Attached files

| file | filename |

|---|---|

| 8-K - FORM 8-K - REGIONS FINANCIAL CORP | d8k.htm |

Barclays Capital 2010 Financial

Services Conference

May 19, 2010

Exhibit 99.1 |

| This presentation may

include forward-looking statements which reflect Regions’ current views with respect to future events and financial performance. The Private

Securities Litigation Reform Act of 1995 (“the Act”) provides a safe harbor for

forward-looking statements which are identified as such and are accompanied by the

identification of important factors that could cause actual results to differ materially from the

forward-looking statements. For these statements, we, together with our subsidiaries,

claim the protection afforded by the safe harbor in the Act. Forward-looking statements are not based on historical information, but rather are related to future

operations, strategies, financial results or other developments. Forward-looking statements

are based on management’s expectations as well as certain assumptions and estimates made

by, and information available to, management at the time the statements are made. Those statements are based on general assumptions and are subject to

various risks, uncertainties and other factors that may cause actual results to differ materially from

the views, beliefs and projections expressed in such statements. These risks,

uncertainties and other factors include, but are not limited to, those described below: ›

In 2008, the Emergency Economic Stabilization Act of 2008 became law, and in February 2009 the

American Recovery and Reinvestment Act of 2009 was signed into law. Additionally, the U.S.

Treasury and federal banking regulators are implementing a number of programs to address capital and liquidity issues in the banking

system, and there are a number of pending legislative, regulatory and tax proposals, all of which may

have significant effects on Regions and the financial services industry, the exact nature of

which cannot be determined at this time.

›

The impact of compensation and other restrictions imposed under the Troubled Asset Relief Program

(“TARP”) until Regions repays the outstanding preferred stock and warrant issued

under TARP.

›

Possible additional loan losses, impairment of goodwill and other intangibles and adjustment of

valuation allowances on deferred tax assets and the impact on earnings and

capital.

›

Possible changes in interest rates may affect funding costs and reduce earning asset yields, thus

reducing margins.

›

Possible changes in general economic and business conditions in the United States in general and in

the communities Regions serves in particular.

›

Possible changes in the creditworthiness of customers and the possible impairment of the

collectability of loans.

›

Possible changes in trade, monetary and fiscal policies, laws and regulations, and other activities of

governments, agencies, and similar organizations, including changes in accounting standards,

may have an adverse effect on business.

›

The current stresses in the financial and real estate markets, including possible continued

deterioration in property values.

›

Regions' ability to manage fluctuations in the value of assets and liabilities and off-balance

sheet exposure so as to maintain sufficient capital and liquidity to support Regions'

business.

›

Regions' ability to achieve the earnings expectations related to businesses that have been acquired or

that may be acquired in the future.

›

Regions' ability to expand into new markets and to maintain profit margins in the face of competitive

pressures.

›

Regions' ability to develop competitive new products and services in a timely manner and the

acceptance of such products and services by Regions' customers and potential

customers.

›

Regions' ability to keep pace with technological changes.

›

Regions' ability to effectively manage credit risk, interest rate risk, market risk,

operational risk, legal risk, liquidity risk, and regulatory and compliance risk.

›

Regions’ ability to ensure adequate capitalization is impacted by inherent uncertainties in

forecasting credit losses.

›

The cost and other effects of material contingencies, including litigation

contingencies.

›

The effects of increased competition from both banks and non-banks.

›

The effects of geopolitical instability and risks such as terrorist attacks.

›

Possible changes in consumer and business spending and saving habits could affect Regions' ability to

increase assets and to attract deposits.

›

The effects of weather and natural disasters such as droughts and hurricanes and the effects of the

Gulf of Mexico oil spill. The foregoing list of factors is not exhaustive; for discussion of these and other risks that may

cause actual results to differ from expectations, please look under the captions

“Forward-Looking Statements” and “Risk Factors” in Regions’ Annual Report

on Form 10-K for the year ended December 31, 2009 and Form 10-Q for the quarter ended

March 31, 2010, as on file with the Securities and Exchange Commission.

The words "believe," "expect," "anticipate," "project," and similar

expressions often signify forward-looking statements. You should not place undue reliance on any forward-

looking statements, which speak only as of the date made. Regions assumes no obligation to update or

revise any forward-looking statements that are made from time to time.

Forward Looking Statements

1 |

| Agenda

›

Company Overview

›

Geographically Diversified Footprint

›

Three Major Lines of Business

›

Solid Capital

›

Economic Environment

›

Well Positioned for Return to Profitability

›

Credit Trends Improving

›

Rigorous Expense Management

›

Focused Loan and Deposit Pricing

›

Strategic Priorities

2 |

Diversified Southeastern U.S. Franchise

›

Strategically important position across

a number of Southeastern markets

Regions

Morgan Keegan

Insurance

Offices

1,774

321

31

As of March 31, 2010

3 |

| Consumer

Services – Core Franchise is Strong

›

Every Business Day, Regions Processes:

›

650,000 Branch Transactions

›

293,000 ATM Transactions

›

2.6 Million Debit Card Transactions

›

During 2009, Regions:

›

Opened Over 1 Million New Checking Accounts

›

Grew Interest Free Deposits by Over 25%

›

Increased Online Banking Customers by 25%

›

Achieved Top 10% for Customer Loyalty

›

Top 20% for Branch Customer Service

›

Loans Outstanding = $33.9 billion

4 |

Superior Customer Satisfaction Drives Growth

1.6%

11.4%

794,236

1,008,106

6.1%

10.4%

0.000

New Checking Sales

Attrition

Household Growth

2008

2009

›

90th percentile among competitors for customer loyalty

according to Gallup

›

Customer

retention rate at a historic high and well above

industry norm

5 |

Strong and Improving

Market Share

Note: Based on June 30, 2009 FDIC data per SNL. Adjusted for brokered

deposits in MS and GA. 6

State

Deposits ($B)

Rank

AL

18.9

20

%

23

%

1

FL

17.4

19

4

4

TN

17.3

18

16

1

LA

7.3

8

9

3

MS

7.0

7

16

1

GA

6.4

7

4

6

AR

4.6

5

9

2

TX

3.7

4

1

16

IL

2.7

3

1

24

MO

2.5

3

2

9

IN

2.4

3

3

9

Other

3.5

4

-

-

% of Total

Mkt. Share |

Business Services Revenue is Well-Diversified

and Positioned for Growth

Commercial

& Industrial

Commercial

Real Estate

Business

Banking

Community

Banking

Private

Banking

Specialized

Groups

›

Business Capital

(ABL)

›

Healthcare

›

Transportation

›

Public, Institutional,

Non-profit

›

Restaurant

&

Beverage

7

Loans Outstanding = $54.3 billion |

| Morgan

Keegan ›

Outstanding Diversified Franchise Operating in an

Attractive Region

›

321 Offices in 16 States

›

4,201 Associates, including 1,249 Financial Advisors

›

$149 Billion in Assets Under Management

›

During 2009, Morgan Keegan achieved:

›

Ninth Consecutive Year of Increased Operating Revenues

›

Top 10 Underwriter of Municipal Securities Nationally

›

Number 1 Ranked Focus List Performance

8 |

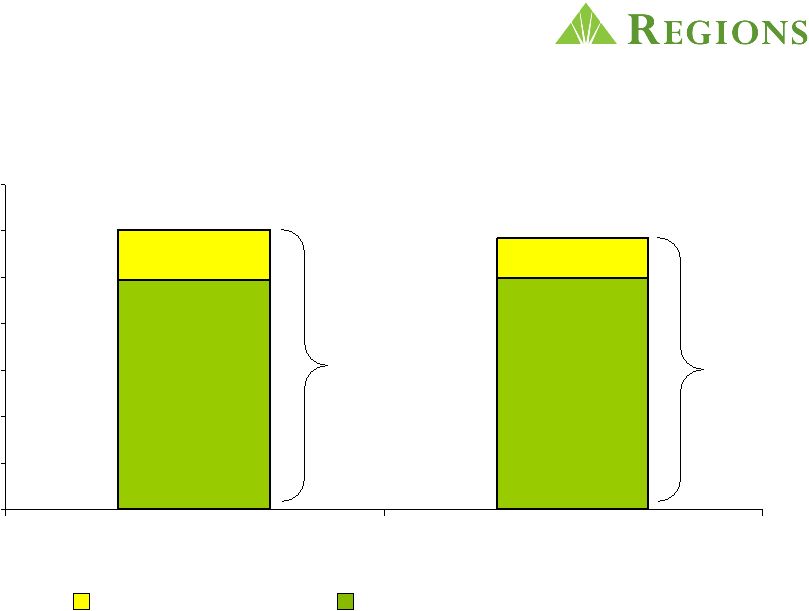

7.1

11.7

RF

Tier 1

T1C

Regions’

Capital Levels Strong and Comparable to Peers

9

Peers include: BAC, BBT, CMA, FITB, KEY, MI, PNC, STI, USB, WFC; MTB

Capital ratios as of March 31, 2010

Source: SNL and Company Reports |

Q4

2009 Risk Weighted Assets/Total Assets Holding Company

69%

71%

73%

80%

82%

84%

85%

86%

89%

92%

93%

104%

RF

Peer Median 85%

Source –

FR Y-9 –

12/31/09

Peers

include:

BAC,

BBT,

CMA,

FITB,

KEY,

MI,

PNC,

STI,

USB,

WFC;

MTB

10 |

Improving Economic Backdrop

GDP

0.1%

2.8%

3.2%

Unemployment

9.3%

9.7%

9.1%

Home Price Index

(4.7%)

(1.3%)

0.7%

Fed Funds

0.2%

0.3%

1.1%

10yr Treasury

3.2%

4.0%

4.5%

2009

2010 (1)

2011 (1)

(1) Blue Chip forecast

11 |

NPA

Migration Declining $0

$500

$1,000

$1,500

$2,000

1Q09

2Q09

3Q09

4Q09

1Q10

Net NPA Change

Gross NPA Additions

$ millions

Net NPA* Change down 41%

4Q09 to 1Q10

* Excludes non-performing assets held for sale

12 |

Disposed of over $3 Billion in Problem Assets

Over Past 18 Months

$0

$300

$600

$900

$1,200

4Q08

1Q09

2Q09

3Q09

4Q09

1Q10

Sales

Transfer to HFS

$ millions

$228

$281

$554

$643

$1,039

Note:

Dispositions

include

loans

sold

or

moved

to

held

for

sale.

The

03/31/10

balance in held for sale was $256MM.

$689

13 |

Charge-Offs Stabilized

$0

$250

$500

$750

$1,000

1Q09

2Q09

3Q09

4Q09

1Q10

Business Services

Consumer

Sales/Transfer to HFS

$ millions

$390

$491

$680

$692

$700

14 |

| Credit

Trends Stable ›

NPAs

peak by the end of 2Q10 and decline thereafter

›

Charge-offs peak by the end of 2Q10 and decline

thereafter

›

Charge-off

guidance remains unchanged: near the

midpoint range of $3.4 billion to $5.9 billion two year loss

range

›

No

reserve build expected in the second half of 2010

15 |

Rigorous Expense Management Muted by

High Recession-Related Expenses

$996

$988

$172

$219

$0

$200

$400

$600

$800

$1,000

$1,200

$1,400

4Q09

1Q10

Other Expenses

Recession-Related Expenses**

$ in millions

$1,207

$1,168

16

**Recession-related expenses includes FDIC premiums, other real estate owned expenses, loan

related legal fees, credit support expenses, etc. |

Strong Focus on Performance Management and

Productivity Improvements

Regions Headcount Trends

37,709

May

2006

Dec

2007

Dec

2008

Dec

2009

33,161

30,784

28,213

25% Reduction

28,509

›

Reduced Total Positions

over 25% since May 2006

›

Focused on Performance

Management/Top Grading

›

Remain focused on

Headcount Management

March

2010

17 |

›

Exceeding 2009 record pace

of new checking account

openings; 248,000 in 1

quarter

›

Average customer deposits

grew $1.9 billion linked

quarter; over $6.5 billion

year-over-year

›

Total deposit costs have

declined 61 basis points in

last 12 months

$80.0

$85.0

$90.0

$95.0

$100.0

1Q09

2Q09

3Q09

4Q09

1Q10

0.90%

1.00%

1.10%

1.20%

1.30%

1.40%

1.50%

1.60%

1.70%

Customer Deposits

Total Deposit Costs

7% year over year

growth in average

customer deposits

Increased Customer Deposits and Lower Cost

18

st |

Improving Net Interest Margin; Expected to Rise

throughout 2010 and Beyond

›

Net interest margin climbed 5 bps

linked quarter; Expected to climb

to 3.00% by year-end 2010

›

Ongoing improvement in deposit

mix and cost with substantial

remaining repricing opportunity in

maturing, higher cost CDs

›

Consistent improvements in

pricing of new and renewed loans

›

Balance sheet well positioned for

eventual rising rate environment

$ in millions

19

$817

$840

$853

$857

$839

$800

$810

$820

$830

$840

$850

$860

1Q09

2Q09

3Q09

4Q09

1Q10

2.50%

2.60%

2.70%

2.80%

2.90%

3.00%

3.10%

Net Interest Income (FTE)

Net Interest Margin |

| Strategic Priorities Guiding Focus and Results

›

Keep Focused on the Customer

›

Protect our Future

›

Restore Financial Performance

›

Execute with Excellence

20 |

|

| Appendix |

Total

Loan Portfolio $88.2bn

Commercial

and Industrial

$21.2bn / 24%

Owner

Occupied

Real Estate

$12.6bn / 15%

1Q10 losses

1.48%

Investor

Real Estate

$20.4bn

23%

Residential

First Mortgage

$15.6bn / 18%

Indirect

$2.2bn / 2%

Direct and

Other

$1.1bn

1%

Home

Equity

$15.1bn

17%

Reduced by $5.4 billion, or 21%, since 2006

Land/Single Family/Condo down $7.3bn

Well diversified by Property Type

Our goal is to further reduce this segment to

no more than 15% of total portfolio

Land

$2.6bn / 13%

Single Family

$1.9bn / 9%

Condo -

$0.5bn / 3

Hotel -

$1.0bn / 5%

Industrial -

$1.4bn / 7%

Office

$2.9bn / 14%

Retail

$3.9bn / 19%

Multi Family

$5.0bn / 24%

Other -

$1.2bn / 6%

Investor Real Estate $20.4bn

›

›

›

› |

Investor Real Estate Portfolio is Well Diversified

23% of Total Portfolio

Other**

$3.7bn / 18%

FL

$4.7bn / 23%

TX

$2.2bn / 11%

GA

$2.2bn / 11%

AL

$1.8bn / 9%

TN

$1.8bn / 9%

NC

$1.2bn / 6%

LA -

$0.9bn / 4%

MO -

$0.7bn / 3%

SC -

$0.7bn / 3%

AR -

$0.5bn / 3%

Loan Size

Geography

0

5,000

10,000

15,000

20,000

25,000

30,000

<$1MM

$1MM-

10MM

$10MM-

25MM

$25MM+

$802 Thousand Average Loan Balance

22,242

2,743

371

78

# of Loans |