Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K 080510 - CPG INTERNATIONAL INC. | form8-k_080510.htm |

| EX-99.1 - EXHIBIT 99.1 PRESS RELEASE - CPG INTERNATIONAL INC. | exhibit_99-1.htm |

2010

Second Quarter Earnings Call

August

6, 2010

Exhibit

99.2

2

Safe

Harbor Statement and Use of Non-GAAP and Pro Forma Information

FORWARD

LOOKING STATEMENTS

This

presentation contains forward-looking statements within the meaning of the

Private Securities Litigation Reform Act of 1995. Statements made in

this

presentation that relate to future events or the Company’s expectations, guidance, projections, estimates, intentions, goals, targets and strategies are forward-

looking statements. You are cautioned that all forward-looking statements are based upon current expectations and estimates and the Company assumes no

obligation to update this information. Because actual results may differ materially from those expressed or implied by the forward-looking statements, the

Company cautions you not to place undue reliance on these statements. For a detailed discussion of the important factors that affect the Company and that

could cause actual results to differ from those expressed or implied by the Company’s forward-looking statements, please see “Management’s Discussion and

Analysis of Financial Condition and Results of Operations” and “Risk Factors” in the Company’s current and future Annual Reports on Form 10-K and Quarterly

Reports on Form 10-Q.

presentation that relate to future events or the Company’s expectations, guidance, projections, estimates, intentions, goals, targets and strategies are forward-

looking statements. You are cautioned that all forward-looking statements are based upon current expectations and estimates and the Company assumes no

obligation to update this information. Because actual results may differ materially from those expressed or implied by the forward-looking statements, the

Company cautions you not to place undue reliance on these statements. For a detailed discussion of the important factors that affect the Company and that

could cause actual results to differ from those expressed or implied by the Company’s forward-looking statements, please see “Management’s Discussion and

Analysis of Financial Condition and Results of Operations” and “Risk Factors” in the Company’s current and future Annual Reports on Form 10-K and Quarterly

Reports on Form 10-Q.

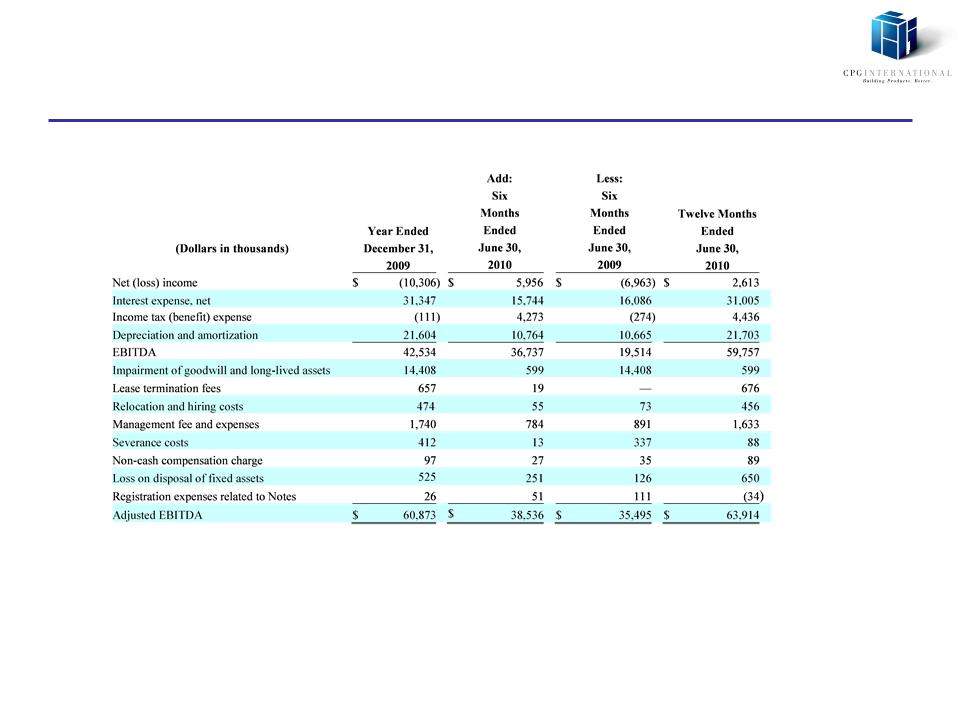

ADJUSTED

EBITDA STATEMENT

We refer

to the term “Adjusted EBITDA” in various places throughout this

presentation. Adjusted

EBITDA, or earnings (adjusted as described below) before

interest, taxes, depreciation and amortization calculated on a pro forma basis as provided herein, is a material component of the significant covenants

contained in our credit agreements and the indenture governing the notes and accordingly, is important to the Company’s liquidity and ability to borrow under

its debt instruments. Adjusted EBITDA is calculated similarly under both the credit agreements and the indenture by adding consolidated net income, income

taxes, interest expense, depreciation and amortization and other non-cash expenses, income or loss attributable to discontinued operations, amounts payable

pursuant to the management agreement with AEA Investors and the impairment charge for goodwill and other intangibles. In addition, consolidated net income

is adjusted to exclude certain items, including certain nonrecurring or unusual charges. Please see the Company’s December 31, 2009 10-K, which contains a

detailed description of our covenants and a thorough description of our use of Adjusted EBITDA, and the use of Adjusted EBITDA in connection with certain

calculations under the covenants, under our credit agreements and indenture.

interest, taxes, depreciation and amortization calculated on a pro forma basis as provided herein, is a material component of the significant covenants

contained in our credit agreements and the indenture governing the notes and accordingly, is important to the Company’s liquidity and ability to borrow under

its debt instruments. Adjusted EBITDA is calculated similarly under both the credit agreements and the indenture by adding consolidated net income, income

taxes, interest expense, depreciation and amortization and other non-cash expenses, income or loss attributable to discontinued operations, amounts payable

pursuant to the management agreement with AEA Investors and the impairment charge for goodwill and other intangibles. In addition, consolidated net income

is adjusted to exclude certain items, including certain nonrecurring or unusual charges. Please see the Company’s December 31, 2009 10-K, which contains a

detailed description of our covenants and a thorough description of our use of Adjusted EBITDA, and the use of Adjusted EBITDA in connection with certain

calculations under the covenants, under our credit agreements and indenture.

While

the determination of appropriate adjustments in the calculation of Adjusted

EBITDA is subject to interpretation under our debt agreements,

management

believes the adjustments are in accordance with the covenants in our credit agreements and indenture, as discussed above. Adjusted EBITDA should not be

considered in isolation or construed as an alternative to our net income or other measures as determined in accordance with GAAP. In addition, other

companies in our industry or across different industries may calculate Adjusted EBITDA differently than we do, limiting its usefulness as a comparative

measure. In future SEC filings, we may be required to change our presentation of Adjusted EBITDA in order to comply with the SEC’s rules regarding the use

of non-GAAP financial measures. In addition, you are cautioned not to place undue reliance on Adjusted EBITDA. For a reconciliation of Adjusted EBITDA to

net income, please see the Appendix to this presentation.

believes the adjustments are in accordance with the covenants in our credit agreements and indenture, as discussed above. Adjusted EBITDA should not be

considered in isolation or construed as an alternative to our net income or other measures as determined in accordance with GAAP. In addition, other

companies in our industry or across different industries may calculate Adjusted EBITDA differently than we do, limiting its usefulness as a comparative

measure. In future SEC filings, we may be required to change our presentation of Adjusted EBITDA in order to comply with the SEC’s rules regarding the use

of non-GAAP financial measures. In addition, you are cautioned not to place undue reliance on Adjusted EBITDA. For a reconciliation of Adjusted EBITDA to

net income, please see the Appendix to this presentation.

3

About

CPG International

Headquartered in

Scranton, Pennsylvania, CPG International is a leading supplier of premium,

low-maintenance building products designed to

replace wood, metal and other materials in the residential, commercial and industrial markets. With a focus on manufacturing excellence,

proprietary technologies and quality, CPG has introduced products through distribution networks to sizable markets increasingly converting to low

maintenance materials. The Company has developed and acquired a number of branded products including AZEK® Trim, AZEK® Deck, AZEK®

Moulding, AZEK® Rail, AZEK® Porch, Comtec and Hiny Hiders® bathroom partition systems, and TuffTec™ locker systems. For additional

information on CPG please visit our web site at http:// www.cpgint.com.

replace wood, metal and other materials in the residential, commercial and industrial markets. With a focus on manufacturing excellence,

proprietary technologies and quality, CPG has introduced products through distribution networks to sizable markets increasingly converting to low

maintenance materials. The Company has developed and acquired a number of branded products including AZEK® Trim, AZEK® Deck, AZEK®

Moulding, AZEK® Rail, AZEK® Porch, Comtec and Hiny Hiders® bathroom partition systems, and TuffTec™ locker systems. For additional

information on CPG please visit our web site at http:// www.cpgint.com.

Please

note:

To

access the conference call, please dial (866) 863-6818, and use conference ID

code 80981126. An

encore presentation will be available for

one week after the completion of the call. In order to access the encore presentation, please dial (800) 642-1687 or (706) 645-9291, and use the

conference ID code 80981126.

one week after the completion of the call. In order to access the encore presentation, please dial (800) 642-1687 or (706) 645-9291, and use the

conference ID code 80981126.

4

2010

Second Quarter Financial Highlights

• Market

Conditions: Stabilizing

residential and industrial construction markets

Commercial

markets continue to decline versus prior year

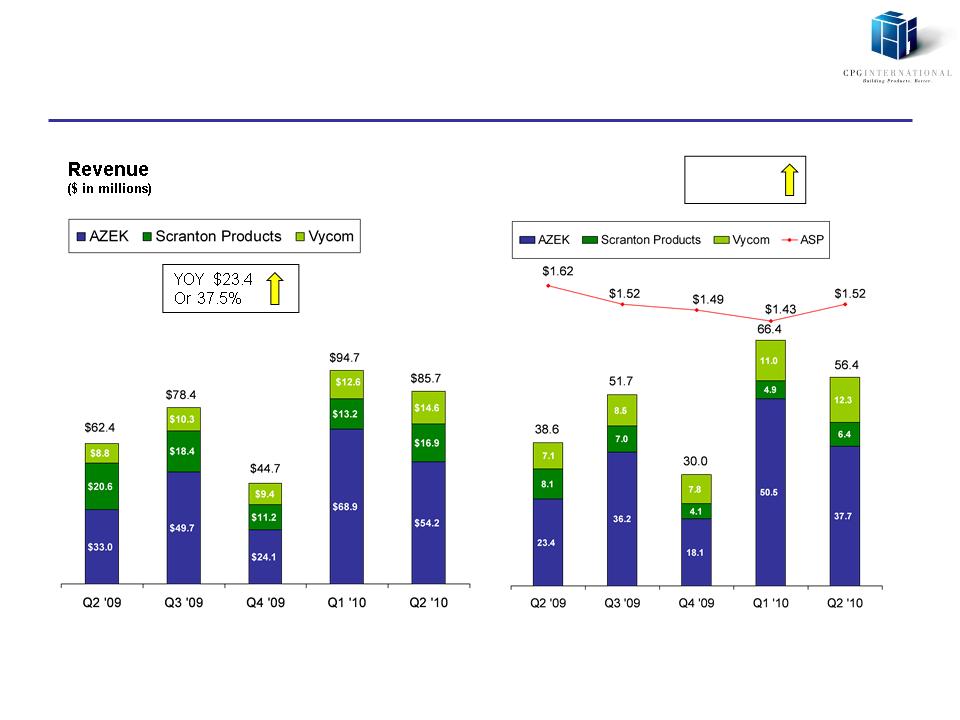

• Revenue: $85.7mm

Q2 2010 vs. $62.4mm in Q2 2009, up 37.5%

– AZEK Deck, AZEK

Trim, AZEK Rail and Vycom growth

offset decline in commercial market

offset decline in commercial market

• Gross

Margin: 30.9%

Q2 2010 vs. 35.6% in Q2 2009

– Material cost

increases versus 2009 impacting gross

margin

margin

• SG&A: $14.9mm

Q2 2010 vs. $14.1mm in Q2 2009

– Increased

marketing and selling expenses

• Adjusted

EBITDA: Up

19.2% to $17.3mm

– 20.1% Adjusted

EBITDA margin

• Net

Income/Loss: $2.8mm

net income in Q2 2010, compared to $0.1mm

in Q2 2009

in Q2 2009

Quarter

Highlights

5

Quarterly

Revenue

Financial

Overview

Volume

& ASP

(lbs

in millions)

YOY

17.8

Or

46.1%

6

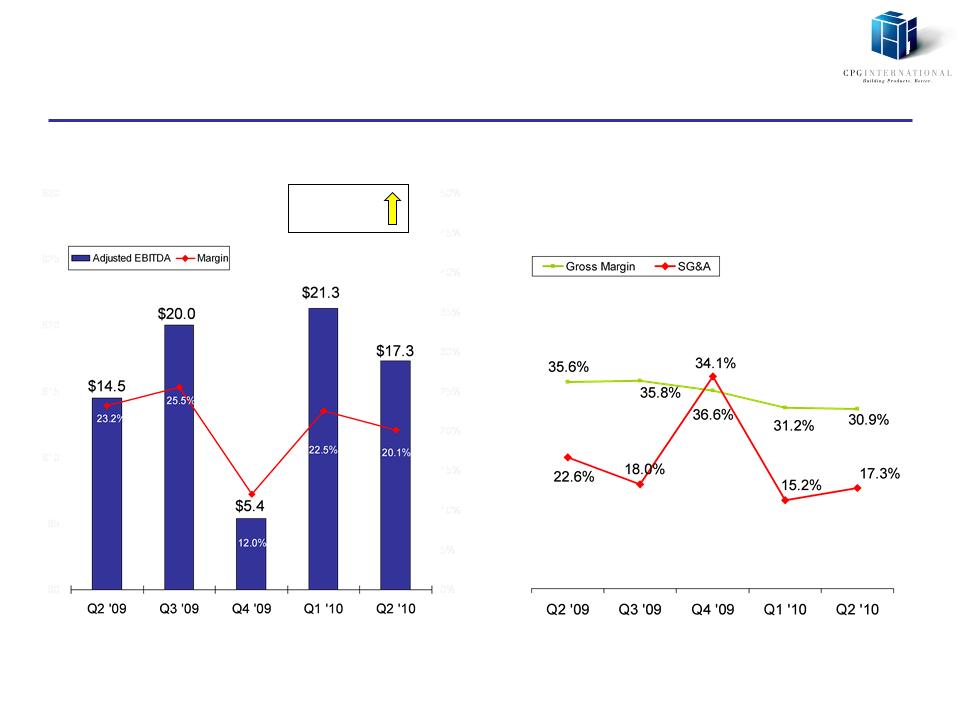

Quarterly

Earnings

Financial

Overview

Adjusted

EBITDA

($

in millions)

Gross

Margin and SG&A

(%

of revenue)

YOY

$2.8

or

19.2%

7

7

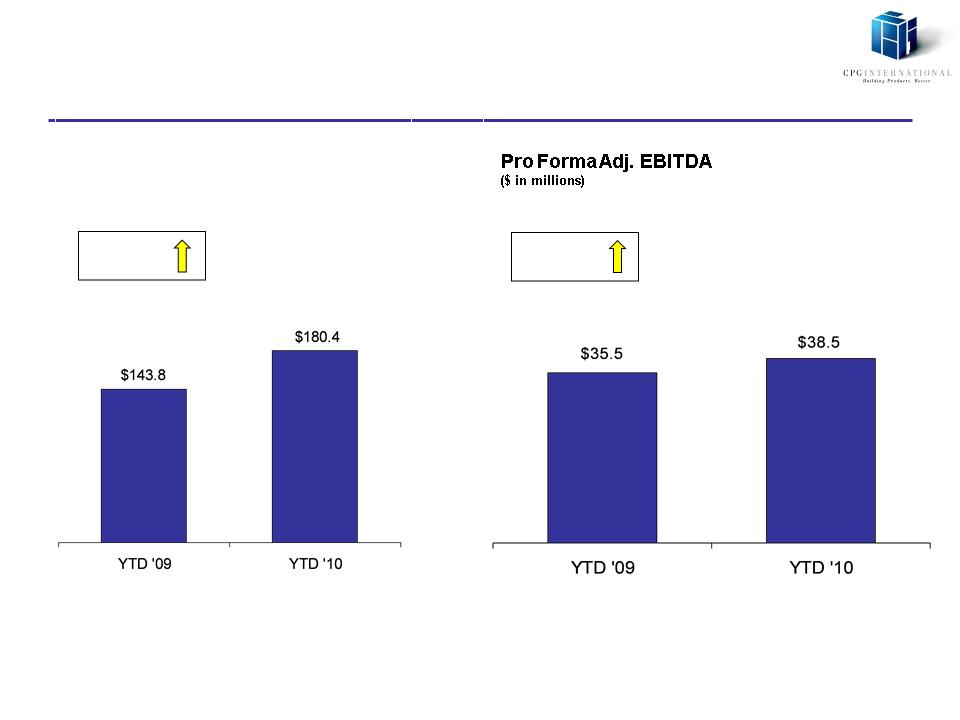

Year to

Date Performance

Financial

Overview

Revenue

/ Pro Forma

($

in millions)

YOY

$3.0

Or

8.6%

YOY

$36.6

Or

25.5%

8

Capital

Expenditures

Financial

Overview

YOY

$2.3

Or

153.3%

Quarter

Cap Ex

($

in millions)

Historical

Cap Ex

($

in millions)

$15-$20

9

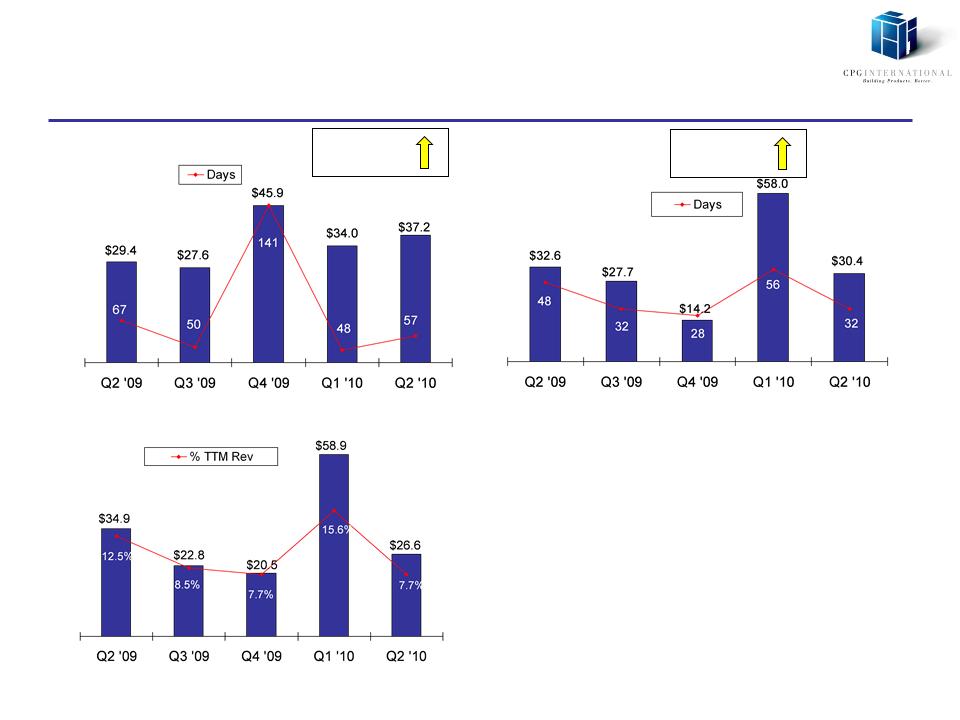

Working

Capital Management

Financial

Overview

YOY

$7.9

Or

26.8%

Inventory

and Inv Days(1)

($

in millions)

AR

and AR Days(1)

($

in millions)

YOY

$(2.2)

or

(6.8)%

Inv/AR/Prepaid

less AP/Accrued

($

in millions)

Footnote:

(1) Based on trailing

three months annualized

10

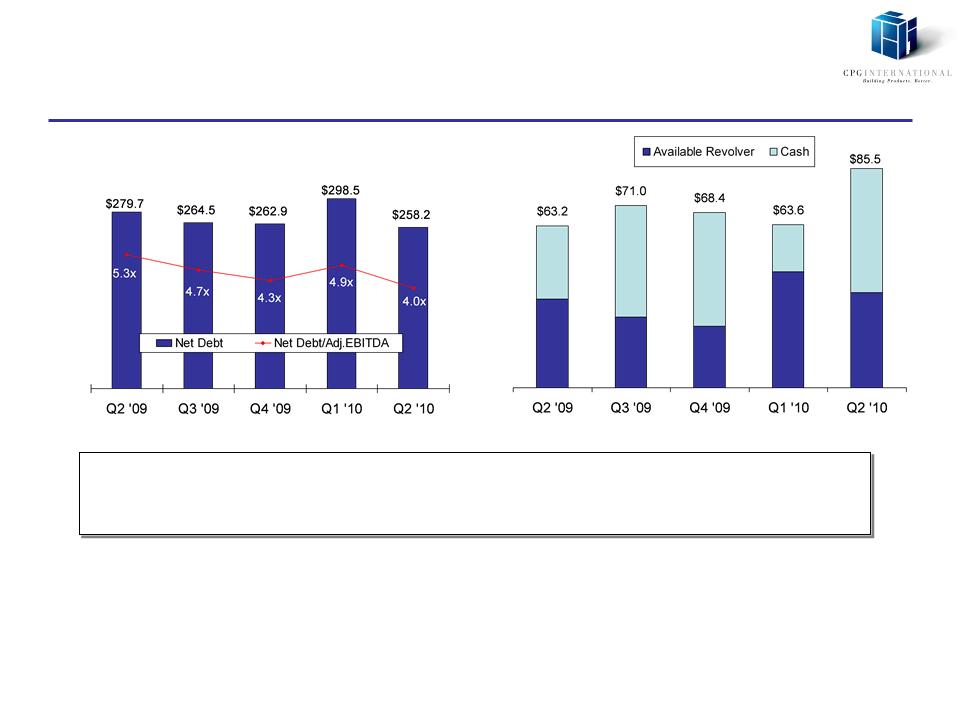

Liquidity

Position

Financial

Overview

Net

Debt(1) & Net

Debt/Adj. EBITDA(2)

($

in millions)

Liquidity(3)

($

in millions)

• Liquidity position

at $85.5mm

• Trailing Twelve

Month June 30, 2010 Adjusted EBITDA of $63.9mm

Footnotes:

(1) Net debt defined as

total debt and capital lease obligations less cash

(2) Trailing twelve month

adjusted EBITDA as defined in Credit Agreements

(3) Liquidity defined as

cash as of 6/30/10 plus availability under our revolver

11

Low

High

$57mm

$67mm

2010

Guidance

2010

Adjusted EBITDA Guidance(1)

Downside:

• Slow economic

recovery

– Residential repair

& remodel activity

– New home

construction

– Industrial

markets

– Commercial

markets/tax revenue

• Resin prices

escalate beyond

expectations

expectations

• Increased

competition

Upside:

• Higher than

anticipated economic

activity

activity

• Increased market

penetration for

AZEK products

AZEK products

• Lower material

costs

• Operational

efficiencies

(1) In

preparation of our Adjusted EBITDA, we used a basis similar to actual interest,

depreciation, amortization and taxes reported in 2009.

12

APPENDIX

13

Net

Income to Adjusted EBITDA Reconciliation

Appendix

14

Quarterly Volume

Information

Appendix

|

|

|

|

|

|

|

|

|

(lbs in

thousands)

|

|

Q1

2010

|

|

Q2

2010

|

|

YTD

|

|

AZEK Building

Products

|

50,502

|

|

37,728

|

|

88,230

|

|

|

Scranton

Products

|

|

4,948

|

|

6,368

|

|

11,316

|

|

Vycom

Industrial

|

|

10,973

|

|

12,281

|

|

23,254

|

|

Total

|

|

66,423

|

|

56,377

|

|

122,800

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(lbs in

thousands)

|

|

Q1

2009

|

|

Q2

2009

|

|

YTD

|

|

AZEK Building

Products

|

44,938

|

|

23,433

|

|

68,371

|

|

|

Scranton

Products

|

|

6,581

|

|

8,121

|

|

14,702

|

|

Vycom

Industrial

|

|

6,662

|

|

7,047

|

|

13,709

|

|

Total

|

|

58,181

|

|

38,601

|

|

96,782

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

%

Change to prior year

|

|

|||

|

|

|

Q1

2010

|

|

Q2

2010

|

|

YTD

|

|

AZEK Building

Products

|

12.4%

|

|

61.0%

|

|

29.0%

|

|

|

Scranton

Products

|

|

-24.8%

|

|

-21.6%

|

|

-23.0%

|

|

Vycom

Industrial

|

|

64.7%

|

|

74.3%

|

|

69.6%

|

|

|

|

|

|

|

|

|

|

Total

|

|

14.2%

|

|

46.1%

|

|

26.9%

|

15

CPG