Attached files

| file | filename |

|---|---|

| EX-3.2 - Formula Acquisition Corp. | v183119_ex3-2.htm |

| EX-5.1 - Formula Acquisition Corp. | v183119_ex5-1.htm |

| EX-4.1 - Formula Acquisition Corp. | v183119_ex4-1.htm |

| EX-23.1 - Formula Acquisition Corp. | v183119_ex23-1.htm |

| EX-10.1 - Formula Acquisition Corp. | v183119_ex10-1.htm |

| EX-3.1(I) - Formula Acquisition Corp. | v183119_ex3-1i.htm |

| EX-3.1(II) - Formula Acquisition Corp. | v183119_ex3-1ii.htm |

As

filed with the Securities and Exchange Commission on __________,

2010

File

No. 333-________

UNITED

STATES SECURITIES AND EXCHANGE COMMISSION

Washington,

D.C. 20549

FORM

S-1

REGISTRATION

STATEMENT

UNDER

THE

SECURITIES ACT OF 1933

_____________________

FORMULA

ACQUISITION CORP.

(Exact

Name of Registrant as Specified in its Charter)

|

Delaware

|

6770

|

27-2320482

|

||

|

(State

or Other Jurisdiction of

Incorporation

or Organization)

|

(Primary

Standard Industrial

Classification

Code Number)

|

(I.R.S.

Employer

Identification

Number)

|

15

Broad Street, Suite 2624

New

York, NY 10005

(Address,

Including Zip Code, and Telephone Number, Including Area Code, of Registrant’s

Principal Executive Offices)

______________________________

Thomas

J. Clarke, Jr., Chairman of the Board and Chief Executive Officer

Formula

Acquisition Corp.

15

Broad Street, Suite 2624

New

York, NY 10005

(203)

512-2161

(Name,

Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent

for Service)

_______________________________

Copies

to:

|

Jay

M. Kaplowitz, Esq.

Arthur

S. Marcus, Esq.

Kristin

J. Angelino, Esq.

Gersten

Savage LLP

600

Lexington Avenue, 9th

floor

New

York, New York 10022

(212)

752-9700

(212)

980-5192 - Facsimile

|

[Underwriter’s

counsel]

|

Approximate date of commencement of

proposed sale to the public: As soon as practicable after the effective

date of this registration statement.

If any of

the securities being registered on this Form are to be offered on a delayed or

continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the

following box. x

If this

Form is filed to register additional securities for an offering pursuant to Rule

462(b) under the Securities Act, please check the following box and list the

Securities Act registration statement number of the earlier effective

registration statement for the same offering. ¨

If this

Form is a post-effective amendment filed pursuant to Rule 462(c) under the

Securities Act, check the following box and list the Securities Act registration

statement number of the earlier effective registration statement for the same

offering. ¨

If this

Form is a post-effective amendment filed pursuant to Rule 462(d) under the

Securities Act, check the following box and list the Securities Act registration

statement number of the earlier effective registration statement for the same

offering. ¨

If

delivery of the prospectus is expected to be made pursuant to Rule 434, please

check the following box. ¨

The

registrant hereby amends this registration statement on such date or dates as

may be necessary to delay its effective date until the registrant shall file a

further amendment which specifically states that this registration statement

shall thereafter become effective in accordance with Section 8(a) of the

Securities Act of 1933 or until the registration statement shall become

effective on such date as the Commission, acting pursuant to said Section 8(a),

may determine.

CALCULATION

OF REGISTRATION FEE

|

Title of Each Class of Security Being Registered

|

Amount Being Registered

|

Proposed Maximum

Offering Price Per

Security(1)

|

Proposed Maximum

Aggregate Offering Price(1)

|

Amount of Registration

Fee

|

||||||||||

|

Units,

each consisting of one share of Common

Stock, $.0001 par value, and one

Warrant

|

1,875,000

Units

|

$

|

8.00

|

$

|

15,000,000

|

$

|

1,069.50

|

|||||||

|

Shares

of Common Stock included as part of the

Units

|

1,875,000

Shares

|

—

|

—

|

—

|

(2)

|

|||||||||

|

Warrants

included as part of the Units

|

1,875,000

Warrants

|

—

|

—

|

—

|

(2)

|

|||||||||

|

Shares

of Common Stock underlying the

Warrants

included in the Units(3)

|

1,875,000

Shares

|

$

|

8.00

|

$

|

15,000,000

|

$

|

1,069.50

|

|||||||

|

Total

|

$

|

30,000,000

|

$

|

2,139.00

|

||||||||||

|

(1)

|

Estimated

solely for the purpose of calculating the registration

fee.

|

|

(2)

|

No

fee pursuant to Rule 457(g).

|

|

(3)

|

Pursuant

to Rule 416, there are also being registered such additional securities as

may be issued to prevent dilution resulting from stock splits, stock

dividends or similar transactions as a result of the anti-dilution

provisions contained in the

Warrants.

|

The

information in this preliminary prospectus is not complete and may be changed.

We may not sell these securities until the registration statement filed with the

Securities and Exchange Commission is effective. This prospectus is not an offer

to sell these securities and is not soliciting an offer to buy these securities

in any state where the offer or sale is not permitted.

SUBJECT

TO COMPLETION, DATED [___________], 2010

PROSPECTUS

$15,000,000

FORMULA

ACQUISITION CORP.

1,875,000

units

Formula

Acquisition Corp. is a newly formed blank check company organized for the

purpose of effecting a merger, capital stock exchange, asset acquisition or

other similar business combination with an operating Internet business. Our

efforts in identifying a prospective target will not be limited to a particular

industry, although we intend to focus our efforts on acquiring one or more

operating Internet businesses in the fields of e-commerce, mobile internet,

social networking, financial information and digital media, online banking

and/or software development. We do not have any specific business

combination under consideration and we have not (nor has anyone on our behalf)

contacted any prospective target business or had any discussions, formal or

otherwise, with respect to such a transaction.

This is

an initial public offering of our securities. Each unit that we are offering has

a price of $8.00 and consists of one share of our common stock and one warrant.

Each warrant entitles the holder to purchase one share of our common stock at a

price of $8.00. Each warrant will become exercisable on the later of our

completion of a business combination and

[______],

2011 [one year from the date of

this prospectus], and will expire on

[______],

2014 [four years from the date

of this prospectus], or earlier upon redemption.

There is

presently no public market for our units, common stock or warrants. We

anticipate that the units will be quoted on the Over the Counter Bulletin Board.

Assuming that the units are quoted on the Over the Counter Bulletin Board,

the units will be quoted under the symbol [_____] on or promptly after the date

of this prospectus. Assuming that the units are quoted on the Over the Counter

Bulletin Board, once the securities comprising the units begin separate trading,

the common stock and warrants will be quoted on the Over the Counter Bulletin

Board under the symbols [_____] and [_____], respectively. We cannot assure you

that our securities will be quoted or will continue to be quoted on the Over the

Counter Bulletin Board.

Investing

in our securities involves a high degree of risk. See “Risk Factors” beginning

on page [12] of this prospectus for a

discussion of information that should be considered in connection with an

investment in our securities.

Neither

the Securities and Exchange Commission nor any state securities commission has

approved or disapproved of these securities or determined if this prospectus is

truthful or complete. Any representation to the contrary is a criminal

offense.

|

Public Offering Price

|

Proceeds, Before

Expenses, to Us

|

|||||||

|

Per

unit

|

$

|

8.00

|

$

|

8.00

|

||||

|

Total

|

$

|

15,000,000

|

$

|

15,000,000

|

||||

$12,750,000

of the net proceeds of this offering, or $6.80 per unit [85%] sold to the

public in this offering, will be deposited into a trust account at [BANK],

maintained by [TRANSFER AGENT], acting as trustee. These funds will not be

released to us until the earlier of the completion of our initial business

combination and our liquidation (which may not occur until [_______] 2012 [24 months from the date of this

prospectus]).

We intend

to offer the units for sale on a firm-commitment basis. We currently are in the

process of retaining an underwriter. In the event that we are able to

retain an underwriter, the above table will be amended to reflect an amount for

the discount and commissions to be given to the underwriter, a portion of which

may be placed in escrow along with the proceeds of this offering.

[___________],

2010

FORMULA

ACQUISITION CORP.

TABLE

OF CONTENTS

|

Page

|

||||

|

Prospectus

Summary

|

1

|

|||

|

The

Offering

|

4

|

|||

|

Summary

Financial Data

|

11

|

|||

|

Risk

Factors

|

12

|

|||

|

Cautionary

Note Regarding Forward-Looking Statements

|

22

|

|||

|

Use

of Proceeds

|

23

|

|||

|

Dilution

|

26

|

|||

|

Capitalization

|

27

|

|||

|

Management’s

Discussion and Analysis of Financial Condition and Results of

Operations

|

28

|

|||

|

Proposed

Business

|

30

|

|||

|

Management

|

43

|

|||

|

Principal

Stockholders

|

46

|

|||

|

Certain

Transactions

|

48

|

|||

|

Description

of Securities

|

49

|

|||

|

Underwriting

|

53

|

|||

|

Legal

Matters

|

53

|

|||

|

Experts

|

53

|

|||

|

Where

You Can Find Additional Information

|

53

|

|||

|

Index

to Financial Statements

|

F-1

|

|||

This

summary highlights certain information appearing elsewhere in this prospectus.

For a more complete understanding of this offering, you should read the entire

prospectus carefully, including the risk factors and the financial statements.

Unless otherwise stated in this prospectus:

|

|

•

|

references to “we,” “us” or

“our company” refer to Formula Acquisition

Corp.;

|

|

|

•

|

references to “initial

stockholders” or “existing stockholders” refer to all of our stockholders

prior to this

offering;

|

|

|

•

|

references to “initial shares”

refer to the 468,750 shares of common stock that

our initial stockholders originally purchased from us for $25,000 in March 2010;

and

|

|

|

•

|

references to the term “public

stockholders” refer to the holders of the shares of common stock that are

being sold as part of the units in the public offering (whether they are

purchased in the initial public offering or in the secondary market),

including any of our existing stockholders to the extent that they

purchase such shares.

|

You

should rely only on the information contained in this prospectus. We have not

authorized anyone to provide you with different information. We are not making

an offer of these securities in any jurisdiction where the offer is not

permitted. You should not assume that the information contained in this

prospectus is accurate as of any date other than the date on the front of this

prospectus.

We are a

blank check company organized under the laws of the State of Delaware on March

23, 2010. We were formed with the purpose of effecting a merger,

capital stock exchange, asset acquisition or other similar business combination

with an operating Internet business. Our efforts in identifying a

prospective target will not be limited to a particular industry, although we

intend to focus our efforts on acquiring one or more operating Internet

businesses in the fields of e-commerce, mobile Internet, social networking,

financial information and digital media, online banking and/or software

development. To date, our efforts have been limited to organizational

activities. Accordingly, we cannot assure you that we will be able to locate a

target business or that we will be able to engage in a business combination with

a target business on favorable terms.

We intend

to look for Internet businesses that have one or several of the following

characteristics:

|

|

·

|

Several

years of revenue growth along with significant market

share;

|

|

|

·

|

Opportunities

for both organic and acquisition

growth;

|

|

|

·

|

Companies

that have a proprietary technology that has “built a moat” around their

business, making it difficult for competitors to encroach upon

it;

|

|

|

·

|

Proven

and experienced management with a strong track record;

and

|

|

|

·

|

Market

leadership positions within their

sector.

|

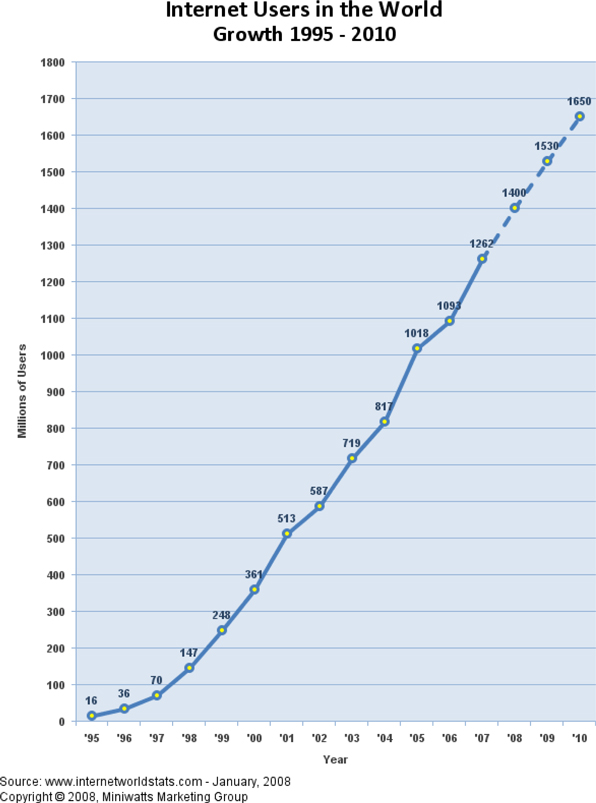

Despite

the ups and downs of the stock market, the growth of the Internet in terms of

both users and data has never experienced a down year1 and management believes that the growth will

be robust for years to come.

Our

management team has experience and contacts in the fields of e-commerce, mobile

Internet, social networking, financial information and digital media, online

banking and/or software development. We have either founded, managed or invested

in companies in each of these sectors and therefore we believe that we are

well-positioned to identify and consummate a business combination with an

Internet company in one of these sectors, particularly in the area of

financial information and digital media as well as social

networking.

Thomas J.

Clarke, Jr., our Chairman of the Board, Chief Executive Officer and President,

has been directly involved in over 15 acquisitions, joint ventures and

transactions involving companies he has owned or managed. From 1999 to 2009, he

was the CEO of a publicly traded financial information and digital media

company, TheStreet.com (NASDAQ: TSCM). While at TheStreet.com, Mr. Clarke

acquired and integrated various sites in the online banking sector (including

bankingmyway.com and geezeo.com) into TheStreet.com’s website. During

his tenure at TheStreet.com, the company went from a $50 million net loss to a

profit, with over $70 million in e-commerce sales, over $80 million in cash

assets and zero debt. In the course of Mr. Clarke’s 30 year career, most of the

companies Mr. Clarke has managed (including a number of Internet companies) have

been in the financial information and digital media sector, allowing Mr. Clarke

to develop a network of relationships in this sector spanning the venture

capital and entrepreneur communities. See the section titled

“Management – Directors and Executive Officers” for a further description of Mr.

Clarke’s background and experience.

1www.internetworldstats.com – January 2008

1

James

Altucher, our Chief Operating Officer, has been the founder and chief executive

of several Internet companies, including Stockpickr.com, a social networking

site in the financial information and digital media space. Mr.

Altucher is a well-known entrepreneur and author of four books on investing as

well as a columnist for Dow Jones Newswires, AOL, and several other

venues. Mr. Altucher has consummated numerous M&A transactions,

and has been involved in venture capital investments which he has helped source,

structure, and consummate. Over the past 20 years, he has developed a wide

network of relationships in the Internet space, particularly in the area of

social networking as well as financial information and digital

media. He co-founded Stockpickr.com with Mr. Kelly, which was sold to

TheStreet.com in 2007. He is also one of the founders of Vaultus

Mobile Technologies, Inc., which provides software solutions to companies to

improve mobile workers’ productivity. He is a board member of bitly.com, a

website that shortens URLs for use on Twitter and other social media sites, and

he is an advisor to Stocktwits.com, a website which serves as a tool for

aggregating financial information and digital media on Twitter. Mr.

Altucher is also an investor in BuddyMedia.com, a software-as-a-service platform

for companies that wish to develop a presence on Facebook, and Ticketfly, Inc.,

an online ticketing company which combines ticketing services with social media

applications. See the section titled “Management-Directors and

Executive Officers” for a further description of Mr. Altucher’s background and

experience.

Dan

Kelly, our Chief Financial Officer, is a former analyst at Credit Suisse

First Boston where he worked in the leveraged finance group. Mr.

Kelly also served as a principal at (212) Ventures, a technology and internet

fund founded by Mr. Altucher, focusing primarily on wireless services and

infrastructure software investments. In his banking and private

equity career, Mr. Kelly worked on over $6 billion worth of leveraged buyouts,

M&A and equity transactions, including Bresnan Communications, Vaultus, Ajax

Magnathermic, 4thpass, Big 5 Sporting Goods and H&E Equipment

Services. He has sourced and evaluated business plans for early-stage

venture capital investments as well as financing scenarios for mature private

equity investments. Additionally, Mr. Kelly has worked with both

early-stage and mature companies to develop strategic direction, implement

financial controls, evaluate acquisition opportunities and explore additional

financing opportunities to help capitalize on growth

opportunities. Mr. Kelly co-founded Stockpickr.com with Mr.

Altucher. Stockpickr.com was sold to TheStreet.com in

2007. Mr. Kelly currently has investments in several internet and

technology companies including bitly.com, a website that shortens URLs for use

on Twitter and other social media sites; Ticketfly, Inc., an online ticketing

company which combines ticketing services with social media applications;

Stocktwits.com, a website which serves as a tool for aggregating financial

information and digital media on Twitter; and BuddyMedia.com, a

software-as-a-service platform for companies that wish to develop a presence on

Facebook. See the section titled “Management-Directors and Executive Officers”

for a further description of Mr. Kelly’s background and experience.

We do not

have any specific business combination under consideration and we have not (nor

has anyone on our behalf) contacted any prospective target business or had any

discussions, formal or otherwise, with respect to such a transaction. We have

not (nor have any of our agents or affiliates) been approached by any candidates

(or representative of any candidates) with respect to a possible acquisition

transaction with our company. Additionally, we have not, nor has anyone on our

behalf, taken any measure, directly or indirectly, to identify or locate any

suitable acquisition candidate, nor have we engaged or retained any agent or

other representative to identify or locate any such acquisition

candidate.

We will

have until [_______], 2012 [24

months from the date of this prospectus] to consummate a business

combination. If we are unable to consummate a business combination by such date,

our corporate existence will cease by operation of corporate law (except for the

purposes of winding up our affairs and liquidating). Our initial business

combination must be with a target business whose fair market value is at least

equal to 80% of our net assets (all of our assets, including the funds then held

in the trust account, less our liabilities) at the time of such acquisition,

although this may entail simultaneous acquisitions of several operating

businesses. The fair market value of the target will be determined by our board

of directors based upon one or more standards generally accepted by the

financial community (which may include actual and potential sales, earnings,

cash flow and/or book value). If our board is not able to independently

determine that the target business has a sufficient fair market value, we will

obtain an opinion from an unaffiliated, independent investment banking firm with

respect to the satisfaction of such criteria. If we determine to simultaneously

acquire several businesses and such businesses are owned by different sellers,

we will need for each of such sellers to agree that our purchase of its business

is contingent on the simultaneous closings of the other acquisitions, which may

make it more difficult for us, and delay our ability, to complete our initial

business combination. With multiple acquisitions, we could also face additional

risks, including additional burdens and costs with respect to possible multiple

negotiations and due diligence investigations (if there are multiple sellers)

and the additional risks associated with the subsequent integration of the

operations and services or products of the acquired companies into a single

operating business.

The target business that we acquire may have a

fair market value substantially in excess of 80% of our net assets. In order to

consummate such a business combination, we may issue a significant amount of

debt or equity securities to the sellers of such business and/or seek to raise

additional funds through a private offering of debt or equity securities. There

are no limitations on our ability to incur debt or issue securities in order to

consummate a business combination. If we issue securities in order to consummate

a business combination, our stockholders could end up owning a minority of the

combined company, as there is no requirement that our stockholders own a certain

percentage of our company after our business combination. Since we have no

specific business combination under consideration, we have not entered into any

such arrangement to issue our debt or equity securities and have no current

intention of doing so.

2

Our

principal executive offices are located at 15 Broad Street, Suite 2624, New

York, NY 10005, and our telephone number is 203-512-2161.

3

THE

OFFERING

In making your decision on whether

to invest in our securities, you should take into account not only the

backgrounds of our management team, but also the special risks we face as a

blank check company. In addition, this offering is not being conducted in compliance with

Rule 419 promulgated under the Securities Act of 1933, as amended, and,

therefore, you will not be entitled to protections normally afforded to

investors in Rule 419 blank check offerings. You should carefully consider these

and the other risks set forth in the section entitled “Risk Factors” beginning

on page [12] of this

prospectus.

|

Securities

offered:

|

1,875,000

units, at $8.00 per unit, each unit consisting of:

|

|

|

•one

share of common stock; and

|

||

|

•one

warrant.

|

||

|

Trading

commencement and separation of common stock and warrants:

|

The

units will begin trading on or promptly after the date of this prospectus.

Each of the common stock and warrants may trade separately on the 90th day

after the date of this prospectus unless [UNDERWRITER] determines that an

earlier date is acceptable (based upon its assessment of the relative

strengths of the securities markets and small capitalization companies in

general, and the trading pattern of, and demand for, our securities in

particular). In no event will [UNDERWRITER] allow separate trading of the

common stock and warrants until we file an audited balance sheet

reflecting our receipt of the gross proceeds of this offering. We will

file our first Current Report on Form 8-K with the Securities and Exchange

Commission, including an audited balance sheet, promptly upon the

consummation of this offering, which is anticipated to take place three

business days from the date the units commence trading. The audited

balance sheet will reflect our receipt of the proceeds from the exercise

of the over-allotment option if the over-allotment option is exercised

prior to the filing of the Form 8-K. If the over-allotment option is

exercised after our initial filing of a Form 8-K, we will file an

amendment to the Form 8-K to provide updated financial information to

reflect the exercise and consummation of the over-allotment option. We

will also include in this Form 8-K, or amendment thereto, or in a

subsequent Form 8-K, information indicating if [UNDERWRITER] has allowed

separate trading of the common stock and warrants prior to the 90th day

after the date of this prospectus.

|

|

|

Securities

being purchased by insiders:

|

Prior

to the date of this prospectus, our initial stockholders purchased an

aggregate of 468,750 shares of common stock for

$25,000.

|

|

|

Common

Stock:

|

||

|

Number

outstanding before this offering

|

468,750

shares

|

|

|

Number

to be outstanding after this offering

|

2,

343,750 shares

|

|

|

Warrants:

|

||

|

Number

outstanding before this offering:

|

0

|

|

|

Number

to be outstanding after this offering:

|

1,875,000

warrants

|

4

|

Exercisability:

|

Each

warrant is exercisable for one share of common stock.

|

|

|

Exercise

price:

|

$8.00

|

|

|

Exercise

period:

|

The

warrants will become exercisable on the later of:

|

|

|

• the

completion of a business combination with a target business;

and

|

||

|

• [__________],

2011 [one year from the

date of this prospectus].

|

||

|

The

warrants will expire at 5:00 p.m., New York City time, on [__________],

2014 [four years from the

date of this prospectus] or earlier upon

redemption.

|

||

|

Redemption:

|

We

may redeem the outstanding warrants:

|

|

|

• in

whole and not in part;

|

||

|

• at

a price of $.01 per warrant at any time while the warrants are exercisable

(which will occur only if a registration statement relating to the common

stock issuable upon exercise of the warrants is effective and

current);

|

||

|

• upon

a minimum of 30 days’ prior written notice of redemption;

and

|

||

|

• if,

and only if, the last sales price of our common stock equals or exceeds

$15.50 per share for any 20 trading days within a 30 trading day period

ending three business days before we send the notice of

redemption.

|

||

|

If

the foregoing conditions are satisfied and we issue a notice of

redemption, each warrant holder can exercise his, her or its warrant prior

to the scheduled redemption date. However, the price of the common stock

may fall below the $15.50 trigger price as well as the $8.00 warrant

exercise price after the redemption notice is issued.

|

||

|

The

redemption criteria for our warrants have been established at a price that

is intended to provide warrant holders with a reasonable premium to the

initial exercise price and provide a sufficient differential between the

then-prevailing common stock price and the warrant exercise price so that

if the stock price declines as a result of our redemption call, the

redemption will not cause the stock price to drop below the exercise price

of the warrants.

|

||

|

Proposed

Over the Counter Bulletin Board symbols for our:

|

||

|

Units

|

[___].U

|

|

|

Common

Stock

|

[___]

|

|

|

Warrants

|

[___].WS

|

5

|

Offering

proceeds to be held in trust:

|

$12,750,000

of the net proceeds of this offering ($6.80 per unit [85%] sold

to the public in this offering) will be placed in a trust account at

[BANK], maintained by [TRANSFER AGENT], acting as trustee pursuant to an

agreement to be signed on the date of this prospectus. Except as set forth

below, these proceeds will not be released until the earlier of the

completion of a business combination and our liquidation. Therefore,

unless and until a business combination is consummated, the proceeds held

in the trust account will not be available for our use for any deferred

expenses related to this offering or expenses which we may incur related

to the investigation and selection of a target business and the

negotiation of an agreement to acquire a target business. Notwithstanding

the foregoing, there can be released to us from the trust account interest

earned on the funds in the trust account (i) up to an aggregate of

$[______] to fund expenses related to investigating and selecting a target

business and our other working capital requirements and (ii) any amounts

we may need to pay our income or other tax obligations. With these

exceptions, expenses incurred by us may be paid prior to a business

combination only from the net proceeds of this offering not held in the

trust account (initially $2,250,000).

|

|

|

None

of the warrants may be exercised until after the consummation of a

business combination and, thus, after the proceeds of the trust account

have been disbursed. Accordingly, the warrant exercise price will be paid

directly to us and not placed in the trust account.

|

||

|

Limited

payments and benefits to insiders:

|

There

will be no fees or other payments of any kind, whether in cash or our

securities, paid to our existing stockholders, officers, directors or

their affiliates prior to, or for any services they render in order

to effectuate the consummation of a business combination (regardless of

the type of transaction that it is) other than:

|

|

|

• payment

of [$7,500] per month to [__________] for office space and related

services; and

|

||

|

• reimbursement

of out-of-pocket expenses incurred by them in connection with certain

activities on our behalf, such as identifying and investigating possible

business targets and business combinations.

|

||

|

There

is no limit on the amount of out-of-pocket expenses reimbursable by us to

such individuals incurred in connection with their activities on our

behalf. Furthermore, the holders of our initial shares will be

entitled to registration rights requiring us to register the resale of

their securities commencing after we consummate our initial business

combination.

|

||

|

Amended

and Restated Certificate of Incorporation:

|

As

discussed below, there are specific provisions in our amended and restated

certificate of incorporation that may not be amended prior to our

consummation of a business combination, including our requirements to seek

stockholder approval of such a business combination and to allow our

stockholders to seek conversion of their shares if they do not approve of

such a business combination. While we have been advised that such

provisions limiting our ability to amend our certificate of incorporation

may not be enforceable under Delaware law, we view these provisions, which

are contained in Article Seventh of our amended and restated certificate

of incorporation, as obligations to our stockholders and will not take any

action to amend or waive these

provisions.

|

6

|

Our

amended and restated certificate of incorporation also provides that we

will continue in existence only until [____________], 2012 [24 months from the date of

this prospectus]. If we have not completed a business combination

by such date, our corporate existence will cease except for the purposes

of winding up our affairs and liquidating, pursuant to Section 278 of the

Delaware General Corporation Law. This has the same effect as if our board

of directors and stockholders had formally voted to approve our

dissolution pursuant to Section 275 of the Delaware General Corporation

Law. Our counsel has advised us, although we have not requested a formal

opinion from them, that, based on their analysis of the Delaware General

Corporation Law and relevant case law, limiting our corporate existence to

a specified date as permitted by Section 102(b)(5) of the Delaware General

Corporation Law removes the necessity to comply with the formal procedures

set forth in Section 275 (which would have required our board of directors

and stockholders to formally vote to approve our dissolution and

liquidation and to have filed a certificate of dissolution with the

Delaware Secretary of State). Asking our counsel to research this issue is

the only step we have taken to support this belief. In connection with any

proposed business combination we submit to our stockholders for approval,

we will also submit to stockholders a proposal to amend our amended and

restated certificate of incorporation to provide for our perpetual

existence, thereby removing this limitation on our corporate existence. We

will only consummate a business combination if stockholders vote both in

favor of such business combination and our amendment to provide for our

perpetual existence. The approval of the proposal to amend our amended and

restated certificate of incorporation to provide for our perpetual

existence would require the affirmative vote of a majority of our

outstanding shares of common stock. We view this provision terminating our

corporate existence by [___________], 2012 [24 months from the date of

this prospectus] as an obligation to our stockholders and will not

take any action to amend or waive this provision to allow us to exist for

a longer period of time except in connection with the consummation of a

business combination.

|

||

|

Stockholders

must approve business combination:

|

Pursuant

to our amended and restated certificate of incorporation, we will seek

stockholder approval before we effect any business combination, even if

the nature of the acquisition would not ordinarily require stockholder

approval under applicable state law. We view this requirement as an

obligation to our stockholders and will not take any action to amend or

waive this provision in our amended and restated certificate of

incorporation. In connection with the vote required for any business

combination, all of our existing stockholders, including all of our

officers and directors, have agreed to vote the shares of common stock

owned by them immediately before this offering in accordance with the

majority of the shares of common stock voted by the public stockholders.

We will proceed with a business combination only if (i) a majority of the

shares of common stock voted by the public stockholders are voted in favor

of the business combination (provided that a quorum is in attendance at

the meeting, in person or by proxy) and (ii) public stockholders owning

less than 30% of the shares sold in this offering exercise their

conversion rights described below. Accordingly, it is our understanding

and intention in every case to structure and consummate a business

combination in which public stockholders owning approximately 29.99% of

the shares sold in this offering may exercise their conversion rights and

the business combination will still go forward. If a significant number of

stockholders vote, or indicate their intention to vote, against a proposed

business combination, our founders, officers, directors or their

affiliates could seek to purchase units or shares of common stock in the

open market or in private transactions in order to influence the vote.

However, they have no present intention to do so, and as a result, have

not taken any steps or contemplated any other methods that would be

utilized in order to influence a vote on a proposed acquisition

transaction.

|

7

|

Conversion

rights for stockholders voting to reject a business

combination:

|

Pursuant

to our amended and restated certificate of incorporation, public

stockholders voting against a business combination will be entitled to

convert their stock into a pro rata share of the trust account (initially

$6.80 per share), plus any interest earned on their portion of the trust

account but less any interest that has been released to us as described

above to fund our working capital requirements and pay any of our tax

obligations, if the business combination is approved and

completed. In order to exercise this right, the public

stockholders must make an affirmative election. Voting against a business

combination does not automatically trigger the conversion right. Public

stockholders who convert their shares of stock into their share of the

trust account will continue to have the right to exercise any warrants

they may hold. Any request for conversion, once made, may be

withdrawn at any time up to the date of the meeting.

In

order for a business combination to be approved, a majority of the shares

of common stock voted by the public stockholders would need to vote in

favor of the combination and our existing shareholders, as described

above, would be required to vote their shares in accordance with the vote

of the majority to approve the business combination. Accordingly, since

they did not vote against the business combination, our existing

stockholders would not be entitled to exercise conversion rights with

respect to stock they own, whether included in their initial shares or

purchased by them in this offering or in the

aftermarket.

|

|

|

If

a vote on our initial business combination is held and the business

combination is not approved, we may continue to try to consummate a

business combination with an alternate target until [_________], 2012 [24 months from the date of

this prospectus]. If the initial business combination is not

approved or completed for any reason, then public stockholders voting

against our initial business combination who exercised their conversion

rights would not be entitled to convert their shares of common stock into

a pro rata share of the aggregate amount then on deposit in the trust

account. In such case, if we have required public stockholders to deliver

their certificates prior to the meeting, we will promptly return such

certificates to the public stockholder.

|

||

|

Liquidation

if no business combination:

|

As

described above, if we have not consummated a business combination by

[______], 2012 [24 months

from the date of this prospectus], our corporate existence will

cease by operation of law and we will promptly distribute only to our

public stockholders the amount in our trust account (including any accrued

interest then remaining in the trust account) plus any remaining net

assets.

|

|

|

We

cannot assure you that the per-share distribution from the trust account,

if we liquidate, will not be less than $6.80, plus interest then held in

the trust account for the following

reasons:

|

8

|

• Prior

to liquidation, pursuant to Section 281 of the Delaware General

Corporation Law, we will adopt a plan that will provide for our payment,

based on facts known to us at such time, of (i) all existing claims, (ii)

all pending claims and (iii) all claims that may be potentially brought

against us within the subsequent 10 years. Accordingly, we would be

required to provide for any creditors known to us at that time as well as

provide for any claims that we believe could potentially be brought

against us within the subsequent 10 years prior to distributing the funds

held in the trust to our public stockholders. We cannot assure you that we

will properly assess all claims that may be potentially brought against

us. As such, our stockholders could potentially be liable for any claims

of creditors to the extent of distributions received by them (but no

more).

|

||

|

• We

will seek to have all vendors and service providers (which would include

any third parties we engaged to assist us in any way in connection with

our search for a target business) and prospective target businesses

execute agreements with us waiving any right, title, interest or claim of

any kind they may have in or to any monies held in the trust account.

However, we have not received any such waivers yet and there is no

guarantee that they will execute such agreements. Nor is there any

guarantee that, even if such entities execute such agreements with us,

they will not seek recourse against the trust account or that a court

would not conclude that such agreements are not legally

enforceable.

|

||

|

We

anticipate the distribution of the funds in the trust account to our

public stockholders will occur by [_________], 2012 [10 business days from the

date our corporate existence ceases]. Our existing stockholders

have waived their rights to participate in any liquidation distribution

with respect to their initial shares. We will pay the costs of liquidation

from our remaining assets outside of the trust account.

|

||

|

Escrow

of initial shares:

|

On

the date of this prospectus, all of our existing stockholders, including

all of our officers and directors, will place their initial shares into an

escrow account maintained by [TRANSFER AGENT] acting as escrow agent.

Subject to certain limited exceptions (such as (i) transfers to an

entity’s members upon its liquidation, (ii) transfers to relatives and

trusts for estate planning purposes or (iii) transfers by private sales

made at or prior to the consummation of a business combination at prices

no greater than the price at which the shares were originally purchased,

in each case where the transferee agrees to the terms of the escrow

agreement), these shares will not be transferable during the escrow period

and will not be released from escrow until the earlier

of:

|

|

|

• one

year after the consummation of a business combination;

|

||

|

• the

last sales price of our common stock equals or exceeds $12.00 per share

for any 20 trading days within any 30-trading day period commencing after

the consummation of our business combination; or

|

||

|

• we

consummate a subsequent liquidation, merger, stock exchange or other

similar transaction that results in our stockholders having the right to

exchange their shares of common stock for cash, securities or other

property.

|

9

|

Right

of first review:

|

In

order to minimize potential conflicts of interest which may arise from

multiple corporate affiliations, each of our officers has agreed, until

the earliest of a business combination, our liquidation or such time as he

or she ceases to be an officer, to present to our company for our

consideration, prior to presentation to any other entity, any suitable

business opportunity which may reasonably be required to be presented to

us, subject to any pre-existing fiduciary or contractual obligations he

might have.

|

|

|

Determination

of offering size:

|

We

agreed to an offering size of $15 million based on the previous

transactional experience of our principals. We also considered the size of

the offering to be an amount we believe will be successfully received

given market conditions, our proposed industry focus and the size of

initial public offerings of other similarly structured blank check

companies.

|

10

SUMMARY

FINANCIAL DATA

The

following table summarizes the relevant financial data for our business and

should be read with our financial statements, which are included in this

prospectus. We have not had any significant operations to date, so only balance

sheet data is presented.

|

[__],

2010

|

||||||||

|

Actual

|

As

Adjusted(1)

|

|||||||

|

Balance

Sheet Data:

|

|

|

||||||

|

Working

capital

|

$ | 25,000 | $ |

[____]

|

||||

|

Total

assets

|

25,000 |

[____]

|

||||||

|

Total

liabilities

|

[____]

|

[____]

|

||||||

|

Value

of common stock which may be converted to cash

|

[____]

|

[____]

|

||||||

|

Stockholders’

equity

|

25,000 |

[____]

|

||||||

The “as

adjusted” information gives effect to the sale of the units we are offering,

including the application of the related gross proceeds and the payment of the

estimated remaining costs from such sale and the repayment of the accrued and

other liabilities required to be repaid.

The “as

adjusted” working capital includes $12,750,000 to be held in the trust account,

which will be available to us only upon the consummation of a business

combination within the time period described in this prospectus. If a business

combination is not so consummated, the trust account, and all accrued interest

earned thereon less (i) up to $[____] that may be released to us to fund our

expenses and other working capital requirements and (ii) any amounts released to

us to pay our income or other tax obligations, will be distributed solely to our

public stockholders (subject to our obligations under Delaware law to provide

for claims of creditors).

We will

not proceed with a business combination if public stockholders owning 30% or

more of the shares sold in this offering vote against the business combination

and exercise their conversion rights. Accordingly, we may effect a business

combination if public stockholders owning up to approximately 29.99% of the

shares sold in this offering exercise their conversion rights. If this occurred,

we would be required to convert to cash up to approximately 29.99% of the

1,875,000 shares sold in this offering, or 562,313 shares of common stock, at an

initial per-share conversion price of $6.80 (for a total of approximately

$3,823,728), without taking into account interest earned on the trust account.

The actual per-share conversion price will be equal to:

|

|

·

|

the

amount in the trust account, including all accrued interest (net of taxes

payable) after distribution of interest income on the trust account

balance to us as described above, as of two business days prior to the

proposed consummation of the business

combination,

|

|

|

·

|

divided

by the number of shares of common stock underlying the units sold in this

offering.

|

11

RISK

FACTORS

An

investment in our securities involves a high degree of risk. You should consider

carefully the material risks described below, which we believe represent all the

material risks related to the offering, together with the other information

contained in this prospectus, before making a decision to invest in our units.

If any of the following events occur, our business, financial condition and

operating results may be materially adversely affected. In that event, the

trading price of our securities could decline, and you could lose all or part of

your investment.

Risks

Associated With Our Business

We

are a development stage company with no operating history and, accordingly, you

will not have any basis on which to evaluate our ability to achieve our business

objective.

We are a

recently incorporated development stage company with no operating results to

date. Therefore, our ability to commence operations is dependent upon obtaining

financing through the public offering of our securities. Since we do not have an

operating history, you will have no basis upon which to evaluate our ability to

achieve our business objective, which is to acquire an operating business. We

have not conducted any discussions and we have no plans, arrangements or

understandings with any prospective acquisition candidates. We will not generate

any operating revenues until, at the earliest, after the consummation of a

business combination.

If

we are forced to liquidate before a business combination and distribute the

trust account, our public stockholders may receive less than $6.80 per share and

our warrants will expire worthless.

If we are

unable to complete a business combination within the prescribed time frames and

are forced to liquidate our assets, the per-share liquidation distribution may

be less than $6.80 because of the expenses of this offering, our general and

administrative expenses and the anticipated costs of seeking a business

combination. Furthermore, there will be no distribution with respect to our

outstanding warrants which will expire worthless if we liquidate before the

completion of a business combination.

If

we are unable to consummate a business combination, our public stockholders will

be forced to wait the full 24 months before receiving liquidation

distributions.

We have

24 months in which to complete a business combination. We have no obligation to

return funds to investors prior to such date unless we consummate a business

combination prior thereto and only then in cases where investors have sought

conversion of their shares. Only after the expiration of this full time period

will public stockholders be entitled to liquidation distributions if we are

unable to complete a business combination. Accordingly, investors’ funds may be

unavailable to them until such date.

If

the net proceeds of this offering not being held in trust are insufficient to

allow us to operate for at least the next 24 months, we may be unable to

complete a business combination.

We

believe that, upon consummation of this offering, the funds available to us

outside of the trust account, plus the interest earned on the funds held in the

trust account that may be available to us, will be sufficient to allow us to

operate for at least the next 24 months, assuming that a business combination is

not consummated during that time. However, we cannot assure you that our

estimates will be accurate. We could use a portion of the funds available to us

to pay fees to consultants to assist us with our search for a target business.

We could also use a portion of the funds as a down payment or to fund a

“no-shop” provision (a provision in a letter of intent designed to keep target

businesses from “shopping” around for transactions with other companies on terms

more favorable to such target businesses) with respect to a particular proposed

business combination, although we do not have any current intention to do so. If

we entered into a letter of intent where we paid for the right of exclusivity

from a target business and were subsequently required to forfeit such funds

(whether as a result of our breach or otherwise), we might not have sufficient

funds to continue searching for, or conduct due diligence with respect to, a

target business.

We

may proceed with a business combination even if public stockholders owning

approximately 29.99% of the shares sold in this offering exercise their

conversion rights.

We may

proceed with a business combination as long as public stockholders owning less

than 30% of the shares sold in this offering exercise their conversion rights.

Accordingly, approximately 29.99% of the public stockholders may exercise their

conversion rights and we could still consummate a proposed business

combination. Our business combination may require us to use substantially

all of our cash to pay the purchase price. In such a case, because we will not

know how many stockholders may exercise such conversion rights, we may need to

arrange third party financing to help fund our business combination in case a

larger percentage of stockholders exercise their conversion rights than we

expect. Additionally, even if our business combination does not require us to

use substantially all of our cash to pay the purchase price, if a significant

number of stockholders exercise their conversion rights, we will have less cash

available to use in furthering our business plans following a business

combination and may need to arrange third party financing. We have not taken any

steps to secure third party financing for either situation. We cannot assure you

that we will be able to obtain such third party financing on terms favorable to

us or at all.

12

You

will not be entitled to protections normally afforded to investors of blank

check companies.

Since the

net proceeds of this offering are intended to be used to complete a business

combination with a target business that has not been identified, we may be

deemed to be a “blank check” company under the United States securities laws.

However, since we will have net tangible assets in excess of $5,000,000 upon the

successful consummation of this offering and will file a Current Report on Form

8-K, including an audited balance sheet demonstrating this fact, we are exempt

from rules promulgated by the SEC to protect investors in blank check companies

such as Rule 419 under the Securities Act. Accordingly, investors will not be

afforded the benefits or protections of those rules. Because the SEC has taken

the position that we are not subject to Rule 419, our units will be immediately

tradable and we have a longer period of time to complete a business combination

than we would if we were subject to such rule.

If

third parties bring claims against us, the proceeds held in trust could be

reduced and the per-share liquidation price received by stockholders will be

less than $6.80 per share.

Our

placing of funds in trust may not protect those funds from third party claims

against us. Although we will seek to have all vendors and service providers we

engage and prospective target businesses we negotiate with, execute agreements

with us waiving any right, title, interest or claim of any kind in or to any

monies held in the trust account for the benefit of our public stockholders,

there is no guarantee that they will execute such agreements. Furthermore, there

is no guarantee that, even if such entities execute such agreements with us,

they will not seek recourse against the trust account. Nor is there any

guarantee that a court would uphold the validity of such agreements.

Accordingly, the proceeds held in trust could be subject to claims that could

take priority over those of our public stockholders.

Additionally,

if we are forced to file a bankruptcy case or an involuntary bankruptcy case is

filed against us which is not dismissed, the proceeds held in the trust account

could be subject to applicable bankruptcy law, and may be included in our

bankruptcy estate and subject to the claims of third parties with priority over

the claims of our stockholders. To the extent any bankruptcy claims deplete the

trust account, we cannot assure you we will be able to return to our public

stockholders at least $6.80 per share.

Our

stockholders may be held liable for claims by third parties against us to the

extent of distributions received by them.

Our

amended and restated certificate of incorporation provides that we will continue

in existence only until 24 months from the date of this prospectus. If we have

not completed a business combination by such date and amended this provision in

connection thereto, pursuant to the Delaware General Corporation Law, our

corporate existence will cease except for the purposes of winding up our affairs

and liquidating. Under Sections 280 through 282 of the Delaware General

Corporation Law, stockholders may be held liable for claims by third parties

against a corporation to the extent of distributions received by them in a

dissolution.

13

If the

corporation complies with certain procedures set forth in Section 280 of the

Delaware General Corporation Law intended to ensure that it makes reasonable

provision for all claims against it, including a 60-day notice period during

which any third-party claims can be brought against the corporation, a 90-day

period during which the corporation may reject any claims brought, and an

additional 150-day waiting period before any liquidating distributions are made

to stockholders, any liability of stockholders with respect to a liquidating

distribution is limited to the lesser of such stockholder’s pro rata share of

the claim or the amount distributed to the stockholder, and any liability of the

stockholder would be barred after the third anniversary of the dissolution.

However, it is our intention to make liquidating distributions to our

stockholders as soon as reasonably possible after the expiration of the 24 month

period and, therefore, we do not intend to comply with those procedures. Because

we will not be complying with those procedures, we are required, pursuant to

Section 281 of the Delaware General Corporation Law, to adopt a plan that will

provide for our payment, based on facts known to us at such time, of (i) all

existing claims, (ii) all pending claims and (iii) all claims that may be

potentially brought against us within the subsequent 10 years. Accordingly, we

would be required to provide for any creditors known to us at that time or those

that we believe could be potentially brought against us within the subsequent 10

years prior to distributing the funds held in the trust to stockholders. We

cannot assure you that we will properly assess all claims that may be

potentially brought against us. As such, our stockholders could potentially be

liable for any claims to the extent of distributions received by them (but no

more) and any liability of our stockholders may extend well beyond the third

anniversary of the date of distribution. Accordingly, we cannot assure you that

third parties will not seek to recover from our stockholders amounts owed to

them by us.

If we are

forced to file a bankruptcy case or an involuntary bankruptcy case is filed

against us which is not dismissed, any distributions received by stockholders

could be viewed under applicable debtor/creditor and/or bankruptcy laws as

either a “preferential transfer” or a “fraudulent conveyance.” As a result, a

bankruptcy court could seek to recover all amounts received by our stockholders.

Furthermore, because we intend to distribute the proceeds held in the trust

account to our public stockholders promptly after [_____], 2012 [24 months from the date of this

prospectus], this may be viewed or interpreted as giving preference to

our public stockholders over any potential creditors with respect to access to

or distributions from our assets. Furthermore, our board may be viewed as having

breached their fiduciary duties to our creditors and/or may have acted in bad

faith, and thereby exposing itself and our company to claims of punitive

damages, by paying public stockholders from the trust account prior to

addressing the claims of creditors. We cannot assure you that claims will not be

brought against us for these reasons.

An

effective registration statement may not be in place when an investor desires to

exercise warrants, thus precluding such investor from being able to exercise

his, her or its warrants and causing such warrants to be practically

worthless.

No

warrant held by public stockholders will be exercisable and we will not be

obligated to issue shares of common stock unless at the time a holder seeks to

exercise such warrant, a prospectus relating to the common stock issuable upon

exercise of the warrant is current. Under the terms of the warrant agreement, we

have agreed to use our best efforts to meet these conditions and to maintain a

current prospectus relating to the common stock issuable upon exercise of the

warrants until the expiration of the warrants. However, we cannot assure you

that we will be able to do so, and if we do not maintain a current prospectus

related to the common stock issuable upon exercise of the warrants, holders will

be unable to exercise their warrants and we will not be required to settle any

such warrant exercise, whether by net cash settlement or otherwise. If the

prospectus relating to the common stock issuable upon the exercise of the

warrants is not current, the warrants may have no value, the market for the

warrants may be limited and the warrants may expire worthless.

An

investor will only be able to exercise a warrant if the issuance of common stock

upon such exercise has been registered or qualified or is deemed exempt under

the securities laws of the state of residence of the holder of the

warrants.

No

warrants will be exercisable and we will not be obligated to issue shares of

common stock unless the common stock issuable upon such exercise has been

registered or qualified or deemed to be exempt under the securities laws of the

state of residence of the holder of the warrants. As a result, the warrants may

be deprived of any value, the market for the warrants may be limited and the

holders of warrants may not be able to exercise their warrants if the common

stock issuable upon such exercise is not qualified or exempt from qualification

in the jurisdictions in which the holders of the warrants reside.

If

you are not an institutional investor, you may purchase our securities in this

offering only if you reside within certain states and may engage in resale

transactions only in those states and a limited number of other

jurisdictions.

We have

applied to register our securities, or have obtained or will seek to obtain an

exemption from registration, in [list states]. If you are not an “institutional

investor,” you must be a resident of these jurisdictions in order to purchase

our securities in the offering. In order to prevent resale transactions in

violation of states’ securities laws, you may engage in resale transactions only

in these states and in a limited number of other jurisdictions in which an

applicable exemption is available or a Blue Sky application has been filed and

accepted. This restriction on resale may limit your ability to resell the

securities purchased in this offering and may impact the price of our

securities. For a more complete discussion of the Blue Sky state securities laws

and registrations affecting this offering, please see the section below entitled

“Underwriting — State Blue Sky Information” below. Even if you are an

institutional investor, you may purchase our securities in this offering only if

you are located in a jurisdiction permitting sales of the units to institutional

investors. You should consult with your own financial and legal advisors to

determine if you are eligible to participate in this offering.

14

Since

we have not currently selected any target business with which to complete a

business combination, we are unable to currently ascertain the merits or risks

of the operations of that business.

Since we

have not yet identified a prospective target business, investors in this

offering have no current basis to evaluate the possible merits or risks of the

operations of that business. To the extent we complete a business combination

with a financially unstable company or an entity in its early stages of

development or growth and/or an entity subject to unknown or unmanageable

liabilities, we may be affected by numerous risks inherent in the business

operations of those entities. We would consider a company to be financially

unstable if, for example, a substantial portion of its cash flow is dedicated to

its debt service obligations or its expected capital expenditure requirements

exceeds the ability of the target business to fund them. In addition, we would

consider a business to be in its early stages of development or growth if it is

newly formed and is in the process of developing its initial technologies,

processes, services, or products. Although our management will endeavor to

evaluate the risks inherent in a particular target business, we cannot assure

you that we will properly ascertain or assess all of the significant risk

factors. We also cannot assure you that an investment in our units will not

ultimately prove to be less favorable to investors in this offering than a

direct investment, if an opportunity is available, in a target

business.

We

may issue shares of our capital stock or debt securities to complete a business

combination, which would reduce the equity interest of our stockholders and

likely cause a change in control of our ownership.

Our

certificate of incorporation offering authorizes the issuance of up to

100,000,000 shares of common stock, par value $.0001 per share, and 1,000,000

shares of preferred stock, par value $.0001 per share. Immediately after this

offering [(assuming no exercise of the over-allotment option)], there will be

95,781,250 authorized but unissued shares of our common stock available for

issuance (after appropriate reservation for the issuance of the shares upon full

exercise of our outstanding warrants) and all of the 1,000,000 shares of

preferred stock available for issuance. Although we have no commitment as of the

date of this offering, we may issue a substantial number of additional shares of

our common or preferred stock, or a combination of common and preferred stock,

to complete a business combination. The issuance of additional shares of our

common stock or any number of shares of our preferred stock:

|

|

•

|

may

significantly reduce the equity interest of investors in this

offering;

|

|

|

•

|

may

subordinate the rights of holders of common stock if we issue preferred

stock with rights senior to those afforded to our common

stock;

|

|

|

•

|

will

likely cause a change in control if a substantial number of our shares of

common stock are issued, which may affect, among other things, our ability

to use our net operating loss carry forwards, if any, and could result in

the resignation or removal of our present officers and directors;

and

|

|

|

•

|

may

adversely affect prevailing market prices for our common

stock.

|

Similarly,

if we issue debt securities, it could result in:

|

|

•

|

default

and foreclosure on our assets if our operating revenues after a business

combination are insufficient to repay our debt

obligations;

|

|

|

•

|

acceleration

of our obligations to repay the indebtedness even if we make all principal

and interest payments when due if we breach certain covenants that require

the maintenance of certain financial ratios or reserves without a waiver

or renegotiation of that

covenant;

|

|

|

•

|

our

immediate payment of all principal and accrued interest, if any, if the

debt security is payable on demand;

and

|

|

|

•

|

our

inability to obtain necessary additional financing if the debt security

contains covenants restricting our ability to obtain such financing while

the debt security is

outstanding.

|

15

Our

ability to successfully effect a business combination and to be successful

thereafter will be totally dependent upon the efforts of our key personnel, some

of whom may join us following a business combination.

Our

ability to successfully effect a business combination is dependent upon the

efforts of our key personnel. The role of our key personnel in the target

business, however, cannot presently be ascertained. Although some of our key

personnel may remain with the target business in senior management or advisory

positions following a business combination, it is likely that some or all of the

management of the target business will remain in place. While we intend to

closely scrutinize any individuals we engage after a business combination, we

cannot assure you that our assessment of these individuals will prove to be

correct. These individuals may be unfamiliar with the requirements of operating

a public company, which could cause us to have to expend time and resources

helping them become familiar with such requirements. This could be expensive and

time-consuming and could lead to various regulatory issues that may adversely

affect our operations.

Our

key personnel may negotiate employment or consulting agreements with a target

business in connection with a particular business combination. These agreements

may provide for them to receive compensation following a business combination

and as a result, may cause them to have conflicts of interest in determining

whether a particular business combination is the most advantageous.

Our key

personnel will be able to remain with the company after the consummation of a

business combination only if they are able to negotiate employment or consulting

agreements in connection with the business combination. Such negotiations would

take place simultaneously with the negotiation of the business combination and

could provide for such individuals to receive compensation in the form of cash

payments and/or our securities for services they would render to the company

after the consummation of the business combination. The personal and financial

interests of such individuals may influence their motivation in identifying and

selecting a target business. However, we believe the ability of such individuals

to remain with the company after the consummation of a business combination will

not be the determining factor in our decision as to whether or not we will

proceed with any potential business combination.

Our

officers and directors will allocate a portion of their time to other businesses

thereby causing conflicts of interest in their determination as to how much time

to devote to our affairs. This conflict of interest could have a negative impact

on our ability to consummate a business combination.

Our

officers and directors are not required to commit their full time to our

affairs, which could create a conflict of interest when allocating their time

between our operations and their other commitments. We do not intend to have any

full time employees prior to the consummation of a business combination. All of

our executive officers are engaged in several other business endeavors and are

not obligated to devote any specific number of hours to our affairs. If our

officers’ and directors’ other business affairs require them to devote more

substantial amounts of time to such affairs, it could limit their ability to

devote time to our affairs and could have a negative impact on our ability to

consummate a business combination. We cannot assure you that these conflicts