Attached files

| file | filename |

|---|---|

| EX-23.1 - CONSENT OF ERNST & YOUNG LLP, AN INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM - Nielsen Holdings plc | dex231.htm |

Table of Contents

As filed with the Securities and Exchange Commission on June 3, 2010

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

NIELSEN HOLDINGS B.V.

(To be converted into Nielsen Holdings N.V.)

(Exact name of registrant as specified in its charter)

| The Netherlands | 7374 | 98-0662038 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

James W. Cuminale, Esq.

Nielsen Holdings B.V.

770 Broadway

New York, New York 10003

(646) 654-5000

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

| Joseph H. Kaufman, Esq. Simpson Thacher & Bartlett LLP 425 Lexington Avenue New York, New York 10017-3954 (212) 455-2000 |

William M. Hartnett, Esq. William J. Miller, Esq. Douglas S. Horowitz, Esq. Cahill Gordon & Reindel LLP 80 Pine Street New York, New York 10005 (212) 701-3000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement is declared effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | ¨ | |||

| Non-accelerated filer | x (Do not check if a smaller reporting company) | Smaller reporting company | ¨ |

CALCULATION OF REGISTRATION FEE

| Title of Each Class of Securities to be Registered |

Proposed Maximum Aggregate Offering Price(1)(2) |

Amount of Registration Fee | ||||

| Common Stock, par value €0.04 per share |

$1,750,000,000 | $124,775 | ||||

| (1) | Includes shares to be sold upon exercise of the underwriters’ option. See “Underwriting.” |

| (2) | Estimated solely for the purpose of calculating the amount of the registration fee pursuant to Rule 457(o) under the Securities Act of 1933, as amended. |

The registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and we are not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to Completion, dated June 3, 2010

Preliminary Prospectus

Shares

Common Stock

We are selling shares of our common stock. This is an initial public offering of our common stock. Prior to this offering, there has been no public market for our common stock. The initial public offering price is estimated to be between $ and $ per share. We intend to apply to have our common stock listed on the under the symbol “ .”

| Per Share |

Total | |||||

| Initial public offering price |

$ | $ | ||||

| Underwriting discount |

$ | $ | ||||

| Proceeds to us, before expenses |

$ | $ | ||||

We have granted the underwriters an option for a period of 30 days to purchase up to additional shares of common stock on the same terms and conditions set forth above to cover over-allotments, if any.

Investing in our common stock involves a high degree of risk. See “Risk Factors ” beginning on page 12.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares of common stock on , 2010.

| J.P. Morgan |

Morgan Stanley |

| Credit Suisse |

Deutsche Bank Securities | Goldman, Sachs & Co. | Citi | |||||

, 2010

Table of Contents

| Page | ||

| ii | ||

| 1 | ||

| 12 | ||

| 26 | ||

| 27 | ||

| 28 | ||

| 29 | ||

| 31 | ||

| 33 | ||

| Management’s Discussion and Analysis of Financial Condition and Results of Operations |

38 | |

| 81 | ||

| 93 | ||

| 101 | ||

| 116 | ||

| 121 | ||

| 124 | ||

| 129 | ||

| 137 | ||

| 139 | ||

| 145 | ||

| 152 | ||

| 152 | ||

| 153 | ||

| F-1 |

You should rely only on the information contained in this prospectus. We have not authorized anyone to provide you with information different from that contained in this prospectus. We are not making an offer to sell nor seeking offers to buy these securities in any jurisdiction where an offer or sale is not permitted. The information contained in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of our common stock.

Nielsen® and our logo are registered trademarks of ours. This prospectus includes other registered and unregistered trademarks of ours. Other products, services and company names mentioned in this prospectus are the service marks/trademarks of their respective owners.

Until , 2010 (25 days after the date of this prospectus), all dealers that effect transactions in our common stock, whether or not participating in this offering, may be required to deliver a prospectus. This requirement is in addition to a dealer’s obligation to deliver a prospectus when acting as an underwriter and with respect to unsold allotments or subscriptions.

i

Table of Contents

The data included in this prospectus regarding market share, market position and industry data pertaining to our business are based on reports of published industry sources and estimates based on our management’s knowledge and experience in the markets in which we operate. These estimates have been based on information obtained from our trade and business organizations and other contacts in the markets in which we operate. We believe these estimates to be accurate as of the date of this prospectus. However, this information may prove to be inaccurate because of the method by which we obtained some of the data for the estimates or because this information cannot always be verified with complete certainty due to the limits on the availability and reliability of raw data, the voluntary nature of the data gathering process and other limitations and uncertainties. As a result, you should be aware that market and industry data included in this prospectus, and estimates and beliefs based on that data, may not be reliable. We cannot guarantee the accuracy or completeness of any such information contained in this prospectus.

ii

Table of Contents

This summary highlights significant aspects of our business and this offering, but it is not complete and does not contain all of the information that you should consider before making your investment decision. You should carefully read the entire prospectus, including the information presented under the section entitled “Risk Factors” and our audited consolidated financial statements, unaudited condensed consolidated financial statements and related notes included elsewhere in this prospectus, before making an investment decision. This summary contains forward-looking statements that involve risks and uncertainties. Our actual results may differ significantly from the results discussed in the forward-looking statements as a result of certain factors, including those set forth in “Risk Factors” and “Cautionary Statement Regarding Forward-Looking Statements.”

The terms “Company,” “Nielsen,” “we,” “our” or “us,” as used herein, refer to Nielsen Holdings B.V. and its affiliates prior to the Conversion (as defined below) and to Nielsen Holdings N.V. and its affiliates upon and after the Conversion, including, in each case, The Nielsen Company B.V., unless otherwise stated or indicated by context. The term “Nielsen Holdings,” as used herein, refers to Nielsen Holdings B.V. prior to the Conversion and to Nielsen Holdings N.V. after the Conversion, in each case, without including any of its affiliates, unless otherwise stated or indicated by context. The term “affiliates” means our direct and indirect subsidiaries and partnerships and joint ventures in which such subsidiaries are partners.

Our Company

We are a leading global information and measurement company that provides clients with a comprehensive understanding of consumers and consumer behavior. We deliver critical media and marketing information, analytics and industry expertise about what consumers watch (consumer interaction with television, online and mobile) and what consumers buy on a global and local basis. Our information, insights and solutions help our clients maintain and strengthen their market positions and identify opportunities for profitable growth. We have a presence in approximately 100 countries, including many developing and emerging markets, and hold leading market positions in many of our services and geographies. Based on the strength of the Nielsen brand, our scale and the breadth and depth of our solutions, we believe we are the global leader in measuring and analyzing consumer behavior in the segments in which we operate.

We help our clients enhance their interactions with consumers and make critical business decisions that we believe positively affect our clients’ sales. Our data and analytics solutions, which have been developed through substantial investment over many decades, are deeply embedded into our clients’ workflow as demonstrated by our long-term client relationships, multi-year contracts and high contract renewal rates. The average length of relationship with our top ten clients, which include The Coca-Cola Company, NBC Universal, Nestle S.A., News Corp., The Procter & Gamble Company and the Unilever Group, is more than 30 years. Typically, before the start of each year, nearly 70% of our annual revenue has been committed under contracts in our combined Watch and Buy segments.

We align our business into three reporting segments, the principal two of which are What Consumers Watch (media audience measurement and analytics) and What Consumers Buy (consumer purchasing measurement and analytics). Our Watch and Buy segments, which together generated 96% of our revenues in 2009, are built on an extensive foundation of proprietary data assets designed to yield essential insights for our clients to successfully measure, analyze and grow their businesses. The information from our Watch and Buy segments, when brought together, can deliver powerful insights into the effectiveness of advertising by linking media consumption trends with consumer purchasing data to better understand how media exposure drives purchase behavior. We believe these integrated insights will better enable our clients to enhance the return on investment of their advertising and marketing spending.

David Calhoun was appointed as our Chief Executive Officer in August 2006 following the purchase of our Company by a consortium of private equity firms on May 24, 2006. Mr. Calhoun and the management team have focused on building an open, simple and integrated operating model that drives innovation, delivers greater value

1

Table of Contents

to our clients and enhances the scalability of our global platform. We have made significant investments in expanding and optimizing our product portfolio and extending our technology platform to strengthen our analytics, measurement science and client delivery capabilities. We have also improved our operating efficiencies by streamlining our organizational structure and processes throughout the Company. As a result of these initiatives, our financial performance has improved significantly between the year ended December 31, 2006 and the year ended December 31, 2009, with revenues increasing to $4.8 billion, a 5.7% compound annual growth rate on a constant currency basis; Adjusted EBITDA increasing to $1.3 billion, a 13.9% compound annual growth rate on a constant currency basis; and Adjusted EBITDA as a percentage of revenue increasing to 27.2% from 21.8%. See note 7 to “—Summary Financial and Other Data” for a definition of Adjusted EBITDA and a reconciliation of Adjusted EBITDA to net income.

Our Segments

Our Watch segment provides viewership data and analytics primarily to the media and advertising industries across television, online and mobile screens. According to ZenithOptimedia, a leading global media services agency, in 2008, total global spending on advertising across television, online and mobile platforms was at least $237 billion. Our Watch data is used by our media clients to understand their audiences, establish the value of their advertising inventory and maximize the value of their content, and by our advertising clients to plan and optimize their spending. Within our Watch segment, our ratings are the primary metrics used to determine the value of programming and advertising in the U.S. total television advertising marketplace, which was approximately $77 billion in 2008 according to a report by Veronis Suhler Stevenson. In addition to the United States, we measure television viewing in 29 countries. We also measure markets that account for approximately 80% of global internet users and offer mobile measurement services in 10 countries, including the United States, where we are the market leader. Watch represented 34% of our total revenues in 2009.

Our Buy segment provides retail transactional measurement data, consumer behavior information and analytics primarily to businesses in the consumer packaged goods industry. According to Euromonitor International, global consumer spending in the product categories we measure was over $7.1 trillion in 2008. Our extensive database of retail and consumer information, combined with our advanced analytical capabilities, helps generate strategic insights that influence our clients’ key business decisions. We track billions of sales transactions per month in retail outlets in approximately 100 countries around the world and our data is used by our clients to measure their sales and market share. We are the only company offering such extensive global coverage for the collection, provision and analysis of this information for consumer packaged goods. Our Buy products and services also enable our clients to better manage their brands, uncover new sources of demand, launch and grow new products, analyze their sales, improve their marketing mix and establish more effective consumer relationships. Buy represented 62% of our total revenues in 2009.

Our Expositions segment operates one of the largest portfolios of business-to-business trade shows in the United States. Each year, we produce approximately 40 trade shows, which in 2009 connected approximately 270,000 buyers and sellers across 20 industries. Expositions represented 4% of our total revenue in 2009.

The Nielsen Opportunity

We believe companies, including our clients, require an increasing amount of data and analytics to set strategy and direct operations. This has resulted in a large market for business information and insight which we believe will continue to grow. Our clients are media, advertising and consumer packaged goods companies in the large and growing markets described above. We believe that significant economic, technological, demographic and competitive trends facing consumers and our clients will provide a competitive advantage to our business and enable us to capture a greater share of our significant market opportunity.

2

Table of Contents

Developing markets present significant expansion opportunities. Brand marketers are focused on attracting new consumers in developing countries as a result of the fast-paced population growth of the middle class in these regions. In addition, the retail trade in these markets is quickly evolving from small, local formats toward larger, more modern formats with electronic points of sale, a similar evolution to what occurred in developed markets over the last several decades. We provide established measurement methodologies to help give consumer packaged goods companies, retailers and media companies an accurate understanding of local consumers to allow them to harness growing consumer buying power in fast growing markets like Brazil, Russia, India and China.

The media landscape is dynamic and changing. Consumers are rapidly changing their media consumption patterns. The growing availability of the internet, and the proliferation of new formats and channels such as mobile devices, social networks and other forms of user-generated media have led to an increasingly fragmented consumer base that is more difficult to measure and analyze. In addition, simultaneous usage of more than one screen is becoming a regular aspect of daily consumer media consumption. We have effectively measured and tracked media consumption through numerous cycles in the industry’s evolution—from broadcast to cable, from analog to digital, from offline to online and from live to time-shifted. We believe our distinct ability to provide metrics across television, online and mobile platforms helps our clients better understand, adapt to and profit from the continued transformation of the global media landscape.

Increasing amounts of consumer information are leading to new marketing approaches. The advent of the internet and other digital platforms has created rapid growth in consumer data that is expected to intensify as more entertainment and commerce are delivered across these platforms. As a result, companies are looking for real-time access to more granular levels of data to understand growth opportunities more quickly and more precisely. This presents a significant opportunity for us to work with companies to effectively manage, integrate and analyze large amounts of information and extract meaningful insights that allow marketers to generate profitable growth.

Consumers are more connected, informed and in control. Today, more than three-quarters of the world’s homes have access to television, there are more than 1.8 billion internet users around the globe, and there are two-thirds as many mobile phones in the world as people. Advances in technology have given consumers a greater level of control of when, where and how they consume information and interact with media and brands. They can compare products and prices instantaneously and have new avenues to learn about, engage with and purchase products and services. These shifts in behavior create significant complexities for our clients. Our broad portfolio of information and insights enables our clients to engage consumers with more impact and efficiency, influence consumer purchasing decisions and actively participate in and shape conversations about their brands.

Demographic shifts and changes in spending behavior are altering the consumer landscape. Consumer demographics and related trends are constantly evolving globally, leading to changes in consumer preferences and the relative size and buying power of major consumer groups. Shifts in population size, age, racial composition, family size and relative wealth are causing marketers to continuously re-evaluate and reprioritize their consumer marketing strategies. We track and interpret consumer demographics that help enable our clients to engage more effectively with their existing consumers as well as forge new relationships with emerging segments of the population.

Consumers are looking for greater value. Economic and social trends have spurred consumers to seek greater value in what they buy as exemplified by the rising demand for “private label” (store branded) products. For instance, in the United States, the absolute dollar share for private label consumer packaged goods increased more than $10 billion over the last two years. This increased focus on value is causing manufacturers, retailers and media companies to re-evaluate brand positioning, pricing and loyalty. We believe companies will increasingly look to our broad range of consumer purchasing insights and analytics to more precisely and effectively measure consumer behavior and target their products and marketing offers at the right place and at the right price.

3

Table of Contents

Our Competitive Advantages

Our key competitive advantages include:

Global Scale and Brand. For nearly 90 years, we have advanced the practice of market research and media audience measurement to provide our clients with a better understanding of their consumer. We provide a breadth of information and insights about the consumer in approximately 100 countries. We believe our global footprint, neutrality, credibility and leading market positions will continue to contribute to our long-term growth and strong operating margins as the number and role of multinational companies expands. Our scale is supported by our global brand, which is defined by the original Nielsen code created by our founder, Arthur C. Nielsen, Sr.: impartiality, thoroughness, accuracy, integrity, economy, price, delivery and service.

Strong, Diversified Client Relationships. Many of the world’s largest brands rely on us as their information and analytics provider to create value for their business. We maintain long-standing relationships across multiple industries, including consumer packaged goods, broadcast and cable television, advertising, online media, telecommunications, retail and automotive. We have more than 20,000 clients across our Watch and Buy segments, with no single client accounting for more than 4% of our total 2009 revenues. In addition, due to our growing presence in developing markets, we have cultivated strong relationships with local market leaders that can benefit from our services as they expand globally. The depth of our client relationships provides a foundation for recurring revenues as well as a platform for growth.

Enhanced Data Assets and Measurement Science. Our extensive portfolio of transactional and consumer behavioral data across our Watch and Buy segments enables us to provide critical information to our clients. Much of the information we provide is not available from any other source and would be difficult and costly for another party to replicate. For decades, we have employed advanced measurement methodologies that yield statistically accurate information about consumer behavior while having due regard for their privacy. We believe that our expertise, established standards and increasingly granular and comprehensive data assets provide us with a distinct advantage as we deliver more precise insights to our clients.

Innovation. We have consistently focused on innovation to deepen our capabilities, expand in new and emerging forms of measurement, enhance our analytical offerings and capitalize on industry trends. We are continuously developing advanced delivery technologies that allow us to maximize the full suite of our data assets for our clients as evidenced by our new delivery platform, Nielsen Answers, which brings a broad portfolio of our data and information to a single client desktop.

Scalable Operating Model. Our global presence and operating model allow us to scale our services and solutions rapidly and efficiently. We have a long track record of establishing leading products that can be quickly expanded across clients, markets and geographies. Our global operations and technology organization enables us to achieve faster, higher quality outcomes for clients in a cost-efficient manner. Our flexible architecture allows us to incorporate leading third-party technologies as well as data from external sources, and enables our clients to use our technology and solutions on their own technology platforms.

4

Table of Contents

Our Growth Strategy

We believe we are well-positioned for growth worldwide and have a multi-faceted strategy that builds upon our brand, strong client relationships and integral role in measuring and analyzing the global consumer.

Continue to grow in developing markets

Developing markets comprised approximately 17% of our 2009 revenues and represent a significant long-term opportunity for us given the growth of the middle class and the rapid evolution and modernization of the retail trade in these regions. Currently, the middle class is growing by 70 million people globally each year, with Brazil, Russia, India and China expected to contribute approximately half of all global consumption growth in 2010. Key elements of our strategy include:

| • | Continuing to grow our existing services in local markets while simultaneously introducing into developing markets new services drawn from our global portfolio; |

| • | Partnering with existing clients as they expand their businesses into developing and emerging markets and providing the high-quality measurement and insights to which they are accustomed; and |

| • | Building relationships with local companies that are expanding beyond their home markets by capitalizing on the global credibility and integrity of the Nielsen brand. |

Continue to develop innovative products and services

We intend to continue developing our product and service portfolio to provide our clients with comprehensive and advanced solutions. Key elements of our strategy include:

| • | Further developing our analytics offerings across all facets of our client base to provide a more comprehensive offering and help our clients think through their most important challenges; |

| • | Continuing to grow our leadership in measurement and insight services related to each individual screen (TV, online and mobile) and expanding our three screen measurement services to help our media clients more effectively reach their target audiences and better understand the value of their content; and |

| • | Expanding our Advertiser Solutions offering, which integrates our proprietary data and analytics from both the Watch and Buy segments, by developing powerful tools to help clients better understand the effectiveness of advertising spending on consumer purchasing behavior. |

Continue to attract new clients and expand existing relationships

We believe that substantial opportunities exist to both attract new clients and to increase our revenue from existing clients. Building on our deep knowledge and the embedded position of our Watch and Buy segments, we expect to sell new and innovative solutions to our new and existing clients, increasing our importance to their decision making processes.

Continue to pursue acquisitions to complement our leadership positions

We have increased our capabilities and expanded our geographic footprint through acquisitions in the areas of online and mobile measurement, social networking, advanced analytics and advertising effectiveness. Going forward, we will consider select acquisitions of complementary businesses that enhance our product and geographic portfolio and can benefit from our scale, scope and status as a global leader.

5

Table of Contents

Key Risks

An investment in our common stock involves substantial risks and uncertainties. Any of the factors set forth under “Risk Factors” may limit our ability to successfully execute our business strategy. Among these important risks are the following:

| • | we may be unable to adapt to significant technological change which could adversely affect our business; |

| • | consolidation in the consumer packaged goods, media, entertainment, telecommunications and technology industries could put pressure on the pricing of our products and services, thereby leading to decreased earnings; |

| • | continued adverse market conditions, particularly in the consumer packaged goods, media, entertainment, telecommunications or technology industries in particular, could adversely impact our revenue; and |

| • | our substantial indebtedness could adversely affect our financial health and we and our subsidiaries may still be able to incur substantially more debt, which could further increase the risk associated with our substantial leverage. |

Company Information

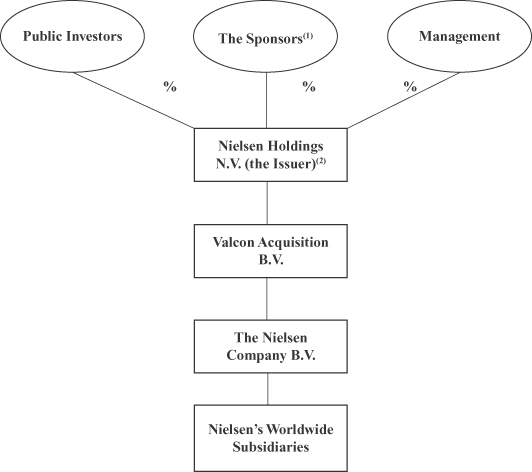

Nielsen Holdings B.V. is a Dutch private company with limited liability (besloten vennootschap met beperkte aansprakelijkeid), incorporated under the laws of the Netherlands on May 17, 2006. The Nielsen Company B.V. and its subsidiaries were purchased on May 24, 2006 through Nielsen Holdings (the “Acquisition”) by a consortium of private equity firms (AlpInvest Partners, The Blackstone Group, The Carlyle Group, Hellman & Friedman, Kohlberg Kravis Roberts & Co. and Thomas H. Lee Partners), who we collectively refer to in this prospectus as the “Original Sponsors.” Subsequently, Centerview Partners invested in the Company. Centerview Partners and the Original Sponsors are collectively referred to in this prospectus as the “Sponsors.”

We are a holding company whose only material asset is 100% of the shares of Valcon Acquisition B.V., a Dutch private company with limited liability, which in turn is a holding company whose only material asset is 100% of the shares of The Nielsen Company B.V. We are owned and controlled by a group of investment funds associated with the Sponsors.

Prior to the completion of this offering, our stockholders will resolve (i) to convert Nielsen Holdings B.V. into a Dutch public company with limited liability (naamloze vennootschap) incorporated under the laws of the Netherlands, and change our name to Nielsen Holdings N.V. and (ii) to amend our articles of association. These actions are collectively referred to herein as the “Conversion.”

Our registered office is located at Diemerhof 2, 1112 XL Diemen, the Netherlands and it is registered at the Commercial Register for Amsterdam under file number 34248449. The phone number of Nielsen in the Netherlands is +31 20 398 8777. Our headquarters are located in New York, New York and the phone number is +1 (646) 654-5000. We maintain a website at www.nielsen.com where general information about our business is available. The information contained on, or accessible from, our website is not a part of this prospectus.

6

Table of Contents

The Offering

| Common stock offered by us |

shares |

| Common stock to be outstanding after this offering |

shares ( shares if the underwriters exercise their option in full) |

| Use of Proceeds |

We estimate that the net proceeds to us from this offering, after deducting underwriting discounts and estimated offering expenses, will be approximately $ million, assuming the shares are offered at $ per share, which is the mid-point of the estimated offering price range set forth on the cover page of this prospectus. |

We intend to use the anticipated net proceeds to repay certain of our existing indebtedness, as will be determined prior to the completion of this offering, and for general corporate purposes.

| Dividend policy |

We do not intend to pay dividends on our common stock for the foreseeable future. |

| Risk Factors |

You should carefully read and consider the information set forth under “Risk Factors” beginning on page 12 of this prospectus and all other information set forth in this prospectus before investing in our common stock. |

Proposed ticker symbol

Unless we indicate otherwise or the context otherwise requires, all information in this prospectus:

| • | assumes (1) no exercise of the underwriters’ option to purchase additional shares of our common stock; and (2) an initial public offering price of $ per share, the midpoint of the initial public offering range indicated on the cover of this prospectus; |

| • | assumes the completion of the Conversion; and |

| • | does not reflect (1) shares of our common stock issuable upon the exercise of outstanding stock options at a weighted average exercise price of $ per share as of March 31, 2010, of which were then exercisable; and (2) shares of our common stock reserved for future grants under our 2006 Stock Acquisition and Option Plan for Key Employees (the “2006 Stock Acquisition and Option Plan”) and/or any new employee benefits plans that we may create prior to the completion of this offering. |

7

Table of Contents

Summary Financial and Other Data

The following table sets forth our summary financial and other data as of the dates and for the periods indicated. The summary consolidated statement of operations and statement of cash flows data for the years ended December 31, 2009, 2008 and 2007 and summary consolidated balance sheet data as of December 31, 2009 have been derived from our audited consolidated financial statements and related notes appearing elsewhere in this prospectus.

The summary financial and other data as of March 31, 2010 and for the three months ended March 31, 2010 and 2009 have been derived from our unaudited condensed consolidated financial statements included elsewhere in this prospectus. The unaudited financial data presented have been prepared on a basis consistent with our audited consolidated financial statements. In the opinion of management, such unaudited financial data reflect all adjustments, consisting only of normal and recurring adjustments, necessary for a fair presentation of the results for those periods.

The results of operations for any period are not necessarily indicative of the results to be expected for any future period. The audited consolidated financial statements from which the historical financial information for the periods set forth below have been derived were prepared in accordance with U.S. generally accepted accounting principles (“GAAP”). The summary financial and other data set forth below should be read in conjunction with, and are qualified by reference to “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” “Selected Financial and Other Data” and our audited consolidated financial statements, unaudited condensed consolidated financial statements and related notes thereto appearing elsewhere in this prospectus.

| Three Months Ended March 31, |

Year Ended December 31, |

|||||||||||||||||||

| (IN MILLIONS, EXCEPT PER SHARE AMOUNTS) |

2010 | 2009 | 2009 | 2008 | 2007 | |||||||||||||||

| Statement of Operations Data: |

||||||||||||||||||||

| Revenues |

$ | 1,196 | $ | 1,102 | $ | 4,808 | $ | 4,806 | $ | 4,458 | ||||||||||

| Cost of revenues, exclusive of depreciation and amortization shown separately below |

520 | 479 | 2,023 | 2,057 | 1,992 | |||||||||||||||

| Selling, general and administrative expenses, exclusive of depreciation and amortization shown separately below |

400 | 376 | 1,523 | 1,616 | 1,506 | |||||||||||||||

| Depreciation and amortization(1) |

141 | 130 | 557 | 499 | 451 | |||||||||||||||

| Impairment of goodwill and intangible assets(2) |

— | — | 527 | 96 | — | |||||||||||||||

| Restructuring costs(3) |

3 | 5 | 62 | 118 | 133 | |||||||||||||||

| Operating income |

$ | 132 | $ | 112 | $ | 116 | $ | 420 | $ | 376 | ||||||||||

| Interest expense, net |

(161 | ) | (162 | ) | (640 | ) | (684 | ) | (661 | ) | ||||||||||

| Other non-operating income/(expense), net(4) |

78 | 54 | (79 | ) | (7 | ) | (69 | ) | ||||||||||||

| Income/(loss) from continuing operations before income taxes and equity in net (loss)/income of affiliates |

49 | 4 | (603 | ) | (271 | ) | (354 | ) | ||||||||||||

| Benefit/(provision) for income taxes |

1 | — | 197 | (36 | ) | (12 | ) | |||||||||||||

| Equity in net (loss)/income of affiliates |

(2 | ) | 3 | (22 | ) | (7 | ) | 2 | ||||||||||||

| Income/(loss) from continuing operations |

48 | 7 | (428 | ) | (314 | ) | (364 | ) | ||||||||||||

| (Loss)/income from discontinued operations, net of tax |

(5 | ) | (4 | ) | (61 | ) | (275 | ) | 10 | |||||||||||

| Net income/(loss) |

43 | 3 | (489 | ) | (589 | ) | (354 | ) | ||||||||||||

| Net income attributable to noncontrolling interests |

1 | 1 | 2 | — | — | |||||||||||||||

| Net income/(loss) attributable to Nielsen stockholders |

$ | 42 | $ | 2 | $ | (491 | ) | $ | (589 | ) | $ | (354 | ) | |||||||

| Income/(loss) from continuing operations per common share (diluted) |

$ | 0.11 | $ | 0.01 | $ | (0.98 | ) | $ | (0.87 | ) | $ | (1.01 | ) | |||||||

| Net income/(loss) attributable to Nielsen stockholders per common share (diluted) |

$ | 0.10 | $ | 0.00 | $ | (1.12 | ) | $ | (1.63 | ) | $ | (0.98 | ) | |||||||

8

Table of Contents

| Three Months Ended March 31, |

Year Ended December 31, |

|||||||||||||||||||

| (IN MILLIONS) |

2010 | 2009 | 2009 | 2008 | 2007 | |||||||||||||||

| Statement of Cash Flows Data: |

||||||||||||||||||||

| Net cash (used in)/provided by operating activities |

$ | (29 | ) | $ | (34 | ) | $ | 517 | $ | 317 | $ | 233 | ||||||||

| Net cash used in investing activities |

(32 | ) | (88 | ) | (227 | ) | (591 | ) | (517 | ) | ||||||||||

| Net cash (used in)/provided by financing activities |

(32 | ) | 81 | (271 | ) | 367 | 9 | |||||||||||||

| (IN MILLIONS) |

March 31, 2010 |

December 31, 2009 | ||||

| Balance Sheet Data (at period end): |

||||||

| Cash and cash equivalents |

$ | 410 | $ | 514 | ||

| Goodwill and intangible assets(5) |

11,720 | 11,813 | ||||

| Total assets |

14,343 | 14,600 | ||||

| Total long-term debt and capital lease obligations, including current portions |

8,558 | 8,640 | ||||

| Total Nielsen stockholders’ equity |

2,809 | 2,798 | ||||

| Three Months Ended March 31, |

Year Ended December 31, |

|||||||||||||||||||

| (IN MILLIONS) |

2010 | 2009 | 2009 | 2008 | 2007 | |||||||||||||||

| Other Financial Data: |

||||||||||||||||||||

| Constant currency revenue growth(6) |

3.6 | % | * | 4.0 | % | 6.1 | % | * | ||||||||||||

| Adjusted EBITDA(7) |

$ | 290 | $ | 257 | $ | 1,312 | $ | 1,205 | $ | 1,081 | ||||||||||

| Capital expenditures |

(53 | ) | (64 | ) | (282 | ) | (370 | ) | (266 | ) | ||||||||||

| Cash paid for income taxes |

(27 | ) | (28 | ) | (139 | ) | (91 | ) | (99 | ) | ||||||||||

| (1) | Depreciation and amortization expense included charges for the depreciation and amortization of acquired tangible and intangible assets of $60 million for the three months ended March 31, 2010 and 2009 and $247 million, $245 million and $233 million for the years ended December 31, 2009, 2008 and 2007, respectively. |

| (2) | Our results for the year ended December 31, 2009 included an aggregate goodwill impairment charge of $282 million and an aggregate customer-related intangible asset impairment charge of $245 million, which were recorded in the third quarter of 2009 relating to our Watch and Expositions segments. Our results for the year ended December 31, 2008 included a goodwill impairment charge of $96 million relating to our Watch segment. See Note 5 – Goodwill and Other Intangible Assets – to the audited consolidated financial statements included elsewhere in this prospectus for additional information. |

| (3) | Represents costs incurred associated with major restructuring initiatives, including the Transformation Initiative and Other Productivity Initiatives discussed further in Note 8 – Restructuring Activities – to the audited consolidated financial statements included elsewhere in this prospectus. |

| (4) | Includes foreign currency exchange transaction gains of $79 million and $78 million for the three months ended March 31, 2010 and 2009, respectively, a loss of $2 million for the year ended December 31, 2009, a gain of $20 million for the year ended December 31, 2008 and a loss of $110 million for the year ended December 31, 2007. These gains and losses resulted primarily from the fluctuation in the value of the U.S. dollar against the Euro applied to certain of our Euro denominated senior secured term loans and debenture loans as well as fluctuations in certain currencies including the Euro and Canadian dollar associated with a portion of our intercompany loan portfolio. Also includes losses on derivative financial instruments, primarily comprised of interest and currency swap arrangements, of $10 million and $22 million for the three months ended March 31, 2010 and 2009, respectively, losses of $60 million and $15 million for the years ended December 31, 2009 and 2008, respectively, and gains of $40 million for the year ended December 31, 2007. In addition, includes other income, net of $9 million and other expense, net of $2 million for the three |

9

Table of Contents

| months ended March 31, 2010 and 2009, respectively, other expenses, net of $17 million and $12 million for the years ended December 31, 2009 and 2008, respectively, and other income, net of $1 million for the year ended December 31, 2007. |

| (5) | Includes intangible assets subject to amortization of $2,748 million and $2,808 million as of March 31, 2010 and December 31, 2009, respectively. |

| (6) | Constant currency revenue growth represents, for each period presented, the percentage growth in revenues from the prior year period removing the positive and negative impacts of changes in foreign currency exchange rates. No data has been presented for the three months ended March 31, 2009 or year ended December 31, 2007 as financial information for the comparable prior year period is not included herein. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations”. |

| (7) | We define Adjusted EBITDA as net income/(loss) attributable to Nielsen stockholders from our consolidated statements of operations before interest income and expense, income taxes, depreciation and amortization, restructuring charges, goodwill and intangible asset impairment charges, stock compensation expense and other non-operating items from our consolidated statements of operations as well as certain other items specifically described below. |

Adjusted EBITDA is not a presentation made in accordance with GAAP, and our use of the term Adjusted EBITDA may vary from the use of similarly titled measures by others in our industry due to the potential inconsistencies in the method of calculation and differences due to items subject to interpretation.

We believe that the presentation of Adjusted EBITDA provides useful information to management and investors regarding financial and business trends related to our results of operations and that when non-GAAP financial information is viewed with GAAP financial information, investors are provided with a more meaningful understanding of our ongoing operating performance. We also use Adjusted EBITDA to compare our results to those of our competitors and to consistently measure our performance from period to period.

Adjusted EBITDA should not be considered as an alternative to net income/(loss), operating income, cash flows from operating activities or any other performance measures derived in accordance with GAAP as measures of operating performance or cash flows as measures of liquidity. Adjusted EBITDA has important limitations as an analytical tool and should not be considered in isolation or as a substitute for analysis of our results as reported under GAAP.

10

Table of Contents

The below table presents a reconciliation from net income/(loss) attributable to Nielsen stockholders to Adjusted EBITDA for the periods presented elsewhere in this prospectus:

| Three Months Ended March 31, |

Year Ended December 31, |

Pro Forma Year Ended December 31, 2006(c) |

||||||||||||||||||||||

| (IN MILLIONS) |

2010 | 2009 | 2009 | 2008 | 2007 | |||||||||||||||||||

| Net income/(loss) attributable to Nielsen stockholders |

$ | 42 | $ | 2 | $ | (491 | ) | $ | (589 | ) | $ | (354 | ) | $ | (419 | ) | ||||||||

| Income attributable to noncontrolling interests |

1 | 1 | 2 | — | — | — | ||||||||||||||||||

| Net income/(loss) |

43 | 3 | (489 | ) | (589 | ) | (354 | ) | (419 | ) | ||||||||||||||

| Loss/(gain) on discontinued operations, net |

5 | 4 | 61 | 275 | (10 | ) | 8 | |||||||||||||||||

| Equity in net loss/(income) of affiliates, net |

2 | (3 | ) | 22 | 7 | (2 | ) | (12 | ) | |||||||||||||||

| (Benefit)/provision for income taxes |

(1 | ) | — | (197 | ) | 36 | 12 | (114 | ) | |||||||||||||||

| Other non-operating (income)/expense, net |

(78 | ) | (54 | ) | 79 | 7 | 69 | 48 | ||||||||||||||||

| Interest expense, net |

161 | 162 | 640 | 684 | 661 | 675 | ||||||||||||||||||

| Operating income |

132 | 112 | 116 | 420 | 376 | 186 | ||||||||||||||||||

| Specified transaction costs(a) |

— | — | — | — | 37 | 143 | ||||||||||||||||||

| Restructuring costs |

3 | 5 | 62 | 118 | 133 | 70 | ||||||||||||||||||

| Impairment of goodwill and intangible assets |

— | — | 527 | 96 | — | — | ||||||||||||||||||

| Depreciation and amortization |

141 | 130 | 557 | 499 | 451 | 423 | ||||||||||||||||||

| Stock compensation expense |

5 | 4 | 14 | 18 | 52 | 34 | ||||||||||||||||||

| Sponsor monitoring fees |

3 | 3 | 12 | 11 | 10 | 10 | ||||||||||||||||||

| Other items(b) |

6 | 3 | 24 | 43 | 22 | 13 | ||||||||||||||||||

| Adjusted EBITDA |

$ | 290 | $ | 257 | $ | 1,312 | $ | 1,205 | $ | 1,081 | $ | 879 | ||||||||||||

| (a) | For the year ended December 31, 2007, we recorded $37 million of charges associated with transaction costs, legal settlements and incremental expenses associated with compensation arrangements and recruiting costs for certain corporate executives. For the year ended December 31, 2006, we recorded a $90 million purchase price adjustment to deferred revenue related to the Valcon Acquisition and we also incurred $53 million in payments in connection with compensation agreements and recruiting expenses for certain corporate executives. |

| (b) | Other items include Transformation Initiative dual running costs of $1 million for the three months ended March 31, 2010 and 2009 and $7 million, $15 million and $7 million for the years ended December 31, 2009, 2008 and 2007, respectively, primarily incurred as a result of the parallel running of data factory systems in Europe. Also includes consulting and other costs of $5 million and $2 million for the three months ended March 31, 2010 and 2009, respectively, and $17 million, $28 million, $15 million and $13 million for the years ended December 31, 2009, 2008, 2007 and 2006, respectively, associated with information technology infrastructure transformation, fees associated with certain consulting arrangements and charges associated with a deferred compensation plan. |

| (c) | The unaudited pro forma presentation for the year ended December 31, 2006 reflects the sum of the results for the Successor period from May 24, 2006 to December 31, 2006 following the Acquisition and the Predecessor period from January 1, 2006 to May 23, 2006 preceding the Acquisition. The 2006 pro forma results are adjusted to reflect the pro forma effect of the Acquisition and the related financing transactions as if they had occurred on January 1, 2006. Pro forma adjustments include: increased interest expense/income net of allocation of interest expense to discontinued operations ($254 million), reversal of transaction costs directly related to the Acquisition ($95 million), reversal of fees associated with extinguishment of bridge financing ($60 million), increased amortization related to purchase price allocation ($40 million), decreased selling, general and administrative expenses ($6 million) consisting of decreased pension costs related to the Acquisition ($10 million) and increased sponsor fees ($4 million) and the related income tax effects. See the “Selected Financial and Other Data” for a further discussion of the unaudited pro forma financial information. |

11

Table of Contents

An investment in our common stock involves risk. You should carefully consider the following risks as well as the other information included in this prospectus, including “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our financial statements and related notes, before investing in our common stock. Any of the following risks could materially and adversely affect our business, financial condition or results of operations. However, the selected risks described below are not the only risks facing us. Additional risks and uncertainties not currently known to us or those we currently view to be immaterial may also materially and adversely affect our business, financial condition or results of operations. In such a case, the trading price of the common stock could decline and you may lose all or part of your investment in our company.

Risks Related to Our Business

We may be unable to adapt to significant technological change which could adversely affect our business.

We operate in businesses that require sophisticated data collection, processing systems, software and other technology. Some of the technologies supporting the industries we serve are changing rapidly. We will be required to adapt to changing technologies, either by developing and marketing new products and services or by enhancing our existing products and services, to meet client demand.

Moreover, the introduction of new products and services embodying new technologies and the emergence of new industry standards could render existing products and services obsolete. Our continued success will depend on our ability to adapt to changing technologies, manage and process ever-increasing amounts of data and information and improve the performance, features and reliability of our existing products and services in response to changing client and industry demands. We may experience difficulties that could delay or prevent the successful design, development, testing, introduction or marketing of our products and services. New products and services, or enhancements to existing products and services, may not adequately meet the requirements of current and prospective clients or achieve any degree of significant market acceptance.

Traditional methods of television viewing are changing as a result of fragmentation of channels and digital and other new television technologies, such as video-on-demand, digital video recorders and internet viewing. If we are unable to continue to successfully adapt our media measurement systems to new viewing habits, our business, financial position and results of operations could be adversely affected.

Consolidation in the consumer packaged goods, media, entertainment, telecommunications and technology industries could put pressure on the pricing of our products and services, thereby leading to decreased earnings.

Consolidation in the consumer packaged goods, media, entertainment, telecommunications and technology industries could reduce aggregate demand for our products and services in the future and could limit the amounts we earn for our products and services. When companies merge, the products and services they previously purchased separately are often purchased by the combined entity in the aggregate in a lesser quantity than before, leading to volume compression and loss of revenue. While we attempt to mitigate the revenue impact of any consolidation by expanding our range of products and services, there can be no assurance as to the degree to which we will be able to do so as industry consolidation continues, which could adversely affect our business, financial position and results of operations.

Client procurement strategies could put additional pressure on the pricing of our information products and services, thereby leading to decreased earnings.

Certain of our clients may continue to seek further price concessions from us. This puts pressure on the pricing of our information products and services, which could limit the amounts we earn. While we attempt to

12

Table of Contents

mitigate the revenue impact of any pricing pressure through effective negotiations and by providing services to individual businesses within particular groups, there can be no assurance as to the degree to which we will be able to do so, which could adversely affect our business, financial position and results of operations.

Continued adverse market conditions, particularly in the consumer packaged goods, media, entertainment, telecommunications or technology industries in particular, could adversely impact our revenue.

As experienced in 2009, a number of adverse financial developments have impacted the U.S. and global financial markets. These developments include a significant economic deterioration both in the United States and globally, volatility and deterioration in the equity markets, and deterioration and tightening of liquidity in the credit markets. In addition, issues related to sovereign debt in Europe recently have negatively affected the global financial markets. The current economic environment has witnessed a significant reduction in consumer confidence and demand, impacting the demand for our customers’ products and services. Those reductions could adversely affect the ability of some of our customers to meet their current obligations to us and hinder their ability to incur new obligations until the economy and their businesses strengthen. The inability of our customers to pay us for our services and/or decisions by current or future customers to forego or defer purchases may adversely impact our business, financial condition, results of operations, profitability and cash flows and may continue to present risks for an extended period of time. We cannot predict the impact of economic slowdowns on our future financial performance.

We expect that revenues generated from our marketing information and television audience measurement services and related software and consulting services will continue to represent a substantial portion of our overall revenue for the foreseeable future. To the extent the businesses we service, especially our clients in the consumer packaged goods, media, entertainment, telecommunications and technology industries, are subject to the financial pressures of, for example, increased costs or reduced demand for their products, the demand for our services, or the prices our clients are willing to pay for those services, may decline.

Clients within our Watch segment derive a significant amount of their revenue from the sale or purchase of advertising. During challenging economic times, advertisers may reduce advertising expenditures and advertising agencies and other media may be less likely to purchase our media information services.

During challenging economic times, clients, typically advertisers, within our Buy segment may reduce their discretionary advertising expenditures and may be less likely to purchase our analytical services.

Our Expositions segment derives a significant amount of its revenues from business-to-business trade shows and events. As experienced in both 2008 and 2009, during challenging economic times exhibitors may cut back on attending our events which would have an adverse effect on our revenue.

We have suffered losses due to goodwill impairment charges and could do so again in the future.

Goodwill and indefinite-lived intangible assets are subject to annual review for impairment (or more frequently should indications of impairment arise). In addition, other intangible assets are also reviewed for impairment whenever events or changes in circumstances indicate that the carrying value of an asset may not be recoverable. Economic volatility has negatively impacted our financial results and, as a direct result, we recorded goodwill impairment charges of $282 million and $96 million for the years ended December 31, 2009 and 2008 respectively (as well as $55 million and $336 million in 2009 and 2008, respectively, relating to discontinued operations) and $245 million of intangible asset impairment charges for the year ended December 31, 2009. Subsequent to the recognition of these impairment charges and as of March 31, 2010, we had goodwill and intangible assets of approximately $11.7 billion. Any further downward revisions in the fair value of our reporting units or our intangible assets could result in further impairment charges for goodwill and intangible assets that could materially affect our financial performance.

13

Table of Contents

Our substantial indebtedness could adversely affect our financial health.

We have now and will continue to have a significant amount of indebtedness. As of March 31, 2010, we had total indebtedness of $8,558 million. Furthermore, the interest payments on our indebtedness could reduce the availability of our cash flow.

Our substantial indebtedness could have important consequences. For example, it could:

| • | increase our vulnerability to the current general adverse economic and industry conditions; |

| • | require us to dedicate a substantial portion of our cash flow from operations to payments on our indebtedness, thereby reducing the availability of our cash flow to fund working capital, capital expenditures, product development efforts and other general corporate purposes; |

| • | limit our flexibility in planning for, or reacting to, changes in our business and the industry in which we operate; |

| • | expose us to the risk of increased interest rates as certain of our borrowings are at variable rates of interest; |

| • | restrict us from making strategic acquisitions or causing us to make non-strategic divestitures; |

| • | limit our ability to obtain additional financing for working capital, capital expenditures, product development, debt service requirements, acquisitions and general corporate or other purposes; |

| • | limit our ability to adjust to changing market conditions; and |

| • | place us at a competitive disadvantage compared to our competitors that have less debt. |

In addition, the indentures governing our outstanding notes and our credit facilities contain financial and other restrictive covenants that will limit the ability of our operating subsidiaries to engage in activities that may be in our best interests in the long term. The failure to comply with those covenants could result in an event of default which, if not cured or waived, could result in the acceleration of all of our debt.

Despite current indebtedness levels, we and our subsidiaries may still be able to incur substantially more debt. This could further increase the risks associated with our substantial leverage.

We and our subsidiaries may be able to incur substantial additional indebtedness in the future. If new debt is added to our and our subsidiaries’ current debt levels, the related risks that we and they now face could intensify.

To service our indebtedness, we will require a significant amount of cash as well as continued access to the capital markets. Our ability to generate cash and our access to the capital markets depend on many factors beyond our control.

Our ability to make payments on our indebtedness and to fund planned capital expenditures and product development efforts will depend on our ability to generate cash in the future and our ability to refinance our indebtedness. This, to a certain extent, is subject to general economic, financial, competitive, legislative, regulatory and other factors that are beyond our control.

We may not be able to generate sufficient cash flow from operations to pay our indebtedness or to fund our other liquidity needs. Our cash interest expense for the years ended December 31, 2009, 2008 and 2007 was $495 million, $494 million and $533 million, respectively, and $147 million and $143 million for the three-month periods ended March 31, 2010 and 2009, respectively. At March 31, 2010, we had $4,689 million of floating-rate debt under our 2006 Senior Secured Credit Facilities and our existing floating rate notes. A one percent increase in our floating rate indebtedness would increase annual interest expense by approximately $47 million. We may need to refinance all or a portion of our indebtedness on or before maturity. We may not be able to refinance any of our indebtedness, including our senior secured credit facilities, on commercially reasonable terms or at all.

14

Table of Contents

The success of our business depends on our ability to recruit sample participants to participate in our research samples.

Our business uses scanners and diaries to gather consumer data from sample households as well as Set Meters, People Meters, Active/Passive Meters and diaries to gather television audience measurement data from sample households. It is increasingly difficult and costly to obtain consent from households to participate in the surveys. In addition, it is increasingly difficult and costly to ensure that the selected sample of households mirrors the behaviors and characteristics of the entire population and covers all of the demographic segments requested by our clients. Additionally, as consumers adopt modes of telecommunication other than traditional telephone service, such as mobile, cable and internet calling, it may become more difficult for our services to reach and recruit participants for consumer purchasing and audience measurement services. If we are unsuccessful in our efforts to recruit appropriate participants and maintain adequate participation levels, our clients may lose confidence in our ratings services and we could lose the support of the relevant industry groups. If this were to happen, our consumer purchasing and audience measurement services may be materially and adversely affected.

Data protection laws may restrict our activities and increase our costs.

Various statutes and rules regulate conduct in areas such as privacy and data protection which may affect our collection, use, storage and transfer of personally identifiable information both abroad and in the United States. Compliance with these laws may require us to make certain investments or may dictate that we not offer certain types of products and services or only offer such services or products after making necessary modifications. Failure to comply with these laws may result in, among other things, civil and criminal liability, negative publicity, data being blocked from use and liability under contractual warranties. In addition, there is an increasing public concern regarding data and consumer protection issues, and the number of jurisdictions with data protection laws has been slowly increasing. There is also the possibility that the scope of existing privacy laws may be expanded. For example, several countries including the United States have regulations that restrict telemarketing to individuals who request to be included on a do-not-call list. Typically, these regulations target sales activity and do not apply to survey research. If the laws were extended to include survey research, our ability to recruit research participants could be adversely affected. These or future initiatives may adversely affect our ability to generate or assemble data or to develop or market current or future products or services, which could negatively impact our business.

Our success will depend on our ability to protect our intellectual property rights.

The success of our business will depend, in part, on:

| • | obtaining patent protection for our technology, products and services; |

| • | defending our patents, copyrights, trademarks, service marks and other intellectual property; |

| • | preserving our trade secrets and maintaining the security of our know-how and data; and |

| • | operating our business without infringing upon intellectual property rights held by third parties. |

We rely on a combination of contractual provisions, confidentiality procedures and the patent, copyright, trademark and trade secret laws of the United States and other countries to protect our intellectual property. These legal measures afford only limited protection and may not provide sufficient protection to prevent the infringement, misuse or misappropriation of our intellectual property. Intellectual property law in several foreign jurisdictions is subject to considerable uncertainty. There can be no assurances that the protections we have available for our proprietary technology in the United States and other countries will be available to us in all of the places we sell our products and services. Any infringement or misappropriation of our technology can have a negative impact on our business. The patents we own could be challenged, invalidated or circumvented by others and may not be of sufficient scope or strength to provide us with meaningful protection or commercial

15

Table of Contents

advantage. The expiration of our patents may lead to increased competition. Although our employees, consultants, clients and collaborators enter into confidentiality agreements with us, our trade secrets, data and know-how could be subject to unauthorized use, misappropriation or unauthorized disclosure. The growing need for global data, along with increased competition and technological advances, puts increasing pressure on us to share our intellectual property for client applications with others, which could result in infringement. Competitors may gain access to our intellectual property and proprietary information. Our trademarks could be challenged, which could force us to rebrand our products or services, result in a loss of brand recognition and require us to devote resources to advertising and marketing new brands. Furthermore, litigation may be necessary to enforce our intellectual property rights, to protect our trade secrets and to determine the validity and scope of our proprietary rights. Given the importance of our intellectual property, we will enforce our rights whenever it is necessary and prudent to do so. Any future litigation, regardless of the outcome, could result in substantial expense and diversion of time and attention of management, may not be resolved in our favor and could adversely affect our business.

If third parties claim that we infringe upon their intellectual property rights, our operating profits could be adversely affected.

We cannot be certain that we do not and will not infringe the intellectual property rights of others in operating our business. We may be subject to legal proceedings and claims in the ordinary course of our business, including claims that we have infringed third parties’ intellectual property rights. Any such claims of intellectual property infringement, even those without merit, could:

| • | be expensive and time-consuming to defend; |

| • | result in our being required to pay possibly significant damages; |

| • | cause us to cease providing our products and services that incorporate the challenged intellectual property; |

| • | require us to redesign or rebrand our products or services; |

| • | divert management’s attention and resources; or |

| • | require us to enter into potentially costly royalty or licensing agreements in order to obtain the right to use a third party’s intellectual property, although royalty or licensing agreements may not be available to us on acceptable terms or at all. |

Any of the above could have a negative impact on our operating profits and harm our future prospects and financial condition.

We generate revenues throughout the world which are subject to exchange rate fluctuations, and our revenue and net income may suffer due to currency translations.

We operate globally, deriving approximately 47% of revenues for the year ended December 31, 2009 in currencies other than U.S. dollars. Our U.S. operations earn revenue and incur expenses primarily in U.S. dollars, while our European operations earn revenue and incur expenses primarily in Euros, which have recently been subject to significant volatility. Outside the United States and the European Union, we generate revenue and expenses predominantly in local currencies. Because of fluctuations (including possible devaluations) in currency exchange rates, we are subject to currency translation exposure on the profits of our operations, in addition to economic exposure. In certain instances, we may not be able to freely convert foreign currencies into U.S. dollars due to limitations placed on such conversions. Certain of the countries in which we operate, such as Venezuela, have currencies which are considered to be hyperinflationary. This risk could have a material adverse effect on our business, results of operations and financial condition.

16

Table of Contents

Our international operations are exposed to risks which could impede growth in the future.

We continue to explore opportunities in major international markets around the world, including China, Russia, India and Brazil. International operations expose us to various additional risks, which could adversely affect our business, including:

| • | costs of customizing services for clients outside of the United States; |

| • | reduced protection for intellectual property rights in some countries; |

| • | the burdens of complying with a wide variety of foreign laws; |

| • | difficulties in managing international operations; |

| • | longer sales and payment cycles; |

| • | exposure to foreign currency exchange rate fluctuation; |

| • | exposure to local economic conditions; |

| • | exposure to local political conditions, including adverse tax policies, civil unrest and seizure of assets by a foreign government; and |

| • | the risks of an outbreak of war, the escalation of hostilities and acts of terrorism in the jurisdictions in which we operate. |

In countries where there has not been a historical practice of using consumer packaged goods retail information or audience measurement information in the buying and selling of advertising time, it may be difficult for us to maintain subscribers.

Criticism of our audience measurement service by various industry groups and market segments could adversely affect our business.

Due to the high-profile nature of our services in the media, internet and entertainment information industries, we could become the target of criticism by various industry groups and market segments. We strive to be fair, transparent and impartial in the production of audience measurement services, and the quality of our U.S. ratings services are voluntarily reviewed and accredited by the Media Rating Council, a voluntary trade organization, whose members include many of our key client constituencies. However, criticism of our business by special interests, and by clients with competing and often conflicting demands on our measurement service, could result in government regulation. While we believe that government regulation is unnecessary, no assurance can be given that legislation will not be enacted in the future that would subject our business to regulation, which could adversely affect our business.

A loss of one of our largest clients could adversely impact our results of operations.

Our top ten clients accounted for approximately 23% of our total revenues for the year ended December 31, 2009. We cannot assure you that any of our clients will continue to use our services to the same extent, or at all, in the future. A loss of one or more of our largest clients, if not replaced by a new client or an increase in business from existing clients, would adversely affect our prospects, business, financial condition and results of operations.

We rely on third parties to provide certain data and services in connection with the provision of our current services.

We rely on third parties to provide certain data and services for use in connection with the provision of our current services. For example, our Buy segment enters into agreements with third parties (primarily retailers of fast-moving consumer goods) to obtain the raw data on retail product sales it processes and edits and from which

17

Table of Contents

it creates products and services. These suppliers of data may increase restrictions on our use of such data, fail to adhere to our quality control standards, increase the price they charge us for this data or refuse altogether to license the data to us. In addition, we may need to enter into agreements with third parties to assist with the marketing, technical and financial aspects of expanding our services for other types of media. In the event we are unable to use such third party data and services or if we are unable to enter into agreements with third parties, when necessary, our business and/or our potential growth could be adversely affected. In the event that such data and services are unavailable for our use or the cost of acquiring such data and services increases, our business could be adversely affected.

We rely on a third party for the performance of a significant portion of our worldwide information technology and operations functions, various services and assistance in certain integration projects. A failure to provide these functions, services or assistance in a satisfactory manner could have an adverse effect on our business.

Pursuant to the terms of a ten year agreement, effective February 19, 2008, we are dependent upon Tata America International Corporation and Tata Consultancy Services Limited (collectively, “TCS”) for the performance of a significant portion of our information technology and operations functions worldwide, the provision of a broad suite of information technology and business process services, including general and process consulting, product engineering, program management, application development and maintenance, coding, data management, finance and accounting services and human resource services, as well as assistance in integrating and centralizing multiple systems, technologies and processes on a global scale. The success of our business depends in part on maintaining our relationships with TCS and their continuing ability to perform these functions and services in a timely and satisfactory manner. If we experience a loss or disruption in the provision of any of these functions or services, or they are not performed in a satisfactory manner, we may have difficulty in finding alternate providers on terms favorable to us, or at all, and our business could be adversely affected.

Long term disruptions in the mail, telecommunication infrastructure and/or air service could adversely affect our business.

Our business is dependent on the use of the mail, telecommunication infrastructure and air service. Long term disruptions in one or more of these services, which could be caused by events such as natural disasters, the outbreak of war, the escalation of hostilities, civil unrest and/or acts of terrorism could adversely affect our business, results of operations and financial condition.

Hardware and software failures, delays in the operation of our computer and communications systems or the failure to implement system enhancements may harm our business.