Attached files

| file | filename |

|---|---|

| EX-32 - NELNET INC | ex32.htm |

| EX-10.3 - NELNET INC | ex10-3.htm |

| EX-31.1 - NELNET INC | ex31-1.htm |

| EX-10.1 - NELNET INC | ex10-1.htm |

| EX-31.2 - NELNET INC | ex31-2.htm |

| EX-10.4 - NELNET INC | ex10-4.htm |

| EX-10.2 - NELNET INC | ex10-2.htm |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

(Mark One)

|

x

|

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the quarterly period ended March 31, 2010

or

|

¨

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

|

For the transition period from to .

COMMISSION FILE NUMBER 001-31924

NELNET, INC.

(Exact name of registrant as specified in its charter)

|

NEBRASKA

(State or other jurisdiction of incorporation or organization)

|

84-0748903

(I.R.S. Employer Identification No.)

|

|

121 SOUTH 13TH STREET, SUITE 201

LINCOLN, NEBRASKA

(Address of principal executive offices)

|

68508

(Zip Code)

|

(402) 458-2370

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [ ] No [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer [ ] Accelerated filer [X]

Non-accelerated filer [ ] Smaller reporting company [ ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes [ ] No [X]

As of April 30, 2010, there were 38,589,242 and 11,495,377 shares of Class A Common Stock and Class B Common Stock, par value $0.01 per share, outstanding, respectively (excluding 11,317,364 shares of Class A Common Stock held by wholly owned subsidiaries).

NELNET, INC.

FORM 10-Q

INDEX

March 31, 2010

|

PART I. FINANCIAL INFORMATION

|

||||||||||

|

Item 1.

|

Financial Statements

|

2

|

||||||||

|

Item 2.

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations

|

25

|

||||||||

|

Item 3.

|

Quantitative and Qualitative Disclosures about Market Risk

|

62

|

||||||||

|

Item 4.

|

Controls and Procedures

|

67

|

||||||||

|

PART II. OTHER INFORMATION

|

||||||||||

|

Item 1.

|

Legal Proceedings

|

67

|

||||||||

|

Item 1A.

|

Risk Factors

|

69

|

||||||||

|

Item 2.

|

Unregistered Sales of Equity Securities and Use of Proceeds

|

69

|

||||||||

|

Item 6.

|

Exhibits

|

71

|

||||||||

|

Signatures

|

72

|

|||||||||

1

PART I. FINANCIAL INFORMATION

ITEM 1. FINANCIAL STATEMENTS

|

NELNET, INC. AND SUBSIDIARIES

|

||||||||

|

CONSOLIDATED BALANCE SHEETS

|

||||||||

|

(Dollars in thousands, except share data)

|

||||||||

|

As of

|

As of

|

|||||||

|

March 31,

2010

|

December 31,

2009

|

|||||||

|

(unaudited)

|

||||||||

|

Assets:

|

||||||||

|

Student loans receivable (net of allowance for loan losses of

|

||||||||

|

$49,400 and $50,887 respectively)

|

$ | 24,835,493 | 23,926,957 | |||||

|

Cash and cash equivalents:

|

||||||||

|

Cash and cash equivalents - not held at a related party

|

34,107 | 12,301 | ||||||

|

Cash and cash equivalents - held at a related party

|

295,972 | 325,880 | ||||||

|

Total cash and cash equivalents

|

330,079 | 338,181 | ||||||

|

Restricted cash and investments

|

727,858 | 625,492 | ||||||

|

Restricted cash - due to customers

|

39,199 | 91,741 | ||||||

|

Accrued interest receivable

|

336,242 | 329,313 | ||||||

|

Accounts receivable (net of allowance for doubtful accounts of

|

||||||||

|

$1,125 and $1,198, respectively)

|

60,704 | 42,043 | ||||||

|

Goodwill

|

143,717 | 143,717 | ||||||

|

Intangible assets, net

|

54,940 | 53,538 | ||||||

|

Property and equipment, net

|

27,649 | 26,606 | ||||||

|

Other assets

|

157,005 | 104,940 | ||||||

|

Fair value of derivative instruments

|

129,059 | 193,899 | ||||||

|

Total assets

|

$ | 26,841,945 | 25,876,427 | |||||

|

Liabilities:

|

||||||||

|

Bonds and notes payable

|

$ | 25,756,182 | 24,805,289 | |||||

|

Accrued interest payable

|

16,814 | 19,831 | ||||||

|

Other liabilities

|

184,463 | 172,514 | ||||||

|

Due to customers

|

39,199 | 91,741 | ||||||

|

Fair value of derivative instruments

|

6,074 | 2,489 | ||||||

|

Total liabilities

|

26,002,732 | 25,091,864 | ||||||

|

Shareholders' equity:

|

||||||||

|

Preferred stock, $0.01 par value. Authorized 50,000,000 shares;

|

||||||||

|

no shares issued or outstanding

|

— | — | ||||||

|

Common stock:

|

||||||||

|

Class A, $0.01 par value. Authorized 600,000,000 shares;

|

||||||||

|

issued and outstanding 38,587,293 shares as of March 31,

|

||||||||

|

2010 and 38,396,791 shares as of December 31, 2009

|

386 | 384 | ||||||

|

Class B, convertible, $0.01 par value. Authorized 60,000,000 shares;

|

||||||||

|

issued and outstanding 11,495,377 shares as of March 31,

|

||||||||

|

2010 and December 31, 2009

|

115 | 115 | ||||||

|

Additional paid-in capital

|

112,980 | 109,359 | ||||||

|

Retained earnings

|

726,982 | 676,154 | ||||||

|

Employee notes receivable

|

(1,250 | ) | (1,449 | ) | ||||

|

Total shareholders' equity

|

839,213 | 784,563 | ||||||

|

Commitments and contingencies

|

||||||||

|

Total liabilities and shareholders' equity

|

$ | 26,841,945 | 25,876,427 | |||||

See accompanying notes to consolidated financial statements.

2

|

NELNET, INC. AND SUBSIDIARIES

|

||||||||

|

CONSOLIDATED STATEMENTS OF INCOME

|

||||||||

|

(Dollars in thousands, except share data)

|

||||||||

|

(unaudited)

|

||||||||

|

Three months

|

||||||||

|

ended March 31,

|

||||||||

|

2010

|

2009

|

|||||||

|

Interest income:

|

||||||||

|

Loan interest

|

$ | 134,967 | 170,919 | |||||

|

Investment interest

|

1,001 | 4,091 | ||||||

|

Total interest income

|

135,968 | 175,010 | ||||||

|

Interest expense:

|

||||||||

|

Interest on bonds and notes payable

|

50,859 | 146,502 | ||||||

|

Net interest income

|

85,109 | 28,508 | ||||||

|

Less provision for loan losses

|

5,000 | 7,500 | ||||||

|

Net interest income after provision for loan losses

|

80,109 | 21,008 | ||||||

|

Other income (expense):

|

||||||||

|

Loan and guaranty servicing revenue

|

36,394 | 26,471 | ||||||

|

Tuition payment processing and campus commerce revenue

|

17,382 | 15,538 | ||||||

|

Enrollment services revenue

|

33,271 | 28,771 | ||||||

|

Software services revenue

|

4,344 | 5,705 | ||||||

|

Other income

|

7,260 | 8,787 | ||||||

|

Gain on sale of loans and debt repurchases, net

|

10,177 | 7,869 | ||||||

|

Derivative market value and foreign currency

|

||||||||

|

adjustments and derivative settlements, net

|

1,682 | 19,478 | ||||||

|

Total other income

|

110,510 | 112,619 | ||||||

|

Operating expenses:

|

||||||||

|

Salaries and benefits

|

41,641 | 38,226 | ||||||

|

Other operating expenses:

|

||||||||

|

Cost to provide enrollment services

|

22,025 | 17,793 | ||||||

|

Professional and other services

|

11,241 | 6,077 | ||||||

|

Depreciation and amortization

|

8,491 | 10,083 | ||||||

|

Occupancy and communications

|

3,588 | 5,354 | ||||||

|

Advertising and marketing

|

3,459 | 1,710 | ||||||

|

Postage and distribution

|

2,869 | 2,656 | ||||||

|

Trustee and other debt related fees

|

1,202 | 2,868 | ||||||

|

Other

|

9,188 | 7,804 | ||||||

|

Total other operating expenses

|

62,063 | 54,345 | ||||||

|

Total operating expenses

|

103,704 | 92,571 | ||||||

|

Income before income taxes

|

86,915 | 41,056 | ||||||

|

Income tax expense

|

(32,593 | ) | (15,601 | ) | ||||

|

Net income

|

$ | 54,322 | 25,455 | |||||

|

Earnings per common share:

|

||||||||

|

Net earnings - basic

|

$ | 1.09 | 0.51 | |||||

|

Net earnings - diluted

|

1.08 | 0.51 | ||||||

|

Dividends paid per common share

|

$ | 0.07 | — | |||||

|

Weighted average common shares outstanding:

|

||||||||

|

Basic

|

49,716,696 | 49,142,324 | ||||||

|

Diluted

|

49,912,589 | 49,334,981 | ||||||

See accompanying notes to consolidated financial statements.

3

|

NELNET, INC. AND SUBSIDIARIES

|

|||||||||||||||||||||||||||||||||||||||

|

CONSOLIDATED STATEMENTS OF SHAREHOLDERS' EQUITY AND COMPREHENSIVE INCOME

|

|||||||||||||||||||||||||||||||||||||||

|

(Dollars in thousands, except share data)

|

|||||||||||||||||||||||||||||||||||||||

|

(unaudited)

|

|||||||||||||||||||||||||||||||||||||||

|

Preferred

|

Class A

|

Class B

|

Additional

|

Employee

|

Total

|

||||||||||||||||||||||||||||||||||

|

stock

|

Common stock shares

|

Preferred

|

common

|

common

|

paid-in

|

Retained

|

notes

|

shareholders’

|

|||||||||||||||||||||||||||||||

|

shares

|

Class A

|

Class B

|

stock

|

stock

|

stock

|

capital

|

earnings

|

receivable

|

equity

|

||||||||||||||||||||||||||||||

|

Balance as of December 31, 2008

|

— | 37,794,067 | 11,495,377 | $ | — | 378 | 115 | 103,762 | 540,521 | (1,550 | ) | 643,226 | |||||||||||||||||||||||||||

|

Comprehensive income:

|

|||||||||||||||||||||||||||||||||||||||

|

Net income

|

— | — | — | — | — | — | — | 25,455 | — | 25,455 | |||||||||||||||||||||||||||||

|

Issuance of common stock, net of forfeitures

|

— | 486,583 | — | — | 5 | — | 2,345 | — | — | 2,350 | |||||||||||||||||||||||||||||

|

Compensation expense for stock based awards

|

— | — | — | — | — | — | 607 | — | — | 607 | |||||||||||||||||||||||||||||

|

Repurchase of common stock

|

— | (3,780 | ) | — | — | — | — | (36 | ) | — | — | (36 | ) | ||||||||||||||||||||||||||

|

Balance as of March 31, 2009

|

— | 38,276,870 | 11,495,377 | $ | — | 383 | 115 | 106,678 | 565,976 | (1,550 | ) | 671,602 | |||||||||||||||||||||||||||

|

Balance as of December 31, 2009

|

— | 38,396,791 | 11,495,377 | $ | — | 384 | 115 | 109,359 | 676,154 | (1,449 | ) | 784,563 | |||||||||||||||||||||||||||

|

Comprehensive income:

|

|||||||||||||||||||||||||||||||||||||||

|

Net income

|

— | — | — | — | — | — | — | 54,322 | — | 54,322 | |||||||||||||||||||||||||||||

|

Cash dividend on Class A and Class B

|

|||||||||||||||||||||||||||||||||||||||

|

common stock - $0.07 per share

|

— | — | — | — | — | — | — | (3,494 | ) | — | (3,494 | ) | |||||||||||||||||||||||||||

|

Issuance of common stock, net of forfeitures

|

— | 203,438 | — | — | 2 | — | 3,532 | — | — | 3,534 | |||||||||||||||||||||||||||||

|

Compensation expense for stock based awards

|

— | — | — | — | — | — | 325 | — | — | 325 | |||||||||||||||||||||||||||||

|

Repurchase of common stock

|

— | (12,936 | ) | — | — | — | — | (236 | ) | — | — | (236 | ) | ||||||||||||||||||||||||||

|

Reduction of employee notes receivable

|

— | — | — | — | — | — | — | — | 199 | 199 | |||||||||||||||||||||||||||||

|

Balance as of March 31, 2010

|

— | 38,587,293 | 11,495,377 | $ | — | 386 | 115 | 112,980 | 726,982 | (1,250 | ) | 839,213 | |||||||||||||||||||||||||||

See accompanying notes to consolidated financial statements.

4

|

NELNET, INC. AND SUBSIDIARIES

|

||||||||

|

CONSOLIDATED STATEMENTS OF CASH FLOWS

|

||||||||

|

(Dollars in thousands)

|

||||||||

|

(unaudited)

|

||||||||

|

Three months ended March 31,

|

||||||||

|

2010

|

2009

|

|||||||

|

Net income

|

$ | 54,322 | 25,455 | |||||

|

Adjustments to reconcile income to net cash provided by operating activities, net of business acquisition:

|

||||||||

|

Depreciation and amortization, including loan premiums and deferred origination costs

|

26,864 | 30,134 | ||||||

|

Provision for loan losses

|

5,000 | 7,500 | ||||||

|

Derivative market value adjustment

|

67,570 | 52,122 | ||||||

|

Foreign currency transaction adjustment

|

(71,675 | ) | (47,242 | ) | ||||

|

Proceeds to terminate and/or amend derivative instruments

|

855 | 50 | ||||||

|

Payments to terminate and/or amend derivative instruments

|

— | (11,760 | ) | |||||

|

Gain from repurchase of bonds and notes payable

|

(10,177 | ) | (8,075 | ) | ||||

|

Loss on sale of loans, net

|

— | 206 | ||||||

|

Deferred income tax expense

|

7,509 | 1,323 | ||||||

|

Non-cash compensation expense

|

523 | 723 | ||||||

|

Other non-cash items

|

254 | 301 | ||||||

|

(Increase) decrease in accrued interest receivable

|

(6,929 | ) | 83,563 | |||||

|

Increase in accounts receivable

|

(18,661 | ) | (487 | ) | ||||

|

(Increase) decrease in other assets

|

(51,071 | ) | 7,236 | |||||

|

Decrease in accrued interest payable

|

(3,017 | ) | (33,500 | ) | ||||

|

Increase in other liabilities

|

1,319 | 2,817 | ||||||

|

Net cash provided by operating activities

|

2,686 | 110,366 | ||||||

|

Cash flows from investing activities, net of business acquisition:

|

||||||||

|

Originations and purchases of student loans, including loan premiums and deferred origination costs

|

(1,027,883 | ) | (972,450 | ) | ||||

|

Purchases of student loans, including loan premiums, from a related party

|

(535,907 | ) | (13,803 | ) | ||||

|

Net proceeds from student loan repayments, claims, capitalized interest, participations, and other

|

615,431 | 734,445 | ||||||

|

Proceeds from sale of student loans

|

20,032 | 125 | ||||||

|

Proceeds from sale of student loans to a related party

|

— | 20,016 | ||||||

|

Purchases of property and equipment, net

|

(2,883 | ) | (62 | ) | ||||

|

Increase in restricted cash and investments, net

|

(102,366 | ) | (221,240 | ) | ||||

|

Business acquisition, net of cash acquired

|

(3,000 | ) | — | |||||

|

Net cash used in investing activities

|

(1,036,576 | ) | (452,969 | ) | ||||

|

Cash flows from financing activities:

|

||||||||

|

Payments on bonds and notes payable

|

(1,028,622 | ) | (642,115 | ) | ||||

|

Proceeds from issuance of bonds and notes payable

|

2,061,893 | 1,039,942 | ||||||

|

Payments of debt issuance costs

|

(4,069 | ) | (1,448 | ) | ||||

|

Dividends paid

|

(3,494 | ) | — | |||||

|

Proceeds from issuance of common stock

|

117 | 118 | ||||||

|

Repurchases of common stock

|

(236 | ) | (36 | ) | ||||

|

Payments received on employee stock notes receivable

|

199 | — | ||||||

|

Net cash provided by financing activities

|

1,025,788 | 396,461 | ||||||

|

Net (decrease) increase in cash and cash equivalents

|

(8,102 | ) | 53,858 | |||||

|

Cash and cash equivalents, beginning of period

|

338,181 | 189,847 | ||||||

|

Cash and cash equivalents, end of period

|

$ | 330,079 | 243,705 | |||||

|

Supplemental disclosures of cash flow information:

|

||||||||

|

Interest paid

|

$ | 49,777 | 177,210 | |||||

|

Income taxes paid, net of refunds

|

$ | 25,123 | 8,096 | |||||

See accompanying notes to consolidated financial statements.

5

NELNET, INC. AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(Information as of March 31, 2010 and for the three months ended

March 31, 2010 and 2009 is unaudited)

(Dollars in thousands, except per share amounts, unless otherwise noted)

1. Basis of Financial Reporting

The accompanying unaudited consolidated financial statements of Nelnet, Inc. and subsidiaries (the “Company”) as of March 31, 2010 and for the three months ended March 31, 2010 and 2009 have been prepared on the same basis as the audited consolidated financial statements for the year ended December 31, 2009 and, in the opinion of the Company’s management, the unaudited consolidated financial statements reflect all adjustments, consisting of normal recurring adjustments, necessary for a fair presentation of results of operations for the interim periods presented. The preparation of financial statements in conformity with U.S. generally accepted accounting principles requires management to make estimates and assumptions that affect the amounts reported in the consolidated financial statements and accompanying notes. Actual results could differ from those estimates. Operating results for the three months ended March 31, 2010 are not necessarily indicative of the results for the year ending December 31, 2010. The unaudited consolidated financial statements should be read in conjunction with the Company’s Annual Report on Form 10-K for the year ended December 31, 2009. Management has evaluated subsequent events, and the impact on the reported results and disclosures through the date these financial statements were filed with the Securities and Exchange Commission (“SEC”).

Reclassifications

Certain amounts previously reported have been reclassified to conform to the current period presentation. The reclassifications were made to change the income statement presentation to provide the users of the financial statements additional information related to the operating results of the Company. These reclassifications include reclassifying the Company’s gains on debt repurchases to “gain on sale of loans and debt repurchases, net” which were previously included in “other income.” The reclassifications had no effect on consolidated net income or consolidated assets and liabilities.

2. Recent Developments

On March 30, 2010, President Obama signed into law the Health Care and Education Reconciliation Act of 2010 (the “Reconciliation Act of 2010”). Effective July 1, 2010, this law prohibits new loan originations under the Federal Family Education Loan Program (“FFELP”) and requires that all new federal loan originations be made through the Federal Direct Loan Program (the “Direct Loan Program”). If a first disbursement has been made on a FFELP loan prior to July 1, 2010, subsequent disbursements of that loan may still be made under the FFELP. The new law does not alter or affect the terms and conditions of existing FFELP loans.

As a result of the Reconciliation Act of 2010, the Company will no longer originate FFELP loans after 2010. During 2009, the Company recognized a gain of $36.6 million from selling $2.1 billion of 2008-2009 academic year loans to the Department of Education (the “Department”) under the Loan Purchase Commitment Program (the “Purchase Program”). The Company continues to use the Department’s Participation Program to fund loans originated for the 2009-2010 academic year. The Company has not yet determined if it will sell these loans to the Department under the Purchase Program. However, based on the number of 2009-2010 academic year loans held by the Company that are eligible for this program ($1.0 billion as of March 31, 2010), the Company estimates that it would recognize a gain of approximately $16 million to $18 million if it chose to sell these loans under this program. This amount does not include loans originated and/or acquired after March 31, 2010 which would increase the gain recognized by the Company. In addition, as a result of the Reconciliation Act of 2010, net interest income on the Company’s existing FFELP loan portfolio, as well as fee-based revenue from guarantee and third-party FFELP servicing and education loan software licensing and consulting fees will decline over time as the Company and its customers’ FFELP loan portfolios pay down.

In June 2009, the Company was one of four private sector companies awarded a student loan servicing contract by the Department. As of April 30, 2010, the Company was servicing $9.5 billion of FFELP loans now owned by the Department, and by August 2010 the Company expects to also begin servicing new loans originated under the Direct Loan Program. The Department has estimated $116 billion of new student loan originations will be funded through the Direct Loan Program for the 2010-2011 academic year. This volume will be allocated by the Department to the four servicers based on performance factors such as customer satisfaction levels and default rates. The Company believes revenue earned under the Department servicing contract and growth in non-FFELP fee-based operating segments in the future will partially offset the loss of future revenue due to the elimination of the FFELP.

Due to the legislative changes in the student loan industry, the Company also believes there will be opportunities to purchase FFELP loan portfolios and/or expand its current level of guarantee and third-party FFELP servicing volume on behalf of current FFELP participants looking to modify their involvement in FFELP and/or exit the market. For example, since April 1, 2010, the Company has purchased approximately $2 billion of FFELP student loans from various third-parties. These loans are not included in the March 31, 2010 balance sheet.

6

3. Student Loans Receivable and Allowance for Loan Losses

Student loans receivable consisted of the following:

|

As of

|

As of

|

|||||||

|

March 31,

2010

|

December 31,

2009

|

|||||||

|

Federally insured loans

|

$ | 24,412,262 | 23,472,553 | |||||

|

Non-federally insured loans

|

138,890 | 163,321 | ||||||

| 24,551,152 | 23,635,874 | |||||||

|

Unamortized loan premiums and deferred origination costs

|

333,741 | 341,970 | ||||||

|

Allowance for loan losses – federally insured loans

|

(30,744 | ) | (30,102 | ) | ||||

|

Allowance for loan losses – non-federally insured loans

|

(18,656 | ) | (20,785 | ) | ||||

| $ | 24,835,493 | 23,926,957 | ||||||

|

Allowance for federally insured loans as a percentage of such loans

|

0.13 | % | 0.13 | % | ||||

|

Allowance for non-federally insured allowance as a percentage of such loans

|

13.43 | % | 12.73 | % | ||||

The Company has provided for an allowance for loan losses related to its student loan portfolio. Activity in the allowance for loan losses for the three months ended March 31, 2010 and 2009 is shown below:

|

2010

|

2009

|

|||||||

|

Beginning balance

|

$ | 50,887 | 50,922 | |||||

|

Provision for loan losses

|

5,000 | 7,500 | ||||||

|

Loans charged off, net of recoveries

|

(5,197 | ) | (3,905 | ) | ||||

|

Purchase of loans

|

710 | — | ||||||

|

Sale of loans

|

(2,000 | ) | (6,020 | ) | ||||

|

Ending balance

|

$ | 49,400 | 48,497 | |||||

As of March 31, 2010, the Company has participated $115.5 million of non-federally insured loans to third parties, including $20.0 million during the first quarter of 2010. Loans participated under these agreements have been accounted for by the Company as loan sales. Accordingly, the participation interests sold are not included on the Company’s consolidated balance sheet. The loss on the sale of these loans was not material. Per the terms of the servicing agreements, the Company’s servicing operations are obligated to repurchase loans subject to the participation interests in the event such loans become 60 or 90 days delinquent. The activity in the accrual account during the three months ended March 31, 2010 and 2009 related to this repurchase obligation, which is included in “other liabilities” in the accompanying consolidated balance sheets, is detailed below.

|

2010

|

2009

|

|||||||

|

Beginning balance

|

$ | 10,600 | — | |||||

|

Transfer from allowance for loan losses

|

2,000 | 5,500 | ||||||

|

Ending balance

|

$ | 12,600 | 5,500 | |||||

Related Party Loan Activity

During 2008 and 2009, the Company sold $611.9 million of FFELP student loans (the “FFELP Loans”) to Union Bank & Trust Company (“Union Bank”), an entity under common control with the Company. These loans were sold pursuant to an affiliate transaction exemption granted by the Federal Reserve Board which allowed Union Bank to purchase FFELP loans from the Company. In connection with the exemption and the loan purchases by Union Bank, an Assurance Commitment Agreement (the “Commitment Agreement”) was also entered into, by and among, the Company, Union Bank, and Michael S. Dunlap, the Company’s Chairman, Chief Executive Officer, and a principal shareholder of the Company. Per the terms of the Commitment Agreement, the Company provided certain assurances to Union Bank designed to mitigate potential losses related to the FFELP Loans, including holding amounts in escrow equal to the unguaranteed portion and reimbursing Union Bank for losses, if any, related to the portfolio. As part of this agreement, the Company was also obligated to buy back loans once they were 30 days delinquent. During the first quarter 2010, the Company purchased $535.9 million (par value) of federally insured student loans from Union Bank, which represented all outstanding FFELP loans remaining under the provisions of the Commitment Agreement. As a result of this loan purchase, the Company no longer has a commitment to hold amounts in escrow, reimburse Union Bank for losses, and buy back delinquent loans related to this portfolio.

7

4. Bonds and Notes Payable

The Company has historically utilized operating cash flow, secured financing transactions (which include warehouse facilities, asset-backed securitizations, and the government’s Participation and Conduit Programs), operating lines of credit, and other borrowing arrangements to fund its Asset Generation and Management operations and student loan acquisitions. In addition, the Company has used operating cash flow, borrowings on its unsecured line of credit, and unsecured debt offerings to fund corporate activities, business acquisitions, and repurchases of common stock.

The following tables summarize the Company’s outstanding debt obligations by type of instrument:

|

As of March 31, 2010

|

|||||||||

|

Carrying

|

Interest rate

|

Final | |||||||

|

amount

|

range

|

maturity

|

|||||||

|

Variable-rate bonds and notes (a):

|

|||||||||

|

Bonds and notes based on indices

|

$ | 20,904,154 | 0.24% - 6.90 | % |

05/26/14 - 11/25/43

|

||||

|

Bonds and notes based on auction or remarketing

|

1,370,510 | 0.30% - 1.75 | % |

05/01/11 - 07/01/43

|

|||||

|

Total variable-rate bonds and notes

|

22,274,664 | ||||||||

|

Commercial paper - FFELP facility (b)

|

80,051 | 0.22% - 0.33 | % |

08/03/12

|

|||||

|

Unsecured debt - Senior Notes

|

66,716 | 5.125 | % |

06/01/10

|

|||||

|

Unsecured debt - Junior Subordinated Hybrid Securities

|

198,250 | 7.40 | % |

09/15/61

|

|||||

|

Unsecured line of credit

|

691,500 | 0.73 | % |

05/08/12

|

|||||

|

Department of Education Participation

|

1,028,402 | 0.71 | % |

09/30/10

|

|||||

|

Department of Education Conduit

|

1,384,819 | 0.23 | % |

05/08/14

|

|||||

|

Other borrowings

|

31,780 | 0.23% - 5.10 | % |

11/14/10 - 11/01/15

|

|||||

| $ | 25,756,182 | ||||||||

|

As of December 31, 2009

|

|||||||||

|

Carrying

|

Interest rate

|

Final | |||||||

|

amount

|

range

|

maturity

|

|||||||

|

Variable-rate bonds and notes (a):

|

|||||||||

|

Bonds and notes based on indices

|

$ | 20,187,356 | 0.26% - 6.90 | % |

05/26/14 - 04/25/42

|

||||

|

Bonds and notes based on auction or remarketing

|

1,726,960 | 0.21% - 3.73 | % |

05/01/11 - 07/01/43

|

|||||

|

Total variable-rate bonds and notes

|

21,914,316 | ||||||||

|

Commercial paper - FFELP facility (b)

|

305,710 | 0.21% - 0.32 | % |

08/03/12

|

|||||

|

Fixed-rate bonds and notes (a)

|

8,940 | 6.15% - 6.34 | % |

07/02/20 - 05/01/29

|

|||||

|

Unsecured debt - Senior Notes

|

66,716 | 5.125 | % |

06/01/10

|

|||||

|

Unsecured debt - Junior Subordinated Hybrid Securities

|

198,250 | 7.40 | % |

09/15/61

|

|||||

|

Unsecured line of credit

|

691,500 | 0.73 | % |

05/08/12

|

|||||

|

Department of Education Participation

|

463,912 | 0.79 | % |

09/30/10

|

|||||

|

Department of Education Conduit

|

1,125,929 | 0.27 | % |

05/08/14

|

|||||

|

Other borrowings

|

30,016 | 0.24% - 5.10 | % |

01/01/10 - 11/01/15

|

|||||

| $ | 24,805,289 | ||||||||

(a) Issued in asset-backed securitizations

(b) Loan warehouse facility

Secured Financing Transactions

The Company has historically relied upon secured financing vehicles as its most significant source of funding for student loans. The net cash flow the Company receives from the securitized student loans generally represents the excess amounts, if any, generated by the underlying student loans over the amounts required to be paid to the bondholders, after deducting servicing fees and any other expenses relating to the securitizations. The Company’s rights to cash flow from securitized student loans are subordinate to bondholder interests and may fail to generate any cash flow beyond what is due to bondholders.

8

The majority of the bonds and notes payable are primarily secured by the student loans receivable, related accrued interest, and by the amounts on deposit in the accounts established under the respective bond resolutions or financing agreements. Certain variable rate bonds and notes are secured by a letter of credit and reimbursement agreement issued by State Street.

Historically, the Company funded loan originations and acquisitions using loan warehouse facilities and asset-backed securitizations. Student loan warehousing allows the Company to buy and manage student loans prior to transferring them into more permanent financing arrangements. In August 2008, the Company began funding FFELP Stafford and PLUS student loan originations for the 2008-2009 and 2009-2010 academic years pursuant to the Department’s Participation Program and a participation agreement with Union Bank. In addition, in March 2009, the Company began funding loans under the Department’s Conduit Program.

Loan warehouse facility

On August 3, 2009, the Company entered into a FFELP warehouse facility (the “2009 FFELP Warehouse Facility”). The 2009 FFELP Warehouse Facility has a maximum financing amount of $500.0 million, with a revolving financing structure supported by 364-day liquidity provisions, which expire on August 2, 2010. The final maturity date of the facility is August 3, 2012. In the event the Company is unable to renew the liquidity provisions by August 2, 2010, the facility would become a term facility at a stepped-up cost, with no additional student loans being eligible for financing, and the Company would be required to refinance the existing loans in the facility by August 3, 2012.

The 2009 FFELP Warehouse Facility provides for formula based advance rates depending on FFELP loan type, up to a maximum of 92 percent to 98 percent of the principal and interest of loans financed. The advance rates for collateral may increase or decrease based on market conditions. The facility contains financial covenants relating to levels of the Company’s consolidated net worth, ratio of adjusted EBITDA to corporate debt interest, and unencumbered cash. Any violation of these covenants could result in a requirement for the immediate repayment of any outstanding borrowings under the facility. As of March 31, 2010, the Company was in compliance with all of these requirements. Unlike the Company’s prior FFELP warehouse facility, the 2009 FFELP Warehouse Facility does not require the Company to refinance or remove a percentage of the pledged student loan collateral on an annual basis. As of March 31, 2010, $80.1 million was outstanding under this facility and $419.9 million was available for future use.

On May 5, 2010, the Company amended the 2009 FFELP Warehouse Facility to increase the maximum financing amount by $500.0 million, to $1.0 billion in total. All loans funded with the additional $500.0 million of capacity must be eligible for the Department’s Straight-A Funding Conduit Program. The financing cost on the entire FFELP Warehouse Facility will increase by 300 basis points on any day after June 30, 2010 when the aggregate note balance is greater than $500.0 million. However, the Company intends to refinance loans in the warehouse facility that are eligible for the Department’s Conduit Program in advance of June 30, 2010 to avoid paying the increased cost.

Asset-backed securitizations

As part of the Company’s issuance of asset-backed securities in March 2008 and May 2008, due to credit market conditions when these notes were issued, the Company purchased the Class B subordinated notes of $36 million (par value) and $41 million (par value), respectively. These notes are not included on the Company’s consolidated balance sheet. If the credit market conditions continue to improve, the Company anticipates selling these notes to third parties. Upon a sale to third parties, the Company would obtain cash proceeds equal to the market value of the notes on the date of such sale. Upon sale, these notes would be shown as “bonds and notes payable” on the Company’s consolidated balance sheet. The Company believes the market value of such notes is currently less than par value. The difference between the par value and market value would be recognized by the Company as interest expense over the life of the bonds.

On February 17, 2010 and March 9, 2010, the Company completed asset-backed securities transactions of $523.3 million and $660.0 million, respectively. Notes issued in these transactions carry interest rates based on a spread to LIBOR. The Company used the proceeds from the sale of these notes to purchase principal and interest on student loans, which were previously financed in other asset-backed securitizations and the 2009 FFELP Warehouse Facility. In addition, the Company used the proceeds to purchase $535.9 million (par value) of federally insured student loans from Union Bank (see note 3).

Department of Education’s Loan Participation and Purchase Commitment Programs

In August 2008, the Department implemented the Purchase Program and the Participation Program pursuant to the Ensuring Continued Access to Student Loans Act of 2008 (“ECASLA”). Under the Department’s Purchase Program, the Department will purchase loans at a price equal to the sum of (i) par value, (ii) accrued interest, (iii) the one percent origination fee paid to the Department, and (iv) a fixed amount of $75 per loan. Under the Participation Program, the Department provides interim short term liquidity to FFELP lenders by purchasing participation interests in pools of FFELP loans. FFELP lenders are charged a rate of commercial paper plus 50 basis points on the principal amount of participation interests outstanding. Loans funded under the Participation Program for the 2009-2010 academic year must be either refinanced by the lender or sold to the Department pursuant to the Purchase Program on or prior to September 30, 2010. To be eligible for purchase or participation under the Department’s programs, loans are limited to FFELP Stafford or PLUS loans first disbursed on or after May 1, 2008 but no later than July 1, 2010, with eligible borrower benefits. As of March 31, 2010 and December 31, 2009, the Company had $1.0 billion and $0.5 billion, respectively, borrowed under the Participation Program. The Company plans to continue to use the Participation Program to fund 2009-2010 academic year loans.

9

Department of Education’s Conduit Program

In January 2009, the Department published summary terms for its program under which it will finance eligible FFELP Stafford and PLUS loans in a conduit vehicle established to provide funding for student lenders (the “Conduit Program”). Loans eligible for the Conduit Program had to be first disbursed on or after October 1, 2003, but not later than June 30, 2009, and fully disbursed before September 30, 2009, and meet certain other requirements. The Conduit Program was launched on May 11, 2009. Funding for the Conduit Program is provided by the capital markets at a cost based on market rates, with the Company being advanced 97 percent of the student loan face amount. Excess amounts needed to fund the remaining 3 percent of the student loan balances are contributed by the Company. The Conduit Program has a term of five years and expires on May 8, 2014. The Student Loan Short-Term Notes (“Student Loan Notes”) issued by the Conduit Program are supported by a combination of (i) notes backed by FFELP loans, (ii) a liquidity agreement with the Federal Financing Bank, and (iii) a put agreement provided by the Department. If the conduit does not have sufficient funds to pay all Student Loan Notes, then those Student Loan Notes will be repaid with funds from the Federal Financing Bank. The Federal Financing Bank will hold the notes for a short period of time and, if at the end of that time, the Student Loan Notes still cannot be paid off, the underlying FFELP loans that serve as collateral to the Conduit Program will be sold to the Department through a put agreement at a price of 97 percent of the face amount of the loans. As of March 31, 2010 and December 31, 2009, the Company had $1.4 billion and $1.1 billion, respectively, borrowed under the facility and $62.7 million and $66.8 million, respectively, advanced as equity support in the facility.

Union Bank Participation Agreement

The Company maintains an agreement with Union Bank, as trustee for various grantor trusts, under which Union Bank has agreed to purchase from the Company participation interests in student loans (the “FFELP Participation Agreement”). The Company has the option to purchase the participation interests from the grantor trusts at the end of a 364-day term upon termination of the participation certificate. As of March 31, 2010 and December 31, 2009, $725.9 million and $613.3 million, respectively, of loans were subject to outstanding participation interests held by Union Bank, as trustee, under this agreement. The agreement automatically renews annually and is terminable by either party upon five business days notice. This agreement provides beneficiaries of Union Bank’s grantor trusts with access to investments in interests in student loans, while providing liquidity to the Company on a short-term basis. The Company can participate loans to Union Bank to the extent of availability under the grantor trusts, up to $750 million or an amount in excess of $750 million if mutually agreed to by both parties. Loans participated under this agreement have been accounted for by the Company as loan sales. Accordingly, the participation interests sold are not included on the Company’s consolidated balance sheet.

Unsecured Line of Credit

The Company has a $750.0 million unsecured line of credit that terminates in May 2012. As of March 31, 2010 there was $691.5 million outstanding on this line. The weighted average interest rate on this line of credit was 0.725% as of March 31, 2010. Upon termination in 2012, there can be no assurance that the Company will be able to maintain this line of credit, find alternative funding, or increase the amount outstanding under the line, if necessary. The lending commitment under the Company’s unsecured line of credit is provided by a total of thirteen banks, with no individual bank representing more than 11% of the total lending commitment. The bank lending group includes Lehman Brothers Bank (“Lehman”), a subsidiary of Lehman Brothers Holdings Inc., which represents approximately 7% of the lending commitment under the line of credit. On September 15, 2008, Lehman Brothers Holdings Inc. filed a voluntary petition for relief under Chapter 11 of the United States Bankruptcy Code. The Company does not expect that Lehman will fund future borrowing requests. As of March 31, 2010, excluding Lehman’s lending commitment, the Company has $51.2 million available for future use under its unsecured line of credit.

The line of credit agreement contains certain financial covenants that, if not met, lead to an event of default under the agreement. The covenants include maintaining:

|

|

·

|

A minimum consolidated net worth

|

|

|

·

|

A minimum adjusted EBITDA to corporate debt interest (over the last four rolling quarters)

|

|

|

·

|

A limitation on subsidiary indebtedness

|

|

|

·

|

A limitation on the percentage of non-guaranteed loans in the Company’s portfolio

|

As of March 31, 2010, the Company was in compliance with all of these requirements. Many of these covenants are duplicated in the Company’s other lending facilities, including its FFELP warehouse facility.

The Company’s operating line of credit does not have any covenants related to unsecured debt ratings. However, changes in the Company’s ratings (as well as the amounts the Company borrows) have modest implications on the pricing level at which the Company obtains funding.

10

A default on the 2009 FFELP Warehouse Facility would result in an event of default on the Company’s unsecured line of credit that would result in the outstanding balance on the line of credit becoming immediately due and payable.

Debt Repurchases

The Company repurchased outstanding debt during the first quarter of 2010 and 2009 as summarized below. Gains recorded by the Company from the repurchase of debt are included in “gain on sale of loans and debt repurchases, net” on the Company’s consolidated statements of income.

|

Three months ended March 31, 2010

|

||||||||||||

|

Notional

amount

|

Purchase

price

|

Gain

|

||||||||||

|

Asset-backed securities

|

$ | 274,250 | 264,073 | 10,177 | ||||||||

|

Three months ended March 31, 2009

|

||||||||||||

|

Notional

amount

|

Purchase

price

|

Gain

|

||||||||||

|

5.125% Senior Notes due 2010

|

$ | 34,866 | 26,791 | 8,075 | ||||||||

As of March 31, 2010, the Company has repurchased $622.4 million of its own asset-backed securities (bonds and notes payable). For accounting purposes, these notes were effectively retired and are not included on the Company’s consolidated balance sheet. However, $155.7 million of these securities are legally outstanding at the trust level and the Company could sell these notes to third parties or redeem the notes at par as cash is generated by the trust estate. Upon a sale to third parties, the Company would obtain cash proceeds equal to the market value of the notes on the date of such sale. Upon sale, these notes would be shown as “bonds and notes payable” on the Company’s consolidated balance sheet.

5. Derivative Financial Instruments

The Company is exposed to certain risks relating to its ongoing business operations. The primary risks managed by using derivative instruments are interest rate risk and foreign currency exchange risk.

Interest Rate Risk

The Company’s primary market risk exposure arises from fluctuations in its borrowing and lending rates, the spread between which could impact the Company due to shifts in market interest rates. Because the Company generates a significant portion of its earnings from its student loan spread, the interest rate sensitivity of the balance sheet is a key profitability driver. The Company has adopted a policy of periodically reviewing the mismatch related to the interest rate characteristics of its assets and liabilities together with the Company's outlook as to current and future market conditions. Based on those factors, the Company uses derivative instruments as part of its overall risk management strategy.

Basis Swaps

The Company issues asset-backed securities, the vast majority being variable rate, to fund its student loan assets. The variable rate debt is generally indexed to three-month LIBOR, set by auction, or through a remarketing process. The income generated by the Company’s student loan assets is generally driven by short term indices (treasury bills, commercial paper, and certain fixed rates) that are different from those which affect the Company’s liabilities, which creates basis risk. Moreover, the Company also faces repricing risk due to the timing of the interest rate resets on its liabilities, which may occur as infrequently as every quarter, and the timing of the interest rate resets on its assets, which generally occurs daily. In a declining interest rate environment, this may cause the Company’s student loan spread to compress, while in a rising rate environment, it may cause the spread to increase. As of March 31, 2010, the Company had $23.4 billion and $1.0 billion of FFELP loans indexed to the three-month financial commercial paper rate and the three-month treasury bill rate, respectively, both of which reset daily, and $20.9 billion of debt indexed to three-month LIBOR, which resets quarterly.

Because of the different index types and different index reset frequencies, the Company is exposed to interest rate risk in the form of basis risk and repricing risk, which, as noted above, is the risk that the different indices may reset at different frequencies, or will not move in the same direction or with the same magnitude. While these indices are short term with rate movements that are highly correlated over a longer period of time, capital market dislocations or other factors not within the Company’s control can impact the level of correlation on these indices.

The Company has used derivative instruments to hedge both the basis and repricing risk on certain student loans in which the Company earns interest based on a treasury bill rate that resets daily and are funded with debt indexed to primarily three-month LIBOR. To hedge these loans, the Company has entered into basis swaps in which the Company receives three-month LIBOR set discretely in advance and pays a weekly treasury bill rate plus a spread as defined in the agreement (“T-Bill/LIBOR Basis Swaps”).

11

However, the Company does not generally hedge the basis risk on those assets indexed to the commercial paper rate that are funded with liabilities in which the Company pays primarily on the LIBOR index, since the derivatives needed to hedge this risk are generally illiquid or non-existent and the relationship between these indices has been highly correlated over a long period of time.

The Company has also used derivative instruments to hedge the repricing risk due to the timing of the interest rate resets on its assets and liabilities. The Company has entered into basis swaps in which the Company:

|

|

·

|

receives three-month LIBOR set discretely in advance and pays a daily weighted average three-month LIBOR less a spread as defined in the agreements (the “Average/Discrete Basis Swaps”)

|

|

|

·

|

receives three-month LIBOR and pays one-month LIBOR plus or minus a spread as defined in the agreements (the “1/3 Basis Swaps”)

|

The following table summarizes the Company’s basis swaps outstanding as of March 31, 2010 and December 31, 2009:

|

Notional amounts

|

||||||||

|

1/3 Basis

Swaps

|

T-Bill/LIBOR

Basis Swaps

|

|||||||

|

Maturity

|

||||||||

|

2010

|

$ | 1,000,000 | — | |||||

|

2011 (a)

|

— | 225,000 | ||||||

|

2013

|

500,000 | — | ||||||

|

2014

|

500,000 | — | ||||||

|

2018

|

1,300,000 | — | ||||||

|

2019

|

500,000 | — | ||||||

|

2021

|

250,000 | — | ||||||

|

2023

|

1,250,000 | — | ||||||

|

2024

|

250,000 | — | ||||||

|

2028

|

100,000 | — | ||||||

|

2039

|

150,000 | — | ||||||

| $ | 5,800,000 | 225,000 | ||||||

(a) These derivatives have forward effective start dates of October 2010 ($75 million), November 2010 ($75 million), and December 2010 ($75 million).

Interest rate swaps

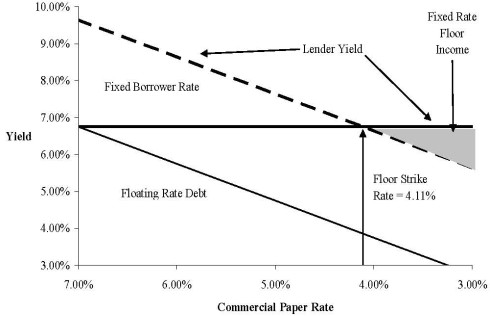

FFELP loans originated prior to April 1, 2006 generally earn interest at the higher of a floating rate based on the Special Allowance Payment (or SAP) formula set by the Department and the borrower rate, which is fixed over a period of time. The SAP formula is based on an applicable index plus a fixed spread that is dependent upon when the loan was originated, the loan’s repayment status, and funding sources for the loan. The Company generally finances its student loan portfolio with variable rate debt. In low and/or declining interest rate environments, when the fixed borrower rate is higher than the rate produced by the SAP formula, the Company’s student loans earn at a fixed rate while the interest on the variable rate debt typically continues to decline. In these interest rate environments, the Company may earn additional spread income that it refers to as floor income.

Depending on the type of loan and when it was originated, the borrower rate is either fixed to term or is reset to an annual rate each July 1. As a result, for loans where the borrower rate is fixed to term, the Company may earn floor income for an extended period of time, which the Company refers to as fixed rate floor income, and for those loans where the borrower rate is reset annually on July 1, the Company may earn floor income to the next reset date, which the Company refers to as variable rate floor income. In accordance with legislation enacted in 2006, lenders are required to rebate fixed rate floor income and variable rate floor income to the Department for all FFELP loans first originated on or after April 1, 2006.

Absent the use of derivative instruments, a rise in interest rates may reduce the amount of floor income received and this may have an impact on earnings due to interest margin compression caused by increasing financing costs, until such time as the federally insured loans earn interest at a variable rate in accordance with their special allowance payment formulas. In higher interest rate environments, where the interest rate rises above the borrower rate and fixed rate loans effectively become variable rate loans, the impact of the rate fluctuations is reduced.

12

As of March 31, 2010 and December 31, 2009, the Company had $10.4 billion and $10.3 billion, respectively, of student loan assets that were earning fixed rate floor income. The following tables summarize the outstanding derivative investments used by the Company to hedge these loans.

| As of March 31, 2010 | ||||||||

|

Weighted

|

||||||||

|

average fixed

|

||||||||

|

Notional

|

rate paid by

|

|||||||

| Maturity | amount | the Company (a) | ||||||

|

2010

|

$ | 4,750,000 | 0.54 | % | ||||

|

2011

|

1,500,000 | 0.66 | ||||||

| $ | 6,250,000 | 0.57 | % | |||||

| As of December 31, 2009 | ||||||||

|

Weighted

|

||||||||

|

average fixed

|

||||||||

|

Notional

|

rate paid by

|

|||||||

| Maturity | amount | the Company (a) | ||||||

|

2010

|

$ | 4,750,000 | 0.54 | % | ||||

|

2011

|

150,000 | 1.03 | ||||||

| $ | 4,900,000 | 0.55 | % | |||||

(a) For all interest rate derivatives, the Company receives discrete three-month LIBOR.

Foreign Currency Exchange Risk

During 2006, the Company completed separate debt offerings of student loan asset-backed securities that included 420.5 million and 352.7 million Euro Notes with interest rates based on a spread to the EURIBOR index. As a result of this transaction, the Company is exposed to market risk related to fluctuations in foreign currency exchange rates between the U.S. dollar and Euro. The principal and accrued interest on these notes is re-measured at each reporting period and recorded on the Company’s balance sheet in U.S. dollars based on the foreign currency exchange rate on that date. Changes in the principal and accrued interest amounts as a result of foreign currency exchange rate fluctuations are included in the “derivative market value and foreign currency adjustments and derivative settlements, net” in the Company’s consolidated statements of income.

The Company entered into cross-currency interest rate swaps in connection with the issuance of the Euro Notes. Under the terms of these derivative instrument agreements, the Company receives from a counterparty a spread to the EURIBOR index based on notional amounts of €420.5 million and €352.7 million and pays a spread to the LIBOR index based on notional amounts of $500.0 million and $450.0 million, respectively. In addition, under the terms of these agreements, all principal payments on the Euro Notes will effectively be paid at the exchange rate in effect as of the issuance of the notes.

The following table shows the income statement impact as a result of the re-measurement of the Euro Notes and the change in the fair value of the related derivative instruments for the three months ended March 31, 2010 and 2009. These items are included in “Derivative market value and foreign currency adjustments and derivative settlements, net” on the accompanying consolidated statements of income.

|

2010

|

2009

|

|||||||

|

Re-measurement of Euro Notes

|

$ | 71,675 | 47,242 | |||||

|

Change in fair value of cross currency interest rate swaps

|

(59,075 | ) | (57,110 | ) | ||||

|

Total impact to statements of income - income (expense)

|

$ | 12,600 | (9,868 | ) | ||||

The re-measurement of the Euro-denominated bonds generally correlates with the change in fair value of the cross-currency interest rate swaps. However, the Company will experience unrealized gains or losses related to the cross-currency interest rate swaps if the two underlying indices (and related forward curve) do not move in parallel. Management intends to hold the cross-currency interest rate swaps through the maturity of the Euro-denominated bonds.

13

Accounting for Derivative Financial Instruments

The Company records derivative instruments on the consolidated balance sheet as either an asset or liability measured at its fair value. Management has structured the majority of the Company’s derivative transactions with the intent that each is economically effective; however, the Company’s derivative instruments do not qualify for hedge accounting. As a result, the change in fair value of the Company’s derivatives at each reporting date are included in “derivative market value and foreign currency adjustments and derivative settlements, net” in the Company’s consolidated statements of income. Changes or shifts in the forward yield curve and fluctuations in currency rates can significantly impact the valuation of the Company’s derivatives. Accordingly, changes or shifts to the forward yield curve and fluctuations in currency rates will impact the financial position and results of operations of the Company.

Any proceeds received or payments made by the Company to terminate a derivative in advance of its expiration date, or to amend the terms of an existing derivative, are included in “derivative market value and foreign currency adjustments and derivative settlements, net” on the consolidated statements of income and are accounted for as a change in fair value on such derivative.

The following table summarizes the fair value of the Company’s derivatives not designated as hedging:

|

Fair value of asset derivatives

|

Fair value of liability derivatives

|

|||||||||||||||

|

As of

March 31,

2010

|

As of

December 31, 2009

|

As of

March 31,

2010

|

As of

December 31, 2009

|

|||||||||||||

|

Interest rate swaps

|

$ | 66 | 4,497 | (5,337 | ) | (2,230 | ) | |||||||||

|

Average/discrete basis swaps

|

— | — | — | — | ||||||||||||

|

1/3 basis swaps

|

17,233 | 17,768 | (170 | ) | — | |||||||||||

|

T-Bill/LIBOR basis swaps

|

— | — | (55 | ) | (259 | ) | ||||||||||

|

Cross-currency interest rate swaps

|

110,742 | 169,817 | — | — | ||||||||||||

|

Other

|

1,018 | 1,817 | (512 | ) | — | |||||||||||

|

Total

|

$ | 129,059 | 193,899 | (6,074 | ) | (2,489 | ) | |||||||||

The following table summarizes the effect of derivative instruments in the consolidated statements of income for the three months ended March 31, 2010 and 2009. All gains and losses recognized in income related to the Company’s derivative activity are included in “Derivative market value and foreign currency adjustments and derivative settlements, net”, on the consolidated statements of income.

|

Amount of gain (or loss)

|

||||||||

|

Derivatives not designated as hedging

|

recognized in income on derivatives

|

|||||||

|

2010

|

2009

|

|||||||

|

Settlements:

|

||||||||

|

Interest rate swaps

|

$ | (3,856 | ) | — | ||||

|

Average/discrete basis swaps

|

— | 10,022 | ||||||

|

1/3 basis swaps

|

131 | 10,744 | ||||||

|

Cross-currency interest rate swaps

|

1,302 | 3,592 | ||||||

|

Total settlements - (expense) income

|

(2,423 | ) | 24,358 | |||||

|

Change in fair value:

|

||||||||

|

Interest rate swaps

|

(7,538 | ) | — | |||||

|

Average/discrete basis swaps

|

— | (286 | ) | |||||

|

1/3 basis swaps

|

(546 | ) | 5,274 | |||||

|

T-Bill/LIBOR basis swaps

|

45 | — | ||||||

|

Cross-currency interest rate swaps

|

(59,075 | ) | (57,110 | ) | ||||

|

Other

|

(456 | ) | — | |||||

|

Total change in fair value - (expense) income

|

(67,570 | ) | (52,122 | ) | ||||

|

Re-measurement of Euro Notes (foreign currency

|

||||||||

|

transaction adjustment) - income

|

71,675 | 47,242 | ||||||

|

Derivative market value and forgeign currency adjustments

|

||||||||

|

and derivative settlements - income

|

$ | 1,682 | 19,478 | |||||

Derivative Instruments - Credit and Market Risk

By using derivative instruments, the Company is exposed to credit and market risk.

When the fair value of a derivative instrument is negative, the Company would owe the counterparty if the derivative was settled and, therefore, has no immediate credit risk. Additionally, if the negative fair value of derivatives with a counterparty exceeds a specified threshold, the Company may have to make a collateral deposit with the counterparty. The threshold at which the Company posts collateral may depend on the Company’s unsecured credit rating. If interest and foreign currency exchange rates move materially, the Company could be required to deposit a significant amount of collateral with its derivative instrument counterparties. The collateral deposits, if significant, could negatively impact the Company’s liquidity and capital resources. As of March 31, 2010, the Company had $3.4 million posted as collateral to derivative counterparties.

14

When the fair value of a derivative contract is positive, this generally indicates that the counterparty would owe the Company if the derivative was settled. If the counterparty fails to perform, credit risk with such counterparty is equal to the extent of the fair value gain in the derivative less any collateral held by the Company. As of March 31, 2010, the Company held $199.1 million of collateral from the counterparty on the cross-currency interest rate swaps.

The Company attempts to manage market and credit risks associated with interest and foreign currency exchange rates by establishing and monitoring limits as to the types and degree of risk that may be undertaken, and by entering into transactions with high-quality counterparties that are reviewed periodically by the Company’s risk committee. The Company also has a policy of requiring that all derivative contracts be governed by an International Swaps and Derivatives Association, Inc. Master Agreement.

6. Segment Reporting

The Company has four operating segments as follows: Student Loan and Guaranty Servicing, Tuition Payment Processing and Campus Commerce, Enrollment Services, and Asset Generation and Management. The Company’s operating segments are defined by the products and services they offer or the types of customers they serve, and they reflect the manner in which financial information is currently evaluated by management. In the first quarter of 2010, internal reporting to executive management (the “chief operating decision maker”) changed to reflect operational changes made within the organization. The operations of various segments changed in 2010 in order for the Company to capitalize on external servicing opportunities while obtaining maximum operating leverage. The change in operating results reviewed by management changed the operating segments historically reported by the Company. The operational and internal reporting changes included moving the majority of software and information technology products and services and related expenses to the Student Loan and Guaranty Servicing operating segment. The internal and external revenue and expenses related to these products and services were historically included within Corporate Activities and the former Software and Technical Services operating segment. The Software and Technical Services operating segment no longer meets the definition of an operating segment as described in the Accounting Standards Codification (“ASC”) Topic 280, Segment Reporting. Prior period segment operating results were restated to conform to the current period presentation.

The accounting policies of the Company’s operating segments are the same as those described in the summary of significant accounting policies. Intersegment revenues are charged by a segment to another segment that provides the product or service. Intersegment revenues and expenses are included within each segment consistent with the income statement presentation provided to management. Changes in management structure or allocation methodologies and procedures may result in changes in reported segment financial information. In 2010, the Company began allocating certain corporate overhead expenses to the individual operating segments. These expenses include certain corporate activities related to executive management, human resources, accounting and finance, legal, and marketing. These costs are allocated to each operating segment based on estimated use of such activities and services. These allocations were not made in 2009, and thus are not reflected in the 2009 segment operating results.

The management reporting process measures the performance of the Company’s operating segments based on the management structure of the Company as well as the methodology used by management to evaluate performance and allocate resources. Management, including the Company’s chief operating decision maker, evaluates the performance of the Company’s operating segments based on their profitability. As discussed further below, management measures the profitability of the Company’s operating segments based on “base net income.” Accordingly, information regarding the Company’s operating segments is provided based on “base net income.” The Company’s “base net income” is not a defined term within generally accepted accounting principles (“GAAP”) and may not be comparable to similarly titled measures reported by other companies. Unlike financial accounting, there is no comprehensive, authoritative guidance for management reporting.

Historically, the Company generated the majority of its revenue from net interest income earned in its Asset Generation and Management operating segment. The Company made several acquisitions that have expanded the Company’s products and services and have diversified its revenue – primarily from fee-based businesses. The Company currently offers a broad range of pre-college, in-college, and post-college products and services to students, families, schools, and financial institutions. These products and services help students and families plan and pay for their education and students plan their careers. The Company’s products and services are designed to simplify the education planning and financing process and are focused on providing value to students, families, and schools throughout the education life cycle. The Company continues to diversify its sources of revenue, including those generated from businesses that are not dependent upon government programs, thereby reducing legislative and political risk.

15

Fee-Based Operating Segments

Student Loan and Guaranty Servicing

The following are the primary product and service offerings the Company offers as part of its Student Loan and Guaranty Servicing segment:

|

|

·

|

Origination and servicing of FFELP loans

|

|

|

·

|

Origination and servicing of non-federally insured student loans

|

|

|

·

|

Servicing federally-owned student loans for the Department of Education

|

|

|

·

|

Servicing and support outsourcing for guaranty agencies

|

|

|

·

|

Student loan servicing software and other information technology products and services

|

The Student Loan and Guaranty Servicing operating segment provides for the servicing of the Company’s student loan portfolios and the portfolios of third parties. The loan servicing activities include loan origination activities, application processing, borrower updates, payment processing, due diligence procedures, and claim processing. These activities are performed internally for the Company’s portfolio in addition to generating fee revenue when performed for third-party clients.

In June 2009, the Department of Education named the Company as one of four private sector companies awarded a servicing contract to service all federally-owned student loans, including FFELP loans purchased by the Department pursuant to ECASLA. No later than August 2010, the Company expects to also begin servicing new loans originated under the Direct Loan Program. The contract spans five years with one, five-year renewal option.

This operating segment also provides servicing activities for guarantee agencies. These activities include providing software and data center services, borrower and loan updates, default aversion tracking services, claim processing services, and post-default collection services.

This operating segment also develops student loan servicing software, which is used internally by the Company and also licensed to third-party student loan holders and servicers. In addition, this operating segment provides information technology products and services, with core areas of business in educational loan software solutions, business intelligence, technical consulting services, and Enterprise Content Management solutions.

Tuition Payment Processing and Campus Commerce

The Tuition Payment Processing and Campus Commerce operating segment provides products and services to help institutions and education-seeking families manage the payment of education costs during the pre-college and college stages of the education life cycle. The Company provides actively managed tuition payment solutions, online payment processing, detailed information reporting, financial needs analysis, and data integration services to K-12 and higher educational institutions, families, and students. In addition, the Company provides customer-focused electronic transactions, information sharing, and account and bill presentment to colleges and universities.

Enrollment Services

The Enrollment Services operating segment offers products and services that are focused on helping colleges recruit and retain students (interactive and list marketing products and services) and helping students plan and prepare for life after high school (publishing and editing services and resource centers). Interactive marketing products and services include vendor lead management services, admissions lead generation, pay per click marketing management, email marketing, and admissions consulting. Publishing and editing services include test preparation study guides and essay and resume editing services. Resource centers and list marketing products and services include online courses and related services and list marketing services.

Asset Generation and Management Operating Segment

The Asset Generation and Management operating segment includes the acquisition, management, and ownership of the Company’s student loan assets. Revenues are primarily generated from the Company’s earnings from the spread, referred to as the Company’s student loan spread, between the yield received on the student loan portfolio and the costs associated with originating, acquiring, and financing its student loan portfolio. The Company generates student loan assets through direct origination or through acquisitions. The student loan assets are held in a series of education lending subsidiaries designed specifically for this purpose. In addition to the student loan portfolio, all costs and activity associated with the generation of assets, funding of those assets, and maintenance of the debt transactions are included in this segment.

Segment Operating Results – “Base Net Income”

The tables below include the operating results of each of the Company’s operating segments. Management, including the chief operating decision maker, evaluates the Company on certain non-GAAP performance measures that the Company refers to as “base net income” for each operating segment. While “base net income” is not a substitute for reported results under GAAP, the Company relies on “base net income” to manage each operating segment because it believes this measure provides additional information regarding the operational and performance indicators that are most closely assessed by management.

16

“Base net income” is the primary financial performance measure used by management to develop the Company’s financial plans, track results, and establish corporate performance targets and incentive compensation. Management believes this information provides additional insight into the financial performance of the core business activities of the Company’s operating segments. Accordingly, the tables presented below reflect “base net income,” which is the operating measure reviewed and utilized by management to manage the business. Reconciliation of the segment totals to the Company’s operating results in accordance with GAAP are also included in the tables below.

Certain amounts previously reported have been reclassified to conform to the current period presentation. The reclassifications were made to change the income statement presentation to provide the users of the financial statements additional information related to the operating results of the Company. These reclassifications include reclassifying the Company’s gains on debt repurchases to “gain on sale of loans and debt repurchases, net” which were previously included in “other income.” In addition, as discussed previously, in the first quarter of 2010, a change in operating results reviewed by management changed the operating segments historically reported by the Company. Prior period segment operating results were restated to conform to the current period presentation.

Segment Results and Reconciliations to GAAP

|

Three months ended March 31, 2010

|

||||||||||||||||||||||||||||||||||||

|