Attached files

| file | filename |

|---|---|

| EX-32 - GC China Turbine Corp. | v181041_ex32.htm |

| EX-31.2 - GC China Turbine Corp. | v181041_ex31-2.htm |

| EX-14.1 - GC China Turbine Corp. | v181041_ex14-1.htm |

| EX-31.1 - GC China Turbine Corp. | v181041_ex31-1.htm |

| EX-10.21 - GC China Turbine Corp. | v181041_ex10-21.htm |

| EX-10.22 - GC China Turbine Corp. | v181041_ex10-22.htm |

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

FORM

10-K

(Mark

One)

x ANNUAL

REPORT PURSUANT TO SECTION 13

OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For

the fiscal year ended December 31, 2009

OR

¨ TRANSITION

REPORT PURSUANT TO SECTION 13

OR 15(d)

OF THE SECURITIES EXCHANGE ACT OF 1934

For the

transition period from __________ to ______________

Commission

File Number: 333-141641

|

GC

CHINA TURBINE CORP.

(Exact

name of registrant as specified in its charter)

|

||

|

Nevada

(State

of incorporation)

|

98-0536305

(I.R.S.

Employer Identification No.)

|

|

No.

86, Nanhu Avenue, East Lake Development Zone,

Wuhan,

Hubei Province 430223

People’s

Republic of China

(Address

of principal executive offices) (Zip Code)

+8627-8798-5051

(Registrant’s

telephone number, including area code)

Securities

registered pursuant to Section 12(b) of the Act:

|

None

|

None

|

|

|

(Title

of each class)

|

(Name

of each exchange on which

registered)

|

Securities

registered pursuant to Section 12(g) of the Act:

Common Stock, $0.001 par value

(Title of

class)

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in

Rule 405 of the Securities Act.

¨ Yes x No

Indicate

by check mark if the registrant is not required to file reports pursuant to

Section 13 or Section 15(d) of the Act.

¨ Yes x No

Indicate

by check mark whether the registrant (1) has filed all reports required to be

filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the

preceding twelve months (or for such shorter period that the registrant was

required to file such reports), and (2) has been subject to such filing

requirements for the past 90 days.

x Yes ¨ No

Indicate

by check mark if disclosure of delinquent filers pursuant to Item 405 of

Regulation S-K, is not contained herein, and will not be contained, to the best

of the registrant’s knowledge, in definitive proxy or information statements

incorporated by reference in Part III of this Form 10-K or any amendment of this

Form 10-K.¨

Indicate

by check mark whether the registrant is a large accelerated filer, an

accelerated filer, a non-accelerated filer, or a smaller reporting

company. See the definitions of “large accelerated filer” and “small

reporting company” in Rule 12b-2 of the Exchange Act.

Large

accelerated filer ¨ Accelerated

filer ¨ Non-accelerated

filer* ¨ Smaller

reporting company x

*(Do not

check if a smaller reporting company)

Indicate

by check mark whether the registrant is a shell company (as defined in Rule

12b-2 of the Exchange Act)

¨ Yes x No

The

aggregate market value of the common stock held by non-affiliates as of June 30,

2009 (the last trading day of the second quarter) was $4,476,030, based on the

last sale price of common stock sold.

As of

April 12, 2010, the last practicable date, 58,970,015 shares of the registrant’s

Common Stock were outstanding at a par value of $0.001.

DOCUMENTS

INCORPORATED BY REFERENCE: Exhibits incorporated by reference are referred to

under Part IV.

TABLE

OF CONTENTS

|

Page

|

||

|

PART

I

|

1

|

|

|

Item

1.

|

Business.

|

1

|

|

Item

1A.

|

Risk

Factors.

|

22

|

|

Item

1B.

|

Unresolved

Staff Comments.

|

34

|

|

Item

2.

|

Properties.

|

35

|

|

Item

3.

|

Legal

Proceedings.

|

35

|

|

Item

4.

|

Submission

of Matters to a Vote of Security Holders.

|

35

|

|

PART

II

|

35

|

|

|

Item

5.

|

Market

For Registrant’s Common Equity, Related Stockholder Matters and Issuer

Purchases of Equity Securities

|

35

|

|

Item

6.

|

Selected

Financial Data.

|

38

|

|

Item

7.

|

Management’s

Discussion and Analysis of Financial Condition and Results of

Operations.

|

39

|

|

Item

7A.

|

Quantitative

and Qualitative Disclosures about Market Risk

|

49

|

|

Item

8.

|

Financial

Statements and Supplementary Data.

|

50

|

|

Item

9.

|

Changes

in and Disagreements With Accountants on Accounting and Financial

Disclosure

|

50

|

|

Item

9A.

|

Controls

and Procedures.

|

50

|

|

Item

9B.

|

Other

Information.

|

52

|

|

PART

III

|

52

|

|

|

Item

10.

|

Directors,

Executive Officers and Corporate Governance.

|

52

|

|

Item

11.

|

Executive

Compensation.

|

55

|

|

Item

12.

|

Security

Ownership of Certain Beneficial Owners and Management and Related

Stockholder Matters.

|

57

|

|

Item

13.

|

Certain

Relationships and Related Transactions, and Director

Independence.

|

59

|

|

Item

14.

|

Principal

Accounting Fees and Services.

|

60

|

|

PART

IV

|

62

|

|

|

Item

15.

|

Exhibits,

Financial Statement Schedules

|

62

|

|

Signatures

|

65

|

|

|

Exhibits

|

PART

I

As used in this Annual Report on

Form 10-K, unless the context indicates

or suggests otherwise,

reference to “we”, “our”, “us”, “GC China Turbine”, the “Company” or the

“Registrant” refer to GC China Turbine Corp., a Nevada corporation and its

wholly-owned subsidiaries. “Luckcharm” shall mean Luckcharm Holdings Limited and

its wholly-owned subsidiaries, including Wuhan Guoce Nordic New Energy Co.,

Ltd.

Disclosure

regarding Forward-Looking Statements

Our

Annual Report on Form 10-K for the fiscal year ended December 31, 2009, and

information we provide in our press releases, telephonic reports and other

investor communications, including those on our website, may contain

forward-looking statements with respect to anticipated future events and our

projected financial performance, operations and competitive position that are

subject to risks and uncertainties that could cause our actual results to differ

materially from those forward-looking statements and our

expectations.

Except

for statements of historical facts, this Annual Report on Form 10-K contains

forward-looking statements involving risks and uncertainties. The words

“anticipate”, “believe”, “estimate”, “expect”, “future”, “intend”, “plan” or the

negative of these terms and similar expressions or variations thereof are

intended to be forward looking statements within the meaning of the Safe Harbor

Provisions of the Private Securities Litigation Reform Act of 1995. Such

statements reflect the current view of the Registrant with respect to future

events and are subject to risks, uncertainties, assumptions and other factors

(including the risks contained in the section of this Annual Report on Form 10-K

entitled “Risk Factors”) relating to the Registrant’s industry, the Registrant’s

operations and results of operations and any businesses that may be acquired by

the Registrant. Should one or more of these risks or uncertainties materialize,

or should the underlying assumptions prove incorrect, actual results may differ

significantly from those anticipated, believed, estimated, expected, intended or

planned.

Although

the Registrant believes that the expectations reflected in the forward looking

statements are reasonable, the Registrant cannot guarantee future results,

levels of activity, performance or achievements. Except as required by

applicable law, including the securities laws of the United States, the

Registrant does not intend to update any of the forward-looking statements to

conform these statements to actual results. The following discussion should be

read in conjunction with the Registrant’s financial statements and the related

notes included in this report on Form 10-K.

Such

risks and uncertainties include, without limitation, our ability to raise

capital to finance our operations, the effectiveness, profitability and the

marketability of our products, our ability to protect our proprietary

information, general economic and business conditions, the impact of

technological developments and competition, adverse results of any legal

proceedings, the impact of current, pending or future legislation and regulation

of the wind power industry, our ability to enter into acceptable relationships

with one or more of our suppliers and the ability of such suppliers to

manufacture products or components of an acceptable quality on a cost-effective

basis, our ability to attract or retain qualified senior management personnel,

including sales and marketing and technical personnel and other risks detailed

from time to time in our filings with the SEC, including those described in Item

1A below. We do not undertake any obligation to update any forward-looking

statements.

ITEM

1. BUSINESS.

Overview

We are a

holding company whose primary business operations are conducted through a

wholly-owned Hong Kong subsidiary, Luckcharm Holdings Limited (“Luckcharm”) and

its wholly-owned Chinese subsidiary Wuhan Guoce Nordic New Energy Co., Ltd. (“GC

Nordic”). GC Nordic is a leading manufacturer of 2-bladed wind turbines located

in Wuhan City of Hubei Province, China. We sought to license and

develop a technology in the wind energy space that would have a high likelihood

of meeting rigorous requirements for low-cost and high reliability. We

identified a 2-bladed wind turbine technology that was developed through a 10

year research project costing over US$ 75 million. Our license to manufacture

and sell this wind turbine in China, if not renewed, will expire on June 30,

2016. While the 2-blade technology is less commonly used in the China

wind farm market compared to 3-blade technology, the development project that

created our technology has been operating for 10 years with 97% availability

(availability is calculated as follow: [annual total hours (24×365) - turbine

downtime - maintenance time]/annual total hours ). Further, the

2-blade technology has the benefits of lower manufacturing cost, lower

installation cost and lower operational costs. Therefore, the product is

uniquely positioned to fulfill our mission. Our launch product is a 1.0 megawatt

(“MW”) utility scale turbine with designs for a 2.5MW and 3.0MW utility scale

turbine in development. We are developing a track record and

brand-awareness through the execution of our initial sales

contracts.

- 1

-

We were

incorporated under the laws of the State of Nevada on August 25, 2006 under the

name of Visa Dorada Corp. for the purpose of acquiring and developing

mineral properties. On August 31, 2006 we changed our name to Vista Dorada

Corp. We are the registered and beneficial owner of a 100% interest in the

Mocambo Gold Claim or the “VDC Claim” situated in the Republic of

Fiji. The VDC Claim is an unpatented mineral claim and was assigned

to us by EGM Resources Inc. on March 4, 2007 and the assignment was filed and

registered with the Mineral Resources Department of the Ministry of Energy and

Natural Resources of the government of the Republic of Fiji. We own no other

mineral property and are not engaged in the exploration of any other mineral

properties. We have not conducted any exploration work on the VDC Claim and

we have not generated any operating revenues from such

business.

On May

18, 2009, we effected a 1-for-2 reverse stock split to improve trading

liquidity, and enhance overall shareholder value. In an effort to grow our

company, on May 22, 2009, we entered into a letter of intent with GC Nordic and

on June 11, 2009 we changed our name to Nordic Turbines, Inc. We

subsequently changed our name to “GC China Turbine Corp.” on September 14,

2009.

Our

Acquisition of Luckcharm and Related Financing

On May

22, 2009, we entered into a Letter of Intent ("LOI") with GC Nordic whereby we

would purchase all of the issued and outstanding shares of GC Nordic from its

shareholders, and the shareholders of GC Nordic would receive a 54% ownership

interest in the Company. Further on July 31, 2009, an Amended and

Restated Binding Letter of Intent ("Revised LOI") was entered among us,

Luckcharm, GC Nordic, New Margin Growth Fund L.P. ("New Margin"), Ceyuan

Ventures II, L.P. ("CV") and Ceyuan Ventures Advisors Fund II, LLC ("CV

Advisors") whereby we would purchase all of the issued and outstanding shares of

Luckcharm from the shareholders, and the shareholders of Luckcharm would receive

a 54% ownership interest in the Company. The Revised LOI further provided that

(i) upon consummation of the reverse acquisition, we would directly or

indirectly own all of the outstanding capital stock of GC Nordic; (ii) the

closing date for the reverse acquisition would be thirty days from the date GC

Nordic completed an audit of its financial statements as required under U.S.

securities laws; and (iii) the obligation of GC Nordic to consummate the reverse

acquisition was conditioned upon an additional financing of at least US$

10,000,000 into the combined entities at closing.

On May

22, 2009, under the terms of the LOI we provided GC Nordic with a secured bridge

loan in the amount of US$ 1,000,000 to be applied toward legal and audit

expenses, and working capital. Upon the closing of the reverse acquisition, the

bridge loan became an intercompany loan. We had been provided these funds

through promissory notes from two foreign accredited investors, and these notes

were later assigned to Clarus Capital Ltd. (“Clarus”).

On July

31, 2009, we, Luckcharm, GC Nordic, New Margin, CV and CV Advisors entered into

an amended and restated financing agreement (the "Financing Agreement"). The

Financing Agreement provided that we agreed to lend Luckcharm (i) US$ 2,500,000

before July 24, 2009 and (ii) US$ 7,500,000 before July 31, 2009. In order to

guarantee Luckcharm’s lending obligations under the Financing Agreement, New

Margin loaned US$ 5,000,000 to us and CV and CV Advisors loaned the aggregate of

US$ 5,000,000 of the above amounts to us, and we in turn loaned US$ 10,000,000

to Luckcharm for purposes of working capital. Upon the consummation

of the reverse acquisition, the US$ 10,000,000 convertible loan made to us by

New Margin, CV and CV Advisors converted into shares of our common stock at a

conversion price equal to US$ 0.80 per share.

On

September 30, 2009, we entered into a voluntary share exchange agreement

(“Exchange Agreement”) with Luckcharm, GC Nordic and Golden Wind Holdings

Limited, a company incorporated in the British Virgin Islands and the parent

entity of Luckcharm, or “Golden Wind.”

- 2

-

On

October 30, 2009, the reverse acquisition was consummated. As a

result of the reverse acquisition, Luckcharm became our wholly-owned subsidiary,

and we acquired the business and operations of GC Nordic. At the

closing of the reverse acquisition, we issued 32,383,808 shares of our common

stock to Golden Wind in exchange for 100% of the issued and outstanding capital

stock of Luckcharm and US$ 10,000,000 in previously issued convertible

promissory notes were converted into 12,500,000 shares of our common stock. Our

acquisition of Luckcharm pursuant to the share exchange agreement was accounted

for as a reverse acquisition wherein Luckcharm is considered the acquirer for

accounting and financial reporting purposes.

Contemporaneous

with the reverse acquisition, we also completed a private placement pursuant to

which we issued 6,400,000 shares of our common stock, at a price of US$

1.25 per share for an aggregate offering price of US$ 8,000,000 to certain

investors (the “Investors”). Additionally, we entered into (i) a Note Purchase

Agreement with Clarus whereby Clarus agreed to loan US$ 1,000,000 to us upon the

effective date of delivery of 20 wind turbine systems by us to our customers in

the form of a convertible promissory note bearing no interest, having a maturity

date of 2 years from the date of issuance and convertible into shares of our

common stock at US$ 2.00 per share, and (ii) an amendment to a convertible

promissory note held by Clarus in the amount of US$ 1,000,000 revising the

conversion feature of such note. We have agreed with Clarus that the period

to fund the loan under the Note Purchase Agreement is extended to April 30,

2010. On the six

month anniversary upon the effective date of delivery of 20 wind turbine systems

by us to our customers, both loans held by Clarus in the aggregate amount of US$

2,000,000 will automatically convert into shares of our common stock at US$ 2.00

per share. In connection with the private placement, we also issued

warrants to investors and placement agents to purchase an aggregate of 1,200,000

shares of our common stock with each warrant having an exercise price of US$

1.00 per share and being exercisable at any time within 3 years

from the date of issuance.

In

connection with the private placement, Golden Wind entered into a make good

escrow agreement with the investors in the private placement offering, whereby

Golden Wind pledged 640,000 shares of our common stock to the investors in order

to secure our make good obligations under the private placement. In the make

good escrow agreement, we established a minimum after tax net income threshold

of US$ 12,500,000 for the fiscal year ending December 31, 2010. If the minimum

after tax net income threshold for the fiscal year 2010 is not achieved, then

the investors will be entitled to receive additional shares of our common stock

held by Golden Wind based upon a pre-defined formula agreed to between the

investors and Golden Wind. Golden Wind deposited a total of 640,000 shares of

our common stock, into escrow with Capitol City Escrow, Inc. under the make good

escrow agreement. Additionally, if the minimum after tax net income

threshold for the fiscal year 2010 is not achieved, then the investors will be

entitled to have the exercise price of the warrants adjusted lower based upon a

pre-defined formula agreed to between the investors and us.

Background

and History of Luckcharm and its Operating Subsidiaries and

Affiliates

Luckcharm

was originally incorporated in Hong Kong on June 15, 2009 by Fernside

Limited. On June 29, 2009, Fernside Limited transferred all of the

equity interest of Luckcharm to Golden Wind. On August 1, 2009, Luckcharm

entered into an agreement to acquire 100% of the equity of GC Nordic from the

original nine individual shareholders (the “Founders”). On August 5,

2009, GC Nordic received approval of this acquisition from the Bureau of

Commerce of the Wuhan City, Hubei Province, PRC.

Prior to

the reverse acquisition, on September 30, 2009, each of the Founders entered

into a Call Option Agreement and a Voting Trust Agreement with Xu Hong Bing, the

sole shareholder of Golden Wind. The Call Option Agreements provide

that, upon the achievement of certain milestones during the six years following

entry into the Call Option Agreements, the Founders can acquire from Golden Wind

shares of our common stock issued to Golden Wind in the reverse acquisition (the

“BVI Shares”), at a price per share of $US 0.0001. The call rights

are exercisable in tranches upon the satisfaction of certain conditions set

forth in the Call Option Agreements, and if all such conditions are met, the

Founders will have the right to acquire 100% of the BVI Shares. The

rights to acquire the BVI Shares under the Call Option Agreements are allocated

to the Founders in the same proportion as their ownership interest in GC

Nordic. The Voting Trust Agreements create a voting trust that

provide the Founders with all rights and powers of ownership with respect to the

BVI Shares, including without limitation the right to vote and receive dividends

thereon. Through the Voting Trust Agreements, the

Founders collectively obtained 100% voting interests with respect to the BVI

Shares, which are allocated among the Founders in the same proportion as their

ownership interest in GC Nordic.

- 3

-

GC Nordic

was organized in the PRC on August 21, 2006 as a limited liability company upon

the issuing of a license by the Administration for Industry and Commerce of the

Wuhan City, Hubei Province, PRC with an operating period of 30 years to August

9, 2039. On August 5, 2009, all of the outstanding equity interests of GC Nordic

were acquired by Luckcharm, and GC Nordic became a wholly-owned subsidiary of

Luckcharm. GC Nordic holds the government licenses and approvals necessary to

operate the wind turbines business in China.

GC Nordic

was founded by nine individual shareholders, including Mr. Hou Tie Xin, Mr. Xu

Jia Rong, Mr. Wu Wei, Mr. Zhang Wei Jun, Mr. Bu Zheng Liang, Mr. Zuo Gang and

Mr. He Zuo Zhi, who were shareholders of Wuhan Guoce Science and Technology Corp

(“Guoce Science and Technology”), and Ms. Qi Na and Ms. Zhao Ying, who were

senior management of Guoce Science and Technology. After GC Nordic was organized

in August 2006, Mr. Hou Tiexin, Mr. Xu Jia Rong and Mr. Bu Zheng Liang remained

as chairman, general manager and engineer of Guoce Science and Technology,

respectively, Ms. Qi Na, Ms. Zhao Ying, Mr. Wu Wei and Mr. Zhang Wei Jun left

Guoce Science and Technology’s management team and focused on GC Nordic’s

management and operation. Mr. Zuo Gang and Mr. He Zuo Zhi currently do not hold

any position in either Guoce Science and Technology or GC Nordic. Guoce Science

and Technology is a leading technology provider to the Chinese utilities

industry and it has a long history as a preferred provider to the utilities

industry in China since 1995 under the former name Wuhan Guoce Electric Power

New Technology Co., Ltd. (“Guoce New Technology”). In 2002 Guoce New Technology

was restructured and was renamed as Wuhan Guoce Science and Technology Corp.

Guoce Science and Technology is a producer of hydraulic systems and electronic

control systems that enjoy dominant market share of approximately 40% in the PRC

hydro-electric generation industry. GC Nordic was founded as part of a strategy

of expanding Guoce Science and Technology’s product offerings in a business that

closely parallels its current business. Guoce Science and Technology is a

company with great reputation in the industry with businesses covering the whole

power industrial chain with productions ranging from power generation to power

transmission to every sector of power utilization.

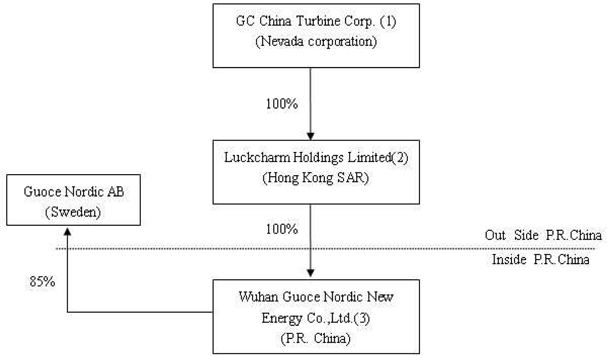

Our

Corporate Structure

The

following diagram illustrates our corporate structure as of December 31,

2009:

- 4

-

|

|

(1)

|

The management of GC China

Turbine includes: Hou Tie Xin as Chairman, Qi Na as Chief Executive

Officer and director, Zhao Ying as Chief Financial Officer, Tomas Lyrner

as Chief Technology Officer, and Xu Jia Rong, Marcus Laun and Chris Walker

Wadsworth as members of the board of directors. As of the date of this

Annual Report on Form 10-K, none of the management owns any shares of GC

China Turbine common stock. Mr. Hou, Ms. Qi, Ms. Zhao and Mr. Xu, however,

are parties to a Call Option Agreement dated September 30, 2009 pursuant

to which they have the right to acquire the shares of GC China Turbine

common stock issued to the Golden Wind in connection with the Exchange

Agreement, and to a Voting Trust Agreement dated September 30, 2009

pursuant to which they are voting trustees under a voting trust created to

hold all such shares.

|

|

|

(2)

|

The management of Luckcharm is

comprised of Xu Hong Bing as the sole

director.

|

|

|

(3)

|

The

management of GC Nordic includes: Hou Tie Xin as Chairman, Qi

Na as General Manager and Director, Xu Jia Rong as Director, Zhao Ying, Wu

Wei, Zhang Hanyun, Bailong and Zhang Weijun as Deputy General

Managers.

|

|

|

(4)

|

The

management of Guoce Nordic AB includes: Hou Tie Xin as Chairman, Tomas

Lyrner as Chief Executive Officer and Director, Wu Wei and Xu Hailian are

Directors.

|

Our

Industry

Wind

Power

Wind

power is the conversion of wind energy into more useful forms of energy, such as

electricity, using wind turbines. Humans have been using wind power

for at least 5,500 years to propel sailboats and sailing ships, and architects

have used wind-driven natural ventilation in buildings since similarly ancient

times.

Compared

to the environmental effects of traditional energy sources, the environmental

effects of wind power are relatively minor. Wind power consumes no fuel, and

emits no air pollution, unlike fossil fuel power sources. The energy consumed to

manufacture and transport the materials used to build a wind power plant is

equal to the new energy produced by the plant within a few months of

operation.

The power

in the wind can be extracted by allowing it to blow past moving wings that exert

torque on a rotor. The amount of power transferred is directly proportional to

the density of the air, the area swept out by the rotor, and the cube of the

wind speed. The mass flow of air that travels through the swept area of a wind

turbine varies with the wind speed and air density. Because so much power is

generated by higher wind speed, much of the average power available to a

windmill comes in short bursts. As a general rule, wind generators

are practical where the average wind speed is 10 mph (16 km/h or 4.5 m/s) or

greater. An ideal location would have a near constant flow of non-turbulent wind

throughout the year and would not suffer too many sudden powerful bursts of

wind. An important turbine siting factor is access to local demand or

transmission capacity. The wind blows faster at higher altitudes because of the

reduced influence of drag on the surface (sea or land) and the reduced viscosity

of the air. The increase in velocity with altitude is most dramatic

near the surface and is affected by topography, surface roughness, and upwind

obstacles such as trees or buildings. As the wind turbine extracts

energy from the air flow, the air is slowed down, which causes it to spread out

and divert around the wind turbine to some extent. Betz' law states

that a wind turbine can extract at most 59% of the energy that would otherwise

flow through the turbine's cross section. The Betz limit applies

regardless of the design of the turbine. Intermittency and the

non-dispatchable nature of wind energy production can raise costs for

regulation, incremental operating reserve, and (at high penetration levels)

could require demand-side management or storage solutions.

Wind

Turbines

A wind

turbine is a rotating machine which converts the kinetic energy in wind into

mechanical energy. If the mechanical energy is used directly by

machinery, such as a pump or grinding stones, the machine is usually called a

windmill. If the mechanical energy is then converted to electricity,

the machine is called a wind generator, wind turbine, wind power unit (WPU),

wind energy converter (WEC), or aerogenerator.

- 5

-

Wind

turbines require locations with constantly high wind speeds. Wind

turbines are designed to exploit the wind energy that exists at a

location. Small wind turbines for lighting of isolated rural

buildings were widespread in the first part of the 20th century. The

modern wind power industry began in 1979 with the serial production of wind

turbines by Danish manufacturers Kuriant, Vestas, Nordtank, and

Bonus. These early turbines were small by today's standards, with

capacities of 20–30 kilowatts each. Since then, they have increased

greatly in size, while wind turbine production has expanded to many

countries.

Wind

Industry

The wind

industry is the world's fastest growing energy sector and offers an

excellent opportunity to begin the transition to a global economy based on

sustainable energy. A report published by The Global Wind Energy Council (“GWEC”) and Greenpeace

in October 2008 references multiple studies that indicate that the long-term

potential supply using existing technology could be double the current worldwide

electricity demand. Prior GWEC reports indicate that there are no

technical, economic or resource barriers to supplying 12% of the world's

electricity needs with wind power alone by 2020, as compared to the challenging

projection of two thirds increase of electricity demand by 2020.

According

to the GWEC’s Global Wind 2007 Report, by the end of 2007 (2008 figures not

currently available), the capacity of global wind energy installations had

reached a generation capacity level of over nearly 94,000 MW, an increase of

nearly 20,000 MW over 2006 figures and representing a worldwide investment of

over US$ 50 billion. Europe accounts for 56,500 MW or 60% of the total installed

capacity followed by the U.S. with 17.9% or 16,800 MW. The fastest

growing market is China with 145% growth or 3,304 MW added in 2007 to over 5,900

MW by the end of 2007. Each of these markets is expected to continue

to drive the worldwide growth of wind turbine installations. The total

value of installed equipment worldwide in 2007 was approximately US$ 1.8 million

per MW for a turbine equipment market size of US$ 36 billion on a total

investment of US$ 50 billion.

Internationally,

demand for electricity has dramatically increased as our society has become more

technologically driven. Demand for “green” energy has also

dramatically increased due to consumers’ desire to become environmentally

conscious. Both trends are expected to

continue. Significant new capacity for the generation of electricity

will be required to meet anticipated demand.

Most of

the world’s primary energy sources are still based on the consumption of

non-renewable resources such as petroleum, coal, natural gas and

uranium. While still a small segment of the energy supply, renewable

sources such as wind power are growing rapidly in market share. Wind

power delivers multiple environmental benefits. It operates without

emitting any greenhouse gases and has one of the lowest greenhouse gas lifecycle

emissions of any power technology. Wind power does not result in any

harmful emissions, extraction of fuel, radioactive or hazardous wastes or use of

water to steam or cool. Wind projects are developed over large areas, but their

carbon footprint is light. Farmers, ranchers and most other land

owners can continue their usual activities after wind turbines are installed on

their property.

According

to the U.S. Department of Energy, Energy Information Administration’s

publication “Renewable Resources in the U.S. Electricity Supply,” wind power

generation was and is projected to increase eight-fold between 1990 and 2010, a

rate of 10.4% per year. Annual growth in the wind power industry for

the past 10 years has exceeded 28% per year according to the

GWEC. Although wind power produces under 1% of electricity worldwide

according to the GWEC’s Global Wind 2007 Report, it is a leading renewable

energy source and accounts for 19% of electricity production in Denmark

(according to the U.S. Department of Energy’s Energy Facts web page), 10% in

Spain and 7% in Germany (according to the GWEC’s Europe region web

page).

- 6

-

Chinese

Wind Industry

Wind-power

generation is a mature technology that is embraced in China due to its

relatively low cost (compared to other renewable energy sources such as solar

power) and abundance of wind resources. Satisfying rocketing

electricity demand and reducing air pollution are also main driving forces

behind the development of wind energy in China. Given the country’s

substantial coal resources and still relatively low cost of coal-fired

generation, cost reduction of wind power is an equally crucial

issue. This is being addressed through the development of large scale

projects and boosting local manufacturing of turbines. The Chinese

government believes that the localization of wind turbine manufacturing brings

benefits to the local economy and helps keep costs down. Moreover,

since most good wind sites are located in remote and poorer rural areas, wind

farm construction benefits the local economy through the annual income tax paid

to county government, local economic development, grid extension for rural

electrification as well as employment in wind farm construction and

maintenance.

Current

Chinese government guideline published in PRC National Development and Reform

Commission’s China Renewable Energy Development Plan 2007 mandates that 30,000

MW of wind power be installed by 2020. The Brussels-based GWEC reported that in

2008, China added more than 6,000 MW of wind-power generation capacity, bringing

China’s total installed wind-power generating capacity to over 12,000MW.

Moreover, the Chinese government has mandated that 70% of wind components be

sourced domestically by 2010. The wind manufacturing industry in

China is booming. In the past, imported wind turbines dominated the

market, but this is changing rapidly as the growing market and clear policy

direction have encouraged domestic production. At the end of 2007,

there were 40 Chinese manufacturers involved in wind energy, accounting for

about 56% of the equipment installed during the year, an increase of 21% over

2006. This percentage is expected to increase substantially in the

future. Total domestic manufacturing capacity is now about 8,000 MW,

and expected to reach about 12 GW by 2010.

Wind

energy resources are widely distributed in China, with rich resources broken

into the southeast coastal areas, the three northern regions (northeast, north,

and northwest) and inland regions.

Presently,

the thriving locations for the development of wind farms are the three northern

regions. However, inland regions where wind resources are abundantly

distributed are at an early development stage, and thus the market potential is

large. Further, some provinces in the inland regions have planned or

promulgated preferential policies for the development of wind power, and thus

the inland wind power industry may also become the new thriving points for

China‘s wind power development.

According

to the 2008 China Wind Power Development Report, published by China

Environmental Science Press in Beijing, abundant wind energy resource areas

along the southeast coast and its coastal areas mainly include Shandong,

Jiangsu, Shanghai, Zhejiang, Fujian, Guangdong, Guangxi and Hainan and other

provinces and cities’ coastal zones of nearly 10km wide with annual wind

power density above 200 w/m² and wind power density line parallels to the

coastlines.

Abundant

wind energy resource areas distributed in north areas mainly include, three

north provinces, Hebei, Inner Mongolia, Gansu, Ningxia and Xinjiang and other

provinces and districts’ of nearly 200 km wide with wind power density above

200—300 w/m², some of which could up to 500 w/m² more, such as Alashankou, Daban

City, Huitengxile, Huitengliang of Xilinhaote, Chengde and

Weichang.

Abundant

wind energy resource areas distributed in inland areas mainly include, Hunan,

Hubei, Jiangxi, Shanxi, Henan, Chongqing, Yunnan and other areas, with a general

wind power density of 100—200 w/m². Wind energy resources are also

abundant in some areas due to the impacts by the lakes and topography.

Technological accepted development capacity for wind power in inland areas

exceeds 12,000,000 kilowatts.

China

Wind Power Potential

Today,

wind power in China is developing rapidly and receives particularly strong

government support. The new Renewable Energy Law and its detailed incentive

policies reflect the Chinese government’s intention to build up this industry.

By 2020, China plans to have 30 gigawatts of wind power. European

companies dominate China’s wind power equipment market. Among U.S. companies,

only GE Wind Power is active in China. In 2005, GE Wind Power occupied 3% of the

in-grid wind turbine market in China.

- 7

-

According

to the China Academy of Meteorological Sciences, the country possesses a total

235 gigawatts of practical onshore wind power potential that can be utilized at

10 meters above the ground. Annual potential production from wind

power could reach 632.5 gigawatts if the annual, full-load operation reaches

2,000-2,500 hours. A detailed survey is needed, however, for economically

utilizable wind power resources. The potential for offshore wind

power is even greater, estimated at 750 gigawatts. Offshore wind

speed is higher and more stable than onshore wind, and offshore wind farm sites

are closer to the major electricity load centers in eastern

China. Areas rich in wind power resources are mainly concentrated in

two areas: northern China’s grasslands and Gobi desert, stretching from Inner

Mongolia, Gansu and Xinjiang provinces; and in the east coast from Shangdong and

Liaoning and the southeast coast in Fujian and Guangdong provinces.

In 1986,

China built its first wind farm in Rongcheng, Shandong Province. From 1996 to

1999, in-grid wind power developed very quickly, entering a localization stage.

By the end of 2004, there were 43 wind farms with 1291 wind turbines in China,

with 764 MW of installed capacity. Liaoning, Xinjiang, Inner Mongolia and

Guangdong experienced the fastest wind power development, representing 60% of

the installed power generating capacity of national wind power. Currently,

Xinjiang’s Dabancheng is the largest wind farm in China, with 100 MW of

installed power generating capacity. Most generators range from 500 kilowatts to

1 MW, accounting for 84% of China’s wind turbine generators.

Our

Products

Our

Company’s core product is the 2-bladed wind turbine which is designed with

technologies of soft concept, compact transmission chain, overall damping,

condition monitoring and other proprietary technologies that reduce vibration

and overheating, lower installation and transportation cost as well as improve

service life and utilization rate with the ultimate benefits of improving wind

turbine quality and lowering the costs of manufacturing, installation and

maintenance.

We use

“soft technology” which is a combination of a passive yaw system, teeter style

hub and the soft tower. By using the soft technology as a damping system for the

vibration and loads of the system, we can produce a transmission chain that does

not have to absorb those forces. Therefore, the transmission chain is

more compact, cheaper, proprietary, and more reliable than other

designs. The technology offers a new approach and significant

opportunities for large scale wind farms including remote onshore and offshore

installations. Additionally, constant feedback ensures we achieve the

highest efficiency.

The key

advantages of the 2-bladed wind turbine with influences on costs by proprietary

technologies are as follows:

|

Proprietary

Technologies

|

Design

Features

|

Influence

on Costs and Benefits

|

||

|

Soft

technology

|

Passive

yaw system

|

·

Yaw is a term used to describe the mechanical system of aiming the

turbine blades into the wind.

·

GC China Turbine has a passive yaw system, eliminating the need for

mechanical yaw braking system.

·

The passive yaw reduces loads on the tower and foundation thereby

allowing for a lighter tower and smaller foundation as well as reducing

the manufacturing costs for a complete machine.

|

||

|

Teeter-style

hub

|

·

The teeter-style hub reduces the negative effects of imbalanced air

pressure on the blades not unlike the function of rubber engine mounts in

a motor vehicle. The rubber bushings greatly reduce twisting loads on the

transmission chain, tower and other components and increase the service

lives of these components. This technology is characterized by rubber

mountings of the blades to the main gearbox.

|

|||

|

Soft

tower

|

·

The soft tower is lighter than a stiff tower so as to directly save

raw material costs. This is achieved by designing a tower that is allowed

to flex during operation. This is partially possible because the turbine

and blades are significantly lighter than a 3-blade

system.

|

- 8

-

|

Compact

transmission

chain

|

Support

tube

|

·

Generator, gearbox and high-speed shaft are directly connected

which greatly improves the service lives of the key components in

transmission chain.

|

||

|

Integrated

gearbox

|

·

Because GC China Turbine’s design eliminates the main shaft and

main bearing of 3-bladed designs, the Company enjoys a lower cost profile

and eliminates a significant component sourcing bottleneck.

·

Integrated main shaft has a longer service life, improves the

availability rate and reduces maintenance costs.

|

|||

|

Overall

damping

design

|

Teeter

and hub rubber elements, nacelle chassis rubber elements

|

·

Significantly reduces fatigue loads on all moving parts, extends

the service life and reduces operational costs.

|

||

|

Condition

monitoring

|

Conducts

maintenance according to actual conditions, instead of preventive and

post-fault maintenance

|

·

Extends service life of wind turbine and reduces maintenance

costs.

|

Our

products also face following challenges and we are working to improve our

2-blade wind turbine.

|

Challenges

|

Details

|

Solutions

|

||

|

Noise

|

Slightly louder than 3-blade wind

turbine

|

Wind farm is normally far away from

residential areas.

GC China Turbine’s 2-blade 1.0MW wind

turbine fully complies with IEC 61400-11 standard set by

IEC.

|

||

|

Efficiency

|

Slightly lower than pitch-control turbines under

low wind (<3.5 meter per second) and high wind (>23.5 meter per

second) conditions

|

We will upgrade our turbines to pitch-control

model.

|

As shown

in the table above, GC China Turbine's 2-blade 1.0MW wind turbine is designed

with proprietary technologies of soft concept, compact transmission chain,

overall damping, condition monitoring and other proprietary technologies that

reduce vibration and operating temperature as well as improve service life and

utilization rate. The resulting benefits are

1) High

Wind Turbine Quality

Our wind

turbine quality standard is to achieve high generating capacity with low cost.

Compared to other wind turbines with same generating capacity, our 2-blade wind

turbine’s cost is lower and availability is higher.

2) Low

Manufacturing Cost

The

manufacturing cost of our 2-blade 1.0MW wind turbine and the tower is 70% and

77.6% of the cost of typical China-made 3-blade 1.5MW wind turbine.

3) Cheaper

Installation.

The

foundation cost and transportation cost of our 2-blade 1.0MW wind turbine are

about 37% of the cost of typical China-made 3-blade 1.5MW wind

turbine.

- 9

-

Our

Company’s advantage is a combination of simple design that makes it cost

effective and that advantage will be enhanced by the replacement of imported

components with high quality Chinese components, which in many cases, come from

well established state-owned enterprises and public companies, and part of which

come from our Company’s European component manufacturers. In order to

sustain the low-cost advantage, the Company has also been actively seeking and

identifying domestic suppliers of all key components that In order to sustain

the low-cost advantage, the Company has also been actively seeking and

identifying domestic suppliers of all key components that made it 100%

Chinese-content wind turbines in 2009 with full distribution into the market by

end of 2009. These efforts will greatly reduce our manufacturing

costs and will help to further enhance the low-cost advantage of our

product.

Our

Sales and Marketing

The

Company will continue to compete in the mainstream wind farm bids as well as

seek out more niche projects where the light weight and easy transportation and

installation of our 2-bladed wind turbine offers additional advantages over the

competition. These projects would include mountainous areas. The Company intends

to bid for offshore application wind turbine bids when the research and

development for 3.0MW wind turbines is completed.

We divide

the Chinese market into 3 segments:

1) Northeast and northwest wind

farms

The wind

resource in this area is allocated between 5 large utility companies. It is

currently deploying product into the Daqing project within this

market.

2) Inland wind farms

Inland

wind farms have less wind resources and more mountainous terrain that will give

GC China Turbine additional advantages over the competition.

3) Coastal and offshore wind

farms

This area

has good wind resource and involves technically more difficult

installations. Thus, the simpler installation of 2-blade turbines has

an advantage over the 3-blade turbine.

China is

actively pursuing a plan to increase the percentage of energy supplied by

renewable means. We have a healthy pipeline of wind farm projects on which to

bid. GC Nordic has established a good relationship with local and

central government departments through its relationship with Guoce Science and

Technology to source potential contracts. Given that all the potential wind

farms projects have to be pre-approved by the central National Development and

Reform Commission (the “NDRC”) or the NDRC at the provincial level, our

relationship with the government will provide us with first hand information of

the potential wind farm projects in our targeted markets and allow us to compete

for such projects.

The

Company intends to create production facilities in many provinces so that it can

enjoy the privileges of being a local manufacturer across many markets. The

Company can create numerous manufacturing facilities efficiently as warehouse

space is inexpensive and the production of these turbines is not labor

intensive. Labor costs for production is approximately 1% of COGS.

The first

step of the selling process includes setting up initial communications with the

owner and obtaining wind conditions, terrain and other project specifications.

Once we have obtained the bidding information on a project, we can begin the

design process. This would include working with the farm developer to make sure

that the GC Nordic is included in the specifications as a possible turbine type.

At this stage it is crucial that the owner understands the characteristics and

advantages of our products before making a selection. The average sales process

for a wind farm takes 6 to 9 months.

- 10

-

The

Company is also planning to adopt a “Resources Exchange Model” to win bids for

potential wind farm projects. The Company sometimes signs wind farm projects

directly with the government and then invites the investors to buy, invest or

co-invest in the projects. As a condition for invitation, these wind farm

projects have to purchase and use of our 2-blade wind turbines.

As a

newcomer to the industry, due to the lack of actual turbines in use, some

cautious customers were taking a wait and see approach to making purchase

decisions from our Company. Now that our wind turbines have been

running steadily for over one year in Daqing wind farm with positive operating

results, buyers will be more confident in our Company and brand.

Currently,

there are 12 members of the sales team, handling the following responsibilities:

planning, project management, technical support and

administration. In the future, we will increase the size of the

planning, project management and technical support teams as necessary to support

these functions.

Our sales

goals and targeted milestones from 2010 to 2015 are as follows:

2010

|

|

·

|

Using the model project of Daqing

wind farm, we will target inland wind farms as the entry point to gain a

foothold in the market, with a goal of being one of the top three

producers in that market.

|

|

|

·

|

Further exploring

northeast/northwest wind farm opportunity starting in 2009, and adopting

resources exchange model to conduct the market development and striving to

compete against large manufacturers with our low-cost

advantage.

|

|

|

·

|

Launch offshore markets and

overseas markets.

|

2011-2013

|

|

·

|

Set up 2 to 3 production and

research bases in coastal areas, achieving top 3 production status and

selling approximately 1,500 MW of installed energy

capacity.

|

|

|

·

|

Develop equipment for a number of

projects in Eastern Europe, Africa and South America markets, striving to

become a top 5 exporter of Chinese turbines and annually exporting

approximately 25 MW of installed energy capacity. Although our

license of 2-blade 1.0MW wind turbine is limited for use in China, we will

work to expand the current license and we have established a research

center in December 2009 in Sweden to develop 1.5MW, 2.5MW and 3.0MW

turbines which will not be restricted to use in

China.

|

2013-2015

|

|

·

|

Continue to extend inland market

share.

|

|

|

·

|

To

have top 3 market share in the coastal wind farm market, achieving 15%

market share and selling approximately 75 MW of installed energy capacity

per year.

|

Our

Customers

We are

currently executing four contracts with the following entities: Daqing Longjiang

Wind Power Co., Ltd (“ Daqing Longjiang ”), Wuhan Kaidi Electric Engineering

Co., Ltd (“ Wuhan Kaidi ”), Kelipu Wind Power Co., Ltd. (“ Kelipu ”) and

Shenzhen Guohan Investment Group (“Shenzhen Guohan”).

- 11

-

1. Daqing

Longjiang

Daqing

Longjiang has signed a wind turbine purchasing contract dated August

30, 2007 (the “DL Contract") with GC Nordic for 50 units of 1.0MW wind turbines.

These wind turbines will be installed in Daqing City, Heilongjiang

Province. Daqing Longjiang was established in 2007 and is a company

within the Daqing Ruihao Energy Group specializing in the research, development,

construction and operation of wind power generation. The company is mainly

engaged in wind power project operations of new energy and high efficient

energy-saving technology and environmental protection technology and currently

possesses the exclusive development right of wind power in Dumeng

County.

Under the

terms of the DL Contract, GC Nordic was obligated to deliver ten of the wind

turbines within four months after signing the DL Contract, and the balance of 40

wind turbines are to be delivered within ten months after receiving notice from

Daqing Longjiang requesting them. GC Nordic delivered the first ten

wind turbines and upon request by Daqing Longjiang , agreed not to deliver the

remaining 40 wind turbines until requested by Daqing Longjiang. The total

contract is valued at approximately US$46 million.

2. Wuhan

Kaidi

Wuhan

Kaidi has signed a purchase contract in September 2008 (the “WK Contract”) with

GC Nordic for 50 units of 1.0MW wind turbines. These wind turbines will be

installed in Pinglu City, Shanxi Province. Wuhan Kaidi is joint-stock high-tech

enterprise registered at Wuhan East Lake High-Tech Development Zone, and it is a

subsidiary of Wuhan Kaidi Holding Investment Co., Ltd. The company was

established in 2004 with businesses in coal-fired power generation, biomass

power generation, wind power, hydropower and other power construction including

power plant consulting, design, equipment procurement, construction,

installation and commissioning and commercial operation.

Under the

terms of the WK Contract, GC Nordic is obligated to deliver 50 wind turbines for

Wuhan Kaidi’s Kaidi Power Pinglu Wind Farm project. The purchase

price is due in several installments. GC Nordic delivered the first

ten wind turbines and upon request by Wuhan Kaidi agreed not to deliver the

remaining 40 wind turbines until requested by Wuhan Kaidi. The total

contract is valued at approximately US$47 million.

3. Kelipu

Kelipu

executed a purchase contract with GC Nordic for 50 units of 1.0MW wind turbines

in July 2009. These wind turbines will be installed at Kelipu’s wind

farm located in Tu Quan County of Inner Mongolia. However, as of date

of this report, Kelipu has applied for but has not yet received final approval

of its wind farm entry procedure from the local

government. Therefore, implementation of this contract with Kelipu

may be delayed until it has received the relevant approvals from the local

government.

4. Shenzhen

Guohan Investment Group

Shenzhen

Guohan signed a purchase contract with GC Nordic in December 2009 for 10 units

of 1.0MW. The total contract is valued at approximately US$8

million.

Production

and Quality Control

The

Company is using production of the 1.0 MW turbines to grow market share by

exploiting its low-cost advantage. Concurrently the Company is investing in

research and development for its larger turbines. The Company is targeting

production of its large turbines for 2010.

The

Company implements quality control in respect of purchasing, production, and

provision and after sale services as follows:

|

|

(1)

|

Purchasing: We choose reliable

suppliers and require complete background information and test data from

such suppliers to make sure their supplies meet our rigorous

standards.

|

- 12

-

|

|

(2)

|

Production: We run inspections

throughout the whole manufacturing and production process. We conduct

follow-up inspections and use specialized instruments to guarantee the

specifications of moment of force and gap. We implement several check

points throughout the process from component manufacturing to provision,

such as a check point for the size and flatness of the bottom portion of

the turbine, a check point for the yaw gear gap of 0.7mm to 0.9 mm, a

check point for the moment of force of the binding bolt, and a check point

for parameters in operation. We keep detailed test data of the check

points and keep a detailed profile of such

information.

|

|

|

(3)

|

Provision and after sale

services: We strictly follow guidelines in adjustment of lubrication,

hydraulic cooling and hydro-electric control

system.

|

The

Company conformed to the quality management system standard ISO 9001:2000 for

the process of manufacturing and servicing wind turbines on September 10,

2008.

Our Suppliers

The

Chinese government’s support of the wind turbine industry has created

significant capacity for components. The Company has signed contracts with all

domestic component suppliers. For key components, GC China Turbine has

investigated several alternative suppliers, 2 to 3 of which will be selected to

sign supply contracts with us, thereby ensuring the supply of components for

future production needs. After components are successfully trial produced

by the suppliers, components will then be tested by the original manufacturers,

and each component is also tested by GC China Turbine for performance before

installation into our wind turbines. All of our principal Chinese

suppliers are Yong Jin Gear Co., Ltd., Chuan Run Stock Co., Ltd., Xiang Tan

Generator Stock Co., Ltd., Jiangsu Tianming Machinery Group, China Erzhong Group

(Deyang) Heavy Industries Co., Ltd., Nanfang Ventilator Industries Co., Ltd.,

Xi’an Dun’an Electric Co., Ltd. and Zhong Neng Wind Power Device Co.,

Ltd. Our only foreign principal supplier is Mita—Teknik

A/S.

Logistics

and Inventory

Because a

wind turbine is a product with a high unit price, we keep low inventory and

follow a make-to-order policy. We make annual orders with our suppliers at the

beginning of the year based on the forecast of our sales. We start production of

the wind turbines upon execution of sales contracts with our customers and upon

receipt of a deposit on such contracts. We generally hold a 10% inventory in

case of unexpected demand.

Seasonality

Our

Company’s operating results are not affected by seasonality.

Competition

The wind

power market is rapidly evolving and is expected to become intensively

competitive. According to the Chinese wind turbine ranking published

independently by Beijing JiPeng Information and Consultancy Co., Ltd., GC Nordic

ranked 13th in

2008. Some of our competitors have established a market position more

prominent than ours and if we fail to attract and retain customers and establish

a successful distribution network for our wind turbines, we may be unable to

increase our sales and market share. We compete with major

international and PRC companies including Dongfang Steam Turbine, Dalian Huarui,

Gold Wind, CSIC, Spanish Gamesa, and Indian Suzion. Some of these

companies are more experienced and more established than us with mature

manufacturing capabilities. Some of these companies are

well-capitalized and benefit from earlier development advantages. We

also expect that our future competition will include new entrants to the wind

power market offering new technological solutions.

However,

we believe that the cost and performance of our technologies, products and

services will have advantages compared to competitive technologies, products and

services. Some of our competitors are large enterprises resulting in

inflexible operations. Some of our competitors receive less

government support. We also have the following advantages over our

competitors:

- 13

-

1. Our

Cost Advantage

We

believe our 2-bladed wind turbine and technological process provides for lower

manufacturing costs resulting from significantly more efficient material usage,

use of fewer parts and fewer manufacturing steps for our product as compared to

our competitors, which commonly use a 3-bladed wind turbine. The

installation costs of our product are also significantly lower as compared to

our competitors because our 2-bladed wind turbine has a simple structure,

lighter total weight and can be more easily installed at less cost than the cost

of installation of 3-bladed wind turbines used by our

competitors. Further, use of our 2-bladed wind turbine can also

significantly reduce overall maintenance costs for a wind farm because it is

equipped with condition monitoring system which monitors the operational

condition of the wind turbine, and signals for maintenance based on actual

turbine condition, increasing revenue and reducing maintenance

costs. These cost advantages greatly reduce the initial investment,

installation costs and maintenance costs of wind farm for owners using our

2-bladed wind turbine.

2. Our

Relationship with Guoce Science and Technology

Since GC

China Turbine Group was formed by certain founders and management of Guoce

Science and Technology, some of these individuals, including Mr. Hou Tie Xin,

Mr. Xu Jia Rong, Ms. Qi Na, Ms. Zhao Ying, also form our core management team,

we have the advantage of initial strategic guidance and the supply of necessary

start-up resources. The main businesses of Guoce Science and Technology’s

include research and development, production, sales, and system engineering

services of power testing instrument, computer-based monitoring system for

hydropower station, hydropower governor, hydropower station excitation, direct

current system, substation automation, power dispatching automation, network

monitoring, cluster server, and computer storage technology.

Guoce

Science and Technology has a strong reputation as a provider of technology

services in the energy industry. Its businesses cover the whole power

industrial chain with products ranging from power generation to power

transmission to every sector of power utilization. With the complete product

framework, it expects to hold the leading position in the industry for a long

time.

Our

relationship with Guoce Science and Technology has many benefits

including:

|

|

·

|

access to engineering

prowess

|

|

|

·

|

access to established technology

in the turbine control arena

|

|

|

·

|

access to the utilities industry

in China as it has large market share for their

products

|

|

|

·

|

credibility within the utilities

industry because it has long-standing relationships and operating history

within the industry

|

The

entire wind power industry also faces competition from other power generation

sources, both conventional and emerging technologies. Large utility

companies dominate the energy production industry. Coal continues to

dominate as the primary resource for electricity production. Other

conventional resources, including natural gas, oil and nuclear compete with wind

energy in generating electricity. Wind power has some advantages and

disadvantages when compared to other power generating

technologies. Wind power is plentiful and widely

distributed. It is a renewable source of energy. Since

wind power does not generate greenhouse gases, it does not contribute to global

warming. Wind power produces no water or air pollution that can

contaminate the environment because no chemical processes are involved in wind

power generation. As a result, wind power reduces toxic atmospheric

gas emissions. However, wind turbines require locations with

constantly high wind speeds and since wind is unpredictable, wind power is not

predictably available.

Research

and Development

GC China

Turbine identified a 2-bladed wind turbine technology that was developed through

a 10 year research project costing over US$ 75 million. While the 2-bladed

technology is relatively less commonly used in the market, the development

project that created GC China Turbine’s technology has been operating for 10

years with 97% availability (for generation). Further, the 2-bladed technology

has the benefits of lower manufacturing cost, lower installation cost and lower

operational costs.

- 14

-

The

2-bladed wind turbine was developed by a firm called Deltawind AB

(“Deltawind”). GC China Turbine has a 10 year license with

Deltawind, with opportunity for renewal, which allows us to manufacture and

distribute these turbines in the Chinese markets. This license, if

not renewed, will expire on June 30, 2016. Some former personnel of

Deltawind joined GC China Turbine and those personnel are assisting in the

research and development efforts as well as the testing of the new Chinese

components. There are no employment or retention agreements with any

former Deltawind employee. Deltawind was subsequently purchased by a

U.S. licensee of the technology named Nordic Windpower Ltd.

In

December 30, 2009, GC Nordic jointly established Guoce Nordic AB with Tomas

Lyrner in Sweden, of which 85% of the shares of Guoce Nordic AB is held by GC

Nordic and 15% by Mr. Lyrner. Guoce Nordic AB is the research and development

center of GC Nordic will contribute to GC Nordic all of the intellectual rights

developed. In 2010, the R&D center will focus on the development of 2.5MW

and 3.0MW wind turbines.

Our

launch product is a 1.0MW utility scale turbine with designs for a 2.5W and

3.0MW utility scale turbine in development. The Company is using

production of the 1.0 MW turbines to grow market share by exploiting its

low-cost advantage. For fiscal years 2008 and 2009, we have spent US$

94,300 and US$ 90,437, respectively, on research and development expenses. The

Company plans to continue investing more in research and development for its

larger turbines. The Company is targeting production of its 2.5MW and 3.0MW

turbines for 2010.

Intellectual

Properties and Licenses

The

following table describes the intellectual property currently owned by GC

Nordic:

|

Type

|

Name

|

Category

Number and Description

|

Issued

By

|

Duration

|

Description

|

|||||

|

Trademark

|

GC-NORDIC

|

39

(transport; packaging and storage of goods; travel

arrangement)

|

State

Trademark Administration

|

September

28, 2009 to September 27, 2019

|

N/A

|

|||||

|

Trademark

|

Nordic

|

39

(transport; packaging and storage of goods; travel

arrangement)

|

State

Trademark Administration

|

June

21, 2009 to June 20, 2019

|

N/A

|

|||||

|

Trademark

|

|

诺德

|

|

7

(Machines and machine tools; motors and engines (except for land

vehicles); machine coupling and transmission components (except for land

vehicles); agricultural implements other than hand-operated; incubators

for eggs)

|

|

State

Trademark Administration

|

|

June

7, 2009 to June 6, 2019

|

|

N/A

|

GC China

Turbine takes all necessary precautions to protect our intellectual

property. Aside from registering our trademarks with the State

Trademark Administration to protect our intellectual property, our marketing

team also diligently conducts market research to ensure that our intellectual

property is not being violated. However, we cannot assure you that we will be

able to protect or enforce our intellectual property rights. In the

event of any infringement upon our intellectual property rights, we will pursue

all legal rights and remedies.

China

Economic Incentive Policies

To

support the development of wind power technology and growth of the in-grid wind

power market, the Chinese government has implemented a series of projects and

also stipulated a series of economic incentive policies. We will

attempt to join the applicable projects and apply for all applicable

incentives.

- 15

-

Ride

the Wind Program

To import

technology from foreign companies and to establish a high-quality Chinese wind

turbine generator sector, the former State Development and Planning Commission

(“SDPC”)

initiated the “Ride the Wind Program” in 1996. This initiative led to two joint

ventures, NORDEX (Germany) and MADE (Spain). These joint ventures

effectively introduced a 600 kilowatts wind turbine generator manufacturing

technology into China.

National

Debt Wind Power Program

To

encourage the development of domestic wind power equipment manufacturing, the

former State Economic & Trade Commission (“SETC”) implemented

the “National Debt Wind Power Program.” This program required the

purchase of qualified, locally-made wind power components for new generation

projects. China’s government provided bank loans with subsidized

interest to wind farm owners as compensation for the risk of using locally-made

wind turbine generators. These loans funded construction of

demonstration project wind farms with a total installed capacity of

8MW. This program has been completed.

Wind

Power Concession Project

The NDRC

initiated the “Wind Power Concession Project” in 2004 with a 20-year operational

period. This program aims to reduce the in-grid wind power tariff by

building large capacity wind farms and achieving economies of scale. Each of the

wind farms built under this program must reach a 100MW capacity. By 2006, NDRC

had approved 5 wind farms, in Jiangsu, Guangdong, Inner Mongolia, and Jilin

Province.

In

February 2005, China’s Renewable Energy Law was formulated and was put into

effect on January 1, 2006. The law stipulates that the power grid

company must sign a grid connection agreement with the wind power generating

company and purchase the full amount of the wind power generated by

it. The wind power tariff will be determined by the wind farm project

tendering. The winner’s quoted tariff will be the tariff of that wind

farm project.

Wind

power is a priority “National Clean Development Mechanism Project” of the

Chinese government. Wind farm developers can sell Certified Emission

Reduction Certificates (“CER’s”) to developed

countries under the terms of the Kyoto Protocol.

Governmental

Regulations

This

section sets forth a summary of the most significant regulations or requirements

that affect our business activities in China.

Compliance with Circular 75, Circular 106 and the 2006 M&A

Regulations

China’s

State Administration of Foreign Exchange (“SAFE”) issued a

public notice known as “Circular 75” in October 2005, requiring PRC residents to

register with the local SAFE branch before establishing or acquiring the control

of any company outside of China for the purpose of financing that offshore

company with assets or equity interest in a PRC company. PRC residents that are

shareholders of offshore special purpose companies established before November

1, 2005 were required to conduct the overseas investment registration with the

local SAFE branch before March 31, 2006, and once the special purpose vehicle

has a major capital change event (including overseas equity or convertible bonds

financing), the residents must conduct a registration relating to the change

within 30 days of occurrence of the event. On May 29, 2007, the SAFE issued an

additional notice known as “Circular 106,” clarifying some outstanding issues

and providing standard operating procedures for implementing the prior notice.

According to the new notice, SAFE sets up seven schedules that track

registration requirements for offshore fundraising and roundtrip

investments.

Likewise,

the “Provisions on Acquisition of Domestic Enterprises by Foreign Investors,”

issued jointly by the Ministry of Commerce (“MOFCOM”), State-owned

Assets Supervision and Administration Commission, State Taxation Bureau, State

Administration for Industry and Commerce, China Securities Regulatory Commission

and SAFE in September 2006, impose approval requirements from MOFCOM for

“round-trip” investment transactions, including acquisitions in which equity was

used as consideration.

- 16

-

Dividend

Distribution

The

principal laws, rules and regulations governing dividends paid by our PRC

operating subsidiary include the Company Law of the PRC (1993), as amended in

2006, Wholly Foreign Owned Enterprise Law (1986), as amended in 2000, and Wholly

Foreign Owned Enterprise Law Implementation Rules (1990), as amended in 2001.

Under these laws and regulations, our PRC subsidiary may pay dividends only out

of its accumulated profits, if any, determined in accordance with PRC accounting

standards and regulations. In addition, our PRC subsidiary is required to set

aside at least 10% of its after-tax profit based on PRC accounting standards

each year to its statutory surplus reserve fund until the accumulative amount of

such reserve reaches 50% of its respective registered capital. These reserves

are not distributable as cash dividends. The board of directors of a