Attached files

Exhibit 13

Guaranty Federal Bancshares, Inc.

2009 Annual Report

|

Contents

i President's Message

1 Investor Information

2 Common Stock Prices & Dividends

4 Selected Consolidated Financial and Other Data

5 Management's Discussion and Analysis of Financial Condition and Results of Operations

17 Consolidated Financial Statements

49 Report of Independent Registered Public Accounting Firm

50 Directors and Officers

|

Investor Information

ANNUAL MEETING OF STOCKHOLDERS:

The Annual Meeting of Stockholders of the Company will be held Wednesday, May 26, 2010 at 6:00 p.m., local time, at the Guaranty Bank Operations Center, 1414 W. Elfindale, Springfield, Missouri.

ANNUAL REPORT ON FORM 10-K:

Copies of the Company's Annual Report on Form 10-K, including the financial statements, filed with the Securities and Exchange Commission are available without charge upon written request to:

Lorene Thomas, Secretary

Guaranty Federal Bancshares, Inc.,

1341 W. Battlefield St., Springfield, MO 65807-4181

TRANSFER AGENT:

Registrar and Transfer Company

10 Commerce Drive

Cranford, NJ 07016

STOCK TRADING INFORMATION:

Symbol: GFED

SPECIAL LEGAL COUNSEL:

Husch Blackwell Sanders LLP

901 St. Louis St., Suite 1900

Springfield, MO 65806

INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM:

BKD, LLP

910 St. Louis St.

PO Box 1190

Springfield, MO 65801-1190

STOCKHOLDER AND FINANCIAL INFORMATION:

Carter Peters,

Executive Vice President, Chief Financial Officer

417-520-4333

|

1

Guaranty Federal Bancshares, Inc.

2009 Annual Report

|

Common Stock Prices & Dividends

|

|

|

The common stock of Guaranty Federal Bancshares, Inc. (the "Company") is listed for trading on the NASDAQ Global Market under the symbol "GFED". As of March 18, 2010, there were approximately 1410 holders of shares of the Company's common stock. At that date the Company had 6,779,800 shares of common stock issued and 2,638,440 shares of common stock outstanding.

|

|

|

During the year ended December 31, 2009, the Company did not declare a cash dividend. During the year ended December 31, 2008, the Company paid dividends of (i) $0.18 per share on April 18, 2008, to stockholders of record as of April 7, 2008, (ii) $0.18 per share on July 18, 2008 to stockholders of record as of July 7, 2008. The Company did not declare a cash dividend in the third or fourth quarters of 2008. Any future dividends, if any, will be at the discretion of the Company's Board of Directors and will depend on, among other things, the Company's results of operations, cash requirements and surplus, financial condition and other factors that the Company's Board of Directors may consider relevant.

|

|

|

The table below reflects the range of common stock high and low closing prices per the NASDAQ Global Market by quarter for the years ended December 31, 2009 and 2008.

|

|

Year ended

|

Year ended

|

|||||||||||||||

|

December 31, 2009

|

December 31, 2008

|

|||||||||||||||

|

High

|

Low

|

High

|

Low

|

|||||||||||||

|

Quarter ended:

|

||||||||||||||||

|

March 31

|

$ | 5.95 | 3.85 | $ | 28.78 | 24.94 | ||||||||||

|

June 30

|

7.50 | 4.61 | 26.43 | 20.25 | ||||||||||||

|

September 30

|

7.00 | 5.05 | 19.75 | 11.40 | ||||||||||||

|

December 31

|

6.74 | 5.04 | 11.50 | 4.25 | ||||||||||||

2

Guaranty Federal Bancshares, Inc.

2009 Annual Report

|

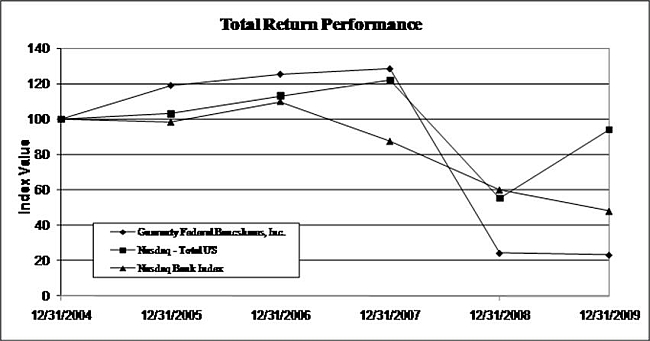

Set forth below is a stock performance graph comparing the cumulative total shareholder return on the Common Stock with (a) the cumulative total stockholder return on stocks included in The Nasdaq – Total U.S. Index and (b) the cumulative total stockholder return on stocks included in The Nasdaq Bank Index. All three investment comparisons assume the investment of $100 as of the close of business on December 31, 2004 and the hypothetical value of that investment as of the Company's fiscal years ended December 31, 2005, 2006, 2007, 2008, and 2009, assuming that all dividends were reinvested. The graph reflects the historical performance of the Common Stock, and, as a result, may not be indicative of possible future performance of the Common Stock. The data used to compile this graph was obtained from NASDAQ.

|

|

Period Ending

|

||||||||||||||||||||||||

|

Index

|

12/31/04

|

12/31/05

|

12/31/06

|

12/31/07

|

12/31/08

|

12/31/09

|

||||||||||||||||||

|

Guaranty Federal Bancshares, Inc.

|

100.00 | 119.13 | 125.48 | 128.49 | 24.31 | 23.26 | ||||||||||||||||||

|

NASDAQ – Total US

|

100.00 | 103.01 | 113.10 | 121.91 | 55.28 | 94.16 | ||||||||||||||||||

|

NASDAQ Bank Index

|

100.00 | 98.21 | 109.88 | 87.40 | 59.99 | 48.02 | ||||||||||||||||||

3

Guaranty Federal Bancshares, Inc.

Selected Consolidated Financial and Other Data

The following tables include certain information concerning the financial position and results of operations of Guaranty Federal Bancshares, Inc. (including consolidated data from operations of the Bank) as of the dates indicated. Dollar amounts are expressed in thousands except per share data.

|

Summary Balance Sheets

|

As of December 31,

|

|||||||||||||||||||

|

2009

|

2008

|

2007

|

2006

|

2005

|

||||||||||||||||

|

ASSETS

|

||||||||||||||||||||

|

Cash and cash equivalents

|

$ | 33,017 | $ | 15,097 | $ | 12,046 | $ | 14,881 | $ | 20,506 | ||||||||||

|

Investments and interest-bearing deposits

|

119,693 | 66,062 | 15,385 | 8,669 | 7,702 | |||||||||||||||

|

Loans receivable, net

|

528,503 | 558,327 | 516,242 | 480,269 | 435,528 | |||||||||||||||

|

Accrued interest receivable

|

2,671 | 2,632 | 3,323 | 2,910 | 2,089 | |||||||||||||||

|

Prepaids and other assets

|

25,249 | 16,573 | 8,613 | 10,075 | 7,696 | |||||||||||||||

|

Foreclosed assets

|

6,760 | 5,655 | 727 | 173 | 27 | |||||||||||||||

|

Premises and equipment

|

11,818 | 11,324 | 9,442 | 7,868 | 7,453 | |||||||||||||||

|

Bank owned life insurance

|

10,069 | - | - | - | - | |||||||||||||||

| $ | 737,780 | $ | 675,670 | $ | 565,778 | $ | 524,845 | $ | 481,001 | |||||||||||

|

LIABILITIES

|

||||||||||||||||||||

|

Deposits

|

$ | 513,051 | $ | 447,079 | $ | 418,191 | $ | 352,230 | $ | 320,059 | ||||||||||

|

Federal Home Loan Bank advances

|

116,050 | 132,436 | 76,086 | 108,000 | 100,000 | |||||||||||||||

|

Securities sold under agreements to repurchase

|

39,750 | 39,750 | 9,849 | 1,703 | 1,594 | |||||||||||||||

|

Subordinated debentures

|

15,465 | 15,465 | 15,465 | 15,465 | 15,465 | |||||||||||||||

|

Other liabilities

|

2,053 | 3,627 | 3,500 | 2,548 | 1,791 | |||||||||||||||

| 686,369 | 638,357 | 523,091 | 479,946 | 438,909 | ||||||||||||||||

|

STOCKHOLDERS' EQUITY

|

51,411 | 37,313 | 42,687 | 44,899 | 42,092 | |||||||||||||||

| $ | 737,780 | $ | 675,670 | $ | 565,778 | $ | 524,845 | $ | 481,001 | |||||||||||

|

Supplemental Data

|

As of December 31,

|

|||||||||||||||||||

| 2009 | 2008 | 2007 | 2006 | 2005 | ||||||||||||||||

|

Number of full-service offices

|

9 | 10 | 8 | 8 | 7 | |||||||||||||||

|

Cash dividends per common share

|

$ | - | $ | 0.36 | $ | 0.70 | $ | 0.67 | $ | 0.65 | ||||||||||

|

Summary Statements of Operations

|

Years ended December 31,

|

|||||||||||||||||||

|

2009

|

2008

|

2007

|

2006

|

2005

|

||||||||||||||||

|

Interest income

|

$ | 33,873 | $ | 36,363 | $ | 37,972 | $ | 35,204 | $ | 27,413 | ||||||||||

|

Interest expense

|

20,527 | 19,524 | 20,519 | 17,386 | 11,860 | |||||||||||||||

|

Net interest income

|

13,346 | 16,839 | 17,453 | 17,818 | 15,553 | |||||||||||||||

|

Provision for loan losses

|

6,900 | 14,744 | 840 | 750 | 945 | |||||||||||||||

|

Net interest income after provision for loan losses

|

6,446 | 2,095 | 16,613 | 17,068 | 14,608 | |||||||||||||||

|

Noninterest income

|

4,288 | 2,316 | 4,729 | 3,660 | 3,468 | |||||||||||||||

|

Noninterest expense

|

14,710 | 12,760 | 11,842 | 10,177 | 8,670 | |||||||||||||||

|

Income (loss) before income taxes

|

(3,976 | ) | (8,349 | ) | 9,500 | 10,551 | 9,406 | |||||||||||||

|

Provision (credit) for income taxes

|

(1,635 | ) | (2,989 | ) | 3,400 | 4,042 | 3,507 | |||||||||||||

|

Net income (loss)

|

$ | (2,341 | ) | $ | (5,360 | ) | $ | 6,100 | $ | 6,509 | $ | 5,899 | ||||||||

|

Preferred stock dividends and discount accretion

|

1,032 | - | - | - | - | |||||||||||||||

|

Net income (loss) available to common shareholders

|

$ | (3,373 | ) | $ | (5,360 | ) | $ | 6,100 | $ | 6,509 | $ | 5,899 | ||||||||

|

Basic income (loss) per common share

|

$ | (1.29 | ) | $ | (2.06 | ) | $ | 2.25 | $ | 2.34 | $ | 2.12 | ||||||||

|

Diluted income (loss) per common share

|

$ | (1.29 | ) | $ | (2.06 | ) | $ | 2.19 | $ | 2.25 | $ | 2.03 | ||||||||

4

Guaranty Federal Bancshares, Inc.

Management's Discussion and Analysis of Financial Condition and Results of Operations

GENERAL

Guaranty Federal Bancshares, Inc. (the "Company") is a Delaware corporation organized on December 30, 1997 that operates as a one-bank holding company. The Bank is a wholly-owned subsidiary of the Company.

The primary activity of the Company is to oversee its investment in the Bank. The Company engages in few other activities, and the Company has no significant assets other than its investment in the Bank. For this reason, unless otherwise specified, references to the Company include the operations of the Bank. The Company's principal business consists of attracting deposits from the general public and using such deposits to originate multi-family, construction and commercial real estate loans, mortgage loans secured by one- to four-family residences, and consumer and business loans. The Company also uses these funds to purchase government sponsored mortgage-backed securities, US government and agency obligations, and other permissible securities. When cash outflows exceed inflows, the Company uses borrowings and brokered deposits as additional financing sources.

The Company derives revenues principally from interest earned on loans and investments and, to a lesser extent, from fees charged for services. General economic conditions and policies of the financial institution regulatory agencies, including the Missouri Division of Finance and the Federal Deposit Insurance Corporation ("FDIC") significantly influence the Company's operations. Interest rates on competing investments and general market interest rates influence the Company's cost of funds. Lending activities are affected by the interest rates at which such financing may be offered. The Company intends to focus on commercial, one- to four-family residential and consumer lending throughout southwestern Missouri.

The Company has two wholly-owned subsidiaries other than the Bank, its principal subsidiary: (i) Guaranty Statutory Trust I, a Delaware statutory trust; and (ii) Guaranty Statutory Trust II, a Delaware statutory trust. These Trusts were formed in December 2005 for the exclusive purpose of issuing trust preferred securities to acquire junior subordinated debentures issued by the Company. The Company's banking operation conducted through the Bank is the Company's only reportable segment. See also the discussion contained in the section captioned "Segment Information" in Note 1 of the Notes to Consolidated Financial Statements in this report.

The discussion set forth below, and in any other portion of this report, may contain forward-looking statements. Such statements are based upon the information currently available to management of the Company and management's perception thereof as of the date of this report. When used in this document, words such as "anticipates," "estimates," "believes," "expects," and similar expressions are intended to identify forward-looking statements but are not the exclusive means of identifying such statements. Such statements are subject to risks and uncertainties. Actual results of the Company's operations could materially differ from those forward-looking comments. The differences could be caused by a number of factors or combination of factors including, but not limited to: changes in demand for banking services; changes in portfolio composition; changes in management strategy; increased competition from both bank and non-bank companies; changes in the general level of interest rates; and other factors set forth in reports and other documents filed by the Company with the Securities and Exchange Commission from time to time including the risk factors of the Company set forth in Item 1A. of the Company's Form 10-K.

FINANCIAL CONDITION

From December 31, 2008 to December 31, 2009, the Company's total assets increased $62,109,459 (9%) to $737,779,852, liabilities increased $48,011,728 (8%) to $686,369,219, and stockholders' equity increased $14,097,731 (38%) to $51,410,633. The ratio of stockholders' equity to total assets increased to 7.0% during this period, compared to 5.5% as of December 31, 2008.

From December 31, 2008 to December 31, 2009, available-for-sale securities increased $37,153,912 (57%). The increase is primarily due to purchases of $82.8 million, offset by sales, maturities and principal repayments of $46.9 million. The purchases were made with funding provided by the Bank's money market deposit campaign and the decline in loan balances. See further explanation below. During fiscal year 2009, the Company sold various securities in its portfolio with a recognized gain of $689,769, including its remaining investment in the Federal Home Loan Mortgage Corporation (26,600 shares).

From December 31, 2008 to December 31, 2009, held-to-maturity securities decreased $83,682 (15%) to $472,783 due to principal repayments received during the year. Stock of the Federal Home Loan Bank of Des Moines ("FHLB") was decreased by $753,500 (11%) to $5,976,600 due to lower stock requirements necessary from the reduction in FHLB advances.

5

Guaranty Federal Bancshares, Inc.

Management's Discussion and Analysis of Financial Condition and Results of Operations

From December 31, 2008 to December 31, 2009, net loans receivable decreased by $31,355,190 (6%) to $525,038,053. During this period, permanent loans secured by both owner and non-owner occupied one to four unit residential real estate increased $919,960 (1%), multi-family permanent loans increased $2,741,088 (9%), construction loans decreased $63,493,411 (75%), permanent loans secured by commercial real estate increased $32,762,341 (16%), commercial loans decreased $3,970,483 (3%), and installment loans decreased $3,007,596 (12%).

As of December 31, 2009, management identified loans totaling $40,009,123 as impaired with a related allowance for loan losses of $7,240,708. Impaired loans increased by $120,458 during 2009, compared to the balance of $39,888,665 at December 31, 2008.

From December 31, 2008 to December 31, 2009, the allowance for loan losses decreased $2,652,369 to $14,076,123. In addition to the provision for loan loss of $6,900,000 recorded by the Company during the year ended December 31, 2009, loan charge-offs exceeded recoveries by $9,552,369 for the twelve months ended December 31, 2009. The allowance for loan losses as of December 31, 2009 and December 31, 2008 was 2.61% and 2.92% of gross loans outstanding (excluding mortgage loans held for sale), respectively. As of December 31, 2009, the allowance for loan losses was 35% of impaired loans versus 42% as of December 31, 2008. Management believes the allowance for loan losses is at a level to be sufficient in providing for potential loan losses in the Bank's existing loan portfolio.

From December 31, 2008 to December 31, 2009, prepaid expense and other assets increased $2,666,050 (66%) to $6,731,409. The change was primarily due to purchases of tax credit investments (for future federal tax benefit) of $3.4 million.

As of December 31, 2009, prepaid FDIC deposit insurance premiums of $4,135,875 consisted of insurance assessments paid for fiscal years 2010, 2011 and 2012. In November 2009, the FDIC adopted a final rule to collect, in advance, all estimated premiums for these years in lieu of another special assessment, as was done for the June 30, 2009 quarter end.

As of December 31, 2009, foreclosed assets held for sale consisted primarily of real estate related to single family residences and one commercial development in Northwest Arkansas of $3.7 million.

From December 31, 2008 to December 31, 2009, premises and equipment increased $494,053 (4%) to $11,817,516 due to purchases of $1.5 million for the Company's new operations center and a branch remodel. These purchases were offset by depreciation of $965,504 in 2009.

From December 31, 2008 to December 31, 2009, bank owned life insurance increased $10,069,540 due to the Company's $10 million purchase of single premium life insurance on key members of management with the purpose of partially offsetting the Company's employee benefit costs as a whole. This purchase was completed on October 30, 2009.

From December 31, 2008 to December 31, 2009, deposits increased $65,971,633 (15%) to $513,051,102. During this period, checking and savings accounts increased by $160.5 million and certificates of deposit decreased by $94.5 million. The increase in the checking and savings accounts was due to the Bank's strong emphasis on increasing money market accounts through an aggressive deposit campaign. Management has implemented additional marketing efforts to obtain additional personal and commercial checking business from these customers. At December 31, 2009, included in the certificates of deposit totals are $19.8 million in deposits classified as "brokered", a decrease of $20.0 million from December 31, 2008.

From December 31, 2008 to December 31, 2009, the Company's borrowings from the FHLB decreased $16.4 million (12%) to $116,050,000, due to principal repayments during the period.

From December 31, 2008 to December 31, 2009, notes payable decreased $1.4 million (100%) due to the full repayment of the Company's notes payable during the period.

From December 31, 2008 to December 31, 2009, stockholders' equity (including unrealized appreciation on available-for-sale securities and interest rate swaps, net of tax) increased $14.1 million (38%) to $51,410,633. As a result of the Company's participation in the Department of the Treasury's Capital Purchase Program (CPP), stockholders' equity increased by $17 million during the period (See Note 15 to the Consolidated Financial Statements for further discussion). In addition, in conjunction with the preferred stock issued under the CPP, the Company has accrued a total of $779,167 of dividends (at 5%). The Company incurred a net loss for the year ended December 31, 2009 of $2,340,718. On a per common share basis, stockholders' equity decreased $.79 from $14.28 as of December 31, 2008 to $13.49 as of December 31, 2009.

6

Guaranty Federal Bancshares, Inc.

Management's Discussion and Analysis of Financial Condition and Results of Operations

AVERAGE BALANCES, INTEREST AND AVERAGE YIELDS

The following table shows the balances as of December 31, 2009 of various categories of interest-earning assets and interest-bearing liabilities and the corresponding yields and costs, and, for the periods indicated: (1) the average balances of various categories of interest-earning assets and interest-bearing liabilities, (2) the total interest earned or paid thereon, and (3) the resulting weighted average yields and costs. In addition, the table shows the Company's rate spreads and net yields. Average balances are based on daily balances. Tax-free income is not material; accordingly, interest income and related average yields have not been calculated on a tax equivalent basis. Average loan balances include non-accrual loans. Dollar amounts are expressed in thousands.

|

As of

|

Year Ended

|

Year Ended

|

Year Ended

|

|||||||||||||||||||||||||||||||||||||||||

|

December 31, 2009

|

December 31, 2009

|

December 31, 2008

|

December 31, 2007

|

|||||||||||||||||||||||||||||||||||||||||

|

Balance

|

Yield / Cost

|

Average Balance

|

Interest

|

Yield / Cost

|

Average Balance

|

Interest

|

Yield / Cost

|

Average Balance

|

Interest

|

Yield / Cost

|

||||||||||||||||||||||||||||||||||

|

ASSETS

|

||||||||||||||||||||||||||||||||||||||||||||

|

Interest-earning:

|

||||||||||||||||||||||||||||||||||||||||||||

|

Loans

|

$ | 542,579 | 5.53 | % | $ | 548,847 | $ | 29,695 | 5.41 | % | $ | 555,828 | $ | 33,019 | 5.94 | % | $ | 482,806 | $ | 37,114 | 7.69 | % | ||||||||||||||||||||||

|

Investment securities

|

103,132 | 2.95 | % | 102,096 | 3,744 | 3.67 | % | 58,727 | 3,125 | 5.32 | % | 10,688 | 537 | 5.02 | % | |||||||||||||||||||||||||||||

|

Other assets

|

51,079 | 0.93 | % | 65,853 | 434 | 0.66 | % | 7,869 | 219 | 2.78 | % | 7,372 | 321 | 4.35 | % | |||||||||||||||||||||||||||||

|

Total interest-earning

|

696,790 | 4.81 | % | 716,796 | 33,873 | 4.73 | % | 622,424 | 36,363 | 5.84 | % | 500,866 | 37,972 | 7.58 | % | |||||||||||||||||||||||||||||

|

Noninterest-earning

|

40,990 | 25,294 | 24,092 | 18,730 | ||||||||||||||||||||||||||||||||||||||||

| $ | 737,780 | $ | 742,090 | $ | 646,516 | $ | 519,596 | |||||||||||||||||||||||||||||||||||||

|

LIABILITIES AND STOCKHOLDERS' EQUITY

|

||||||||||||||||||||||||||||||||||||||||||||

|

Interest-bearing:

|

||||||||||||||||||||||||||||||||||||||||||||

|

Savings accounts

|

$ | 14,644 | 0.99 | % | $ | 13,069 | $ | 121 | 0.93 | % | $ | 12,980 | $ | 143 | 1.10 | % | $ | 13,474 | $ | 320 | 2.37 | % | ||||||||||||||||||||||

|

Transaction accounts

|

255,420 | 2.88 | % | 215,494 | 6,152 | 2.85 | % | 102,341 | 1,806 | 1.76 | % | 100,689 | 2,940 | 2.92 | % | |||||||||||||||||||||||||||||

|

Certificates of deposit

|

214,056 | 3.01 | % | 262,719 | 9,108 | 3.47 | % | 285,845 | 12,270 | 4.29 | % | 246,785 | 12,600 | 5.11 | % | |||||||||||||||||||||||||||||

|

FHLB advances

|

116,050 | 2.72 | % | 112,851 | 3,152 | 2.79 | % | 119,957 | 3,238 | 2.70 | % | 65,575 | 3,470 | 5.29 | % | |||||||||||||||||||||||||||||

|

Subordinated debentures

|

15,465 | 6.62 | % | 15,465 | 1,024 | 6.62 | % | 15,465 | 1,024 | 6.62 | % | 15,465 | 1,024 | 6.62 | % | |||||||||||||||||||||||||||||

|

Other borrowed funds

|

39,750 | 2.91 | % | 39,750 | 970 | 2.44 | % | 38,604 | 1,043 | 2.70 | % | 3,691 | 165 | 4.47 | % | |||||||||||||||||||||||||||||

|

Total interest-bearing

|

655,385 | 2.94 | % | 659,348 | 20,527 | 3.11 | % | 575,192 | 19,524 | 3.39 | % | 445,679 | 20,519 | 4.60 | % | |||||||||||||||||||||||||||||

|

Noninterest-bearing

|

30,984 | 30,467 | 30,516 | 28,401 | ||||||||||||||||||||||||||||||||||||||||

|

Total liabilities

|

686,369 | 689,815 | 605,708 | 474,080 | ||||||||||||||||||||||||||||||||||||||||

|

Stockholders' equity

|

51,411 | 52,275 | 40,808 | 45,516 | ||||||||||||||||||||||||||||||||||||||||

| $ | 737,780 | $ | 742,090 | $ | 646,516 | $ | 519,596 | |||||||||||||||||||||||||||||||||||||

|

Net earning balance

|

$ | 41,405 | $ | 57,448 | $ | 47,232 | $ | 55,187 | ||||||||||||||||||||||||||||||||||||

|

Earning yield less costing rate

|

1.87 | % | 1.62 | % | 2.45 | % | 2.98 | % | ||||||||||||||||||||||||||||||||||||

|

Net interest income, and net yield spread on interest-earning assets

|

$ | 13,346 | 1.86 | % | $ | 16,839 | 2.71 | % | $ | 17,453 | 3.48 | % | ||||||||||||||||||||||||||||||||

|

Ratio of interest-earning assets to interest-bearing liabilities

|

106 | % | 109 | % | 108 | % | 112 | % | ||||||||||||||||||||||||||||||||||||

7

Guaranty Federal Bancshares, Inc.

Management's Discussion and Analysis of Financial Condition and Results of Operations

The following table sets forth information regarding changes in interest income and interest expense for the periods indicated resulting from changes in average balances and average rates shown in the previous table. For each category of interest-earning assets and interest-bearing liabilities information is provided with respect to changes attributable to: (i) changes in balance (change in balance multiplied by the old rate), (ii) changes in interest rates (change in rate multiplied by the old balance); and (iii) the combined effect of changes in balance and interest rates (change in balance multiplied by change in rate). Dollar amounts are expressed in thousands.

|

Year ended

|

Year ended

|

|||||||||||||||||||||||||||||||

|

December 31, 2009 versus December 31, 2008

|

December 31, 2008 versus December 31, 2007

|

|||||||||||||||||||||||||||||||

|

Average Balance

|

Interest Rate

|

Rate & Balance

|

Total

|

Average Balance

|

Interest Rate

|

Rate & Balance

|

Total

|

|||||||||||||||||||||||||

|

Interest income:

|

||||||||||||||||||||||||||||||||

|

Loans

|

$ | (415 | ) | $ | (2,946 | ) | $ | 37 | $ | (3,324 | ) | $ | 5,613 | $ | (8,433 | ) | $ | (1,275 | ) | $ | (4,095 | ) | ||||||||||

|

Investment securities

|

2,308 | (972 | ) | (717 | ) | 619 | 2,414 | 32 | 142 | 2,588 | ||||||||||||||||||||||

|

Other assets

|

1,614 | (167 | ) | (1,232 | ) | 215 | 22 | (116 | ) | (8 | ) | (102 | ) | |||||||||||||||||||

|

Net change in interest income

|

3,507 | (4,085 | ) | (1,912 | ) | (2,490 | ) | 8,049 | (8,517 | ) | (1,141 | ) | (1,609 | ) | ||||||||||||||||||

|

Interest expense:

|

||||||||||||||||||||||||||||||||

|

Savings accounts

|

1 | (23 | ) | - | (22 | ) | (12 | ) | (171 | ) | 6 | (177 | ) | |||||||||||||||||||

|

Transaction accounts

|

1,997 | 1,115 | 1,234 | 4,346 | 48 | (1,163 | ) | (19 | ) | (1,134 | ) | |||||||||||||||||||||

|

Certificates of deposit

|

(993 | ) | (2,360 | ) | 191 | (3,162 | ) | 1,994 | (2,006 | ) | (318 | ) | (330 | ) | ||||||||||||||||||

|

FHLB advances

|

(192 | ) | 113 | (7 | ) | (86 | ) | 2,878 | (1,700 | ) | (1,410 | ) | (232 | ) | ||||||||||||||||||

|

Subordinated debentures

|

- | - | - | - | - | - | - | - | ||||||||||||||||||||||||

|

Other borrowed funds

|

31 | (101 | ) | (3 | ) | (73 | ) | 1,561 | (65 | ) | (618 | ) | 878 | |||||||||||||||||||

|

Net change in interest expense

|

844 | (1,256 | ) | 1,415 | 1,003 | 6,469 | (5,105 | ) | (2,359 | ) | (995 | ) | ||||||||||||||||||||

|

Change in net interest income

|

$ | 2,663 | $ | (2,829 | ) | $ | (3,327 | ) | $ | (3,493 | ) | $ | 1,580 | $ | (3,412 | ) | $ | 1,218 | $ | (614 | ) | |||||||||||

RESULTS OF OPERATIONS - COMPARISON OF YEAR ENDED DECEMBER 31, 2009 AND DECEMBER 31, 2008

|

Average for the Year Shown

|

||||||||||||

|

Prime

|

Ten-Year Treasury

|

One-Year Treasury

|

||||||||||

|

December 31, 2009

|

3.25 | % | 3.26 | % | 0.47 | % | ||||||

|

December 31, 2008

|

5.09 | % | 3.66 | % | 1.83 | % | ||||||

|

Change in rates

|

-1.84 | % | -0.40 | % | -1.36 | % | ||||||

Interest Rates. The Bank charges borrowers and pays depositors interest rates that are largely a function of the general level of interest rates. The above table sets forth the weekly average interest rates for the 52 weeks ending December 31, 2009 and December 31, 2008 as reported by the Federal Reserve. The Bank typically indexes its adjustable rate commercial loans to prime and its adjustable rate mortgage loans to the one-year treasury rate. The ten-year treasury rate is a proxy for 30-year fixed rate home mortgage loans.

Rates were steady and remained low for 2009 as the Federal Reserve Open Market Committee ("FOMC") left the discount rate at 25 basis points. As of December 31, 2009, the prime rate was 3.25% and unchanged from December 31, 2008.

Interest Income. Total interest income decreased $2,489,956 (7%). The average balance of interest-earning assets increased $94,372,000 (15%) while the yield on average interest earning assets decreased 111 basis points to 4.73%.

8

Guaranty Federal Bancshares, Inc.

Management's Discussion and Analysis of Financial Condition and Results of Operations

The impact of the Federal Reserve's interest rate cuts throughout 2008 adversely impacted the Bank's loan portfolio in 2009, specifically those loans which are directly tied to the prime rate. Interest on loans decreased $3,323,730 (10%) and the average loan receivable balance decreased $6,981,000 (1%) while the average yield decreased 53 basis points to 5.41%. Another factor that has impacted the Company's yield on loans is the level of nonaccrual loans which has increased to $34.3 million as of December 31, 2009, as compared to $20.7 million as of December 31, 2008. Also, during 2009, the Company increased its investment securities and interest-bearing deposits during the year which, because of the low rate environment for investment yields, decreased the average yield on investment securities by 165 basis points as compared to fiscal year 2008.

Interest Expense. Total interest expense increased $1,002,361 (5%) as the average balance of interest-bearing liabilities increased $84,156,000 (15%) while the average cost of interest-bearing liabilities decreased 28 basis points to 3.11%.

The primary increase in interest-bearing liabilities was due to the Bank's strong emphasis on increasing money market accounts through an aggressive deposit campaign. This initiative to improve core deposit liquidity has increased the Bank's interest expense on deposits. Interest expense on deposits increased $1,161,458 (8%) during 2009 as the average balance of interest bearing deposits increased $90,116,000 (22%), but the average interest rate paid to depositors decreased 41 basis points to 3.13%.

The average balance of FHLB advances decreased $7,106,000 (6%) while the average cost of those advances increased 9 basis points to 2.79%. As a result, interest expense on these advances decreased $85,135 (3%). As of December 31, 2009, FHLB advances were 16% of total assets, compared to 20% of total assets as of December 31, 2008.

Net Interest Income. The Company's net interest income decreased $3,492,317 (21%). During the year ended December 31, 2009, the average balance of interest-earning assets exceeded the average balance of interest-bearing liabilities by $57,448,000, resulting in an increase in the average net earning balance of $10,216,000 (22%). In addition, the Company's spread between the average yield on interest-earning assets and the average cost of interest-bearing liabilities decreased by 83 basis points from 2.45% to 1.62%.

Provision for Loan Losses. Provisions for loan losses are charged or credited to earnings to bring the total allowance for loan losses to a level considered adequate by the Company to provide for potential loan losses in the existing loan portfolio. When making its assessment, the Company considers prior loss experience, volume and type of lending, local banking trends and past due loans in the Company's loan portfolio. In addition, the Company considers general economic conditions and other factors related to collectibility of the Company's loan portfolio.

Based on its internal analysis and methodology, management recorded a provision for loan losses of $6,900,000 and $14,744,079 for the years ended December 31, 2009 and 2008, respectively. Provisions recorded in 2009 are due to the Bank's charge-offs during the year, increases in nonperforming loans, continuing concerns over the local and national economy and certain specific borrowers. However, despite growing nonperforming loan balances during 2009, the Company has experienced a significant decline in overall loan balances as of December 31, 2009, as compared to December 31, 2008 (a decline of $32.5 million or 6%). The Company has also experienced lower reserve requirements on newly classified nonperforming credits during the year ended December 31, 2009 and this is reflected in a lower provision requirement for fiscal year 2009, as compared to fiscal year 2008.

The Bank will continue to monitor its allowance for loan losses and make future additions based on economic and regulatory conditions. Management of the Company anticipates the need to continue increasing the allowance for loan losses through charges to the provision for loan losses if growth in the Bank's loan portfolio is experienced or other circumstances warrant. Although the Bank maintains its allowance for loan losses at a level which it considers to be sufficient to provide for potential loan losses in its existing loan portfolio, there can be no assurance that future loan losses will not exceed internal estimates. In addition, the amount of the allowance for loan losses is subject to review by regulatory agencies which can order the establishment of additional loan loss provisions.

Non-Interest Income. Non-interest income increased $1,971,343 (85%). The gain on sale of loans of $1,443,385 for 2009, compared to $875,010 for 2008, was the result of mortgage banking activities related to the sale of single-family conforming residential loans in the secondary market. The Bank attempts to minimize its risk of price changes by committing to sell loans while the loans are in the origination process. Gains on investment securities for the year ended December 31, 2009 were $689,769, compared to a loss of $563,615 for the year ended December 31, 2008. The gains in fiscal 2009 were due to the Company recognizing certain gains in its available-for-sale portfolio to reduce potential credit and interest rate risk issues. The losses in fiscal 2008 were attributable to other-than-temporary impairment charges on its equity securities associated with companies operating in the financial sector. Deposit service charges decreased $225,403 (11%) due primarily to declines in overdraft charges. Loss on foreclosed assets decreased $260,274 (33%) in 2009, but remained elevated primarily due to the difficult market conditions causing sharp declines in real estate values on foreclosed properties held or sold by the Company.

9

Guaranty Federal Bancshares, Inc.

Management's Discussion and Analysis of Financial Condition and Results of Operations

Non-Interest Expense. Non-interest expense increased $1,949,873 (15%). This increase was primarily due to increases in salaries and employee benefits of $434,820 (6%) and FDIC deposit insurance premiums of $1,135,555 (295%).

The increase in compensation was due to additions in several key managerial positions in the areas of commercial lending, credit administration, finance and risk management. However, overall staff decreased from 163 full-time equivalent employees as of December 31, 2008 to 162 full-time equivalent employees as of December 31, 2009.

Increases in FDIC deposit insurance premiums were due to increases in premium rates that began in the first quarter of 2009 and the special assessment that was incurred as of June 30, 2009, and was paid on September 30, 2009.

Income Taxes. The credit for income taxes is a direct result of the Company's taxable loss for the year ended December 31, 2009.

Cash Dividends Paid. The Company did not pay dividends on its common shares during 2009. During 2009, the Company paid $672,917 in dividends on its preferred stock issued under the CPP.

RESULTS OF OPERATIONS - COMPARISON OF YEAR ENDED DECEMBER 31, 2008 AND DECEMBER 31, 2007

|

Average for the Year Shown

|

||||||||||||

|

Prime

|

Ten-Year Treasury

|

One-Year Treasury

|

||||||||||

|

December 31, 2008

|

5.09 | % | 3.66 | % | 1.83 | % | ||||||

|

December 31, 2007

|

8.05 | % | 4.63 | % | 4.53 | % | ||||||

|

Change in rates

|

-2.96 | % | -0.97 | % | -2.70 | % | ||||||

Interest Rates. The above table sets forth the weekly average interest rates for the 52 weeks ending December 31, 2008 and December 31, 2007 as reported by the Federal Reserve.

Rates were steady for the first eight months of 2007, but due to several economic factors, the FOMC began decreasing the discount rate at its September 2007 meeting and continued for each meeting thereafter in 2007. The FOMC continued its aggressive easing of rates in the first quarter of 2008 and then again in the fourth quarter. As of December 31, 2008, the prime rate was 3.25%.

Interest Income. Total interest income decreased $1,609,148 (4%). The average balance of interest-earning assets increased $121,558,000 (24%) while the yield on average interest earning assets decreased 174 basis points to 5.84%.

Interest on loans decreased $4,094,632 (11%) and the average loan receivable balance increased $73,022,000 (15%) while the average yield decreased 175 basis points to 5.94%.

10

Guaranty Federal Bancshares, Inc.

Management's Discussion and Analysis of Financial Condition and Results of Operations

Interest Expense. Total interest expense decreased $995,079 (5%) as the average balance of interest-bearing liabilities increased $129,513,000 (29%) while the average cost of interest-bearing liabilities decreased 121 basis points to 3.39%.

Interest expense on deposits decreased $1,641,062 (10%) as the average balance of interest bearing deposits increased $40,218,000 (11%) and the average interest rate paid to depositors decreased 88 basis points to 3.52%.

The average balance of advances increased $54,382,000 (83%) and the average cost of those advances decreased 259 basis points to 2.70%. As a result, interest expense on these advances decreased $232,062 (7%). As of December 31, 2008 FHLB advances were 20% of total assets, compared to 13% of total assets as of December 31, 2007.

Net Interest Income. The Company's net interest income decreased $614,069 (4%). During the year ended December 31, 2008, the average balance of interest-earning assets exceeded the average balance of interest-bearing liabilities by $47,232,000, resulting in a decrease in the average net earning balance of $7,955,000 (14%). In addition, the Company's spread between the average yield on interest-earning assets and the average cost of interest-bearing liabilities decreased by 53 basis points from 2.98% to 2.45%.

Provision for Loan Losses. Provisions for loan losses are charged or credited to earnings to bring the total allowance for loan losses to a level considered adequate by the Company to provide for potential loan losses in the existing loan portfolio. When making its assessment, the Company considers prior loss experience, volume and type of lending, local banking trends and past due loans in the Company's loan portfolio. In addition, the Company considers general economic conditions and other factors related to collectibility of the Company's loan portfolio.

During the year ended December 31, 2008, the Company experienced loan charge-offs, in excess of recoveries, of $3,978,510 and, based on a review as discussed above, elected to record a provision for loan loss of $14,744,079 to increase the allowance for loan losses to $16,728,492 as of December 31, 2008. The provision for loan losses recorded by the Company during year ended December 31, 2007 was $840,000. The increase in the provision for loan losses was due primarily to the significant increase in impaired and nonperforming loans during 2008. Management of the Company anticipates the need to continue increasing the loan loss allowance in the future through charges to provision for loan losses based on potential increases in problem credits, any growth in its loan portfolio or other circumstances.

Non-Interest Income. Non-interest income decreased $2,412,416 (51%). The gain on sale of loans of $875,010 for 2008, compared to $1,177,017 for 2007, was the result of mortgage banking activities related to the sale of single-family conforming residential loans in the secondary market. The Bank attempts to minimize its risk of price changes by committing to sell loans while the loans are in the origination process. The loss on investments for the year ended December 31, 2008 was $563,615, compared to a gain of $618,363 for the year ended December 31, 2007. The losses in fiscal 2008 were attributable to other-than-temporary impairment charges on its equity securities associated with companies operating in the financial sector. The gains recognized in 2007 were solely due to the sale of shares in FHLMC stock. The Company suspended its sale of its shares in FHLMC stock in the fourth quarter of 2007 due to its significant financial downturn and a sharp decline in the FHLMC stock price. Deposit service charges decreased $187,950 (8%) due primarily to declines in overdraft charges. Loss on foreclosed assets increased $741,922 (1,770%) primarily due to the difficult market conditions causing sharp declines in real estate values on foreclosed properties held or sold by the Company.

Non-Interest Expense. Non-interest expense increased $917,659 (8%). This increase was primarily due to increases in salaries and employee benefits of $443,036 (6%) and FDIC deposit insurance premiums of $342,441 (805%).

The increase in compensation was due to additions in several staff positions in the areas of commercial lending, corporate services, human resources and internal audit with the majority of these new hires beginning in fiscal 2008 or late in fiscal 2007. The staff increased from 150 full-time equivalent employees as of December 31, 2007 to 163 full-time equivalent employees as of December 31, 2008.

11

Guaranty Federal Bancshares, Inc.

Management's Discussion and Analysis of Financial Condition and Results of Operations

Increases in FDIC premiums were due to insurance assessments that began in 2007. Because of credits available to the Company for 2007, these increased costs were not owed by the Company until the first quarter of 2008.

Income Taxes. The credit for income taxes is a direct result of the decrease in the Company's taxable income for the year ended December 31, 2008 as compared to the year ended December 31, 2007.

Cash Dividends Paid. The Company paid dividends of $0.18 per share on April 18, 2008, to stockholders of record as of April 7, 2008, and $0.18 per share on July 18, 2008 to stockholders of record as of July 7, 2008.

ASSET / LIABILITY MANAGEMENT

The goal of the Bank's asset/liability policy is to manage interest rate risk so as to maximize net interest income over time in changing interest rate environments. Management monitors the Bank's net interest spreads (the difference between yields received on assets and paid on liabilities) and, although constrained by market conditions, economic conditions, and prudent underwriting standards, it offers deposit rates and loan rates that maximize net interest income. Management also attempts to fund the Bank's assets with liabilities of a comparable duration to minimize the impact of changing interest rates on the Bank's net interest income. Since the relative spread between financial assets and liabilities is constantly changing, the Bank's current net interest income may not be an indication of future net interest income.

The Bank has continued to emphasize the origination of short-term commercial real estate, construction, commercial business, home equity, consumer and adjustable-rate, one- to four-family residential loans while originating fixed-rate, one- to four-family residential loans primarily for immediate resale in the secondary market.

The Bank constantly monitors its deposits in an effort to decrease their interest rate sensitivity. Rates of interest paid on deposits at the Bank are priced competitively in order to meet the Bank's asset/liability management objectives and spread requirements. As of December 31, 2009 and 2008, the Bank's savings accounts, checking accounts, and money market deposit accounts totaled $298,995,433 or 58% of its total deposits and $138,504,922 or 31% of total deposits, respectively. The weighted average rate paid on these accounts increased 136 basis points from 1.13% on December 31, 2008 to 2.49% on December 31, 2009 primarily due to the Bank's money market deposit campaign. The Bank expects to have the ability to significantly reduce the rate paid on these accounts in 2010 while closely monitoring its liquidity position. The Bank believes, based on historical experience, that a significant portion of such accounts represents non-interest rate sensitive core deposits. The Bank does believe that certain accounts generated from the 2009 money market deposit campaign to be interest rate sensitive, however, the Bank does not have the historical experience with this type of campaign to predict fluctuations based on expected rate reductions.

INTEREST RATE SENSITIVITY ANALYSIS

The following table sets forth as of December 31, 2009, management's estimates of the projected changes in net portfolio value ("NPV") in the event of instantaneous and permanent increases and decreases in market interest rates. Dollar amounts are expressed in thousands.

|

BP Change

|

Estimated Net Portfolio Value

|

NPV as % of PV of Assets

|

|||||||||||||||||||

|

in Rates

|

$ Amount

|

$ Change

|

% Change

|

NPV Ratio

|

Change

|

||||||||||||||||

| +300 | 57,416 | (2,520 | ) | -4 | % | 8.01 | % | -0.10 | % | ||||||||||||

| +200 | 58,222 | (1,714 | ) | -3 | % | 8.04 | % | -0.07 | % | ||||||||||||

| +100 | 58,996 | (940 | ) | -2 | % | 8.07 | % | -0.04 | % | ||||||||||||

|

NC

|

59,936 | - | 0 | % | 8.11 | % | 0.00 | % | |||||||||||||

| -100 | 61,320 | 1,384 | 2 | % | 8.20 | % | 0.09 | % | |||||||||||||

| -200 | 64,410 | 4,474 | 7 | % | 8.52 | % | 0.41 | % | |||||||||||||

Computations of prospective effects of hypothetical interest rate changes are based on an internally generated model using actual maturity and repricing schedules for the Bank's loans and deposits, and are based on numerous assumptions, including relative levels of market interest rates, loan repayments and deposit run-offs, and should not be relied upon as indicative of actual results. Further, the computations do not contemplate any actions the Bank may undertake in response to changes in interest rates.

12

Guaranty Federal Bancshares, Inc.

Management's Discussion and Analysis of Financial Condition and Results of Operations

Management cannot predict future interest rates or their effect on the Bank's NPV in the future. Certain shortcomings are inherent in the method of analysis presented in the computation of NPV. For example, although certain assets and liabilities may have similar maturities or periods to repricing, they may react in differing degrees to changes in market interest rates. Additionally, certain assets, such as adjustable-rate loans, which represent the Bank's primary loan product, have an initial fixed rate period typically from one to five years and over the remaining life of the asset changes in the interest rate are restricted. In addition, the proportion of adjustable-rate loans in the Bank's loan portfolio could decrease in future periods due to refinancing activity if market interest rates remain constant or decrease in the future. Further, in the event of a change in interest rates, prepayment and early withdrawal levels could deviate significantly from those assumed in the table. Finally, the ability of many borrowers to service their adjustable-rate debt may decrease in the event of an interest rate increase.

The Bank's Board of Directors is responsible for reviewing the Bank's asset and liability policies. The Bank's management is responsible for administering the policies and determinations of the Board of Directors with respect to the Bank's asset and liability goals and strategies. Management expects that the Bank's asset and liability policies and strategies will continue as described above so long as competitive and regulatory conditions in the financial institution industry and market interest rates continue as they have in recent years.

LIQUIDITY AND CAPITAL RESOURCES

Liquidity refers to the ability to manage future cash flows to meet the needs of depositors and borrowers and fund operations. Maintaining appropriate levels of liquidity allows the Company to have sufficient funds available for customer demand for loans, withdrawal of deposit balances and maturities of deposits and other liabilities. The Company's primary sources of liquidity include cash and cash equivalents, customer deposits and FHLB borrowings. The Company also has established borrowing lines available from the Federal Reserve Bank which is considered a secondary source of funds.

The Company's most liquid assets are cash and cash equivalents, which are cash on hand, amounts due from financial institutions, and certificates of deposit with other financial institutions that have an original maturity of three months or less. The levels of such assets are dependent on the Bank's operating, financing, and investment activities at any given time. The Company's cash and cash equivalents totaled $33,016,697 as of December 31, 2009 and $15,097,015 as of December 31, 2008, representing an increase of $17,919,682. The Company's interest-bearing deposits totaled $16,560,802 as of December 31, 2009 and $0 as of December 31, 2008. The variations in levels of cash and cash equivalents are influenced by deposit flows and anticipated future deposit flows, which are subject to, and influenced by, many factors.

In addition to the capital necessary to meet the Company's conditional commitments discussed under the caption "Off-Balance Sheet Arrangements" below, the Bank also has $140,285,863 in certificates of deposit that are scheduled to mature in one year or less. Management anticipates that the majority of these certificates will renew in the normal course of operations. Based on existing collateral as well as the FHLB's limitation of advances to 30% of assets, the Bank has the ability to borrow an additional $41,549,000 from the FHLB, as of December 31, 2009. Based on existing collateral, the Bank has the ability to borrow $12,987,000 from the Federal Reserve Bank as of December 31, 2009. The Bank plans to maintain its FHLB and Federal Reserve Bank borrowings to a level that will provide a borrowing capacity sufficient to provide for contingencies.

The Company's Tier 1 capital position of $64,678,000 is 8.8% of average assets as of December 31, 2009. The Company has an excess of $35,324,000, $41,562,000, and $25,740,000 of required regulatory levels of tangible, core, and risk-based capital, respectively. In addition, under current regulatory guidelines, the Bank is classified as well capitalized. See also additional information provided under the caption "Regulatory Matters" in Note 1 of the Notes to Consolidated Financial Statements.

With regards to the securities sold to the Treasury under the CPP, if the Company is unable to redeem the Series A Preferred Stock within five years of its issuance, the cost of capital to the Company will increase significantly from 5% per annum ($850,000 annually) to 9% per annum ($1,530,000 annually). Depending on the Company's financial condition at the time, the increase in the annual dividend rate on the Series A Preferred Stock could have a material adverse effect on the Company's liquidity and net income available to common stockholders.

13

Guaranty Federal Bancshares, Inc.

Management's Discussion and Analysis of Financial Condition and Results of Operations

OFF-BALANCE SHEET ARRANGEMENTS

Various commitments and contingent liabilities arise in the normal course of business, which are not required to be recorded on the balance sheet. The most significant of these are loan commitments, lines of credit and standby letters of credit. Commitments to extend credit are agreements to lend to a customer as long as there is no violation of any condition established in the contract. As of December 31, 2009 and 2008, the Bank had outstanding commitments to originate loans of approximately $5,589,000 and $5,001,000, respectively. Lines of credit are agreements to lend to a customer as long as there is no violation of any condition established in the contract. As of December 31, 2009 and 2008, unused lines of credit to borrowers aggregated approximately $32,539,000 and $49,253,000 for commercial lines and $17,820,000 and $20,829,000 for open-end consumer lines. Since a portion of the loan commitment and line of credit may expire without being drawn upon, the total unused commitments and lines do not necessarily represent future cash requirements.

Standby letters of credit are irrevocable conditional commitments issued by the Bank to guarantee the performance of a customer to a third party. The credit risk involved in issuing standby letters of credit is essentially the same as that involved in extending loans to customers. The Bank had total outstanding standby letters of credit amounting to $15,623,000 and $15,059,000 as of December 31, 2009 and 2008, respectively. The commitments extend over varying periods of time.

In connection with the Company's issuance of the Trust Securities and pursuant to two guarantee agreements by and between the Company and Wilmington Trust Company, the Company issued a limited, irrevocable guarantee of the obligations of each Trust under the Trust Securities whereby the Company has guaranteed any and all payment obligations of the Trusts related to the Trust Securities including distributions on, and the liquidation or redemption price of, the Trust Securities to the extent each Trust does not have funds available.

AGGREGATE CONTRACTUAL OBLIGATIONS

The following table summarizes the Company's fixed and determinable contractual obligations by payment date as of December 31, 2009. Dollar amounts are expressed in thousands.

|

Payments Due By Period

|

||||||||||||||||||||

|

Contractual Obligations

|

Total

|

One Year or less

|

One to Three Years

|

Three to Five Years

|

More than Five Years

|

|||||||||||||||

|

Deposits without stated maturity

|

$ | 298,995 | 298,995 | - | - | - | ||||||||||||||

|

Time and brokered certificates of deposit

|

214,056 | 140,286 | 66,621 | 6,352 | 797 | |||||||||||||||

|

Other borrowings

|

39,750 | - | - | - | 39,750 | |||||||||||||||

|

Federal Home Loan Bank advances

|

116,050 | 23,000 | 25,000 | 15,700 | 52,350 | |||||||||||||||

|

Subordinated debentures

|

15,465 | - | - | - | 15,465 | |||||||||||||||

|

Operating leases

|

356 | 94 | 100 | 75 | 87 | |||||||||||||||

|

Purchase obligations

|

- | - | - | - | - | |||||||||||||||

|

Other long term obligations

|

248,671 | 248,671 | - | - | - | |||||||||||||||

|

Total

|

$ | 933,343 | 711,046 | 91,721 | 22,127 | 108,449 | ||||||||||||||

IMPACT OF INFLATION AND CHANGING PRICES

The Company prepared the consolidated financial statements and related data presented herein in accordance with accounting principles generally accepted in the United States of America which require the measurement of financial position and operating results in terms of historical dollars, without considering changes in the relative purchasing power of money over time due to inflation.

14

Guaranty Federal Bancshares, Inc.

Management's Discussion and Analysis of Financial Condition and Results of Operations

Unlike most companies, the assets and liabilities of a financial institution are primarily monetary in nature. As a result, interest rates have a more significant impact on a financial institution's performance than the effects of general levels of inflation. Interest rates do not necessarily move in the same direction or in the same magnitude as the price of goods and services, since such prices are affected by inflation. In the current interest rate environment, liquidity and the maturity structure of the Bank's assets and liabilities are critical to the maintenance of acceptable performance levels.

CRITICAL ACCOUNTING POLICIES

Management's Discussion and Analysis of Financial Condition and Results of Operations is based upon the Company's consolidated financial statements and the notes thereto, which have been prepared in accordance with accounting principles generally accepted in the United States of America. The preparation of these financial statements requires management to make estimates and judgments that affect the reported amounts of assets and liabilities and the disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reported periods. On an on-going basis, management evaluates its estimates and judgments.

Management bases its estimates and judgments on historical experience and on various other factors that are believed to be reasonable under the circumstances, the results of which form the basis for making judgments about the carrying values of assets and liabilities that are not readily apparent from other sources. There can be no assurance that actual results will not differ from those estimates. If actual results are different than management's judgements and estimates, the Company's financial results could change, and such change could be material to the Company.

Material estimates and judgments that are particularly susceptible to significant change relate to the determination of the allowance for loan losses. In connection with the determination of the allowance for loan losses, management obtains independent appraisals for significant properties.

The Company has identified the accounting policies for the allowance for loan losses and related significant estimates and judgments as critical to its business operations and the understanding of its results of operations. For a detailed discussion on the application of these significant estimates and judgments and our accounting policies, also see Note 1 of the notes to consolidated financial statements in this report.

IMPACT OF NEW ACCOUNTING PRONOUNCEMENTS

In June 2009, the Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) No. 2009-1 (formerly SFAS No. 168), "Topic 105 - Generally Accepted Accounting Principles - Accounting Standards Codification and the Hierarchy of Generally Accepted Principles." This standard establishes the FASB Accounting Standards Codification (ASC) as the single source of authoritative U.S. generally accepted accounting principles (GAAP) to be applied by nongovernmental entities. Rules and interpretative releases of the SEC under authority of federal securities laws are also sources of authoritative guidance for SEC registrants. The Codification does not change current GAAP, but is intended to simplify user access to all authoritative GAAP by providing all the authoritative literature related to a particular topic in one place. All non-grandfathered, non-SEC accounting literature not included in the Codification will become non-authoritative. The standard was effective for the third quarter of 2009 and did not have a material impact on the Company's consolidated financial statements. However, the appropriate changes to GAAP references have been made to the consolidated financial statements.

In June 2009, the FASB issued SFAS No. 167, "Amendments to FASB Interpretation No. 46R"(not yet reflected in FASB ASC). The standard amends FIN No. 46R to require a company to analyze whether its interest in a variable interest entity ("VIE") gives it a controlling financial interest. A company must assess whether it has an implicit financial responsibility to ensure that the VIE operates as designed when determining whether it has the power to direct the activities of the VIE that significantly impact its economic performance. Ongoing reassessments of whether a company is the primary beneficiary are also required by the standard. SFAS No. 167 amends the criteria to qualify as a primary beneficiary as well as how to determine the existence of a VIE. This Statement will be effective as of the beginning of each reporting entity's first annual reporting period that begins after November 15, 2009, for interim periods within the first annual reporting period, and for interim and annual reporting periods thereafter. Earlier application is not permitted.

15

Guaranty Federal Bancshares, Inc.

Management's Discussion and Analysis of Financial Condition and Results of Operations

In August 2009, the FASB issued ASU 2009-05, "Fair Value Measurements and Disclosures (Topic 820) – Measuring Liabilities at Fair Value" to provide guidance when estimating the fair value of a liability. When a quoted price in an active market for the identical liability is not available, fair value should be measured using:

|

·

|

the quoted price of an identical liability when traded as an asset,

|

|

·

|

quoted prices of similar liabilities or similar liabilities when traded as assets, or

|

|

·

|

another valuation technique consistent with the principles of Topic 820 such as an income approach or a market approach.

|

If a restriction exists that prevents the transfer of the liability, a separate adjustment related to the restriction is not required when estimating fair value. The ASU was effective for the Company on October 1, 2009. Its adoption had no material impact on the Company's consolidated financial statements.

SUMMARY OF UNAUDITED QUARTERLY OPERATING RESULTS

|

Year Ended December 31, 2009, Quarter ended

|

||||||||||||||||

|

Mar-09

|

Jun-09

|

Sep-09

|

Dec-09

|

|||||||||||||

|

Interest income

|

$ | 8,323,301 | $ | 8,504,112 | $ | 8,534,335 | $ | 8,511,688 | ||||||||

|

Interest expense

|

5,307,991 | 5,204,374 | 5,086,082 | 4,928,138 | ||||||||||||

|

Net interest income

|

3,015,310 | 3,299,738 | 3,448,253 | 3,583,550 | ||||||||||||

|

Provision for loan losses

|

980,000 | 3,300,000 | 670,000 | 1,950,000 | ||||||||||||

|

Gain on loans and investment securities

|

355,410 | 759,812 | 656,036 | 361,896 | ||||||||||||

|

Other noninterest income, net

|

453,562 | 762,651 | 674,332 | 263,795 | ||||||||||||

|

Noninterest expense

|

3,744,565 | 4,035,322 | 3,391,956 | 3,537,840 | ||||||||||||

|

Income (loss) before income taxes

|

(900,283 | ) | (2,513,121 | ) | 716,665 | (1,278,599 | ) | |||||||||

|

Provision (credit) for income taxes

|

(308,163 | ) | (881,039 | ) | 142,202 | (587,620 | ) | |||||||||

|

Net income (loss)

|

(592,120 | ) | (1,632,082 | ) | 574,463 | (690,979 | ) | |||||||||

|

Preferred stock dividends and discount accretion

|

187,594 | 281,390 | 281,391 | 281,391 | ||||||||||||

|

Net income (loss) available to common shareholders

|

$ | (779,714 | ) | $ | (1,913,472 | ) | $ | 293,072 | $ | (972,370 | ) | |||||

|

Basic earnings (loss) per share

|

$ | (0.30 | ) | $ | (0.73 | ) | $ | 0.11 | $ | (0.37 | ) | |||||

|

Diluted earnings (loss) per share

|

$ | (0.30 | ) | $ | (0.73 | ) | $ | 0.11 | $ | (0.37 | ) | |||||

|

Year Ended December 31, 2008, Quarter ended

|

||||||||||||||||

|

Mar-08

|

Jun-08

|

Sep-08

|

Dec-08

|

|||||||||||||

|

Interest income

|

$ | 9,231,033 | $ | 8,925,204 | $ | 9,267,799 | $ | 8,939,356 | ||||||||

|

Interest expense

|

5,201,066 | 4,811,710 | 4,747,203 | 4,764,245 | ||||||||||||

|

Net interest income

|

4,029,967 | 4,113,494 | 4,520,596 | 4,175,111 | ||||||||||||

|

Provision for loan losses

|

820,000 | 5,684,079 | 1,675,000 | 6,565,000 | ||||||||||||

|

Gain (loss) on sale of loans and investment securities

|

231,077 | 159,640 | 207,870 | (287,192 | ) | |||||||||||

|

Other noninterest income, net

|

650,774 | 660,770 | 641,024 | 52,188 | ||||||||||||

|

Noninterest expense

|

3,101,408 | 3,213,100 | 3,167,272 | 3,278,030 | ||||||||||||

|

Income (loss) before income taxes

|

990,410 | (3,963,275 | ) | 527,218 | (5,902,923 | ) | ||||||||||

|

Provision (credit) for income taxes

|

373,552 | (1,466,995 | ) | 227,759 | (2,123,175 | ) | ||||||||||

|

Net income (loss)

|

$ | 616,858 | $ | (2,496,280 | ) | $ | 299,459 | $ | (3,779,748 | ) | ||||||

|

Basic earnings (loss) per share

|

$ | 0.24 | $ | (0.96 | ) | $ | 0.11 | $ | (1.45 | ) | ||||||

|

Diluted earnings (loss) per share

|

$ | 0.23 | $ | (0.96 | ) | $ | 0.11 | $ | (1.45 | ) | ||||||

16

Guaranty Federal Bancshares, Inc.

Consolidated Balance Sheets

December 31, 2009 and 2008

|

December 31, 2009

|

December 31, 2008

|

|||||||

|

ASSETS

|

||||||||

|

Cash and due from banks

|

$ | 4,527,813 | $ | 3,826,567 | ||||

|

Interest-bearing deposits in other financial institutions

|

28,488,884 | 11,270,448 | ||||||

|

Cash and cash equivalents

|

33,016,697 | 15,097,015 | ||||||

|

Interest-bearing deposits

|

16,560,802 | - | ||||||

|

Available-for-sale securities

|

102,659,251 | 65,505,339 | ||||||

|

Held-to-maturity securities

|

472,783 | 556,465 | ||||||

|

Stock in Federal Home Loan Bank, at cost

|

5,976,600 | 6,730,100 | ||||||

|

Mortgage loans held for sale

|

3,465,080 | 1,933,798 | ||||||

|

Loans receivable, net of allowance for loan losses of December 31, 2009 and 2008 - $14,076,123 and $16,728,492, respectively

|

525,038,053 | 556,393,243 | ||||||

|

Accrued interest receivable:

|

||||||||

|

Loans

|

2,014,418 | 2,310,062 | ||||||

|

Investments

|

657,145 | 322,388 | ||||||

|

Prepaid expenses and other assets

|

6,731,409 | 4,065,359 | ||||||

|

Prepaid FDIC deposit insurance premiums

|

4,135,875 | - | ||||||

|

Foreclosed assets held for sale

|

6,759,648 | 5,655,257 | ||||||

|

Premises and equipment

|

11,817,516 | 11,323,463 | ||||||

|

Bank owned life insurance

|

10,069,540 | - | ||||||

|

Income taxes receivable

|

3,718,970 | 9,091 | ||||||

|

Deferred income taxes

|

4,686,065 | 5,768,813 | ||||||

| $ | 737,779,852 | $ | 675,670,393 | |||||

|

LIABILITIES AND STOCKHOLDERS' EQUITY

|

||||||||

|

LIABILITIES

|

||||||||

|

Deposits

|

$ | 513,051,102 | $ | 447,079,469 | ||||

|

Federal Home Loan Bank advances

|

116,050,000 | 132,436,000 | ||||||

|

Securities sold under agreements to repurchase

|

39,750,000 | 39,750,000 | ||||||

|

Subordinated debentures

|

15,465,000 | 15,465,000 | ||||||

|

Notes payable

|

- | 1,435,190 | ||||||

|

Advances from borrowers for taxes and insurance

|

135,610 | 166,327 | ||||||

|

Accrued expenses and other liabilities

|

519,385 | 448,226 | ||||||

|

Accrued interest payable

|

1,398,122 | 1,577,279 | ||||||

| 686,369,219 | 638,357,491 | |||||||

|

COMMITMENTS AND CONTINGENCIES

|

- | - | ||||||

|

STOCKHOLDERS' EQUITY

|

||||||||

|

Capital Stock:

|

||||||||

|

Series A preferred stock, $0.01 par value; authorized 2,000,000 shares; issued and outstanding December 31, 2009 - 17,000 shares

|

15,874,788 | - | ||||||

|

Common stock, $0.10 par value; authorized 10,000,000 shares; issued December 31, 2009 and 2008 - 6,779,800 shares;

|

677,980 | 677,980 | ||||||

|

Common stock warrants; December 31, 2009 - 459,459 shares

|

1,377,811 | - | ||||||

|

Additional paid-in capital

|

58,523,646 | 58,535,159 | ||||||

|

Unearned ESOP shares

|

(660,930 | ) | (888,930 | ) | ||||

|

Retained earnings, substantially restricted

|

35,741,705 | 39,114,189 | ||||||

|

Accumulated other comprehensive income

|

||||||||

|

Unrealized appreciation on available-for-sale securities and effect of interest rate swaps, net of income taxes; December 31, 2009 and 2008 - $996,342 and $991,281, respectively

|

1,696,502 | 1,687,858 | ||||||

| 113,231,502 | 99,126,256 | |||||||

|

Treasury stock, at cost; December 31, 2009 and December 31, 2008 -4,079,067 and 4,077,567 shares, respectively

|

(61,820,869 | ) | (61,813,354 | ) | ||||

| 51,410,633 | 37,312,902 | |||||||

| $ | 737,779,852 | $ | 675,670,393 | |||||

See Notes to Consolidated Financial Statements

17

Guaranty Federal Bancshares, Inc.

Consolidated Statements of Operations

Years Ended December 31, 2009, 2008 and 2007

|

2009

|

2008

|

2007

|

||||||||||

|

Interest Income

|

||||||||||||

|

Loans

|

$ | 29,695,487 | $ | 33,019,217 | $ | 37,113,849 | ||||||

|

Investment securities

|

3,743,688 | 3,124,862 | 537,176 | |||||||||

|

Other

|

434,261 | 219,313 | 321,515 | |||||||||

| 33,873,436 | 36,363,392 | 37,972,540 | ||||||||||

|

Interest Expense

|

||||||||||||

|

Deposits

|

15,381,190 | 14,219,732 | 15,860,794 | |||||||||

|

Federal Home Loan Bank advances

|

3,152,354 | 3,237,489 | 3,469,551 | |||||||||

|

Subordinated debentures

|

1,023,783 | 1,023,783 | 1,023,783 | |||||||||

|

Other

|

969,258 | 1,043,220 | 165,175 | |||||||||

| 20,526,585 | 19,524,224 | 20,519,303 | ||||||||||

|

Net Interest Income

|

13,346,851 | 16,839,168 | 17,453,237 | |||||||||

|

Provision for Loan Losses

|

6,900,000 | 14,744,079 | 840,000 | |||||||||

|

Net Interest Income After

|

||||||||||||

|

Provision for Loan Losses

|

6,446,851 | 2,095,089 | 16,613,237 | |||||||||

|

Noninterest Income

|

||||||||||||

|

Service charges

|

1,802,288 | 2,027,691 | 2,215,641 | |||||||||

|

Other fees

|

52,233 | 40,129 | 90,360 | |||||||||

|

Gain (loss) on investment securities

|

689,769 | (563,615 | ) | 618,363 | ||||||||

|

Gain on sale of loans

|

1,443,385 | 875,010 | 1,177,017 | |||||||||

|

Loss on foreclosed assets

|

(523,557 | ) | (783,831 | ) | (41,909 | ) | ||||||

|

Other income

|

823,376 | 720,767 | 669,095 | |||||||||

| 4,287,494 | 2,316,151 | 4,728,567 | ||||||||||

|

Noninterest Expense

|

||||||||||||

|

Salaries and employee benefits

|

7,952,105 | 7,517,285 | 7,074,249 | |||||||||

|

Occupancy

|

1,806,100 | 1,682,277 | 1,614,403 | |||||||||

|

FDIC deposit insurance premiums

|

1,520,551 | 384,996 | 42,555 | |||||||||

|

Data processing

|

423,205 | 374,123 | 391,679 | |||||||||

|

Advertising

|

316,666 | 399,996 | 399,996 | |||||||||

|

Other expense

|

2,691,056 | 2,401,133 | 2,319,269 | |||||||||

| 14,709,683 | 12,759,810 | 11,842,151 | ||||||||||

|

Income (Loss) Before Income Taxes

|

(3,975,338 | ) | (8,348,570 | ) | 9,499,653 | |||||||

|

Provision (Credit) for Income Taxes

|

(1,634,620 | ) | (2,988,859 | ) | 3,399,771 | |||||||

|

Net Income (Loss)

|

$ | (2,340,718 | ) | $ | (5,359,711 | ) | $ | 6,099,882 | ||||

|

Preferred Stock Dividends and Discount Accretion

|

1,031,766 | - | - | |||||||||

|

Net Income (Loss) Available to Common Shareholders

|

$ | (3,372,484 | ) | $ | (5,359,711 | ) | $ | 6,099,882 | ||||

|

Basic Income (Loss) Per Common Share

|

$ | (1.29 | ) | $ | (2.06 | ) | $ | 2.25 | ||||

|

Diluted Income (Loss) Per Common Share

|

$ | (1.29 | ) | $ | (2.06 | ) | $ | 2.19 | ||||

See Notes to Consolidated Financial Statements

18

Guaranty Federal Bancshares, Inc.

Consolidated Statements of Cash Flows

Years Ended December 31, 2009, 2008 and 2007

|

2009

|

2008

|

2007

|

||||||||||

|

CASH FLOWS FROM OPERATING ACTIVITIES

|

||||||||||||

|

Net income (loss)

|

$ | (2,340,718 | ) | $ | (5,359,711 | ) | $ | 6,099,882 | ||||

|

Items not requiring (providing) cash:

|

||||||||||||

|

Deferred income taxes

|

701,199 | (4,143,816 | ) | (187,839 | ) | |||||||

|

Depreciation

|

965,504 | 934,941 | 902,322 | |||||||||

|

Provision for loan losses

|

6,900,000 | 14,744,079 | 840,000 | |||||||||

|

Gain on sale of loans and investment securities

|

(2,133,154 | ) | (777,222 | ) | (1,795,380 | ) | ||||||

|

Other than temporary impairment on investment securities

|

- | 465,827 | - | |||||||||

|

Loss (gain) on sale of foreclosed assets

|

285,010 | 627,888 | (4,621 | ) | ||||||||

|

Accretion of gain on termination of interest rate swaps

|

(1,017,492 | ) | (169,582 | ) | - | |||||||

|

Amortization of deferred income, premiums and discounts, net

|

352,345 | (47,702 | ) | 108,733 | ||||||||

|

Stock award plans

|

95,268 | 92,846 | 71,325 | |||||||||

|

Origination of loans held for sale

|

(78,535,230 | ) | (51,082,040 | ) | (71,861,627 | ) | ||||||

|

Proceeds from sale of loans held for sale

|

78,447,333 | 52,165,250 | 73,901,281 | |||||||||

|

Release of ESOP shares

|

121,219 | 408,388 | 672,765 | |||||||||

|

Increase in cash surrender value of bank owned life insurance

|

(69,540 | ) | - | - | ||||||||

|

Changes in:

|

||||||||||||

|

Prepaid FDIC deposit insurance premiums

|

(4,135,875 | ) | - | - | ||||||||

|

Accrued interest receivable

|

(39,113 | ) | 690,998 | (413,139 | ) | |||||||

|

Prepaid expenses and other assets

|

767,817 | 372,439 | 114,073 | |||||||||

|

Accrued expenses and other liabilities

|

(214,248 | ) | (67,163 | ) | 235,832 | |||||||

|

Income taxes payable

|

(3,333,407 | ) | (519,838 | ) | 1,051,189 | |||||||

|

Net cash provided by (used in) operating activities

|

(3,183,082 | ) | 8,335,582 | 9,734,796 | ||||||||

|

CASH FLOWS FROM INVESTING ACTIVITIES

|

||||||||||||

|

Net change in loans

|