Attached files

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C.

20549

FORM 10-K

(Mark One)

[ x ] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended: December 31, 2009

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ________________to ________________

Commission File Number: 0-24721

LEXON TECHNOLOGIES, INC.

(Exact name of registrant as specified in charter)

| Delaware | 87-0502701 |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer I.D. No.) |

| 14830 Desman Road | 90638 |

| (Address of principal executive offices) | (Zip Code) |

Issuer's telephone number, including area code: (714) 522-0270

Securities registered pursuant to section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered |

| None | N/A |

Securities registered pursuant to section 12(g) of the Act:

Common Stock, par value $0.001 per share

(Title of class)

Check whether the issuer is not required to file reports pursuant to Section 13 or 15(d) of the Exchange Act. [ ]

Check whether the issuer (1) filed all reports required to be filed by section 13 or 15(d) of the Exchange Act during the past 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. (1) Yes [ x ] No [ ] (2) Yes [ x ] No [ ]

Check if there is no disclosure of delinquent filers in response to Item 405 of Regulation S-B is not contained in this form, and no disclosure will be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer (as defined in Rule 12b-2 of the Act). See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer [ ] | Accelerated filer [ ] | Non-accelerated filer [ ] | Smaller reporting company [ x ] |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes No[ x ]

State issuer's revenues for its most recent fiscal year: $$5,446,742.

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the stock was sold, or the average bid and asked prices of such common equity, as of a specified date within the past 60 days.

As of April 15, 2010, Lexon had 515, 289, 722 shares of common stock outstanding. Based on the closing price of the common stock on April 14, 2010, of $0.017 per share, the market value of shares held by non-affiliates would be $3,213,406.96, based on 189,023,939 shares. Lexon’s stock is traded on the over-the-counter bulletin board system .under the symbol “LEXO” however trades are thin and sporadic. Therefore, the bid and ask price may not be indicative of any actual value in the stock.

DOCUMENTS INCORPORATED BY REFERENCE

List hereunder the following documents if incorporated by reference and the part of the form 10-K (e.g., part I, part II, etc.) into which the document is incorporated: (1) Any annual report to security holders; (2) Any proxy or other information statement; and (3) Any prospectus filed pursuant to rule 424(b) or (c) under the Securities Act of 1933:

None.

PART I.

| ITEM 1. | DESCRIPTION OF BUSINESS |

Lexon Technologies, Inc. ("the Company" or "Lexon") was incorporated in April 1989 under the laws of state of Delaware, and owns 90.16% of Lexon Semiconductor Corporation ("Lexon Semi" or formerly known as Techone Co., Ltd ("Techone")) which had developed and manufactured Low Temperature Cofired Ceramic (LTCC) components, including LTCC wafer probe cards, LTCC circuit boards, LTCC Light Emitting Diode (LED) displays and related products for the semiconductor testing and measurement, custom Printed Circuit Board (PCB), and cellular phone industries. The Company currently has no business activities.

Initially registered as California Cola Distributing Company, Inc, the Company changed its name twice; first to Rexford, Inc. in October 1992, and to the current name in July 1999.

In July 1999, Lexon acquired 100% of the outstanding common stock of Chicago Map Corporation (CMC) in exchange for 10,500,000 shares of the Company's common stock through a reverse acquisition accompanied by a recapitalization. The surviving entity, Lexon, reflected the assets and liabilities of Lexon and CMC at their historical book values. Lexon dissolved CMC in 2002.

In April 2002, Lexon acquired 100% of the outstanding common stock of Phacon Corporation (Phacon) in exchange for 17,500,000 shares of Company's common stock through a reverse acquisition accompanied by a recapitalization. As part of the agreement, the Company elected a 1 for 10 reverse stock split and the acquired shares of Phacon were entirely canceled leaving the Company as the surviving entity.

In March 2003, the Company incorporated Lexon Korea Corporation (“Lexon Korea”) as a wholly-owned subsidiary in Korea for the purpose of entering into potential business combinations with Korean operating entities. Lexon Korea was reorganized in August 2005, and as a result, the Company’s equity share in Lexon Korea was reduced to 10%.

In December 2004, the Company acquired 90.16% of the voting stock of Techone Company, Ltd, a company in Korea, by investing $1,588,000. The Company recognized goodwill of $1,851,692 in the acquisition. The Company acquired Techone to develop it as the Company’s core operating business in Korea for manufacturing and selling LTCC related products. However, the development of the LTCC related products was not successful, and the operations of Techone became highly leveraged financially. In August 2005, certain creditors filed an involuntary foreclosure and sold Techone’s assets through public auction to satisfy secured debts. This disposal of assets resulted in a gain $1,315,469 for the year ended December 31, 2005. In February 2006, Techone changed its name to Lexon Semiconductor Corporation and all of its operation has been suspended due to lack of operating working capital. Lexon Semi was dissolved on October 28, 2009 based on a decision of shareholders meeting. Lexon Semi has $241,000 of due to related party and $415,000 of liabilities relation to discontinued operations as of September 30, 2009.

On October 7, 2009, Paragon Toner Inc., a California corporation, entered into an Agreement and Plan of Merger (the “Merger Agreement”) with the Company whereby the Company issued 347,448,444 shares of common stock (the “Common Stock”) of the Company (the “Acquisition Shares”) to the shareholders of Paragon, representing approximately 67% of the issued and outstanding Common Stock after completion of the merger in October 2009. The effective date of the Merger was October 22, 2009 (“Effective Date”). We have decided to maintain the name of our predecessor company.

Overview

Lexon Technologies, Inc. or dba Paragon Toner Inc. (“Paragon” or the “Company”) are one of the first movers in recycling toner cartridges for laser printers, fax and multifunction copiers. We specialize in difficult to find toner as well as color and special niche cartridges. We have a 35,000 square foot factory, 67 employees and the capacity to manufacture 50,000 cartridges per month and recycle 350 different models of toner cartridges. Our main clients include multinational companies such as Micro Center, Royal Imaging, Staples, Inc.and Royal Typewriter. We also operate an online website for the sale of its toner products and is also a supplier numerous independent online websites.

Current Business Model

The process we employ when recycling toner cartridges is as follows:

| a. |

Disassemble Empty (Used) Cartridges – We inspect and evaluate components to determine if the components can be recycled. | |

| b. |

CleanComponents – We remove old components and clean components to be recycled. | |

| c. |

Inspect Components – We inspect all new and recycled components before assembly. | |

| d. |

AssembleComponents – We assemble all of the components to create a refurbished cartridge and refill the cartridge with toner. | |

| e. |

Perform Quality Control Tests – We test all finished products using accurate testing equipment. | |

| f. |

Package – We package the product for shipping to the consumer. |

We are a vendor to:

| a. |

Big Box Clients (including Staples, Inc. and Micro Center by Micro Electronics, Inc.) | |

| b. |

Distributors | |

| c. |

Online Retailers | |

| d. |

Small Businesses and Individuals through our online direct sales division. |

We havebenefited from the significant growth trends in theglobal recycled toner industry. We have experienced a dramatic upward trend in its overall sales and net profits.

Post Merger Strategy

We plan to focus on the following activities after the merger:

| a. |

Attract High Caliber Management - Our management has demonstrated the ability to create value and maintain a profitable operation. As a private enterprise the company has been successful in achieving solid growth in sales and profits. As a public company, we intend to both improve the efficiency of our operations to optimize our organic growth and expand our operationsby rapid growth through acquisition. Therefore, we will seek seasoned managementhaving an in- depth knowledge of our industry and the requisite expertise to create a more efficient operation, by effectively introducing new products while expanding our client base. In addition, we will attract talented individuals with experience in mergers and acquisitions who can successfully identify ideal target companies, maximize terms during negotiation and successfully integrate these targets with our company’s operations. As a public company, we can create competitive incentive packages by allotting a certain percentage of the compensation in the form of equity and/or stock options. | |

| b. |

Invest in Infrastructure - We will identify aspects of our operations that can be upgraded or improved to increase sales and productivity. These improvements may include factory automation and identification of more cost effective suppliers. | |

| c. |

Increase Marketing – We have achieved growth in revenues and profitability with minimal expenditures towards marketing our products. Our current marketing efforts are comprised primarily of word of mouth and our staff’s persistent cold-calling sales efforts. After raising additional funds, we expect to expand our client base by hiring a more seasoned |

|

marketing staff and by investing in advertising with a specific focus on internet advertising. | ||

| d. |

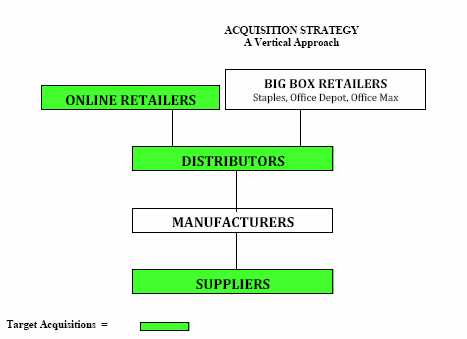

Growth by Acquisition - We will acquire other companies or assets within our industry or related industries, focusing on a vertical acquisition approach. |

We will focus our merger and acquisition activities on suppliers, distributors and online retailers. This vertical approach will increase sales and profitability. Integratingwith these types of firms is relatively easier sinceeach target in the vertical chain has a distinct role. By utilizing our stock, we can acquire companies with a combination of cash and stock to minimize excess use of our cash reserves.

| (i) |

Suppliers –(empty cartridge collectors and brokers) Maintaining a supply of empty cartridges is critical for our success. While we are proficient in both directly collecting and sourcing empty cartridges, an acquisition in this sector will ultimately increase our product quality control, sales and profitability. By controlling the source of our empty cartridges, we can insure the highest quality for our customers. In addition, by securing direct and preferential access to the empty cartridges, we can readily meet any order and reduce the raw material costs, thereby leading to higher net margins. | |

| (ii) |

Distributors – Many of our clients are large distributors who buy products from us and resell them to retailers and end users at higher prices. We will seek acquisition of a large distributor with a large client database, so we can utilize its sales channels and offer its clients high quality product at cheaper price while maintaining a high degree of profitability. While we favor already profitable distribution companies, we also view distressed distributors as viable acquisition targets. We can restructure these distributors and realize significant value from aggressively marketing to their client base. | |

| (iii) |

Online Retailers– Our online division at “www.yourcartridges.com” has significantly higher margins and real time cash flow. By acquiring online retailers, we can again provide the product at a cheaper cost and be more competitive in the internet market. Moreover, the cost of integration will be marginal as we already have a staff in place for both marketing and customer service. Based on our experience, online retailers can be purchased at low cost since they are often operated and owned by small independent business owners. By having access to their client database, we can create an aggressive marketing strategy to maximize their existing customer base. In the future, we intend to have more than half our revenues generated from online sources in order to optimize our margins and cashflow. |

Quality Standards

Our laser toner cartridges not only meet OEM standards, but often exceed OEM standards. Our defect ratio is less than 1%, which is considered low in the toner industry. We also offer a 100% guarantee for all of our finished products.

Profitability

Since our establishment and most notably for the last two years we have seen an increase in both our profits and our revenues. This can be attributed to our experience in maintaining a streamline operation and our ability to reduce costs while maintaining high quality standards. The defective rate of our products is less than 1% and our repeat and long standing business with the major market players illustrate the high quality of our products.

Strong Online Presence

Our website YourCartridges.com is a leader in the online industry. The website alone has annual revenue of $650,000 without any significant marketing effort on our part. The net profit margin for the online segment of operation is close to 20% with greater cash flow. We have also acquired two more internet properties which have been successfully integrated into our online division. We are currently identifying more online retailers for possible acquisition.

Competition

We compete primarily with other small remanufacturers of toner cartridge products. However, due to the recent economic downturn and the failure of many individual companies to achieve profitability in this industry, many of our direct competitors have exited the market.

Insurance

We maintain medical and accident insurance for our employees to the extent required under federal laws and the laws of the State of California, and we also maintain fire and general commercial insurance with respect to our facilities. We do not have any business liability or disruption insurance coverage for our operations.

ISO 9001, 14001, Minority Status

We have minority owned business status in the state of California. We are in process of obtaining our ISO Certification for 9001and 14001.

The Recycled Toner Cartridge Market

The recycled toner business is a multi-billion dollar industry with continuing growth. According to Lyra Research, the recycled toner market size in 2008 was $6 Billion and is expected to grow to $8.2 Billion by the year 2012. As recycled toner is considerably less expensive than retail toner while maintaining equal quality, the market is expanding annually. Moreover, the market penetration of our products is still at its early stage. Wal-Mart, Best Buy, Costco, Target, and most othermajor retailers do not yet carry recycled toner. In addition, the United Nations and U.S. federal, state and local governments have still not adopted a policy for the use of recycled toner.

Finally, recycled toner serves the protection of the environment as plastic cartridges are now being reused numerous times. More recently, the Obama administration is actively promoting clean technology and recycling of all products in the U.S. For example, under the new Stimulus Plan, tax breaks are being offered to recycling manufacturers. Staples Canada recently held an empty cartridge drive to collect one million empty cartridges for Earth Day April 22, 2009. Moreover, companies throughout the U.S. and internationally are emphasizing the use of the “green” products. Inevitably, companies and individuals will use products such as ours as it not only cheaper but helpful in preserving our economy.

For the consumer there is an effort to market “green” products, Wal-Mart will introduce a “Sustainability Index” to mark each product based on their environmental impact.

Cartridges require tremendous energy to produce and recycling cartridges will save energy for the environment and reduce pollution. Secondly, an empty cartridge takes 400 – 1000 years to biodegrade. According to the UDC, there are 400 million empty cartridges being disposed of every year in the U.S. While saving costs and helping to protect the environment, the use of refurbished toner will continue to grow in the U.S.

Our Employees

As of April 15, 2010, we employed 67 full-time employees. The following table sets forth the number of our full-time employees by function as of March 15, 2010:

| As of | |||

| April 15, | |||

| Functions | 2010 | ||

| Executives Management & Sales | 6 | ||

| Technical & Engineering Staff | 3 | ||

| Production Staff | 50 | ||

| Administrative Staff | 8 | ||

| Total | 67 |

We believe that we maintain a satisfactory working relationship with our employees and we have not experienced any significant labor disputes or any difficulty in recruiting new employees.

| ITEM 2. | DESCRIPTION OF PROPERTIES |

Facilities

Lexon leases office space at 14830 Desman Road, La Mirada, California 90638. The lease will expire in 2011 and the monthly rent is $23,000.

| ITEM 3. | LEGAL PROCEEDINGS |

To the best knowledge of management, there are two pending legal proceedings against us.

On July 14, 2008, Advanced Digital Technology Co. Ltd., a Korean corporation (“ADT”), filed a claim against Lexon and certain named individuals who are former and current officers of the Company. The claim alleges breach of an agreement to settle an earlier dispute, involving ADT's investment of $150,000 in Lexon on or about January 16, 2007 and ADT's subsequent unilateral decision to rescind and demand a refund of this investment. The total amount of damages claimed under the pending lawsuit is the investment amount of $150,000 plus filing costs, interest and attorney fees for an aggregate amount of $178,522. On or about May 2, 2009, Lexon became aware of a default judgment entered in the amount above. Such judgment was entered on December 22, 2009. On or about May 8, 2009, Lexon has retained the law firm of Smith, Chapman & Campbell for the purpose of setting aside the default judgment as the Company was never in receipt of the notice of default entry. On or about July 21, 2009, the court set aside the default as the court agreed that service was never properly served. We are currently in the discovery stage of the proceedings.

On September 5, 2008, Vivien and David Bollenberg, a current shareholder (the “Bollenbergs”), filed a claim against Lexon and other third parties, including Byung Hwee Hwang (also referred to as "Ben Hwang") and other financial agents and institutions involved in the alleged fraudulent transaction. The lawsuit is currently pending in the Orange County Superior Court in Santa Ana, California. The filed complaint alleges that Ben Hwang together with his representatives, including his accountant, escrow agent and real estate agent/broker, made certain representations to and solicited the Bollenbergs to make an investment in several companies and ventures including Lexon with the intent to misappropriate the solicited funds for personal use. The Bollenbergs allege that they invested a total of $1,500,000 among and between the various companies and ventures recommended by Ben Hwang, of which investment amount approximately $550,000 was invested in Lexon ($150,000 for 600,000 shares at $0.25 per share and $400,000 initially invested in Lexon Korea and later converted into 1,150,000 shares in Lexon for a total of 1,750,000 shares in Lexon). The final disposition of this case has not yet been resolved.

| ITEM 4. | SUBMISSION OF MATTERS TO A VOTE OF SECURITIES HOLDERS |

None.

PART II

| ITEM 5. | MARKET FOR COMMON EQUITY AND RELATED STOCKHOLDER MATTERS |

As of April 15, 2010, we have approximately 380 shareholders and we have 515,289,722 shares outstanding.

Unregistered Sales of Securities

On November 3, 2009, 4,200,000 shares were issued to Fresh Cure Inc. in exchange for assets as per our 8k dated November 4, 2009.

On November 3, 2009, 2,500,000 shares were issued to Stacey Park for $50,000.00. Use of proceeds were for working capital purposes.

On November 9, 2009, 50,000 shares were issued to Todd W. Henreckson for $1,000.00. Use of proceeds were for working capital purposes.

On November 9, 2009, 12,500 shares were issued to Michael T. Henreckson for $250.00. Use of proceeds were for working capital purposes.

On November 9, 2009, 5,000 shares were issued to Sara L. Henreckson for $100.00. Use of proceeds were for working capital purposes.

On November 9, 2009, 5,000 shares were issued to Jonathan D. Henreckson for $100.00. Use of proceeds were for working capital purposes.

On November 9, 2009, 2,500 shares were issued to Rebecca M. Henreckson for $50.00. Use of proceeds were for working capital purposes.

On November 9, 2009, 50,000 shares were issued to Todd Henreckson for $1,000.00. Use of proceeds were for working capital purposes.

On November 10, 2009, 500,000 shares were issued to Paul N. Carson for $10,000.00. Use of proceeds were for working capital purposes.

On November 11, 2009, 100,000 shares were issued to Joshua Gluckman for $2,000.00. Use of proceeds were for working capital purposes.

On November 11, 2009, 200,000 shares were issued to Kimberly Yoshizawa for $4,000.00. Use of proceeds were for working capital purposes.

On November 12, 2009, 25,000 shares were issued to Winton Low for $500.00. Use of proceeds were for working capital purposes.

On November 13, 2009, 5,000,000 shares were issued to Peter Pak for $100,000.00. Use of proceeds were for working capital purposes.

On November 13, 2009, 50,000 shares were issued to Peter Park for $1,000.00. Use of proceeds were for working capital purposes.

On November 13, 2009, 2,500,000 shares were issued to Samuel Shim for $50,000.00. Use of proceeds were for working capital purposes.

On November 13, 2009, 1,500,000 shares were issued to Samuel Shim for $30,000.00. Use of proceeds were for working capital purposes.

On November 16, 2009, 50,000 shares were issued to The Wurtzer Trust for $100,000.00. Use of proceeds were for working capital purposes.

On November 16, 2009, 375,000 shares were issued to Ji Soon Lee for $7,500.00. Use of proceeds were for working capital purposes.

On November 16, 2009, 75,000 shares were issued to Sarah Kim for $1,500.00. Use of proceeds were for working capital purposes.

On November 20, 2009, 100,000 shares were issued to Carol Gluckman for $30,000.00. Use of proceeds were for working capital purposes.

On January 25, 2010, 5,000,000 shares were issued to Fresh Cure Inc. in exchange for assets as per our 8k dated January 28, 2010.

On February 3, 2010, 250,000 shares were issued to Juan Wozniak for $5,000.00. Use of proceeds were for working capital purposes.

On February 16, 2010, 300,000 shares were issued to Kyungwhan Doh for $6,000.00. Use of proceeds were for working capital purposes.

| ITEM 6. | SELECTED FINANCIAL STATEMENT DATA |

None.

| ITEM 7. | MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

Cautionary Statement Regarding Forward-Looking Statements

This report may contain “forward-looking” statements. Examples of forward-looking statements include, but are not limited to: (a) projections of revenues, capital expenditures, growth, prospects, dividends, capital structure and other financial matters; (b) statements of plans and objectives of our management or Board of Directors; (c) statements of future economic performance; (d) statements of assumptions underlying other statements and statements about us and our business relating to the future; and (e) any statements using the words “anticipate,” “expect,” “may,” “project,” “intend” or similar expressions. All forward-looking statements included in this Report are based on information available to the Company on the date hereof, and the Company assumes no obligation to update any such forward-looking statement. It is important to note that the Company's actual results could differ materially from those in such forward-looking statements. Additionally, the following discussion and analysis should be read in conjunction with the Financial Statements and notes thereto appearing elsewhere in this Report.

General

Effective December 8, 2004, we acquired a majority control (90.16%) of Techone Company, Ltd., a Republic of South Korea corporation (“Techone”), through an investment of $1,585,000 financed through the sale of our restricted common stock to two accredited investors. During February 2006, the Company changed the name of Techone to Lexon Semiconductor Corporation (“Lexon Semi”). Lexon Semi is a corporation that manufactures and sells Low Temperature Cofired Ceramic (LTCC) components. The Company has operated Lexon Semi as a majority-owned subsidiary and the business of Lexon Semi has been the operating business of the Company.

On October 22, 2009, Lexon successfully completed a reverse merger with Paragon Toner Inc. Thereafter our source of liquidity stemmed from the operation of the existing business of Paragon.

Results of Operations for the Year Ended December 31, 2009 compared to December 31, 2008

Revenues. Total revenues during the year ended December 31, 2009 were $5,446,742 compared to $6,707,301 for the year ended December 31, 2008.

Operating Expenses. Total operating expenses during the year ended December 31, 2009 were $1,446,036 in selling, general and administrative expenses compared to $1,588,655 for the year ended December 31, 2008.

Other Income (Expense). Other income for the year ended December 31, 2009 was $374,595 which consisted of interest expense of $47,903 and gain on forgiveness of debt of 418,970 compared to other income of ($66,039) for the year ended in 2008 which consisted of interest expense of $66,039.

Liquidity and Capital Resources

At December 31, 2009, we had current assets of $1,386,702 and current liabilities of $1,476,763, for negative working capital of $90,061. Current assets consisted solely of cash and cash equivalents, accounts receivables, inventory and other current assets. We also had net property and equipment of $112,392, intangibles, net of amortization of $276,365, security deposits of $20,748 and goodwill of $3,214,289 for total assets of $5,200,496.

Current liabilities at December 31, 2009, consisted of accounts payable of $552,634, accounts payable-related parties of $91,960, line of credit of $450,000, current accrued expenses of $110,747, notes payable of $249,534, capital lease obligations of $21,888, for total current liabilities of $1,476,763. We also had contingent liabilities of $274,610.

For the year ended December 31, 2009, net cash flows used in operating activities totaled $180,096, compared to net cash flows provided by operating activities of $488,988 in the prior year.

For the year ended December 31, 2009, there was $53,089 cash provided by investing activities compared to the net cash used in investing activities of $210,859.

Net cash provided by financing activities for the year ended December 31, 2009 was $108,405, compared net cash used of $209,970 for the prior year which consisted of cash paid on notes payable of $89,268, payment on capital lease obligations of $32,152 and distribution to shareholder of $193,285, offset by proceeds from line of credit of $104,735.

Going forward, with a viable cash flow positive operation in place, we expect to fund our business with cash flow from our current

business. To date, we have retained earnings of $130,510 and a working capital deficit of approximately $90,000 at December 31, 2009.

| ITEM 8. | FINANCIAL STATEMENTS |

Our financial statements for the reporting period are set forth immediately following the signature page to this form 10-K.

| ITEM 9. | CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE |

None

| ITEM 9 A. | CONTROLS AND PROCEDURES |

Evaluation of Disclosure Controls and Procedures

Our Chief Executive Officer and Chief Financial Officer (the “Certifying Officers”) are responsible for establishing and maintaining our disclosure controls and procedures. The Certifying Officers have designed such disclosure controls and procedures to ensure that material information is made known to them, particularly during the period in which this report was prepared. The Certifying Officers have evaluated the effectiveness of our disclosure controls and procedures as of the end of the period covered by this Report. Based on that evaluation, the Certifying Officers have concluded that our disclosure controls and procedures were not effective at the reasonable assurance level due to the material weakness described below.

Management’s Report on Internal Control Over Financial Reporting

Our management is responsible for establishing and maintaining adequate internal control over financial reporting (as defined in Rule 13a-15(f) under the Exchange Act) and for assessing the effectiveness of our internal control over financial reporting. Our internal control system is designed to provide reasonable assurance to our management and board of directors regarding the preparation and fair presentation of published financial statements in accordance with United States’ generally accepted accounting principles.

Our internal control over financial reporting is supported by written policies and procedures that pertain to the maintenance of records that, in reasonable detail, accurately and fairly reflect the transactions and dispositions of our assets; provide reasonable assurance that transactions are recorded as necessary to permit preparation of financial statements in accordance with generally accepted accounting principles and that our receipts and expenditures are being made only in accordance with authorizations of our management and our board of directors; and provide reasonable assurance regarding prevention or timely detection of unauthorized acquisition, use or disposition of our assets that could have a material effect on our financial statements.

Our management has assessed the effectiveness of our internal control over financial reporting as of the end of our most recent fiscal year. Management’s assessment included an evaluation of the design of our internal control over financial reporting and testing of the operational effectiveness of our internal control over financial reporting. Based on this assessment, our management has concluded that our internal control over financial reporting was not effective at the reasonable assurance level due to the material weaknesses described below.

In light of the material weaknesses described below, we performed additional analysis and other post-closing procedures to ensure our consolidated financial statements were prepared in accordance with generally accepted accounting principles. Accordingly, we believe that the consolidated financial statements included in this Report fairly present, in all material respects, our financial condition, results of operations and cash flows for the periods presented.

A material weakness is a control deficiency (within the meaning of the Public Company Accounting Oversight Board (“PCAOB”) Auditing Standard No. 2) or combination of control deficiencies that result in more than a remote likelihood that a material misstatement of the annual or interim financial statements will not be prevented or detected. The Certifying Officers have identified the following three material weaknesses which have caused the Certifying Officers to conclude that our disclosure controls and procedures were not effective at the reasonable assurance level:

1. We do not yet have written documentation of our internal control policies and procedures. Written documentation of key internal controls over financial reporting is a requirement of Section 404 of the Sarbanes-Oxley Act and will be applicable to us for the year ending December 31, 2008. The Certifying Officers evaluated the impact of our failure to have written documentation of our internal controls and procedures on our assessment of our disclosure controls and procedures and has concluded that the control deficiency that resulted represented a material weakness.

2. We do not have a sufficient segregation of duties within accounting functions, which is a basic internal control. Due to our size and nature, segregation of all conflicting duties may not always be possible and may not be economically feasible. However, to the extent possible, the initiation of transactions, the custody of assets and the recording of transactions should be performed by separate

individuals. The Certifying Officers evaluated the impact of our failure to have segregation of duties on our assessment of our disclosure controls and procedures and has concluded that the control deficiency that resulted represented a material weakness.

To remediate the material weaknesses in our disclosure controls and procedures identified above, in addition to working with our independent auditors, we have continued to refine our internal procedures to begin to implement segregation of duties and to prepare a written documentation of our internal control policies and procedures.

This Report does not include an attestation report of our independent registered public accounting firm regarding internal control over financial reporting. Management’s report was not subject to attestation by our independent registered public accounting firm pursuant to temporary rules of the SEC that permit the Company to provide only management’s report in this Annual Report.

There were no changes in our internal control over financial reporting that occurred during our most recent fiscal quarter that have materially affected, or reasonably likely to materially affect, our internal control over financial reporting.

| ITEM 9 B. | OTHER INFORMATION |

None.

PART III

| ITEM 10 . | DIRECTORS AND EXECUTIVE OFFICERS, PROMOTERS, AND CONTROL PERSONS; COMPLIANCE WITH SECTION 16(a) OF THE EXCHANGE ACT |

Directors and Executive Officers

The following table sets forth certain information relating to our directors and executive officers as of April 15, 2010. The business address of all of our directors and executive officers is our registered office at 14830 Desman Road, La Mirada, CA 90638.

| Name | Age | Position |

| James Park | 42 | President, Chief Executive Officer and Chairman of the Board of Directors |

| Young Won | 48 | Chief Operating Officer and Director |

| Bong S. Park | 75 | Chief Financial Officer and Director |

| Hyung Soon Lee | 58 | Director |

James Park is the founder of We and has worked at the company since 1993. Mr. Park was instrumental to our growth from a small independent business. Mr. Park is a graduate of the University of California of Los Angeles.

Young Won has worked at We for the last 14 years. Mr. Won is in charge of the production, operation, research and development of the company. He is has been integral in the success of We. Previously, he worked for the Los Angeles Metropolitan Water District as a metallurgical engineer. Mr. Wonreceived a B.S. in mechanical engineering from Korea University. He also graduated from the University of Southern California with an M.S.in material science.

Bong S. Park was the Chief Financial Officer of the Company since 1997. He was previously the CEO of Tokyo Printing Ink, Corp. USA from 1985-1997. His experience as a seasoned executive and his extensive knowledge in the ink and toner industryhas been instrumental for the growth of the Company. Mr. Parkreceived a B.A. degree in business administration from Korea University.

Compliance with Section 16(a) of the Exchange Act

Section 16(a) of the Securities and Exchange Act of 1934, as amended, requires our directors and certain officers, as well as persons who own more than 10% of a registered class of our equity securities, (“Reporting Persons”) to file reports of ownership and changes in ownership on Forms 3, 4 and 5 with the Securities and Exchange Commission. To the best of our knowledge, we believe that all Reporting Persons have complied on a timely basis with all filing requirements applicable to them.

Code of Ethics

None.

| ITEM 11. | EXECUTIVE COMPENSATION |

Summary Compensation Table— Fiscal Year Ended December 31, 2009

The following table sets forth information concerning all cash and non-cash compensation awarded to, earned by or paid to the named persons for services rendered in all capacities during the noted periods. No other executive officers received total annual salary and bonus compensation in excess of $100,000 during the fiscal year ended December 31, 2009.

| Name and | Stock | Option | All Other | |||||||||||||||

| Principal | Salary | Awards | Awards | Compensation | Total | |||||||||||||

| Position (1) | ($) | Bonus ($) | ($) | ($) | ($) | ($) | ||||||||||||

| James Park | 98,000 | 0 | 0 | 0 | 0 | 98,000 | ||||||||||||

| Young Won | 98,000 | 0 | 0 | 0 | 0 | 98,000 | ||||||||||||

| Bong S. Park | 98,000 | 0 | 0 | 0 | 0 | 98,000 |

Note: The above three executives became Executive Officers of the Company as of October 22, 2010 which is the effective date of the Reverse Merger between Lexon Technologies Inc. and Paragon Toner Inc.

Employment Agreements

As the incoming CEO of the Company, Mr. Park has entered into a new employment contract with the Company. Under the terms of the contract, he will receive a salary of $168,000 for a one-year term. No bonus or stock options are included in the contract. Any change in compensation will be determined by the Board of Directors after conclusion of the initial one-year term.

Director Compensation

For the fiscal year 2009, no director received compensation for services as a director.

Compensation Committee Interlocks and Insider Participation

During the last fiscal year we did not have a standing Compensation Committee. The Board was responsible for the functions that would otherwise be handled by the compensation committee.

Indemnification of Directors and Executive Officers and Limitation of Liability

The General Corporation Law of Delaware, Section 102(b)(7) provides that directors, officers, employees or agents of Delaware corporations are entitled, under certain circumstances, to be indemnified against expenses (including attorneys’ fees) and other liabilities actually and reasonably incurred by them in connection with any suit brought against them in their capacity as a director, officer, employee or agent, if they acted in good faith and in a manner they reasonably believed to be in or not opposed to the best interests of the corporation, and with respect to any criminal action or proceeding, if they had no reasonable cause to believe their conduct was unlawful. This statute provides that directors, officers, employees and agents may also be indemnified against expenses (including attorneys’ fees) actually and reasonably incurred by them in connection with a derivative suit brought against them in their capacity as a director, if they acted in good faith and in a manner they reasonably believed to be in or not opposed to the best interests of the corporation, except that no indemnification may be made without court approval if such person was adjudged liable to the corporation

Compensation Pursuant to Plans

None.

Pension Table

Not Applicable.

Other Compensation

None.

Compensation of Directors

Our directors do not receive any cash compensation, but are entitled to reimbursement of their reasonable expenses incurred in attending directors’ meetings.

| ITEM 12 . | SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT |

The following table sets forth as of April 15, 2010 the name and address and the number of shares of our Common Stock, par value $0.001 per share, held of record or beneficially by each person who held of record, or was known by us to own beneficially, more than 5% of the shares of our Common Stock issued and outstanding.

| Number of | ||||||

| Shares | Percentage | |||||

| Beneficially | Beneficially | |||||

| Name | Owned | Owned | ||||

| James Park | 198,406,990 | 38.50% | ||||

| Young Won | 99,030,531 | 19.22% | ||||

| Hyung Soon Lee | 28,828,333 | 5.59% |

Securities Ownership of Officers and Directors

The following table sets forth certain information relating to the shareholdings of our Executive and Directors. The business address is our registered office at 14830 Desman Road, La Mirada, CA 90638.

| Number of | ||||||

| Shares | Percentage | |||||

| Beneficially | Beneficially | |||||

| Name | Owned | Owned | ||||

| Management and Directors | ||||||

| James Park (CEO and Director) | 198,406,990 | 38.50% | ||||

| Young Won (COO and Director) | 99,030,531 | 19.22% | ||||

| Hyung Soon Lee (Director) | 28,828,333 | 5.59% | ||||

| Total of Management and Directors | 326,265,854 | 63.31% |

| ITEM 13 . | CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS |

Our directors are not independent as that term is defined under the Nasdaq Marketplace Rules.

Joon Ho Chang, a former director of the Company, received 8,000,000 shares of Common Stock as a fee for professional services rendered in the merger transaction.

| ITEM 14. | PRINCIPAL ACCOUNTANT FEES AND SERVICES |

Choi, Kim & Park LLP (“CKP”)

CKP was our independent auditor and examined our financial statements for the year ended December 31, 2009, and reviewed the financial statements included in our quarterly reports on Form 10-QSB in the year 2009. The audit and review of the annual financial statements for the year ended December 31, 2008 was performed by Choi, Kim and Park LLP (“CKP”), as our new independent auditor as of April 24, 2009

Audit Fees

CKP was paid aggregate fees of $6,000 for the year ended December 31, 2008 for professional services rendered for the reviews of the financial statements included in our quarterly reports on Form 10-QSB during this period.

Audit for Reverse Merger

CKP was paid $40,000 in total for the audit of Paragon Toner Inc. for the filing of the Form 8-K on October 8, 2009 which was necessary to complete the reverse merger.

Audited-Related Fees

CKP was not paid additional fees for either the year ended December 31, 2009, or the fiscal year ended December 31, 2009 for assurance and related services reasonably related to the performance of the audit or review of our financial statements.

All Other Fees

CKP was not paid any other fees for professional services during the year ended December 31, 2009 or the fiscal year ended December 31, 2008.

PART IV

| ITEM 15. | EXHIBITS |

(a)(1) FINANCIAL STATEMENT SCHEDULES. The following financial statement schedules are included as part of this report.

(a)(2) EXHIBITS. The following exhibits are included as part of this report:

SIGNATURES

In accordance with Section 13 or 15(d) of the Exchange Act, the registrant caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| LEXON TECHNOLOGIES, INC. | ||

| Date: April 15, 2010 | By: | /s/ James Park |

| James Park | ||

| President, Chief Executive Officer | ||

In accordance with the Exchange Act, this report has been signed below by the following persons on behalf of the registrant and in the capacities and on the dates stated.

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Directors and Stockholders of Lexon Technologies, Inc.

We have audited the accompanying balance sheets of Lexon Technologies, Inc. the “Company”) as of December 31, 2009 and 2008 and the related statements of operations, stockholders’ equity, and cash flows for the years then ended. These financial statements are the responsibility of the Company's management. Our responsibility is to express an opinion on these financial statements based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, such financial statements present fairly, in all material respects, the financial position of Lexon Technologies, Inc. as of December 31, 2009 and 2008, and the results of their operations and cash flows for the years then ended, in conformity with accounting principles generally accepted in the United States of America.

/s/ Choi, Kim & Park LLP

Los Angeles, California

Certified Public Accountants

April 12, 2010

LEXON TECHNOLOGIES, INC.

Balance Sheets

December 31, 2009 and 2008

| ASSETS | ||||||

| December 31, | December 31, | |||||

| 2009 | 2008 | |||||

| Current assets: | ||||||

| Cash and cash equivalents | $ | 61,661 | $ | 80,263 | ||

| Accounts receivable, net | 468,821 | 464,789 | ||||

| Inventory | 838,220 | 458,936 | ||||

| Other current assets | 18,000 | 1,800 | ||||

| Total current assets | 1,386,702 | 1,005,788 | ||||

| Due from related parties | 190,000 | 273,650 | ||||

| Property and equipment, net | 112,392 | 214,659 | ||||

| Other assets: | ||||||

| Intangibles, net of amortization | 276,365 | 30,284 | ||||

| Security deposits | 20,748 | 20,748 | ||||

| Other assets | - | 245 | ||||

| Goodwill | 3,214,289 | - | ||||

| Total other assets | 3,511,402 | 51,277 | ||||

| Total Assets | $ | 5,200,496 | $ | 1,545,374 |

The accompanying notes are an integral part of the financial statements.

| LEXON TECHNOLOGIES, INC. |

| Balance Sheets |

| December 31, 2009 and 2008 |

| LIABILITIES AND STOCKHOLDERS’ EQUITY | ||||||

| December 31, | December 31, | |||||

| 2009 | 2008 | |||||

| Current liabilities: | ||||||

| Accounts payable | $ | 552,634 | $ | 492,804 | ||

| Due to related parties | 91,960 | - | ||||

| Line of credit | 450,000 | 600,000 | ||||

| Current portion of notes payable | 249,534 | 92,592 | ||||

| Current portion of capital lease obligations | 21,888 | 35,761 | ||||

| Accrued expenses | 110,747 | 49,436 | ||||

| Total current liabilities | 1,476,763 | 1,270,593 | ||||

| Contingent liabilities | 274,610 | - | ||||

| Long-term liabilities: | ||||||

| Notes payable, net of current portion | 99,460 | 47,996 | ||||

| Capital lease obligations, net of current portion | 28,561 | 50,449 | ||||

| Deferred rent | 53,398 | 57,984 | ||||

| Total long-term liabilities | 181,419 | 156,429 | ||||

| Total liabilities | 1,932,792 | 1,427,022 | ||||

| Stockholders’ equity: | ||||||

| Common

stock - $0.001 par value;

2,000,000,000 shares authorized, 499,739,721 and 34,183,778 shares issued and outstanding as of December 31, 2009 and 2008, respectively |

499,740 |

34,184 |

||||

| Additional paid-in capital | 2,737,454 | 94,816 | ||||

| Stock subscription receivable | (100,000 | ) | - | |||

| Retained earnings (accumulated deficit) | 130,510 | (10,648 | ) | |||

| Total stockholders’ equity | 3,267,704 | 118,352 | ||||

| Total liabilities and stockholders’ equity | $ | 5,200,496 | $ | 1,545,374 |

The accompanying notes are an integral part of the financial statements.

| LEXON TECHNOLOGIES, INC. |

| Statements of Operations |

| For the Years Ended December 31, 2009 and 2008 |

| For the Years Ended | ||||||

| December 31, | ||||||

| 2009 | 2008 | |||||

| Net sales | $ | 5,446,742 | $ | 6,707,301 | ||

| Cost of goods sold | 3,899,328 | 4,990,324 | ||||

| Gross profits | 1,547,414 | 1,716,977 | ||||

| Selling, general and administrative expenses | 1,446,036 | 1,588,655 | ||||

| Income from operations | 101,378 | 128,322 | ||||

| Other income (expenses): | ||||||

| Gain on forgiveness of debt from discontinued operations | 418,970 | - | ||||

| Interest expense | (47,903 | ) | (66,039 | ) | ||

| Other income, net | 3,528 | - | ||||

| Net other income(expense) | 374,595 | (66,039 | ) | |||

| Income before income tax provision | 475,973 | 62,283 | ||||

| Provision for income taxes | 3,883 | 2,249 | ||||

| Net income | $ | 472,090 | $ | 60,034 | ||

The accompanying notes are an integral part of the financial statements.

| LEXON TECHNOLOGIES, INC. |

| Statement of Stockholders' Equity |

| For the Years Ended December 31, 2009 and 2008 |

| Common Stock | ||||||||||||||||||

| Retained | ||||||||||||||||||

| Additional | Earnings | Stock | Total | |||||||||||||||

| Paid-in | (Accumulated | Subscription | Stockholders’ | |||||||||||||||

| Shares | Amounts | Capital | Deficit) | Receivable | Equity | |||||||||||||

| Balance at January 1,2008 |

34,183,778 |

$ | 34,184 |

$ | 94,816 |

$ | 218,757 |

$ | - |

$ | 347,757 |

|||||||

| Distributions to stockholders for the year 2008 |

- |

- |

- |

(289,439 |

) | - |

(289,439 |

) | ||||||||||

| Net income for the year 2008 |

- |

- |

- |

60,034 |

- |

60,034 |

||||||||||||

| Balance at December 31, 2008 |

34,183,778 |

34,184 |

94,816 |

(10,648 |

) | - |

118,352 |

|||||||||||

| Issuance of common stock for conversion of notes payable |

68,178,333 |

68,178 |

340,892 |

- |

- |

409,070 |

||||||||||||

| Merger related equity transactions |

347,448,444 |

347,448 |

1,642,426 |

- |

- |

1,989,874 |

||||||||||||

| Issuance of common stock |

13,062,500 |

13,063 |

248,187 |

- |

- |

261,250 |

||||||||||||

| Issuance of stock subscription |

16,666,666 |

16,667 |

83,333 |

- |

(100,000 |

) | - |

|||||||||||

| Stock award | 16,000,000 | 16,000 | 80,000 | - | - | 96,000 | ||||||||||||

| Acquisition of intangibles with common stock |

4,200,000 |

4,200 |

247,800 |

- |

- |

252,000 |

||||||||||||

| Distributions to stockholders for the year 2009 |

- |

- |

- |

(330,932 |

) | - |

(330,932 |

) | ||||||||||

| Net income for the year 2009 |

- |

- |

- |

472,090 |

- |

472,090 |

||||||||||||

| Balance at December 31, 2009 |

499,739,721 |

$ | 499,740 |

$ | 2,737,454 |

$ | 130,510 |

$ | (100,000 |

) | $ | 3,267,704 |

||||||

The accompanying notes are an integral part of the financial statements.

| LEXON TECHNOLOGIES, INC. |

| Statements of Cash Flows |

| For the Years Ended December 31, 2009 and 2008 |

| For the Years Ended | ||||||

| December 31, | ||||||

| 2009 | 2008 | |||||

| Cash flows from operating activities: | ||||||

| Net income | $ | 472,090 | $ | 60,034 | ||

| Adjustments to reconcile net income | ||||||

| to net cash provided by (used in) operating activities: | ||||||

| Bad debt expense | 85,611 | 247,793 | ||||

| Depreciation and amortization | 138,747 | 93,772 | ||||

| Gain on forgiveness of debt from discontinued operations | (418,970 | ) | - | |||

| Provision for inventory obsolescence | - | 6,143 | ||||

| Changes in assets and liabilities: | ||||||

| Accounts receivable | (89,643 | ) | (4,506 | ) | ||

| Inventory | (379,284 | ) | 190,039 | |||

| Other current assets | (16,200 | ) | (1,800 | ) | ||

| Other assets | 245 | - | ||||

| Accounts payable | 32,983 | (69,730 | ) | |||

| Accrued expenses | (1,089 | ) | (47,659 | ) | ||

| Deferred rent | (4,586 | ) | 14,902 | |||

| Total adjustments | (652,186 | ) | 428,954 | |||

| Net cash provided by (used in) operating activities | (180,096 | ) | 488,988 | |||

| Cash flows from investing activities: | ||||||

| Due from related party | 83,650 | (197,855 | ) | |||

| Acquisition of property | (5,561 | ) | (13,004 | ) | ||

| Acquisition of intangible | (25,000 | ) | - | |||

| Net cash provided by (used in) investing activities | 53,089 | (210,859 | ) | |||

| Cash flows from financing activities: | ||||||

| Net proceeds from line of credit | - | 104,735 | ||||

| Net payments on notes payable | (111,577 | ) | (89,268 | ) | ||

| Payments on capital lease obligations | (35,761 | ) | (32,152 | ) | ||

| Issuance of common stock | 261,250 | - | ||||

| Issuance of Paragon stock (prior to Merger) | 325,425 | - | ||||

| Distributions to stockholder | (330,932 | ) | (193,285 | ) | ||

| Net cash provided by (used in) financing activities | 108,405 | (209,970 | ) | |||

| Net increase (decrease) in cash | (18,602 | ) | 68,159 | |||

| Cash at beginning of year | 80,263 | 12,104 | ||||

| Cash at end of year | $ | 61,661 | $ | 80,263 | ||

The accompanying notes are an integral part of the financial statements.

| LEXON TECHNOLOGIES, INC. |

| Statements of Cash Flows |

| For the Years Ended December 31, 2009 and 2008 |

| For the Years Ended | ||||||

| December 31, | ||||||

| 2009 | 2008 | |||||

| Supplemental disclosures: | ||||||

| Cash paid during the year: | ||||||

| Income taxes | $ | 2,247 | $ | 4,276 | ||

| Interest expense | $ | 47,903 | $ | 66,039 | ||

| Noncash investing and financing activities: | ||||||

| Common stock issued for merger activity | $ | 1,989,874 | $ | - | ||

| Common stock issued pursuant to conversion of notes payable | $ | 409,070 | $ | - | ||

| Common stock issued pursuant to acquisition of intangible | $ | 252,000 | $ | - | ||

| Conversion of line of credit to note payable | $ | 150,000 | $ | - | ||

| Conversion of

due to related parties to distributions to

Stockholder |

$ | - |

$ | 96,154 |

||

The accompanying notes are an integral part of the financial statements.

| LEXON TECHNOLOGIES, INC. |

| Notes to Consolidated Financial Statements |

| December 31, 2009 and 2008 |

Note 1 - Nature of Business

Lexon Technologies, Inc. ("the Company" or "Lexon") was incorporated in April 1989 under the laws of state of Delaware, and owns 90.16% of Lexon Semiconductor Corporation ("Lexon Semi" or formerly known as Techone Co., Ltd ("Techone")) which had developed and manufactured Low Temperature Cofired Ceramic (LTCC) components, including LTCC wafer probe cards, LTCC circuit boards, LTCC Light Emitting Diode (LED) displays and related products for the semiconductor testing and measurement, custom Printed Circuit Board (PCB), and cellular phone industries.

Initially registered as California Cola Distributing Company, Inc, the Company changed its name twice; first to Rexford, Inc. in October 1992, and to the current name in July 1999.

In July 1999, Lexon acquired 100% of the outstanding common stock of Chicago Map Corporation (CMC) in exchange for 10,500,000 shares of the Company's common stock through a reverse acquisition accompanied by a recapitalization. The surviving entity, Lexon, reflected the assets and liabilities of Lexon and CMC at their historical book values. Lexon dissolved CMC in 2002.

In April 2002, Lexon acquired 100% of the outstanding common stock of Phacon Corporation (Phacon) in exchange for 17,500,000 shares of Company's common stock through a reverse acquisition accompanied by a recapitalization. As part of the agreement, the Company elected a 1 for 10 reverse stock split and the acquired shares of Phacon were entirely canceled leaving the Company as the surviving entity.

In March 2003, the Company incorporated Lexon Korea Corporation (“Lexon Korea”) as a wholly-owned subsidiary in Korea for the purpose of entering into potential business combinations with Korean operating entities. Lexon Korea was reorganized in August 2005, and as a result, the Company’s equity share in Lexon Korea was reduced to 10%.

In December 2004, the Company acquired 90.16% of the voting stock of Techone Company, Ltd, a company in Korea, by investing $1,588,000. The Company recognized goodwill of $1,851,692 in the acquisition. The Company acquired Techone to develop it as the Company’s core operating business in Korea for manufacturing and selling LTCC related products. However, the development of the LTCC related products was not successful, and the operations of Techone became highly leveraged financially. In August 2005, certain creditors filed an involuntary foreclosure and sold Techone’s assets through public auction to satisfy secured debts. This disposal of assets resulted in a gain $1,315,469 for the year ended December 31, 2005. In February 2006, Techone changed its name to Lexon Semiconductor Corporation and all of its operation has been suspended due to lack of operating working capital. Lexon Semi was dissolved on October 28, 2009 based on a decision of shareholders meeting. Lexon Semi has $241,000 of due to related party and $415,000 of liabilities relation to discontinued operations as of September 30,2009.

On October 7, 2009, Paragon Toner, Inc. (Paragon), a California corporation, entered into an Agreement and Plan of Merger (the “Merger Agreement”) with the Company whereby the Company issued 347,448,444 shares of common stock (the “Common Stock”) of the Company (the “Acquisition Shares”) to the shareholders of Paragon, representing approximately 72% of the issued and outstanding Common Stock after completion of the merger in October 2009. The effective date of the Merger was October 22, 2009 (“Effective Date”). The Company has decided to maintain the name of the predecessor company. The Merger has been accounted for as a recapitalization of Paragon with Paragon as the acquirer (reverse merger).

Shortly after the Merger, Lexon Semi was dissolved. The Company’s sole line of business is now in manufacturing, marketing and selling of recycled monochrome and color toner cartridges for laser printers and other related devices.

LEXON TECHNOLOGIES, INC.

Notes to Consolidated

Financial Statements

December 31, 2009 and 2008

Note 2 - Summary of Significant Accounting Policies

This summary of significant accounting policies of the Company is presented to assist in understanding the Company’s financial statements. The financial statements and notes are representations of the Company’s management, who is responsible for their integrity and objectivity. These accounting policies conform to accounting principles generally accepted in the United States of America and have been consistently applied in the preparation of the financial statements.

Use of Estimates

The preparation of the financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the amounts reported in the financial statements and accompanying notes. Estimates are primarily used for depreciation of property and equipment, amortization of intangible assets, allowances for doubtful accounts and inventory valuation. Actual results could differ from those estimates.

Revenue Recognition

The Company recognizes revenues from product sales when earned. Specifically, revenue is recognized when persuasive evidence of an arrangement exists, delivery has occurred (or services have been rendered), the price is fixed or determinable, and collectability is reasonably assured. Revenue is not recognized until title and risk of loss have transferred to the customer. The shipping terms for the majority of the Company’s revenue arrangements are FOB (free on board) destination. Revenue is recorded net of customer returns, allowances and discounts that occur under arrangements established with customers.

Cash and Cash Equivalents

The Company considers all highly liquid investments purchased with original maturities of three months or less to be categorized as cash and cash equivalents.

Allowance for Doubtful Accounts

The allowance for doubtful accounts is computed based upon the management’s estimate of uncollectible accounts and historical experience. The Company performs ongoing credit evaluations of its customers to estimate potential credit losses. Amounts are written off against the allowance in the period the Company determines that the receivable is uncollectible. As a result, the Company wrote off $0 and $247,793 of uncollectible amount for the years ended December 31, 2009 and 2008, respectively. The allowance for doubtful accounts is $85,611 and $0 as of December 31, 2009 and 2008, respectively.

Inventory

Inventory is stated at the lower of cost or market. Cost is determined by the first-in, first-out (FIFO) method. Appropriate consideration is given to obsolescence, slow moving items and other factors in evaluating net realizable value.

Property and Equipment

Property and equipment are stated at cost.The straight-line method is used to calculate depreciation over their estimated useful lives ranging as follows:

LEXON TECHNOLOGIES, INC.

Notes to Consolidated

Financial Statements

December 31, 2009 and 2008

| Automobile | 3 years |

| Furniture & fixture | 5 to 7 years |

| Leasehold improvement | 5 years |

| Machinery and equipment | 5 years |

Leasehold improvements are depreciated to expense over the shorter of the life of the improvement or the remaining lease term. Capital expenditures that enhance the value or materially extend the useful life of the related assets are reflected as additions to property and equipment. Expenditures for repairs and maintenance are charged to expense as incurred. Upon a sale or disposition of assets, a gain or a loss is included in the statement of operations.

Impairment of Long-lived Assets

The Company periodically reviews the recoverability of its long-lived assets using the methodology prescribed in accounting guidance now codified as FASB ASC Topic 360, “Property, Plant and Equipment.” The Company also reviews these assets for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable. Recoverability of these assets is determined by comparing the forecasted undiscounted future net cash flows from the operations to which the assets relate, based on management’s best estimates using appropriate assumptions and projections at the time, to the carrying amount of the assets. If the carrying value is determined not to be recoverable from future operating cash flows, the asset is deemed impaired and an impairment loss is recognized equal to the amount by which the carrying amount exceeds the estimated fair value of the asset. In management’s opinion, no such impairment existed as of December 31, 2009 and 2008.

Accrued Expenses

The Company’s accrued expenses consist of amounts payable for salaries, payroll taxes and sales taxes.

Deferred Rent

The Company recognizes rent expense equal to the total of the payments and free rent received due over the lease term, divided by the number of months of the lease term applying the straight-line method. The difference between rent expense recorded and the amount paid is credited or charged to deferred rent.

Shipping and Handling

Certain shipping and handling fees are charged to customers and these are classified as revenue. The costs associated with all shipping to customers are recorded as operating expenses. Shipping expenses for the years ended December 31, 2009 and 2008 amounted to $183,602 and $157,450, respectively.

Income Taxes

The Company elected to be subject to the S corporation provisions of the Internal Revenue Code for federal and state income tax purposes effective January 27, 2004. Accordingly, as an S corporation, the Company’s taxable income or losses and applicable tax credits are passed through to its shareholder and reported on shareholder’s

LEXON TECHNOLOGIES, INC.

Notes to Consolidated

Financial Statements

December 31, 2009 and 2008

individual income tax return. However, the State of California requires S Corporation to pay a state franchise tax (currently 1.5% on its taxable income).

Recent Accounting Pronouncements

In June 2009, the Financial Accounting Standards Board (“FASB”) issued Statement of Financial Accounting Standards No. 168, The FASB Accounting Standards Codification and the Hierarchy of Generally Accepted Accounting Principles – a replacement of FASB Statement No. 162 (“Statement No. 168”). This Statement establishes the FASB Accounting Standards Codification (the “Codification” or “ASC”) as the single source of authoritative GAAP. All previous GAAP standards have been superseded by the Codification. Rules and interpretive releases of the U.S. Securities and Exchange Commission (the “SEC”) under authority of federal securities laws are also sources of authoritative GAAP for SEC registrants, and the Codification neither replaces nor affects that guidance. Statement No. 168 is effective for interim and annual financial statements issued for periods ending after September 15, 2009, and references to GAAP in this report have been updated as a result. Subsequent changes to GAAP will be incorporated into the Codification through the issuance of Accounting Standards Updates (“ASU”) rather than FASB Statements, Staff Positions, Interpretations or Emerging Issues Task Force (“EITF”) Abstracts. The adoption of Statement No. 168 did not impact the Company’s financial condition, results of operations or cash flows.

In August 2009, the FASB issued Accounting Standards Update (ASU) 2009-05, Fair Value Measurements and Disclosures (Topic 820) – Measuring Liabilities at Fair Value. ASU 2009-05 provides clarification that in circumstances in which a quoted price in an active market for the identical liability is not available, a reporting entity is required to measure fair value of such liability using one or more of the techniques prescribed by the update. The adoption of this guidance is not expected to have a material impact on the Company’s financial position, results of operations or cash flows.

In April 2008, the FASB issued staff position FSP FAS 142-3 (FSP 142-3), "Determination of the Useful Life of Intangible Assets", and has subsequently been codified under FASB ASC 350-30-35, "Determining the Useful Life of an Intangible Asset" and is hereon referred to as ASC 350-30-35, amends the factors that should be considered in developing renewal or extension assumptions used to determine the useful life of a recognized intangible asset. The intent of ASC 350-30-35 is to improve the consistency between the useful life of a recognized intangible asset and the period of expected cash flows used to measure the fair value of the asset as outlined by the U.S. generally accepted accounting principles (GAAP). ASC 350-30-35 is effective for fiscal years beginning after December 15, 2008 and interim periods within those fiscal years and should be applied prospectively to intangible assets acquired after the effective date. Early adoption is prohibited. The Company does not expect this to have an impact on its results of operations, financial position or cash flows at the date of adoption, but it could have a material impact on its results of operations, financial position or cash flows in future periods.

“Business Combinations" (ASC 805) (formerly SFAS No. 141 and its revision 141(R)) changes how business acquisitions are accounted for and will impact financial statements both on the acquisition date and in subsequent periods. ASC 805 as it relates to recognizing all (and only) the assets acquired and liabilities assumed in a business combination, costs an acquirer expects but it not obligated to incur in the future to exit an activity of an acquiree or to terminate or relocate an acquiree's employees are not liabilities at the acquisition date but must be expensed in accordance with other applicable generally accepted accounting principles. Additionally, during the measurement period, which should not exceed one year from the acquisition date, any adjustments that are needed to assets acquired and liabilities assumed to reflect new information obtained about facts and circumstances that existed as of that date will be adjusted retrospectively. The acquirer will be required to expense all acquisition-related costs in the periods such costs are incurred other than costs to issue debt or equity securities. ASC 805 will have no impact on the Company’s results of operations, financial position or cash flows at the date of adoption, but it could have a material impact on the Company’s results of operations, financial position or cash flows in the future when it is

LEXON TECHNOLOGIES, INC.

Notes to Consolidated Financial

Statements

December 31, 2009 and 2008

applied to acquisitions which occur in the fiscal year beginning after November 1, 2009.

In May 2009, the FASB issued authoritative guidance establishing general standards of accounting for and disclosure of events that occur after the balance sheet date but before financial statements are issued. This guidance, which was incorporated into ASC Topic 855, "Subsequent Events", was effective for interim or annual periods ended after June 15, 2009, and the adoption did not have any impact on the Company's financial statements.

Note 3 - Merger

On October 7, 2009, Paragon Toner, Inc. (Paragon), a California corporation, entered into an Agreement and Plan of Merger (the “Merger Agreement”) with the Company whereby the Company issued 347,448,444 shares of common stock (the “Common Stock”) of the Company (the “Acquisition Shares”) to the shareholders of Paragon, representing approximately 72% of the issued and outstanding Common Stock after completion of the merger in October 2009. The effective date of the Merger was October 22, 2009 (“Effective Date”). The Company has decided to maintain the name of the predecessor company. The Merger has been accounted for as a recapitalization of Paragon with Paragon as the acquirer (reverse merger).

Note 4 - Inventory

Inventory consists of the following at December 31:

| 2009 | 2008 | ||||||

| Finished goods | $ | 582,603 | $ | 170,717 | |||

| Raw materials | 290,603 | 323,205 | |||||

| 873,206 | 493,922 | ||||||

| Less: Inventory reserve | (34,986 | ) | (34,986 | ) | |||

| Total | $ | 838,220 | $ | 458,936 |

The Company recorded a reserve for slow moving and obsolete inventory of $0, and $6,143 as cost of goods sold in 2009 and 2008, respectively. Overhead allocated to the inventory amounted to $35,640 and $20,079 for the years ended December 31, 2009 and 2008, respectively.

Note 5- Property and Equipment

Property and equipment consist of the following as of December 31:

LEXON TECHNOLOGIES, INC.

Notes to Consolidated Financial

Statements

December 31, 2009 and 2008

| 2009 | 2008 | ||||||

| Automobile | $ | 34,092 | $ | 34,092 | |||

| Furniture and fixture | 53,388 | 53,388 | |||||

| Leasehold improvement | 5,060 | 5,060 | |||||

| Machinery and equipment | 439,030 | 433,469 | |||||

| 531,570 | 526,009 | ||||||

| Less: Accumulated depreciation | (419,178 | ) | (311,350 | ) | |||

| Net property and equipment | $ | 112,392 | $ | 214,659 |

Depreciation expense amounted to $107,828 and $77,653 for the years ended December 31, 2009 and 2008, respectively.

Note 6 - Transactions with Related Parties

Due from related parties

Advances to family members of the stockholder are unsecured, non-interest bearing and due on demand. The Company has $190,000 and $273,650 due from related parties as of December 31, 2009 and 2008, respectively.

Due to related parties

As of December 31, interest bearing notes payable to related parties consisting of the following:

| 2009 | 2008 | ||||||

| Unsecured note payable to a shareholder,

with interest at 7.5% per annum. Note is in default and is payable on demand. |

$ |

5,000 |

$ |

- |

|||

| Expired convertible debt issued to a former

employee, with interest at 7.5% per annum. The conversion maturity date was in October 2004. The note is payable on demand. |

30,000 |

- |

|||||

| Expired convertible debt issued to a

Director, with interest at 7.5% per annum. The conversion maturity date was in October 2005. The note is payable on demand. |

56,960 |

- |

|||||

| Total notes payable | $ | 91,960 | $ | - |

LEXON TECHNOLOGIES, INC.

Notes to Consolidated Financial

Statements

December 31, 2009 and 2008

Note 7-Line of Credit

The Company has a line of credit with a bank with a maximum borrowing limit of $450,000. The outstanding balance was $450,000 and $600,000 as of December 31, 2009 and 2008, respectively. This line of credit matures on June 7, 2010 and is secured by the Company’s accounts receivable, inventory and other miscellaneous assets. Interest is accrued at the bank’s prime plus 1.00% (4.25% as of December 31, 2009).

The Company incurred interest expenses on this line of credit of $27,286and $35,296 for the years ended December 31 2009 and 2008, respectively. This line of credit contains certain covenants, and in management opinion, the Company is in compliance with the covenants as of December 31, 2009.

Note 8 - NotesPayable

As of December 31, the Company has long term notes payable as follows:

| 2009 | 2008 | ||||||

| A note payable to a bank, due in monthly

installments of $2,931, including interest at the bank’s prime plus 1.25% (4.50% as of December 31, 2009). The note matures in May 2011, and is collateralized by substantially all the assets of the Company. The note is subject to various restrictive covenants, including maintenance of financial ratios at all times. |

$ | 48,162 |

$ | 80,331 |

|||

| A note payable to a bank, due in monthly

installments of $3,249, including interest at the bank’s prime plus 1.25% (4.50% as of December 31, 2009). The note matures in November 2009, and is collateralized by substantially all the assets of the Company. The note was fully paid in November 2009. |

- |

33,182 |

|||||

| A note payable to a bank, due in monthly

installments of $2,533, including interest at the bank’s prime plus 2.00% (5.25% as of December 31, 2009). The note matures in May 2011, and is collateralized by substantially all bank accounts of the Company. The note was fully paid in November 2009. |

- |

27,075 |

|||||

| A note payable to a bank, due in monthly

installments of $4,587, including interest at the bank’s prime plus 1.50% (6.50% as of December 31, 2009). The note matures in January 2012, and is collateralized by substantially all the assets of the Company. |

130,850 |

- |

|||||

| Unsecured note payable to an unrelated

individual, with interest at 7.5% per annum. The note is in default and is payable on demand. |

20,000 |

- |

|||||

| Unsecured note payable to an unrelated

party, with interest at 7.5% per annum. As disclosed in Note 11, the creditor has filed suit to collect on this note. |

149,982 |

- |

|||||

| Total notes payable | 348,994 | 140,588 | |||||

| Less: Current portion | (249,534 | ) | (92,592 | ) | |||

| Notes payable, net of current | $ | 99,460 | $ | 47,996 |

LEXON TECHNOLOGIES, INC.

Notes to Consolidated

Financial Statements

December 31, 2009 and 2008

Maturities of notes payable are as follows for the years ending December 31:

| Years ending December 31, | Amount | ||

| 2010 | $ | 249,534 | |

| 2011 | 66,567 | ||

| 2012 | 32,893 | ||

| Total | $ | 348,994 |