Attached files

Table of Contents

As filed with the Securities and Exchange Commission on July 14, 2010

Registration No. 333-167041

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

Amendment No. 1

to

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

SHG Services, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 8051 | 13-4230695 | ||

| (State of Incorporation) | (Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

18831 Von Karman, Suite 400

Irvine, CA 92612

(949) 255-7100

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

William A. Mathies

President and Chief Operating Officer

SHG Services, Inc.

18831 Von Karman, Suite 400

Irvine, CA 92612

(949) 255-7100

(Name, address, including zip code, and telephone number, including area code, of agent for service)

With copies to:

| Andor D. Terner, Esq. Robert T. Plesnarski, Esq. O’Melveny & Myers LLP 610 Newport Center Drive, 17th Floor Newport Beach, CA 92660 (949) 823-6900 |

Jeffrey Bagner, Esq. Steven Epstein, Esq. Fried, Frank, Harris, Shriver & Jacobson LLP One New York Plaza New York, NY 10004 (212) 859-8000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this registration statement is declared effective and all conditions to the proposed transaction have been satisfied or waived.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ¨ | Accelerated filer ¨ | |

| Non-accelerated filer x (Do not check if smaller reporting company) |

Smaller reporting company ¨ | |

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until this registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

EXPLANATORY NOTE

SHG Services, Inc. (“New Sun”), a wholly owned subsidiary of Sun Healthcare Group, Inc. (“Sun”), has filed this registration statement on Form S-1 to register the issuance of shares of its common stock, $0.01 par value per share, which will be distributed on a pro rata basis to Sun stockholders (the “Separation”) together with a cash distribution of approximately $ per share. The actual amount of the cash distribution will not be determined until the time of the Separation. Immediately following the Separation, Sun intends to merge with and into Sabra Health Care REIT, Inc., a wholly owned subsidiary of Sun (“Sabra”), with Sabra surviving the merger and Sun stockholders receiving shares of Sabra common stock in exchange for their shares of Sun common stock (the “REIT Conversion Merger”). Concurrently with the filing of this registration statement on Form S-1, Sabra has filed a registration statement on Form S-4 (Reg. No. 333-167040) to register the issuance of shares of its common stock, par value $0.01 per share, in exchange for shares of Sun common stock in connection with the REIT Conversion Merger. This registration statement also includes a proxy statement relating to a special meeting of Sun stockholders to consider and vote on the Separation and the adoption of the agreement and plan of merger to implement the REIT Conversion Merger.

Table of Contents

The information in the proxy statement/prospectus is not complete and may be changed. Neither New Sun nor Sabra may sell the securities offered by the proxy statement/prospectus until their respective registration statements are effective with the Securities and Exchange Commission. The proxy statement/prospectus is not an offer to sell these securities and neither New Sun nor Sabra is soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED JULY 14, 2010

[SUN HEALTHCARE GROUP, INC. LETTERHEAD]

, 2010

Dear Stockholder:

You are cordially invited to attend a special meeting of stockholders of Sun Healthcare Group, Inc. (“Sun”) to be held on , 2010 at at a.m., local time, and at any adjournment or postponement thereof.

Sun intends to restructure its business by separating its real estate assets and its operating assets into the following two separate publicly traded companies (SHG Services, Inc. and Sabra Health Care REIT, Inc.), subject to the approval of its stockholders and other conditions:

| • | SHG Services, Inc., a Delaware corporation and a wholly owned subsidiary of Sun (“New Sun”), will own and continue to operate all of Sun’s operating subsidiaries. New Sun will be renamed “Sun Healthcare Group, Inc.” and the shares of New Sun common stock are expected to trade on the NASDAQ Global Select Market under the symbol “SUNH.” Sun will distribute to its stockholders on a pro rata basis all of the outstanding shares of New Sun common stock. This distribution is referred to in the proxy statement/prospectus as the “Separation.” |

| • | Sabra Health Care REIT, Inc., a Maryland corporation and a wholly owned subsidiary of Sun (“Sabra”), will own substantially all of Sun’s currently owned real property assets and will lease those assets to New Sun’s subsidiaries. Sabra expects to grow its portfolio through acquisitions as a broad-based healthcare REIT. Immediately following the Separation, Sun will be merged with and into Sabra with Sabra surviving the merger. This merger is referred to in the proxy statement/prospectus as the “REIT Conversion Merger.” The shares of Sabra common stock are expected to trade on the NASDAQ Global Select Market under the symbol “SBRA.” Sabra currently intends to qualify and elect to be treated as a real estate investment trust for U.S. federal income tax purposes commencing with its taxable year beginning on January 1, 2011. This election, together with the REIT Conversion Merger, is collectively referred to in the proxy statement/prospectus as the “REIT Conversion.” |

In connection with the Separation, Sun also intends to make a cash distribution to holders of Sun common stock of approximately $ per share, although the actual amount of this cash distribution will not be determined until the time of the Separation. The issuance of shares of New Sun common stock and the cash distribution by Sun in connection with the Separation should be treated as a taxable distribution to taxable U.S. stockholders for U.S. federal income tax purposes.

The board of directors of Sun has unanimously approved the Separation and REIT Conversion Merger, and recommends that stockholders vote “FOR” the Separation and “FOR” the REIT Conversion Merger as further described in the proxy statement/prospectus.

Your vote is very important. Whether or not you plan to attend the special meeting in person, it is important that your shares be represented and voted at the special meeting. You may submit your proxy or voting instructions by completing, signing, dating and returning the proxy or voting instruction card enclosed with the proxy materials you received or by submitting your proxy or voting instructions over the Internet or by telephone. We urge you to promptly submit your proxy or voting instructions in order to ensure your representation and the presence of a quorum at the special meeting. Please note that if you do not submit a proxy or voting instruction form or do not vote in person at the special meeting, the effect will be the same as a vote against the adoption of the agreement and plan of merger to implement the REIT Conversion Merger. In addition, if you “ABSTAIN” from voting on the Separation or on the adoption of the agreement and plan of merger to implement the REIT Conversion Merger, the effect will be the same as a vote against each of these proposals.

The proxy statement/prospectus provides you with important information about the Separation and REIT Conversion. Please give this information your careful attention. In particular, you should read and consider carefully the discussion in the section entitled “Risk Factors ” beginning on page 27 of the proxy statement/prospectus.

Sincerely,

Richard K. Matros

Chairman and Chief Executive Officer

Neither the Securities and Exchange Commission nor any state securities regulator has approved or disapproved the issuance of the shares of common stock of New Sun and Sabra as described in the proxy statement/prospectus or passed upon the adequacy or accuracy of this proxy statement/prospectus. Any representation to the contrary is a criminal offense.

The proxy statement/prospectus is dated , 2010, and is first being mailed to stockholders of Sun on or about , 2010.

Table of Contents

SUN HEALTHCARE GROUP, INC.

18831 Von Karman, Suite 400

Irvine, California 92612

NOTICE OF SPECIAL MEETING OF STOCKHOLDERS

TO BE HELD ON , 2010

To the Stockholders of Sun Healthcare Group, Inc.:

The special meeting of stockholders of Sun Healthcare Group, Inc., a Delaware corporation (“Sun”), will be held on , 2010 at at a.m., local time, and at any adjournment or postponement thereof, to consider and vote on the following matters described in the proxy statement/prospectus:

| 1. | To consider and vote upon a proposal to distribute to Sun stockholders on a pro rata basis all of the outstanding shares of common stock of SHG Services, Inc., a Delaware corporation and a wholly owned subsidiary of Sun (the “Separation”). |

| 2. | To consider and vote upon a proposal to adopt the agreement and plan of merger between Sun and Sabra Health Care REIT, Inc., a Maryland corporation and a wholly owned subsidiary of Sun (“Sabra”), which contemplates that, immediately following the Separation, Sun will be merged with and into Sabra with Sabra surviving the merger and Sun stockholders receiving shares of Sabra in exchange for their shares of Sun common stock (the “REIT Conversion Merger”). |

| 3. | To consider and vote upon a proposal to adjourn the special meeting to a later date, if necessary, to solicit additional proxies if there are insufficient votes at the time of the special meeting to approve the Separation or adopt the agreement and plan of merger to implement the REIT Conversion Merger. |

| 4. | To transact such other business as may properly come before the special meeting, and any adjournments or postponements thereof. |

The Separation and REIT Conversion Merger are conditioned on approval by Sun stockholders and satisfaction or waiver of all other conditions to the transactions as described in this proxy statement/prospectus.

The board of directors of Sun has fixed the close of business on , 2010 as the record date for determining stockholders entitled to receive notice of and vote at the special meeting and at any adjournment or postponement thereof. At the close of business on the record date, there were shares of Sun common stock outstanding and entitled to vote.

All stockholders are cordially invited to attend the special meeting in person. Whether or not you plan to attend the special meeting, you are urged to promptly submit your proxy or voting instructions. If you attend the special meeting and wish to vote your own shares in person, you may withdraw your proxy at that time.

For the Board of Directors,

Michael T. Berg

Secretary

, 2010

After careful consideration, the board of directors of Sun has unanimously determined that the Separation and REIT Conversion Merger are advisable and in the best interests of Sun and you, the Sun stockholders. The board of directors of Sun unanimously recommends that you vote “FOR” the Separation, “FOR” the adoption of the agreement and plan of merger to implement the REIT Conversion Merger and “FOR” the adjournment of the special meeting to a later date, if necessary, to solicit additional proxies if there are insufficient votes at the time of the special meeting to approve the Separation or adopt the agreement and plan of merger to implement the REIT Conversion Merger.

Important Notice Regarding the Availability of Proxy Materials for Sun’s Special Meeting of Stockholders to Be Held on , 2010. The accompanying proxy statement/prospectus is available at www.sunh.com.

Table of Contents

REFERENCES TO ADDITIONAL INFORMATION

This proxy statement/prospectus incorporates important information about Sun Healthcare Group, Inc. (“Sun”) that is not included in or delivered with this proxy statement/prospectus. For a listing of the documents incorporated by reference into this proxy statement/prospectus, see “Where You Can Find More Information.” You may obtain these documents through the website of the Securities and Exchange Commission (the “SEC”) at www.sec.gov. You may also request a copy of these documents at no cost by writing or telephoning Sun at:

Sun Healthcare Group, Inc.

101 Sun Avenue, N.E.

Albuquerque, New Mexico 87109

(505) 468-2341

Attention: Investor Relations

You may also obtain a copy of these documents by requesting them in writing or by telephone from Sun’s proxy solicitation agent at the following address and telephone number:

Innisfree M&A

501 Madison Avenue

New York, NY 10022

(212) 750-5833

To obtain timely delivery of such information, you must request such information no later than , 2010.

i

Table of Contents

ii

Table of Contents

| Page | ||

| 66 | ||

| 69 | ||

| 69 | ||

| 70 | ||

| 71 | ||

| 72 | ||

| U.S. Federal Income Tax Consequences of the REIT Conversion Merger |

73 | |

| 74 | ||

| 85 | ||

| 86 | ||

| 86 | ||

| 86 | ||

| 87 | ||

| 87 | ||

| 87 | ||

| 88 | ||

| 88 | ||

| 89 | ||

| 89 | ||

| 91 | ||

| 92 | ||

| 93 | ||

| 96 | ||

| 97 | ||

| 97 | ||

| 97 | ||

| 98 | ||

| 99 | ||

| 100 | ||

| 100 | ||

| 102 | ||

| 102 | ||

| 103 | ||

| 104 | ||

| 104 | ||

| 105 | ||

| 105 | ||

| 105 | ||

| 106 | ||

| 106 | ||

| 107 | ||

| 110 | ||

| SABRA PRO FORMA CAPITALIZATION AND SUPPLEMENTAL PRO FORMA FINANCIAL INFORMATION |

111 | |

| NEW SUN UNAUDITED PRO FORMA CONSOLIDATED FINANCIAL STATEMENTS |

112 | |

| 120 | ||

| 127 | ||

| 127 | ||

| 128 | ||

| 129 | ||

| 134 |

iii

Table of Contents

| Page | ||

| 135 | ||

| 170 | ||

| 172 | ||

| Information Regarding Directors and Executive Officers of New Sun |

172 | |

| 172 | ||

| 175 | ||

| 176 | ||

| 177 | ||

| Stockholder and Interested Party Communications with Directors |

178 | |

| 179 | ||

| Information Regarding Directors and Executive Officers of Sabra |

179 | |

| 179 | ||

| 180 | ||

| 180 | ||

| 181 | ||

| Stockholder and Interested Party Communications with Directors |

182 | |

| 183 | ||

| 185 | ||

| 208 | ||

| SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT |

209 | |

| 213 | ||

| 215 | ||

| 219 | ||

| 228 | ||

| 238 | ||

| 238 | ||

| 238 | ||

| 238 | ||

| 240 |

iv

Table of Contents

| Q: | What transactions are being proposed? |

| A: | The board of directors of Sun has approved a plan to restructure its business by separating its real estate assets and its operating assets into two separate publicly traded companies. This plan consists of the following key transactions: |

| • | reorganizing, through a series of internal corporate restructurings, such that: |

| ¡ | substantially all of Sun’s owned real property and related mortgage indebtedness owed to third parties will be held or assumed by Sabra Health Care REIT, Inc., a Maryland corporation and a wholly owned subsidiary of Sun (“Sabra”), or by one or more subsidiaries of Sabra; and |

| ¡ | all of Sun’s operations and other assets and liabilities will be held or assumed by SHG Services, Inc. (to be renamed “Sun Healthcare Group, Inc.”), a Delaware corporation and a wholly owned subsidiary of Sun (“New Sun”), or by one or more subsidiaries of New Sun; |

| • | New Sun and Sabra entering into certain agreements with each other, including multiple master lease agreements (the “Lease Agreements”) that will set forth the terms pursuant to which New Sun will lease from Sabra all of the real property that Sabra will own immediately following the restructuring of Sun’s business (representing 87 of the 202 properties that subsidiaries of Sun operated as of March 31, 2010); |

| • | Sun distributing to its stockholders on a pro rata basis all of the outstanding shares of New Sun common stock (this distribution is referred to in this proxy statement/prospectus as the “Separation”); |

| • | Sun distributing cash to its stockholders who hold shares of Sun common stock on the record date for the Separation, the actual amount of the cash distribution to be determined at the time of the Separation (the cash distribution is currently expected to be approximately $ per share, resulting in an aggregate cash distribution to Sun’s stockholders of approximately $13 million); |

| • | Sun merging with and into Sabra, with Sabra surviving the merger as a Maryland corporation and Sun stockholders receiving shares of Sabra common stock in exchange for their shares of Sun common stock (this merger is referred to in this proxy statement/prospectus as the “REIT Conversion Merger”); and |

| • | Sabra qualifying and electing to be treated as a real estate investment trust (“REIT”) for U.S. federal income tax purposes, which is currently expected to occur commencing with its taxable year beginning on January 1, 2011 (this election, together with the REIT Conversion Merger, is collectively referred to in this proxy statement/prospectus as the “REIT Conversion”). |

| Q: | What is a REIT? |

| A: | A REIT is a company that derives most of its income from real estate mortgages or real property. If a corporation qualifies and elects to be treated as a REIT, it generally will not be subject to U.S. federal corporate income taxes on income that it currently distributes to its stockholders. A company’s qualification as a REIT depends on its ability to meet on a continuing basis various tests under the Internal Revenue Code of 1986, as amended (the “Code”), relating to various matters, including the sources of its gross income, the composition and value of its assets, its distribution levels to its stockholders and the diversity of ownership of its stock. |

| Q: | When will the Separation and REIT Conversion Merger occur? |

| A: | The Separation and REIT Conversion Merger are expected to occur on or about , 2010. The board of directors of Sun will set the record date for the Separation after the special meeting. The REIT Conversion |

1

Table of Contents

| Merger is expected to occur immediately following the Separation. The timing of the Separation and REIT Conversion Merger will ultimately depend upon the satisfaction or waiver of certain conditions, including obtaining stockholder approval of the Separation and REIT Conversion Merger and completing the debt financing transactions described under the caption “Description of Material Indebtedness.” |

Sun reserves the right to abandon, defer or modify the Separation and REIT Conversion Merger at any time, even if Sun stockholders approve the Separation and REIT Conversion Merger. Sun may not proceed with the Separation and REIT Conversion Merger if the board of directors of Sun determines for any reason that these transactions are no longer in the best interests of Sun and its stockholders.

| Q: | What will I receive in connection with the Separation and REIT Conversion Merger? |

| A: | As a result of the Separation, you will be entitled to receive shares of New Sun common stock for each share of Sun common stock held by you on the record date for the Separation. In addition, Sun intends to make a cash distribution to holders of Sun common stock on the record date for the Separation of approximately $ per share resulting in an aggregate cash distribution of approximately $13 million. The actual amount of the cash distribution to Sun’s stockholders will not be determined until the time of the Separation. |

In addition, your Sun common stock will automatically convert in the REIT Conversion Merger into shares of Sabra common stock for each share of Sun common stock held by you at the effective time of the REIT Conversion Merger.

| Q: | Will I receive fractional shares of New Sun common stock or Sabra common stock in connection with the Separation and REIT Conversion Merger? |

| A: | No fractional shares of New Sun common stock or Sabra common stock will be issued in connection with the Separation and REIT Conversion Merger. Instead, American Stock Transfer & Trust Company, LLC (“American Stock Transfer”), who will serve as the distribution agent for the Separation and as the exchange agent for the REIT Conversion Merger, will aggregate all fractional shares that would otherwise have been distributed to Sun stockholders into whole shares, sell these whole shares in the open market at prevailing market prices and distribute the net cash proceeds from these sales to those stockholders who would have been entitled to receive fractional shares. This payment will be made from these sales on a pro rata basis based on the fractional interest in a share of New Sun common stock or Sabra common stock, as applicable, that the stockholder would have otherwise been entitled to receive. The amount of the cash payment will depend on the prices at which the aggregated fractional shares are sold by American Stock Transfer and the timing of such payment will be based upon the time that will be necessary for American Stock Transfer to sell these shares in an orderly manner. New Sun will be responsible for the payment of any brokerage or other fees in connection with the sale of aggregated fractional shares of New Sun common stock and Sabra will be responsible for the payment of any brokerage or other fees in connection with the sale of aggregated fractional shares of Sabra common stock. Recipients of cash in lieu of fractional shares will not be entitled to any interest on payments made in lieu of fractional shares. |

| Q: | Will I still own my shares of Sun after the completion of the transactions? |

| A: | No. You will receive shares of New Sun common stock as a result of the Separation and, upon the completion of the REIT Conversion Merger, your existing shares of Sun common stock will automatically convert into shares of Sabra common stock. |

| Q: | Should I send in my stock certificates now? |

| A: | No. If the Separation and REIT Conversion Merger are completed, you will not be required to return your stock certificates representing shares of Sun common stock in order to receive your shares of New Sun common stock or Sabra common stock. Neither New Sun nor Sabra will issue physical certificates for the |

2

Table of Contents

| shares you will receive in connection with the Separation or REIT Conversion Merger in exchange for your shares of Sun common stock, even if you currently hold a physical certificate. Instead, New Sun and Sabra will direct American Stock Transfer to electronically issue shares of New Sun common stock and Sabra common stock to you or to your bank, broker or other nominee on your behalf by way of direct registration in book-entry form. Any physical certificates representing shares of Sun common stock will be deemed cancelled and will no longer represent any ownership interest. |

| Q: | How will the rights of Sun stockholders change following the Separation and REIT Conversion Merger? |

| A: | Upon the Separation, Sun stockholders as of the record date for the Separation will also become stockholders of New Sun. The rights of the stockholders of New Sun following the Separation will be governed by the Delaware General Corporation Law (the “DGCL”) and the provisions of the certificate of incorporation and bylaws of New Sun as described in this proxy statement/prospectus. As a Delaware corporation, Sun is also governed by the DGCL. There will be no material differences between New Sun’s certificate of incorporation and bylaws and Sun’s existing amended and restated certificate of incorporation and bylaws. |

Following the REIT Conversion Merger, Sun stockholders will become stockholders of Sabra and their rights will be governed by the Maryland General Corporation Law (the “MGCL”) and the provisions of Sabra’s charter and bylaws as described in this proxy statement/prospectus. One of the primary differences between Sun’s existing amended and restated certificate of incorporation and Sabra’s charter is that Sabra’s charter will contain transfer and ownership restrictions on the percentage of outstanding shares of its stock that a person may own or acquire. These restrictions are intended to assist Sabra in qualifying and maintaining its qualification as a REIT for U.S. federal income tax purposes. Under Sabra’s charter, subject to certain limitations, no person or entity may beneficially own, or be deemed to own by virtue of the applicable constructive ownership provisions of the Code, more than 9.9% in value or number of shares, whichever is more restrictive, of Sabra’s outstanding common stock. For a more detailed discussion of the material differences between the current rights of Sun stockholders and the rights those stockholders would have as stockholders of Sabra following the REIT Conversion Merger, see “Comparative Rights of Sabra and Sun Stockholders.”

| Q: | When will I be able to trade shares of New Sun common stock or shares of Sabra common stock? |

| A: | It is expected that, upon completion of the Separation and REIT Conversion Merger, the shares of New Sun common stock will trade on the NASDAQ Global Select Market under the symbol “SUNH” and the shares of Sabra common stock will trade on the NASDAQ Global Select Market under the symbol “SBRA.” |

Shares of New Sun common stock are expected to trade on a “when-issued” basis beginning on or shortly before the record date for the Separation and continuing through the distribution date for the Separation. “When-issued” trading in the context of the Separation refers to a sale or purchase effected on or before the date of the Separation and made conditionally because the securities of New Sun have not yet been distributed. “When-issued” trades are generally expected to settle within three trading days after the distribution date for the Separation. You may trade this entitlement to receive New Sun common stock, without the Sun common stock you own, on the “when-issued” market. On the first trading day following the distribution date for the Separation, “when-issued” trading with respect to New Sun common stock will end and “regular trading” will begin.

| Q: | Why did Sun adopt a stockholder rights agreement, and will the stockholder rights agreement continue at New Sun and Sabra after completion of the transactions? |

| A: | Sabra may not qualify for REIT status if a single stockholder owned 10% or more of Sun common stock immediately prior to the Separation and REIT Conversion Merger. The stockholder rights agreement (the “Rights Plan”) was adopted to discourage third parties from exceeding this ownership limitation and will |

3

Table of Contents

| terminate upon the earlier of the effective time of the REIT Conversion Merger or May 24, 2011. Accordingly, the Rights Plan will not continue in respect of shares of New Sun common stock or shares of Sabra common stock. Neither New Sun nor Sabra will initially have a stockholder rights agreement and neither has plans to adopt one, although each of their respective boards of directors could make the determination at a future date to adopt a stockholder rights agreement. Sabra’s charter will contain restrictions on the transfer and ownership of its stock. See “Description of Sabra Stock—Restrictions on Transfer and Ownership of Sabra Stock.” |

| Q: | Who will pay the costs of the Separation and REIT Conversion Merger? |

| A: | New Sun will pay all costs associated with the Separation and REIT Conversion Merger that are incurred prior to the Separation, except that Sabra will bear all costs of the Separation and REIT Conversion Merger specifically identifiable to it, including the costs incurred by Sabra in entering into the financing transactions described under the caption “Description of Material Indebtedness.” All costs relating to the Separation or REIT Conversion Merger incurred after the Separation will be borne by the party incurring such costs. |

| Q: | What items of business am I being asked to vote on at the special meeting? |

| A: | At the special meeting, you will be asked to consider and vote on the following proposals: |

| • | a proposal to approve the Separation (Proposal No. 1); |

| • | a proposal to adopt the agreement and plan of merger by and between Sun and Sabra to implement the REIT Conversion Merger (Proposal No. 2); and |

| • | a proposal to adjourn the special meeting to a later date, if necessary, to solicit additional proxies if there are insufficient votes at the time of the special meeting to approve the Separation and adopt the agreement and plan of merger to implement the REIT Conversion Merger (Proposal No. 3). |

| Q: | What will be the effect on the proposals if the Separation or the REIT Conversion Merger is not approved by Sun stockholders? |

| A: | A condition to each of the Separation and REIT Conversion Merger is that both transactions have been approved by Sun stockholders. Even if stockholder approval of the Separation has been obtained, the Separation will not proceed unless all other required conditions to the Separation have been satisfied or waived, including the satisfaction or waiver of all required conditions to the REIT Conversion Merger. Similarly, even if stockholder approval of the REIT Conversion Merger has been obtained, the REIT Conversion Merger will not proceed unless the Separation has been completed and all other required conditions to the REIT Conversion Merger have been satisfied or waived. |

| Q: | How does the board of directors of Sun recommend that I vote? |

| A: | The board of directors of Sun has unanimously approved the Separation and the REIT Conversion Merger and has determined that these actions are advisable and in the best interests of Sun and its stockholders. The board of directors of Sun unanimously recommends that you vote your shares “FOR” approval of the Separation, “FOR” adoption of the agreement and plan of merger to implement the REIT Conversion Merger and “FOR” the adjournment proposal. |

| Q: | What votes are required? |

| A: | The Separation. The affirmative vote of a majority of the outstanding shares of Sun common stock present, either in person or represented by proxy, at the special meeting and entitled to vote on the proposal is required to approve the Separation. If you “ABSTAIN” from voting on approval of the Separation, the effect will be the same as a vote against the Separation. Please note that stockholder approval of the Separation is not required by applicable law, although it is a condition to the completion of the Separation. See “The Proposals—Proposal No. 1—Approval of the Separation—Conditions to the Separation.” Sun will |

4

Table of Contents

| not complete the Separation and REIT Conversion Merger as contemplated in this proxy statement/ prospectus if Sun’s stockholders do not approve the Separation at the special meeting. However, if stockholder approval is not obtained, Sun reserves the right to consider, and implement without stockholder approval if permitted by applicable law, other restructuring plans in the future, and such plans may be substantially similar to the transactions proposed in this proxy statement/prospectus. |

The REIT Conversion Merger. The affirmative vote of a majority of the outstanding shares of Sun common stock entitled to vote at the special meeting is required to adopt the agreement and plan of merger to implement the REIT Conversion Merger. If you do not submit a proxy or voting instruction form or do not vote in person at the special meeting, or if you “ABSTAIN” from voting on adoption of the agreement and plan of merger, the effect will be the same as a vote against the adoption of the agreement and plan of merger.

Adjournment of the special meeting. The affirmative vote of a majority of the outstanding shares of Sun common stock present, either in person or represented by proxy, at the special meeting and entitled to vote on the proposal is required to adjourn the special meeting to a later date, if necessary, to solicit additional proxies if there are insufficient votes at the time of the special meeting to approve the Separation and adopt the agreement and plan of merger to implement the REIT Conversion Merger. If you “ABSTAIN” from voting on approval of the adjournment, the effect will be the same as a vote against the adjournment of the special meeting.

| Q: | How many shares of Sun common stock must be present or represented to conduct business at the special meeting? |

| A: | The holders of a majority in voting power of the outstanding shares of Sun common stock entitled to vote at the special meeting will constitute a quorum for the transaction of business at the special meeting and any adjournments or postponements thereof. If you submit a proxy or voting instructions, your shares will be counted for purposes of determining the presence of a quorum, even if you “ABSTAIN” from voting your shares on the proposals. If a quorum is not present at the special meeting, the special meeting may be adjourned until a quorum is obtained. |

| Q: | Who is entitled to vote at the special meeting? |

| A: | Only stockholders of record at the close of business on , 2010, the record date for the special meeting, will be entitled to notice of and to vote at the special meeting. At the close of business on the record date for the special meeting, shares of Sun common stock were outstanding and entitled to vote. |

As of the close of business on the record date for the special meeting, executive officers and directors of Sun held an aggregate of shares of Sun common stock, which represents approximately % of all shares entitled to vote at the special meeting.

| Q: | What is the difference between a “stockholder of record” and a “beneficial stockholder”? |

| A: | Whether you are a stockholder of record or a beneficial stockholder depends on how you hold your shares of Sun common stock. |

Stockholders of Record. If your shares of Sun common stock are registered directly in your name with Sun’s transfer agent, American Stock Transfer, you are considered the stockholder of record with respect to those shares, and the proxy materials for the special meeting are being mailed to you directly by Sun.

Beneficial Stockholders. Most of Sun’s stockholders hold their shares through a bank, broker or other nominee (that is, in “street name”) rather than directly in their own name. If you hold your shares of Sun common stock in street name, you are a “beneficial stockholder,” and the proxy materials are being mailed

5

Table of Contents

to you by the organization holding your shares. This organization, or its nominee, is considered the stockholder of record for purposes of voting at the special meeting. As a beneficial stockholder, you have the right to instruct that organization on how to vote the shares held in your account.

| Q: | May I vote in person? |

| A: | If you are a stockholder of record as of the close of business on the record date for the special meeting, you may attend the special meeting and vote your shares of Sun common stock in person rather than signing and returning your proxy card or otherwise providing your proxy instructions. Your name will be verified against the list of stockholders of record on the record date for the special meeting prior to your being admitted to the special meeting. |

If you are a beneficial stockholder, you are also invited to attend the special meeting but you may not vote these shares of Sun common stock in person at the special meeting unless you obtain a “legal proxy” from the bank, broker or other nominee, giving you the right to vote the shares at the special meeting. You will be asked to provide proof of beneficial ownership on the record date for the special meeting, such as your most recent account statement, a copy of the voting instruction form provided by your bank, broker or other nominee, or other similar evidence of ownership, prior to your being admitted to the special meeting.

If you do not comply with the procedures outlined above, you will not be admitted to the special meeting. Even if you plan to attend the special meeting, it is recommended that you submit your proxy or voting instructions in advance of the special meeting as described below so that your vote will be counted if you later decide not to attend the special meeting.

| Q: | How can I vote my shares without attending the special meeting? |

| A: | Whether you are a stockholder of record or a beneficial stockholder, you may direct how your shares of Sun common stock are voted without attending the special meeting. If you are a stockholder of record, you may submit a proxy to instruct how your shares of Sun common stock are to be voted at the special meeting. You can submit a proxy by mail by completing, signing, dating and returning the proxy card enclosed with the proxy materials you received or by telephone or Internet by following the instructions provided on the proxy card. If you are a beneficial stockholder, you may submit voting instructions to your bank, broker or other nominee to instruct how your shares of Sun common stock are to be voted at the special meeting. Your voting instructions can be submitted by mail by completing, signing, dating and returning the voting instruction form enclosed with the proxy materials you received or by telephone or Internet, if those voting options are available to you, by following the instructions provided on the voting instruction form. |

| Q: | May I change or revoke my proxy or voting instructions? |

| A: | You have the power to revoke or change your proxy or voting instructions before your shares of Sun common stock are voted at the special meeting. If you are a stockholder of record, you may do this by submitting a written notice of revocation to Sun’s Secretary, by submitting a duly executed written proxy bearing a date that is later than the date of your original proxy or by submitting a later dated proxy electronically via the Internet or by telephone. A previously submitted proxy will not be voted if the stockholder of record who executed it is present at the special meeting and votes the shares of Sun common stock represented by the proxy in person at the special meeting. If you are a beneficial stockholder, you may change your vote by submitting new voting instructions to your bank, broker or other nominee, or, if you have obtained a legal proxy from your bank, broker or other nominee giving you the right to vote your shares of Sun common stock, by attending the special meeting and voting in person. Please note that attendance at the special meeting will not by itself constitute revocation of a proxy. |

6

Table of Contents

| Q: | How will my shares be voted if I do not provide specific instructions in the proxy or voting instruction form I submit? |

| A: | If you submit a proxy or voting instruction form but do not indicate your specific voting instructions on one or more of the proposals listed in the notice of the special meeting, your shares of Sun common stock will be voted as recommended by the board of directors of Sun on those proposals and, in the case of a proxy, as the proxyholders may determine in their discretion with respect to any other matters properly presented for a vote at the special meeting. |

| Q: | If my shares are held in “street name” by a bank, broker or other nominee, how will my shares be voted? |

| A: | You should instruct your bank, broker or other nominee how to vote your shares of Sun common stock, following the directions provided to you. If you do not instruct your broker, your broker will generally not have the discretion to vote your shares of Sun common stock without your instructions on matters that are not considered routine. Sun believes that the Separation proposal, the REIT Conversion Merger proposal and the proposal to adjourn the special meeting are each considered not to be routine matters. Therefore, your broker cannot vote shares of Sun common stock that it holds in “street name” on any of the proposals unless you return the voting instruction form you received from your broker. Accordingly, Sun does not believe that there will be any broker non-votes occurring in connection with any of the proposals at the special meeting. Please note, however, that if you properly return the voting instruction form to your broker but do not indicate how you want your shares of Sun common stock to be voted, Sun believes your shares of Sun common stock generally will be voted “FOR” all of the proposals listed in the notice for the special meeting. |

| Q: | Am I entitled to dissenters’ or appraisal rights? |

| A: | Under Delaware law, you are not entitled to dissenters’ or appraisal rights in connection with the Separation or the REIT Conversion Merger. |

| Q: | What if I want to transfer my shares of Sun common stock? |

| A: | You should consult with your financial advisor, such as your broker, bank or tax advisor. Sun, New Sun and Sabra make no recommendations concerning the purchase, retention or sale of shares of Sun common stock or of the New Sun common stock or Sabra common stock you will receive if the Separation and REIT Conversion Merger are completed. |

The record date for the special meeting is earlier than the record date for the Separation and the effective time of the REIT Conversion Merger. Therefore, if you sell your shares of Sun common stock after the record date of the special meeting, but prior to the record date for the Separation or the effective time of the REIT Conversion Merger (neither of which has yet been determined), you will retain the right to vote at the special meeting, but the right to receive New Sun common stock in connection with the Separation and Sabra common stock in connection with the REIT Conversion Merger will transfer with the shares of Sun common stock.

| Q: | As a Sun stockholder, what should I consider in deciding whether to vote in favor of the Separation and the REIT Conversion Merger? |

| A: | You should carefully review this proxy statement/prospectus, including the section entitled “Risk Factors” which sets forth certain risks and uncertainties related to the Separation and REIT Conversion Merger and certain risks and uncertainties to which New Sun and Sabra will be subject if these transactions are implemented. |

7

Table of Contents

| Q: | Who is paying for this proxy solicitation? |

| A: | Sun is making this solicitation and will pay the entire cost of preparing and distributing these proxy materials and soliciting proxies. Sun has also retained Innisfree M&A, a proxy solicitation firm, to solicit proxies on behalf of Sun. Sun has agreed to pay Innisfree M&A an estimated fee of $25,000, plus its out-of-pocket expenses in connection with such solicitation of proxies on behalf of Sun. In addition to these mailed proxy materials, Sun’s directors, executive officers and other employees may also solicit proxies or votes in person, by telephone or by other means of communication. Directors, executive officers and employees will not be paid any additional compensation for soliciting proxies. Sun will also reimburse banks, brokers and other nominees for their costs in forwarding proxy materials to Sun’s beneficial stockholders. |

| Q: | Who can help answer my questions? |

| A: | If you have any questions or need further assistance in voting your shares of Sun common stock, or if you need additional copies of this proxy statement/prospectus or the proxy card, please contact: |

Sun Healthcare Group, Inc.

101 Sun Avenue, N.E.

Albuquerque, New Mexico 87109

Attention: Investor Relations

Telephone number: (505) 468-2341

or

Innisfree M&A

501 Madison Avenue

New York, NY 10022

Telephone number: (212) 750-5833

8

Table of Contents

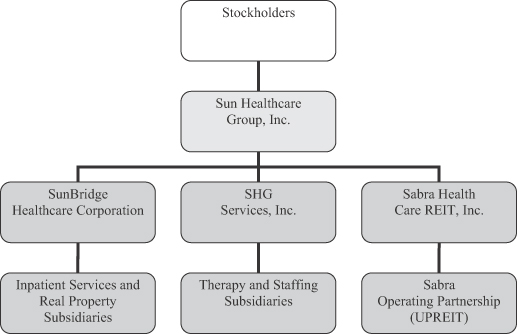

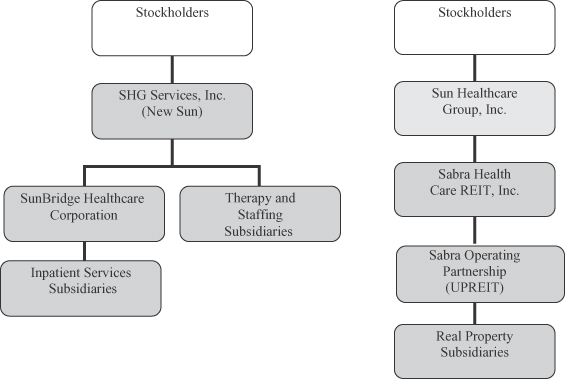

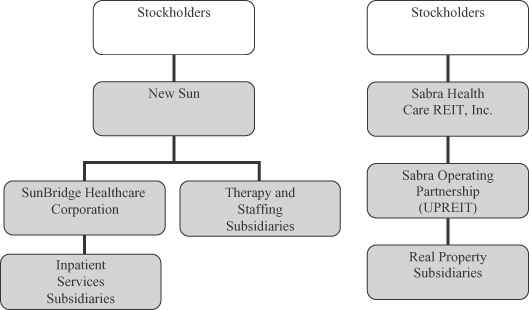

STRUCTURE OF THE SEPARATION AND REIT CONVERSION MERGER

In order to help you better understand the structure of the Separation and REIT Conversion Merger, the charts below illustrate, in simplified form, the organizational structure of Sun Healthcare Group, Inc., SHG Services, Inc. and Sabra Health Care REIT, Inc. as they exist currently, and as they will exist immediately following the Separation and immediately following the REIT Conversion Merger:

Current

9

Table of Contents

After the Separation

After the REIT Conversion Merger

10

Table of Contents

This summary highlights selected information contained or incorporated by reference in this proxy statement/prospectus and may not contain all of the information that is important to you. This summary is not intended to be complete and reference is made to, and this summary is qualified in its entirety by, the more detailed information contained or incorporated by reference in this proxy statement/prospectus. To fully understand the restructuring of Sun’s business, including the Separation and REIT Conversion, and for a more complete description of the terms of the Separation and REIT Conversion, you should read carefully this proxy statement/prospectus, together with the documents referred to in this proxy statement/prospectus. Unless the context otherwise requires, references in this proxy statement/prospectus to “Sun” shall be deemed to refer to Sun Healthcare Group, Inc. prior to completion of the Separation and REIT Conversion Merger.

Information about the Companies

Sun Healthcare Group, Inc.

18831 Von Karman, Suite 400

Irvine, CA 92612

(949) 255-7100

Sun Healthcare Group, Inc. (NASDAQ GS: SUNH) is referred to in this proxy statement/prospectus as Sun. Sun, through its subsidiaries, provides nursing, rehabilitative and related specialty healthcare services principally to the senior population in the United States. Sun’s core business is providing, through its subsidiaries, inpatient services, primarily through 166 skilled nursing centers, 16 combined skilled nursing, assisted and independent living centers, 10 assisted living centers, two independent living centers and eight mental health centers as of March 31, 2010. As of that date, Sun’s centers had 23,205 licensed beds located in 25 states, of which 22,423 were available for occupancy. Of the 202 centers operated by Sun’s subsidiaries as of March 31, 2010, 112 centers were leased from third parties and 90 centers were owned by Sun’s subsidiaries. Sun’s subsidiaries also provide rehabilitation therapy services to affiliated and non-affiliated centers and medical staffing and other ancillary services primarily to non-affiliated centers and other third parties. For the year ended December 31, 2009, Sun’s total net revenues from continuing operations were $1.9 billion. For the three months ended March 31, 2010, Sun’s total net revenues from continuing operations were $0.5 billion.

Business Segments

Sun’s subsidiaries currently engage in the following three principal business segments:

| • | inpatient services, primarily skilled nursing centers; |

| • | rehabilitation therapy services; and |

| • | medical staffing services. |

Inpatient services. Sun operates its healthcare facilities through SunBridge and other subsidiaries. Sun’s skilled nursing centers provide services that include daily nursing, therapeutic rehabilitation, social services, housekeeping, nutrition and administrative services for individuals requiring certain assistance for activities in daily living. Rehab Recovery Suites, which specialize in Medicare and managed care patients, are located in 65 of Sun’s skilled nursing centers, and 46 of Sun’s skilled nursing centers contain wings dedicated to the care of residents afflicted with Alzheimer’s disease. Sun’s assisted living centers provide services that include minimal nursing assistance, housekeeping, nutrition, laundry and administrative services for individuals requiring minimal assistance for activities in daily living. Sun’s independent living centers provide services that include security, housekeeping, nutrition and limited laundry services for individuals requiring no assistance for activities in daily living. Sun’s mental health centers provide a range of inpatient and outpatient behavioral health services for adults and children through specialized treatment programs. Sun also provides hospice services, including

11

Table of Contents

palliative care, social services, pain management and spiritual counseling, through its subsidiary SolAmor Hospice Corporation (“SolAmor”), in eight states for individuals facing end of life issues. Sun generated 89.1%, 88.6%, and 87.8% of its total net revenues from continuing operations through inpatient services in 2009, 2008, and 2007, respectively.

Rehabilitation therapy services. Sun provides rehabilitation therapy services through SunDance Rehabilitation Corporation (“SunDance”). SunDance provides a broad array of rehabilitation therapy services, including speech pathology, physical therapy and occupational therapy. As of March 31, 2010, SunDance provided rehabilitation therapy services to 468 centers in 36 states, 337 of which were operated by nonaffiliated parties and 131 of which were operated by affiliates. In most of Sun’s 71 healthcare centers for which SunDance does not provide rehabilitation therapy services, those services are provided by staff employed by the centers, although some centers engage third-party therapy companies for such services. Sun generated 5.6%, 4.9%, and 5.3% of its total net revenues from continuing operations through rehabilitation therapy services in 2009, 2008, and 2007, respectively.

Medical staffing services. Sun provides temporary medical staffing in 44 states through CareerStaff Unlimited, Inc. (“CareerStaff”). For the year ended December 31, 2009, CareerStaff derived 56.1% of its revenues from hospitals and other providers, 24.7% from skilled nursing centers, 15.3% from schools and 3.9% from prisons. CareerStaff provides (i) licensed therapists skilled in the areas of physical, occupational and speech therapy, (ii) nurses, (iii) pharmacists, pharmacist technicians and medical imaging technicians, (iv) physicians and (v) related medical personnel. Sun generated 5.3%, 6.5%, and 6.9% of its total net revenues from continuing operations through medical staffing services in 2009, 2008, and 2007, respectively.

SHG Services, Inc.

18831 Von Karman, Suite 400

Irvine, CA 92612

(949) 255-7100

SHG Services, Inc. is referred to in this proxy statement/prospectus as New Sun. New Sun is a wholly owned subsidiary of Sun which, as a result of the restructuring of Sun’s business described in this proxy statement/prospectus, will hold or assume immediately prior to the Separation, through its subsidiaries, all of Sun’s operations and other assets and liabilities (other than substantially all of Sun’s owned real property). New Sun will retain ownership of four healthcare properties that are located in Georgia, Maryland, Massachusetts and Wyoming as well as administrative office buildings in Albuquerque, New Mexico (the “New Sun Retained Properties”). Following the Separation, New Sun will be renamed “Sun Healthcare Group, Inc.” and through its subsidiaries, will continue to provide the same nursing, rehabilitative and related specialty healthcare services provided by Sun immediately prior to the Separation and will continue to engage in Sun’s three business segments of inpatient services, rehabilitation therapy services and medical staffing services. Shares of New Sun common stock are expected to trade on the NASDAQ Global Select Market under the symbol “SUNH.”

Sabra Health Care REIT, Inc.

, CA

( ) -

Sabra Health Care REIT, Inc. is referred to in this proxy statement/prospectus as Sabra. Sabra is a wholly owned subsidiary of Sun which, as a result of the restructuring of Sun’s business described in this proxy statement/prospectus, will hold immediately prior to the Separation, through its subsidiaries, all of Sun’s owned real

12

Table of Contents

property, other than the New Sun Retained Properties. The owned real property to be held by Sabra includes fixtures and certain personal property associated with the real property. Pursuant to the Lease Agreements, Sabra will lease those assets to New Sun’s subsidiaries. Following the consummation of the REIT Conversion Merger, Sabra currently intends to qualify and elect to be treated as a REIT for U.S. federal income tax purposes commencing with its taxable year beginning on January 1, 2011. Sabra expects to grow its portfolio through acquisitions as a broad-based healthcare REIT. As Sabra acquires additional properties and expands its portfolio, it expects to diversify by geography, asset class and tenant within the healthcare sector. Shares of Sabra common stock are expected to trade on the NASDAQ Global Select Market under the symbol “SBRA.”

Risks Associated with the Separation and REIT Conversion

The Separation and REIT Conversion pose a number of risks to Sun stockholders. Sun stockholders will receive shares of New Sun and Sabra common stock as a result of the Separation and REIT Conversion Merger. After the Separation and REIT Conversion Merger, each of New Sun and Sabra will be subject to various risks associated with their respective businesses. Some of these risks include:

Risks Relating to the Separation and REIT Conversion

| • | The receipt of the stock and cash distribution in the Separation may be taxable, in whole or in part, to Sun’s stockholders as a dividend, which could cause Sun’s stockholders to incur tax liabilities. |

| • | The historical and pro forma financial information included in this proxy statement/prospectus is not necessarily representative of the results New Sun or Sabra would have achieved as separate, publicly traded companies. |

| • | The Separation and REIT Conversion could give rise to liabilities, disputes, increased costs or other unfavorable effects that may not have otherwise arisen. |

Risks Associated with the Status of Sabra as a REIT

| • | Because the timing of the REIT Conversion is not certain, Sabra may not realize the anticipated tax benefits from the REIT Conversion commencing with its taxable year beginning on January 1, 2011. |

| • | Failure to qualify as a REIT would subject Sabra to U.S. federal income tax, which would reduce the cash available for distribution to stockholders of Sabra. |

| • | Complying with REIT requirements may cause Sabra to forego otherwise attractive acquisition opportunities or liquidate otherwise attractive investments, which could materially hinder Sabra’s performance. |

Risks Relating to New Sun’s Business

| • | New Sun’s business will be dependent on reimbursement rates under federal and state programs, and legislation or regulatory action may reduce or otherwise materially adversely affect the reimbursement rates. |

| • | Healthcare reform may affect New Sun’s revenues and increase New Sun’s costs and otherwise materially adversely affect New Sun’s business. |

| • | New Sun’s revenue and collections may be materially adversely affected by the economic downturn. |

| • | Possible changes in the case mix of residents and patients, as well as payor mix and payment methodologies, may materially affect New Sun’s revenues and profitability. |

13

Table of Contents

Risks Relating to Sabra’s Business

| • | Sabra’s business will be dependent on New Sun until Sabra substantially diversifies its portfolio. |

| • | Sabra may be unable to make, on a timely or cost-effective basis, the changes necessary to operate as a separate publicly traded company focused on owning a portfolio of healthcare properties. |

| • | An increase in market interest rates could increase Sabra’s interest costs on existing and future debt. |

| • | Sabra is dependent on the healthcare industry and may be susceptible to the risks associated with healthcare reform. |

These and other risks relating to the Separation and REIT Conversion and the businesses of New Sun and Sabra following the Separation and REIT Conversion Merger are discussed in greater detail under the caption “Risk Factors.” You should read and consider all of these risks carefully.

The Special Meeting of Sun Stockholders

Date, Time and Place. The special meeting of Sun stockholders will be held on , 2010, at at a.m. local time, and at any adjournment or postponement thereof.

Purpose of the Special Meeting. At the special meeting, Sun’s stockholders will be asked to consider and vote upon (i) a proposal to approve the Separation; (ii) a proposal to adopt the agreement and plan of merger by and between Sun and Sabra to implement the REIT Conversion Merger; and (iii) a proposal to adjourn the special meeting to a later date, if necessary, to solicit additional proxies if there are insufficient votes at the time of the special meeting to approve the Separation and adopt the agreement and plan of merger to implement the REIT Conversion Merger.

Record Date; Shares Entitled to Vote; Quorum. Only stockholders of record at the close of business on , 2010, the record date for the special meeting, will be entitled to notice of and to vote at the special meeting. At the close of business on the record date for the special meeting, shares of Sun common stock were outstanding and entitled to vote. As of the close of business on the record date for the special meeting, executive officers and directors of Sun held an aggregate of shares of Sun common stock, which represents approximately % of all shares of Sun common stock entitled to vote at the special meeting. The presence in person or by proxy of the holders of a majority in voting power of the outstanding shares of Sun common stock entitled to vote at the special meeting will constitute a quorum for the transaction of business at the meeting and any adjournments or postponements thereof.

Vote Required

The Separation. The affirmative vote of a majority of the outstanding shares of Sun common stock present, either in person or represented by proxy, at the special meeting and entitled to vote on the proposal is required to approve the Separation. If you “ABSTAIN” from voting on approval of the Separation, the effect will be the same as a vote against the Separation. Stockholder approval of the Separation is not required by applicable law, although it is a condition to the completion of the Separation. See “The Proposals—Proposal No. 1—Approval of the Separation—Conditions to the Separation.” Sun will not complete the Separation and REIT Conversion Merger as contemplated in this proxy statement/prospectus if Sun’s stockholders do not approve the Separation at the special meeting. However, if stockholder approval is not obtained, Sun reserves the right to consider, and implement without stockholder approval if permitted by applicable law, other restructuring plans in the future, and such plans may be substantially similar to the transactions proposed in this proxy statement/prospectus.

14

Table of Contents

The REIT Conversion Merger. The affirmative vote of a majority of the outstanding shares of Sun common stock entitled to vote at the special meeting is required to adopt the agreement and plan of merger to implement the REIT Conversion Merger. If you do not submit a proxy or voting instruction form or do not vote in person at the special meeting, or if you “ABSTAIN” from voting on adoption of the agreement and plan of merger, the effect will be the same as a vote against the adoption of the agreement and plan of merger.

Adjournment of the Special Meeting. The affirmative vote of a majority of the outstanding shares of Sun common stock present, either in person or represented by proxy, at the special meeting and entitled to vote on the proposal is required to adjourn the special meeting to a later date, if necessary, to solicit additional proxies if there are insufficient votes at the time of the special meeting to approve the Separation and adopt the agreement and plan of merger to implement the REIT Conversion Merger. If you “ABSTAIN” from voting on approval of the adjournment, the effect will be the same as a vote against the adjournment of the special meeting.

Overview of the Separation and REIT Conversion

Pursuant to the restructuring plan approved by the board of directors of Sun to separate Sun’s real estate assets and its operating assets into two publicly traded companies, Sun will reorganize, through a series of internal corporate restructurings. After the restructuring, subsidiaries of Sabra will hold all of Sun’s owned real property (other than the New Sun Retained Properties). Sabra will assume the liabilities, including the mortgage indebtedness, of Sun that are related to the real property to be owned by it. All of Sun’s operations and other assets and liabilities will be held or assumed by New Sun or by one or more of its subsidiaries. New Sun and Sabra will enter into certain agreements, including the Lease Agreements pursuant to which subsidiaries of New Sun will lease from Sabra all of the real property that Sabra will own immediately following the restructuring of Sun’s business.

Upon satisfaction or waiver of the conditions to the Separation and REIT Conversion Merger, Sun will distribute to its stockholders on a pro rata basis all of the outstanding shares of New Sun common stock, together with an additional cash distribution. The actual amount of the cash distribution will not be determined until the time of the Separation, but Sun currently expects it to be approximately $ per share, resulting in an aggregate cash distribution to Sun’s stockholders of approximately $13 million. Sun will then merge with and into Sabra, with Sabra surviving the merger as a Maryland corporation and Sun stockholders receiving shares of Sabra common stock in exchange for their shares of Sun common stock. In each case, cash will be paid in lieu of fractional shares. The Separation and REIT Conversion Merger are expected to occur on or about , 2010. Sabra currently intends to qualify and elect to be treated as a REIT for U.S. federal income tax purposes commencing with its taxable year beginning on January 1, 2011.

Following the REIT Conversion, Sabra intends to be a self-managed and self-administered REIT. Sabra expects to operate through an umbrella partnership (commonly referred to as an UPREIT) structure in which substantially all of its properties and assets will be held by Sabra Health Care Limited Partnership, a Delaware limited partnership, of which Sabra is the sole general partner.

Background and Reasons for the Separation and REIT Conversion

The board of directors of Sun believes that the Separation and REIT Conversion Merger will create two focused companies—one that will concentrate on providing quality care to residents and patients and the other that will concentrate on building a diversified healthcare real property company. The board of directors of Sun believes that the two separate public companies will:

| • | more readily enable Sun stockholders to maximize their investment in Sun; |

| • | lower the level of indebtedness for each of New Sun and Sabra following the Separation and REIT Conversion Merger in order to better position New Sun and Sabra to pursue their respective business |

15

Table of Contents

| and growth strategies, including, in the case of Sabra, pursuing acquisitions of healthcare properties at lower borrowing costs than would otherwise have been available for Sun; and |

| • | better position Sabra to realize the full value of Sun’s portfolio of healthcare properties and to strategically expand it in the healthcare sector beyond such properties while affording Sabra stockholders the benefit of a tax-advantaged REIT security. |

Relationship Between New Sun and Sabra After the Separation and REIT Conversion Merger

To govern their ongoing relationship, on or prior to the Separation, New Sun and Sabra or their respective subsidiaries, as applicable, will enter into: (i) a distribution agreement, providing for certain organizational matters, the mechanics related to the Separation and REIT Conversion Merger as well as other ongoing obligations of New Sun and Sabra (the “Distribution Agreement”), (ii) the Lease Agreements, (iii) an agreement relating to tax allocation matters (the “Tax Allocation Agreement”), and (iv) an agreement pursuant to which New Sun may provide certain services to Sabra on a transitional basis (the “Transition Services Agreement”). Although it is expected that the agreements between New Sun and Sabra will contain terms and conditions that generally are consistent with current market terms and conditions, because these agreements are being negotiated in the context of the Separation, the terms and conditions in the agreements may be different than those that either Sabra or New Sun may have obtained from unaffiliated parties. See “Risk Factors—New Sun and Sabra may have been able to receive better terms from unaffiliated third parties than the terms they receive in agreements entered into in connection with the Separation.”

Each of New Sun and Sabra will adopt certain policies to minimize potential conflicts of interest that may result from the service of Mr. Foster and Mr. Walters on the boards of directors of each of Sabra and New Sun. No other person will be a director, executive officer or other employee of both New Sun and Sabra.

Description of Material Indebtedness

Prior to completion of the Separation, New Sun and Sabra will enter into debt agreements that potentially will be secured by substantially all of their respective assets (other than assets securing mortgage indebtedness). The amount of indebtedness that New Sun and Sabra will incur will depend on the net cash generated by Sun between April 1, 2010 and the Separation (which will include the $ of net proceeds received by Sun from its recent equity offering). Based on Sun’s cash position as of March 31, 2010 together with the anticipated net proceeds of the equity offering reflected in the unaudited pro forma financial information of New Sun and Sabra included in this proxy statement/prospectus, Sun currently anticipates that New Sun will incur $182.9 million of indebtedness and Sabra will incur $205.0 million of indebtedness prior to completion of the Separation. The actual amount of indebtedness to be incurred by New Sun and Sabra could decrease if Sun’s cash position at the time the debt agreements are entered into is greater than Sun’s cash position as of March 31, 2010 together with the anticipated net proceeds of the equity offering or, conversely, could increase if Sun’s cash position at the time the debt agreements are entered into is less than Sun’s cash position as of March 31, 2010 together with the anticipated net proceeds of the equity offering. The terms and structure of the indebtedness to be incurred by New Sun and Sabra have not yet been determined. It is anticipated that the debt agreements will contain customary covenants that will include restrictions on each of New Sun’s and Sabra’s ability to make acquisitions and other investments, pay dividends, incur additional indebtedness and make capital expenditures as well as customary events of default.

It is also anticipated that the debt agreements to be entered into by New Sun and Sabra will each provide for a revolving credit facility to provide borrowing capacity for unusual or unexpected needs, and, in the case of Sabra, is expected to be used for acquisitions or other capital needs. The amount, terms and structure of such revolving credit facilities have not yet been determined. In addition, at the time of the Separation, New Sun is expected to have mortgage indebtedness to third parties of $6.7 million and Sabra is expected to have mortgage indebtedness to third parties of $162.8 million. For additional information relating to these debt financing arrangements, see “Description of Material Indebtedness.”

16

Table of Contents

Accounting Treatment for the Separation and REIT Conversion

Following the Separation, New Sun will continue the business and operations of Sun. Sabra will not have operated prior to the Separation. Immediately following the Separation and REIT Conversion Merger, Sabra will hold, through its subsidiaries, all of Sun’s owned real property (other than the New Sun Retained Properties). The owned real property to be held by Sabra includes fixtures and certain personal property associated with the real property. The only material liabilities of Sabra will consist of the indebtedness incurred by Sabra at the time of the Separation and the mortgage indebtedness to third parties on the real property to be owned by Sabra. The liabilities of New Sun will consist of indebtedness of New Sun incurred at the time of the Separation and substantially all of the liabilities of Sun immediately prior to the Separation, excluding the indebtedness of Sun repaid at the time of the Separation and the mortgage indebtedness to third parties assumed by Sabra. The historical consolidated financial statements of Sun will become the historical consolidated financial statements of New Sun at the time of the Separation. At the time of the Separation, the balance sheet of Sabra will include the owned real property and the mortgage indebtedness to third parties on the real property as well as the indebtedness incurred by Sabra prior to completion of the Separation. The statement of operations and cash flows of Sabra will consist solely of its operations after the Separation.

The assets and liabilities of Sabra will be recorded at their respective historical carrying values at the time of the Separation in accordance with the provisions of FASB ASC 505-60, “Spinoffs and Reverse Spinoffs.” Sun has concluded that the Separation should be accounted for as a reverse spinoff, and accordingly, the assets and liabilities to be distributed will be recorded based on the historical carrying values after reduction, if appropriate, for any indicated impairment of value. Indicators that a spinoff should be accounted for as a reverse spinoff include:

| • | whether the “legal” spinnee (i.e., New Sun) is larger than the “legal” spinnor (i.e., Sabra) based on a comparison of assets, revenues and earnings |

| • | the relative fair value of the “legal” spinnor to the “legal” spinnee |

| • | which entity retains the majority of senior management after the spinoff |

Based on these and other factors, the Separation will be accounted for as a reverse spinoff where New Sun is designated as the “accounting” spinnor and Sabra is designated as the “accounting” spinnee.

Regulatory Approvals Required for the Separation and REIT Conversion Merger

In connection with the Separation and the restructuring of Sun’s business, Sun will be required to file notices with, and in some jurisdictions obtain approvals or consents from, the various governmental agencies and commissions responsible for the licensure or certification of Sun’s inpatient centers and other lines of business. In some cases, these filings must be made, and approvals obtained, before the Separation can be completed. In other cases, notice filings will need to be made by New Sun after the Separation has been completed.

In addition, Sun and Sabra will be required to submit applications to the U.S. Department of Housing and Urban Development (“HUD”) to seek approvals regarding ten inpatient centers operated by Sun in order to complete the restructuring of Sun’s business as well as the Separation and REIT Conversion Merger.

Compensation

Following the Separation and REIT Conversion Merger, New Sun’s compensation committee and board of directors will discuss and approve the executive compensation program for New Sun’s executive officers. This compensation program is expected to be substantially similar to the compensation program currently in place at Sun, except with respect to Mr. Mathies. The details of Mr. Mathies’ compensation as the Chief Executive

17

Table of Contents

Officer of New Sun have not yet been determined. Prior to the Separation, New Sun will adopt new equity incentive plans containing substantially the same terms as Sun’s 2009 Performance Incentive Plan and Sun’s other equity incentive plans. New Sun will also assume the 401(k) plan and the deferred compensation plan of Sun.

Following the Separation and REIT Conversion Merger, Sabra’s compensation committee and board of directors will discuss and approve the executive compensation program for Sabra’s executive officers. The details of Mr. Matros’ compensation as Chief Executive Officer of Sabra, and the compensation of other executives of Sabra, have not yet been determined. Sabra will assume Sun’s 2009 Performance Incentive Plan and Sun’s other equity incentive plans in connection with the REIT Conversion Merger.

Treatment of Equity Awards in the Separation and REIT Conversion Merger

Except as described below for Mr. Matros, Sun options, whether vested or unvested, and unvested restricted stock units of Sun will be converted, and adjusted as described below, into awards with respect to shares of New Sun common stock. The number of shares subject to and the exercise price of each converted option, and the number of shares subject to each unvested restricted stock unit, will be adjusted to preserve the same intrinsic value of the awards that existed immediately prior to the Separation and REIT Conversion Merger. These converted awards will otherwise have the same general terms and conditions as the outstanding Sun awards, including the applicable vesting conditions. Each Sun restricted stock unit which has vested but the payment of which has been deferred to a later date will be converted into an award with respect to the same number of shares of New Sun common stock and Sabra common stock that a Sun stockholder will receive for each share of Sun common stock in connection with the Separation and REIT Conversion Merger. In addition, under the terms of the outstanding restricted stock unit awards, the holders of such awards will receive at the time the restricted stock units vest a per share cash distribution equal to the per share amount of cash to be paid to the holders of Sun common stock at the time of the Separation. Based upon the expected amount of the cash distribution of $ per share, the aggregate amount of the cash distribution, assuming all of the outstanding restricted stock units (other than those restricted stock units held by Mr. Matros, which units will terminate at the time of the Separation) become fully vested, is expected to be approximately $500,000. The actual amount of the distribution will not be determined until the time of the Separation. See “The Proposals—Proposal No. 1—Approval of the Separation.” Holders of Sun options do not have rights to receive cash distributions.

The unvested Sun options and restricted stock units held by Mr. Matros will be terminated for no consideration, while vested options held by Mr. Matros will terminate for no consideration if they are not exercised prior to or within up to three months following the Separation and REIT Conversion Merger. The termination of the existing Sun awards held by Mr. Matros will be taken into account by Sabra’s compensation committee when determining the amount of Sabra equity awards to be initially granted to Mr. Matros.

18

Table of Contents

PROPOSAL NO. 1—APPROVAL OF THE SEPARATION

Manner of Effecting the Separation