Attached files

| file | filename |

|---|---|

| EX-23.1 - CONSENT OF ERNST & YOUNG LLP, INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM - Univar Solutions Inc. | dex231.htm |

Table of Contents

As filed with the Securities and Exchange Commission on June 29, 2010

Registration No. 333-

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Univar Inc.

(Exact name of Registrant as specified in its charter)

| Delaware | 5169 | 26-1251958 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

17425 NE Union Hill Road

Redmond, Washington 98052

(425) 889-3900

(Address, including zip code, and telephone number, including area code, of Registrant’s principal executive offices)

John J. Zillmer

Univar Inc.

17425 NE Union Hill Road

Redmond, Washington 98052

(425) 889-3900

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Scott D. Miller Sullivan & Cromwell LLP 1870 Embarcadero Road Palo Alto, California 94303-3308 (650) 461-5600 |

Peter D. Heinz Univar Inc. 17425 NE Union Hill Road Redmond, Washington 98052 (425) 889-3900 |

Leslie N. Silverman Michael J. Volkovitsch Cleary Gottlieb Steen & Hamilton LLP One Liberty Plaza New York, New York 10006 (212) 225-2000 |

Approximate date of commencement of proposed sale to the public:

As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are being offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, as amended (the “Securities Act”), check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act (Check one):

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | x (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

CALCULATION OF REGISTRATION FEE

| Title of Each Class of Securities to be Registered |

Proposed Maximum |

Amount of Fee | ||

| Common Stock, $0.01 par value per share |

$862,500,000 |

$61,497 | ||

| (1) | Estimated solely for the purpose of computing the amount of the registration fee pursuant to Rule 457(a) under the Securities Act of 1933. |

| (2) | Includes offering price of additional shares which the underwriters have the option to purchase. See “Underwriting.” |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to Completion

Preliminary Prospectus dated June 29, 2010

P R O S P E C T U S

Shares

Univar Inc.

Common Stock

This is an initial public offering of shares of common stock of Univar Inc.

We are selling shares of our common stock and the selling stockholder is selling shares of our common stock. We will not receive any of the proceeds from the shares of our common stock sold by the selling stockholder.

Prior to this offering, there has been no public market for our common stock. The initial public offering price of our common stock is expected to be between $ and $ per share. We intend to apply to list our common stock on the under the symbol “ ”.

Investing in our common stock involves risks that are described in the “Risk Factors” section beginning on page 12 of this prospectus.

| Price to Public |

Underwriting Discounts and Commissions |

Proceeds to Univar Inc. |

Proceeds to Selling Stockholder | |||||

| Per Share |

$ | $ | $ | $ | ||||

| Total |

$ | $ | $ | $ |

The underwriters may also purchase up to an additional shares from the selling stockholder, at the public offering price less underwriting discounts and commissions, within 30 days from the date of this prospectus to cover overallotments, if any.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The shares will be ready for delivery on or about , 2010.

Joint Book-Running Managers

| Goldman, Sachs & Co. | BofA Merrill Lynch |

| Barclays Capital | Deutsche Bank Securities | |||

| J.P. Morgan |

Morgan Stanley |

Prospectus dated , 2010.

Table of Contents

ABOUT THIS PROSPECTUS

You should rely only on the information contained in this prospectus. We are responsible for the information contained in this prospectus. We have not, and the selling stockholder and the underwriters have not, authorized anyone to provide you with information that is different from that contained in this prospectus, and we take no responsibility for any other information that others may give you. We are offering to sell shares of our common stock and seeking offers to buy shares of our common stock only in jurisdictions where offers and sales are permitted. The information in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of our common stock.

Except as otherwise indicated, market data and industry statistics used throughout this prospectus are based on independent industry publications and other publicly available information, including, without limitation, a publicly available industry report published by Boston Consulting Group in January 2010. We do not guarantee, and we have not independently verified, this information. Accordingly, investors should not place undue reliance on this information.

| Page | ||

| 1 | ||

| 12 | ||

| 29 | ||

| 31 | ||

| 32 | ||

| 33 | ||

| 34 | ||

| 35 | ||

| Management’s Discussion and Analysis of Financial Condition and Results of Operations |

38 | |

| 66 | ||

| 70 | ||

| 91 | ||

| 96 | ||

| 107 | ||

| 109 | ||

| 111 | ||

| 114 | ||

| 117 | ||

| Certain United States Tax Consequences to Non-U.S. Holders of Common Stock |

119 | |

| 123 | ||

| 126 | ||

| 130 | ||

| 130 | ||

| 130 | ||

| F-1 |

i

Table of Contents

This summary highlights information contained elsewhere in this prospectus. Before making an investment decision, you should read this entire prospectus carefully, including the section entitled “Risk Factors,” our consolidated financial statements and the related notes included elsewhere in this prospectus. Unless otherwise indicated, the terms “Univar,” the “Company,” “we,” “us,” “our,” “our company” and “our business” refer to Univar Inc. together with its consolidated subsidiaries.

Univar

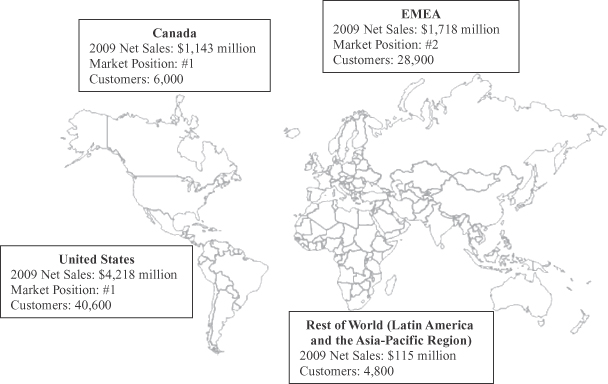

Founded in 1924 and headquartered in Redmond, Washington, we are a leading global distributor of commodity and specialty chemicals. For the year ended December 31, 2009, we generated $7.2 billion in net sales from the distribution of approximately 5.4 million metric tons of chemicals, making us one of the world’s largest independent chemicals distributors, with a #1 market position in both the United States and Canada and a #2 market position in Europe. We operate a network of over 170 distribution facilities in North America, Europe, the Asia-Pacific region and Latin America, with additional sales offices located in Eastern Europe, the Middle East and Africa. We distribute over 11,000 products in more than 110,000 stockkeeping units, or SKUs, to over 80,000 customers with more than 250,000 customer delivery locations in over 100 countries. As we have grown over the last nine decades, we have refined our core competencies in the sales and marketing of chemicals, logistics, product stewardship and technical expertise to become a strategic resource to both our customers and the chemicals producers whose products we distribute.

Our extensive distribution network and comprehensive product portfolio enable us to offer customers a “one-stop shop” solution for their chemicals needs. Our extensive footprint of facilities and transportation assets dedicated to, and licensed and permitted for, the storage and transportation of chemicals in compliance with the extensive and complex safety, health and environmental regulations applicable throughout the regions in which we operate provides us with a competitive advantage. We also provide our customers with access to an industry-focused salesforce and the technical expertise to customize products and services to fit their particular needs. Our ability to offer customers value-added services, such as repackaging, blending and mixing, technical support, labeling, inventory management, “just-in-time” delivery and vendor rationalization programs, has enabled us to build a loyal customer base. We source chemicals from more than 2,500 producers, including many of the premier global chemicals manufacturers. Our scale, geographic reach, diversified distribution channels and industry expertise enable us to develop strong, long-term relationships with our suppliers, allowing us to integrate our service and logistics capabilities into their business processes and to promote collaboration on supply chain optimization, marketing and other revenue enhancement strategies. The producers we work with also benefit from the insight we provide into customer buying patterns and trends. Our scale and close relationships with chemicals producers often enable us to benefit from attractive pricing for our chemicals purchasing.

1

Table of Contents

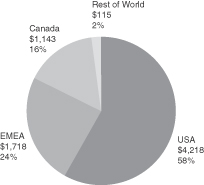

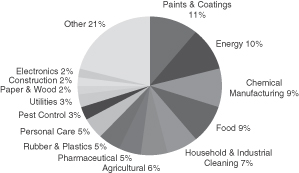

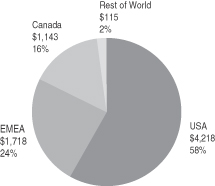

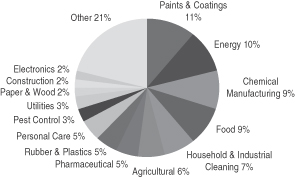

Our business sales strategy is focused on population-driven industries, including paints and coatings, energy, food, household and industrial cleaning, or HIC, pharmaceutical and personal care. We believe that this strategy, combined with our diversity across products, customers, suppliers and geography, allows us to mitigate the effects of volatility on our business in any one region or end market. The following charts illustrate the breakdown of our 2009 net sales to external customers by region and end market:

| 2009 Net Sales by Region (dollars in millions) |

2009 Net Sales by End Market | |||

|

|

Industry Opportunity

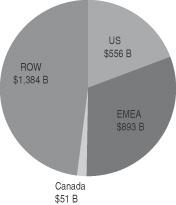

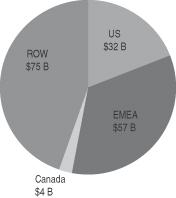

According to an independent study published by the Boston Consulting Group in January 2010, the global chemicals industry represents over $2.9 trillion in annual consumption. Approximately $170 billion of this demand in 2008 was channeled through independent chemicals distributors such as Univar. During the period from 2006 through 2008, our industry grew on average 1.5% per annum greater than the combined rate of growth in industrial output, chemicals consumption and underlying prices.

The chemicals production and distribution industries are both highly fragmented, with more than 100,000 chemicals producers, many of which produce only a limited range of products, and approximately 10,000 independent chemicals distributors, very few of which have a multi-national presence or multi-product sales and distribution capabilities. The 10 largest independent chemicals distributors worldwide comprise less than 25% of the global chemicals distribution market. The U.S. market is relatively less fragmented than Europe, Asia and the rest of the world.

We believe that the trend towards increased outsourcing of chemicals distribution and opportunities for consolidation suggest that independent chemicals distributors will be able to compete for a larger portion of the overall chemicals distribution market in the future and that businesses such as Univar, with our global scale and diverse customer, supplier and product portfolio, are well-positioned to capture a growing share of that market.

2

Table of Contents

Competitive Strengths

As our company has grown, we have continued to refine our business model, developing numerous competitive strengths and core competencies in sales and marketing, logistics, product stewardship and technical expertise, enabling us to become an important resource to both our suppliers and customers and to build and maintain leading market positions in many of the key regions and end markets that we serve. Our competitive strengths include:

| • | Leading global market positions. With $7.2 billion in net sales and 5.4 million metric tons of chemicals distributed in the year ended December 31, 2009, we are one of the world’s leading independent chemicals distribution companies with a #1 market position in both the United States and Canada and a #2 market position in Europe. Our extensive global footprint enables us to serve more than 80,000 customers with over 250,000 customer delivery locations in over 100 countries. We also continue to focus on increasing our market share through organic growth, marketing alliances and strategic acquisitions in established and high-growth emerging markets, such as the Asia-Pacific region and Latin America. |

| • | Extensive global distribution network. We operate one of the most extensive chemicals distribution networks in the world, comprised of over 170 distribution facilities, more than 80 million gallons of storage capacity, nearly 2,400 tractors, tankers and trailers, over 600 railcars, eight rail/barge terminals and six deep sea terminals. This broad footprint enables us to leverage best practices across multiple regions. Our purchasing power allows us to maintain a competitive advantage over local and regional chemicals distributors and efficiently serve customers throughout the world, including difficult to reach areas such as the oil sands regions of Northern Canada. Our global distribution platform also creates significant value for both our suppliers and customers through the combination of our comprehensive inventory, electronic ordering and shipment tracking, “just-in-time” delivery, centralized order handling and fulfillment and access to networked inventory sourcing. |

| • | Established scale and operational efficiencies. We believe that the scale of our global distribution network and the breadth and depth of our product offering and value-added service portfolio provide us with significant operational efficiencies, especially in our established markets. Our geographic reach also offers significant operational efficiencies in areas such as global procurement, purchasing scale and supplier relationships, which often enable us to realize volume-based discounts from our suppliers. As one of the world’s largest independent chemicals distributors, we are able to leverage our cost structure through developed logistical networks by aggregating demand and implementing best practices to operate with increasing efficiency as we expand into new markets. We also benefit from a “hub and spoke” distribution network in many of our markets, providing multiple touchpoints for efficient delivery. |

| • | Long-standing, strong relationships with major chemicals producers. We have developed and continue to cultivate strong, mutually beneficial relationships with more than 2,500 chemicals producers, including BASF, Dow Chemical, Dow Corning, DuPont, Eastman Chemical, ExxonMobil Chemical, LyondellBasell, Mitsubishi and Syngenta. We believe that chemicals producers value our distribution network, product stewardship and industry expertise, as we are able to provide them with more efficient and effective access to smaller customers whose purchasing patterns make them more difficult and costly for producers to serve directly. Our long-standing supplier relationships not only allow us often to purchase chemicals on favorable market terms but also often afford us preferred status, particularly during periods of market dislocation, helping to ensure that we are able to source scarce products from multiple producers. |

3

Table of Contents

| • | Broad product offering and value-added service portfolio. We provide a comprehensive portfolio of over 11,000 products, made up of more than 110,000 SKUs, to customers in a diverse range of industries. We also offer value-added services, including repackaging, blending and mixing chemicals in accordance with customer specifications, and procurement solutions that leverage our chemicals, supply chain and logistics expertise, networked inventory sourcing and supplier relationships. We provide our customers with a “one-stop shop” solution for their commodity and specialty chemicals needs and offer a reliable and stable source of quality products. |

| • | End market and product-specific expertise. Our end market and product-specific expertise enables us to work closely with our customers to identify and select chemicals to enhance the performance characteristics of our customers’ end products. For each of the principal end markets that we serve, we have dedicated teams that are composed of professionals with industry-specific expertise. We also have laboratory facilities that provide formulation support and analytical services for our customers. |

| • | Industry leading marketing supported by highly skilled salesforce. We operate one of the leading sales and marketing efforts in the chemicals distribution industry, focused on providing our customers with both regional and industry expertise. We believe our customers and suppliers value our sales and marketing teams, as we are able to help our suppliers and customers better tailor their product portfolios and purchases by providing them with insight into regional and local end market demand patterns and changing customer product preferences. Our highly trained salesforce of nearly 2,400 professionals has the technical expertise to assist customers in the selection and application of commodity and specialty chemicals for their products and processes. Our experienced product management teams focus on the global market dynamics for some of the higher-volume commodity chemicals that we supply. These teams provide our customers with insight into the key market drivers that impact pricing and availability, which is particularly important to our large purchasers of commodity chemicals whose operations often depend on the price and supply of these products. |

| • | Experienced management team with a proven track record. We are led by a committed and seasoned management team that has, on average, over 25 years of operating experience, including extensive experience in managing public companies. Our team has a proven track record of enhancing shareholder value by controlling costs, identifying and integrating strategic acquisitions and successfully operating throughout various economic cycles, including the recent global recession. John Zillmer, our Chief Executive Officer, has over 30 years of operating experience, most recently in the waste management industry, which, like the chemicals distribution industry, focuses on managing and achieving operational efficiencies in a sophisticated logistics environment. Our core team has successfully implemented sustainable operational initiatives and successfully integrated value-enhancing acquisitions, such as Chemcentral, despite challenging market conditions. |

Growth Strategy

We believe that we are well-positioned to capitalize on industry growth and market opportunities to increase our market share by focusing on expanding our scale and global infrastructure, while at the same time further cultivating our relationships with key suppliers and customers. We intend to capitalize on the growth of the global chemicals and chemicals distribution industries and to continue to implement strategies to improve our operating margins. The key elements of our growth strategy are to:

| • | Enhance offerings in key industry and product areas. We seek to position ourselves as the market leader in select industry and product markets, particularly to customers that produce and sell |

4

Table of Contents

| consumer goods or other population-driven products. Because many of our suppliers and customers look for distributors with specialized industrial or product knowledge, we will continue to strengthen our technical and industry-specific expertise by expanding our product lines and our laboratory and other value-added services to become the preferred distributor for a broader range of chemicals producers and end markets. We also seek to offer our suppliers attractive supplemental distribution channels, such as our ChemPoint business, a leading web-based distributor of specialty and fine chemicals to smaller customers, principally in North America and Europe. |

| • | Leverage scale to capitalize on market opportunities. We intend to leverage our scale to capitalize on market opportunities as major chemicals producers outsource an increasing portion of their distribution operations. We believe that we are well-positioned to capture additional sales volume and grow organically at the expense of smaller competitors as we reinforce our position as a “one-stop” provider of chemicals to customers and related supply chain management services for chemicals producers. Our scale also positions us to target markets and customers that large chemicals manufacturers typically find more difficult and costly to serve. |

| • | Build on long-standing customer relationships to enter new markets. As many of our major customers enter new geographic markets, our long-standing relationships position us well to expand our own footprint to serve their chemicals needs at their new locations and to leverage these strong customer relationships to develop or improve our ties with chemicals manufacturers in these locations. |

| • | Capitalize on shifting of chemicals production to lower-cost and higher growth regions. We intend to capitalize on our extensive geographic footprint and long-standing supplier relationships as our suppliers shift production to lower-cost and higher growth regions. In markets where we have a distribution foothold, we plan to expand our market share by offering these producers access to our existing customer base. As we expand into new geographic markets, we plan to grow through consolidation of smaller regional and local distributors, as well as deepen our existing producer relationships by distributing chemicals from new production locations to customers in established markets. |

| • | Expand and deepen our supplier relationships. We intend to develop and cultivate new and existing long-term relationships with key chemicals producers by using our industry experience and broad geographic footprint to target chemicals producers with substantial logistics and distribution needs. We believe we can strengthen our supplier relationships by demonstrating our ability to reduce their overall costs, risks and operating complexity. We also seek to become better integrated into our existing suppliers’ businesses by identifying opportunities to provide additional value-added services and distribute a larger share of their chemicals production globally. |

| • | Implement further operating margins and operational excellence initiatives. We intend to continue to implement our current initiatives designed to improve operating margins through price discipline and the use of product and customer profitability tools, while also targeting operational excellence and efficiency. Some of these key initiatives include: |

| • | expanding the use of our Economic Contribution Margin, or ECM, tool to identify pricing opportunities and profitability drivers; |

| • | optimizing our global sourcing and supply chain network; |

| • | leveraging our distribution network; |

5

Table of Contents

| • | increasing salesforce efficiency; |

| • | improving sales management, price discipline and implementing additional cost control measures; and |

| • | focusing on working capital improvements through management of terms of sale, collection efforts and inventory management. |

| • | Pursue strategic acquisitions. We intend to pursue strategic acquisitions that complement our organic growth initiatives. Specifically, we seek acquisition opportunities that will: |

| • | strengthen our distribution network in existing markets, such as North America and Western Europe—for example, our 2007 acquisition of Chemcentral allowed us to increase market share and improve operational efficiencies in North America. We believe our pending acquisition of Quaron Group will allow us to expand our regional distribution capabilities in Europe and enable us to improve regional efficiencies; |

| • | expand our geographic footprint by providing us with either the opportunity to extend the reach of our existing distribution network into markets that are contiguous to those we already serve—for example, by taking advantage of our growing network in Western Europe to expand into Central Europe; or |

| • | enable us to establish a presence in new geographic markets, particularly major emerging and rapidly growing markets, such as Brazil, China and India. |

Company History

Our history dates back to 1924 when George Van Waters and Nat Rogers began a brokerage business, buying and selling naval stores, paint, raw materials and cotton linters in the Pacific Northwest region of the United States. The Company progressed into the chemicals distribution business and grew through the West and into the Eastern United States. We entered the Canadian market in 1950. In 1986, we acquired McKesson Chemical, then the third largest U.S. chemicals distributor, solidifying our presence throughout the United States and making us the largest chemicals distributor in North America. In 2001, we continued the expansion of our European operations through the acquisition of Ellis & Everard, which specialized in distribution of chemicals in the United Kingdom and Ireland and had additional facilities in Europe and the Eastern United States. In 2007, we acquired Chemcentral, which enabled us to improve our market share and operational efficiencies in North America.

Univar was a public company listed on the New York Stock Exchange until it was acquired by a Dutch company in 1996. Univar was split off and re-established as an independent company organized under Dutch law in 2002 with its shares listed on Euronext, resuming its position as an independent global leader in chemicals distribution. In 2007, the outstanding shares of our parent and the selling stockholder in this offering, Univar N.V., were acquired by investment funds advised by CVC Capital Partners Advisory (U.S.), Inc., or CVC Capital Partners.

Recent Developments

In February 2010, we entered into an agreement to acquire Quaron Group, a chemicals distributor operating in Belgium, France and The Netherlands, for approximately $130 million in cash, subject to regulatory approvals and other customary closing conditions. With a strong presence in commodity chemicals distribution,

6

Table of Contents

we expect that our acquisition of Quaron Group will complement our strong European position in specialty chemicals, provide significant synergies and help reduce our capital expenditures. We expect to close the transaction in the third quarter of this year.

In connection with this offering, we are amending the terms of our credit facilities described under the headings “Description of Our Indebtedness” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Long-term Debt.”

Risk Factors

Participating in this offering involves substantial risk. Our ability to execute our strategy is subject to certain risks. The risks described under the heading “Risk Factors” immediately following this summary may cause us not to realize the full benefits of our competitive strengths or may cause us to be unable to successfully execute all or part of our growth strategy. Before you participate in this offering, you should carefully consider all the information in this prospectus, including matters set forth under the heading “Risk Factors.”

Principal Stockholders

Our capital stock is indirectly held by Ulysses Luxembourg S.à.r.l., or Ulysses Luxembourg, and Ulysses Finance S.à.r.l., or Ulysses Finance, two Luxembourg private limited liability companies, the capital stock of which is principally held by investment funds advised by CVC Capital Partners. Upon completion of this offering, these stockholders will own beneficially approximately % of our outstanding shares, or % if the underwriters’ overallotment option is exercised in full.

CVC Capital Partners is a leading global private equity firm. It advises funds with committed capital of over $42 billion. Founded in 1981, CVC Capital Partners today has a network of 19 offices throughout Europe, Asia and the United States, and has completed over 250 investments across a wide range of industries and countries.

Our principal executive offices are located at 17425 NE Union Hill Road, Redmond, Washington 98052, and our telephone number at this address is (425) 889-3900. Our website is www.univarcorp.com. Information contained on our website is not part of this prospectus.

“Univar,” “ChemPoint,” “ChemCare” and the Univar logo are trademarks of Univar. All other trademarks appearing in this prospectus are the property of their respective owners.

We operate in an industry in which it is difficult to obtain precise industry and market information. We have obtained some industry data from a publicly available industry report published by Boston Consulting Group in 2010 and other third-party sources that we believe to be reliable. In certain cases we have based certain statements contained in this prospectus regarding our industry and our position in the industry on our estimates concerning our customers and competitors.

7

Table of Contents

The Offering

| Common stock offered by us |

shares |

| Common stock offered by the selling stockholder |

shares |

| Common stock to be outstanding after this offering |

shares |

| Use of proceeds |

We will receive net proceeds from our sale of common stock in this offering of approximately $ million, assuming an initial offering price of $ per share, the mid-point of the range of prices set forth on the cover of this prospectus, after deducting underwriting discounts and commissions and estimated offering expenses payable by us. We intend to use these proceeds to redeem or repay a portion of our outstanding indebtedness described under the headings “Description of Our Indebtedness” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Long-term Debt” and for general corporate purposes. Certain of the underwriters or their affiliates are lenders under or holders of certain of our indebtedness and we intend to use these proceeds to redeem or repay a portion of that outstanding indebtedness. |

We will not receive any of the proceeds from sales of our common stock by the selling stockholder in this offering.

| Risk factors |

Please read “Risk Factors” and other information included in this prospectus for a discussion of factors you should carefully consider before deciding to invest in our common stock. |

| Dividends |

We have not declared or paid cash dividends on our capital stock in our most recent two full fiscal years. We currently expect to retain future earnings, if any, for use in the operation and expansion of our business and do not anticipate paying any cash dividends in the foreseeable future. See “Dividend Policy.” |

| Proposed trading symbol |

“ ” |

The number of shares of common stock to be outstanding after this offering is based on shares outstanding as of , 2010 and excludes any shares to be reserved for issuance under our stock option plans that may be adopted prior to the completion of this offering.

Except as otherwise indicated, all information in this prospectus:

| • | assumes no exercise of the underwriters’ overallotment option; |

| • | assumes the filing of our amended and restated certificate of incorporation and the adoption of our amended and restated bylaws concurrently with the completion of this offering; and |

| • | gives effect to the -for-one stock split of our common stock, which will occur prior to the completion of this offering. |

8

Table of Contents

Summary Consolidated Financial Data

The following summary consolidated financial data should be read together with our consolidated financial statements and the related notes included elsewhere in this prospectus and the discussion under “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” The summary consolidated historical financial data set forth below are not necessarily indicative of the results of future operations. For additional information regarding the below financial data including our use of the terms “predecessor” and “successor,” see “Selected Consolidated Financial Data.”

| Predecessor(1) | Successor(1) | |||||||||||||||||||||||||||||||||

| Years Ended December 31, | Years Ended December 31, |

Three Months Ended March 31, |

||||||||||||||||||||||||||||||||

| (unaudited) | (unaudited) | |||||||||||||||||||||||||||||||||

| 2005 | 2006 | Period from January 1, 2007 to October 11, 2007 |

Period from October 12, 2007 to December 31, 2007 |

2008 | 2009 | 2009 | 2010 | |||||||||||||||||||||||||||

| (in millions) |

||||||||||||||||||||||||||||||||||

| Income Statement Data: |

||||||||||||||||||||||||||||||||||

| Net sales |

$ | 5,987.7 | $ | 6,617.0 | $ | 6,326.9 | $ | 1,790.1 | $ | 9,428.2 | $ | 7,194.5 | $ | 1,791.5 | $ | 1,810.2 | ||||||||||||||||||

| Cost of sales |

5,064.1 | 5,620.2 | 5,441.5 | 1,522.6 | 8,039.2 | 5,985.9 | 1,500.2 | 1,495.6 | ||||||||||||||||||||||||||

| 923.6 | 996.8 | 885.4 | 267.5 | 1,389.0 | 1,208.6 | 291.3 | 314.6 | |||||||||||||||||||||||||||

| Total operating expenses |

715.5 | 761.3 | 713.1 | 237.8 | 1,062.7 | 974.1 | 231.1 | 232.8 | ||||||||||||||||||||||||||

| Operating income |

208.1 | 235.5 | 172.3 | 29.7 | 326.3 | 234.5 | 60.2 | 81.8 | ||||||||||||||||||||||||||

| Other income (expense) |

(27.9 | ) | (31.0 | ) | (58.0 | ) | (37.7 | ) | (315.6 | ) | (307.3 | ) | (76.2 | ) | (73.8 | ) | ||||||||||||||||||

| Income (loss) before income taxes |

180.2 | 204.5 | 114.3 | (8.0 | ) | 10.7 | (72.8 | ) | (16.0 | ) | 8.0 | |||||||||||||||||||||||

| Income tax expense (benefit) |

58.9 | 71.2 | 53.0 | 6.6 | 18.7 | (30.1 | ) | (6.0 | ) | 4.4 | ||||||||||||||||||||||||

| Net income (loss) |

$ | 121.3 | $ | 133.3 | $ | 61.3 | $ | (14.6 | ) | $ | (8.0 | ) | $ | (42.7 | ) | $ | (10.0 | ) | $ | 3.6 | ||||||||||||||

| As of March 31, 2010 | ||||||

| Actual | As adjusted(2) | |||||

| (unaudited) | ||||||

| Balance Sheet Data: |

||||||

| Cash and cash equivalents |

$ | 114.7 | $ | |||

| Total assets |

5,357.3 | |||||

| Working capital(3) |

514.4 | |||||

| Long-term debt |

1,677.1 | |||||

| Total stockholders’ equity |

445.5 | |||||

9

Table of Contents

| Predecessor(1) | Successor (1) | |||||||||||||||||||

| Years Ended December 31, |

Three Months Ended March 31, | |||||||||||||||||||

| Period from January 1, 2007 to October 11, 2007 |

Period from October 12, 2007 to December 31, 2007 |

2008 | 2009 | 2009 | 2010 | |||||||||||||||

| (in millions) | ||||||||||||||||||||

| (unaudited) | ||||||||||||||||||||

| Other Data: |

||||||||||||||||||||

| Adjusted EBITDA(4) |

$ | 252.2 | $ | 80.6 | $ | 498.0 | $ | 427.7 | $ | 92.4 | $ | 118.1 | ||||||||

| Net cash flow from operating activities |

49.8 | 180.8 | 9.4 | 217.4 | 169.4 | 172.8 | ||||||||||||||

| Capital expenditures |

62.6 | 29.1 | 77.5 | 65.9 | 9.6 | 8.3 | ||||||||||||||

| (1) | Predecessor company was acquired on October 11, 2007 by investment funds advised by CVC Capital Partners, a private equity and investment advisory firm. Financial information presented reflects adjustment of assets and liabilities to then-fair value at October 11, 2007, which became the basis for amounts included in results of operations subsequent to October 11, 2007. |

| (2) | As adjusted to give effect to this offering and the application of a portion of the net proceeds therefrom to reduce our outstanding indebtedness. |

| (3) | Current assets, less current liabilities. |

| (4) | We believe that adjusted earnings before interest, income taxes, depreciation and amortization (Adjusted EBITDA) is a useful financial metric to assess our ability to generate cash from operations sufficient to pay taxes, to service debt and to undertake capital expenditures. We also believe that Adjusted EBITDA will provide investors with a useful tool for assessing the comparability between periods of our ability to generate cash from operations sufficient to pay taxes, to service debt and to undertake capital expenditures because, among other things, it eliminates depreciation and amortization expense attributable to our historically higher levels of capital expenditures. We define Adjusted EBITDA as our consolidated net income, plus the sum of: (1) total interest expense, net of interest income; (2) provisions for taxes; (3) depreciation, amortization and goodwill impairment charges; (4) extraordinary losses and unusual or non-recurring charges, including severance costs and relocation costs; (5) expenses incurred in connection with acquisition, investment, recapitalization, disposition and debt or equity issuance transactions; (6) other non-cash charges; and (7) any costs, including cash costs, incurred pursuant to management equity and stock option or other benefit plans; less (1) extraordinary and unusual, non-recurring gains; and (2) non-cash gains. The term Adjusted EBITDA is not defined under U.S. generally accepted accounting principles, or U.S. GAAP, and Adjusted EBITDA is not a measure of operating income, operating performance or liquidity presented in accordance with U.S. GAAP. In addition, Adjusted EBITDA is impacted by reorganization of businesses and other restructuring-related charges. When assessing our operating performance or our liquidity, you should not consider this data in isolation or as a substitute for our net cash from operating activities or other cash flow data that is calculated in accordance with U.S. GAAP. In addition, our Adjusted EBITDA may not be comparable to Adjusted EBITDA or similarly titled measures utilized by other companies since such other companies may not calculate Adjusted EBITDA in the same manner as we do. A reconciliation of net income (loss), the most directly comparable U.S. GAAP measure, to Adjusted EBITDA for each of the respective periods indicated is as follows. |

10

Table of Contents

| Predecessor | Successor | |||||||||||||||||||||||

| Years Ended December 31, |

Three Months Ended March 31, | |||||||||||||||||||||||

| Period from January 1, 2007 to October 11, 2007 |

Period

from October 12, 2007 to December 31, 2007 |

2008 | 2009 | 2009 | 2010 | |||||||||||||||||||

| (in millions) | ||||||||||||||||||||||||

| (unaudited) | ||||||||||||||||||||||||

| Net income (loss) |

$ | 61.3 | $ | (14.6 | ) | $ | (8.0 | ) | $ | (42.7 | ) | $ | (10.0 | ) | $ | 3.6 | ||||||||

| Provision (benefit) for income taxes |

53.0 | 6.6 | 18.7 | (30.1 | ) | (6.0 | ) | 4.4 | ||||||||||||||||

| Interest expense, net |

58.0 | 69.0 | 315.6 | 307.3 | 76.2 | 73.8 | ||||||||||||||||||

| Depreciation |

48.3 | 16.8 | 81.6 | 80.1 | 19.1 | 20.1 | ||||||||||||||||||

| Amortization |

5.6 | 10.9 | 50.8 | 46.3 | 12.0 | 11.2 | ||||||||||||||||||

| Extraordinary losses and unusual or non-recurring charges |

26.0 | 23.2 | 39.3 | 29.6 | 1.1 | — | ||||||||||||||||||

| Expenses incurred for acquisition, investment, recapitalization and disposition |

— | — | — | 1.2 | — | 1.4 | ||||||||||||||||||

| Other non-cash charges reducing net income |

— | — | — | 36.0 | — | 3.6 | ||||||||||||||||||

| Extraordinary gain and unusual or non-recurring gains |

— | (31.3 | ) | — | — | — | — | |||||||||||||||||

| Adjusted EBITDA |

$ | 252.2 | $ | 80.6 | $ | 498.0 | $ | 427.7 | $ | 92.4 | $ | 118.1 | ||||||||||||

11

Table of Contents

The purchase of our common stock involves significant investment risks, some of which are described below. You should consider the risks carefully before investing in our common stock. There may also be risks of which we are currently unaware, or that we currently regard as immaterial based on the information available to us, that later prove to be material. These risks may adversely affect our business, financial condition and operating results. As a result, the trading price of our common stock could decline, and you could lose some or all of your investment.

Risks Related to Our Business

We are affected by general economic conditions, particularly fluctuations in industrial production; and prolonged economic weakening could adversely affect our operations and financial results.

We are a leading global distributor of commodity and specialty chemicals. We sell chemicals that are used principally in industrial and manufacturing processes and our sales are correlated with and affected by fluctuations in the level of industrial production and manufacturing output and general economic activity. In particular, our suppliers, producers of commodity and specialty chemicals, are likely to reduce their output in periods of significant contraction in industrial and consumer demand, while demand for the products we distribute depends largely on trends in demand in the end markets that our customers serve, including consumer goods, as we seek to focus on chemicals sales to customers that produce and sell population driven products. A majority of our sales are in North America and Europe and our business is therefore susceptible to downturns in those economies as well as, to a lesser extent, the economies in the rest of the world. Our profit margins, as well as overall demand for our products, could decline as a result of a large number of factors outside our control, including economic recessions, changes in industrial production processes or consumer preferences, changes in laws and regulations affecting the chemicals industry and the manner in which they are enforced, inflation, fluctuations in interest and currency exchange rates and changes in the fiscal or monetary policies of governments in the areas in which we operate.

General economic conditions and macroeconomic trends could affect overall demand for chemicals, as well as the creditworthiness of our customers. Any overall decline in the demand for chemicals could significantly reduce our sales and profitability. If the creditworthiness of our customers declines, we would face increased credit risk with respect to our trade receivables. In addition, volatility and disruption in financial markets could adversely affect our sales and results of operations by limiting our customers’ ability to obtain financing necessary to maintain or expand their own operations.

Over the past two years, significant economic weakness has affected all regions of the world and all business sectors, especially industrial and manufacturing output. One feature of this economic weakness has been significant destocking of inventories, including inventories of chemicals used in industrial and manufacturing processes. Adverse economic conditions contributed to a 23.7% reduction in our net sales from 2008 to 2009 that was due in large part to lower sales volumes. Our customers reduced purchases because of lower demand from end users as well as inventory destocking. Although there have recently been signs of recovery in many regions, economic weakness could continue or worsen, as has occurred in certain regions of Europe due to concerns over the fiscal and monetary situation in a number of countries, including Greece, Portugal and Spain. The industrial and manufacturing end markets on which we depend may not return to former, higher levels of production in the near term or at all. In addition, it is possible that an improvement in our net sales in a particular period may be attributable in part to restocking of inventories by our customers and represent a level of sales or sales growth that will not be sustainable over the longer term. Further economic weakness could lead to insolvencies among our customers or our suppliers, as well as among financial institutions that are counterparties on financial instruments or accounts that we hold. Any of these developments could have a material adverse effect on our business, financial condition and results of operations.

12

Table of Contents

Disruptions in the supply of chemicals that we distribute or in the operations of our customers could adversely affect our business.

Our business depends on access to adequate supplies of the chemicals that our customers purchase from us. From time to time, we may be unable to access adequate quantities of certain chemicals because of supply disruptions due to natural disasters (including hurricanes and other extreme weather), industrial accidents, scheduled production outages, high demand leading to allocation, port closures and other transportation disruptions and other circumstances beyond our control, or we may be unable to purchase chemicals that we are obligated to deliver to our customers at prices that enable us to earn a profit. In addition, unpredictable events may have a significant impact on the industries in which many of our customers operate, reducing demand for products that we normally distribute in significant volumes. For example, the Gulf of Mexico oil disaster has had a major impact on our customers that manufacture and operate offshore drilling equipment. Significant disruptions of supply and in customer industries could have a material adverse effect on our business, financial condition and results of operations.

In 2005 and 2008, major hurricanes caused significant disruptions in operations of several of our suppliers and customers on the U.S. Gulf Coast, logistics across the region and the supply of certain raw materials, all of which had an adverse impact on the demand for and cost of some of the chemicals products we sell. In addition, adverse weather events may affect our distribution facilities, in particular at deep water ports. Future significant weather related events could negatively affect our results of operations.

Significant changes in the business strategies of our suppliers could also disrupt our supply. Large chemicals manufacturers may elect to distribute certain products (or products in certain regions) directly to end user customers, instead of relying on independent distributors such as us. While we do not believe that our results depend materially on access to any individual producer’s products, a reversal of the trend toward more outsourced distribution of chemicals would likely result in increasing margin pressure or products becoming unavailable to us. Any of these developments could have a material adverse effect on our business, financial condition and results of operations.

To the extent we have contracts with suppliers and customers, they are generally short term or terminable upon notice, and termination of our relationships with suppliers and customers contracts could negatively affect our business.

Our purchases and sales of chemicals are typically made pursuant to purchase orders rather than long-term contracts. While some of our relationships for the distribution and sale of specialty chemicals have exclusivity provisions, we may be unable to enforce these provisions effectively for legal or business reasons. Many of our contracts with both customers and suppliers are terminable without cause upon 30 days’ notice to us from the supplier or customer. Our business relationships and reputation may suffer if we are unable to meet our delivery obligations to customers which may occur because many of our suppliers are not subject to contracts or can terminate contracts on short notice. In addition, renegotiation of purchase or sales terms to our disadvantage could reduce our sales margins. Any of these developments could adversely affect our business, financial condition and results of operations.

We might not be able to pass through cost increases to our customers. We could experience financial losses if our inventories of one or more chemicals exceed our sales and the price of those chemicals decreases significantly or if they fall short of our sales and the purchase price of those chemicals increases significantly. In addition, we could lose customers and suffer damage to our reputation if we are unable to meet customer demand for a particular product.

We purchase and sell a wide variety of chemicals, the price and availability of which may fluctuate. Our business is exposed to these fluctuations, as well as to fluctuations in our costs for transportation and distribution due to rising fuel prices or increases in charges from common carriers, rail companies and other third-party

13

Table of Contents

transportation providers, as well as other factors. We have in the past generally been able to pass on chemicals and transportation price increases to our customers. Nevertheless, changes in chemicals prices affect our net sales and cost of goods sold, as well as our working capital requirements, levels of debt and financing costs. We might not always be able to reflect increases in our chemicals, transportation and other costs in our own pricing. Any inability to pass cost increases onto customers may adversely affect our business, financial condition and results of operations.

In order to meet customer demand, we typically maintain significant inventories and are therefore subject to a number of risks associated with our inventory levels, including the following:

| • | declines in the prices of chemicals; |

| • | the need to maintain significant inventory of chemicals that may be in limited supply and therefore difficult to procure; |

| • | buying chemicals in bulk for the best pricing; |

| • | responding to the unpredictable demand for chemicals; |

| • | cancellation of customer orders; and |

| • | responding to customer requests for quick delivery. |

In order to manage our inventories successfully, we must estimate demand from our customers and purchase chemicals on a regional basis that substantially corresponds to that demand. If we overestimate demand and purchase too much of a particular chemical, we face a risk that the price of that chemical will fall, leaving us with inventory that we cannot sell profitably and that we may have to write down if we are unable to sell it for its recorded value. If we underestimate demand and purchase insufficient quantities of a particular chemical and prices of that chemical rise, we could be forced to purchase that chemical at a higher price and forego profitability in order to meet customer demand. Our business, financial condition and results of operations could suffer a material adverse effect if either or both of these situations occur frequently or in large volumes.

We also face the risk of dissatisfied customers and damage to our reputation if we cannot meet customer demand for a particular chemical because we are short on inventories. In addition, particularly in cases of pronounced cyclicality in the end market, it can be difficult to anticipate our customers’ requirements for particular chemicals, and we could be asked to deliver larger-than-expected quantities of a particular chemical on short notice. If for any reason we experience widespread, systemic difficulties in filling customer orders, our customers may be dissatisfied and discontinue their relationship with us or we may be required to pay a higher price in order to obtain the needed chemical on short notice, thereby adversely affecting our margins.

We have in the past and intend in the future to make acquisitions and strategic investments, which will involve numerous risks. We may not be able to address these risks without substantial expense, delay or other operational or financial problems.

Part of our strategy is to acquire or make investments in related businesses. Acquisitions or investments involve various risks, such as:

| • | integrating the operations and personnel of any acquired business; |

| • | the potential disruption of our ongoing business, including the diversion of management attention; |

| • | the possible inability to obtain the desired financial and strategic benefits from the acquisition or investment; |

14

Table of Contents

| • | customer attrition arising from preferences to maintain redundant sources of supply; |

| • | assumption of contingent or unanticipated liabilities; |

| • | dependence on the retention and performance of existing management and work force of acquired businesses for the future performance of these businesses; and |

| • | the risks inherent in entering geographic or product markets in which we have limited prior experience. |

Future acquisitions and investments would likely need to be financed in part through additional financing from banks, through public offerings or private placements of debt or equity securities or other arrangements, and could result in substantial cash expenditures. The necessary acquisition financing may not be available to us on acceptable terms if and when required, particularly because our current high leverage may make it difficult or impossible for us to secure additional financing for acquisitions. We may also finance an acquisition by issuing equity securities or equity-linked securities that may have a dilutive effect on our stockholders.

To the extent that we make acquisitions that result in our recording significant goodwill or other intangible assets, the requirement to review goodwill and other intangible assets for impairment periodically may result in impairments that could have a material adverse effect on our financial condition and results of operations.

In connection with acquisitions or divestitures, we may inadvertently become subject to liabilities.

In connection with any acquisitions, we may acquire liabilities or defects such as legal claims, including but not limited to third-party liability and other tort claims; claims for breach of contract; employment-related claims; environmental liabilities, conditions or damage; hazardous materials or liability for hazardous materials; or tax liabilities. If we acquire any of these liabilities, and they are not adequately covered by insurance or an enforceable indemnity or similar agreement from a creditworthy counterparty, we may be responsible for significant out-of-pocket expenditures. These liabilities, if they materialize, could have a material adverse effect on our business, financial condition and results of operations.

We generate a significant portion of our net sales internationally and intend to continue to expand our international operations. We face particular challenges in emerging markets. Our results of operations could suffer if we are unable to manage our international operations effectively or as a result of various risks beyond our control.

During the year ended December 31, 2009, over 40% of our net sales were generated outside of the United States. We intend to continue to expand our penetration in certain foreign markets and to enter new foreign markets. Expansion of our international business will require significant management attention and resources. The profitability of our international operations will largely depend on our continued success in the following areas:

| • | securing key supplier relationships to help establish our presence in international markets; |

| • | hiring and training personnel capable of supporting our suppliers and customers and managing operations in foreign countries; |

| • | localizing our business processes to meet the specific needs and preferences of foreign suppliers and customers, which may differ in certain respects from our experience in the United States; |

| • | building our reputation and awareness of our services among foreign suppliers and customers; and |

15

Table of Contents

| • | implementing new financial, management information and operational systems, procedures and controls to monitor our operations in new markets effectively, without causing undue disruptions to our operations and customer relationships. |

In addition, we are subject to risks associated with operating in foreign countries, including:

| • | varying and often unclear legal and regulatory requirements that may be subject to inconsistent or disparate enforcement, particularly regarding environmental issues and security or other certification requirements, as well as other laws and business practices that favor local competitors, such as exposure to possible expropriation, nationalization, restrictions on investments by foreign companies or other governmental actions; |

| • | competition from existing market participants that may have a longer history in and greater familiarity with the foreign markets where we operate; |

| • | tariffs, export duties, quotas and other barriers to trade; as well as possible limitations on the conversion of foreign currencies into U.S. dollars or remittance of dividends and other payments by our foreign subsidiaries; |

| • | divergent labor regulations and cultural expectations regarding employment; |

| • | different cultural expectations regarding industrialization, international business and business relationships; |

| • | foreign taxes and related regulations, including foreign taxes that we may not be able to offset against taxes imposed upon us in the United States, and foreign tax and other laws limiting our ability to repatriate earnings to the United States; |

| • | extended payment terms and challenges in our ability to collect accounts receivable; and |

| • | changes in a specific country’s or region’s political or economic conditions. |

If we fail to address the challenges and risks associated with international expansion, we may encounter difficulties implementing our strategy, thereby impeding our growth and harming our operating results.

Our operations in the Asia-Pacific region and Latin America are at an early stage, and it may prove difficult to achieve our goals and take advantage of growth and acquisition opportunities in those or in other emerging markets due to a lack of comprehensive market knowledge and network and legal restrictions and other factors that often characterize emerging markets, such as significant government influence over local economies, substantial fluctuations in economic growth, high levels of inflation and volatility in currency values, exchange controls or restrictions on expatriation of earnings, high domestic interest rates, wage and price controls, changes in governmental economic or tax policies, imposition of trade barriers, unexpected changes in regulation, and overall political social and economic instability. In addition, the heightened exposure to terrorist attacks against or acts of war or civil unrest involving our facilities, if they occur, could result in damage to our facilities, substantial financial losses or injuries to our personnel.

Our operations are generally structured in a decentralized manner. Although we exercise what we believe to be an appropriate level of central control and active supervision of our operations around the world, our local subsidiaries retain significant operational flexibility. There is a risk that our operations around the world will experience problems that could damage our reputation, or that could otherwise have a material adverse effect on our business, financial condition and results of operations.

16

Table of Contents

Fluctuations in currency exchange rates may adversely affect our results of operations.

We sell products in over 100 countries and we generated over 40% of our 2009 net sales outside the United States. The revenues we receive from such foreign sales are often denominated in currencies other than the U.S. dollar. We enter into forward currency exchange contracts and other arrangements intended to hedge virtually all of our transactional exposure to adverse fluctuations in exchange rates with respect to our purchases and sales of inventory. Nevertheless, these arrangements may not always be effective, particularly in the context of sudden, severe or unexpected market movements. We do not hedge our foreign currency exposure with respect to our investment in and earnings from our foreign businesses. Accordingly, we might suffer significant losses if there is a significant adverse movement in exchange rates.

In addition, we report our consolidated results in U.S. dollars. The results of operations and the financial position of our local operations are generally reported in the relevant local currencies and then translated into U.S. dollars at the applicable exchange rates for inclusion in our consolidated financial statements, exposing us to currency translation risk. Consequently, any change in exchange rates between our foreign subsidiaries’ functional currencies and the U.S. dollar will affect our consolidated income statement and balance sheet when the results of those operating companies are translated into U.S. dollars for reporting purposes. Decreases in the value of our foreign subsidiaries’ functional currencies against the U.S. dollar will tend to reduce those operating companies’ contributions in dollar terms to our financial condition and results of operations. In 2009, our most significant currency exposures were to the euro, the Canadian dollar and the British pound sterling versus the U.S. dollar. The exchange rates between these and other foreign currencies and the U.S. dollar may fluctuate substantially, and such fluctuations have had a significant effect on our results in recent periods. For additional details on our currency exposure and risk management practices, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “—Quantitative and Qualitative Disclosures about Market Risk—Foreign currency risk.”

The markets in which we compete are highly competitive.

The markets for the chemicals we sell and distribute are highly competitive. Chemicals can be purchased from a variety of sources, including traders, brokers, wholesalers and other distributors, as well as directly from producers. Many of the products we distribute are made to industry standard specifications, and are essentially fungible with products offered by our competition. The competitive pressure we face is particularly strong in sectors and markets where local competitors have strong positions. Increased competition from distributors of products similar to or competitive with ours could result in price reductions, reduced margins and a loss of market share.

We expect to continue to experience significant and increasing levels of competition in the future. We must also compete with smaller companies that have been able to develop strong local or regional customer bases. In certain countries, some of our competitors are more established, benefit from greater name recognition and have greater resources within these countries than we do.

We rely on our computer and data processing systems, and a large-scale malfunction could disrupt our business.

Our ability to keep our business operating effectively depends on the functional and efficient operation of our enterprise resource planning and telecommunications systems, including our inventory tracking and billing systems. We rely on these systems to track transactions, billings, payments and inventory, as well as to make a variety of day-to-day business decisions. Our systems are susceptible to malfunctions and interruptions (including due to equipment damage, power outages, computer viruses and a range of other hardware, software and network problems) and we may experience such malfunctions or interruptions in the future. Although our systems are diversified, including multiple server locations and a range of software applications for different regions and functions, a significant or large-scale malfunction or interruption of our computer or data processing

17

Table of Contents

systems could adversely affect our ability to manage and keep our operations running efficiently, and damage our reputation if we are unable to track transactions and deliver products to our customers. A malfunction that results in a wider or sustained disruption to our business could have a material adverse effect on our business, financial condition and results of operations.

Our implementation of our enterprise resource planning project in Europe may cause interruptions in our business or impact our internal controls.

We are proceeding with a project to implement our enterprise resource planning, or ERP, system throughout our European operations. Implementation of the project carries a number of risks, including the risk of interruptions of our business activities such as ordinary sales, delivery and billing that would have an adverse impact on our business, financial condition and results of operations. In addition, we may need to modify or redesign our current internal controls to support implementation and operation of our ERP system. Deficiencies may occur in the design or operation of our internal control over financial reporting that could lead to a material weakness in our internal control over financial reporting.

We depend on transportation assets, some of which we do not own, in order to deliver products to our customers.

Although we maintain a significant portfolio of owned and leased transportation assets in North America, including trucks, trailers, railcars and barges, we also rely on transportation provided by third parties (including common carriers and rail companies) to deliver products to our customers, particularly outside the United States and Canada. Our access to third-party transportation is not guaranteed, and we may be unable to transport chemicals at economically attractive rates in certain circumstances, particularly in cases of adverse market conditions or disruptions to transportation infrastructure. We are also subject to increased costs that we may not always be able to recover from our customers, including rising fuel prices, as well as increases in the charges imposed by common carriers, leasing companies and other third parties involved in transportation. In particular, our U.S. operations rely to a significant extent on rail shipments, and we are therefore required to pay rail companies’ network access fees, which have increased significantly in recent periods, while bulk shipping rates have also recently been highly volatile. We are also subject to the risks normally associated with product delivery, including inclement weather, disruptions in the transportation infrastructure, disruptions in our lease arrangements and the availability of fuel, as well as liabilities arising from accidents to the extent we are not adequately covered by insurance. Our failure to deliver products in a timely and accurate manner could harm our reputation and brand, which could adversely affect our business, financial condition and results of operations.

Our business exposes us to significant risks associated with hazardous substances and activities, not of all which are covered by insurance.

Because we are engaged in the handling, storing, treating, selling and transporting of chemicals and chemical waste products, many of which are hazardous materials, product liability, health, fire damage, safety and environmental risks are a significant concern for us. We are also subject to federal legislation enforced by the Occupational Safety and Health Administration, or OSHA, as well as present and future claims with respect to workplace exposure; exposure of contractors on our premises, as well as other persons located nearby; workers’ compensation and other matters. We carry insurance to protect us against many accident-related risks involved in the conduct of our business and we maintain environmental damage and pollution insurance coverage in accordance with our assessment of the risks involved or ability to bear those risks and the cost and availability of insurance. Each of these insurance policies is subject to customary exclusions, deductibles and coverage limits that we believe are generally in accordance with industry standards and practices. We do not insure against all risks and may not be able to insure adequately against certain risks (whether relating to our activities or other matters) and may not have insurance coverage that will pay any particular claim. We also may be unable to obtain adequate insurance coverage for the risks we currently insure at commercially reasonable rates in the future, and certain risks could become completely uninsurable or eligible for coverage only to a reduced extent.

18

Table of Contents

In particular, more stringent environmental or safety and health regulations may increase our costs for, or impact the availability of, insurance against the risks of environmental damage or pollution. Our business, financial condition and results of operations could be materially impaired by accidents that substantially reduce our revenues, increase our costs or subject us to other liabilities in excess of available insurance.

Accidents, environmental damage, major or systemic delivery failures involving our distribution network or the products we carry, or adverse health effects or other harm related to hazardous materials that we carry or store could damage our reputation and result in substantial remedial obligations.

Our business depends to a significant extent on our customers’ and suppliers’ trust in our reputation for quality, safety and environmental responsibility. Actual or alleged instances of safety deficiencies, inferior product quality, exposure to hazardous materials resulting in illness, injury or other harm to persons or property, or of environmental damage caused by us or our products, could damage our reputation and lead to customers and suppliers curtailing the volume of business they do with us. Any of these events, outcomes or allegations could also subject us to substantial legal claims, and we could incur substantial expenses, including legal fees and other costs, in defending such legal claims.

Actual or alleged accidents or other incidents at our facilities or that otherwise involve our personnel or operations could also subject us to claims for damages by third parties. Because many of the chemicals that we handle, such as chlorine gas, are dangerous, we are subject to the ongoing risk of hazards, including explosions and fires that may cause property damage, illness, physical injury or death. Several of our distribution facilities, including our Los Angeles facility, one of our largest, are located relatively near high-density population centers. If such events occur, whether through our own fault, through preexisting conditions at our facilities, through the fault of a third party, or through a natural disaster, terrorist incident or other event outside our control, our reputation could be damaged significantly. We could also become responsible, as a result of environmental or other laws or by court order, for substantial monetary damages or expensive remedial obligations related to such accidents, including but not limited to those resulting from third-party lawsuits or environmental clean-up obligations on and off-site. The amount of any costs, including fines, damages and/or remedial obligations, that we may become obligated to pay under such circumstances could substantially exceed any insurance we have to cover such losses.

We depend to a significant extent on our customers’ and suppliers’ trust in our reputation for reliability, quality, safety and environmental responsibility. Actual or alleged safety deficiencies or inferior product quality, late delivery, or damage caused by us or our products, could damage our reputation and could lead to customers and suppliers curtailing the volume of business they do with us. Any of these risks, if they materialize, could significantly harm our reputation, expose us to substantial liabilities and have a material adverse effect on our business, financial condition and results of operations.

We are subject to extensive environmental, health and safety laws and regulations. Changes in these laws and regulations or in their interpretation could hurt our business by increasing our costs of doing business and reducing our profitability.

Because we store, handle, transport and arrange for the disposal of chemicals and waste materials, we are subject to extensive environmental, health and safety laws and regulations in multiple jurisdictions. These include laws and regulations governing our management, storage and transportation of chemicals; air, water and ground contamination; and the cleanup of contaminated sites, including any spills that may result from our transportation of chemicals. Aspects of our business require that we hold a number of permits and licenses. Compliance with these laws, regulations, permits and licenses requires that we expend significant amounts for ongoing compliance and remediation. If we fail to comply with such laws or regulations we may be subject to fines and other civil, administrative or criminal sanctions, including the revocation of permits and licenses necessary to continue our business activities. In addition, we may be required to pay damages or civil judgments in respect of third-party claims, including those relating to personal injury (including exposure to hazardous

19

Table of Contents

substances we store, handle, transport or dispose of), property damage or contribution to remedial obligations. Some environmental laws could impose on us the entire cost of clean-up of contamination present at a site even though we did not cause the contamination. These laws often identify parties that can be jointly and severally liable for remediation, regardless of fault or whether the original activity was legal at the time it occurred. We may be identified as a potentially responsible party with regard to additional sites beyond those for which we already have remedial obligations. Such developments could have a material adverse effect on our business, financial condition and results of operations. See “Business—Regulatory Matters—Environmental Matters.”

We believe that we comply in all material respects with applicable environmental laws and regulations. We have health and safety management programs in place to monitor compliance with applicable regulatory requirements and with internal policies and procedures, as appropriate. Previous operations (including those of acquired companies), however, carried out under then prevailing standards may have resulted in contamination at various sites, which must be remediated. In addition, we are subject to environmental liabilities for a share of remediation expenses required to address contamination of third-party sites. We have spent substantial sums on such remediation and we expect to continue to incur such expenditures in the future, which we have incorporated into our environmental accruals. Based on current estimates, we believe that none of these ongoing remediation costs will materially affect our business. There is no guarantee, however, that our estimates will be accurate, that new contamination will not be discovered or that new environmental laws or regulations will not require us to incur additional costs. Any such inaccuracies, discoveries or new laws or regulations could have a material adverse effect on our business, financial condition and results of operations. We also may incur substantial costs, including fines, damages, criminal or civil sanctions and remediation costs, or experience interruptions in our operations for violations under environmental, health and safety laws or permit requirements.