UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 8-K

CURRENT REPORT PURSUANT TO SECTION 13 OR 15 (d)

OF THE SECURITIES EXCHANGE ACT OF 1934

Date of Report: July 19, 2010

(Date of earliest event reported)

INTERNATIONAL BUSINESS MACHINES

CORPORATION

(Exact name of registrant as specified in its charter)

|

New York |

|

1-2360 |

|

13-0871985 |

|

(State of Incorporation) |

|

(Commission File Number) |

|

(IRS employer Identification No.) |

|

ARMONK, NEW YORK |

|

10504 |

|

(Address of principal executive offices) |

|

(Zip Code) |

914-499-1900

(Registrant’s telephone number)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

o Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425)

o Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12)

o Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b))

o Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c))

Item 2.02. Results of Operations and Financial Condition.

The registrant’s press release dated July 19, 2010, regarding its financial results for the periods ended June 30, 2010, including consolidated financial statements for the periods ended June 30, 2010, is Attachment I of this Form 8-K. Attachment II are the slides for IBM’s Chief Financial Officer Mark Loughridge’s second quarter earnings presentation on July 19, 2010, as well as certain reconciliation and other information (“Non-GAAP Supplementary Materials”) for information in Attachment I (press release), Attachment II (slides) and in Mr. Loughridge’s presentation. All of the information in Attachment I and II is hereby filed.

IBM’s web site (www.ibm.com) contains a significant amount of information about IBM, including financial and other information for investors (www.ibm.com/investor/). IBM encourages investors to visit its various web sites from time to time, as information is updated and new information is posted.

SIGNATURE

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, hereunto duly authorized.

|

Date: July 19, 2010 |

|

|

|

|

|

|

|

|

By: |

/s/ James J. Kavanaugh |

|

|

|

|

|

|

|

James J. Kavanaugh |

|

|

|

Vice President and Controller |

ATTACHMENT I

IBM REPORTS 2010 SECOND-QUARTER RESULTS

· Diluted earnings per share of $2.61, up 13 percent;

· 30 consecutive quarters of EPS growth, 12 of last 14 at double digits;

· Full-year 2010 EPS expectations raised to at least $11.25;

· Net income of $3.4 billion, up 9 percent;

· Pre-tax income of $4.6 billion, up 7 percent;

· Pre-tax margin of 19.3 percent, up 1 point;

· Revenue of $23.7 billion, up 2 percent, as reported and adjusting for currency;

· Growth markets revenue up 14 percent; first-half revenue as large as total Euro zone revenue;

· BRIC countries revenue up 22 percent;

· Business Analytics revenue up 14 percent;

· Software revenue up 2 percent, 6 percent excluding divested PLM operations;

· Systems and Technology revenue up 3 percent;

· Services revenue up 2 percent;

· Services backlog of $129 billion, up $1 billion, adjusting for currency.

ARMONK, N.Y., July 19, 2010 . . . IBM (NYSE: IBM) today announced second-quarter 2010 diluted earnings of $2.61 per share compared with diluted earnings of $2.32 per share in the second quarter of 2009, an increase of 13 percent.

Second-quarter net income was $3.4 billion compared with $3.1 billion in the second quarter of 2009, an increase of 9 percent. Total revenues for the second quarter of 2010 of $23.7 billion increased 2 percent (2 percent, adjusting for currency) from the second quarter of 2009. The impact of changes in currency rates since IBM’s first-quarter earnings report in April reduced revenue by approximately $500 million in the second quarter.

“In the second quarter we again delivered double-digit earnings-per-share growth, increased margins, as well as improving constant-currency revenue performance in our on going software, services and hardware businesses, and in all geographies,” said Samuel J. Palmisano, IBM chairman, president and chief executive officer.

“With the benefit of our strategic growth investments, our mix of higher-value business and the introduction of new System z and Power Systems, we are confident of our ability in the second half of the year to continue our strong business performance, grow profit and drive shareholder returns. As a result, we expect full-year 2010 diluted earnings per share of at least $11.25.”

From a geographic perspective, the Americas’ second-quarter revenues were $10.2 billion, an increase of 3 percent (2 percent, adjusting for currency) from the 2009 period. Revenues from Europe/Middle East/Africa were $7.4 billion, down 6 percent (1 percent, adjusting for currency). Asia-Pacific revenues increased 9 percent (3 percent, adjusting for currency) to $5.4 billion. OEM revenues were $677 million, up 26 percent compared with the 2009 second quarter. Revenues from the company’s growth markets organization increased 14 percent (9 percent, adjusting for currency) and represented 20 percent of IBM’s total geographic revenue in the quarter. In the first half, revenue for the growth markets organization was as large as the total revenue of the Euro zone countries for the first time.

Total Global Services revenues increased 2 percent (1 percent, adjusting for currency). Global Technology Services segment revenues increased 1 percent (flat, adjusting for currency) to $9.2 billion. Global Business Services segment revenues were up 3 percent (3 percent, adjusting for currency) at $4.5 billion.

IBM signed services contracts totaling $12.3 billion, at actual rates, a decrease of 12 percent (12 percent, adjusting for currency). In the quarter, 15 services contracts greater than $100 million were signed compared with 13 contracts last quarter.

Total Outsourcing services (GTS Outsourcing and Application Management Outsourcing) signings decreased 19 percent (19 percent, adjusting for currency) to $6.5 billion. Signings of larger new-business outsourcing services contracts, which result in more immediate revenue than contract extensions, had strong growth.

Signings in Transactional services (Consulting, Integrated Technology Services and Application Management Systems Integration) were $5.8 billion, a decrease of 3 percent (3 percent, adjusting for currency).

The estimated services backlog at June 30 was $129 billion at actual rates, down $2 billion year over year (up $1 billion, adjusting for currency).

Revenues from the Software segment were $5.3 billion, an increase of 2 percent (2 percent, adjusting for currency), or 6 percent excluding the first-quarter divestiture of the Product Lifecycle Management operations (PLM), compared with the second quarter of 2009. Revenues from IBM’s key middleware products, which include WebSphere, Information Management, Tivoli, Lotus and Rational products, were $3.3 billion, an increase of 9 percent (10 percent, adjusting for currency) versus the second quarter of 2009. Operating systems revenues of $544 million increased 3 percent (2 percent, adjusting for currency) compared with the prior-year quarter.

Revenues from the WebSphere family of software products, which delivers capabilities that enable clients to integrate and manage business processes across the organization, increased 17 percent year over year. Revenues from Information Management software, which enables clients to integrate, manage and use information to gain business value, increased 7 percent. Revenues from Tivoli software, which helps clients manage technology and business assets by providing visibility, control and automation across the organization, increased 18 percent, and revenues from Lotus software, which connects people and processes for more effective communication and increased productivity through collaboration, messaging and social networking software, decreased 6 percent. Revenues from Rational software, which supports software development for both IT and embedded system solutions, increased 1 percent.

Revenues from the company’s Business Analytics operations within Global Business Services and Software increased 14 percent.

Revenues from the Systems and Technology segment totaled $4.0 billion for the quarter, up 3 percent (4 percent, adjusting for currency) from the second quarter of 2009. Systems revenues increased 1 percent (2 percent, adjusting for currency). Revenues from the System x increased 30 percent. Revenues from Power Systems decreased 10 percent compared with the 2009 period. Revenues from System z mainframe server products decreased 24 percent compared with the year-ago period. Total delivery of System z computing power, as measured in MIPS (millions of instructions per second), decreased 14 percent. Revenues from System Storage increased 5 percent, and revenues from Retail Store Solutions increased 31 percent. Revenues from Microelectronics OEM increased 23 percent.

Global Financing segment revenues decreased 4 percent (5 percent, adjusting for currency) in the second quarter to $544 million.

The company’s total gross profit margin was 45.6 percent in the 2010 second quarter compared with 45.5 percent in the 2009 second-quarter period, led by improving margins in Software and Global Business Services.

Total expense and other income decreased 1 percent to $6.2 billion compared with the prior-year period. SG&A expense of $5.1 billion decreased 1 percent year over year compared with prior-year expense. RD&E expense of $1.5 billion increased 3 percent compared with the year-ago period. Intellectual property and custom development income decreased to $297 million compared with $302 million a year ago. Other (income) and expense was income of $95 million compared with prior-year income of $28 million. Interest expense decreased to $90 million compared with $101 million in the prior year.

IBM’s tax rate in the second-quarter 2010 was 26.0 percent compared with 27.2 percent in the second quarter of 2009.

The weighted-average number of diluted common shares outstanding in the

second-quarter 2010 was 1.30 billion compared with 1.34 billion shares in the same period of 2009. As of June 30, 2010, there were 1.26 billion basic common shares outstanding.

Debt, including Global Financing, totaled $26.7 billion, compared with $26.1 billion at year-end 2009. From a management segment view, Global Financing debt totaled $21.2 billion versus $22.4 billion at year-end 2009, resulting in a debt-to-equity ratio of 7.1 to 1. Non-global financing debt totaled $5.5 billion, an increase of $1.7 billion since year-end 2009, resulting in a debt-to-capitalization ratio of 23.1 percent from 16.0 percent.

IBM ended the second-quarter 2010 with $12.2 billion of cash on hand and generated free cash flow of $3.0 billion, down approximately $400 million year over year. Free cash flow for the first half of the year was $4.4 billion, flat year over year. The company returned $4.9 billion to shareholders through $0.8 billion in dividends and $4.1 billion of share repurchases. The balance sheet remains strong, and the company is well positioned to support its full-year objectives.

Year-To-Date 2010 Results

Net income for the six months ended June 30, 2010 was $6.0 billion compared with $5.4 billion in the year-ago period, an increase of 11 percent. Diluted earnings per share were $4.57 compared with $4.02 per diluted share for the 2009 period, an increase of 14 percent. Revenues for the six-month period totaled $46.6 billion, an increase of 4 percent (1 percent, adjusting for currency) compared with $45.0 billion for the six months of 2009.

Forward-Looking and Cautionary Statements

Except for the historical information and discussions contained herein, statements contained in this release may constitute forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements are based on the company’s current assumptions regarding future business and financial performance. These statements involve a number of risks, uncertainties and other factors that could cause actual results to differ materially, including the following: a downturn in economic environment and corporate IT spending budgets; the company’s failure to meet growth and productivity objectives, a failure of the company’s innovation initiatives; risks from investing in growth opportunities; failure of the company’s intellectual property portfolio to prevent competitive offerings and the failure of the company to obtain necessary licenses; breaches of data security; fluctuations in revenue and purchases, impact of local legal, economic, political and health conditions; adverse effects from environmental matters, tax matters and the company’s pension plans; ineffective internal controls; the company’s use of accounting estimates; the company’s ability to attract and retain key personnel and its reliance on critical skills; impact of relationships with critical suppliers; currency fluctuations and customer financing risks; impact of changes in market liquidity conditions and customer credit risk on receivables; reliance on third party distribution channels; the company’s ability to successfully manage acquisitions and alliances; risk factors related to IBM securities; and other risks, uncertainties and factors discussed in the company’s Form 10-Q, Form 10-K and in the company’s other filings with the U.S. Securities and Exchange Commission (SEC) or in materials incorporated therein by reference. Any forward-looking statement in this release speaks only as of the date on which it is made. The company assumes no obligation to update or revise any forward-looking statements.

Presentation of Information in this Press Release

In an effort to provide investors with additional information regarding the company’s results as determined by generally accepted accounting principles (GAAP), the company has also disclosed in this press release the following non-GAAP information which management believes provides useful information to investors:

IBM Results —

· presenting non-global financing debt-to-capitalization ratio;

· adjusting for free cash flow;

· adjusting for currency (i.e., at constant currency);

· excluding divested PLM operations.

The rationale for management’s use of non-GAAP measures is included as part of the supplementary materials presented within the second-quarter earnings materials. These materials are available on the IBM investor relations Web site at www.ibm.com/investor and are being included in Attachment II (“Non-GAAP Supplementary Materials”) to the Form 8-K that includes this press release and is being submitted today to the SEC.

Conference Call and Webcast

IBM’s regular quarterly earnings conference call is scheduled to begin at 4:30 p.m. EDT, today. Investors may participate by viewing the Webcast at www.ibm.com/investor/2q10. Presentation charts will be available on the Web site shortly before the Webcast.

Financial Results Below (certain amounts may not add due to use of rounded numbers; percentages presented are calculated from the underlying whole-dollar amounts).

INTERNATIONAL BUSINESS MACHINES CORPORATION

COMPARATIVE FINANCIAL RESULTS

(Unaudited; Dollars in millions except per share amounts)

|

|

|

Three Months |

|

Six Months |

|

||||||||||||

|

|

|

Ended June 30, |

|

Ended June 30, |

|

||||||||||||

|

|

|

|

|

|

|

Percent |

|

|

|

|

|

Percent |

|

||||

|

|

|

2010 |

|

2009 |

|

Change |

|

2010 |

|

2009 |

|

Change |

|

||||

|

REVENUE |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Global Technology Services |

|

$ |

9,234 |

|

$ |

9,108 |

|

1.4 |

% |

$ |

18,540 |

|

$ |

17,862 |

|

3.8 |

% |

|

Gross margin |

|

34.6 |

% |

34.8 |

% |

|

|

34.5 |

% |

34.3 |

% |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Global Business Services |

|

4,483 |

|

4,338 |

|

3.3 |

% |

8,893 |

|

8,736 |

|

1.8 |

% |

||||

|

Gross margin |

|

28.5 |

% |

27.2 |

% |

|

|

27.9 |

% |

26.8 |

% |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Software |

|

5,277 |

|

5,166 |

|

2.1 |

% |

10,296 |

|

9,705 |

|

6.1 |

% |

||||

|

Gross margin |

|

87.1 |

% |

85.9 |

% |

|

|

85.9 |

% |

85.1 |

% |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Systems and Technology |

|

3,985 |

|

3,855 |

|

3.4 |

% |

7,370 |

|

7,083 |

|

4.1 |

% |

||||

|

Gross margin |

|

36.1 |

% |

37.1 |

% |

|

|

34.9 |

% |

35.7 |

% |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Global Financing |

|

544 |

|

568 |

|

-4.1 |

% |

1,081 |

|

1,146 |

|

-5.6 |

% |

||||

|

Gross margin |

|

50.1 |

% |

47.1 |

% |

|

|

49.9 |

% |

46.5 |

% |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Other |

|

200 |

|

215 |

|

-7.0 |

% |

400 |

|

429 |

|

-6.8 |

% |

||||

|

Gross margin |

|

17.7 |

% |

47.4 |

% |

|

|

-8.9 |

% |

50.1 |

% |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

TOTAL REVENUE |

|

23,724 |

|

23,250 |

|

2.0 |

% |

46,581 |

|

44,962 |

|

3.6 |

% |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

GROSS PROFIT |

|

10,809 |

|

10,581 |

|

2.2 |

% |

20,785 |

|

20,012 |

|

3.9 |

% |

||||

|

Gross margin |

|

45.6 |

% |

45.5 |

% |

|

|

44.6 |

% |

44.5 |

% |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

EXPENSE AND OTHER INCOME |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

S, G&A |

|

5,061 |

|

5,115 |

|

-1.1 |

% |

10,737 |

|

10,379 |

|

3.5 |

% |

||||

|

% of revenue |

|

21.3 |

% |

22.0 |

% |

|

|

23.1 |

% |

23.1 |

% |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

R, D&E |

|

1,475 |

|

1,434 |

|

2.9 |

% |

2,984 |

|

2,914 |

|

2.4 |

% |

||||

|

% of revenue |

|

6.2 |

% |

6.2 |

% |

|

|

6.4 |

% |

6.5 |

% |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Intellectual property and custom development income |

|

(297 |

) |

(302 |

) |

-1.8 |

% |

(558 |

) |

(570 |

) |

-2.1 |

% |

||||

|

Other (income) and expense |

|

(95 |

) |

(28 |

) |

nm |

|

(640 |

) |

(331 |

) |

93.2 |

% |

||||

|

Interest expense |

|

90 |

|

101 |

|

-11.1 |

% |

172 |

|

237 |

|

-27.5 |

% |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

TOTAL EXPENSE AND OTHER INCOME |

|

6,234 |

|

6,319 |

|

-1.4 |

% |

12,695 |

|

12,628 |

|

0.5 |

% |

||||

|

% of revenue |

|

26.3 |

% |

27.2 |

% |

|

|

27.3 |

% |

28.1 |

% |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

INCOME BEFORE INCOME TAXES |

|

4,575 |

|

4,262 |

|

7.3 |

% |

8,090 |

|

7,385 |

|

9.6 |

% |

||||

|

Pre-tax margin |

|

19.3 |

% |

18.3 |

% |

|

|

17.4 |

% |

16.4 |

% |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Provision for income taxes |

|

1,190 |

|

1,159 |

|

2.6 |

% |

2,103 |

|

1,986 |

|

5.9 |

% |

||||

|

Effective tax rate |

|

26.0 |

% |

27.2 |

% |

|

|

26.0 |

% |

26.9 |

% |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

NET INCOME |

|

$ |

3,386 |

|

$ |

3,103 |

|

9.1 |

% |

$ |

5,987 |

|

$ |

5,398 |

|

10.9 |

% |

|

Net margin |

|

14.3 |

% |

13.3 |

% |

|

|

12.9 |

% |

12.0 |

% |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

EARNINGS PER SHARE OF COMMON STOCK: |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

ASSUMING DILUTION |

|

$ |

2.61 |

|

$ |

2.32 |

|

12.5 |

% |

$ |

4.57 |

|

$ |

4.02 |

|

13.7 |

% |

|

BASIC |

|

$ |

2.65 |

|

$ |

2.34 |

|

13.2 |

% |

$ |

4.64 |

|

$ |

4.04 |

|

14.9 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

WEIGHTED-AVERAGE NUMBER OF COMMON SHARES OUTSTANDING (M’s): |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

ASSUMING DILUTION |

|

1,296.7 |

|

1,336.9 |

|

|

|

1,309.2 |

|

1,343.2 |

|

|

|

||||

|

BASIC |

|

1,278.6 |

|

1,326.1 |

|

|

|

1,289.9 |

|

1,335.2 |

|

|

|

||||

nm - not meaningful

INTERNATIONAL BUSINESS MACHINES CORPORATION

CONSOLIDATED STATEMENT OF FINANCIAL POSITION

(Unaudited)

|

|

|

At June 30, |

|

At December 31, |

|

||

|

(Dollars in Millions) |

|

2010 |

|

2009 |

|

||

|

ASSETS |

|

|

|

|

|

||

|

|

|

|

|

|

|

||

|

Current Assets: |

|

|

|

|

|

||

|

Cash and cash equivalents |

|

$ |

10,325 |

|

$ |

12,183 |

|

|

Marketable securities |

|

1,916 |

|

1,791 |

|

||

|

Notes and accounts receivable - trade |

|

|

|

|

|

||

|

(net of allowances of $291 in 2010 and $217 in 2009) |

|

9,051 |

|

10,736 |

|

||

|

Short-term financing receivables |

|

|

|

|

|

||

|

(net of allowances of $376 in 2010 and $438 in 2009) |

|

13,301 |

|

14,914 |

|

||

|

Other accounts receivable |

|

|

|

|

|

||

|

(net of allowances of $11 in 2010 and $15 in 2009) |

|

1,140 |

|

1,143 |

|

||

|

Inventories, at lower of average cost or market: |

|

|

|

|

|

||

|

Finished goods |

|

493 |

|

533 |

|

||

|

Work in process and raw materials |

|

2,102 |

|

1,960 |

|

||

|

|

|

|

|

|

|

||

|

Total inventories |

|

2,595 |

|

2,494 |

|

||

|

Deferred taxes |

|

1,444 |

|

1,730 |

|

||

|

Prepaid expenses and other current assets |

|

5,124 |

|

3,946 |

|

||

|

Total Current Assets |

|

44,895 |

|

48,935 |

|

||

|

|

|

|

|

|

|

||

|

Plant, rental machines, and other property |

|

38,292 |

|

39,596 |

|

||

|

Less: Accumulated depreciation |

|

24,758 |

|

25,431 |

|

||

|

|

|

|

|

|

|

||

|

Plant, rental machines, and other property - net |

|

13,534 |

|

14,165 |

|

||

|

Long-term financing receivables |

|

|

|

|

|

||

|

(net of allowances of $84 in 2010 and $97 in 2009) |

|

9,185 |

|

10,644 |

|

||

|

Prepaid pension assets |

|

3,575 |

|

3,001 |

|

||

|

Deferred taxes |

|

3,122 |

|

4,195 |

|

||

|

Goodwill |

|

20,544 |

|

20,190 |

|

||

|

Intangible assets - net |

|

2,526 |

|

2,513 |

|

||

|

Investments and sundry assets |

|

6,038 |

|

5,379 |

|

||

|

Total Assets |

|

$ |

103,420 |

|

$ |

109,022 |

|

|

|

|

|

|

|

|

||

|

LIABILITIES AND EQUITY |

|

|

|

|

|

||

|

|

|

|

|

|

|

||

|

Current Liabilities: |

|

|

|

|

|

||

|

Taxes |

|

$ |

2,895 |

|

$ |

3,826 |

|

|

Short-term debt |

|

5,633 |

|

4,168 |

|

||

|

Accounts payable |

|

7,233 |

|

7,436 |

|

||

|

Compensation and benefits |

|

4,022 |

|

4,505 |

|

||

|

Deferred income |

|

10,671 |

|

10,845 |

|

||

|

Other accrued expenses and liabilities |

|

4,539 |

|

5,223 |

|

||

|

Total Current Liabilities |

|

34,993 |

|

36,002 |

|

||

|

|

|

|

|

|

|

||

|

Long-term debt |

|

21,017 |

|

21,932 |

|

||

|

Retirement and nonpension postretirement benefit obligations |

|

14,598 |

|

15,953 |

|

||

|

Deferred income |

|

3,341 |

|

3,562 |

|

||

|

Other liabilities |

|

8,295 |

|

8,819 |

|

||

|

Total Liabilities |

|

82,244 |

|

86,267 |

|

||

|

|

|

|

|

|

|

||

|

Contingencies and Commitments |

|

|

|

|

|

||

|

|

|

|

|

|

|

||

|

Equity: |

|

|

|

|

|

||

|

IBM Stockholders’ Equity: |

|

|

|

|

|

||

|

Common stock |

|

43,522 |

|

41,810 |

|

||

|

Retained earnings |

|

85,323 |

|

80,900 |

|

||

|

Treasury stock — at cost |

|

(89,276 |

) |

(81,243 |

) |

||

|

Accumulated other comprehensive income/(loss) |

|

(18,510 |

) |

(18,830 |

) |

||

|

|

|

|

|

|

|

||

|

Total IBM stockholders’ equity |

|

21,059 |

|

22,637 |

|

||

|

|

|

|

|

|

|

||

|

Noncontrolling interests |

|

117 |

|

118 |

|

||

|

Total Equity |

|

21,176 |

|

22,755 |

|

||

|

Total Liabilities and Equity |

|

$ |

103,420 |

|

$ |

109,022 |

|

INTERNATIONAL BUSINESS MACHINES CORPORATION

CASH FLOW ANALYSIS

(Unaudited)

|

|

|

Three Months Ended |

|

Six Months Ended |

|

||||||||

|

|

|

June 30, |

|

June 30, |

|

||||||||

|

(Dollars in Millions) |

|

2010 |

|

2009 |

|

2010 |

|

2009 |

|

||||

|

Net Cash from Operations |

|

$ |

3,766 |

|

$ |

4,741 |

|

$ |

8,203 |

|

$ |

9,127 |

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Less: Global Financing (GF) Accounts Receivable |

|

(218 |

) |

430 |

|

1,883 |

|

3,014 |

|

||||

|

|

|

|

|

|

|

|

|

|

|

||||

|

Net Cash from Operations |

|

|

|

|

|

|

|

|

|

||||

|

(Excluding GF Accounts Receivable) |

|

3,985 |

|

4,311 |

|

6,320 |

|

6,113 |

|

||||

|

|

|

|

|

|

|

|

|

|

|

||||

|

Net Capital Expenditures |

|

(970 |

) |

(864 |

) |

(1,873 |

) |

(1,624 |

) |

||||

|

|

|

|

|

|

|

|

|

|

|

||||

|

Free Cash Flow |

|

|

|

|

|

|

|

|

|

||||

|

(Excluding GF Accounts Receivable) |

|

3,015 |

|

3,447 |

|

4,446 |

|

4,490 |

|

||||

|

|

|

|

|

|

|

|

|

|

|

||||

|

Acquisitions |

|

(185 |

) |

(79 |

) |

(1,009 |

) |

(100 |

) |

||||

|

Divestitures |

|

0 |

|

0 |

|

0 |

|

356 |

|

||||

|

Share Repurchase |

|

(4,104 |

) |

(1,670 |

) |

(8,121 |

) |

(3,436 |

) |

||||

|

Dividends |

|

(833 |

) |

(732 |

) |

(1,551 |

) |

(1,407 |

) |

||||

|

Non-GF Debt |

|

920 |

|

(266 |

) |

1,261 |

|

(2,181 |

) |

||||

|

Other (including GF Accounts Receivable, GF Debt) |

|

(548 |

) |

(469 |

) |

3,241 |

|

1,898 |

|

||||

|

|

|

|

|

|

|

|

|

|

|

||||

|

Change in Cash and Marketable Securities |

|

$ |

(1,736 |

) |

$ |

231 |

|

$ |

(1,732 |

) |

$ |

(381 |

) |

INTERNATIONAL BUSINESS MACHINES CORPORATION

SEGMENT DATA

(Unaudited)

|

|

|

SECOND-QUARTER 2010 |

|

||||||||||||

|

|

|

Revenue |

|

Pre-tax |

|

Pre-tax |

|

||||||||

|

(Dollars in Millions) |

|

External |

|

Internal |

|

Total |

|

Income |

|

Margin |

|

||||

|

SEGMENTS |

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Global Technology Services |

|

$ |

9,234 |

|

$ |

332 |

|

$ |

9,566 |

|

$ |

1,422 |

|

14.9 |

% |

|

Y-T-Y Change |

|

1.4 |

% |

-3.0 |

% |

1.2 |

% |

1.2 |

% |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Global Business Services |

|

4,483 |

|

197 |

|

4,680 |

|

683 |

|

14.6 |

% |

||||

|

Y-T-Y Change |

|

3.3 |

% |

-12.0 |

% |

2.6 |

% |

12.3 |

% |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Software |

|

5,277 |

|

690 |

|

5,967 |

|

1,988 |

|

33.3 |

% |

||||

|

Y-T-Y Change |

|

2.1 |

% |

12.4 |

% |

3.2 |

% |

7.4 |

% |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Systems and Technology |

|

3,985 |

|

202 |

|

4,187 |

|

221 |

|

5.3 |

% |

||||

|

Y-T-Y Change |

|

3.4 |

% |

-16.9 |

% |

2.2 |

% |

-33.8 |

% |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Global Financing |

|

544 |

|

431 |

|

975 |

|

463 |

|

47.4 |

% |

||||

|

Y-T-Y Change |

|

-4.1 |

% |

-3.5 |

% |

-3.9 |

% |

-0.5 |

% |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

TOTAL REPORTABLE SEGMENTS |

|

23,523 |

|

1,852 |

|

25,376 |

|

4,777 |

|

18.8 |

% |

||||

|

Y-T-Y Change |

|

2.1 |

% |

-0.9 |

% |

1.9 |

% |

2.4 |

% |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Eliminations / Other |

|

200 |

|

(1,852 |

) |

(1,652 |

) |

(202 |

) |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

TOTAL IBM CONSOLIDATED |

|

$ |

23,724 |

|

$ |

0 |

|

$ |

23,724 |

|

$ |

4,575 |

|

19.3 |

% |

|

Y-T-Y Change |

|

2.0 |

% |

|

|

2.0 |

% |

7.3 |

% |

|

|

||||

|

|

|

SECOND-QUARTER 2009 |

|

||||||||||||

|

|

|

Revenue |

|

Pre-tax |

|

Pre-tax |

|

||||||||

|

(Dollars in Millions) |

|

External |

|

Internal |

|

Total |

|

Income |

|

Margin |

|

||||

|

SEGMENTS |

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Global Technology Services |

|

$ |

9,108 |

|

$ |

343 |

|

$ |

9,451 |

|

$ |

1,405 |

|

14.9 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Global Business Services |

|

4,338 |

|

223 |

|

4,562 |

|

608 |

|

13.3 |

% |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Software |

|

5,166 |

|

614 |

|

5,780 |

|

1,852 |

|

32.0 |

% |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Systems and Technology |

|

3,855 |

|

244 |

|

4,098 |

|

333 |

|

8.1 |

% |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Global Financing |

|

568 |

|

447 |

|

1,014 |

|

465 |

|

45.8 |

% |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

TOTAL REPORTABLE SEGMENTS |

|

23,035 |

|

1,870 |

|

24,905 |

|

4,663 |

|

18.7 |

% |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Eliminations / Other |

|

215 |

|

(1,870 |

) |

(1,655 |

) |

(401 |

) |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

TOTAL IBM CONSOLIDATED |

|

$ |

23,250 |

|

$ |

0 |

|

$ |

23,250 |

|

$ |

4,262 |

|

18.3 |

% |

INTERNATIONAL BUSINESS MACHINES CORPORATION

SEGMENT DATA

(Unaudited)

|

|

|

SIX-MONTHS 2010 |

|

||||||||||||

|

|

|

Revenue |

|

Pre-tax |

|

Pre-tax |

|

||||||||

|

(Dollars in Millions) |

|

External |

|

Internal |

|

Total |

|

Income |

|

Margin |

|

||||

|

SEGMENTS |

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Global Technology Services |

|

$ |

18,540 |

|

$ |

652 |

|

$ |

19,192 |

|

$ |

2,387 |

|

12.4 |

% |

|

Y-T-Y Change |

|

3.8 |

% |

-4.7 |

% |

3.5 |

% |

-4.9 |

% |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Global Business Services |

|

8,893 |

|

400 |

|

9,293 |

|

1,128 |

|

12.1 |

% |

||||

|

Y-T-Y Change |

|

1.8 |

% |

-12.2 |

% |

1.1 |

% |

-0.1 |

% |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Software |

|

10,296 |

|

1,448 |

|

11,743 |

|

4,040 |

|

34.4 |

% |

||||

|

Y-T-Y Change |

|

6.1 |

% |

18.0 |

% |

7.4 |

% |

26.8 |

% |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Systems and Technology |

|

7,370 |

|

376 |

|

7,746 |

|

51 |

|

0.7 |

% |

||||

|

Y-T-Y Change |

|

4.1 |

% |

-10.5 |

% |

3.2 |

% |

-85.9 |

% |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Global Financing |

|

1,081 |

|

834 |

|

1,916 |

|

890 |

|

46.5 |

% |

||||

|

Y-T-Y Change |

|

-5.6 |

% |

-0.3 |

% |

-3.4 |

% |

7.9 |

% |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

TOTAL REPORTABLE SEGMENTS |

|

46,181 |

|

3,710 |

|

49,891 |

|

8,496 |

|

17.0 |

% |

||||

|

Y-T-Y Change |

|

3.7 |

% |

2.4 |

% |

3.6 |

% |

6.0 |

% |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Eliminations / Other |

|

400 |

|

(3,710 |

) |

(3,310 |

) |

(406 |

) |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

TOTAL IBM CONSOLIDATED |

|

$ |

46,581 |

|

$ |

0 |

|

$ |

46,581 |

|

$ |

8,090 |

|

17.4 |

% |

|

Y-T-Y Change |

|

3.6 |

% |

|

|

3.6 |

% |

9.6 |

% |

|

|

||||

|

|

|

SIX-MONTHS 2009 |

|

||||||||||||

|

|

|

Revenue |

|

Pre-tax |

|

Pre-tax |

|

||||||||

|

(Dollars in Millions) |

|

External |

|

Internal |

|

Total |

|

Income |

|

Margin |

|

||||

|

SEGMENTS |

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Global Technology Services |

|

$ |

17,862 |

|

$ |

685 |

|

$ |

18,547 |

|

$ |

2,509 |

|

13.5 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Global Business Services |

|

8,736 |

|

456 |

|

9,191 |

|

1,130 |

|

12.3 |

% |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Software |

|

9,705 |

|

1,227 |

|

10,933 |

|

3,186 |

|

29.1 |

% |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Systems and Technology |

|

7,083 |

|

420 |

|

7,503 |

|

361 |

|

4.8 |

% |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Global Financing |

|

1,146 |

|

836 |

|

1,982 |

|

825 |

|

41.6 |

% |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

TOTAL REPORTABLE SEGMENTS |

|

44,533 |

|

3,624 |

|

48,156 |

|

8,011 |

|

16.6 |

% |

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Eliminations / Other |

|

429 |

|

(3,624 |

) |

(3,195 |

) |

(627 |

) |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

TOTAL IBM CONSOLIDATED |

|

$ |

44,962 |

|

$ |

0 |

|

$ |

44,962 |

|

$ |

7,385 |

|

16.4 |

% |

|

Contact: |

IBM |

|

|

Mike Fay, 914/499-6107 |

|

|

mikefay@us.ibm.com |

|

|

|

|

|

John Bukovinsky, 732/618-3531 |

|

|

jbuko@us.ibm.com |

ATTACHMENT II

|

|

2Q 2010 Earnings Presentation July 19, 2010 |

|

|

Forward Looking Statements Certain comments made in this presentation may be characterized as forward looking under the Private Securities Litigation Reform Act of 1995. Forward-looking statements are based on the company's current assumptions regarding future business and financial performance. Those statements by their nature address matters that are uncertain to different degrees. Those statements involve a number of factors that could cause actual results to differ materially. Additional information concerning these factors is contained in the Company's filings with the SEC. Copies are available from the SEC, from the IBM web site, or from IBM Investor Relations. Any forward-looking statement made during this presentation speaks only as of the date on which it is made. The company assumes no obligation to update or revise any forward-looking statements. These charts and the associated remarks and comments are integrally related, and are intended to be presented and understood together. |

|

|

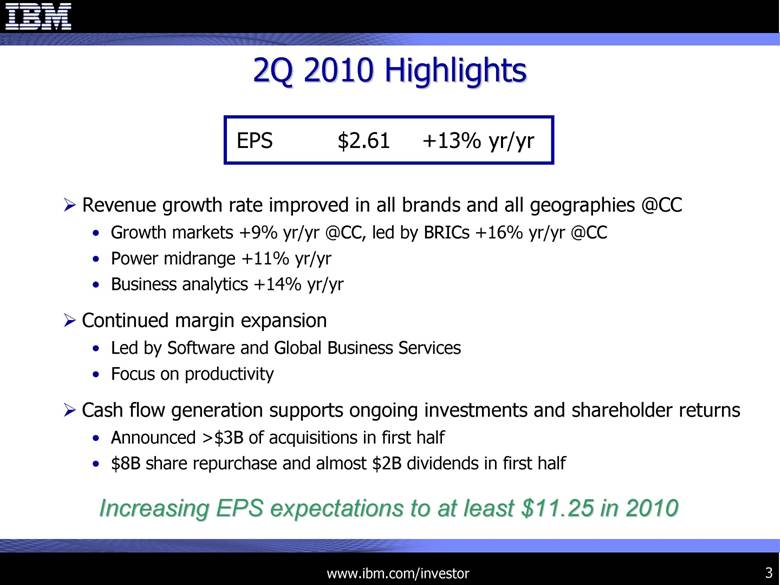

2Q 2010 Highlights Increasing EPS expectations to at least $11.25 in 2010 Revenue growth rate improved in all brands and all geographies @CC Growth markets +9% yr/yr @CC, led by BRICs +16% yr/yr @CC Power7 +11% yr/yr Business analytics +14% yr/yr Continued margin expansion Led by Software and Global Business Services Focus on productivity Cash flow generation supports ongoing investments and shareholder returns Announced >$3B of acquisitions in first half $8B share repurchase and almost $2B dividends in first half +13% yr/yr $2.61 EPS |

|

|

Financial Summary 1.0 pts 19.3% PTI Margin 13% $2.61 EPS 3% 1,296.7 Shares (Diluted) (M) 9% $3.4 Net Income 1.2 pts 26.0% Tax Rate 7% $4.6 Pre-Tax Income 1% $6.2 Expense 0.1 pts 45.6% GP % 2% @CC 2% $23.7 Revenue B/(W) Yr/Yr 2Q10 $ in Billions, except EPS Improving revenue growth and margin expansion drive profit performance |

|

|

Revenue by Geography +3 pts +1 pts +1 pts +2 pts +8 pts +2 pts +1 pts +2 pts (1%) (1%) Major Markets 9% 14% Growth Markets 16% 22% BRIC Countries (1%) (6%) 7.4 Europe/ME/A 26% 26% 0.7 OEM 2% 2% $23.7 IBM 2Q10 3% 9% 5.4 Asia Pacific 2% 3% $10.2 Americas Rptd @CC $ in Billions APac +7% @CC OEM +26% U.S. +1% EMEA Canada/ LA Japan -1% @CC Growth markets now as large as Euro-based business B/(W) Yr/Yr 2Q10 Yr/Yr vs. 1Q10 Yr/Yr @CC |

|

|

Revenue by Segment @CC +2 pts +7 pts +2 pts +1 pts* +8 pts +<1 pts 6%* 6%* 5.3 Software 2Q10 2% 2% $23.7 Total IBM (5%) (4%) 0.5 Global Financing 4% 3% 4.0 Systems & Technology 3% 3% 4.5 Global Business Services Flat 1% $9.2 Global Technology Services Rptd $ in Billions Broad-based improvement in revenue growth rate * Revenue growth excluding PLM Global Technology Services Global Business Services Systems & Technology Software Global Financing B/(W) Yr/Yr 2Q10 Yr/Yr vs. 1Q10 Yr/Yr @CC |

|

|

Expense Summary 5 pts (1 pts) 4 pts Ops (2 pts) (2 pts) 1% $6.2 Total Expense & Other Income 11% 0.1 Interest Expense nm (0.1) Other (Income)/Expense (2%) (0.3) IP and Development Income (1 pts) (1 pts) (3%) 1.5 RD&E (2 pts) (1 pts) 1% $5.1 SG&A Acq.* Currency B/(W) Yr/Yr 2Q10 * Includes acquisitions made in the last twelve months $ in Billions B/(W) Yr/Yr Drivers 8th consecutive quarter of operational expense improvement |

|

|

(2.9 pts) 5.3% (1.0 pts) 36.1% Systems & Technology 1.3 pts 33.3% 1.2 pts 87.1% Software 1.0 pts 1.6 pts 1.3 pts Flat B/(W) Yr/Yr Pts 19.3% 47.4% 14.6% 14.9% 2Q10 2Q10 0.1 pts 45.6% Total IBM 3.0 pts 50.1% Global Financing 1.3 pts 28.5% Global Business Services (0.2 pts) 34.6% Global Technology Services B/(W) Yr/Yr Pts Margins by Segment External Gross Profit Margins Total Pre-Tax Margins Margin expansion led by Global Business Services and Software |

|

|

Flat 14.9% PTI Margin @CC Rptd 2Q10 (0.2 pts) 34.6% Gross Margin (External) Flat 1% $9.2 Revenue (External) B/(W) Yr/Yr Services Segments GTS Outsourcing 39% Global Business Services 33% Integrated Technology Services 15% Maint. 13% $ in Billions Global Technology Services (GTS) Global Business Services (GBS) Return to revenue growth with positive trends 2Q10 Revenues (% of Total Services) (Growth @CC) Flat Yr/Yr 3% Yr/Yr 3% Yr/Yr (2%) Yr/Yr @CC Rptd 2Q10 (12%) (12%) $12.3 Total Signings (3%) (3%) 5.8 Transactional - ITS, Consulting, AMS SI (19%) (19%) $6.5 Outsourcing - GTS O/S, Appl. O/S (AMS) B/(W) Yr/Yr Global Services Signings $ in Billions 1.3 pts 14.6% PTI Margin @CC Rptd 2Q10 1.3 pts 28.5% Gross Margin (External) 3% 3% $4.5 Revenue (External) B/(W) Yr/Yr $ in Billions |

|

|

Software Segment 2% 2% $5.3 Revenue (External) incl. PLM @CC Rptd 2Q10 1.3 pts 33.3% PTI Margin 1.2 pts 87.1% Gross Margin (External) 6% 6% $5.3 Revenue (External) excl. PLM B/(W) Yr/Yr @CC Rptd 6% 6% 10% 2% (6%) 19% 7% 16% 6% Total Software excl. PLM 6% Total Middleware 9% Key Branded Middleware 1% Rational (6%) Lotus Yr/Yr 2Q10 Revenue 18% Tivoli 7% Information Management 17% WebSphere Family 2Q10 Revenue (% of Total Software) Key Branded Middleware 62% Operating Systems 10% Other Middleware 21% Other 7% $ in Billions Continued share gains in Branded Middleware |

|

|

Systems & Technology Segment @CC Rptd 2Q10 (2.9 pts) 5.3% PTI Margin (1.0 pts) 36.1% Gross Margin (External) 4% 3% $4.0 Revenue (External) B/(W) Yr/Yr $ in Billions 2Q10 Revenue (% of Total Sys & Tech) Servers 62% Storage 20% Micro OEM 13% RSS 12% 11% Midrange 14% 12% Disk Yr/Yr 2Q10 Revenue 4% 23% 2% 33% 6% 30% (10%) (22%) @CC (10%) Power Systems 1% Total Systems 3% Total Systems & Technology 23% Microelectronics OEM 31% Retail Store Solutions 5% Storage 30% System x Rptd (24%) System z New System z and Power7 high-end in 3Q |

|

|

12 Cash Flow Analysis 2Q10 B/(W) Yr/Yr YTD 1H10 B/(W) Yr/Yr Net Cash from Operations $3.8 ($1.0) $8.2 ($0.9) Less: Global Financing Receivables (0.2) (0.6) 1.9 (1.1) Net Cash from Operations (excluding GF Receivables) 4.0 (0.3) 6.3 0.2 Net Capital Expenditures (1.0) (0.1) (1.9) (0.2) Free Cash Flow (excluding GF Receivables) 3.0 (0.4) 4.4 0.0 Acquisitions (0.2) (0.1) (1.0) (0.9) Divestitures 0.0 0.0 0.0 (0.4) Dividends (0.8) (0.1) (1.6) (0.1) Share Repurchases (4.1) (2.4) (8.1) (4.7) Non-GF Debt 0.9 1.2 1.3 3.4 Other (includes GF A/R & GF Debt) (0.5) (0.1) 3.2 1.3 Change in Cash & Marketable Securities ($1.7) ($2.0) ($1.7) ($1.4) $ in Billions |

|

|

7.1 23% 21.2 82.2 26.7 21.2 5.5 55.6 103.4 29.5 61.6 $12.2 June 10 7.1 16% 22.8 86.3 26.1 22.4 3.7 60.2 109.0 33.3 61.7 $14.0 Dec. 09 15.5 Equity 88.2 Total Liabilities 29.4 Total Debt 22.8 Global Financing Debt 6.6 Non-GF Debt* 6.9 Global Financing Leverage 35% 58.8 103.7 30.9 60.2 $12.5 June 09 Non-GF Debt / Capital Other Liabilities Total Assets Global Financing Assets Non-GF Assets* Cash & Marketable Securities Balance Sheet Summary $ in Billions * Includes eliminations of inter-company activity |

|

|

2Q09 EPS Revenue Growth @ Actual Operating Leverage Share Repurchases 2Q10 EPS $0.05 $0.16 $0.08 EPS Bridge – 2Q09 to 2Q10 $0.11 $0.04 $0.01 Tax Rate Expense Productivity Gross Margin $2.32 $2.61 |

|

|

2Q 2010 Summary Double-digit earnings growth off strong base Steady improvement in the business Investing for growth Superior shareholder returns Note: 2006-2008 EPS reflects the adoption of amendments to ASC 260, “Earnings Per Share” 2006 2007 2008 2009 2010 At Least $11.25 $6.05 $7.15 $8.89 $10.01 Dow indexed to IBM 2006 EPS, excludes Financials and GM for all periods. Data Source: Bloomberg Increasing EPS expectations to at least $11.25 in 2010 2Q EPS |

|

|

[LOGO] |

|

|

Supplemental Materials Currency – Year/Year Comparison Supplemental Segment Information – Global Services Services Transactional Signings Trends Supplemental Segment Information – Systems & Technology, Software Global Financing Portfolio Revenue by Key Industry Sales Unit Cash Flow (FAS 95) Supplemental Information – Operating Earnings Non-GAAP Supplementary Materials Constant Currency, Cash Flow Debt-to-Capital Ratio, PLM Sale Reconciliation of Total Revenue Growth Rates Reconciliation of Revenue Growth Rates - Segments, Geographies Reconciliation of Geography Revenue Growth Reconciliation of Services Segment Revenue Growth Rates Reconciliation of Debt-to-Capital Ratio Some columns and rows in these materials, including the supplemental exhibits, may not add due to rounding |

|

|

18 Currency – Year/Year Comparison 1Q10 Yr/Yr 2Q10 Yr/Yr 7/16 Spot 3Q10 4Q10 FY10 Euro 0.72 6% 0.79 (7%) 0.77 (11%) (14%) (6%) Pound 0.64 8% 0.67 (4%) 0.65 (7%) (6%) (2%) Yen 91 3% 92 5% 87 7% 3% 5% Revenue Impact - Pts 5 pts 0 pts ~(1 pts) (3-4 pts) ~0 pts @ 7/2/10 Rates - $B $1.2 $0.1 Vs. 4/19 View - Pts B/(W) (2 pts) (1 pts) (1 pts) (1 pts) - $B B/(W) ($0.5) ($0-0.5) ($0-0.5) ~($1.0) Vs. 1/19 View - Pts B/(W) (1-2 pts) (4 pts) (2-3 pts) (3 pts) (3 pts) - $B B/(W) ($0.3) ($0.9) ~($0.5) ($0.5-1.0) ~($3.0) Yr/Yr @ 7/16 Spot Quarterly Averages per US $ |

|

|

Supplemental Segment Information – 2Q 2010 @CC Yr/Yr Global Services 3% 3% Global Business Services Flat 1% Global Technology Services 3% 5% Maintenance Revenue Growth (2%) (2%) Integrated Tech Services Flat 2% GTS Outsourcing $129B Backlog Backlog 2Q10 Global Services ($3B) Year-to-Year ($4B) Quarter-to-Quarter Change in Backlog due to Currency |

|

|

Services Transactional Signings Trends Services Transactional Signings Yr/Yr Growth @CC -7% -5% -12% -10% -5% -1% -4% -8% -18% -3% -7% -4% -5% -7% -15% -6% -6% -3% -20% -15% -10% -5% 0% 1Q09 2Q09 3Q09 4Q09 1Q10 2Q10 GTS Transactional GBS Transactional Services Transactional |

|

|

Supplemental Segment Information – 2Q 2010 Share GP% @CC Yr/Yr Systems & Technology 4% 23% 2% 33% 6% 30% (10%) (22%) = = 3% Total Systems & Technology 23% Microelectronics OEM 1% Total Systems 31% Retail Store Solutions 5% Storage 30% System x Revenue Growth (10%) Power Systems (24%) System z * 2% 2% Total Software incl. PLM Revenue Growth 6% 6% Total Software excl. PLM (28%) (28%) Other Software/Services 2% 2% Operating Systems 6% 6% Total Middleware (4%) (3%) Other Middleware 10% 9% Key Branded Middleware 2% 1% Rational (6%) (6%) Lotus @CC Yr/Yr Software 19% 18% Tivoli 7% 7% Information Management 16% 17% WebSphere Family * MIPS down 14% yr/yr |

|

|

2Q10 1Q10 2Q09 Identified Loss Rate 1.8% 1.9% 1.7% Anticipated Loss Rate 0.3% 0.4% 0.6% Reserve Coverage 2.1% 2.3% 2.3% Client Days Delinquent Outstanding 3.7 3.3 3.4 Commercial A/R > 30 Days $27M $49M $48M Global Financing Portfolio 2Q10 – $21.9B Net External Receivables 24% 40% 17% 11% 5% 3% 0% 5% 10% 15% 20% 25% 30% 35% 40% 45% Aaa-A3 Baa1-Baa3 Ba1-Ba2 Ba3-B1 B2-B3 Caa-D Investment Grade 64% Non-Investment Grade 36% |

|

|

2% 2% $23.7 Total IBM 5% 5% 4.7 General Business 2Q10 1% 2% $23.1 All Sectors (2%) (1%) 2.3 Communications 5% 5% 2.4 Distribution (3%) (3%) 2.4 Industrial (2%) (2%) 3.9 Public 3% 4% $6.7 Financial Services B/(W) Yr/Yr Rptd @CC Revenue by Key Industry Sales Unit $ in Billions General Business Comms Distribution Industrial Public Financial Services |

|

|

Cash Flow (FAS 95) ($1.9) (0.3) (7.1) 1.8 (8.1) (1.6) 0.7 (2.6) 0.2 (1.0) 0.0 (1.9) 8.2 1.9 (2.4) 0.3 2.4 $6.0 YTD 1H10 ($1.1) 0.0 (8.3) 0.5 (3.4) (1.4) (4.0) (1.9) (0.5) (0.1) 0.4 (1.6) 9.1 3.0 (2.0) 0.3 2.5 $5.4 YTD 1H09 ($0.6) 0.2 (3.7) 0.3 (1.7) (0.7) (1.6) (1.8) (0.9) (0.1) 0.0 (0.9) 4.7 0.4 (0.2) 0.1 1.2 $3.1 QTD 2Q09 ($2.1) (0.2) (3.7) 0.9 (4.1) (0.8) 0.2 (1.9) (0.8) (0.2) 0.0 (1.0) 3.8 (0.2) (0.7) 0.2 1.2 $3.4 QTD 2Q10 Net Change in Cash & Cash Equivalents Working Capital / Other Effect of Exchange Rate changes on Cash Net Cash used in Financing Activities Common Stock Transactions - Other Common Stock Repurchases Dividends Debt, net of payments & proceeds Net Cash used in Investing Activities Marketable Securities / Other Investments, net Acquisitions, net of cash acquired Divestitures, net of cash transferred Capital Expenditures, net of payments & proceeds Net Cash provided by Operating Activities Global Financing A/R Stock-based Compensation Depreciation / Amortization of Intangibles Net Income from Operations $ in Billions |

|

|

Supplemental Information – Operating Earnings The company is including a view of the impact of certain acquisition- related charges and certain retirement-related elements on IBM's earnings results (Operating Earnings). The company believes that providing investors with a view of operating earnings will provide better transparency into the operational results of the business; improve visibility to management decisions and their impacts on operational performance; enable better comparison to peer companies; and, allow the company to provide a long-term strategic view of the business going forward. |

|

|

Supplemental Information – Operating Earnings - 2010 $2.62 $2.00 EPS $3,402 $2,638 Net Income $4,584 $3,556 Pre-Tax Income Operating (Non-GAAP) $0.01 $0.03 EPS $17 $37 Net Income 7 ($4) Tax Impact*** 122 116 Acquisition-Related Charges** (113) (76) Non-Operating Pension* $9 $41 Pre-Tax Income Total Adjustments $2.61 $1.97 EPS $3,386 $2,601 Net Income $4,575 $3,515 Pre-Tax Income As Reported 2Q10 1Q10 $ in Millions, except EPS * Includes Retirement Related Interest Cost, Expected ROA, Recognized actuarial losses or gains, amortization of transition assets, other settlements, curtailments, multi-employer plans and insolvency insurance ** Includes Amortization of Purchased Intangibles, In Process R&D, Severance Cost for Acquired employees, vacant space for acquired companies, deal costs *** The tax impact on the Operating (Non-GAAP) Pre Tax Income will be calculated under the same accounting principles applied to the As Reported Pre Tax Income under ACS 740, which employs an annual effective tax rate concept to the results. |

|

|

Supplemental Information – Operating Earnings - 2009 $10.03 $3.59 $2.41 $2.31 $1.72 EPS $13,452 $4,810 $3,224 $3,094 $2,324 Net Income $18,126 $6,359 $4,375 $4,239 $3,153 Pre-Tax Income Operating (Non-GAAP) $0.02 $0.00 $0.01 ($0.01) $0.02 EPS $27 ($3) $10 ($9) $29 Net Income $39 $19 $8 $14 ($2) Tax Impact*** 498 127 124 122 125 Acquisition-Related Charges** (509) (149) (121) (145) (94) Non-Operating Pension* ($12) ($22) $3 ($23) $31 Pre-Tax Income Total Adjustments $10.01 $3.59 $2.40 $2.32 $1.70 EPS $13,425 $4,813 $3,214 $3,103 $2,295 Net Income $18,138 $6,381 $4,373 $4,262 $3,122 Pre-Tax Income As Reported FY09 4Q09 3Q09 2Q09 1Q09 $ in Millions, except EPS * Includes Retirement Related Interest Cost, Expected ROA, Recognized actuarial losses or gains, amortization of transition assets, other settlements, curtailments, multi-employer plans and insolvency insurance ** Includes Amortization of Purchased Intangibles, In Process R&D, Severance Cost for Acquired employees, vacant space for acquired companies, deal costs *** The tax impact on the Operating (Non-GAAP) Pre Tax Income will be calculated under the same accounting principles applied to the As Reported Pre Tax Income under ACS 740, which employs an annual effective tax rate concept to the results. |

|

|

Supplemental Information – Operating Earnings - 2008 $8.86 $3.20 $2.04 $2.01 $1.65 EPS $12,293 $4,330 $2,821 $2,817 $2,325 Net Income $16,569 $5,642 $3,897 $3,839 $3,191 Pre-Tax Income Operating (Non-GAAP) ($0.03) ($0.07) $0.00 $0.04 $0.00 EPS ($41) ($97) ($3) $52 $7 Net Income $105 $70 ($5) $27 $13 Tax Impact*** 544 130 134 165 115 Acquisition-Related Charges** (691) (297) (132) (140) (121) Non-Operating Pension* ($147) ($167) $2 $24 ($6) Pre-Tax Income Total Adjustments $8.89 $3.27 $2.04 $1.97 $1.64 EPS $12,334 $4,427 $2,824 $2,765 $2,319 Net Income $16,715 $5,808 $3,895 $3,814 $3,198 Pre-Tax Income As Reported FY08 4Q08 3Q08 2Q08 1Q08 $ in Millions, except EPS * Includes Retirement Related Interest Cost, Expected ROA, Recognized actuarial losses or gains, amortization of transition assets, other settlements, curtailments, multi-employer plans and insolvency insurance ** Includes Amortization of Purchased Intangibles, In Process R&D, Severance Cost for Acquired employees, vacant space for acquired companies, deal costs *** The tax impact on the Operating (Non-GAAP) Pre Tax Income will be calculated under the same accounting principles applied to the As Reported Pre Tax Income under ACS 740, which employs an annual effective tax rate concept to the results. |

|

|

Non-GAAP Supplementary Materials In an effort to provide investors with additional information regarding the company's results as determined by generally accepted accounting principles (GAAP), the company also discusses, in its earnings press release and/or earnings presentation materials, the following Non-GAAP information which management believes provides useful information to investors. Constant Currency Management refers to growth rates at constant currency or adjusting for currency so that the business results can be viewed without the impact of fluctuations in foreign currency exchange rates, thereby facilitating period-to-period comparisons of the company's business performance. Constant currency revenue results are calculated by translating current period revenue in local currency using the prior year's currency conversion rate. This consistent approach is based on the pricing currency for each country which is typically the functional currency. Generally, when the dollar either strengthens or weakens against other currencies, the growth at constant currency rates or adjusting for currency will be higher or lower than growth reported at actual exchange rates. Cash Flow Management includes presentations of both cash flow from operations and free cash flow that exclude the effect of Global Financing Receivables. For a financing business, increasing receivables is the basis for growth. Receivables are viewed as an investment and an income-producing asset. Therefore, management presents financing receivables as an investing activity. Management’s view is that this presentation gives the investor the best perspective of cash available for new investment or for distribution to shareholders. |

|

|

Non-GAAP Supplementary Materials Debt-to-Capital Ratio Management presents its debt-to-capital ratio excluding the Global Financing business. A financing business is managed on a leveraged basis. The company funds its Global Financing segment using a debt-to-equity ratio target of approximately 7 to 1. Given this significant leverage, the company presents a debt-to-capital ratio which excludes the Global Financing segment debt and equity because the company believes this is more representative of the company’s core business operations. PLM Sale Management presents certain financial results excluding the effects of the PLM sale. In March 2010, the company completed the sale of its activities associated with the sales and support of Dassault Systemes’ (Dassault) product lifecycle management (PLM) software, including customer contracts and related assets to Dassault. Given this sale, management believes that presenting financial information regarding revenue and software segment revenue without this item is more representative of operational performance and provides additional insight into, and clarifies the basis for, historical and/or future performance, which may be more useful for investors. |

|

|

Non-GAAP Supplementary Materials Reconciliation of Revenue Growth Rates @CC As Rptd 7 pts 1 pts Total Revenue 2Q10 Yr/Yr vs. 4Q09 Yr/Yr The above serves to reconcile the Non-GAAP financial information contained in the “2Q 2010 Financial Highlights” discussion regarding revenue growth in the company’s earnings presentation. See Slide 29 of this presentation for additional information on the use of these Non-GAAP financial measures. |

|

|

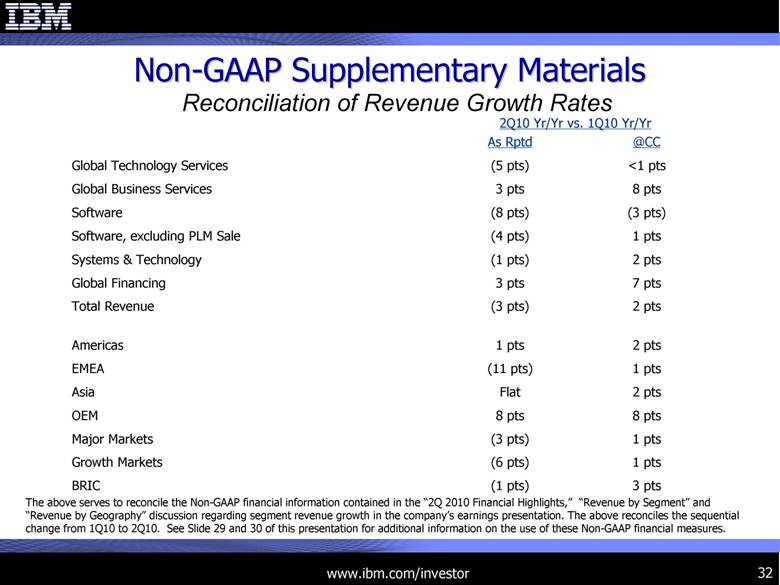

Non-GAAP Supplementary Materials Reconciliation of Revenue Growth Rates 2 pts (1 pts) Systems & Technology 7 pts 3 pts Global Financing 2 pts (3 pts) Total Revenue 2 pts 1 pts Americas 1 pts (11 pts) EMEA 2 pts Flat Asia 8 pts 8 pts OEM 1 pts (3 pts) Major Markets 1 pts (6 pts) Growth Markets 3 pts (1 pts) BRIC 1 pts (4 pts) Software, excluding PLM Sale (3 pts) (8 pts) Software 8 pts 3 pts Global Business Services <1 pts (5 pts) Global Technology Services @CC As Rptd 2Q10 Yr/Yr vs. 1Q10 Yr/Yr The above serves to reconcile the Non-GAAP financial information contained in the “2Q 2010 Financial Highlights,” “Revenue by Segment” and “Revenue by Geography” discussion regarding segment revenue growth in the company’s earnings presentation. The above reconciles the sequential change from 1Q10 to 2Q10. See Slide 29 of this presentation for additional information on the use of these Non-GAAP financial measures. |

|

|

Non-GAAP Supplementary Materials Reconciliation of Geography Revenue Growth @CC As Rptd 7% (1%) 11% 14% 5% 6% Asia Pacific, other than Japan Japan UK 2Q10 Yr/Yr The above serves to reconcile the Non-GAAP financial information contained in the “Revenue by Geography” discussion regarding revenue growth in certain geographies/countries in the company’s earnings presentation. See Slide 29 of this presentation for additional information on the use of these Non-GAAP financial measures. |

|

|

Non-GAAP Supplementary Materials Reconciliation of Services Segment Revenue Growth The above serves to reconcile the Non-GAAP financial information contained in the “Services Segment” discussion regarding revenue growth in certain segments in the company’s earnings presentation. See Slide 29 of this presentation for additional information on the use of these Non-GAAP financial measures. 8% 8% 8% 19% 13% 10% Growth Markets – GTS Outsourcing Growth Markets - ITS North America – Consulting & AMS @CC As Rptd 2Q10 Yr/Yr |

|

|

Reconciliation of Debt-to-Capital Ratio 35% 65% 2Q09 16% 53% FY09 2Q10 23% 56% Non-Global Financing Debt / Capital IBM Consolidated Debt / Capital The above serves to reconcile the Non-GAAP financial information contained in the “Balance Sheet Summary” discussion regarding the non-Global Financing debt to capital ratio in the company’s earnings presentation. See Slide 30 of this presentation for additional information on the use of these Non-GAAP financial measures. Non-GAAP Supplementary Materials |

|

|

[LOGO] |