Attached files

| file | filename |

|---|---|

| EX-31.1 - FLORHAM CONSULTING CORP | v180081_ex31-1.htm |

| EX-32.1 - FLORHAM CONSULTING CORP | v180081_ex32-1.htm |

| EX-31.2 - FLORHAM CONSULTING CORP | v180081_ex31-2.htm |

| EX-32.2 - FLORHAM CONSULTING CORP | v180081_ex32-2.htm |

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

Form 10-K/A

(Amendment

No. 1)

|

x

|

ANNUAL

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT

OF 1934

|

|

For

the fiscal year ended December 31, 2009

|

|

|

o

|

TRANSITION

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT

OF 1934

|

|

For

the transition period from __________ to

__________

|

Commission

File Number: 000-52634

FLORHAM

CONSULTING CORP.

(Exact

name of registrant as specified in its charter)

|

Delaware

|

20-2329345

|

|

(State

or other jurisdiction of

|

(I.R.S.

Employer

|

|

incorporation

or organization)

|

Identification

No.)

|

845

Third Avenue, 6th Floor,

New York, New York 10022

(Address

of principal executive offices, including zip code)

Registrant’s

telephone number, including area code:

(646)

290-5290

Securities

registered pursuant to Section 12(b) of the Act:

None

Securities

registered pursuant to Section 12(g) of the Act:

Common

Stock, par value $.0001 per share

________________

Indicate by check mark if the

registrant is a well-known seasoned issuer, as defined in Rule 405 of the

Securities Act. Yes ¨ No

x

Indicate by check mark if the

registrant is not required to file reports pursuant to Section 13 or 15(d) of

the Exchange Act. Yes ¨ No

x

Indicate by check mark whether the

registrant (1) has filed all reports required to be filed by

Section 13 or 15(d) of the Securities Exchange Act of 1934 during the

preceding 12 months (or for such shorter period that the registrant was

required to file such reports), and (2) has been subject to such filing

requirements for the past 90 days. Yes x No

¨

Indicate

by check mark whether the registrant has submitted electronically and posted on

its corporate Web site, if any, every Interactive Data File required to be

submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this

chapter) during the preceding 12 months (or for such shorter period that the

registrant was required to submit and post such files). Yes ¨ No

x

Indicate

by check mark if disclosure of delinquent filers pursuant to Item 405 of

Regulation S-K (§229.405 of this chapter) is not contained herein, and will

not be contained, to the best of registrant’s knowledge, in definitive proxy or

information statements incorporated by reference in Part III of this

Form 10-K or any amendment to this Form 10-K.

Yes ¨ No

x

Indicate

by check mark whether the registrant is a large accelerated filer, an

accelerated filer, a non-accelerated filer or a smaller reporting company. See

the definitions of “large accelerated filer,” “accelerated filer”

and “smaller reporting company” in Rule 12b-2 of the Exchange

Act.

Large accelerated

filer ¨ Accelerated

filer ¨

Non-accelerated filer (Do not check if

a smaller reporting company) ¨

Smaller reporting company x

Indicate

by check mark whether the registrant is a shell company (as defined in

Rule 12b-2 of the Exchange Act). Yes ¨ No

x

The

aggregate market value of the voting and non-voting common equity held by

non-affiliates of the registrant was approximately $39,585 as of June 30,

2009.

As of

March 30, 2010, 6,705,622 shares of the registrant’s common stock, par value

$.0001 per share, were issued and outstanding, of which 179,741 shares are held

in escrow subject to future earnings attainment.

Documents

Incorporated by Reference: None.

EXPLANATORY

NOTE

This Amendment No. 1 to the

Annual Report on Form 10-K (“Amended Form 10-K”) of Florham Consulting Corp.

amends our Annual Report on Form 10-K for the year ended December 31, 2009,

filed with the Securities and Exchange Commission on March 31, 2010 (the

“Original Form 10-K”). This Amended Form 10-K is being filed solely

to include the Report of Independent Registered Public Accounting Firm in “Item

8. Financial Statements and Supplementary Data”, which was inadvertently omitted

by the EDGAR filing service provider used by the Company in the edgarization

process.

Except as described above, no other

amendments are being made to the Original Form 10-K. This Amended

Form 10-K does not reflect events occurring after the Original Form 10-K or

modify or update the disclosure contained therein in any other way other than as

required to reflect the amendments discussed above.

The Company has attached to this

Amended Form 10-K updated certifications executed as of the date of this Amended

Form 10-K by the Chief Executive Officer and Chief Financial Officer as required

by Sections 302 and 906 of the Sarbanes Oxley Act of 2002. These

updated certifications are attached as Exhibits 31.1, 31.2, 32.1 and 32.2 to

this Amended Form 10-K.

FLORHAM

CONSULTING CORP.

2009

FORM 10-K/A ANNUAL REPORT

TABLE

OF CONTENTS

|

Page

|

|||

|

PART

I

|

3

|

||

|

Item 1.

|

Business.

|

4

|

|

|

Item 1A.

|

Risk

Factors.

|

16

|

|

|

Item 1B.

|

Unresolved

Staff Comments.

|

22

|

|

|

Item 2.

|

Properties.

|

22

|

|

|

Item 3.

|

Legal

Proceedings.

|

22

|

|

|

Item 4.

|

Submission

of Matters to a Vote of Security Holders.

|

22

|

|

|

PART II

|

22

|

||

|

Item 5.

|

Market

for Registrant’s Common Equity, Related Stockholder Matters and Issuer

Purchases of Equity Securities.

|

22

|

|

|

Item 6.

|

Selected

Financial Data.

|

27

|

|

|

Item 7.

|

Management’s

Discussion and Analysis of Financial Condition and Results of

Operations.

|

27

|

|

|

Item

7A.

|

Quantitative

and Qualitative Disclosures About Market Risk.

|

31

|

|

|

Item 8.

|

Financial

Statements and Supplementary Data.

|

32

|

|

|

Item 9.

|

Changes

and Disagreements With Accountants on Accounting and Financial

Disclosure.

|

33

|

|

|

Item 9A.

|

Controls

and Procedures.

|

33

|

|

|

Item 9B.

|

Other

Information.

|

34

|

|

|

PART III

|

35

|

||

|

Item 10.

|

Directors,

Executive Officers and Corporate Governance.

|

35

|

|

|

Item 11.

|

Executive

Compensation.

|

38

|

|

|

Item

12.

|

Security

Ownership of Certain Beneficial Owners and Management and Related

Stockholder Matters.

|

44

|

|

|

Item

13.

|

Certain

Relationships and Related Transactions, and Director

Independence.

|

45

|

|

|

Item

14.

|

Principal

Accounting Fees and Services.

|

50

|

|

|

PART IV

|

50

|

||

|

Item

15.

|

Exhibits,

Financial Statement Schedules.

|

50

|

|

|

Signatures

|

52

|

2

PART I

Cautionary

Statement Concerning Forward-Looking Statements

Our representatives and we may from

time to time make written or oral statements that are "forward-looking,"

including statements contained in this Annual Report on Form 10-K and other

filings with the Securities and Exchange Commission, reports to our stockholders

and news releases. All statements that express expectations, estimates,

forecasts or projections are forward-looking statements within the meaning of

the Act. In addition, other written or oral statements which constitute

forward-looking statements may be made by us or on our behalf. Words such as

"expects," "anticipates," "intends," "plans," "believes," "seeks," "estimates,"

"projects," "forecasts," "may," "should," variations of such words and similar

expressions are intended to identify such forward-looking statements. These

statements are not guarantees of future performance and involve risks,

uncertainties and assumptions which are difficult to predict. These risks may relate to,

without limitation:

|

|

·

|

if

we are not able to continue to successfully recruit and retain our

students, we will not be able to sustain our revenue growth rate;

|

|

|

·

|

we

are subject to risks relating to tuition pricing, which could have a

material adverse affect on our financial results;

|

|

|

·

|

our

financial performance depends, in part, on our ability to keep pace with

changing market needs and technology; if we fail to keep pace or fail in

implementing or adapting to new technologies, our business may be

adversely affected;

|

|

|

·

|

we

are subject to risks relating to our information technology, system

applications and security systems, which could have a material adverse

affect on our financial results;

|

|

|

·

|

future

acquisitions may have an adverse effect on our ability to manage our

business;

|

|

|

·

|

if

regulators do not approve our domestic acquisitions, the acquired schools’

state licenses, accreditation, and ability to participate in Title IV

programs (if applicable) may be

impaired;

|

|

|

·

|

if

regulators do not approve or delay their approval of transactions

involving a change of control of our company, our state licenses and

accreditation may be impaired;

|

|

|

·

|

if

any regulatory audit, investigation or other proceeding finds us not in

compliance with the numerous laws and regulations applicable to the

postsecondary education industry, we may not be able to successfully

challenge such finding and our business could

suffer;

|

|

|

·

|

if

we fail to maintain any of our state authorizations, we would lose our

ability to operate in that state;

|

|

|

·

|

government

regulations relating to the Internet could increase our cost of doing

business, affect our ability to grow or otherwise have a material adverse

effect on our business, financial condition, results of operations and

cash flows;

|

|

|

·

|

our

success depends on attracting and retaining qualified

personnel;

|

|

|

·

|

we

may not be able to adequately protect our intellectual property, and we

may be exposed to infringement claims by third

parties;

|

|

|

·

|

we

may be subject to infringement and misappropriation claims in the future,

which may cause us to incur significant expenses, pay substantial damages

and be prevented from providing our

services;

|

|

|

·

|

our

limited operating history and the unproven long-term potential of our

business model make evaluating our business and prospects

difficult;

|

|

|

·

|

we

may need additional capital and may not be able to obtain such capital on

acceptable terms;

|

|

|

·

|

our

business may be adversely affected by a further economic slowdown in the

U.S. or abroad or by an economic recovery in the

U.S.;

|

|

|

·

|

we

may not be able to sustain our recent growth rate or profitability, and we

may not be able to manage future growth

effectively;

|

|

|

·

|

insiders

have substantial control over us, and they could delay or prevent a change

in our corporate control even if our other stockholders wanted it to

occur;

|

|

|

·

|

there

may not be sufficient liquidity in the market for our securities in order

for investors to sell their

securities;

|

|

|

·

|

the

market price of our common stock may be

volatile;

|

|

|

·

|

the

outstanding convertible securities may adversely affect us in the future

and cause dilution to existing

shareholders;

|

|

|

·

|

our

common stock may be considered a “penny stock” and may be difficult to

sell; and

|

|

|

·

|

we

have not paid dividends in the past and do not expect to pay dividends in

the future, and any return on investment may be limited to the value of

our stock.

|

Therefore,

actual outcomes and results may differ materially from what is expressed or

forecasted in or suggested by such forward-looking statements. We undertake no

obligation to publicly revise these forward-looking statements to reflect events

or circumstances that arise after the date hereof. Readers should carefully

review the factors described herein and in other documents we file from time to

time with the Securities and Exchange Commission, including our Quarterly

Reports on Form 10-Q, Annual Reports on Form 10-K, and any Current Reports on

Form 8-K filed by us.

3

Item 1. Business.

In this

report, the “Company,” "we", "us" and "our", refer to Florham Consulting Corp.,

Educational Investors, Inc., a Delaware corporation (“EII”), Valley Anesthesia,

Inc., a Delaware corporation and Valley Anesthesia Educational Programs, Inc.,

an Iowa corporation (collectively, “Valley”), and Training Direct, LLC, a

Connecticut limited liability company (“Training Direct”, and together with EII

and Valley, the “EII Group”), unless the context otherwise

requires.

Introduction

Prior to the reverse merger, we were a

publicly reporting Delaware corporation offering Internet professional services,

including providing our clients with an integrated set of strategic creative and

technology services that enable such clients to effect and maximize their

Internet business. These services helped our clients create and

enhance relationships with their customers, staff, business partners and

suppliers.

Prior

to the reverse merger, our strategic services included advising clients on

developing business models for their Internet activities, identifying

opportunities to improve operational efficiencies through online opportunities

and planning for the operations and organization necessary to support an online

business. Our creative services included developing graphic designs and Web

sites for our clients. Our technology services included recommending and

installing appropriate hardware and software networks to enable online sales,

support and communication. We also managed the hosting of clients' websites in

certain cases.

As a

result of the reverse merger, we will carry out the business and operations of

the EII Group.

EII

EII was incorporated in the State of

Delaware on July 20, 2009 for the purpose of acquiring vocational, training and

technical schools, with an initial emphasis on the health care and medical

industries. EII’s wholly-owned subsidiary, Valley Anesthesia, Inc., was

incorporated on July 15, 2009 in the State of Delaware and has its corporate

offices located in New York, New York. Effective August 20, 2009, Valley

Anesthesia, Inc. purchased certain assets and assumed certain liabilities and

operations of Valley Anesthesia Educational Programs, Inc. for an aggregate

purchase price of $3,838,215, plus certain contingent payments which are subject

to the achievement of predetermined operating milestones. EII’s wholly-owned

subsidiary, Training Direct, LLC, was organized as a limited liability company

in the State of Connecticut on January 7, 2004.

Valley

Through Valley, EII provides

comprehensive review and update courses and study materials that aid Student

Registered Nurse Anesthetists (“SRNA”) and Graduate Registered Nurse

Anesthetists (“GRNA”) in preparation for the National Certifying Exam (“NCE”)

throughout the continental United States.

Valley’s principal service is a

three-day comprehensive review and update course designed to prepare SRNAs for

the NCE. Valley also offers a 600-page basic manual. Additionally, Valley offers

MemoryMasterTM, which

is a collection of approximately 4,000 questions and answers designed to further

assist its students in preparation for the NCE. Valley presented 10 courses in

2007, 11 courses in 2008 and 12 courses in 2009. In addition, Valley has 13

courses scheduled for 2010.

Valley’s revenue is currently generated

from three sources: (i) seminars, (ii) manuals, and (iii) MemoryMasterTM. In

addition, Valley anticipates that there will be a fourth revenue source

beginning in 2010, which is from on-line practice examinations that management

expects to launch in the second quarter of 2010.

Training

Direct

Through

its Training Direct subsidiary, EII provides “distance learning” and

“residential training” educational programs for students to become eligible for

entry-level employment in a variety of fields and industries. Training Direct

strives to assist those who may not have realized their full potential in the

workplace by finding such individuals a new career direction and assisting in

progressing their learning skills necessary to reach their earning and personal

development possibilities and goals. Training Direct maintains licenses from the

Connecticut Commissioner of Higher Education, the Connecticut Department of

Health Services and the National Health Career Association, and is an Eligible

Training Provider under the Workforce Investment Act. Such licenses require that

Training Direct have a competent faculty, offer educationally sound and

up-to-date courses and course materials, and be subject to inspections and

approvals by outside examining committees.

4

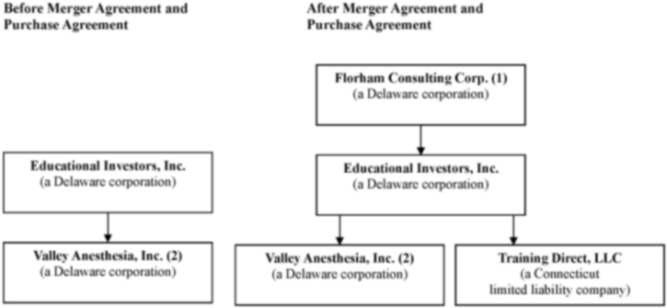

The following diagrams set forth our

corporate structure, both before and after giving effect to consummation of the

transactions contemplated by the Merger Agreement and the Purchase Agreement

described below.

(1) Corporate

name will be changed to “Educational Investors Corp.” pursuant to the Merger

Agreement.

(2) Effective

August 20, 2009, Valley Anesthesia, Inc. purchased certain assets and assumed

certain liabilities and operations of Valley Anesthesia Educational Programs,

Inc. for an aggregate purchase price of $3,838,215, plus certain contingent

payments which are subject to the achievement of predetermined operating

milestones.

Corporate

Information

Agreement

and Plan of Merger

On December 16, 2009, we executed an

agreement and plan of merger with EII Acquisition Corp. (a newly formed

acquisition subsidiary of Florham) (“Mergerco”), EII and its security holders,

Sanjo Squared, LLC, Kinder Investments, LP, Joseph Bianco and Anil Narang

(collectively, the “EII Securityholders”) pursuant to which Mergerco was merged

with and into EII, with EII as the surviving corporation of the merger, as a

result of which EII became a wholly-owned subsidiary of our company. Under the

terms of the merger agreement, the EII Securityholders received (i) an aggregate

of 6,000,000 shares of our common stock, (ii) options to acquire 2,558,968

additional shares of our common stock, 50% of which have an initial exercise

price of $0.41 per share and 50% of which have an initial exercise price of

$0.228 per share, subject to certain performance targets set forth in the merger

agreement, and (iii) 250,000 shares of our Series A Preferred Stock, with each

share of Series A Preferred Stock automatically convertible into

49.11333 shares of common stock upon the filing by us of an amendment to our

certificate of incorporation which increases the authorized shares of our common

stock to at least 50,000,000.

Pursuant to the terms of the reverse

merger, we agreed to cause (i) the shares of common stock issued and outstanding

prior to the effective time of the reverse merger; and (ii) up to 930,000 shares

of common stock issuable upon exercise of warrants expiring on June 30, 2016 at

an exercise price of $0.05 per share, to be registered for resale under the

Securities Act of 1933, as amended, as soon as practicable following the

effective time of the reverse merger.

The closing of the transactions

contemplated by the merger agreement were subject to a number of conditions

including, without limitation, completion of due diligence, approval of the

merger agreement by the Boards of Directors of EII and our company and the prior

or simultaneous closing of the interest purchase agreement (as discussed below).

On December 31, 2009, the parties to the merger agreement deemed all closing

conditions to be satisfied and accordingly, the reverse merger was consummated.

As a result of the reverse merger, we believe we are no longer a shell

corporation as that term is defined in Rule 405 of the Securities Act of 1933,

as amended, and Rule 12b-2 of the Securities Exchange Act of 1934, as

amended.

5

At the closing of the reverse merger,

all of our officers resigned and Joseph Bianco was appointed as our Chief

Executive Officer, Anil Narang was appointed as our President and Chief

Operating Officer, and Kellis Veach was appointed as our Chief Financial Officer

and Secretary. In addition, our sole director resigned and Joseph Bianco, Anil

Narang, Dov Perlysky, Howard Spindel and David Cohen were appointed as our

directors, with such resignation and appointments effective on January 22, 2010,

representing the tenth day after mailing our Schedule 14f-1 Information

Statement to our shareholders of record.

We have filed an Information Statement

on Schedule 14C under the Exchange Act, and upon the effectiveness of such

Information Statement and the expiration of the requisite 20 day period

following mailing of such Information Statement to our shareholders, we will

amend and restate our certificate of incorporation to, among other

things:

|

·

|

increase

our authorized common stock to 50,000,000 shares; and

|

|

|

·

|

change

our corporate name to “Educational Investors

Corp.”.

|

On December 23, 2009, holders of a

majority of our issued and outstanding shares of common stock have consented in

writing to approve (i) the merger agreement and the transactions contemplated

therein, (ii) our corporate name change; (iii) the increase in our authorized

shares of common stock; and (iv) our 2009 Stock Incentive Plan for key

employees, directors, consultants and others providing services to us, pursuant

to which up to 1,500,000 shares of common stock shall be authorized for issuance

thereunder. Although the Company elected to obtain consents to the

merger from holders of a majority of the then outstanding Company shares, the

Company believes that under Delaware law, neither such consents nor any other

Company shareholder approvals were required as a pre-condition to the valid

consummation of the reverse merger, which was structured as a reverse triangular

merger. Subject to approval from the SEC, Kinder Investments, L.P.

and Sanjo Squared, LLC, each affiliates of the Company, propose to enter into a

new written shareholder consent authorizing each of the name change, the share

capital increase and the 2009 Stock Incentive Plan.

Interest

Purchase Agreement

In addition to the merger agreement, on

December 16, 2009, EII entered into an interest purchase agreement

with the members of Training Direct, and our company, pursuant to which EII

acquired all outstanding membership interests, on a fully diluted basis, of

Training Direct in exchange for (a) $200,000 cash, (b) shares of our common

stock having a deemed value of $600,000 (the “Acquisition Shares”),

with such number of Acquisition Shares to be determined by dividing $600,000 by

the “Discounted VWAP” (as defined below) for the 20 “Trading Days” (as defined

below) immediately following the consummation of the reverse merger, and (c)

shares of our common stock having a deemed value of $300,000 (the

“Escrow Shares”), with such number of Escrow Shares to be determined by dividing

$300,000 by the Discounted VWAP for the 20 Trading Days immediately following

the consummation of the reverse merger. The Escrow Shares will be held in escrow

and released therefrom as provided in the purchase agreement. “Discounted VWAP”

is defined in the purchase agreement as 70% of the “VWAP” of our common stock,

but in no event less than $0.40 per share. “VWAP” is defined in the purchase

agreement as a fraction, the numerator of which is the sum of the product of (i)

the closing trading price for our common stock on the applicable national

securities exchange on each Trading Day of the 20 Trading Days following the

consummation of the reverse merger, and (ii) the volume of our common stock on

the applicable national securities exchange for each such day and the

denominator of which is the total volume of our common stock on the applicable

national securities exchange during such twenty day period, each as reported by

Bloomberg Reporting Service or other recognized market price reporting service.

“Trading Day” is defined in the purchase agreement as any day on which the New

York Stock Exchange or other national securities exchange on which our common

stock trades is open for trading. The Discounted VWAP for the twenty

Trading Days after the effective date of the reverse merger was

$1.67. Accordingly, on March 3, 2010 we issued an aggregate of

359,281 Acquisition Shares and 179,641 Escrow Shares.

The

closing of the purchase agreement was subject to a number of conditions

including, without limitation, approval of the change of ownership of Training

Direct by the Connecticut Department of Higher Education, the execution by us,

EII and the EII Securityholders of all documents necessary to affect

the reverse merger, approval of the purchase agreement by the Board of Directors

of EII and the board of managers of Training Direct and execution of a certain

employment agreement and consulting agreement. On December 31, 2009, the parties

to the purchase agreement deemed all closing conditions to be satisfied and

accordingly, the purchase and sale of the Training Direct membership interests

was consummated.

Valley’s

Program Offerings

Seminars

Each review and update course includes

26 hours over a three-day time period. The courses are located throughout the

United States in areas with high concentrations of nursing programs. Seminars

are typically held in hotel conference rooms located close to airports to

minimize logistical issues for traveling students.

6

Registration for the seminars can be

completed online, by mail or by telephone. Registration for courses for the

following year occurs at the end of August. Once the registration period has

commenced, there is significant enrollment in the seminars within a couple days.

Seminars in Cleveland and Philadelphia have traditionally had the highest

student enrollments with two courses in Cleveland that included 217 and 216

students, respectively, and 215 students in Philadelphia in 2007. In 2008, the

seminars had enrollments for two courses in Philadelphia of 224 and 220

students, respectively, and in Cleveland for two courses of 219 and 216

students, respectively. In 2009, the seminars had enrollments for two courses in

Cleveland of 211 and 209 students, respectively, a course in Philadelphia with

enrollment of 218 students and a course in Dallas with enrollment of 217

students.

Manuals

Valley publishes a course manual which

is purchased by students enrolled in the seminars and others. The course manual

consists of over 600 pages and is printed by a third party. While the volume is

fairly substantial, the complexity of the printing is not excessive and the

manuals are not bound. Production costs were approximately $175,000 in 2007,

$186,000 in 2008 and $182,000 in 2009. The manuals are ordered

from the printers each fall after registration has begun for the following

year’s courses and correspondingly, the majority of the printing costs are

incurred in the fourth quarter. Since the per unit cost to print 100

manuals is the same as the cost to print one, Valley only orders enough books to

meet its known demand. As Valley receives additional orders, it places orders

with its vendor to print the required quantity to meet the additional

demand.

MemoryMasterTM

Valley offers its MemoryMasterTM study

guide collection of approximately 4,000 questions and answers to aid its

students in preparation for the NCE by facilitating the memorization and

understanding of a large body of anesthesia-related facts, concepts and issues.

MemoryMasterTM content

is categorized according to the outline provided by the Council on Certification

of Nurse Anesthesia, which includes:

|

·

|

basic

and related clinical sciences;

|

|

|

·

|

equipment,

instrumentation and technology;

|

|

·

|

basic

principles of anesthesia;

|

|

|

·

|

advanced

principles of anesthesia; and

|

|

·

|

professional

issues.

|

MemoryMasterTM is

offered in two forms: (i) a bound, soft covered book, and (ii) flash

cards. The book provides the entire MemoryMasterTM content

in a side-by-side format, with questions appearing on the left side of each page

and the corresponding answers on the right side.

MemoryMasterTM is

printed by the same third party source as the course manuals. MemoryMasterTM can

also be ordered from the printers on an as needed basis. Management estimates

that MemoryMasterTM

accounted for approximately $340,000 of revenue in 2009. Historically, the

fourth quarter includes the greatest amount of MemoryMasterTM

shipments and related revenue.

On-Line

Practice Examinations

Valley anticipates that there will be a

fourth revenue source beginning in 2010, which is from on-line practice

examinations that management expects to launch in the second quarter

of 2010. Valley’s on-line practice examinations will be a test assessment

program where students can visit a mock testing center (the “Center”) on-line.

Practice examinations and subject-specific quizzes will be available for student

practice purposes. Valley believes that this will be a popular addition to its

offerings, and that most students who take its courses, and others who do not,

will avail themselves of the new test assessment Center. As of the date hereof,

pricing for this program has not been finalized but it is expected that the

Center will be fully functional during the second quarter of

2010.

Training

Direct’s Program Offerings

Distance

Learning Programs

Distance

learning programs provide an additional opportunity to individuals who may not

have acquired all of the education they need and are unable to take advantage of

residential training educational opportunities. Distance learning is

defined as enrollment and study with an educational institution that provides

lesson materials prepared in a sequential and logical order for study by

students on their own, allowing students to acquire new professional skills

while studying at home at their own pace. In order to help each student in their

field of study, Training Direct provides counseling and lesson assistance by

telephone and through mail.

7

Training Direct’s distance learning

offerings include educational programs in the following fields and

industries:

|

·

|

medical

office assistance;

|

|

|

·

|

medical

billing and coding;

|

|

·

|

hotel-motel

front office;

|

|

|

·

|

veterinary

assistant;

|

|

·

|

paralegal;

and

|

|

|

·

|

pharmacy

technician.

|

All of

Training Direct’s courses are priced at $1,295 to $1,600 per

program. Students may pay via cash, credit card, money order or

check.

When each

lesson is completed, the student mails the assigned work to the school for

correcting, grading, comment and subject matter guidance by qualified

instructors. Corrected assignments are rapidly returned to the student,

providing a personalized student-teacher relationship.

Medical

Office Assistant Program

Training Direct’s medical office

assistant curriculum prepares the student for a wide range of entry-level office

positions in different areas of the health industry. The curriculum prepares a

student for potential employment in medical offices, clinics, public health

departments and hospitals. The student acquires a basic understanding of medical

terminology, records management, financial administration and administrative

procedures which relate to the functioning of a medical office. An outline of

the medical office assistant curriculum includes the following, without

limitation:

|

·

|

introduction

to medical office assistance;

|

|

|

·

|

introduction

to medical terminology;

|

|

·

|

advanced

medical terminology and pharmacology;

|

|

|

·

|

administrative

medical assistance;

|

|

·

|

medical,

legal and ethical responsibilities;

|

|

|

·

|

computers

and information processing;

|

|

·

|

patients'

medical records;

|

|

|

·

|

drug

and prescription records;

|

|

·

|

office

maintenance and management;

|

|

|

·

|

fees,

credit and collection;

|

|

·

|

health

insurance systems;

|

|

|

·

|

bookkeeping;

|

|

·

|

payroll

procedures; and

|

|

|

·

|

job

search techniques.

|

A high school diploma or general

education degree is required for applicants to become eligible for the program.

Upon successful completion of the program, the student receives a

diploma.

Medical

Billing and Coding Program

Training Direct’s medical insurance

billing and coding curriculum prepares the student for entry-level employment to

process insurance claims for a medical office. There are multiple roles that the

student can fulfill with this curriculum, such as patient and administration

contact, working with computers, and accounting tasks. Specific potential career

duties consist of: (i) data collection from patients, hospitals, laboratories

and physicians; (ii) diagnostic and procedure coding; (iii) timely generation of

claims to maximize cash flow for the medical practice; (iv) keeping up to date

on insurance plans, rules and regulations; (v) bookkeeping transactions; and

(vi) follow-up on claims.

An outline of the medical billing and

coding curriculum includes the following, without limitation:

|

·

|

introduction

to medical terminology;

|

|

|

·

|

advanced

medical terminology and pharmacology;

|

|

|

·

|

fundamentals

of health insurance coverage;

|

8

|

·

|

source

documents and the insurance claim cycle;

|

|

|

·

|

coding

diagnosis;

|

|

·

|

coding

procedures;

|

|

|

·

|

the

health insurance claim form;

|

|

·

|

fees:

private insurance and managed care, the Medicaid

program;

|

|

|

·

|

the

Medicare program;

|

|

·

|

workers’

compensation coverage and other disability programs;

and

|

|

|

·

|

patient

billing: credit and collection

practices.

|

In this program, the student acquires

an understanding of basic medical terminology, anatomy and physiology,

procedural and diagnostic coding, types of medical insurance programs, insurance

claims completion and submission, payment and follow-up procedures, relevant

office skills and the role of computers in the medical office. Upon successful

completion of the program, the student receives a diploma. In addition, this

course offers students an optional opportunity to become nationally certified by

the National Healthcare Association.

Hotel-Motel

Program

Training Direct’s hotel-motel career

training curriculum prepares the student for entry-level employment in the

Hospitality industry. The student learns about the typical organizational

structure of the industry, how each department functions, what the staffing

requirements are for each department, as well as the character traits necessary

for successful employment for each part of the organization. At the completion

of the curriculum, the student is ready to apply for employment in any number of

hospitality functions such as front desk operations, catering, housekeeping,

sales and promotions, maintenance, purchasing and convention organization.

Considerable attention is also given to personnel selection, organization and

management. This is an employee intensive industry where human relations are an

important component to successful career advancement.

An outline of the hotel-motel

curriculum includes the following, without limitation:

|

·

|

the

Hospitality industry;

|

|

|

·

|

personnel

requirements;

|

|

·

|

the

General Manager and Assistant Manager;

|

|

|

·

|

front

desk operations;

|

|

·

|

the

desk clerk;

|

|

|

·

|

uniformed

services;

|

|

·

|

guest

relations;

|

|

|

·

|

the

sales department;

|

|

·

|

conventions

and meetings;

|

|

|

·

|

accounting

procedures;

|

|

·

|

cleaning

and maintenance personnel;

|

|

|

·

|

food

and beverage management team;

|

|

·

|

inventories

and control; and

|

|

|

·

|

career

guidance.

|

Upon successful completion of the

program, the student receives a diploma.

Veterinary

Assistant Program

Training Direct’s veterinary assistant

curriculum prepares the student for entry-level employment under the supervision

of veterinarians to diagnose and treat animals for injuries, illness and routine

veterinary needs such as standard inoculations and periodic check ups.

Veterinary assistants perform many tasks ranging from soothing and quieting

animals under treatment to drawing blood, inserting catheters and conducting

laboratory tests.

An outline of the veterinary assistant

curriculum includes the following, without limitation:

|

·

|

introduction

to medical terminology;

|

|

|

·

|

advanced

medical terminology and

pharmacology;

|

|

·

|

introduction

to small animal care;

|

|

|

·

|

animal

rights and welfare;

|

|

·

|

nutrition

and digestive system;

|

9

|

·

|

animal

studies, including dogs, cats, rabbits, hamsters, amphibians, reptiles,

birds, fish and others;

|

|

·

|

introduction

to veterinary practice;

|

|

|

·

|

care

and maintenance of a veterinary

facility;

|

|

·

|

administrative

duties;

|

|

|

·

|

ethics;

and

|

|

·

|

fee

collection procedures, billing and

payroll.

|

In this program, the student acquires

an understanding of basic medical terminology, the history, breeds and types of

animal groups, feeding, handling, care, housing and diseases of animals, key

terms, organizational structure and functions of the veterinary clinic, and

interacting with professional aspects of veterinary practices. Upon successful

completion of the program, the student receives a diploma.

Paralegal

Program

Training Direct’s paralegal course

prepares students for entry-level employment positions to assist lawyers.

The student gains an understanding of the scope of law that is practiced in law

offices, corporations and government agencies.

This is an intensive course requiring

extensive reading including cases in many areas of the law. In addition to

understanding the breadth of the paralegal profession, students begin by

learning legal terminology and then study the judicial system, civil and

criminal law, the anatomy of a trial as well as pretrial procedures and

research. Students also study different areas of law including Bankruptcy,

Estate Planning, Family Law, Real Estate, Contracts, Torts, Immigration and

Naturalization and Collections.

An outline of the paralegal curriculum

includes the following, without limitation:

|

·

|

the

paralegal profession;

|

|

|

·

|

law

seminars covering roots of American law, organization of the American

legal system, sources of law, the trial, and legal

terminology;

|

|

·

|

legal

research tools;

|

|

|

·

|

cause

of action in a civil case, pre-trial discovery, admissibility and use of

evidence, and trial preparation;

|

|

·

|

contracts;

|

|

|

·

|

Federal

bankruptcy;

|

|

·

|

criminal

law;

|

|

|

·

|

estate

planning;

|

|

·

|

family

law;

|

|

|

·

|

real

estate;

|

|

·

|

torts;

|

|

|

·

|

immigration

and naturalization; and

|

|

·

|

collections.

|

The duration of this course is six

months on a part-time basis. Upon successful completion of the program, the

student receives a diploma.

Pharmacy

Technician Program

Training Direct’s pharmacy technician

curriculum prepares the student for entry-level employment positions to work

under the supervision of pharmacists, to help prepare medications for dispensing

to patients, label of medications, perform inventories and order supplies,

prepare intravenous solutions, help maintain records, and perform other duties

as directed by pharmacists.

An outline of the pharmacy technician

curriculum includes the following, without limitation:

|

·

|

introduction

to pharmacy technicians;

|

|

|

·

|

introduction

to medical terminology;

|

|

·

|

advanced

medical terminology and pharmacology;

|

|

|

·

|

home

and long term health care;

|

|

·

|

regulatory

standards in pharmacy practice;

|

|

|

·

|

computer

applications;

|

|

·

|

medication

errors;

|

|

|

·

|

pharmaceutical

dosage forms;

|

10

|

·

|

pharmaceutical

calculations;

|

|

|

·

|

drug

distribution systems; and

|

|

·

|

customer

care.

|

In this course, the student acquires a

basic understanding of medical terminology, pharmacological terms,

organizational structure and function of the pharmacy, regulatory standards in

the practice of pharmacy, drug-use control and information services,

administrative aspects of pharmacy technology and professional aspects of

pharmacy technology. The duration of this course is six months on a part-time

basis. The completion of this program provides the student with the knowledge

necessary to pass the national Pharmacy Technician Certification Board exam. A

high school diploma or general education degree is required for applicants to

become eligible for this program. Upon successful completion of the program, the

student receives a diploma.

Residential

Training Program

Training Direct offers a comprehensive

Certified Nurse's Aide Program to assist its students with developing the skills

and knowledge necessary to obtain an entry-level position as a Nurse's Aide in a

health care facility. The training program provides the student with both basic

knowledge and practical experience in the terminology, procedures, and

techniques required of a Nurse's Aide. This training program meets the

Connecticut Department of Health Services guidelines for eligibility to take the

State certification exam for Nurse's Aides.

Student

Services

Students may write or call Training

Direct’s academic advisors for course assistance. For each course there is an

advisor specialized in that study area who is available to answer questions and

discuss subject matter.

Every program at the school includes

career preparation lessons to review hiring procedures, to help students write

resumes and to improve employment interview skills. Student Services matches

students with potential employers who contact Training Direct throughout the

year to fill openings.

Our

Industry

General

The

domestic non-traditional education sector is a significant and growing component

of the postsecondary degree-granting education industry, which was estimated to

be a $386 billion industry in 2007, according to the Digest of Education

Statistics published in 2009 by the U.S. Department of Education’s National

Center for Education Statistics. According to the same study, in 2007, over

6.9 million, or 38%, of all students enrolled in higher education programs

were over the age of 24, and enrollment in degree-granting institutions between

2008 and 2017 is expected to increase 19% for students over age 25. These

students would not be classified as traditional (i.e., 18 to 24 years of

age, living on campus, supported by parents, and not working full-time). The

non-traditional students typically are looking to improve their skills and

enhance their earnings potential within the context of their careers. We believe

that the demand for non-traditional education will continue to increase,

reflecting the knowledge-based economy in the U.S.

Many

working learners seek accredited degree programs that provide flexibility to

accommodate the fixed schedules and time commitments associated with their

professional and personal obligations. The education formats offered by our

institutions enable working learners to attend classes and complete coursework

on a more convenient schedule than traditional universities offer. Although more

colleges and universities are beginning to address some of the needs of working

learners, many universities and institutions do not effectively address the

needs of working learners for the following reasons:

|

·

|

Traditional

universities and colleges were designed to fulfill the educational needs

of conventional, full-time students ages 18 to 24, and that industry

sector remains the primary focus of these universities and institutions.

This focus has resulted in a capital-intensive teaching/learning model

that may be characterized by: (i) a high percentage of full-time, tenured

faculty; (ii) physical classrooms, library facilities and related

full-time staff; (iii) dormitories, student unions, and other significant

physical assets to support the needs of younger students; and (iv) an

emphasis on research and related laboratories, staff, and other

facilities.

|

|

|

·

|

The

majority of accredited colleges and universities continue to provide the

bulk of their educational programming on an agrarian calendar with time

off for traditional breaks. The traditional academic year runs from

September to mid-December and from mid-January to May. As a result, most

full-time faculty members only teach during that limited period of time.

While this structure may serve the needs of the full-time, resident, 18 to

24-year-old student, it limits the educational opportunities for working

learners who must delay their education for up to four months during these

traditional breaks.

|

|

·

|

Traditional

universities and colleges may also be limited in their ability to provide

the necessary customer service for working learners because they lack the

necessary administrative and enrollment

infrastructure.

|

11

|

·

|

Diminishing

financial support for public colleges and universities has required them

to focus more tightly on their existing student populations and missions,

which has reduced access to

education.

|

Valley

According to the American Association

of Nurse Anesthetists (“AANA”), in the United States there were 118 accredited

nurse anesthesia programs in 2010. This number grew from 108 programs in 2006,

2007, 2008 and 2009, and from 95 programs in 2005. Most SRNAs are

registered with the AANA. As set forth in the table below, the number

of SRNAs registered with the AANA has increased substantially over the past ten

years. Valley has developed strategic relationships with accredited nurse

anesthesia programs and with the AANA. Many of the programs have requested that

Valley provide courses specifically for their programs, however, Valley

currently provides courses for only one school located in

Tennessee.

|

SRNAs Registered with AANA

|

||||

|

Year

|

Registered SRNAs

|

|||

|

1999

|

2,372

|

|||

|

2005

|

4,300

|

|||

|

2006

|

4,800

|

|||

|

2007

|

5,042

|

|||

|

2008

|

5,317

|

|||

|

2009

|

5,610

|

|||

Source:

AANA

As indicated above, the number of

registered SRNAs more than doubled from 1999 to 2009. This growth in SRNAs in

the United States has expanded Valley’s potential customer base to whom Valley

markets its services. The following table sets forth a comparison of

registered SRNAs with the number of students enrolled in Valley’s courses each

year:

|

Valley’s Market Share

|

||||||||||||

|

Year

|

Registered SRNAs

|

Students Enrolled in

Valley’s Courses

|

% Registered SRNAs

Enrolled

|

|||||||||

|

1999

|

2,372

|

986

|

41.6

|

%

|

||||||||

|

2005

|

4,300

|

1,522

|

35.4

|

%

|

||||||||

|

2006

|

4,800

|

1,901

|

39.6

|

%

|

||||||||

|

2007

|

5,042

|

1,976

|

39.1

|

%

|

||||||||

|

2008

|

5,317

|

2,085

|

39.2

|

%

|

||||||||

|

2009

|

5,610

|

2,147

|

38.3

|

%

|

||||||||

Source:

AANA

Training

Direct

Training Direct is one of the largest

schools operating in the state of Connecticut within the Higher Educational

Community that offers short term training programs, which lead to numerous

employment opportunities within the Health Care Profession. Our Certified

Nurse’s Aide training program as well as Medical Billing and Coding Specialist

course are both under four weeks in length and have been very popular among our

student population.

Training Direct is also one of the only

private schools offering distance learning education programs in the State of

Connecticut. Our distance education programs offer our students the

ability to take courses from home without having to attend a classroom setting

due to such things as family or transportation constraints. Training

Direct enrollments in our programs have increased 25% from 2008 to

2009.

12

Our

Strategy and Key Corporate Objectives

Our goal is to strengthen and

capitalize on our position as a provider of high quality, accessible education

for individuals throughout the United States. Our principal focus is to provide

high quality educational products and services to our students in order for them

to maximize the benefit of their educational experience.

Generally, we intend to use our

expertise to enhance the quality, delivery and student outcomes associated with

the respective curricula across our entire group of subsidiaries. We believe we

can leverage our organizational capabilities to offer innovative products,

optimize our cost structure and create new growth opportunities. Finally, we

intend to continue to invest in our people, systems and organization,

as they are the foundation for our future success. In our opinion, these

efforts are the basis for enabling us to meet and exceed our customer’s

expectations and further differentiate us from our competition.

Specifically, EII’s key business

development objectives over the next three to five years are to seek and

consummate potential acquisitions with companies engaged in the business of

providing vocational training and test preparation products and services. In

addition, management intends to launch and further develop on-line test

assessment programs and web-based course offerings.

Management has identified a number of

such potential acquisitions within the broad context of vocational training and

test preparation, although we have not signed any definitive agreement with

respect to any additional acquisitions. Management believes that in addition to

the usual advantages of “rolling up” similar companies, such as reduced

administrative overhead, vocational schools in particular lend themselves to

significant enhancement through synergy among the schools. For example, Training

Direct’s licensure in the State of Connecticut can be used to sanction related

course offerings currently in place in an acquisition target. Thus by

acquisition, Training Direct may be able to significantly expand its course

offerings and subject areas, without commensurate increases in overhead.

Similarly, Valley, which management believes has a valuable brand name among

anesthetists, can acquire a program that actually trains (rather than

test-prepares) anesthetists, making profitable use of its reputation that has

been established over the course of a decade.

Moreover, management believes that the

vocational training space is highly fragmented and offers many opportunities for

the acquisition and enhancement of small-niche schools, and we plan to

aggressively pursue an acquisition strategy over the course of the next three to

five years.

Generally, we believe that because of

the small, development-stage nature of many potential acquisition targets that

opportunities for synergy, such as those described above for Valley and Training

Direct, will provide significant opportunities for revenue-expansion and

increased profitability, without significant operational cost

increases.

Valley and Training Direct, as well as

many potential acquisition targets, have limited or nascent on-line utilities.

As with the new Valley test assessment center, we believe that both Valley and

Training Direct can expand revenue by offering distance learning and distance

practice products related to their existing in-classroom programs. Training

Direct believes that its existing distance learning program described above,

which involves mailing student work papers back and forth, can be substantially

enhanced by use of the Internet, both in terms of enlarging the number of

students who can take such courses and by significantly reducing

costs.

Valley intends to eventually develop an

online course, so that students who cannot travel to a specific classroom

seminar can still enroll for a Valley course. Such an online program would also

be a useful addition for refresher training for students who have actually

attended a seminar. Development of this program has just begun and it is not

expected to be available for at least two years.

Our

Research and Development

Valley and Training Direct have been

developing on-line educational programs, including Valley’s on-line testing

examination center. In addition, Valley’s and Training Direct’s programs are

continually updated to ensure that students are always current with the most

updated practices and procedures. Any major revisions to

Training Direct’s curriculum are always reviewed by the Connecticut Department

of Higher Education for final approval. All programs lead to certification

from the National Health Career Association or Connecticut State Licensure. To

date, the costs of such research and development activities have been immaterial

and are not borne by our customers.

Our

Customers and Marketing

Valley

Customers

13

Valley’s customer base consists almost

exclusively of SRNAs preparing to take the NCE. It takes considerable commitment

by individuals to become a Certified Registered Nurse Anesthetist (“CRNA”). The

education and experience requirements to become a CRNA include the

following:

|

·

|

a

Bachelor’s of Science in Nursing or other appropriate baccalaureate

degree;

|

|

|

·

|

a

current license as a registered

nurse;

|

|

·

|

at

least one year’s experience in an acute care nursing

setting;

|

|

|

·

|

graduation

from an accredited graduate school of nurse

anesthesia;

|

|

·

|

clinical

training in university-based or large community hospitals;

and

|

|

|

·

|

passing

a national certification examination following

graduation.

|

Because there are extensive steps and

financial resources required for eligibility to sit for the NCE, SRNAs are

highly incented to pass the exam and are typically willing to enroll in courses

to obtain any advantage for passing the NCE. According to the AANA,

in 2005 the reported average annual salary for a CRNA was $160,000. The high

salaries paid to CRNAs provide further incentive to SRNAs to pass the

certification exam on the first or second attempt. Moreover, due to what

management believes is a high demand for CRNAs in the industry, students that

pass the certifying exam are employed almost immediately.

As a result of the strong demand for

CRNAs and the benefits associated with passing the exam, annual enrollment in

Valley’s courses has increased since 1998:

|

Student Enrollments in Valley’s Courses

|

||||||||

|

Year

|

No. of Students Enrolled

|

Growth Rate

|

||||||

|

1998

|

935

|

N/A

|

||||||

|

1999

|

986

|

5.5

|

%

|

|||||

|

2000

|

1,113

|

12.9

|

%

|

|||||

|

2001

|

1,211

|

8.8

|

%

|

|||||

|

2002

|

1,354

|

11.8

|

%

|

|||||

|

2003

|

1,488

|

9.9

|

%

|

|||||

|

2004

|

1,510

|

1.5

|

%

|

|||||

|

2005

|

1,522

|

0.8

|

%

|

|||||

|

2006

|

1,901

|

24.9

|

%

|

|||||

|

2007

|

1,976

|

4.0

|

%

|

|||||

|

2008

|

2,085

|

5.5

|

%

|

|||||

|

2009

|

2,147

|

3.0

|

%

|

|||||

Marketing

Once a year, Valley undertakes a

mailing of approximately 5,000 brochures to students and program directors for

schools that teach SRNAs. Such brochures include information regarding Valley’s

review and update course, course schedules, course pricing, and other related

data. In addition, Valley relies on word of mouth amongst SRNAs, program

directors and schools with respect to its review and update

courses.

Training

Direct

Customers

Training Direct enrolls a wide variety

of students in its programs; from working executives in our distance education

courses, to the unemployed who have been referred to us by a variety of state

agencies for our residential programs. Training Direct targets people

looking to enhance their current careers or seeking to enter the Health Care

Industry.

Marketing

Training Direct does a variety of

community outreach as well as print media, which covers over half of the State

of Connecticut. Because of its reputation in the community, Training Direct’s

referral business has been consistently strong. Training Direct expects

advertising and promotional costs to remain consistent with our growth and

revenue.

14

Our

Competition and Competitive Advantages

Valley

Valley recognizes few if any direct

competitors. There are a limited number of companies publishing manuals designed

to help students prepare for the NCE, including, without limitation, Concepts

Anesthesia Review, and Board Stiff Live. However, these competitors are not

providing an exam review course. Management believes that this enables Valley to

take advantage of potential growth opportunities within its market with limited

price or other competition. Within the past 30 to 60 days,

Dannemiller, a company engaged in the continuing medical education business,

announced that it will be offering a review course for the NCE.

Training

Direct

Training Direct has very limited

competition in Connecticut. Both the Nurse’s Aide Training and Medical

Billing and Coding courses are very much in demand because Training Direct is

located in an area which has a very high concentration of hospitals and medical

facilities.

Our

Regulatory Environment

Our operations are subject to

significant regulations. New or revised interpretations of regulatory

requirements could have a material adverse effect on us. In addition, changes in

existing or new interpretations of applicable laws, rules, or regulations could

have a material adverse effect on our accreditation, authorization to operate in

various states, permissible activities, and operating costs. The failure to

maintain or renew any required regulatory approvals, accreditation, or state

authorizations could have a material adverse effect on us.

Training Direct’s operations are

regulated by the Department of Higher Education of the State of Connecticut (the

“DHE”) from which Training Direct received its initial approval and license in

2004. The DHE seeks to promote a postsecondary system of distinctive strengths

which, through overall coordination and focused investment, assures state

citizens access to high quality educational opportunities, responsiveness to

individual and State needs, and efficiency and effectiveness in the use of

resources. The Board of Governors for Higher Education is the statewide

coordinating and planning authority for Connecticut's public and independent

colleges and universities. The Board makes higher education policy,

reviews public college and university missions and budgets, recommends

system-wide budgets to the Governor and State General Assembly, licenses and

accredits academic programs and institutions (both public and independent),

evaluates institutional effectiveness and coordinates programs and services

between the public and independent sectors. Under the Board’s supervision,

the DHE carries out Board policy, administers statewide student financial

aid programs, oversees private occupational schools and conducts research and

analysis on issues important to legislators and the public.

The DHE maintains and ensures that the

approved occupational schools offer programs and courses that have proper

organization and structure that meet their stated objectives. Also, the

DHE maintains and ensures that approved occupational schools under their

licensure follow all state statutes and regulations.

Our

Intellectual Property

We own and use the trademark

MemoryMasterTM, which

is registered with the United States Patent and Trademark Office in the name of

Valley. In addition, all of Valley’s other course materials are the subject of

copyright registrations with the United States Patent and Trademark Office in

the name of Valley. Copyright registrations expire over various periods of time.

We vigorously defend against infringements of our trademarks, service marks, and

copyrights.

Seasonality

Our cash receipts fluctuate primarily

as a result of the pattern of student enrollments. Generally, the

schools’ highest enrollment and cash receipts typically occur in the fall, which

corresponds to the third and fourth quarters our fiscal year. Enrollment is

slightly lower in the spring, and the lowest enrollment generally occurs during

the summer months. Our operating costs are relatively fixed and do

not fluctuate as significantly on a quarterly basis. Our variable

expenses fluctuate in accordance with course offerings and include course

materials, salaries and (for Valley) facility costs.

Employees

After the reverse merger and the

acquisition of Training Direct, we have 3 executive officers. Valley has a total

of 4 full-time employees. Training Direct has a total of 6 full-time

employees and 10 part-time employees. Over the next 12 months, we do not

expect to add significant personnel. None of our employees are covered by

collective bargaining agreements. We believe that our relations with our

employees are good.

15

Item 1A. Risk Factors.

You should carefully consider the

risks described below in conjunction with our forward looking statement related risks as

set forth in the beginning of this report, as well as the other information in

this report, when evaluating our business and future prospects. Should any of the

following risks actually occur, our business, financial condition and results of

operations could be seriously harmed. In that event, the market price of our

common stock could decline and investors could lose all or a portion of the value of

their investment in our common stock.

Risks

Related to Our Business and Industry in Which We Operate

We

are subject to risks relating to enrollment of students. If we are

not able to continue to successfully recruit and retain our students, we will

not be able to sustain our revenue growth rate.

Building

awareness of our schools and the programs we offer is critical to our ability to

attract prospective students. If our schools are unable to successfully market

and advertise their educational programs, our schools’ ability to attract and

enroll prospective students in such programs could be adversely affected, and,

consequently, our ability to increase revenue or maintain profitability could be

impaired. It is also critical to our success that we convert these prospective

students to enrolled students in a cost-effective manner and that these enrolled

students remain active in our programs. Some of the factors that could prevent

us from successfully enrolling and retaining students in our programs

include:

|

·

|

the

emergence of more attractive competitors;

|

|

|

·

|

factors

related to our marketing, including the cost and effectiveness of Internet

advertising and broad-based branding

campaigns;

|

|

·

|

inability

to expand program content and develop new programs in a timely and

cost-effective manner;

|

|

|

·

|

performance

problems with, or capacity constraints of, our online education delivery

systems;

|

|

·

|

failure

to maintain accreditation;

|

|

|

·

|

inability

to continue to recruit, train and retain quality

faculty;

|

|

·

|

student

or employer dissatisfaction with the quality of our services and

programs;

|

|

|

·

|

student

financial, personal or family

constraints;

|

|

·

|

adverse

publicity regarding us, our competitors or online or for-profit education

generally;

|

|

|

·

|

tuition

rate reductions by competitors that we are unwilling or unable to

match;

|

|

·

|

a

decline in the acceptance of online education;

|

|

|

·

|

increased

regulation of online education, including in states in which we do not

have a physical presence;

|

|

·

|

a

decrease in the perceived or actual economic benefits that students derive

from our programs or education in general; and

|

|

|

·

|

litigation

or regulatory investigations that may damage our

reputation.

|

In

addition, our educational programs are concentrated in selected areas of

healthcare, law and business. If applicant career interests shift away from

these fields, and we do not anticipate or adequately respond to that trend,

future enrollment and revenue may decline. If employment

opportunities for our graduates in fields related to their educational programs

decline, future enrollment and revenue may decline as potential applicants

choose to enroll at other educational institutions offering different courses of

study.

We

are subject to risks relating to tuition pricing, which could have a material

adverse affect on our financial results.

If other educational institutions

reduce their price of tuition, our educational programs could become less

attractive to prospective students. In addition, we may be unable, for

competitive reasons, to maintain and increase tuition rates in the future,

thereby adversely affecting future revenues and earnings.

Our

financial performance depends, in part, on our ability to keep pace with

changing market needs and technology; if we fail to keep pace or fail in

implementing or adapting to new technologies, our business may be adversely

affected.

Increasingly,

prospective employers of students who graduate from our schools demand that

their new employees possess appropriate technological skills and also

appropriate “soft” skills, such as communication, critical thinking and teamwork

skills. These skills can evolve rapidly in a changing economic and technological

environment. Accordingly, it is important for our schools’ educational programs

to evolve in response to these economic and technological changes. The expansion