Attached files

| file | filename |

|---|---|

| EX-21.1 - LianDi Clean Technology Inc. | v188968_ex21-1.htm |

| EX-31.1 - LianDi Clean Technology Inc. | v188968_ex31-1.htm |

| EX-31.2 - LianDi Clean Technology Inc. | v188968_ex31-2.htm |

| EX-32.1 - LianDi Clean Technology Inc. | v188968_ex32-1.htm |

| EX-32.2 - LianDi Clean Technology Inc. | v188968_ex32-2.htm |

U.S.

SECURITIES AND EXCHANGE COMMISSION

Washington,

D.C. 20549

FORM

10-K

(MARK

ONE)

|

x

|

ANNUAL REPORT PURSUANT TO

SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF

1934

|

For

the Fiscal Year Ended March 31, 2010

OR

|

¨

|

TRANSITION REPORT PURSUANT TO

SECTION 13 or 15(d) OF THE SECURITIES EXCHANGE ACT OF

1934

|

For

the Transition Period from _______________ to _________________

Commission

file number: 000-52235

LIANDI

CLEAN TECHNOLOGY INC.

(Exact

name of Registrant as Specified in Its Charter)

|

NEVADA

|

75-2955368

|

|

|

(State or Other Jurisdiction

|

||

|

of Incorporation or Organization)

|

(I.R.S. Employer

Identification No.)

|

|

|

4th

Floor Tower B. Wanliuxingui Building, No. 28

Wanquanzhuang

Road

|

||

|

Haidian

District, Beijing, 100089 China

|

||

|

100089

|

||

|

(Address of principal executive offices)

|

(Zip Code)

|

Registrant’s

telephone number, including area code:

(86)

10-5872-0171

SECURITIES

REGISTERED PURSUANT TO SECTION 12 (B) OF THE ACT: NONE

SECURITIES

REGISTERED PURSUANT TO SECTION 12 (G) OF THE ACT:

COMMON

STOCK, PAR VALUE $0.001 PER SHARE

Name of

each exchange on which registered: The OTC Bulletin Board

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in

Rule 405 of the Securities Act. ¨ Yes x

No

Indicate

by check mark if the registrant is not required to file reports pursuant to

Section 13 or Section 15(d) of the Act. ¨ Yes x No

Indicate

by check mark whether the registrant (1) has filed all reports required to be

filed by Section 13 or 15(d) of the Exchange Act of 1934 during the preceding 12

months (or for such shorter period that the registrant was required to file such

reports), and (2) has been subject to such filing requirements for the past 90

days. x

Yes ¨ No

Indicate

by check mark whether the registrant has submitted electronically and posted on

its corporate Web site, if any, every Interactive Data File required to be

submitted and posted pursuant to Rule 405 of Regulation S-T (§229.405 of this

chapter) during the preceding 12 months (or for such shorter period that the

registrant was required to submit and post such files). Yes ¨ No ¨

Indicate

by check mark if disclosure of delinquent filers pursuant to Item 405 of

Regulation S-K (§ 229.405) is not contained herein, and will not be contained,

to the best of registrant’s knowledge, in definitive proxy or information

statements incorporated by reference in Part III of this Form 10-K or any

amendment to this Form 10-K. £

Indicate

by check mark whether the registrant is a large accelerated filer, an

accelerated filer, a non-accelerated filer, or a smaller reporting company. See

the definitions of “large accelerated filer,” “accelerated filer” and “smaller

reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

|

Large accelerated

filer ¨

|

Accelerated

filer ¨

|

Non-accelerated filer ¨

|

Smaller reporting

company x

|

|

(Do not check if a smaller reporting company)

|

Indicate

by check mark whether the registrant is a shell company (as defined in Rule

12b-2 of the Exchange Act). ¨ Yes ¨ No x

The

aggregate market value of the shares of common stock, par value $0.001 per

share, of the registrant held by non-affiliates on June 30, 2009 was $226,738,

which was computed upon the basis of the closing price on that

date.

There

were 29,358,772 shares of common stock of the registrant outstanding as of June

21, 2010.

TABLE

OF CONTENTS

|

PART

I

|

2 | |||||

|

Item

1

|

Business

|

2 | ||||

|

Item

1A.

|

Risk

Factors

|

20 | ||||

|

Item

1B.

|

Unresolved

Staff Comments

|

31 | ||||

|

Item

2

|

Properties.

|

31 | ||||

|

Item

3

|

Legal

Proceedings

|

32 | ||||

|

PART

II

|

33 | |||||

|

Item

4

|

Market

for Registrant’s Common Equity, Related Stockholder Matters and Issuer

Purchases of Equity Securities.

|

33 | ||||

|

Item

5

|

Selected

Financial Data

|

34 | ||||

|

Item

6

|

Management’s

Discussion and Analysis of Financial Condition and Results of

Operations

|

34 | ||||

|

Item

7

|

Financial

Statements and Supplementary Financial Data

|

58 | ||||

|

Item

8

|

Changes

in and Disagreements With Accountants on Accounting and Financial

Disclosure.

|

58 | ||||

|

Item

8A(T).

|

Controls

and Procedures

|

58 | ||||

|

Item

8B.

|

Other

Information

|

59 | ||||

|

PART

III

|

60 | |||||

|

Item

9

|

Directors,

Executive Officers and Corporate Governance

|

60 | ||||

|

Item

10

|

Executive

Compensation

|

63 | ||||

|

Item

11

|

Security

Ownership of Certain Beneficial Owners and Management and Related

Stockholder Matters.

|

64 | ||||

|

Item

12

|

Certain

Relationships and Related Transactions and Director

Independence

|

66 | ||||

|

Item

13

|

Principal

Accounting Fees and Services.

|

67 | ||||

|

PART

IV

|

68 | |||||

|

Item

14

|

EXHIBITS

AND FINANCIAL STATEMENT SCHEDULES

|

68 |

i

INTRODUCTORY

NOTE

Except as otherwise indicated by the

context, references in this Annual Report on Form 10-K (this “Form 10-K”) to the

“Company,” “LianDi,” “we,” “us” or “our” are references to the combined business

of LianDi Clean Technology Inc. and its consolidated

subsidiaries. References to “Hua Shen HK” are references to our

wholly-owned subsidiary, Hua Shen Trading (International) Ltd.; references to

“China LianDi” are references to our wholly-owned subsidiary, China LianDi Clean

Technology Engineering Ltd.; references to “PEL HK” are to our wholly-owned

subsidiary, Petrochemical Engineering Ltd.; and references to “Beijing JianXin”

are to our wholly-owned subsidiary, Beijing JianXin Petrochemical Technology

Development Ltd. References to “China” or “PRC” are references to the People’s

Republic of China. References to “RMB” are to Renminbi, the legal

currency of China, and all references to “$” and dollar are to the U.S. dollar,

the legal currency of the United States.

Special

Note Regarding Forward-Looking Statements

This report contains forward-looking

statements and information relating to LianDi Clean Technology Inc. that are

based on the beliefs of our management as well as assumptions made by and

information currently available to us. Such statements should not be

unduly relied upon. When used in this report, forward-looking

statements include, but are not limited to, the words “anticipate,” “believe,”

“estimate,” “expect,” “intend,” “plan” and similar expressions, as well as

statements regarding new and existing products, technologies and opportunities,

statements regarding market and industry segment growth and demand and

acceptance of new and existing products, any projections of sales, earnings,

revenue, margins or other financial items, any statements of the plans,

strategies and objectives of management for future operations, any statements

regarding future economic conditions or performance, uncertainties related to

conducting business in China, any statements of belief or intention, and any

statements or assumptions underlying any of the foregoing. These

statements reflect our current view concerning future events and are subject to

risks, uncertainties and assumptions. There are important factors

that could cause actual results to vary materially from those described in this

report as anticipated, estimated or expected, including, but not limited

to: competition in the industry in which we operate and the impact of such

competition on pricing, revenues and margins, volatility in the securities

market due to the general economic downturn; Securities and Exchange Commission

(the “SEC”) regulations which affect trading in the securities of “penny

stocks,” and other risks and uncertainties. Except as required by

law, we assume no obligation to update any forward-looking statements publicly,

or to update the reasons actual results could differ materially from those

anticipated in any forward- looking statements, even if new information becomes

available in the future. Depending on the market for our stock and

other conditional tests, a specific safe harbor under the Private Securities

Litigation Reform Act of 1995 may be available. Notwithstanding the

above, Section 27A of the Securities Act of 1933, as amended (the “Securities

Act”) and Section 21E of the Securities Exchange Act of 1934, as amended (the

“Exchange Act”) expressly state that the safe harbor for forward-looking

statements does not apply to companies that issue penny

stock. Because we may from time to time be considered to be an issuer

of penny stock, the safe harbor for forward-looking statements may not apply to

us at certain times.

1

PART

I

|

Item

1

|

Business

|

Company

Background

We are a holding company that provides

downstream flow equipment and engineering services to China’s leading petroleum

and petrochemical companies. Prior to the consummation of the share

exchange transaction described below, we were a shell company with nominal

operations and nominal assets. Our wholly-owned subsidiary, China LianDi Clean

Technology Engineering Ltd. (“China LianDi”), was established in July 2004 to

serve the largest Chinese petroleum and petrochemical companies. Through our

four operating subsidiaries, which are Hua Shen Trading (International) Ltd.

(“Hua Shen HK”), Petrochemical Engineering Ltd. (“PEL HK”), Bright Flow Control

Ltd. and Beijing JianXin Petrochemical Engineering Ltd. (“Beijing JianXin”), we:

(i) distribute a wide range of petroleum and petrochemical valves and equipment,

including unheading units for the delayed coking process, as well as provide

associated value-added technical services; (ii) provide systems integration

services; and (iii) develop and market proprietary optimization software for the

polymerization process. Our products and services are provided both

bundled or individually, depending on the needs of the

customer.

We are engaged in modernizing China’s

delayed coking industry, and, as such, are strategically positioned to

capitalize on growth opportunities as new technologies enter our market. For

example, in 2011, we plan to install and assemble enclosed unheading units for

the delayed coking process at a facility in China (unheading units are used in

delayed coking to “unhead” or open the coke drum for the removal of the residual

coke). This would represent the first facility of its kind in the

PRC.

We intend to purchase a 16.5-acre land

parcel in the Tianjin Port Industry Area for approximately $5.9 million. We

intend to use the land to construct a new manufacturing facility for our

state-of-the-art, totally enclosed delayed coking unheading units. We expect the

purchase to close within the next 60 days. Upon the closing of the land

purchase, a three-month site preparation project will begin as will our design

of the manufacturing facility. The completion of the new facility will be

accomplished in two major phases: Phase I includes the installation of major

utility infrastructure, which includes water, gas and electricity supply and

Phase II includes the construction of the manufacturing facility. Phase I is

expected to be completed by the end of 2010. Production is expected to begin by

the third quarter of calendar year 2011, with five initial shipments of

unheading units planned for the first full year of production, which is expected

to contribute at least $10 million in revenues for our fiscal year ending March

31, 2012.

Delayed coking refers to a process used

in oil refining. In simple terms, oil refining is a cooking process where crude

oil is subject to extremely high temperatures. When the oil is “cooked,” it will

leave crumbs at the bottom of the refinery. These crumbs are coke. Coke is a

valuable commodity that can be sold for profit. The key is how to clean up the

coke that accumulates at the bottom of the oil refinery plant so that it can be

sold to third parties. Traditionally, China has hired workers with shovels who

shovel the coke into a drum. However, this is a highly inefficient process and

harms the environment because the coke will seep into the air, seep into the

water supply and will seep into the respiratory systems of the workers. We are

modernizing the industry by adapting U.S. technology which automates this

process. This technology automates the process of cleaning up the coke, and in

so doing, minimizes the harmful impact to workers and to the

environment.

Our objectives are to enhance

the reputation of our brand, continue our growth and strengthen our position in

clean technology for the petroleum and petrochemical industry in China. In the

next three years, we intend to strengthen our optimization software for the

polymerization reaction of ethylene production, enhancing its function and

reliability. We intend to leverage our current relationships in the petroleum

and petrochemical industry to become a leading player in clean technology by

bringing totally enclosed unheading units to China. We also intend to expand and

further develop our long-term relationships with our customers, helping them to

reduce their production costs and increase the efficiency and safety of their

facilities.

2

Our

Operating Subsidiaries

Hua Shen HK is a company organized

under the laws of Hong Kong Special Administrative Region of the PRC and was

incorporated in 1999. Beginning in 2005, Hua Shen HK started to distribute

industrial equipment for the petroleum and petrochemical industry. Currently,

Hua Shen HK has become a qualified supplier for China Petroleum & Chemical

Corporation, China National Petroleum Corporation, China National Offshore Oil

Corporation, SinoChem Corporation and ChemChina Group Corporation.

PEL HK was established in Hong Kong

under the laws of Hong Kong Special Administrative Region of the PRC in 2007.

This company primarily distributes petroleum and petrochemical equipment and

provides related technical services. Currently, PEL HK has become a qualified

supplier for China National Petroleum Corporation, China National Offshore Oil

Corporation, SinoChem Corporation, ChemChina Group Corporation and China Shenhua

Energy Company Limited.

Bright Flow Control Ltd. was

established in Hong Kong in 2007. This company is mainly engaged in the

distribution of petrochemical equipment.

Beijing JianXin was incorporated in

Beijing, PRC in May 2008, and is a wholly-owned subsidiary of PEL HK. Beijing

JianXin is mainly engaged in distributing industrial oil and gas equipment and

providing related technical and engineering services, developing and marketing

optimization software for the polymerization process and providing clean

technology solutions for the delayed coking industry. Our customers are large

domestic Chinese petroleum and petrochemical companies and other energy

companies. Currently, Beijing JianXin has five software copyrights and is

qualified as a “software enterprise” that can benefit from an income tax

exemption for two years beginning with its first profitable year and a 50% tax

reduction to a rate of 12.5% for the subsequent three years. We believe this

helps strengthen our position as an industry leader in the clean technology area

and contribute to our growth.

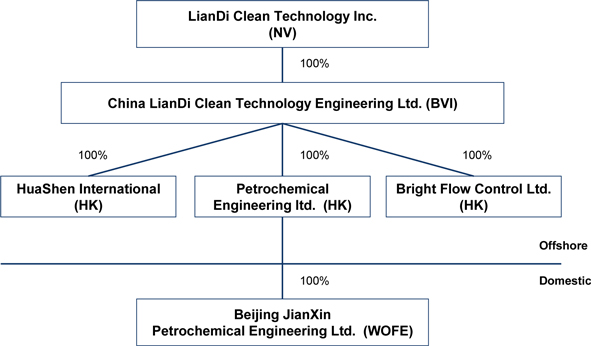

Corporate

Structure

Our

current corporate structure is set forth below:

3

Name

Change

Prior to April 1, 2010, our company

name was Remediation Services, Inc. For the sole purpose of changing our name,

on April 1, 2010, we merged into a newly-formed, wholly owned subsidiary

incorporated under the laws of Nevada called LianDi Clean Technology Inc. As a

result of the merger, our corporate name was changed to LianDi Clean Technology

Inc.

Share

Exchange Agreement with China LianDi and Private Placement

Share

Exchange Agreement

On February 26, 2010 (the “Closing

Date”), we entered into a Share Exchange Agreement (the “Exchange Agreement”),

by and among (i) China LianDi and China LianDi’s shareholders, SJ Asia Pacific

Ltd., a company organized under the laws of the British Virgin Islands, which is

a wholly-owned subsidiary of SJI Inc., a Jasdaq listed company organized under

the law of Japan, China Liandi Energy Resources Engineering Technology Limited,

a company organized under the laws of the British Virgin Islands, Hua Shen

Trading (International) Limited, a company organized under the laws of the

British Virgin Islands, Rapid Capital Holdings Limited, a company organized

under the laws of the British Virgin Islands, Dragon Excel Holdings Limited, a

company organized under the laws of the British Virgin Islands, and TriPoint

Capital Advisors, LLC, a limited liability company organized under the laws of

Maryland (collectively, the “China LianDi Shareholders”), who together owned

shares constituting 100% of the issued and outstanding ordinary shares of China

LianDi (the “China LianDi Shares”) and (ii) Reed Buley, our former principal

stockholder. Pursuant to the terms of the Exchange Agreement, the China LianDi

Shareholders transferred to us all of the China LianDi Shares in exchange for

27,354,480 shares of our common stock (such transaction, the “Share Exchange”).

As a result of the Share Exchange, we are now a holding company, which through

our operating companies in the PRC, provides downstream flow equipment and

engineering services to the leading petroleum and petrochemical companies in the

PRC.

Immediately prior to the Share

Exchange, 4,690,000 shares of our common stock then outstanding were cancelled

and retired, so that immediately prior to the private placement described below,

we had 28,571,430 shares issued and outstanding. China LianDi also deposited

$275,000 into an escrow account which amount was paid to Reed Buley, owner of

the cancelled shares, as a result of the Share Exchange having been

consummated.

Private

Placement

On February 26, 2010 and immediately

following the Share Exchange, we entered into a securities purchase agreement

with certain investors (collectively, the “Investors”) for the issuance and sale

in a private placement of 787,342 units (the “Units”) at a purchase price of $35

per Unit, consisting of, in the aggregate, (a) 7,086,078 shares of Series A

convertible preferred stock, par value $0.001 per share (the “Series A Preferred

Stock”) convertible into the same number of shares of common stock (the

“Conversion Shares”), (b) 787,342 shares of common stock (the “Issued Shares”),

(c) three-year Series A Warrants (the “Series A Warrants”) to purchase up to

1,968,363 shares of common stock, at an exercise price of $4.50 per share (the

“Series A Warrant Shares”), and (d) three-year Series B Warrants (the “Series B

Warrants” and, together with the Series A Warrants, the “Warrants”) to purchase

up to 1,968,363 shares of common stock, at an exercise price of $5.75 per share

(the “Series B Warrant Shares” and, together with the Series A Warrant Shares,

the “Warrant Shares”), for aggregate gross proceeds of approximately $27.56

million (the “Private Placement”). The issuance of the Units was exempt from

registration pursuant to Section 4(2) of the Securities Act, and Regulation D or

Regulation S promulgated thereunder.

In connection with the Private

Placement, we also entered into a registration rights agreement (the

“Registration Rights Agreement”) with the Investors, in which we agreed to file

a registration statement with the SEC to register for resale the Issued Shares,

the Conversion Shares and the Warrant Shares within 30 calendar days of the

Closing Date, and to have such registration statement declared effective within

180 calendar days of the Closing Date. We agreed to keep such registration

statement continuously effective under the Securities Act until such date as is

the earlier of the date when all of the securities covered by such registration

statement have been sold or the date on which such securities may be sold

without any restriction pursuant to Rule144. If we do not comply with the

foregoing obligations under the Registration Rights Agreement, we will be

required to pay cash liquidated damages to each investor, at the rate of 2% of

the applicable subscription amount for each 30 day period in which we are not in

compliance; provided, that such liquidated damages will be capped at 10% of the

subscription amount of each investor and will not apply to any shares that may

be sold pursuant to Rule 144 under the Securities Act, or are subject to an SEC

comment with respect to Rule 415 promulgated under the Securities

Act.

4

We also entered into a make good escrow

agreement with the Investors (the “Securities Escrow Agreement”), pursuant to

which China LianDi Energy Resources Engineering Technology Ltd. (the “Principal

Stockholder”), an affiliate of Jianzhong Zuo, our Chief Executive Officer,

President and Chairman, delivered into an escrow account 1,722,311 shares of

common stock (the “Escrow Shares”) to be used as a share escrow for the

achievement of a fiscal year 2011 net income performance threshold of $20.5

million. With respect to the 2011 performance year, if we achieve less than 95%

of the 2011 performance threshold, then the Escrow Shares for such year will be

delivered to the Investors in the amount of 86,115.55 shares (rounded up to the

nearest whole share and pro rata based on the number of shares of Series A

Preferred Stock owned by such Investor at such date) for each full percentage

point by which such threshold was not achieved up to a maximum of 1,722,311

shares. Any Escrow Shares not delivered to any Investor because such Investor no

longer holds shares of Series A Preferred Stock or Conversion Shares, or because

the 2011 performance threshold was met, shall be returned to the Principal

Stockholder.

For the purposes of the Securities

Escrow Agreement, net income is defined in accordance with US GAAP and reported

by us in our audited financial statements for fiscal year ended 2011; provided,

however, that net income for fiscal year ended 2011 shall be increased by any

non-cash charges incurred (i) as a result of the Private Placement, including

without limitation, as a result of the issuance and/or conversion of the Series

A Preferred Stock, and the issuance and/or exercise of the Warrants, (ii) as a

result of the release of the Escrow Shares to the Principal Stockholder and/or

the Investors, as applicable, pursuant to the terms of the Securities Escrow

Agreement, (iii) as a result of the issuance of ordinary shares of the Principal

Stockholder to its PRC shareholders, upon the exercise of options granted to

such PRC shareholders by the Principal Stockholder, as of the date of the

Securities Escrow Agreement, (iv) as a result of the issuance of Warrants to any

placement agent and its designees in connection with the Private Placement, (v)

the exercise of any Warrants to purchase common stock outstanding and (vi) the

issuance under any performance based equity incentive plan that we adopt. Net

income will also be increased to adjust for any cash or non-cash charges

resulting from the payment of dividends on the Series A Preferred Stock in

connection with the Private Placement.

On the Closing Date, we and China

LianDi Energy Resources Engineering Technology Ltd., an affiliate of Jianzhong

Zuo, our Chief Executive Officer, President and Chairman, entered into a lock-up

agreement whereby such entity is prohibited from selling our securities until

six (6) months after the effective date of the registration statement required

to be filed under the Registration Rights Agreement. For one (1) year

thereafter, it will be permitted to sell up to one-twelfth (1/12) of its initial

holdings every month.

Industry

and Market Overview

China

Petroleum and Petrochemical Industries

According to the U.S. Energy

Information Administration Report dated July 2009, we have obtained the

following industry and market overview.

China consumed an estimated 7.8 million

barrels per day (“bbl/d”) of oil in 2008, making it the second-largest oil

consumer in the world behind the United States. During that same year, China

produced an estimated 4.0 million bbl/d of total oil liquids, of which 96

percent was crude oil. China’s net oil imports were approximately 4.1 million

bbl/d in 2009, again making it the second-largest net oil importer in the world

behind the United States. Energy Information Administration forecasts that

China’s oil consumption will continue to grow during 2010, with oil demand

reaching 8.2 million bbl/d in 2010. This anticipated growth of over 390,000

bbl/d between 2008 and 2010 represents 31 percent of the projected world oil

demand growth in non-OECD countries according to the July 2009 Short-Term Energy

Outlook. According to Oil & Gas Journal (“OGJ”), China had 16 billion

barrels of proven oil reserves as of January 2009.

China’s national oil companies (“NOCs”)

wield a significant amount of influence in China’s oil sector. Between 1994 and

1998, the Chinese government reorganized most state-owned oil and gas assets

into two vertically integrated firms: the China National Petroleum Corporation

(“CNPC”) and the China Petroleum and Chemical Corporation (“Sinopec”). These two

conglomerates operate a range of local subsidiaries, and together dominate

China’s upstream and downstream oil markets. CNPC remains the much larger NOC

and is the leading upstream participant in China. CNPC, along with its

publicly-listed arm PetroChina, accounts for roughly 60 percent and 80 percent

of China’s total oil and gas output, respectively. Sinopec, on the other hand,

has traditionally focused on downstream activities such as refining and

distribution with these sectors making up 76 percent of the company’s revenues

in 2007.

5

Additional state-owned oil firms have

emerged in the competitive landscape in China over the last several years. The

China National Offshore Oil Corporation (“CNOOC”), which is responsible for

offshore oil exploration and production, has seen its role expand as a result of

growing attention to offshore zones. Also, the Company has proven to be a

growing competitor to CNPC and Sinopec by not only increasing its oil

exploration and production expenditures in the South China Sea but also

extending its reach into the downstream sector particularly in the southern

Guangdong Province through its recent 300 billion yuan investment plan. The

Sinochem Corporation and CITIC Group have also expanded their presence in

China’s oil sector, although their involvement in the oil sector remains dwarfed

by CNPC, Sinopec, and CNOOC. The government intends to use the stimulus plan to

enhance energy security and strengthen Chinese NOCs’ global position by offering

various incentives to invest in both upstream and downstream oil

markets.

China

Oil Refineries

China had 6.4 million bbl/d of crude

oil refining capacity at 53 facilities as of January 2009, according to OGJ.

China’s National Energy Administration’s goal is to raise refining capacity to

8.8 million bbl/d by 2011. According to the BP Statistical Review of World

Energy, refinery utilization in China increased from 67 percent in 1998 to 89

percent in 2008.

Sinopec and CNPC are historically the

two dominant providers in China’s oil refining sector, accounting for 50 percent

and 35 percent of the capacity, respectively. However, CNOOC entered the

downstream arena and commissioned the company’s first refinery, the 240,000

bbl/d Huizhou plant, in March 2009 in order to process the high-sulfur crudes

from its Bohai Bay fields. Sinochem has also proposed a number of new

refineries, and national oil companies from Kuwait, Saudi Arabia, Russia, and

Venezuela have entered into joint-ventures with Chinese companies to build new

refining facilities. Sinopec and PetroChina plan to commission about 450,000

bbl/d and 400,000 bbl/d, respectively, of expansion and greenfield capacity by

2011. In light of the recent economic downturn, some firms have postponed

launching refinery projects until product demand picks up again. Also, the

National Development and Reform Commission (“NDRC”) outlined in May 2009 that it

plans to eliminate refineries of 20,000 bbl/d with inefficient equipment and ban

any new projects in efforts to encourage economies of scale and energy

efficiency measures. In addition, PetroChina is branching out to acquire

refinery stakes in other countries in efforts to move downstream and secure more

global trading and arbitrage opportunities. The Company recently purchased a

45.5 percent stake in Singapore Petroleum for $1 billion, and received approval

to purchase 49 percent of Nippon Oil’s Osaka refinery in Japan in June

2009.

The expansive refining sector has

undergone modernization and consolidation in recent years, with dozens of small

refineries, accounting for about 20 percent of total fuel output, shut down and

larger refineries expanding and upgrading their existing systems.

China

Oil Prices

The Chinese government decided to

launch a fuel tax and reform of the country’s product pricing mechanism in

December 2008 to tie retail oil product prices more closely to international

crude oil market, attract downstream investment, ensure profit margins for

refiners, and reduce energy intensity caused by distortions in the market

pricing. When international crude oil prices skyrocketed in mid-2008, the capped

fuel prices downstream caused some refiners, especially the smaller refiners, to

cease production causing supply shortfalls and the major NOCs, particularly

Sinopec, to incur substantial profit losses. In order to stem state-refiners’

losses during the first half of last year, the government issued value added tax

rebates on fuel imports and some direct subsidies.

China is currently taking advantage of

the economic recession to liberalize its pricing system and encourage more

market responsiveness. When fuel prices fluctuate more than 4 percent of the

average crude oil price of three grades for over 22 consecutive working days,

the NDRC can alter the ex-refinery price. The government also sets

transportation charges, processing costs, and refining margins (5% when crude

prices are below $80/bbl). Additionally, a consumption tax and value-added tax

is added for gasoline and diesel fuels. These taxes are set to replace six

transportation fees established by local authorities.

6

Imports

of Heavy Crude Oil

China has swelled into the world’s

second-largest consumer of oil. According to government statistics, China’s

imports have grown from about 6 percent of its oil needs a decade ago, to

roughly one-third in 2004 and are forecast to rise to 60 percent by 2020. China

has emerged from being a net oil exporter in the early 1990s to become the

world’s second-largest net importer of oil in 2009. Despite the economic

slowdown in exports and domestic demand in the past year, China’s demand for

energy remains high. China has turned to the Middle East, South America, Russia,

Central Asia and Africa for sources of crude oil. The Middle East remains the

largest source of China’s oil imports, although African countries also

contribute a significant amount. According to FACTS Global Energy, China

imported 3.6 million bbl/d of crude oil in 2008, of which approximately 1.8

million bbl/d (50%) came from the Middle East, 1.1 million bbl/d (30%) from

Africa, 101,000 bbl/d (3%) from the Asia-Pacific region, and 603,000 bbl/d (17%)

came from other countries. In 2008, Saudi Arabia and Angola were China’s two

largest sources of oil imports, together accounting for over one-third of

China’s total crude oil imports. Recently, China has taken bold steps to

significantly increase its oil imports from Venezuela. The Chinese government

has signed contracts with Venezuela for purchase contracts and production

projects, as part of an effort to diversify and increase oil imports from

Venezuela to 1 million bbl/d from the existing 400,000 bbl/d. In addition,

China’s largest oil producer, CNPC and CNOOC have signed agreements to develop

oil and gas resources in Venezuela. The sound relationship between the Chinese

and Venezuelan governments will contribute to a greater number of partnerships

between Chinese oil production companies and the Venezuelan oil and gas

resources, increasing oil imports from Venezuela.

As China diversifies its crude oil

import sources and expands oil production domestically, state-owned refiners

will have to adjust to the changing crude slate. Traditionally, many of China’s

refineries were built to handle relatively light and sweet crude oils, such as

Daqing and other domestic sources. However, the viscosity and specific gravity

of crude oil from South America and Africa are both higher than the other

countries from which China traditionally acquired imports, especially the heavy

crude oil with high resin from Venezuela. Because delayed coking unit technology

is necessary for processing this crude oil, the increase in heavy crude oil

imports will increase demand for unheading units. Furthermore, China’s growing

dependence on heavy crude oil imports from Venezuela will make it necessary for

refineries across China to acquire advanced technology for the delayed coking

process.

China

Environmental Regulations

In recent years, the Chinese government

has made protection of the environment a priority, strengthening its

environmental legislation. In 2005, the Chinese government’s State Environmental

Protection Administration enacted a new, far-reaching regulatory and

environmental initiative including reduced total emissions by 15% and increasing

China’s energy efficiency by 30%. Furthermore, each province in China has

followed the central government’s directive and established their own targets

for pollution issues that affect their province. Most of the provinces pollution

reduction targets have focused on air pollution caused largely by sulfur dioxide

emissions and water pollution. Also, since China entered the World Trade

Organization in 2001 and has begun to play an increasingly larger role in

international politics, the government has been held more accountable for its

climate footprint. At the Copenhagen Climate Conference, the central Chinese

government pledged to cut emissions by 40 percent and is expected to agree to

new targets to reduce pollution at the next U.N. Climate Summit in Mexico City

December 2010.

Our

Principal Products and Services

Our principal products and services

include:

|

·

|

distributing

a wide range of petroleum and petrochemical valves and equipment,

includingunheading units for the delayed coking process, as well as

providing associated value-addedtechnical

services;

|

|

·

|

providing

systems integration services; and

|

|

·

|

developing

and marketing proprietary optimization software for the polymerization

process.

|

7

Enclosed

Unheading Units

A primary method in the refining

industry of refining crude oil into gasoline, jet and diesel fuel requires a

process known as delayed coking. Delayed coking is the most efficient and

cost-effective solution for refining a range of inferior-grade domestic and

imported crude oil. Delayed coking is a severe form of thermal cracking

requiring high temperatures for an extended period of time, heating crude oil to

high temperatures and pumping it into large pressurized drums. Using a delayed

coking unit, this process breaks the heavy crude oil into lighter, more valuable

fluids which are vaporized and removed, while the solid, unconverted, coal-like

byproduct called “coke” remains in the drum. Due to the extreme temperatures

required in the process and volume of the coke, unheading, or opening both the

bottom and top of the drum to remove the coke, has the potential to be one of

the most dangerous refinery operations and has been the cause of numerous severe

accidents. This portion of delayed coking operations (drum switching and coke

cutting) creates unique hazards, resulting in relatively frequent and serious

accidents due to the significant hands on component required in the process.

Historically, this manual, less efficient and dangerous method has been used in

the process of delayed coking. We are providing a fully automated and totally

enclosed process of delayed coking, eliminating exposure risks for the workers

involved. We believe that this new delayed coking equipment will enjoy broad

adoption by Chinese refineries (broad adoption has already occurred in US and

European markets) due to its improved safety and efficiency.

We have had close relationships with

manufacturers of industrial valves and delayed coking unheading systems. We plan

to install the first totally enclosed unheading units in China in 2011 for

Sinochem Quanzhou. In addition, as part of one of our many potential growth

strategies, we are in discussions to invest in the first facility in China to

manufacture select supporting components and assemble the unheading units for

DeltaValve, a division of Curtiss-Wright Flow Control Corporation

(“DeltaValve”). Investing in a facility like the potential venture with

DeltaValve would allow us to significantly increase our gross margin on the sale

of unheading units.

We intend to purchase a 16.5-acre land

parcel in the Tianjin Port Industry Area for approximately $5.9 million. We

intend to use the land to construct a new manufacturing facility for our

state-of-the-art, totally enclosed delayed coking unheading units. We expect the

purchase to close within the next 60 days. Upon the closing of the land

purchase, a three-month site preparation project will begin as will our design

of the manufacturing facility. The completion of the new facility will be

accomplished in two major phases: Phase I includes the installation of major

utility infrastructure, which includes water, gas and electricity supply and

Phase II includes the construction of the manufacturing facility. Phase I is

expected to be completed by the end of 2010. Production is expected to begin by

the third quarter of calendar year 2011, with five initial shipments of

unheading units planned for the first full year of production, which is expected

to contribute at least $10 million in revenues for our fiscal year ending March

31, 2012.

The DeltaValve unheading unit has

significant safety advantages over all other currently available unheading

equipment because it eliminates exposure risks to personnel and the atmosphere.

With a fully automated system, workers are safely able to conduct unheading

delayed coking remotely and mitigate potential dangers. In addition, these

unheading units significantly increase refinery throughput and lower operation

costs.

An unheading unit with one-million ton

annual capacity can generate a total economic benefit of $7.4 million for our

customers for the following reasons:

· cost

per unit installation is $3 million, and total cost for an upgraded delayed

coking system is recouped typically within one year;

· 30% – 40%

less expensive to buy than the competing product from Z&J Technologies

GmbH;

· shorter

cycle times and reduced maintenance expenses;

· lower

costs for water usage and wastewater treatment;

· increased

ability to process inferior grades of crude oil; and

· 25%

tax deduction for energy saving and environment-friendly products.

Currently, there are 120 existing

coking units in China that could potentially benefit from a totally enclosed

unheading unit. The number of coking units is expected to grow at a rate of 10%

annually and is projected to have a market size of almost $1 billion over the

next 10 years, of which we expect significant penetration.

8

Distribution

& Technical Services

We distribute hundreds of different

types of valves and related equipment from manufacturers/suppliers such as

Cameron (NYSE: CAM) and Poyam Valves. We also provide related value-added

technical services to manufacturers and petroleum and petrochemical companies.

We provide locally customized technical services for international companies who

sell products in China but who do not have local offices. For these companies,

we offer our services by enlisting our engineers on the ground to provide

localized services for their products. Our technical services include, but are

not limited to: communicating with the R&D arms of the large Chinese oil

companies; verifying and confirming the specification of products; and product

inspecting, maintenance and debugging assistance.

Currently we are negotiating with a

large manufacturer to set up its valve technology service center in China. We

will provide their technical services and conduct marketing campaigns in the

Chinese market. We have also provided technical services to principle European

manufacturers and assisted one to become the vender of block valves for the

second line in the West-East Gas Pipeline Project.

Systems

Integration

We provide systems integration services

for self-control of the chemical production process. This process includes

integration of storage operations and transportation of valve instruments from

tank farms, as well as providing upgrading services of programmable logic

controllers with instrument systems. Currently, we are undertaking systematic

integrations of operations in several chemical plant tank farm

projects.

Software

Polymerization reaction is very

important in the petrochemical process. It converts ethylene, propylene and

other major gas-phase products into solid products which in turn can be further

processed. Polymerization provides raw materials for downstream industries. The

conditions important to the polymerization reaction process are mainly

temperature, pressure, flow, liquid level and the catalyst. Prior to using a new

process or before a catalyst is put into mass production, as well as before

products are officially used, the process needs to be tested. Our software helps

test the processes by producing data collection, performance analysis and

process optimization indications. Polymerization reaction data collection and

analysis software provides production process automation control. Our software

can also be applied to other industries including the coal and steel

industries.

Depending on customers’ needs, our

products and services may be bundled together or provided

individually.

Our

Competitive Strengths

Our

competitive strengths include:

Product

advantages

We import high-quality petroleum and

petrochemical valves and distribute them to our domestic clients who are large

petroleum and petrochemical companies located and operating in China. Our

suppliers are global and reputable industrial equipment manufacturers with

leading technology among their competitors. Our international suppliers include

Cameron, DeltaValve and Poyam Valves. We also work with the R&D subsidiaries

of CNPC and Sinopec, as well as other independent research institutes, to

determine standards in the petroleum and petrochemical industries. Our software

is used by petrochemical companies during the polymerization reaction of

ethylene production for data collection, performance analysis and process

optimization. We believe it has several advantages over similar products,

including lower costs, better quality control, improved process optimization and

customization to individual customers.

9

Client

relationship advantages

Most of the petroleum and petrochemical

companies are very large state-owned enterprises in China which set high

standards and thresholds for products and services providers. We have agreements

with the three largest industry leaders, CNOOC, Sinochem Group and CNPC, to

provide equipment and technical services and have worked closely with them for

almost 10 years. Material terms of the agreements vary, however, our key

management personnel have at least 10-20 years of experience in the industry,

have established broad channels and networks within the industry and have earned

the trust of these large state-owned industry leaders. We have also maintained

strong relationships with our suppliers and research institutions.

Research

and development advantage

We have partnered with the leading

industrial research and development institutions throughout China to develop

standards for the petroleum and petrochemical industries, which has led to the

development of our integrated products and services and their achievement of a

higher level of technological sophistication as compared with our competitors.

Specifically, we have partnered and/or worked with Luoyang Petrochemical

Engineering Corporation and Sinopec Engineering Incorporation, which are R&D

institutions wholly owned by Sinopec; and China Huanqiu Contracting &

Engineering Corporation and China Petroleum Pipeline Engineering Corporation,

which are R&D institutions wholly owned by CNPC. These engineering companies

are actually Sinopec and CNPC’s R&D institutions. These companies assist

Sinopec and CNPC with the design and construction of both new and old production

facilities. Generally, our role focuses on assisting these companies with

locating suitable products from around the world to complete various aspects of

the facilities design. For example, the Company uses its expertise in flow

control equipment to help identify and select valves and other equipment that

meet specific design requirements.

We currently have approximately 120

employees, many from China’s largest petroleum and petrochemical companies and

research and development subsidiaries and possessing extensive technology and

R&D capabilities.

Comprehensive

localized system integration advantage

We have accumulated more than five

years of comprehensive system integration services experience with a relatively

stable base of clients and products and an effective operational team. This

experience has allowed us to emerge as a high-end integrator of industrial

products and related engineering services. We have the ability to understand our

customers’ current systems and needs, and then design the total solution to

integrate international products and technologies with their local

systems.

Clean

technology advantage

We are engaged in modernizing China’s

delayed coking industry by being the first company to bring DeltaValve’s

affordable, environment-friendly, safe and maintenance-free coke-drum enclosed

unheading system to the Chinese marketplace. The delayed coking process produces

more pollution than any other refining step. The totally enclosed unheading

units we distribute and install significantly reduce emissions. Given the

Chinese government’s aggressive industry targets to reduce air pollution,

traditional delayed coking units will have to be updated. In addition, our

product is superior in price, performance and reliability.

Benefit

from income tax policy

Our PRC subsidiary, Beijing JianXin,

has been qualified as a software enterprise by the related government

authorities. Accordingly, Beijing JianXin can benefit from an income tax

exemption for two years beginning with its first profitable year of 2009 and a

50% tax reduction to a rate of 12.5% for the subsequent three years. This tax

benefit will reduce the capital demands in our operating activities and allow us

to invest more funding into long-term projects and to better serve our

clients.

Experienced

workforce

Currently, many of our senior managers

and engineers have significant prior experience in the petroleum and

petrochemical industry. Many of our employees have graduated from petrochemical

based institutions and colleges. Our executive team has over 100 years of

management experience in the aggregate and provides excellent operating and

technical administration for our company.

10

Healthy

financial growth

We are projecting 100% year-to-year net

income growth for fiscal year 2010 ending March 31, 2010, compared with that of

2009, and 67.7% year-to-year projected organic net income growth to $25 million

for fiscal year 2011.

Supplier

Relationships

We distribute high quality products of

international suppliers, which affords us a distinctive reputation and

significant profit. We have close relationships with reputable brand name

manufacturers, and remain the largest distributor of many of their products in

China. For example, we currently have agreements with AMPO S. COOP — Poyam

Valves (“AMPO”) and DeltaValve. Both AMPO and DeltaValve are equipment

suppliers. We have signed an agreement with AMPO dated January 2010, where we

will set up an after-sale services institution in China of AMPO valves and

provide spare parts of AMPO valves to the China market. The agreement is for the

duration of 2 years with the option to sign additional agreements after

expiration. We also recently signed an agreement with DeltaValve dated February

2010 to be an independent distributor for purchase and resale of coker unheading

systems, isolation valves and related spare parts for 2 years.

A description of each of these

agreements is as follows:

After-sale

Services Agreement by and between AMPO S. coop Poyam Valves and Petrochemical

Engineering Limited

On June 17, 2009, we entered into a

two-year agreement with AMPO S. coop Poyam Valves pursuant to which AMPO

appointed us as a provider of after-sale services for AMPO products in China.

Pursuant to this agreement, AMPO provides training to our engineers, who in turn

service AMPO products for customers. We are prohibited from providing

after-sale services for any competitor of AMPO in any territory where we provide

after-sale services for AMPO, and we warrant our repairs for 6 months. For

service that falls within AMPO’s warranty to its customers, AMPO pays us between

RMB 200 and 600 / hour / person for our engineers’ time, plus travel

costs. Otherwise, the end-user pays AMPO at negotiated

rates. Either party may terminate the agreement on three months

notice.

International

Distributor Agreement Between DeltaValve and PetroChemical Engineering

Limited

On February 12, 2010, we entered into a

two-year agreement with Curtiss-Wright Flow Control Corporation, a Delaware

corporation, acting through its DeltaValve Division, pursuant to which

DeltaValve appointed us to act as an independent distributor of certain of its

products in order to market, promote service and sell DeltaValve products in

China. Pursuant to this agreement, we agreed to purchase at least

$10,000,000 of DeltaValve Coker Unheading Systems, Isolation Valves and related

spares parts per year for resale. The agreement restricts us from

providing similar services to any entity within China providing competing

products. DeltaValve may terminate the agreement at will upon 90 days

notice, or otherwise for cause. Upon termination, DeltaValve determines whether

we may sell our existing inventory of its products to end-users or whether we

must sell them to DeltaValve at then current prices less any applicable

discounts or at the net price paid by us, whichever is lower. Such

sales, as applicable, are our only remedies for the termination or expiration of

the agreement and shall be in lieu of all other claims.

Growth

Strategy

We plan to strengthen our leading

position and achieve rapid growth through the following strategies:

|

·

|

Product

localization: we plan to localize our products by establishing a

manufacturing andassembly facility in China, which will significantly

decrease our costs and increase ourcompetitive

strength;

|

|

·

|

Strengthen

our research and development effort to increase the functions and the

stability of ouroptimization software to increase the sales volume of our

software products which have arelatively high gross margin;

and

|

|

·

|

Expand

our distribution channels and network by increasing the sales force to

collect moreindustrial information and enhance the communication with

existing potential clients.

|

11

Competition

We compete against other companies

which seek to provide the Chinese petroleum refinery industry with a wide range

of petroleum and petrochemical valves and equipment and associated technical and

engineering services. Much like us, these companies compete on the basis of

cost, the size of their distribution product portfolio, and level of technical

and engineering expertise. In addition, similar products to those distributed by

us are available from domestic Chinese and foreign manufacturers and compete

with the products in our distribution portfolio.

Z&J Technologies GmbH is a German

industrial valve company and a direct competitor to China LianDi/DeltaValve’s

enclosed unheading units. Honeywell is also a competitor of China LianDi’s

optimization software.

Methods

of Distribution

We maintain aggressive sales channels

and distribution networks in China with an approximately 21 member sales team.

We have spent significant amount of time developing relationships with

international equipment suppliers, and with the PRC’s largest petroleum and

petrochemical companies.

Our

Suppliers

We maintain close relationships with,

and distribute products for large, industry leading valve and equipment

manufacturers, including Cameron, Poyam Valves, Rotork, Perar S.p.A, Kanon

Loading Equipment BV, and DeltaValve. Most of our suppliers renew annually,

though some suppliers have signed multi-year agreements. We expect all existing

supplier relationships will continue on an ongoing basis, and that going forward

we will add new partners to diversify our supplier base.

Significant

Customers

For the fiscal year ended March 31,

2010, our major customer breakdown as a percentage of revenues was as follows:

Sinopec: 51%; CNPC: 40%; and other: 9%. We are dependent on China’s largest

petroleum and petrochemical companies in our distribution business. As we grow

our business, we intend to diversify our customer relationships that can benefit

from our technology and software business.

Research and

Development

We have partnered with the leading

industrial research and development institutions throughout the PRC to develop

standards for the petroleum and petrochemical industries, which has led to the

development of our integrated products and services and their achievement of a

higher level of technological sophistication as compared with our

competitors.

The leading industrial research and

development institutions we have partnered with are Luoyang Petrochemical

Engineering Corporation and Sinopec Engineering Incorporation, which are R&D

institutions wholly owned by Sinopec; and China Huanqiu Contracting &

Engineering Corporation and China Petroleum Pipeline Engineering Corporation,

which are R&D institutions wholly owned by CNPC. These engineering companies

are actually Sinopec and CNPC’s R&D institutions. They assist Sinopec and

CNPC with the design and construction of both new and old production facilities.

During this process, the Company’s role focuses primarily on assisting these

companies with locating suitable products from around the world to complete

various aspects of the facilities design. For example, the Company uses its

expertise in flow control equipment to help identify and select valves and other

equipment that meet specific design requirements.

Specifically, our engineering staff

understands all specifications, budget parameters and functional project

requirements. We then use this understanding to find suitable products and

suppliers. As part of this process, we help our partners reduce costs by

designing and/or improving certain systems, including hydraulic systems, control

systems, supporting bracket, and other systems. Finally, we assist with the

integration of these products within their core products.

We currently have approximately 40

employees dedicated to research and development activities. During the fiscal

year ended March 31, 2010, we spent approximately $91,000 on such

activities.

12

Government

Regulation

Our business operations do not require

any special government licenses or permits.

Compliance

with Environmental Laws

We believe that we are in compliance

with the current material environmental protection requirements. Our costs

attributed to compliance with environmental laws is negligible.

Intellectual

Property

The PRC has adopted legislation

governing intellectual property rights, including patents, copyrights and

trademarks. The PRC is a signatory to the main international conventions on

intellectual property rights and became a member of the Agreement on Trade Related Aspects

of Intellectual Property Rights upon its accession to the WTO in December

2001.

We have five software copyright

certificates issued by the State Copyright Office of the PRC as listed

below:

|

Names of Software

|

Registration Number

|

|

V1.0 V1.0 |

2008SRBJ6676

|

|

|

Software

V1.0 of Data Processing Platform for Chemical Production

System.

|

||

V1.0 V1.0 |

2009SRBJ5672

|

|

|

Software

V1.0 of Dispatch Management Platform for Oil and Gas

Pipeline

|

||

V1.0 V1.0 |

2009SR036455

|

|

|

Software

V1.0 of Automatic Calibration for Oil and Gas Pipeline Measuring

Station

|

||

V1.0 V1.0 |

2009SR036454

|

|

|

Software

V1.0 of Data Collection Post-Processing Platform

|

||

V1.0 V1.0 |

2009SRBJ5783

|

With this

intellectual property, we believe we can facilitate the services that are in

demand by our customers.

Legal

Proceedings

We are currently not a party to any

material legal or administrative proceedings and are not aware of any pending or

threatened legal or administrative proceedings against us in all material

aspects. We may from time to time become a party to various legal or

administrative proceedings arising in the ordinary course of our

business.

Employees

As of March 31, 2010, we had 124

full-time employees, including 40 in technology and R&D; 39 engineers; 21 in

sales; 6 members of management and 18 others, including accounting,

administration and human resources.

We are compliant with local prevailing

wage, contractor licensing and insurance regulations, and have good relations

with our employees.

As required by PRC regulations, we

participate in various employee benefit plans that are organized by municipal

and provincial governments, including pension, work-related injury benefits,

maternity insurance, medical and unemployment benefit plans. We are required

under PRC laws to make contributions to the employee benefit plans at specified

percentages of the salaries, bonuses and certain allowances of our employees, up

to a maximum amount specified by the local government from time to time. Members

of the retirement plan are entitled to a pension equal to a fixed proportion of

the salary prevailing at the member’s retirement date.

13

Generally, we enter into a standard

employment contract with our officers and managers for a set period of years and

a standard employment contract with other employees for a set period of years.

According to these contracts, all of our employees are prohibited from engaging

in any activities that compete with our business during the period of their

employment with us. Furthermore, the employment contracts with officers or

managers include a covenant that prohibits officers or managers from engaging in

any activities that compete with our business for two years after the period of

employment.

Corporation

Information

Our principal executive offices are

located at Unit 401-405.4/F, Tower B, Wanliuxingui Building, 28 Wanquanzhuang

Road, Haidian District, Beijing, China 100089, Tel: (86) (0)10-5872 0171, Fax:

(86) (0)10-5872 0181.

PRC

Government Regulations

Our operations are subject to numerous

laws, regulations, rules and specifications of the PRC relating to various

aspects. We are in compliance in all material respects with such laws,

regulations, rules, specifications and have obtained all material permits,

approvals and registrations relating to human health and safety, the

environment, taxation, foreign exchange administration, financial and auditing,

and labor and employments. We make capital expenditures from time to time to

stay in compliance with applicable laws and regulations. Below we set forth a

summary of the most significant PRC regulations or requirements that may affect

our business activities operated in the PRC or our shareholders’ right to

receive dividends and other distributions of profits from Beijing JianXin, a

wholly foreign owned enterprise under the PRC laws.

Business

license

Any company that conducts business in

the PRC must have a business license that covers a particular type of work. The

business license of Beijing JianXin covers its present business of distributing

industrial oil and gas equipment and providing related technical and engineering

services, developing and marketing optimization software for the polymerization

process and providing clean technology solutions for the delayed coking

industry. Prior to expanding Beijing JianXin’s business beyond that of its

business license, we are required to apply and receive approval from the PRC

government.

Annual

Inspection

In accordance with relevant PRC laws,

all types of enterprises incorporated under the PRC laws are required to conduct

annual inspections with the State Administration for Industry and Commerce of

PRC or its local branches. In addition, foreign-invested enterprises are also

subject to annual inspections conducted by PRC government authorities. In order

to reduce enterprises’ burden of submitting inspection documentation to

different government authorities, the Measures on Implementing Joint

Annual Inspection issued by the PRC Ministry of Commerce together with

other six ministries in 1998 stipulated that foreign-invested enterprises shall

participate in a joint annual inspection jointly conducted by all relevant PRC

government authorities. Beijing JianXin, as a foreign-invested enterprise, has

participated and passed all such annual inspections since its establishment on

May 6, 2008.

Employment

laws

We are subject to laws and regulations

governing our relationship with our employees, including: wage and hour

requirements, working and safety conditions, citizenship requirements, work

permits and travel restrictions. These include local labor laws and regulations,

which may require substantial resources for compliance.

14

China’s National Labor Law,

which became effective on January 1, 1995, and China’s National Labor Contract

Law, which became effective on January 1, 2008, permit workers in both

state and private enterprises in China to bargain collectively. The National Labor Law and the

National Labor Contract

Law provide for collective contracts to be developed through

collaboration between the labor union (or worker representatives in the absence

of a union) and management that specify such matters as working conditions, wage

scales, and hours of work. The laws also permit workers and employers in all

types of enterprises to sign individual contracts, which are to be drawn up in

accordance with the collective contract.

Foreign

Investment in PRC Operating Companies

The Foreign Investment Industrial

Catalogue jointly issued by the Ministry of Commerce, or the MOFCOM, and

the National Development and Reform Commission, or the NDRC, in 2007 classified

various industries/businesses into three different categories: (i) encouraged

for foreign investment; (ii) restricted to foreign investment; and (iii)

prohibited from foreign investment. For any industry/business not covered by any

of these three categories, they will be deemed industries/businesses permitted

to have foreign investment. Except for those expressly provided restrictions,

encouraged and permitted industries/businesses are usually 100% open to foreign

investment and ownership. With regard to those industries/businesses restricted

to or prohibited from foreign investment, there is always a limitation on

foreign investment and ownership. Beijing JianXin’s business does not fall under

the industry categories that are restricted to, or prohibited from foreign

investment and is not subject to limitation on foreign investment and

ownership.

Regulation

of Foreign Currency Exchange

Foreign currency exchange in the PRC is

governed by a series of regulations, including the Foreign Currency Administrative

Rules (1996), as amended, and the Administrative Regulations Regarding

Settlement, Sale and Payment of Foreign Exchange (1996), as amended.

Under these regulations, the Renminbi is freely convertible for trade and

service-related foreign exchange transactions, but not for direct investment,

loans or investments in securities outside the PRC without the prior approval of

the State Administration of Foreign Exchange, or SAFE. Pursuant to the Administrative Regulations Regarding

Settlement, Sale and Payment of Foreign Exchange (1996), Foreign Invested

Enterprises, or FIEs, may purchase foreign exchange without the approval of the

SAFE for trade and service-related foreign exchange transactions by providing

commercial documents evidencing these transactions. They may also retain foreign

exchange, subject to a cap approved by SAFE, to satisfy foreign exchange

liabilities or to pay dividends. However, the relevant Chinese government

authorities may limit or eliminate the ability of FIEs to purchase and retain

foreign currencies in the future. In addition, foreign exchange transactions for

direct investment, loan and investment in securities outside the PRC are still

subject to limitations and require approvals from the SAFE.

Regulation

of FIEs’ Dividend Distribution

The principal laws and regulations in

the PRC governing distribution of dividends by FIEs include:

|

|

(i)

|

The

Sino-foreign Equity Joint Venture Law (1979), as amended, and the

Regulations for the Implementation of the Sino-foreign Equity Joint

Venture Law (1983), as amended;

|

|

|

(ii)

|

The

Sino-foreign Cooperative Enterprise Law (1988), as amended, and the

Detailed Rules for the Implementation of the Sino-foreign Cooperative

Enterprise Law (1995), as amended;

|

|

|

(iii)

|

The

Foreign Investment Enterprise Law (1986), as amended, and the Regulations

of Implementation of the Foreign Investment Enterprise Law (1990), as

amended.

|

Under these regulations, FIEs in the

PRC may pay dividends only out of their accumulated profits, if any, determined

in accordance with Chinese accounting standards and regulations. In addition,

foreign-invested enterprises in the PRC are required to set aside at least 10%

of their respective accumulated profits each year, if any, to fund certain

reserve funds unless such reserve funds have reached 50% of their respective

registered capital. These reserves are not distributable as cash dividends. The

board of directors of a FIE has the discretion to allocate a portion of its

after-tax profits to staff welfare and bonus funds, which may not be distributed

to equity owners except in the event of liquidation.

15

Regulation

of a Foreign Currency’s Conversion into RMB and Investment by FIEs

On August 29, 2008, the SAFE issued a

Notice of the General Affairs Department of the State Administration of Foreign

Exchange on the Relevant Operating Issues concerning the Improvement of the

Administration of Payment and Settlement of Foreign Currency Capital of

Foreign-Invested Enterprises or Notice 142, to further regulate the foreign

exchange of FIEs. According to the Notice 142, FIEs shall obtain verification

report from a local accounting firm before converting its registered capital of

foreign currency into Renminbi, and the converted Renminbi shall be used for the

business within its permitted business scope. The Notice 142 explicitly

prohibits FIEs from using RMB converted from foreign capital to make equity

investments in the PRC, unless the domestic equity investment is within the

approved business scope of the FIE and has been approved by SAFE in

advance.

Regulation

of Foreign Exchange in Certain Onshore and Offshore Transactions

In October 2005, the SAFE issued the

Notice on Issues Relating to the Administration of Foreign Exchange in

Fund-raising and Return Investment Activities of Domestic Residents Conducted

via Offshore Special Purpose Companies, or SAFE Notice 75, which became

effective as of November 1, 2005, and was further supplemented by two

implementation notices issued by the SAFE on November 24, 2005 and May 29, 2007,

respectively. SAFE Notice 75 states that PRC residents, whether natural or legal

persons, must register with the relevant local SAFE branch prior to establishing

or taking control of an offshore entity established for the purpose of overseas

equity financing involving onshore assets or equity interests held by them. The

term “PRC legal person residents” as used in SAFE Notice 75 refers to those

entities with legal person status or other economic organizations established

within the territory of the PRC. The term “PRC natural person residents” as used

in SAFE Notice 75 includes all PRC citizens and all other natural persons,

including foreigners, who habitually reside in the PRC for economic benefit. The

SAFE implementation notice of November 24, 2005 further clarifies that the term

“PRC natural person residents” as used under SAFE Notice 75 refers to those “PRC

natural person residents” defined under the relevant PRC tax laws and those

natural persons who hold any interests in domestic entities that are classified

as “domestic-funding” interests.

PRC residents are required to complete

amended registrations with the local SAFE branch upon: (i) injection of equity

interests or assets of an onshore enterprise to the offshore entity, or (ii)

subsequent overseas equity financing by such offshore entity. PRC residents are

also required to complete amended registrations or filing with the local SAFE

branch within 30 days of any material change in the shareholding or capital of

the offshore entity, such as changes in share capital, share transfers and

long-term equity or debt investments or, providing security, and these changes

do not relate to return investment activities. PRC residents who have already

organized or gained control of offshore entities that have made onshore

investments in the PRC before SAFE Notice 75 was promulgated must register their

shareholdings in the offshore entities with the local SAFE branch on or before

March 31, 2006.

Under SAFE Notice 75, PRC residents are

further required to repatriate into the PRC all of their dividends, profits or

capital gains obtained from their shareholdings in the offshore entity within

180 days of their receipt of such dividends, profits or capital gains. The

registration and filing procedures under SAFE Notice 75 are prerequisites for

other approval and registration procedures necessary for capital inflow from the

offshore entity, such as inbound investments or shareholders loans, or capital

outflow to the offshore entity, such as the payment of profits or dividends,