Attached files

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| x | Annual report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the fiscal year ended January 30, 2010

Commission file number 1-32349

SIGNET JEWELERS LIMITED

(Exact name of Registrant as specified in its charter)

| Bermuda | Not Applicable | |

| (State or other jurisdiction of incorporation) | (I.R.S. Employer Identification Number) |

Clarendon House

2 Church Street

Hamilton HM11

Bermuda

(441) 296 5872

(Address and telephone number including area code of principal executive offices)

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class |

Name of Each Exchange on which Registered | |

| Common Shares of $0.18 each | The New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ¨ No x

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained to the best of Registrant’s knowledge in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company.

Large accelerated filer x Accelerated filer ¨ Non-accelerated filer ¨ Smaller reporting company ¨

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

The aggregate market value of voting Common Shares held by non-affiliates of the Registrant (based upon the closing sales price quoted on the New York Stock Exchange) as of July 31, 2009 was $1,884,972,890.

Number of Common Shares outstanding on March 21, 2010: 85,511,574

DOCUMENTS INCORPORATED BY REFERENCE

The Registrant will incorporate by reference information required in response to Part III, Items 10-14, in its definitive proxy statement for its annual meeting of shareholders, to be filed with the Securities and Exchange Commission within 120 days of January 30, 2010.

Table of Contents

CHANGE OF REPORTING STATUS

Effective January 31, 2010, Signet ceased to be a foreign private issuer and became a foreign issuer subject to the rules and regulations under the U.S. Securities Exchange Act of 1934 (“Exchange Act”) applicable to domestic US issuers. Signet is filing this Annual Report on Form 10-K, whereas previously it filed on Form 20-F.

REFERENCES

Unless the context otherwise requires, references to “Signet,” refer to Signet Jewelers Limited (and before September 11, 2008, to Signet Group plc) and its consolidated subsidiaries. References to the “Company” are to Signet Jewelers Limited. References to “Predecessor Company” are to Signet Group plc prior to the reorganization that was effected on September 11, 2008, and financial and other results and statistics for fiscal 2008 and prior periods relate to Signet prior to such reorganization.

PRESENTATION OF FINANCIAL INFORMATION

All references to “dollars,” “US dollars,” “$,” “cents” and “c” are to the lawful currency of the United States of America. Signet prepares its financial statements in US dollars. All references to “pounds,” “pounds sterling,” “sterling,” “£,” “pence,” and “p” are to the lawful currency of the United Kingdom.

Percentages in tables have been rounded and accordingly may not add up to 100%. Certain financial data may have been rounded. As a result of such rounding, the totals of data presented in this document may vary slightly from the actual arithmetical totals of such data.

Throughout this Annual Report on Form 10-K, financial data has been prepared in accordance with accounting principles generally accepted in the United States (“GAAP”). However Signet gives certain additional non-GAAP measures in order to provide increased insight into the underlying or relative performance of the business. An explanation of each non-GAAP measure used can be found in Item 6.

Fiscal Year

Signet’s fiscal year ends on the Saturday nearest to January 31. As used herein, “fiscal 2012,” “fiscal 2011,” “fiscal 2010,” “fiscal 2009” and “fiscal 2008” refer to the 52 week periods ending January 28, 2012, January 29, 2011, January 30, 2010, January 31, 2009 and February 2, 2008 respectively. As used herein, “fiscal 2007” refers to the 53 week period ending February 3, 2007, “fiscal 2006” and “fiscal 2005” refer to the 52 week periods ended January 28, 2006 and January 29, 2005 respectively.

This Annual Report on Form 10-K contains statements which are forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These statements, based upon management’s beliefs and expectations as well as on assumptions made by and information currently available to management, include statements regarding, among other things, the results of operation, financial condition, liquidity, prospects, growth, strategies and the industry in which Signet operates. The use of the words “expects,” “intends,” “anticipates,” “estimates,” “predicts,” “believes,” “should,” “potential,” “may,” “forecast,” “objective,” “plan” or “target,” and other similar expressions are intended to identify forward-looking statements. These forward-looking statements are not guarantees of future performance and are subject to a number of risks and uncertainties, including but not limited to general economic conditions, the merchandising, pricing and inventory policies followed by Signet, the reputation of Signet, the level of competition in the jewelry sector, the price and availability of diamonds, gold and other precious metals, seasonality of the business and financial market risk.

Important factors which may cause actual results to differ materially from those expressed in any forward looking statement include, but are not limited to, those described in Item 1A and elsewhere in this Form 10-K. Except as required by applicable law, rules or regulations, Signet undertakes no obligation to update publicly any forward-looking statements in this Annual Report on Form 10-K that may occur due to any change in management’s expectations or to reflect future events or circumstances.

1

Table of Contents

FISCAL 2010 ANNUAL REPORT ON FORM 10-K

TABLE OF CONTENTS

| PAGE | ||||

| 1 | ||||

| PART I | ||||

| ITEM 1. |

3 | |||

| ITEM 1A. |

31 | |||

| ITEM 1B. |

38 | |||

| ITEM 2. |

38 | |||

| ITEM 3. |

40 | |||

| ITEM 4. |

40 | |||

| PART II | ||||

| ITEM 5. |

41 | |||

| ITEM 6. |

47 | |||

| ITEM 7. |

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

55 | ||

| ITEM 7A. |

87 | |||

| ITEM 8. |

90 | |||

| ITEM 9. |

CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE |

131 | ||

| ITEM 9A. |

131 | |||

| ITEM 9B. |

132 | |||

| PART III | ||||

| ITEM 10. |

133 | |||

| ITEM 11. |

133 | |||

| ITEM 12. |

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS |

133 | ||

| ITEM 13. |

CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS, AND DIRECTOR INDEPENDENCE |

133 | ||

| ITEM 14. |

133 | |||

| PART IV | ||||

| ITEM 15. |

134 | |||

2

Table of Contents

PART I

| ITEM 1. | BUSINESS |

OVERVIEW

Signet is the world’s largest specialty retail jeweler by sales, with stores in the US, UK, Republic of Ireland and Channel Islands. Signet is incorporated in Bermuda and its address and telephone number are shown on the cover of this document. Its corporate website is www.signetjewelers.com, from where documents that the Company is obliged to file or furnish with the US Securities and Exchange Commission (“SEC”) may be viewed or downloaded free of charge.

Signet’s US division operated 1,361 stores in 50 states at January 30, 2010. Its stores trade nationally in malls and off-mall locations as Kay Jewelers (“Kay”), and regionally under a number of well-established mall-based brands. Destination superstores trade nationwide as Jared The Galleria Of Jewelry (“Jared”). The US market accounts for about 40% of worldwide diamond sales (source: IDEX Online). Based on publicly available data, management believes Signet’s US division was the largest specialty jeweler in the US in calendar 2009 with sales approximately 1.8 times those of the next biggest such retailer. See page 8 for a description of Signet’s US division.

The UK division’s stores trade as “H.Samuel,” “Ernest Jones,” and “Leslie Davis,” and are situated in prime ‘High Street’ locations (main shopping thoroughfares with high pedestrian traffic) or major shopping malls. The UK market accounts for less than 2% of worldwide diamond sales (source: IDEX Online/Office for National Statistics). The UK division operated 552 stores at January 30, 2010, including 14 stores in the Republic of Ireland and three in the Channel Islands. Based on publicly filed accounts, management believes Signet’s UK division was the largest specialty retailer of fine jewelry in the UK with sales in calendar 2008 approximately 1.7 times those of the next biggest such retailer. See page 22 for a description of Signet’s UK division.

Competition and sector consolidation

In the US, for calendar 2009 Signet had an approximate 4.4% share of the $58.8 billion total jewelry market (source: U.S. Bureau of Economic Analysis (“BEA”)). The specialty retail jewelry market was provisionally estimated to be $27.2 billion (source: US Census Bureau). During calendar 2008 and calendar 2009, the US specialty jewelry sector underwent an accelerated rate of consolidation, as weak competitors exited the market. Three of the top ten middle market brands by sales at January 1, 2008 liquidated, and a fourth has been in Chapter 11 for over a year. Management estimates that the number of US specialty jewelry outlets has declined by between 10% and 15% since January 1, 2008, and believes that financial and liquidity issues are reducing the ability of many other specialty jewelers to compete effectively.

As a result of management’s strategy to focus on enhancing its competitive strengths, the US division was able to take advantage of these trends and increased its market share by 40 basis points from 9.0% of the US specialty jewelry sector in calendar 2008 to 9.4% in calendar 2009 (source: US Census Bureau). These sector trends are anticipated to continue in calendar 2010 and provide further opportunity for the US division to gain profitable market share. In addition, management believes the US division will be better prepared than many in its sector to take advantage of an upturn in consumer expenditure, whenever it occurs, due to its focus on customer needs, its operating philosophy of continuous improvement and its strong balance sheet.

In the UK, for calendar 2008, the most recent year for which data is available, Signet had an approximate 11% share of the £4.9 billion total jewelry market (source: Office for National Statistics). Data for 2009 is due for publication on March 30, 2010. While similar specialty retail jewelry data is not available for the UK market as for the US market, management believes that the economic environment has also resulted in an acceleration of the rate at which other jewelry stores are leaving the market and a weakening of many competitors.

3

Table of Contents

Operating principles

Management aims to build long term value by focusing on the customer and providing a superior merchandise selection in high quality real estate locations. Effective advertising draws consumers into our stores, where the objective is to provide outstanding service. The operating principles that help management achieve these aims are:

| • | excellence in execution; |

| • | test before investing; |

| • | continuous improvement; and |

| • | disciplined investment. |

Operational execution

Management recognizes that while the level of expenditure on jewelry is discretionary and consumers may trade down in a more challenging economic environment, the expression of romance and appreciation, for example through bridal jewelry and gift giving, remain very important human needs, as is self reward. Therefore, helping to satisfy those needs is central to driving sales. As a result, the training of staff to better understand the shopper’s requirements, communicate the value of the merchandise selected and ‘close the sale,’ remains a high priority. Management also aims to increase the attraction of Signet’s store brands to consumers through the use of differentiated merchandise (see page 15), while also offering a compelling value proposition in more basic ranges, including increased use of “value items” (see page 16), by utilizing its supply chain and merchandising expertise, scale and balance sheet strength. In addition, management intends to leverage national television advertising and customer relationship marketing, which it believes are the most effective and cost efficient forms of marketing available, to at least maintain its leading share of relevant marketing messages (“share of voice”).

STRATEGY AND OBJECTIVES

In the more buoyant economic conditions experienced between fiscal 2002 and mid fiscal 2009, management’s strategy had been to:

| • | maintain a strong balance sheet; |

| • | continue the achievement of sector leading performance standards on both sides of the Atlantic; |

| • | maximize store productivity in the US and the UK; and |

| • | grow new store space in the US. |

Fiscal 2010 strategy

Reflecting the dramatic change in economic and financial market conditions in the second half of fiscal 2009, same store sales declined by 14.9% in the fourth quarter of fiscal 2009 and underlying operating margin was materially reduced. As a result management reviewed and amended Signet’s strategy to:

| • | enhance Signet’s position as the strongest middle market specialty retail jeweler; |

| • | focus on profit and cash flow maximization to maintain a strong balance sheet; and |

| • | reduce business risk. |

In the changed economic environment, management judged that it was preferable, and a much lower risk strategy, to aim to maximize sales by gaining profitable market share in existing stores by focusing on enhancing competitive strengths rather than opening additional locations.

4

Table of Contents

Fiscal 2010 financial objectives

For fiscal 2010, this strategy resulted in the following financial objectives being set:

| • | $100 million US cost saving program; |

| • | significantly reduce working capital; |

| • | lower capital expenditure by about 50%, to approximately $55 million; and |

| • | achieve a positive free cash flow of between $175 million and $225 million. |

The US division slightly exceeded the cost savings target of $100 million (excluding inflation, net bad debt and volume related costs on sales above plan). Signet achieved a $221.5 million reduction in working capital primarily through reducing inventory by $226.5 million. Capital expenditure was $43.6 million, $11 million below the target level. The positive free cash flow; non-GAAP measure, see Item 6, in fiscal 2010 was $471.9 million, more than twice the objective, reflecting the reduction in working capital and a better than expected trading performance.

Fiscal 2011 strategy

While the results for fiscal 2010 exceeded the financial objectives for that year, and the US and UK economies showed some initial signs of stabilization in late fiscal 2010, activity remains below former levels and the outlook continues to be uncertain, particularly in the UK. The strategy in fiscal 2011 is therefore broadly similar to that of fiscal 2010. However, it is not anticipated that a further realignment of costs and working capital will be implemented given the stable sales performance in fiscal 2010.

Consistent with Signet’s strategy, management remains focused on improving store productivity, primarily by gaining profitable market share. Both the US and UK divisions entered the downturn as industry leaders and continue to endeavor to better meet customer requirements by further enhancing their competitive advantages.

This is expected to increase the performance gap between Signet and others in the sector in the basic retail disciplines of store operations, supply chain management and merchandising, marketing and quality of real estate. Over the last decade, the US division’s share of the US specialty jewelry market has increased from 5.2% to 9.4%; the aim is to achieve a further profitable increase in 2010. Significant store capacity exited the US specialty jewelry marketplace in calendar 2009 and management believes that many of the remaining firms are less able to compete due to financial pressures.

As always, profit and cash flow maximization remain a priority. Therefore management will continue to keep a tight control of gross merchandise margin, costs and inventory.

The strategy also encompasses maintaining a strong balance sheet and financial flexibility. These are significant advantages within the specialty jewelry sector when negotiating with landlords and suppliers. The business is able to invest in new merchandise ranges to drive sales and in information technology to improve productivity. In addition, a strong balance sheet enables the US division to provide credit to customers that meet consistent authorization standards at a time when other sources of consumer finance are contracting and many specialty jewelry competitors are finding third party provision of credit to be increasingly expensive.

5

Table of Contents

Fiscal 2011 financial objectives

In fiscal 2011, management’s financial objectives for the business are the following:

| • | Controllable costs to be little changed from fiscal 2010 at constant exchange rates, that is costs excluding net bad debt charge, expenses that vary with sales, the US vacation entitlement policy change (see page 66) and the impact from the amendments to the Truth in Lending Act (see page 21) |

| • | Capital expenditure of about $80 million |

| • | Positive free cash flow of between $150 million and $200 million |

MEDIUM TERM OUTLOOK

Management believes that Signet’s two operating divisions have the opportunity to take advantage of their enhanced competitive positions to gain profitable market share and, as any improvements to the economy take place, grow sales and increase store productivity. In addition, as the economy stabilizes there is the potential for the ratio of the net bad debt charge on customer receivables to sales within the US division to return to nearer historic, lower levels. The increasing consolidation of the jewelry supply chain may allow the business to strengthen relationships with suppliers, facilitating the possibility of developing differentiated merchandise, and potentially improving the efficiency of its supply chain. Management also believe that Signet’s strong balance sheet and superior operating metrics should allow its operating divisions to take advantage of investment opportunities that meet management’s return criteria, particularly space growth in the US, more quickly than competitors. Furthermore, Signet is in a position to take advantage of strategic opportunities that meet management’s demanding investment returns, should they arise.

BACKGROUND

Business segment

Signet’s results derive from one business segment – the retailing of jewelry, watches and associated services. The business is managed as two geographical operating divisions: the US division (approximately 78% of sales) and the UK division (approximately 22% of sales). Both divisions are managed by executive committees, which report through divisional Chief Executives to Signet’s Chief Executive to the Board of Directors of Signet (the “Board”). Each divisional executive committee is responsible for operating decisions within parameters established by the Board.

Detailed financial information about both divisions is found in Note 2 of Item 8.

History and development

Signet Group plc was incorporated in England and Wales on January 27, 1950 under the name Ratners (Jewellers) Limited. The name of the company was changed on December 10, 1981 to Ratners (Jewellers) Public Limited Company, on February 9, 1987 to Ratners Group plc, and on September 10, 1993 to Signet Group plc. On September 11, 2008, Signet Group plc became a wholly-owned subsidiary of Signet Jewelers Limited, a new company incorporated in Bermuda under the Companies Act 1981 of Bermuda, following the completion of a scheme of arrangement approved by the High Court of Justice in England and Wales under the UK Companies Act 2006. Shareholders of Signet Group plc became shareholders of Signet Jewelers Limited, owning 100% of that company. Signet Jewelers Limited is governed by the laws of Bermuda.

Signet expanded rapidly by acquisition during the period 1984 to 1990. It first entered the US market in 1987 by acquiring Sterling Inc., a company based in Akron, Ohio. Kay Jewelers, Inc. was acquired in 1990. Since 1990 the only corporate acquisition made by Signet was that of Marks & Morgan Jewelers Inc. in 2000.

6

Table of Contents

Signet listed on the London Stock Exchange (“LSE”) in 1968. In 1988, American Depositary Shares (“ADSs”) of Signet began trading on NASDAQ and in November 2004 the listing for the ADSs was moved to the New York Stock Exchange (“NYSE”). On September 11, 2008, as part of the scheme of arrangement discussed above, each Signet Group plc share was consolidated on a 1-for-20 basis, and each ADS on a 1-for-2 basis. On the same date Signet Jewelers Limited’s shares were listed on the NYSE and a secondary listing was obtained on the Official List of the United Kingdom Listing Authority (from April 2010, following implementation of the FSA’s review of the UK listing regime, all secondary listings, including the Company’s, will be relabeled as standard listings).

Trademarks and trade names

Signet is not dependent on any material patents or licenses in either the US or the UK. However, it does have several well-established trademarks and trade names which are significant in maintaining its reputation and competitive position in the jewelry retailing industry. These registered trademarks and trade names include the following in Signet’s US operations: Kay Jewelers; Jared The Galleria Of Jewelry; JB Robinson Jewelers; Marks & Morgan Jewelers; Belden Jewelers; Weisfield Jewelers; Osterman Jewelers; Shaw’s Jewelers; Rogers Jewelers; LeRoy’s Jewelers; Goodman Jewelers; Friedlander’s Jewelers; Every kiss begins with Kay; Peerless Diamond; Hearts Desire; Perfect Partner; Open Hearts by Jane Seymour; and Love’s Embrace. Trademarks and trade names include the following in Signet’s UK operations: H.Samuel; Ernest Jones; Leslie Davis; Forever Diamond; and Perfect Partner.

The value of Signet’s trademarks and trade names are material but are not reflected on its balance sheet. Their value is maintained and increased by Signet’s expenditure on staff training, marketing and store investment.

Seasonality

Signet’s sales are seasonal, with the first and second quarters each normally accounting for slightly more than 20% of annual sales, the third quarter a little under 20% and the fourth quarter for about 40% of sales, with December being by far the most important month of the year. Due to sales leverage, Signet’s operating income is even more seasonal, with nearly all of the UK division’s, and a little over 50% of the US division’s operating income normally occurring in the fourth quarter. Selling, general and administrative costs occur broadly evenly during the year, while net financing expenses are usually higher in the second half of the year reflecting the normal peak in working capital requirements just ahead of the key holiday trading period.

Employees

In fiscal 2010 the average number of full-time equivalent persons employed was 16,320 (US: 12,596; UK: 3,724). Signet usually employs a limited number of temporary employees during its fourth quarter. None of Signet’s employees in the UK and less than 1% of Signet’s employees in the US are covered by collective bargaining agreements. Signet considers its relationship with its employees to be excellent.

Further information on Signet’s employees can be found elsewhere in this Report.

| Year ended | ||||||

| Fiscal 2010 | Fiscal 2009 | Fiscal 2008 | ||||

| Average number of employees |

||||||

| US |

12,596 | 13,218 | 13,396 | |||

| UK |

3,724 | 3,697 | 3,847 | |||

| Total |

16,320 | 16,915 | 17,243 | |||

7

Table of Contents

US DIVISION

US market

Total US jewelry sales, including watches and fashion jewelry, are provisionally estimated by the BEA to have been $58.8 billion in calendar 2009. The BEA figures are subject to frequent and sometimes large revisions. During July 2009, the BEA made significant downward revisions to its sales database back to 1993.

The US jewelry market has grown at a compound annual growth rate of 4.5% over the last 25 years. While Signet’s major competitors are other specialty jewelers, Signet also faces competition from other retailers that sell jewelry including department stores, discount stores, apparel outlets and internet retailers. Management believes that the jewelry category competes with other sectors, such as electronics, clothing and furniture, as well as travel and restaurants for consumers’ discretionary spending, particularly with regard to gift giving but less so with regard to bridal (engagement, wedding and anniversary) jewelry.

In calendar 2009, the US jewelry market contracted by a provisional estimated 1.9% (source: BEA), reflecting the continuing challenging economic environment. Based on provisional estimates, the specialty jewelry sector fell by 3.9% to $27.2 billion in calendar 2009 (source: US Census Bureau). As with the BEA figures, during 2009 downward revisions were made to the US Census Bureau figures for the preceding four years. The specialty sector saw a provisional decline in market share to 46.2% in calendar 2009 from 47.1% in calendar 2008.

The US division’s share of the specialty jewelry market increased to 9.4% in calendar 2009 from 9.0% in calendar 2008, based on initial estimates by the US Census Bureau. In fiscal 2010, the US division’s same store sales fell by 3.5% in the first three quarters, but increased by 7.4% in the fourth quarter. Spending by higher income consumers was weak in the first three quarters, but began to recover in the fourth quarter and this was reflected in the performance of Jared.

US Competitive Strengths

Store operations and human resources

The ability of the sales associate to explain the merchandise and its value is essential to most jewelry purchases

| • | Centrally prepared training schedules and materials are used by all stores and help ensure a consistently high level of customer service |

| • | All store managers are required to be trained diamontologists, so as to provide expert knowledge to customers |

| • | The US division employs over 5,000 qualified diamontologists, about 17% of all those awarded this qualification by the Diamond Council of America since 1998 |

| • | Measurable daily store standards provide staff with clear performance targets |

| • | Each store receives a monthly customer experience report helping to identify opportunities to improve customer service |

Merchandising

Offering the consumer greater value and selection

| • | Leading supply chain capability among middle market specialty jewelers provides better value to the customer |

| • | Each store is merchandised on an individual basis so as to provide appropriate selection |

| • | Highly responsive demand-driven merchandise systems enable swifter response to changes in customer behavior |

8

Table of Contents

| • | 24 hour re-supply capability means items wanted by customers are more likely to be in stock |

| • | In fiscal 2010, about 20% of merchandise sales accounted for by differentiated ranges (see page 15) |

Marketing

Leading brands in middle market sector

| • | Largest marketing budget in specialty jewelry sector, based on publicly available data, allowing more advertising impressions than competitors |

| • | Kay and Jared are able to achieve leverage through national television advertising |

| • | A proprietary marketing database of 26 million names provides significant opportunities for customer relationship marketing |

Real estate

Well designed stores in primary locations with high visibility and traffic flows

| • | Strict real estate criteria consistently applied over time has resulted in a high-quality store base |

| • | Well tested formats and locations reduce the risk of investing in new stores |

| • | The division’s high store productivity and financial strength make Signet an attractive tenant for landlords |

Customer finance

Ability to facilitate customer transactions

| • | About 53% of sales utilize financing provided by Signet |

| • | Dedicated, proprietary credit underwriting standards more accurately reflect Signet’s customer than those used by a typical third party scorecard |

| • | Manage the provision of customer finance in the context of the US business rather than by a third party’s priorities |

9

Table of Contents

US Brand Reviews

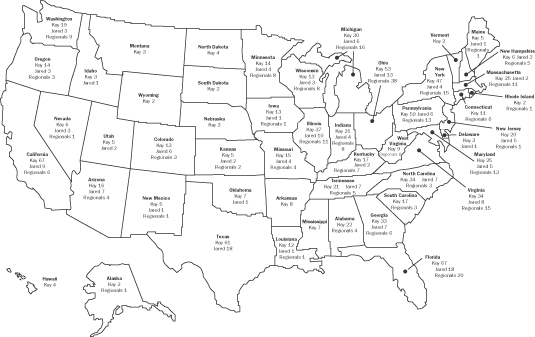

Location of Kay, Jared and Regional stores by state January 30, 2010

| Fiscal 2011 Planned |

Fiscal 2010 |

Fiscal 2009 |

Fiscal 2008 |

|||||||||

| Total opened during the year |

8 | 16 | 77 | 108 | ||||||||

| Kay |

6 | 8 | (1) | 57 | (1) | 68 | ||||||

| Jared |

2 | 7 | 17 | 19 | ||||||||

| Regional brands |

— | 1 | 3 | 21 | ||||||||

| Total closed during the year |

(50 | ) | (56 | ) | (75 | ) | (17 | ) | ||||

| Kay |

(14 | ) | (11 | ) | (25 | ) | (6 | ) | ||||

| Jared |

— | — | — | — | ||||||||

| Regional brands |

(36 | ) | (45 | )(1) | (50 | )(1) | (11 | ) | ||||

| Total open at the end of the year |

1,319 | 1,361 | 1,401 | 1,399 | ||||||||

| Kay |

915 | 923 | 926 | 894 | ||||||||

| Jared |

180 | 178 | 171 | 154 | ||||||||

| Regional brands |

224 | 260 | 304 | 351 | ||||||||

| Average sales per store in thousands(2) |

$1,814 | $1,788 | $1,996 | |||||||||

| Kay |

$1,582 | $1,536 | $1,710 | |||||||||

| Jared |

$4,046 | $4,491 | $5,341 | |||||||||

| Regional brands |

$1,163 | $1,160 | $1,344 | |||||||||

| (Decrease)/increase in net new store space |

(2 | )% | (1 | )% | 4 | % | 10 | % | ||||

| Percentage increase/(decrease) in same store sales |

0.2 | % | (9.7 | )% | (1.7 | )% | ||||||

| (1) | Includes two regional stores rebranded as Kay in fiscal 2010, and 14 in fiscal 2009. |

| (2) | Based only upon stores operated for the full fiscal year. |

10

Table of Contents

Sales data by brand

| Change on previous year | ||||||||||||||||

| Fiscal 2010 |

Sales | Average unit selling price |

Sales | Same store sales |

Average unit selling price |

|||||||||||

| Kay |

$ | 1,508.2m | $ | 307 | 4.8 | % | 4.4 | % | (7.4 | )% | ||||||

| Jared |

$ | 722.5m | $ | 713 | (1) | (0.5 | )% | (6.0 | )% | (7.3 | )%(1) | |||||

| Regional brands |

$ | 326.8m | $ | 329 | (11.9 | )% | (4.0 | )% | (4.8 | )% | ||||||

| US |

$ | 2,557.5m | $ | 324 | 0.8 | % | 0.2 | % | (16.8 | )% | ||||||

| (1) | Excludes the charm bracelet category, see page 14. |

Kay Jewelers

Kay operated 923 stores in 50 states at January 30, 2010 (January 31, 2009: 926 stores). Since fiscal 2005, Kay has been the largest specialty retail jewelry brand in the US, based on sales, and has subsequently increased its leadership position. Kay targets households with an income of between $35,000 and $100,000. Such households account for between 45% and 50% of US jewelry expenditure. Details of Kay’s performance over the last five years are given below:

| Fiscal 2010 |

Fiscal 2009 |

Fiscal 2008 |

Fiscal 2007(1) |

Fiscal 2006 | |||||||||||

| Sales (million) |

$ | 1,508.2 | $ | 1,439.1 | $ | 1,489.6 | $ | 1,486.7 | $ | 1,290.1 | |||||

| Stores at year end |

923 | 926 | 894 | 832 | 781 | ||||||||||

| (1) | 53 week year. |

Kay sales were $1,508.2 million during fiscal 2010 (fiscal 2009: $1,439.1 million). The increase in sales was due to a 14% rise in the number of transactions partly offset by a decrease in the average retail price of merchandise sold to $307 (fiscal 2009: $331), primarily reflecting changes in merchandise mix. Same store sales increased by 4.4% during the year, with the fourth quarter up 7.7%. During fiscal 2010, the number of Kay stores fell by three to 923. The Kay website, www.kay.com, was enhanced further and e-commerce sales increased significantly, but remain small in the context of the brand.

Kay stores typically occupy about 1,500 square feet and have around 1,250 square feet of selling space. They have historically been located in enclosed regional malls. Since 2002, new formats have been developed for locations outside of traditional malls, because management believes these alternative locations present an opportunity to reach new customers who are aware of the brand but have no convenient access to a store, or for customers who prefer not to shop in an enclosed mall. Such stores further leverage the strong Kay brand, marketing support and the central overhead. In addition, nearly all current retail construction projects undertaken in recent years by developers are in formats other than enclosed regional malls.

Recent net openings, current composition and planned openings in fiscal 2011 are shown below:

| Expected net change fiscal 2011 |

Stores at January 30, 2010 |

Net openings | |||||||||||||||

| Fiscal 2010 |

Fiscal 2009 |

Fiscal 2008 |

Fiscal 2007 |

Fiscal 2006 | |||||||||||||

| Enclosed mall |

(6 | ) | 794 | (1 | )(1) | 6 | (1) | 17 | 26 | 25 | |||||||

| Off-mall |

(4 | ) | 111 | (2 | ) | 18 | 40 | 21 | 14 | ||||||||

| Outlet |

2 | 18 | — | 8 | 5 | 4 | — | ||||||||||

| Total |

(8 | ) | 923 | (3 | ) | 32 | 62 | 51 | 39 | ||||||||

| (1) | Includes two regional stores rebranded as Kay in fiscal 2010, and 14 in fiscal 2009. |

11

Table of Contents

Jared The Galleria Of Jewelry

Jared is the leading off-mall destination specialty retail jewelry chain in its sector of the market, based on sales, with 178 stores in 35 states as at January 30, 2010 (January 31, 2009: 171). The first Jared store was opened in 1993, and, since its roll-out began in 1998, it has grown to become the fourth largest US specialty retail jewelry brand by sales. Each Jared is equivalent in size to about four of the division’s mall stores and its average retail price of diamond merchandise sold, is more than double that of a Kay store. In space terms, Jared is equivalent to over 700 US division mall stores. Its main competitors are independent operators. The next two largest such chains significantly reduced their store numbers during fiscal 2010 from 23 to 20 and 20 to 10 stores respectively. Jared targets households with an income of between $50,000 and $150,000. Management believe that such households account for about 45% of US jewelry expenditure. Management believes this to be an under-served sector. An important distinction of a destination store is that the potential customer visits the store with a greater intention of making a jewelry purchase, whereas in a mall there is a possibility that the potential shopper is undecided about the product category in which they will ultimately make a purchase.

Details of Jared’s performance over the last five years are given below:

| Fiscal 2010 |

Fiscal 2009 |

Fiscal 2008 |

Fiscal 2007(1) |

Fiscal 2006 | |||||||||||

| Sales (million) |

$ | 722.5 | $ | 726.2 | $ | 756.4 | $ | 664.4 | $ | 534.2 | |||||

| Stores at year end |

178 | 171 | 154 | 135 | 110 | ||||||||||

| (1) | 53 week year. |

Jared sales were $722.5 million during fiscal 2010 (fiscal 2009: $726.2 million). Same store sales decreased by 6.0% during the year, but increased by 9.1% in the fourth quarter. The decrease in same store sales was due to a fall in the number of transactions excluding the charm bracelet category and, primarily reflecting changes in the merchandise mix, a decrease in the average retail price of merchandise sold to $713 (fiscal 2009: $769), excluding the impact of a charm bracelet range rolled out during fiscal 2010 (see page 14). The portfolio of stores increased by seven to 178. The Jared website, www.jared.com, was enhanced having become transactional during fiscal 2009. E-commerce sales increased significantly but are only a small proportion of sales.

A key point of differentiation, compared to a typical mall store, is Jared’s higher quality of customer service. As a result of its larger size, more specialist staff are available and additional in-depth selling methodologies may be used, such as the ‘white glove’ presentation of timepieces.

Every Jared store has an on-site design and repair workshop where most repairs are completed within one hour. The center also mounts loose diamonds in settings and provides a custom design service when required. Each store also has at least one diamond viewing room, a children’s play area and complimentary refreshments.

The typical Jared store continues to have about 4,800 square feet of selling space and around 6,000 square feet of total space. Jared locations are normally free-standing sites in shopping developments with high visibility and traffic flow, and positioned close to major roads. Jared stores operate in retail centers that normally contain strong retail co-tenants, including other category killer destination stores such as Barnes & Noble, Best Buy, Home Depot and Bed, Bath & Beyond, as well as some smaller specialty units.

Recent net openings, current composition and planned openings in fiscal 2011 are shown below:

| Expected net openings fiscal 2011 |

Stores at January 30, 2010 |

Net openings | ||||||||||||

| Fiscal 2010 |

Fiscal 2009 |

Fiscal 2008 |

Fiscal 2007 |

Fiscal 2006 | ||||||||||

| Total |

2 | 178 | 7 | 17 | 19 | 25 | 17 | |||||||

12

Table of Contents

US Regional Brands

Signet also operates mall stores under a variety of established regional trading names. At January 30, 2010, 260 regional brand stores operated in 36 states (January 31, 2009: 304 stores in 37 states). The leading brands include JB Robinson Jewelers, Marks & Morgan Jewelers and Belden Jewelers. Nearly all of these stores are located in malls where there is also a Kay store and target a similar customer. As the average sales per store is less than that of the Kay chain, and they do not have the leverage of national TV advertising, regional brand stores are more likely to be closed than Kay stores. Details of regional brands’ performance over the last five years are given below:

| Fiscal 2010 |

Fiscal 2009 |

Fiscal 2008 |

Fiscal 2007(1) |

Fiscal 2006 | |||||||||||

| Sales (million) |

$ | 326.8 | $ | 370.8 | $ | 459.7 | $ | 501.0 | $ | 484.5 | |||||

| Stores at year end |

260 | 304 | 351 | 341 | 330 | ||||||||||

| (1) | 53 week year. |

Regional brand sales for fiscal 2010 were $326.8 million (fiscal 2009: $370.8 million). The decrease in sales was due to store closures, a fall in the number of transactions, and a decrease in the average retail price of merchandise sold to $329 (fiscal 2009: $346), primarily reflecting changes in merchandise mix. Same store sales decreased by 4.0% during the year, but increased in the fourth quarter by 2.8%.

The location and size of regional brand stores within a mall is similar to that of a Kay store, and consideration is given to changing a regional brand store to Kay where the overall return on capital employed, including any resulting impact on other stores operated by the US division, may be increased. In fiscal 2010, two regionally branded stores were converted to the Kay format (fiscal 2009: 14). New regional chain stores are opened only if real estate satisfying the US division’s investment criteria becomes available in their respective trading areas.

Recent net closures and openings, current composition and planned closures in fiscal 2011 are shown below:

| Expected net change fiscal 2011 |

Stores at January 30, 2010 |

Net (closures) / openings | |||||||||||||||

| Fiscal 2010 |

Fiscal 2009 |

Fiscal 2008 |

Fiscal 2007 |

Fiscal 2006 | |||||||||||||

| Total |

(36 | ) | 260 | (44 | )(1) | (47 | )(1) | 10 | 11 | 9 | |||||||

| (1) | Includes two regional stores rebranded as Kay in fiscal 2010 and 14 in fiscal 2009. |

US Functional Review

Operating structure

While the US division operates under 12 different brands, many functions are integrated to gain economies of scale. For example, store operations have a separate dedicated field management team for the mall brands, Jared and the in-store repair function, while there is a combined diamond sourcing function.

US Customer Service and Human Resources

In specialty jewelry retailing, the level and quality of customer service is a key competitive factor as nearly every in-store transaction involves the sales associate taking a piece of jewelry or a watch out of a display case and presenting it to the potential customer. Therefore the ability to recruit, train and retain suitably qualified sales staff is important in determining sales, profitability and the rate of net store space growth. Consequently the US division has in place comprehensive recruitment, training and incentive programs and uses employee attitude and customer satisfaction surveys. A continual priority of the US division is to improve the quality of

13

Table of Contents

customer experiences in its existing stores, while providing sufficient staff that are well trained and with suitable experience to run any new stores being opened.

During fiscal 2010, focus was on increasing the efficiency of in-store execution and aligning store staff hours to sales volume, subject to minimum staffing levels. In addition, at the start of fiscal 2010 a further reduction in staffing levels at the divisional head office was implemented. Staff training, which centered on product knowledge and selling skills, remained a priority. In a difficult year, employees remained motivated, focused on maintaining excellence in execution, and were well, and appropriately, incentivized.

US Merchandising and Purchasing

Management believes that merchandise selection, availability, and value for money are critical factors to success for a specialty retail jeweler. In the US business, the range of merchandise offered and the high level of inventory availability are supported centrally by extensive and continuous research and testing. Best-selling products are identified and replenished rapidly through analysis of sales by stock keeping unit. This approach enables the US division to deliver a focused assortment of merchandise to maximize sales and inventory turn, and minimize the need for discounting. Management believes that the US division is better able than its competitors to offer greater value and consistency of merchandise, due to its supply chain advantages discussed below. In addition, in recent years management has developed and continues to execute a strategy to increase the proportion of differentiated merchandise sold in response to consumer demand.

In the second half of fiscal 2009, a charm bracelet range was tested in a limited number of Jared stores. The test was successful and the range was rolled out to nearly all Jared stores in October 2009. The typical customer for this range was in the Jared demographic, but had not previously shopped at a Jared store. The typical average selling price of an item from the range was significantly below the average for Jared, but the purchase frequency was greater. As a result, the introduction of the charm bracelet range materially increased traffic and transaction volume for Jared, but greatly lowered the average selling price. Therefore items from this range have been excluded from the calculation of the average selling price for Jared. Management believes that this provides a better indication of the trend in buying patterns of the core Jared customer.

Average merchandise unit selling price ($), excluding repairs, warranty and other miscellaneous sales

| Fiscal 2010 |

Fiscal 2009 |

Fiscal 2008 |

Fiscal 2007 |

Fiscal 2006 | ||||||

| Kay |

307 | 331 | 327 | 317 | 305 | |||||

| Jared(1) |

713 | 769 | 747 | 719 | 697 | |||||

| Regional brands |

329 | 346 | 343 | 332 | 324 |

| (1) | Excluding the charm bracelet category. |

The average unit selling price fell in fiscal 2010 compared to fiscal 2009. During the first nine months of fiscal 2010, the decrease was 13% (mall brands down by 7% and Jared, excluding charm bracelets was down by 9%). This reflected mix changes offset by a small benefit from price increases implemented in the first quarter of fiscal 2009. In the fourth quarter of fiscal 2010, the average unit selling price decreased by 20% (mall brands down by 7% and Jared, excluding charm bracelets, down by 3%).

Merchandise mix

About 76% of the jewelry and watch sales of the US division contain one or more diamonds. Other significant merchandise categories are gold and silver jewelry (including charms) without any gemstone; other jewelry which mostly contains gemstones, such as sapphires, rubies, emeralds and pearls; and watches. In fiscal 2010, sales of silver jewelry and charms increased markedly.

14

Table of Contents

Sales of jewelry can also be divided by purpose of purchase, with bridal, which includes engagement, wedding and anniversary purchases, accounting for 45% to 50% of the US division’s sales. Other reasons for buying jewelry and watches include gift giving, which is important at Christmas, Valentine’s Day and Mother’s Day, and self reward. The bridal category is believed by management to be more stable than the other two major reasons for buying jewelry, but it is still dependent on the economic environment as customers can trade down to lower price points.

A further categorization of merchandise is generic, branded and differentiated. Generic merchandise are items and styles available from a wide range of jewelry retailers, such as solitaire rings and diamond stud earrings. It also includes styles such as diamond fashion bracelets, ‘circle’ items and concepts promoted by De Beers such as ‘Journey’ diamond jewelry and ‘right hand’ rings. Within the generic category, the US division has exclusive designs of particular styles and also has ‘value items’, see page 16. Branded merchandise is mostly watches, but also includes ranges such as the Pandora™ charm bracelet which was rolled out to most Jared stores for Christmas 2009. Differentiated merchandise, are items that are branded and exclusive to the US division in its marketplace or where it is not widely available in other specialty jewelry retailers. The US division’s sales of differentiated merchandise increased significantly in fiscal 2010, see below.

In addition to selling jewelry and watches, the US division also makes other related sales such as design and repair services, and warranties. See page 18.

US division merchandise mix, excluding repairs, warranty and other miscellaneous sales

| Fiscal 2010 |

Fiscal 2009 |

Fiscal 2008 | ||||

| % | % | % | ||||

| Diamonds and diamond jewelry |

76 | 75 | 75 | |||

| Gold & silver jewelry, including charms |

8 | 7 | 7 | |||

| Other jewelry |

9 | 11 | 11 | |||

| Watches |

7 | 7 | 7 | |||

| 100 | 100 | 100 | ||||

Differentiated ranges

Differentiated merchandise includes:

| • | the Leo Diamond® range, which is sold exclusively by Signet in the US and the UK, was the first diamond to be independently and individually certified to be visibly brighter; |

| • | the Peerless Diamond® , an Ideal Cut diamond with a superior, measured return of light, available only in Jared stores; |

| • | exclusive ranges of jewelry by Le Vian®, a prestigious fashion jewelry brand with a 500 year history. In addition, the US division’s mall brand stores are the only specialty retail jeweler to offer Le Vian® merchandise in covered regional malls; |

| • | Open Hearts by Jane Seymour®, a range of jewelry designed by the actress and artist Jane Seymour, which was successfully tested and launched in fiscal 2009; and |

| • | Love’s EmbraceTM, a new collection, which was tested and rolled out during fiscal 2010. |

Management believes that the US division’s scale, well trained sales staff, ability to advertise on national television, strong balance sheet and record of success, make it the preferred retail partner for jewelry manufacturers wishing to develop distinctive new jewelry merchandise. As a result, management also believes that it is offered such merchandise before other US retailers and is well positioned to negotiate restricted

15

Table of Contents

distribution agreements with such manufacturers. Differentiated ranges raise the profile of the US division’s store brands, help to drive sales, have a gross merchandise margin rate a little above the US division as a whole and improve inventory turn. Differentiated merchandise performed very well and increased as a share of sales to about 20% in fiscal 2010 (fiscal 2009: 10% to 15%). The US division further developed the Open Hearts by Jane Seymour® selection and successfully launched the Love’s EmbraceTM range. There was continued success with the Leo Diamond® and merchandise from Le Vian®. Therefore it is planned to develop additional differentiated ranges and to further expand those already launched.

Value items

By planning ahead and using its expertise in the loose, polished diamond market and the jewelery manufacturing sector, the US division engineered value items that appealed to the more cost conscious consumer. These items utilize Signet’s ability to identify anomalies in the supply chain, together with its scale and balance sheet strength, to purchase merchandise on advantageous terms. The savings achieved, together with a lower gross merchandise margin, result in such value items offering great value to the consumer. These items are prominently displayed in printed marketing materials. In fiscal 2010, due to parts of the supply chain being under financial pressure, there were more anomalies in pricing than normal. Management took advantage of this to offer a greater range of value items in the Christmas 2009 catalog, so as to cater to an anticipated increase in the proportion of consumers that would be value-conscious. In fiscal 2010 these items performed well and helped drive achieved gross merchandise margin dollars, but did contribute to a lower gross merchandise margin rate in the fourth quarter.

Direct sourcing of polished diamonds

Management believes that the US division has a competitive cost and quality advantage because about 42% (fiscal 2009: 43%) of diamond merchandise sold is sourced through contract manufacturing. This involves Signet purchasing loose polished diamonds on the world markets and outsourcing the casting, assembly and finishing operations to third parties. By using this approach, the cost of merchandise is reduced, enabling the US division to provide better value to the consumer, which helps to increase market share and achieve higher gross merchandise margins. Contract manufacturing is generally utilized on basic items with proven, non-volatile, historical sales patterns that represent a lower risk of over or under purchasing the quantity required.

The contract manufacturing strategy also allows Signet’s buyers to gain a detailed understanding of the manufacturing cost structure and improves the prospects of negotiating better prices for the supply of finished products.

The proportion of diamonds sourced loose decreased in fiscal 2010 due to the growth of differentiated ranges, where merchandise is more likely to be bought complete.

Rough diamond initiative

In fiscal 2006, Signet commenced a multi-year trial involving the purchase and contract cutting and polishing of rough diamonds to supply the US division. In the third quarter of fiscal 2009, given the prevailing economic environment, the initiative was discontinued. The remaining associated inventory was disposed of during fiscal 2010.

Sourcing of finished merchandise

Merchandise is purchased as a finished product where the complexity of the item is great, the merchandise is considered likely to have a less predictable sales pattern or where cost can be reduced. In addition, a significant proportion of differentiated merchandise is purchased in this way. This method of buying inventory provides the opportunity to reserve inventory held by vendors and to make returns or exchanges with the supplier, thereby reducing the risk of over or under purchasing. Management believes that the division’s scale and strong balance sheet enables it to purchase merchandise at a lower price, and on better terms, than most of its competitors.

16

Table of Contents

Merchandise held on consignment

Merchandise held on consignment is used to enhance product selection and test new designs. This minimizes exposure to changes in fashion trends and obsolescence, and provides the flexibility to return non-performing merchandise. At January 30, 2010, the US division held $135 million (January 31, 2009: $202 million) of merchandise on consignment (see Note 11, Item 8).

Suppliers

In fiscal 2010, the five largest suppliers collectively accounted for approximately 25% (fiscal 2009: 22%) of the US division’s total purchases, with the largest supplier accounting for approximately 7% (fiscal 2009: 8%). The US division’s supply chain is integrated on a worldwide basis, with diamond cutting and jewelry manufacturing being predominantly carried out in Asia.

The division benefits from close commercial relationships with a number of suppliers and damage to, or loss of, any of these relationships could have a detrimental effect on results. Although management believes that alternative sources of supply are available, the abrupt loss or disruption of any significant supplier during the three month period (August to October) leading up to the Christmas season could result in a material adverse effect on performance. Therefore a regular dialogue is maintained with suppliers, particularly in the present economic climate.

The luxury and prestige watch manufacturers and distributors normally grant agencies to sell their ranges on a store by store basis. Signet sells its luxury watch brands primarily through Jared and management believes that the watch brands help attract customers to Jared and build sales in all categories.

Raw materials and the supply chain

The jewelry industry generally is affected by fluctuations in the price and supply of diamonds, gold and, to a much lesser extent, other precious and semi-precious metals and stones.

The ability of Signet to increase retail prices to reflect higher commodity costs varies, and an inability to increase retail prices could result in lower profitability. Historically, jewelry retailers have, over time, been able to increase prices to reflect changes in commodity costs. However, particularly sharp increases and volatility in commodity costs usually result in a time lag before increased commodity costs are fully reflected in retail prices due to the slow inventory turn, hedging activities and the use of average cost accounting in the calculation of costs of goods sold by some retailers. Diamonds account for about 55% of the US division’s cost of goods sold, and in fiscal 2010, the cost of diamonds in the qualities and sizes required, declined. While diamond prices increased somewhat towards the end of the year, they remained below the level paid in fiscal 2009. The cost of gold, which accounts for about 20% of the US division’s cost of goods sold, again increased in fiscal 2010. Overall, commodity cost movements in fiscal 2010 had a limited net impact on the cost of goods sold.

In early fiscal 2011, the US division implemented selective price increases for merchandise that contains a significant proportion of gold to reflect higher commodity costs. These ranges account for less than 30% of the US division’s sales.

Signet undertakes some hedging of its requirement for gold through the use of options, forward contracts and commodity purchasing. It does not hedge against fluctuations in the cost of diamonds. The cost of raw materials is only part of the costs involved in determining the retail selling price of jewelry, with labor costs also being a significant factor. Management continues to seek ways to reduce the cost of goods sold by improving the efficiency of its supply chain.

The largest product category sold by Signet is diamonds and diamond jewelry. The supply and price of diamonds in the principal world markets are significantly influenced by a single entity, De Beers, through its subsidiary, the

17

Table of Contents

Diamond Trading Company, although its market share has been decreasing. Significant changes in the diamond supply chain in recent years have also resulted from changes in government policy in a number of African diamond producing countries. In addition, the sharp downturn in worldwide demand for diamonds, reflecting the challenging economic environment, may result in further significant changes in the supply chain.

Inventory management

Sophisticated inventory management systems for merchandise testing, assortment planning, allocation and replenishment are in place, thereby reducing inventory risk by enabling management to identify and respond quickly to changes in consumers’ buying patterns. The majority of merchandise is common to all US division mall stores, with the remainder allocated to reflect demand in individual stores. Management believes that the merchandising and inventory management systems, as well as improvements in the productivity of the centralized distribution center, have allowed the US division to achieve inventory turns at least comparable to those of competitors, even though it has a significantly less mature store base and undertakes more direct sourcing of merchandise. The vast majority of inventory is held at stores rather than in the central distribution facility.

In fiscal 2010, management reduced inventory levels by about $225 million, primarily reflecting the lower level of sales experienced in fiscal 2009. This was achieved by tight control of purchases rather than discounting, as the US division’s procedures are designed to minimize clearance merchandise. A further inventory realignment is not planned in fiscal 2011. As a result of superior systems and a very experienced inventory management team, together with Signet’s strong balance sheet and liquidity, the US division was able to quickly respond to better than expected demand in the fourth quarter.

Other sales

While design and repair services represent less than 10% of sales, they account for approximately 30% of transactions and have been identified by management as an important opportunity to build consumers’ trust, particularly in the Jared division. All Jared stores have a highly visible jewelry workshop, which is open the same hours as the store. The workshops meet the repair requirements of the store in which they are located and also carry out work for the US division’s mall brand stores. As a result, nearly all customer repairs are carried out by the US division’s own staff, unlike most other chain jewelers which do this through sub-contractors. The design and repair function has its own field management and training structure.

For about 15 years, the US division has sold a lifetime repair warranty for jewelry. The warranty covers services such as ring sizing, refinishing and polishing, rhodium plating white gold, earring repair, chain soldering and the resetting of diamonds and gemstones that arise due to the normal usage of the merchandise. This work is carried out in-house.

US Marketing and Advertising

Management believes customers’ confidence in the retailer, store brand name recognition and advertising of differentiated ranges, are important factors in determining buying decisions in the specialty jewelry sector because the majority of merchandise is unbranded. Therefore, the US division continues to strengthen and promote its reputation by aiming to deliver superior customer service and build brand name recognition. In fiscal 2010, there was increased focus on including differentiated merchandise in national television advertising. The marketing channels used include television, radio, print, catalog, direct mail, telephone marketing, point of sale signage, in-store displays and electronic methods. Marketing activities are carefully tested and their success monitored by methods such as market research and sales productivity.

While marketing activities are undertaken throughout the year, the level of activity is concentrated at periods when customers are expected to be most receptive to marketing messages, which is before Christmas Day,

18

Table of Contents

Valentine’s Day and Mother’s Day. A significant majority of the marketing expenditure is on national television advertising which provides an opportunity to leverage its cost over time if the number of stores or sales increases.

Statistical and technology-based systems are employed to support a customer marketing program that uses a proprietary database of 26 million names to strengthen the relationship with customers through mail, telephone and email communications. The program targets current customers with special savings and merchandise offers during key trading periods. In addition, invitations to special in-store promotional events are extended throughout the year.

Historically, generic marketing activity undertaken by De Beers in the US to promote diamonds and diamond jewelry designs was important in influencing the size of the total jewelry market and the popularity of particular styles of jewelry. With the significant reduction by De Beers of its promotional expenditure on diamonds and diamond jewelry, management believes that marketing carried out by specialty jewelry retailers has become more important. Given the size of the marketing budgets for Kay and Jared, management believes this has increased the US division’s competitive marketing advantage, in particular the ability to advertise differentiated merchandise on national television is of growing importance. The US division’s five year record of gross advertising spend is given below:

| Fiscal 2010 |

Fiscal 2009 |

Fiscal 2008 |

Fiscal 2007(1) |

Fiscal 2006 | |||||||||||

| Gross advertising spend (million) |

$ | 153.0 | $ | 188.4 | $ | 204.0 | $ | 184.5 | $ | 152.8 | |||||

| Percent to sales (%) |

6.0 | 7.4 | 7.5 | 7.0 | 6.6 | ||||||||||

| (1) | 53 week year. |

In fiscal 2010, to reflect lower anticipated sales levels, marketing expenditure was further concentrated on the most productive channels and brands, and was planned to be in line with the advertising to sales ratio typical before fiscal 2008. The ratio of gross advertising spend to sales during fiscal 2010 was 6.0% (fiscal 2009: 7.4%), which was below the planned level due to the better than expected sales growth achieved in the fourth quarter of fiscal 2010. Dollar gross marketing expenditure was reduced by 18.8% to $153.0 million (fiscal 2009: $188.4 million). Marketing efforts were focused on national television advertising for Kay and Jared, and the US division continued to have the leading ‘share of voice’ within the US jewelry sector. Television advertising impressions in the fourth quarter of fiscal 2010 for Kay were down mid single digits and for Jared increased marginally.

Websites

The Kay and Jared websites are among the most visited in the specialty jewelry sector and primarily provide potential customers with a source of information about the merchandise available. A significant majority of customers who buy after visiting the websites, do so in store where they can physically examine the product. Sales made directly from the websites rose significantly in fiscal 2010 but remain small in the context of the US division.

US Real Estate

Given the challenging environment, and management’s strict investment criteria, action was taken in early fiscal 2009 to sharply slow the rate of store space growth and the level of store refurbishments. This was achieved by reducing the number of stores opened and increasing store closures as leases expired. Net store space in fiscal 2010 decreased by 1% (fiscal 2009: increase 4%), see table on page 82 for details. Capital expenditure in new and existing stores was $18.2 million (fiscal 2009: $56.3 million). Working capital investment, that is inventory and receivables, associated with new stores was $28.2 million (fiscal 2009: $66.5 million). In fiscal 2011, store capital expenditure is planned to amount to about $5 million on new space and about $35 million on existing stores, with about $11 million of working capital investment associated with new store openings.

19

Table of Contents

Recent and planned investment in the store portfolio is set out below:

| Fiscal 2011 planned |

Fiscal 2010 |

Fiscal 2009 |

Fiscal 2008 | |||||

| $million | $million | $million | $million | |||||

| New store fixed capital investment |

5 | 10.1 | 39.0 | 60.1 | ||||

| Other store fixed capital investment |

35 | 8.1 | 17.3 | 28.0 | ||||

| Total store fixed capital investment |

40 | 18.2 | 56.3 | 88.1 | ||||

| Working capital investment in new stores |

11 | 28.2 | 66.5 | 118.8 |

As a result of the growth of Jared and the development of Kay outside of its enclosed mall base, the US division is increasingly competing with independent specialty jewelry retailers that are able to adjust their competitive stance, for example on pricing, to local market conditions. This can put individual stores at a competitive disadvantage as the US division has a national pricing strategy.

US Customer Finance

In the US jewelry market, management believes that it is necessary for specialty retailers to offer credit facilities to the consumer. In fiscal 2010, 53.5% (fiscal 2009: 53.2%) of the US division’s sales were made using one of its in-house customer finance programs.

Management regards the provision of an in-house customer finance program, rather than one provided by a third party, as a competitive advantage for a number of reasons:

| • | credit policies are decided by taking into account the overall impact on the business rather than by a third party whose priorities may conflict with those of the division; |

| • | authorization and collection models are based on the behavior of the division’s consumers; |

| • | it allows management to establish and implement customer service standards appropriate for the business; |

| • | it provides a database of regular customers and their spending patterns; |

| • | investment in systems and management of credit offerings appropriate for the business can be facilitated; and |

| • | it maximizes cost effectiveness by utilizing in-house capability. |

Furthermore the various customer finance programs help to establish long term relationships with customers and complement the marketing strategy by enabling a greater number of purchases, higher units per transaction and greater value sales.

In addition to interest-bearing accounts, a significant proportion of credit sales are made using interest-free financing for one year or less, subject to certain conditions. In most US states, customers are offered optional third party credit insurance.

The customer financing operation is fully integrated into the management of the US division and is not a separate operating division nor does it report separate results. All assets and liabilities relating to customer financing are shown on the balance sheet and there are no associated off-balance sheet arrangements. Signet’s current balance sheet and access to liquidity do not constrain the US division’s ability to grant credit, which is a further competitive advantage in the current economic environment.

Allowances for uncollectible amounts are recorded as a charge to cost of goods sold in the income statement. The allowance is calculated using a model that analyzes factors such as delinquency rates, recovery rates and other portfolio data. A 100% allowance is made for any amount that is 90 days past due on a recency basis. The calculation is reviewed by management to assess whether, based on economic events, additional analyses are required to appropriately estimate losses inherent in Signet’s portfolio.

20

Table of Contents

Credit authorization and collection systems were centralized in 1994 and the overall credit offer to customers has been little changed during the last 15 years although the detailed terms have been changed, for example due to amendments to the Truth in Lending Act.

Each individual application for credit is evaluated against set criteria. The risks associated with the granting of credit to particular groups of customers with similar characteristics are balanced against the gross merchandise margin earned by the proposed sales to those customers. During fiscal 2010, an increase in credit acceptance rates followed the introduction of revised authorization criteria for some credit applicants based on the historic performance of parts of the credit portfolio. This did not reflect a change in the risk profile by which the credit operation was managed and was part of the normal review of such criteria. Management believes that a primary driver of the level of uncollectible receivables is the rate of change in the level of unemployment. Cash flows associated with the granting of credit to customers of the individual store are included in the projections used when considering store investment proposals.

As at January 30, 2010, the gross US receivables stood at $921.5 million (January 31, 2009: $886.1 million) and there was a bad debt allowance of $72.2 million (January 31, 2009: $69.5 million). The average level of gross receivables during fiscal 2010 was $845.1 million (fiscal 2009: $840.5 million).

Customer financing statistics

| Fiscal 2010 |

Fiscal 2009 |

Fiscal 2008 |

||||||||||

| Opening receivables (million) |

$ | 886.1 | $ | 900.6 | $ | 828.8 | ||||||

| Credit sales (million) |

$ | 1,368.2 | $ | 1,349.2 | $ | 1,422.4 | ||||||

| Closing receivables (million) |

$ | 921.5 | $ | 886.1 | $ | 900.6 | ||||||

| Credit sales as % of total sales |

53.5 | % | 53.2 | % | 52.6 | % | ||||||

| Number of active credit accounts at year end |

936,286 | 893,740 | 940,069 | |||||||||

| Average outstanding account balance |

$ | 1,016 | $ | 1,028 | $ | 997 | ||||||

| Average monthly collection rate |

12.5 | % | 13.1 | % | 13.9 | % | ||||||

| Net bad debt to total sales |

5.6 | % | 4.9 | % | 3.4 | % | ||||||

| Net bad debt to credit sales |

10.4 | % | 9.2 | % | 6.5 | % | ||||||

| Period end bad debt allowance to period end receivables |

7.8 | % | 7.8 | % | 6.7 | % | ||||||

In fiscal 2010, the net bad debt charge at 5.6% of total US sales (fiscal 2009: 4.9%) was 0.7% higher than in fiscal 2009 and was again well above the tight range of 2.8% to 3.4% experienced in the ten years prior to fiscal 2009. However the performance in the fourth quarter showed some initial signs of stabilizing. Credit participation was little changed at 53.5% (fiscal 2009: 53.2%), and in the fourth quarter it was 20 basis points lower than in the comparable quarter in fiscal 2009.

Customer financing administration

Authorizations and collections are performed centrally at the US head office, rather than in each individual store. The majority of credit applications are processed and approved automatically after being initiated via in-store terminals, through a toll-free phone number or on-line through the US division’s websites. The remaining applications are reviewed by credit authorization agents. All applications are evaluated by scoring credit and using data obtained through third party credit bureaus. Collection procedures use risk-based calling and first call resolution strategies. In fiscal 2010, information technology, systems support and collection strategies were made more effective and additional investment is planned in fiscal 2011.

Truth in Lending Act

In fiscal 2011, the US division will have to comply with certain new provisions of the Truth in Lending Act, that became effective on February 22, 2010 and others of which will come into force in August 2010. Where possible,

21

Table of Contents

actions have been taken to reduce the impact of these new provisions. Management expects that these new provisions will directly and adversely impact operating income by a net $15 million to $20 million in fiscal 2011, primarily because they will limit the timing and actions that the US division can take when a customer fails to make an agreed repayment. There may be a further indirect impact on sales arising from these amendments as a result of changes in consumer behavior. In addition, systems, procedures and credit terms have been amended to comply with changes in legislation.

Third party credit sales

In addition to in-house credit sales, the US stores accept major credit cards. Third party credit sales are treated as cash sales and accounted for approximately 39% (fiscal 2009: 38%) of total US sales during fiscal 2010.

US Management Tools and Communications

The US division’s integrated and comprehensive information systems provide detailed, timely information to monitor and evaluate many aspects of the business. They are designed to support financial reporting and management control functions such as merchandise testing, loss prevention and inventory control, as well as reduce the time sales staff spend on administrative tasks and increase time spent on sales activities.

All stores are supported by the internally developed Store Information System, which includes electronic point of sale (“EPOS”) processing, in-house credit authorization and support, a district manager information system and constant broadband connectivity for all retail locations for data communications including e-mail. The EPOS system updates sales, in-house credit and perpetual inventory replenishment systems throughout the day for each store.

US Regulation

The US division is required to comply with numerous US federal and state laws and regulations covering areas such as consumer protection, consumer privacy, consumer credit (including the Truth in Lending Act, see above), consumer credit insurance, truth in advertising and employment legislation. Management monitors changes in these laws to ensure that its practices comply with applicable requirements.

UK DIVISION

Movements in the US dollar to pound sterling exchange rate have an impact on the results of Signet as the UK division is managed in pounds sterling as sales and costs are both incurred in that currency, and its results are then translated into US dollars for external reporting purposes. The following information for the UK division is given in pounds sterling. Management believes that this presentation assists in the understanding of the performance of the UK division. The impact on reported US dollar figures of movements in pound sterling to the US dollar exchange rate is particularly marked in periods of exchange rate volatility. See Item 6 for analysis of results at constant exchange rates; non-GAAP measures.

UK market