Attached files

As Filed with Securities and Exchange Commission on May 17, 2010

SECURITIES AND EXCHANGE COMMISSION

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

VR HOLDINGS, INC.

(Exact name of registrant as specified in its charter)

Delaware (State or other jurisdiction of | 8111 (Primary Standard Industrial | 52-2130901 (I.R.S. Employer Identification No.) |

1615 Chester Road, Chester, Maryland 21619 (443) 519-0129 (Address and Telephone Number of Registrant’s Principal Executive Offices and Principal Place of Business) | Mr. John E. Baker Chief Executive Officer VR Holdings, Inc. 1615 Chester Road, Chester, Maryland 21619 (443) 519-0129 (Name, Address and Telephone Number of Agent for Service) |

With a Copy to:

Norman T. Reynolds, Esq.

Norman T. Reynolds Law Firm

3262 Westheimer Road, Suite 234

Houston, Texas 77098

Telephone No.: (713) 503-9411

Telecopier No.: (713) 621-0230

Approximate date of commencement of proposed sale to the public: From time to time after this registration statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act, check the following box.

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.

i

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

[ ] Large accelerated filer | [ ] Accelerated filer |

[ ] Non-accelerated filer (Do not check if a smaller reporting company) | [X] Smaller reporting company |

CALCULATION OF REGISTRATION FEE

Title of Each Class of Securities To Be Registered | Amount To Be Registered (1) | Offering Price Per Share (2) | Aggregate Offering Price | Amount of Registration Fee |

Common stock, selling stockholders (3) | 26,000,000 | $0.10 | $2,600,000 | $185.38 |

Common stock, the claimants (4) | 5,644,346 | $0.10 | 564,435 | 40.24 |

Common stock, to be sold (5) | 20,000,000 | $0.10 | 2,000,000 | 142.60 |

Total | 51,644,346 | $5,164,435 | $368.22 |

(1)

In the event of a stock split, stock dividend, or similar transaction involving the common stock, the number of shares registered shall automatically be increased to cover the additional shares of common stock issuable pursuant to Rule 416 under the Securities Act.

(2)

Based on Rule 457 under the Securities Act.

(3)

Represents shares held by the selling stockholders. See “Selling Stockholders.”

(4)

Represents shares to be issued to the claimants. See “Prospectus Summary – The Offering” and “Plan of Distribution.”

(5)

Represents shares to be sold to new investors. See “Prospectus Summary – The Offering” and “Plan of Distribution.”

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, or until this registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

ii

PRELIMINARY PROSPECTUS SUBJECT TO COMPLETION, DATED MAY _____, 2010

VR HOLDINGS, INC.

51,644,346 Shares of Common Stock

This prospectus relates to the offering of up to 51,644,346 shares of the common stock of VR Holdings, Inc., a Delaware corporation, $0.000001 par value per share, as follows:

·

The registration for resale of 26,000,000 shares by the selling stockholders identified in this prospectus. The shares were issued in a private placement of our common stock. Please refer to “Selling Stockholders” beginning on page 48 of this prospectus.

·

The registration of the issuance of to 5,644,346 shares of our common stock to various claimants identified in this prospectus. Please refer to “Prospectus Summary – The Offering” beginning on page 1 of this prospectus and “Plan of Distribution.”

·

The registration of the issuance of 20,000,000 shares of our common stock to new investors. Please refer to “Prospectus Summary – The Offering” beginning on page 1 of this prospectus and “Plan of Distribution.”

We will not receive any proceeds from the sale of the shares of our common stock by the selling stockholders or the claimants. We will receive proceeds from the sale of shares of our common stock only to the new investors. We will bear all expenses in connection with the registration of all of the shares of our common stock covered by this prospectus. We are offering the shares to the claimants and the new investors without the use of any placement agent. In the case of the new investors, we will receive all of the proceeds from the sale of the shares of our common stock to the new investors, less any expenses related to this offering. Since we will be selling our shares directly to the new investors, we will not be paying any underwriting discounts or selling commissions.

The selling stockholders are offering shares of our common stock. The selling stockholders may sell all or a portion of these shares from time to time in market transactions through any market on which our common stock is then traded, in negotiated transactions or otherwise, at a price of $0.10 per share until such time as our shares are quoted for sale on the “Pink Sheets” or the OTC Bulletin Board as described in this prospectus, and thereafter, at prices and on terms that will be determined by the then prevailing market price or at privately negotiated prices directly or through a broker or brokers, who may act as agent or as principal or by a combination of such methods of sale. For additional information on the methods of sale, you should refer to the section in this prospectus entitled “Plan of Distribution.”

The selling stockholders and intermediaries through whom the shares of the selling stockholders may be sold may be deemed “underwriters” within the meaning of the Securities Act of 1933, as amended, with respect to the securities offered hereby, and any profits realized or commissions received may be deemed underwriting compensation. We have agreed to indemnify the selling stockholders, the claimants, and the new investors against certain liabilities, including liabilities under the Securities Act.

The shares of our common stock are not currently listed for sale on any exchange, although we do plan to attempt to have our shares quoted for sale on the “Pink Sheets” or the OTC Bulletin Board after the effective date of this prospectus.

THE SECURITIES OFFERED HERBY INVOLVE A HIGH DEGREE OF RISK.

INVESTING IN OUR COMMON STOCK INVOLVES RISKS WHICH ARE DESCRIBED UNDER “RISK FACTORS” BEGINNING ON PAGE 4.

NEITHER THE SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES COMMISSION HAS APPROVED OR DISAPPROVED OF THESE SECURITIES OR

DETERMINED IF THIS PROSPECTUS IS TRUTHFUL OR COMPLETE. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

iii

The date of this prospectus is ____, 2010

The information in this prospectus is not complete and may be changed. A registration statement relating to these securities has been filed with the Securities and Exchange Commission. No one may sell these securities nor may offers to buy be accepted until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any state where the offer, solicitation or sale is not permitted.

|

TABLE OF CONTENTS Prospectus Summary ...............................................................................................................................................................1 Risk Factors ...........................................................................................................................................................................4 Special Note Regarding Forward-Looking Statements .............................................................................................................9 Use of Proceeds ...................................................................................................................................................................10 Market Price of and Dividends on our Common Equity and Related Stockholder Matters...................................................... 11 Capitalization ........................................................................................................................................................................11 Selected Consolidated Financial Data ....................................................................................................................................12 Management’s Discussion and Analysis of Financial Condition and Results of Operations........................................................12 Business................................................................................................................................................................................ 16 Management .........................................................................................................................................................................35 Certain Transactions.............................................................................................................................................................. 41 Principal Stockholders ...........................................................................................................................................................42 Description of Securities........................................................................................................................................................ 43 Certain Provisions of our Certificate of Incorporation and Bylaws ...........................................................................................44 Shares Eligible for Future Sale............................................................................................................................................... 47 Selling Stockholders ..............................................................................................................................................................48 Plan of Distribution ................................................................................................................................................................49 Legal Matters ........................................................................................................................................................................50 Experts .................................................................................................................................................................................50 Reports to Stockholders ........................................................................................................................................................50 Where You Can Find More Information ................................................................................................................................51 Schedule A, The Creditors of Valley Rivet Company, Inc..........................................................................................Schedule A Schedule B, The Creditors of Transcolor Corp. Described in Schedule C, Other Creditors of Transcolor Corp. ...................................................................................................Schedule C |

iv

PROSPECTUS SUMMARY

You should read the entire prospectus carefully, including the more detailed information regarding VR Holdings, Inc., the risks of purchasing our common stock discussed under “Risk Factors,” and our financial statements and the accompanying notes. Throughout this prospectus references to “VRH,” “we,” “us” and “our” refer to VR Holdings, Inc., a Delaware corporation, unless otherwise specified or the context otherwise requires.

The Company

VR Holdings, Inc., a Delaware corporation, was incorporated in 1998 to be the parent company of MML, Inc., a Maryland corporation, the parent company of Alleco, Inc., a Maryland corporation, Allegheny Pepsi Cola Bottling Company, a Maryland corporation, Transcolor Inc., a Maryland corporation and its subsidiary Valley Rivet Company, Inc., an Illinois corporation, entities owned by MML, Inc. which was in turn controlled by Morton M. Lapides, Sr. and his family. VR Holdings itself has never had any operations or employees but has acted as a holding company only. As of the date of this prospectus, Alleco, Inc., Allegheny Pepsi Cola Bottling Company, Transcolor Inc. and its subsidiary, Valley Rivet Company, Inc., and MML, Inc. (collectively, the “VRH Subsidiaries”) are no longer in existence. Mr. Lapides, along with his wife are the controlling stockholders of Deoghe Corp., a Maryland corporation, which is the controlling stockholder of VR Holdings. See “Principal Stockholders.”

Due to a series of events involving alleged illegal practices by various lenders and other parties, VR Holdings lost control of the VRH Subsidiaries and the loss of an estimated $1.6 billion associated with these operations. As a result, it was decided by the stockholders of VR Holdings to reorganize VRH, change our business plan, and file a law suit against various lenders and related parties to recover the damages allegedly caused by alleged illegal activities. See “Business – Legal Proceedings.” Going forward our business is expected to consist of two strategies:

·

Build a diversified portfolio of investments in various legal claims and to provide our stockholders with an attractive level of capital growth through investing directly and indirectly in litigation and arbitration cases, claims and disputes. See “Business - Financing Litigation.”

·

The business of buying and securitizing structured settlement lawsuit payments. See “Business – Structured Settlements.”

There are a number of risks associated with an investment in VRH going forward, many of which are discussed in the sections “Risk Factors” and “Business,” and elsewhere in this prospectus. Any potential investor should be particularly mindful that we have a limited operating history on which to evaluate our business and that a comparison of our results of operations from period to period is not necessarily meaningful. Further, our results of operations for any period are not necessarily indicative of our future performance.

For the fiscal year ended September 30, 2009, we generated no revenues and incurred a net loss of $136,063. As a result, our auditors in their report on our financials for the fiscal year ended September 30, 2009, have expressed substantial doubt about our ability to continue as a going concern. If we are unable to successfully execute our marketing plans with limited resources, we will not be able to generate enough revenue to achieve and maintain profitability or to continue our operations.

During the six months ended March 31, 2010, we incurred a loss of $174,712 as compared to a loss of $58,563 for the six months ended March 31, 2009.

Our principal executive offices are located at 1615 Chester Road, Chester, Maryland 21619, telephone and telecopier number (443) 519-0129, and email cfausa100@aol.com. As of the date of this prospectus, we do not have a website, although, we do expect have one soon. Once our website is established, the information contained in our website shall not constitute part of this prospectus.

1

The Offering

In the fall of 1998, MML, Inc. was the parent of all of the other VRH Subsidiaries. Valley Rivet Company, Inc. was contemplating an acquisition and financing related thereto. Our bank requested restructuring whereby a new parent would own Valley Rivet and MML, Inc, directly, which in turn would own Transcolor and its subsidiaries and Alleco. As a result, VR Holdings became the parent of the VRH Subsidiaries in November 1998, with the same owners that owned MML, Inc. prior to the restructuring.

Valley Rivet filed a voluntary bankruptcy proceeding in 2002, with the result being that VR Holdings did not retain any of the assets of Valley Rivet. However, VR Holdings did retain the assets of MML, Inc. which had a substantial claim resulting from the Winterland transaction (see “Business – Legal Proceedings”). VR Holdings, through Transcolor, although placed in bankruptcy by Marshall & Ilsley Trust Co., the Indenture Trustee, retained litigation claims against Marshall & Ilsley and other parties. See “Business – Legal Proceedings.”

The registration of the issuance of 5,644,346 shares of our common stock to various claimants by means of this prospectus is meant to be in exchange for the claims against VR Holdings or the VRH Subsidiaries by their various creditors, all of whom are referred to as the “claimants” in this prospectus. See “Business – Legal Proceedings” and the discussion in this section and the below referenced Schedules attached to this prospectus.

The calculation of shares proposed to be issued to the claimants is based upon the original amount owed or due certain parties plus interest accrued at a cumulative annual rate of 6% through December 31, 2007. The resulting total due was then divided by $4.47 to determine the actual number of shares to be issued. The value of $4.47 per share was based upon the total estimated claim of VR Holdings which is composed of lost income of VR Holdings and the VRH Subsidiaries, liabilities of VR Holdings at the date of bankruptcy or ceasing of operations, as the case may be, and other related costs such as legal expenses plus an interest assumption. Before any shares of our common stock are issued to a claimant by means of this prospectus, as described below, the claimant must accept the shares in complete settlement and release of all claims against VR Holdings.

As of the date of this prospectus, VR Holdings does not have any legal obligation to offer any of its shares to any of the below described claimants. However, we wish to do so to resolve all potential claims against us so that we can move forward with the expectation that our past liabilities, both asserted and unasserted, have been extinguished.

The projected distribution of the 5,644,346 shares to the accepting claimants would be as follows:

·

Up to 2,471,440 shares to be offered and issued to the various claimants described in Marshall & Ilsley Trust Co. v. Morton M. Lapides, et al. pending in Case No. C-08-134371 in the Circuit Court for Anne Arundel County, Maryland more fully described in “Business – Legal Proceedings.”

·

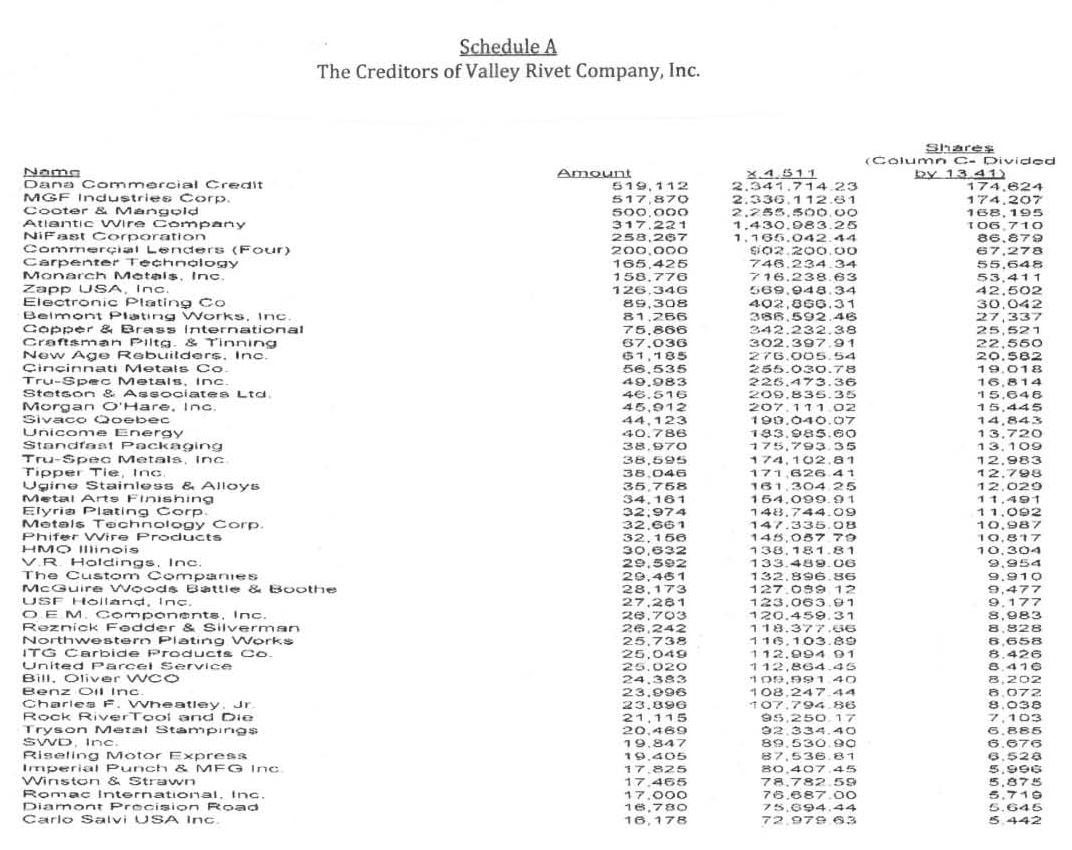

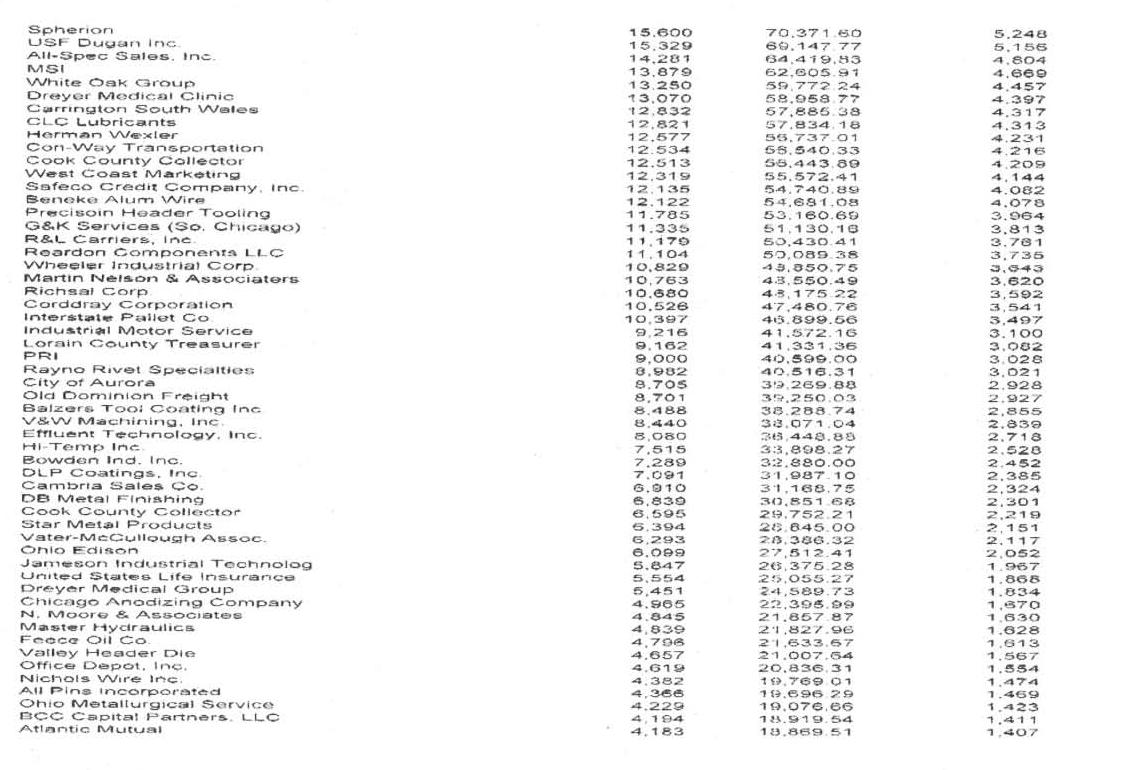

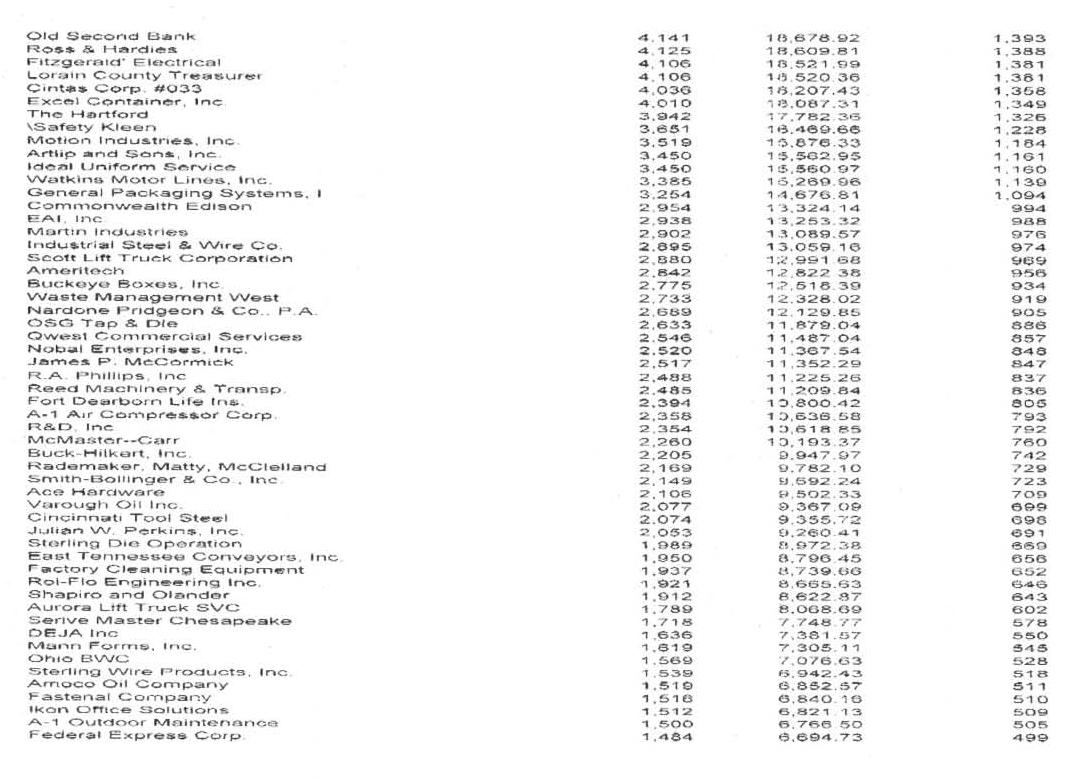

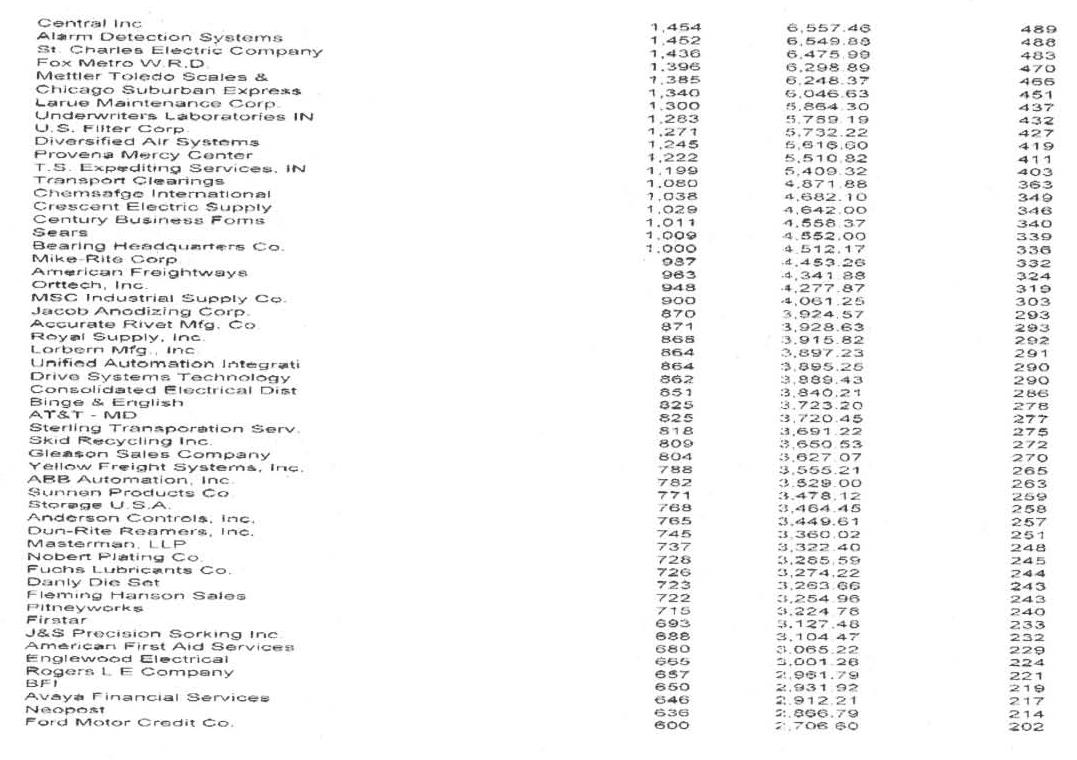

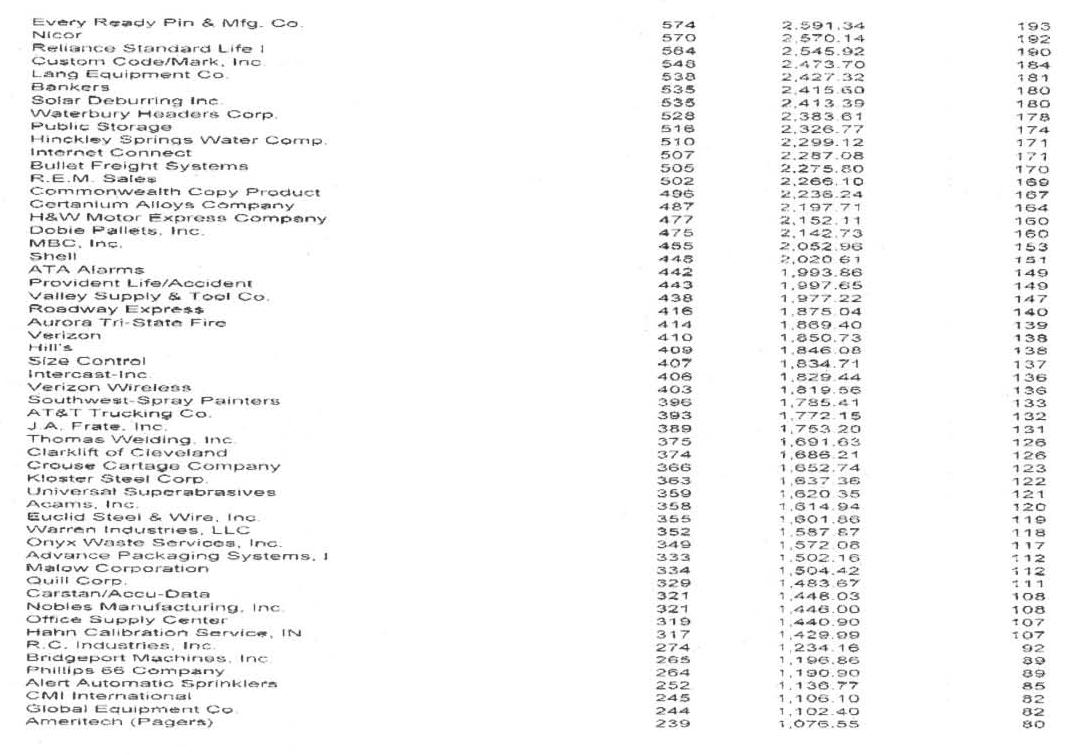

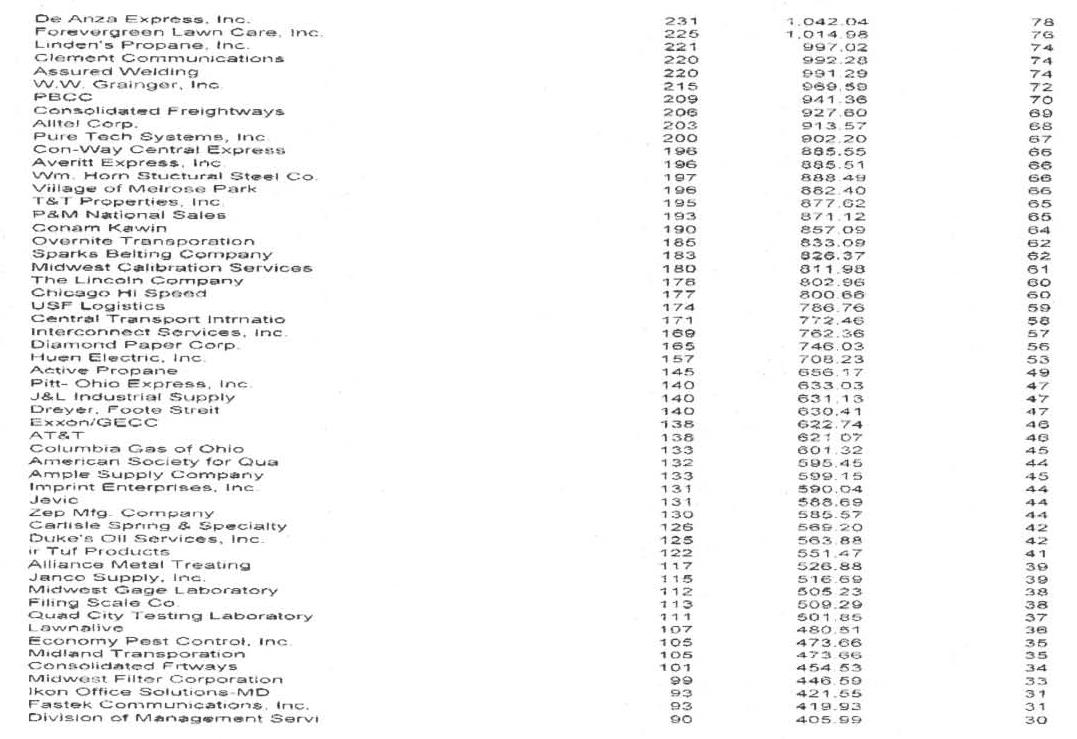

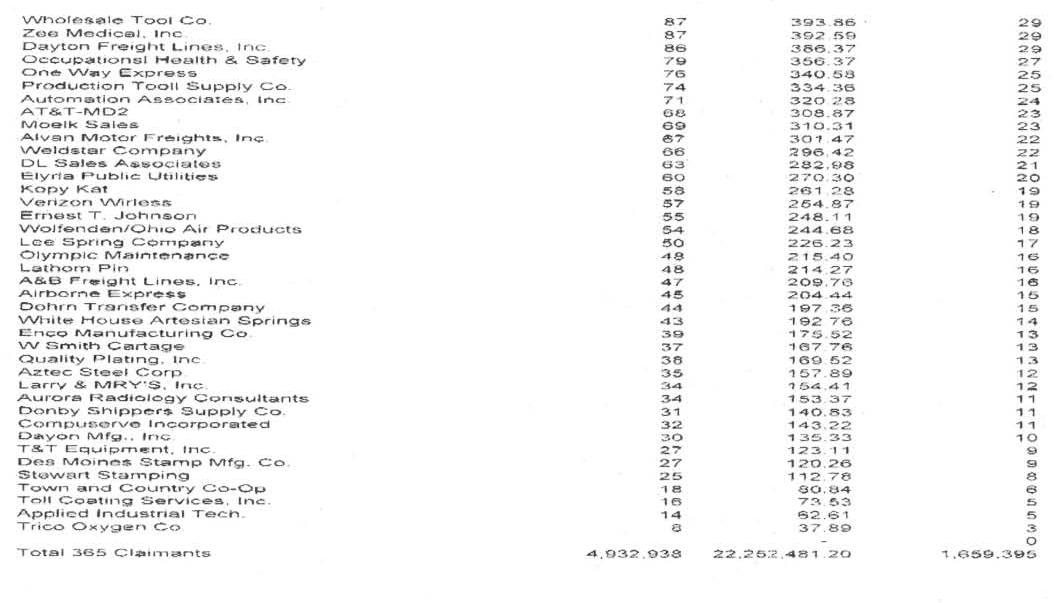

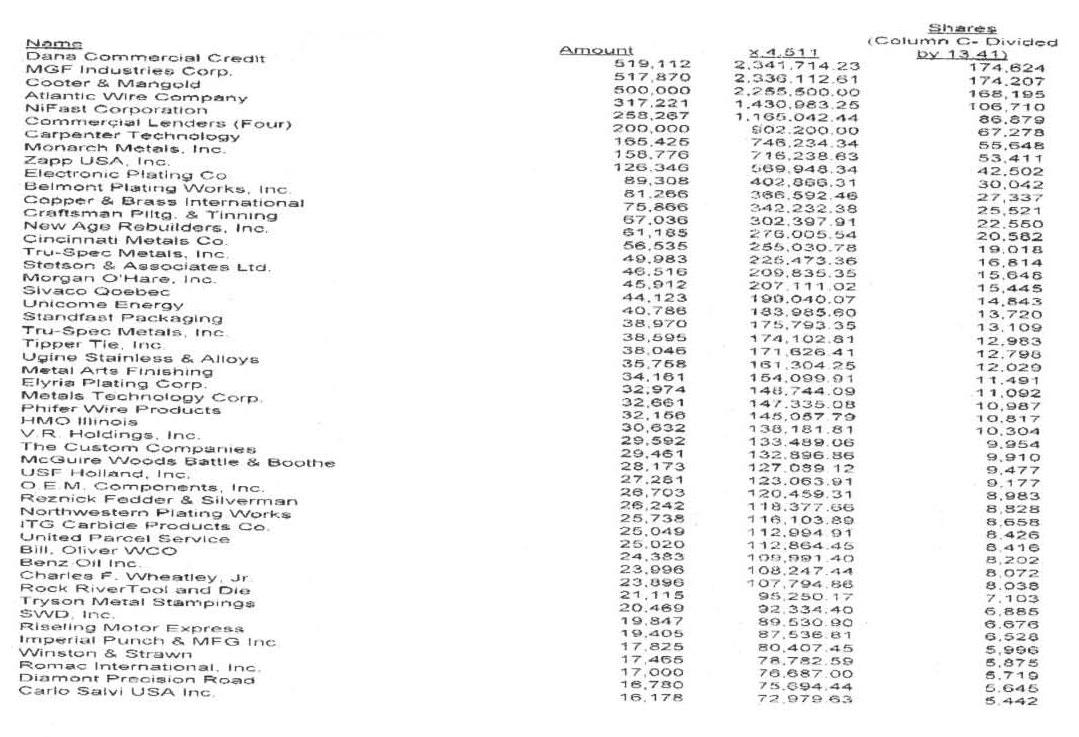

Up to 1,659,395 shares to be offered and issued to the creditors of Valley Rivet Company, Inc., as shown on Schedule B to this prospectus. Valley Rivet Company was previously a subsidiary of VR Holdings.

·

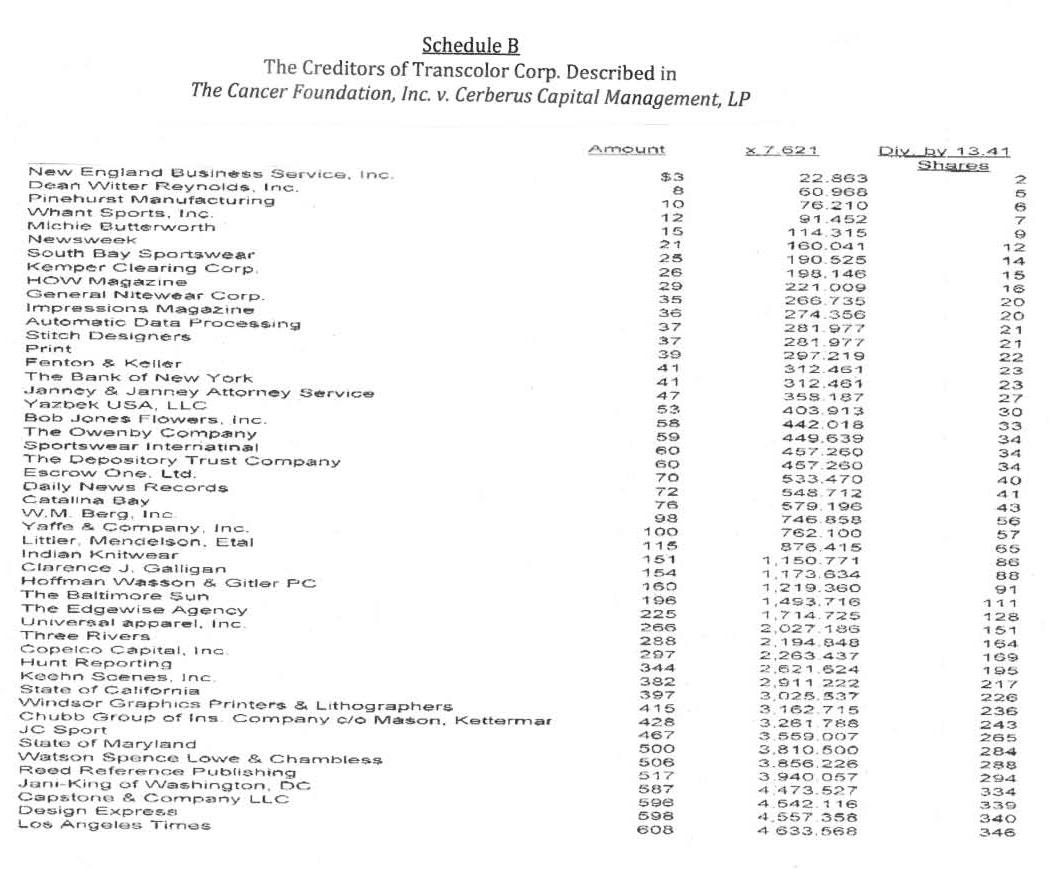

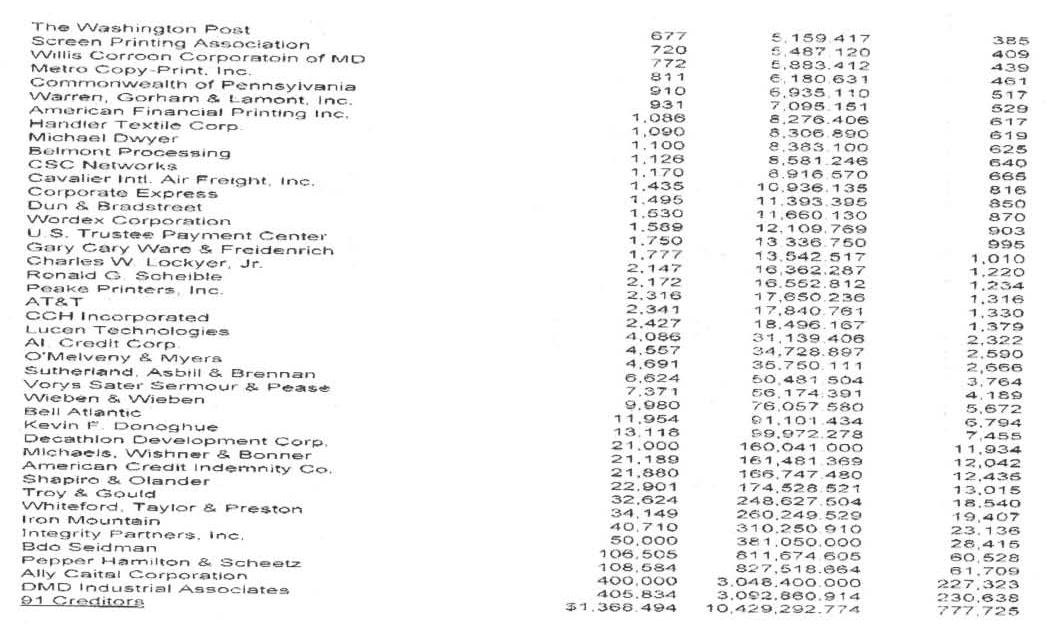

Up to 777,725 shares to be offered and issued to the creditors of Transcolor Corp. described in The Cancer Foundation, Inc. v. Cerberus Capital Management, LP pending in the Circuit Court of Cook County, Illinois under Cause No. 09 L 004607 more fully described in “Business – Legal Proceedings.” The creditors are shown on Schedule B to this prospectus.

·

Up to 735,786 shares to be offered to investors, lenders, and other claimants for funds advanced to Transcolor Corp. and shown on Schedule C to this prospectus.

2

In addition to the up to 5,644,346 shares to the accepting claimants described above, we are also offering for sale to new investors up to 20,000,000 shares of our common stock at a price of $0.10 per share. See “Plan of Distribution.” Further we are registering for resale, 26,000,000 shares of our common stock held by two selling stockholders. See “Selling Stockholders.”

Common stock offered | Up to 51,644,346 shares. |

Common stock to be outstanding | 398,752,689 shares. |

Use of proceeds | We will not receive any proceeds from the issuance of our common stock to the claimants or the sale of shares of the selling stockholders. However, we will receive proceeds fro the sale of our shares to new investors which will be used for the payment of litigation fees and working capital purposes. See “Use of Proceeds” of this prospectus. |

Trading symbol | The shares of our common stock are not currently listed for sale on any exchange. We plan to attempt to have our shares quoted for sale on the “Pink Sheets” or OTC Bulletin Board after the effective date of this prospectus. |

Risk factors | An investment in our common stock involves a high degree of risk. See “Risk Factors” beginning on page 4 of this prospectus. |

3

RISK FACTORS

This investment has a high degree of risk. Before you invest you should carefully consider the risks and uncertainties described below and the other information in this prospectus. If any of the following risks actually occur, our business, operating results and financial condition could be harmed and the value of our stock could go down. This means you could lose all or a part of your investment.

Risks Relating to Our Business

We are a holding company of several affiliated companies, with no operating businesses.

We have no recent operating history upon which you can evaluate our business and prospects. You must consider the risks and uncertainties frequently encountered by companies whose business deals with litigation. If we are unsuccessful in addressing these risks and uncertainties, our business, results of operations and financial condition will be materially and adversely affected.

Our future revenues are unpredictable and our quarterly operating results may fluctuate significantly.

Although we were incorporated in 1998, we have no recent operating history, and have no recent revenue to date. We cannot forecast with any degree of certainty whether any of our proposed litigation services will ever generate revenue or the amount of revenue to be generated. In addition, we cannot predict the consistency of our quarterly operating results. We are currently involved in two lawsuits more fully described in “Business - Legal Proceedings.” If we are successful in the litigation, we plan on utilizing the proceeds to be received to fund our operations. If we are not successful in the litigation, or if we receive only a minimal amount, we will not have sufficient money to fund our proposed operations. In such event, we will have to raise capital either through equity or debt offerings.

Factors which may cause our operating results to fluctuate significantly from quarter to quarter include:

·

Our ability to be successful in litigation in which we might invest;

·

The failure of any of the structured settlements in which we might invest and

·

Unanticipated delays or cost increases.

We might need additional specialized personnel.

Although we are committed to the continued development and growth of our business, the addition of specialized key personnel, such as underwriters and legal personnel, to assess risks of investing in lawsuits and structured settlements, to assist VRH in the execution of our business model is necessary. It is possible that we will not be able to locate and hire such specialized personnel on acceptable terms. We will make every effort to recruit executives with proven experience and expertise as needed to achieve our plan.

We may have difficulty in attracting and retaining management and outside independent members to our board of directors as a result of their concerns relating to their increased personal exposure to lawsuits and stockholder claims by virtue of holding these positions in a publicly held company, if we should become a publicly held company.

We anticipate that our shares of common stock will become publicly traded on either the Pink Sheets or on the Over-the–Counter Bulletin Board (the “OTCBB”) discussed below. The directors and management of publicly traded corporations are increasingly concerned with the extent of their personal exposure to lawsuits and stockholder claims, as well as governmental and creditor claims which may be made against them, particularly in view of recent changes in securities laws imposing additional duties, obligations and liabilities on management and directors. Due to these perceived risks, directors and management are also becoming increasingly concerned with the availability of directors and officers’ liability insurance to pay on a timely basis the costs incurred in defending such claims. We currently do not carry limited directors and officers’ liability insurance. Directors and officers’ liability insurance has recently become much more expensive and difficult to obtain. If we are unable to provide directors and officers’ liability insurance at affordable rates or at all, it may become increasingly more difficult to attract and retain qualified outside directors to serve on our board of directors.

4

Legislative actions and potential new accounting pronouncements are likely to impact our future financial position and results of operations.

We are currently a privately-held company. However, we intend to file a Form 211 promulgated pursuant to the Securities Exchange Act of 1934, as amended (the “Exchange Act”) to allow us to have our shares of common stock to be traded on the OTCBB and the “Pink Sheets.” As of the date of this prospectus, we have not received authorization for the trading of our shares.

The Pink Sheets is an electronic quotation system operated by Pink OTC Markets that displays quotes from broker-dealers for many over-the-counter (OTC) securities. These securities tend to be inactively traded stocks, including penny stocks and those with a narrow geographic interest. Market makers and other brokers can use Pink Quote to publish their bid and ask quotation prices. The term Pink Sheets is also used to refer to a market tier within the current Pink Quote system. The Pink Sheets is not a stock exchange. To be quoted in the Pink Sheets, companies do not need to fulfill any requirements (e.g., filing financial statements with the Securities and Exchange Commission). With the exception of foreign issuers, mostly represented by ADRs, the companies quoted in the Pink Sheets tend to be closely held, extremely small, thinly traded, or bankrupt. Most do not meet the minimum U.S. listing requirements for trading on a stock exchange such as the New York Stock Exchange. Many of these companies do not file periodic reports or audited financial statements with the SEC, making it very difficult for investors to find reliable, unbiased information about those companies. For these reasons, companies listed on Pink Sheets are the most risky investments and potential investors should heavily research the companies in which they plan to invest.

By means of a registration statement included with this prospectus which is filed with the SEC, we will seek to issue shares of our common stock to various creditors of VRH and purchasers of our stock. See “Prospectus Summary – The Offering” and “Plan of Distribution.” Upon the effectiveness of the registration statement, we will be subject to the Exchange Act, and the reporting and regulatory requirements of the Exchange Act, including the Sarbanes-Oxley Act of 2002 and other rule changes as well as proposed legislative initiatives which will increase our general and administrative costs as we will have to incur increased legal and accounting fees to comply with such rule changes.

Further, proposed initiatives are expected to result in changes in certain accounting rules. These and other potential changes could materially increase the expenses we report under accounting principles generally accepted in the United States, and adversely affect our operating results.

Risks Relating to Our Stock

Deoghe Corp. owns approximately 79.8 percent of our common stock. This concentration of ownership could discourage or prevent a potential takeover of VR Holdings that might otherwise result in your receiving a premium over the market price for your common stock.

Deoghe Corp., owned and controlled by the family of Mr. Morton M. Lapides, Sr., owns 314,681,091 shares of our common stock, which represent approximately 79.8 percent of our issued and outstanding common stock as of the date of this prospectus. The result of the ownership of our common stock by Deoghe Corp. is that it has voting control on all matters submitted to our stockholders for approval and is able to control our management and affairs, including extraordinary transactions such as mergers and other changes of corporate control, and going private transactions. Additionally, this concentration of voting power could discourage or prevent a potential takeover of VR Holdings that might otherwise result in your receiving a premium over the market price for your common stock.

5

If we become a publicly traded company, in the event that your shares become free-trading, our common stock will most likely be thinly traded, so you may be unable to sell at or near ask prices or at all if you need to sell your shares to raise money or otherwise desire to liquidate your shares.

If our shares become publicly traded, our common stock will be sporadically or “thinly-traded” on the Pink Sheets, and possibly on the OTCBB, meaning that the number of persons interested in purchasing our common stock at or near ask prices at any given time may be relatively small or nonexistent. This situation will be attributable to a number of factors, including the fact that we are a small company which will be relatively unknown to stock analysts, stock brokers, institutional investors and others in the investment community that generate or influence sales volume, and that even if we came to the attention of such persons, they tend to be risk-averse and would be reluctant to follow an unproven company such as ours or purchase or recommend the purchase of our shares until such time as we became more seasoned and viable.

As a consequence, there may be periods of several days or more when trading activity in our shares is minimal or non-existent, as compared to a mature issuer which has a large and steady volume of trading activity that will generally support continuous sales without an adverse effect on share price. It is possible that a broader or more active public trading market for our common stock will not develop or be sustained, or that trading levels will not continue.

Even if our shares become publicly traded, your shares may not be “free-trading.”

Investors should understand that their shares of our common stock will not become “free-trading” merely because VRH is a publicly-traded company. In order for the shares to become “free-trading,” the shares must be registered, or entitled to an exemption from registration under applicable law. See “Shares Eligible for Future Sale.”

If our shares become publicly traded, the market price for our common stock will most likely be particularly volatile given our status as a relatively unknown company with a small and thinly traded public float, limited operating history and lack of net revenues which could lead to wide fluctuations in our share price. The price at which you purchase our common stock may not be indicative of the price that will prevail in the trading market.

If our shares become publicly traded, the market for our common stock will most likely be characterized by significant price volatility when compared to seasoned issuers, and we expect that our share price will continue to be more volatile than a seasoned issuer for the indefinite future. As a consequence of this lack of liquidity, the trading of relatively small quantities of shares by our stockholders may disproportionately influence the price of those shares in either direction. The price for our shares could, for example, decline precipitously in the event that a large number of shares of our common stock are sold on the market without commensurate demand, as compared to a seasoned issuer which could better absorb those sales without adverse impact on its share price.

Secondly, we will most likely be a speculative or “risky” investment due to our dependence on success of our litigation and the litigation in which we invest. As a consequence of this enhanced risk, more risk-adverse investors may, under the fear of losing all or most of their investment in the event of negative news or lack of progress, be more inclined to sell their shares on the market more quickly and at greater discounts than would be the case with the stock of a seasoned issuer.

6

You may be unable to sell your common stock at or above your purchase price, which may result in substantial losses to you.

If our shares become publicly traded, the following factors may add to the volatility in the price of our common stock: actual or anticipated variations in our quarterly or annual operating results; government regulations, announcements of significant acquisitions, strategic partnerships or joint ventures; our capital commitments; and additions or departures of our key personnel. Many of these factors are beyond our control and may decrease the market price of our common stock, regardless of our operating performance. We cannot make any predictions or projections as to what the prevailing market price for our common stock will be at any time, including as to whether our common stock will sustain the current market price, or as to what effect the sale of shares or the availability of common stock for sale at any time will have on the prevailing market price.

If our shares become publicly traded, volatility in our common stock price may subject VRH to securities inquiries.

If our shares become publicly traded, the market for our common stock will most likely be characterized by significant price volatility when compared to seasoned issuers, and we expect that our share price would be more volatile than a seasoned issuer for the indefinite future. In the past, plaintiffs have often initiated securities class action litigation against a company following periods of volatility in the market price of its securities. We may in the future be the target of similar litigation. Securities litigation could result in substantial costs and liabilities and could divert management’s attention and resources.

We may need to raise additional capital. If we are unable to raise necessary additional capital, our business may fail or our operating results and our stock price may be materially adversely affected.

Because we are a newly operational company, we need to secure adequate funding. We hope to be able to fund our operations in part if our current ligation is successful. See “Business - Legal Proceedings.” If our litigation is not successful, we will need to raise the necessary capital through equity or debt offerings, which may reduce the value of our outstanding securities. We may be unable to secure additional financing on favorable terms or at all.

Selling additional stock, either privately or publicly, would dilute the equity interests of our stockholders. If we borrow more money, we will have to pay interest and may also have to agree to restrictions that limit our operating flexibility. If we are unable to obtain adequate financing, we may have to curtail our litigation and our business would fail.

Our issuance of additional common stock in exchange for services or to repay debt would dilute your proportionate ownership and voting rights and could have a negative impact on the market price of our common stock.

Our board of directors may generally issue shares of common stock to pay for debt or services, without further approval by our stockholders based upon such factors as our board of directors may deem relevant at that time. It is likely that we will issue additional securities to pay for services and reduce debt in the future. It is possible that we will issue additional shares of common stock under circumstances we may deem appropriate at the time.

The elimination of monetary liability against our directors, officers and employees under our certificate of incorporation and the existence of indemnification rights for our directors, officers and employees may result in substantial expenditures by VRH and may discourage lawsuits against our directors, officers and employees.

Our certificate of incorporation contains provisions which eliminate the liability of our directors for monetary damages to VRH and our stockholders. Our bylaws also require us to indemnify our officers and directors. We may also have contractual indemnification obligations under our agreements with our directors, officers and employees. The foregoing indemnification obligations could result in VRH incurring substantial expenditures to cover the cost of settlement or damage awards against directors, officers and employees, which we may be unable to recoup. These provisions and resultant costs may also discourage VRH from bringing a lawsuit against directors, officers and employees for breaches of their fiduciary duties, and may similarly discourage the filing of derivative litigation by our stockholders against our directors, officers and employees even though such actions, if successful, might otherwise benefit VRH and our stockholders.

7

Absence of dividends.

We have never paid or declared any dividends on our common stock. Likewise, we do not anticipate paying, in the near future, dividends or distributions on our common stock or our common stock to be sold in this offering. Any future dividends will be declared at the discretion of our board of directors and will depend, among other things, on our earnings, our financial requirements for future operations and growth, and other facts as we may then deem appropriate.

Our directors have the right to authorize the issuance of additional shares of our common stock.

Our directors, within the limitations and restrictions contained in our certificate of incorporation and without further action by our stockholders, have the authority to issue shares of common stock from time to time. Should we issue additional shares of our common stock at a later time, each investor’s ownership interest in our stock would be proportionally reduced. No investor will have any preemptive right to acquire additional shares of our common stock, or any of our other securities.

If our shares become publicly traded and our shares are traded on the Pink Sheets or OTCBB, and we fail to remain current in our reporting requirements, we could be removed from the OTCBB, which would limit the ability of broker-dealers to sell our securities and the ability of stockholders to sell their securities in the secondary market.

Companies trading on the OTC Bulletin Board and some trading on the Pink Sheets must be reporting issuers under Section 12 of the Exchange Act, and must be current in their reports under Section 13 of the Exchange Act, in order to maintain price quotation privileges on the Pink Sheets and OTC Bulletin Board. If our shares become publicly traded and our shares are traded on the OTC Bulletin Board, and we fail to remain current in our reporting requirements, we could be removed from the OTC Bulletin Board. As a result, the market liquidity for our securities could be adversely affected by limiting the ability of broker-dealers to sell our securities and the ability of stockholders to sell their securities in the secondary market.

If our shares become publicly traded, our common stock will most likely be subject to the “penny stock” rules of the Securities and Exchange Commission, and the trading market in our common stock will be limited, which would make transactions in our stock cumbersome and may reduce the investment value of our stock.

If our shares become publicly traded, our shares of common stock will most likely be “penny stocks” because they most likely will not be registered on a national securities exchange or listed on an automated quotation system sponsored by a registered national securities association, pursuant to Rule 3a51-1(a) under the Exchange Act. For any transaction involving a penny stock, unless exempt, the rules require:

·

That a broker or dealer approve a person’s account for transactions in penny stocks; and

·

That the broker or dealer receives from the investor a written agreement to the transaction, setting forth the identity and quantity of the penny stock to be purchased.

8

The broker or dealer must also deliver, prior to any transaction in a penny stock, a disclosure schedule prescribed by the Securities and Exchange Commission relating to the penny stock market, which, in highlight form:

·

Sets forth the basis on which the broker or dealer made the suitability determination; and

·

That the broker or dealer received a signed, written agreement from the investor prior to the transaction.

Generally, brokers may be less willing to execute transactions in securities subject to the “penny stock” rules. This may make it more difficult for investors to dispose of our common stock and cause a decline in the market value of our stock.

Disclosure also has to be made about the risks of investing in penny stocks in both public offerings and in secondary trading and about the commissions payable to both the broker-dealer and the registered representative, current quotations for the securities and the rights and remedies available to an investor in cases of fraud in penny stock transactions. Finally, monthly statements have to be sent disclosing recent price information for the penny stock held in the account and information on the limited market in penny stocks.

The market for penny stocks has suffered in recent years from patterns of fraud and abuse.

Stockholders should be aware that, according to SEC Release No. 34-29093, the market for penny stocks has suffered in recent years from patterns of fraud and abuse. Such patterns include:

·

Control of the market for the security by one or a few broker-dealers that are often related to the promoter or issuer;

·

Manipulation of prices through prearranged matching of purchases and sales and false and misleading press releases;

·

Boiler room practices involving high-pressure sales tactics and unrealistic price projections by inexperienced salespersons;

·

Excessive and undisclosed bid-ask differential and markups by selling broker-dealers; and

·

The wholesale dumping of the same securities by promoters and broker-dealers after prices have been manipulated to a desired level, along with the resulting inevitable collapse of those prices and with consequential investor losses.

Our management is aware of the abuses that have occurred historically in the penny stock market. Although we do not expect to be in a position to dictate the behavior of the market or of broker-dealers who participate in the market, if our shares become publicly traded, management will strive within the confines of practical limitations to prevent the described patterns from being established with respect to our securities. The occurrence of these patterns or practices could increase the volatility of our share price.

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

In this prospectus, we make a number of statements, referred to as “forward-looking statements” which are intended to convey our expectations or predictions regarding the occurrence of possible future events or the existence of trends and factors that may impact our future plans and operating results. We note, however, that these forward-looking statements are derived, in part, from various assumptions and analyses we have made in the context of our current business plan and information currently available to VRH and in light of our experience and perceptions of historical trends, current conditions and expected future developments and other factors we believe to be appropriate in the circumstances.

9

You can generally identify forward-looking statements through words and phrases such as “seek,” “anticipate,” “believe,” “estimate,” “expect,” “intend,” “plan,” “budget,” “project,” “may be,” “may continue,” “may likely result,” and similar expressions. When reading any forward-looking statement you should remain mindful that all forward-looking statements are inherently uncertain as they are based on current expectations and assumptions concerning future events or future performance of VRH, and that actual results or developments may vary substantially from those expected as expressed in or implied by that statement for a number of reasons or factors, including those relating to:

·

Whether or not markets for our services develop and, if they do develop, the pace at which they develop;

·

Our ability to attract and retain the qualified personnel to implement our growth strategies;

·

Our ability to fund our short-term and long-term financing needs;

·

General economic conditions;

·

Changes in our business plan and corporate strategies; and

·

Other risks and uncertainties discussed in greater detail in the sections of this prospectus, including those captioned “Risk Factors” and “Business.”

Each forward-looking statement should be read in context with, and with an understanding of, the various other disclosures concerning VRH and our business made elsewhere in this prospectus. You should not place undue reliance on any forward-looking statement as a prediction of actual results or developments. We are not obligated to update or revise any forward-looking statement contained in this prospectus to reflect new events or circumstances unless and to the extent required by applicable law.

USE OF PROCEEDS

We will not receive any proceeds from the sale of our common stock offered by this prospectus to the claimants or the selling stockholders. However, we will receive proceeds from the sale of our common stock to the new investors as described in this prospectus. See “Selling Stockholders” and “Plan of Distribution.” The proceeds from the sale of our shares to the new investors pursuant to the registration statement will be used for working capital and general corporate expenses.

We propose to expend these proceeds as follows:

Use of Proceeds | If 100 percent, or 20,000,000 Shares are Sold | If 50 percent, or 10,000,000 Shares are Sold |

Gross proceeds | $2,000,000 | $1,000,000 |

Less offering expenses: | 90,000 | 90,000 |

Miscellaneous expenses | 10,000 | 10,000 |

Net proceeds | $1,900,000 | $ 900,000 |

The net proceeds include working capital needs which are needed to pay our accounts payable and to provide funds for the implementation of our business plan. See “Business.”

10

MARKET PRICE OF AND DIVIDENDS ON OUR

COMMON EQUITY AND RELATED STOCKHOLDER MATTERS

As of the date of this prospectus, the shares of our common stock are not quoted for sale on any public market. We currently have 394,108,343 shares of our common stock issued and outstanding, which are held of record and beneficially owned by 105 persons.

As for our shares which we have agreed to issue to new investors, the claimants, and register for resale by means of this prospectus and our shares which may be sold subject to the provisions of Rule 144 under the Securities Act, please see “Prospectus Summary – The Offering,” “Selling Stockholders,” and “Shares Eligible for Future Sale.”

Dividends

We have not paid or declared any dividends on our common stock, nor do we anticipate paying any cash dividends or other distributions on our common stock in the foreseeable future. Any future dividends will be declared at the discretion of our board of directors and will depend, among other things, on our earnings, if any, our financial requirements for future operations and growth, and other facts as our board of directors may then deem appropriate.

Securities Authorized for Issuance under Equity Compensation Plans

We do not have any equity compensation plans as of the date of this prospectus.

CAPITALIZATION

The following table sets forth our capitalization as of March 31, 2010.

This information should be read in conjunction with our Management’s Discussion and Analysis or Plan of Operation and our consolidated financial statements and the related notes appearing elsewhere in this prospectus.

We had net losses of $136,063 for the year ended September 30, 2009 and $174,712 for the six months ended March 31, 2010 included in the accumulated deficit in the table below.

March 31, 2010 | ||

Actual | As Adjusted (1) | |

Common stock, $0.000001 par value per share; 550,000,000 shares authorized, 394,108,343 and 419,752,689 shares issued and outstanding, as adjusted | $ 394 | $ 420 |

Additional paid-in capital | 8,544,782 | 10,448,450 |

Deficit accumulated during development stage | (777,677) | (781,371) |

Accumulated deficit | (15,492,955) | (15,492,955) |

Total stockholders’ equity (deficit) | (7,725,456) | (5,825,456) |

Total capitalization (deficiency) | (7,725,456) | (5,825,456) |

___________

(1)

Reflects the sale of: (a) up to 5,644,346 shares to up to the claimants, and (b) up to 20,000,000 shares of our common stock at $0.10 per share with offering costs of $100,000. See “Prospectus Summary – The Offering.”

11

SELECTED CONSOLIDATED FINANCIAL DATA

The following consolidated selected financial data are derived from our consolidated financial statements for the years ended September 30, 2009 and 2008, which have been audited by GBH CPAs, PC, independent registered public accounting firm, and the unaudited consolidated financial statements for the six months ended March 31, 2010 and 2009 and are included elsewhere in this prospectus. The data set forth below should be read in conjunction with our Financial Statements and Notes thereto included elsewhere in this prospectus and with “Management’s Discussion and Analysis of Financial Condition and Results of Operation.”

Years Ended September 30, | Six Months Ended March 31, | |||

2009 | 2008 | 2010 | 2009 | |

(Unaudited) | (Unaudited) | |||

Revenue | $ – | $ – | $ – | $ – |

General and administrative expenses | 38,063 | 15,000 | 125,846 | 9,697 |

Interest expense | 98,000 | 98,000 | 48,866 | 48,866 |

Net loss | $ 136,063 | $ 113,000 | $ 174,712 | $ 58,563 |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION

AND RESULTS OF OPERATIONS

The following discussion reflects our plan of operation. This discussion should be read in conjunction with the financial statements which are attached to this prospectus. This discussion contains forward-looking statements, including statements regarding our expected financial position, business and financing plans. These statements involve risks and uncertainties. Our actual results could differ materially from the results described in or implied by these forward-looking statements as a result of various factors, including those discussed below and elsewhere in this prospectus, particularly under the headings “Special Note Regarding Forward-Looking Statements” and “Risk Factors.”

Since the business previously operated by VRH no longer has any relevance, the discussion which follows relates primarily to our proposed business of investing in litigation and arbitration cases, claims and disputes, and the business of buying and securitizing structured settlement lawsuit payments. Therefore, unless the context otherwise suggests, “we,” “our,” “us,” and similar terms, as well as references to “VRH or VR Holdings,” all refer to VRH as of the date of this prospectus. See “Business.”

Seasonality

Our proposed business is not subject to seasonality.

Impact of Inflation

General inflation in the economy has driven the operating expenses of many businesses higher, and, accordingly we have experienced increased salaries and higher prices for supplies, goods and services. We will continuously seek methods of reducing costs and streamlining operations while maximizing efficiency through improved internal operating procedures and controls. While we are subject to inflation as described above, our management believes that inflation currently does not have a material effect on our operating results. However, inflation may become a factor in the future.

Critical Accounting Policies

The preparation of financial statements and related disclosures in conformity with accounting principles generally accepted in the United States requires us to make judgments, assumptions and estimates that affect the amounts reported. Note 1 of Notes to Financial Statements describes the significant accounting policies used in the preparation of the financial statements. Certain of these significant accounting policies are considered to be critical accounting policies, as defined below.

12

A critical accounting policy is defined as one that is both material to the presentation of our financial statements and requires management to make difficult, subjective or complex judgments that could have a material effect on our financial condition or results of operations. Specifically, critical accounting estimates have the following attributes:

·

We are required to make assumptions about matters that are highly uncertain at the time of the estimate; and

·

Different estimates we could reasonably have used, or changes in the estimate that are reasonably likely to occur, would have a material effect on our financial condition or results of operations.

Estimates and assumptions about future events and their effects cannot be determined with certainty. We base our estimates on historical experience and on various other assumptions believed to be applicable and reasonable under the circumstances. These estimates may change as new events occur, as additional information is obtained and as our operating environment changes. These changes have historically been minor and have been included in the consolidated financial statements as soon as they became known. Based on a critical assessment of our accounting policies and the underlying judgments and uncertainties affecting the application of those policies, management believes that our financial statements are fairly stated in accordance with accounting principles generally accepted in the United States, and present a meaningful presentation of our financial condition and results of operations.

In preparing our financial statements to conform to accounting principles generally accepted in the United States, we make estimates and assumptions that affect the amounts reported in our financial statements and accompanying notes. These estimates include useful lives for fixed assets for depreciation calculations and assumptions for valuing options and warrants. Actual results could differ from these estimates.

Results of Operations

Year Ended September 30, 2009 Compared to Year Ended September 30, 2008.

Revenues. We had no revenues for the years ended September 30, 2009 and 2008.

General and Administrative Expenses. Our general and administrative expenses increased from $15,000 in 2008 to $38,063 in 2009. This increase was primarily the result of common shares valued at $17,018 issued to attorneys for services.

Net Loss. Our net loss increased to $136,063 for 2009 from $113,000 for 2008.

Six Months Ended March 31, 2010 Compared to Six Months Ended March 31, 2009.

Revenues. We had no revenues for the six months ended March 31, 2010 and 2009.

General and Administrative Expenses. Our general and administrative expenses increased from $9,697 in 2009 to $125,846 in 2010. This increase was primarily the result of professional fees incurred in connection with the litigation and the registration of our common shares.

Net Loss. Our net loss increased to $174,712 for 2010 from $58,563 for 2009.

Liquidity and Capital Resources

Our primary source of liquidity has been expenses paid by The Cancer Foundation. As of March 31, 2010, we had $0 in cash and cash equivalents.

13

As of March 31, 2010, we had outstanding liabilities of $7,723,456. All of this amount is past due or payable within 12 months. In the event that we are unable to repay all or any portion of these outstanding amounts from cash from operations, we would be required to:

·

Seek one or more extensions for the payment of such amounts;

·

Refinance such debt to the extent available;

·

Raise additional equity capital; or

·

Consummate any combination of the foregoing transactions.

Financing Activities

We plan to fund our proposed operations from the proceeds to be realized from the sale of 20,000,000 shares of our common stock pursuant to a registration statement of which this prospectus is a part. The prospectus seeks to raise up to $2,000,000 in exchange for the sale of our shares of common stock to the public. See “Plan of Distribution.” If we are successful in some or all of our litigation efforts, we expect to receive some additional funds which we will be able to apply to our business operations. If we are unsuccessful in our litigation, we will have to raise additional capital by means of borrowings or the sale of shares of our common stock. At present, we do not have any commitments with respect to future financings. If we are unable to raise the capital we need to finance our business, and our litigation is unsuccessful, our proposed business will likely fail.

At present, we do not have sufficient capital on hand to fund our proposed operations for the next 12 months. Recently, The Cancer Foundation, Inc., a charitable foundation established by the uncle and father of Mr. Morton M. Lapides, Sr., who along with his wife are the controlling stockholders of Deoghe Corp., our majority stockholder, has loaned us money to pay our current operating expenses. However, we cannot continue to rely upon any future funding from The Cancer Foundation, Inc.

Quantitative and Qualitative Disclosures About Market Risk

We conduct all of our transactions in U.S. dollars. We are therefore not directly subject to the risks of foreign currency fluctuations and do not hedge or otherwise deal in currency instruments in an attempt to minimize such risks.

Controls and Procedures

The term disclosure controls and procedures means controls and other procedures of an issuer that are designed to ensure that information required to be disclosed by the issuer in the reports that it files or submits under the Exchange Act (15 U.S.C. 78a, et seq.) is recorded, processed, summarized and reported, within the time periods specified in the Commission’s rules and forms. Disclosure controls and procedures include, without limitation, controls and procedures designed to ensure that information required to be disclosed by an issuer in the reports that it files or submits under the Exchange Act is accumulated and communicated to the issuer’s management, including its principal executive and principal financial officers, or persons performing similar functions, as appropriate to allow timely decisions regarding required disclosure.

The term internal control over financial reporting is defined as a process designed by, or under the supervision of, the issuer’s principal executive and principal financial officers, or persons performing similar functions, and effected by the issuer’s board of directors, management and other personnel, to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles and includes those policies and procedures that:

14

·

Pertain to the maintenance of records that in reasonable detail accurately and fairly reflect the transactions and dispositions of the assets of the issuer;

·

Provide reasonable assurance that transactions are recorded as necessary to permit preparation of financial statements in accordance with generally accepted accounting principles, and that receipts and expenditures of the issuer are being made only in accordance with authorizations of management and directors of the issuer; and

·

Provide reasonable assurance regarding prevention or timely detection of unauthorized acquisition, use or disposition of the issuer’s assets that could have a material effect on the financial statements.

Our management, including our chief executive officer and chief financial officer, does not expect that our disclosure controls and procedures or our internal controls over financial reporting will prevent all error and all fraud. A control system, no matter how well conceived and operated, can provide only reasonable, not absolute, assurance that the objectives of the control system are met. Further, the design of a control system must reflect the fact that there are resource constraints, and the benefits of controls must be considered relative to their costs. Because of inherent limitations in all control systems, internal control over financial reporting may not prevent or detect misstatements, and no evaluation of controls can provide absolute assurance that all control issues and instances of fraud, if any, within VRH have been detected. Also, projections of any evaluation of effectiveness to future periods are subject to the risk that controls may become inadequate because of changes in conditions, or that the degree of compliance with the policies or procedures may deteriorate.

Evaluation of Disclosure and Controls and Procedures. Our management is responsible for establishing and maintaining adequate internal control over financial reporting as defined in Rule 13a-15(f) under the Exchange Act. Our internal control over financial reporting is a process designed to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with accounting principles generally accepted in the United States. We carried out an evaluation, under the supervision and with the participation of our management, including our chief executive officer and chief financial officer, of the effectiveness of the design and operation of our disclosure controls and procedures as of the end of the period covered by this prospectus. The evaluation was undertaken in consultation with our accounting personnel. Based on that evaluation, our chief executive officer and chief financial officer concluded that our disclosure controls and procedures are currently effective to ensure that information required to be disclosed by us in the reports that we file or submit under the Exchange Act is recorded, processed, summarized and reported within the time periods specified in the SEC’s rules and forms. As we develop new business or if we engage in an extraordinary transaction, we will review our disclosure controls and procedures and make sure that they remain adequate.

Changes in Internal Controls over Financial Reporting. There were no changes in the internal controls over our financial reporting that occurred during the period covered by this prospectus that have materially affected, or are reasonably likely to materially affect, our internal control over financial reporting.

This prospectus does not include an attestation report of our independent registered public accounting firm regarding internal control over financial reporting. Management’s report was not subject to attestation by our independent registered public accounting firm pursuant to temporary rules of the Securities and Exchange Commission that permit us to provide only management’s report in this prospectus.

Stock-Based Compensation

We recognize compensation cost for stock-based awards based on the estimated fair value of the award on date of grant. We measure compensation cost at the grant date based on the fair value of the award and recognize compensation cost upon the probable attainment of a specified performance condition or over a service period.

15

Recently Issued Accounting Pronouncements

In May 2009, the FASB issued SFAS No. 165, Subsequent Events (“SFAS 165” or ASC 855). SFAS 165 (ASC 855) establishes general standards of accounting for and disclosure of events that occur after the balance sheet date but before financial statements are issued or are available to be issued. SFAS 165 (ASC 855) sets forth (1) The period after the balance sheet date during which management of a reporting entity should evaluate events or transactions that may occur for potential recognition or disclosure in the financial statements, (2) The circumstances under which an entity should recognize events or transactions occurring after the balance sheet date in its financial statements and (3) The disclosures that an entity should make about events or transactions that occurred after the balance sheet date. SFAS 165 (ASC 855) was effective for interim or annual financial periods ending after June 15, 2009.

In June 2009, the FASB issued SFAS No. 168, The FASB Accounting Standards Codification and the Hierarchy of Generally Accepted Accounting Principles—a replacement of FASB Statement No. 162 (“SFAS 168” or ASC 105-10). The FASB Accounting Standards Codification (“Codification”) will be the single source of authoritative nongovernmental U.S. generally accepted accounting principles. Rules and interpretive releases of the SEC under authority of federal securities laws are also sources of authoritative GAAP for SEC registrants. SFAS 168 (ASC 105-10) was effective for interim and annual periods ending after September 15, 2009. All existing accounting standards are superseded as described in SFAS 168. All other accounting literature not included in the Codification is non-authoritative. The Codification did not have a significant impact on our financial statements.

Off-Balance Sheet Arrangements

We do not have any off-balance sheet arrangements.

BUSINESS

Company Overview

VR Holdings, Inc., a Delaware corporation, was incorporated in 1998 to be the parent company of a group of entities owned by MML, Inc. which was in turn controlled by Morton M. Lapides, Sr. and his family. The companies included in this consolidation were MML, Inc., Transcolor Corp., Valley Rivet Company, Alleco, Inc. and Allegheny Pepsi Cola Bottling Company. VR Holdings, Inc. itself has never had any operations or employees but acted as a holding company only.

During the period from 2003 to 2006, through an investigation instituted by The Cancer Foundation, Inc., a charitable foundation established by the uncle and father of Mr. Morton M. Lapides, Sr., who along with his wife are the controlling stockholders of Deoghe Corp., our majority stockholder, it was determined by Mr. Lapides and others that certain lenders, through alleged illegal practices, had taken advantage of Mr. Lapides and other stockholders of VR Holdings to gain control of a certain operating subsidiary while Mr. Lapides was undergoing treatment for life threatening pancreatic cancer. These alleged illegal practices resulted in VR Holdings losing control of various operating subsidiaries and allegedly ultimately causing VR Holdings to lose an estimated $1.6 billion associated with these operations. As a result, it was decided by the stockholders of VR Holdings to reorganize the ownership of the company and to file a law suit against the lenders and related parties to recover the damages caused by the lender’s alleged illegal activities.

16

Our business going forward is expected to consist of two strategies:

·

Build a diversified portfolio of investments in various legal claims and to provide our stockholders with an attractive level of capital growth through investing directly and indirectly in litigation and arbitration cases, claims and disputes. See “Business - Financing Litigation.”

·

The business of buying and securitizing structured settlement lawsuit payments. See “Business – Structured Settlements.”

Financing Litigation

One of the objectives of VRH is to build a diversified portfolio of investments in claims and to provide our stockholders with an attractive level of capital growth through investing directly and indirectly in litigation and arbitration cases, claims and disputes. It is expected that these investments will initially be made predominantly in the United States and in international arbitration cases although, in the medium term, VRH would expect to make investments outside of the United States in jurisdictions where such investments are lawful and permitted under local law and rules on professional ethics.

VRH intends to invest approximately 50 percent of our available funds through loans to law firms to finance legal fees and costs in connection with active participation in claims (through co-counsel agreements with other lawyers).

Investments by way of loans to law firms will be made when:

·

A direct investment by VRH is not possible or preferred because (for example) it is not permitted for legal or ethical reasons; and

·

In instances where it is not practicable to get all plaintiffs individually to agree to a direct investment.

The ultimate goal of VRH is to be a leading source of value-added and direct financing for large claims in complex litigation and arbitration worldwide where such financing is considered to be lawful and permitted under local law and rules on professional ethics.

The U.S. Market

We believe that statistics on the litigation marketplace in the U.S. are scarce, except with relation to the insurance industry and the related area of tort claims. According to the U.S. Bureau of Economic Analysis (BEA), over $180 billion was spent in 2005 on ‘‘legal services’’ in the United States. A 2002 White House Council of Economic Advisers report estimated that the cost of legal fees and penalties as a percentage of U.S. GDP was more than double that in other industrialized countries. The White House Council of Economic Advisors report also indicated that, in 2000, approximately $30 billion was spent on plaintiff’s lawyers to prosecute tort claims and that over $75 billion was paid in damages to tort claimants.

Historically, legal and ethical concerns about third parties profiting from investments in litigation have restricted the growth of litigation financing. However, there has been a recent trend towards eliminating or relaxing such barriers. We consider that the ability of a plaintiff to fund part of its case in cash and part on a contingent fee basis may act as an incentive for plaintiffs to generate cash for a portion of their interest in a claim, which allows them to negotiate a lower contingent fee percentage with their lawyers.

Contingent fees are commonplace in U.S. court proceedings (with the law firms being remunerated by reference to a percentage of the proceeds of the litigation or arbitration) and are specifically allowed by statute in a number of U.S. states. Commonly, U.S. lawyers’ contingent fees range between 25 percent and 33 percent of the plaintiff’s total recovery in a case undertaken on a ‘‘no win, no fee’’ basis.

17

Markets Outside the U.S.

Australia provides a market suitable for investment by VRH. Several companies have emerged in the Australian litigation financing field. The shares of at least one law firm and one litigation financing company in Australia are now listed on the Australian Stock Exchange.

In the United Kingdom, litigation or claims financing companies exist and are making investments in U.K. litigation (although funding is currently limited to after-the-event insurance and flexible fee arrangements). One recent example involves a major U.K. law firm securing one of the largest third party findings in litigation against an accounting firm. However, there are currently significant legal restrictions on the type of investments in litigation that can be made in the U.K. The U.K. Legal Services Act 2007 received Royal Assent on October 30, 2007. This legislation allows outside investment in law firms, which we believe will lead to additional opportunities to finance claims, although it is not certain when the relevant provisions will be implemented. Current consultation material suggests that outside investment in U.K. law firms will not be possible until 2011 or 2012.

Other opportunities for investment by VRH are not connected to any particular jurisdiction. For example, we intend to examine investments in arbitrations that are pending in various arbitration forums in Europe and elsewhere under the auspices of international organizations, such as the London Court of International Arbitration and the International Chamber of Commerce.

Competition

A number of U.S. companies already exist which purchase claims directly from individual plaintiffs in the U.S. or provide loans to law firms secured by an interest in the law firm’s portfolio of contingent fee cases or interests in a particular case. At the present time, there are over 30 businesses advertising their services in the litigation financing business in the U.S., Australia, the U.K. and Germany. We believe that a growing number of U.S. companies have targeted investments in intellectual property claims and cases. We anticipate that the introduction of the U.K. Legal Services Act 2007 may lead to the development of a significant number of competitors in the litigation finance industry in the U.K. although it is uncertain when the relevant provisions will be implemented (current consultation material suggests that outside investment in U.K. law firms will not be possible until 2011 or 2012, as discussed above).

Investment Objective and Policy

VRH intends to invest in a wide variety of arbitration and litigation claims. Initially, these investments are expected to be made predominantly in the U.S. and in international arbitration cases. The investment objective of VRH is to build a diversified portfolio of investments in claims and to provide our stockholders with an attractive level of capital growth through investing directly and indirectly in litigation and arbitration cases, claims and disputes.

VRH will seek to meet its investment and yield objectives through investing in large claims, typically where the total recoveries sought exceed $2,000,000. Except where specifically approved by our board of directors, no single investment of VRH will exceed $1,000,000. We anticipate that we will consider or examine several investment opportunities for every investment that is actually funded.

Investment opportunities will be selected using underwriting criteria set out below. We will seek to achieve diversification of investments by industry, jurisdiction, claim size and expected time-to-return, although most investments will be long-term with an expected return within two to five years of investment.

Investments will be structured as loans when a direct investment by VRH is not possible because (for example) it is not clearly permitted for legal or ethical reasons, in instances where it is not practicable to get all plaintiffs individually to agree to a direct investment.

18

In the medium term, VRH intends to make direct and indirect investments outside the United States, where we have received a reasoned, written legal opinion that such investments are considered to be lawful and permitted under local laws and/or rules on professional ethics. As at the date hereof, VRH has not made (nor entered into any commitment to make) any direct or indirect investments.

Direct Investments

VRH intends to make direct investment in a variety of different claims, including but not limited to the following:

·

Property damage, defaulted debt, breach of contract, insurance, antitrust, indemnification, subrogation, environmental liability, securities, expropriation and government taking, unregistered intellectual property and other business claims (‘‘Business Claims’’);

·

Claims and interests involving registered intellectual property (copyright, trademark and patent) (‘‘Registered Intellectual Property Claims’’); and

·

Claims in foreign (non-U.S.) litigation and in arbitration matters.

VRH will use a variety of structures to make direct investments in litigation and arbitration claims. These structures will be carefully customized by us for each case opportunity in order to seek compliance with legal requirements and local rules on professional ethics as well as seeking to ensure the enforceability of VRH’s direct investment contracts and collectability of the relevant share of the recoveries.

It is anticipated that typically VRH will pay money to the plaintiff(s) themselves, in connection with the purchase of a percentage of the case recovery. In some instances, the terms of the investment will require some or all of the claim purchase monies to be paid to the prosecuting lawyer to finance the case.

Loans to Law Firms