Attached files

As filed with the Securities and Exchange Commission on April 15, 2010

Registration No. 333-152512

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 7

TO

Form S-1

REGISTRATION STATEMENT

UNDER THE SECURITIES ACT OF 1933

AutoGenomics, Inc.

(Exact name of registrant as specified in its charter)

| Delaware | 3826 | 80-0252299 | ||

| (State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification No.) |

2980 Scott Street

Vista, California 92081

(760) 477-2248

(Address, including zip code and telephone number, including area code, of registrant’s principal executive offices)

Fareed Kureshy

President and Chief Executive Officer

AutoGenomics, Inc.

2980 Scott Street

Vista, California 92081

(760) 477-2248

(Name, address, including zip code and telephone number, including area code, of agent for service)

Copy to:

| J. Scott Hodgkins David A. Zaheer Latham & Watkins LLP 355 South Grand Avenue Los Angeles, CA 90071-1560 (213) 485-1234 |

Frederick T. Muto Charles S. Kim Sean M. Clayton Cooley Godward Kronish LLP 4401 Eastgate Mall San Diego, CA 92121-1909 (858) 550-6000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ¨ | Accelerated filer ¨ | |

| Non-accelerated filer x | Smaller reporting company ¨ | |

| (Do not check if a smaller reporting company) |

CALCULATION OF REGISTRATION FEE

| Title of Each Class of Securities to be Registered |

Proposed Maximum Aggregate Offering Price (1) (2) |

Amount of Registration Fee (3) | ||

| Common Stock, $0.01 par value |

$86,300,000 | $3,391.59 | ||

| (1) | Estimated solely for the purpose of computing the amount of the registration fee, in accordance with Rule 457(o) promulgated under the Securities Act of 1933. |

| (2) | Includes offering price of shares that the underwriters have the option to purchase to cover overallotments, if any. |

| (3) | Previously paid in connection with the original filing of the Registration Statement. |

THE REGISTRANT HEREBY AMENDS THIS REGISTRATION STATEMENT ON SUCH DATE OR DATES AS MAY BE NECESSARY TO DELAY ITS EFFECTIVE DATE UNTIL THE REGISTRANT SHALL FILE A FURTHER AMENDMENT WHICH SPECIFICALLY STATES THAT THIS REGISTRATION STATEMENT SHALL THEREAFTER BECOME EFFECTIVE IN ACCORDANCE WITH SECTION 8(a) OF THE SECURITIES ACT OF 1933, OR UNTIL THE REGISTRATION STATEMENT SHALL BECOME EFFECTIVE ON SUCH DATE AS THE COMMISSION, ACTING PURSUANT TO SAID SECTION 8(a), MAY DETERMINE.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any jurisdiction where such offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED APRIL 14, 2010

Preliminary Prospectus

Shares

Common Stock

We are offering shares of our common stock. This is our initial public offering, and no public market currently exists for our common stock. We expect the initial public offering price to be between $ and $ per share. We have applied to list our common stock on the NASDAQ Global Market under the symbol “AGMX.”

Investing in our common stock involves a high degree of risk. Please read “Risk Factors” beginning on page 12.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| PER SHARE | TOTAL | |||

| Public Offering Price |

$ | $ | ||

| Underwriting Discounts and Commissions |

$ | $ | ||

| Proceeds to AutoGenomics, Inc. (Before Expenses) |

$ | $ | ||

Delivery of the shares of common stock is expected to be made on or about , 2010. We have granted the underwriters an option for a period of 30 days to purchase, on the same terms and conditions set forth above, up to an additional shares of our common stock to cover overallotments. If the underwriters exercise the option in full, the total underwriting discounts and commissions payable by us will be $ and the total proceeds to us, before expenses, will be $ .

Sole Book-Running Manager

Jefferies & Company

Co-Managers

| Baird | Thomas Weisel Partners LLC |

Prospectus dated , 2010

Table of Contents

| 1 | ||

| 12 | ||

| 34 | ||

| 35 | ||

| 36 | ||

| 38 | ||

| 40 | ||

| Management’s Discussion and Analysis of Financial Condition and Results of Operations |

42 | |

| 60 | ||

| 88 | ||

| 93 | ||

| 112 | ||

| 114 | ||

| 117 | ||

| 121 | ||

| Material United States Federal Income Tax Consequences to Non-U.S. Holders |

124 | |

| 127 | ||

| 132 | ||

| 132 | ||

| 132 | ||

| F-1 |

INFINITI, BioFilmChip, Intellipac and Qmatic are our trademarks. All other service marks, trademarks and trade names referred to in this prospectus are the property of their respective owners.

We intend to effectuate a for reverse stock split of our common stock prior to the consummation of the offering.

You should rely only on the information contained in this prospectus. Neither we, nor the underwriters, have authorized anyone to provide you with additional information or information different from that contained in this prospectus. We are offering to sell, and seeking offers to buy, shares of our common stock only in jurisdictions where offers and sales are permitted. The information contained in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of shares of our common stock. Our business, financial condition, results of operations and prospects may have changed since that date.

Until , 2010 (25 days after the date of this prospectus), all dealers that buy, sell or trade in our common stock, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to the dealers’ obligation to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

This summary highlights the information contained in this prospectus. Because this is only a summary, it does not contain all of the information that may be important to you. For a more complete understanding of the information that you may consider important in making your investment decision, we encourage you to read this entire prospectus. Among the other information in this prospectus, you should carefully consider the information set forth under the heading “Risk Factors” and our financial statements and accompanying notes included elsewhere in this prospectus. Unless the context requires otherwise, the words “we,” “us,” “our,” “Company” and “AutoGenomics” refer to AutoGenomics, Inc.

Overview

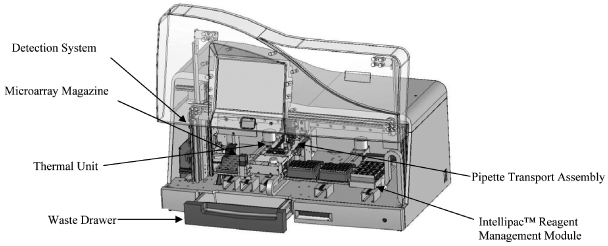

We design, develop, manufacture and market a fully integrated molecular diagnostics platform called the INFINITI system that includes our highly automated bench-top INFINITI Analyzer, which has the versatility to run a large menu of genetic tests. By eliminating the need for multiple specialized instruments and automating many of the discrete processes of genetic testing, we believe our system can significantly improve laboratory productivity, workflow and cost per reportable result over many existing technologies and methods. Our system is easy to use, provides a high level of sensitivity and accuracy, and is capable of high volume testing and detecting multiple biomarkers at the same time on the same sample, or multiplexing. Our system is designed to allow for the development of new and enhanced tests without modification to our platform. We believe these and other attributes of our system could reduce the cost and complexity of genetic testing and the need for specialized personnel, equipment and facilities, allowing a broader range of reference laboratories, hospital laboratories and specialty clinics to perform molecular diagnostics tests, and facilitating the acceptance and rapid adoption of our system.

As of March 31, 2010, we offered 42 tests for use on our INFINITI Analyzer, including tests focused in the areas of women’s health, cancer and personalized medicine, which we believe represent large and growing market opportunities in genetic testing. We intend to establish a large installed base of INFINITI Analyzers which in turn should generate significant recurring demand for our high margin testing consumables, including our test-specific BioFilmChips and Intellipac Reagent Management Modules. As of March 31, 2010, we had an installed base of 151 INFINITI Analyzers in reference laboratories, hospital laboratories and specialty clinics in North America, Europe, Asia, the Middle East and South America.

We have received U.S. Food and Drug Administration, or FDA, clearance for the INFINITI Analyzer and our Warfarin, FII, FV and FII-FV Panel tests, and we intend to seek clearance or approval, as necessary, for our other tests. Like many other companies offering molecular testing products on a commercial basis, most of the tests that we offer have not been cleared or approved for diagnostic use by the FDA. These molecular tests are available to laboratories on a research use only, or RUO, basis. As required by FDA regulations, these tests must be labeled “For Research Use Only. Not for use in diagnostic procedures.” Although our RUO products are used for clinical purposes by laboratories certified under the Clinical Laboratory Improvement Amendments of 1988, or CLIA, as laboratory-developed tests pursuant to guidelines issued by the College of American Pathologists, we are not permitted to market these products for diagnostic purposes. As of March 31, 2010, 38 of our 42 tests were offered on an RUO basis. For the year ended December 31, 2009, sales of our RUO tests represented 86% of our revenue from the sale of consumables. We believe that many other companies offering molecular tests on a commercial basis also derive significant revenue from the sale of RUO tests.

Industry Background

Molecular diagnostics tests, a new and expanding part of the in vitro diagnostics market, are used to detect genetic biomarkers associated with a predisposition to, or the presence of a particular disease, condition or other genetic variance. This information may enable physicians to achieve better patient outcomes and better contain health care costs through, for example, earlier diagnosis of disease, improved monitoring of disease progression and more personalized treatment selection. According to Kalorama Information, an independent market research firm, the

1

global molecular diagnostics market is expected to grow from an estimated $3.2 billion in 2007 to $5.4 billion in 2012, which represents a compound annual growth rate of 11%. Kalorama Information stated that a large portion of molecular diagnostic tests currently are performed through the use of tests assembled in-house by laboratories, commonly referred to as “home-brew” tests, and that these tests are not included in their global molecular diagnostics market estimates. We believe there are a number of trends that will increase the demand for molecular diagnostics tests, including the discovery of biomarkers associated with diseases, tailoring of therapies based on a patient’s genetic profile, decentralization of the molecular diagnostics market and the FDA’s consideration of new regulations that would require the relabeling of certain drugs to require genetic testing. We believe these trends are being driven primarily by an increased focus on cost containment and improved patient care.

We believe many existing technologies suffer from a number of drawbacks which significantly have limited the use of molecular diagnostics testing, including lack of automation, and the need for multiple specialized instruments and the utilization of expensive, highly-skilled technicians. Many of these existing technologies also have limited testing menus, are unable to multiplex, have a high cost per reportable result and/or have low sensitivity or accuracy. We believe these limitations have created the need in the molecular diagnostics market for a fully integrated, automated, multiplexing system to perform a large menu of cost-effective and easy to use tests with a high degree of accuracy and sensitivity.

Our Solution

We believe our INFINITI system addresses many of the current limitations of existing molecular diagnostic technologies. The INFINITI system is cost-effective, easy to use, highly sensitive, accurate and designed to multiplex. To use our system, an operator only needs to load prepared test samples into the bench-top INFINITI Analyzer, along with the specific BioFilmChips and Intellipac Reagent Management Modules for the desired tests. Once the INFINITI Analyzer is loaded and the tests are initiated, no supervision is required. After the test is completed, the system generates an electronic report that can be transmitted directly to a laboratory information system. Our system has several key advantages, including:

| • | Cost-effective and easy to use. The integrated, “load and go” design of the INFINITI Analyzer eliminates the need for complex protocols and manual intervention once a test is initiated, which should reduce the cost of tests by simplifying work flow and allowing the instrument to be operated without the need for highly-skilled laboratory technicians. |

| • | Broad menu of tests. As of March 31, 2010, we offered 42 tests. We believe that this represents one of the broadest menus of commercially available molecular research use or diagnostic tests provided on a single platform. As we increase the number of tests available for use on our system, laboratories using our system will be able to broaden their molecular diagnostics offerings without additional capital investment or operator training. Our system is designed to allow for the development of new and enhanced tests without modification to our platform. |

| • | Ability to multiplex. In many cases, the predisposition to a genetic disorder, or the presence of a particular disease, condition or genetic variance affecting therapy, is caused by multiple genetic mutations which necessitate testing for multiple biomarkers to diagnose those diseases, conditions or variances. Our system is able to multiplex, which reduces the amount of sample needed and the time required to run the test, and may reduce the need for multiple tests. |

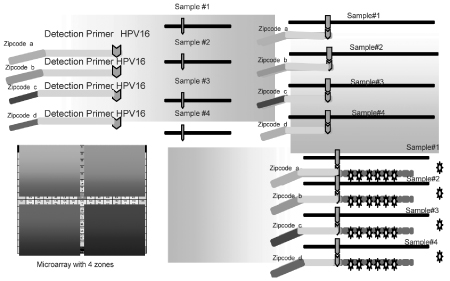

| • | Multiple Patient Array technology. Our proprietary Multiple Patient Array, or MPA, technology permits samples from up to four patients to be processed simultaneously on a single microarray, increasing system throughput by up to 300% and reducing the cost per sample by up to 75% as compared to our single patient microarrays. We also have developed the ability to produce an MPA that permits samples from up to eight patients to be processed simultaneously on a single microarray. We believe this technology will better enable us to address high volume molecular testing markets, such as those for Human Papillomavirus, or HPV, and other sexually transmitted diseases, or STDs. As these and other tests gain broader market acceptance, we believe that this technology affords us the flexibility to continue to offer highly competitive pricing while seeking to maintain our margins. |

2

| • | Higher-throughput. We believe we can substantially increase a laboratory’s throughput over existing “home-brew” and other manual and semi-automated tests by enabling them to perform their tests on our fully integrated and automated system that has the ability to multiplex and run high volume MPAs. The INFINITI Analyzer also can run multiple different tests simultaneously which reduces or eliminates the need for laboratories to run tests in batches. |

| • | Increased accuracy of results and higher sensitivity. By reducing the risk of human error and contamination, we believe our system can provide more accurate and repeatable test results than other, less automated systems. In addition, where certain systems only use target or signal amplification, we believe our combined target and signal amplification, or TSA, technologies can increase the sensitivity and specificity over these widely-used stand-alone amplification methods. |

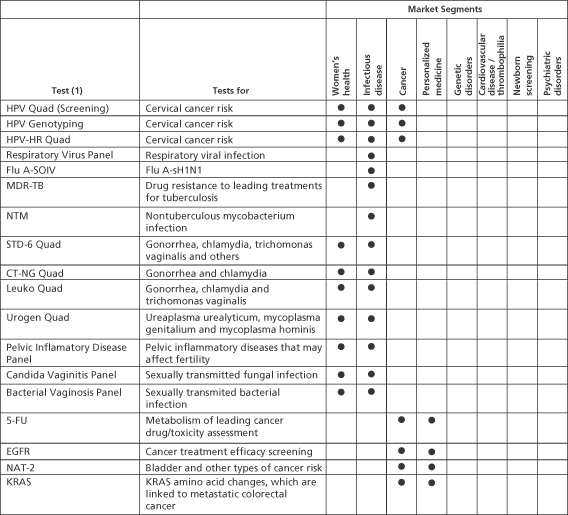

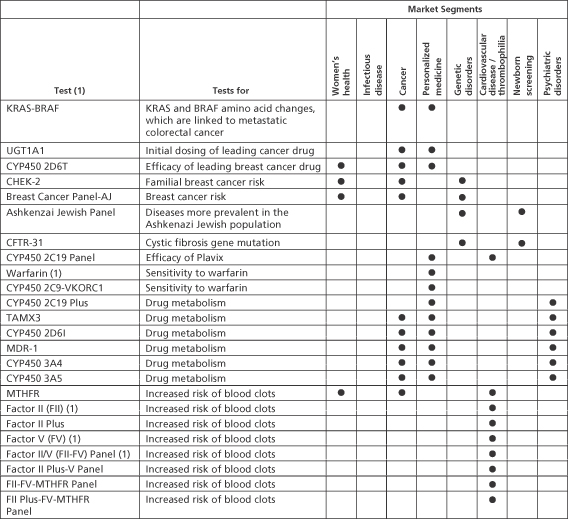

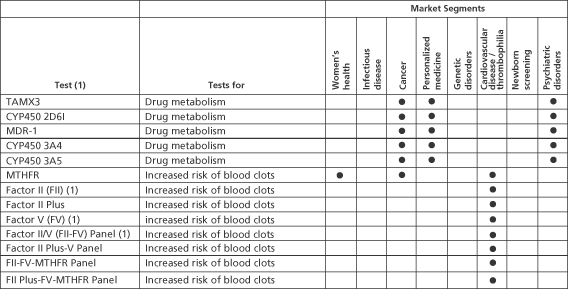

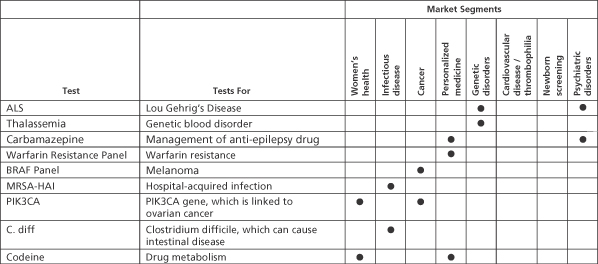

Our Tests

As of March 31, 2010, we offered the following 42 tests which can be run on the INFINITI Analyzer and focus on the areas of women’s health, infectious disease, cancer, personalized medicine, genetic disorders, cardiovascular disease/thrompbophilia, newborn screening and psychiatric disorders:

3

| (1) | The tests listed in this table have not been cleared or approved for diagnostic use by the FDA and are sold on an RUO basis, except for our Warfarin, FII, FV and FII-FV Panel tests. |

Key Market Opportunities

In developing our menu of tests, we have focused on a broad range of areas, with a particular focus on the areas of women’s health, cancer and personalized medicine, which we believe are potentially high value market segments. By offering a wide variety of tests for each of these markets, all of which can be run on our single platform, we believe we will provide a significant value proposition to laboratories that focus in these areas by allowing them to consolidate multiple testing platforms and/or expand their testing capabilities with limited additional investment in equipment or training.

4

Women’s Health

We believe we are uniquely positioned to capitalize on substantial market opportunities in certain areas of women’s health, such as HPV, other STDs and breast cancer. According to Frost & Sullivan, an independent market research firm, HPV testing products represented a worldwide market opportunity of $1.0 billion in 2006. We believe this is one of the largest segments of the women’s health genetic testing market today. In addition, we believe that the STD and breast cancer testing markets represent large and growing opportunities in women’s health. We currently offer 14 tests that may be used by laboratories in the area of women’s health.

Cancer

Due to the severity of the disease and the often high cost of treatment, tests to determine the predisposition to, diagnose or direct the treatment of various forms of cancer are becoming an important area of growth in molecular diagnostic testing. According to Frost & Sullivan, the U.S. market for cancer-focused molecular diagnostic tests was approximately $270 million in 2007 and is projected to grow to approximately $1.8 billion by 2014. We currently offer 18 tests that may be used by laboratories in the cancer-focused molecular diagnostic market.

Personalized Medicine

We also intend to become a leading provider of genetic tests in the area of personalized medicine. We believe that the use of these tests in diagnostic applications may help physicians better identify patients who will benefit from certain medications, potentially resulting in improved treatment quality and a reduction in health care costs associated with the prescription of ineffective medications. We believe this represents a significant market opportunity as physicians adopt these tests and as additional genetic variances are identified that may be relevant to treatment decisions. We currently offer 16 tests that may be used by laboratories in the area of personalized medicine.

Key Tests

HPV. Our strategy is to become a leading provider of HPV testing products. We have developed three HPV tests, our HPV Quad (Screening), HPV Genotyping and HPV-HR Quad tests, which are designed for screening and/or genotyping and each of which addresses a different segment of the HPV market. We believe that our tests offer several competitive advantages over many existing HPV screening and genotyping tests, such as the consolidation of multiple testing steps required in screening and genotyping, full automation, low sample requirement and a high degree of accuracy and specificity. We plan to seek pre-market approval, or PMA, from the FDA for our HPV-HR Quad test and 510(k) clearance for our HPV Genotyping test. Our HPV Quad (Screening) and HPV Genotyping tests have been CE marked.

Other STDs. We also intend to become a leading provider of other STD testing products. We have launched a variety of panels to enable laboratories to screen for several of the most common sexually transmitted organisms, including Chlamydia trachomatis, Neisseria gonorrhea and Trichomonas vaginalis, among others. We believe that our tests allow laboratories to address some of the limitations of many of the current testing methods, including the ability to efficiently identify a broader range of organisms in a cost effective manner, and the ability to screen for multiple organisms in a single sample collection.

Breast Cancer. We intend to become a leading provider of tests related to the diagnosis and treatment of breast cancer. We have developed tests such as our CHEK-2 and the Breast Cancer Panel-AJ tests, which are designed for use by laboratories as their tests to determine individuals at greater risk for early onset breast cancer, and our CYP450 2D6T test, which is designed for use as a laboratory-developed test to determine if a woman will benefit from Tamoxifen, a frequently prescribed drug for the prevention of breast cancer recurrence. We believe that our tests could play an important role in improving patient outcomes and reducing health care costs related to breast cancer, and in improving the screening, early diagnosis and effective treatment of certain individuals with, or potentially at risk of developing, breast cancer.

5

Colorectal Cancer. We also have developed tests focused on genetic mutations associated with a response to certain treatments of colorectal cancer. Anti-epidermal growth factor receptor, or EGFR, drugs have emerged as prevalent anticancer therapeutics as they help neutralize EGFR over-activity that has been linked to several cancers, including colorectal cancer. However, certain genetic mutations are associated with poor response to anti-EGFR therapies. We have developed KRAS and KRAS-BRAF tests, which enable laboratories to identify these mutations. We believe that our tests could assist in reducing health care costs and maximizing the effectiveness of cancer treatment by assisting in the determination of the efficacy of anti-EGFR drugs.

Pharmacogenetic Tests. In addition, we intend to become a leading provider of tests designed to assess genetically determined variations in responses to drugs, an area known as pharmacogenetics. One of our leading offerings in this area is our CYP450 2C19 Panel test, which is designed to enable laboratories to identify certain gene variants that affect the metabolism and efficacy of the anticoagulant drug Plavix. Our other leading tests in this area currently include our CYP450 2C19 Plus, Warfarin and CYP450 2D6I tests, which are designed to enable laboratories to identify certain gene variants associated with responsiveness to certain medications for psychiatric disorders, the oral anticoagulant warfarin and certain antidepressants and cancer drugs, respectively. Our Warfarin test has been cleared by the FDA and our other pharmacogenetic tests currently are available on an RUO basis. We believe that our tests could improve patient care and diminish health care costs when used by laboratories to assess the efficacy and side effects of certain medications before they are given to patients.

Our Strategy

Our objective is to become a leading provider of molecular diagnostics products to reference laboratories, hospital laboratories and specialty clinics. To achieve our objective, we intend to:

| • | Establish a large installed base of INFINITI Analyzers to generate significant recurring demand for testing consumables, including our BioFilmChips and Intellipac Reagent Management Modules. |

| • | Develop and launch new tests to increase the value of our system and drive additional INFINITI Analyzer placements and increased consumable purchases. |

| • | Expand our domestic sales force and international distribution of our products. |

| • | Pursue regulatory clearances, approvals and certifications for certain products and facilities, as necessary. |

| • | Align with key opinion leaders and increase scientific awareness of our products. |

Risks Affecting Us

Our business is subject to numerous risks, as more fully described in the section entitled “Risk Factors” elsewhere in this prospectus, including the following:

| • | There is limited information available to evaluate our business since we have a limited operating history and limited current revenue. |

| • | We have a history of losses and negative cash flows since our inception and may not be able to achieve or maintain profitability. |

| • | Our financial results depend on commercial acceptance of the INFINITI system and its tests and the development of additional tests. |

| • | Many of our competitors are large and well capitalized, and we face significant competition. |

| • | Most of our products currently are available on an RUO basis and we cannot market those products for diagnostic purposes, although laboratories can use our products as their own laboratory-developed tests. The regulatory requirements applicable to RUO products are complex and evolving, and the FDA may disagree with our interpretation of those requirements. Our failure to comply with regulatory requirements or receive regulatory clearance or approval for our products or facilities in the U.S. or abroad, as necessary, would adversely affect our revenue and potential for future growth. |

6

| • | If third-party payors do not reimburse our customers for the use of our products or if they reduce reimbursement levels, our ability to sell our products will be materially and adversely affected. |

| • | Our success will depend partly on our ability to operate without infringing or misappropriating the proprietary rights of others, on our ability to own or license patents that are adequate to reduce competition and on our ability to license intellectual property from third parties for certain tests and manufacturing processes needed for our business. |

| • | If the medical relevance of the biomarkers is not demonstrated or is not recognized by others, we may have reduced demand for our products. |

Corporate Information

We were originally incorporated as Neuron Technologies, Incorporated in California in April 1999, and changed our name to AutoGenomics Incorporated in August 2000. We subsequently changed our name to AutoGenomics, Inc. in October 2002 and reincorporated in Delaware in November 2008. Our principal executive offices are located at 2980 Scott Street, Vista, California, 92081. Our telephone number is (760) 477-2248. Our website address is www.autogenomics.com. Information contained in or that can be accessed through our website is not incorporated by reference into this prospectus and should not be considered to be part of this prospectus.

7

| Common stock offered by us |

shares | |

| Common shares to be outstanding immediately after this offering |

shares |

Use of proceeds

We estimate that our net proceeds (after deducting underwriting discounts and commissions payable to the underwriters and our estimated offering expenses) from this offering will be $ million ($ million if the underwriters exercise their overallotment option in full), based upon an assumed initial public offering price of $ per share, which is the midpoint of the range listed on the cover page of this prospectus.

From the anticipated net proceeds from this offering, we anticipate that we will use (i) approximately $ to repay the principal and interest under the $19.1 million of aggregate principal amount of outstanding subordinated promissory notes, (ii) approximately $ to fund research and development activities and clinical studies and clinical trials of our tests, including a clinical trial to support a PMA for our HPV-HR Quad test, (iii) approximately $ to fund the expansion of our sales and marketing operations and (iv) approximately $ to fund the expansion of our manufacturing capacity, including purchasing equipment. We anticipate that we will use the remainder of the net proceeds from this offering for additional working capital and general corporate purposes. See “Use of Proceeds.”

NASDAQ Global Market listing

We have applied to list our common stock on the NASDAQ Global Market under the symbol “AGMX.”

Risk factors

Investing in our common stock involves a high degree of risk. You should carefully read and consider the information set forth under the heading “Risk Factors” and all other information set forth in this prospectus before deciding to invest in our common stock.

Outstanding shares

The number of shares of common stock outstanding after this offering is based on the following as of December 31, 2009: 7,748,931 shares of common stock, 1,579,227 shares of Series A Convertible Preferred Stock, 4,302,040 shares of Series B Convertible Preferred Stock, 6,411,089 shares of Series C Convertible Preferred Stock and 3,423,258 shares of Series D Convertible Preferred Stock, and excludes as of that date:

| • | 4,430,077 shares of common stock issuable upon exercise of options outstanding at a weighted average exercise price of $1.29 per share; |

| • | 1,536,192 and 250,000 shares of common stock reserved for future issuance under our 2008 Equity Incentive Award Plan and 2008 Employee Stock Purchase Plan, respectively; and |

| • | warrants to purchase 4,018,740 shares of common stock, warrants to purchase 213,818 shares of Series B Convertible Preferred Stock and warrants to purchase 438,909 shares of Series C Convertible Preferred Stock. |

The number of shares to be outstanding after this offering also excludes warrants to purchase 1,824,100 shares of common stock we issued between January and March 2010 at a weighted average exercise price of $4.79 per share. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations — Contractual Obligations” and “Certain Relationships and Related Person Transactions — Warrant Issuances.”

8

Effective immediately prior to the completion of this offering, each outstanding share of Series A Convertible Preferred Stock will automatically convert into two shares of our common stock and each outstanding share of our Series B, Series C and Series D Convertible Preferred Stock will convert into one share of our common stock.

Except as otherwise indicated, all information contained in this prospectus assumes no exercise by the underwriters’ of their overallotment option.

The information in this prospectus does not reflect the for reverse stock split of our common stock that we plan to complete prior to the consummation of this offering.

9

The following tables provide our summary financial data and should be read in conjunction with our audited financial statements, the related notes and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included elsewhere in this prospectus. The summary statement of operations data for each of the years ended December 31, 2007, 2008 and 2009 were derived from our audited financial statements appearing elsewhere in this prospectus. Historical results are not necessarily indicative of results to be expected for future periods.

| Years ended December 31, | ||||||||||||

| 2007 | 2008 | 2009 | ||||||||||

| (in thousands, except share and per share data) | ||||||||||||

| Statement of operations data: |

||||||||||||

| Product sales |

$ | 1,607 | $ | 5,036 | $ | 5,877 | ||||||

| Cost of sales |

3,655 | 5,483 | 6,935 | |||||||||

| Gross profit (loss) |

(2,048 | ) | (447 | ) | (1,058 | ) | ||||||

| Operating expenses |

||||||||||||

| Research and development |

2,566 | 3,657 | 3,540 | |||||||||

| General and administrative |

2,423 | 3,773 | 4,692 | |||||||||

| Sales and marketing |

2,685 | 4,762 | 4,419 | |||||||||

| Total operating expenses |

7,674 | 12,192 | 12,651 | |||||||||

| Loss from operations |

(9,722 | ) | (12,639 | ) | (13,709 | ) | ||||||

| Interest income |

284 | 169 | 19 | |||||||||

| Interest expense |

(1 | ) | (416 | ) | (2,370 | ) | ||||||

| Other income (expense), net |

7 | (32 | ) | (2,534 | ) | |||||||

| Change in fair value of warrant liabilities |

139 | (186 | ) | (911 | ) | |||||||

| Net loss |

(9,293 | ) | (13,104 | ) | (19,505 | ) | ||||||

| Accretion to liquidation value of convertible preferred stock |

(74 | ) | 145 | — | ||||||||

| Net loss attributable to common stockholders |

$ | (9,367 | ) | $ | (12,959 | ) | $ | (19,505 | ) | |||

| Basic and diluted net loss per share attributable to common stockholders |

$ | (1.40 | ) | $ | (1.73 | ) | $ | (2.52 | ) | |||

| Shares used to compute basic and diluted net loss per share attributable to common stockholders |

6,671,063 | 7,489,239 | 7,730,282 | |||||||||

| Actual | As of December 31, 2009 | ||||||||||||||

| Pro forma (1) | Pro forma as adjusted (2) |

Pro forma as further adjusted (3) | |||||||||||||

| (in thousands) | |||||||||||||||

| Balance sheet data: |

|||||||||||||||

| Cash and cash equivalents |

$ | 580 | $ | 580 | $ | 580 | $ | ||||||||

| Current assets |

5,768 | 5,768 | 5,768 | ||||||||||||

| Total assets |

9,225 | 9,225 | 9,225 | ||||||||||||

| Total debt (4) |

13,306 | 13,306 | 19,081 | ||||||||||||

| Convertible preferred stock (5) |

45,577 | — | — | ||||||||||||

| Total stockholders’ deficit |

(58,927 | ) | (13,350 | ) | (13,350 | ) | |||||||||

| (1) | On a pro forma basis after giving effect to the conversion of all outstanding shares of convertible preferred stock into common stock, which will occur immediately prior to the completion of this offering. |

10

| (2) | On a pro forma as adjusted basis after giving effect to (i) the conversion of all outstanding shares of convertible preferred stock into common stock and (ii) the issuance of approximately $5.8 million aggregate principal amount of subordinated notes in February and March 2010. |

| (3) | On a pro forma as adjusted basis after giving effect to (i) the conversion of all outstanding shares of convertible preferred stock into common stock, (ii) the issuance of approximately $5.8 million aggregate principal amount of subordinated notes and (iii) the sale of shares of our common stock in this offering at an assumed initial offering price of $ per share, the midpoint of the range on the cover page of this prospectus, and after deducting underwriting discounts and commissions and our estimated offering expenses. A $1.00 increase or decrease in the assumed initial public offering price of $ per share would increase or decrease, as applicable, the net proceeds to us from this offering by approximately $ million, assuming the number of shares offered by us, as set forth on the cover page of this prospectus, remains the same and after deducting underwriting discounts and commissions and our estimated offering expenses. |

| (4) | Amounts include principal only. |

| (5) | Our convertible preferred stock had been classified as temporary equity on our balance sheets instead of in stockholders’ deficit due to the possibility of the occurrence of certain change in control events that are outside of our control, including our liquidation, sale or transfer of control, holders of the convertible preferred stock can cause its redemption. Accordingly, these shares are considered contingently redeemable. We have adjusted the carrying values of the convertible preferred stock to their liquidation values at each period end. |

11

Before deciding to invest in our common stock, you should carefully consider each of the following risk factors and all of the other information set forth in this prospectus. The following risks and the risks described elsewhere in this prospectus, including in the section entitled “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” could materially harm our business, financial condition, future results and cash flow. If that occurs, the trading price of our common stock could decline, and you could lose all or part of your investment. The risks and uncertainties described below are not the only ones we face. Additional risks and uncertainties not presently known to us or that we currently believe to be immaterial may also adversely affect our business.

Risks Relating to Our Business

Since we have a limited operating history and limited current revenue, there is limited information available to evaluate our business.

We have a limited operating history upon which one can evaluate our business and our products. As an early commercial-stage company in the new and rapidly evolving market for molecular diagnostics, we face numerous risks and uncertainties. Based on our limited experience in developing and marketing new products and tests, we may not be able to effectively:

| • | drive adoption of our system; |

| • | attract and retain customers for our products; |

| • | demonstrate and maintain the accuracy of our tests; |

| • | comply with evolving regulatory requirements applicable to products that are intended for research use only; |

| • | obtain regulatory approvals to market and sell our products; |

| • | anticipate and adapt to changes in the molecular diagnostics market; |

| • | focus our research and development efforts in areas that generate returns on these efforts; |

| • | maintain and develop strategic relationships with vendors and manufacturers to acquire necessary materials and the production of our products; |

| • | implement an effective marketing strategy to promote awareness of our products; |

| • | scale our manufacturing capacity to meet potential demand; |

| • | avoid infringement and misappropriation of third-party intellectual property; |

| • | obtain licenses on commercially reasonable terms to third-party intellectual property; |

| • | obtain valid and enforceable patents that give us a competitive advantage; |

| • | protect our proprietary technology; |

| • | provide appropriate levels of customer training and support for our products; |

| • | protect our systems from any equipment- or software-related system failures; |

| • | develop and operate computer systems and related infrastructure that are adequate to manage our growth and provide our services effectively; and |

| • | attract, retain and motivate qualified personnel. |

Our operations are subject to many of the risks inherent in the growth of a new business enterprise. The likelihood of our success must be evaluated in light of the challenges, expenses, difficulties, complications and delays frequently encountered in the operation of a new business. We cannot assure you that we will achieve anticipated revenue growth and become profitable. Our failure to meet any of these goals could have a material adverse effect on us and may force us to reduce or cease our operations.

12

We have a history of operating losses and negative cash flows since our inception and we may not be able to achieve or maintain profitability.

Since our inception, we have not been profitable. We have incurred substantial costs to develop our technology. As of December 31, 2009, we had an accumulated deficit of $63.7 million. We expect to continue to spend substantial financial and other resources on conducting clinical trials, seeking regulatory approvals, introducing new tests, expanding our sales and marketing activities, developing our technology, engaging in laboratory testing and manufacturing new products. As a result, we will need to generate significant revenue to achieve and maintain profitability.

Our ability to generate significant revenue will depend on our ability to successfully implement our business strategies and address the risks and uncertainties facing us, and we cannot assure you that we will be successful in these efforts. Even if we do address these risks successfully and implement our business strategies, we may not generate sufficient revenue to become profitable. If we were to achieve profitability, we cannot assure you that we would be able to sustain or increase profitability on a quarterly or annual basis in the future. We expect operating losses and negative cash flows to continue at least for 2010 as we continue to incur significant expenses.

Our operating results may be variable and unpredictable.

Due to the nature of the molecular diagnostics testing market, our revenue and operating results may be difficult to predict and may vary significantly from period to period. The sales cycles for our products may be lengthy, which will make it difficult for us to accurately forecast revenue in a given period. Specifically, initial sales of our products are often dependent on completing customer validation processes which may be time-consuming and unique to each customer. In addition to its length, the sales cycle associated with our products is subject to a number of significant risks, including the budgetary constraints of our customers, their inventory management practices and possibly internal acceptance reviews and the timing of FDA approval and review, all of which are beyond our control. Sales of our products will also involve the purchasing decisions of reference laboratories, hospital laboratories and specialty clinics, which can require many levels of pre-approvals, further lengthening sales time. These purchasing decisions are subject to a number of significant risk factors beyond their and our control and are difficult for us to predict. For example, reference laboratories, hospitals and specialty clinics may purchase fewer of our consumable products due to a decline in the volumes of tests needed at these facilities. As a result, we may expend considerable resources on unsuccessful sales efforts or we may not be able to complete sales as anticipated. Our international sales are also difficult to predict because they depend upon the activities of our distributors, over which we have limited control.

Our revenue and operating results may also vary due to the evolving mix between sales of our INFINITI Analyzer and consumables and the introduction of new tests. Changes in the relative mix of our INFINITI Analyzer and consumables sales can have a significant impact on our gross margin, as consumable sales typically have significantly higher margins than those of INFINITI Analyzer sales. Further, our revenue and operating results are difficult to predict because many of our tests have only recently been launched and we do not have sufficient history to forecast revenue reliably for those tests. The difficulty in accurately forecasting, and any period to period variations in, our revenue and operating results may cause our stock price to fluctuate significantly in the future.

We may not be able to meet our cash requirements without obtaining additional capital from external sources, and if we are unable to do so, we may have to curtail or cease operations.

We expect capital outlays and operating expenditures to increase over the next several years as we expand our infrastructure, commercialization, training and support, manufacturing and research and development activities. We anticipate that our current cash and cash equivalents and cash provided by operating activities and this offering will be sufficient to meet our currently estimated cash requirements for at least the next 12 months. However, we operate in a market that makes our prospects difficult to evaluate, and we may need additional financing to execute on our current or future business strategies. The amount of additional capital we may need to raise depends on many factors, including:

| • | the level of research and development investment required to maintain and improve our technology, including efforts to expand our molecular diagnostic test menu, to fund clinical studies and clinical trials of our tests and to invest in the development of new products; |

13

| • | the amount of future cash provided by or used in operating activities; |

| • | the costs of filing, prosecuting, defending and enforcing patent claims and other intellectual property rights; |

| • | our need or decision to acquire or license complementary technologies or acquire complementary businesses; and |

| • | changes in regulatory policies or laws that affect our operations. |

We have a history of operating losses and negative cash flows since our inception and we may not be able to achieve or maintain profitability. If we do not consummate this offering or obtain additional capital from other external sources we do not expect to have sufficient working capital to fund our planned operations through December 31, 2010. As a result, our independent registered public accounting firm included an explanatory paragraph relating to our ability to continue as a going concern in its report on our audited financial statements for the year ended December 31, 2009.

We cannot be certain that additional capital will be available when and as needed or that our actual cash requirements will not be greater than anticipated. If we require additional capital at a time when investment in diagnostics companies or in the marketplace in general is limited due to the then-prevailing market or other conditions, we may not be able to raise such funds at the time that we desire or any time thereafter. If we are unable to raise additional capital, we may be required to curtail some or all of our operations, including commercialization and research and development efforts, and forced to forego otherwise valuable business opportunities. Any failure to raise additional capital when needed could have a material adverse effect on us. In addition, if we raise additional funds through the issuance of common stock, preferred stock or convertible securities, the percentage ownership of our stockholders could be significantly diluted, and any preferred stock or convertible securities may have rights, preferences or privileges senior to those of common stockholders. If we obtain additional debt financing, a substantial portion of our operating cash flow or other cash resources may be dedicated to the payment of principal and interest on such indebtedness, and the terms of the debt securities issued could impose significant restrictions on our operations. If we raise additional funds through collaborations and licensing arrangements, we may be required to relinquish significant rights to our technologies or products, or grant licenses on terms that are not favorable to us.

Our level of indebtedness could adversely affect our ability to raise additional capital to fund our operations, limit our ability to react to changes in the economy or our industry and prevent us from meeting our obligations.

As of December 31, 2009, our total indebtedness was approximately $13.3 million. On a pro forma basis after giving effect to the issuance of approximately $5.8 million in aggregate principal amount of subordinated notes in February and March 2010, as of December 31, 2009, our total indebtedness would have been approximately $19.1 million. Our outstanding debt and related debt service obligations could have important adverse consequences to us, including:

| • | heightening our vulnerability to downturns in our business or our industry or the general economy and restricting us from making improvements or acquisitions, or exploring business opportunities; |

| • | requiring a substantial portion of our cash flow from operations to be dedicated to the payment of principal and interest on our indebtedness, therefore reducing our ability to use our cash flow to fund our operations, capital expenditures and future business opportunities; |

| • | limiting our ability to obtain additional financing for working capital, capital expenditures, debt service requirements, acquisitions and general corporate or other purposes; |

| • | limiting our ability to adjust to changing market conditions and placing us at a competitive disadvantage compared to our competitors who have greater capital resources; and |

| • | subjecting us to financial and other restrictive covenants in our indebtedness, the failure with which to comply could result in an event of default. |

If our cash flows and capital resources are insufficient to fund our debt service obligations, we may be forced to reduce or delay capital expenditures, sell assets, seek additional capital or restructure or refinance our indebtedness. These

14

alternative measures may not be successful and may not permit us to meet our scheduled debt service obligations. Failure to pay our indebtedness on time would constitute an event of default under the agreements governing our indebtedness, which would give rise to our creditors’ ability to accelerate our debt obligations and/or seek other remedies against us.

We may incur substantially more debt in the future. This could further exacerbate the risks associated with our existing leverage.

We may incur substantial additional indebtedness in the future. The terms of certain of our debt securities restrict, but do not in all circumstances prohibit, our ability to do so. Specifically, the terms of certain of our outstanding subordinated notes restrict us from incurring additional indebtedness without the written consent of the holders of (i) 75% of the aggregate principal amount of all subordinated notes then outstanding ($19.1 million as of March 31, 2010), and (ii) 75% of the aggregate principal amount of notes held by two noteholders ($5.1 million as of March 31, 2010), in each case subject to exceptions for certain indebtedness in an amount not exceeding $4.0 million and for permitted refinancing indebtedness. Subject to these restrictions, we are not prohibited from issuing additional debt securities or incurring other indebtedness. Moreover, we intend to use a portion of the proceeds from this offering to repay all of our outstanding subordinated notes. After repayment of the subordinated notes, the debt incurrence restrictions described above would no longer apply. If our existing and contemplated levels of indebtedness are further increased, the related risks will increase correspondingly.

Our financial results depend on commercial acceptance of the INFINITI system, its menu of tests and the development of additional tests.

Our future depends on the success of the INFINITI system, which depends primarily on its acceptance by hospitals, reference laboratories and specialty clinics as a reliable, accurate and cost-effective replacement for traditional molecular diagnostics systems. Many hospitals and reference laboratories already use molecular diagnostics testing instruments in which they have made substantial investments, and may be reluctant to change their current procedures for performing such analyses. In addition, many laboratories and some hospitals and specialty clinics currently rely on their own “home-brew” testing methods. These laboratories, hospitals and specialty clinics may be reluctant to discontinue using “home-brew” tests due to the time and expense already invested in developing and validating these tests and their familiarity with these tests compared to the INFINITI system. If we are unable to displace molecular diagnostics testing instruments and “home-brew” tests currently in use, our market opportunity will be limited and we may not be able to achieve significant sales of our consumable products.

We continue to develop additional tests for our INFINITI system to respond to the needs of reference laboratories, hospital laboratories and specialty clinics. However, we cannot guarantee that we will be able to develop enough additional tests in a timely manner or in a manner that is cost-effective or at all. The development of new or enhanced products is a complex and uncertain process requiring the accurate anticipation of technological and market trends, as well as precise technological execution. We are currently not able to estimate when or if we will be able to develop, obtain licenses to third-party intellectual property on commercially acceptable terms for, obtain regulatory approval or clearance for, commercialize or sell, additional tests or enhance existing products. If we are unable to increase sales of the INFINITI system and its tests or to successfully develop, obtain licenses to third-party intellectual property on commercially acceptable terms for, obtain regulatory approval or clearance for and commercialize, other products or tests, our revenue and our ability to achieve profitability would be impaired.

Our business may suffer if we have difficulty acquiring and retaining customers.

We may not succeed in acquiring and retaining a sufficiently large customer base for our molecular research use and diagnostics products. A large part of our business strategy depends on our ability to place a large number of INFINITI Analyzers with customers to drive sales of our consumable products. If we are unable to establish a large installed base of INFINITI Analyzers or if customers with which we place INFINITI Analyzers do not use them, we may not be able to generate revenue or implement our business strategy. In addition, if we are unable to bring our products to market as quickly as anticipated or to acquire and develop our customer base as quickly as we have projected, our ability to generate revenue could be materially adversely impacted.

15

Because we derive a significant portion of our revenue from one of our customers, our business, financial condition and results of operations could be materially adversely affected by the loss of this customer, or a significant decline in sales to or a delay in collection of payments from this customer.

We have in the past and expect to continue to derive a significant portion of our revenue from a single customer. For the year ended December 31, 2009, sales of consumable products to Bostwick Laboratories, Inc. accounted for approximately 17% of our revenue. Our continued business relationship with this customer and the amount of purchases and timing of payment by this customer may be impacted by several factors beyond our control, including product offerings by our competitors, pricing pressures or the financial health of this customer. The loss of this customer, or a significant decline in sales to or a delay in collection of payments from this customer, could materially adversely affect our business, financial condition and results of operations.

Failure by our customers or distributors to pay for products we have sold to them could have a material adverse effect on our financial condition and results of operations.

In certain cases, we may not be able to recognize revenue on sales even though we may have delivered products to our customers or distributors. For example, we have in the past sold, and may continue to sell, our INFINITI Analyzers to certain of our international distributors where our ability to collect payment was not reasonably assured. Although our distributors are required to pay us for INFINITI Analyzers that we sell to them, from time to time certain of our distributors have not paid us or have delayed payment. Where the collection of payment is not reasonably assured, in the past we have deferred, and in the future we may be required to defer, the recognition of revenue until we receive payment. Deferring the recognition of revenue could impact our results of operations negatively for any period in which the related sales occurred. We also may incur unexpected costs or losses resulting from the sales in the event of any delays or failures to make payment for the products. If we are unable to collect payment from our customers or distributors for products we have sold to them, we may have to spend additional time and resources to reclaim our products and may never be able to recover our costs to manufacture and sell such products, which could have a material adverse effect on our financial condition and results of operations.

If our customers are unwilling or unable to validate the INFINITI system or follow required protocols, our business could be harmed.

In most cases, we are dependent on our customers to validate our INFINITI system and the associated tests we offer. Individual laboratories have their own validation procedures and protocols that our system and tests must pass and we cannot predict how long each validation process will take or whether laboratories will be willing or able to validate our system and tests. To the extent that any laboratories are unwilling or unable to validate our system and tests, we will not be able to generate meaningful revenue from sales to these laboratories.

Proper use of the INFINITI system also requires our customers to follow certain sample collection and other protocols. If we are unable to develop these protocols and train our customers in their use or if, despite our efforts, customers do not follow the required protocols, the INFINITI system may not generate a result or a correct result. Failure by our customers to follow required protocols may lead to a perception, even if unfounded, that the INFINITI system does not function properly. Such perceptions could damage our reputation and brand and reduce the frequency that our customers use the INFINITI system and purchase our consumable products.

Our business may be materially adversely affected if the molecular research use and diagnostics market fails to develop or if we fail to capture a significant share of the market.

Our business may suffer if the market for research use and molecular diagnostics products fails to develop or develops more slowly than expected. Our revenue is dependent on the acceptance of molecular research use and diagnostics products by laboratories, hospitals and specialty clinics and on the expanded use of molecular diagnostic testing by physicians and hospitals. Even if we are successful in gaining acceptance of our products in laboratories, hospitals and specialty clinics, our revenue may be limited if physicians and hospitals curtail or do not expand the use of molecular diagnostic testing. Moreover, we rely in part on reference laboratories to drive demand for molecular diagnostic testing with physicians and hospitals. If these laboratories are unsuccessful in these efforts, or if laboratories that use

16

our INFINITI system lose market share to other laboratories that use competing molecular diagnostics products, our growth potential will be limited. Even if the market does develop, we cannot assure you that we will be successful in capturing a significant share of it by expanding the sale of our products at the prices we currently project. In the event that the market in general, or our market share in particular, does not grow as we expect, our business may be materially adversely affected.

We have limited experience pricing and marketing our products and we may not be able to appropriately adjust our pricing and marketing efforts in response to changes in the market.

We intend to generate revenue from one-time sales of the INFINITI Analyzer and recurring sales of consumables, including our BioFilmChips and Intellipac Reagent Management Modules. We have limited experience marketing and pricing molecular research use and diagnostics products. As such, we cannot assure you that our expectations as to pricing and marketing of these products are appropriate. The molecular research use and diagnostics market is also rapidly evolving, including due to regulatory changes and the introduction of new technologies. If we are unable to appropriately adjust our pricing and marketing efforts in response to this changing environment, we may lose market share by pricing our products too high or lose potential revenue by pricing our products lower than required to maintain or grow our market share. Our failure to price and market our products appropriately could impact our ability to attract and retain customers in the molecular research use and diagnostics market, or to establish and maintain recurring revenue streams on acceptable terms. In light of these factors, we cannot assure you that we will be able to attract a sufficient number of customers or generate sufficient revenue to support our operations.

We are subject to risks relating to the placement of INFINITI Analyzers under our Reagent Access Plan.

In the U.S., we offer the INFINITI Analyzer through direct sale and a Reagent Access Plan. Under the Reagent Access Plan, an INFINITI Analyzer is placed at the customer’s location at no direct cost to the customer in return for a commitment by the customer to purchase a minimum volume of tests, through which the direct cost of the equipment is recouped. We bear the costs of producing these INFINITI Analyzers and rely on the purchasing commitment of our customers to recoup our costs. As a result, we could expend significant resources to produce INFINITI Analyzers for our Reagent Access Plan but our customers may not purchase the expected quantity of consumables. In a limited number of instances, we have reclaimed INFINITI Analyzers placed under a Reagent Access Plan because our customer failed to meet its consumables commitment. In the event that our customers under our Reagent Access Plan do not purchase consumables as expected, our business could be materially adversely affected.

The capital spending policies of our customers have a significant effect on the demand for our products.

Our customers include reference laboratories, hospital laboratories and specialty clinics, and their capital spending policies can have a significant effect on the demand for our products. These policies are based on a wide variety of factors, including governmental regulation or price controls, reimbursement policies, the resources available for purchasing diagnostic tests, the spending priorities among various types of diagnostic tests and the policies regarding capital expenditures during recessionary periods. Any decrease in capital spending by reference laboratories, hospital laboratories or specialty clinics could cause our revenue to decline. As a result, we are subject to significant volatility in revenue. Therefore, our operating results can be materially affected by the spending policies and priorities of our customers.

Many of our competitors are large and well capitalized, and we face significant competition.

We face, and will continue to face, significant competition from organizations such as large in vitro diagnostics companies that compete directly or indirectly with us in the general molecular diagnostics market. We compete in an industry characterized by: (i) rapid technological change, (ii) evolving industry standards and regulatory requirements, (iii) emerging competition and (iv) new product introductions. Our competitors may develop and commercialize products and technologies that may mitigate any advantages our products may currently have and compete successfully with our products and technologies. Since several potentially competing companies and institutions have greater financial resources, more well-established brand names and larger existing customer bases than we do, they may be able to: (a) provide broader services and product lines, (b) make greater investments in research and development, (c) undertake more extensive sales efforts and marketing campaigns and (d) adopt more aggressive

17

pricing policies than we are able. In addition, we compete against companies on the basis of the relative regulatory status of their and our products. Some of our competitors may have already received regulatory approval and conducted extensive clinical trials for tests we seek to sell. For example, other companies have received approval of PMAs from the FDA for HPV screening tests. We expect that it may take us several years to receive approval of a PMA for our HPV-HR Quad test and approval of a PMA by the FDA is not assured. Any tests that we offer on an RUO basis may be at a competitive disadvantage to similar tests offered by others that have received FDA approval, since FDA-approved tests generally do not require separate validation by customers.

We face competition from enhanced or alternative technologies and products.

We expect to continue to face competition from enhanced or alternative technologies and products. Our technology and products may be rendered obsolete or uneconomical by advances in existing technologies or products or the development of different technologies or products by one or more of our competitors. One of our competitors could develop a product that is superior to a product we offer or intend to offer. If we are unable to keep pace with technological advances in the molecular diagnostics market, our business, financial condition and results of operations may suffer.

We rely on the innovation and resources of larger industry participants and public programs to advance genetic research, establish the medical relevance of biomarkers, and educate physicians and clinicians on molecular diagnostics.

The link between the genetic variations that our products detect and the underlying disease states or response to medications are not always fully medically validated, and our current and future products may involve biomarkers whose medical relevance is unproven. Additionally, the availability of validated biomarkers is dependent on significant investment in genetic research, often funded through public programs for which there are no assurances of on-going support. Should any government limit patent rights to specific genetic information, private investment in this area could also be significantly curtailed. In addition, the adoption of molecular diagnostics is dependent to a great extent on the education and training of physicians and clinicians. We do not have the resources to undertake such training, and we are relying on larger industry participants and professional medical colleges to establish, communicate and educate physicians and clinicians regarding the use and application of molecular diagnostics.

Growth in our business could strain our managerial, operational, manufacturing, customer support, sales, financial and information systems resources.

The anticipated future growth necessary to establish and expand our operations will place a significant strain on our managerial, operational, manufacturing, sales, financial and information systems resources. These increased demands could cause us to operate our business less effectively, which in turn could cause deterioration in the financial performance of our business. To increase revenues and achieve growth, we will need to establish and expand our sales efforts and continue to improve and develop our products. The future growth of our business will also require us to expand our customer support resources, including adding additional personnel for customer training and technical product support. If our customer support infrastructure does not keep pace with future growth of our customer base, we may lose customers and our reputation and future sales potential may be harmed. In addition, we expect that we will need to improve our financial and managerial controls, reporting systems and procedures, and that we also will need to expand, train and manage our workforce. We may be unable to hire, train and retain a sufficient number of qualified personnel or successfully manage our growth. This growth may also place increased burdens on our international distributors, increase the complexities we face related to international sales and increase our inventory-related risk. Future growth will also make it difficult for us to adequately predict the expenditures we will need to make in the future.

If we do not make the necessary capital or other expenditures to accommodate our anticipated growth, or if we are unable to manage our growth effectively, our business, financial condition and results of operations will suffer. We cannot anticipate all of the demands that our expanding operations will impose on our business, personnel, systems and controls and procedures, and our failure to appropriately address such demands could have a material adverse effect on us.

18

The loss of the services of one or more of our key personnel or failure to attract and retain other highly qualified personnel in the future could adversely affect operations and result in a loss of revenue.

We are dependent on the continued services and performance of senior management and educated, technically-trained personnel. We currently do not have employment or severance agreements with any of these persons. Our business also depends and will depend in the future on the ability to identify, attract, hire, train, retain and motivate other highly skilled technical, managerial, marketing and customer service personnel. Competition for such personnel is intense, and we cannot assure you that we will be able to successfully attract and retain sufficiently qualified personnel in the future. The failure to attract and retain necessary technical, managerial, marketing and customer service personnel could adversely affect our business and result in a loss of revenue.

Our failure to comply with regulatory requirements or receive regulatory clearance or approval for our products or operations in the U.S. or abroad would adversely affect our revenue and potential for future growth.

As a manufacturer of molecular research use and diagnostics products, our products are medical devices that are subject to extensive regulation in the U.S. by the FDA, and by respective authorities in foreign countries where we do business. The FDA regulates virtually all aspects of a medical device’s design and testing, manufacture, safety, labeling, storage, recordkeeping, reporting, clearance and approval, promotion and distribution. The FDA also regulates the export of medical devices to foreign countries. Failure to comply with the regulatory requirements of the FDA and other applicable U.S. regulatory requirements may subject a company to administrative or judicially imposed sanctions ranging from warning letters to criminal penalties or product withdrawal or recall. Unless an exemption applies, a medical device must receive either clearance or premarket approval from the FDA before it can be marketed in the U.S. For example, in limited circumstances, a product may be sold on an RUO basis before receiving clearance or premarket approval. The FDA’s 510(k) clearance process for Class II devices usually takes from three to twelve months, but may take significantly longer. The premarket approval process for Class III devices generally takes from one to three years from the time the application is filed with the FDA, but also can be significantly longer. Premarket approval typically requires extensive clinical data and can be significantly longer, more expensive and more uncertain than the 510(k) clearance process. Despite the time, effort and expense expended, there can be no assurance that a particular device ultimately will be approved or cleared by the FDA through either the 510(k) clearance process or the premarket approval process.

Medical devices may only be marketed for the indications for which they are approved or cleared. We may be required to obtain additional new premarket approvals, premarket approval supplements or 510(k) clearances to market additional products or for new indications for or modifications to our existing products. We cannot be certain that we would obtain additional premarket approvals or 510(k) clearances in a timely manner or at all. We have modified various aspects of our devices in the past and we determined that new approvals, supplements or clearances were not required. The FDA may not agree with our decisions not to seek approvals, supplements or clearances for particular device modifications. If the FDA requires us to obtain premarket approvals, supplement approvals, or 510(k) clearances for any modification to a previously cleared or approved device, we may be required to cease manufacturing and marketing the modified device or to recall such modified device until we obtain FDA clearance or approval and we may be subject to significant regulatory fines or penalties. In addition, we cannot assure you that the FDA will clear or approve such submissions in a timely manner, if at all.

We currently sell tests that have not been cleared or approved for clinical use by the FDA. These tests are labeled “For Research Use Only. Not for use in diagnostic procedures.” as required by FDA regulations. These tests are marketed to allow for the collection of research data and, in some cases, are used for clinical purposes by laboratories certified under CLIA as laboratory-developed tests pursuant to guidelines issued by the College of American Pathologists. We are not permitted to represent these products as effective in vitro diagnostic products, and must establish distribution controls to assure that our tests distributed for research, method comparisons or clinical studies or trials are used only for those purposes. As a result of a directed inspection for RUO issues in April 2009, on December 4, 2009, the FDA issued a letter to us indicating that certain of our promotional materials for our RUO tests may include diagnostic/clinical claims which may cause these products to be in vitro diagnostic tests for clinical use for which FDA clearance or approval is required. In addition, FDA noted that the allegations in its letter may not constitute an exhaustive list

19

of potential violations and noted that we are required to comply with the RUO requirements for all of our products that have not received FDA clearance or approval. We responded to the FDA’s allegations in a letter dated December 14, 2009 and believe that we have taken appropriate action to modify and revise the promotional materials in light of the FDA’s concerns. However, the FDA has not yet responded to our submission and has not confirmed its agreement with our approach. If the FDA does not agree with our approach, it could require that we take additional steps, initiate enforcement action or require that we recall or withdraw certain or all of our RUO products from the market. Our failure to comply with the FDA’s regulatory requirements, obtain FDA clearance or approvals of new or existing products or new indications or product modifications that we develop in the future, any limitations imposed by the FDA on such products’ development or use, or the costs of obtaining FDA clearance or approvals could have a material adverse effect on our business, particularly given the proportion of our business that is reliant upon RUO products.

Furthermore, the FDA has expressed its general concerns about the marketing of RUO products for use in the diagnosis or treatment of diseases. In addition, molecular diagnostics-related regulatory policies are complex and continuing to develop, and it is possible that the FDA could disagree with our interpretation of the existing regulations or that we could be exposed to additional regulation in the future. If any regulatory change results in the application of additional regulations to the molecular diagnostics industry, this could increase substantially the cost of developing and selling such testing products. For instance, our pharmacogenetic tests are in certain cases “companion diagnostics” for marketed drug and biologic products. Certain manufacturers of drugs and biologics have requested that the FDA enforce the requirement for 510(k) clearance or PMA approval in order for a test to be used to aid in the determination of a patient’s responsiveness and dosing to drugs and biologics. If the FDA were in the future to selectively take enforcement action against RUO and laboratory-developed tests functioning as companion diagnostics, we may be forced to stop selling certain of our RUO tests and our business would be materially adversely affected.