Attached files

Table of Contents

As filed with the Securities and Exchange Commission on June 30, 2010

Registration Statement No. 333-165554

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 3

to

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

The Telx Group, Inc.

(Exact name of Registrant as specified in its charter)

| Delaware | 4899 | 13-4129783 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

1 State Street, 21st Floor

New York, NY 10004

(212) 480-3300

(Address, including zip code, and telephone number, including area code, of Registrants’ principal executive offices)

Eric Shepcaro

Chief Executive Officer

The Telx Group, Inc.

1 State Street, 21st Floor

New York, NY 10004

(212) 480-3300

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| Michael L. Zuppone, Esquire Paul, Hastings, Janofsky & Walker, LLP 75 East 55th Street New York, New York 10022 (212) 318-6000 Facsimile: (212) 319-4090 |

William P. Rogers, Jr., Esquire 825 Eighth Avenue New York, New York 10019 (212) 474-1000 Facsimile: (212) 474-3700 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this form are being offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If delivery of the prospectus is expected to be made pursuant to Rule 434, check the following box. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ¨ | Accelerated filer ¨ | |||||

| Non-accelerated filer x | (Do not check if a smaller reporting company) | Smaller reporting company ¨ |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. We and the selling stockholders may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED JUNE 30, 2010

Shares

Common Stock

This is the initial public offering of shares of common stock of The Telx Group, Inc.

We are selling shares of our common stock and the selling stockholders are selling shares of our common stock. We will not receive any of the proceeds from the shares of common stock sold by the selling stockholders.

Prior to this offering, there has been no public market for our common stock. The initial public offering price of our common stock is expected to be between $ and $ per share. We have applied to list our common stock on The Nasdaq Global Market under the symbol “TELX.”

See the section entitled “Risk Factors” beginning on page 10 to read about factors you should consider before buying shares of our common stock.

| Per Share |

Total | |||

| Initial public offering price |

||||

| Underwriting discounts and commissions |

||||

| Proceeds, before expenses, to the company |

||||

| Proceeds, before expenses, to the selling stockholders |

The underwriters have an option to purchase a maximum of additional shares of our common stock from us and/or the selling stockholders at the initial public offering price less the underwriting discounts and commissions.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares against payment in New York, New York on , 2010.

| Goldman, Sachs & Co. | Deutsche Bank Securities |

| RBC Capital Markets | ||||

| Oppenheimer & Co. | Piper Jaffray | SunTrust Robinson Humphrey | ||

The date of this prospectus is , 2010.

Table of Contents

Table of Contents

| Page | ||

| 1 | ||

| 10 | ||

| 27 | ||

| 29 | ||

| 30 | ||

| 31 | ||

| 33 | ||

| 35 | ||

| Management’s Discussion and Analysis of Financial Condition and Results of Operations |

37 | |

| 68 | ||

| 84 | ||

| 90 | ||

| 106 | ||

| 110 | ||

| 112 | ||

| 116 | ||

| 118 | ||

| 120 | ||

| 125 | ||

| 129 | ||

| 129 | ||

| 129 | ||

| F-1 |

Through and including , 2010 (the 25th day after the date of this prospectus), all dealers effecting transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to a dealer’s obligation to deliver a prospectus when acting as an underwriter and with respect to an unsold allotment or subscription.

We have not authorized anyone to provide any information or to make any representations other than those contained in this prospectus. We take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. This prospectus is an offer to sell only the shares offered hereby, but only under circumstances and in jurisdictions where it is lawful to do so. The information contained in this prospectus is current only as of its date.

Market data and industry statistics and forecasts used throughout this prospectus are based on independent industry publications, reports by market research firms and other published independent sources. Tier1 Research, Cisco, Gartner, The Insight Research Corporation, the U.S. Census and Nemertes Research are the primary sources for third-party market data and industry statistics and forecasts. Some data and other information are also based on our good faith estimates, which are derived from our review of internal surveys and independent sources. Although we believe these sources are credible, we have not independently verified the data or information obtained from these sources.

The Gartner reports described herein (the “Gartner Reports”) represent data, research opinion or viewpoints published, as part of a syndicated subscription service by Gartner, Inc. (“Gartner”), and are not representations of fact. Each Gartner Report speaks as of its original publication date (and not as of the date of this prospectus) and the opinions expressed in the Gartner Reports are subject to change without notice.

Table of Contents

This summary highlights certain information contained elsewhere in this prospectus. This summary does not contain all of the information you should consider before investing in our common stock. You should carefully read the entire prospectus, including the section entitled “Risk Factors” and our financial statements and related notes, before you decide whether to invest in our common stock. If you invest in our common stock, you are assuming a high degree of risk. See the section entitled “Risk Factors.” References to “we,” “our,” “our company,” “us,” “the company,” “Telx,” or “The Telx Group, Inc.” refer to The Telx Group, Inc. and its consolidated subsidiaries. References to “GI Partners Funds” refer to GI Partners Fund II, L.P. and GI Partners Side Fund II, L.P., collectively and references to “GI Partners” refer to the entities that control or manage the GI Partners Funds. Unless otherwise indicated, industry data are derived from publicly available sources, which we have not independently verified.

Business Overview

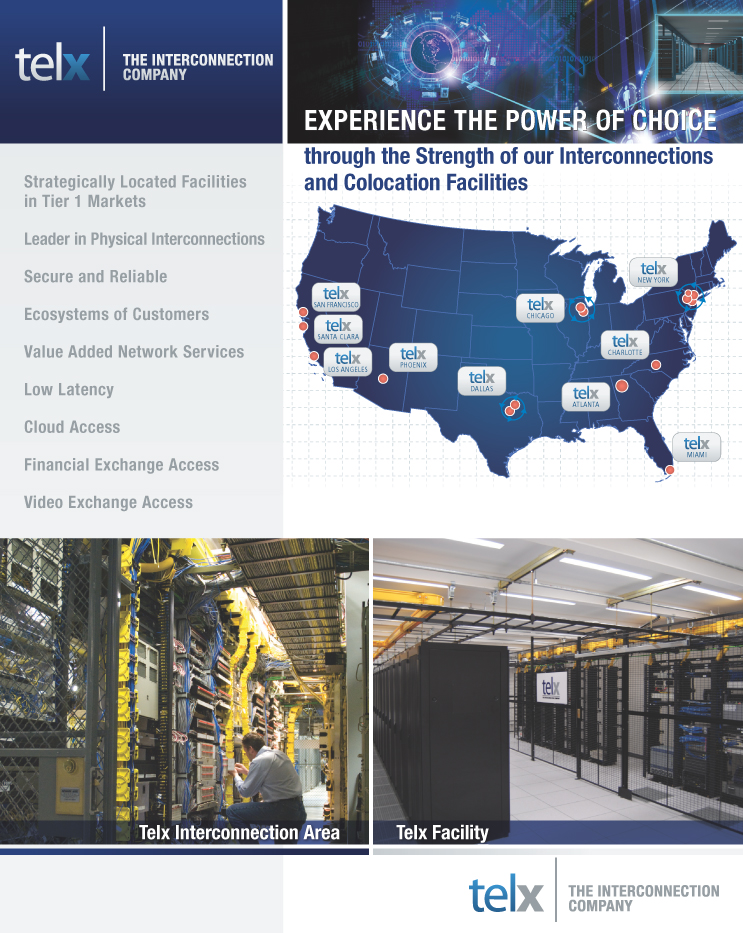

Telx is a leading provider of network neutral, global interconnection and colocation solutions in the United States. Our interconnection and colocation offerings enable customers to seamlessly connect to hundreds of diverse communications networks and other enterprises. Additionally, we provide a secure and reliable environment to house customers’ mission-critical equipment and time sensitive data. We believe that our 15 facilities, located in nine tier-1 markets, are some of the most strategically positioned datacenters in the United States. These facilities are located at the primary intersections of multiple, major international and domestic fiber routes where we believe Internet and private network traffic is most concentrated and interconnection demand is highest. We believe that our average of 36 physical interconnections per customer as of March 31, 2010 gives us greater physical interconnection density than our competitors. Over the last two years, we have grown our revenues from $50.8 million in 2007 to $98.3 million in 2009, representing a compound annual growth rate of 39%, and our net losses have decreased from $36.4 million to $9.9 million over the same period. For the three months ended March 31, 2010, we had revenues of $29.7 million and net income of $1.7 million.

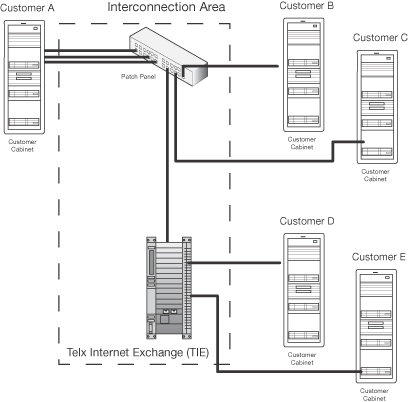

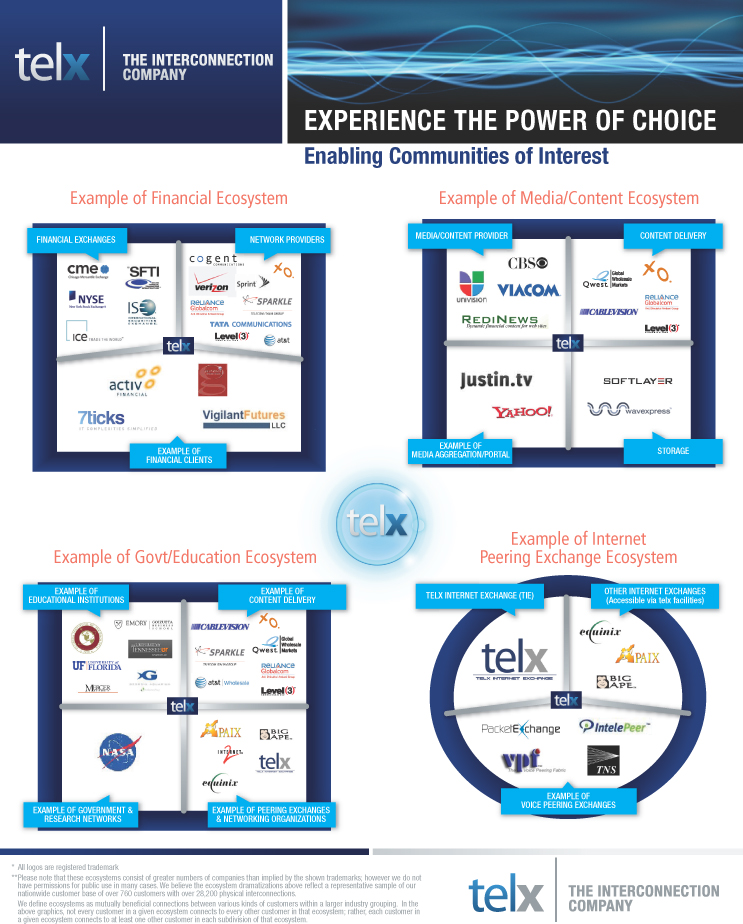

As a network neutral provider, we are an unbiased intermediary that provides the necessary interconnection products and related services that facilitate the exchange of communications network traffic between our customers. Customers within a Telx facility are able to connect to any other customer within the facility, including up to 300 communications service providers, depending on the facility. These interconnections effectively allow a customer to replace their existing and more expensive network alternatives. Through these interconnections, our facilities host diverse and densely populated ecosystems of communications service providers, enterprises, online media, video and content providers, and other entities. We view an ecosystem as a set of related businesses and organizations that use our facilities to exchange information with each other. For example, a financial ecosystem can consist of financial exchanges, financial clients and information exchanges that exchange large volumes of real-time financial market data. Our customers benefit from greater choice of networks, reduced network costs, improved capital budget efficiency, improved performance and access to revenue opportunities with accelerated time to market.

1

Table of Contents

With 804 customers and 29,324 total physical interconnections within our facilities as of March 31, 2010, our interconnection-centric model targets customers that value the interconnection density in our secure and reliable environments. The table below is a representative list of those customers:

| Communications Service Providers |

Enterprises/Institutions |

Online Media, Video and Content Providers |

Government / Cloud / SaaS / Other | |||

| AT&T Clearwire Cogent Level 3 Communications Qwest Reliance Globalcom Sprint Switch & Data Tata Telecom Telecom Italia Verizon |

ACTIV Financial Systems Emory University Hewlett Packard International Securities Exchange (ISE) University of Florida |

CBS Cumulus Media Justin TV JahJah Viacom Yahoo! |

iland Internet Solutions NASA (via

Arcata Salesforce.com SoftLayer Technologies |

We evaluate market leadership based on publicly available information for physical interconnections per customer and our experience in the industry. Based on this framework, we believe that our average of 36 physical interconnections per customer as of March 31, 2010 makes us a leading network neutral, global interconnection and colocation solutions provider in the United States. We believe that the interconnection density within our facilities can create a network effect that increases the value proposition of our products and related services. Because each additional customer added to a facility can connect to all of the other customers already in that facility, with the addition of each new customer, the potential number of interconnections in our facilities increases. We believe that this enhances our ability to both retain existing customers and attract new customers. Our 15 interconnection and colocation facilities are located in the New York Metropolitan area, the San Francisco Bay area, Los Angeles, Dallas, Chicago, Atlanta, Phoenix, Charlotte and Miami.

The global Internet datacenter market is estimated to grow at a compound annual growth rate of 19% from $9.2 billion in 2008 to $15.5 billion in 2011 according to Tier1 Research’s Internet Datacenter Global Markets Overview—2010 report. Increasing demand for our network neutral interconnection and colocation products and related services is being driven by powerful trends, including favorable datacenter supply and demand dynamics, continued growth in Internet traffic, increasing enterprise adoption of datacenter outsourcing and network based applications, continued adoption of Ethernet technologies, continued growth of Internet video, emerging computing technologies such as cloud computing, increasing demand for proximity hosting and low latency (or low time delay) networking, and increasing datacenter power and cooling requirements.

Our business is characterized by significant monthly recurring revenue, low churn (or loss of revenue), and a predictable cost structure. We generate revenue by charging our customers a recurring monthly fee for our interconnection and colocation products and related services, a one-time fee for the installation of related colocation and interconnection products, and an hourly or a subscription fee for technical support services. The combination of our recurring revenues, representing approximately 93% of our total revenue for the three months ended March 31, 2010, and our low churn provides us significant visibility into our revenue generating capabilities for the coming years. We believe our high interconnection density demonstrates an interconnection-centric business model that differentiates us from our competition. It improves our ability to maximize revenues and profitability relative to other predominately colocation-centric providers that do not have a similar level of interconnection density within a comparable physical footprint. Additionally, our interconnection-centric model improves our profitability and capital efficiency because we can add a significant number of interconnections between existing customers within our facilities without leasing additional space or incurring significant additional costs.

2

Table of Contents

Our revenue growth since 2007 is primarily the result of organic growth, consisting of increasing amounts of our products and related services provided to existing and new customers. From December 31, 2007 to December 31, 2009, we grew our customer base from 495 to 763 customers representing a 24% compound annual growth rate and our total physical interconnections increased from 19,692 to 28,272 representing a 20% compound annual growth rate. Over the same period, to meet our customers’ increasing demand for our products and related services, we expanded our footprint from 370,543 gross square feet to 478,412 gross square feet representing a compound annual growth rate of 14%. At March 31, 2010, our customer base had increased to 804, total physical interconnections had increased to 29,324 and our footprint had expanded to 487,072 square feet. The growth in our facility footprint was accomplished through the addition of three new facilities and the expansion of our existing space within our other facilities. We believe that our existing customer base, products and services will continue to grow, which will enhance the ecosystems within our facilities and in turn support our ability to attract new customers.

Our Competitive Strengths

Customers typically use our products and related services because we provide them with a level of interconnection access, quality of service, reliability and flexibility that is difficult to replicate independently or with another interconnection and colocation provider. We believe that our key competitive strengths, which are described below, position us well to take advantage of the favorable trends in our industry.

Strategically Focused Footprint. Our 15 facilities in nine tier-1 markets across the United States are located at the primary intersections of multiple, major international and domestic fiber routes where we believe Internet and private network traffic is most concentrated and interconnection demand is highest.

Industry Leader in Physical Interconnections. As of March 31, 2010, we facilitated a total of 29,324 physical interconnections between our customers, which represent an average of 36 physical interconnections per customer. This allows our customers to achieve the seamless exchange of information across hundreds of communications service providers, enterprises, online media, video and content providers, government agencies, cloud computing providers and Software as a Service (SaaS) providers. We believe that our average of 36 physical interconnections per customer as of March 31, 2010, represents greater physical interconnection density than our peers in the United States.

Network Neutral Business Model. We do not own or operate our own network. The ecosystems in our facilities provide our customers with the flexibility to optimize their connection partners based on their individual application and connectivity requirements. We believe this optionality provides for increased operational efficiency and reduced cost for the customer.

High Barriers to Entry. We believe our interconnection-centric model has high barriers to entry primarily resulting from the difficulty in replicating the ecosystems that exist within our facilities and the resulting network effect that exists among our customers. Significant time and resources are required to develop these ecosystems. In addition, we believe that the buildings in which we operate are already the primary landing points and crossroads for global fiber networks and the ability to replicate this network proximity would be difficult and cost prohibitive. While significant barriers to entry exist, we believe that our experience, relationships with a critical mass of communities of interest and leading communications service providers, reputable brand, associated track record and proven business model enable us to pursue expansion opportunities more effectively than potential competitors.

Exclusive Operator of Interconnection Areas within 10 Digital Realty Trust Wholesale Datacenter Buildings. Our relationship with Digital Realty Trust, Inc., or Digital Realty Trust, one of the leading datacenter real estate investment trusts, generally provides us with the exclusive ability to operate the interconnection areas in 10 tier-1 wholesale datacenter buildings across the United States.

3

Table of Contents

Engineering and Operational Excellence. Our facilities provide the structural integrity and redundant power and cooling infrastructure required for a secure, reliable and effective networking and computing environment. Since 2003, we have provided our customers with over 99.999% uptime on our overall power and cooling systems. Based on our industry experience and customer feedback, we believe that we also offer best-in-class installation and technical support services that enhance networking opportunities and maximum exposure to the global communications marketplace.

Our Strategy

Our goal is to expand our leadership position in network neutral, global interconnection and colocation products and related services. Our strategy for accomplishing this goal includes the key elements described below.

Continue to Expand our Relationships with Existing Customers. We will continue to offer our existing customers best-in-class interconnection and colocation products and related services to meet their growing requirements. Over 70% of our revenue growth during 2008 and 2009 resulted from revenues from existing customers. 80% of our revenue growth for the three months ended March 31, 2010 resulted from revenues from existing customers. We will strive to continue to provide the quality of service and interconnections that have resulted in low average monthly churn of 0.8% and 0.6%, respectively, during 2008 and 2009. Our average monthly churn was 0.6% for the three months ended March 31, 2010.

Continue to Acquire Profitable New Customers. We recognize the ability of additional customers to enhance the value proposition of our interconnection ecosystems. We will continue to target and develop relationships with customers that will benefit most from their inclusion in a Telx ecosystem and that will increase the value proposition to our other customers due to their expected demand for interconnection. We intend to continue to price our products and services at a level that reflects both the market demand for our products and related services, as well as our short and long term profitability goals and return on invested capital expectations.

Further Penetrate Attractive Industry Sectors. A substantial portion of our revenue is derived from communications service providers that require the high level of interconnections we offer. Revenue from other industry sectors, however, has grown from an annualized rate of 15% of our revenues in December 2007 to an annualized rate of 24% in December 2009. The enterprise, online media, video and content provider, government, cloud computing provider and SaaS provider industry sectors have grown significantly within the ecosystems that exist within our facilities and provide attractive opportunities for further ecosystems development and growth. We also believe other industry sectors, such as healthcare, will provide additional long-term opportunities for ecosystems development and growth. We intend to continue to focus our efforts to further penetrate these sectors.

Increase Network Densities. As our network densities increase, our customer value proposition increases. As an interconnection-centric company, we aim to continuously increase the number of interconnections we facilitate. We will continue to focus our sales, marketing, technology and facilities efforts accordingly.

Selective Product and Services Expansion. We intend to continually develop our interconnection and colocation offerings and introduce new products and related services to meet our customers’ needs. Product and services launched during 2009 included the Telx Video Exchange and our Managed Security Services offerings. In 2010, we plan to introduce an Ethernet Exchange offering.

Selective Expansion in Existing and New Markets. As we grow our business, we aim to grow efficiently by increasing our gross square footage to satisfy the demand for our products and related services in existing facilities and by selectively identifying domestic and international opportunities for expansion into new markets. We only begin new expansions once we have identified customers and we have the capital to fully fund the build out. Our expansions are done in phases in order to manage the timing and scale of our capital expenditure obligations, reduce risk and improve our return on capital.

4

Table of Contents

Pursue Selective Acquisitions. We believe our industry has favorable consolidation characteristics and we expect this trend to continue in the foreseeable future. Given the limited availability of interconnection and colocation facilities within tier-1 markets, acquisitions of existing businesses may provide a cost-effective method of increasing network densities, expanding our customer base and broadening our geographic footprint. We intend to pursue attractive opportunities as they arise.

Summary Risk Factors

Investing in our common stock involves a high degree of risk. You should consider carefully the risks and uncertainties summarized below, the risks described under “Risk Factors,” the other information contained in this prospectus and our consolidated financial statements and the related notes before you decide whether to invest in our common stock.

| • | We have incurred substantial losses in the past and may continue to incur losses in the future. |

| • | Our operating results have fluctuated historically and could continue to fluctuate in the future, which could affect our ability to maintain our current market position or expand. |

| • | In the past, significant deficiencies and material weaknesses in our internal control over financial reporting have been identified. If new material weaknesses arise or if we fail to maintain proper and effective internal controls going forward, our ability to produce accurate and timely financial statements could be impaired, which could adversely affect our business, operating results and financial condition. |

| • | Our ability to maximize the utilization of our facilities is limited by the availability and cost of sufficient electrical power and cooling capacity, which may result in our inability to accept new customers at our facilities. This could lead to a decline in our revenue growth and may cause us to incur additional costs to increase the power supply, increase cooling capacity or acquire space at an additional facility. |

| • | We are dependent upon third-party suppliers for power and certain other services, and we are vulnerable to service failures of our third-party suppliers and to price increases by such suppliers. |

| • | We are continuing to invest in our expansion efforts, but we may not experience sufficient customer demand in the future to realize expected returns on these investments. |

| • | Changes in technology could adversely affect our business. |

| • | Our success largely depends upon retaining the services of our management team. |

| • | The forecasts of market growth included in this prospectus may prove to be inaccurate, and even if the markets in which we compete achieve the forecasted growth, we cannot assure you our business will grow at similar rates, or at all. |

Recent Developments

On June 17, 2010, we and certain of our subsidiaries entered into a senior secured credit facility, consisting of a $150.0 million term loan and a $25.0 million revolving facility, which we refer to herein as the New Credit Facility. The term loan matures on June 17, 2015 and the revolving loan matures on June 17, 2014. The New Credit Facility is guaranteed by all of our current subsidiaries, and certain of our subsidiaries that we may acquire or create in the future, and is secured by substantially all of our and such subsidiary guarantors’ assets. The non-default interest rates for the loans under the New Credit Facility are determined by reference to either LIBOR plus 6.00% or, at our election, a prime-based rate plus 5.00%. These margins are subject to increase in certain circumstances as set forth in the credit agreement. The margin increases will terminate, to the extent they

5

Table of Contents

occur, if our senior secured leverage ratio drops below a threshold set forth in the credit agreement or once all of our leasehold mortgages with Digital Realty Trust have been obtained. The credit agreement provides for a floor of 2.00% for LIBOR and a floor of 3.00% for loans based on the prime rate.

We used $138.1 million of the proceeds of the term loan to repay indebtedness outstanding under our prior credit agreement with CIT Lending Services Corporation and loans associated with our ownership of a facility in Atlanta, Georgia, other minor indebtedness, and to pay the fees and expenses of the transaction, and we used an additional $1.1 million of proceeds to pay accrued interest on repaid indebtedness. We intend to use the remaining proceeds from the borrowings to fulfill our and our subsidiaries’ working capital requirements and for general corporate purposes. We did not draw upon the revolving facility at closing, but when or if we do so, such proceeds will be used to fulfill our and our subsidiaries’ working capital requirements and for general corporate purposes.

Corporate Information

We were incorporated on August 3, 2000 as a Delaware corporation. We currently conduct certain operations through our wholly owned subsidiaries. We are headquartered in New York, New York. Our principal executive offices are located at 1 State Street, 21st Floor, New York, New York 10004 and our telephone number at this location is (212) 480-3300. Our website address is www.telx.com. Information included or referred to on, or otherwise accessible through, our website is not intended to form a part of or be incorporated by reference into this prospectus.

The Offering

| Common stock offered by us |

shares |

| Common stock offered by the selling stockholders |

shares |

| Common stock to be outstanding after this offering |

shares |

| Option to purchase additional shares |

shares |

| Use of proceeds |

We intend to use the net proceeds of this offering for capital expenditures, working capital and general corporate purposes. We may also use a portion of the net proceeds to finance growth through the acquisition of, or investment into, businesses, products, services or technologies complementary to our current business. We will not receive any of the proceeds from the sale of shares by the selling stockholders. See the section entitled “Use of Proceeds.” |

| Proposed Nasdaq Global Market symbol |

TELX |

The number of shares of our common stock to be outstanding immediately after this offering is based on the number of shares outstanding as of , 2010, after giving effect to the conversion of all of our outstanding shares of preferred stock into shares of common stock; and excludes:

| • | 117,018 shares of common stock issuable upon the exercise of options outstanding as of May 14, 2010, having a weighted average exercise price of $34.12 per shares; |

| • | 7,375 shares of common stock reserved for issuance under our equity incentive plans as of May 14, 2010; and |

6

Table of Contents

| • | 1,000 shares issuable upon the exercise of warrants outstanding as of May 14, 2010, having an exercise price of $40.00 per share. |

Assumptions Used in This Prospectus

Except as otherwise indicated, all information contained in this prospectus assumes:

| • | an offering price of $ per share of common stock, which is the mid-point of the range set forth on the cover of this prospectus; |

| • | the underwriters do not exercise their option to purchase up to an additional shares of our common stock from us and/or the selling stockholders; |

| • | the conversion of all outstanding shares of our preferred stock into an aggregate of shares of common stock effective immediately prior to the closing of this offering; |

| • | a for stock split of our outstanding capital stock that was effected on , 2010; |

| • | the filing of our amended and restated certificate of incorporation upon the completion of this offering; and |

| • | our issuance of shares of common stock in this offering. |

7

Table of Contents

Summary Consolidated Financial Data

The following summary consolidated financial data for the fiscal years ended December 31, 2009, 2008 and 2007 are derived from our audited financial statements. Summary consolidated financial data for the three months ended March 31, 2010 and 2009 are derived from our unaudited financial statements. You should read this data together with our audited financial statements and related notes included elsewhere in this prospectus and the information under the sections entitled “Selected Financial Data” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

| Three Months Ended March 31, |

Years Ended December 31, | |||||||||||||||||||

| 2010 | 2009 | 2009 | 2008 | 2007 | ||||||||||||||||

| (in thousands, except share and per share data) |

||||||||||||||||||||

| (unaudited) | ||||||||||||||||||||

| Statement of Operations Data:(1)(2)(3)(4) |

||||||||||||||||||||

| Revenues |

$ | 29,651 | $ | 21,820 | $ | 98,335 | $ | 70,038 | $ | 50,762 | ||||||||||

| Operating expenses |

25,779 | 26,758 | 99,937 | 93,332 | 78,063 | |||||||||||||||

| Operating income (loss) |

3,872 | (4,938 | ) | (1,602 | ) | (23,294 | ) | (27,301 | ) | |||||||||||

| Interest income |

62 | 65 | 374 | 396 | 612 | |||||||||||||||

| Interest expense |

(1,990 | ) | (1,144 | ) | (7,221 | ) | (7,380 | ) | (9,769 | ) | ||||||||||

| Other expense |

— | (5 | ) | (12 | ) | (330 | ) | (739 | ) | |||||||||||

| Income (loss) from operations before income taxes |

1,944 | (6,022 | ) | (8,461 | ) | (30,608 | ) | (37,197 | ) | |||||||||||

| Income tax benefit (expense) |

(231 | ) | (1,037 | ) | (1,458 | ) | (772 | ) | 811 | |||||||||||

| Net income (loss) |

1,713 | (7,059 | ) | $ | (9,919 | ) | $ | (31,380 | ) | $ | (36,386 | ) | ||||||||

| Less: preferred dividends |

(6,411 | ) | (5,808 | ) | (24,452 | ) | (21,743 | ) | (17,676 | ) | ||||||||||

| Net loss available for common stockholders |

$ | (4,698 | ) | $ | (12,867 | ) | $ | (34,371 | ) | $ | (53,123 | ) | $ | (54,062 | ) | |||||

| Net loss per common share |

$ | (6,654 | ) | $ | (57,442 | ) | $ | (63,066 | ) | $ | (290,290 | ) | $ | (540,620 | ) | |||||

| Weighted average common shares outstanding |

706 | 224 | 545 | 183 | 100 | |||||||||||||||

|

|

||||||||||||||||||||

| (1) Includes stock-based compensation of: |

$ | 407 | $ | 288 | $ | 1,179 | $ | 919 | $ | 379 | ||||||||||

| (2) Includes depreciation and amortization of: |

$ | 2,643 | $ | 8,635 | $ | 21,686 | $ | 32,256 | $ | 31,560 | ||||||||||

| (3) Includes non-cash rent expense of: |

$ | 2,025 | $ | 1,809 | $ | 7,953 | $ | 6,720 | $ | 5,373 | ||||||||||

| (4) Includes non-cash compensation expense for executive loan forgiveness of: |

$ | 414 | $ | — | $ | — | $ | — | $ | — | ||||||||||

Adjusted EBITDA Reconciliation

We use a non-GAAP financial metric that we call Adjusted EBITDA to track, analyze and understand our financial performance, which we define as operating income from continuing operations, plus depreciation and amortization, stock-based compensation expense and other non-cash items such as deferred rent (income)/expense. We believe that Adjusted EBITDA is a helpful metric for the following reasons:

| • | As a measurement of operating performance, it assists management in comparing our operating results for various periods, since it removes the impact of items not directly resulting from operations; |

| • | For planning purposes, we use it to help prepare our internal operating budgets; |

| • | It allows us to establish targets for certain management compensation that relate to the results of our operations, avoiding the impact of items not directly resulting from operations; and |

| • | It allows us to effectively evaluate our capacity to incur and service debt, fund capital expenditures and expand our business. |

8

Table of Contents

The following is a reconciliation of our net income (loss) for the three months ended March 31, 2010 and 2009, and the years ended December 31, 2009, 2008 and 2007 to Adjusted EBITDA.

| Three Months Ended March 31, |

Year Ended December 31, | ||||||||||||||||||

| 2010 | 2009 | 2009 | 2008 | 2007 | |||||||||||||||

| (in thousands) |

|||||||||||||||||||

| (unaudited) | |||||||||||||||||||

| Net income (loss) |

$ | 1,713 | $ | (7,059 | ) | $ | (9,919 | ) | $ | (31,380 | ) | $ | (36,386 | ) | |||||

| Interest expense, net |

1,928 | 1,079 | 6,847 | 6,984 | 9,157 | ||||||||||||||

| Other expense |

— | 5 | 12 | 330 | 739 | ||||||||||||||

| Income tax expense (benefit) |

231 | 1,037 | 1,458 | 772 | (811 | ) | |||||||||||||

| Non-cash rent expense (1) |

2,025 | 1,809 | 7,953 | 6,720 | 5,373 | ||||||||||||||

| Depreciation and amortization expense |

2,643 | 8,635 | 21,686 | 32,256 | 31,560 | ||||||||||||||

| Non-cash compensation expense (2) |

821 | 288 | 1,179 | 919 | 379 | ||||||||||||||

| Adjusted EBITDA |

$ | 9,361 | $ | 5,794 | $ | 29,216 | $ | 16,601 | $ | 10,011 | |||||||||

| (1) | Non-cash rent expense includes deferred rent expense and non-cash rent expense related to a stock option granted to a landlord. Deferred rent expense represents the non-cash component of rent expense required by GAAP to reflect the total escalating rent payments under our long-term leases as a straight-line expense each period over the estimated term of the lease. |

| (2) | Non-cash compensation expense includes the non-cash component of compensation expense related to our equity incentive plans and in the first quarter of 2010, the non-cash compensation related to executive loan forgiveness of $414. |

Our Adjusted EBITDA is not necessarily comparable to similarly titled measures used by other companies. In addition, Adjusted EBITDA: (a) does not represent net income or cash flows from operating activities as defined by U.S. generally accepted accounting principles, or GAAP; (b) is not necessarily indicative of cash available to fund our cash flow needs; and (c) should not be considered as an alternative to net income, operating income, cash flows from operating activities or other financial information as determined under GAAP.

We prepare Adjusted EBITDA by adjusting net loss to eliminate the impact of a number of items that we do not consider indicative of our core operating performance. You are encouraged to evaluate each adjustment and the reasons we consider them appropriate. As an analytical tool, Adjusted EBITDA is subject to all of the limitations applicable to net loss. In addition, in evaluating Adjusted EBITDA, you should be aware that in the future we may incur expenses similar to the adjustments in this presentation. Our presentation of Adjusted EBITDA should not be construed as an implication that our future results will be unaffected by unusual or non-recurring items.

9

Table of Contents

An investment in our common stock involves a high degree of risk. In deciding whether to invest, you should carefully consider the following risk factors, as well as the financial and other information contained in this prospectus, including our consolidated financial statements and related notes. Any of the following risks as well as other risks and uncertainties discussed in this prospectus could have a material adverse effect on our business, financial condition, results of operations or prospects and cause the value of our stock to decline, which could cause you to lose all or part of your investment. Additional risks and uncertainties of which we are unaware, or that are currently deemed immaterial by us, also may become important factors that affect us.

Risks Related to Our Business and Industry

We have incurred substantial losses in the past and may continue to incur losses in the future.

Although we had net income of $1.7 million for the three months ended March 31, 2010, for the years ended December 31, 2009, 2008 and 2007, we incurred net losses of approximately $9.9 million, $31.4 million and $36.4 million, respectively. As of March 31, 2010, we had an accumulated deficit of $82.6 million. Going forward, there can be no guarantee that we will achieve and sustain profitability. Our ability to achieve and sustain profitability is dependent upon a number of risks and uncertainties discussed below, many of which are beyond our control. Given the competitive and evolving nature of the industry in which we operate, we may not be able to sustain or increase profitability on a quarterly or annual basis.

Our operating results have fluctuated historically and could continue to fluctuate in the future, which could affect our ability to maintain our current market position or expand.

Our operating results have fluctuated in the past and may continue to fluctuate in the future as a result of a variety of factors, many of which are beyond our control, including the following:

| • | changes in general economic conditions and specific market conditions in the telecommunications and Internet-related industries; |

| • | demand for interconnection and colocation products and services in general or at our facilities in particular; |

| • | competition from other suppliers of the products and services we offer; |

| • | timing and magnitude of operating expenses, capital expenditures and expenses related to sales and marketing, including expenses incurred as a result of expansions and acquisitions, if any; |

| • | cost and availability of power and cooling capacity; |

| • | cost and availability of additional space inventory either through lease or acquisition in our target markets; |

| • | our acquisition of additional facilities; |

| • | mix of our current products and services; |

| • | financial condition and credit risk of our customers; and |

| • | our access to capital and ability to fund capital expenditure projects. |

Any of the foregoing factors could have a material adverse effect on our business, results of operations and financial condition. Although we have experienced growth in revenues in recent quarters, this growth rate is not necessarily indicative of future operating results. A relatively large portion of our expenses are fixed in the short-term, particularly with respect to lease and personnel expenses, depreciation and amortization expenses, and interest expense. Therefore, our results of operations are particularly sensitive to fluctuations in revenues. Comparisons to prior periods should not be relied upon as indications of our future performance.

10

Table of Contents

In the past, significant deficiencies and material weaknesses in our internal control over financial reporting have been identified. If new material weaknesses arise or if we fail to maintain proper and effective internal controls going forward, our ability to produce accurate and timely financial statements could be impaired, which could adversely affect our business, operating results, and financial condition.

In connection with the audit of our consolidated financial statements as of and for the year ended December 31, 2008, our independent registered public accounting firm did not identify any material weaknesses but did identify two significant deficiencies in our internal controls relating to an inadequate system of internal controls during 2008 in certain processes and several deficiencies related to information technology, or IT, processes, controls and documentation. A significant deficiency is a deficiency, or combination of deficiencies, in internal control over financial reporting that is less severe than a material weakness, yet important enough to merit attention by those responsible for oversight of our financial reporting. In connection with the audit of our consolidated statements as of and for the year ended December 31, 2007, our independent registered public accounting firm identified a deficiency that constituted a material weakness in our internal control over financial reporting for the year ended and as of December 31, 2007. This material weakness related to an inadequate system of internal controls during the first half of 2007 (as we documented a comprehensive set of accounting policies and procedures in the second half of the year) and several control deficiencies related to IT processes, controls and documentation. A material weakness is a deficiency or a combination of deficiencies, in internal control over financial reporting, such that there is a reasonable possibility that a material misstatement of the company’s annual or interim financial statements will not be prevented or detected on a timely basis.

In connection with the audit of our consolidated financial statements as of December 31, 2006 and for the periods from January 1 to October 3, 2006 and October 4 to December 31, 2006, our independent registered public accounting firm identified two control deficiencies that represented material weaknesses in our internal control over financial reporting for such periods. These material weaknesses related to insufficient technical resources in accounting, financial reporting and income taxes and an inadequate system of internal controls including a lack of a comprehensive set of accounting policies and procedures and several deficiencies related to IT processes, controls and documentation. Because of these material weaknesses, there is heightened risk that a material misstatement of our financial statements as of and for the periods ended December 31, 2007 and December 31, 2006 was not prevented or detected.

We have taken steps to remediate our material weaknesses and significant deficiencies. However, there are no assurances that the measures we have taken to remediate these internal control weaknesses were completely effective or that similar weaknesses will not recur. Additionally, as part of our ongoing efforts to improve our financial accounting organization and processes, from 2007 to the present we have hired several senior accounting personnel. We plan to continue to assess our internal controls and procedures and intend to take further action as necessary or appropriate to address any other matters we identify.

No material weaknesses or significant deficiencies were identified for the year ended December 31, 2009, and, accordingly, we believe that our remediation efforts were successful. However, we did not perform an assessment of our internal controls over financial reporting nor did our auditors perform an audit over our internal controls over financial reporting; we therefore cannot assure you that these or other similar issues will not arise in future periods. We anticipate that we will next evaluate our internal control over financial reporting in connection with management’s preparation of our financial statements for the year ended December 31, 2010. Although an evaluation of internal controls will only be performed at year end, we will review internal controls in connection with our quarterly reporting.

11

Table of Contents

Our ability to maximize the utilization of our facilities is limited by the availability and cost of sufficient electrical power and cooling capacity, which may result in our inability to accept new customers at our facilities. This could lead to a decline in our revenue growth and may cause us to incur additional costs to increase the power supply, increase cooling capacity or acquire space at an additional facility.

The availability of an adequate supply of electrical power and cooling capacity, and the infrastructure to deliver that power and cooling, is critical to our ability to provide our products and services. Even though physical space may be available in a facility, the demand for electrical power may exceed our designed capacity. We may be unable to meet the increasing power and cooling needs of our customers if our customer mix does not match our expectations or our customers further increase their use of high density electrical power equipment. In addition, the amount of sellable space within our facilities is reduced to the extent that we house generators and batteries to provide back-up power. Further, certain of the leases for our facilities also contain provisions that limit the supply of electrical power and cooling capacity to such facilities, as a result of which our ability to reach full utilization may be constrained in these facilities. If the availability of power and cooling capacity limits our ability to fully utilize the space within our facilities, we may be unable to accept new customers at our facilities and our revenue growth will decline. We also may incur additional costs to increase the power supply and/or cooling capacity or acquire space at an additional facility, which could increase our losses, or reduce our ability to become profitable.

We are dependent upon third-party suppliers for power and certain other services, and we are vulnerable to service failures of our third-party suppliers and to price increases by such suppliers.

We rely on third parties to provide power, and we cannot ensure that these third parties will deliver such power in adequate quantities or on a consistent basis. If the amount of power available to us is inadequate to support our customer requirements or delivery of power does not occur in a timely manner, we may be unable to provide our services to our customers and our operating results and cash flow may be materially and adversely affected. In addition, our facilities are susceptible to power shortages and planned or unplanned power outages caused by these shortages such as those that occurred in California in 2001, in New York City and the Northeast in 2003 and in Miami in 2005. We attempt to limit exposure to power shortages by using backup generators and batteries. Power outages, which may last beyond our backup and alternative power arrangements, would harm our customers and our business. Although we have maintained power availability in excess of the Tier 4 fault tolerant standards resulting in aggregate availability in excess of 99.999% across our facilities since 2003, a limited number of our customers have experienced temporary losses of power, for which we generally provided credits against future invoices. We could incur similar or other financial obligations or be subject to lawsuits by our customers in connection with a loss of power. In addition, any loss of services or equipment damage could reduce the confidence of our customers in our products and services and could consequently impair our ability to attract and retain customers, which would adversely affect both our ability to generate revenues and our operating results.

We are dependent upon third-party suppliers for the resale of Internet access and other services, and we have no control over the quality and reliability of the services provided by these suppliers. In the past, some of these providers have experienced significant system failures. Users of our products and services may in the future experience difficulties due to service failures unrelated to our systems, products and services. If for any reason these suppliers fail to provide certain services to us, our business, financial condition and results of operations could be adversely affected.

While most of our facilities operate in regulated energy markets, power costs increase from time to time. We generally have the option to pass along increases in the cost of power to our customers, but we may choose not to do so for a variety of operating reasons. To the extent that we do not pass these costs along, or that we delay in passing them along, we will pay higher energy prices, increasing our operating costs and depressing our margins. In addition, even if we do pass these power costs along, we will effectively increase the price for our products and services, which could reduce overall demand for our products and services.

12

Table of Contents

The high utilization of our facilities may limit our ability to grow in certain key markets, and we may be unable to expand our existing facilities or locate and secure suitable sites for additional facilities.

Our facilities have reached high rates of utilization in many of our key markets. Our ability to meet the growing needs of our existing customers and to attract new customers in these key markets depends on our ability to add additional capacity by incrementally expanding our existing facilities or by locating and securing additional facilities in these markets that meet specific infrastructure requirements such as access to multiple communications service providers, a significant supply of electrical power and sufficient cooling capacity, high ceilings and the ability to sustain heavy floor loading. In many markets, the supply of facilities with these characteristics is limited and subject to high demand. If we are unable to expand our facilities in a timely and cost-effective manner, or to locate facilities with characteristics similar to our current facilities, our revenue growth will decline, and we may not achieve profitability.

We are continuing to invest in our expansion efforts, but we may not experience sufficient customer demand in the future to realize expected returns on these investments.

We expect to acquire or lease additional properties, and potentially may construct new facilities. If successful, we will be required to commit substantial operational and financial resources to these facilities, generally up to 12 months in advance of securing customer contracts, and we may not experience sufficient customer demand in those markets in which we choose to expand to support these facilities once they are built. In addition, unanticipated technological changes could affect customer requirements, and we may not have built such requirements into our new facilities. Any of these contingencies, if they were to occur, could make it difficult for us to realize expected or reasonable returns on these investments and could have a material adverse effect on our operating results.

Moreover, there can be no assurance that we will be able to successfully integrate these new facilities. Specific challenges we have encountered in such prior acquisitions include the following:

| • | occasional unexpected additional capital expenditures to improve the condition of the acquired equipment so as to achieve the desired level of quality of service; |

| • | the need to create and maintain uniform policies, procedures and controls; and |

| • | the necessary internal corporate skill-sets to properly manage our expanded customer base. |

Acquiring or leasing additional properties (including the construction of new facilities) may expose us to the challenges set forth above and other risks such as:

| • | the diversion of senior management’s attention from daily operations to the negotiation of transactions and integration of such properties; |

| • | the inability to achieve projected synergies; |

| • | the possible loss or reduction in value of acquired properties; |

| • | the possible loss of key personnel; and |

| • | the assumption of undisclosed liabilities. |

The failure to successfully integrate such new properties could have a material adverse effect on our business, results of operations and financial condition. Successful integration will depend on our ability to manage acquired operations, realize revenue growth from an expanded customer base and eliminate duplicative and excess costs, among other factors.

Our construction of additional facilities could involve significant risks to our business.

Construction involves substantial planning and allocation of company resources. Construction also requires us to carefully select and rely on the experience of one or more general contractors and associated subcontractors

13

Table of Contents

during the construction process. Should a general contractor or significant subcontractor experience financial or other problems during the construction process, we could experience significant delays, increased costs to complete the project and other negative impacts to our expected returns.

In the event we decide to construct new facilities separate from our existing facilities, we may provide services to interconnect these two facilities. Should these services not provide the necessary reliability to sustain service, this could result in lower interconnection revenue, lower margins and could have a negative impact on customer retention over time.

If we are unable to manage our growth effectively, our financial results could suffer.

We have increased our number of full-time employees from 103 as of December 31, 2007 to 163 as of December 31, 2009 and have increased our revenue from $50.8 million in 2007 to $98.3 million in 2009. Further, we intend to continue to expand our overall business, customer base, headcount, and operations, domestically and possibly internationally. Creating a global organization and managing a geographically dispersed workforce will require substantial management effort and significant additional investment in our operating and financial system capabilities and controls. If our information systems are unable to support the demands placed on them by our rapid growth, we may be forced to implement new systems which would be disruptive to our business. We may be unable to manage our expenses effectively in the future due to the expenses associated with these expansions, which may negatively impact our gross margins or operating expenses. If we fail to improve our operational systems or to expand our customer service capabilities to keep pace with the growth of our business, we could experience customer dissatisfaction, cost inefficiencies, and lost revenue opportunities, which may materially and adversely affect our operating results.

We lease all but one of our facilities, and the termination or non-renewal of leases poses significant risk to our ongoing operations.

We only own one of our facilities (Atlanta), and operate the rest of them pursuant to commercial leasing arrangements. The initial terms of such leases expire over a period ranging from 2022 to 2050. We would incur significant costs if we were forced to vacate one of our facilities due to the high costs of relocating the equipment in our facilities and installing the necessary infrastructure in a new facility. In addition, if we were forced to vacate a facility, we could lose customers that chose our products and services based on our location. Our landlords could attempt to evict us for reasons beyond our control. Further, we may be unable to maintain good working relationships with our landlords, which would adversely affect our customer service and could result in the loss of current customers.

In addition, our business would be harmed by our inability to renew leases at favorable terms. Most of our leases provide two ten-year renewal options with rents set at then-prevailing market rates. We expect that the then-prevailing market rates will be higher than present rates. To maintain the operating profitability associated with our present cost structure, we must increase revenues within existing facilities to offset the anticipated increase in lease payments at the end of the original and renewal terms. Failure to increase revenue sufficiently to offset these projected higher costs would adversely impact our operating income.

The majority of our leases are with a single landlord, Digital Realty Trust, which makes us more vulnerable than if our leases were diversified. In addition, a significant portion of our revenue is generated by interconnection products and services we provide to customers located in Digital Realty Trust facilities, which we may lose if contractual arrangements we have with Digital Realty Trust are terminated or our rights under such contracts are impaired.

Ten of our 14 leased facilities are leased to us by a single landlord, Digital Realty Trust, representing approximately 28% of our total facility space. The initial terms of these Digital Realty Trust leases expire in 2026, and we have options to extend them through 2046. The terms of all these leases with Digital Realty Trust

14

Table of Contents

are generally similar. In the event that we are unable to come to agreement with Digital Realty Trust regarding the renewal of these leases, or come to a disagreement regarding our rights and obligations under these agreements, a significant portion of our available inventory may be impaired or lost.

Subject to certain exceptions, we have the general right to exclusively operate the interconnection areas at ten Digital Realty Trust facilities. Although we lease space from Digital Realty Trust (which we then license to our customers) in such facilities, due to our exclusivity arrangement with Digital Realty Trust, a significant number of companies that lease space from Digital Realty Trust directly make their interconnections in our interconnection areas. The revenue generated by the interconnections in such interconnection areas represents a significant portion of our overall revenue. If we were to lose the right to operate these interconnection areas in the future, we may also lose the revenue associated with the interconnections in such interconnection areas, and our business could suffer as a result.

If our contracts with our customers are not renewed or are terminated, our business could be substantially harmed.

Our customer contracts typically have terms of one to three years. Our customers may not elect to renew these contracts. Furthermore, our customer contracts are terminable for cause if we breach a material provision of the contract, including the failure to provide power or connectivity for extended periods of time, or if we violate applicable laws or regulations. We may face increased competition and pricing pressure as our customer contracts become subject to renewal. Our customers may negotiate renewal of their contracts at lower rates, for fewer products and services or for shorter terms. In addition, if we lose one customer, others may elect not to renew their contracts to the extent that such other customers depend substantially on interconnection with the lost customer. If we are unable to successfully renew our customer contracts on their current terms, or if our customer contracts are terminated, our business could suffer.

Any failure of our physical infrastructure or our products and services, or failure to meet performance standards under our service level agreements, could result in our customers terminating their relationship with us and could lead to significant costs and disruptions that could reduce our revenues, harm our business reputation and have a material adverse effect on our financial results.

Our business depends on providing customers with highly reliable products and services. The products and services we provide are subject to failure resulting from numerous factors, including:

| • | human error; |

| • | power loss; |

| • | improper building maintenance by the landlords of the buildings in which our facilities are located; |

| • | physical or electronic security breaches; |

| • | fire, earthquake, hurricane, flood and other natural disasters; |

| • | water damage; |

| • | the effect of war, terrorism and any related conflicts or similar events worldwide; and |

| • | sabotage and vandalism. |

Problems at one or more of our facilities, whether or not within our control, could result in service interruptions or equipment damage. We have service level agreements with substantially all of our customers in which we provide various guarantees regarding our levels of service. We may have difficulty meeting these levels of service if we experience service interruptions. Service interruptions or equipment damage in our facilities could result in credits for service interruptions to these customers. We have at times in the past given credits to our customers against future invoices as a result of service interruptions due to equipment failures. We

15

Table of Contents

cannot assure you that our customers will accept these credits as compensation in the future. In addition, our inability to meet our service level commitments may damage our reputation and could consequently limit our ability to retain existing customers and attract new customers, which would adversely affect our ability to generate revenues and negatively impact our operating results. Also, service interruptions and equipment failures could result in lost profits or other indirect or consequential damages to our customers and may expose us to additional legal liability and impair our brand image. We depend on our landlords and other third-party providers to properly maintain the buildings in which our facilities are located. Improper maintenance by such landlords and third parties increase the risk of service interruptions and equipment damage.

Additionally, certain of our facilities, including those in New York, California, Florida and Texas, are located in areas particularly susceptible to terrorist activity and natural disasters such as earthquakes, hurricanes and tornadoes. The occurrence of any terrorist activity or natural disaster could shut down one or more of our facilities and result in a material adverse effect upon our results of operations. Moreover, we may not have adequate property or liability insurance to cover catastrophic events.

We may not be able to compete successfully against current and future competitors. If we fail to differentiate our facilities and products and services from those of our competitors, we may not be able to compete successfully and our business and results of operations may be adversely affected.

We compete with network neutral interconnection and colocation service providers and other service providers, including U.S.-based communications service providers, Internet service providers, managed service providers and web hosting companies. Many of our competitors have longer operating histories and significantly greater financial, technical, marketing and other resources than us, and some have a greater presence in our markets and in other markets across the United States and around the world. Because of their greater financial resources, some of our competitors have the ability to adopt aggressive pricing policies. As a result, we may suffer from pricing pressure that would adversely affect our ability to generate revenues and adversely affect our operating results. In addition, most of these competitors currently offer interconnection and colocation products and services in the same markets and buildings where we have facilities, and other competitors may start doing so in the future. Some of these competitors may also provide our current and potential customers with additional benefits and may do so in a manner that is more attractive to our potential customers than our products and services. These competitors may be able to provide bundled interconnection and colocation products and services at prices lower than our cost structure allows. If, as a result of such efficiencies, these competitors are able to adopt aggressive pricing policies for interconnection and colocation products and services, our ability to generate revenues would be materially and adversely affected.

In addition, our competitors may operate more successfully or form alliances to acquire significant market share. Once businesses locate their networking and computing equipment in competitors’ facilities, it may be extremely difficult to convince them to relocate to our facilities. Furthermore, a business that has already invested substantial resources in such arrangements may be reluctant or slow to replace or limit its existing services by becoming our customer. Finally, we may also experience competition from our landlords. Rather than leasing available space in our buildings to us or other large single tenants, they may decide to convert the space instead to smaller units designed for multi-tenant interconnection and colocation use. Landlords may enjoy a cost advantage in providing products and services similar to those provided by us, and this could also reduce the amount of space available to us for expansion in the future.

We depend upon a limited number of communications service providers in certain of our facilities, and the loss of one or more of these providers in those facilities could adversely affect our business.

Because we do not own or operate our own network, we depend upon communications service providers to interconnect and/or colocate as customers in our facilities and contribute to the network density that attracts our other customers. In some of our smaller markets, we have agreements with only a limited number of communications service providers. In these smaller market facilities, we expect that we will continue to rely

16

Table of Contents

upon a limited number of communications service provider customers to maintain network density within those facilities. Our agreements with these customers are generally for one to three year terms (if not renewed). A loss of one or more of these providers could have a material and adverse effect on the operations of one or more of our smaller facilities.

We may make acquisitions of complementary businesses, customers, products or service lines or technologies, and such acquisitions may pose integration and other risks that could harm our business.

We may acquire complementary businesses, product or service lines and technologies in the future as we did in March 2007 when we acquired certain assets owned by NYC Connect, LLC. There can be no assurance that we will be able to successfully integrate any such acquisitions. To finance these acquisitions, we may incur additional debt and issue additional shares of our stock, which will dilute existing stockholders’ ownership interests in us, and such debt may adversely affect our business and operations.

Specific challenges we have encountered in our acquisition of certain assets owned by NYC Connect, LLC include the following:

| • | occasional unexpected additional capital expenditures to improve the condition of the acquired equipment so as to achieve the desired level of quality of service; |

| • | creating and maintaining uniform policies, procedures and controls; and |

| • | building the necessary internal corporate skill-sets to properly manage our expanded customer base. |

Future acquisitions may expose us to the challenges set forth above and other risks such as:

| • | Certain financial risks, including, but not limited to (i) the payment of a purchase price that exceeds the future value that we may realize from the acquired operations and businesses; (ii) an increase in our expenses and working capital requirements, which could reduce our return on invested capital; (iii) potential known and unknown liabilities of the acquired businesses; (iv) costs associated with integrating acquired businesses, operations, or technologies; (v) the incurrence of additional debt; and (vi) possible adverse tax and accounting effects. |

| • | Operating risks, including, but not limited to (i) the diversion of management’s attention to the assimilation of the businesses, operations, or technologies to be acquired; (ii) the risk that the acquired businesses, operations, or technologies will fail to maintain the quality of services that we have historically provided; (iii) the need to implement financial and other systems; (iv) the need to maintain customer, supplier or other favorable business relationships of acquired operations and restructure or terminate unfavorable relationships; and (v) the potential for deficiencies in internal controls of the acquired operations. |

The failure to successfully integrate acquired businesses, customers, products, service lines or technologies could have a material adverse effect on our business, results of operations and financial condition. Successful integration will depend on our ability to manage acquired operations, realize revenue growth from an expanded customer base and eliminate duplicative and excess costs, among other factors.

Our products and services have a sales cycle that may have a material adverse effect on our business, financial condition and results of operations. The sales cycle may lengthen due to the current macroeconomic environment.

A customer’s decision to license cabinet or cage space in one of our facilities and to purchase interconnection products typically involves a significant commitment of our time and resources. Many customers are reluctant to commit to purchasing our interconnection and colocation products and services until they are confident that our facility has adequate available communications service provider connections and network

17

Table of Contents

density. As a result, we may experience a longer than average sales cycle for our products and services. Furthermore, we may expend significant time and resources in pursuing a particular sale or customer that does not generate revenue. Delays due to the length of our sales cycle or costs incurred that do not result in sales may have a material adverse effect on our business, financial condition and results of operations.

Our success largely depends upon retaining the services of our management team.

We are highly dependent on our management team. We expect that our continued success and future growth will largely depend upon the efforts and abilities of members of our management team. The loss of services of any key executive, including Eric Shepcaro, our Chief Executive Officer, Christopher W. Downie, our President, Chief Financial Officer and Treasurer, William Kolman, our Executive Vice President, Sales, Michael Terlizzi, our Executive Vice President, Operations, and J. Todd Raymond, our Senior Vice President, Facility Acquisition, for any reason could have a material adverse effect upon us. Our success also depends upon our ability to identify, develop and retain qualified employees. The loss of some of our management and other employees could have a material adverse effect on our operations. We do not maintain key man insurance on any members of our management team.

Government regulation of dark fiber is largely unsettled, and depending on its evolution, may adversely affect our business.

The telecommunications industry is currently undergoing a transformation as it moves from a traditional dedicated circuit network architecture to a design where all forms of traffic—voice, video, and information—are transmitted as digital bits over IP-based networks. With the advent of these digital data transmissions and the growth of the Internet, data networks are becoming the networks over which all communications services can be offered. Determining the appropriate regulatory framework for these data networks is one of the most significant challenges facing federal and state telecommunication policy makers. As a result of this fundamental shift in the telecommunications industry’s underlying technology, various laws and governmental regulations at the federal, state and local level in the U.S. and in Canada, governing IP-based services, related communications services and information technologies remain largely unsettled.

Although we do not offer telecommunications services on a common carrier basis, and thus are not subject to federal regulations, there is a risk that we will become subject to regulation. For example, the Federal Communications Commission, or the FCC, has not yet made a final determination of its intent or ability to regulate the provision and sale of so-called “dark fiber,” which we use to connect certain of our facilities, such as our facilities in New York and New Jersey, and offer to our customers for use as part of the larger Telx product and service offerings. The FCC presently considers dark fiber to be a “network element” and not a “telecommunications service” regulated by the FCC. We currently do not believe that we are subject to regulation due to our use of dark fiber in the interconnection between certain of our facilities, although we cannot be certain that the FCC would adopt this position. Additionally, the FCC may change its position in the future. Due to changing technology and applications of that technology, it is uncertain whether and how existing laws or regulations or new laws or regulations will be applied by the FCC and other regulatory bodies in the future to other currently unregulated products and services we offer, or to new products or services that we may offer in the future. Future regulatory, judicial and legislative changes may have a material adverse effect on our ability to deliver products and services within various jurisdictions.

We may not be able to continue to add new customers and increase sales to our existing customers, which could adversely affect our operating results.

Our growth is dependent on our ability to continue to attract new customers while retaining and expanding our products and services to existing customers. Growth in the demand for our products and services may be inhibited and we may be unable to sustain growth in our customer base, for a number of reasons, such as:

| • | our inability to market our products and services in a cost-effective manner to new customers; |

18

Table of Contents

| • | the inability of our customers to differentiate our products and services from those of our competitors or our inability to effectively communicate such distinctions; |