Attached files

| file | filename |

|---|---|

| 8-K - SUNOCO INC--FORM 8-K - SUNOCO INC | d8k.htm |

| EX-99.2 - PRESS RELEASE - SUNOCO INC | dex992.htm |

Sunoco, Inc.

ANALYST MEETING

JUNE 16, 2010

Exhibit 99.1 |

2

Statements in this presentation that are not historical facts are

forward-looking statements intended to be covered by the safe harbor

provisions of Section 27A of the Securities Act of 1933 and Section 21E of the

Securities

Exchange

Act

of

1934.

These

forward-looking

statements

are

based

upon

assumptions

by

Sunoco

concerning

future

conditions,

any

or

all

of

which

ultimately

may

prove

to

be

inaccurate,

and

upon

the

current

knowledge, beliefs and expectations of Sunoco management. These forward-looking

statements are not guarantees of future performance.

Forward-looking statements are inherently uncertain and involve significant

risks and uncertainties that could cause actual results to differ materially

from those described during this presentation. Such risks and uncertainties

include economic, business, competitive and/or regulatory factors affecting Sunoco's business,

as

well

as

uncertainties

related

to

the

outcomes

of

pending

or

future

litigation.

In

accordance

with

the

safe

harbor provisions of the Private Securities Litigation Reform Act of 1995, Sunoco

has included in its Annual Report on Form 10-K for the year ended

December 31, 2009, and in its subsequent Form 10-Q and Form 8- K

filings, cautionary language identifying important factors (though not necessarily all such factors) that could

cause

future

outcomes

to

differ

materially

from

those

set

forth

in

the

forward-looking

statements.

For

more

information concerning these factors, see Sunoco's Securities and Exchange

Commission filings, available on Sunoco's website at www.SunocoInc.com.

Sunoco expressly disclaims any obligation to update or alter its

forward-looking statements, whether as a result of new information, future events or otherwise.

This presentation includes certain non-GAAP financial measures intended to

supplement, not substitute for, comparable GAAP measures. Reconciliations of

non-GAAP financial measures to GAAP financial measures are

provided

in

the

Appendix

at

the

end

of

this

presentation.

Investors

are

urged

to

consider

carefully

the

comparable GAAP measures and the reconciliations to those measures provided in the

Appendix, or on our website at www.SunocoInc.com.

Safe Harbor Statement |

3

Refining

& Supply

1,100

Chemicals

690

Logistics

1,070

Lynn Elsenhans, Chairman, CEO and President………..

15 minutes

Bob Owens, SVP of

Marketing…………………………….

30 minutes

Mike Hennigan, President and COO of

Sunoco Logistics Partners,

L.P…………………………… 30

minutes Anne-Marie Ainsworth, SVP of

Refining…………………. 30 minutes

Break………………………………………………………….

15 minutes

Mike Thomson, SVP and President of SunCoke………..

40 minutes

Brian MacDonald, SVP and

CFO…………………………. 20

minutes Q &

A………………………………………………………….

30 minutes

Agenda |

Sunoco, Inc.

Lynn Elsenhans |

5

Refining

& Supply

1,100

Chemicals

690

Logistics

1,070

Market demand for transportation fuels will exist for a long time

Biofuels

and other alternatives will become increasingly available

Sunoco wants to provide the alternatives that customers demand

Ownership and operation of terminals becomes essential to meet

these marketplace needs

Capability at terminals to blend a variety of fuels

Use Sunoco brand to pull those fuels through our network

Refining will be a source of supply through our network

Focus on safety, reliability and being cost competitive

Market View |

6

Refining

& Supply

1,100

Chemicals

690

Logistics

1,070

Optimize the Refining/Logistics and Retail operations with

the aspiration of becoming the premier fuel supplier within

the markets in which we operate

Strengthen our fuels business through improved retail

operations and growth opportunities in both Logistics and

Retail Marketing

Improve the reliability of our refining assets

Maintain financial flexibility and discipline

Sunoco Strategy |

Marketing

Bob Owens |

|

9

Optimize margins across all marketing channels

“Pull”

more volume thru high netback sites

Retail Marketing

Operations excellence is essential

Brand equity is a driver of value creation

Real estate aggressively managed

Supply and Distribution

Alignment with Retail Marketing

Opportunity to create value

BioFuels

–

Participate in the evolving transportation fuels

marketplace

Ethanol manufacturing

Distribution and marketing at retail sites

Value Creation |

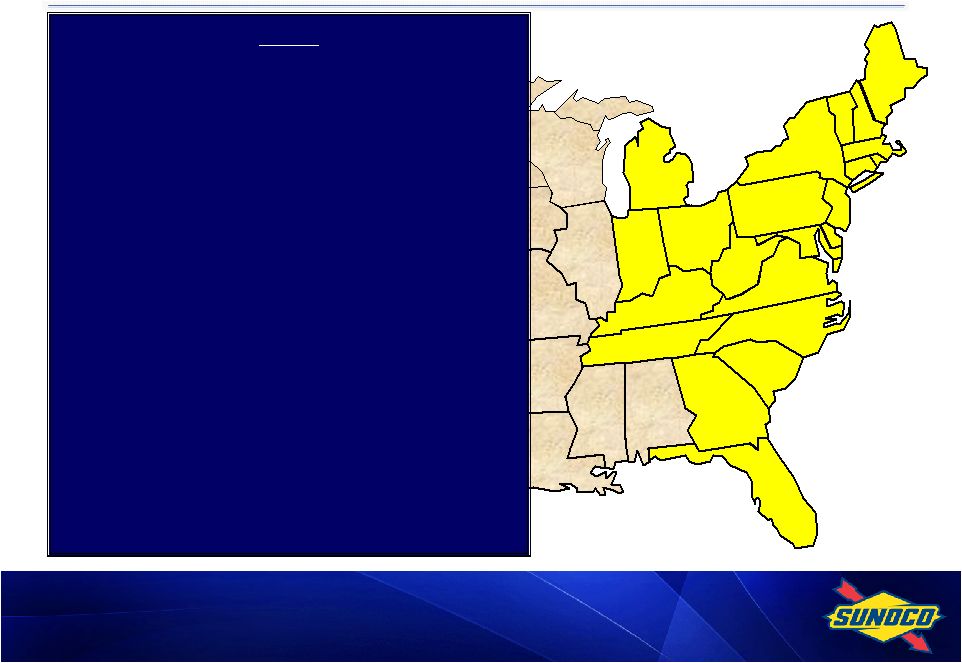

10

Retail

Marketing

Profile

FL

PA

WV

VA

FL

SC

NC

NY

ME

NH

VT

OH

MI

IN

KY

TN

GA

NJ

CT

DE

MD

2009

Refined Volume

4.9B gallons EBITDA

$241MM

EBITDA –

6 yr avg* $219MM

Total Retail Outlets 4,711

Distributors sites 3,312

Dealers sites

1,004

Co-op

sites 395

*Excludes 2008, when EBITDA=$439MM

MA

RI |

11

Brand

Value –

Building Customer Loyalty

1

2

3

4

5

6

7

8

Exxon/Mobil

5

Shell

6

Chevron

4

Bronze

Texaco

3

Silver

Sunoco

2

Gold

BP

1

Brandweek

Customer

Loyalty

Award

Ranking

High quality performance

fuel

Strong station image and

customer service

Delivering effective

marketing programs

Competitive alternative

profit centers in APlus

convenience stores and

Ultra Service Centers

st

nd

rd

th

th

th |

12

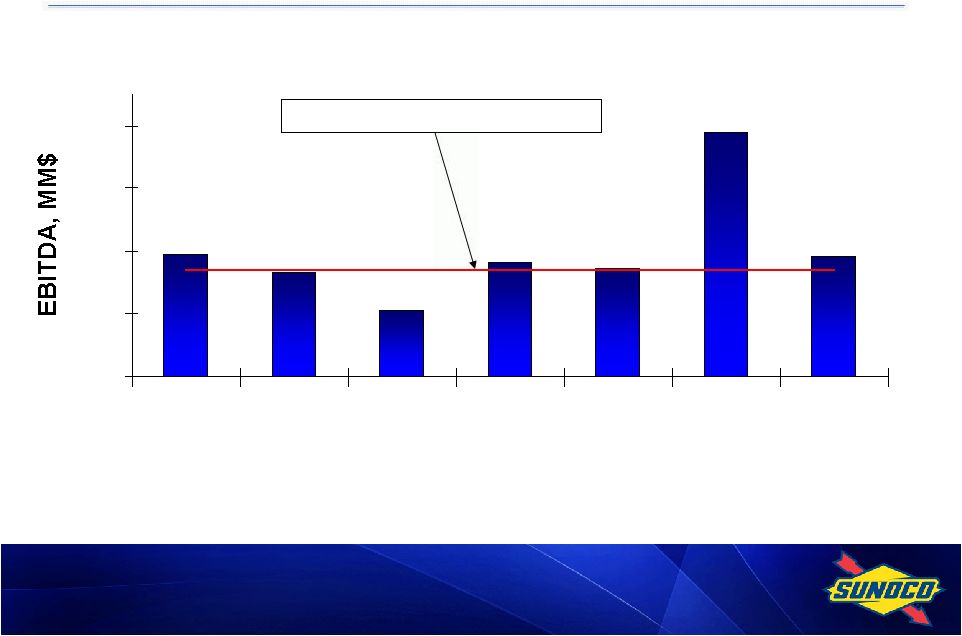

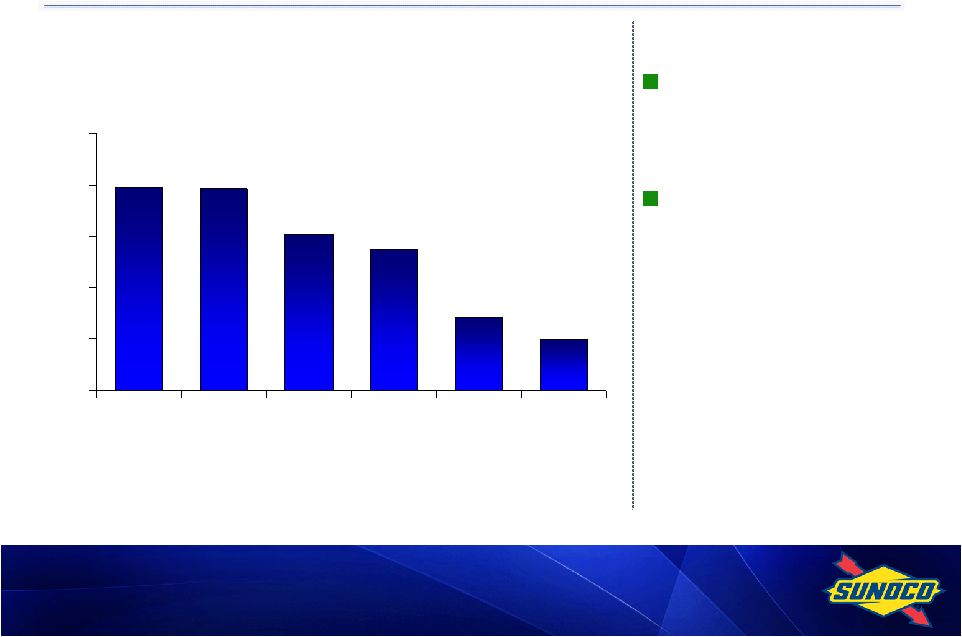

Financial Performance

6 year avg EBITDA, excluding 2008

* For reconciliation to Net Income, see Slide A1.

Retail Marketing Provides Steady Earnings & Cash Flow

244

221

439

241

155

233

217

50

150

250

350

450

2003

2004

2005

2006

2007

2008

2009 |

13

0

20

40

60

80

100

120

140

2008

2009

2010P

"Stay in Business"

Income Improvement

$MM

Manage Capital Spending

Future “stay in business”

capital to average $80

million

Income improvement capital

includes turnpike

refurbishments and “raze

and rebuilds”

Capital allocated to growth

projects

Organic growth

Distributor conversion

Acquisitions |

14

…within our markets, we must continue to strengthen

and leverage our Sunoco Brand, our market presence

and our integration on the U.S. East Coast

Pull >100% refinery gasoline output through our retail network,

growing organically and through acquisitions

Continue to grow our brand recognition and loyalty

Optimize and seek opportunities in supply, distribution and marketing

Continue to manage capital employed by high-grading retail portfolio

Position retail network for alternative fuels longer term

To Become the Premier Fuel Supplier… |

Sunoco Logistics

Partners L.P. (NYSE: SXL)

Mike Hennigan |

16

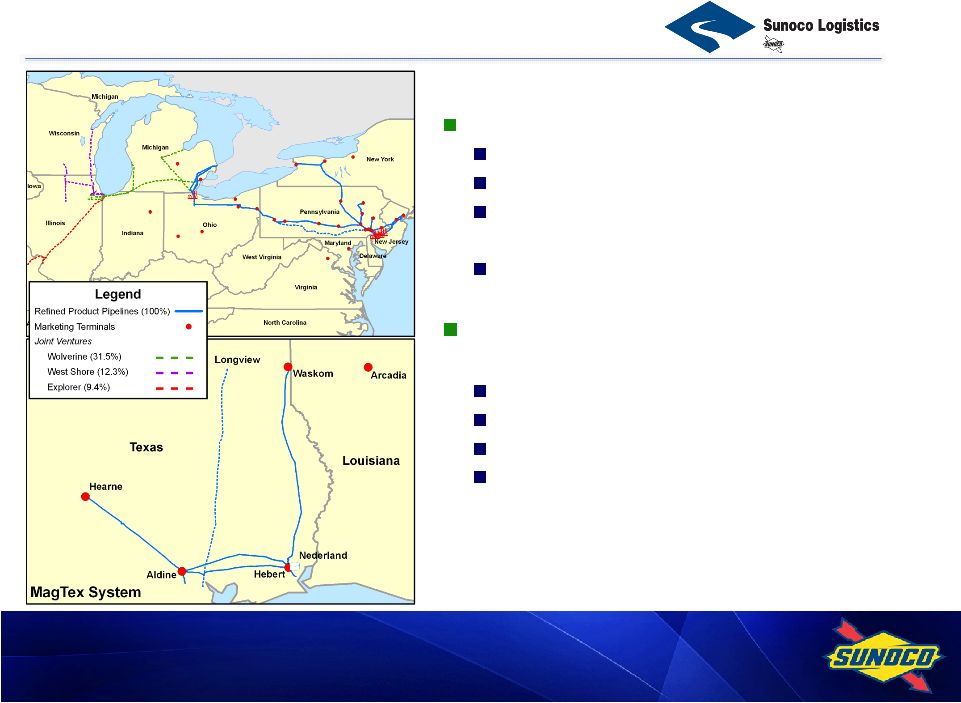

3

Serve key Northeast,

Midwest & Gulf Coast

production/refining centers

2,200 miles of refined

product pipelines

3,850 miles of crude

pipelines

41 refined product terminals

23 million barrels of crude oil

storage capacity

Asset Overview |

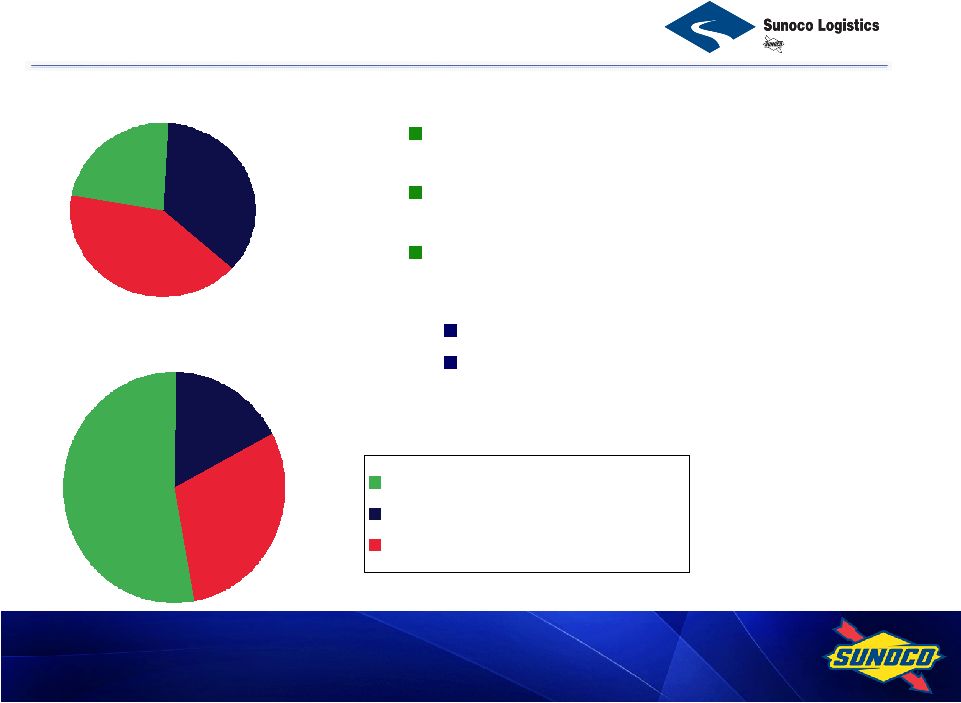

17

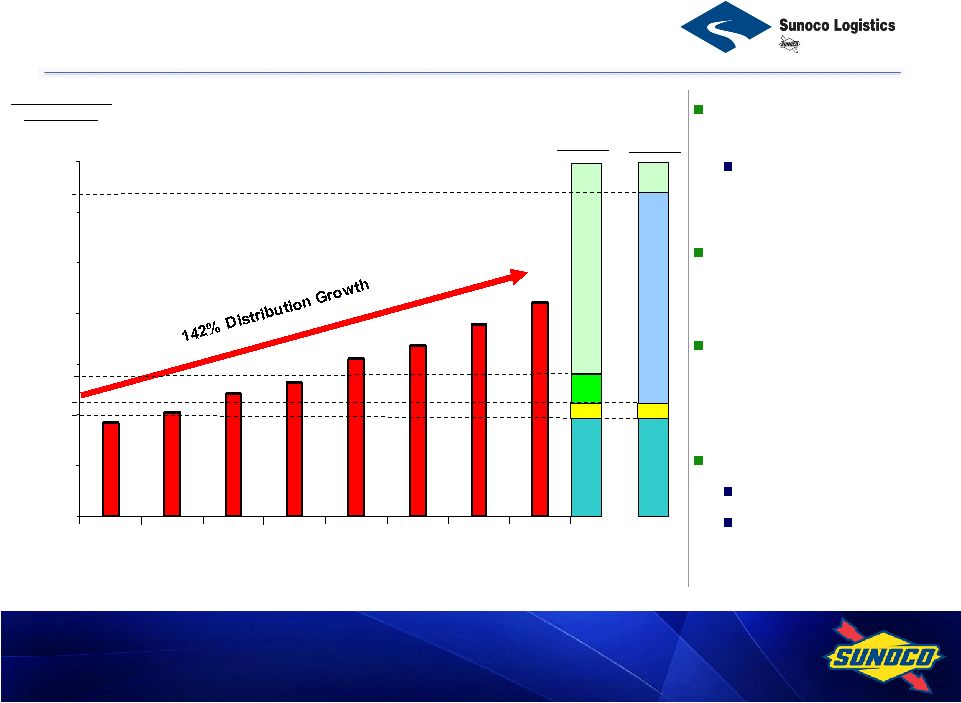

$22MM

23%

$ 35MM

36%

$40MM

41%

9

2009 EBITDA $343MM

2002 EBITDA $97MM

Growth Strategy

Crude Oil Pipeline System

Refined Products Pipeline System

Terminal Facilities

$182 MM

53%

$103MM

30%

$58MM

17%

Optimize current asset base

Invest in organic extensions

Opportunistically

acquire

complementary assets

Continue focus on platform growth

Successfully integrated 15

acquisitions since 2002 IPO

* For reconciliation to Net Income, see Slide A2.

|

18

3

SXL Future Growth

Outside Sunoco footprint

Nederland terminal

MagTex

organic growth

Crude oil pipeline organic growth

Inside Sunoco footprint

Terminal services and pipeline infrastructure

Blending

Alternative fuels

Debottleneck where appropriate

Most of the historical growth has been outside the Sunoco

footprint. Future growth opportunities exist in both areas.

|

19

11

Organic growth opportunities accelerate

Biodiesel

New terminal at Aldine, TX

Crude pipeline to products pipeline

conversion to supply Longview, TX

Marcellus Shale Mariner project

Blending services are becoming more

essential as market needs expand

Ethanol

Biodiesel

Additive package

More expected in the future

Refined Products Platform |

20

Value from SXL

Average Annual

Distribution

(per LP unit)

50/50

75/25

85/15

98/2

Cancelled

LP/GP

Split (%)

63/37

85/15

98/2

50/50

New

LP/GP

Split (%)

Latest 12 month

distribution growth: 10%

Highest in competitive

class

LP Distribution increased

in 27 of last 28 quarters

Current annualized

distribution of $4.46

(6.8% yield as of 5/28/10)

Strong balance sheet

3.6x Debt/EBITDA

Investment grade

2002

2003

2004

2005

2006

2007

2008

2009

$7.00

$6.00

$5.00

$4.00

$3.00

$2.00

$1.00

$0.00 |

21

8

Summary

Consistent track record of distribution growth

Excellent prospects for future growth both outside and inside

the Sunoco footprint

Particular emphasis on the refined products system

Additional growth expected from integrated opportunities with Sunoco

Improve the refining/logistics/marketing integrated network

Identify possible terminal acquisitions

Work together on integrated opportunities (i.e. Marcellus Shale)

Supporting Sunoco’s aspiration to become the premier provider of

transportation fuels in its markets |

Refining

Anne-Marie Ainsworth |

23

Process Safety

Safe operations

Better environmental performance

Improved reliability

Margin capture improvements

Sustainable low cost structure

Driving Excellence |

24

Protects people and the environment

Increases productivity and reduces cost

Improves reliability and product quality; supports Brand

Excellence in Process Safety |

25

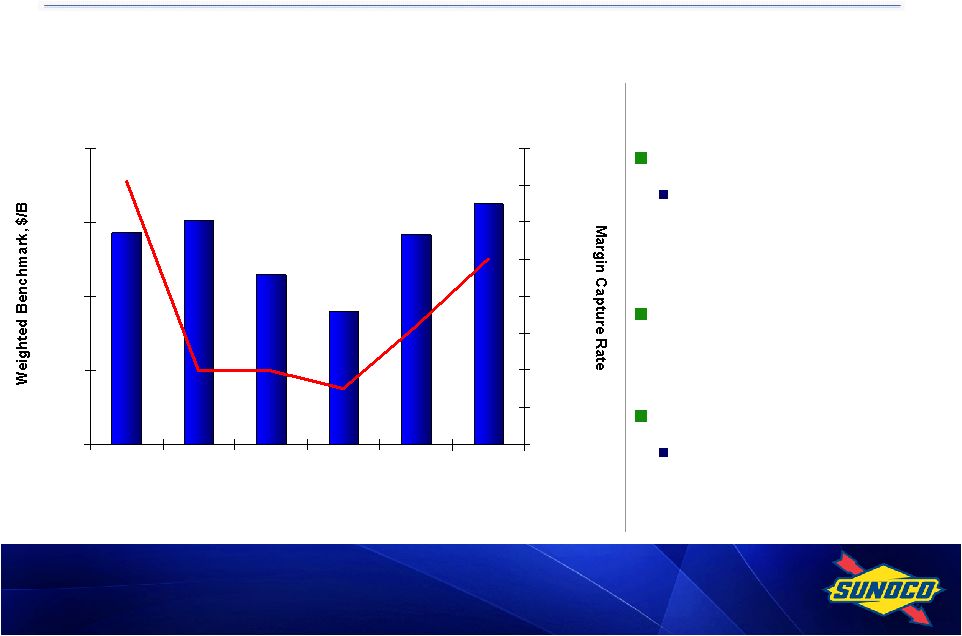

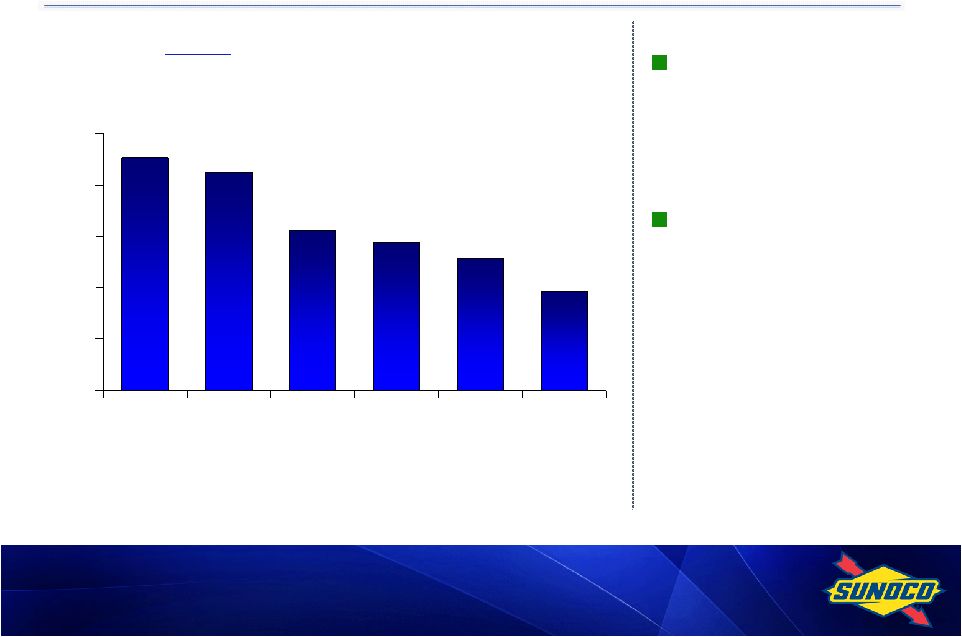

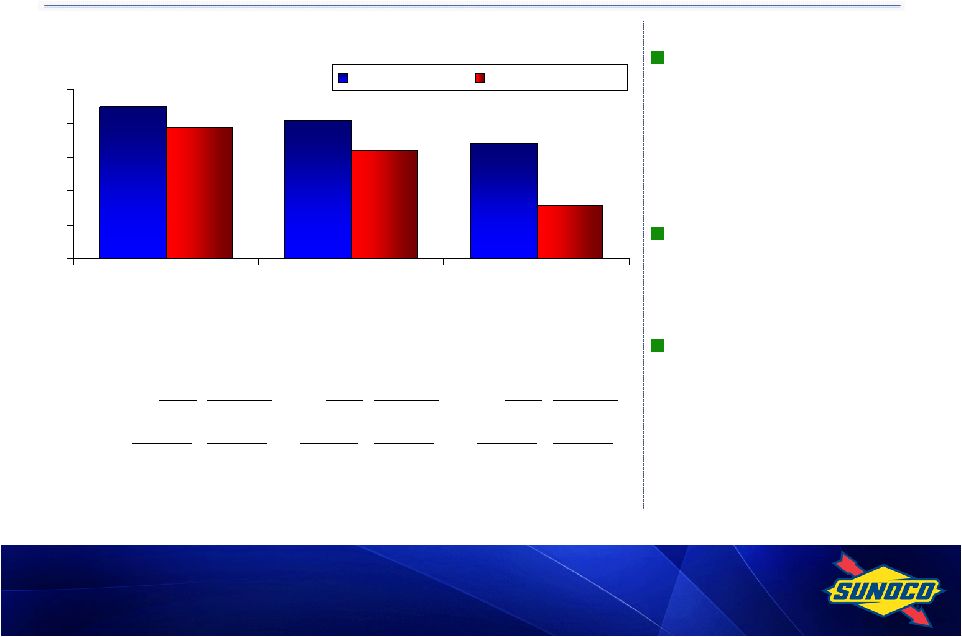

Margin Capture Improvements

Streamlined crude slate

Enables more stable

operations and lower

demurrage

Improved modeling and

scheduling tools

Product quality

Tighter adherence to product

specifications

Main Areas of Focus

4.57

3.59

5.67

6.50

5.71

6.05

0.00

2.00

4.00

6.00

8.00

1Q09

2Q09

3Q09

4Q09

1Q10

2Q10 to

date

40%

50%

60%

70%

80%

90%

100%

110%

120%

Margin capture improvement from 1Q 2010 expected to carry into 2Q

|

26

Eagle Point shut down

November 2009

Increased utilization at

remaining NE system

Turnaround activity in

1Q10 reduced crude

utilization by 9%

Expect improved

utilization in 2Q10

Goal to run >90%

utilization in NE (subject

to market conditions)

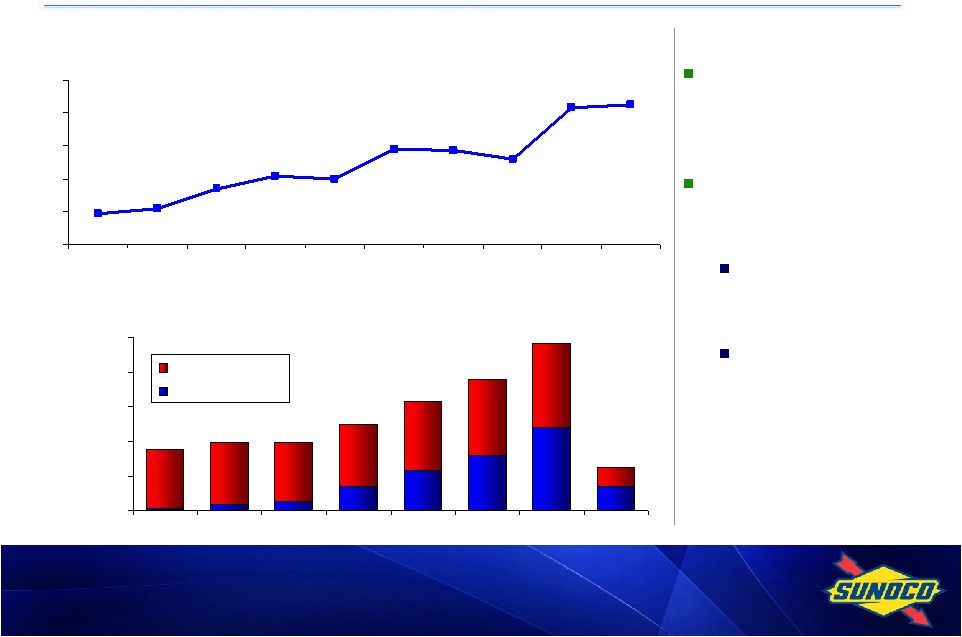

Refining Utilization

79%

90%

85%

76%

90%

77%

89%

76%

0%

10%

20%

30%

40%

50%

60%

70%

80%

90%

100%

Crude Unit Utilization

Conversion Unit Utilization

Turnaround impact to

utilization: 9% crude

& 11% conversion

9/30/09

YTD

4Q09

1Q10

P 2Q10 |

27

* Total

Refining

&

Supply

business

unit

cash

expenses

including

overhead

divided

by

net

production available for sale.

Steady reduction in

refinery cash costs

beginning in late 2008

Cost structure must

match reality of

competitive, import-

accessible market

Efforts continue to

further reduce

expenses while

optimizing production

Sustainable Low Cost Structure

Refining

Cash

Cost

Per

Barrel*,

Rolling Four Quarters (ex-Tulsa)

4.48

4.64

4.72

4.78

5.06

5.13

4.00

4.25

4.50

4.75

5.00

5.25

4Q08

1Q09

2Q09

3Q09

4Q09

1Q10

Four Quarters Ending |

28

Reduced 2010 capital to

$275 million, in line with

depreciation expense

Pursuing lower cost

alternatives for future

requirements

Expect 2011 capital

spending to be below

DD&A

652

380

275*

0

100

200

300

400

500

600

700

2008

2009

2010P

Growth

Turnarounds

Legally Required and Base Infrastructure

Lower Capital Spending

($MM)

*

Excludes

Northeast

Biofuels

plant

start-up

capital |

29

Summary

Driving excellence in process safety

Margin capture improvement

Competitive cost structure

Actions Yielding Results —

More to Come |

SunCoke Energy

Mike Thomson |

31

SunCoke Energy Today

Steel & Coke Industry Outlook

Markets & Business Development

Technology Development

SunCoke Energy Growth Potential

Strategy Execution

Agenda |

32

Haverhill 1 & 2

(ArcelorMittal/AK

Steel/ Severstal )

Jewell Coal

1.3MM tpy

premium mid-vol

coal

(Expansion underway to

1.8MM tpy

by 2013)

Vitória*

(ArcelorMittal)

Brazil

Under construction

Existing facilities

Headquarters

Jewel Coke

(ArcelorMittal)

Indiana Harbor

(ArcelorMittal)

Knoxville

Granite City

(US Steel)

Middletown

(AK Steel)

SunCoke Energy Today

*SunCoke holds an equity ownership interest of $41 million in Vitória.

Jewell Coke

Indiana Harbor

Haverhill 1

Vitória*

Haverhill 2

Granite City

Middletown

0.0

1.0

2.0

3.0

4.0

5.0

6.0

7.0

2004

2005

2006

2007

2008

2009

2010

2011

2012 |

33

33

Global Growth Outlook for Steel and Coke

mmtpy

crude steel

Steel Production

mmtpy

Coke Production

5-5.5%

growth

expected

Prices for coking coal and coke have responded accordingly on tight

supplies and increasing demand

Sources: CRU, The Annual Outlook for Metallurgical Coke

and company analysis |

34

Global Coke Market Opportunity in Next Decade

Americas

Rest of the World

Europe/CIS

India

China

6 -

9

3-4

<3

Replacement

8 -

14

New

Replacement

50+

New

80+

Replacement

20+

New

30+

Replacement

1 -

6

New

10+

Replacement

85+

New

125+

Global total

Number of coke plant projects*

(2010-2020)

*Average of ~1MM tpy

/ plant

Replacement

New |

35

Current Development Activities

US/Canada

Leveraging existing

customer relationships

On-going discussions

with multiple customers

for integrated and

central plants

Contract renewals

Brazil

Leveraging Vitória facility

as strong reference plant

•Player in major Greenfield

developments

Europe

Early stages for both

central and integrated

plants in both Western

and Eastern Europe

India

Developing presence

on the ground in India

Brand recognition

with customers, EPC

firms and other

strategic players |

36

Technology Development

Perfect Core

Technology

Adapt Technology

for World Markets

Game-Changing

Technology

2015+

2010

2010-2014

Horizon 1

Horizon 2

Horizon 3

Key Drivers of

Coke Economics

Raw Material Cost

Production Flexibility

Conversion Cost/Efficiency

Capital Investment

1

2

3

4 |

37

37

Coke Growth Potential

SunCoke: Tons of coke produced

mmtpy

Track record

11 years

5 projects

4.8 mm tons

0.7

5.5

14.5

‘98

‘05

‘07

‘08

‘09

Growth plan

10 years

6-10 projects (mid)

4-9 mm tons

~ 0.4 mm tons/yr

12.0

9.5

~ 0.6 mm tons/yr

*SunCoke holds an equity ownership interest of $41 million in Vitória.

*

Range of growth |

38

Coal Expansion Opportunity

Coal expansion plan capital outlay of $25MM is expected to result in

40% increased production by the end of 2012

Current

2011

2012

Production: ~1.75mm tons

Employees: ~350

Production: ~1.40mm tons

Employees: ~315

Production: 1.25mm tons

Employees: 215 |

39

Projected Growth

2010 Guidance

2012 Pro forma

$215-$235MM

$315-$355MM*

Middletown and Gateway

at full production

Coal expansion &

operational excellence

~ 45% growth projected based on existing projects underway

*Pro forma uses coal prices assumption of $125 to $135/ton.

|

40

Horizon Outlook for Successful Coke Growth Strategy

Prepare for growth and

defend core position

Execute growth platform

Create options for new

opportunities

2014+

2009-2010

2011-2013

Horizon 1

Horizon 2

Horizon 3

Business Imperatives

for Growth

Customer Value Proposition

1

2

3

4

Proven reliability from reference plants

Leading know-how and expertise

Demonstrated product quality

Higher energy production

Capital funding

Competitive life-cycle costs

Operating reliability and

cost competitiveness

Capital cost

competitiveness

Technology development

Business development

capability |

41

Summary

Successful track record of growth and demonstrated execution

Large and growing market for coke driven by steel demand in

emerging economies

SunCoke technology, operational capability and brand may

present growth opportunities in attractive markets

SunCoke management is executing a cohesive strategy

around four key pillars to position SunCoke for success

Operations: The SunCoke Way

Technology Development

Capital Cost Competitiveness

Business Development Capability |

Financial Strategy

& Wrap Up Brian MacDonald |

43

Reset the company’s cost

base

20% reduction in salaried workforce

$300MM annualized

Mar 09

Sep 09

Jun 09

Date

Action

Purpose

Sale of Tulsa Refinery ($157MM)

Focus on core refining assets

Sale of Retail Heating Oil business

($83MM)

Exit non-core business at

attractive price

2010 Annual Incentive Plan Metrics –

60% Pre-Tax Operating Income

Strategic & Financial Actions |

44

Reset the company’s cost base,

preserve cash

Pension and retiree medical plan

freeze

Nov 09

Realign with broader market while

maintaining a competitive payout

versus peers

50% reduction in common stock

dividend

Oct 09

Oct 09

Date

Action

Purpose

Shutdown of Eagle Point refinery

Leverage underutilized capacity to

reduce refining cost per barrel

Strategic & Financial Actions |

45

Exit non-core business that failed

to return its cost of capital

Sale of Polypropylene business

($351MM of proceeds)

Mar 10

Remove funding

overhang/optimize tax position

Pension plan contribution

($230MM)

Feb 10

Monetize and highlight a portion

of existing value

Reset SXL’s GP IDR (~$201MM)

and sale of Limited Partner units

(~$145MM)

Feb 10

Date

Action

Purpose

Strategic & Financial Actions |

46

Exit non-core business that failed to return its cost of capital

Sale of Polypropylene business

($351MM of proceeds)

Mar 10

Remove funding overhang/optimize tax position

Pension plan contribution ($230MM)

Feb 10

Reset the company’s cost base, preserve cash

Pension and retiree medical plan freeze

Nov 09

Monetize and highlight a portion of existing value

Reset SXL’s GP IDR (~$201MM) and sale of Limited Partner units

(~$145MM)

Feb 10

Realign with broader market while maintaining a competitive payout versus

peers

50% reduction in common stock dividend

Oct 09

Reset the company’s cost base

20% reduction in salaried workforce

$300MM annualized

Mar 09

Oct 09

Sep 09

Jun 09

Date

Action

Purpose

Sale of Tulsa Refinery ($157MM)

Focus on core refining assets

Sale of Retail Heating Oil business ($83MM)

Exit non-core business at attractive price

Shutdown of Eagle Point refinery

Leverage underutilized capacity to reduce refining cost per barrel

Strategic & Financial Actions

Realigning the cost structure and

strengthening the balance sheet to

maximize value creation |

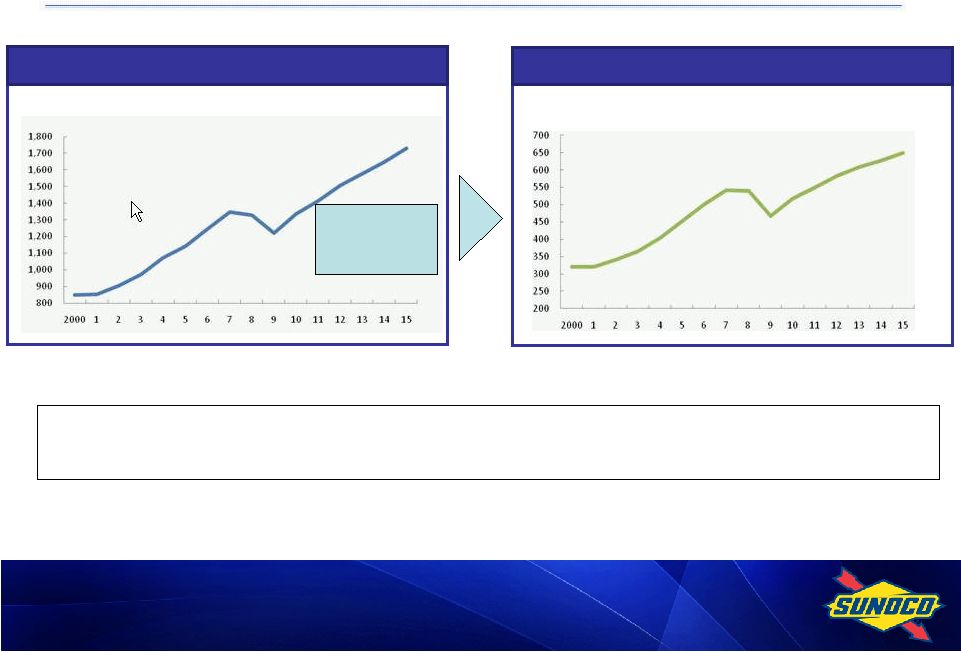

47

* Total

Refining

&

Supply

business

unit

cash

expenses

including

overhead

divided

by

net

production available for sale.

Steady reduction

in refinery cash

costs

Efforts continue to

further reduce

expenses while

optimizing reliable

and safe

operations

Results: Manufacturing Costs Coming Down

Refining

Cash

Cost

Per

Barrel*,

$/B

Rolling Four Quarters (ex-Tulsa)

4.48

4.64

4.72

4.78

5.06

5.13

4.00

4.25

4.50

4.75

5.00

5.25

4Q08

1Q09

2Q09

3Q09

4Q09

1Q10

Four Quarters Ending |

48

* Selling, general and administration expenses from Sunoco’s

Consolidated Statement of Operations, restated to treat the Tulsa refinery

that was sold on June 1, 2009 and the polypropylene chemical operations

that were sold on March 31, 2010 as discontinued operations.

Steady reduction in

SG&A costs

Moving to low-cost

culture --

essential to

maintain long-term

competitiveness

Results: Overhead Costs Coming Down

Total Sunoco SG&A*, MM$

Rolling Four Quarters

(ex-Tulsa and Polypropylene Operations)

649

671

737

752

796

798

600

650

700

750

800

850

4Q08

1Q09

2Q09

3Q09

4Q09

1Q10

Four Quarters Ending |

49

Recent actions led to

significant

strengthening in

balance sheet

$2.7 billion of liquidity

as of 3/31/10

$351 million proceeds

from sale of

polypropylene assets

received in April

Results: Strong Balance Sheet

34%

41%

45%

16%

32%

39%

0%

10%

20%

30%

40%

50%

9/30/09

12/31/09

3/31/10

Consolidated *

Sunoco (ex-SXL)

Net Debt-to-Capital Ratio, %

* Revolver Covenant basis. For calculation, see Slide A4.

Cash

Net Debt

Cash

Net Debt

Cash

Net Debt

SXL

2

887

2

866

2

1,139

SUN (ex SXL)

176

1,539

375

1,223

810

498

Consolidated

178

2,426

377

2,089

812

1,637

Balance Sheet Data, MM$

9/30/09

12/31/09

3/31/10 |

50

Results: Embedded Logistics Value

Currently, Sunoco

receives approximately

half of SXL’s cash

distribution

Implied value of Sunoco’s

combined interests =

$1.2B to $1.4B

10 million LP units

implying ~$600MM -

$700MM value

GP current

distributions of

~$40MM per year

implying ~$600MM -

$700MM value

SXL Market Capitalization, MM$

(LP Interest Only)

2,127

2,072

1,294

1,432

461

546

840

1,032

1,000

1,442

0

500

1,000

1,500

2,000

2,500

2/8/02

12/31/02

12/31/03

12/31/04

12/31/05

12/31/06

12/31/07

12/31/08

12/31/09

3/31/10

SXL Cash to Sunoco, Inc.,

MM$

(excludes cash from sales of LP units and IDR reset)

0

20

40

60

80

100

2003

2004

2005

2006

2007

2008

2009

1Q10

LP Distribution

GP

Distribution |

51

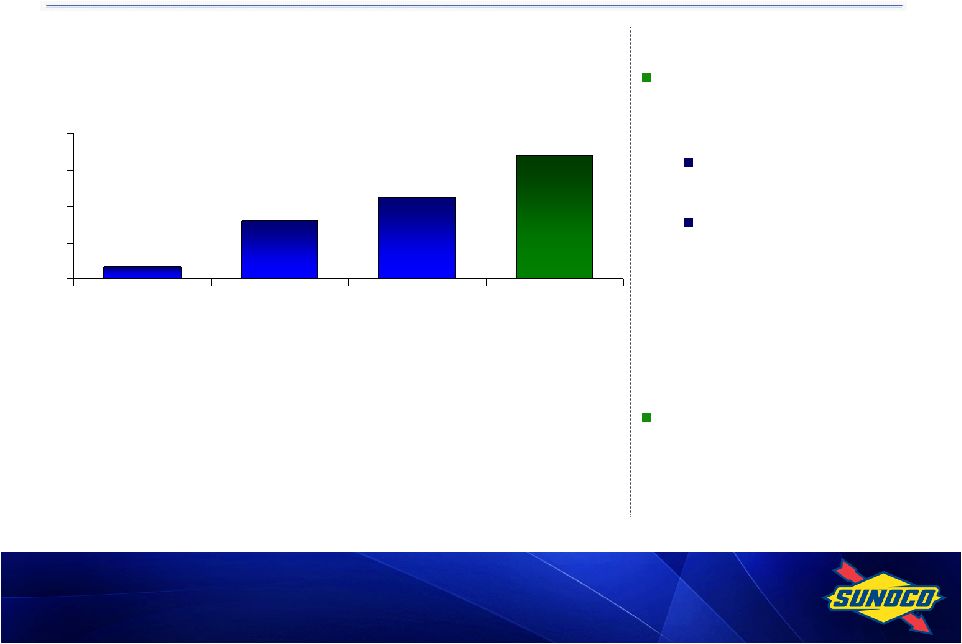

Results: Embedded Coke Value

Coke has strong earnings

growth profile with significant

improvement in pipeline

2010 EBITDA guidance of

$215MM -

$235MM

Pro forma EBITDA by

2012 of $315MM -

$355MM, with full run-rate

of Granite City,

Middletown and coal

expansion

Significant potential to unlock

value for SUN shareholders

and enhance both businesses

34

160

226

315-355

-

100

200

300

400

2007

2008

2009

Pro forma

2012**

Coke EBITDA*, MM$

* For reconciliation to Net Income, see Slide A3.

** Sunoco projection based on current projects. |

52

Refining

& Supply

1,100

Chemicals

690

Logistics

1,070

Will create two well-positioned businesses:

Leading

high-quality

metallurgical

coke

manufacturer

with

operations in the U.S. and abroad

Streamlined fuels business that is better positioned to become the

premier provider of transportation fuels in its markets

Separation planned for first half of 2011

Evaluating a number of strategic options for separation

Will ultimately separate 100%

Enhances both businesses and allows each to pursue

more focused strategic plan

Unlocking Shareholder Value via SunCoke Separation |

53

Refining

& Supply

1,100

Chemicals

690

Logistics

1,070

Protect balance sheet during continued challenging

economic downturn in refining industry

Pursue attractive growth opportunities in business lines

with best returns and growth prospects

Logistics

–

both

within

Sunoco

footprint

and

outside

Brand-led growth strategy in Retail Marketing

Support SunCoke growth opportunities prior to separation

Evaluate appropriate deleveraging for Sunoco

Path Forward: Cash Priorities |

54

Strategic Goals

Premier provider of transportation fuels in our markets

Growing Coke business generating increased shareholder value as

a separate company

Significant progress made

Positive expense trends

Improved balance sheet

Improving margin capture

Continued growth in Coke and Logistics

Areas of forward focus

Further reduce expenses to maintain competitiveness

Protect the balance sheet

Redeploy capital toward the highest returns and best growth

prospects

Unlock the embedded value of portfolio

Path Forward: Strategic Summary |

APPENDIX

|

Retail

Marketing Financial Summary 2003

2004

2005

2006

2007

2008

2009

EBITDA, $MM

244

217

155

233

221

439

241

Less: Depreciation

99

106

105

104

108

110

95

Less: Income Tax

54

43

20

53

44

128

60

Net Income

91

68

30

76

69

201

86

A1 |

Sunoco

Logistics Partners L.P. Financial Summary * Net of Capitalized Interest

A2

2002

2009

EBITDA, $MM

97

343

Less: Depreciation

31

48

Less: Income Tax

2

-

Less: Interest Cost & Debt Expense, Net*

17

45

Net Income

47

250 |

SunCoke Financial Summary

*

Projected

**

Pro forma based on announced projects

A3

Proforma

2007

2008

2009

2010*

2012**

EBITDA, $MM

34

160

226

215-235

315-355

Less: Depreciation

20

25

33

42

55

Less: Income Tax

3

46

73

66-71

101-116

Plus: Tax Credits

18

16

19

18

16

Plus: Granite City

one-time tax credit

-

-

41

-

-

Net Income

29

105

180

125-140

175-200 |

Net

Debt / Capital Calculation Financial Ratios, MM$ except ratios

*

Represents Partners’

Capital for SXL and Shareholders’

Equity for Sunoco

**

The Net Debt / Capital ratio is used by Sunoco management in its

internal financial analysis and by investors and

creditors in the assessment of Sunoco’s financial position

*** Capital excludes noncontrolling

interests

Proforma

Proforma

Proforma

SUN

SUN

SUN

SXL

(ex SXL)

Sunoco

SXL

(ex SXL)

Sunoco

SXL

(ex SXL)

Sunoco

Debt

889

1,713

2,602

868

1,596

2,464

1,141

1,306

2,447

Plus: Debt Guarantees

-

2

2

-

2

2

-

2

2

Less: Cash

(2)

(176)

(178)

(2)

(375)

(377)

(2)

(810)

(812)

Net Debt

887

1,539

2,426

866

1,223

2,089

1,139

498

1,637

Equity*

852

2,443

2,443

862

2,557

2,557

657

2,712

2,712

SXL Noncontrolling Interest

-

-

485

-

-

488

-

-

414

Capital

1,739

3,982

5,354

1,728

3,780

5,134

1,796

3,210

4,763

Net Debt / Capital (Sunoco

Revolver Covenant Basis)**

51%

39%

45%

50%

32%

41%

63%

16%

34%

Debt / Capital (GAAP Basis) ***

52%

49%

47%

12/31/2009

3/31/2010

9/30/2009

A4 |