Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - VALLEY NATIONAL BANCORP | d8k.htm |

Investor

Presentation EXHIBIT 99.1 |

Information

For

Investors

And

Shareholders

This presentation contains forward-looking statements concerning Valley’s future business

outlook, financial condition and operating results. Generally, the words "will,"

"may," "should," "continue," "believes," "expects,"

"anticipates" or similar expressions identify forward-looking statements.

Readers are advised not to place undue reliance on these forward-looking statements as they

are influenced by certain risk factors and unpredictable events. The foregoing contains forward-looking statements within the meaning of the Private Securities

Litigation Reform Act of 1995. Such statements are not historical facts and include

expressions about management’s confidence and strategies and management’s

expectations about new and existing programs and products, relationships, opportunities,

taxation, technology and market conditions. These statements may be identified by such

forward-looking terminology as “expect,” “believe,” “view,”

“opportunity,” “allow,” “continues,” “reflects,” “typically,” “usually,” “anticipate,” or

similar statements or variations of such terms. Such forward-looking statements involve

certain risks and uncertainties. Actual results may differ materially from such

forward-looking statements. Factors that may cause actual results to differ materially from

those contemplated by such forward-looking statements include, but are not limited to those

factors disclosed in Valley’s Quarterly Report on Form 10-Q for the three months ended

March 31, 2010 and Annual Report on Form 10-K for the year ended December 31, 2009.

Valley disclaims any obligation to update or revise forward-looking statements for any

reason. |

Investor

Presentation •

History of Valley National Bank

–

Organic Growth and Acquisitions

•

Valley National Bank Today

–

About Us

–

Footprint

–

Recent Highlights

–

Balance Sheet Composition

–

Shareholder Returns

•

Credit Culture

–

Non-Performing Assets

–

Net Charge-Offs

–

Delinquencies

•

Additional Information

–

Demographics

–

Executive Management |

Valley

National Bank Today About Valley

•

Regional Bank Holding Company

•

Approximately $14.5 Billion in

Assets

•

Headquartered in Wayne, New

Jersey

•

36

Largest

United

States

Chartered

Commercial Bank

–

Largest Commercial Bank

Headquartered in New Jersey

•

Operates 202 Branches in 135

Communities Serving 14 counties

throughout Northern and Central

New Jersey, Manhattan, Brooklyn

and Queens

•

Traded on the NYSE (VLY)

Significant Attributes

•

Consistent Shareholder Returns

•

Focus on Credit Quality

•

Conservative Strategies

•

Affluent and Heavily Populated

Footprint

•

Strong Customer Service

•

Large Bank that Operates and

Feels Like a Small Closely Held

Company

•

Experienced Senior and Executive

Management

th |

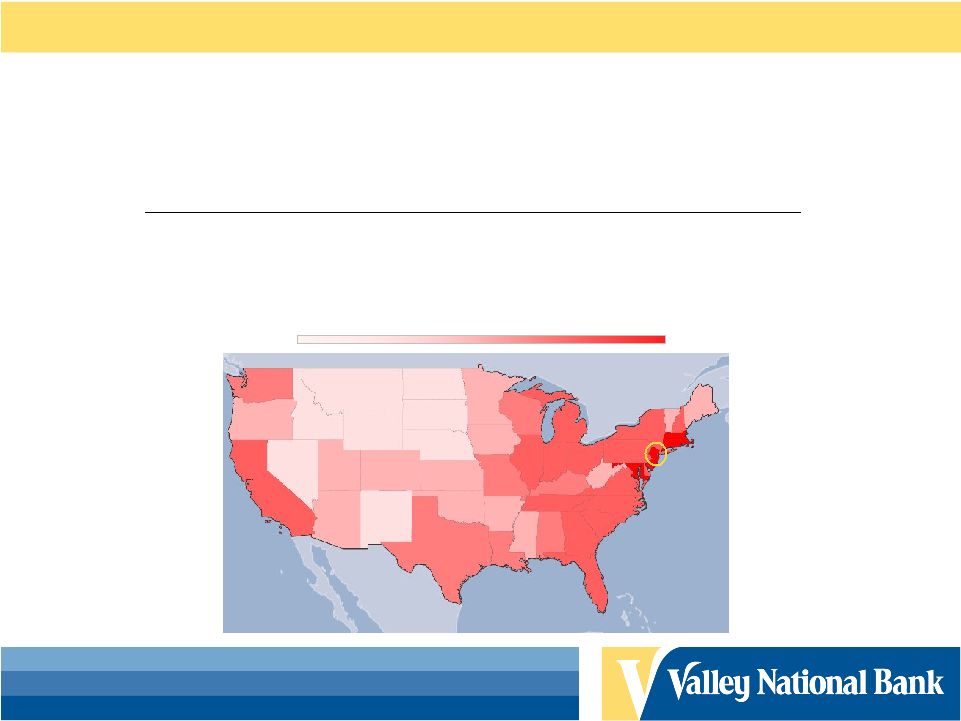

Footprint

& Demographics Valley’s Emerging NJ Market

Valley’s Core NJ Market

Branches Under Construction

Current Branches

Valley’s Core New Jersey Market

•

Total

Market

Deposits

-

$106.9

billion

•

Market Average Deposits per Branch $76.0 million

•

Valley

Branches

–

134

•

Valley’s

Market

Share

–

6.63%

Valley’s Emerging New Jersey Market

•

Total Market Deposits -

$64.3 billion

•

Market Average Deposits per Branch $68.2 million

•

Existing

Valley

Branches

–

38

•

Branches

Under

Construction

–

3

•

Valley’s

Market

Share

–

1.59%

Headquarters

$245 billion

$73,077

8.8 million

NJ Total

$74 billion

$61,436

2.9 million

Balance of NJ Marketplace

$171 billion

$78,074

5.9 million

Valley’s NJ Marketplace

Total Market

Deposits

Median HH

Income

Population

Region

Valley’s NJ Marketplace

Demographic Data from SNL Financial Inc. as of 6/2009

Valley Branch data as of 3/31/2010 |

Footprint

& Demographics Valley’s Emerging Manhattan Market

•

Total Market Deposits -

$418.3 billion

•

Market Average Deposits per Branch $621.6 million

•

Existing Valley Branches –

17

•

Valley’s Market Share –

0.28%

Valley’s Emerging Queens Market

•

Total Market Deposits -

$41.3 billion

•

Market Average Deposits per Branch $96.3 million

•

Existing Valley Branches –

5

•

Valley’s Market Share –

0.17%

Valley’s Emerging Brooklyn/Kings Market

•

Total Market Deposits -

$34.1 billion

•

Market Average Deposits per Branch $99.6 million

•

Existing Valley Branches –

8

•

Branches Under Construction -

1

•

Valley’s Market Share –

0.58%

$288 billion

$52,640

13.0 million

Balance of NY Marketplace

$781 billion

$52,893

19.5 million

NY Total

$493 billion

$57,864

6.5 million

Valley’s NY Marketplace

Total Market

Deposits

Median HH

Income

Population

Region

Valley’s Emerging NYC Markets

Branches Under Construction

Current Branches

Valley’s NY Marketplace

Demographic Data from SNL Financial Inc. as of 6/2009

Valley Branch data as of 3/31/2010 |

Valley’s

1Q 2010 Highlights FDIC-assisted Transactions

Acquired Manhattan-based LibertyPointe Bank and The Park Avenue Bank from the FDIC as

receiver and benefitted from two loss-sharing agreements with the FDIC

Acquired combined deposits of $654 million and certain assets totaling approximately $692

million, before purchase accounting adjustments

Credit Quality

Total 30+ day delinquencies were 1.68% of entire loan portfolio

Out

of

approximately

22,000

residential

mortgages

and

home

equity

loans

only

216

loans

were

past

due

30

days

or more at March 31, 2010

Net charge-offs were only $11.0 million or 0.47% of average total loans on an annualized

basis Total non-performing loans were only 0.96% of total loans compared to 0.98%

last quarter Net Income

1Q net income available to common shareholders was $27.4 million

Net

interest

margin

on

a

tax

equivalent

basis

increased

18

basis

points

to

3.65%

compared

to

the

previous

quarter

$3.3 million non-cash charge on change in fair value of Valley’s junior subordinated

debt ($0.01 Diluted EPS) Capital

Continued strong capital ratios

Tangible Common Equity to Risk-Weighted Assets of 8.65%

Tier I Ratio of 10.54%

Tier II Ratio of 12.46% |

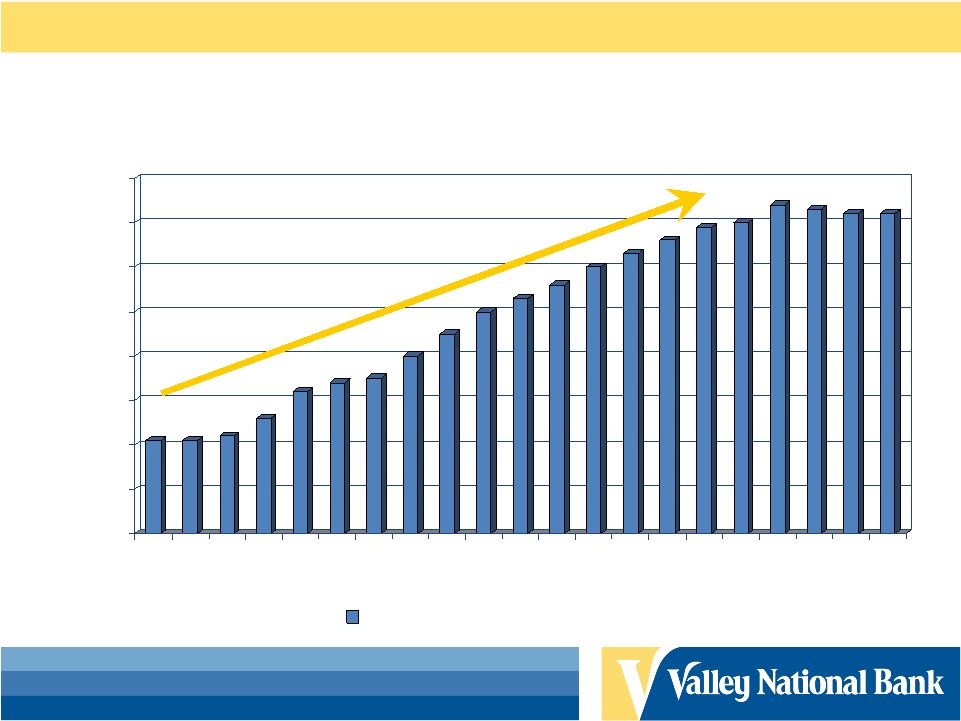

$-

$2,000

$4,000

$6,000

$8,000

$10,000

$12,000

$14,000

$16,000

1989

1991

1993

1995

1997

1999

2001

2003

2005

2007

2009

Organic Assets

Assets Acquired

Asset Growth of Valley National Bank

•

Over the past 83 years, Valley has grown organically and

through the acquisition of 30 financial institutions

CAGR = Compounded annual growth rate

Organic CAGR = 7.80%

Total CAGR = 10.85% |

Asset and Loan

Composition Other Assets*

8%

Covered Loans

3%

Intangible

Assets 2%

Cash 3%

Securities 21%

Non-Covered

Loans 63%

Total Assets = $14.5 Billion

As of 3/31/10

Commercial

Real Estate

38%

Residential

Mortgages

21%

Commercial

Loans 19%

Construction

Loans 5%

Auto Loans

10%

Other

Consumer

7%

Non-Covered Loans (Gross) = $9.1 Billion

*Other Assets includes bank owned branch locations carried at a

cost estimated to be less than the current market value. |

Total

Commercial Real Estate - $3.4 Billion

(Non-Covered Loans)

As of 3/31/10

46%

1%

24

Other

2%

3%

6%

7%

11%

11%

13%

21%

25%

% of

Total

58%

52%

50%

61%

45%

49%

54%

53%

50%

Average

LTV

367

Mixed Use

361

Apartments

439

Office

717

Industrial

858

Retail

69

Land Loans

88

Residential

213

Specialty

233

Healthcare

$ Amount

(Millions)

Primary Property Type

Diversified Commercial Real Estate Portfolio

25%

21%

13%

11%

11%

7%

6%

3%

2%

1%

-Average LTV based on current balances and original appraised value

-The total CRE loan balance is based on Valley’s internal loan hierarchy

structure and does not reflect loan classifications reported in Valley’s

SEC and bank regulatory reports.

-The chart above does not include $392 million in construction loans.

|

27%

22%

18%

12%

6%

5%

4%

4%

2%

Total Retail Property Types -

$858 Million

(Non-Covered Loans)

43%

4%

Entertainment Facilities

51%

5%

Food Establishments

2%

4%

6%

12%

18%

22%

27%

% of

Total

52%

51%

32%

52%

55%

51%

49%

Average

LTV

Auto Dealership

Multi-Tenanted -

No Anchor

Single Tenant

Multi-Tenanted -

Anchor

Retail Property Type

Auto Servicing

Private Education Facilities

Private & Public Clubs

As of 3/31/10

Retail Composition of Commercial Real Estate

-Average LTV based on current balances and original appraised

value

-The chart above does not include construction loans. |

As

of 3/31/10 14%

13%

8%

4%

4%

3%

2%

1%

1%

50%

Construction Loan Composition

Total

(Non-Covered)

Construction

Loans

-

$392

Million

1%

5

Industrial

1%

6

Specialty

2%

9

Healthcare

3%

11

Apartments

4%

12

Office

4%

17

Other

8%

32

Retail

13%

51

Land Loans

14%

56

Mixed Use

50%

193

Residential

% of

Total

$ Amount

(Millions)

Primary Property Type

-Construction loan balance is based on Valley’s internal loan hierarchy

structure and does not reflect loan classifications reported in

Valley’s SEC and bank regulatory reports. |

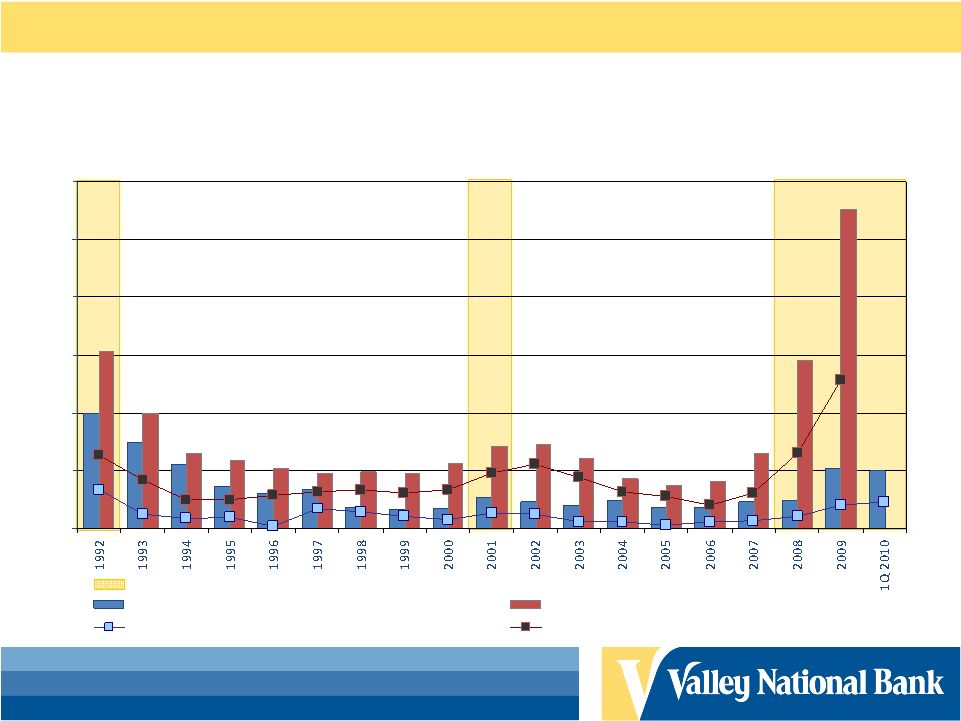

Loan

Quality 1992 – 1Q 2010

Source –

FDIC

Recession

Total Loan Portfolio

Non-Current Loans: Loans and leases 90 days or more past due

plus loans in non accrual status, as a percent of gross loans and leases.

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

Valley's Non-Current Loans to Total Loans

FDIC Insured Banks Non-Current Loans to Total Loans

Valley Net Charge-offs to Average Loans

FDIC Insured BanksNet Charge-offs to Average Loans |

Loan

Quality 1992 – 1Q 2010

Recession

Residential Mortgages

Valley’s elevated levels between 1993 and 1997 are mainly attributable to

acquisitions. Source –

FDIC

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

Valley's Non-Current Loans to Total Loans

FDIC Insured Banks Non-Current Loans to Total Loans

Valley Net Charge-offs to Average Loans

FDIC Insured BanksNet Charge-offs to Average Loans |

Loan

Quality 1992 – 1Q 2010

Valley’s elevated levels between 1993 and 1997 are mainly attributable to

acquisitions. Source –

FDIC

Recession

Home Equity

-0.50%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

Valley's Non-Current Loans to Total Loans

FDIC Insured Banks Non-Current Loans to Total Loans

Valley Net Charge-offs to Average Loans

FDIC Insured BanksNet Charge-offs to Average Loans |

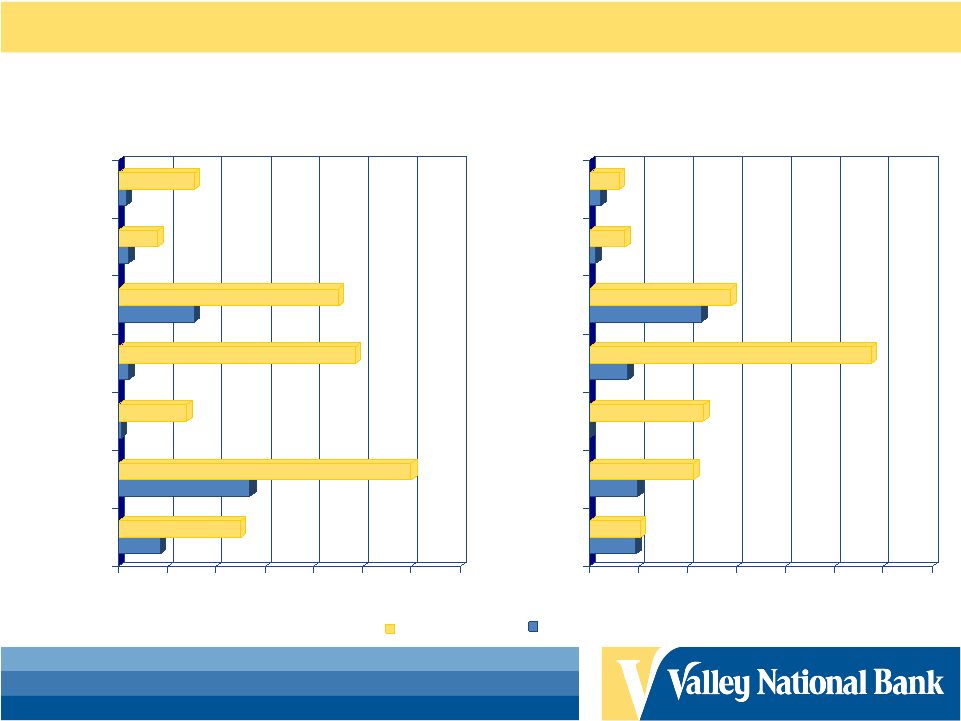

0.17%

0.50%

0.54%

1.20%

0.01%

0.28%

0.04%

0.97%

0.31%

0.90%

0.04%

0.16%

0.03%

0.31%

0.00%

0.20%

0.40%

0.60%

0.80%

1.00%

1.20%

1.40%

Net Charge-offs to Average Loans (%)

Total Loans

Consumer

Home Equity

Construction &

Development

Commercial Loans

Commercial Real

Estate

1-4 Family

Peer Group

0.47%

0.52%

0.49%

1.06%

0.00%

1.16%

0.39%

2.88%

1.14%

1.44%

0.06%

0.36%

0.11%

0.30%

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

Net Charge-offs to Average Loans (%) Annualized

Total Loans

Consumer

Home Equity

Construction &

Development

Commercial Loans

Commercial Real

Estate

1-4 Family

Valley

Net Charge-offs to Average Loans

Source -

SNL Financial As of 04/26/10

Peer group consists of banks with total assets between $3 billion and $50 billion.

2003 -

2009

2010 1Q |

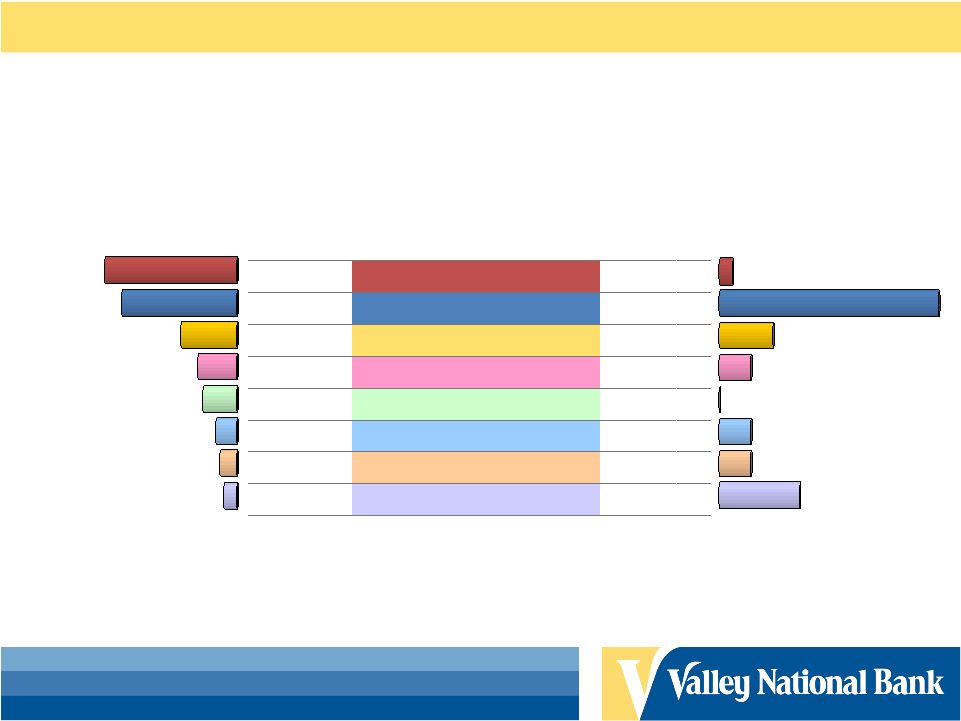

Investment

Portfolio Investment Portfolio

Corporate Debt

Private Label MBS

Other

US Treasury

State, County & Municipals

Trust Preferred

GSE MBS (FNMA/FHLMC)

GSE MBS (GNMA)

Investment Types

$3.1 Billion

$3.0 Billion

18%

3%

5%

4%

7%

5%

0%

8%

7%

9%

12%

13%

49%

28%

3%

30%

2007

Q1 2010

As of 3/31/10 and 12/31/07 |

Securities by

Investment Grade •

AAA Rated 69%

•

AA Rated 5%

•

A Rated 6%

•

BBB Rated 6%

•

Non Investment Grade 4%

•

Not Rated 10%

As of 3/31/10

AAA Rated

Not Rated

Non-investment

grade

A Rated

AA Rated

BBB Rated |

Deposits and

Borrowings Composition Total Deposits

74%

Other

Liabilities 3%

Short-term

Borrowings 1%

Long-term

Borrowings

22%

Total Liabilities = $13.2 Billion

As of 3/31/10

Savings

42%

Non-

Interest

Bearing

25%

Time

Deposits

33%

Total Deposits = $9.8 Billion |

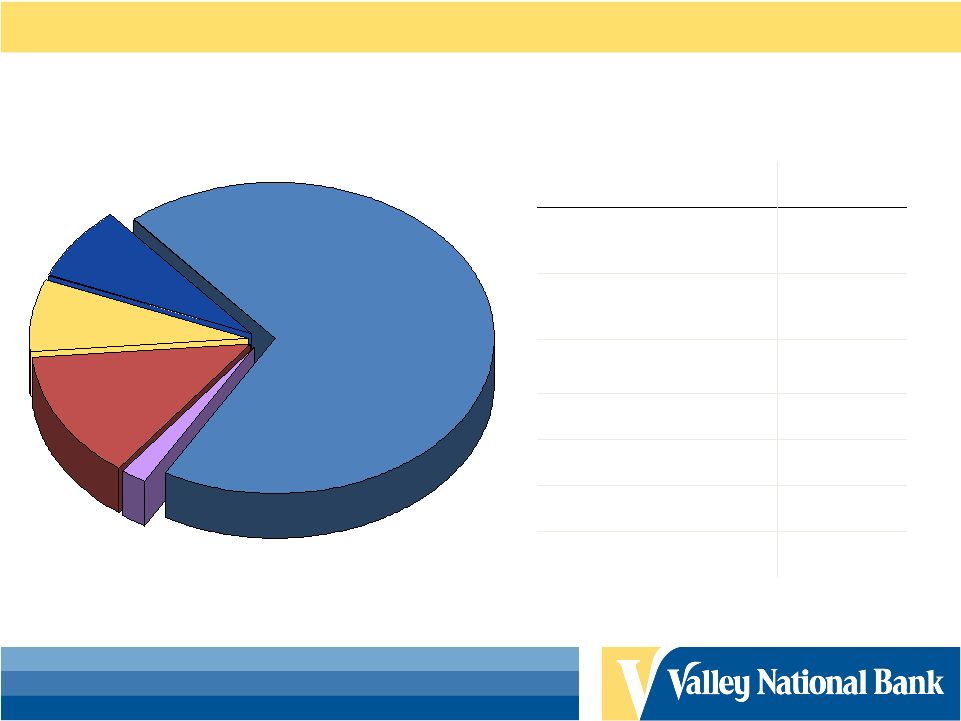

Equity

Composition / Ratios* Tangible

Common

Equity 69%

Other Equity

3%

Trust Preferred

13%

Sub-debt 7%

LL Reserve 8%

Total Tier II Equity = $1.3 Billion

As of 3/31/10

$5.76

$7.83

8.18%

12.46%

10.54%

8.65%

6.55%

As Reported

Tangible Book Value

Book Value

Leverage

Tier II

Tier I

Tangible Common Equity /

Risk-Weighted Assets

Tangible Common Equity /

Tangible Assets

Capital Ratios

As Reported

Unrealized gain on facilities owned of approximately $200 million over

book, not incorporated in capital ratios reflected above.

*Non-GAAP reconciliations shown on slide 25. |

Shareholder

Returns Historical Financial Data (1)

(Dollars in millions, except for share data)

3/2010

14,474

$

27.4

$

$0.17

0.77

%

8.72

%

$0.18

5/10 -

5%

Stock Dividend

2009

14,284

116.1

0.64

0.81

8.64

0.72

5/09 -

5%

Stock Dividend

2008

14,718

93.6

0.64

0.69

8.74

0.73

5/08 -

5%

Stock Dividend

2007

12,749

153.2

1.10

1.25

16.43

0.74

5/07 -

5%

Stock Dividend

2006

12,395

163.7

1.15

1.33

17.24

0.70

5/06 -

5%

Stock Dividend

2005

12,436

163.4

1.17

1.39

19.17

0.69

5/05 -

5%

Stock Dividend

2004

10,763

154.4

1.16

1.51

22.77

0.66

5/04 -

5%

Stock Dividend

2003

9,873

153.4

1.15

1.63

24.21

0.63

5/03 -

5%

Stock Dividend

2002

9,148

154.6

1.12

1.78

23.59

0.60

5/02 -

5:4

Stock Split

2001

8,590

135.2

0.94

1.68

19.70

0.56

5/01 -

5%

Stock Dividend

2000

6,426

106.8

0.90

1.72

20.28

0.53

5/00 -

5%

Stock Dividend

1999

6,360

106.3

0.85

1.75

18.35

0.50

5/99 -

5%

Stock Dividend

1998

5,541

97.3

0.82

1.82

18.47

0.45

5/98 -

5:4

Stock Split

1997

5,091

85.0

0.75

1.67

18.88

0.40

5/97 -

5%

Stock Dividend

1996

4,687

67.5

0.66

1.47

17.23

0.35

5/96 -

5%

Stock Dividend

1995

4,586

62.6

0.60

1.40

16.60

0.34

5/95 -

5%

Stock Dividend

1994

3,744

59.0

0.66

1.60

20.03

0.32

5/94 -

10%

Stock Dividend

1993

3,605

56.4

0.65

1.62

21.42

0.26

4/93 -

5:4

Stock Split

1992

3,357

43.4

0.50

1.36

19.17

0.22

4/92 -

3:2

Stock Split

1991

3,055

31.7

0.37

1.29

15.40

0.21

Year End

Total Assets

Net Income

(2)

Common Stock Splits and Dividends

Diluted

Earnings Per

Common

Share

Return on

Average

Assets

Return on

Average

Equity

Cash Dividends

Declared Per

Common Share

(1) All per share amounts have been adjusted retroactively for stock

splits

and stock

dividends during the periods presented. (2) Net

income

includes

other-than-temporary

impairment

charges

on

investment

securities

totaling

$1.6

million,

$4.0

million, $49.9 million, and $10.4 million, net of tax benefit, for Q1 2010, 2009,

2008, and 2007, respectively. |

$-

$0.10

$0.20

$0.30

$0.40

$0.50

$0.60

$0.70

$0.80

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010*

Dividend Per Common Share

Dividend Growth Per Share

*2010 Dividend Annualized |

Valley’s

Long-Term Objectives •

Maintain a quality balance sheet

•

Manage balance sheet, not be managed by balance sheet

growth

•

Continue to produce strong operating results

•

Minimize earnings volatility

•

Maintain strong capital position

•

Consistently generate solid shareholder returns |

Valley

National Bank Additional Information |

History of

Valley National Bank •

Founded in 1927 as The Passaic Park Trust Co.

•

1956 Purchased The Bank of Allwood

-

Clifton

•

1976 The Name Valley National Bank Chosen

•

1976 Acquired The Bank of Wayne

•

1977 Acquired Bankers National Bank -

Elmwood Park

•

1981 Acquired Liberty National Bank -

Hillsdale

•

1982 Acquired Fair Lawn State Bank

•

1983 Formed Valley National Bancorp

•

1984 Purchased First National Bank & Trust Co. of Kearny

•

1990 Purchased Mayflower Savings Bank -

Livingston

•

1991 Acquired the Deposits from RTC for

–

North Jersey Savings -

Clifton

–

First Jersey Savings -

Wyckoff

–

Nutley Savings

–

Yorkwood

Savings (Warren)

•

1992 Acquired Powder

Mill

Bank

-

Morris

Plains

•

1993 Acquired People's Bank –

Fairfield

•

1994 Acquired

Rock

Bank

-

N.

Plainfield

•

1995 Acquired American

Union

Bank

–

Union

•

1995 Acquired Lakeland Savings Bank –

Succasunna

•

1997 Acquired Midland Bancorp –

Paramus

•

1998 Acquired Wayne Bancorp

•

1999 Acquired Commonwealth All Service Title Agency

•

1999 Acquired

Ramapo

Financial

Corporation

–

Wayne

•

1999 Acquired New Century Asset Management Co.

•

2000 Acquired Hallmark Capital Management, Inc.

•

2001 Acquired Merchants Bank of New York

•

2001 Formed Valley Commercial Capital, LLC

•

2002 Acquired Masters Coverage Corp.

•

2002 Acquired NIA/Lawyers Title Agency, LLC

•

2005 Acquired Shrewsbury State Bank

•

2005 Acquired NorCrown

Bank –

Livingston

•

2008

Acquired

Greater

Community

Bank

-

Totowa

•

2010 Acquired Certain Assets and Deposits from FDIC for

–

LibertyPointe Bank –

New York

–

The Park Avenue Bank –

New York

•

Valley’s 30 acquisitions have included commercial banks, savings

and loans banks, title agencies, asset management companies

and an insurance company among others |

Valley

National Bank Today •

Subsidiaries include:

–

Mortgage servicing company

•

$3.1 billion in serviced mortgages

–

Title insurance agency

–

Asset management advisors (SEC registered) and Trust services

•

$786 million in assets under management

–

All-line insurance agency

•

Offers property, casualty, life and health insurance

–

Commercial equipment leasing & financing for general aviation

aircrafts

–

Healthcare equipment leasing |

Footprint

& Demographics $54,749

United States

$54,719

New York

$72,809

New Jersey

Median Household Income*

Least Income

Most Income

*Source: SNL Financial Inc. as of 12/31/2009 |

Footprint

& Demographics Least Densely Populated

Most Densely Populated

Per km

²

Per square mile

Country/State

New York

New Jersey (Most Densely Populated State)

United States

33.8

87.6

159.4

412.9

459.9

1,191.1

Population Density*

*Source: SNL Financial Inc. as of 12/31/2009 |

Executive

Management •

Office of the Chairman

–

Eight senior executives offering strong senior management

succession

–

Tenured at Valley for a combined 172 years

•

22 years on average

–

Backgrounds include:

•

Regulatory experience

•

CEOs of acquired financial institutions

•

Senior executives with national exposure working for local NJ/NY

companies

•

Mortgage banking & thrift experience |

Executive

Management Gerald Lipkin

Chairman of the Board, President &

Chief Executive Officer

•

Tenured with Valley since 1975

–

Chairman and Chief Executive Officer since 1989

–

President since 1996

–

As chairman, has been instrumental in the acquisition of 24 financial institutions

–

Vice Chairman and Member of the Executive Committee of the New Jersey

Bankers Association

•

Career in banking since 1963

–

Former Deputy Regional Administrator, New York Region, U.S. Comptroller of

the Currency |

Executive

Management •

Tenured with Valley since 1990

–

Senior Vice President and Controller in 1998

–

Executive Vice President since 2000

•

Oversees Finance, Accounting, Treasury, Wealth Management & Shareholder

Relations

•

Career in banking since 1976

–

Residential Financial

Corporation

–

Commercial

Mortgage

Broker

–

Suburban

Savings

and

Loan

–

Executive

Vice

President

–

Employed at both local and national CPA Firms

–

Member American Institute of CPA’s and New Jersey State Society of CPA’s

Alan Eskow

Senior Executive Vice President

Chief Financial Officer |

Executive

Management •

Tenured with Valley since 1977

–

Executive Officer since 1990

•

Oversees Retail Banking Network of over 200 Branches, Bank Operations, Information

Technology and Administration

–

Provided oversight for the 3 most recent acquisitions of Greater

Community

Bank, Shrewsbury State Bank and NorCrown

Bank

•

Career in banking since 1977

–

Held a variety of positions with the bank, including Branch Banking, Lending and

Operations

Peter Crocitto

Senior Executive Vice President

Chief Operating Officer |

Executive

Management •

Tenured with Valley since 1997

–

Executive Officer in since 1997

•

Oversees Commercial Lending, Commercial Real Estate Lending, SBA, Community

Lending,

Aircraft Finance, Leasing,

Cash Management, Government Banking, Legal and

Special Assets

•

Career in banking since 1969

–

Former President and CEO of Midland Bancorporation and Midland Bank and

Trust for 6 years

–

Former President and CEO of First Jersey National Bank/Central (subsidiary of

First Jersey National Corp ) for 5 years

Robert Meyer

Executive Vice President

Chief Commercial Lending Officer |

•

Tenured with Valley since 1996

–

Executive Officer since 1998

•

Oversees

Residential

1

&

2

Mortgage,

Auto,

Floor

Plan,

Credit/Debit

Cards,

Personal Loans and Auto Loan Servicing

–

Oversees mortgage loan servicing subsidiary servicing $3.2 billion in mortgage

loans (purchased and originated)

•

Career in banking since 1970

–

Executive VP of America’s largest, privately held Realtor’s mortgage

affiliate –

Over 37 years of mortgage lending / banking experience

Al Engel

Executive Vice President

Chief Retail Lending Officer

Executive Management

st

nd |

Executive

Management •

Tenured with Valley since 1991

–

Executive Officer since 1991

•

Oversees

Information

Technology,

Bank

Operations,

Facilities

and

Security

–

Former President of Wealth Management and head of Retail Banking

•

Career in banking since 1969

–

Former President & CEO of Pilgrim State Bank for 3 years

–

Former President & COO of 1 National Bank & Trust Co. of Kearny for 18

years Robert Mulligan

Executive Vice President

Chief Administrative Officer

st |

Executive

Management •

Tenured with Valley since 1990

–

Executive Officer since 1992

•

Oversees all credit risk exposure within the Bank

–

Former Head of New Jersey Commercial Lending Division and Former

Chief

Credit Policy and Administration Officer

•

Career in banking since 1968

–

National Bank Examiner, U.S. Comptroller of the Currency for over 10 years

–

Director, EVP and Chief Credit Officer Peoples National Bank of North Jersey

–

President and CEO of two de novo Banks

Robert Farrell

Executive Vice President

Chief Credit Officer |

Executive

Management •

Tenured with Valley since 1992

–

Executive Officer since 2009

•

Oversees all business and sales initiatives within Valley’s footprint of 135

communities and over 200 branches throughout NJ and NY

–

Former Retail Banking Metropolitan Division Executive

•

Career in banking since 1977

–

Extensive experience at Citibank, including corporate and consumer lending,

private banking, sales, branch management and credit operations

Bernadette Mueller

Executive Vice President

Director of Sales and Client Development |

For More

Information –

Log onto our web site: www.valleynationalbank.com

–

E-mail requests to: dgrenz@valleynationalbank.com

–

Call Shareholder Relations at: (973) 305-3380

–

Write to: Valley National Bank

1455 Valley Road

Wayne, New Jersey 07470

Attn: Dianne M. Grenz, First Senior Vice President

Director of Marketing, Shareholder & Public Relations

–

Log onto our website above or www.sec.gov to obtain free copies of

documents filed by Valley with the SEC |

Non-GAAP

Disclosure Reconciliations ($ in Thousands)

8.65%

TCE / RWA

6.55%

TCE / TA

Ratios

$926,522

Total Tangible Shareholders’

Equity

(332,730)

Less: Goodwill & Other Intangible

Assets

$1,259,252

Total Equity

$10,710,868

Risk Weighted Assets

$14,141,066

Total Tangible Assets

(332,730)

Less: Goodwill & Other Intangible

Assets

$14,473,796

Total

Assets

As Reported

*All data as of 3/31/10

$5.76

Tangible Book Value

$926,522

Tangible Shareholder’s Equity

(332,730)

Less: Goodwill and Other Intangible

Assets

-

Less: Preferred Stock

$1,259,252

Shareholders’

Equity

160,805,450

Common Shares Outstanding

As Reported |