tax considerations for non-U.S. shareholders |

134 | |

| 136 | ||

| 141 | ||

| 141 | ||

| 141 | ||

| 141 | ||

| F-1 |

You should rely only on the information contained in this prospectus. We have not authorized anyone to provide you with information different from that contained in this prospectus. If you receive any information not authorized by us, then you should not rely on it.

We are offering to sell, and seeking offers to buy, shares of our Common Stock only in jurisdictions where offers and sales are permitted. The information contained in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of our Common Stock.

No action is being taken in any jurisdiction outside the United States to permit a public offering of the Common Stock or possession or distribution of this prospectus in that jurisdiction. Persons who come into possession of this prospectus in jurisdictions outside the United States are required to inform themselves about and to observe any restrictions as to this offering and the distribution of this prospectus applicable to that jurisdiction.

i

Table of Contents

Summary

This summary highlights certain information contained elsewhere in this prospectus. This summary is not complete and does not contain all of the information that you should consider before investing in our Common Stock. You should read this entire prospectus carefully, including the risks discussed under “Risk factors” and the financial statements and notes thereto included elsewhere in this prospectus. Some of the statements in this summary constitute forward-looking statements. See “Forward-looking statements.”

As used in this prospectus, unless the context otherwise indicates, the references to “we,” “us,” “our,” “our company” or “PlainsCapital” refer to PlainsCapital Corporation, a Texas corporation, and its consolidated subsidiaries as a whole, references to the “Bank” refer to PlainsCapital Bank, a Texas banking association (a wholly owned subsidiary of PlainsCapital Corporation), references to “First Southwest” refer to First Southwest Holdings, LLC, a Delaware limited liability company (a wholly owned subsidiary of the Bank) and its subsidiaries as a whole, references to “FSC” refer to First Southwest Company, a Delaware corporation (a wholly owned subsidiary of First Southwest Holdings, LLC) and references to “PrimeLending” refer to PrimeLending, a PlainsCapital Company, a Texas corporation (a wholly owned subsidiary of the Bank) and its subsidiaries as a whole. Statistical information concerning metropolitan markets are calculated based upon the applicable Metropolitan Statistical Area

Overview

We are a Texas corporation and a financial holding company registered under the Bank Holding Company Act of 1956 (as amended, the “Bank Holding Company Act”), as amended by the Gramm-Leach-Bliley Act of 1999 (the “Gramm-Leach-Bliley Act”). Five members of our senior executive team have worked together for the last 22 years. We have paid constant or increased dividends to our shareholders for each of the past 21 years and have been profitable for each of those years. For the years 1990 though 2009, our consolidated assets increased from $346.0 million to $4.6 billion and our consolidated net income increased from $2.0 million to $31.3 million, representing a compounded annual growth rate of 14% and 15%, respectively. As of June 30, 2010, we employed approximately 2,800 people in 245 locations in 36 states across our three business segments.

We provide the personalized client service and responsiveness most often associated with smaller financial institutions while offering the sophisticated products and services frequently associated with larger financial institutions. In addition to traditional banking services, we also provide wealth and investment management, treasury management, capital equipment leasing, residential mortgage lending, investment banking, public finance advisory services, fixed income sales and trading, asset management and correspondent clearing.

As of June 30, 2010, on a consolidated basis, we had total assets of approximately $4.9 billion, total deposits of approximately $3.7 billion, total loans, including loans held for sale, of approximately $3.7 billion and shareholders’ equity of approximately $434.1 million. We have experienced significant organic and acquisitive growth since our inception. Over the five-year period ending December 31, 2009, our net revenues, which we define as the sum of net interest income and noninterest income, increased 159.7% from $190.7 million to $495.3 million.

Business segments

We operate through three complementary business segments: banking, mortgage origination and financial advisory. We believe the diversification of income sources from each of our business segments mitigates business risk and provides opportunities for growth in varied economic conditions. We derive our revenue and net income primarily from our banking and mortgage origination segments, while the remainder of our revenue and net income is generated from our financial advisory segment. During 2009 and the first six months of 2010, approximately 35.9% and 38.5%, respectively, of our net revenue and 29.4% and 64.6%, respectively, of our net income, were derived from our banking segment. The mortgage origination segment generated approximately 43.3% and 43.3%, respectively, of our net revenue and 54.3% and 24.4%, respectively, of our net income during 2009 and the first six months of 2010. During 2009 and the first six months of 2010, the financial advisory segment contributed 20.8% and 18.2%, respectively, of our net revenue and 16.3% and 11.0%, respectively, of our net income.

1

Table of Contents

Banking. The Bank was the ninth largest bank headquartered in Texas based upon deposits as of June 30, 2009, and currently has 36 locations in the Austin, Dallas/Fort Worth, Lubbock and San Antonio markets. The Bank seeks to differentiate itself from its competitors by offering highly personalized service and tailoring its operating strategy to different markets. The Lubbock market serves as a strong source of core deposits for the Bank. In other markets, we operate a model focusing on middle-market companies and high net worth individuals. With $4.6 billion in assets as of June 30, 2010, and capital ratios that significantly exceed regulatory guidelines for “well capitalized” banks, we believe the Bank is well positioned for continued growth.

Mortgage origination. Our mortgage origination segment is operated through the Bank’s wholly owned subsidiary, PrimeLending, and offers a variety of residential mortgage loan products from offices in 32 states. We sell substantially all mortgage loans we originate in the secondary market and do not service these loans. Last year we originated approximately $5.7 billion in mortgage loans, setting a company record for the highest aggregate dollar amount of loans originated in a year. By dollar volume, approximately half of our loans originated during the first six months of 2010 were collateralized by residential real estate located in Texas. In 2009, according to Computer Business Methods, Inc., we ranked as the 20th largest retail mortgage loan producer in the United States and first in Texas for Federal Housing Administration (“FHA”) mortgage loan originations in Texas.

Financial advisory. Through our wholly owned subsidiary, First Southwest, we offer public finance, advisory and related services, which, for the six months ended June 30, 2010, represented a majority of the net revenues of First Southwest. Additionally, First Southwest offers corporate finance, investment banking, fixed income sales and trading services, asset management and correspondent clearing. Our financial advisory segment includes 24 offices nationwide, 12 of which are in Texas. We believe that the public finance industry is well positioned to capitalize on the federal government’s infrastructure stimulus legislation. Our public finance advisory business ranked first nationally, based upon number of issuances, and third nationally, based upon par volume of issuances, for the five-year period ending on June 30, 2010, according to information derived from MuniAnalytics. First Southwest currently has a financial advisory relationship with more than 1,600 public sector clients.

History and expansion

We were founded in Lubbock, Texas, in 1987 by current Chairman and Chief Executive Officer Alan B. White, other members of senior management and a group of investors. At the time we acquired the Bank in 1988, it had approximately $198.8 million in assets and was the fifth largest bank in the Lubbock market by deposits. Over the next 21 years, our market share and service offering grew, highlighted by the following events:

| • | In 1998, we expanded our product offerings beyond traditional banking services by entering the mortgage origination segment through the acquisition of a Lubbock-based mortgage company. |

| • | In 1999, we entered a new geographic market by expanding our mortgage origination operations through the acquisition of PrimeLending, a Dallas-based mortgage company with five locations in the Dallas-Fort Worth metroplex. The Bank also opened its first banking location outside of the West Texas region in the Turtle Creek neighborhood of Dallas. |

| • | In 2000, we moved our corporate headquarters to Dallas and opened our first banking location in Austin. |

| • | In 2004, the Bank entered the Fort Worth and San Antonio markets. |

| • | In 2008, we acquired First Southwest, a diversified private investment banking firm, in order to expand our financial advisory segment. |

Markets

We are based in Texas, a state with a population expected to grow 15.1% over the next 10 years compared to expected growth of 10.0% for the United States. If Texas were its own country, it would have the 10th largest economy in the world according to the Texas Comptroller of Public Accounts. Texas is tied with California in hosting the headquarters of Fortune 500 companies according to the August 2010 edition of Fortune published by cnnmoney.com and as of June 2010 had an unemployment rate that was 1.7 percentage points below the national average according to the U.S. Bureau of Labor Statistics.

2

Table of Contents

We have an expanding footprint in the “Texaplex,” the geographic region encompassing Dallas-Fort Worth, Houston, San Antonio and Austin. Of the 24 million Texas residents, four out of five live inside this region according to GMAC Real Estate. The Texaplex is projected to grow by 14 million people by the year 2030 according to GMAC Real Estate and represents the primary focus of our geographic growth efforts.

We also benefit from having our headquarters and a strong presence in Dallas. The Dallas-Fort Worth region ranks second for revenue generated from Fortune 500 companies and fourth nationally in the number of Fortune 500 corporate headquarters according to the North Texas Commission. To capture opportunities in this region, the Bank has 14 branches in the Dallas-Fort Worth market with $1.17 billion in deposits as of June 30, 2010.

In addition, we are a leader in the Lubbock market, with approximately $1.0 billion in deposits and a 19.2% deposit market share as of June 30, 2009. In the Lubbock market, we employ a traditional community bank marketing strategy. Our Lubbock deposit base has provided dependable funding for our historical growth.

Although each of our segments generated most of its revenue from within Texas during 2009, our mortgage origination and financial advisory segments also operate in markets outside of Texas. We intend to expand our existing footprint into other markets.

Business and growth strategies

We intend to grow by employing the following business strategies:

Focus on medium-sized businesses owned and operated by high net worth individuals. Unlike many of our competitors, the Bank has, with the exception of the Lubbock market, foregone a branch intensive, mass marketing retail strategy. Rather, we have focused, and we will continue to focus, the Bank’s growth efforts on privately held businesses with $5 million—$250 million in annual revenue. Often through a banking relationship with these types of businesses, we also develop business relationships with associated high net worth individuals and affluent households.

Emphasize customer responsiveness and personalized service. We provide clients with prompt, local decision-making concerning their borrowing and other financial needs. We entrust our experienced leadership teams with the authority and flexibility to enable us to implement and maintain the most effective solutions personalized for our customers. As a result, we intend to continue to capitalize on attracting new customers from our competitors who have not adequately met the dynamic and fast-paced financial needs of entrepreneurs and middle market businesses. As an example of our personalized services, our staff of couriers bring branch banking services to our business customers and other select high net worth customers.

Cross-sell products and realize operational synergies among our three businesses. We intend to continue to identify products and services to cross-sell to customers among our business segments. In addition, we expect to increase revenues by continuing to realize synergies among our three business segments. For example, the Bank provides our mortgage origination segment with a consistent source of funding, and First Southwest’s correspondent clearing business represents a dependable and significant source of deposits for the Bank.

Target hiring of experienced professionals that fit with our culture. We intend to continue to hire and retain highly experienced and qualified banking and financial professionals with successful track records and, for account managers, established relationships within our target customer population. Our historical growth has primarily been the result of hiring experienced bankers rather than acquiring banks. Our success has resulted from our knowledge of, and relationships with, our clients that our bankers have developed over time. We believe this knowledge and these relationships have enabled us to mitigate many of the credit difficulties that our competitors have experienced.

Corporate information

Our principal executive office is located at 2323 Victory Avenue, Suite 1400, Dallas, TX 75219. Our telephone number is (214) 252-4100 and our corporate website address is www.plainscapital.com. Information contained on our website is not incorporated by reference into this prospectus and you should not consider information contained on, or accessible through, our website as part of this prospectus.

3

Table of Contents

The offering

The following summary of the offering contains basic information about the offering and the Common Stock and is not intended to be complete. It does not contain all the information that is important to you. For a more complete understanding of the Common Stock, please refer to the section of this prospectus entitled “Description of capital stock.”

| Common Stock offered: | ||

| By PlainsCapital Corporation | shares. | |

| shares if the underwriters exercise their over-allotment option in full. | ||

| By the selling shareholders | shares. | |

| Total Common Stock offered | shares. | |

| Common Stock to be outstanding immediately after this offering: | ||

| Common Stock | shares. | |

| shares if the underwriters exercise their over-allotment option in full. | ||

| Original Common Stock |

shares.1 | |

| Total shares | shares. | |

| Use of proceeds | We estimate that our net proceeds from this offering, after deducting underwriting discounts, commissions and offering expenses, will be approximately $ , or approximately $ if the underwriters exercise their over-allotment option in full, based on an assumed initial offering price of $ per share (the midpoint of the estimated public offering price set forth on the cover page of this prospectus). We intend to use the net proceeds: | |

| • first, to redeem for approximately $92 million our Fixed Rate Cumulative Perpetual Preferred Stock, Series A and Fixed Rate Cumulative Perpetual Preferred Stock, Series B (the “Series A and Series B Preferred Stock”) that we issued to the U.S. Department of the Treasury (the “U.S. Treasury”) pursuant to the U.S. Treasury’s Capital Purchase Program; | ||

| • second, to repay approximately $ million of our existing debt under revolving lines of credit and term loans owed to an affiliate of J.P. Morgan Securities Inc.; and | ||

| • third, the remainder to support and enhance our operations. | ||

| The approval of the Board of Governors of the Federal Reserve System (the “Federal Reserve Board”) is required for the repurchase of these | ||

| 1 | No later than June 30, 2011, each share of Original Common Stock will convert into one share of Common Stock. See “Description of capital stock.” |

4

Table of Contents

| Series A and Series B Preferred Stock. We do not know when, or if, we will receive such approval. If we do not receive the necessary regulatory approval to repurchase the Series A and Series B Preferred Stock, or our Board of Directors subsequently determines not to repurchase the Series A and Series B Preferred Stock, then we intend to use approximately $ million of the net proceeds of the offering to repay existing debt owed to an affiliate of J.P. Morgan Securities Inc. and to use the remaining net proceeds to support and enhance operations. We will not receive any proceeds from the sales of our Common Stock by the Selling Shareholders. | ||

| Risk factors | You should carefully read and consider the information set forth under “Risk factors,” together with all of the other information set forth in this prospectus, before deciding to invest in shares of our Common Stock. | |

| Proposed New York Stock Exchange Listing | We have applied to list our Common Stock on the New York Stock Exchange (the “NYSE”) under the symbol “PCB.” Our Original Common Stock will not be listed. | |

| Conflicts of interest | Our indirect wholly owned subsidiary, First Southwest Company, is participating as a broker-dealer in this offering, and an affiliate of J.P. Morgan Securities Inc., one of the underwriters, will receive a portion of the net proceeds from this offering and, therefore, each has a “conflict of interest.” For more information, see “Conflicts of interest.” | |

The number of shares of our Common Stock and Original Common Stock to be outstanding after this offering based on 33,991,465 shares of our Original Common Stock outstanding as of August 1, 2010 will be , including 1,720,740 shares of Original Common Stock escrowed pursuant to the earnout provisions of the Merger Agreement (defined herein) but excluding 774,704 shares of common stock reserved for issuance upon the exercise of outstanding options at a weighted average exercise price of $9.58 per share.

Except as otherwise indicated, all information contained in this prospectus assumes:

| • | an initial offering price of $ per share (which is the midpoint of the range on the cover page of this prospectus); and |

| • | the underwriters’ option to purchase up to additional shares of Common Stock is not exercised. |

All share and per share information referenced through this prospectus has been retroactively adjusted to reflect the following actions effected on August 28, 2009:

| • | a redesignation of our then-outstanding shares of common stock as “Original Common Stock” (except for our audited consolidated financial statements for the years ended December 31, 2008 and 2007 and the notes thereto) and |

| • | a three-for-one stock split of our Original Common Stock and a change in the par value of our Original Common Stock from $10.00 per share to $0.001 per share. |

5

Table of Contents

Summary historical consolidated financial information

The following tables set forth our summary historical consolidated financial information for each of the periods indicated. The historical information as of and for the years ended December 31, 2005 through 2009 has been derived from our audited consolidated financial statements for the years ended December 31, 2005 through 2009, and our historical information for the six months ended June 30, 2010 and 2009 has been derived from our unaudited financial statements for the six months ended June 30, 2010 and 2009. The historical results set forth below and elsewhere in this prospectus are not necessarily indicative of our future performance.

The following selected historical financial information is only a summary and should be read in conjunction with “Use of proceeds,” “Capitalization,” “Management’s discussion and analysis of financial condition and results of operations,” “Certain relationships and related party transactions” and our audited and unaudited financial statements and related notes included elsewhere in this prospectus. The operating results and financial condition of First Southwest are included in the tables below as of January 1, 2009 and December 31, 2008, respectively.

SUMMARY CONSOLIDATED FINANCIAL DATA

PlainsCapital Corporation

| As of and for the Six Months Ended June 30, |

As of and for the Years Ended December 31, | ||||||||||||||||||||

| 2010 | 2009 | 2009 | 2008 | 2007 | 2006 | 2005 | |||||||||||||||

| Income Statement Data: |

|||||||||||||||||||||

| Total interest income |

$ | 108,360 | $ | 98,506 | $ | 202,823 | $ | 193,392 | $ | 220,895 | $ | 192,812 | $ | 148,636 | |||||||

| Total interest expense |

19,385 | 21,162 | 42,464 | 66,069 | 104,805 | 86,973 | 58,307 | ||||||||||||||

| Net interest income |

88,975 | 77,344 | 160,359 | 127,323 | 116,090 | 105,839 | 90,329 | ||||||||||||||

| Provision for loan losses |

33,200 | 24,763 | 66,673 | 22,818 | 5,517 | 5,049 | 5,516 | ||||||||||||||

| Net interest income after provision for loan losses |

55,775 | 52,581 | 93,686 | 104,505 | 110,573 | 100,790 | 84,813 | ||||||||||||||

| Total noninterest income |

177,628 | 162,031 | 334,908 | 119,066 | 84,281 | 101,776 | 110,027 | ||||||||||||||

| Total noninterest expense |

209,100 | 174,203 | 382,037 | 186,285 | 150,815 | 162,595 | 162,922 | ||||||||||||||

| Income from continuing operations before income taxes |

24,303 | 40,409 | 46,557 | 37,286 | 44,039 | 39,971 | 31,918 | ||||||||||||||

| Federal income tax provision |

7,596 | 14,286 | 15,009 | 12,725 | 14,904 | 13,624 | 12,612 | ||||||||||||||

| Income from continuing operations |

16,707 | 26,123 | 31,548 | 24,561 | 29,135 | 26,347 | 19,306 | ||||||||||||||

| Income from discontinued Amarillo operations (net-of-tax) |

— | — | — | — | — | — | 11,536 | ||||||||||||||

| Net income |

16,707 | 26,123 | 31,548 | 24,561 | 29,135 | 26,347 | 30,842 | ||||||||||||||

| Less: Net income attributable to noncontrolling interest |

370 | 56 | 220 | 437 | 543 | 608 | 786 | ||||||||||||||

| Net income attributable to PlainsCapital Corporation |

16,337 | 26,067 | 31,328 | 24,124 | 28,592 | 25,739 | 30,056 | ||||||||||||||

| Dividends on preferred stock and other |

2,778 | 2,938 | 5,704 | — | — | — | — | ||||||||||||||

| Income applicable to PlainsCapital Corporation common shareholders |

13,559 | 23,129 | 25,624 | 24,124 | 28,592 | 25,739 | 30,056 | ||||||||||||||

| Less: income applicable to participating securities |

839 | 1,528 | 1,585 | — | — | — | — | ||||||||||||||

| Income applicable to PlainsCapital Corporation common shareholders for basic earnings per common share |

$ | 12,720 | $ | 21,601 | $ | 24,039 | $ | 24,124 | $ | 28,592 | $ | 25,739 | $ | 30,056 | |||||||

| Per Share Data: |

|||||||||||||||||||||

| Income from continuing operations - basic |

$ | 0.43 | $ | 0.74 | $ | 0.83 | $ | 0.92 | $ | 1.10 | $ | 1.00 | $ | 0.73 | |||||||

| Discontinued operations - basic |

$ | — | $ | — | $ | — | $ | — | $ | — | $ | — | $ | 0.45 | |||||||

| Net income - basic |

$ | 0.43 | $ | 0.74 | $ | 0.83 | $ | 0.92 | $ | 1.10 | $ | 1.00 | $ | 1.18 | |||||||

| Weighted average shares outstanding - basic |

29,236,642 | 29,023,677 | 29,034,743 | 26,117,934 | 26,012,250 | 25,785,612 | 25,552,734 | ||||||||||||||

| Income from continuing operations - diluted |

$ | 0.41 | $ | 0.70 | $ | 0.77 | $ | 0.92 | $ | 1.09 | $ | 0.99 | $ | 0.71 | |||||||

| Discontinued operations - diluted |

$ | — | $ | — | $ | — | $ | — | $ | — | $ | — | $ | 0.45 | |||||||

| Net income - diluted |

$ | 0.41 | $ | 0.70 | $ | 0.77 | $ | 0.92 | $ | 1.09 | $ | 0.99 | $ | 1.16 | |||||||

| Weighted average shares outstanding - diluted |

33,471,955 | 33,084,885 | 33,351,626 | 26,256,165 | 26,195,211 | 26,030,505 | 25,874,433 | ||||||||||||||

| Book value per common share |

$ | 10.97 | $ | 10.70 | $ | 10.66 | $ | 9.99 | $ | 8.97 | $ | 8.06 | $ | 7.26 | |||||||

| Tangible book value per common share |

$ | 9.37 | $ | 9.10 | $ | 9.02 | $ | 8.82 | $ | 7.54 | $ | 6.63 | $ | 5.81 | |||||||

| Dividends per common share |

$ | 0.10 | $ | 0.10 | $ | 0.20 | $ | 0.20 | $ | 0.19 | $ | 0.19 | $ | 0.18 | |||||||

6

Table of Contents

SUMMARY CONSOLIDATED FINANCIAL DATA

PlainsCapital Corporation

| As of and for the Six Months Ended June 30, |

As of and for the Years Ended December 31, |

|||||||||||||||||||||||||||

| 2010 | 2009 | 2009 | 2008 | 2007 | 2006 | 2005 | ||||||||||||||||||||||

| Balance Sheet Data(1): |

||||||||||||||||||||||||||||

| Total assets |

$ | 4,924,570 | $ | 4,407,674 | $ | 4,570,720 | $ | 3,951,996 | $ | 3,182,863 | $ | 2,880,697 | $ | 2,690,305 | ||||||||||||||

| Loans held for sale |

701,046 | 405,671 | 432,202 | 198,866 | 100,015 | 126,839 | 194,712 | |||||||||||||||||||||

| Investment securities |

721,679 | 438,417 | 545,737 | 385,327 | 191,175 | 187,225 | 177,379 | |||||||||||||||||||||

| Loans, net of unearned income |

3,012,806 | 3,072,099 | 3,071,769 | 2,965,619 | 2,597,362 | 2,203,019 | 1,956,066 | |||||||||||||||||||||

| Allowance for loan losses |

(56,375 | ) | (31,778 | ) | (52,092 | ) | (40,672 | ) | (26,517 | ) | (24,722 | ) | (22,666 | ) | ||||||||||||||

| Goodwill and intangible assets, net |

50,409 | 49,925 | 51,496 | 36,568 | 37,307 | 37,136 | 37,362 | |||||||||||||||||||||

| Total deposits |

3,736,235 | 2,930,958 | 3,278,039 | 2,926,099 | 2,393,354 | 2,496,050 | 2,321,109 | |||||||||||||||||||||

| Capital lease obligations |

11,915 | 8,512 | 12,128 | 8,651 | 3,994 | 4,148 | 72 | |||||||||||||||||||||

| Notes payable |

67,450 | 70,180 | 68,550 | 151,014 | 40,256 | 35,860 | 46,460 | |||||||||||||||||||||

| Junior subordinated debentures |

67,012 | 67,012 | 67,012 | 67,012 | 51,548 | 51,548 | 51,548 | |||||||||||||||||||||

| PlainsCapital Corporation shareholders’ equity |

434,056 | 422,428 | 422,500 | 399,815 | 233,890 | 209,332 | 186,431 | |||||||||||||||||||||

| Performance Ratios: |

||||||||||||||||||||||||||||

| Return on average shareholders’ equity |

7.74 | % | 12.91 | % | 7.50 | % | 7.61 | % | 12.98 | % | 13.20 | % | 17.42 | % | ||||||||||||||

| Return on average assets |

0.69 | % | 1.25 | % | 0.71 | % | 0.68 | % | 0.95 | % | 0.95 | % | 1.19 | % | ||||||||||||||

| Net interest margin (taxable equivalent)(2) |

4.11 | % | 4.10 | % | 4.00 | % | 4.17 | % | 4.27 | % | 4.36 | % | 3.96 | % | ||||||||||||||

| Efficiency ratio(3) |

78.43 | % | 72.77 | % | 77.14 | % | 75.93 | % | 75.40 | % | 78.20 | % | 81.19 | % | ||||||||||||||

| Asset Quality Ratios: |

||||||||||||||||||||||||||||

| Total nonperforming assets to total loans and other real estate |

3.00 | % | 2.14 | % | 2.88 | % | 1.96 | % | 0.92 | % | 0.66 | % | 1.11 | % | ||||||||||||||

| Allowance for loan losses to nonperforming loans |

77.99 | % | 59.44 | % | 75.47 | % | 86.87 | % | 153.81 | % | 226.79 | % | 119.43 | % | ||||||||||||||

| Allowance for loan losses to total loans |

1.87 | % | 1.03 | % | 1.70 | % | 1.37 | % | 1.02 | % | 1.12 | % | 1.16 | % | ||||||||||||||

| Net charge-offs to average loans outstanding(4) |

1.93 | % | 2.26 | % | 1.82 | % | 0.37 | % | 0.16 | % | 0.15 | % | 0.26 | % | ||||||||||||||

| Capital Ratios: |

||||||||||||||||||||||||||||

| Leverage ratio |

9.41 | % | 10.43 | % | 9.45 | % | 12.71 | % | 8.06 | % | 8.22 | % | 7.92 | % | ||||||||||||||

| Tier 1 risk-based capital ratio |

12.10 | % | 12.14 | % | 12.10 | % | 12.83 | % | 8.99 | % | 9.27 | % | 9.24 | % | ||||||||||||||

| Total risk-based capital ratio |

13.90 | % | 13.58 | % | 13.90 | % | 14.53 | % | 10.67 | % | 10.91 | % | 10.97 | % | ||||||||||||||

| Equity to assets ratio |

8.81 | % | 9.58 | % | 9.24 | % | 10.12 | % | 7.35 | % | 7.27 | % | 6.93 | % | ||||||||||||||

| Dividend payout ratio(5) |

25.05 | % | 14.62 | % | 26.40 | % | 22.02 | % | 17.26 | % | 19.06 | % | 15.33 | % | ||||||||||||||

| Tangible common equity to tangible assets |

6.05 | % | 6.53 | % | 6.25 | % | 7.04 | % | 6.25 | % | 6.06 | % | 5.62 | % | ||||||||||||||

| * | Annualized for interim periods. |

| (1) | Balance sheet includes First Southwest as of December 31, 2008. |

| (2) | Net interest income divided by average interest-earning assets. |

| (3) | Noninterest expenses divided by the sum of total noninterest income and net interest income for the year. |

| (4) | Average loans outstanding exclude loans held for sale. |

| (5) | Total dividends to common shares paid divided by net income attrubutable to PlainsCapital Corporation for the year. |

7

Table of Contents

Risk factors

Investing in our Common Stock involves a high degree of risk. You should consider carefully the following risk factors and the other information in this prospectus (including our consolidated financial statements and related notes appearing at the end of this prospectus) before you decide to purchase our Common Stock. The risks described below are those that we believe are the material risks we face currently, but are not the only risks facing us and our business prospects. If any of the events contemplated by the following discussion should occur, our business, financial condition and operating results could be adversely affected. As a result, the trading price of our Common Stock could decline and you could lose part or all of your investment.

Risks related to our business

Recent negative developments in the financial industry and the domestic and international credit markets may adversely affect our operations and results.

The U.S. and global economies have suffered a dramatic downturn during the past few years, which has negatively impacted many industries, including the financial industry. As a result, commercial as well as consumer loan portfolio performances have deteriorated at many financial institutions, and the competition for deposits and quality loans has increased significantly. In addition, the values of real estate collateral supporting many commercial loans and home mortgages have declined and may continue to decline, which has contributed to a greater degree of loan defaults. Financial institutions have also been particularly impacted by the lack of liquidity and loss of confidence in the financial sector. These factors collectively have negatively impacted our business, financial condition and results of operations, including decreased net income due to increased provisions for loan losses, and there is no guarantee or clear indication of when market conditions will improve.

In response to some of these concerns, the federal government has adopted significant new laws and regulations relating to financial institutions, including, without limitation, the Emergency Economic Stabilization Act of 2008 (the “EESA”), the American Recovery and Reinvestment Act of 2009 (the “ARRA”) and the Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Dodd-Frank Act”). Numerous other actions have been taken by the Federal Reserve Board, the U.S. Congress, the U.S. Treasury, the Federal Deposit Insurance Corporation (the “FDIC”), the Securities and Exchange Commission (the “SEC”) and others to address the current liquidity and credit crisis, and we cannot predict the full effect of these actions or any future regulatory reforms. Negative developments in the financial industry and the domestic and international credit markets, and the impact of new or future legislation in response to those developments, may negatively impact our operations by restricting our business operations, including our ability to originate or sell loans and attract and retain experienced personnel, and adversely impact our financial performance.

A further adverse change in real estate market values may result in losses and otherwise adversely affect our profitability.

As of June 30, 2010, approximately 50% of our loan portfolio was comprised of loans with real estate as a primary or secondary component of collateral. The real estate collateral in each case provides an alternate source of repayment in the event of default by the borrower and may deteriorate in value during the time the credit is extended. The recent negative developments in the financial industry and economy as a whole have adversely affected real estate market values generally and in our market areas in Texas specifically and may continue to decline. A further decline in real estate values could further impair the value of our collateral and our ability to sell the collateral upon any foreclosure. In the event of a default with respect to any of these loans, the amounts we receive upon sale of the collateral may be insufficient to recover the outstanding principal and interest on the loan. As a result, our profitability and financial condition may be adversely affected by a further decrease in real estate market values.

If our allowance for loan losses is insufficient to cover actual loan losses, our earnings will be adversely affected.

As a lender, we are exposed to the risk that our loan customers may not repay their loans according to the terms of these loans, and the collateral securing the payment of these loans may be insufficient to fully compensate us for the outstanding balance of the loan plus the costs to dispose of the collateral. We may experience significant loan losses that may have a material adverse effect on our operating results and financial condition.

8

Table of Contents

We maintain an allowance for loan losses intended to cover loan losses inherent in our loan portfolio. In determining the size of the allowance, we rely on an analysis of our loan portfolio, our experience and our evaluation of general economic conditions. We also make various assumptions and judgments about the collectibility of our loan portfolio, including the diversification by industry of our commercial loan portfolio, the effect of changes in the economy on real estate and other collateral values, the results of recent regulatory examinations, the effects on the loan portfolio of current economic indicators and their probable impact on borrowers, the amount of charge-offs for the period and the amount of non-performing loans and related collateral security. If our assumptions prove to be incorrect, our current allowance may not be sufficient and adjustments may be necessary to allow for different economic conditions or adverse developments in our loan portfolio. Material additions to the allowance for loan losses would materially decrease our net income and adversely affect our financial condition generally.

In addition, federal and state regulators periodically review our allowance for loan losses and may require us to increase our provision for loan losses or recognize additional loan charge-offs, based on judgments different than our own. Any increase in our allowance for loan losses or loan charge-offs required by these regulatory agencies could have a material adverse effect on our operating results and financial condition.

Our geographic concentration may magnify the adverse effects and consequences of any regional or local economic downturn.

We conduct our operations primarily in Texas. Substantially all of the real estate loans in our loan portfolio are secured by properties located in Texas, with more than 75% secured by properties located in the Dallas/Fort Worth and Austin/San Antonio markets. Likewise, substantially all of the real estate loans in our loan portfolio are made to borrowers who live and conduct business in Texas. In addition, mortgage origination fee income is heavily dependent on economic conditions in Texas. During the first six months of 2010, approximately one-third by dollar volume of our mortgage loans originated were collateralized by properties located in Texas. Our businesses are affected by general economic conditions such as inflation, recession, unemployment and many other factors beyond our control. Adverse economic conditions in Texas may result in a reduction in the value of the collateral securing our loans. Any regional or local economic downturn that affects Texas or existing or prospective property or borrowers in Texas may affect us and our profitability more significantly and more adversely than our competitors that are less geographically concentrated.

Our business is subject to interest rate risk, and fluctuations in interest rates may adversely affect our earnings, capital levels and overall results.

The majority of our assets are monetary in nature and, as a result, we are subject to significant risk from changes in interest rates. Changes in interest rates may impact our net interest income as well as the valuation of our assets and liabilities. Our earnings are significantly dependent on our net interest income, which is the difference between interest income on interest-earning assets, such as loans and securities, and interest expense on interest-bearing liabilities, such as deposits and borrowings. We expect to periodically experience “gaps” in the interest rate sensitivities of our assets and liabilities, meaning that either our interest-bearing liabilities will be more sensitive to changes in market interest rates than our interest-earning assets, or vice versa. In either event, if market interest rates should move contrary to our position, this “gap” may work against us, and our earnings may be adversely affected.

An increase in the general level of interest rates may also, among other things, adversely affect the demand for loans and our ability to originate loans. In particular, if mortgage interest rates increase, the demand for residential mortgage loans and the refinancing of residential mortgage loans will likely decrease, which will have an adverse effect on our income generated from mortgage origination activities. Conversely, a decrease in the general level of interest rates, among other things, may lead to prepayments on our loan and mortgage-backed securities portfolios and increased competition for deposits. Accordingly, changes in the general level of market interest rates may adversely affect our net yield on interest-earning assets, loan origination volume and our overall results.

9

Table of Contents

Although our asset-liability management strategy is designed to control and mitigate exposure to the risks related to changes in the general level of market interest rates, market interest rates are affected by many factors outside of our control, including inflation, recession, unemployment, money supply, and international disorder and instability in domestic and foreign financial markets. We may not be able to accurately predict the likelihood, nature and magnitude of such changes or how and to what extent such changes may affect our business. We also may not be able to adequately prepare for, or compensate for, the consequences of such changes. Any failure to predict and prepare for changes in interest rates, or adjust for the consequences of these changes, may adversely affect our earnings and capital levels and overall results.

We are heavily dependent on dividends from our subsidiaries.

We are a bank holding company and a financial holding company engaged in the business of managing, controlling and operating our subsidiaries, including the Bank and the Bank’s subsidiaries, PrimeLending and First Southwest. We conduct no material business or other activity other than activities incidental to holding stock in the Bank. As a result, we rely substantially on the profitability of the Bank and dividends from the Bank to pay our operating expenses, to satisfy our obligations and the expenses and obligations of all of our subsidiaries and to pay dividends on our common stock and preferred stock. As with most financial institutions, the profitability of the Bank is subject to the fluctuating cost and availability of money, changes in interest rates and in economic conditions in general. The Bank has several subsidiaries, including PrimeLending and First Southwest, that may also contribute to its profitability and ability to pay dividends to us. However, if the Bank is unable to make cash distributions to us, then we may also be unable to obtain funds from PrimeLending and First Southwest, and we may be unable to satisfy our obligations or make distributions on our common stock and preferred stock.

We are subject to extensive supervision and regulation that could restrict our activities and impose financial requirements or limitations on the conduct of our business and limit our ability to generate income.

We are subject to extensive federal and state regulation and supervision, including that of the Federal Reserve Board, the Texas Department of Banking, the FDIC, the SEC and FINRA. Banking regulations are primarily intended to protect depositors’ funds, federal deposit insurance funds and the banking system as a whole, not security holders. Likewise, regulations promulgated by FINRA are primarily intended to protect customers of broker-dealer businesses rather than security holders. These regulations affect our lending practices, capital structure, investment practices, dividend policy and growth, among other things. Failure to comply with laws, regulations or policies could result in sanctions by regulatory agencies, damages, civil money penalties or reputational damage, which could have a material adverse effect on our business, financial condition and results of operations. While we have policies and procedures designed to prevent any such violations, there can be no assurance that such violations will not occur.

The U.S. Congress and federal regulatory agencies frequently revise banking and securities laws, regulations and policies. On July 21, 2010, President Obama signed into law the Dodd-Frank Act, which significantly alters the regulation of financial institutions and the financial services industry. The Dodd-Frank Act establishes the Bureau of Consumer Financial Protection (the “BCFP”) and requires the BCFP and other federal agencies to implement many provisions of the Dodd-Frank Act.

We expect that several aspects of the Dodd-Frank Act may affect our business, including, without limitation, higher deposit insurance premiums and new examinations, consumer protection rules, and disclosure and reporting requirements. At this time, it is difficult to predict the extent to which the Dodd-Frank Act or the resulting rules and regulations will affect our business. Compliance with these new laws and regulations likely will result in additional costs, which could be significant and may adversely impact our results of operations, financial condition, and liquidity.

During the second quarter of 2010, the Bank received its 2008 Community Reinvestment Act Performance Evaluation from the Federal Reserve. Despite “high satisfactory” or “outstanding” ratings on the various components of the Community Reinvestment Act (“CRA”) rating, the Federal Reserve lowered the Bank’s overall CRA rating from “satisfactory” to “needs to improve” as a result of alleged fair lending issues associated with our

10

Table of Contents

mortgage origination segment in prior years. Unless and until the Bank’s CRA rating improves, we, as a financial holding company, may not commence new activities that are “financial in nature” or acquire companies engaged in these activities. Our current CRA rating may also adversely affect the Bank’s ability to establish new branches.

In November 2009, the Federal Reserve Board issued a final rule that, effective July 1, 2010, prohibits financial institutions from charging consumers fees for paying overdrafts on automated teller machine and one-time debit card transactions, unless a consumer consents, or opts in, to the overdraft service for those types of transactions. Consumers must be provided a notice that explains the financial institution’s overdraft services, including the fees associated with the service, and the consumer’s choices. Because the Bank’s customers must provide advance consent to the overdraft service for automated teller machine and one-time debit card transactions, we cannot provide any assurance as to the ultimate impact of this rule on the amount of overdraft/insufficient funds charges reported in future periods.

We cannot predict whether or in what form any other proposed regulations or statutes will be adopted or the extent to which our business may be affected by any new regulation or statute. Such changes could subject our business to additional costs, limit the types of financial services and products we may offer and increase the ability of non-banks to offer competing financial services and products, among other things.

Our banking segment is subject to funding risks associated with its high deposit concentration and reliance on brokered deposits.

At June 30, 2010, our fifteen largest depositors, excluding First Southwest, our indirect wholly owned subsidiary, accounted for approximately 22.2% of our total deposits, and our five largest depositors, excluding First Southwest, accounted for approximately 14.7% of our total deposits. Brokered deposits at June 30, 2010 accounted for 12.2% of our total deposits. Loss of one or more of our largest Bank customers, a significant decline in our deposit balances due to ordinary course fluctuations related to these customers’ businesses, or a loss of a significant amount of our brokered deposits could adversely affect our liquidity. Additionally, such circumstances could require us to raise deposit rates in an attempt to attract new deposits, or purchase federal funds or borrow funds on a short-term basis at higher rates, which would adversely affect our results of operations. Under applicable regulations, if the Bank were no longer “well capitalized,” the Bank would not be able to accept broker deposits without the approval of the FDIC. See “Business—Government supervision and regulation—PlainsCapital Corporation.”

We are subject to losses due to fraudulent and negligent acts.

Our business is subject to potential losses resulting from fraudulent activities. Our banking segment is subject to the risk that our customers may engage in fraudulent activities, including fraudulent access to legitimate customer accounts or the use of a false identity to open an account, or the use of forged or counterfeit checks for payment. The banking segment is subject to the risk of higher than expected charge offs for loans it holds to maturity on its balance sheet if its borrowers supply fraudulent information. Such types of fraud may be difficult to prevent or detect, and we may not be able to recover the losses caused by such activities. Any such losses could have a material adverse effect on our business, financial condition and operating results.

In our mortgage origination segment, we rely heavily upon information supplied by third parties including the information contained in the loan application, property appraisal, title information and employment and income documentation. If any of this information is intentionally or negligently misrepresented and such misrepresentation is not detected prior to loan funding, the investment value of the loan may be significantly lower than expected. Whether a misrepresentation is made by the loan applicant, another third party or one of our own employees, we generally bear the risk of loss associated with the misrepresentation. A mortgage loan subject to a material misrepresentation is typically unsalable to investors in the secondary market. If we have already sold the loan when the material misrepresentation is discovered, then the loan is subject to repurchase, but we will often instead agree to indemnify the purchaser for any losses arising from such loan because in the general course of business we do not seek to hold for investment the mortgage loans we originate. Even though we may have rights against persons and entities who made or knew about the misrepresentation, such persons and entities are often difficult to locate, and it is often difficult to collect any monetary losses that we have suffered from them. We cannot assure you that we have detected, or will detect, all misrepresented information in our loan originations. If

11

Table of Contents

we experience a significant number of such fraudulent or negligent acts, our business, financial condition, liquidity and results of operations could be significantly harmed. We cannot assure you that we have detected or will detect all misrepresented information in our loan originations.

First Southwest engages in the underwriting of municipal and other tax-exempt and taxable debt securities. As an underwriter, First Southwest may be liable jointly and severally under federal, state and foreign securities laws for false and misleading statements concerning the securities, or the issuer of the securities, that it underwrites. We are sometimes brought into lawsuits based on actions of our correspondents. In addition, First Southwest may act as a fiduciary in other capacities. Liability under such laws or under common law fiduciary principles could have a material adverse effect on our business, financial condition, liquidity and results of operations.

Our mortgage origination segment is subject to investment risk on loans that it originates.

We intend to sell, and not hold for investment, all residential mortgage loans that we originate through PrimeLending. At times, however, we may originate a loan or execute an interest rate lock commitment (“IRLC”) with a customer pursuant to which we agree to originate a mortgage loan on a future date at an agreed-upon interest rate without having identified a purchaser for such loan or the loan underlying such IRLC. An identified purchaser may also decline to purchase a loan for a variety of reasons. In these instances, we will bear interest rate risk on an IRLC until, and unless, we are able to find a buyer for the loan underlying such IRLC and the risk of investment on a loan until, and unless, we are able to find a buyer for such loan. In addition, if a customer defaults on a mortgage payment shortly after the loan is originated, the purchaser of the loan may have a put right, whereby they can require us to repurchase the loan at the full amount paid by the purchaser. During periods of market downturn, we have at times chosen to hold mortgage loans when the identified purchasers have declined to purchase such loans because we could not obtain an acceptable substitute bid price for such loan. The failure of mortgage loans that we hold on our books to perform adequately will have a material adverse effect our financial condition, liquidity and results of operations.

First Southwest is subject to various risks associated with the securities industry, particularly those impacting the public finance industry.

Our financial advisory business, conducted primarily through First Southwest, is subject to uncertainties that are common in the securities industry. These uncertainties include:

| • | intense competition in the public finance and other sectors of the securities industry; |

| • | the volatility of domestic and international financial, bond and stock markets; |

| • | extensive governmental regulation; |

| • | litigation; and |

| • | substantial fluctuations in the volume and price level of securities. |

As a result, the revenues and operating results of our financial advisory segment may vary significantly from quarter to quarter and from year to year. In periods of low transaction volume such as in the current economic downturn, profitability is impaired because certain expenses remain relatively fixed. First Southwest is much smaller and has much less capital than many competitors in the securities industry. During the current market downturn, First Southwest’s business has been, and could continue to be, adversely affected in many ways. In addition, First Southwest is an operating subsidiary of the Bank, which means that its activities are limited to those that are permissible for the Bank.

We only recently became a public reporting company, and the obligations associated with being a public reporting company will require significant resources and management attention.

We have only recently become a public reporting company, and the expenses of being a public reporting company, including compliance with periodic disclosure requirements and the Sarbanes-Oxley Act of 2002, as amended (the “Sarbanes-Oxley Act”), are not fully reflected in our audited financial statements, and are not fully reflected in our unaudited interim financial statements. The Sarbanes-Oxley Act requires, among other things, our management to assess annually the effectiveness of our internal control over financial reporting beginning with our Annual Report on Form 10-K for the year ending December 31, 2010 and, if we complete this offering, our independent registered public accounting firm will be required to issue a report on our internal control over financial reporting. As a result, we will incur significant legal, accounting and other expenses that we did not previously incur.

12

Table of Contents

Financial markets are susceptible to disruptive events that may lead to little or no liquidity for auction rate bonds.

As of June 30, 2010, the Bank held in its securities portfolio auction rate bonds backed by pools of student loans under the Federal Family Education Loan Program with approximately $107.3 million in face value and an estimated fair market value of $95.9 million. The market for auction rate securities began experiencing disruptions in late 2007 through the failure of auctions for auction rate securities issued by leveraged closed-end funds, municipal governments, state instrumentalities and student loan companies backed by pools of student loans guaranteed by the U.S. Department of Education. These conditions will likely continue until either these securities are restructured or refunded or a liquid secondary market re-emerges for these securities. If the Bank were forced to sell these securities, our results of operations could be adversely affected. The estimated fair value of these auction rate bonds may further decline and require write-downs and losses as additional market information is obtained or in the event the current market conditions continue or worsen, in which case, our results of operations would be adversely affected.

The accuracy of our financial statements and related disclosures could be affected if we are exposed to actual conditions different from the judgments, assumptions or estimates used in our critical accounting policies.

The preparation of financial statements and related disclosure in conformity with accounting principles generally accepted in the United States of America (“GAAP”) requires us to make judgments, assumptions and estimates that affect the amounts reported in our consolidated financial statements and accompanying notes. Our critical accounting policies, which are included in this prospectus, describe those significant accounting policies and methods used in the preparation of our consolidated financial statements that are considered “critical” by us because they require judgments, assumptions and estimates that materially impact our consolidated financial statements and related disclosures. As a result, if future events differ significantly from the judgments, assumptions and estimates in our critical accounting policies, such events or assumptions could have a material impact on our audited consolidated financial statements and related disclosures.

We are dependent on our management team, and the loss of our senior executive officers or other key employees could impair our relationship with customers and adversely affect our business and financial results.

Our success is dependent, to a large degree, upon the continued service and skills of our existing management team, including Messrs. Alan B. White, Allen Custard, Jerry Schaffner, Hill A. Feinberg and Ms. Roseanna McGill and other key employees with long-term customer relationships. Our business and growth strategies are built primarily upon our ability to retain employees with experience and business relationships within their respective segments. The loss of one or more of these key personnel could have an adverse impact on our business because of their skills, knowledge of the market, years of industry experience and the difficulty of finding qualified replacement personnel. In addition, we currently do not have non-competition agreements with certain members of management and other key employees. If any of these personnel were to leave and compete with us, our business, financial condition, results of operations and growth could suffer.

Federal stimulus legislation imposes, and the Federal Reserve Board has published, certain executive compensation and corporate governance requirements that may adversely affect us and our business, including our ability to recruit and retain qualified employees, and by requiring reimbursement of disapproved executive compensation.

The EESA, as amended by the ARRA, includes extensive restrictions on our ability to pay retention awards, bonuses and other incentive compensation during the period in which we have any outstanding obligation arising under the Troubled Asset Relief Program (“TARP”) Capital Purchase Program. Many of the restrictions are not limited to our senior executives and cover other employees whose contributions to revenue and performance can be significant.

13

Table of Contents

In addition, on June 15, 2009, the U.S. Treasury adopted and made effective an interim final rule (the “Interim Rule”), which implemented and further expanded the limitations and restrictions imposed on executive compensation and corporate governance by the TARP Capital Purchase Program and the EESA, as amended by the ARRA. Pursuant to the Interim Rule, the U.S. Treasury established the Office of the Special Master for TARP Executive Compensation (the “Special Master”). The Interim Rule authorizes the Special Master to review the compensation structures and payments of, and to independently issue advisory opinions to, those financial institutions that have participated in the TARP Capital Purchase Program with respect to compensation structures and payments made by those financial institutions during the period that the financial institution received financial assistance under TARP. If the Special Master finds that a TARP recipient’s compensation structure or the payments that it has made to its employees are inconsistent with the purposes of the EESA or TARP, or otherwise contrary to the public interest, the Special Master may negotiate with the TARP recipient and the subject employee for appropriate reimbursements to the TARP recipient or the federal government. Because we are participating in the TARP Capital Purchase Program, the Special Master may review our compensation structure and payments that we have made to our employees.

These provisions and any future rules issued by the U.S. Treasury could adversely affect our ability to attract and retain management capable and motivated sufficiently to manage and operate our business through difficult economic and market conditions, especially if we are competing for management talent against institutions that are not subject to the same restrictions. If we are unable to attract and retain qualified employees to manage and operate our business, we may not be able to successfully execute our business and growth strategies. These provisions could also adversely affect our business by requiring us or our employees to reimburse the federal government for any executive compensation that the Special Master finds inconsistent with the purposes of EESA or TARP, or otherwise contrary to the public interest. For more information, see the section entitled “Executive compensation—Compensation discussion and analysis—TARP Capital Purchase Program.”

Our compensation practices are also subject to oversight by the federal banking agencies. On June 21, 2010, the Federal Reserve Board issued final guidance on incentive compensation policies that applies to all bank holding companies, such as PlainsCapital. The final guidance sets forth three key principles for incentive compensation arrangements that are designed to help ensure that incentive compensation plans do not encourage excessive risk-taking and are consistent with the safety and soundness of banking organizations. The three principles provide that a banking organization’s incentive compensation arrangements should:

| • | provide employees with incentives that do not encourage risk-taking beyond the organization’s ability to effectively identify and manage risks; |

| • | be compatible with effective controls and risk management; and |

| • | be supported by strong corporate governance. |

During the next stage of the final guidance, federal banking agencies will conduct reviews of incentive compensation practices at large, complex banking organizations for employees in certain business lines, such as mortgage originators. Any deficiencies in compensation practices that are identified may be incorporated into the organization’s supervisory ratings, which can affect its ability to make acquisitions or perform other actions. The final guidance provides that enforcement actions may be taken against a banking organization if its incentive compensation arrangements, related risk-management control or governance processes pose a risk to the organization’s safety and soundness and the organization is not taking prompt and effective measures to correct the deficiencies. The scope and content of the Federal Reserve Board’s policies on executive compensation are continuing to develop, and we expect that these policies will continue to evolve over time.

Our compensation structure will be further affected by the Dodd-Frank Act. The Dodd-Frank Act will impact the governance of executive compensation at public companies by implementing proxy disclosure requirements related to executive compensation, “say on pay” shareholder voting requirements, compensation committee independence and procedure requirements, additional proxy disclosures regarding executive compensation in relation to median compensation and in relation to the financial performance of the company (for example, the company will be required to show the relationship between compensation paid to executives and the company’s financial performance), and expanded clawback requirements applicable to incentive compensation. At this time, it is difficult to predict the extent to which the Dodd-Frank Act or the resulting rules and regulations will affect our business. It is also difficult to predict how the numerous executive compensation regulations discussed herein will work together.

14

Table of Contents

A decline in the market for advisory services could adversely affect our business and results of operations.

First Southwest has historically earned a significant portion of its revenues from advisory fees paid to it by its clients, in large part upon the successful completion of the client’s transaction. Financial advisory revenues represented a majority of First Southwest’s net revenues for the six months ended June 30, 2010. Unlike other investment banks, First Southwest earns most of its revenues from its advisory fees and, to a lesser extent, from other business activities such as underwriting. We expect that First Southwest’s reliance on advisory fees will continue for the foreseeable future, and a decline in advisory engagements or the market for advisory services generally would have an adverse effect on our business and results of operations.

An interruption in, or breach in security of, our information systems may result in a loss of customer business.

We rely heavily on communications and information systems to conduct our business. Any failure or interruption or breach in security of these systems could result in failures or disruptions in our customer relationship management, securities trading, general ledger, deposits, servicing or loan origination systems. If such failures or interruptions occur, we may not be able to adequately address them at all or in a timely fashion. The occurrence of any failures or interruptions could result in a loss of customer business, expose us to civil litigation and possible financial liability and could have a material adverse effect on our public relations, reputation, results of operations and financial condition.

Changes in government monetary policies may have an adverse effect on our earnings.

Our earnings are affected by domestic economic conditions and the monetary and fiscal policies of the U.S. government and its agencies. The monetary policies of the Federal Reserve Board have had, and are likely to continue to have, an important impact on the operating results of financial institutions through its power to implement national monetary policy in order to, among other things, curb inflation or combat a recession. The monetary policies of the Federal Reserve Board affect the levels of bank loans, investments and deposits through its control over the issuance of U.S. government securities, its regulation of the discount rate applicable to member banks and its influence over reserve requirements to which member banks are subject. We cannot predict the nature or impact of future changes in monetary and fiscal policies, and any such changes may have an adverse effect upon our liquidity, capital resources and results of operations. See the section entitled “Government supervision and regulation.”

Changes in accounting standards could impact our reported earnings and financial condition.

The accounting standards setters, including the Financial Accounting Standards Board (the “FASB”), the SEC and other regulatory bodies, periodically change the financial accounting and reporting standards that govern the preparation of our consolidated financial statements. These changes can be hard to predict and can materially impact how we record and report our financial condition and results of operations. In some cases, we could be required to apply a new or revised standard retroactively, which would result in the restatement of our prior period financial statements.

We face strong competition from other financial institutions and financial service companies, which may adversely affect our operations and financial condition.

Our banking and mortgage origination businesses face vigorous competition from banks and other financial institutions, including savings and loan associations, savings banks, finance companies and credit unions. A number of these banks and other financial institutions have substantially greater resources and lending limits, larger branch systems and a wider array of banking services than we do. We also compete with other providers of financial services, such as money market mutual funds, brokerage firms, consumer finance companies, insurance companies and governmental organizations, each of which may offer more favorable financing than we are able

15

Table of Contents

to provide. In addition, some of our non-bank competitors are not subject to the same extensive regulations that govern us. The banking business in Texas, particularly in the Austin, Dallas/Fort Worth, Lubbock and San Antonio metropolitan and surrounding areas, has become increasingly competitive over the past several years, and we expect the level of competition we face to further increase. Our profitability depends on our ability to compete effectively in these markets. This competition may reduce or limit our margins on banking services, reduce our market share and adversely affect our results of operations and financial condition.