Attached files

| file | filename |

|---|---|

| EX-23.2 - EXHIBIT 23.2 - Fairfield County Bank Corp. | dex232.htm |

Table of Contents

As filed with the Securities and Exchange Commission on May 10, 2010

Registration No. 333-165480

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

PRE-EFFECTIVE AMENDMENT NO. 2

TO

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Fairfield County Bank Corp.

and

Fairfield County Bank Incentive Retirement Plan

(Exact name of registrant as specified in its charter)

| United States | 6035 | To be Applied For | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(IRS Employer Identification No.) |

150 Danbury Road

Ridgefield, Connecticut

(203) 438-6518

(Address, including zip code, and telephone number,

including area code, of registrant’s principal executive offices)

Gary C. Smith

Chief Executive Officer

Fairfield County Bank Corp.

150 Danbury Road

Ridgefield, Connecticut 06877

(203) 438-6518

(Name, address, including zip code, and telephone number,

including area code, of agent for service)

Copies to:

| Paul M. Aguggia, Esquire Lori M. Beresford, Esquire Kilpatrick Stockton LLP 607 14th Street, NW, Suite 900 Washington, DC 20005 (202) 508-5800 |

William W. Bouton, III, Esquire Hinckley, Allen & Snyder LLP 20 Church Street Hartford, Connecticut 06103 (860) 725-6200 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act, check the following box. x

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Calculation of Registration Fee

| Title of each class of securities to be registered |

Amount to be registered |

Proposed maximum offering price per unit |

Proposed maximum Aggregate offering price (1) |

Amount of Registration fee | ||||

| Common Stock $0.01 par value |

6,837,325 (2) | $10.00 | $68,373,250 | $ — (3) | ||||

| Participation Interests |

— (4) | — | $ — (4) | $ — (4) | ||||

| (1) | Estimated solely for the purpose of calculating the registration fee. |

| (2) | In addition, pursuant to Rule 416(c) under the Securities Act, this registration statement also covers an indeterminate amount of interests to be offered or sold pursuant to the employee benefit plan described herein. |

| (3) | The registration fee of $4,876 was previously paid upon the initial filing of the Form S-1 on March 15, 2010. |

| (4) | The securities of Fairfield County Bank Corp. to be purchased by the Registrant’s 401(k) Plan are included in the amount shown for the common stock. Accordingly, no separate fee is required for the participation interests. In accordance with Rule 457(h) of the Securities Act of 1933, as amended, the registration fee has been calculated on the basis of the number of shares of common stock that may be purchased with the current assets of such Plan. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to Section 8(a), may determine.

Table of Contents

PARTICIPATION INTERESTS IN

FAIRFIELD COUNTY BANK

INCENTIVE RETIREMENT PLAN

AND

OFFERING OF 2,752,215 SHARES OF

FAIRFIELD COUNTY BANK CORP.

COMMON STOCK ($.01 PAR VALUE)

This prospectus supplement relates to the offer and sale to participants in the Fairfield County Bank Incentive Retirement Plan (the “401(k) Plan”) of participation interests and shares of common stock of Fairfield County Bank Corp. (“Fairfield County”) in connection with the initial public offering of Fairfield County.

401(k) Plan participants may direct Countybank, as the trustee for the Fairfield County Stock Fund, to use all or a portion of their account balances to subscribe for and purchase shares of Fairfield County common stock through the Fairfield County Stock Fund. Based on the value of the 401(k) Plan assets as of March 1, 2010, the trustee may purchase up to 2,752,215 shares of Fairfield County common stock at a purchase price of $10.00 per share. This prospectus supplement relates to the election of 401(k) Plan participants to direct the trustee to invest their 401(k) Plan account funds in Fairfield County common stock.

The Fairfield County prospectus dated , 2010, which is attached to this prospectus supplement, includes detailed information regarding the offering of shares of Fairfield County common stock and the financial condition, results of operations and business of Fairfield County Bank (the “Bank”). This prospectus supplement provides information regarding the 401(k) Plan. You should read this prospectus supplement together with the prospectus and keep both for future reference.

Please refer to “Risk Factors” beginning on page of the prospectus.

Neither the Securities and Exchange Commission, the Office of Thrift Supervision, the Federal Deposit Insurance Corporation, nor any other state or federal agency or any state securities commission, has approved or disapproved these securities. Any representation to the contrary is a criminal offense.

These securities are not deposits or accounts and are not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency.

This prospectus supplement may be used only in connection with offers and sales by Fairfield County of participation interests or shares of common stock under the 401(k) Plan in the offering. No one may use this prospectus supplement to re-offer or resell interests or shares of common stock acquired through the 401(k) Plan.

You should rely only on the information contained in this prospectus supplement and the attached prospectus. Neither Fairfield County, the Bank nor the 401(k) Plan has authorized anyone to provide you with different information.

This prospectus supplement does not constitute an offer to sell or solicitation of an offer to buy any securities in any jurisdiction to any person to whom it is unlawful to make such an offer or solicitation in that jurisdiction. Neither the delivery of this prospectus supplement and the prospectus nor any sale of common stock shall under any circumstances imply that there has been no change in the affairs of the Bank or the 401(k) Plan since the date of this prospectus supplement, or that the information contained in this prospectus supplement or incorporated by reference is correct as of any time after the date of this prospectus supplement.

The date of this Prospectus Supplement is , 2010.

Table of Contents

| Page | ||

| 1 | ||

| Election to Purchase Fairfield County Common Stock in the Stock Offering |

1 | |

| 2 | ||

| 2 | ||

| 2 | ||

| 2 | ||

| 2 | ||

| 2 | ||

| Nature of a Participant’s Interest in Fairfield County Common Stock |

3 | |

| 3 | ||

| 3 | ||

| 3 | ||

| 4 | ||

| 4 | ||

| 5 | ||

| 6 | ||

| 8 | ||

| 8 | ||

| 8 | ||

| 8 | ||

| 9 | ||

| 9 | ||

| 9 | ||

| 9 | ||

| 10 | ||

| 11 | ||

| 11 | ||

i

Table of Contents

The securities offered in connection with this prospectus supplement are participation interests in the 401(k) Plan. At a purchase price of $10.00 per share, the trustee may acquire up to 2,752,215 shares of Fairfield County common stock in the initial public offering (the “Stock Offering”) on behalf of the plan participants. The interests offered by means of this prospectus supplement are conditioned on the close of the Stock Offering. Certain subscription rights and purchase limitations also govern your investment in the Fairfield County Stock Fund in connection with the Stock Offering. See “The Conversion and Stock Offering – Subscription Offering and Subscription Rights” and “– Limitations on Purchases of Shares” in the prospectus attached to this prospectus supplement for further discussion of these subscription rights and purchase limitations.

This prospectus supplement contains information regarding the 401(k) Plan. The attached prospectus contains information regarding the Stock Offering and the financial condition, results of operations and business of the Bank and its affiliates. The address of the principal executive office of Fairfield County Bank is 150 Danbury Road, Ridgefield, Connecticut 06877. The telephone number of the Bank is (203) 438-6518.

Election to Purchase Fairfield County Common Stock in the Stock Offering

In connection with the Stock Offering, you may direct the trustee to use your 401(k) Plan funds to subscribe for Fairfield County common stock through the Fairfield County Stock Fund. In order to use your 401(k) Plan funds to subscribe for shares in the Stock Offering, you must first transfer funds from your current 401(k) Plan investments into the Fairfield County Stock Cash Account (“FCS Cash Account”). The funds you transfer to FCS Cash Account must be divisible by $10.00 (the per share price of common stock in the Stock Offering). Once you transfer funds into the FCS Cash Account you will not be able to move those funds out of the FCS Cash Account until after the close of the Stock Offering. If there is not enough Fairfield County common stock available in the Stock Offering to fill all subscriptions, the common stock will be apportioned and the trustee may not be able to purchase all of the common stock you requested. If the Stock Offering is oversubscribed and your order is cut back, your 401(k) Plan funds (which are not invested in Fairfield County Stock Fund) will be held in the FCS Cash Account, earning a market rate of interest, until after the close of the Stock Offering at which time you can then reinvest your funds in any of the 401(k) Plan investments. If you do not reinvest your funds held in the FCS Cash Account within 30 days after the close of the Stock Offering, your funds will be automatically transferred to the Morley Stable Value Fund.

All plan participants can direct the trustee to subscribe for shares of Fairfield County common stock through the Fairfield County Stock Fund. However, your directions are subject to your subscription rights, purchase limitations and purchase priorities. See “Summary – Persons Who Can Order Stock in the Offering” in the attached prospectus. Fairfield County has granted rights to subscribe for shares of Fairfield County common stock to the following persons in the following order of priority: (1) persons with $50 or more on deposit at the Bank as of the close of business on December 31, 2008; (2) the Fairfield County Bank Employee Stock Ownership Plan; (3) persons with $50 or more on deposit at the Bank as of the close of business on March 31, 2010; and (4) depositors of the Bank as of the close of business on , 20 , who are not eligible under categories 1 and 3 above. If you fall into one of the above subscription offering categories, you have subscription rights to purchase shares of Fairfield County common stock in the Stock Offering and you may use your account balance in the 401(k) Plan to subscribe for shares of Fairfield County common stock.

The limitations on the total amount of Fairfield County common stock that you may purchase in the Stock Offering, as described in the prospectus (see “The Conversion and Stock Offering – Limitations on Purchases of Shares”), will be calculated based on the aggregate amount that you subscribed for: (a) through your 401(k) Plan account and (b) through your sources of funds outside of the 401(k) Plan. Whether you place an order through the 401(k) Plan, outside the 401(k) Plan, or both, the number of shares of Fairfield County common stock, if any, that you receive will be determined based on the total number of subscriptions, your purchase priority and the allocation priorities described in the prospectus. If, as a result of the calculation, you are allocated insufficient shares to fill all of your orders, available shares will be allocated between orders on a pro rata basis.

1

Table of Contents

Value of Participation Interests

As of March 1, 2010, the market value of the 401(k) Plan assets equaled approximately $27.0 million. The plan administrator distributed quarterly benefit statements to each participant reflecting the value of his or her beneficial interest in the 401(k) Plan as of March 31, 2010. The value of the 401(k) Plan assets represents past contributions made to the 401(k) Plan on your behalf, plus or minus earnings or losses on the contributions, less previous withdrawals.

In order to facilitate your investment in the Fairfield County Stock Fund in connection with the Stock Offering, you must complete, sign and submit the blue form included with this prospectus supplement (the “Investment Form”). In addition to the general purchaser information required on the Investment Form, you must indicate the following information: (1) the exact dollar amount that you would like to invest in the Fairfield County Stock Fund; (2) the type of subscription rights you have in the Stock Offering (if any); and (3) that the funds to be used to subscribe for shares of Fairfield County common stock, through the Fairfield County Stock Fund, will be debited from your interest in the FCS Cash Account as of June , 2010. You must transfer a sufficient amount of your 401(k) Plan assets to the FCS Cash Account before you submit the Investment Form to Tim Kidman in the Human Resources Department. You can facilitate the transfer of funds by accessing the USI Consulting website at www.usicg.com or calling the toll free benefits hotline at 1-866-305-8846. If you have never accessed your account through the USI Consulting website or if you forgot your login or password information, please call USI Consulting at 1-866-305-8846. If you have insufficient funds in the FCS Cash Account when you submit your Investment Form, your subscription order will be pro-rated based on the funds you have in the FCS Cash Account as of , 2010.

If you do not wish to invest in the Fairfield County Stock Fund at this time, you do not need to take any action. The minimum investment in the Fairfield County Stock Fund during the offering is $250 and the maximum individual investment is $1,000,000. All funds transferred into the FCS Cash Account during the Stock Offering cannot be transferred out of the FCS Cash Account until after the close of the Stock Offering.

Purchases After the Close of the Stock Offering

Following the close of the Stock Offering, you will be able to direct the investment of your 401(k) Plan funds and future deferrals into the Fairfield County Stock Fund through the internet or by phone. You will receive a separate prospectus after the close of the Stock Offering which will explain the terms and conditions of all future purchases of Fairfield County common stock through the Fairfield County Stock Fund.

The deadline to submit your Investment Form to Tim Kidman, in the Human Resources Department, is 5:00 pm local time, on June , 2010, unless extended by the Bank. If you have any questions regarding the Fairfield County Stock Fund, you can call Tim Kidman at (203) 431-7525.

Irrevocability of Transfer Direction

Once you have submitted your Investment Form, you cannot change your investment direction. Following the closing of the Stock Offering and the initial purchase of shares in the Fairfield County Stock Fund, you will again have complete access to any funds you directed towards the purchase of shares of Fairfield County common stock in the Stock Offering. Special restrictions may apply to transfers directed to and from the Fairfield County Stock Fund by participants who are subject to Section 16(b) of the Securities Exchange Act of 1934, as amended. See “SEC Reporting and Short-Swing Profit Liability.”

Purchase Price of Fairfield County Common Stock

The trustee will pay the same price for shares of Fairfield County common stock ($10.00 per share) as all other persons who purchase shares of Fairfield County common stock in the Stock Offering. If there is not enough

2

Table of Contents

common stock available in the Stock Offering to fill all subscriptions, the common stock will be apportioned and the trustee may not be able to purchase all of the common stock you requested. If the Stock Offering is oversubscribed and your order is cut back, your 401(k) Plan funds (which are not invested in Fairfield County common stock) remain in the FCS Cash Account earning market rates of interest until the close of the Stock Offering at which time you will be able to re-invest the funds in any of the 401(k) Plan investments.

Nature of a Participant’s Interest in Fairfield County Common Stock

Countybank, as the Fairfield County Stock Fund trustee, will hold Fairfield County common stock in the name of the 401(k) Plan. The trustee will credit shares of Fairfield County common stock acquired at your direction to your account under the 401(k) Plan. Your interest in the Fairfield County Stock Fund will be recorded in stock units. Immediately following the close of the Stock Offering, each stock unit will have the same value as a share of Fairfield County common stock. As future deferrals are invested in the Fairfield County Stock Fund, each stock unit will be comprised of a cash and stock component based on an overall liquidity target for the Fairfield County Stock Fund of 5.0%.

Voting and Tender Rights of Fairfield County Common Stock

The trustee will exercise voting and tender rights attributable to all Fairfield County common stock held in the Fairfield County Stock Fund, as directed by participants with interests in the Fairfield County Stock Fund. With respect to each matter as to which holders of Fairfield County common stock have a right to vote, you will have voting instruction rights that reflect your proportionate interest in the Fairfield County Stock Fund. The number of shares of Fairfield County common stock held in the Fairfield County Stock Fund voted for and against each matter will be proportionate to the number of voting instruction rights exercised. If there is a tender offer for Fairfield County common stock, the 401(k) Plan allots each participant a number of tender instruction rights reflecting each participant’s proportionate interest in the Fairfield County Stock Fund. The percentage of shares of Fairfield County common stock held in the Fairfield County Stock Fund that will be tendered will be the same as the percentage of the total number of tender instruction rights exercised in favor of the tender offer. The remaining shares of Fairfield County common stock held in the Fairfield County Stock Fund will not be tendered. The 401(k) Plan provides that participants will exercise their voting instruction rights and tender instruction rights on a confidential basis.

DESCRIPTION OF THE 401(k) PLAN

The Bank adopted the amended and restated 401(k) Plan effective January 1, 2010. The Bank intends for the 401(k) Plan to comply, in form and in operation, with all applicable provisions of the Internal Revenue Code and the Employee Retirement Income Security Act of 1974, as amended (“ERISA”). The Bank may amend the 401(k) Plan from time to time in the future to ensure continued compliance with these laws. The Bank may also amend the 401(k) Plan from time to time in the future to add, modify, or eliminate certain features of the plan, as it sees fit. Federal law provides you with various rights and protections as a participant in the 401(k) Plan, which is governed by ERISA. However, the Pension Benefit Guaranty Corporation does not guarantee your benefits under the 401(k) Plan.

Reference to Full Text of the Plan. The following portions of this prospectus supplement summarize the material provisions of the 401(k) Plan. The Bank qualifies this summary in its entirety by reference to the full text of the 401(k) Plan. You may obtain copies of the 401(k) Plan document, including any amendments to the plan and a summary plan description, by contacting Tim Kidman at (203) 431-7525. You should carefully read the 401(k) Plan documents to understand your rights and obligations under the 401(k) Plan.

You are eligible to participate in the 401(k) Plan for all plan purposes if you are 19 years of age or older and have completed 30 days of service with the Bank. Once you have satisfied the eligibility requirements, you will be automatically enrolled in the 401(k) Plan and 3% of your pay will be withheld from your paycheck, unless you affirmatively opt out of the Plan or elect to increase or decrease your deferral percentages.

3

Table of Contents

As of March 1, 2010, 322 of the 331 active eligible employees of the Bank participated in the 401(k) Plan.

Contributions Under the 401(k) Plan

Employee Pre-Tax Salary Deferrals. Subject to certain Internal Revenue Service limitations, the 401(k) Plan currently permits you to make pre-tax salary deferrals each payroll period of up to 100% of your compensation. For purposes of the plan, compensation is defined as your wages, bonus, commissions or other cash compensation paid to you by the Bank that is subject to tax withholding. In addition to pre-tax salary deferrals, you may make “catch up” contributions if you are currently age 50 or will be 50 before the end of the calendar year. You are always 100% vested in your elective deferrals.

Matching Contributions. The 401(k) Plan currently provides that the Bank will make matching contributions on behalf of each eligible participant with respect to each eligible participant’s elective deferrals. If you elect to defer funds into the 401(k) Plan, the Bank will match 50% of your elective deferrals up to 6% of your compensation. The Bank makes matching contributions only to those participants who actively defer a percentage of their compensation into the 401(k) Plan. Participants vest in their matching contributions at a rate of 25% after two years of service and 25% each year thereafter.

Discretionary Contributions. The 401(k) Plan provides that the Bank may make a discretionary contribution under the 401(k) Plan at the end of the plan year. The amount of the contribution is determined at the end of the plan year. In order to be eligible for the contribution you must be employed by the Bank on the last day of the plan year or terminate employment due to death, disability or retirement at age 65. In 2009, the Bank made a discretionary contribution to eligible participants equal to 3% of compensation. Participant’s vest in their discretionary contributions at a rate of 25% after two years of service and 25% each year thereafter.

Rollover Contributions. The Bank allows employees who receive a distribution from a previous employer’s tax-qualified employee benefit plan to deposit that distribution into a Rollover Contribution account under the 401(k) Plan, provided the rollover contribution satisfies IRS requirements. For additional information on Rollover Contributions see the Summary Plan Description for the 401(k) Plan.

Limitation on Employee Salary Deferrals. By law, your total deferrals under the 401(k) Plan, together with similar plans, may not exceed $16,500 for 2010. Eligible employees who are age 50 and over may also make additional “catch-up” contributions to the plan, up to a maximum of $5,500 for 2010. The Internal Revenue Service periodically increases these limitations. An eligible participant who exceeds these limitations must include any excess deferrals in gross income for federal income tax purposes in the year of deferral. In addition, the participant must pay federal income taxes on any excess deferrals when distributed by the 401(k) Plan to the participant, unless the plan distributes the excess deferrals and any related income no later than the first April 15th following the close of the taxable year in which the participant made the excess deferrals. Any income on excess deferrals distributed before such date is treated, for federal income tax purposes, as earned and received by the participant in the taxable year of the distribution.

Limitation on Annual Additions and Benefits. As required by the Internal Revenue Code, the 401(k) Plan provides that the total amount of contributions and forfeitures (annual additions) credited to a participant during any year under all defined contribution plans of the Bank (including the 401(k) Plan and the proposed the Fairfield County Community Bank Employee Stock Ownership Plan) may not exceed the lesser of 100% of the participant’s annual compensation or $49,000 for 2010.

Limitation on Plan Contributions for Highly Compensated Employees. Special provisions of the Internal Revenue Code limit the amount of pre-tax and matching contributions that may be made to the 401(k) Plan in any year on behalf of highly compensated employees, in relation to the amount of pre-tax and matching contributions made by or on behalf of all other employees eligible to participate in the 401(k) Plan. If pre-tax and matching contributions exceed these limitations, the plan must adjust the contribution levels for highly compensated employees.

4

Table of Contents

In general, a highly compensated employee includes any employee who (1) was a 5% owner of the sponsoring employer at any time during the year or the preceding year, or (2) had compensation for the preceding year in excess of $110,000 and, if the sponsoring employer so elects, was in the top 20% of employees by compensation for that year. The preceding dollar amount applies for 2010 and may be adjusted periodically by the Internal Revenue Service.

Top-Heavy Plan Requirements. If the 401(k) Plan is a “Top-Heavy Plan” for any calendar year, the Bank may be required to make certain minimum contributions to the 401(k) Plan on behalf of non-key employees. In general, the 401(k) Plan will be treated as a Top-Heavy Plan for any calendar year if, as of the last day of the preceding calendar year, the aggregate balance of the accounts of “Key Employees” exceeds 60% of the aggregate balance of the accounts of all employees under the plan. A Key Employee is generally any employee who, at any time during the calendar year or any of the four preceding years, is:

| (1) | an officer of the Bank whose annual compensation exceeds $160,000; |

| (2) | a 5% owner of the employer, meaning an employee who owns more than 5% of the outstanding stock of Fairfield County, or who owns stock that possesses more than 5% of the total combined voting power of all stock of Fairfield County; or |

| (3) | a 1% owner of the employer, meaning an employee who owns more than 1% of the outstanding stock of Fairfield County, or who owns stock that possesses more than 1% of the total combined voting power of all stock of Fairfield County, and whose annual compensation exceeds $150,000. |

The foregoing dollar amounts are for 2010.

Effective March 1, 2010, the 401(k) Plan offers the following investment choices:

| Annual Rates of Return as of December 31, | |||||||||

| Fund Name |

2009 | 2008 | 2007 | ||||||

| Morley Stable Value |

1.65 | % | 3.43 | % | 3.61 | ||||

| PIMCO Real Return Admin |

18.67 | (6.66 | ) | 11.31 | |||||

| American Funds Bond Fund of America |

14.91 | (12.33 | ) | 3.37 | |||||

| American Funds Income Fund of America |

24.51 | (28.85 | ) | 3.77 | |||||

| Russell LifePoints 2010 Strategy R3 |

22.75 | (21.88 | ) | 6.18 | |||||

| Russell LifePoints 2020 Strategy R3 |

26.02 | (29.22 | ) | 6.55 | |||||

| Russell LifePoints 2030 Strategy R3 |

29.87 | (39.32 | ) | 6.88 | |||||

| Russell LifePoints 2040 Strategy R3 |

30.01 | (39.72 | ) | 6.73 | |||||

| American Funds Investment Company of America |

27.18 | (34.73 | ) | 5.94 | |||||

| Vanguard 500 Index Investor |

26.49 | (37.02 | ) | 5.39 | |||||

| American Funds Growth Fund of America |

34.48 | (39.07 | ) | 10.95 | |||||

| American Funds New Economy A |

45.16 | (41.86 | ) | 11.39 | |||||

| Goldman Sachs Mid Cap Value A |

32.70 | (36.73 | ) | 2.91 | |||||

| T. Rowe Price Mid-Cap Growth |

45.46 | (39.69 | ) | 17.65 | |||||

| Oppenheimer Main Street Small Cap N |

36.55 | (38.41 | ) | (1.86 | ) | ||||

| American Funds Euro Pacific Growth A |

39.10 | (40.53 | ) | 18.96 | |||||

| American Funds New Perspective A |

37.43 | (37.83 | ) | 16.04 | |||||

5

Table of Contents

The Morley Stable Value fund is a collective investment fund consisting of a diversified portfolio of high quality stable value investment contracts issued by life insurance companies, banks and other financial institutions. The principal value of these assets remain stable regardless of stock and bond market fluctuations. The return is a blend of all the rates of the various investments purchased by the fund.

The PIMCO Real Return Admin seeks maximum real return. The fund normally invests at least 80% of net assets in inflation-indexed bonds of varying maturities. It invests primarily in investment-grade securities, but may invest up to 10% of total assets in high-yield securities (“junk bonds”). The fund may invest all of assets in derivative instruments. It is nondiversified.

The American Funds Bond Fund of America seeks current income consistent with preservation of capital. The fund normally invests at least 80% of assets in bonds. It normally invests at least 60% of assets in bonds and debt securities rated A or better at the time of purchase. The fund will not invest more than 40% of assets in other debt obligations, including lower rated bonds.

The American Funds Income Fund of America seeks current income; capital appreciation is secondary. The fund allocates among common and preferred stock, straight debt securities, convertibles, and cash equivalents. It normally maintains 60% of assets in equity-type securities. It may invest up to 20% of assets in debt securities rated Ba or below. The fund may invest up to 20% of assets in equity securities domiciled outside of the U.S. and 10% of assets in debt securities of non-U.S. issuers.

The Russell LifePoints 2010 Strategy fund seeks to provide capital growth and income consistent with its current asset allocation. The fund pursues this objective by investing in a diversified portfolio initially consisting of approximately 45% stock funds and 55% fixed income funds, with an increasing allocation to fixed income funds over time. Its allocation to fixed income funds will be fixed at 80% approximately 20 years after the year 2010.

The Russell LifePoints 2020 Strategy fund seeks to provide capital growth and income consistent with its current asset allocation. The fund pursues this objective by investing in a diversified portfolio initially consisting of approximately 55% stock funds and 45% fixed income funds, with an increasing allocation to fixed income funds over time. Its allocation to fixed income funds will be fixed at 80% approximately 20 years after the year 2020.

The Russell LifePoints 2030 Strategy fund seeks to provide capital growth and income consistent with its current asset allocation. The fund pursues this objective by investing in a diversified portfolio initially consisting of approximately 64% stock funds and 36% fixed income funds, with an increasing allocation to fixed income funds over time. Its allocation to fixed income funds will be fixed at 80% approximately 20 years after the year 2030.

The Russell LifePoints 2040 Strategy fund seeks to provide capital growth and income consistent with its current asset allocation. The fund pursues this objective by investing in a diversified portfolio initially consisting of approximately 72% stock funds and 28% fixed income funds, with an increasing allocation to fixed income funds over time. Its allocation to fixed income funds will be fixed at 80% approximately 20 years after the year 2040.

The American Funds Investment Company of America seeks long-term growth of capital and income. The fund invests primarily in common stocks. It may invest up to 15% of assets, at the time of purchase, in securities of issuers domiciled outside the United States and not included in Standard & Poor’s 500 Composite Index. The fund may also hold cash or money market instruments. There is no guarantee that the fund’s investment objective will be met.

The Vanguard 500 Index fund seeks investment results that correspond with the price and yield performance of the S&P 500 Index. The fund employs a passive management strategy designed to track the performance of the S&P 500 Index, which is dominated by the stocks of large U.S. companies. It attempts to replicate the target index by investing all or substantially all of its assets in the stocks that make up the index.

The American Funds Growth Fund of America seeks capital growth. The fund invests primarily in common stocks. Management selects securities that it believes are reasonably priced and represent solid long-term

6

Table of Contents

investment opportunities. The fund may invest up to 15% of assets in securities of issuers domiciled outside of the U.S. and Canada, and not included in the S&P 500 Index. It may also invest up to 10% of assets in debt securities rated below investment-grade.

The American Funds New Economy fund seeks long-term growth of capital; current income is secondary. The fund normally invests in equity securities of companies involved in the services sector. It primarily invests in common and preferred stocks, securities convertible into common stocks, and cash and equivalents. The fund may invest up to 40% of assets in securities of foreign issuers.

The Goldman Sachs Mid Cap fund is a core mid cap value fund that seeks long-term capital appreciation. The fund normally invests at least 80% of assets in equity securities, typically with market capitalizations within the range of the market capitalization of companies in the Russell MidCap Value Index.

The Fidelity Advisor Mid Cap fund seeks long-term growth of capital. The fund normally invests at least 80% of assets in companies with medium market capitalizations. These companies generally have market capitalizations that fall within the range of the S&P MidCap 400 Index. The fund will potentially invest in companies with smaller or larger market capitalizations. It may invest in domestic and foreign issuers, as well as growth stocks, value stocks, or both.

The T. Rowe Price Mid-Cap Growth fund seeks long-term capital appreciation. The fund normally invests at least 80% of assets in a diversified portfolio of common stocks of mid-cap companies whose earnings T. Rowe Price expects to grow at a faster rate than the average company. While it invests most assets in U.S. common stocks, the fund may also purchase other securities including foreign stocks, futures, and options.

The Oppenheimer Main Street Small Cap fund is a small cap blend fund that seeks capital appreciation. The fund normally invests at least 80% of assets in common stocks and other equity securities of small cap companies, defined by management as companies with market capitalization of $2.5 billion or less. It can invest in companies that have been in operation less than three years. However, management does not intend to invest more than 20% of assets in such companies.

The American Funds EuroPacific Growth fund is a foreign large blend fund that seeks long-term growth of capital. The fund normally invests at least 80% of assets in equity securities of issuers domiciled in Europe and the Pacific Basin. It may also hold cash or money market instruments.

The American Funds New Perspective seeks long-term growth of capital; income is a secondary consideration. The fund primarily invests in common stocks of foreign and U.S. companies. The advisor looks for worldwide changes in international trade patterns and economic and political relationships. It then searches for companies that may benefit from the new opportunities created by such changes. The advisor closely follows securities, industries, governments, and currency exchange markets worldwide.

The Fairfield County Stock Fund invests primarily in the common stock of Fairfield County. Participants in the 401(k) Plan may direct the trustee to invest all or a portion of their 401(k) Plan account balances in the Fairfield County Stock Fund during the Stock Offering.

The Fairfield County Stock Fund consists of investments in the common stock of Fairfield County made on the closing date of the Stock Offering. Your investment in the Fairfield County Stock Fund will be recorded using the unitized accounting method. If cash dividends are paid on Fairfield County common stock, the trustee will, to the extent practicable, use the dividends held in the Fairfield County Stock Fund to purchase shares of the common stock. Pending investment in the common stock, assets held in the Fairfield County Stock Fund will be placed in the short term investment component of the Fairfield County Stock Fund. The Stock Fund will maintain a 5% cash ratio target following the Stock Offering.

As of the date of this prospectus supplement, no shares of Fairfield County common stock have been issued or are outstanding, and there is no established market for Fairfield County common stock. Accordingly, there is no record of the historical performance of the Fairfield County Stock Fund. Performance of the Fairfield County Stock

7

Table of Contents

Fund depends on a number of factors, including the financial condition and profitability of the Bank and general stock market conditions. See “Risk Factors” in the attached prospectus.

Once you have submitted your Investment Form, you may not change your investment directions in the Stock Offering.

Benefits Under the 401(k) Plan

Vesting. All participants are 100% vested in their pre-tax elective deferrals. This means that participants have a non-forfeitable right to these funds and any earnings on the funds at all times. Participants vest in their matching and discretionary contributions at a rate of 25% after the second year of employment with the Bank and 25% each year thereafter.

Withdrawals and Distributions from the 401(k) Plan

Withdrawals Before Termination of Employment. While in active service, participants may take loans and in-service withdrawals from the 401(k) Plan (subject to the restrictions set forth in the 401(k) Plan and the Bank loan policy). Participants may have no more then three (3) loans outstanding at anytime, other than those grandfathered pursuant to the terms of the loan policy.

Distribution Upon Termination for Any Other Reason. If a participant’s accounts are $1,000 or less upon termination of employment, payment will be in the form of a lump sum as of a valuation date as soon thereafter as administratively possible.

Nonalienation of Benefits. Except with respect to federal income tax withholding, and as provided for under a qualified domestic relations order, benefits payable under the 401(k) Plan will not be subject in any manner to anticipation, alienation, sale, transfer, assignment, pledge, encumbrance, charge, garnishment, execution, or levy of any kind, either voluntary or involuntary, and any attempt to anticipate, alienate, sell, transfer, assign, pledge, encumber, charge or otherwise dispose of any rights to benefits payable under the 401(k) Plan will be void.

Applicable federal tax law requires the 401(k) Plan to impose substantial restrictions on your right to withdraw amounts held under the 401(k) Plan before your termination of employment with the Bank. Federal law may also impose an excise tax on withdrawals from the 401(k) Plan before you attain 59 1/2 years of age, regardless of whether the withdrawal occurs during your employment with the Bank or after termination of employment.

ADMINISTRATION OF THE 401(k) PLAN

The board of directors of the Bank has appointed Countybank to serve as trustee for the Fairfield County Stock Fund. The Personnel and Compensation Committee of the Board of Directors of the Company serves as the trustee for all other 401(k) Plan assets. The trustees receive, hold and invest the contributions to the 401(k) Plan in trust and distribute them to participants and beneficiaries in accordance with the terms of the 401(k) Plan and the directions of the Plan Administrator. The trustees are responsible for the investment of the trust assets, as directed by the Plan Administrator and the participants.

Reports to 401(k) Plan Participants

The Plan Administrator furnishes participants quarterly statements that show the balance in their accounts as of the statement date, contributions made to their accounts during that period and any additional adjustments required to reflect earnings or losses.

8

Table of Contents

The Bank acts as Plan Administrator for the 401(k) Plan. The Plan Administrator handles the following administrative functions: interpreting the provisions of the plan, prescribing procedures for filing applications for benefits, preparing and distributing information explaining the plan, maintaining plan records, books of account and all other data necessary for the proper administration of the plan, preparing and filing all returns and reports required by the U.S. Department of Labor and the IRS and making all required disclosures to participants, beneficiaries and others under ERISA.

The Bank expects to continue the 401(k) Plan indefinitely. Nevertheless, the Bank may terminate the 401(k) Plan at any time. If the Bank terminates the 401(k) Plan in whole or in part, all affected participants become fully vested in their accounts, regardless of other provisions of the 401(k) Plan. The Bank reserves the right to make, from time to time, changes which do not cause any part of the trust to be used for, or diverted to, any purpose other than the exclusive benefit of participants or their beneficiaries. The Bank may amend the plan, however, as necessary or desirable, in order to comply with ERISA or the Internal Revenue Code.

Merger, Consolidation or Transfer

If the 401(k) Plan merges or consolidates with another plan or transfers the trust assets to another plan, and either the 401(k) Plan or the other plan is subsequently terminated, the 401(k) Plan requires that you receive a benefit immediately after the merger, consolidation or transfer that would equal or exceed the benefit you would have been entitled to receive immediately before the merger, consolidation or transfer, if the 401(k) Plan had terminated at that time.

Federal Income Tax Consequences

The following briefly summarizes the material federal income tax aspects of the 401(k) Plan. You should not rely on this summary as a complete or definitive description of the material federal income tax consequences of the 401(k) Plan. Statutory provisions change, as do their interpretation, and their application may vary in individual circumstances. Finally, applicable state and local income tax laws may have different tax consequences than the federal income tax laws. 401(k) Plan participants should consult a tax advisor with respect to any transaction involving the 401(k) Plan, including any distribution from the 401(k) Plan.

As a “tax-qualified retirement plan,” the Internal Revenue Code affords the 401(k) Plan certain tax advantages, including the following:

| (1) | the sponsoring employer may take an immediate tax deduction for the amount contributed to the plan each year; |

| (2) | participants pay no current income tax on amounts contributed by the employer on their behalf; and |

| (3) | earnings of the plan are tax-deferred, thereby permitting the tax-deferred accumulation of income and gains on investments. |

The Bank administers the 401(k) Plan to comply in operation with the requirements of the Internal Revenue Code as of the applicable effective date of any change in the law. If the Bank should receive an adverse determination letter from the Internal Revenue Service regarding the 401(k) Plan’s tax exempt status, all participants would generally recognize income equal to their vested interests in the 401(k) Plan, the participants would not be permitted to transfer amounts distributed from the 401(k) Plan to an Individual Retirement Account or to another qualified retirement plan, and the Bank would be denied certain tax deductions taken in connection with the 401(k) Plan.

9

Table of Contents

Lump Sum Distribution. A distribution from the 401(k) Plan to a participant or the beneficiary of a participant qualifies as a lump sum distribution if it is made within one taxable year, on account of the participant’s death, disability or separation from service, or after the participant attains age 59 1/2; and consists of the balance credited to the participant under this plan and all other profit sharing plans, if any, maintained by the Bank. The portion of any lump sum distribution included in taxable income for federal income tax purposes consists of the entire amount of the lump sum distribution, less the amount of after-tax contributions, if any, made to any other profit-sharing plans maintained by the Bank, if the distribution includes those amounts.

Fairfield County Common Stock Included in Lump Sum Distribution. If a lump sum distribution includes Fairfield County common stock, the distribution generally is taxed in the manner described above. The total taxable amount is reduced, however, by the amount of any net unrealized appreciation on Fairfield County common stock; that is, the excess of the value of Fairfield County common stock at the time of the distribution over the cost or other basis of the securities to the trust. The tax basis of Fairfield County common stock, for purposes of computing gain or loss on a subsequent sale, equals the value of Fairfield County common stock at the time of distribution, less the amount of net unrealized appreciation. Any gain on a subsequent sale or other taxable disposition of Fairfield County common stock, to the extent of the net unrealized appreciation at the time of distribution, is long-term capital gain, regardless of how long you hold the Fairfield County common stock, or the “holding period.” Any gain on a subsequent sale or other taxable disposition of Fairfield County common stock that exceeds the amount of net unrealized appreciation upon distribution is considered long-term capital gain, regardless of the holding period. The recipient of a distribution may elect to include the amount of any net unrealized appreciation in the total taxable amount of the distribution, to the extent allowed under IRS regulations.

We have provided you with a brief description of the material federal income tax aspects of the 401(k) Plan that are generally applicable under the Internal Revenue Code. We do not intend this description to be a complete or definitive description of the federal income tax consequences of participating in or receiving distributions from the 401(k) Plan. Accordingly, you should consult a tax advisor concerning the federal, state and local tax consequences of participating in and receiving distributions from the 401(k) Plan.

Any “affiliate” of Fairfield County under Rules 144 and 405 of the Securities Act of 1933, as amended, who receives a distribution of common stock under the 401(k) Plan, may re-offer or resell such shares only under a registration statement filed under the Securities Act of 1933, as amended, assuming the availability of a registration statement, or under Rule 144 or some other exemption from these registration requirements. An “affiliate” of Fairfield County is someone who directly or indirectly, through one or more intermediaries, controls, is controlled by, or is under common control with, Fairfield County. Generally, a director, principal officer or major shareholder of a corporation is deemed to be an “affiliate” of that corporation.

Any person who may be an “affiliate” of Fairfield County may wish to consult with counsel before transferring any common stock they own. In addition, participants should consult with counsel regarding the applicability to them of Section 16 of the Securities Exchange Act of 1934, as amended, which may restrict the sale of Fairfield County common stock acquired under the 401(k) Plan or other sales of Fairfield County common stock.

Persons who are not deemed to be “affiliates” of Fairfield County at the time of resale may resell freely any shares of Fairfield County common stock distributed to them under the 401(k) Plan, either publicly or privately, without regard to the registration and prospectus delivery requirements of the Securities Act of 1933, as amended, or compliance with the restrictions and conditions contained in the exemptions available under federal law. A person deemed an “affiliate” of Fairfield County at the time of a proposed resale may publicly resell common stock only under a “re-offer” prospectus or in accordance with the restrictions and conditions contained in Rule 144 of the Securities Act of 1933, as amended, or some other exemption from registration, and may not use this prospectus supplement or the accompanying prospectus in connection with any such resale. In general, Rule 144 restricts the amount of common stock which an affiliate may publicly resell in any three-month period to the greater of one percent of Fairfield County common stock then outstanding or the average weekly trading volume reported on the Nasdaq Capital Market during the four calendar weeks before the sale. Affiliates may sell only through brokers

10

Table of Contents

without solicitation and only at a time when Fairfield County is current in filing all required reports under the Securities Exchange Act of 1934, as amended.

SEC Reporting and Short-Swing Profit Liability

Section 16 of the Securities Exchange Act of 1934, as amended, imposes reporting and liability requirements on officers, directors and persons who beneficially own more than 10% of public companies such as Fairfield County. Section 16(a) of the Securities Exchange Act of 1934, as amended, requires the filing of reports of beneficial ownership. Within ten days of becoming a person required to file reports under Section 16(a), such person must file a Form 3 reporting initial beneficial ownership with the Securities and Exchange Commission (“SEC”). Such persons must also report periodically certain changes in beneficial ownership involving the allocation or reallocation of assets held in their 401(k) Plan accounts, either on a Form 4 within two business days after a transaction, or annually on a Form 5 within 45 days after the close of a company’s fiscal year.

In addition to the reporting requirements described above, Section 16(b) of the Securities Exchange Act of 1934, as amended, provides for the recovery by Fairfield County of profits realized from the purchase and sale or sale and purchase of its common stock within any six-month period by any officer, director or person who beneficially owns more than 10% of the common stock.

The SEC has adopted rules that exempt many transactions involving the 401(k) Plan from the “short-swing” profit recovery provisions of Section 16(b). The exemptions generally involve restrictions upon the timing of elections to buy or sell employer securities for the accounts of any officer, director or person who beneficially owns more than 10% of the common stock of a company.

Except for distributions of the common stock due to death, disability, retirement, termination of employment or under a qualified domestic relations order, persons who are subject to Section 16(b) may be required, under limited circumstances involving the purchase of common stock within six months of the distribution, to hold the shares of common stock distributed from the 401(k) Plan for six months after the distribution date.

The validity of the issuance of the common stock of Fairfield County will be passed upon by Kilpatrick Stockton LLP, Washington, DC. Kilpatrick Stockton LLP is acting as special counsel for Fairfield County in connection with the Stock Offering.

11

Table of Contents

FAIRFIELD COUNTY BANK INCENTIVE RETIREMENT PLAN (“401(k) PLAN”)

INVESTMENT FORM

| Name of Plan Participant: | ||

| Social Security Number: |

||

1. Instructions. If you would like to use your 401(k) Plan funds to subscribe for shares of Fairfield County Bank Corp. common stock in the Fairfield County Bank Corp. initial public offering (“Stock Offering”), you must complete, sign and submit this form to the Human Resources Department no later than 5:00 p.m. on June , 2010. A representative for the Plan Administrator will retain a copy of this form and return a copy to you. If you need any assistance in completing this form, please contact Tim Kidman in Human Resources. If you do not complete and return this form to the Human Resources Department by 5:00 p.m. on , , 2010, you will not be able to subscribe for shares of Fairfield County Bank Corp. common stock (“Common Stock”) in the Stock Offering through the 401(k) Plan.

2. Investment Directions. I hereby direct the trustee to debit $ from the dollars I have transferred to the Fairfield County Stock Cash Account (“FCS Cash Account”) to subscribe for and purchase shares of Common Stock through the Fairfield County Stock Fund. I understand that the amount I direct the trustee to debit from the FCS Cash Account must be divisible by $10.00. I further understand that all funds I wish to use to subscribe for shares of Fairfield County common stock through the Fairfield County Stock Fund must be transferred to the FCS Cash Account in the 401(k) Plan by June , 2010 and that I may not transfer funds out of FCS Cash Account until after the close of the Stock Offering.

The minimum investment in the Stock Offering is $250 and the maximum investment is $1,000,000.

3. Purchaser Information. The ability of a 401(k) Plan participant to purchase common stock through the Fairfield County Stock Fund is based on the participant’s subscription rights and purchase limitations. Please indicate your status by checking the appropriate boxes below.

| ¨ | Check here if you had $50.00 or more on deposit with Fairfield County Bank as of the close of business on December 31, 2008. |

| ¨ | Check here if you had $50.00 or more on deposit with Fairfield County Bank as of the close of business on March 31, 2010. |

| ¨ | Check here if you are a depositor of Fairfield County Bank as of the close of business on , 20 , who are not eligible under the categories listed above. |

| ¨ | Check here if none of the above apply. |

4. Acknowledgment of Plan Participant. I understand that this Investment Form shall be subject to all of the terms and conditions of the Plan. I acknowledge that I have received a copy of the Prospectus and the Prospectus Supplement.

| Signature of Participant | Date |

| Acknowledgment of Receipt by the Plan Administrator. This Investment Form was received by the Plan Administrator and will become effective on the date noted below. | ||||||

| By: | ||||||

| Date | ||||||

12

Table of Contents

THE PARTICIPATION INTERESTS REPRESENTED BY THE COMMON STOCK OFFERED HEREBY ARE NOT DEPOSIT ACCOUNTS AND ARE NOT INSURED BY THE BANK INSURANCE FUND OR THE SAVINGS ASSOCIATION INSURANCE FUND OF THE FEDERAL DEPOSIT INSURANCE CORPORATION OR ANY OTHER GOVERNMENT AGENCY AND ARE NOT GUARANTEED BY FAIRFIELD COUNTY BANK OR FAIRFIELD COUNTY BANK CORP. THE COMMON STOCK IS SUBJECT TO AN INVESTMENT RISK, INCLUDING THE POSSIBLE LOSS OF THE PRINCIPAL INVESTED.

PLEASE COMPLETE AND RETURN TO

TIM KIDMAN IN

THE HUMAN RESOURCES DEPARTMENT

AT FAIRFIELD COUNTY BANK

BY 5:00 P.M. ON JUNE , 2010.

13

Table of Contents

| PROSPECTUS | [LOGO] |

Fairfield County Bank Corp.

(Holding Company for Fairfield County Bank)

Up to 5,945,500 Shares of Common Stock

This is the initial public offering of shares of common stock of Fairfield County Bank Corp. The shares we are offering will represent 47.0% of our outstanding common stock. Fairfield County Bank, MHC, our federally chartered mutual holding company parent, will own 53.0% of our outstanding common stock. Upon completion of the offering, we expect that shares of our common stock will be quoted on the Nasdaq Global Market under the symbol “FFBK.”

If you are or were a depositor of Fairfield County Bank:

| • | You may have priority rights to purchase shares of common stock. |

If you are a participant in the Fairfield County Bank Incentive Retirement Plan (the “401(k) Plan”):

| • | You may direct that all or part of your 401(k) Plan account balance be invested in shares of Fairfield County Bank Corp. common stock. |

| • | You will receive a separate supplement to this prospectus that describes your rights under the 401(k) Plan. |

If you fit none of the categories above, but are interested in purchasing shares of our common stock:

| • | You may have an opportunity to purchase shares of common stock after priority orders are filled. |

We are offering up to 5,945,500 shares of common stock for sale on a best efforts basis, subject to certain conditions. We must issue a minimum of 4,394,500 shares to complete the offering. If, as a result of regulatory considerations, demand for the shares or changes in market conditions, the independent appraiser determines our market value has increased, we may sell up to 6,837,325 shares without giving you further notice or the opportunity to change or cancel your order.

The offering is scheduled to terminate at 4:00 p.m., Eastern time, on , 2010. We may extend this termination date without notice to you until , 2010, unless the Office of Thrift Supervision approves a later date. Funds received before completion of the offering will be maintained at Fairfield County Bank or, at our discretion, in an escrow account at an independent insured depository institution. All subscriptions received will earn interest at our passbook savings rate, which is currently 0.35% per annum but which is subject to change at any time.

The minimum purchase is 25 shares. Once submitted, orders are irrevocable unless the offering is terminated or extended beyond , 2010. If we extend the offering beyond , 2010, we will promptly return the funds of all subscribers who do not reconfirm their subscriptions. If we terminate the offering because we fail to sell the minimum number of shares or for any other reason, we will promptly return your funds with interest.

Sandler O’Neill & Partners, L.P. will use its best efforts to assist us in our selling efforts, but is not required to purchase any of the common stock that is offered for sale. Purchasers will not pay a commission to purchase shares of common stock in the offering. All shares offered for sale are offered at a price of $10.00 per share.

We expect our current directors and executive officers, together with their associates, to subscribe for 731,000 shares, which equals an aggregate 12.3% of the shares offered for sale at the maximum of the offering range.

The Office of Thrift Supervision conditionally approved our plan of stock issuance on , 2010. However, such approval does not constitute a recommendation or endorsement of this offering.

This investment involves a degree of risk, including the possible loss of principal.

Please read “Risk Factors” beginning on page 15.

OFFERING SUMMARY

Price Per Share: $10.00

| Minimum | Maximum | Maximum As Adjusted | |||||||

| Number of shares |

4,394,500 | 5,945,500 | 6,837,325 | ||||||

| Gross cash offering proceeds |

$ | 43,945,000 | $ | 59,455,000 | $ | 68,373,250 | |||

| Estimated offering expenses, excluding selling agent fees |

$ | 1,416,400 | $ | 1,416,400 | $ | 1,416,400 | |||

| Estimated selling agent fees (1) |

$ | 340,000 | $ | 482,000 | $ | 564,000 | |||

| Estimated net cash proceeds |

$ | 42,188,600 | $ | 57,556,600 | $ | 66,392,850 | |||

| Estimated net cash proceeds per share |

$ | 9.60 | $ | 9.68 | $ | 9.71 | |||

| (1) | Does not include fees to be paid to broker-dealers in the event a syndicated offering is conducted. See “The Stock Offering—Marketing Arrangements” on page . |

These securities are not deposits or savings accounts and are not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency.

Neither the Securities and Exchange Commission, the Office of Thrift Supervision nor any state securities regulator has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

Sandler O’Neill + Partners, L.P.

The date of this prospectus is , 2010

Table of Contents

Table of Contents

| Page | ||

| 1 | ||

| 15 | ||

| 24 | ||

| 25 | ||

| 27 | ||

| 35 | ||

| 37 | ||

| 37 | ||

| 38 | ||

| 39 | ||

| 40 | ||

| 45 | ||

| Management’s Discussion and Analysis of Results of Operations and Financial Condition |

57 | |

| 88 | ||

| 104 | ||

| 105 | ||

| 114 | ||

| 116 | ||

| 132 | ||

| 136 | ||

| 137 | ||

| 137 | ||

| 137 | ||

| 137 | ||

| 137 | ||

| 139 |

Table of Contents

This summary highlights material information from this document and may not contain all the information that is important to you. To understand the stock offering fully, you should read this entire document carefully. For assistance, please call our Stock Information Center at .

The Companies

Fairfield County Bank, MHC

Fairfield County Bank Corp.

Fairfield County Bank

Fairfield County Bank, MHC is our federally chartered mutual holding company parent. On January 1, 2007, Fairfield County Bank reorganized into the mutual holding company structure and became the wholly owned subsidiary of Fairfield County Bank, MHC. As a mutual holding company, Fairfield County Bank, MHC is a non-stock company. Upon completion of the offering, Fairfield County Bank, MHC will own 53.0% of Fairfield County Bank Corp.’s common stock. So long as Fairfield County Bank, MHC exists, it will own a majority of the voting stock of Fairfield County Bank Corp. and, through its board of directors, will be able to exercise voting control over most matters put to a vote of stockholders. Following the offering, Fairfield County Bank, MHC is not expected to engage in any business activity other than owning a majority of the common stock of Fairfield County Bank Corp. The officers of Fairfield County Bank, MHC are also the officers of Fairfield County Bank Corp. The directors of Fairfield County Bank, MHC are the directors of Fairfield County Bank Corp. and Fairfield County Bank.

Fairfield County Bank Corp. is being organized as our federally chartered mid-tier stock holding company in connection with the minority stock issuance. This offering is made by Fairfield County Bank Corp. Fairfield County Bank Corp. will own all of Fairfield County Bank’s capital stock and will direct, plan and coordinate Fairfield County Bank’s business activities.

Fairfield County Bank is a Connecticut chartered savings bank that operates from 23 full-service locations in Fairfield County, Connecticut and has served the needs of its local community since 1871. We offer a variety of deposit and loan products to individuals, businesses and local real estate developers, most of which are located in our primary market of Fairfield County. At December 31, 2009, Fairfield County Bank had assets of $1.6 billion, deposits of $1.3 billion and total equity of $138.2 million.

Our executive offices are located at 150 Danbury Road, Ridgefield, Connecticut 06877, and our telephone number there is (203) 438-6518. Our website address is www.fairfieldcountybank.com. Information on our website should not be considered a part of this prospectus.

1

Table of Contents

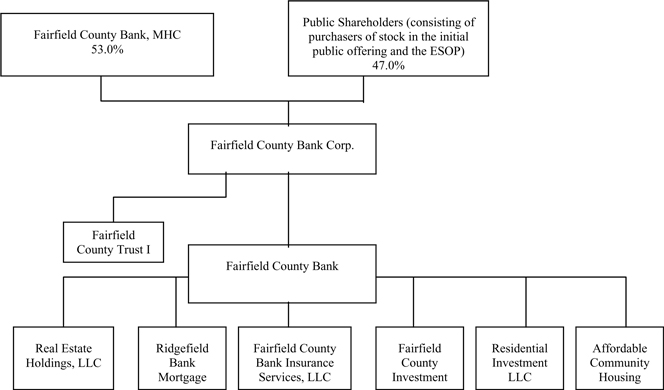

Our Corporate Structure

Our corporate structure after the offering is illustrated below:

Our Business Strategy (page )

Our current management team has largely been in place for many years, and our Chairman of the Board and Chief Executive Officer have served in their respective roles for over 20 years. During that time, we have focused on building a profitable, community-oriented financial institution offering outstanding service, added convenience and the products and services our customers require to meet their dynamic financial needs. Our objective is to continue this focus, and our strategies for achieving the objective include the following:

| • | continued growth of our diversified lending portfolio; |

| • | maintaining a strong emphasis on asset quality; |

| • | capturing our customers’ financial relationship; |

| • | leveraging our existing operating structure; and |

| • | managing our balance sheet risk. |

Regulation and Supervision (page )

Fairfield County Bank, MHC and Fairfield County Bank Corp. are subject to regulation, supervision and examination by the Office of Thrift Supervision. Fairfield County Bank is subject to regulation by the Connecticut Department of Banking and the Federal Deposit Insurance Corporation.

2

Table of Contents

The Offering

Offering Range

We are offering shares of Fairfield County Bank Corp. common stock for sale pursuant to an offering range that is based upon an independent appraisal of our pro forma market value and that has been approved by our board of directors. We are offering 4,394,500 shares of common stock for sale at the minimum of the offering range, 5,170,000 shares of common stock for sale at the midpoint of the offering range and 5,945,500 shares of common stock for sale at the maximum of the offering range. We must issue a minimum of 4,394,500 shares to complete the offering. If, as a result of regulatory considerations, demand for the shares or changes in market conditions, our independent appraiser determines that our pro forma market value has increased, we may increase the maximum of the offering range by 15% and sell up to 6,837,325 shares of common stock in the offering.

Purchase Price

The purchase price is $10.00 per share. You will not pay a commission to buy any shares in the offering.

Number of Shares to be Sold

We are offering for sale between 4,394,500 and 5,945,500 shares of Fairfield County Bank Corp. common stock in this offering. The amount of capital being raised is based on an independent appraisal of Fairfield County Bank Corp. Most of the terms of this offering are required by Office of Thrift Supervision regulations. With regulatory approval, we may increase the number of shares to be issued to 6,837,325 shares without giving you further notice or the opportunity to change or cancel your order. In considering whether to increase the offering size, the Office of Thrift Supervision will consider the level of subscriptions, the views of our independent appraiser, our financial condition and results of operations and changes in market conditions.

How We Determined the Offering Range (page )

We decided to offer between 4,394,500 and 5,945,500 shares, which is our offering range, based on an independent appraisal of our pro forma market value prepared by FinPro, Inc., an appraisal firm experienced in appraisals of financial institutions. FinPro will receive fees totaling $70,000 for the preparation and delivery of the original appraisal report, plus reimbursement of out-of-pocket expenses and $6,500 for the preparation and delivery of each required updated appraisal report. FinPro estimates that as of March 2, 2010, our pro forma market value on a fully converted basis, which includes the total number of shares that will be issued by Fairfield County Bank Corp. to Fairfield County Bank, MHC and the total number of shares that will be sold in the offering, was between $93.5 million and $126.5 million, with a midpoint of $110.0 million. The term “fully converted” means that FinPro assumed that 100% of our common stock had been sold to the public, rather than the 47.0% of the total outstanding stock that will be sold to the public in the offering. The percentage of stock that will be held publicly by individuals and entities other than Fairfield County Bank, MHC will be 47.0%, regardless of whether the shares in the offering are sold at the minimum, midpoint, maximum or maximum, as adjusted, of the offering range.

Office of Thrift Supervision regulations require that Fairfield County Bank, MHC own at least 50.1% of Fairfield County Bank Corp.’s outstanding common stock after the completion of the offering. Based upon our pro forma market value, and taking into consideration the need to ensure that less than 49.9% of the total shares that will be issued by us will be issued to individuals and entities other than Fairfield County Bank, MHC, the board of directors determined how many shares would be issued in the offering. For a more detailed discussion of how many shares will be issued in connection with the offering, see “Pro Forma Data—Analysis of Pro Forma Outstanding Shares of Fairfield County Bank Corp. Common Stock.”

In preparing its appraisal, FinPro considered the information in this prospectus, including our consolidated financial statements. FinPro also considered the following factors, among others:

| • | our historical, present and projected operating results and financial condition and the economic and demographic characteristics of our market area; |

3

Table of Contents

| • | a comparative evaluation of the operating and financial statistics of Fairfield County Bank with those of other similarly-situated, publicly-traded savings associations and savings association holding companies; |

| • | the effect of the capital raised in this offering on our stockholders’ equity and earnings potential; and |

| • | the trading market for securities of comparable institutions and general economic conditions in the market for such securities. |

Our board of directors determined that the common stock should be sold at $10.00 per share and that a maximum of 5,945,500 shares of our common stock should be issued through the sale of common stock to the public through the offering.

Two measures that some investors use to analyze whether a stock might be a good investment are the ratio of the offering price to the issuer’s “tangible book value” and the ratio of the offering price to the issuer’s annual core earnings. FinPro considered these ratios in preparing its appraisal, among other factors. Tangible book value is the same as total equity, less intangibles, and represents the difference between the issuer’s tangible assets and liabilities. Core earnings, for purposes of the appraisal, was defined as net earnings after taxes, excluding the after-tax portion of income from nonrecurring items. FinPro’s appraisal also incorporates an analysis of a peer group consisting of the following publicly-traded mutual holding companies that FinPro considered to be comparable to us.

| Ticker |

Name |

Exchange | City | State | ||||

| BFSB | Brooklyn Federal Bancorp, Inc. (MHC) | NASDAQ | Brooklyn | NY | ||||

| CSBK | Clifton Savings Bancorp, Inc. (MHC) | NASDAQ | Clifton | NJ | ||||

| MGYR | Magyar Bancorp, Inc. (MHC) | NASDAQ | New Brunswick | NJ | ||||

| MLVF | Malvern Federal Bancorp, Inc. (MHC) | NASDAQ | Paoli | PA | ||||

| EBSB | Meridian Interstate Bancorp, Inc. (MHC) | NASDAQ | East Boston | MA | ||||

| NECB | Northeast Community Bancorp, Inc. (MHC) | NASDAQ | White Plains | NY | ||||

| NFBK | Northfield Bancorp, Inc. (MHC) | NASDAQ | Avenel | NJ | ||||

| PBIP | Prudential Bancorp, Inc. of Pennsylvania (MHC) | NASDAQ | Philadelphia | PA | ||||

| RCKB | Rockville Financial, Inc. (MHC) | NASDAQ | Vernon Rockville | CT | ||||

| SIFI | SI Financial Group, Inc. (MHC) | NASDAQ | Willimantic | CT |

In selecting the peer group companies, FinPro limited the group to mutual holding companies located in the Mid-Atlantic and Northeastern regions of the United States whose common stock is traded on a national securities exchange. The group was further limited by asset size and percentage of publicly-held outstanding shares. Mutual holding companies that were in the process of a second step conversion were excluded from the group.

4

Table of Contents

The following table presents a summary of selected pricing ratios for us and the peer group companies, which were all “first step” mutual holding companies, utilized by FinPro in its appraisal. These ratios are based on core earnings for the 12 months ended December 31, 2009 and book value as of December 31, 2009 and are shown on a fully-converted equivalent basis.

| Price to Core Earnings Multiple |

Price to Book Value Ratio |

Price to Tangible to Book Value Ratio |

||||||

| Fairfield County Bank Corp. (pro forma): |

||||||||

| Minimum |

38.46x | 42.83 | % | 44.48 | % | |||

| Midpoint |

43.48x | 47.28 | % | 49.00 | % | |||

| Maximum |

50.00x | 51.20 | % | 52.94 | % | |||

| Maximum, as adjusted |

55.56x | 55.19 | % | 56.95 | % | |||

| Peer group companies as of March 2, 2010: |

||||||||

| Average |

67.58x | 70.46 | % | 71.09 | % | |||

| Median |

51.63x | 69.27 | % | 69.27 | % |

Compared to the median pricing ratios of the peer group at the maximum of the offering range, our stock would be priced at a premium of 1.94% to the peer group on a price-to-earnings basis, a discount of 26.09% to the peer group on a price-to-book basis and a discount of 23.57% to the peer group on a price-to-tangible book basis. This means that, at the maximum of the offering range, a share of our common stock would be more expensive than the peer group based on an earnings per share basis and less expensive than the peer group based on a book value per share basis and a tangible book value per share basis.

The independent appraisal does not indicate market value. You should not assume or expect that the valuation described above means that our common stock will trade at or above the $10.00 purchase price after the public offering.

Mutual Holding Company Data

The following table presents a summary of selected pricing ratios for publicly traded mutual holding companies and the pricing ratios for us, without the ratios being adjusted to the hypothetical case of being fully converted.

| Non-Fully Converted Price to Core Earnings Multiple |

Non-Fully Converted Price to Book Value Ratio |

Non-Fully Converted Price to Tangible Book Value |

||||||

| Fairfield County Bank Corp. (pro forma): |

||||||||

| Minimum |

45.45x | 53.48 | % | 56.09 | % | |||

| Midpoint |

52.63x | 60.61 | % | 63.41 | % | |||

| Maximum |

58.82x | 67.20 | % | 70.22 | % | |||

| Maximum, as adjusted |

66.67x | 74.24 | % | 77.46 | % | |||

| Peer group companies as of March 2, 2010 (1): |

||||||||

| Average |

62.39x | 116.10 | % | 118.08 | % | |||

| Median |

52.90x | 120.00 | % | 120.00 | % |

| (1) | The information for publicly traded mutual holding companies may not be meaningful for investors because it presents average and median information for mutual holding companies that issued a different percentage of their stock in their offerings than the 47.0% that we are selling to the public in the offering. In addition, the effect of stock repurchases also affects the ratios to a greater or lesser degree depending upon repurchase activity. |

Possible Change in Offering Range (page )

FinPro will update its appraisal before we complete the offering. If, as a result of regulatory considerations, demand for the shares or changes in market conditions, FinPro determines that our pro forma market value has increased, we may sell up to 6,837,325 shares without further notice to you. If our pro forma market value at that time is either below $93.5 million or above $145.5 million, then, after consulting with the Office of Thrift

5

Table of Contents

Supervision, we may: terminate the stock offering and promptly return all funds; set a new offering range and give all subscribers the opportunity to modify or rescind their purchase orders for shares of Fairfield County Bank Corp.’s common stock; or take such other actions as may be permitted by the Office of Thrift Supervision and the Securities and Exchange Commission.

Possible Termination of the Offering

We must sell a minimum of 4,394,500 shares to complete the offering. If we terminate the offering because we fail to sell the minimum number of shares or for any other reason, we will promptly return your funds with interest at our passbook savings rate.

After-Market Performance of “First-Step” Mutual Holding Company Offerings