Attached files

| file | filename |

|---|---|

| EX-32 - EXHIBIT 32 - THQ INC | a2198997zex-32.htm |

| EX-21 - EXHIBIT 21 - THQ INC | a2198997zex-21.htm |

| EX-31.1 - EXHIBIT 31.1 - THQ INC | a2198997zex-31_1.htm |

| EX-23.1 - EXHIBIT 23.1 - THQ INC | a2198997zex-23_1.htm |

| EX-10.37 - EXHIBIT 10.37 - THQ INC | a2198997zex-10_37.htm |

| EX-10.47 - EXHIBIT 10.47 - THQ INC | a2198997zex-10_47.htm |

| EX-10.38 - EXHIBIT 10.38 - THQ INC | a2198997zex-10_38.htm |

| EX-10.18 - EXHIBIT 10.18 - THQ INC | a2198997zex-10_18.htm |

| EX-31.2 - EXHIBIT 31.2 - THQ INC | a2198997zex-31_2.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

ý ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended March 31, 2010

OR

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission file number 0-18813

THQ INC.

(Exact Name of Registrant as Specified in Its Charter)

| Delaware | 13-3541686 | |

| (State or Other Jurisdiction of Incorporation or Organization) |

(I.R.S. Employer Identification No.) |

|

29903 Agoura Road |

||

| Agoura Hills, CA | 91301 | |

| (Address of principal executive offices) | (Zip Code) |

Registrant's telephone number, including area code: (818) 871-5000

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class: | Name of each exchange on which registered: | |

| Common Stock, $.01 par value | The NASDAQ Stock Market LLC | |

| Preferred Stock Purchase Rights | The NASDAQ Stock Market LLC |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 229.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes o No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of "large accelerated filer", "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer o | Accelerated filer þ | Non-accelerated filer o (Do not check if a smaller reporting company) |

Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No þ

The aggregate market value of the voting and non-voting common equity held by non-affiliates, computed by reference to the price at which the common equity was last sold, as of the last business day of the registrant's most recently completed second fiscal quarter, September 26, 2009 was approximately $478.0 million.

The number of shares outstanding of the registrant's common stock as of May 28, 2010 was approximately 67,746,675.

DOCUMENTS INCORPORATED BY REFERENCE

The registrant's 2010 Proxy Statement is incorporated by reference into Part III herein.

THQ INC.

INDEX TO ANNUAL REPORT ON FORM 10-K

FILED WITH THE SECURITIES AND EXCHANGE COMMISSION

FOR THE FISCAL YEAR ENDED MARCH 31, 2010

ITEMS IN FORM 10-K

The statements contained in this Annual Report on Form 10-K that are not historical facts may be "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act of 1995. Such statements include, but are not limited to statements regarding industry prospects and future results of operations or financial position. We generally use words such as "anticipate," "believe," "could," "estimate," "expect," "forecast," "future" "intend," "may," "plan," "positioned," "potential," "project," "scheduled," "set to," "subject to," "upcoming" and other similar expressions to help identify forward-looking statements. These forward-looking statements are based on current expectations, estimates and projections about the business of THQ Inc. and its subsidiaries and are based upon management's current beliefs and certain assumptions made by management. Such forward-looking statements are subject to risks and uncertainties that could cause actual results to differ materially from those expressed or implied by such forward-looking statements, including, but not limited to, business, competitive, economic, legal, political and technological factors affecting our industry, operations, markets, products or pricing. The forward-looking statements contained herein speak only as of the date on which they were made, and we disclaim any obligation to update any forward-looking statements to reflect events or circumstances after the date of this Annual Report. Risks and uncertainties that may affect our future results include, but are not limited to, those discussed under the heading "Risk Factors," included in Item 1A herein.

All references to "we," "us," "our," "THQ," or the "Company" in the following discussion and analysis mean THQ Inc. and its subsidiaries. Most of the properties and titles referred to in this Annual Report are subject to trademark protection.

Introduction

We are a leading worldwide developer and publisher of interactive entertainment software for all popular game systems, including:

- •

- home video game consoles such as the Microsoft Xbox 360 ("Xbox 360"), Nintendo Wii ("Wii"), Sony PlayStation

3 ("PS3") and Sony PlayStation 2 ("PS2");

- •

- handheld platforms such as the Nintendo DS and DSi (collectively referred to as "DS"), and Sony PlayStation Portable

("PSP");

- •

- wireless devices, including the iPhone, iTouch and iPad; and

- •

- personal computers ("PCs"), including games played online.

We also develop and publish titles for digital distribution via Sony's PlayStation Network ("PSN") and Microsoft's Xbox LIVE Marketplace ("Xbox LIVE") and Xbox LIVE Arcade ("XBLA"), as well as digitally offer our PC titles through online download stores and services such as Steam. We believe that digital delivery of games and game content is becoming an increasingly important part of our business.

Our titles span a wide range of categories, including action, adventure, fighting, racing, role-playing, simulation, sports and strategy. We have created, licensed and acquired a group of highly recognizable brands, which we market to a variety of consumer demographics ranging from products targeted at core gamers to products targeted to children and the mass market. Our portfolio of Core Games includes games based on popular fighting brands such as the Ultimate Fighting Championship ("UFC") and World Wrestling Entertainment ("WWE"); racing games based on our MX vs. ATV brand; and action, shooter and strategy games based on our owned intellectual properties such as Company of Heroes, Darksiders, Red Faction, and Saints Row, as well as games based on Games Workshop's Warhammer 40,000 universe. Our Kids, Family and Casual portfolio includes games based on popular brands such as DreamWorks

1

Animation, Disney•Pixar, Marvel Entertainment, NBC's The Biggest Loser, Nickelodeon, and Sony Picture Consumer Product's JEOPARDY! and Wheel of Fortune, as well as games based on our owned intellectual properties, including de Blob and Drawn to Life.

We develop our products using both internal and external development resources. The internal resources consist of producers, game designers, software engineers, artists, animators and game testers located within our internal development studios and corporate headquarters. The external development resources consist of third-party software developers and other independent resources such as artists, voice-over actors and composers. We refer to this group of development resources as our Studio System.

Our global sales network includes offices throughout North America, Europe and Asia Pacific. In the U.S. and Canada, we market and distribute games directly to mass merchandisers, consumer electronic stores, discount warehouses and other national retail chain stores. Internationally, we market and distribute games on a direct-to-retail basis in the territories where we have a direct sales force and to a lesser extent, in the territories where we do not have a direct sales force, third parties distribute our games. We also globally market and distribute games digitally via the Internet and through high-end wireless devices, such as the iPhone, iTouch and iPad.

We were originally incorporated in New York in 1989 as Trinity Acquisition Corporation, which changed its name in 1991 to T.HQ, Inc. following a merger with THQ, Inc., a California corporation. We were reincorporated in Delaware as THQ Inc. in 1997. Our principal executive offices are located at 29903 Agoura Road, Agoura Hills, California 91301, and our telephone number is (818) 871-5000. Our Internet address is http://www.thq.com.

Fiscal Periods

Our fiscal year ends on the Saturday nearest March 31st. For simplicity, all fiscal periods are presented or referenced as ending on a calendar month end. The fiscal year ending March 31, 2011 and the fiscal years ended March 31, 2010, 2009 and 2008 contain the following number of weeks:

Fiscal Period

|

Number of Weeks | Fiscal Period End Date | ||

|---|---|---|---|---|

| Year ending March 31, 2011 ("fiscal 2011") | 52 weeks | April 2, 2011 | ||

| Year ended March 31, 2010 ("fiscal 2010") | 53 weeks | April 3, 2010 | ||

| Year ended March 31, 2009 ("fiscal 2009") | 52 weeks | March 28, 2009 | ||

| Year ended March 31, 2008 ("fiscal 2008") | 52 weeks | March 29, 2008 |

Changes to our Operating Structure and Strategy in Fiscal 2010

During the last two fiscal years, we have restructured our organization in order to support our more focused product strategy. This strategy consists of the following operating goals:

- 1.

- develop

a select number of high quality owned intellectual properties targeted at the core gamer each year;

- 2.

- extend

our leadership in fighting games;

- 3.

- reinvigorate

our kids portfolio and improve profitability in our kids business;

- 4.

- build

our portfolio of casual games that appeal to a broad gamer demographic; and

- 5.

- embrace digital integration and extend our brands to online gaming markets.

During fiscal 2010, we restructured our organization into three business units—Core Games; Kids, Family and Casual Games; and Online Games. Each business unit operates globally with dedicated game development and marketing teams. We also created our Global Publishing unit, which operates in three

2

regions—North America, Europe and Asia Pacific—and is responsible for global distribution and sales of our products.

Core Games

Our Core Games group oversees the production and marketing of action, fighting, racing, shooter and strategy games primarily targeted to avid or "core" gamers. The THQ Core Games franchise portfolio includes games based on popular fighting brands such as UFC and WWE; racing games based on our MX vs. ATV brand; and action, shooter and strategy games based on our established franchises such as Darksiders, Red Faction, Saints Row and Warhammer 40,000. THQ's Core Games are developed primarily at the following THQ studios: Kaos Studios, Relic Entertainment, THQ Digital Studio Phoenix, THQ Digital Studio UK, THQ San Diego, Vigil Games and Volition, Inc. THQ Core Games may also be developed externally. For example, our UFC Undisputed and WWE SmackDown vs. Raw fighting games are currently being developed by external studio Yuke's Co. Ltd., of which we own approximately 15%.

Kids, Family and Casual Games

Our Kids, Family and Casual Games group oversees production and marketing of games targeted to the mass market and families. Our Kids, Family and Casual Games portfolio includes original games such as de Blob, Drawn to Life: The Next Chapter and World of Zoo, and games based on leading entertainment brands such as DreamWorks Animation's MegaMind, Marvel Super Hero Squad, Disney•Pixar's Up, NBC's The Biggest Loser, and Sony Pictures Consumer Products' popular game shows JEOPARDY! and Wheel of Fortune. THQ's Kids, Family and Casual Games are developed at THQ's Blue Tongue studio and Studio Australia, as well as by external game developers.

Online Games

THQ's Online Games group oversees production and marketing of dedicated online games. Our online strategy is to leverage our established brands such as Company of Heroes, Warhammer 40,000 and WWE into the dedicated online space. We are currently partnering with companies in China and Korea to deliver Company of Heroes and WWE online in those markets. We also plan to launch Company of Heroes Online in North America. In addition, we are internally developing a Massively Multiplayer Online ("MMO") game based on the Warhammer 40,000 universe.

Our Industry

The interactive entertainment software industry includes the economic sector involved with the development, marketing and sale of video, PC and online games. It encompasses dozens of job disciplines and employs thousands of people worldwide. Video games have increasingly become a mainstream entertainment choice for both children and adults. According to the Entertainment Software Association, more than two-thirds of American households play games, and the average gamer is aged 35 and has been playing for 12 years. In addition, 40% of all players are women.

According to the International Development Group, Inc. ("IDG"), an independent consulting and advisory services company that analyzes the consumer electronics and interactive entertainment industries, sales of console, handheld and PC games (excluding wireless and online) surpassed $21.0 billion in North America and Europe combined in calendar 2009.

The first modern video game platform was introduced by Nintendo in 1985. Since then, advances in technology have resulted in continuous increases in the processing power of the chips that power both the consoles and PC. Today's video game consoles—the PS3, Xbox 360 and Wii—are not simply gaming platforms, but also function as multimedia hubs that can deliver high-quality digital movies and television programs. Video games are also played on PCs that contain powerful graphics cards, and on advanced

3

handheld devices such as the PSP and DS. Additionally, both online gaming and wireless gaming have become popular platforms for video game players over the last several years.

Our Products

We develop, market and sell video games and other interactive software and content for play on console platforms, handheld platforms, mobile devices, PCs and online. The following games generated 10% or more of our net sales during the respective fiscal years:

- •

- in fiscal 2010, UFC 2009 Undisputed and WWE

SmackDown vs. Raw 2010;

- •

- in fiscal 2009, WWE SmackDown vs. Raw 2009, Saints

Row 2, and Wall-E; and

- •

- in fiscal 2008, WWE SmackDown vs. Raw 2008 and Ratatouille.

Our games are based on intellectual property that is either wholly-owned by us or licensed from third parties. We develop our games using both internal development resources and external development resources working for us pursuant to contractual agreements. Whether a game is developed internally or externally, upon completion of development we extensively play-test each game, and if required, send the game to the platform manufacturer (Microsoft, Nintendo or Sony) for its review and approval. Other than games we release for PCs, for online play or for wireless devices, the platform manufacturers or their authorized vendors manufacture our products for us. We then market and distribute our games for sale throughout the world.

Creating and Acquiring Our Intellectual Property

Our business process begins with an idea. Inspiration for our interactive entertainment software comes from many sources—from our internal studios, from our external studio partners, and from existing intellectual properties that we either license or acquire. Historically, most of our titles have been based upon licensed properties that have attained a high level of consumer recognition or acceptance. We have relationships with many well-known licensors and create games based on certain properties they own or control. Licensors generally do not grant exclusive output agreements for all of their properties with any one publisher and thus our licenses are limited to certain of a licensor's properties. Our current key licenses allow us to publish games based on the following properties:

Licensor

|

Properties | |

|---|---|---|

| Disney•Pixar | "Ratatouille," "WALL•E," "Up," and a future, yet to be announced title | |

DreamWorks Animation |

"MegaMind," "Kung Fu Panda: The Kaboom of Doom," "Puss In Boots," and "The Penguins of Madagascar" |

|

Games Workshop |

Warhammer 40,000 universe |

|

Marvel Entertainment |

"Super Hero Squad" |

|

NBC |

"The Biggest Loser" |

|

Nickelodeon |

Kids 6-14 animated properties and related live action movies, including "SpongeBob SquarePants" and "The Last Airbender" |

|

Sony Pictures Consumer Products |

"JEOPARDY!" and "Wheel of Fortune" |

|

World Wrestling Entertainment |

World Wrestling Entertainment content |

|

Zuffa, LLC |

Ultimate Fighting Championship content |

4

These intellectual property licenses generally grant us the exclusive use of the property for specified titles, on specified platforms and for a specified license term. The licenses are of varying duration, and we pay royalties to our property licensors generally based on our net sales of the title that includes the licensor's intellectual property. We typically advance payments against minimum guaranteed royalties over the license term. Royalty rates are generally higher for properties with proven popularity and less perceived risk of commercial failure.

In addition to licensed properties, we continue to create or acquire new intellectual properties that we own. We refer to these properties as our "owned intellectual property[ies]". Our owned intellectual property is generally created by one of our development studios or by a third-party developer with whom we contract. We have also acquired intellectual properties from other publishers or developers. The titles we create based on our owned intellectual properties may contain certain licensed content, such as music or rights to use of a name or object (such as a brand-name vehicle). In this case, we enter into a license agreement with the content owner and pay either a fixed fee or royalty for the use of such content.

Developing Our Products

We develop our products using both internal and external development resources. The internal resources consist of producers, game designers, software engineers, artists, animators and game testers located within our internal studios located throughout North America, in the United Kingdom and in Australia, and in our corporate headquarters. The external development resources consist of third-party software developers and other independent resources such as artists, voice-over actors and composers. We refer to this collective group of development resources as our Studio System.

We make the decision as to which development resources to use based upon the creative and technical challenges of the product, including whether the intellectual property being developed into a game is licensed, an original concept that we created, or an original concept created by a third-party developer. Once we determine where a product will be developed, our product development team oversees the internal or external resources in its design, technical assessment and construction of each game.

The development cycle for a new game depends on the platform and the complexity and scope of the game. Additionally, when developing an intellectual property into a game that is simultaneously being made into a motion picture, our development schedule is designed to ensure that our games are commercially available by the motion picture's theatrical release. Our development cycles generally range as follows:

- •

- 18-36 months for our console and PC games;

- •

- 9-18 months for our handheld games;

- •

- 6-18 months for our casual/social online games; and

- •

- 1-5 years for our Core Online Games (with the longer end of that range for our large scale MMO games).

These development cycles require that we assess whether there will be adequate retailer and consumer demand for a game and its platform well in advance of its release.

The investments in our product development, prior to when a game reaches technological feasibility, and other non-capitalizable costs, are recorded as product development expenses in our consolidated statement of operations. In fiscal 2010, 2009, and 2008, we had product development expenses of $87.2 million, $109.2 million, and $128.9 million, respectively.

Upon completion of development, each game is extensively play-tested by us to ensure compatibility with the appropriate hardware systems and configurations, and to minimize the number of bugs and other defects found in the products. If required, we also send the game to the manufacturer for its review and

5

approval. To support our products after release, we provide online access to our customers on a 24 hour basis as well as operator help lines during regular business hours. The customer support group tracks customer inquiries, and we use this data to help improve the development and production processes.

Manufacturing Our Products

Other than games we release for sale on PCs, digital download, or wireless devices, our video games are manufactured for us by the platform manufacturers or their authorized vendors. We contract with various DVD replicators for the manufacturing of our PC products.

The platform game manufacturing process begins with our placing a purchase order with a manufacturer. We then send the approved software code to the manufacturer (together with related artwork, user instructions, warranty information, brochures and packaging designs) for manufacturing. We order a sufficient amount of product units to meet the requirements of our customers, based upon our sales forecasts for a game. Because we do not manufacture our products ourselves, we do not carry significant amounts of inventory to meet rapid delivery requirements of customers or to assure ourselves of a continuous allotment of goods from manufacturers. At the time our product unit orders are filled by the manufacturer, we become responsible for the costs of manufacturing and the applicable per unit royalty on such units, even if the units do not ultimately sell.

We are required by our platform licenses to provide a standard defective product warranty on all of the products sold. Generally, we are responsible for resolving, at our own expense, any warranty or repair claims. We have not experienced any material warranty claims, but there is no guarantee that we will not experience such claims in the future.

Marketing Our Products

The manner in which we drive consumer demand for our brands across the globe has evolved significantly in recent years as we have expanded our franchise portfolio. At the global brand management level, we take a disciplined approach to defining and refining positioning for our key game releases. We implement extensive consumer research including concept and play testing that is conducted in conjunction with our development studios and third party developers. This research, conducted prior to the commencement of a product and continued through a project's development, allows us to create game experiences that are optimally targeted to the appropriate demographic via content and play patterns that provide maximum marketability to consumers.

Our marketing plans vary by target demographic but generally consist of a three-pronged media plan encompassing TV, print and online advertising. Certain of our campaigns also include billboard advertising, event sponsorship, in-theater advertising and radio placements. We also perform extensive consumer testing of game packaging and TV creative prior to launch in order to determine the efficacy of the creative in communicating the game's positioning, tone, and attributes as well as measuring to what extent the creative drives purchase interest. Retail or Channel Marketing efforts for our games include pre-sell give-aways, displays and/or demonstrations at retailer-specific trade shows, and cooperative retail advertising campaigns.

We are taking a more aggressive approach in what we term the "connected marketing" space. This includes how we build our brand in the online space via editorial opportunities; screen shot, trailer and other game content releases online; advertising; official game websites; and community outreach and management. Social media sites have grown in both their popularity and influence within our diverse target demographic. This new consumer immersion in social media has allowed us to create new ways to drive brand awareness and purchase intent via a medium that is both relevant and authentic to our target demographics' acquisition of information. Game trial has been a key driver of consumer demand for several of our Core Games, through consumer demos released at retail or online, or game demos available at kiosks stationed at sports or other entertainment events.

6

Publicity is another key driver of awareness for our game portfolio, as well as for THQ, as a publicly-held company. We maintain strong relationships with a broad group of business, consumer, entertainment and games enthusiast reporters across the globe, working closely to secure positive editorial coverage across broadcast, print and online editorial outlets.

Distributing and Selling Our Products

In North America, our products are primarily sold directly to mass merchandisers, consumer electronics stores, discount warehouses and national retail chain stores. Our products are also sold to smaller, regional retailers, as well as distributors who, in turn, sell our products to retailers that we do not service directly, such as grocery and drug stores. Our North American sales activities are conducted by THQ sales representatives throughout the United States, as well as by our representatives in Canada and Mexico.

Our international publishing activities are conducted via our offices throughout Europe and Asia Pacific. The international offices market and distribute to direct-to-retail customers and through distributors in both their home territories and, collectively, to approximately 60 additional territories.

We utilize electronic data interchange with most of our major customers in order to (i) efficiently receive, process, and ship customer product orders, and (ii) accurately track and forecast sell-through of products to consumers in order to determine whether to order additional products from the manufacturers. We believe that the direct relationship model we use allows us to better manage inventory, merchandise and communications. We ship all of our products to our North American customers from warehouses located in Michigan and Minnesota, and we ship most of our products to our international customers from warehouses located throughout Europe and Asia Pacific.

As discussed in Part II—Item 7, "Management's Discussion and Analysis of Financial Condition and Results of Operations," we typically only allow returns for our PC products; however, we may decide to provide price protection or allow returns for our video games after we analyze: (i) inventory remaining in the retail channel, (ii) the rate of inventory sell-through in the retail channel, and (iii) our remaining inventory on hand. We maintain a policy of giving credits for price protection and returns, but we do not give cash refunds.

We also globally market and distribute games and content digitally via the Internet and through high-end wireless devices, such as the iPhone, iTouch, and iPad. The industry is delivering a growing amount of games, downloadable content and product add-ons by direct digital download through the Internet and gaming consoles. We believe that much of the growth in the industry will come via online distribution such as massively multi-player games (both subscription and free-to-play), casual micro-transaction based games, paid downloadable content and digital downloads of games. Accordingly, we plan to continue integrating a digital strategy into all of our key franchises.

Platform License Agreements

Before we can develop, market, or sell video games on a console or handheld platform, we must enter into a license agreement with the manufacturer of such platform. The current "platform manufacturers" are Microsoft, Nintendo and Sony. Each of these platform license agreements allows us a non-exclusive right to use, for a fixed term and in a designated territory, technology that is owned by the platform manufacturer in order to publish our games on such platform. We are currently licensed to publish, in most countries throughout the world, titles on Xbox 360; PS3, PS2, and PSP; and the Wii and DS. Additionally, we are authorized to develop and publish online content compatible with each console that utilizes online content. As each platform license expires, if we intend to continue publishing games on such platform, we must enter into a new agreement or an amendment with the platform manufacturer to extend the term of the agreement. Certain agreements, such as the licenses with Sony for the PS3 and PS2 and with Microsoft for the Xbox 360, automatically renew each year unless either party gives notice by the applicable date that it intends to terminate the agreement.

7

Our platform licenses require that each title be approved by the applicable platform manufacturer. The platform manufacturers have the right to review, evaluate and approve a prototype of each title and the title's packaging and marketing materials. Once a title is developed and has been approved by the platform manufacturer, except for online content, the title is manufactured solely by such platform manufacturer or its designated vendor. The licenses establish the payment terms for the manufacture of each cartridge or disc made, which generally provide for a charge for every cartridge or disc manufactured, and also establish a royalty rate for delivery of online content compatible with such manufacturer's platform. The amounts charged by the platform manufacturers for both console discs and handheld cartridges include a manufacturing, printing and packaging fee as well as a royalty for the use of the platform manufacturer's name, proprietary information and technology, and are subject to adjustment by the platform manufacturers at their discretion.

The platform license agreements also require us to indemnify the platform manufacturers with respect to all loss, liability and expense resulting from any claim against the platform manufacturer involving the development, marketing, sale, or use of our games, including any claims for copyright or trademark infringement brought against the platform manufacturer. Each platform license may be terminated by the platform manufacturer if a breach or default by us is not cured after we receive written notice from the platform manufacturer, or if we become insolvent. Upon termination of a platform license for any reason other than our breach or default, we have a limited period of time to sell any existing product inventory remaining as of the date of termination. The length of this sell-off period varies between 90 and 180 days, depending upon the platform agreement. We must destroy any such inventory remaining after the end of the sell-off period. Upon termination as a result of our breach or default, we must destroy any remaining inventory within a minimum number of days as specified by the platform manufacturer.

Seasonality and Deferral of Revenue

The interactive entertainment software industry is highly seasonal, with sales typically significantly higher during the third quarter of our fiscal year, due primarily to the increased demand for interactive games during the year-end holiday buying season.

Net sales are impacted by the deferral and/or recognition of revenue from the sale of titles for which the online service is more-than-inconsequential to the overall functionality of the game and as such represents a deliverable. Such deferrals are recognized ratably over the estimated service period of six months beginning the month after initial sale.

Major Customers

Our largest customers worldwide include Best Buy, GameStop, Target and Wal-Mart. We also sell our products to other national and regional retailers, discount store chains, specialty retailers and distributors. GameStop and Wal-Mart each accounted for more than 10% of our gross sales in fiscal 2010. We have two "Vendor" agreements with Wal-Mart (one for our console products and one for our PC products) that we entered into in 2001 and 2002, respectively, that address certain standard terms and conditions, such as payment terms, between us and Wal-Mart; however, the agreements do not contain any commitment for Wal-Mart to purchase, or for us to sell, any minimum level of products. We do not have any agreements with GameStop. With respect to both Wal-Mart and GameStop, as well as our other customers, the customer submits a purchase order for each purchase request, and that purchase order contains basic pricing and delivery terms for such purchase. None of the purchase orders individually, with any customer, accounted for more than 10% of the Company's consolidated net sales for fiscal 2010. A substantial reduction in purchases, termination of purchases, or business failure by any of our largest customers could have a material adverse effect on us.

8

Competition

As a publisher of interactive entertainment software, we consider ourselves to be part of the entertainment industry. At the most fundamental level, our products compete with other forms of entertainment, such as motion pictures, television, music, Internet and online services for the leisure time and discretionary spending of consumers. Our primary competition for sales of video games comes from Microsoft, Nintendo and Sony, each of which is a large developer and publisher of software for its own platforms, as well as other publishers and developers of interactive entertainment software, such as Activision/Blizzard, Atari, Electronic Arts, LucasArts, Namco, Sega, Take-Two Interactive Software, and Ubisoft. Additionally, certain large intellectual property owners, such as Disney, Viacom, and Warner Bros. have established video game units to develop and publish games based upon certain of the properties they own. In recent years, our competition has expanded to include online publishers of interactive entertainment, such as Zynga and Shanda Interactive Entertainment.

In addition to competing for video game sales, we compete with our competitors over licenses and brand-name recognition, access to distribution channels, and effectiveness of marketing and price. We also face intense competition from our competitors for the services of talented video game producers, artists, engineers and other employees.

Employees

As of March 31, 2010, we employed approximately 1,680 people, of whom over 640 were outside the United States. We believe that our ability to attract and retain qualified employees is a critical factor in the successful development and exploitation of our products and that our future success will depend, in large measure, on our ability to continue to attract and retain qualified employees. None of our employees are represented by a labor union or covered by a collective bargaining agreement and we consider our relations with employees to be favorable.

Financial Information About Geographic Areas

See Part II—Item 7, "Management Discussion and Analysis of Financial Condition and Results of Operations" and "Note 22—Segment and Geographic Information" in the notes to the consolidated financial statements included in Part II—Item 8.

Available Information

We file annual, quarterly and current reports, proxy statements and other information with the Securities and Exchange Commission ("SEC"). Our SEC filings, including our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and any amendments to those reports filed or furnished pursuant to Section 13(a) of the Exchange Act are available to the public free of charge over the Internet at our website at http://www.thq.com or at the SEC's web site at http://www.sec.gov. Our SEC filings will be available on our website as soon as reasonably practicable after we have electronically filed or furnished them to the SEC. Information contained on our website is not incorporated by reference into this annual report on Form 10-K. You may also read and copy any materials we file with the SEC at the SEC's Public Reference Room at 100 F Street, NE, Washington D.C. 20549. You may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. You can view our Code of Business Conduct and Ethics, our Code of Ethics for Executive Officers and Other Senior Financial Officers and the charters for each of our committees of the Board of Directors free of charge on the corporate governance section of our website.

9

Our business is subject to many risks and uncertainties that may impact our future financial performance. Some of those important risks and uncertainties that may cause our operating results to vary or may materially and adversely impact our operating results are as follows:

We must continue to develop and sell new titles in order to generate net sales and remain profitable.

We derive almost all of our net sales from sales of interactive software games. Even the most successful video games remain popular for only limited periods of time, often less than six months, and thus the success of our business is dependent upon our ability to continually develop and sell successful new games. Because net sales associated with an initial product launch generally constitutes a high percentage of the total net sales associated with the life of a product, the inability of our products to achieve significant market acceptance, delays in product releases or disruptions following the commercial release of our products may have a material adverse impact our net sales and profitability.

Our business is "hit" driven. If we do not deliver "hit" games, our net sales and profitability can suffer.

While many new products are regularly introduced, only a relatively small number of "hit" titles account for a significant portion of video game sales. If we fail to develop "hit" titles, or if "hit" products published by our competitors take a larger share of consumer spending than we anticipate, our product sales could fall below our expectations, which could negatively impact both our net sales and profitability.

Ongoing uncertainty regarding the duration and extent of the recent economic downturn could result in a reduction in discretionary spending by consumers that could reduce demand for our products.

Our products involve discretionary spending on the part of consumers. Consumers are generally more willing to make discretionary purchases, including purchases of products like ours, during periods in which favorable economic conditions prevail. As a result, our products may be sensitive to general economic conditions and economic cycles. A continuation or worsening of current, adverse worldwide economic conditions, including declining consumer confidence, inflation, recession and rising unemployment may lead consumers to delay or reduce purchases of our products. Reduced consumer spending may also require us to incur increased selling and promotional expenses. A reduction or shift in domestic or international consumer spending could negatively impact our business, results of operations and financial condition.

We may not be able to adequately adjust our cost structure in a timely fashion in response to a sudden decrease in demand.

A significant portion of our selling and marketing and our general and administrative expense is attributable to expenses for personnel and facilities. In the event of a significant decline in net sales, we may not be able to dispose of facilities, reduce personnel or make other changes to our cost structure without disruption to our operations or without significant termination and exit costs. Management may not be able to implement such actions in a timely manner, if at all, to offset an immediate shortfall in net sales and profit. Moreover, reducing costs may impair our ability to produce and develop software titles at sufficient levels in the future.

We have significant net operating loss and tax credit carryforwards ("NOLs"). If we are unable to use our NOLs, our future profitability may be significantly impacted.

As of March 31, 2010, we had federal net operating loss carryforwards of $353.8 million and federal R&D tax credit carryforwards of $24.5 million. Under applicable tax rules, we may "carry forward" these NOLs in certain circumstances to offset any current and future taxable income and thus reduce our income tax liability, subject to certain requirements and restrictions. Therefore, we believe that these NOLs could be a

10

substantial asset. However, if we experience an "ownership change," as defined in Section 382 of the Internal Revenue Code, our ability to use the NOLs could be substantially limited, which could significantly increase our future income tax liability. An "ownership change" generally is deemed to occur if our "5-percent shareholders" increase their aggregate percentage ownership of our stock by more than 50 percentage points over the lowest percentage of our stock owned by these 5-percent shareholders at any time during the three-year period prior to any such increase in ownership. While the rules for identifying 5-percent shareholders and their ownership are quite complex, 5-percent shareholders generally include persons that own, at any time during the three-year testing period, 5% or more of our stock directly, as well as by attribution from other persons, and certain groups of stockholders, each of whom owns less than 5% of our stock. On May 12, 2010, we entered into a Section 382 Rights Agreement with Computershare Trust Company, N.A., as rights agent, in an effort to prevent an "ownership change" from occurring and thereby protect the value of the NOLs. There can be no assurance, however, that the Section 382 Rights Plan will prevent an ownership change from occurring, or that entering into the Section 382 Rights Plan will, in fact, protect the value of the NOLs.

We believe our financial condition is sufficient to meet our operating requirements for at least the next twelve months. However, in the event our net sales differ significantly from our expectations, we may need to defer and/or curtail currently-planned expenditures, and/or pursue additional funding to meet our cash needs.

In fiscal 2010, we generated positive operating cash flow and raised $100.0 million through the issuance of convertible senior notes, bringing our cash, cash equivalents and short-term investments to $271.3 million as of March 31, 2010, from $140.7 million as of March 31, 2009. However, we operate in a capital intensive business and intend to invest in product development and licenses in fiscal 2011 and thus do not expect to generate positive cash flow from operations in fiscal 2011. Although we believe that our financial condition is sufficient to meet our operating requirements for at least the next twelve months, in the event our net sales and/or required expenditures differ significantly from our expectations, we may need to defer and/or curtail currently-planned expenditures, and/or pursue additional funding to meet our cash needs.

Since a significant portion of our net sales are based upon licensed properties, failure to renew such licenses, or renewals of such licenses on less advantageous terms, could cause our net sales and/or our profitability to decline.

Games we develop based upon licensed brands make up a substantial portion of our sales each year. Sales of our games based upon our two top-selling licensed brands, UFC and WWE, comprised approximately 35% of our net sales in fiscal 2010. In fiscal 2009, sales of our games based upon our three top-selling licensed brands, Disney•Pixar, Nickelodeon, and WWE, comprised 47% of our net sales. A limited number of licensed brands may continue to produce a disproportionately large amount of our sales. Due to the importance to us of a limited number of brands and the intense competition from other video game publishers to publish games based upon these licensed brands, we may not be able to renew our current licenses or may have to renew a brand license on less advantageous terms, which could significantly lower our net sales and/or our profitability. On January 1, 2010, we entered into an eight year license with WWE. Our license with UFC expires on December 31, 2011; however, we have the right to extend the term of the license to December 31, 2015 if we pay a certain amount of royalties to the licensor based upon units sold, which we believe will be achieved in fiscal 2011. There can be no assurance that we will be able to extend such licenses and if we are not able to extend them, our net sales may decline significantly.

A decrease in the popularity of our licensed brands could materially impact our net sales and financial position.

As previously mentioned, a significant portion of our net sales are derived from products based on popular licensed properties. A decrease in the popularity of the underlying property of our licenses could negatively impact our ability to sell games based on such licenses and could lead to lower net sales, profitability, and/or an impairment of our licenses.

11

Our inability to acquire or create new intellectual property that has a high level of consumer recognition or acceptance could negatively impact our net sales and profitability.

We generate a portion of our net sales from wholly-owned intellectual property. The success of our internal brands depends upon our ability to create original ideas that appeal to the core gamer. Titles based on wholly-owned intellectual property can be expensive to develop and market since they do not have a built-in consumer base or licensor support. Our inability to create new products that find consumer acceptance could negatively impact our net sales and profitability.

Increasing development costs for games which may not perform as anticipated and failure of platforms to achieve significant market penetration could decrease our profitability and result in potential impairments of capitalized software development costs.

Over the last few years, video games have become increasingly expensive to develop. Because the current generation console platforms and PCs have greater complexity and capabilities than the earlier platforms and PCs, costs to develop games for the current generation platforms and PCs are higher. In the last two fiscal years, these greater costs have led to lower operating margins, negatively impacting our profitability. If these increased costs are not offset by higher net sales and other cost efficiencies in the future, our margins and profitability will continue to be impacted, and could result in impairment of capitalized software development costs. If these platforms, or games we develop for these platforms, do not achieve significant market penetration, we may not be able to recover our development costs, which could result in the impairment of capitalized software costs, which would negatively impact our profitability.

We rely on a small number of customers that account for a significant amount of our sales. If these customers reduce their purchases of our products or become unable to pay for them, our business could be harmed.

Our largest customers, Best Buy, GameStop, Target and Wal-Mart, accounted for approximately 43% of our gross sales in fiscal 2010. A substantial reduction, termination of purchases, or business failure by any of our largest customers could have a material adverse impact on us.

A significant portion of our net sales are derived from our international operations, which may subject us to economic, currency, political, regulatory and other risks.

In fiscal 2010, we derived 38% of our net sales from outside of North America. Our international operations subject us to many risks, including: different consumer preferences; challenges in doing business with foreign entities caused by distance, language and cultural differences; unexpected changes in regulatory requirements, tariffs and other barriers; difficulties in staffing and managing foreign operations; and possible difficulties collecting foreign accounts receivable. These factors or others could have an adverse impact on our future foreign sales or the profits generated from those sales.

There are additional risks inherent in doing business in certain international markets, such as China. For example, foreign exchange controls may prevent us from expatriating cash earned in China, and standard business practices in China may increase our risk of violating U.S. laws such as the Foreign Corrupt Practices Act.

Additionally, sales generated by our international offices will generally be denominated in the currency of the country in which the sales are made, and may not correlate to the currency in which inventory is purchased, or software is developed. To the extent our foreign sales are not denominated in U.S. dollars, our sales and profits could be materially and adversely impacted by foreign currency fluctuations. Year-over-year changes in foreign currency translation rates had the mathematical effect of increasing our reported net loss by approximately $0.2 million in fiscal 2010.

12

Fluctuations in our quarterly operating results due to seasonality in the interactive entertainment software industry and other factors related to our business operations could result in substantial losses to investors.

We have experienced, and may continue to experience, significant quarterly fluctuations in sales and operating results. The interactive entertainment software industry is highly seasonal, with sales typically significantly higher during the year-end holiday buying season. Other factors that cause fluctuations in our sales and operating results include:

- •

- the timing of our release of new titles as well as the release of our competitors' products;

- •

- the popularity of both new titles and titles released in prior periods;

- •

- the profit margins for titles we sell;

- •

- the competition in the industry for retail shelf space;

- •

- fluctuations in the size and rate of growth of consumer demand for titles for different platforms;

- •

- the timing of the introduction of new platforms and the accuracy of retailers' forecasts of consumer demand; and

- •

- the deferral or subsequent recognition of net sales and costs related to certain of our products which contain online functionality.

We believe that quarter-to-quarter comparisons of our operating results are not a good indication of our future performance. We may not be able to maintain consistent profitability on a quarterly or annual basis. It is likely that in some future quarter, our operating results may be below the expectations of public market analysts and investors as a result of the factors described above and others described throughout this "Risk Factors" section, which may in turn cause the price of our common stock to fall or significantly fluctuate.

Our stock price has been volatile and may continue to fluctuate significantly.

The market price of our common stock historically has been, and we expect will continue to be, subject to significant fluctuations. These fluctuations may be due to factors specific to us (including those discussed in this "Risk Factors" section, as well as others not currently known to us or that we currently do not believe are material), to changes in securities analysts' earnings estimates or ratings, to our results or future financial guidance falling below our expectations and analysts' and investors' expectations, to factors impacting the entertainment, computer, software, Internet, media or electronics industries, to our ability to successfully integrate any acquisitions we may make, or to national or international economic conditions. In particular, economic downturns may contribute to the public stock markets' experiencing extreme price and trading volume volatility. These broad market fluctuations have and could continue to adversely impact the market price of our common stock.

Video game product development schedules are difficult to predict and can be subject to delays. Postponements in shipments can substantially impact our sales and profitability in any given quarter.

Our ability to meet product development schedules is impacted by a number of factors, including the creative processes involved, the coordination of large and sometimes geographically-dispersed development teams required by the complexity of our products, the need to localize certain products for distribution outside of the U.S., the need to refine our products prior to their release, and the time required to manufacture a game once it is submitted to the platform manufacturer. In the past, we have experienced development and manufacturing delays for several of our products. Failure to meet anticipated production schedules may cause a shortfall in our expected sales and profitability and cause our operating results in any given quarter to be materially different from expectations. Delays that prevent

13

release of our products during peak selling seasons or in conjunction with specific events, such as the release of a related movie, could significantly impact the sales of such products and thus our profitability.

Our business is dependent upon the success and availability of the video game platforms on which consumers play our games.

We derive most of our net sales from the sale of products for play on video game platforms manufactured by third parties, such as PS3 and PSP, Xbox 360, and the Wii and DS. The following factors related to such platforms can adversely impact sales of our video games and our profitability:

Popularity of platforms. In the previous console platform cycle, the PS2 was the best-selling platform and games for that platform dominated software sales. In the current platform cycle, the Wii is the best-selling console platform to date, and in calendar 2009, the Wii surpassed the Xbox 360 as the most popular console in terms of software game sales, according to IDG. However, recent trends indicate that the PS3 and Xbox 360 may be gaining popularity over the twelve months ended March 31, 2011. Since the typical development cycle for a console, handheld, or PC game is from 9 to 36 months, we must make decisions about which games to develop on which platforms based on current expectations of what the consumer preference for the platforms will be when the game is finished. Launching a game on a platform that has declined in popularity, or failure to launch a game on a platform that has grown in popularity, could negatively impact our net sales and profitability.

Platform pricing. Prices for the current generation of console platforms are higher than for their respective predecessor platforms. The Xbox 360 can cost as much as $299.99, the Wii is priced at $199.99 and the PS3 costs $299.99. The cost of the hardware could adversely impact the sales of these platforms, which could in turn negatively impact sales of our products for these platforms since consumers need a platform in order to play our games.

Platform shortages. In the past few years, many of the platforms on which our games are played have experienced shortages. Platform shortages generally negatively impact the sales of video games since consumers do not have consoles on which to play the games.

Our inability to enter into agreements with the manufacturers to develop, publish and distribute titles on their platforms could seriously impact our operations.

We are dependent on the platform manufacturers (Microsoft, Nintendo and Sony) and our non-exclusive licenses with them, both for the right to publish titles for their platforms and for the manufacture of our products for their platforms. Our existing platform licenses require that we obtain approval for the publication of new games on a title-by-title basis. As a result, the number of titles we are able to publish for these platforms, and our sales from titles for these platforms, may be limited. Should any manufacturer choose not to renew or extend our license agreement at the end of its current term, or if any license were terminated, we would be unable to publish additional titles for that manufacturer's platform, which could negatively impact our operating results.

Additionally, since each of the manufacturers publishes games for its own platform, and also manufactures products for all of its other licensees, a manufacturer may give priority to its own products or those of other publishers in the event of insufficient manufacturing capacity. Unanticipated delays in the delivery of products due to delayed manufacturing could also negatively impact our operating results.

14

Software pricing and sales allowances may impact our net sales and profitability.

Software prices for games sold for play on the PS3 and Xbox 360 are generally higher than prices for games for the Wii, handheld platforms or PC games. Our product mix in any given fiscal quarter or fiscal year may cause our net sales to significantly fluctuate depending on which platforms we release games on in that quarter or year. Additionally, reductions in software pricing on any platform may result in lower net sales, which could materially impact our profitability.

In addition, we establish sales allowances based on estimates of future price protection and returns with respect to current period product net sales. While we believe that we can reliably estimate future returns and price protection, if product sell-through does not perform in line with our current expectations, return rates and price protection could exceed our reserves, and our net sales could be negatively impacted in future periods.

Increased sales of used video game products could reduce demand for new copies of our games.

Large retailers, including one of our largest customers, GameStop, have increased their focus on selling used video games, which provides higher margins for the retailers than sales of new games. This focus reduces demand for new copies of our games. We believe customer retention through compelling online play and downloadable content offers may reduce consumers' propensity to trade in games; however, continued sales of used games, rather than new games, may negatively impact our ability to sell new games and thus lower our net sales in any given quarter.

We may face difficulty obtaining access to retail shelf space necessary to market and sell our products effectively.

Retailers typically have a limited amount of shelf space and promotional resources, and there is intense competition among consumer interactive entertainment software products for high quality retail shelf space and promotional support from retailers. To the extent that the number of products and platforms increases, competition for shelf space may intensify and may require us to increase our marketing expenditures. Retailers with limited shelf space typically devote the most and highest quality shelf space to those products expected to be best sellers. We cannot be certain that our new products will consistently achieve such "best seller" status. Due to increased competition for limited shelf space, retailers and distributors are in an increasingly better position to negotiate favorable terms of sale, including price discounts, price protection, marketing and display fees, and product return policies. Our products constitute a relatively small percentage of most retailers' sales volume. We cannot be certain that retailers will continue to purchase our products or to provide those products with adequate levels of shelf space and promotional support on acceptable terms. A prolonged failure in this regard may significantly harm our business and financial results.

Competitive launches may negatively impact the sales of our games.

We compete for consumer dollars with several other video game publishers, and consumers must make choices among available games. If we make our games available for sale at the same time as our competitors' games become available, consumers may choose to spend their money on products published by our competitors rather than our products and retailers may choose to give more shelf space to our competitors' products, leaving less space to sell our products. Since the life cycle of a game is short, strong sales of our competitors' games could negatively impact the sales of our games.

Failure to appropriately adapt to rapid technological changes or emerging distribution channels may negatively impact our market share and our operating results.

Rapid technology changes in our industry require us to anticipate, sometimes years in advance, which technologies we must implement and take advantage of in order to make our products and services competitive. Currently, our industry is experiencing an increasing shift to online content and digital

15

downloads. We believe that much of the growth in the industry will come via online markets or digital distribution such as massively multi-player games (both subscription and free-to-play), casual micro-transaction based games, paid downloadable content and digital downloads of games. Accordingly, we plan to continue integrating a digital strategy into all of our key franchises. However, if we fail to anticipate and adapt to these and other technological changes, our market share and our operating results may suffer. Our future success in providing online games, wireless games and other content will depend upon our ability to adapt to rapidly-changing technologies, develop applications to accommodate evolving industry standards, and improve the performance and reliability of our applications.

Our platform licensors control the fee structures for online distribution of our games on their platforms.

Certain platform licensors have retained the right to change the fee structures for online distribution of both paid content and free content (including patches and corrections) on their platforms. Each licensor's ability to set royalty rates makes it difficult for us to forecast our costs. Increased costs could negatively impact our operating margins. We may be unable to distribute our content in a cost-effective or profitable manner through this distribution channel, which could adversely impact our results of operations.

Development of software by platform manufacturers may lead to reduced sales of our products.

The platform manufacturers, Microsoft, Nintendo and Sony, each develop software for their own hardware platforms. As a result of their commanding positions in the industry, the platform manufacturers may have better bargaining positions with respect to retail pricing, shelf space and retailer accommodations than do any of their licensees, including us. Additionally, the platform manufacturers can bundle their software with their hardware, creating less demand for individual sales of our products. In the twelve month period ended March 31, 2010, Nintendo's market share across North America and top European territories was nearly 49% on its Wii platform and more than 37% on its DS platforms. Continued or increased dominance of software sales by the platform manufacturers may lead to reduced sales of our products and thus lower net sales.

Increased development of software and online games by intellectual property owners may lead to reduced net sales.

As discussed above, a significant portion of our net sales are due to sales of games based upon licensed properties. In recent years, some of our key licensors, including Disney and Viacom (Nickelodeon), have increased their development of video games, which could lead to such licensors not renewing our licenses to publish games based upon their properties that we currently publish, or not granting future licenses to us to develop games based on their other properties. For example, in fiscal 2009, Disney decided to internally develop video games based upon its upcoming movie Toy Story 3 rather than granting the license to develop and publish the game to an external publisher such as us. This may impact our net sales in fiscal 2011, as we are not releasing a new Disney•Pixar title this year. If intellectual property owners continue expanding internal efforts to develop video games based upon properties that they own rather than renewing our licenses or granting us additional licenses, our net sales could be significantly impacted.

Competition for licenses may negatively impact our profitability.

Some of our competitors have greater name recognition among consumers and licensors of properties, a broader product line, or greater financial, marketing and other resources than we do. Accordingly, these competitors may be able to market their products more effectively or make larger offers or guarantees in connection with the acquisition of licensed properties. As competition for popular properties increases, our cost of acquiring licenses for such properties may increase, which could result in reduced margins and thus negatively impact our profitability.

16

Competition with emerging forms of home-based entertainment may reduce sales of our products.

We also compete with other forms of entertainment and leisure activities. For example, we believe the overall growth in the use of the Internet and online services, including social networking, by consumers may pose a competitive threat if customers and potential customers spend less of their available time using interactive entertainment software and more of their time using the Internet and online services.

Competition for qualified personnel is intense in the interactive entertainment software industry and failure to hire and retain qualified personnel could seriously harm our business.

To a substantial extent, we rely on the management, marketing, sales, technical and software development skills of a limited number of employees to formulate and implement our business plan. To a significant extent, our success depends upon our ability to attract and retain key personnel. Competition for employees can be intense and the process of locating key personnel with the right combination of skills is often lengthy. The loss of key personnel could have a material adverse impact on our business.

We rely on external developers for the development of some of our titles.

A large percentage of our net sales are derived from games developed by third-party developers. While we own approximately 15% of Yuke's, the developer of our UFC Undisputed and WWE SmackDown vs. Raw games, we do not have direct control over the business, finances and operational practices of these external developers, including Yuke's. A delay or failure to complete the work performed by external developers has and may in the future result in delays in, or cancellations of, product releases. Additionally, the future success of externally-developed titles will depend on our continued ability to maintain relationships and secure agreements on favorable terms with skilled external developers. Our competitors may acquire the businesses of key developers or sign them to exclusive development arrangements. In either case, we would not be able to continue to engage such developers' services for our products, except for those that they are contractually obligated to complete for us. We cannot guarantee that we will be able to establish or maintain such relationships with external developers, and failure to do so could result in a material adverse impact on our business and financial results.

Defects in our game software could harm our reputation or decrease the market acceptance of our products.

Our game software may contain defects. In addition, because we do not manufacture our games for console platforms, we may not discover defects until after our products are in use by retail customers. Any defects in our software could damage our reputation, cause our customers to terminate relationships with us or to initiate product liability suits against us, divert our engineering resources, delay market acceptance of our products, increase our costs or cause our net sales to decline.

We may not be able to protect our intellectual property rights against piracy, infringement by third parties, or declining legal protection for intellectual property.

We defend our intellectual property rights and combat unlicensed copying and use of software and intellectual property rights through a variety of techniques. Preventing unauthorized use or infringement of our rights is difficult. Unauthorized production occurs in the computer software industry generally, and if a significant amount of unauthorized production of our products were to occur, it could materially and adversely impact our results of operations. We hold copyrights on the products, manuals, advertising and other materials owned by us and we maintain certain trademark rights. We regard our titles, including the underlying software, as proprietary and rely on a combination of trademark, copyright and trade secret laws as well as employee and third-party nondisclosure and confidentiality agreements, among other methods, to protect our rights. We include with our products a "shrink-wrap" or "click-wrap" license agreement which imposes limitations on use of the software. It is uncertain to what extent these agreements and limitations are enforceable, especially in foreign countries. Policing unauthorized use of

17

our products is difficult, and software piracy is a persistent problem, especially in some international markets. Further, the laws of some countries where our products are or may be distributed, either do not protect our products and intellectual property rights to the same extent as the laws of the U.S., or are poorly enforced. Legal protection of our rights may be ineffective in such countries. We cannot be certain that existing intellectual property laws will provide adequate protection for our products.

Software piracy may negatively impact our business.

Software piracy is increasing rapidly in the video game industry. Piracy related to customers obtaining products through peer-to-peer networks and other Internet channels has increased substantially. Modified chips for the Xbox 360 and Wii systems have allowed increased piracy of games for those systems, and the R4 chip has dramatically increased illegal downloads of DS games. While we are taking various steps to protect our intellectual property and prevent illegal downloading of our video games, we may not be successful in preventing or controlling such piracy, which may negatively impact our business.

Third parties may claim we infringe their intellectual property rights.

Although we believe that we make reasonable efforts to ensure our products do not violate the intellectual property rights of others, from time to time, we receive notices from others claiming we have infringed their intellectual property rights. The number of these claims may grow. Responding to these claims may require us to enter into royalty and licensing agreements on unfavorable terms, require us to stop selling or to redesign impacted products, or pay damages or satisfy indemnification commitments including contractual provisions under various license arrangements. If we are required to enter into such agreements or take such actions, our operating margins may decline as a result.

We cannot be certain of the future effectiveness of our internal control over financial reporting or the impact of the same on our operations and the market price for our common stock.

Pursuant to Section 404 of the Sarbanes-Oxley Act of 2002, we are required to include in our Annual Report on Form 10-K our assessment of the effectiveness of our internal control over financial reporting. Furthermore, our independent registered public accounting firm is required to report on whether it believes we maintain, in all material respects, effective internal control over financial reporting. Although we believe that we currently have adequate internal control procedures in place, we cannot be certain that our internal control over financial reporting will be effective in the future. If we cannot adequately maintain the effectiveness of our internal control over financial reporting, we might be subject to sanctions or investigation by regulatory authorities, such as the SEC. Any such action could adversely impact our financial results and the market price of our common stock.

Rating systems and future legislation may make it difficult to successfully market and sell our products.

Currently, the interactive entertainment software industry is self-regulated and products are rated by the Entertainment Software Rating Board ("ESRB"). Our retail customers take the ESRB rating into consideration when deciding which of our products they will purchase. If the ESRB or a manufacturer determines that a product should have a rating directed to an older or more mature consumer, we may be less successful in our marketing and sales of a particular product.

From time to time, legislation has been introduced for the establishment of a government mandated rating and governing system in the U.S. and in foreign countries for our industry. In April 2010, the U.S. Supreme Court granted the state of California's certiorari petition in connection with the constitutionality of California's proposed legislation to regulate the sale of violent video games to minors. Various foreign countries already allow government censorship of interactive entertainment products. We believe that if our industry were to become subject to a government rating system or other regulation (such as the law at

18

issue in the California case), our ability to successfully market and sell our products could be adversely impacted.

Item 1B. Unresolved Staff Comments

None.

Our principal corporate and administrative office is located in approximately 100,000 square feet of leased space in a building located at 29903 Agoura Road, Agoura Hills, California. Including this office, the following is a summary of the square footage of the principal leased offices we maintained as of March 31, 2010:

Purpose

|

North America | Europe | Asia Pacific | Total | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Sales and administrative |

123,900 | 62,400 | 18,400 | 204,700 | ||||||||||

Product development |

424,700 | 6,100 | 27,500 | 458,300 | ||||||||||

Total leased square footage |

548,600 | 68,500 | 45,900 | 663,000 | ||||||||||

We also own 10,820 square feet of space in Phoenix, Arizona, which serves as our data center.

From time to time we are involved in ordinary routine litigation incidental to our business. In the opinion of our management, none of such pending litigation is expected to have a material adverse effect on our consolidated financial condition or results of operations.

Item 4. (Removed and Reserved)

19

Item 5. Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

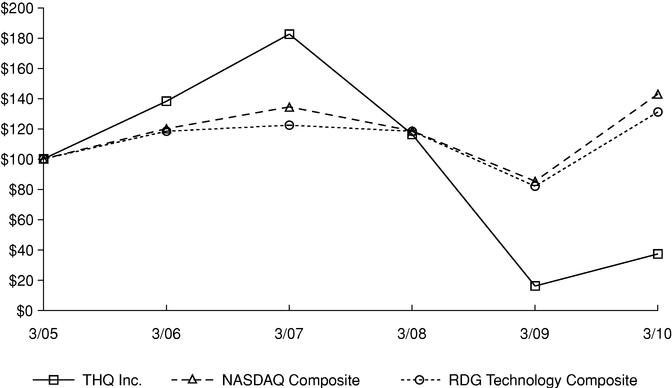

THQ's common stock is quoted on the NASDAQ Global Select Market under the symbol "THQI." The following table sets forth, for the periods indicated, the high and low intraday sales prices of our common stock as reported by the NASDAQ Global Select Market:

| |

Sales Prices | |||||||

|---|---|---|---|---|---|---|---|---|

| |

High | Low | ||||||

Fiscal Year Ended March 31, 2010 |

||||||||

Fourth Quarter ended March 31, 2010 |

$ | 7.30 | $ | 4.88 | ||||

Third Quarter ended December 31, 2009 |

7.45 | 4.12 | ||||||

Second Quarter ended September 30, 2009 |

8.82 | 5.29 | ||||||

First Quarter ended June 30, 2009 |

9.03 | 2.95 | ||||||

Fiscal Year Ended March 31, 2009 |

||||||||

Fourth Quarter ended March 31, 2009 |

$ | 5.40 | $ | 2.23 | ||||

Third Quarter ended December 31, 2008 |

12.25 | 3.29 | ||||||

Second Quarter ended September 30, 2008 |

20.79 | 11.74 | ||||||

First Quarter ended June 30, 2008 |

23.40 | 17.99 | ||||||