Attached files

Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2009

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number: 000-50679

CORCEPT THERAPEUTICS INCORPORATED

(Exact Name of Corporation as Specified in Its Charter)

| Delaware | 77-0487658 | |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

149 Commonwealth Drive

Menlo Park, CA 94025

(Address of principal executive offices, including zip code)

(650) 327-3270

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12 (b) of the Act:

| Title of Each Class: |

Name of Each Exchange on which Registered: | |

| Common Stock, $0.001 par value | The NASDAQ Capital Market |

Securities registered pursuant to Section 12 (g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15 (d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the Registrant’s knowledge, in definitive proxy or information statements incorporated by reference to Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large Accelerated Filer ¨ |

Accelerated Filer ¨ | |

| Non-accelerated filer ¨ (Do not check if a smaller reporting company) |

Smaller reporting company x |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of voting and non-voting common equity held by non-affiliates of the Registrant was approximately $14,000,000 as of June 30, 2009 based upon the closing price on the Nasdaq Capital Market reported for such date. This calculation does not reflect a determination that certain persons are affiliates of the Registrant for any other purpose.

On March 15, 2010 there were 62,703,717 shares of common stock outstanding at a par value $.001 per share.

DOCUMENTS INCORPORATED BY REFERENCE

None.

Table of Contents

Form 10-K

For the year ended December 31, 2009

| Page | ||||

| PART I | ||||

| ITEM 1. | Business | 1 | ||

| ITEM 1A. | Risk Factors | 19 | ||

| ITEM 1B. | Unresolved Staff Comments | 40 | ||

| ITEM 2. | Properties | 40 | ||

| ITEM 3. | Legal Proceedings | 40 | ||

| ITEM 4. | (Removed and Reserved) | 40 | ||

| PART II | ||||

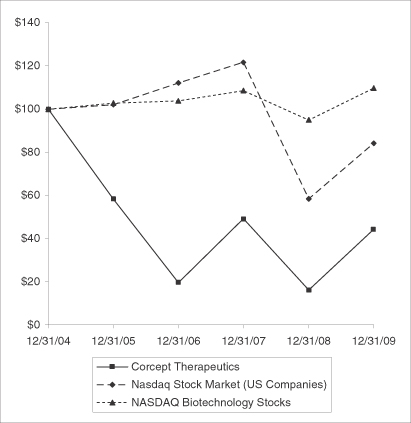

| ITEM 5. | 41 | |||

| ITEM 6. | 43 | |||

| ITEM 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

44 | ||

| ITEM 7A. | 56 | |||

| ITEM 8. | 56 | |||

| ITEM 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

56 | ||

| ITEM 9A (T). | 56 | |||

| ITEM 9B. | 57 | |||

| PART III | ||||

| ITEM 10. | 58 | |||

| ITEM 11. | 62 | |||

| ITEM 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

72 | ||

| ITEM 13. | Certain Relationships and Related Transactions, and Director Independence |

75 | ||

| ITEM 14. | 76 | |||

| PART IV | ||||

| ITEM 15. | Exhibits, Financial Statement Schedules | 77 | ||

| Signatures and Power of Attorney | 81 | |||

Table of Contents

This Annual Report on Form 10-K, or Form 10-K, contains forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended (Exchange Act), and Section 27A of the Securities Act of 1933, as amended (Securities Act). All statements contained in this Form 10-K, other than statements of historical fact, are forward-looking statements. When used in this report or elsewhere by management from time to time, the words “believe,” “anticipate,” “intend,” “plan,” “estimate,” “expect,” “may,” “will,” “should,” “seeks” and similar expressions are forward-looking statements. Such forward-looking statements are based on current expectations, but the absence of these words does not necessarily mean that a statement is not forward-looking. Forward-looking statements made in this Form 10-K include, but are not limited to, statements about:

| • | the progress of our research, development, clinical programs and the timing of regulatory activities; |

| • | our estimates of the dates by which we expect to report results of our clinical trials and the anticipated results of these trials; |

| • | the timing of market introduction of CORLUX® and future product candidates, including CORT 108297; |

| • | our ability to market, commercialize and achieve market acceptance for CORLUX or other future product candidates, including CORT 108297; |

| • | uncertainties associated with obtaining and enforcing patents; |

| • | our estimates for future performance; and |

| • | our estimates regarding our capital requirements and our needs for, and ability to obtain, additional financing. |

Forward-looking statements are not guarantees of future performance and involve risks and uncertainties. Actual events or results may differ materially from those discussed in the forward-looking statements as a result of various factors. For a more detailed discussion of such forward-looking statements and the potential risks and uncertainties that may impact upon their accuracy, see the “Risk Factors” section of this Form 10-K and the “Overview” and “Liquidity and Capital Resources” sections of the “Management’s Discussion and Analysis of Financial Condition and Results of Operations” section of this Form 10-K. These forward-looking statements reflect our view only as of the date of this report. Except as required by law, we undertake no obligations to update any forward-looking statements. Accordingly, you should also carefully consider the factors set forth in other reports or documents that we file from time to time with the Securities and Exchange Commission (SEC).

| ITEM 1. | BUSINESS |

Overview

We are a pharmaceutical company engaged in the discovery and development of drugs for the treatment of severe metabolic and psychiatric disorders. Our focus is on those disorders that are associated with a steroid hormone called cortisol. Elevated levels and abnormal release patterns of cortisol have been implicated in a broad range of human disorders. Since our inception in May 1998, we have been developing our lead product, CORLUX, a potent glucocorticoid receptor II (GR-II) antagonist that blocks the activity of cortisol. We have also discovered three series of novel selective GR-II antagonists and have moved one of these compounds, CORT 108297, into development.

Cushing’s Syndrome. Cushing’s Syndrome is a disorder caused by prolonged exposure of the body’s tissues to high levels of the hormone cortisol. Sometimes called “hypercortisolism,” it is relatively uncommon and most often affects adults aged 20 to 50. An estimated 10 to 15 of every one million people are newly diagnosed with this syndrome each year, resulting in approximately 3,000 new patients and an estimated prevalence of 20,000 patients with Cushing’s Syndrome in the United States.

1

Table of Contents

The Investigational New Drug application (IND) for the evaluation of CORLUX for the treatment of Cushing’s Syndrome was opened in September 2007. The United States Food and Drug Administration (FDA) has indicated that our single 50-patient open-label study may provide a reasonable basis for the submission of a New Drug Application (NDA) for this indication. We expect to complete enrollment in this Phase 3 study in April, as the requisite 50 patients have now been dosed or identified. We expect to announce results of this study in the fourth quarter of this year and to submit our NDA for the use of CORLUX in Cushing’s Syndrome by year-end 2010.

In July 2007, we received Orphan Drug Designation from the FDA for CORLUX for the treatment of endogenous Cushing’s Syndrome. Orphan Drug Designation is a special status granted by the FDA to encourage the development of treatments for diseases or conditions that affect fewer than 200,000 patients in the United States. Drugs that receive Orphan Drug Designation obtain seven years of marketing exclusivity from the date of drug approval, as well as tax credits for clinical trial costs, marketing application filing fee waivers and assistance from the FDA in the drug development process.

Psychotic depression. We are developing CORLUX for the treatment of the psychotic features of psychotic major depression under an exclusive patent license from Stanford University. Psychotic major depression will hereafter be referred to as psychotic depression. The FDA has granted “fast track” status to evaluate the safety and efficacy of CORLUX for the treatment of the psychotic features of psychotic depression.

In March of 2008, we began enrollment in Study 14, our ongoing Phase 3 trial in psychotic depression. The protocol for this trial incorporates what we have learned from our three previously completed Phase 3 trials. It attempts to address the established relationship between increased drug plasma levels and clinical response and to decrease the random variability observed in the results of the psychometric instruments used to measure efficacy. In one of the previously completed Phase 3 trials, Study 06, we prospectively tested and confirmed that patients whose plasma levels rose above a predetermined threshold statistically separated from both those patients whose plasma levels were below the threshold and those patients who received placebo; this threshold was established from data produced in earlier studies.

As expected, patients who took 1200 mg of CORLUX in Study 06 developed higher drug plasma levels than patients who received lower doses. Further, there was no discernable difference in the incidence of adverse events between patients who received placebo in Study 06 and those who received 300 mg, 600 mg or 1200 mg of CORLUX in that study. Based on this information, we are using a CORLUX dose of 1200 mg once per day for seven days in Study 14.

In addition, we also are utilizing a third party centralized rating service to independently evaluate the patients for entry into the study as well as to evaluate their level of response throughout their participation in the study. We believe the centralization of this process will improve the consistency of rating across clinical trial sites and reduce the background noise that was experienced in earlier studies and is endemic to many psychopharmacologic studies. We believe that this change in dose, as well as the other modifications to the protocol, should allow us to demonstrate the efficacy of CORLUX in the treatment of the psychotic symptoms of psychotic depression. In March 2009, we announced that, in order to conserve financial resources, we were scaling back our planned rate of spending on this trial and extended the timeline for its completion. As of early July 2009, we had completed the implementation of this strategy, which included reducing the number of clinical sites to eight.

Antipsychotic-induced Weight Gain Mitigation. In 2005, we published the results of studies in rats that demonstrated that CORLUX both reduced the weight gain associated with the ongoing use of olanzapine and mitigated the weight gain associated with the initiation of treatment with olanzapine (the active ingredient in Zyprexa). This study was paid for by Eli Lilly and Company (Eli Lilly).

2

Table of Contents

During 2007 we announced positive results from our clinical proof-of-concept study in lean healthy male volunteers evaluating the ability of CORLUX to mitigate weight gain associated with the use of Zyprexa. The results show a statistically significant reduction in weight gain in those subjects who took Zyprexa plus CORLUX compared to those who took Zyprexa plus placebo. Also, the addition of CORLUX to treatment with Zyprexa had a beneficial impact on secondary metabolic measures such as fasting insulin, triglycerides and abdominal fat, as indicated by waist circumference. Eli Lilly provided Zyprexa and financial support for this study. In January 2009 we announced positive results from a similar proof-of-concept study evaluating the ability of CORLUX to mitigate weight gain associated with the use of Johnson & Johnson’s Risperdal. This study, which began in 2008, confirmed and extended the earlier results seen with CORLUX and Zyprexa, demonstrating a statistically significant reduction in weight and secondary metabolic endpoints of fasting insulin, triglycerides and abdominal fat, as indicated by waist circumference. The results from the study of CORLUX and Risperdal were presented at several scientific conferences, including the American Diabetes Association meeting in June 2009.

The combination of Zyprexa or Risperdal and CORLUX is not approved for any indication. The purpose of these studies was to explore the hypothesis that GR-II antagonists, such as CORLUX and our next generation of selective GR-II antagonists, would mitigate weight gain associated with antipsychotic medications. The group of medications known as second generation antipsychotic medication, including Zyprexa, Risperdal, Clozaril and Seroquel, are widely used to treat schizophrenia and bipolar disorder. All medications in this group are associated with treatment emergent weight gain of varying degrees and carry a warning in their labels relating to treatment emergent hyperglycemia and diabetes mellitus.

We have completed IND enabling work with CORT 108297, which included preclinical studies in the rat in antipsychotic induced weight gain, diet induced weight gain and insulin sensitivity. In February 2010, we initiated a Phase 1 study to evaluate the tolerability of this compound in healthy volunteers. CORT 108297 is the lead compound from our three series of selective GR-II antagonists. Preclinical studies of CORT 108297, presented at scientific conferences during 2009, demonstrated a statistically significant mitigation in weight gain and other metabolic effects when added to olanzapine, the active ingredient in Eli Lilly’s medication Zyprexa. CORT 108297 also demonstrated the potential to mitigate weight gain caused by consumption of a high fat, high sucrose diet and improve insulin sensitivity in a preclinical mouse model.

Additional Indications. We have discovered and patented three series of next-generation selective GR-II receptor antagonists. As discussed above, the lead compound from these series, CORT 108297, is being developed for the prevention of weight gain induced by antipsychotic medication and is currently in a Phase 1 trial. There are numerous additional compounds in these three series that may be developed for weight gain mitigation or other diseases in which excess cortisol plays a role. The role of excess cortisol has been well established and documented in the scientific literature in diabetes, obesity, hypertension, osteoporosis, glaucoma, Alzheimer’s disease and various other neurodegenerative diseases, in addition to antipsychotic-induced weight gain.

The Role of Cortisol in Disease

Cortisol is a steroid hormone that plays a significant role in the way the body reacts to stressful conditions and is essential for survival. Cortisol significantly influences metabolism, exerts a clinically useful anti-inflammatory effect and contributes to emotional stability. Insufficient levels of cortisol may lead to dehydration, hypotension, shock, fatigue, low resistance to infection, trauma, stress and hypoglycemia. Excessive levels of cortisol may lead to edema, hypertension, fatigue and impaired glucose tolerance.

Elevated levels and abnormal release patterns of cortisol have also been linked to a broad range of metabolic and psychiatric conditions, such as weight gain, diabetes, hypertension, mood changes, psychosis and cognitive impairment.

3

Table of Contents

While excess release of cortisol may play a role in numerous diseases, Cushing’s Syndrome is the fundamental disease of excess cortisol, as patients have tumors that produce excess levels of the hormone cortisol or its precursor, adrenocorticotropic hormone (ACTH). Sometimes called “hypercortisolism”, the body’s exposure to high levels of cortisol can result in weight gain, diabetes, hypertension, infections, severe fatigue and psychosis.

Many studies have shown that patients with psychotic depression have elevated levels and abnormal release patterns of cortisol. This abnormal cortisol activity is not usually present in patients with nonpsychotic depression. More than 20 years ago, one of our scientific co-founders postulated that elevated levels of cortisol in patients with psychotic depression lead to elevated levels of dopamine, an important chemical substance found in the brain. Elevated levels of dopamine have been implicated in both delusional thinking and hallucinations. This hypothesis led to the concept that, by regulating the level and release patterns of cortisol, one could normalize dopamine levels in the brain, which may, in turn, ameliorate the symptoms of psychotic depression. In addition to cortisol’s effect on dopamine levels, research has shown that prolonged elevated cortisol may also play a direct role in causing the symptoms of psychotic depression.

The challenge in regulating levels of cortisol, however, is that it is needed for natural processes in the human body. Destroying the ability of the body to make cortisol or to drastically reduce its presence would result in serious detrimental effects. To have a viable therapeutic effect, a compound must be able to selectively modulate cortisol effects.

Glucocorticoid Receptor Antagonists

Cortisol is produced by the adrenal glands and is carried via the bloodstream to the brain, where it directly influences neuronal function. In the brain, cortisol binds to two receptors, Glucocorticoid Receptor I and Glucocorticoid Receptor II, also known as GR-I and GR-II. GR-I is a high-affinity receptor that is involved in the routine functions of cortisol in the brain. It has approximately ten times the affinity of GR-II for cortisol and its binding sites are filled with cortisol nearly all the time. In general, GR-II binding sites do not fill until levels of cortisol become elevated. Short-term activation of GR-II has benefits, which include helping the individual to be more alert and better able to function under stressful conditions. Long-term activation of GR-II, however, has been shown to have significant toxicity and appears to be linked to multiple metabolic and psychiatric disease states, such as Cushing’s Syndrome and psychotic depression. The action of cortisol can be moderated by the use of blockers, or antagonists, that prevent the binding of the hormone to its receptors. These antagonists, referred to as glucocorticoid, or cortisol, receptor antagonists, may prevent the undesirable effects of elevated levels and abnormal release patterns of cortisol.

CORLUX, also known as mifepristone, works by selectively blocking the binding of cortisol to GR-II; CORLUX is neither an antagonist nor agonist of GR-I. It also blocks the progesterone receptor (PR). Because of its selective affinity, we believe that CORLUX can have a therapeutic benefit by modulating the effects of abnormal levels and release patterns of cortisol without compromising the necessary normal functions of cortisol. We have also discovered three series of additional compounds, one of which includes our lead candidate CORT 108297, which, like CORLUX, potently block the GR-II receptor, but, unlike CORLUX, do not block the progesterone receptor.

Overview of Cushing’s Syndrome

Endogenous Cushing’s Syndrome is caused by prolonged exposure of the body’s tissues to high levels of the hormone cortisol due to a variety of pathologic conditions. In endogenous Cushing’s Syndrome, the production of excess cortisol is stimulated or directly produced by pituitary, adrenal or ectopic tumors. Cushing’s Syndrome is an orphan indication which most commonly affects adults aged 20 to 50. An estimated 10 to 15 of every one million people are newly diagnosed with this syndrome each year, resulting in over 3,000 new patients in the United States. An estimated 20,000 patients in the United States have been diagnosed with Cushing’s

4

Table of Contents

Syndrome. Symptoms vary, but most people have one or more of the following manifestations: high blood sugar, diabetes, high blood pressure, upper body obesity, rounded face, increased fat around the neck, thinning arms and legs, severe fatigue and weak muscles. Irritability, anxiety, cognitive disturbances and depression are also common. Cushing’s Syndrome can affect every organ system in the body and can be lethal if not treated effectively. There is no FDA-approved treatment for Cushing’s Syndrome.

Current Treatments for Cushing’s Syndrome

Current treatment depends on the specific cause of cortisol excess and may include surgery, radiation and chemotherapy. Patients sometimes may be treated with drugs that prevent the body from producing cortisol. Approximately 70% of the patients diagnosed with Cushing’s Syndrome are candidates for surgery. Depending on the type of tumor there are varying rates of success and complications related to removing the tumor. If the tumor is successfully removed in its entirety, the patient is essentially cured and will not require additional treatment for Cushing’s Syndrome. However, in approximately half of the patients, it is clear that surgery is not successful or, while surgery may appear to be successful initially, the patient later relapses. These patients currently have limited treatment options.

CORLUX for Cushing’s Syndrome

CORLUX represents a potentially attractive treatment option with the potential for long-term oral dosing. CORLUX is a GR-II antagonist that appears to mitigate the effects of the elevated levels of cortisol in patients suffering from Cushing’s Syndrome. We intend for CORLUX to be a once-daily chronic treatment in this indication. Mifepristone, the active ingredient in CORLUX, in addition to blocking GR-II, blocks the progesterone receptor and has been approved by the FDA for termination of early pregnancy.

We believe that CORLUX may significantly reduce a broad range of symptoms typically associated with Cushing’s Syndrome. These symptoms can include weight gain, diabetes, hypertension, poor tissue quality, fatigue and psychosis. Cushing’s Syndrome has a five-year 50% mortality rate if left untreated.

The FDA has granted Orphan Drug Designation for CORLUX for the treatment of endogenous Cushing’s Syndrome. “Orphan” drugs receive seven years of marketing exclusivity from the date of approval, as well as tax credits for clinical trial costs, marketing application filing fee waivers and assistance from the FDA in the drug development process.

CORLUX for Cushing’s Syndrome Clinical Experience

There have been reports in the scientific literature of more than 40 Cushing’s Syndrome patients who have been treated with mifipristone, the active ingredient in CORLUX. The clinical benefit supported by these data served as the rationale for our IND for CORLUX and design of our Phase 3 trial. While there have been no formal trials completed, the published results of the treatment of Cushing’s Syndrome patients with mifepristone include improvement in glucose tolerance and hemoglobin A1C levels, blood pressure, depression and psychosis, and improvement in the patient’s general quality of life.

CORLUX for Cushing’s Syndrome Phase 3 Study

We are conducting a Phase 3 trial with CORLUX for the treatment of endogenous Cushing’s Syndrome. The IND for the evaluation of CORLUX for the treatment of Cushing’s Syndrome was opened in September 2007. We are conducting a single 50-patient open-label study, in which patients’ dose is titrated to clinical benefit, and endpoints are focused on improvement in glucose tolerance and blood pressure, as well as broader measures of patient outcomes. The FDA has indicated that this trial may provide a reasonable basis for the submission of an NDA for this indication. We expect to complete enrollment in this Phase 3 study in April, as the requisite 50 patients have now been dosed or identified, and expect to announce results of this study in the fourth quarter of 2010.

5

Table of Contents

The primary endpoint in the trial is either 1) improvement in glucose tolerance (as measured by the area under the curve of an oral glucose tolerance test) at 24 weeks relative to baseline, or 2) if a patient is not glucose intolerant at baseline, improvement in diastolic blood pressure at 24 weeks relative to baseline. A patient in the glucose tolerance group is considered a responder if there is a 25% or greater improvement in the area under the curve of a standard oral glucose tolerance test over the 24-week course of the study. A patient in the hypertension group is considered a responder if there is a 5 millimeter or greater drop in diastolic blood pressure at 24 weeks relative to baseline. If a sufficient number of patients in either group are responders (such that the lower limit of the exact one-sided 95% binomial confidence interval for the responder rate is greater than 20%, or approximately 35% of the patients are responders, depending on the number of patients in each group) then the trial will have met its primary endpoint. The key secondary endpoint in the trial, global clinical improvement, is designed to capture the broader clinical benefit of CORLUX in this patient population.

Additional Trials and Preclinical Studies

In support of our planned NDA submission, we are conducting a long-term extension study in patients who completed the Phase 3 trial to assess safety of chronic dosing. We are conducting several small trials to evaluate how the drug acts on the human body, how the human body acts on the drug and the drug’s safety. In addition to our clinical trials, we have completed a standard 12-month toxicology study in dogs, a carcinogenicity study in rats, and a carcinogenicity study in mice. These studies are designed to meet FDA requirements and the guidelines of an international regulatory body called the International Conference on Harmonisation of Technical Requirements for Registration of Pharmaceuticals for Human Use. We anticipate completing all of the additional trials required for our NDA submission for CORLUX for the treatment of Cushing’s Syndrome by the time of completion of our Phase 3 efficacy study.

Overview of Psychotic Depression

Psychotic depression is a serious psychiatric disease in which a patient suffers from severe depression accompanied by delusions, hallucinations or both. These psychotic features typically develop after the onset of a depressed mood, but may develop concurrently as well. Once psychotic symptoms occur, they usually reappear with each subsequent depressive episode. Of particular importance, when the patient’s mood returns to normal the psychosis also resolves.

Data from the National Institutes of Mental Health published in 2005 indicate that depressive disorders affect an estimated 9.5% of adults in the United States, or about 19 million people each year. Of these 19 million people, many published studies show that approximately 15-20%, or about three million people, have psychotic depression. Most patients with psychotic depression suffer their first episode of major depression between the ages of 30 and 40 and the majority will experience more than one episode in their lifetime. People with psychotic depression are approximately 70 times more likely to commit suicide in their lifetime than the general population and often require lengthy and expensive hospital stays.

Current Treatments for Psychotic Depression

There are two treatment approaches for psychotic depression currently used by psychiatrists: electroconvulsive therapy ECT and combination drug therapy, which is a combination of antidepressant and antipsychotic medication. Neither of these treatments has been approved by the FDA for psychotic depression and both approaches almost always have a slow onset of action, which may result in lengthy and costly hospitalization. Each of these treatments can have debilitating side effects. Of the two treatments, ECT is generally considered to be more effective.

| • | ECT involves passing an electrical current through the brain until the patient has a seizure. At least 100,000 patients receive ECT each year in the United States, with each patient requiring approximately six to twelve procedures over a period of three to five weeks. |

6

Table of Contents

| • | Combination drug therapy is an alternative treatment for psychotic depression that involves taking antipsychotic drugs such as olanzapine, haloperidol or chlorpromazine in combination with antidepressant drugs, such as fluoxetine, imipramine or venlafaxine. Patients on combination drug therapy often require three weeks or more to show improvement in their symptoms and treatment can take months before the symptoms are resolved entirely. Antipsychotic drugs can cause significant adverse side effects, including weight gain, diabetes, sedation, permanent movement disorders and sexual dysfunction. |

CORLUX for the Psychotic Features of Psychotic Depression

We are also developing CORLUX as an oral medication to treat the psychotic features of psychotic depression. As a GR-II antagonist, CORLUX appears to mitigate the effects of the elevated and abnormal release patterns of cortisol in patients suffering from psychotic depression. We intend CORLUX to be a once-daily treatment given to patients with psychotic depression over 7 consecutive days in a controlled setting, such as a hospital or physician’s office.

We believe that CORLUX may significantly reduce psychotic symptoms of psychotic depression in many patients within one week and allow patients to be more easily maintained on antidepressant therapy alone without the need for ECT or antipsychotic medication. We believe that CORLUX may be superior to currently available treatments because we believe that CORLUX will enable patients with psychotic depression to improve their quality of life more quickly and with fewer side effects than with ECT or combination drug therapy.

Completed Clinical Trials of CORLUX for Psychotic Depression

We have completed seven prior clinical trials evaluating CORLUX in psychotic depression, in addition to our ongoing Phase 3 trial. The trials include three Phase 3 trials conducted from 2004 through 2007, in addition to four earlier stage clinical trials with CORLUX. These completed trials generated important data confirming the safety profile of CORLUX (alone and in combination with commonly prescribed antipsychotic and antidepressant medications), demonstrated positive efficacy trends, and provided insights into the design of future clinical trials which might improve the probability of clinical success.

Completed Phase 3 Clinical Trials. In addition to Phase 1 and 2 studies, we have completed three randomized, double-blind, placebo-controlled Phase 3 clinical trials to further assess the safety and efficacy of CORLUX for the treatment of the psychotic features of psychotic depression. Two of these trials (Study 06 and Study 07) were conducted primarily in the United States. The third trial (Study 09) was conducted in Eastern Europe.

The primary endpoint for Study 06 and Study 07 was the proportion of patients with at least a 50% improvement in the Brief Psychiatric Rating Scale Positive Symptom Subscale (BPRS PSS) at both Day 7 and Day 56. The primary endpoint for Study 09 was the proportion of patients with at least a 50% improvement in the BPRS PSS, at both Day 7 and Day 28, with day 56 as a secondary endpoint. Patients must have had at least mild psychotic symptoms (BPRS PSS ³12) to enter the studies and were hospitalized if clinically necessary.

| • | Study 07: The first of these trials, which began in September 2004, enrolled 257 patients randomized one-to-one to either treatment or placebo. Patients in the treatment arm received 600 mg of CORLUX once daily for a period of seven days. Patients did not take any antidepressant or antipsychotic medication for at least one week before beginning the seven day treatment period. After the seven days of CORLUX treatment, all patients received antidepressant therapy through Day 56. Treatment with antipsychotic medications or ECT was not allowed at any time during the study. |

In this study patients receiving CORLUX did not have a statistically significant difference in response rate at the primary endpoint than did the patients receiving placebo. A retrospective analysis of the data showed that patients achieving drug plasma levels higher than 1800 nanograms per milliliter (ng/ml)

7

Table of Contents

had a statistically significant greater response rate than placebo. There was also a statistically significant site by treatment effect in this trial. Among the twenty sites who participated from the trial onset, patients who were given CORLUX had a significantly higher response rate than patients who received placebo. Among the sites added later in the trial, there was no significant difference in response rate between CORLUX and placebo patients. These findings were published in 2009 by Contemporary Clinical Trials.

| • | Study 09: This study, which commenced in May 2005, was a randomized, double-blind, placebo-controlled study in which 247 patients were enrolled at sites in Eastern Europe. The primary endpoint was the proportion of patients with at least a 50% improvement in the BPRS PSS score at both Day 7 and Day 28. The study did not demonstrate a significant difference in response between patients receiving CORLUX and patients receiving placebo as measured by the primary endpoint. The results at the two key secondary endpoints of Study 09 also were not statistically significant. Study 09 had an extremely high placebo response rate. |

| • | Study 06: This trial began in October 2004, and enrolled 443 patients. These patients were randomly assigned to three active dose groups (300 mg, 600 mg and 1200 mg) or a placebo group, with patients receiving once daily dosing for a period of seven days. The three dosing levels responded to the FDA’s request to supplement data on a range of doses to augment the data provided by our open label dose ranging study completed in 2001. |

The study did not achieve statistical significance with respect to the primary endpoint. However, there was a statistically significant correlation between plasma levels and clinical outcome achieved during treatment. Response rates for patients whose plasma levels rose above a predetermined threshold of 1661 ng/mL were statistically different than those patients whose plasma levels were below the threshold and those patients who received placebo. Further, the incidence of serious adverse events did not differ between placebo and any of the three CORLUX dose groups.

Ongoing Phase 3 trial – Study 14: We believe that the confirmation of a correlation between drug concentration and clinical response, as well as other observations from Study 06 and our two other completed Phase 3 clinical trials, served as a strong basis for the design of our ongoing Phase 3 study, which commenced in March 2008. The protocol for this trial incorporates information learned from the three completed Phase 3 trials in that it addresses the established relationship between increased drug plasma levels and clinical response, and it attempts to decrease the random variability observed in the results of the psychometric instruments used to confirm diagnosis and measure efficacy.

| • | Increased Signal: In this trial we are administering a CORLUX dose of 1200 mg once per day for seven days instead of 600 mg once per day for seven days. |

| • | Decreased “Noise”: We also are utilizing a third party centralized rating service to independently evaluate the patient’s diagnosis prior to entry into the study as well as to assess response. We believe the centralization of this process will improve the accuracy of diagnosis and the consistency of rating across clinical trial sites and reduce the background noise that is endemic to many psychopharmacologic studies and clearly visible in our earlier studies. |

We believe that these changes in the protocol should allow us to establish the efficacy of CORLUX in the treatment of the psychotic features of psychotic depression. Given the serious nature of psychotic depression, the lack of any approved drugs for the disorder and the data from our first clinical trial, the FDA granted a fast track designation for CORLUX for the treatment of the psychotic features of psychotic depression. In addition, the FDA has indicated that CORLUX will receive a priority review if no other treatment is approved for psychotic depression at the time we submit our NDA.

Clinical Trial Agreements. Many of our Phase 3 clinical trials are conducted through the use of clinical research organizations (CROs.) At our request, these organizations oversee clinical trials at various institutions to test the safety and efficacy of our product candidates for the targeted indications. Our ongoing Phase 3 clinical

8

Table of Contents

trial, Study 14, evaluating CORLUX for the treatment of the psychotic features of psychotic depression is being conducted under an agreement with ICON Clinical Research, LP (ICON). We may terminate this agreement with 60 days notice to ICON, or sooner based on mutual agreement of the parties. In addition, we entered into an agreement with MedAvante, Inc., in March 2008, to provide the centralized psychiatric diagnosis and rating services for patients being screened and enrolled in Study 14. We may terminate this agreement with 30 days notice to MedAvante.

CORLUX for Other Metabolic Disorders

In April 2005, we announced results from two preclinical studies conducted in a rat model of olanzapine-induced weight gain. These studies demonstrated that CORLUX’s GR-II antagonist action has the potential to both reduce the weight gain associated with olanzapine and to prevent the weight gain associated with the initiation of treatment with olanzapine, which led to our studies in humans.

In 2007, we announced results of our human clinical proof-of-concept study evaluating the ability of CORLUX to mitigate weight gain associated with the administration of Eli Lilly’s Zyprexa® (olanzapine). The results indicated a statistically significant reduction in weight gain in those subjects who took Zyprexa plus CORLUX compared to those who took Zyprexa plus placebo. Eli Lilly provided Zyprexa and financial support for this study. During 2009, we announced results from another proof-of-concept study evaluating the ability of CORLUX to mitigate weight gain associated with the administration of Johnson & Johnson’s Risperdal (risperidone). The results indicated a statistically significant reduction in weight gain in those subjects who took Risperdal plus CORLUX compared to those who took Risperdal plus placebo. Both Zyprexa and Risperdal are indicated for the treatment of schizophrenia and bipolar disorder.

In the study of CORLUX and Zyprexa, 57 lean, healthy men (body mass index of 25 or less) were randomized to receive either Zyprexa plus placebo (n=22), Zyprexa plus CORLUX (n=24) or CORLUX plus placebo (n=11). This study took place in an institutional setting where daily weights were recorded and a range of metabolic parameters were measured. In the two week study, subjects in the Zyprexa plus placebo group gained an average of 7.0 pounds and subjects in the Zyprexa plus CORLUX group gained an average of 4.4 pounds; which is a highly statistically significant difference (p<.001). Subjects in the CORLUX plus placebo group gained an average of 4.4 pounds. The difference in weight gain trajectory was apparent in the first days of the study, reaching statistical significance during the first week. The increase in waist circumference, a surrogate for abdominal fat, in subjects who received Zyprexa plus placebo was also significantly greater than subjects who received Zyprexa plus CORLUX (p<.01). The study was not designed to enroll a sufficient number of patients to have statistical power to detect significant effects on metabolic measures, including waist circumference. However, in addition to the finding about waist circumference, notable additional non-statistically significant group differences were observed. Patients taking Zyprexa plus placebo experienced greater increases from baseline to end of study in both triglycerides and fasting insulin compared to patients taking Zyprexa plus CORLUX. No unexpected study drug related adverse events were observed.

In the study of CORLUX and Risperdal, 75 lean, healthy men (body mass index of 23 or less) were randomized to receive either Risperdal plus placebo (n=30), Risperdal plus CORLUX (n=30) or CORLUX plus placebo (n=15). This study also took place in an institutional setting where daily weights were recorded and a range of metabolic parameters were measured. In this four-week randomized double-blind controlled study, subjects in the Risperdal plus placebo group gained an average of 9.2 pounds, compared to a gain of 5.1 pounds in the Risperdal plus CORLUX group. This difference was highly statistically significant (p<0.0001). Additional important metabolic parameters, including fasting insulin, triglycerides and abdominal fat, as reflected by waist circumference, were also measured. The addition of CORLUX to Risperdal resulted in a statistically significant reduction in fasting insulin levels, triglyceride levels, and abdominal fat (as measured by waist circumference). Consistent with prior studies, CORLUX appeared to be well tolerated.

9

Table of Contents

The combinations of Zyprexa and CORLUX or Risperdal and CORLUX are not approved for any indication. The purpose of these studies was to explore the hypothesis that GR-II antagonists would mitigate weight gain and other metabolic effects associated with antipsychotic medications. The group of medications sometimes referred to as “atypical antipsychotics,” including Zyprexa, Risperdal, Clozaril® (clozapine) and Seroquel® (quetiapine), are widely used to treat schizophrenia and bipolar disorder. All medications in this group are associated with treatment emergent weight gain of varying degrees and carry a warning in the label relating to treatment emergent hyperglycemia and diabetes mellitus.

CORT 108297 for the Prevention and Reversal of Antipsychotic Induced Weight Gain

In January 2009 we announced results from two preclinical studies of our next-generation selective GR-II receptor antagonist, CORT 108297 for the prevention and reversal of weight gain associated with olanzapine, which is marketed by Eli Lilly as Zyprexa. The data demonstrated that CORT 108297 has the potential to both reduce weight gain caused by olanzapine and to prevent weight gain caused by initiation of treatment with olanzapine. The two studies were conducted in the rat model of olanzapine induced weight gain described above, in which CORLUX was tested with olanzapine.

| • | One study evaluated the potential for CORT 108297 to reverse weight gain caused by treatment with olanzapine. In this study six groups (n = 12 per group) of rats were allowed to eat a normal diet for 56 days. Five groups were dosed orally with olanzapine daily. The sixth group received placebo. At day 35, the five groups receiving olanzapine had gained a statistically significant amount of weight compared to the group receiving placebo. The five olanzapine groups then began to receive daily oral doses either of CORT 108297 (at one of three dose levels), CORLUX or placebo through day 56. The data demonstrated that the rats administered olanzapine plus placebo continued to gain weight through day 56. In contrast, the rats given olanzapine along with CORT 108297 and those administered olanzapine with CORLUX did not. By day 56, there was a highly statistically significant difference between these groups and the group administered olanzapine plus placebo. In addition, the ameliorization of olanzapine induced weight gain by CORT 108297 was dose dependent. The rats that received the combination of olanzapine with CORT 108297, or with CORLUX, also had significantly less abdominal fat than the group dosed with olanzapine alone. |

| • | The other study evaluated the potential for CORT 108297 to prevent weight gain when administered concurrently with olanzapine. In this study six groups (n = 12 per group) of rats were allowed to eat a normal diet for 21 days. Five groups were dosed orally with olanzapine daily and one group was given placebo daily. Four of the groups that received olanzapine were also dosed orally with either CORT 108297 (at one of three dose levels) or CORLUX; one group received olanzapine plus placebo. The sixth group was dosed with only placebo. The data demonstrated that at day 21, the three groups dosed with the combination of olanzapine and CORT 108297 had gained significantly less weight compared to the group administered olanzapine alone. Rats administered olanzapine plus CORLUX also gained less weight than rats administered olanzapine alone, but this result did not reach statistical significance. |

These first two studies used dose levels of 20 milligrams per kilogram (mg/kg), 60 mg/kg and 120 mg/kg of CORT 108297. Eli Lilly provided olanzapine and funded the costs of these two studies.

| • | A third study in the rat further evaluated the dose response relationship of CORT 108297 in preventing olanzapine induced weight gain with doses from 2 mg/kg to 20 mg/kg. |

In summary, these studies in the rat demonstrated a constant dose response relationship from 2 mg/kg to 120 mg/kg.

CORT 108297 has also produced statistically significant results in the prevention of weight gain and insulin insensitivity in mice fed a high fat, high sucrose diet.

10

Table of Contents

If CORT 108297 or other GR-II antagonists prove to mitigate the weight gain and metabolic disturbances associated with the use of antipsychotic medication, they could be of benefit to the millions of people currently taking this important pharmacotherapy. We advanced CORT 108297 into a Phase 1 clinical trial during the first quarter of 2010. We plan to advance the compound into a Phase 2 trial in 2011, subject to availability of funds.

GR-II Antagonist Platform

We have assembled a patent portfolio covering a broad range of uses, as well as the composition of our new chemical entities.

| • | We have composition of matter claims on three patent families of novel selective glucocorticoid receptor (GR-II) antagonists. Applications for all of the three families have been allowed in Europe. In the United States, applications for two of the three families have been allowed. Examination has not yet begun in the United States on our third novel selective GR-II antagonist family. |

| • | We also have a portfolio of patents describing the use of drugs that block the GR-II receptor for the treatment of metabolic and psychiatric disorders. In addition to psychotic depression, we own or have exclusively licensed issued patents for the use of GR-II antagonists for treatment and / or prevention of: |

| • | weight gain following treatment with antipsychotic medication; |

| • | mild cognitive impairment; |

| • | stress disorders; |

| • | early dementia, including early Alzheimer’s disease; |

| • | delirium; |

| • | gastroesophageal reflux disease; |

| • | cognitive deterioration in adults with Down’s Syndrome; |

| • | psychosis associated with cocaine addiction and |

| • | increasing the therapeutic response to ECT. |

Discovery Research

In 2003, we initiated a discovery research program to identify and patent selective GR-II antagonists at a contract research organization in the United Kingdom. Through the research program, we identified and filed patent applications for three distinct series of GR-II antagonists. These compounds appear to be as potent as Corcept’s lead product CORLUX in blocking cortisol but, unlike CORLUX, they do not appear to block the progesterone or other steroid receptors. Currently, we are evaluating several compounds in our research programs, including CORT 108297, a lead compound from our discovery efforts. CORT 108297 has demonstrated attractive characteristics, with high plasma and brain concentrations in an animal model and promising results in a human microdosing study, including good bioavailability and potential for once-daily dosing. CORT 108297 has also demonstrated the ability to prevent and reduce olanzapine induced weight gain in a rat model, as well as to prevent weight gain from a high fat, high sugar diet and increase insulin sensitivity in a mouse model. CORT 108297 is being evaluated in a Phase 1 study.

Research and Development

We incurred approximately $14.4 million, $14.2 million and $7.9 million of research and development expenses, respectively, in the years ended December 31, 2009, 2008 and 2007, which accounted for approximately 71%, 71% and 62% of our total expenses in these respective fiscal years. For a further discussion, see Part II, Item 7, Management’s Discussion and Analysis of Financial Conditions and Results of Operations – Results of Operations.

11

Table of Contents

Medical Education and Commercialization

We are planning for the commercialization of CORLUX. To achieve commercial success for any approved product, we must either develop a marketing and sales force or enter into arrangements with others to market and sell our products. We intend to develop our own medical affairs and commercialization infrastructure in the United States for CORLUX because we believe that the initial markets for Cushing’s Syndrome and psychotic depression in the United States are highly concentrated and accessible. We intend to engage a partner to commercialize CORLUX in territories outside of the United States.

| • | If approved, we expect to hire a small, experienced field sales force, supported by medical affairs and other infrastructure, to sell CORLUX for the treatment of Cushing’s Syndrome. We intend to focus on patients who are in the care of an endocrinologist and in active treatment for their disease. We estimate that there are fewer than 1000 endocrinologists who would need to be targeted to reach the Cushing’s Syndrome population in active treatment. We plan to reach out directly to patients utilizing web-based initiatives and interactions with patient groups. We expect distribution and logistical support to be provided by specialty pharmacies. |

A large portion of the people who suffer from Cushing’s Syndrome remain unrecognized or undertreated. We intend to develop programs to educate the medical community about early diagnosis of this Syndrome and increase awareness regarding CORLUX.

| • | If approved for the treatment of psychotic depression, we plan to reach patients who are candidates for ECT by marketing to hospitals and psychiatrists that perform ECT. We estimate that there are approximately 900 hospitals with more than 30 in-patient psychiatric beds. Of these, we estimate that approximately 300 offer ECT. We believe that approximately 1000 psychiatrists administer most ECT procedures. Subsequently, we also intend to expand our commercialization efforts to address the larger set of patients with psychotic depression currently undergoing combination drug therapy, which would require an increase in the size of our initial sales force. |

As with Cushing’s Syndrome, a large portion of the people who suffer from psychotic depression remain unrecognized or undertreated. We intend to develop programs to educate the medical community about early diagnosis of psychotic depression and increase awareness regarding CORLUX as a treatment for this disorder.

Manufacturing

As a drug development entity, we intend to continue to utilize our financial resources to complete the development of CORLUX and advance other product candidates rather than diverting resources to establishing our own manufacturing facilities.

We intend to continue to rely on experienced contract manufacturers to produce our product candidates. We have entered into manufacturing agreements with two contract manufacturers, Produits Chimiques Auxiliaires et de Synthese SA (PCAS) and ScinoPharm Taiwan (ScinoPharm), to produce the active pharmaceutical ingredient (API) for CORLUX. The agreement with PCAS, which was executed in early November 2006, is for an initial period of five years with an automatic extension for one additional year unless either party gives twelve month’s prior notice that it does not want the extension. There is no guaranteed minimum purchase commitment under this agreement. If PCAS is unable to manufacture the product for a consecutive six-month period, we have the right to terminate the agreement. The agreement with ScinoPharm obligates us to purchase at least $1,000,000 of bulk mifepristone per year following the commercial launch of CORLUX. This agreement is terminable by either party at any time. We have also entered into an agreement with another contract manufacturer, PharmaForm, L.L.C., for the production of CORLUX tablets for use in clinical activities. To date, our need for CORLUX tablets has been limited to the amounts required to support our clinical trials.

12

Table of Contents

Competition

If approved for commercial use as a treatment for Cushing’s Syndrome or the psychotic features of psychotic depression, CORLUX will compete with established treatments, including other potential compounds under development for Cushing’s Syndrome or, in the case of psychotic depression, with ECT and combination drug therapy.

We are aware that Laboratoire HRA Pharma has received an Orphan Drug Designation in the United States and Europe for the use of mifepristone to treat a subtype of Cushing’s Syndrome and has begun a clinical trial in Europe and the United States. If this product is approved for commercialization before CORLUX, our potential future revenue could be reduced. We are also aware that Exelgyn Laboratories received Orphan Drug Designation for Cushing’s Syndrome in Europe, but they have stated that they have not yet conducted any clinical trials. We may also experience competition from Novartis, which is developing a somatostatin analogue, pasireotide, that is in Phase 3 trials for various endocrine disorders, including Cushing’s disease, which is a subset of the patients with Cushing’s Syndrome.

ECT has been shown to be the most effective treatment for psychotic depression, but it carries the risks of general anesthesia, potential memory loss and other adverse effects as well as the stigma associated with the procedure. Use of CORLUX does not require anesthesia and, in our clinical trials conducted to date, patients treated with CORLUX have not exhibited the adverse effects associated with ECT.

Other competitors include companies that market antipsychotic drugs that are used off-label as part of combination drug therapy for psychotic depression. To reduce the psychotic features of psychotic depression, these drugs generally are taken in combination with antidepressant medication over a period of weeks to several months. Unlike the use of CORLUX, this extended course of treatment may put patients at risk of significant adverse side effects, including weight gain, diabetes, sedation, permanent movement disorders and sexual dysfunction. Antipsychotics include Bristol-Myers Squibb’s Abilify, Novartis’ Clozaril, Pfizer’s Geodon and Navane, Ortho-McNeil’s Haldol, Janssen Pharmaceutica’s Risperdal, AstraZeneca’s Seroquel, GlaxoSmithKline’s Stelazine and Thorazine, Mylan’s Mellaril, Schering Corporation’s Trilafon and Eli Lilly’s Zyprexa.

We are aware of one clinical trial that has taken place, conducted by the pharmaceutical division of Akzo Nobel, a division of Schering Plough, for a new chemical entity for the treatment of psychotic depression. This medicine is a GR-II antagonist, the commercial use of which would be covered by our patent. In 2004, Akzo Nobel filed an observation in our exclusively licensed European patent application with claims directed to psychotic depression, in which Akzo Nobel challenged the claims of that patent application. In 2005, we filed a rebuttal to Akzo Nobel’s observation. In February 2006, the European Patent Office (EPO) allowed our patent application. In July 2006, the patent was issued. We are not aware of any public disclosures by any company, other than Akzo Nobel, regarding the development of new medicinal products to treat psychotic depression. However, other companies may be developing new drug products to treat psychotic depression and the other conditions we are exploring. Our present and potential competitors include major pharmaceutical companies, as well as specialty pharmaceutical firms. Most of our competitors have considerably greater financial, technical and marketing resources than we do. We expect competition to intensify as technical advances are made.

Many colleges, universities and public and private research organizations are also active in the human health care field. While these entities focus on education, they may develop or acquire proprietary technology that we may require for the development of our product candidates. We may attempt to obtain licenses to this proprietary technology.

Our ability to compete successfully will be based on our ability to develop proprietary products, attract and retain scientific personnel, obtain patent or other protection for our product candidates, obtain required regulatory approvals and manufacture and successfully market our future products either alone or through outside parties.

13

Table of Contents

Intellectual Property

Patents and other proprietary rights are important to our business. It is our policy to seek patent protection for our inventions, and to rely upon trade secrets, know-how, continuing technological innovations and licensing opportunities to develop and maintain our competitive position.

Under an agreement with Stanford University, we have licensed exclusive rights to the following issued U.S. patents and any corresponding foreign patents:

| U.S. Patent Number |

Subject Matter |

Expiration Date | ||

| 6,150,349 | Use of GR-II antagonists in the treatment of psychotic major depression | October 5, 2018 | ||

| 6,362,173 | Use of GR-II antagonists in the treatment of cocaine-induced psychosis | October 5, 2018 | ||

| 6,369,046 | Use of GR-II antagonists in the treatment of early dementia | February 4, 2019 | ||

We are required to make milestone payments and pay royalties to Stanford University on sales of products commercialized under any of the above patents. We are currently in compliance with our obligations under the agreement. If Stanford University were to terminate any of our exclusive licenses due to breach of the license on our part, we would not be able to commercialize CORLUX for the treatment of the psychotic features of psychotic depression, cocaine-induced psychosis or early dementia.

We also own issued U.S. patents for the use of GR-II antagonists in the treatment of mild cognitive impairment, for the treatment of weight gain following treatment with antipsychotic medication, for the prevention and treatment of stress disorders, for increasing the therapeutic response to ECT, for the treatment of delirium, for the treatment of gastroesophageal reflux disease and for inhibiting cognitive deterioration in adults with Down’s Syndrome.

In addition, we have eight U.S. method of use patent applications covering certain GR-II antagonists, including the treatment of:

| • | patients suffering from mental disorders by optimizing mifepristone levels in plasma serum; |

| • | postpartum psychosis; |

| • | neurological damage in premature infants; |

| • | catatonia; |

| • | migraine headaches; |

| • | psychosis associated with interferon-alpha therapy; |

| • | depression in patients taking Interleukin-2 (IL-2) and |

| • | amyotrophic lateral sclerosis (ALS). |

We have composition of matter claims on three patent families of novel selective GR-II antagonists. Applications for all of the three families have been allowed in Europe. In the United States, applications for two of the three families have been allowed. Examination has not yet begun in the United States on our third novel selective GR-II antagonist family.

14

Table of Contents

We have also filed, where we deemed appropriate, foreign patent applications corresponding to our U.S. patents and applications.

However, we cannot assure you that any of our patent applications will result in the issuance of patents, that any issued patent will include claims of the breadth sought in these applications or that competitors will not successfully challenge or circumvent our patents if they are issued.

Although two of our patents and one of our patent applications have claims directed to the composition of compounds, we do not have a patent with claims directed to the composition of mifepristone. Our rights under our issued patents related to mifepristone cover only the use of that compound in the treatment of specific diseases.

The patent covering the product mifepristone has expired. The only FDA-approved use of mifepristone is to terminate pregnancy. The FDA has imposed significant restrictions on the use of mifepristone to terminate pregnancy and may impose restrictions on CORLUX for the treatment of Cushing’s Syndrome and the psychotic features of psychotic depression. We plan to rely on (1) the scope of our use patent, (2) the restrictions imposed by the FDA on the use of mifepristone to terminate pregnancy and (3) the different patient populations, administering physicians and treatment settings between the use of mifepristone to terminate pregnancy and to treat Cushing’s Syndrome and psychotic depression.

The patent positions of companies in the pharmaceutical industry are highly uncertain, involve complex legal and factual questions and have been and continue to be the subject of much litigation. Our product candidates may give rise to claims that we infringe on the products or proprietary rights of others. If it is determined that our drug candidates infringe on others’ patent rights, we may be required to obtain licenses to those rights. If we fail to obtain licenses when necessary, we may experience delays in commercializing our product candidates while attempting to design around other patents, or determine that we are unable to commercialize our product candidates at all. If we do become involved in intellectual property litigation, we are likely to incur considerable costs in defending or prosecuting the litigation. We believe that we do not currently infringe any third party’s patents or other proprietary rights, and we are not obligated to pay royalties to any third party other than Stanford University.

In November 2003, McLean Hospital had alleged that it also had rights to the technology that led to the patent for the use of GR-II antagonists to treat the psychotic features of psychotic depression. McLean Hospital was a prior employer of one of our founders, Dr. Alan Schatzberg and it alleged that the invention of the technology underlying this patent was conceived by Dr. Schatzberg and/or Dr. Anthony Rothschild while the two were employed by McLean Hospital. We contended that the invention was actually conceived by Dr. Schatzberg and Dr. Joseph Belanoff while they were employed by Stanford University and that the patent was appropriately assigned by them to Stanford University. In October 2004, we announced a resolution of this issue in which we retained our exclusive rights under the patent and which required us to make no additional payments under the license, regardless of the resolution of the impending inventorship dispute. In January 2005, the inventorship issue was resolved in favor of Stanford University.

As discussed earlier under “Competition,” in 2004 Akzo Nobel filed an observation to the grant of our exclusively licensed European patent application with claims directed to psychotic depression. In February 2006, the EPO allowed our patent application. We are not aware of any other disputes related to patent issues.

License Agreement

Under our exclusive license agreement with Stanford University to patents covering the use of CORLUX to treat the psychotic features of psychotic depression and for the treatment of early dementia, we are required to pay Stanford $50,000 annually as a nonrefundable royalty payment. This payment is creditable against future royalties. We are also obligated to pay Stanford a $50,000 milestone upon the filing of the NDA for CORLUX

15

Table of Contents

for the treatment of psychotic depression and a further $200,000 milestone payment upon FDA approval of CORLUX. The milestone payments are also creditable against future royalties. This license agreement expires upon expiration of the related patents or upon notification by us to Stanford.

Government Regulation

Prescription pharmaceutical products are subject to extensive pre- and post-market regulation, including regulations that govern the testing, manufacturing, safety, efficacy, labeling, storage, record keeping, advertising, and promotion of the products under the Federal Food, Drug and Cosmetic Act. All of our product candidates will require regulatory approval by government agencies prior to commercialization. The process required by the FDA before a new drug may be marketed in the United States generally involves the following: completion of preclinical laboratory and animal testing; submission of an IND, which must become effective before clinical trials may begin; performance of adequate and well controlled human clinical trials to establish the safety and efficacy of the proposed drug or biologic’s intended use; and, in the case of a new drug, approval by the FDA of an NDA. The process of complying with these and other federal and state statutes and regulations in order to obtain the necessary approvals and subsequently complying with federal and state statutes and regulations involves significant time and expense.

Preclinical studies are generally conducted in laboratory animals to evaluate the potential safety and the efficacy of a product. Drug developers submit the results of preclinical studies to the FDA as a part of an IND, which must be approved before beginning clinical trials in humans. Typically, human clinical trials are conducted in three sequential phases that may overlap.

| • | Phase 1. Clinical trials are conducted with a small number of subjects to determine the early safety profile, maximum tolerated dose and pharmacokinetics of the product candidate in human volunteers. |

| • | Phase 2. Clinical trials are conducted with groups of patients afflicted with a specific disease to determine preliminary efficacy, optimal dosages and expanded evidence of safety. |

| • | Phase 3. Large-scale, multi-center, comparative trials are conducted with patients afflicted with a target disease to establish the overall risk/benefit ratio of the drug and to provide enough data to demonstrate with substantial evidence the efficacy and safety of the product, as required by the FDA. |

The FDA and the Institutional Review Boards closely monitor the progress of each of the three phases of clinical trials that are conducted in the United States and may reevaluate, alter, suspend or terminate the testing at any time for various reasons, including a belief that the subjects are being exposed to an unacceptable health risk. The FDA may also require that additional studies be conducted, such as studies demonstrating that the drug being tested does not cause cancer.

After Phase 3 trials are completed, drug developers submit the results of preclinical studies, clinical trials, formulation studies and data supporting manufacturing to the FDA in the form of an NDA for approval to commence commercial sales. The FDA reviews all NDAs submitted before it accepts them for filing. The FDA may request additional information rather than accept an NDA for filing. If the FDA accepts an NDA for filing, they may grant marketing approval, request additional information or deny the application if it determines that the application does not meet regulatory approval criteria. FDA approvals may not be granted on a timely basis, or at all.

If the FDA approves an NDA, the subject drug becomes available for physicians to prescribe in the United States. Once approved, the FDA may withdraw the product approval if compliance with pre- and post-market regulatory standards is not maintained. The drug developer must submit periodic reports to the FDA. Adverse experiences with the product must be reported to the FDA and could result in the imposition of marketing restrictions through labeling changes or product removal. Product approvals may be withdrawn if problems with

16

Table of Contents

safety or efficacy occur after the product reaches the marketplace. In addition, the FDA may require post- marketing studies, referred to as Phase 4 studies, to monitor the effect of approved products, and may limit further marketing of the product based on the results of these post-market studies.

Facilities used to manufacture drugs are subject to periodic inspection by the FDA and other authorities where applicable, and must comply with current Good Manufacturing Practices regulations (cGMP). Failure to comply with the statutory and regulatory requirements subjects the manufacturer to possible legal or regulatory action, such as suspension of manufacturing, seizure of product or voluntary recall of a product.

With respect to post-market product advertising and promotion, the FDA imposes a number of complex regulations on entities that advertise and promote pharmaceuticals, which include, among others, standards and regulations for direct-to-consumer advertising, off-label promotion, industry sponsored scientific and educational activities, and promotional activities involving the Internet. The FDA has very broad enforcement authority under the Federal Food, Drug and Cosmetic Act, and failure to abide by these regulations can result in penalties including the issuance of a warning letter directing a company to correct deviations from FDA standards, a requirement that future advertising and promotional materials be pre-cleared by the FDA, and state and federal civil and criminal investigations and prosecutions.

In addition to studies requested by the FDA after approval, a drug developer may conduct other trials and studies to explore use of the approved compound for treatment of new indications. The purpose of these trials and studies and related publications is to broaden the application and use of the drug and its acceptance in the medical community. Data supporting the use of a drug for these new indications must be submitted to the FDA in a new or supplemental NDA that must be approved by the FDA before the drug can be marketed for the new indications.

Approvals outside the United States. We have not started the regulatory approval process in any jurisdiction other than the United States and we are unable to estimate when, if ever, we will commence the regulatory approval process in any foreign jurisdiction. We or our partners will have to complete an approval process similar to the U.S. approval process in foreign target markets for our product candidates before we can commercialize our product candidates in those countries. The approval procedure and the time required for approval vary from country to country and can involve additional testing. Foreign approvals may not be granted on a timely basis, or at all. Regulatory approval of prices is required in most countries other than the United States. The prices approved may be too low to generate an acceptable return to us.

Orphan Drug Designation. The FDA has granted us Orphan Drug designation for CORLUX for the treatment of endogenous Cushing’s Syndrome. The designation provides special status to a product to treat a rare disease or condition providing that the product meets certain criteria. Orphan designation qualifies the sponsor of the product for the tax credit and marketing incentives of the Orphan Drug Act. A marketing application for a prescription drug product that has been designated as a drug for a rare disease or condition is not subject to a prescription drug user fee unless the application includes an indication for other than a rare disease or condition.

Fast Track Designation. The FDA sometimes grants “fast track” status under the Food and Drug Administration Modernization Act of 1997. The fast track mechanism was created to facilitate the development and approval of new drugs intended for the treatment of life-threatening conditions for which there are no effective treatments and which demonstrate the potential to address unmet medical needs for the condition. The fast track process includes scheduling of meetings to seek FDA input into development plans, the option of submitting an NDA serially in sections rather than submitting all components simultaneously, the option to request evaluation of studies using surrogate endpoints, and the potential for a priority review.

17

Table of Contents

We have been granted fast track status for CORLUX for the treatment of the psychotic features of psychotic depression. However, the fast track designation may be withdrawn by the FDA at any time. The fast track designation does not guarantee that we will qualify for or be able to take advantage of the expedited review procedures and does not increase the likelihood that CORLUX will receive regulatory approval.

Priority Review. The FDA has indicated to us that it will grant us a priority review of our NDA of CORLUX for the treatment of the psychotic features of psychotic depression if no other medications have been approved for this indication at the time of our submission.

Employees

We are managed by a core group of experienced pharmaceutical executives with a track record of bringing new drugs to market. To facilitate advancement of development programs, we also enlist the expertise of associates and advisors with extensive pharmaceutical development experience.

As of December 31, 2009, we had 16 full-time employees, three part-time employees and 11 long-term contract staff. Four of our employees are M.D.s. We consider our employee relations to be good. None of our employees is covered by a collective bargaining agreement.

General

We were incorporated in the State of Delaware on May 13, 1998. Our registered trademarks include Corcept® and CORLUX®. Other service marks, trademarks and trade names referred to in this document are the property of their respective owners.

Available Information

We are subject to the information requirements of the Securities Exchange Act of 1934 and we therefore file periodic reports, proxy statements and other information with the SEC relating to our business, financial statements and other matters. The reports, proxy statements and other information we file may be inspected and copied at prescribed rates at the SEC’s Public Reference Room, 100 F Street, N.E., Washington, D.C. 20549, on official business days during the hours of 10:00 A.M. to 3:00 P.M. You may obtain information on the operation of the SEC’s Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC also maintains an Internet site that contains reports, proxy statements and other information regarding issuers like us that file electronically with the SEC. The address of the SEC’s Internet site is www.sec.gov. For more information about us, please visit our website at www.corcept.com. You may also obtain a free copy of our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports on the day the reports or amendments are filed with or furnished to the SEC by visiting our website at www.corcept.com. The information found on, or otherwise accessible through, our website, is not incorporated information, and does not form a part of, this Form 10-K.

18

Table of Contents

| ITEM 1A. | RISK FACTORS |