Attached files

| file | filename |

|---|---|

| EX-32 - Cullen Agricultural Holding Corp | v178855_ex32.htm |

| EX-31 - Cullen Agricultural Holding Corp | v178855_ex31.htm |

| EX-21.1 - Cullen Agricultural Holding Corp | v178855_ex21-1.htm |

UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

WASHINGTON,

D.C. 20549

FORM

10-K

|

x

|

Annual

Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of

1934

|

For the

fiscal year ended December 31, 2009

|

¨

|

Transition

Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of

1934

|

For the

transition period from ______________to ______________

Commission

File Number 000-53806

CULLEN

AGRICULTURAL HOLDING CORP.

(Exact

Name of Issuer as Specified in Its Charter)

|

Delaware

(State

of Incorporation)

|

27-0863248

(Issuer

I.R.S. Employer I.D. Number)

|

|

320

East Clayton Street, Suite 514

Athens,

Georgia

(Address

of principal executive offices)

|

30601

(zip

code)

|

(646)

240-4240

(Issuer’s

Telephone Number, Including Area Code)

Securities

registered pursuant to Section 12(b) of the Act:

None

Securities

registered pursuant to Section 12(g) of the Act:

Common

Stock, $.0001 par value per share

Warrants

to purchase shares of Common Stock

Indicate

by check mark if the registrant is a well-known seasoned issuer, as defined in

Rule 405 of the Securities Act. Yes ¨ No

x

Indicate

by check mark if the registrant is not required to file reports pursuant to

Section 13 or 15(d) of the Exchange Act. Yes ¨ No

x

Indicate

by check mark whether the registrant (1) has filed all reports required to be

filed by Section 13 or 15(d) of the Exchange Act of 1934 during the past 12

months (or for such shorter period that the registrant was required to file such

reports), and (2) has been subject to such filing requirement for the past 90

days. Yes x No

¨

Indicate

by check mark whether the registrant has submitted electronically and posted on

its corporate Web site, if any, every Interactive Data File required to be

submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding

12 months (or for such shorter period that the registrant was required to submit

and post such files). Yes ¨ No

¨

Indicate

by check mark if there is no disclosure of delinquent filers in response to Item

405 of Regulation S-K contained in this form, and no disclosure will be

contained, to the best of the registrant’s knowledge, in definitive proxy or

information statements incorporated by reference in Part III of this Form 10-K

or any amendment to this Form 10-K.

x

Indicate

by check mark whether the Registrant is a large accelerated filer, an

accelerated filer, a non-accelerated filer or a smaller reporting

company. See definition of “accelerated filer” and “large accelerated

filer” in Rule 12b-2 of the Exchange Act (Check one).

|

Large

accelerated filer ¨

|

Accelerated

filer ¨

|

|

Non-accelerated

filer x

|

Smaller

reporting company ¨

|

|

(Do

not check if a smaller reporting company)

|

Indicate

by check mark whether the registrant is a shell company (as defined in Rule

12b-2 of the Exchange Act). Yes ¨ No

x

The

registrant has not had a completed second fiscal quarter. As of

December 31, 2009, the aggregate market value of the common stock held by

non-affiliates of the registrant was approximately $9,530,745.

As of

March 31, 2010, there were 19,255,714 shares of Common Stock, $.0001 par value

per share, outstanding.

Documents

incorporated by reference: None.

FORM

10-K

TABLE

OF CONTENTS

|

PART

I

|

1

|

|

|

ITEM

1.

|

BUSINESS

|

1

|

|

ITEM

1A.

|

RISK

FACTORS

|

11

|

|

ITEM

1B.

|

UNRESOLVED

STAFF COMMENTS

|

18

|

|

ITEM

2.

|

PROPERTIES

|

18

|

|

ITEM

3.

|

LEGAL

PROCEEDINGS

|

18

|

|

ITEM

4.

|

[REMOVE

AND RESERVE]

|

|

|

PART

II

|

19

|

|

|

ITEM

5.

|

MARKET

FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER

PURCHASES OF EQUITY SECURITIES

|

19

|

|

ITEM

6.

|

SELECTED

FINANCIAL DATA

|

19

|

|

ITEM

7.

|

MANAGEMENT’S

DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF

OPERATIONS

|

21

|

|

ITEM

7A.

|

QUANTITATIVE

AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

|

27

|

|

ITEM

8.

|

FINANCIAL

STATEMENTS AND SUPPLEMENTARY DATA

|

27

|

|

ITEM

9.

|

CHANGES

IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL

DISCLOSURE

|

27

|

|

ITEM

9A(T).

|

CONTROLS

AND PROCEDURES

|

28

|

|

ITEM

9B.

|

OTHER

INFORMATION

|

29

|

|

PART

III

|

30

|

|

|

ITEM

10.

|

DIRECTORS,

EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE

|

30

|

|

ITEM

11.

|

EXECUTIVE

COMPENSATION

|

36

|

|

ITEM

12.

|

SECURITY

OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED

STOCKHOLDER MATTERS

|

44

|

|

ITEM

13.

|

CERTAIN

RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR

INDEPENDENCE

|

47

|

|

ITEM

14.

|

PRINCIPAL

ACCOUNTANT FEES AND SERVICES

|

50

|

|

PART

IV

|

50

|

|

|

ITEM

15.

|

EXHIBITS

AND FINANCIAL STATEMENT SCHEDULES

|

50

|

i

PART

I

|

BUSINESS.

|

Cullen

Agricultural Holding Corp. (the “Company”) was incorporated in Delaware on

August 27, 2009. References herein to “we,” “us” or “our” refer to the

Company.

We are a

development stage company. Our principal focus is to use our intellectual

property in forage and animal sciences to improve agricultural yields. To date,

we have not generated any revenue and will not do so until we have sufficient

funds to implement our business plan described below.

Corporate

History

We were

formed as a wholly-owned subsidiary of Triplecrown Acquisition Corp.

(“Triplecrown”), a blank check company. CAT Merger Sub, Inc. (“Merger Sub”), a

Georgia corporation, was incorporated as our wholly-owned subsidiary on August

31, 2009. We were formed in order to allow Triplecrown to complete a business

combination (the “Merger”) with Cullen Agricultural Technologies, Inc. (“Cullen

Agritech”), as contemplated by the Agreement and Plan of Reorganization (the

“Merger Agreement”), dated as of September 4, 2009, as amended, among

Triplecrown, our Company, Merger Sub, Cullen Agritech and Cullen Inc. Holdings

Ltd. (“Cullen Holdings”). Cullen Agritech was formed on June 3, 2009. Cullen

Agritech’s primary operations are conducted through Natural Dairy Inc., a wholly

owned subsidiary of Cullen Agritech. Cullen Holdings is an affiliated entity

controlled by Eric J. Watson, our Chief Executive Officer, Secretary, Chairman

of the Board and Treasurer and, prior to the Merger, was the holder of all of

the outstanding common stock of Cullen Agritech.

Pursuant

to the Merger, (i) Triplecrown merged with and into the Company with the Company

surviving as the new publicly-traded corporation and (ii) Merger Sub merged with

and into Cullen Agritech with Cullen Agritech surviving as a wholly owned

subsidiary of the Company. As a result of the Merger, the former security

holders of Triplecrown and Cullen Agritech became the security holders of the

Company. Thus, the Company became a holding company, operating through its

wholly-owned subsidiary, Cullen Agritech. The Merger was consummated on October

22, 2009.

As of the

closing of the Merger (the “Closing”), the former shareholders of Triplecrown

had an approximate 18% voting interest in the Company and Cullen Holdings had an

approximate 82% voting interest in the Company. The Merger has been accounted

for as a reverse merger accompanied by a recapitalization of the Company. Under

this accounting method, Cullen Agritech is considered the acquirer for

accounting purposes because it has obtained effective control of the Company as

a result of the Merger. This determination was primarily based on the following

facts: Cullen Holdings’ retention of a majority voting interest in the Company;

and Cullen Holdings’ senior management serving as the senior management of the

Company. Under this method of accounting, the recognition and measurement

provisions of ASC 805, “Business Combinations” (“ASC 805”), do not apply and

therefore, the Company will not recognize any goodwill or other intangible

assets based upon fair value or related amortization expense associated with

amortizable intangible assets. Instead, the share exchange transaction utilizes

the capital structure of the Company with Cullen Agritech surviving as a

subsidiary and the assets and liabilities of Cullen Agritech are recorded at

historical cost.

1

Business

Strategy

Our

principal focus is to use our intellectual property in forage and animal

sciences to improve agricultural yields. Cullen Agritech was formed to develop,

adapt and implement grazing-based farming systems in regions of the world where

the geophysical and climatic conditions are suitable for a pasture-based model.

However, while the potential for the pasture or grazing model is significant in

many of the world’s developed and developing economies, the systems are highly

specific and require significant adaptation and modification to be successful.

The construction of a robust management framework is essential to deploy the

systems effectively in regions of the world where unique sets of geophysical,

climatic and social conditions exist. Specifically, Chile, China, Uruguay, the

United States and parts of Eastern Europe fit this criteria.

We have

identified the global dairy industry as a primary opportunity in which our

systems can be applied to improve yields on land and drive cost-base

efficiencies. Accordingly, in connection with the Merger, we acquired

approximately 3,300 acres of farmland in the State of Georgia that we believe is

suitable for the use of our proprietary farming system. We intend to begin

utilizing this property once we have sufficient capital to acquire the necessary

livestock and supplies for the farmland. We have entered into an agreement to

purchase up to 350 cows with Struve Technologies, Inc. (“Struve”), the closing

of which is expected to take place in May 2010. We intend to purchase additional

cows over the next 12 months as capital becomes available. Natural Dairy intends

to utilize the farmland to produce Class I raw milk for the liquid market in the

Eastern Seaboard and it will strive to produce milk that is of the highest

quality in conformation with food safety standards. Natural Dairy intends to use

a majority of crossbred cows that have a higher milk solid content (butter fat,

protein and lactose) than US Holsteins which we believe will consistently

produce milk which will exceed the 3.5% butter fat standard for Class I milk.

Natural Dairy will not use the Bovine Growth Hormone to produce its milk.

Natural Dairy milk should receive Class I (fluid) milk grading and pricing with

its high butter fat content, low somatic cell and bacteria counts. As a result

of its milk production operations, Natural Dairy will also be generating revenue

from the sale of livestock. This could take various forms, including, but not

limited to the sale of surplus livestock as well as the sale of livestock that

will be strategically culled as part of a herd management program. The Company

is also considering utilizing a portion of the land for the production of

pasture-finished beef products.

In

addition to the planned operation of our farmland, we intend to offer a range of

farm management and technology services such as forage techniques and genetics

and feed management strategies that are designed to help improve the

productivity and profitability of food animal production. While we specialize in

grazing systems and pasture technologies, products and services can be provided

for the traditional confinement-based dairy farm operator to integrate one or

more grazing technologies into their operations or refine their feed and animal

management strategies to improve profitability within a confinement

system.

We are

working with producers, industry leaders and governments to improve the economic

and environmental sustainability of food animal production. This includes whole

farm management plans and feasibility studies, feed production, storage and

feeding strategies, genetic improvement and rearing of replacement stock and

engineering waste management solutions.

2

Intellectual

Property

Upon

consummation of the Merger, we acquired the intellectual property that makes up

our proprietary farming system. Our intellectual property includes all

constituent components of the proprietary farming system (including forage

growth and yields, animal genetics and milking systems) that has been developed

by adapting established grazing science, processes, technology and genetics to

liquid milk production in the Southeastern United States.

Although

we may seek to register this intellectual property at a later date, none of the

intellectual property is currently registered. In the absence of registration,

protection of the intellectual property will be afforded by the scientifically

advanced nature of the information subsisting in the proprietary system. This

complexity means our system could not be readily imitated or adopted by current

or future market participants. We will seek to protect our intellectual property

by using a combination of trademark, patent and trade secrets laws, licensing

and nondisclosure agreements and other security measures.

Key

Components to Cullen Agritech’s Pasture-Based Farming System

Our first

proprietary farming system is applicable to the United States dairy industry and

has the potential to significantly increase yields on land in the Southeastern

United States. This system is based on a grazing-based farming model, whereby

dairy cows are primarily fed a renewable pasture resource as opposed to a

corn-based feed. We believe that with time, effort and resources the

intellectual property can be adapted for implementation in markets beyond the

Southeastern United States. Key components to the farming system are as

follows:

Farm Selection and Design:

The pasture-based farming system requires land with specific

characteristics. These characteristics include key soil properties and base

fertility suitable for high quality forage crop production. It also requires

contiguous blocks with shapes that minimize walking distances of grazing animals

and a high proportion of clear irrigated crop acres that enable the system to

achieve its optimum production efficiency. The farming system intellectual

property includes paddock designs that provide a high level of control over the

pasture feed resource – allowing many different varieties of pasture to be grown

and various different rates throughout the year. Paddock area and layout is a

fundamental tool that enables pasture to be accurately allocated to meet the

nutritional demand of the livestock. Paddocks and lanes are also designed to

minimize walking distances to and from the milk harvesting system and enable

efficient irrigation of grazed acreage and cooling of livestock in the summer.

Water reticulation and stock watering systems are also designed to ensure that

milking cows receive adequate fresh water to each paddock. In addition, nutrient

management plans are produced for each system so that they meet environmental

regulations. The farming system intellectual property incorporates the knowledge

and understanding of the above elements that are required to successfully

identify and convert land into a successful pasture-based dairy.

We have

identified over 40,000 effective acres (farmable acres, typically 75-80% of the

property) suitable for deployment of the pasture-based farming systems which may

be acquired and developed as capital availability allows. These sites are

primarily located in the State of Georgia and have access to an ample supply of

high quality water. Engineers and other contractors have been identified to

complete the conversion of land as well as manufacturing companies for the

installation of sheds and milking systems. Livestock required to stock the

potential farms is also being identified through multiple breeders. In

connection with the Merger, we acquired approximately 3,300 acres of farmland in

the State of Georgia that we believe is suitable for the use of our proprietary

farming system. We intend to begin utilizing this property once we have

sufficient capital to acquire the necessary livestock and supplies for the

farmland. We have entered into an agreement with Struve to purchase 350 cows and

intend to purchase additional cows over the next 12 months. As additional

capital becomes available to us, we will also begin to attempt to acquire more

acreage and deploy our pasture-based farming system on such

acreage.

3

Pasture Sciences: The farming

system incorporates a proprietary pasture production strategy that optimizes

annual cow feed supply and milk production through an integrated mix of

different pasture crop species and varieties, and management thereof. The system

incorporates a matrix of summer and winter active species that provide a

year-round supply of quality forage. The different pastures are designed to

achieve the desired quantitative and qualitative traits, including provision of

sufficient energy, protein, and trace elements to the livestock to ensure a

targeted milk production is achieved. The intellectual property includes a

detailed understanding of pasture inventory methodologies such as indirect

pasture assessment technologies, feed budgeting and pasture wedge construction

for the specific forage species used in the system. This allows efficient

utilization of the pasture resource and can identify where supplemental feeds

are required to address any quantitative or qualitative deficiency in the

pasture. The intellectual property delivers the knowledge and understanding of

the pasture production strategy including the management tools required to

manage it on a day to day basis. Without this understanding, an efficient

pasture-based production system cannot be achieved. In addition,

pasture-specific fertilization and irrigation strategies are also a key

component of the farming system intellectual property. Soil moisture sensors are

planned to be installed to ensure that irrigation is used optimally to achieve

maximum plant growth rates for the specific crop species. To complement this,

the intellectual property delivers an understanding of fertilizer application

strategies, which are used to ensure that soil fertility is not limiting forage

growth.

Animal Genetics, Breeding &

Health: The farming system intellectual property includes an

understanding of animal management systems and genetic selection criteria to

compliment the pasture-based grazing model. The farming system intellectual

property incorporates an understanding of key selection criteria to optimize cow

type for grazing. These traits include body size and conformation aspects that

improved structural health, lower feed requirements for body maintenance, and

improved tolerance to environmental extremes (heat and cold). Animals are

selected for improved conception rates and maternal traits to increase calf

numbers, reduce culling due to reproductive failure and ensure seasonal calving.

The environment where the farming system is deployed has hot summers where

production is affected if tolerance to heat is not included as a breeding

objective. The intellectual property delivers an understanding of specific

strategies for identifying heat tolerant animals and building this trait more

quickly into the herd. These strategies include low pressure misting lines on

center pivot irrigators to cool cows in the summer months as well as mister and

sprinkler systems in the milking parlor to further lower body temperature in the

summer. Specific milk harvesting strategies such as timing of the milking

process have been developed to maximize milk production and cow comfort during

milking.

Genetic

selection pressure is also driven towards animals that have greater efficiency

in the conversion of cellulosic plant (forage-based) diets into milk. Genetic

improvement programs are planned be further enhanced with the use of automated

animal management systems with radio frequency ID tags that individually track

animal performance, feeding, and health status, and allow animals to be selected

on these criteria. The understanding of these genetic-selection criteria, which

is a key component of the intellectual property, will enable rapid development

of livestock lines that are ideally adapted to pasture based production in the

Southeast US environment.

4

Farm Management: In addition

to the pasture management strategies and breeding and culling programs, the

pasture-based farming system is designed around significant labor, herd

management and waste management efficiencies. The intellectual property includes

an understanding of how to maximize the speed and efficiency of the milking

systems, which, if used correctly, can allow two people to milk up to 500 cows

per hour, greatly reducing labor requirements and waste production. Animal

management systems such as fencing, lanes and yards allow animals to be quickly

moved to various pasture crops on the farm and brought in for milking twice a

day with little labor required. The fencing and stock water systems also allow

the animals to be allocated variable amounts of pasture feed as needed by the

movement of herds between pasture blocks as well as the use of temporary

electric fencing. A key component of the farming system intellectual property is

an understanding of how to execute this movement of the herds on a daily basis

in order to maximize the pasture utilization. The herd management systems also

allow the separate management of different herds in their contemporary groups by

calving season, age structure, and production targets enabling differential

feeding to individual groups as their status requires. The understanding and

management of such systems is critical in order to achieve the expected

operational efficiencies that a pasture-based system can deliver. Effluent

management systems quickly and efficiently recycle waste water by reapplication

back onto the pasture using a holding sump, pump and traveling irrigator system

designed for grazing systems, eliminating the need for any storage of animal

waste, as is necessary in confinement animal operations. The effluent applied

over a relatively large land base becomes a valuable source of fertilizer rather

than a costly waste product with a significant risk of environmental

contamination.

Systems & Training: Day

to day management of the farms is critical to success. Therefore, highly trained

farm managers who are skilled in grazing management, pasture crop production and

animal sciences will need to be trained. As explained, the system includes

various specific requirements including detailed management processes such as

those associated with pasture production, culling strategies, herd management

and effluent management systems. Therefore, an accurate understanding how to

communicate and train the key day to day farm managers will be essential to

efficiently run a large pasture-based dairy operation. A key part of the

intellectual property includes the understanding of how to train and manage the

farm management staff to ensure the key performance criteria are

achieved.

Testing

of Cullen Agritech’s Farming System

During

2008 and 2009, our intellectual property was tested on several research farms.

This testing was led by Dr. Richard Watson, the Company’s Chief Scientific

Officer and director. None of the testing procedures or results have been

independently verified by a third party.

5

Forage

Systems

The

research farm conducted forage variety and species testing on both a ‘small

plot’ and whole farm scale to determine key forage characteristics such as dry

matter (yield) growth profiles by month, nutrient content (energy and crude

protein), persistence under grazing and compatibility with other forage species.

Species evaluated include C4 perennials such as Bermuda Grass (Cynodon dactylon), several C4

annual species such as Millet and Sudangrass, C3 annual and perennial temperate

grasses and legumes, as well as perennial herbs such as chicory. Monthly samples

were collected from the replicated small plots to analyze dry matter growth

(pounds of dry matter per acre per day), metabolizable energy and crude protein.

The ‘small plot’ trials are in a ‘replicated complete block design’ according to

strict scientific rigor that is embedded within larger pastures on the research

farm. These plot trials allow the simultaneous evaluation of many species and

forage varieties in a common environment, across a range of key parameters. The

larger whole paddock and farm systems trials were a phase 2 follow-on from the

small plot work where the most promising candidates can be assessed on a larger

scale.

The

results of these trials provided us with a nutritional and growth profile

database of many forage crop species and varieties. This database has been used

to create a forage species matrix that provides a best fit solution to the

nutritional (qualitative) and dry matter (quantitative) requirements of the

dairy herd. Such research and development strategies will continue to be used to

develop and evaluate new forage species as they become available through

commercial breeding programs and from within our own breeding

collaborations.

Animal

Genetics and Type Evaluations

The

research farm acquired livestock across a range of breed types and calving

seasons. Detailed records have been kept on productivity (milk yield),

reproductive performance (conception rate to artificial insemination and natural

mating), health, body condition and heat tolerance. Analysis of these records

has resulted in the development of a livestock strategy that will complement the

forage strategy and produce the desired performance both on a production and

cost basis. The key findings indicated that USA Holsteins are less suitable for

the pasture-based farming systems than Holstein / Jersey crosses and purebred

Jersey breeds. The ideal calving season to make most effective use of grown

forage and minimize environmental stress on the cow is to have herd calving

seasons in the spring and autumn and in particular avoid trying to calve and

mate in the summer when heat adversely affects both production and reproductive

performance in the cow. Specific mating systems and seasonal calving strategies

are a key differentiator of a pasture-based system when compared to a

traditional, confinement dairy system. The results of such testing allowed us to

develop strategies which are instrumental to the intellectual property including

those surrounding species selection, culling programs and reproduction

management strategies.

Supplemental

Feed Inputs

The

prevalence of United States genetics in the herd required that supplemental feed

input analysis be undertaken to assess what feed levels and feed formulations

were necessary to complement a pasture-based diet. This analysis is required in

order to achieve the targeted stocking rates while maintaining a feed plan that

will deliver sufficient energy to the livestock. The use of supplementary feeds

is contrary to a New Zealand-based system where it would not be unusual for

there to not be any supplemental feeding strategy utilized. Led by Dr. Watson,

we undertook a close examination of energy and trace element intake, which is

required to ensure that a complete diet is fed to the livestock to meet the

nutritional requirements for body maintenance and milk production.

6

Results

of this work have indicated that a pasture only diet is not possible with a 100%

United States genetic base. The research has resulted in the development of a

specific supplemental feeding strategy which incorporates between 25% and 30%

concentrated corn-based feed. An understanding of how to manage this

supplemental feeding strategy on a day to day basis, in response to monitoring

forage development and key performance indicators such as production per cow, is

also core to the intellectual property that has been developed through this

research. Such a strategy must be included in the overall system to balance

energy and mineral requirements of the milking animal. From this data, a genetic

improvement program has been developed that will look to increase the proportion

of Jersey and Jersey crosses and incorporate smaller framed New Zealand Holstein

genetics into the herd to improve reproductive performance and feed efficiency

on a pasture-based system.

Nutrient

Management

The

research farm has undertaken studies to evaluate the environmental impact of the

pasture based system and associated effluent management processes. Serial soil

analyses have been used to track the profile of key nutrients and organic matter

in the soil including nitrates, phosphate and potassium and carbon

sequestration. Results to date indicate that the system developed on the

research farms delivers no nutrient loading, an improvement in nitrogen

fertilizer use efficiency over row crop production and an improvement in soil

physical properties (organic matter, and structure). It is anticipated that

these trials will identify key areas where pasture based animal production has

significant environmental advantages.

Research

has been undertaken to quantify the impact of animal waste production and

management in the grazing system. We have worked closely with Land Grant

Universities and State Departments of Agriculture to quantify waste management

parameters and implement policy changes that reflect the improvements of the

grazing system over the confinement feeding systems.

Competitive

Strengths

Key

Cullen Agritech personnel have extensive experience in improving yields through

applying pasture based farming techniques

Significant

time and resources have been invested by our key personnel, including Dr.

Richard Watson, a member of our board of directors and the Chief Scientific

Officer of Natural Dairy, in developing the necessary capabilities to deploy our

pasture-based technologies. Dr. Watson has an extensive background in pastoral

science and technology, from the laboratory to commercialization and industry

application of technologies. Dr. Watson is supported by Dr. Todd White, Cullen

Agritech’s Farming Systems Technical Manager, who, prior to joining the Company

on January 1, 2010, was a senior scientist at AgResearch in New Zealand. During

his time at AgReseach, Dr. White led research and development programs utilizing

and improving pasture-based animal production and biophysical ecosystem models.

Prior to joining AgResearch, Dr. White spent three years in a post-doctoral

forage research position at Iowa State University.

We have

also assembled an experienced group of pastoral scientists and dairy science

industry participants to serve on our advisory board to further enhance our

position as an innovative technology company with the ability to bring efficient

pasture-based production systems to the agricultural community in the United

States. The members of our advisory board have access to embryo, semen and

genetic screening technologies (SNP-chip) that may accelerate genetic

improvement and deployment of these lines in the United States dairy

industry.

7

Tested

model through research farms developed by key Cullen Agritech personnel to

provide cost advantages

Our

proprietary farming system was developed and tested on research farms in Girard,

Georgia. These farms were established to develop and test the proprietary

grazing system that Natural Dairy plans to roll-out in the Southeastern United

States. Although we do not own these research farms, we own all the intellectual

property associated with the farming system developed on these farms. The first

research farm began producing milk in March 2008. During 2008, it was used to

refine and develop the farming system. This research was focused on the

development of a pasture crop system that maximized the production and

utilization of grown pastures. Breeding and calving season trials have been

conducted to optimize the relationship between feed grown on farm and the feed

demand of the herd. During 2009, the farming system was refined and has achieved

favorable production cost results, proving the efficiency of the

system.

Forage

based system provides lower cost per hundred pounds (“cwt”) of dairy

production:

The cost

of producing milk will vary greatly depending on the region, the exact

management practices and quality of farmers. For a majority of dairy farmers,

the high dependence on the use of corn-based concentrate as a feedstock results

in a high cost base. The use of pasture as a replacement for corn-based

concentrate in our model reduces this expense, creating a much more

economically-sustainable cost structure. Our model will also be less labor

intensive and is more likely to have reduced animal health costs due to

healthier and less confined conditions.

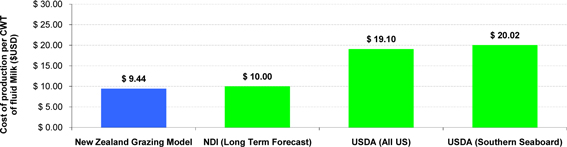

The chart

below depicts the cost structures of various dairy farm operating models. The

New Zealand pasture-based grazing model has generally operated at $8.00-$10.00

per cwt cost levels. Given the research and development completed to date,

Natural Dairy’s management believes that a cost structure as low as $10.00 per

cwt is achievable in the long term. In comparison, the traditional United States

confinement based model operated at an average of $19.10 per cwt during 2007 and

2008 ($20.02 per cwt for the US Southern Seaboard region).

Chart 7

Cost Comparison of Different Farming Models

Source:

United States Department of Agriculture (“USDA”), Cullen Agritech

Management

Natural

Dairy is strategically located in a region of high demand coupled with a

shortage in supply

Natural

Dairy’s roll-out will be focused in the Southeastern United States where there

is currently a shortage in the supply of fresh liquid milk. In addition, the

United States represents the third largest liquid milk market in the world, a

large proportion of which is represented by the Eastern Seaboard. Natural Dairy

will be strategically positioned to help fill that supply gap and produce milk

for this market, which is currently undersupplied.

8

Efficient

production per cow

We intend

to utilize pasture production systems that optimize seasonal qualitative

attributes of the pasture to best match the energy demands of its herds. Under

these systems, the cow is provided sufficient nutrients to meet her needs for

body maintenance and milk production. We intend to employ energy balances (the

difference between the energy gained from feed intake and the energy expenditure

associated with different physiological functions such as maintenance, milk

production, pregnancy, and growth) to ensure that the cows are fed enough

pasture to achieve the highest possible production targets in the most cost

effective manner. Management believes this level of feed management sets us

apart from other grazing operations in the USA.

Cullen

Agritech’s system will result in healthier livestock and increased

longevity

The

common United States dairy industry cow is the US Holstein. Our model is suited

to smaller framed livestock such as Jersey/Holstein cross-breeds or a Friesian

Holstein. These breeds of livestock generally have longer productive lives than

a typical US Holstein, which is further lengthened by the healthier conditions

associated with our pasture-based farming system which we own. This longevity is

expected to result in reduced livestock culling rates and additional revenue

from surplus livestock sales. Livestock managed under the system are also likely

to have fewer health issues due to increased exercise and exposure to cleaner,

less confined living conditions. As a result animals are healthier and the speed

at which infection can spread throughout a herd is reduced. This, in turn,

results in increased longevity as well as reduced health-related operating

expenses on the farms.

Reduced

labor costs

We will

utilize milking systems which are custom made to maximize efficiency and

minimize labor costs. This technology, combined with a unique and efficient farm

design and management strategy, results in reduced labor costs, further reducing

the cost of production under the system that we will utilize.

Potential

to achieve higher pricing in the future

Management

believes the demand for naturally produced food animal products is increasing as

the population’s concern with how their food is produced increases. General

awareness of the animal ethics and human health benefits of the grazing-based

production system have also grown. For instance, a USDA survey showed that 48%

of United States consumers now recognize “Grass-fed” as a brand.

Products

from animals fed on a pasture dominant diet have been found to contain higher

levels of a number of naturally occurring metabolites that have proven human

health benefits. The fermentation of the pasture diet in grazing animals by

rumen bacteria create higher levels of conjugated linoleic acid (CLA), omega-3

and 6 fatty acids and vitamins A and E in the milk. Production of these

qualities in milk produced by confinement cows is reduced by the heavy-starch

grain diet, which reduces the formation of these beneficial fermentation

products.

9

Currently,

there is a small but rapidly growing market for grass-fed or pasture-fed beef

products. However, grass-fed milk products are limited due to dominance of the

confinement model and the lack of producers who have the technical knowledge to

produce milk on pasture year round.

Natural

Dairy has the ability to produce grass-fed milk year round in selected markets.

Further, expected milk production levels may in the future result in

availability of separate processing, with Natural Dairy’s grass-fed milk being

processed separately from other milk. However, Natural Dairy milk will be

initially sold as standard milk along with milk from confinement production.

This means it will not initially receive premium pricing for its milk products

on the basis of its “grass-fed” product. The Company is also exploring the

ability to produce grass-fed beef products, which also could be sold for a

premium in the marketplace.

Strategic

agreements and relationships allow for efficient large scale rollout of pasture

based system

As

described in more detail below, Cullen Agritech entered into a strategic

cooperation agreement with New Zealand Agritech, Inc. (“NZ Agritech”), New

Zealand’s national representative body for agricultural technology companies

operating in New Zealand, to promote the interests of NZ Agritech and its

members. Cullen Agritech will assist members of NZ Agritech to mitigate barriers

of market entry and provide the opportunity to realize potential growth in

various markets. This alliance reflects an important connection to participants

of New Zealand’s agricultural technology industry and enables us to offer its

customers the benefit of our advanced technologies.

We

believe that this and other potential strategic relationships will help to build

our business and operations.

Our

business encompasses a broad exposure to third parties operating within the

agricultural science industry, including those which have developed or that

otherwise promote products and/or technologies that compliment our business

objectives. A number of these third parties are seeking to expand into markets

in which we will undertake business activities. Management believes that we are

positioned to partner with such third parties to assist with market entry and

that joint venture opportunities exist in respect to product and technology

adaptation services, in addition to potential marketing

arrangements.

On August

11, 2009, Cullen Agritech entered into a strategic cooperation agreement with NZ

Agritech. Pursuant to the agreement, Cullen Agritech will assist members of NZ

Agritech to mitigate barriers of market entry and provide the opportunity to

realize the potential growth in various markets. NZ Agritech in turn will

actively promote to its members its alliance with Cullen Agritech. Accordingly,

this relationship with NZ Agritech presents Cullen Agritech with the opportunity

to enter joint ventures and strategic alliances with New Zealand companies

offering innovative products and technologies which promote efficient farming

systems, including those seeking assistance with adaptation to the Southeastern,

United States. The agreement is perpetual in nature but may be terminated by

either party upon three months’ notice. Cullen Agritech is obligated to pay a

fee to NZ Agritech annually, in arrears, based on its dealings with NZ

Agritech’s members. No such dealings have taken place to date and therefore no

fee is currently owed. The fee is to be negotiated on a year by year

basis.

10

Within

the United States, we believe the know-how residing in its pasture-based farming

system will present the opportunity for joint ventures with federal and state

departments and businesses including dairy cooperatives, universities, training

institutions and farmers.

Customers/Sales

and Marketing

We intend

to partner with and provide services to some of the world’s largest agricultural

companies, including producer cooperatives, corporate farmers, investment funds

and agricultural technology providers. Our expertise can be applied across a

range of global regions and production systems that utilize pasture systems and

technologies for food animal production and can assist industry and government

organizations in adapting these technologies to their regions and production

requirements. Natural Dairy’s customer base will be predominately milk

cooperatives that supply processing facilities.

Competition

Potential

competitors are large agricultural technology and service providers that might

develop a globally focused consultancy capacity that is focused on the grazing

model and technologies. To our knowledge, there is currently no other entity

operating in the global grazing technology industry, provided, however companies

could potentially develop this capability. These potential competitors include

PGG Wrightson (NZ), Livestock Improvement Corporation (NZ), New Zealand Farming

System Uruguay (NZ), Grasslands Consultancy LLC (Mo, USA), Manuka Farming

(Chile) and Fonterra. To management’s knowledge, none of these companies

currently provide agricultural consultancy services of significance outside

their country of incorporation and may have limited capacity to move to other

regions as a technology provider.

Although

Natural Dairy will face competition from other liquid milk producers across the

United States, the effect of such competition is not expected to be adverse

given the supply gap that exists in the liquid milk market in the Southeastern

United States.

Employees

Currently,

we have four employees, all of which are not represented by any unions, nor are

we otherwise subject to any collective bargaining agreements. We have never

experienced a strike or similar work stoppage. We consider our relations with

our employees to be good.

|

ITEM

1A.

|

RISK

FACTORS

|

Risks

Related to Cullen Agritech’s Business

Cullen

Agritech has no operating history and may not be able to successfully operate

its business or generate sufficient revenue to make or sustain distributions to

its stockholders.

We were

incorporated in August 2009 in order to consummate the Merger and acquire Cullen

Agritech. Cullen Agritech was incorporated in June 2009, is a development stage

company and has no operating history. We cannot assure you that we will be able

to operate our business successfully or implement our policies and strategies as

described in this annual report.

11

If

we are unable to purchase certain assets material to the implementation of our

business in a timely manner or at all, such inability would materially adversely

affect our business and results of operations.

The

implementation of our business plan relies on our ability to purchase land,

livestock and other material assets. We do not currently have sufficient funds

available to implement our business plan as originally anticipated. We cannot

assure you that we will be able to locate financing or funding on suitable terms

or at all. If such financing or funding is not available, we may not be able to

implement our business plan to any extent.

The

land we currently own is subject to a mortgage.

We own

approximately 3,300 acres of farmland in the State of Georgia. Such land is the

subject of a mortgage granted to Cullen Holdings securing our obligations owed

to it pursuant to a promissory note that is due on January 20, 2011. If we fail

to repay this promissory note when due, Cullen Holdings may foreclose on the

land and take possession of it. We cannot assure you that we will have

sufficient capital to repay the note or our other obligations when they come

due. If we are unable to pay our obligations as they come due, it could have a

material adverse effect on our operations.

The

recent disruptions in the overall economy and the financial markets may

adversely impact our business and results of operations.

The

agricultural industry is sensitive to changes in general economic conditions,

both nationally and locally. Recent disruptions in global financial markets and

banking systems have made it more difficult for companies to access credit and

capital markets. The economic crisis may adversely affect our business in a

variety of ways. Access to lines of credit or the capital markets may be

severely restricted, which may preclude us from raising funds required for

operations and to fund continued expansion. It may be more difficult for us to

complete strategic transactions with third parties. Continuing volatility in the

credit and capital markets could potentially impair our customers’ ability to

access these markets and increase associated costs, and we may be materially

affected by these financial market disruptions as economic events and

circumstances continue to evolve. The financial and credit market turmoil could

also negatively impact our potential suppliers and customers, which could

decrease our ability to source, produce and distribute our products and could

decrease demand for its products.

If

economic conditions continue to worsen, it is possible these factors could

significantly impact our financial condition and ability to implement our

strategic growth plan.

Any

negative public perception regarding our products or industry, or any ill

effects of product liability claims, could harm our reputation, damage its

brand, result in costly and damaging recalls and expose us to government

investigations and sanctions, which would materially and adversely affect its

results of operations.

We will

sell products for human consumption, which involves a number of risks. Product

contamination, spoilage or other adulteration could result in the inability to

sell our products. We also may be subject to liability if our products or

operations violate applicable laws or regulations or in the event its products

cause injury, illness or death. A significant product liability or other legal

judgment against us or a widespread product recall may negatively impact our

profitability. Even if a product liability or consumer fraud claim is

unsuccessful or is not merited, the negative publicity surrounding such

assertions regarding our products or processes could materially and adversely

affect our reputation, brand image and results of operations. Finally, serious

product quality concerns could result in governmental action against us, which,

among other things, could result in the suspension of production or distribution

of our products, or other governmental penalties, including possible criminal

liability.

12

We

may not realize anticipated benefits from our strategic growth

plan.

We will

implement a strategic growth plan, which includes a number of initiatives, that

we believe are necessary in order to position our business for future success

and growth. Over the next several years, these initiatives will require

investments in people, systems, tools and facilities. Our success and earnings

growth depends in part on our ability to maintain budgeted costs and

efficiencies. If we are unable to successfully implement these initiatives, or

fail to implement them as timely as anticipated, our results of operations could

be adversely impacted.

Our

business is subject to various environmental laws, which may increase our

compliance costs.

Our

business operations are subject to various environmental and governmental

regulations. These laws and regulations cover the discharge of pollutants,

wastewater, and hazardous materials into the environment. In addition, various

laws and regulations addressing climate change are being considered or

implemented at the federal and state levels. New legislation, as well as current

federal and other state regulatory initiatives, relating to these environmental

matters could require us to replace equipment, install additional pollution

controls, purchase various emission allowances or curtail operations. These

costs could adversely affect our results of operations and financial

condition.

Our

operations are subject to numerous laws and regulations, exposing us to

potential claims and compliance costs that could adversely affect its

business.

We are

subject to Federal, state and local laws and regulations relating to the

manufacturing, labeling, packaging, health and safety, sanitation, quality

control, fair trade practices, and other aspects of its business. In addition,

zoning, construction and operating permits are required from governmental

agencies which focus on issues such as land use, environmental protection, waste

management, and the movement of animals across state lines. These laws and

regulations may, in certain instances, affect its ability to develop and market

new products and to utilize technological innovations in our business. In

addition, changes in these rules might increase the cost of operating our

facilities or conducting our business which would adversely affect our

finances.

Our dairy

business will be affected by Federal price support programs and federal and

state pooling and pricing programs to support the prices of certain products we

sell. Federal and certain state regulations help ensure that the supply of raw

milk flows in priority to fluid milk and soft cream producers before producers

of hard products such as cheese and butter. If any of these programs was no

longer available to us, the prices it pays for milk could increase and reduce

its profitability.

Several

states also have laws that restrict the ability of corporations to engage in

farming activities. These regulations may require us to alter or restrict its

operations or cause it to incur additional costs in order to comply with the

regulations.

13

Inability

to protect our trademarks and other proprietary rights could damage our

competitive position.

Any

infringement or misappropriation of our intellectual property could damage its

value and could limit our ability to compete. We may have to engage in

litigation to protect our rights to intellectual property, which could result in

significant litigation costs and require a significant amount of management’s

time.

We

believe that the know-how associated with our farming systems for the production

of raw milk are trade secrets. In addition, we have amassed a large body of

knowledge regarding animal nutrition and pasture-based farming which we believe

to be proprietary. Because most of this proprietary information is not patented,

it may be more difficult to protect. We rely on security procedures and

confidentiality agreements to protect this proprietary information; however,

such agreements and security procedures may be insufficient to keep others from

acquiring this information. Any such dissemination or misappropriation of this

information could deprive us of the value of its proprietary information and

negatively affect its results.

Our

proprietary farming system could be replicated creating additional competition

in the grass-fed dairy industry.

Despite

our first mover advantage and the substantial amount of research and development

that we believe would be required to replicate our farming system, over time and

with significant capital, it is possible that other producers could replicate

our model with a certain degree of success. This could put our market share and

competitive advantages at risk.

The

efficiencies of our farming system may not be scalable.

Our

farming system has only been tested on a farm which is smaller than those farms

we are expecting to roll-out in the future. If its system is not as efficient on

a larger scale, this could impair our ability to implement our strategic plan

and negatively affect our operating results.

Key

assets such as land, livestock and infrastructure could increase in price,

reducing the ability to roll-out farms under the current budgeted capital

requirements.

An

increase in the cost of our key capital items such as land, livestock and

infrastructure could reduce our ability to roll-out farms. Key assets may

increase substantially in price and additional capital may not be available to

us on acceptable terms when needed.

The

price of land could decrease, reducing the underlying asset value of the

business.

Our

current business plan involves buying land assets. If these assets were to be

acquired and then the value of these assets decreased, this could reduce the

strength of our balance sheet in the future and affect its ability to obtain

additional capital and implement its business plan.

We

may establish and maintain relationships with only a small number of

co-operatives for the collection and processing of our raw milk.

The dairy

processing industry is made up of a number of co-operatives that collect and

process all raw milk produced at farms. Our business plan anticipates that it

will establish and maintain relationships with co-operatives for the collection

and processing of its raw milk. It is anticipated that it will not initially, if

at all, establish contracts with a large number of different co-operatives,

which could expose us to a customer concentration risk.

14

Milk

and corn price volatility could reduce revenues and negatively affect our

results of operations.

If the

price of milk decreased to that which is substantially lower than expected, this

could result in a material reduction in our revenues and negatively affect our

results of operations.

Our

feeding strategy will utilize a certain proportion of other feedstocks, some of

which are corn-based, the price of which fluctuates according to the price of

corn. If corn prices were to rise significantly, we could experience a material

reduction in our operating margins.

Raw

milk production is influenced by a number of factors that are beyond our

control, such factors may have a material adverse effect on our

business.

Raw milk

production is influenced by a number of factors that are beyond our control,

including, not limited to, the following:

|

•

|

Seasonal Factors: dairy

cows generally produce more milk in temperate weather than in cold or hot

weather and extended unseasonably cold or hot weather could lead to lower

than expected production;

|

|

|

•

|

Environmental Factors:

the volume and quality of milk produced by dairy cows is closely linked to

the quality of the nourishment provided by the environment around them,

and, therefore, if environmental factors cause the quality of nourishment

to decline, our milk production could decline; and

|

|

|

•

|

Governmental Agricultural and

Environmental Policy: declines in government grants, subsidies,

provision of land, technical assistance and other changes in agricultural

and environmental policies may have a negative effect on the viability of

our farms, and the numbers of dairy cows and quantities of milk they are

able to produce.

|

Such

factors could have a material adverse effect on our business.

The

milk production business is highly competitive and, therefore, we face

substantial competition in connection with the sale of our

products.

We face

competition from other milk producers across the U.S. Most of our competitors

are well established, have greater financial, marketing, personnel and other

resources, have been in business for longer periods of time than we have, and

have products that have gained wide customer acceptance in the marketplace. We

may be unable to compete successfully or our competitors may develop products

which have superior qualities or gain wider market acceptance than

ours.

15

Large-scale

disease could harm a significant portion of our livestock, reducing its ability

to produce revenue.

The

productivity and profitability of Natural Dairy’s businesses depend on animal

and crop health and on disease control. Natural Dairy will face the risk of

outbreaks of bovine spongiform encephalopathy (“BSE”) which could lead to

decreased milk and livestock sales and increased costs to produce its products.

There have been three confirmed cases as having BSE in the United States in

Washington, Alabama and Texas. Various countries have halted the import of U.S.

fed beef in response to the discovery of BSE in the U.S. marketplace. In

response to the discovery of BSE in the U.S. marketplace, the USDA has increased

testing requirements for cows and is exploring additional inspection

requirements which could increase the cost of production of dairy products. The

discovery of additional cases of BSE could lead to widespread destruction of

dairy cows, could cause consumer demand for dairy products to decrease and could

result in increased inspection costs and procedures as well as reduce revenues

from the sale of livestock. If this occurs, Natural Dairy could have decreased

production and sales of its dairy products due to decreased consumer demand or

decreased milk supply and decreased operating margins as a result of increased

dairy production costs.

Natural

Dairy will face the risk of outbreaks of foot-and-mouth disease, which could

lead to a significant destruction of cloven-hoofed animals such as dairy cattle,

beef cattle, swine, sheep and goats and significantly reduce the demand for meat

products. Because foot-and-mouth disease is highly contagious and destructive to

susceptible livestock, any outbreak of foot-and-mouth disease could result in

the widespread destruction of all potentially infected livestock. If this

happens, Natural Dairy could also have difficulty procuring the livestock it

needs for its dairy operations and incur increased cost to produce its dairy

products, which could reduce its production, sales and operating

margins.

Our

ability to produce revenue will be dependent on the continual survival and

health of Natural Dairy’s livestock. If a significant number of Natural Dairy’s

livestock died or were infected with a disease, Natural Dairy’s ability to

produce revenue form the sale of milk would be reduced.

Our

results of operations will fluctuate by season and will be affected by weather

conditions.

Any

adverse or major deviations from the typical weather conditions expected in a

region could negatively impact our ability to produce revenue under our current

strategy. In addition, severe weather conditions and natural disasters, such as

floods, droughts, frosts or earthquakes, or adverse growing conditions, diseases

and insect-infestation problems may reduce the quantity and quality of its milk

production. For example, dairy cows produce less milk when subjected to extreme

weather conditions, including hot and cold temperatures. A significant reduction

in the quantity or quality of milk produced due to adverse weather conditions,

disease, insect problems or other factors could result in increased processing

costs and decreased production, with adverse financial consequences to

us.

A

change in the water availability may negatively impact the efficiency of the

business model.

The

success of our farming system is dependent on the availability of water to

successfully grow forage. If there was a reduction in water availability on a

farm subsequent to acquiring and converting that property, due to drought,

contamination or otherwise, our ability to produce milk on that farm could be

negatively affected.

We

depend upon our key personnel and our ability to retain and recruit additional

qualified personnel to implement our business strategy. The loss of such key

personnel or the inability to retain or recruit qualified personnel in the

future could have a material adverse impact on the implementation of the

business strategy.

Our

success depends largely on our ability to attract, develop, motivate and retain

highly skilled professionals. The loss or unavailability of any of our key

personnel or the inability to train and retain additional qualified personnel

and advisory board members for any significant period of time or at all would

have a material adverse effect on the business, prospects, financial condition

and results of operations.

16

We

may be unable to develop and implement a marketing strategy for our advisory and

consulting services, which may have a material adverse effect on our

business.

We do not

have any long-term agreements with clients for the provision of advisory and

consulting services we intend to offer. Although we have not included consulting

revenues in our forecasts, the success of our business will depend in part on

our ability to secure advisory clients. If we are unable to secure advisory

clients due to ineffective marketing, because of an economic downturn decreasing

the demand for outsourced professional services or otherwise, our business is

likely to be materially adversely affected.

Inability

to obtain required import permits could reduce our ability to achieve certain

long term operating efficiencies.

Our

business plan includes the potential future requirement for importation of

certain farm products, technologies or animal products into the US as well as

movement of these products or technologies between States within the US. The

importation of Agritech products from New Zealand into the US is subject to

various regulatory and licensing restrictions including but not limited to those

imposed by the U.S. Customs Service; the United States International Trade

Commission; the United States Department of Agriculture; the Food and Drug

Administration; the Animal & Plant Health Inspection Service; the Farm

Service Agency; the Environmental Protection Agency and the Occupational Health

& Safety Administration. We might also be exposed to certain quota

limitations. Specifically, for animal products including semen and embryos, the

U.S. Federal Law requires that the USDA Animal and Plant Health Inspection

Service (APHIS) issue a permit. The current regulatory environment in the U.S.

in regards to importation of Agritech products from New Zealand could change

sometime in the future. As such, it is possible that we might be unable to

obtain such permits or our activities will be limited by an inability to comply

with the required regulatory and licensing restrictions. This could limit the

ability for us to achieve our financial forecasts.

A

forage-based strategy could result in reduced production in the winter

months.

Due to

the reliance on forage as a primary feed source, the colder winter months could

reduce forage growth and therefore reduce feed availability for the farm’s

livestock. This could result in either the requirement to increase the use of

supplemental feed or reduced milk production. This could negatively impact our

ability to produce milk or maintain expected operating margins.

Our

warrants may be exercised in the future, which would increase the number of

shares eligible for future resale in the public market.

We have

outstanding warrants to purchase an aggregate of 74,000,000 shares of common

stock. To the extent such warrants are exercised, additional shares of our

common stock will be issued, which would dilute the ownership of existing

stockholders.

Eric

J. Watson effectively controls us.

Eric

Watson beneficially owns 15,881,148 shares of our common stock and effectively

controls us through such ownership. Because of this ownership, he will be able

to have considerable influence over our corporate actions in the

future.

17

Our

stock price could fluctuate and could cause you to lose a significant part of

your investment.

The

market price of our securities may be influenced by many factors, some of which

are beyond our control, including those described above and the

following:

|

•

|

changes

in financial estimates by analysts;

|

|

|

•

|

fluctuations

in its quarterly financial results or the quarterly financial results of

companies perceived to be similar to it;

|

|

|

•

|

general

economic conditions;

|

|

|

•

|

changes

in market valuations of similar companies;

|

|

|

•

|

terrorist

acts;

|

|

|

•

|

changes

in its capital structure, such as future issuances of securities or the

incurrence of additional debt;

|

|

|

•

|

future

sales of common stock;

|

|

|

•

|

regulatory

developments in the United States, foreign countries or

both;

|

|

|

•

|

litigation

involving us, our subsidiaries or our general industry;

and

|

|

|

•

|

additions

or departures of key personnel.

|

|

ITEM

1B.

|

UNRESOLVED

STAFF COMMENTS.

|

None.

|

ITEM

2.

|

PROPERTIES.

|

Additionally,

we own approximately 3,300 acres of farmland in the State of

Georgia.

|

ITEM

3.

|

LEGAL

PROCEEDINGS.

|

See Note

7 to our consolidated financial statements included in Part II, Item 8 of this

annual report.

18

PART

II

|

MARKET

FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER

PURCHASES OF EQUITY SECURITIES.

|

Market

Information

Our

common stock and warrants are listed on the OTC Bulletin Board under the

symbols, CAGZ and CAGZW, respectively. The following table sets forth the range

of high and low sales prices for the common stock and warrants for the periods

indicated since the common stock and warrants commenced public trading on

October 23, 2009.

|

Common Stock

|

Warrants

|

|||||||||||||||

|

High

|

Low

|

High

|

Low

|

|||||||||||||

|

Fiscal

2010:

|

||||||||||||||||

|

First

Quarter*

|

$ | 3.95 | $ | 1.75 | $ | 0.05 | $ | 0.02 | ||||||||

|

Fiscal

2009:

|

||||||||||||||||

|

Fourth

Quarter

|

$ | 6.20 | $ | 3.60 | $ | 0.12 | $ | 0.03 | ||||||||

* Through

March 24, 2010.

Holders

As of

March 24, 2010, there were 17 holders of record of our common stock and 14

holders of record of our warrants.

Dividends

Recent

Sales of Unregistered Securities and Use of Proceeds

We did

not effect the sale of any unregistered securities during the fourth quarter of

2009.

|

ITEM

6.

|

SELECTED

FINANCIAL DATA.

|

The

selected financial data set forth below is derived from our audited financial

statements. This selected financial data should be read in conjunction with the

section under the caption “Management’s Discussion and Analysis of Financial

Condition and Results of Operations” and the Consolidated Financial Statements

included elsewhere in this Annual Report on Form 10-K:

19

|

For

the period from

|

||||

|

June

3, 2009

|

||||

|

(inception)

through

|

||||

|

December

31, 2009

|

||||

|

Total

revenues

|

$ | — | ||

|

Loss

from operations

|

(524,924 | ) | ||

|

Net

loss

|

(612,526 | ) | ||

|

Earnings

per share basic and diluted

|

(0.03 | ) | ||

|

Weighted

average shares outstanding

|

19,247,311 | |||

|

Working

capital

|

2,199,282 | |||

|

Total

assets

|

11,855,329 | |||

|

Stockholders’

equity

|

$ |

5,451,319

|

||

20

|

ITEM

7.

|

MANAGEMENT’S

DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF

OPERATIONS.

|

The

following discussion should be read in conjunction with our Consolidated

Financial Statements and footnotes thereto contained in this

report.

Forward

Looking Statements

All

statements other than statements of historical fact included in this Form 10-K

including, without limitation, statements under “Management’s Discussion and

Analysis or Plan of Operation” regarding our financial position, business

strategy and the plans and objectives of management for future operations, are

forward looking statements. When used in this Form 10-K, words such as

“anticipate,” “believe,” “estimate,” “expect,” “intend” and similar expressions,

as they relate to us or our management, identify forward looking statements.

Such forward looking statements are based on the beliefs of management, as well

as assumptions made by, and information currently available to, our management.

Actual results could differ materially from those contemplated by the forward

looking statements as a result of certain factors detailed in our filings with

the Securities and Exchange Commission. All subsequent written or oral forward

looking statements attributable to us or persons acting on our behalf are

qualified in their entirety by this paragraph.

In

assessing forward-looking statements contained herein, readers are urged to

carefully read those statements. Among the factors that could cause actual

results to differ materially are: inability to protect our intellectual

property; inability to obtain necessary financing; competition; loss of key

personnel; increases of costs of operations; continued compliance with

government regulations; and general economic conditions.

A

description of key factors that have a direct bearing on our results of

operations is provided under “Risk Factors” included on Item 1A of this form

10-K.

Overview

Business

Combination

On

October 22, 2009, pursuant to the “Merger Agreement”, the Company consummated

the Merger. Prior to the Merger, the Company was a wholly owned subsidiary of