Attached files

| file | filename |

|---|---|

| EX-23.1 - EXHIBIT 23.1 - Euramax Holdings, Inc. | a2199444zex-23_1.htm |

As filed with the Securities and Exchange Commission on July 22, 2010

Registration No. 333-

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT UNDER

THE SECURITIES ACT OF 1933

EURAMAX HOLDINGS, INC.

(Exact Name of Registrant as Specified in Its Charter)

| Delaware (State or Other Jurisdiction of Incorporation or Organization) |

3444 (Primary Standard Industrial Classification Code Number) |

58-2502320 (I.R.S. Employer Identification Number) |

5445 Triangle Parkway, Suite 350

Norcross, GA 30092

(770) 449-7066

(Address, Including Zip Code, and Telephone Number,

Including Area Code, of Registrant's Principal Executive Offices)

R. Scott Vansant

Vice President, Secretary and Chief Financial Officer

5445 Triangle Parkway, Suite 350

Norcross, GA 30092

(770) 449-7066

(Name, Address, Including Zip Code, and Telephone Number,

Including Area Code, of Agent for Service)

With a copy to:

Michael A. Levitt Fried, Frank, Harris, Shriver & Jacobson LLP One New York Plaza New York, New York 10004 (212) 859-8000 |

Samir A. Gandhi Sidley Austin LLP 787 Seventh Avenue New York, New York 10019 (212) 839-5300 |

Approximate date of commencement of proposed sale to the public:

As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer ý (Do not check if a smaller reporting company) |

Smaller reporting company o |

CALCULATION OF REGISTRATION FEE

|

|||||||

| Title of Each Class of Securities to be Registered |

Proposed Maximum Aggregate Offering Price(1)(2) |

Amount of Registration Fee(2) |

|||||

|---|---|---|---|---|---|---|---|

Common Stock, $0.01 par value |

$ | 175,000,000 | $ | 12,477.50 | |||

|

|||||||

- (1)

- Includes

offering price of shares which the underwriters have an option to purchase. See "Underwriting."

- (2)

- Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(o) of the Securities Act of 1933, as amended.

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to Completion

Preliminary Prospectus dated July 22, 2010

P R O S P E C T U S

Shares

Euramax Holdings, Inc.

Common Stock

We are offering shares of our common stock.

Currently, no public market exists for the shares. We expect the public offering price to be between $ and $ per share. We intend to apply to list the common stock on the under the symbol "EMAX."

Investing in our common stock involves risks that are described in the "Risk Factors" section beginning on page 14 of this prospectus.

| |

Per Share | Total | |||||

|---|---|---|---|---|---|---|---|

Public offering price |

$ | $ | |||||

Underwriting discount |

$ | $ | |||||

Proceeds, before expenses, to us |

$ | $ | |||||

The underwriters may also purchase up to an additional shares from us at the public offering price, less the underwriting discount, within 30 days from the date of this prospectus to cover overallotments, if any.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The shares will be ready for delivery on or about , 2010.

Joint Book-Running Managers

BofA Merrill Lynch |

Deutsche Bank Securities |

The date of this prospectus is , 2010.

You should rely only on the information contained in this prospectus and any free writing prospectus prepared by us or on our behalf that we have referred you to. Neither we nor the underwriters have authorized anyone to provide you with additional or different information. If anyone provides you with additional, different or inconsistent information, you should not rely on it. We and the underwriters are not making an offer to sell these securities in any jurisdiction where an offer or sale is not permitted. You should not assume that the information in this prospectus and any free writing prospectus is accurate as of any date other than the date of the applicable document, regardless of its time of delivery or the time of any sales of our common stock. Our business, financial condition, results of operations or prospects may have changed since the date of the applicable document.

i

INDUSTRY, RANKING AND MARKET DATA

Market and industry data included in this prospectus, including all market share and market size data and our position and the positions of our competitors within these markets, are based on estimates derived from our management's knowledge and experience in the markets in which we operate, as well as information obtained from internal research and surveys, our customers, distributors, suppliers, trade and business organizations and other contacts in the markets in which we operate. Although we believe that these sources were reasonably derived and are accurate as of the date of this prospectus, we have not independently verified data from these sources or obtained third party verification of market share data. Further, data regarding market position and market share within our industry is intended to provide general guidance but is inherently imprecise. Market share data is subject to change and cannot always be verified with certainty due to limits on the availability and reliability of raw data, the voluntary nature of the data gathering process and other limitations and uncertainties inherent in any statistical survey of market shares. In addition, customer preferences can and do change. Also, the discussion herein regarding our various markets is based on our views regarding the end markets for our products, which products may be either part of larger overall markets or markets that include other types of products. As a result, you should be aware that market share, ranking and other similar data set forth herein, and estimates and beliefs based on such data, may not be reliable. We cannot guarantee the accuracy or completeness of any such information contained in this prospectus.

ii

This summary highlights significant aspects of our business and this offering, but it is not complete and does not contain all of the information you should consider before making your investment decision. You should carefully read this entire prospectus, including the "Risk Factors" and our consolidated financial statements and related notes included elsewhere in this prospectus, before making an investment decision. This summary contains forward-looking statements that involve risks and uncertainties. Our actual results may differ significantly from the results discussed in the forward-looking statements as a result of certain factors, including those set forth in the sections entitled "Risk Factors" and "Cautionary Statement Regarding Forward-Looking Statements." In this prospectus, all references to "the Company," "Euramax," "we," "us" and "our" refer to Euramax Holdings, Inc. and its consolidated subsidiaries, unless the context indicates or requires an alternative reference.

We are a leading international producer of metal and vinyl products sold to the residential repair and remodel, non-residential construction and recreational vehicle (RV) markets primarily in North America and Europe. We are a leader in several niche product categories, including preformed roof-drainage products sold in the U.S., metal roofing and siding for wood frame construction in the U.S., and aluminum siding for towable RVs in the U.S. and Europe. Sales to the building products and RV markets accounted for approximately 77% and 14% of our 2009 sales, respectively.

Our customers are located predominantly throughout North America and Europe and include distributors, contractors and home improvement retailers, as well as RV, transportation and other original equipment manufacturers, or OEMs. We have extensive in-house manufacturing and distribution capabilities for our more than 10,000 unique products and operate through a network consisting of 44 facilities, including 36 in the U.S., two in Canada and six in Europe. We have over 50 years of experience manufacturing building products and RV exterior components, including our time as a division of our former parent, Alumax Inc. ("Alumax"), a fully integrated aluminum producer acquired by Alcoa Inc. in 1998. We have operated as an independent company since 1996 when our division was acquired in a management-led buyout.

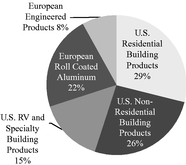

Our total net sales were $812.1 million for the year ended December 25, 2009. The following charts show our net sales by segment and geography during the year ended December 25, 2009:

| Net Sales by Segment | Net Sales by Geography | |

|

|

Our Segments

We manage our business and serve our customers through five reportable segments differentiated by market, product type and geography. Our structure and business model trace their roots to our history as a downstream producer of aluminum products and have evolved in response to customer demand for products made from materials other than aluminum and in pursuit of growth

1

opportunities in different end markets and geographies. Today we offer a full complement of products responsive to the demands of the markets we serve and produced from various materials, including aluminum, steel, copper, vinyl and fiberglass.

Our five reportable segments are described below:

U.S. Residential Building Products

Our U.S. Residential Building Products segment utilizes aluminum, steel, copper and vinyl to produce residential roof drainage products, including preformed gutters, downspouts, elbows, soffit, drip edge, fascia, flashing, snow guards and related accessories. These products are used primarily for the repair, replacement or enhancement of residential roof drainage systems. We sell these products to home improvement retailers, lumber yards, distributors and contractors from 10 manufacturing and distribution facilities located in North America.

This segment accounted for $232.1 million, or 28.6%, of our net sales in 2009. In 2009 we were the leading manufacturer of preformed metal gutters sold in North America. Further, we believe that we are the only North American supplier that produces preformed roof drainage systems from each of the four most common gutter materials: aluminum, steel, copper and vinyl.

U.S. Non-Residential Building Products

Our U.S. Non-Residential Building Products segment utilizes light gauge steel and aluminum coil to produce exterior building components, including roofing and siding panels, ridge caps, flashing, trim, soffit and other accessories. We sell these products to builders, contractors, lumber yards and home improvement retailers from 11 manufacturing and distribution facilities located in the U.S. These products are predominantly used in the construction of a wide variety of small scale non-residential, agricultural and industrial building types on either wood or metal frames.

This segment accounted for $211.9 million, or 26.1%, of our net sales in 2009. We believe that we are the second largest supplier of steel roofing and siding utilized for wood frame construction in the U.S. and believe that we have the largest market share of steel roofing and siding supplied to the Northeastern U.S. wood frame market.

U.S. RV and Specialty Building Products

Our U.S. RV and Specialty Building Products segment utilizes various materials including aluminum coil, steel coil and fiberglass to create exterior components for the towable RV, cargo and manufactured housing markets. These products include sidewall components, siding, doors and trim. We also produce specialty made-to-order vinyl replacement windows and aluminum patio and awning components sold primarily to home improvement contractors in the Western U.S. Our vinyl windows and patio and awning products are high-end replacement and remodel products that carry strong brand recognition in the regional markets where they are sold. This segment operates from 15 manufacturing and distribution facilities located in the U.S.

This segment accounted for $119.0 million, or 14.7%, of our net sales in 2009. We estimate that we sold at least 44% of the aluminum sidewalls and 32% of the doors used in the production of towable RVs in the United States in 2009. In addition, we believe that we are the only supplier of aluminum sidewalls in the U.S. with in-house coil coating capabilities.

European Roll Coated Aluminum

Our European Roll Coated Aluminum segment uses a roll coating process to apply paint to bare aluminum coil and, to a lesser extent, bare steel coil in order to produce specialty coated coil, which we also process into specialty coated sheets and panels. We sell these products to building panel

2

manufacturers, contractors and UK "holiday home," RV and transportation OEMs that sell to customers throughout Europe and in parts of Asia. Our customers use our specialty coated metal products to manufacture, among other things, RV sidewalls, commercial roofing panels, interior ceiling panels, and liner panels for shipping containers. We produce and distribute these roll coated products from one facility in The Netherlands and one facility in the UK.

This segment accounted for $180.3 million, or 22.2%, of our net sales in 2009. We estimate that we sold at least 85% of the aluminum sidewall material used in the production of RVs in Europe in 2009.

European Engineered Products

Our European Engineered Products segment utilizes aluminum and vinyl extrusions to produce residential windows, doors and shower enclosures. These products are sold to home improvement retailers, distributors and factory-built "holiday home" builders in the UK. We also produce windows used in the operator compartments of heavy equipment, components sold to suppliers to automotive OEMs in Western Europe and RV doors. We produce and distribute these engineered products from two facilities in France and two facilities in the UK and have developed extensive in-house manufacturing capabilities, including powder coating, glass cutting, anodizing and glass toughening.

This segment accounted for $68.8 million, or 8.4%, of our net sales in 2009. We believe that we are the largest supplier of residential vinyl windows to the UK home improvement and holiday home markets.

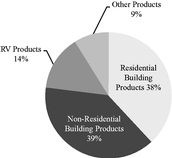

Our End Markets

Through our five segments we serve three primary end markets—Residential Building Products, Non-Residential Building Products and Recreational Vehicle Products. We believe our geographic network, broad product portfolio and customization capabilities allow us to effectively meet the diverse requirements of our customers within our end markets. These primary end markets are discussed below:

| Net Sales by End Market in 2009 |

|

Residential Building Products

Our net sales to the Residential Building Products end market in 2009 were $308.6 million, or 38% of our net sales, of which approximately 88% were from North America and approximately 12% were from Europe. We supply roof drainage components, vinyl windows, patio components, roofing and siding panels and other related products to the Residential Building Products market. Our roof drainage products are typically used for repair, remodel or replacement projects which are driven by wear and tear and weather damage. Roof drainage repair projects are often low cost and non-discretionary in nature. We believe that over 95% of our sales to this end market are derived from repair and remodel activity, with demand typically driven by turnover and aging of housing stock,

3

consumer sentiment, availability of home equity and consumer financing and, in the case of our vinyl window products, increasing consumer interest in energy efficiency. Growth in the U.S. residential repair and remodel market is expected to be driven in the short term by expenditures that were deferred during the economic downturn and over the longer term by the aging of existing housing stock, improvements in consumer confidence and a general recovery in the U.S. residential housing sector.

Non-Residential Building Products

Our net sales to the Non-Residential Building Products end market in 2009 were $312.3 million, or 39% of our net sales, of which approximately 68% were from the U.S. and Canada and approximately 32% were from Europe. Our non-residential building products are typically used in new construction and include, in the U.S., light gauge steel and aluminum roofing and siding panels, trim and hardware and, in Europe, the Middle East and Asia, roll coated aluminum coil and sheet. In the U.S. and Canada, our products are used in a variety of building applications including barns, smaller commercial buildings, storage sheds, schools, churches, shopping centers, parking garages, pavilions, boat docks and carports. Demand for these products varies according to end use and project scale, with smaller projects driven by consumer confidence and the availability of consumer credit and farm or rural applications driven by the strength of agricultural markets. Outside the U.S. and Canada, our specialty coated aluminum coil is used by customers who produce interior and exterior panels for roofs, ceilings, and siding used in larger commercial construction projects. Demand for these products is generally tied to commercial construction activity throughout Europe, the Middle East and Asia. The Non-Residential Building Products end market contracted significantly during the economic downturn, but as the economy recovers this end market is ultimately expected to benefit from accompanying improvements in consumer confidence, increased consumer disposable income and greater access to financing.

Recreational Vehicle Products

Our net sales to the Recreational Vehicle Products end market in 2009 were $113.3 million, or 14% of our net sales, of which approximately 43% were from the U.S. and approximately 57% were from Europe. We supply aluminum siding, doors and accessories for RVs in both the U.S. and Europe. This end market is comprised of two distinct RV products: motorhomes and towables. Motorhomes are generally larger, motorized vehicles and towables are lower-cost units towed by automobiles or light trucks. The majority of our sales to this end market are within the towable segment, which comprises the majority of global RV industry unit shipments, and includes sales to substantially all major towable RV OEMs in both the U.S. and Europe. We believe we are the number one supplier of aluminum siding for towable RVs in the combined U.S. and European markets.

The U.S. RV market is a $5 billion industry that is currently rebounding following substantial contraction in 2008 and 2009, according to the Recreation Vehicle Industry Association (RVIA). Significant pent-up demand for RVs, the return of attractive RV financing options, improved macro-economic conditions and stabilized gasoline prices are expected to support the rebound of the U.S. RV industry. According to an RVIA report from June 2010, total RV shipments in the U.S. are expected to increase annually by 23% from 2009 through 2011. The European RV industry generated $6.5 billion of revenue in 2009, according to the European Caravan Federation (ECF). In Europe, touring RV shipments are expected to decline by 10% annually from 2009 through 2011, while motorhome shipments are expected to decline by 4% annually over the same period, according to the European Caravan Federation (ECF).

4

Other Products

Our net sales of Other Products in 2009 were $77.9 million, or 9% of our net sales, of which approximately 40% were from the U.S. and Canada and approximately 60% were from Europe. In addition to serving our three primary end markets, we have taken advantage of our available manufacturing capacity and leveraged our materials expertise to develop and sell new products into other markets. These include various metal-based products, such as micro-car frames, heavy equipment operator compartments, utility trailer sidewalls, automobile sunroofs and windows for buses and trains.

The following competitive strengths have contributed to our success and are critical to maintaining the market positions that we enjoy and to achieving our plans for future growth. We believe that the combination of these strengths is unique to us among our competitors in the markets we serve. They include:

Well positioned leader in rebounding end markets. We maintain leading market positions in a number of niche markets which we believe are likely to rebound following a severe cyclical downturn. These positions include:

- •

- #1 position in preformed residential gutters sold in the U.S.

- •

- #1 position in metal roofing and siding for wood frame construction in the Northeast U.S.

- •

- #1 position in aluminum siding for towable RV exteriors in the U.S.

- •

- #1 position in aluminum siding and roofing for towable RVs in Europe

- •

- #1 position in steel exterior panels for manufactured housing in the U.S.

- •

- #1 position in vinyl windows for the UK holiday home and home center markets

Our total net sales derived from these #1 positions were $295.6 million in 2009, or 36.4% of our total net sales. We believe our leading market positions have positioned us to grow sales and improve our profitability amid a period of anticipated recovery in the residential repair and remodel, non-residential construction and RV markets.

Unique fabrication capabilities specifically tailored for niche markets. Our unique manufacturing capabilities are critical to maintaining our strong position in several niche markets for our products. In the U.S., our integrated metal coil coating capabilities provide us with a competitive advantage in the home improvement retail and RV industries as an integrated low-cost supplier of metal products with the ability to meet the demanding delivery requirements of customers in these industries. We believe we are also the only supplier who can manufacture roof drainage components from each of the four most common gutter materials: aluminum, steel, copper and vinyl. In Europe, our 103" wide aluminum coating line in The Netherlands is one of only two such lines in the world that coat metal in excess of 96" wide.

Strong, established customer relationships. We maintain long-standing relationships among our major customers across our end markets and are a critical supplier to many of our customers. Our top ten accounts have been customers of ours for more than 20 years on average, and include The Home Depot® and Lowe's, the two largest home improvement retailers in the U.S., each of whom have been our customer for over 25 years. In addition, since 2005, the year-over-year retention rate of our top 100 customers has averaged over 97%. The depth and longevity of our customer relationships provide a foundation for recurring revenues and an outlet for the introduction of new products.

More efficient, lower cost business. Since the third quarter of 2008 we have worked to operate a more efficient, lower cost business. Recent improvements reflect the results of our ongoing initiatives to

5

centralize certain management controls, rationalize our operating structure and implement best practices to improve our manufacturing culture. Specific initiatives include:

- •

- Facility rationalization. Between January 2008 and

December 2009, we closed 26 facilities representing approximately 24% of our square footage devoted to U.S. manufacturing and distribution. These closures eliminated redundant and less profitable or

unprofitable facilities while reducing supervisory and administrative personnel. In closing these facilities, we endeavored to and believe we did retain a significant portion of the profitable

business previously served by these closed facilities. We believe we have enhanced the overall productivity potential of our facilities and will be able to support the peak volumes that existed prior

to these closures.

- •

- Centralized lean manufacturing deployment. Beginning in

June 2008, we centralized the implementation and execution of our lean manufacturing initiatives and related integrated sales and operational planning. As a result, we have achieved significant

reductions in inventory, improved our efficiency and strengthened customer service at many of our facilities. We expect to continue to benefit from greater efficiencies incrementally as we implement

these best practices across our global platform.

- •

- Information technology deployment. We have deployed a

market leading enterprise resource planning, or ERP, system in our U.S. Non-Residential Building Products segment, and expect to deploy this system in our other U.S. segments over the next several

years. Our new ERP system enables us to better support our manufacturing and selling processes by providing critical information related to product cost, supply chain status and customer

profitability. In 2009, for instance, our ERP system allowed us to more easily identify and ultimately terminate over 750 customer relationships which represented insignificant revenue, while

accounting for a disproportionate portion of our costs.

- •

- Improved freight and logistics productivity. We have

undertaken a significant number of initiatives to improve our freight and logistics productivity and reduce our shipping costs, including outsourcing routes, implementing load optimization software,

changing our driver compensation structure and adding on-board GPS systems to track productivity and manage mileage-based compensation within our captive shipping fleet.

- •

- Non-metal procurement cost management. Under our procurement cost reduction initiatives, in 2009 we reduced our non-metal procurement costs by more than $6 million.

As a result of these and other initiatives, we have a more favorable cost structure than we did prior to 2008. For example, we estimate that we increased our net sales per employee by 7.5% in the twelve months ended April 2, 2010 compared to the year ended December 28, 2007. We also estimate that we reduced our selling and general expenses (excluding depreciation) as a percentage of sales volume by 3.8% in the twelve months ended April 2, 2010 compared to the year ended December 28, 2007. These improvements were achieved despite a 22.6% reduction in net sales volume during the same period. We believe that these improvements have made us more competitive and have positioned us to improve our operating margins as our key end markets recover.

Significant diversification across products, materials, customers, end markets and geography. We produce and deliver over 10,000 unique products, utilizing aluminum, steel, copper, vinyl and fiberglass, through a multi-channel distribution network that serves customers across multiple end markets and geographies. Our customer base is highly diverse, with our top ten customers accounting for less than 31% and no single customer accounting for more than 12% of our total 2009 net sales. Further, our top ten customers include customers from each of our five segments. Our sales are also diversified geographically, with 69% of our 2009 net sales originating in the U.S. and Canada, and the remainder originating in the UK, The Netherlands and France. This diversity has helped to offset the cyclicality

6

that is experienced in some of the markets we serve, while allowing us to address profitable growth opportunities as they arise in different product lines, end markets and geographies.

Committed and experienced management team. We have an experienced management team led by our chief executive officer Mitchell B. Lewis and chief financial officer R. Scott Vansant. Messrs. Lewis and Vansant each have approximately 20 years of industry experience with us and our predecessor and have effectively led us through various industry cycles, economic conditions and capital and ownership structures.

Our strategy is to leverage the strengths and experience that have provided us leading market positions to grow our business beyond our current product offerings and the customers and geographic markets we currently serve. In addition, we will endeavor to improve our capabilities and profitability through process improvement initiatives and further cost reductions.

Capture growth related to anticipated market recovery. As a leading manufacturer of exterior building products, we intend to capitalize on the anticipated recovery in the residential repair and remodel, non-residential construction and RV markets. We believe that our leading market positions, well-established customer relationships, broad product portfolio, national distribution capabilities and low cost manufacturing platform provide us with a competitive advantage over other suppliers.

Continue to focus on operational leverage. We believe that we have created significant operating leverage within our current manufacturing platform that will provide substantially greater earnings potential in a rising volume environment and position us for continued improvement in our profitability. We intend to continue to improve our cost structure through incremental lean manufacturing deployment, improved supply chain management, reduced freight and procurement costs, incremental facility rationalization, and implementation of best practices throughout our organization. We also intend to continue to integrate new information technologies across our business, which we expect will further enhance our management capabilities, improve our data quality and enable further integration of our businesses. We have already shown significant improvement in operational leverage, but we believe there remain significant opportunities for further improvements in each of these categories.

Drive growth through business development initiatives. We have instituted a series of business development initiatives that we believe will position us to achieve profitable organic growth. As part of our planning process, we task each segment to broaden its geographic presence and product offering. Given our efficient and adaptable manufacturing and distribution platform, as well as our existing channel partners and industry relationships, we believe that we are particularly well positioned to develop and profitably commercialize new products as well as modify existing products to respond to new and expanding markets, particularly as our markets continue to recover from 2009 levels. As part of our efforts, we have instituted an incentive compensation structure that specifically rewards business development efforts among key managers.

- •

- Expand into new geographic markets. Given our efficient and adaptable manufacturing and distribution platform as well as our established channel partners and industry relationships, we are well positioned to identify and selectively act on growth opportunities in new geographic markets. The versatility of our product line allows us to modify already successful products for use in other geographic areas both in the U.S. and abroad. For example, we plan to grow our sales of roof drainage products in Canada and our sales to the distributor channel outside the Northeastern U.S. Internationally, we have increased our sales effort and representation in emerging markets where our manufacturing and distribution expertise can be leveraged profitably.

7

- •

- Increase sales to new customers. We plan to continue to

identify and develop new market opportunities for our products, such as sales to government entities (including the military) or through government contractors, and leverage our product portfolio to

increase penetration of our full product line across all building materials sales channels.

- •

- Develop innovative new products. We plan to continue to engage in research and development of new products and leverage our existing relationships to distribute these products, such as our recent successful introduction of a new solid gutter cover in the U.S. as well as a roll coated aluminum coil offering with unique sand-resistant properties specifically designed for applications in the Middle East.

Identify and integrate selected value-enhancing acquisitions. Our acquisition strategy is designed to complement our business development efforts. We intend to selectively pursue bolt-on acquisitions that enable us to broaden our product offering to existing customers or to accelerate our growth in new geographic areas.

Risks Relating to Our Business

We face certain risks that could materially affect our business, financial condition, results of operations and prospects. You should carefully consider the risks and uncertainties summarized below, the risks described under "Risk Factors," the other information contained in this prospectus and our consolidated financial statements and the related notes before you decide whether to invest in our common stock. Some of the more significant challenges and risks we face include the following:

- •

- our susceptibility to cyclical fluctuations in the end markets we serve, declines in U.S., European and global general

economic conditions and the stability of our end markets;

- •

- our ability to maintain positive relations with our key customers and the risk to our business if we lose business from or

terminate relationships with our major customers;

- •

- the cost and availability of raw materials used in our products, particularly aluminum and steel, and our ability to pass

through increases in these costs to our customers;

- •

- our reliance on unique fabrication techniques and risks associated with manufacturing processes;

- •

- our dependence on information technology in our operations, including our new ERP system;

- •

- the highly competitive nature of our business;

- •

- risks arising from the international scope of our business;

- •

- our substantial indebtedness; and

- •

- restrictions contained in our debt agreements which may limit our flexibility in operating our business.

Euramax Holdings, Inc. is a corporation formed under the laws of Delaware. Our headquarters and principal executive offices are located at 5445 Triangle Parkway, Suite 350, Norcross, Georgia 30092 and our telephone number is (770) 449-7066. Our website address is www.euramax.com. Our website and the information contained therein or connected thereto is not incorporated into this prospectus or the registration statement of which this prospectus forms a part, and you should not rely on any such information in making your decision whether to purchase our securities.

8

The Euramax logo, "Flex-A-SpoutTM" and other trademarks or service marks of Euramax appearing in this prospectus are the property of Euramax. This prospectus contains additional trade names, trademarks and service marks of other companies, which are the property of their respective owners.

We operate on a 52 or 53 week fiscal year ending on the last Friday in December. Our fiscal years consisted of 52 weeks for the years ended December 25, 2009, December 26, 2008 and December 28, 2007, respectively. Fiscal years are referred to in this prospectus according to the closest calendar year. For example, 2009 refers to the fiscal year ended December 25, 2009.

9

Issuer |

Euramax Holdings, Inc. | |

Common stock offered by us |

shares. |

|

Option to purchase additional shares of common stock from us |

shares. |

|

Common stock outstanding immediately after the offering |

shares. |

|

Use of proceeds |

We estimate that the net proceeds to us in this offering, after deducting the underwriters' discount and the estimated expenses of the offering payable by us, will be approximately $ million (based on the midpoint of the price range set forth on the cover page of this prospectus). We expect to use the net proceeds of this offering to repay $ million of the term loans under our first lien credit facility. If the underwriters exercise their option to purchase additional shares from us in full, the additional net proceeds to us would be approximately $ million (and the total net proceeds to us would be approximately $ million) and we intend to use such additional net proceeds in the manner described above. See "Use of Proceeds." |

|

Dividend policy |

We do not intend to pay any dividends on our common stock for the foreseeable future following completion of the offering. See "Dividend Policy." |

|

Proposed ticker symbol |

"EMAX" |

|

Risk factors |

See "Risk Factors" beginning on page 14 of this prospectus for a discussion of factors that you should carefully consider before deciding to invest in our common stock. |

Unless we indicate otherwise or the context requires, all information in this prospectus relating to the number of shares of common stock to be outstanding after the offering:

- •

- excludes (1) shares of restricted stock

and restricted stock units granted to

employees pursuant to our Executive Incentive Plan, none of which are currently vested, and (2) shares of common stock reserved for issuance under

our equity award plans;

- •

- assumes no exercise by the underwriters of their option to purchase up to shares of

common stock from us;

and

- •

- gives effect to a for stock split with respect to our common stock that will be effected prior to consummation of this offering.

10

Summary Consolidated Financial Information

The following table sets forth our summary historical consolidated financial data as of and for the periods indicated. The financial data for the fiscal years ended December 25, 2009, December 26, 2008 and December 28, 2007 are derived from our consolidated financial statements which have been audited by Ernst & Young LLP, independent registered public accounting firm. The financial data for the fiscal year ended December 29, 2006 and the six month periods ended July 1, 2005 and December 30, 2005 have been derived from our unaudited consolidated financial statements. The summary historical consolidated financial data for fiscal year 2005 are divided into Predecessor and Successor periods as a result of the acquisition of our business by private equity funds and certain members of management on July 1, 2005, which required the application of the purchase method of accounting under GAAP. The summary historical consolidated financial data for the three months ended April 2, 2010 and March 27, 2009 have been derived from our unaudited consolidated financial statements. The unaudited consolidated interim financial information set forth below has been prepared on the same basis as our audited consolidated financial statements and includes all adjustments, consisting of normal recurring adjustments, that we consider necessary for a fair presentation of our financial position and operating results for such periods. The financial data set forth in this table are not necessarily indicative of our future results of operations and should be read in conjunction with our consolidated financial statements and related notes included elsewhere in this prospectus and the information under "Selected Consolidated Financial Data" and "Management's Discussion and Analysis of Financial Condition and Results of Operations."

11

| |

Successor(1) | Predecessor | ||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

Three months ended April 2, 2010 |

Three months ended March 27, 2009 |

Year ended December 25, 2009 |

Year ended December 26, 2008 |

Year ended December 28, 2007 |

Year ended December 29, 2006 |

Six months ended December 30, 2005 |

Six months ended July 1, 2005(2) |

||||||||||||||||||

| |

(Unaudited) |

(Unaudited) |

|

|

|

(Unaudited) |

(Unaudited) |

(Unaudited) |

||||||||||||||||||

| |

(in thousands, except per share data) |

|||||||||||||||||||||||||

Statements of Operations Data: |

||||||||||||||||||||||||||

Net sales |

$ | 200,539 | $ | 159,685 | $ | 812,055 | $ | 1,173,493 | $ | 1,245,631 | $ | 1,140,417 | $ | 511,138 | $ | 508,023 | ||||||||||

Cost of goods sold (excluding depreciation and amortization) |

164,878 | 146,289 | 675,126 | 1,009,392 | 1,052,838 | 941,426 | 420,665 | 412,792 | ||||||||||||||||||

Gross profit |

35,661 | 13,396 | 136,929 | 164,101 | 192,793 | 198,991 | 90,473 | 95,231 | ||||||||||||||||||

Selling and general (excluding depreciation and amortization) |

23,439 | 23,271 | 91,802 | 110,608 | 101,189 | 90,793 | 42,169 | 39,861 | ||||||||||||||||||

Debt restructuring, acquisition and forbearance expenses |

— | 4,001 | 13,307 | 3,798 | — | — | — | 90,905 | ||||||||||||||||||

Depreciation and amortization |

9,097 | 9,817 | 39,721 | 55,348 | 57,590 | 52,689 | 28,684 | 10,190 | ||||||||||||||||||

Goodwill and other impairments |

— | — | 3,516 | 401,376 | — | — | — | — | ||||||||||||||||||

Income (loss) from operations |

3,125 | (23,693 | ) | (11,417 | ) | (407,029 | ) | 34,014 | 55,509 | 19,620 | (45,725 | ) | ||||||||||||||

Interest expense |

(18,695 | ) | (26,540 | ) | (84,204 | ) | (109,527 | ) | (84,923 | ) | (74,675 | ) | (36,761 | ) | (24,402 | ) | ||||||||||

Gain on extinguishment of debt |

— | — | 8,723 | — | — | — | — | — | ||||||||||||||||||

Other income (loss), net |

(4,075 | ) | (4,340 | ) | 1,303 | (22,716 | ) | 5,143 | 11,949 | (1,173 | ) | (19,567 | ) | |||||||||||||

Loss from continuing operations before income taxes |

(19,645 | ) | (54,573 | ) | (85,595 | ) | (539,272 | ) | (45,766 | ) | (7,217 | ) | (18,314 | ) | (89,694 | ) | ||||||||||

Benefit for income taxes |

(557 | ) | (10,360 | ) | (1,297 | ) | (61,078 | ) | (2,529 | ) | (3,374 | ) | (3,811 | ) | (27,989 | ) | ||||||||||

Loss from continuing operations |

(19,088 | ) | (44,213 | ) | (84,298 | ) | (478,194 | ) | (43,237 | ) | (3,843 | ) | (14,503 | ) | (61,705 | ) | ||||||||||

Loss from discontinued operations, net of tax |

(96 | ) | (1,015 | ) | (1,330 | ) | (22,413 | ) | (6,194 | ) | (1,830 | ) | (603 | ) | 559 | |||||||||||

Net loss |

(19,184 | ) | (45,228 | ) | (85,628 | ) | (500,607 | ) | (49,431 | ) | (5,673 | ) | (15,106 | ) | (61,146 | ) | ||||||||||

Per Share Data: |

||||||||||||||||||||||||||

Pro forma basic and diluted net loss per share(3): |

||||||||||||||||||||||||||

Basic |

||||||||||||||||||||||||||

Diluted |

||||||||||||||||||||||||||

Pro forma weighted average shares outstanding(3): |

||||||||||||||||||||||||||

Basic |

||||||||||||||||||||||||||

Diluted |

||||||||||||||||||||||||||

Other Financial Data: |

||||||||||||||||||||||||||

Net cash flow provided by (used in): |

||||||||||||||||||||||||||

Operating activities |

(28,717 | ) | (403 | ) | 59,482 | (16,455 | ) | 74,916 | (12,639 | ) | 45,319 | (4,311 | ) | |||||||||||||

Investing activities |

664 | (1,006 | ) | (2,026 | ) | (6,784 | ) | (50,076 | ) | (65,901 | ) | (7,782 | ) | (20,964 | ) | |||||||||||

Financing activities |

(2,191 | ) | (12,688 | ) | (35,929 | ) | 59,598 | (27,893 | ) | 45,645 | (28,329 | ) | 24,135 | |||||||||||||

Capital expenditures |

(1,519 | ) | (1,022 | ) | (4,351 | ) | (14,824 | ) | (21,255 | ) | (25,048 | ) | (9,846 | ) | (7,526 | ) | ||||||||||

Adjusted EBITDA(4) |

13,226 | (6,090 | ) | 56,344 | 68,291 | 101,685 | 115,403 | 51,855 | 57,772 | |||||||||||||||||

Balance Sheet Data: |

||||||||||||||||||||||||||

Cash and cash equivalents |

38,320 | — | 69,944 | 48,658 | 8,272 | 16,425 | 47,409 | — | ||||||||||||||||||

Working capital(5) |

158,709 | — | 163,393 | 167,849 | 138,828 | 217,296 | 161,957 | — | ||||||||||||||||||

Total assets |

729,163 | — | 758,626 | 841,966 | 1,423,648 | 1,190,767 | 1,072,292 | — | ||||||||||||||||||

Total debt, including current portion |

523,295 | — | 525,319 | 884,740 | 812,401 | 807,849 | 735,337 | — | ||||||||||||||||||

Total shareholders' equity (deficit) |

23,674 | — | 47,060 | (259,282 | ) | 273,771 | 320,276 | 237,731 | — | |||||||||||||||||

- (1)

- Our

fiscal year ends on the last Friday in December of each calendar year. Each of our fiscal years presented is based on a 52 week period. Our

fiscal year ended December 31, 2010 will include 53 weeks.

- (2)

- On

July 1, 2005, we were acquired by certain private equity funds and members of management, as described under "Management's Discussion and

Analysis of Financial Condition and Results of Operations—History." As a result of the application of the purchase method of accounting in connection with the acquisition, our

shareholders' equity increased by $156.8 million. In addition, our net income for the six months ended July 1, 2005 reflects certain costs and expenses associated with the acquisition.

- (3)

- All

share and per share amounts reflect a for stock split with

respect to our common stock which will be effected prior to

consummation of this offering.

- (4)

- Adjusted EBITDA is defined as net loss plus (i) benefit for income taxes, (ii) interest expense and (iii) depreciation and amortization, as further adjusted to exclude the effects of certain income and expense items that management believes make it more difficult to assess the Company's actual operating performance.

12

- We

believe Adjusted EBITDA is helpful to investors and our management in highlighting trends because Adjusted EBITDA excludes the results of

certain decisions of operating management that can differ significantly from company to company depending on long-term strategic decisions regarding capital structure, the tax

jurisdictions in which companies operate and capital investments. We believe that excluding items such as goodwill and asset impairment charges, restructuring charges, gain on extinguishment of debt

and the other charges specified below helps investors compare our operating performance with our results in prior periods. We believe it is appropriate to exclude these items as they are not related

to ongoing operating performance and, therefore, limit comparability between periods and between us and similar companies. Management compensates for the limitations of using non-GAAP

financial measures by using them to supplement GAAP results to provide a more complete understanding of the factors and trends affecting the business than GAAP results alone.

- We

also believe Adjusted EBITDA is useful to investors because it is frequently used by securities analysts, investors and other interested

parties in the evaluation of companies in our industry. We understand that investors use Adjusted EBITDA, among other things, to assess our period-to-period operating

performance and to gain insight into the manner in which management analyzes operating performance. In addition, we believe that Adjusted EBITDA is useful in evaluating our operating performance

compared to that of other companies in our industry because the calculation of Adjusted EBITDA generally eliminates the effects of financing and income taxes and the accounting effects of capital

spending and acquisitions, which items may vary for different companies for reasons unrelated to overall operating performance. Using several measures to evaluate the business allows us and investors

to assess our relative performance against our competitors and ultimately monitor our capacity to generate returns for our stockholders.

- Although we believe that Adjusted EBITDA can make an evaluation of our operating performance more consistent because it removes items that do not reflect our core operations, other companies, even in the same industry, may define Adjusted EBITDA differently than we do. Because not all companies use identical calculations, our presentation of Adjusted EBITDA may not be comparable to similarly titled measures of other companies. As a result, it may be difficult to use Adjusted EBITDA or similarly named non-GAAP measures that other companies may use to compare the performance of those companies to our performance. We do not, and investors should not, place undue reliance on Adjusted EBITDA as a measure of operating performance. Adjusted EBITDA is not a measure of financial performance under accounting principles generally accepted in the U.S., and should not be considered an alternative to net income as a measure of operating performance or cash flows from operating, investing and financing activities as a measure of liquidity. In addition, Adjusted EBITDA is not intended to be a measure of free cash flow available for management's discretionary use, as it does not consider certain cash requirements such as interest payments, tax payments and other debt service requirements.

Reconciliation of net income (loss) attributable to Adjusted EBITDA is as follows:

| |

Three months ended April 2, 2010 |

Three months ended March 27, 2009 |

Year ended December 25, 2009 |

Year ended December 26, 2008 |

Year ended December 28, 2007 |

Year ended December 29, 2006 |

Six months ended December 30, 2005 |

Six months ended July 1, 2005 |

|||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Net loss |

$ | (19,184 | ) | $ | (45,228 | ) | $ | (85,628 | ) | $ | (500,607 | ) | $ | (49,431 | ) | $ | (5,673 | ) | $ | (15,106 | ) | $ | (61,146 | ) | |

Add: |

|||||||||||||||||||||||||

Provision (benefit) for income taxes |

(557 | ) | (10,360 | ) | (1,297 | ) | (61,078 | ) | (2,529 | ) | (3,374 | ) | (3,811 | ) | (27,989 | ) | |||||||||

Interest expense |

18,695 | 26,540 | 84,204 | 109,527 | 84,923 | 74,675 | 36,761 | 24,402 | |||||||||||||||||

Depreciation and amortization |

9,263 | 10,270 | 41,347 | 57,689 | 60,116 | 55,009 | 29,235 | 10,190 | |||||||||||||||||

Adjustments: |

|||||||||||||||||||||||||

Goodwill and other impairments |

— | — | 3,516 | 401,376 | — | — | — | — | |||||||||||||||||

Other income/loss net |

4,075 | 4,340 | (1,303 | ) | 22,716 | (5,143 | ) | (11,949 | ) | 1,173 | 19,567 | ||||||||||||||

Debt restructuring, acquisition and forbearance expenses(a) |

— | 4,001 | 13,307 | 4,234 | 1,206 | 169 | 3,000 | 92,441 | |||||||||||||||||

Management and advisory fees(b) |

— | — | — | — | — | — | — | 482 | |||||||||||||||||

Gain on extinguishment of debt(c) |

— | — | (8,723 | ) | — | — | — | — | — | ||||||||||||||||

Loss from discontinued operations, net of tax |

96 | 1,015 | 1,330 | 22,413 | 6,194 | 1,830 | 603 | (559 | ) | ||||||||||||||||

Stock compensation expense |

583 | 315 | 2,885 | 925 | 1,107 | 1,261 | — | 384 | |||||||||||||||||

Non-recurring expenses |

255 | 3,017 | 6,707 | 11,096 | 5,242 | 3,455 | — | — | |||||||||||||||||

Adjusted EBITDA |

13,226 | (6,090 | ) | 56,344 | 68,291 | 101,685 | 115,403 | 51,855 | 57,772 | ||||||||||||||||

- (a)

- Debt

restructuring, acquisition and forbearance expenses include: (i) for the six months ended July 1, 2005, expenses associated with the

acquisition of the Company by certain private equity funds and members of management, and the impact on cost of goods sold of purchase accounting adjustments to inventory resulting from an

acquisition, and (ii) for the years ended December 26, 2008 and December 25, 2009, expenses associated with a series of forbearance and limited waiver agreements in place from

November 10, 2008 to June 29, 2009 with our then-existing lenders. See "Management's Discussion and Analysis of Financial Condition and Results of

Operations—History."

- (b)

- Represents

advisory fees paid to Goldman, Sachs & Co. prior to June 29, 2009, and advisory fees paid to CVC Management LLC

prior to July 1, 2005.

- (c)

- Represents

the gain recognized in connection with our June 2009 debt restructuring, in which lenders cancelled 100% of amounts owed under our

then-existing Second Lien Credit Agreement consisting of principal and accrued interest of $191 million and $12 million, respectively, in exchange for 100% of our issued and

outstanding shares of common stock. See "Management's Discussion and Analysis of Financial Condition and Results of Operations—History."

- (5)

- We define working capital as current assets less current liabilities.

13

An investment in our common stock involves a high degree of risk. You should carefully consider the risk factors set forth below as well as the other information contained in this prospectus before investing in our common stock, or deciding whether you will or will not participate in this offering. The risks described below are not the only risks facing us. Any of the following risks, and additional risks and uncertainties not currently known to us or those we currently view to be immaterial, could materially and adversely affect our business, financial condition, results of operations, prospects or cash flows. In such a case, the trading price of our common stock may decline and you may lose all or part of your original investment.

Risks Relating to Our Business

Demand for our products is cyclical, and reduced demand in our end markets is likely to adversely affect our profitability and cash flow.

Demand for many of our products is cyclical in nature. Because the ultimate end users of our products are most typically individuals electing whether to make discretionary expenditures, our results are affected by various macroeconomic trends which affect consumer confidence and access to financing. Sales of our residential building products for repair, remodel and replacement applications depend upon the availability of home equity and consumer financing, low interest rates, the turnover and aging of housing stock, wear and tear, weather damage and consumer sentiment. Expenditures in the broader U.S. residential repair and remodel industry declined substantially between 2007 and 2009 due to adverse changes in many of these factors. Sales of our non-residential building products are affected by consumer confidence, interest rates, consumer disposable income, the strength of agricultural markets, consumer access to affordable financing and commercial construction trends. Demand for our RV products is driven by trends in disposable income, interest rates and general economic conditions, as well as demographic trends relating to consumers in the 55 through 74 year old age group, who constitute a significant source of demand for RV products. For example, the U.S. towable RV market suffered a 30% decline in shipments in 2008 and an additional 27% decline in 2009 due to changes in certain of these economic factors. Adverse trends in these and other cyclical factors are likely to materially reduce demand for and sales of our products. Moreover, simultaneous declines in multiple end markets, such as those we experienced in 2008 and 2009, could have a material adverse effect on our business, financial condition, results of operations, prospects and cash flows.

In addition, our sales to the European RV industry, which comprised 8%, 10% and 11% of our net sales in 2009, 2008 and 2007, respectively, are expected to decline as this end market continues to contract. The overall European RV industry is forecast to contract by 8% per year from 2009 through 2011. Any contraction in this market will reduce our sales, which would adversely affect our profitability and cash flow.

Our business, financial condition, results of operations, prospects and cash flows have been and in the future may be materially and adversely affected by U.S., European and global general economic conditions.

Many aspects of our business, including demand for our products and the pricing and availability of raw materials, are affected by global general economic conditions and, specifically, economic conditions in the U.S. and Europe. General economic conditions and predictions regarding future economic conditions also affect our business strategies, and a decrease in demand for our products or other adverse effects resulting from an economic downturn affecting our geographic end markets may cause us to fail to achieve our anticipated financial results. General economic factors beyond our control that affect our business and end-markets include interest rates, inflation, deflation, consumer credit availability, consumer debt levels, consumer confidence, employment levels, business confidence levels, housing markets, energy costs, tax rates and policy, unemployment rates,

14

commencement or escalation of war or hostilities, the threat or possibility of war, terrorism or other global or national unrest, political or financial instability, and other matters that influence spending by our customers and in our end markets. Increasing volatility in financial markets may cause these factors to change with a greater degree of frequency or increase in magnitude.

Beginning in the fall of 2008 and continuing through 2009 and into 2010, the global economy entered a financial crisis and severe global recession, which materially and adversely impacted our business and the businesses of our customers. Volatile capital and credit markets, declining business and consumer confidence and increased unemployment precipitated a continuing economic slowdown. The economic slowdown decreased demand for the products offered by our customers, resulting in decreased sales volumes and reduced earnings. The severe downturn affected all of our end markets, ultimately required us to restructure our debt in June 2009 and caused our then-existing equity holders to lose the full value of their investment. See "Management's Discussion and Analysis of Financial Condition and Results of Operations—History." Part of our business strategy anticipates recovery in the residential repair and remodel, non-residential construction and RV markets; however, there can be no assurances that a recovery in any of these markets will occur as anticipated. Although there have recently been signs of recovery in many regions, economic weakness could continue or worsen, as has occurred in certain regions of Europe due to concerns over the fiscal and monetary situation in a number of countries. There can be no assurance that governmental or other measures to aid economic recovery, including economic stimulus legislation, will be effective or that our sales volumes will increase or stabilize in the future. There can also be no assurance that the conditions that affected us beginning in the fall of 2008 and during 2009 will not recur or worsen. Continued adverse economic conditions could have a material adverse effect on our business, financial condition, results of operations, prospects and cash flows.

A decline in our relations with our key customers or the amount of products they purchase from us could materially adversely affect our business, financial position, results of operations, prospects and cash flows.

Our business depends on our ability to maintain positive relations with our key customers. In 2009 our largest customer accounted for approximately 11.3% of our net sales and our top ten customers combined accounted for approximately 30.9% of our net sales. Although we have established and maintain significant long-term relationships with our key customers, we cannot assure you that all of these relationships will continue or will not diminish. In addition, we generally do not enter into long-term contracts with our customers and they generally do not have an obligation to purchase products from us. The loss of, or a diminution in, our relationship with any of our largest customers would have a material adverse effect on us. In addition, the loss of any of our largest customers in any of our segments could have a material adverse effect on the results of operations of that segment.

Our competitors may adopt more aggressive sales policies and devote greater resources to the development, promotion and sale of their products than we do, which could result in a loss of customers. Generally, our customers are price sensitive, which could further lead to the loss of customers if our prices do not remain competitive. The loss of, or a reduction in orders from, any significant customers, losses arising from customer disputes regarding shipments, fees, merchandise condition or related matters, or our inability to collect accounts receivable from any major customer could have a material adverse effect on our business. Customers accounting for a significant amount of our revenues may also become more resistant to price changes as their purchase volumes increase relative to our other customers, limiting our ability to increase prices to these customers and eroding our margins. Also, revenue from customers that have accounted for significant revenue in past periods, individually or as a group, may not continue in future periods or, if continued, may not reach or exceed historical levels in any period.

Further, we have no operational or financial control over our customers and have limited influence over how they conduct their businesses. If any of these customers fail to remain competitive

15

in their respective markets or encounter financial or operational problems, our revenue and profitability may decline. Market conditions could also result in our significant customers experiencing financial difficulties. We are exposed to the credit risk of our customers, and their failure to meet their financial obligations when due because of their bankruptcy, lack of liquidity, operational failure or other reasons could result in decreased sales and earnings for us. The decreased availability of consumer credit resulting from the financial crisis, as well as general unfavorable economic conditions, may cause consumers to further decrease their spending, which would reduce the demand for the products of our customers, which would affect our sales and cash flow.

Certain of our customers have been expanding and may continue to expand through consolidation and internal growth, potentially increasing their buying power, which could materially and adversely affect our business, financial condition, results of operations, prospects and cash flows. Certain of our important customers are large companies with significant buying power. In addition, potential further consolidation among our customers could enhance the ability of these customers to seek more favorable terms, including pricing, for the products that they purchase from us. Accordingly, our ability to maintain or raise prices in the future may be limited, including during periods of raw material and other cost increases. See "—Our financial performance is affected by the prices of our key raw materials, particularly aluminum and steel. Price fluctuations relating to aluminum and steel could have a material adverse effect on our business, financial condition, results of operations, prospects and cash flows and limit our operating flexibility." If we are forced to reduce prices or to maintain prices during periods of increased production costs, or if we lose customers because of pricing or other methods of competition, our business, financial condition, results of operations, prospects and cash flows may be materially and adversely affected.

Our financial performance is affected by the prices of our key raw materials, particularly aluminum and steel. Price fluctuations relating to aluminum and steel could have a material adverse effect on our business, financial condition, results of operations, prospects and cash flows and limit our operating flexibility.

The manufacture of our products requires substantial amounts of raw materials, which consist principally of aluminum and steel and, to a lesser extent, paint, glass, copper and vinyl. Over 75% of our raw material costs consist of the cost of aluminum and steel. Our manufacturing operations and our financial performance is affected to a substantial extent by the market prices for these raw materials.

Aluminum and steel are cyclical commodities with prices subject to global market forces of supply and demand and other related factors. Such factors include speculative activities by market participants, production capacity, strength or weakness in key end markets such as housing and transportation, political and economic conditions and production costs in major production regions. Prices have been historically volatile. For example, from January 2008 through May 2010 the London Metals Exchange settlement price for spot aluminum ranged from a high of $1.49 per pound in July 2008 to a low of $0.57 per pound in February 2009. Changes in the prices of aluminum and steel could have a material adverse effect on our business, financial condition, results of operations, prospects and cash flows.

We have historically priced our products by reference to raw material costs and generally we seek to pass through raw material price increases to our customers. However, due to the uncertainty of aluminum and steel prices and the time between material purchases and product sales, we cannot assure you that we always will be able to successfully pass through such price increases to our customers or fully offset the effects of high raw materials costs through productivity improvements. For example, in the U.S., we purchase aluminum based upon the 30-day average price in the month prior to the month of delivery. If we cannot pass increases in the cost of raw materials to our customers, higher prices could cause our customers to consider competitors' products, some of which may be available at a lower cost. For example, where a competitor had previously purchased a large quantity of

16

raw materials into inventory at a lower price, such a competitor could afford to pass on savings from subsequently higher prices to its customers. We also risk purchasing materials for delivery commitments to customers who later file for bankruptcy protection or repudiate or cancel their purchase agreement with us during a falling price environment, causing us to take delivery of raw materials at an above market cost. As a result, to the extent that the time lag associated with a price increase pass through becomes significant, such increases may have a material adverse effect on our business, financial condition, results of operations, prospects and cash flows.

Where changes in aluminum and steel prices are passed through to our customers, increases or decreases in aluminum and steel prices will cause corresponding increases and decreases in reported net sales, causing fluctuations in reported revenues that are unrelated to our level of business activity. Accordingly, any change in the price of aluminum and/or steel could have a material adverse effect on our business, financial condition, results of operations, prospects and cash flows. See "Management's Discussion and Analysis of Financial Condition and Results of Operations—Overview and Executive Summary—Key Factors Affecting our Business" and "Business—Raw Materials."

Our performance is dependent on the continued availability of necessary raw materials, particularly aluminum and steel.

We are dependent on the continued availability of critical raw materials, particularly aluminum and steel. The supply and demand for these critical raw materials are subject to cyclical price fluctuations and other market disturbances, including supply shortages. We purchase a majority of our steel from domestic steel producers, but we have no long-term contracts with any steel suppliers and we generally purchase steel at market prices. In the event of an industry-wide general shortage of raw materials we use, or a shortage or discontinuation of certain types of raw materials, we may not be able to arrange for alternative sources of such raw materials and products. The number of available suppliers has been reduced in recent years due to industry consolidation and bankruptcies affecting steel and metal producers and this trend may continue. Our top ten suppliers accounted for 35% of our purchases during 2009. If we are required to utilize alternative suppliers, this could cause delays in the delivery of such raw materials and possible losses in revenue. Also, alternative suppliers may not be available, or may not provide their products and services at similar or favorable prices. Additionally, increased demand from other countries such as China has put upward pressure on the market prices for raw materials. We also purchase raw materials on a regular basis in an effort to maintain our inventory at levels that we believe are sufficient to satisfy the anticipated needs of our customers based upon historic buying practices and market conditions. However, we cannot assure you that there will always be an adequate supply to meet our demand for aluminum and steel, and we are subject to the risk of lost revenue in the event that we cannot obtain quantities of aluminum and steel necessary to meet customer demand. Interruptions in the operations of our suppliers due to labor or production problems, delivery interruptions, fires, floods, explosions, environmental issues, other Acts of God or other events could disrupt the supply of raw materials. Any disruption in the supply of aluminum and/or steel could have a material adverse effect on our business, financial condition, results of operations, prospects and cash flows, including temporarily impairing our ability to manufacture our products for our customers or requiring us to pay higher prices in order to obtain aluminum and/or steel from other sources, which could affect our net sales and profitability.

Due to our reliance on unique fabrication techniques for the niche markets we serve, our business is subject to risks associated with manufacturing processes.

We manufacture most of our products at our own production facilities. Any loss of the use of all or a portion of any of our facilities due to accidents, fires, explosions, labor issues, adverse weather conditions, natural disasters such as floods, tornados, hurricanes, ice storms and earthquakes, supply interruptions, transportation interruptions, human error, mechanical failure, terrorist acts, power

17

outages, discharges or releases of toxic or hazardous substances or gases, storage tank leaks and other environmental issues, or otherwise, whether short or long-term, could have a material adverse effect on us and our operations. As such events occur, we may experience substantial business losses, production delays, third party lawsuits and significant repair costs, as well as personal injury and/or loss of life, which could materially and adversely affect our business, financial condition, results of operations, prospects and cash flows.

In addition, unexpected failures of our equipment and machinery may result in production delays, revenue loss and significant repair costs, as well as injuries to our employees. Any interruption in production capability may require us to make large capital expenditures to remedy the situation, which could have a negative impact on our profitability and cash flows. A loss or interruption of production at certain of our facilities, such as our manufacturing facilities in The Netherlands, could significantly disrupt our operations and affect a large number of customers, decreasing our revenues. Moreover, there are a limited number of manufacturers that make the machines we use in our business. Because we supply certain of our products to OEMs, a temporary or long-term business disruption could result in a permanent loss of customers, who may be required to seek alternate suppliers. If this were to occur, our future sales levels, and therefore our business, financial condition, results of operations, prospects and cash flows, could be materially and adversely affected.

We are also subject to losses associated with equipment shutdowns which may be caused by the loss or interruption of electrical power to our facilities due to unusually high demand, blackouts, adverse weather, equipment failure or other catastrophic events. Losses caused by disruptions in the supply of electrical power could materially and adversely affect our business, financial condition, results of operations, prospects and cash flows. See "—Losses caused by disruptions in the supply of power or increases in energy costs would adversely affect our operations."

Our production facilities are located throughout North America and Europe. In the future, we may construct new manufacturing plants or repair or refurbish existing plants. Delays in the construction, repair and refurbishment of a manufacturing plant can occur as a result of events such as insolvency, work stoppages, other labor actions or "force majeure" events experienced by the companies working on the plants that are beyond our control. Any termination or breach of contract following such an event may result in, among other things, the forfeiture of prior deposits or payments made by us, potential claims and impairment of losses. A significant delay in the construction of a new plant or repair of an existing plant could have a material adverse effect on our business, financial condition, results of operations, prospects and cash flows.

Losses caused by disruptions in the supply of power or increases in energy costs would adversely affect our operations.

We use large amounts of electricity, natural gas and other energy sources to operate our manufacturing facilities. Any loss of power which reduces the amperage to our equipment or causes an equipment shutdown would result in a reduction in production volume. Interruptions in the supply of electrical power to our facilities can be caused by a number of circumstances, including unusually high demand, blackouts, equipment or transformer failure, human error, natural disasters or other catastrophic events. If such a condition were to occur, we may lose production for a prolonged period of time and incur significant losses. In addition, the volatility in costs of fuel, principally natural gas, and other utility services, principally electricity, used by our production facilities affect operating costs. Fuel and utility prices have been, and will continue to be, affected by factors outside our control, such as supply and demand for fuel and utility services in both local and regional markets and the potential regulation of greenhouse gases. Future increases in fuel and utility prices may have a material adverse effect on our business, financial condition, results of operations, prospects and cash flows.

18

The insurance that we maintain may not fully cover all potential exposures.

We maintain property, casualty and workers' compensation insurance, but such insurance does not cover all risks associated with the hazards of our business and is subject to limitations, including deductibles and maximum liabilities covered. We may incur losses beyond the limits, or outside the coverage, of our insurance policies, including liabilities for environmental compliance or remediation. In addition, from time to time, various types of insurance for companies in our industries have not been available on commercially acceptable terms or, in some cases, have not been available at all. In the future, we may not be able to obtain coverage at current levels, and our premiums may increase significantly on coverage that we maintain.