Attached files

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

| þ | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended June 30, 2010

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Mirant Americas Generation, LLC

(Exact Name of Registrant as Specified in Its Charter)

Commission File Number: 333-63240

51-0390520 (I.R.S. Employer Identification No.)

Mirant North America, LLC

(Exact Name of Registrant as Specified in Its Charter)

Commission File Number: 333-134722

20-4514609 (I.R.S. Employer Identification No.)

Mirant Mid-Atlantic, LLC

(Exact Name of Registrant as Specified in Its Charter)

Commission File Number: 333-61668

58-2574140 (I.R.S. Employer Identification No.)

Delaware

(State or Other Jurisdiction of Incorporation or Organization of All Registrants)

1155 Perimeter Center West, Suite 100, Atlanta, Georgia 30338

(Address of Principal Executive Offices, Including Zip Code, of All Registrants)

(678) 579-5000

(Registrant’s Telephone Number, Including Area Code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

| Mirant Americas Generation, LLC |

þ Yes ¨ No | |||

| Mirant North America, LLC |

þ Yes ¨ No | |||

| Mirant Mid-Atlantic, LLC |

þ Yes ¨ No | |||

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

| Mirant Americas Generation, LLC |

¨ Yes ¨ No | |||

| Mirant North America, LLC |

¨ Yes ¨ No | |||

| Mirant Mid-Atlantic, LLC |

¨ Yes ¨ No | |||

Table of Contents

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large Accelerated Filer |

Accelerated Filer | Non-accelerated Filer |

Smaller Reporting Company | |||||

| Mirant Americas Generation, LLC |

¨ | ¨ | þ | ¨ | ||||

| Mirant North America, LLC |

¨ | ¨ | þ | ¨ | ||||

| Mirant Mid-Atlantic, LLC |

¨ | ¨ | þ | ¨ | ||||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

| Mirant Americas Generation, LLC |

¨ Yes þ No | |||

| Mirant North America, LLC |

¨ Yes þ No | |||

| Mirant Mid-Atlantic, LLC |

¨ Yes þ No | |||

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Section 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court.

| Mirant Americas Generation, LLC |

þ Yes ¨ No | |||

| Mirant North America, LLC |

þ Yes ¨ No | |||

| Mirant Mid-Atlantic, LLC |

þ Yes ¨ No | |||

All of the registrant’s outstanding membership interests are held by its parent and there are no membership interest held by nonaffiliates.

| Registrant |

Parent |

|||||

| Mirant Americas Generation, LLC |

Mirant Americas, Inc. | |||||

| Mirant North America, LLC |

Mirant Americas Generation, LLC | |||||

| Mirant Mid-Atlantic, LLC |

Mirant North America, LLC | |||||

This combined Form 10-Q is separately filed by Mirant Americas Generation, LLC, Mirant North America, LLC and Mirant Mid-Atlantic, LLC. Information contained in this combined Form 10-Q relating to Mirant Americas Generation, LLC, Mirant North America, LLC and Mirant Mid-Atlantic, LLC is filed by such registrant on its own behalf and each registrant makes no representation as to information relating to registrants other than itself.

NOTE: WHEREAS MIRANT AMERICAS GENERATION, LLC, MIRANT NORTH AMERICA, LLC AND MIRANT MID-ATLANTIC, LLC MEET THE CONDITIONS SET FORTH IN GENERAL INSTRUCTION H(1)(a) AND (b) OF FORM 10-Q, THIS COMBINED FORM 10-Q IS BEING FILED WITH THE REDUCED DISCLOSURE FORMAT PURSUANT TO GENERAL INSTRUCTION H(2).

Table of Contents

| Page | ||||

| i-iii | ||||

| 4 | ||||

| PART I—FINANCIAL INFORMATION | ||||

| Item 1. |

Interim Financial Statements (Unaudited): | |||

| Mirant Americas Generation, LLC | ||||

| 7 | ||||

| 8 | ||||

| 9 | ||||

| 10 | ||||

| Mirant North America, LLC | ||||

| 11 | ||||

| 12 | ||||

| 13 | ||||

| 14 | ||||

| Mirant Mid-Atlantic, LLC | ||||

| 15 | ||||

| 16 | ||||

| 17 | ||||

| 18 | ||||

| Combined Notes to Condensed Consolidated Financial Statements (Unaudited) |

19 | |||

| Item 2. |

Management’s Discussion and Analysis of Results of Operations and Financial Condition |

|||

| 67 | ||||

| 92 | ||||

| 102 | ||||

| Item 3. |

119 | |||

| Item 4. |

124 | |||

| PART II—OTHER INFORMATION | ||||

| Item 1. |

125 | |||

| Item 1A. |

125 | |||

| Item 6. |

Exhibits |

|||

| 137 | ||||

| 138 | ||||

| 139 | ||||

3

Table of Contents

Glossary of Certain Defined Terms

Ancillary Services—Services that ensure reliability and support the transmission of electricity from generation sites to customer loads. Such services include regulation service, reserves and voltage support.

Administrative Services Agreement—Management, personnel and services agreement with Mirant Services, effective January 3, 2006.

APSA—Asset Purchase and Sale Agreement dated June 7, 2000, between Mirant and Pepco.

Bankruptcy Code—United States Bankruptcy Code.

Bankruptcy Court—United States Bankruptcy Court for the Northern District of Texas, Fort Worth Division.

Baseload Generating Units—Units that satisfy minimum baseload requirements of the system and produce electricity at an essentially constant rate and run continuously.

CAIR—Clean Air Interstate Rule.

CAISO—California Independent System Operator.

Cal PX—California Power Exchange.

Clean Air Act—Federal Clean Air Act.

Clean Water Act—Federal Water Pollution Control Act.

CO2—Carbon dioxide.

Companies—Mirant Americas Generation, LLC, Mirant North America, LLC, Mirant Mid-Atlantic, LLC and their subsidiaries.

CPUC—California Public Utilities Commission.

DC Circuit—The United States Court of Appeals for the District of Columbia Circuit.

DWR—California Department of Water Resources.

EBITDA—Earnings before interest, taxes, depreciation and amortization.

EOB—California Electricity Oversight Board.

EPA—United States Environmental Protection Agency.

EPC—Engineering, procurement and construction.

Exchange Act—Securities Exchange Act of 1934.

Exchange Ratio—Right of Mirant Corporation stockholders to receive 2.835 shares of common stock of RRI Energy, Inc.

FASB—Financial Accounting Standards Board.

FERC—Federal Energy Regulatory Commission.

GAAP—United States generally accepted accounting principles.

GenOn Energy—GenOn Energy, Inc.

Gross Margin—Operating revenue less cost of fuel, electricity and other products, excluding depreciation and amortization.

Hart-Scott-Rodino Act—Hart-Scott-Rodino Antitrust Improvements Act of 1976, as amended.

Hudson Valley Gas—Hudson Valley Gas Corporation.

IBEW—International Brotherhood of Electrical Workers.

i

Table of Contents

Intermediate Generating Units—Units that meet system requirements that are greater than baseload and less than peaking.

ISO—Independent System Operator.

LIBOR—London InterBank Offered Rate.

MDE—Maryland Department of the Environment.

Merger Agreement—The agreement and plan of merger into which Mirant Corporation entered with RRI Energy, Inc. and RRI Energy Holdings, Inc. on April 11, 2010.

Mirant—Old Mirant prior to January 3, 2006, and New Mirant on or after January 3, 2006.

Mirant Americas—Mirant Americas, Inc.

Mirant Americas Energy Marketing—Mirant Americas Energy Marketing, LP.

Mirant Bowline—Mirant Bowline, LLC.

Mirant California—Mirant California, LLC.

Mirant Chalk Point—Mirant Chalk Point, LLC.

Mirant Delta—Mirant Delta, LLC.

Mirant Energy Trading—Mirant Energy Trading, LLC.

Mirant Kendall—Mirant Kendall, LLC.

Mirant Lovett—Mirant Lovett, LLC, owner of the former Lovett generating facility, which was shut down on April 19, 2008, and has been demolished.

Mirant MD Ash Management—Mirant MD Ash Management, LLC.

Mirant New York—Mirant New York, LLC.

Mirant NY-Gen—Mirant NY-Gen, LLC sold by Mirant North America in the second quarter of 2007.

Mirant Potomac River—Mirant Potomac River, LLC.

Mirant Potrero—Mirant Potrero, LLC.

Mirant Services—Mirant Services, LLC.

MW—Megawatt.

MWh—Megawatt hour.

NAAQS—National ambient air quality standard.

Net Capacity Factor—Actual production of electricity as a percentage of net dependable capacity to produce electricity.

New Mirant—Mirant Corporation on or after January 3, 2006.

NOL—Net operating loss.

NOV—Notice of violation.

NOx—Nitrogen oxides.

NSR—New source review.

NYISO—New York Independent System Operator.

NYMEX—New York Mercantile Exchange.

ii

Table of Contents

NYSE—New York Stock Exchange.

Old Mirant—MC 2005, LLC, known as Mirant Corporation prior to January 3, 2006.

OTC—Over-the-Counter.

Ozone Season—The period between May 1 and September 30 of each year.

Peaking Generating Units—Units used to meet demand requirements during the periods of greatest or peak load on the system.

Pepco—Potomac Electric Power Company.

PG&E—Pacific Gas & Electric Company.

PJM—PJM Interconnection, LLC.

Plan—The plan of reorganization that was approved in conjunction with Mirant’s and the Companies’ emergence from bankruptcy protection on January 3, 2006.

Power Sale, Fuel Supply and Services Agreement—Power sale, fuel supply and services agreement with Mirant Americas Energy Marketing, effective January 3, 2006. As of February 1, 2006, the agreement was transferred to Mirant Energy Trading.

Reserve Margin—Excess capacity over peak demand.

RGGI—Regional Greenhouse Gas Initiative.

RMR—Reliability-must-run.

RRI Energy—RRI Energy, Inc.

RTO—Regional Transmission Organization.

Scrubbers—Flue gas desulfurization emissions controls.

Securities Act—Securities Act of 1933, as amended.

SO2—Sulfur dioxide.

Spark Spread—The difference between the price received for electricity generated compared to the market price of the natural gas required to produce the electricity.

VaR—Value at risk.

Virginia DEQ—Virginia Department of Environmental Quality.

iii

Table of Contents

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING INFORMATION

In addition to historical information, the information presented in this combined Form 10-Q includes forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. These statements involve known and unknown risks and uncertainties and relate to future events, our future financial performance or our projected business results. In some cases, one can identify forward-looking statements by terminology such as “may,” “will,” “should,” “expect,” “intend,” “seek,” “plan,” “think,” “anticipate,” “estimate,” “predict,” “target,” “potential” or “continue” or the negative of these terms or other comparable terminology.

Forward-looking statements are only predictions. Actual events or results may differ materially from any forward-looking statement as a result of various factors, which include:

| • | legislative and regulatory initiatives regarding deregulation, regulation or restructuring of the industry of generating, transmitting and distributing electricity (the “electricity industry”); changes in state, federal and other regulations affecting the electricity industry (including rate and other regulations); changes in, or changes in the application of, environmental and other laws and regulations to which we and our subsidiaries and affiliates are or could become subject; |

| • | failure of our plants to perform as expected, including outages for unscheduled maintenance or repair; |

| • | environmental regulations (including the cumulative effect of many such regulations) that restrict our ability or render it uneconomic to operate our business, including regulations related to the emission of CO2 and other greenhouse gases; |

| • | increased regulation that limits our access to adequate water supplies and landfill options needed to support power generation or that increases the costs of cooling water and handling, transporting and disposing off-site of ash and other byproducts; |

| • | changes in market conditions, including developments in the supply, demand, volume and pricing of electricity and other commodities in the energy markets, including efforts to reduce demand for electricity and to encourage the development of renewable sources of electricity, and the extent and timing of the entry of additional competition in our markets; |

| • | continued poor economic and financial market conditions, including impacts on financial institutions and other current and potential counterparties, and negative impacts on liquidity in the power and fuel markets in which we hedge and transact; |

| • | increased credit standards, margin requirements, market volatility or other market conditions that could increase our obligations to post collateral beyond amounts that are expected, including additional collateral costs associated with OTC hedging activities as a result of new or proposed rules and regulations governing derivative financial instruments; |

| • | our inability to access effectively the OTC and exchange-based commodity markets or changes in commodity market conditions and liquidity, including as a result of new or proposed rules and regulations governing derivative financial instruments, which may affect our ability to engage in asset management and, for Mirant Americas Generation and Mirant North America, proprietary trading and fuel oil management activities as expected, or result in material gains or losses from open positions; |

| • | deterioration in the financial condition of Mirant Americas Generation’s, Mirant North America’s and Mirant Mid-Atlantic’s counterparties or Mirant Mid-Atlantic’s affiliates and the failure of such parties to pay amounts owed to us or to perform obligations or services due to us beyond collateral posted; |

| • | hazards customary to the power generation industry and the possibility that we may not have adequate insurance to cover losses resulting from such hazards or the inability of our insurers to provide agreed upon coverage; |

4

Table of Contents

| • | the expected timing and likelihood of completion of Mirant’s proposed merger with RRI Energy, including the timing, receipt and terms and conditions of required stockholder, governmental and regulatory approvals that may reduce anticipated benefits or cause the parties to abandon the merger; the ability of the parties to arrange debt financing in an amount sufficient to fund the refinancing contemplated in, and on terms consistent with, the Merger Agreement; the diversion of management’s time and attention from our ongoing business during the time we are seeking to complete the merger; the ability to maintain relationships with employees, customers and suppliers; the ability to integrate successfully the businesses and realize cost savings and any other synergies; and the risk that credit ratings of the combined company or its subsidiaries may be different from what the companies expect; |

| • | price mitigation strategies employed by ISOs or RTOs that reduce our revenue and may result in a failure to compensate our generating units adequately for all of their costs; |

| • | changes in the rules used to calculate capacity, energy and ancillary services payments; |

| • | legal and political challenges to the rules used to calculate capacity, energy and ancillary services payments; |

| • | volatility in our gross margin as a result of our accounting for derivative financial instruments used in our asset management and Mirant Americas Generation’s and Mirant North America’s proprietary trading and fuel oil management activities and volatility in our cash flow from operations resulting from working capital requirements, including collateral, to support our asset management and Mirant Americas Generation’s and Mirant North America’s proprietary trading and fuel oil management activities; |

| • | our ability to enter into intermediate and long-term contracts to sell power or to hedge our expected future generation of power, and to obtain adequate supply and delivery of fuel for our generating facilities, at our required specifications and on terms and prices acceptable to us; |

| • | our failure to utilize new or advancements in power generation technologies; |

| • | the inability of Mirant Americas Generation’s and Mirant North America’s operating subsidiaries to generate sufficient cash flow to support their operations; |

| • | our and our affiliates’ ability to borrow additional funds and access capital markets; |

| • | strikes, union activity or labor unrest; |

| • | our ability to obtain or develop capable leaders and our ability to retain or replace the services of key employees; |

| • | weather and other natural phenomena, including hurricanes and earthquakes; |

| • | the cost and availability of emissions allowances; |

| • | curtailment of operations and reduced prices for electricity resulting from transmission constraints; |

| • | the ability of Mirant Americas Generation and Mirant North America to execute the business plan in California, including entering into new tolling arrangements for their existing generating facilities; |

| • | our relative lack of geographic diversification of revenue sources resulting in concentrated exposure to the Mid-Atlantic market; |

| • | the ability of lenders under Mirant North America’s revolving credit facility to perform their obligations; |

| • | war, terrorist activities, cyberterrorism and inadequate cybersecurity, or the occurrence of a catastrophic loss; |

| • | our failure to provide a safe working environment for our employees and visitors thereby increasing our exposure to additional liability, loss of productive time, other costs and a damaged reputation; |

5

Table of Contents

| • | Mirant Americas Generation’s and Mirant North America’s consolidated indebtedness and the possibility that Mirant Americas Generation, Mirant North America or their subsidiaries may incur additional indebtedness in the future; |

| • | restrictions on the ability of Mirant Americas Generation’s subsidiaries to pay dividends, make distributions or otherwise transfer funds to Mirant Americas Generation, including restrictions on Mirant North America contained in its financing agreements and restrictions on Mirant Mid-Atlantic contained in its leveraged lease documents, which may affect Mirant Americas Generation’s ability to access the cash flows of those subsidiaries to make debt service and other payments; |

| • | restrictions on the ability of Mirant North America’s subsidiaries to pay dividends, make distributions or otherwise transfer funds to Mirant North America, including restrictions on Mirant Mid-Atlantic contained in its leveraged lease documents, which may affect Mirant North America’s ability to access the cash flows of those subsidiaries to make debt service and other payments; |

| • | our failure to comply with or monitor provisions of our loan agreements and debt may lead to a breach and, if not remedied, result in an event of default thereunder, which would limit access to needed capital and damage our reputation and relationships with financial institutions; and |

| • | the disposition of the pending litigation described in this combined Form 10-Q. |

Many of these risks, uncertainties and assumptions are beyond our ability to control or predict. All forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by cautionary statements contained throughout this report. Because of these risks, uncertainties and assumptions, you should not place undue reliance on these forward-looking statements. Furthermore, forward-looking statements speak only as of the date they are made.

Factors that Could Affect Future Performance

We undertake no obligation to update publicly or revise any forward-looking statements to reflect events or circumstances that may arise after the date of this report.

In addition to the discussion of certain risks in Management’s Discussion and Analysis of Results of Operations and Financial Condition and the accompanying combined Notes to Mirant Americas Generation, LLC’s, Mirant North America, LLC’s and Mirant Mid-Atlantic, LLC’s unaudited condensed consolidated financial statements, other factors that could affect the Companies’ future performance (business, results of operations or financial condition and cash flows) are set forth in the Companies’ 2009 Annual Report on Form 10-K and elsewhere in this Form 10-Q and are incorporated herein by reference.

Certain Terms

As used in this report, unless the context requires otherwise, “we,” “us,” “our,” and the “Companies” refer to Mirant Americas Generation, LLC, Mirant North America, LLC, Mirant Mid-Atlantic, LLC and their subsidiaries. In addition, as used in this report, unless the context requires otherwise, “Mirant Americas Generation” refers to Mirant Americas Generation, LLC and its subsidiaries, “Mirant North America” refers to Mirant North America, LLC and its subsidiaries and “Mirant Mid-Atlantic” refers to Mirant Mid-Atlantic, LLC and its subsidiaries.

6

Table of Contents

MIRANT AMERICAS GENERATION, LLC AND SUBSIDIARIES

(Wholly-Owned Indirect Subsidiary of Mirant Corporation)

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS (UNAUDITED)

| Three Months Ended June 30, |

Six Months Ended June 30, |

|||||||||||||||

| 2010 | 2009 | 2010 | 2009 | |||||||||||||

| (in millions) | ||||||||||||||||

| Operating revenues (including unrealized gains (losses) of $(231) million, $(44) million, $132 million and $211 million, respectively) |

$ | 244 | $ | 496 | $ | 1,124 | $ | 1,374 | ||||||||

| Cost of fuel, electricity and other products—nonaffiliate (including unrealized losses (gains) of $109 million, $(30) million, $120 million and $(29) million, respectively) |

271 | 148 | 475 | 417 | ||||||||||||

| Cost of fuel, electricity and other products—affiliate (including unrealized losses (gains) of $0, $0, $0 and $0, respectively) |

1 | 2 | 4 | 4 | ||||||||||||

| Total cost of fuel, electricity and other products |

272 | 150 | 479 | 421 | ||||||||||||

| Gross Margin (excluding depreciation and amortization) |

(28 | ) | 346 | 645 | 953 | |||||||||||

| Operating Expenses: |

||||||||||||||||

| Operations and maintenance—nonaffiliate |

93 | 93 | 182 | 181 | ||||||||||||

| Operations and maintenance—affiliate |

72 | 69 | 142 | 137 | ||||||||||||

| Depreciation and amortization |

50 | 34 | 99 | 68 | ||||||||||||

| Gain on sales of assets, net |

(1 | ) | (2 | ) | (3 | ) | (17 | ) | ||||||||

| Total operating expenses, net |

214 | 194 | 420 | 369 | ||||||||||||

| Operating Income (Loss) |

(242 | ) | 152 | 225 | 584 | |||||||||||

| Other Expense (Income), net: |

||||||||||||||||

| Interest expense |

49 | 34 | 99 | 72 | ||||||||||||

| Interest income |

— | — | — | (1 | ) | |||||||||||

| Other, net |

1 | — | 2 | 1 | ||||||||||||

| Total other expense, net |

50 | 34 | 101 | 72 | ||||||||||||

| Net Income (Loss) |

$ | (292 | ) | $ | 118 | $ | 124 | $ | 512 | |||||||

The accompanying combined notes are an integral part of these unaudited condensed consolidated financial statements.

7

Table of Contents

MIRANT AMERICAS GENERATION, LLC AND SUBSIDIARIES

(Wholly-Owned Indirect Subsidiary of Mirant Corporation)

CONDENSED CONSOLIDATED BALANCE SHEETS (UNAUDITED)

| At June 30, 2010 |

At December 31, 2009 |

|||||||

| (in millions) | ||||||||

| ASSETS |

||||||||

| Current Assets: |

||||||||

| Cash and cash equivalents |

$ | 431 | $ | 404 | ||||

| Funds on deposit |

176 | 180 | ||||||

| Receivables |

251 | 401 | ||||||

| Derivative contract assets |

1,687 | 1,416 | ||||||

| Inventories |

310 | 241 | ||||||

| Prepaid rent and other payments |

115 | 134 | ||||||

| Total current assets |

2,970 | 2,776 | ||||||

| Property, Plant and Equipment, net |

3,615 | 3,606 | ||||||

| Noncurrent Assets: |

||||||||

| Intangible assets, net |

166 | 171 | ||||||

| Derivative contract assets |

751 | 599 | ||||||

| Prepaid rent |

358 | 304 | ||||||

| Debt issuance costs, net |

25 | 29 | ||||||

| Other |

32 | 32 | ||||||

| Total noncurrent assets |

1,332 | 1,135 | ||||||

| Total Assets |

$ | 7,917 | $ | 7,517 | ||||

| LIABILITIES AND MEMBER’S EQUITY |

||||||||

| Current Liabilities: |

||||||||

| Current portion of long-term debt |

$ | 562 | $ | 74 | ||||

| Accounts payable and accrued liabilities |

489 | 646 | ||||||

| Payable—affiliate |

28 | 42 | ||||||

| Derivative contract liabilities |

1,440 | 1,150 | ||||||

| Other |

8 | 8 | ||||||

| Total current liabilities |

2,527 | 1,920 | ||||||

| Noncurrent Liabilities: |

||||||||

| Long-term debt, net of current portion |

1,999 | 2,556 | ||||||

| Derivative contract liabilities |

284 | 163 | ||||||

| Other |

59 | 49 | ||||||

| Total noncurrent liabilities |

2,342 | 2,768 | ||||||

| Commitments and Contingencies |

||||||||

| Member’s Equity: |

||||||||

| Member’s interest |

3,242 | 3,109 | ||||||

| Preferred stock in affiliate |

(194 | ) | (280 | ) | ||||

| Total member’s equity |

3,048 | 2,829 | ||||||

| Total Liabilities and Member’s Equity |

$ | 7,917 | $ | 7,517 | ||||

The accompanying combined notes are an integral part of these unaudited condensed consolidated financial statements.

8

Table of Contents

MIRANT AMERICAS GENERATION, LLC AND SUBSIDIARIES

(Wholly-Owned Indirect Subsidiary of Mirant Corporation)

CONDENSED CONSOLIDATED STATEMENTS OF MEMBER’S EQUITY (UNAUDITED)

| Member’s Interest |

Preferred Stock in Affiliate |

Total Member’s Equity | ||||||||

| (in millions) | ||||||||||

| Balance, December 31, 2009 |

$ | 3,109 | $ | (280 | ) | $ | 2,829 | |||

| Net income |

124 | — | 124 | |||||||

| Amortization of discount on preferred stock in affiliate |

9 | (9 | ) | — | ||||||

| Redemption of preferred stock |

— | 95 | 95 | |||||||

| Balance, June 30, 2010 |

$ | 3,242 | $ | (194 | ) | $ | 3,048 | |||

The accompanying combined notes are an integral part of these unaudited condensed consolidated financial statements.

9

Table of Contents

MIRANT AMERICAS GENERATION, LLC AND SUBSIDIARIES

(Wholly-Owned Indirect Subsidiary of Mirant Corporation)

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS (UNAUDITED)

| Six Months Ended June 30, |

||||||||

| 2010 | 2009 | |||||||

| (in millions) | ||||||||

| Cash Flows from Operating Activities: |

||||||||

| Net income |

$ | 124 | $ | 512 | ||||

| Adjustments to reconcile net income and changes in other operating assets and liabilities to net cash provided by operating activities: |

||||||||

| Depreciation and amortization |

104 | 73 | ||||||

| Gain on sales of assets, net |

(3 | ) | (17 | ) | ||||

| Unrealized gains on derivative contracts, net |

(12 | ) | (240 | ) | ||||

| Lower of cost or market inventory adjustments |

20 | 22 | ||||||

| Funds on deposit |

7 | 30 | ||||||

| Changes in other operating assets and liabilities |

(87 | ) | 4 | |||||

| Total adjustments |

29 | (128 | ) | |||||

| Net cash provided by operating activities |

153 | 384 | ||||||

| Cash Flows from Investing Activities: |

||||||||

| Capital expenditures |

(155 | ) | (376 | ) | ||||

| Proceeds from the sales of assets |

3 | 17 | ||||||

| Other |

— | 1 | ||||||

| Net cash used in investing activities |

(152 | ) | (358 | ) | ||||

| Cash Flows from Financing Activities: |

||||||||

| Redemption of preferred stock |

95 | 84 | ||||||

| Repayments of long-term debt |

(69 | ) | (41 | ) | ||||

| Net cash provided by financing activities |

26 | 43 | ||||||

| Net Increase in Cash and Cash Equivalents |

27 | 69 | ||||||

| Cash and Cash Equivalents, beginning of period |

404 | 354 | ||||||

| Cash and Cash Equivalents, end of period |

$ | 431 | $ | 423 | ||||

| Supplemental Cash Flow Disclosures: |

||||||||

| Cash paid for interest, net of amounts capitalized |

$ | 92 | $ | 63 | ||||

The accompanying combined notes are an integral part of these unaudited condensed consolidated financial statements.

10

Table of Contents

MIRANT NORTH AMERICA, LLC AND SUBSIDIARIES

(Wholly-Owned Indirect Subsidiary of Mirant Corporation)

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS (UNAUDITED)

| Three Months Ended June 30, |

Six Months Ended June 30, |

|||||||||||||||

| 2010 | 2009 | 2010 | 2009 | |||||||||||||

| (in millions) | ||||||||||||||||

| Operating revenues (including unrealized gains (losses) of $(231) million, $(44) million, $132 million and $211 million, respectively) |

$ | 244 | $ | 496 | $ | 1,124 | $ | 1,374 | ||||||||

| Cost of fuel, electricity and other products—nonaffiliate (including unrealized losses (gains) of $109 million, $(30) million, $120 million and $(29) million, respectively) |

271 | 148 | 475 | 417 | ||||||||||||

| Cost of fuel, electricity and other products—affiliate (including unrealized losses (gains) of $0, $0, $0 and $0, respectively) |

1 | 2 | 4 | 4 | ||||||||||||

| Total cost of fuel, electricity and other products |

272 | 150 | 479 | 421 | ||||||||||||

| Gross Margin (excluding depreciation and amortization) |

(28 | ) | 346 | 645 | 953 | |||||||||||

| Operating Expenses: |

||||||||||||||||

| Operations and maintenance—nonaffiliate |

93 | 93 | 182 | 181 | ||||||||||||

| Operations and maintenance—affiliate |

72 | 69 | 142 | 137 | ||||||||||||

| Depreciation and amortization |

50 | 34 | 99 | 68 | ||||||||||||

| Gain on sales of assets, net |

(1 | ) | (2 | ) | (3 | ) | (17 | ) | ||||||||

| Total operating expenses, net |

214 | 194 | 420 | 369 | ||||||||||||

| Operating Income (Loss) |

(242 | ) | 152 | 225 | 584 | |||||||||||

| Other Expense (Income), net: |

||||||||||||||||

| Interest expense |

19 | 5 | 39 | 12 | ||||||||||||

| Interest income |

— | — | — | (1 | ) | |||||||||||

| Other, net |

1 | — | 2 | 1 | ||||||||||||

| Total other expense, net |

20 | 5 | 41 | 12 | ||||||||||||

| Net Income (Loss) |

$ | (262 | ) | $ | 147 | $ | 184 | $ | 572 | |||||||

The accompanying combined notes are an integral part of these unaudited condensed consolidated financial statements.

11

Table of Contents

MIRANT NORTH AMERICA, LLC AND SUBSIDIARIES

(Wholly-Owned Indirect Subsidiary of Mirant Corporation)

CONDENSED CONSOLIDATED BALANCE SHEETS (UNAUDITED)

| At June 30, 2010 |

At December 31, 2009 |

|||||||

| (in millions) | ||||||||

| ASSETS |

||||||||

| Current Assets: |

||||||||

| Cash and cash equivalents |

$ | 431 | $ | 403 | ||||

| Funds on deposit |

176 | 180 | ||||||

| Receivables—nonaffiliate |

251 | 401 | ||||||

| Receivables—affiliate |

10 | 9 | ||||||

| Notes receivable—affiliate |

93 | 93 | ||||||

| Derivative contract assets |

1,687 | 1,416 | ||||||

| Inventories |

310 | 241 | ||||||

| Prepaid rent and other payments |

115 | 134 | ||||||

| Total current assets |

3,073 | 2,877 | ||||||

| Property, Plant and Equipment, net |

3,613 | 3,604 | ||||||

| Noncurrent Assets: |

||||||||

| Intangible assets, net |

166 | 171 | ||||||

| Derivative contract assets |

751 | 599 | ||||||

| Prepaid rent |

358 | 304 | ||||||

| Debt issuance costs, net |

19 | 23 | ||||||

| Other |

32 | 32 | ||||||

| Total noncurrent assets |

1,326 | 1,129 | ||||||

| Total Assets |

$ | 8,012 | $ | 7,610 | ||||

| LIABILITIES AND MEMBER’S EQUITY |

||||||||

| Current Liabilities: |

||||||||

| Current portion of long-term debt |

$ | 27 | $ | 74 | ||||

| Accounts payable and accrued liabilities |

465 | 621 | ||||||

| Payable—affiliate |

28 | 42 | ||||||

| Derivative contract liabilities |

1,440 | 1,150 | ||||||

| Other |

8 | 8 | ||||||

| Total current liabilities |

1,968 | 1,895 | ||||||

| Noncurrent Liabilities: |

||||||||

| Long-term debt, net of current portion |

1,152 | 1,174 | ||||||

| Derivative contract liabilities |

284 | 163 | ||||||

| Other |

59 | 49 | ||||||

| Total noncurrent liabilities |

1,495 | 1,386 | ||||||

| Commitments and Contingencies |

||||||||

| Member’s Equity: |

||||||||

| Member’s interest |

4,596 | 4,467 | ||||||

| Preferred stock in affiliate |

(47 | ) | (138 | ) | ||||

| Total member’s equity |

4,549 | 4,329 | ||||||

| Total Liabilities and Member’s Equity |

$ | 8,012 | $ | 7,610 | ||||

The accompanying combined notes are an integral part of these unaudited condensed consolidated financial statements.

12

Table of Contents

MIRANT NORTH AMERICA, LLC AND SUBSIDIARIES

(Wholly-Owned Indirect Subsidiary of Mirant Corporation)

CONDENSED CONSOLIDATED STATEMENTS OF MEMBER’S EQUITY (UNAUDITED)

| Member’s Interest |

Preferred Stock in Affiliate |

Total Member’s Equity |

||||||||||

| (in millions) | ||||||||||||

| Balance, December 31, 2009 |

$ | 4,467 | $ | (138 | ) | $ | 4,329 | |||||

| Net income |

184 | — | 184 | |||||||||

| Amortization of discount on preferred stock in affiliate |

4 | (4 | ) | — | ||||||||

| Redemption of preferred stock |

— | 95 | 95 | |||||||||

| Distribution to member |

(59 | ) | — | (59 | ) | |||||||

| Balance, June 30, 2010 |

$ | 4,596 | $ | (47 | ) | $ | 4,549 | |||||

The accompanying combined notes are an integral part of these unaudited condensed consolidated financial statements.

13

Table of Contents

MIRANT NORTH AMERICA, LLC AND SUBSIDIARIES

(Wholly-Owned Indirect Subsidiary of Mirant Corporation)

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS (UNAUDITED)

| Six Months Ended June 30, |

||||||||

| 2010 | 2009 | |||||||

| (in millions) | ||||||||

| Cash Flows from Operating Activities: |

||||||||

| Net income |

$ | 184 | $ | 572 | ||||

| Adjustments to reconcile net income and changes in other operating assets and liabilities to net cash provided by operating activities: |

||||||||

| Depreciation and amortization |

103 | 73 | ||||||

| Gain on sales of assets, net |

(3 | ) | (17 | ) | ||||

| Unrealized gains on derivative contracts, net |

(12 | ) | (240 | ) | ||||

| Lower of cost or market inventory adjustments |

20 | 22 | ||||||

| Funds on deposit |

7 | 30 | ||||||

| Changes in other operating assets and liabilities |

(86 | ) | 4 | |||||

| Total adjustments |

29 | (128 | ) | |||||

| Net cash provided by operating activities |

213 | 444 | ||||||

| Cash Flows from Investing Activities: |

||||||||

| Capital expenditures |

(155 | ) | (376 | ) | ||||

| Proceeds from the sales of assets |

3 | 17 | ||||||

| Other |

— | 1 | ||||||

| Net cash used in investing activities |

(152 | ) | (358 | ) | ||||

| Cash Flows from Financing Activities: |

||||||||

| Redemption of preferred stock |

95 | 84 | ||||||

| Repayments of long-term debt |

(69 | ) | (41 | ) | ||||

| Distribution to member |

(59 | ) | (60 | ) | ||||

| Net cash used in financing activities |

(33 | ) | (17 | ) | ||||

| Net Increase in Cash and Cash Equivalents |

28 | 69 | ||||||

| Cash and Cash Equivalents, beginning of period |

403 | 354 | ||||||

| Cash and Cash Equivalents, end of period |

$ | 431 | $ | 423 | ||||

| Supplemental Cash Flow Disclosures: |

||||||||

| Cash paid for interest, net of amounts capitalized |

$ | 33 | $ | 4 | ||||

The accompanying combined notes are an integral part of these unaudited condensed consolidated financial statements.

14

Table of Contents

MIRANT MID-ATLANTIC, LLC AND SUBSIDIARIES

(Wholly-Owned Indirect Subsidiary of Mirant Corporation)

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS (UNAUDITED)

| Three Months Ended June 30, |

Six Months Ended June 30, |

|||||||||||||||

| 2010 | 2009 | 2010 | 2009 | |||||||||||||

| (in millions) | ||||||||||||||||

| Operating revenues—nonaffiliate (including unrealized gains (losses) of $(97) million, $(30) million, $103 million and $145 million, respectively) |

$ | (39 | ) | $ | 44 | $ | 219 | $ | 266 | |||||||

| Operating revenues—affiliate (including unrealized gains (losses) of $(108) million, $26 million, $30 million and $93 million, respectively) |

209 | 347 | 690 | 797 | ||||||||||||

| Total operating revenues |

170 | 391 | 909 | 1,063 | ||||||||||||

| Cost of fuel, electricity and other products—nonaffiliate (including unrealized losses (gains) of $0, $0, $0 and $0, respectively) |

5 | 3 | 9 | 10 | ||||||||||||

| Cost of fuel, electricity and other products—affiliate (including unrealized losses (gains) of $112 million, $(4) million, $104 million and $(5) million, respectively) |

245 | 131 | 396 | 289 | ||||||||||||

| Total cost of fuel, electricity and other products |

250 | 134 | 405 | 299 | ||||||||||||

| Gross Margin (excluding depreciation and amortization) |

(80 | ) | 257 | 504 | 764 | |||||||||||

| Operating Expenses: |

||||||||||||||||

| Operations and maintenance—nonaffiliate |

70 | 57 | 135 | 117 | ||||||||||||

| Operations and maintenance—affiliate |

47 | 44 | 95 | 89 | ||||||||||||

| Depreciation and amortization |

36 | 24 | 69 | 48 | ||||||||||||

| Gain on sales of assets, net—affiliate |

(1 | ) | (2 | ) | (3 | ) | (10 | ) | ||||||||

| Total operating expenses, net |

152 | 123 | 296 | 244 | ||||||||||||

| Operating Income (Loss) |

(232 | ) | 134 | 208 | 520 | |||||||||||

| Other Expense, net: |

||||||||||||||||

| Interest expense |

— | 1 | 1 | 2 | ||||||||||||

| Other, net |

1 | — | 1 | — | ||||||||||||

| Total other expense, net |

1 | 1 | 2 | 2 | ||||||||||||

| Net Income (Loss) |

$ | (233 | ) | $ | 133 | $ | 206 | $ | 518 | |||||||

The accompanying combined notes are an integral part of these unaudited condensed consolidated financial statements.

15

Table of Contents

MIRANT MID-ATLANTIC, LLC AND SUBSIDIARIES

(Wholly-Owned Indirect Subsidiary of Mirant Corporation)

CONDENSED CONSOLIDATED BALANCE SHEETS (UNAUDITED)

| At June 30, 2010 |

At December 31, 2009 |

|||||||

| (in millions) | ||||||||

| ASSETS |

||||||||

| Current Assets: |

||||||||

| Cash and cash equivalents |

$ | 159 | $ | 125 | ||||

| Funds on deposit |

16 | 14 | ||||||

| Receivables—nonaffiliate |

17 | 27 | ||||||

| Receivables—affiliate |

178 | 187 | ||||||

| Derivative contract assets—nonaffiliate |

170 | 155 | ||||||

| Derivative contract assets—affiliate |

424 | 464 | ||||||

| Inventories |

116 | 117 | ||||||

| Prepaid rent |

96 | 96 | ||||||

| Other |

— | 18 | ||||||

| Total current assets |

1,176 | 1,203 | ||||||

| Property, Plant and Equipment, net |

3,023 | 3,000 | ||||||

| Noncurrent Assets: |

||||||||

| Goodwill, net |

616 | 616 | ||||||

| Other intangible assets, net |

135 | 138 | ||||||

| Derivative contract assets—nonaffiliate |

490 | 399 | ||||||

| Derivative contract assets—affiliate |

139 | 127 | ||||||

| Prepaid rent |

358 | 304 | ||||||

| Other |

17 | 20 | ||||||

| Total noncurrent assets |

1,755 | 1,604 | ||||||

| Total Assets |

$ | 5,954 | $ | 5,807 | ||||

| LIABILITIES AND EQUITY |

||||||||

| Current Liabilities: |

||||||||

| Current portion of long-term debt |

$ | 4 | $ | 4 | ||||

| Accounts payable and accrued liabilities |

96 | 168 | ||||||

| Payable—affiliate |

125 | 123 | ||||||

| Derivative contract liabilities—nonaffiliate |

11 | 4 | ||||||

| Derivative contract liabilities—affiliate |

363 | 374 | ||||||

| Contract retention liability |

127 | 112 | ||||||

| Other |

3 | 2 | ||||||

| Total current liabilities |

729 | 787 | ||||||

| Noncurrent Liabilities: |

||||||||

| Long-term debt, net of current portion |

19 | 21 | ||||||

| Derivative contract liabilities—nonaffiliate |

9 | 13 | ||||||

| Derivative contract liabilities—affiliate |

141 | 84 | ||||||

| Other |

19 | 16 | ||||||

| Total noncurrent liabilities |

188 | 134 | ||||||

| Commitments and Contingencies |

||||||||

| Member’s Equity: |

||||||||

| Member’s interest |

5,084 | 5,024 | ||||||

| Preferred stock in affiliate |

(47 | ) | (138 | ) | ||||

| Total member’s equity |

5,037 | 4,886 | ||||||

| Total Liabilities and Member’s Equity |

$ | 5,954 | $ | 5,807 | ||||

The accompanying combined notes are an integral part of these unaudited condensed consolidated financial statements.

16

Table of Contents

MIRANT MID-ATLANTIC, LLC AND SUBSIDIARIES

(Wholly-Owned Indirect Subsidiary of Mirant Corporation)

CONDENSED CONSOLIDATED STATEMENTS OF MEMBER’S EQUITY (UNAUDITED)

| Member’s Interest |

Preferred Stock in Affiliate |

Total Member’s Equity |

||||||||||

| (in millions) | ||||||||||||

| Balance, December 31, 2009 |

$ | 5,024 | $ | (138 | ) | $ | 4,886 | |||||

| Net income |

206 | — | 206 | |||||||||

| Amortization of discount on preferred stock in affiliate |

4 | (4 | ) | — | ||||||||

| Redemption of preferred stock |

— | 95 | 95 | |||||||||

| Distribution to member |

(150 | ) | — | (150 | ) | |||||||

| Balance, June 30, 2010 |

$ | 5,084 | $ | (47 | ) | $ | 5,037 | |||||

The accompanying combined notes are an integral part of these unaudited condensed consolidated financial statements.

17

Table of Contents

MIRANT MID-ATLANTIC, LLC AND SUBSIDIARIES

(Wholly-Owned Indirect Subsidiary of Mirant Corporation)

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS (UNAUDITED)

| Six Months Ended June 30, |

||||||||

| 2010 | 2009 | |||||||

| (in millions) | ||||||||

| Cash Flows from Operating Activities: |

||||||||

| Net income |

$ | 206 | $ | 518 | ||||

| Adjustments to reconcile net income and changes in other operating assets and liabilities to net cash provided by operating activities: |

||||||||

| Depreciation and amortization |

69 | 48 | ||||||

| Gain on sales of assets, net—affiliate |

(3 | ) | (10 | ) | ||||

| Unrealized gains on derivative contracts, net |

(29 | ) | (243 | ) | ||||

| Lower of cost or market inventory adjustments |

12 | 21 | ||||||

| Changes in other operating assets and liabilities |

(24 | ) | (56 | ) | ||||

| Total adjustments |

25 | (240 | ) | |||||

| Net cash provided by operating activities |

231 | 278 | ||||||

| Cash Flows from Investing Activities: |

||||||||

| Capital expenditures |

(144 | ) | (331 | ) | ||||

| Proceeds from the sales of assets |

4 | 9 | ||||||

| Other |

— | 1 | ||||||

| Net cash used in investing activities |

(140 | ) | (321 | ) | ||||

| Cash Flows from Financing Activities: |

||||||||

| Redemption of preferred stock |

95 | 84 | ||||||

| Repayment of long-term debt |

(2 | ) | (2 | ) | ||||

| Distribution to member |

(150 | ) | — | |||||

| Net cash provided by (used in) financing activities |

(57 | ) | 82 | |||||

| Net Increase in Cash and Cash Equivalents |

34 | 39 | ||||||

| Cash and Cash Equivalents, beginning of period |

125 | 125 | ||||||

| Cash and Cash Equivalents, end of period |

$ | 159 | $ | 164 | ||||

| Supplemental Cash Flow Disclosures: |

||||||||

| Cash paid for interest |

$ | 1 | $ | 1 | ||||

The accompanying combined notes are an integral part of these unaudited condensed consolidated financial statements.

18

Table of Contents

MIRANT AMERICAS GENERATION, LLC AND SUBSIDIARIES

MIRANT NORTH AMERICA, LLC AND SUBSIDIARIES

MIRANT MID-ATLANTIC, LLC AND SUBSIDIARIES

COMBINED NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED)

| A. | Description of Business and Accounting and Reporting Policies (Mirant Americas Generation, Mirant North America and Mirant Mid-Atlantic) |

Mirant Americas Generation and Mirant North America are competitive energy companies that produce and sell electricity in the United States. Mirant Americas Generation and Mirant North America own or lease 10,076 MW of net electric generating capacity in the Mid-Atlantic and Northeast regions and in California. Mirant Americas Generation and Mirant North America also operate an integrated asset management and energy marketing organization based in Atlanta, Georgia.

Mirant Mid-Atlantic operates and owns or leases 5,194 MW of net electric generating capacity in the Washington, D.C. area. Mirant Mid-Atlantic’s electric generating capacity is part of the 10,076 MW of net electric generating capacity of Mirant Americas Generation and Mirant North America. Mirant Mid-Atlantic’s generating facilities serve the PJM markets. The PJM ISO operates the largest centrally dispatched control area in the United States.

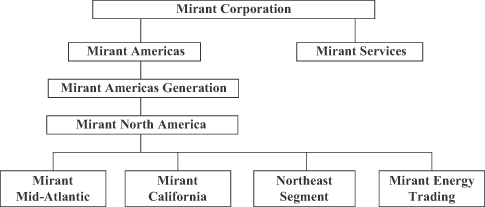

Mirant Americas Generation, Mirant North America and Mirant Mid-Atlantic are Delaware limited liability companies and indirect wholly-owned subsidiaries of Mirant Corporation. Mirant North America is a wholly-owned subsidiary of Mirant Americas Generation. Mirant Mid-Atlantic is a wholly-owned subsidiary of Mirant North America and an indirect wholly-owned subsidiary of Mirant Americas Generation. The chart below is a summary representation of the Companies’ organizational structure and is not a complete organizational chart of Mirant Corporation.

Mirant Americas Generation, Mirant North America and Mirant Mid-Atlantic have a number of service agreements for labor and administrative services with Mirant Services. See Note F for further discussion of arrangements with these related parties.

19

Table of Contents

Mirant’s Proposed Merger with RRI Energy

On April 11, 2010, Mirant entered into the Merger Agreement with RRI Energy and RRI Energy Holdings, Inc. (“Merger Sub”), a direct and wholly-owned subsidiary of RRI Energy. Upon the terms and subject to the conditions set forth in the Merger Agreement, which has been unanimously approved by each of the boards of directors of Mirant and RRI Energy, Merger Sub will merge with and into Mirant, with Mirant continuing as the surviving corporation and a wholly-owned subsidiary of RRI Energy. The merger is intended to qualify as a tax-free reorganization under the Internal Revenue Code of 1986, as amended, so that none of RRI Energy, Merger Sub, Mirant or any of the Mirant stockholders generally will recognize any gain or loss in the transaction, except that Mirant stockholders will recognize gain with respect to cash received in lieu of fractional shares of RRI Energy common stock. Pursuant to the Merger Agreement, upon the closing of the merger, each issued and outstanding share of Mirant common stock, including grants of restricted common stock, will automatically be converted into shares of common stock of RRI Energy based on the Exchange Ratio. Additionally, upon the closing of the merger, RRI Energy will be renamed GenOn Energy. Mirant stock options and other equity awards will generally convert upon completion of the merger into stock options and equity awards with respect to RRI Energy common stock, after giving effect to the Exchange Ratio. As a result of the merger, Mirant stockholders will own approximately 54% of the equity of the combined company and RRI Energy stockholders will own approximately 46%.

Completion of the merger is subject to various customary conditions, including, among others, (i) approval by RRI Energy stockholders of the issuance of RRI Energy common stock in the merger, (ii) adoption of the Merger Agreement by Mirant stockholders, (iii) effectiveness of the registration statement for the RRI Energy common stock to be issued in the merger, (iv) approval of the listing on the NYSE of the RRI Energy common stock to be issued in the merger, (v) expiration or termination of the applicable Hart-Scott-Rodino Act waiting period, (vi) receipt of all required regulatory approvals and (vii) consummation by GenOn Energy of debt financings in an amount sufficient to fund the refinancing transactions contemplated by, and on terms consistent with, the Merger Agreement.

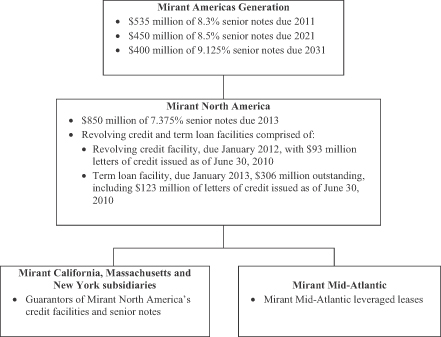

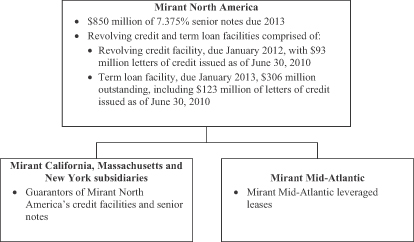

Among the refinancing transactions noted above, the completion of the merger is conditioned on GenOn Energy consummating certain debt financing transactions, including securing a new revolving credit facility. The new GenOn Energy debt financing and revolving credit facility will be used, in part, to redeem the Mirant North America senior notes and to repay and terminate the Mirant North America term loan and revolving credit facility. See Note D for additional information on Mirant North America’s debt.

Mirant and RRI Energy are in the process of arranging mutually acceptable debt financing as contemplated under the Merger Agreement. Mirant, together with RRI Energy, have entered into agreements pursuant to which financial institutions have committed to provide a $750 million to $1.0 billion five-year revolving credit facility, subject to customary conditions to closing, including:

| • | the consummation of the merger; |

| • | the receipt of at least $1.9 billion in gross cash proceeds from the issuance of senior unsecured notes and term loan borrowings; and |

| • | the closing of the credit facility on or before December 31, 2010. |

The revolving credit facility and term loan facility, and the subsidiary guarantees thereof, will be senior secured obligations of RRI Energy (proposed to be renamed GenOn Energy in connection with the merger) and certain of its subsidiaries; provided, however, that Mirant Americas Generation’s subsidiaries (other than Mirant Mid-Atlantic and Mirant Energy Trading and their subsidiaries) will guarantee the revolving credit facility and term loan only to the extent permitted under the indenture for the senior notes of Mirant Americas Generation. The participating financial institutions, or affiliates thereof, have also agreed:

| • | to use commercially reasonable efforts to arrange a syndication of a $500 million term loan; and |

| • | to act as underwriters or placement agents in connection with the proposed offering of senior unsecured notes. |

20

Table of Contents

Mirant and RRI Energy anticipate closing the proposed note offering into escrow. Upon consummation of the merger and satisfaction of the other escrow conditions, such notes will be senior unsecured obligations of GenOn Energy.

Both Mirant and RRI Energy are subject to restrictions on their ability to solicit alternative acquisition proposals, provide information and engage in discussions with third parties, except under limited circumstances to permit Mirant’s and RRI Energy’s boards of directors to comply with their fiduciary duties. The Merger Agreement contains certain termination rights for both Mirant and RRI Energy, and further provides that, upon termination of the Merger Agreement under specified circumstances, Mirant or RRI Energy may be required to pay the other a termination fee of either $37.15 million or $57.78 million. Further information concerning Mirant’s proposed merger was included in a joint proxy statement/prospectus contained in the registration statement on Form S-4 filed by RRI Energy with the SEC on May 28, 2010, and amended on July 6, 2010.

On July 15, 2010, Mirant and RRI Energy each received a request for additional information (commonly referred to as a “second request”) from the Antitrust Division of the United States Department of Justice under the Hart-Scott-Rodino Act with respect to the merger. On July 20, 2010, the New York State Public Service Commission issued an order declaring that it will not further review the merger. On August 2, 2010, the FERC issued an order approving the merger.

Provided neither has experienced an ownership change between December 31, 2009, and the closing date of the merger, each of Mirant and RRI Energy is expected separately to experience an ownership change, as defined in Section (“§”) 382 of the Internal Revenue Code of 1986, on the merger date as a consequence of the merger. Immediately following the merger, Mirant and RRI Energy will be members of the same consolidated federal income tax group. The ability of this consolidated tax group to deduct the pre-merger NOL carry forwards of Mirant and RRI Energy against the post-merger taxable income of the group will be substantially limited as a result of these ownership changes.

The merger is expected to be completed by the end of 2010. Prior to the completion of the merger, Mirant and RRI Energy will continue to operate as independent companies. Except for specific references to Mirant’s proposed merger and the associated debt financing transactions, the disclosures contained in this report on Form 10-Q relate solely to Mirant and the Companies.

Mid-Atlantic Collective Bargaining Agreement

During the second quarter of 2010, Mirant Services entered into a new collective bargaining agreement with the Mid-Atlantic employees represented by IBEW Local 1900. The previous collective bargaining agreement expired on June 1, 2010. The new agreement has a five-year term expiring on June 1, 2015. As part of the new agreement, Mirant Services is required to provide additional retirement contributions through the defined contribution plan currently sponsored by Mirant Services, increases in pay and other benefits. In addition, the new agreement provides for a change to the postretirement healthcare benefit plan covering Mid-Atlantic union employees to eliminate employer-provided healthcare subsidies through a gradual phase-out. The Companies will reimburse Mirant Services for the costs associated with providing the benefits through the Administrative Services Agreement. See Note F for further discussion of arrangements with related parties.

Basis of Presentation

The accompanying unaudited condensed consolidated financial statements of the Companies have been prepared in accordance with GAAP for interim financial information and with the instructions for Form 10-Q and Article 10 of Regulation S-X. Accordingly, they do not include all of the information and footnotes required by GAAP for complete financial statements. In the opinion of management, all adjustments (consisting of normal recurring accruals) considered necessary for a fair presentation have been included. For further information, refer to the consolidated financial statements and notes thereto included in the Companies’ 2009 Annual Report on Form 10-K.

21

Table of Contents

The accompanying unaudited condensed consolidated financial statements include the accounts of the Companies and their wholly-owned subsidiaries. The consolidated financial statements have been prepared from records maintained by the Companies and their subsidiaries. All significant intercompany accounts and transactions within consolidated entities have been eliminated in consolidation.

The preparation of the unaudited condensed consolidated financial statements in conformity with GAAP requires management to make various estimates and assumptions that affect the reported amounts of assets and liabilities, disclosures of contingent assets and liabilities at the date of the unaudited condensed consolidated financial statements and the reported amounts of revenues and expenses during the period. Actual results could differ from those estimates. Certain prior period amounts have been reclassified to conform to the current period financial statement presentation.

The Companies evaluate events that occur after their balance sheet date but before their financial statements are issued for potential recognition or disclosure. Based on their evaluations, the Companies determined that there were no material subsequent events for recognition or disclosure other than those disclosed herein.

Inventories

Inventories consist primarily of fuel oil, coal, materials and supplies and purchased emissions allowances. Inventory is generally stated at the lower of cost or market value and is expensed on a weighted average cost basis. Fuel inventory is removed from the inventory account as it is used in the generation of electricity or sold to third parties. Materials and supplies are removed from the inventory account when they are used for repairs, maintenance or capital projects. Purchased emissions allowances are removed from inventory and charged to cost of fuel, electricity and other products in the Companies’ accompanying unaudited condensed consolidated statements of operations as they are utilized for emissions volumes.

Inventories were comprised of the following (in millions):

Mirant Americas Generation and Mirant North America

| At June 30, 2010 |

At December 31, 2009 | |||||

| Fuel inventory: |

||||||

| Fuel oil |

$ | 167 | $ | 99 | ||

| Coal |

47 | 52 | ||||

| Other |

1 | 1 | ||||

| Materials and supplies |

69 | 66 | ||||

| Purchased emissions allowances |

26 | 23 | ||||

| Total inventories |

$ | 310 | $ | 241 | ||

Mirant Mid-Atlantic

| At June 30, 2010 |

At December 31, 2009 | |||||

| Fuel inventory: |

||||||

| Fuel oil |

$ | 22 | $ | 20 | ||

| Coal |

47 | 52 | ||||

| Other |

1 | 1 | ||||

| Materials and supplies |

46 | 43 | ||||

| Purchased emissions allowances |

— | 1 | ||||

| Total inventories |

$ | 116 | $ | 117 | ||

22

Table of Contents

Impairment of Long-Lived Assets

The Companies evaluate long-lived assets, such as property, plant and equipment and purchased intangible assets subject to amortization, for impairment whenever events or changes in circumstances indicate that the carrying amount of the asset may not be recoverable. Such evaluations are performed in accordance with the accounting guidance related to evaluating long-lived assets for impairment. Recoverability of assets to be held and used is measured by a comparison of the carrying amount of an asset to the estimated undiscounted future cash flows expected to be generated by the asset. If the carrying amount of an asset exceeds its estimated undiscounted future cash flows, an impairment charge is recognized as the amount by which the carrying amount of the asset exceeds its fair value. In the second quarter of 2010, the Companies evaluated the Dickerson generating facility for impairment, but did not record an impairment charge. See Note C for further discussion.

Capitalization of Interest Cost (Mirant Americas Generation and Mirant North America)

Mirant Americas Generation and Mirant North America capitalize interest on projects during their construction period. Mirant Americas Generation and Mirant North America determine which debt instruments represent a reasonable measure of the cost of financing construction in terms of interest costs incurred that otherwise could have been avoided. These debt instruments and associated interest costs are included in the calculation of the weighted average interest rate used for determining the capitalization rate. Once a project is placed in service, capitalized interest, as a component of the total cost of the construction, is amortized over the estimated useful life of the asset constructed.

For the three and six months ended June 30, 2010 and 2009, Mirant Americas Generation and Mirant North America incurred the following interest costs on debt to nonaffiliates (in millions):

Mirant Americas Generation

| Three Months Ended June 30, |

Six Months Ended June 30, |

|||||||||||||||

| 2010 | 2009 | 2010 | 2009 | |||||||||||||

| Total interest costs |

$ | 50 | $ | 52 | $ | 102 | $ | 105 | ||||||||

| Capitalized and included in property, plant and equipment, net |

(1 | ) | (18 | ) | (3 | ) | (33 | ) | ||||||||

| Interest expense |

$ | 49 | $ | 34 | $ | 99 | $ | 72 | ||||||||

The amounts of capitalized interest above include interest accrued. For the three and six months ended June 30, 2010, cash paid for interest was $93 million and $95 million, respectively, of which $3 million and $3 million, respectively, was capitalized. For the three and six months ended June 30, 2009, cash paid for interest was $93 million and $96 million, respectively, of which $31 million and $33 million, respectively, was capitalized.

Mirant North America

| Three Months Ended June 30, |

Six Months Ended June 30, |

|||||||||||||||

| 2010 | 2009 | 2010 | 2009 | |||||||||||||

| Total interest costs |

$ | 20 | $ | 23 | $ | 42 | $ | 45 | ||||||||

| Capitalized and included in property, plant and equipment, net |

(1 | ) | (18 | ) | (3 | ) | (33 | ) | ||||||||

| Interest expense |

$ | 19 | $ | 5 | $ | 39 | $ | 12 | ||||||||

The amounts of capitalized interest above include interest accrued. For the three and six months ended June 30, 2010, cash paid for interest was $34 million and $36 million, respectively, of which $3 million and

23

Table of Contents

$3 million, respectively, was capitalized. For the three and six months ended June 30, 2009, cash paid for interest was $34 million and $37 million, respectively, of which $31 million and $33 million, respectively, was capitalized.

Recently Adopted Accounting Guidance

On January 21, 2010, the FASB issued guidance that enhances the disclosures for fair value measurements. The guidance requires the Companies to disclose separately the amount of significant transfers between Level 1 and Level 2 of the fair value hierarchy, the reasons for the significant transfers, the valuation techniques and inputs used and the classes of assets and liabilities accounted for at fair value on a recurring basis. The Companies adopted this accounting guidance for the quarter ended March 31, 2010. See Note B for additional information on fair value measurements.

On February 25, 2010, the FASB issued guidance that amends its requirement for public companies to disclose the date through which the Companies have evaluated subsequent events and whether that date represents the date the financial statements were issued or were available to be issued. The Companies adopted the subsequent event disclosure requirements for the quarter ended March 31, 2010, and the adoption had no effect on the Companies’ unaudited condensed consolidated statements of operations, financial positions or cash flows. The Companies continue to evaluate subsequent events through the date when the financial statements are issued.

New Accounting Guidance Not Yet Adopted at June 30, 2010

On January 21, 2010, the FASB issued guidance that requires a reconciliation for Level 3 fair value measurements, including presenting separately the amounts of purchases, issuances and settlements on a gross basis. The Companies currently disclose the amounts of purchases, issuances and settlements on a net basis within their roll forward of Level 3 fair value measurements in Note B. These disclosure requirements are effective for fiscal years beginning after December 15, 2010. The Companies will present these disclosures in their Form 10-Q for the quarter ended March 31, 2011.

| B. | Financial Instruments (Mirant Americas Generation, Mirant North America and Mirant Mid-Atlantic) |

Derivative Financial Instruments

In connection with the business of generating electricity, the Companies are exposed to energy commodity price risk associated with the acquisition of fuel and emissions allowances needed to generate electricity, the price of electricity produced and sold and the fair value of fuel inventories. In addition, the open positions in Mirant Americas Generation’s and Mirant North America’s trading activities, comprised of proprietary trading and fuel oil management activities, expose them to risks associated with changes in energy commodity prices. The Companies, through their asset management activities, enter into a variety of exchange-traded and OTC energy and energy-related derivative financial instruments, such as forward contracts, futures contracts, option contracts and financial swap agreements to manage exposure to commodity price risks. These contracts have varying terms and durations, which range from a few days to years, depending on the instrument. Mirant Americas Generation’s and Mirant North America’s proprietary trading activities also utilize similar derivative financial instruments in markets where they have a physical presence to attempt to generate incremental gross margin. Mirant Americas Generation’s and Mirant North America’s fuel oil management activities use derivative financial instruments to hedge economically the fair value of their physical fuel oil inventories and to optimize the approximately three million barrels of storage capacity that they own or lease.

Changes in the fair value and settlements of derivative financial instruments used to hedge electricity economically are reflected in operating revenue, and changes in the fair value and settlements of derivative financial instruments used to hedge fuel economically are reflected in cost of fuel, electricity and other products in the accompanying unaudited condensed consolidated statements of operations.

24

Table of Contents

In May 2010, the Companies concluded that they could no longer assert that physical delivery is probable for many of their coal agreements. The conclusion was based on expected generation levels, changes observed in the coal markets and substantial progress in the construction of their coal blending facility at the Morgantown generating facility that will allow for greater flexibility of their coal supply. Because the Companies can no longer assert that physical delivery of coal from these agreements is probable, they are required to apply fair value accounting for these contracts in the current period and prospectively. The Companies’ coal agreements requiring the application of fair value accounting represented a net derivative contract liability of approximately $98 million at June 30, 2010 in the accompanying unaudited condensed consolidated balance sheets.

Changes in the fair value and settlements of Mirant Americas Generation’s and Mirant North America’s derivative contracts for trading activities, comprised of proprietary trading and fuel oil management, are recorded on a net basis as operating revenue in the accompanying unaudited condensed consolidated statements of operations. As of June 30, 2010, the Companies do not have any derivative financial instruments for which hedge accounting has been elected and option contracts comprise less than 1% of the Companies’ net derivative contract assets.

The Companies also consider risks associated with interest rates, counterparty credit and Mirant Americas Generation’s, Mirant North America’s and Mirant Mid-Atlantic’s own non-performance risk when valuing their derivative financial instruments. The nominal value of the derivative contract assets and liabilities is discounted to account for time value using a LIBOR forward interest rate curve based on the tenor of the Companies’ transactions being valued.

Mirant Americas Generation and Mirant North America

The following table presents the fair value of each class of derivative financial instruments related to commodity price risk (in millions):

| Fair Value at | ||||||||||

| Commodity Derivative Contracts |

Balance Sheet Location |

June 30, 2010 |

December 31, 2009 |

|||||||

| Asset management: |

||||||||||

| Power |

Derivative contract assets |

$ | 1,238 | $ | 1,178 | |||||

| Fuel |

Derivative contract assets |

35 | 26 | |||||||

| Total asset management |

1,273 | 1,204 | ||||||||

| Trading activities |

Derivative contract assets |

1,165 | 811 | |||||||

| Total derivative contract assets |

2,438 | 2,015 | ||||||||

| Asset management: |

||||||||||

| Power |

Derivative contract liabilities |

(420 | ) | (488 | ) | |||||

| Fuel |

Derivative contract liabilities |

(143 | ) | (15 | ) | |||||

| Total asset management |

(563 | ) | (503 | ) | ||||||

| Trading activities |

Derivative contract liabilities |

(1,161 | ) | (810 | ) | |||||

| Total derivative contract liabilities |

(1,724 | ) | (1,313 | ) | ||||||

| Asset management, net: |

||||||||||

| Power |

818 | 690 | ||||||||

| Fuel |

(108 | ) | 11 | |||||||

| Total asset management |

710 | 701 | ||||||||

| Trading activities, net |

4 | 1 | ||||||||

| Total derivative contracts, net |

$ | 714 | $ | 702 | ||||||

25

Table of Contents

The following tables present the net gains (losses) for derivative financial instruments recognized in income in the unaudited condensed consolidated statements of operations (in millions):

| Commodity |

Location of Net Gains (Losses) |

Amount of Net Gains (Losses) Recognized in Income for the Three Months Ended |

||||||||||||||||||||||||

| June 30, 2010 | June 30, 2009 | |||||||||||||||||||||||||

| Realized | Unrealized | Total | Realized | Unrealized | Total | |||||||||||||||||||||

| Asset management |

Operating revenues | $ | 91 | $ | (218 | ) | $ | (127 | ) | $ | 191 | $ | (10 | ) | $ | 181 | ||||||||||

| Trading activities |

Operating revenues | (21 | ) | (13 | ) | (34 | ) | 46 | (34 | ) | 12 | |||||||||||||||

| Asset management |

Cost of fuel, electricity and other products | (11 | ) | (109 | ) | (120 | ) | (28 | ) | 30 | 2 | |||||||||||||||

| Total |

$ | 59 | $ | (340 | ) | $ | (281 | ) | $ | 209 | $ | (14 | ) | $ | 195 | |||||||||||

| Commodity Derivative Contracts |

Location of Net Gains (Losses) |

Amount of Net Gains (Losses) Recognized in Income for the Six Months Ended |

||||||||||||||||||||||||

| June 30, 2010 | June 30, 2009 | |||||||||||||||||||||||||

| Realized | Unrealized | Total | Realized | Unrealized | Total | |||||||||||||||||||||

| Asset management |

Operating revenues | $ | 176 | $ | 135 | $ | 311 | $ | 327 | $ | 260 | $ | 587 | |||||||||||||

| Trading activities |

Operating revenues | (2 | ) | (3 | ) | (5 | ) | 74 | (49 | ) | 25 | |||||||||||||||

| Asset management |

Cost of fuel, electricity and other products | (26 | ) | (120 | ) | (146 | ) | (44 | ) | 29 | (15 | ) | ||||||||||||||

| Total |

$ | 148 | $ | 12 | $ | 160 | $ | 357 | $ | 240 | $ | 597 | ||||||||||||||

The following table presents the notional quantity on long (short) positions for derivative financial instruments on a gross and net basis at June 30, 2010 (in equivalent MWh):

| Notional Quantity | ||||||||

| Derivative Contract Assets |

Derivative Contract Liabilities |

Net Derivative Contracts |

||||||

| (in millions) | ||||||||

| Commodity Type: |

||||||||

|

Power1 |

(91 | ) | 48 | (43 | ) | |||

| Natural gas |

(66 | ) | 68 | 2 | ||||

| Fuel oil |

(3 | ) | 2 | (1 | ) | |||

| Coal |

11 | 8 | 19 | |||||

| Total |

(149 | ) | 126 | (23 | ) | |||

| 1 | Includes MWh equivalent of natural gas transactions used to hedge power economically. |

26

Table of Contents

Mirant Mid-Atlantic

The following table presents the fair value of each class of derivative financial instruments related to commodity price risk (in millions):

| Commodity Derivative Contracts |

Balance Sheet Location |

Fair Value at | ||||||||

| June 30, 2010 |

December 31, 2009 |

|||||||||

| Asset management—nonaffiliate: |

||||||||||

| Power |

Derivative contract assets | $ | 660 | $ | 554 | |||||

| Fuel |

Derivative contract assets | — | — | |||||||

| Asset management—affiliate: |

||||||||||

| Power |

Derivative contract assets | 536 | 584 | |||||||

| Fuel |

Derivative contract assets | 27 | 7 | |||||||

| Total derivative contract assets |

1,223 | 1,145 | ||||||||

| Asset management—nonaffiliate: |

||||||||||

| Power |

Derivative contract liabilities | (20 | ) | (17 | ) | |||||

| Fuel |

Derivative contract liabilities | — | — | |||||||

| Asset management—affiliate: |

||||||||||

| Power |

Derivative contract liabilities | (380 | ) | (457 | ) | |||||

| Fuel |

Derivative contract liabilities | (124 | ) | (1 | ) | |||||

| Total derivative contract liabilities |

(524 | ) | (475 | ) | ||||||

| Asset management—nonaffiliate, net: |

||||||||||

| Power |

640 | 537 | ||||||||

| Fuel |

— | — | ||||||||

| Asset management—affiliate, net: |

||||||||||

| Power |

156 | 127 | ||||||||

| Fuel |

(97 | ) | 6 | |||||||

| Total derivative contracts, net |

$ | 699 | $ | 670 | ||||||

The following tables present the net gains (losses) for derivative financial instruments recognized in income in the unaudited condensed consolidated statements of operations (in millions):

| Commodity |

Location of Net Gains (Losses) |

Amount of Net Gains (Losses) Recognized in Income for the Three Months Ended | |||||||||||||||||||||||

| June 30, 2010 | June 30, 2009 | ||||||||||||||||||||||||

| Realized | Unrealized | Total | Realized | Unrealized | Total | ||||||||||||||||||||

| Asset management |

Operating revenues | $ | 86 | $ | (205 | ) | $ | (119 | ) | $ | 174 | $ | (4 | ) | $ | 170 | |||||||||

| Asset management |

Cost of fuel, electricity and other products | (4 | ) | (112 | ) | (116 | ) | (2 | ) | 4 | 2 | ||||||||||||||

| Total |

$ | 82 | $ | (317 | ) | $ | (235 | ) | $ | 172 | $ | — | $ | 172 | |||||||||||

| Commodity |

Location of Net Gains (Losses) |

Amount of Net Gains (Losses) Recognized in Income for the Six Months Ended | |||||||||||||||||||||||

| June 30, 2010 | June 30, 2009 | ||||||||||||||||||||||||

| Realized | Unrealized | Total | Realized | Unrealized | Total | ||||||||||||||||||||

| Asset management |